Better quality amenities — rich, creamy soap, for example, and thirsty plush cotton towels — make a statement. (Photo: dreamstime.com)

“I think of you every time I buy soap,” says the young woman, a friend of my daughter’s from college. We are chatting at a wedding. “Triple-milled,” she continues. “Your daughter drilled this into my head.”

I’m not sure how to take this.

“Well, I’m glad some lessons have sunk in,” I say.

My son-in-law overhears this exchange and chimes in, “How about the time she said that if anyone ever smothers her with a pillow, she hopes it has a 400-thread-count, Egyptian cotton pillowcase.”

“I said that?”

He nods vigorously. I don’t recall that, but It sounds like the way I would want to go.

Though the soap-and-linen dialogue may seem trifling, it lies at the heart of a topic I’ve thought a lot about and written a lot about this past year —rightsizing. It’s the subject of my next book, which will come out in January.

Here I thought I was addressing my generation when exploring how to decide where to live, in what size house and with what stuff to create a rightsized life, but the younger generation is tuning in, too. Living a rightsized life means not only having just enough house in just the right place, but also furnishing it with the fewest, best-performing household goods possible.

The message applies to all ages.

That means choosing only those sheets, towels, soaps, knives, pans, wineglasses, furnishings and other household basics that excel at their jobs and that elevate your life. Owning fewer, higher quality items leads to living large while spending less. It’s the key to gracious, clutter-free, rightsized living.

Imagine no more sheets that don’t fit right and don’t breathe, no more towels that aren’t thirsty, no harsh bath soap that dissolves into the drain after three showers, no pans that scorch your food, no pillows that fall flat, no sofas that you avoid because they aren’t comfortable. Instead, everything you have is a pleasure to use and look at and live with. It was all money well and thoughtfully spent.

Unfortunately, many homes are filled with the opposite: subpar products that aren’t quite right, that don’t quite work, and that we continue to buy wrong, because we don’t always know how to buy them right. Then, because we feel guilty getting rid of these barely used items, they clog our cupboards, closets, and lives … unless we learn how to buy them right.

That was part of my aim when I wrote this book, because I love nice things but hate to waste money. I wanted to discover — and help you discover — the luxury of less. So I interviewed experts on the various staples needed to outfit every room of the house, from tea towels to sectionals, and teased out what makes some items exceptional and how to buy those everyday items right.

Here’s the SparkNotes version so you, too, can buy once and buy right.

Study up. Become a student of quality. Look beyond the brand, packaging hype and marketing ploys to discover the properties that make a product the best in its class. To pick great household products out from a noisy and confusing line-up, learn about the production process, the materials used to make them and when to choose one material over another: linen or cotton, crystal or glass, cast iron or stainless-steel? Understand why you should choose hand-knotted rugs over machine-made ones, triple vs. single-milled soap and the best chromium-nickel ratio in flatware (18/10).

Avoid cooking sets. Big box sets of pots and pans and knives seem like a bargain, but they contain filler pieces you will likely never use. Buy good pans and good knives one at a time.

Try before you buy. Before investing in a full set of sheets or towels, buy a pillowcase and a face towel. Use them, wash them and use them again to make sure you like the feel and function. You can also test drive area rugs by purchasing (and returning) the smallest size — 2 by 3 feet — and seeing how the colors and pattern look in your home before you invest in the 9 by 12.

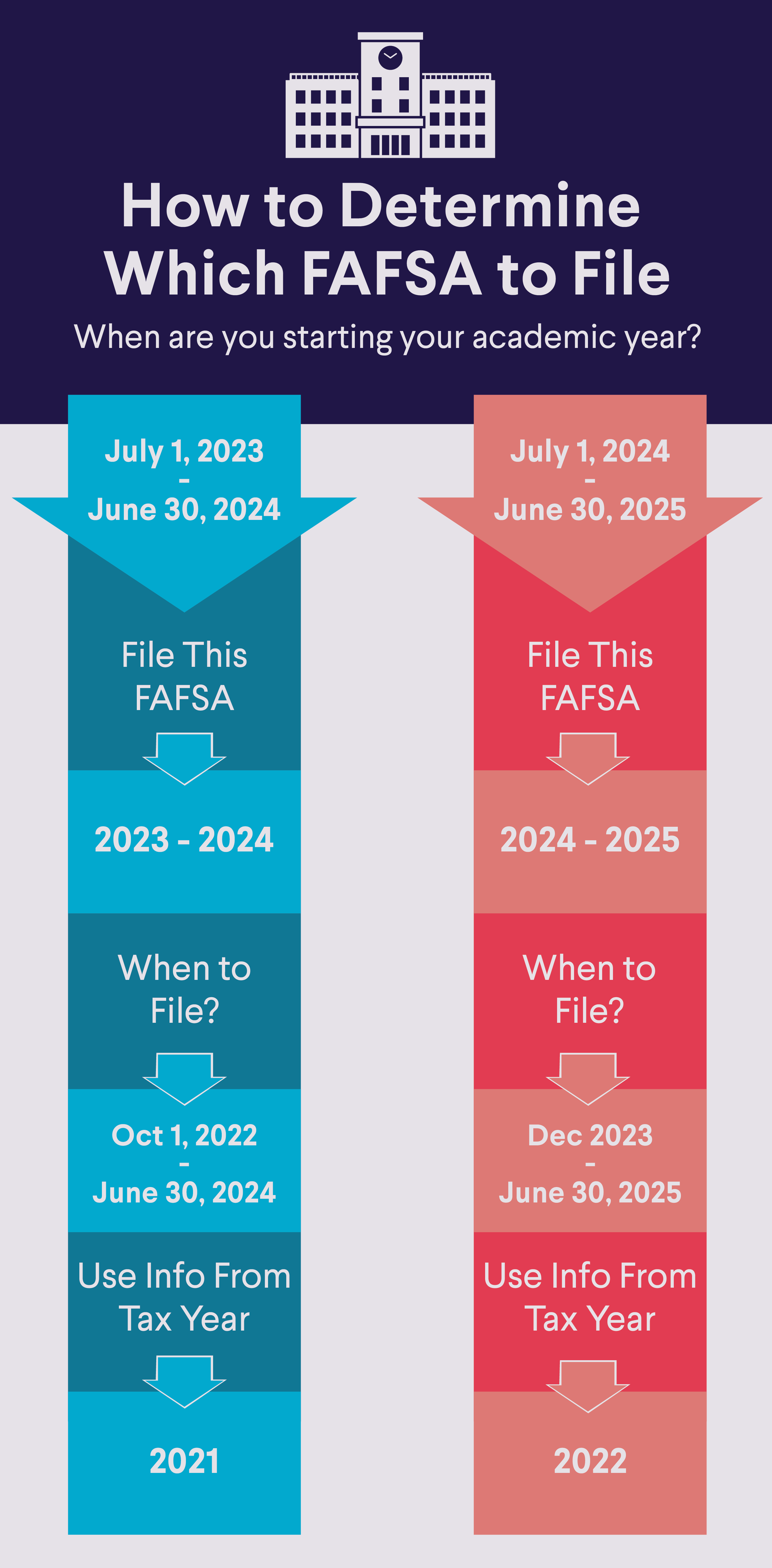

Editor’s Note: Due to major changes coming to the FAFSA, the form for the 2024-2025 academic year is delayed until December 2023. This article reflects the most recent information, but final details will not be available until the new FAFSA form is released.

The Free Application for Federal Student Aid, or FAFSA®, is a form students can fill out each school year to apply for college grants, work-study programs, federal student loans, and certain state-based aid.

By not filling out the form, or missing the FAFSA deadline, students may not receive financial aid that could help them pay for college. Indeed, the graduating class of 2022 left roughly $3.6 billion in need-based federal Pell Grants on the table by not completing the FAFSA, according to a new report by the National College Attainment Network (NCAN).

Typically, the FAFSA becomes available on October 1 for the following academic year. The 2024-2025 academic year, however, is an exception. Due to upcoming changes to the FAFSA (and some adjustments to how student aid will be calculated), the form will be available in December 2023.

It’s helpful to fill out your FAFSA as early as possible and not miss the important application deadlines, as there is a limited amount of aid available.

Read on for key federal, state, and institutional FAFSA deadlines to know.

What Is the FAFSA?

The FAFSA is the online form that you must fill out to apply for financial aid from the federal government, state governments, and most colleges and universities. The form requires students and their parents to submit information about household income and assets. That information is used to calculate financial need and determine how much aid will be made available.

If you are a dependent student, you will need to submit your parents’, as well as you own, financial information. If you are considered independent, you are not required to submit your parents’ financial information.

If you are already in school, remember that the FAFSA must be filled out every year, since income and tax information might have changed.

Federal financial aid includes student loans, grants, scholarships, and work-study jobs. In general, the eligibility requirements for federal aid state that for most programs, students:

• Must demonstrate financial need (though there is some non-need based aid, such as unsubsidized student loans) and,

• Must be a U.S. citizen or an eligible noncitizen, and

• Be enrolled in an qualifying degree or certificate program at their college or career school

For further details, take a look at the basic eligibility requirements on the Student Aid website. 💡 Quick Tip: You can fund your education with a low-rate, no-fee private student loan that covers all school-certified costs.

FAFSA Open Date and Deadline

File Your FAFSA for Next Year Close to December

Generally, it makes sense to submit the FAFSA promptly after the October 1st application release — or, in the case of the 2024-25 FAFSA, December 2023. Some aid is awarded on a first-come, first-served basis, so submitting it early could help improve your chances of receiving financial help for college.

File Your FAFSA for Last Year by June 30

You must file the FAFSA no later than June 30th for the school year you are requesting aid for. So, for the academic year 2023-24, you must file by June 30th, 2024, at the very latest, and for the academic year 2024-25, the final federal deadline is June 30th, 2025.

This FAFSA deadline comes after you’ve already attended and, likely, paid for school. You generally don’t want to wait this long. However, if you do, you can often receive grants and loans retroactively to cover what you’ve already paid for the spring and fall semester. Or, in some cases, you may be able to apply the funds to pay for 2023 summer courses.

State and institutional FAFSA deadlines

When the FAFSA is due is also dependent on where you want to go to college. Individual states and colleges have different deadlines — which may be much earlier than the federal deadline — for awarding financial aid to students. Here’s a look at two other key FAFSA deadlines to know.

Institutional FAFSA Deadlines

While students have until the end of the school year to file the FAFSA, individual schools may have earlier deadlines. These priority deadlines mean you need to get your FAFSA application in by the school’s date to be considered for the college’s own institutional aid. So if you are applying to several colleges, you may want to check each school’s FAFSA deadline and complete the FAFSA by the earliest one.

While filling out your FAFSA, you can include every school you’re considering, even if you haven’t been accepted to college yet.

State FAFSA Deadlines

States often have their own FAFSA deadlines. You can get information about state deadlines at Studentaid.gov. Some states have strict cutoffs, while others are just best-practice suggestions — so you’ll want to check carefully. States may have limited funds to offer as well.

Federal FAFSA Deadline

Typically, the FAFSA becomes available on October 1, almost a full year in advance of the year that aid is awarded. For the 2024-25 academic year, the FAFSA will open a few months later than usual — some time in December 2023. However, the federal government gives you until June 30th of the year you are attending school to apply for aid.

It’s generally recommended that students fill out the FAFSA as soon as possible after it’s released for the next school year’s aid to avoid missing out on available funds. Plus, there are often earlier school and state deadlines you’ll need to meet.

Recommended: FAFSA Delay: 5 Steps to Help Ensure Your State and College Aid Aren’t Affected

Taking the Next Steps After Submitting the FAFSA

So what happens after you hit “submit” on your FAFSA? Here’s a look at next steps:

• Wait for your Student Aid Report (SAR). If you submitted your FAFSA online, the U.S. Department of Education will process it within three to five days. If you submit a paper form, it will take seven to 10 days to process. The SAR summarizes the information you provided on your FAFSA form. You can find your SAR by logging in to fafsa.gov using your FSA ID and selecting the “View SAR” option on the My FAFSA page

• Review your SAR. Check to make sure all of the information is complete and accurate. If you see any missing or inaccurate information, you’ll want to complete or correct your FAFSA form as soon as possible. The SAR will give you some basic information about your eligibility for federal student aid. However, the school(s) you listed on the FAFSA form will use your information to determine your actual eligibility for federal — and possibly non-federal — financial aid.

• Wait for acceptance. Most college decisions come out in the spring, often March or early April. If you applied to a college early action or early decision, you can expect an earlier decision notification, often around December. Typically, you will receive a financial aid award letter along with your acceptance notification. This letter contains important information about the cost of attendance and your financial aid options.

Understanding Your Financial Aid Award

Receiving financial aid can be a great relief when it comes to paying for higher education. Your financial aid award letter will include the annual total cost of attendance and a list of financial aid options. Your financial aid package may be a mix of gift aid (which doesn’t have to be repaid), loans (which you have to repay with interest), and federal work-study (which helps students get part-time jobs to earn money for college).

If, after accounting for gift aid and work-study, you still need money to pay for school, federal student loans might be your next consideration. As an undergraduate student, you may have the following loan options:

• Direct Subsidized Loans Students with financial need can qualify for subsidized loans. With this type of federal loan, the government covers the interest that accrues while you’re in school, for six months after you graduate, and during periods of deferment.

• Direct Unsubsidized Loans Undergraduates can take out direct unsubsidized loans regardless of financial need. With these loans, you’re responsible for all interest that accrues when you are in school, after you graduate, and during periods of deferment.

• Parent PLUS Loans These loans allow parents of undergraduate students to borrow up to the total cost of attendance, minus any financial aid received. They carry higher interest rates and higher loan origination fees than Direct Subsidized and Unsubsidized Loans.

If financial aid, including federal loans, isn’t enough to cover school costs, students can also apply for private student loans, which are available through banks, credit unions, and online lenders.

Private loan limits vary by lender, but students can often get up to the total cost of attendance, which gives you more borrowing power than you have with the federal government. Each lender sets its own interest rate and you can often choose to go with a fixed or variable rate. Unlike federal loans, qualification is not need-based. However, you will need to undergo a credit check and students often need a cosigner.

Keep in mind that private loans may not offer the borrower protections — like income-based repayment plans and deferment or forbearance — that come with federal student loans. 💡 Quick Tip: Parents and sponsors with strong credit and income may find much lower rates on no-fee private parent student loans than federal parent PLUS loans. Federal PLUS loans also come with an origination fee.

The Takeaway

Completing the FAFSA application allows you to apply for federal aid (including scholarships, grants, work-study, and federal student loans). The FAFSA form is generally released on October 1st of the year before the award year and closes on July 30th of the school year you are applying for.

The 2024–25 FAFSA will be delayed until December 2023 due to changes the U.S. Department of Education is implementing to make the application more streamlined for students and families. That application will close on June 30, 2025. However, individual colleges and states have their own deadlines which are typically earlier than the federal FAFSA deadline.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

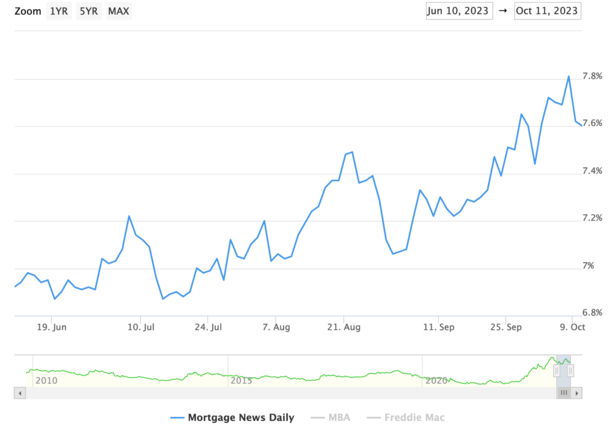

If you’ve been keeping track lately, you might be wondering why mortgage rates plunged this week.

Last week was a totally different story, with a hotter-than-expected jobs report almost enough to push the 30-year fixed across the daunting 8% threshold.

But then the unexpected happened over the weekend, as is often the case with geopolitical events.

In times of uncertainty, bonds are typically a safe haven, and when demand for them rises, their associated yields (or interest rates) fall.

This, coupled with some more dovish talk from Fed speakers, might explain the recent pullback in rates.

How Much Have Mortgage Rates Plunged?

First off, the word “plunge” might be a strong one given how much mortgage rates have climbed over the past 18 months.

While mortgage rates have indeed fallen all week, they remain well above recent lows. And even much higher than levels seen this summer.

If we want to use MND’s widely cited daily rate survey as the measure, the 30-year fixed now stands at 7.60%.

That’s down from 7.81% on Friday October 6th. So basically mortgage rates have improved by about 20 basis points, or perhaps .25% depending on the lender.

It also reduced the year-over-year change in rates from 0.77% to 0.46%, providing a glimmer of hope that the worst could be behind us.

And better yet, perhaps mortgage rates have peaked. While that remains to be seen, it’s been hard to get any meaningful relief lately.

Typically, any pullback or improvement in rates has been met with further increases. And the wins are generally short-lived.

Will that be the case again this time or is there finally light at the end of the tunnel?

Mortgage Rates Helped by New Geopolitical Risks

As for why mortgage rates improved this week, one would be quick to point to the events that took place in Israel (and continue to unfold).

Generally, mortgage rates tend to go down if there is the threat of war or similar tension in the air.

The reason is uncertainty, which is a friend to bonds because of their relative certainty.

In short, investors will flee riskier markets like equities and pile into bonds, which is known as the flight to safety.

If more investors are buying bonds, the price goes up and the yield drops. Since Friday, the 10-year bond yield has fallen from 4.84 to about 4.61 today.

Of course, this could prove to be a short-term reaction to what has been a clear move higher for bond yields lately.

So it’s entirely possible that the 10-year yield marches on back to those recent levels (and beyond) depending on what transpires.

And the conflict in the Middle East could actually exacerbate inflation if oil prices (and gas prices) rise.

No More Fed Rate Hikes Could Take Pressure Off Mortgage Rates

Another factor related to the recent mortgage rate plunge has been some dovish talk from Fed officials.

Atlanta Fed President Raphael Bostic came out this week and basically said no more interest rate hikes were needed.

The Fed has already raised its key policy rate 11 times since early 2022, pushing mortgage rates up along with it.

But Bostic “told the American Bankers Association that Fed policy is sufficiently restrictive.”

Additionally, he said rate cuts could even be in the cards “if things get ugly in the Middle East.”

“You can pretty much count on the Fed taking that into its world view and that’s only going to be lower rates.”

Earlier in the week, Dallas Fed President Lorie Logan said higher bond yields could do the heavy lifting for the Fed, requiring no additional tightening on their part.

And Fed Vice Chair Jefferson made comments that suggested he was in favor of pausing the fed rate hikes.

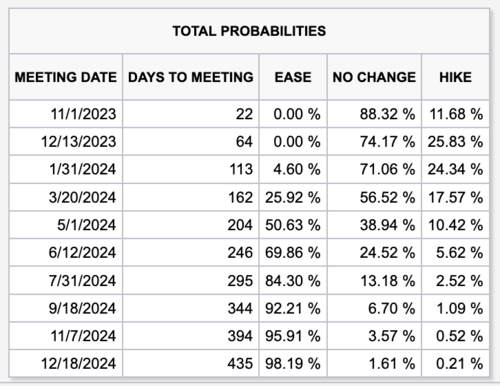

Interest rate traders have taken that to mean that the Fed rate hikes could be over, and the next move might be lower.

Per the CME FedWatch Tool, that cut could come by the June meeting, based on the current odds.

Though if the situation worsens in the Middle East, cuts could materialize even earlier in 2024.

As it stands now, another rate hike looks exceedingly unlikely, while a rate cut appears to be coming sooner-than-expected.

Now it’s important to note that the Fed doesn’t control mortgage rates, but their long-term outlook can have an effect on mortgage rates.

Fed Clarity Can Lower Bond Yields and Narrow the Spread

Additionally, more clarity from the Fed could go a long way in fixing the spread between 10-year bond yields and mortgage rates.

It’s currently about double its usual amount, at around 300 bps vs. 170. Knowing the Fed’s position on monetary policy could normalize spreads.

If we assume the 10-year bond yield settles in at current levels of say 4.50%, adding a more typical spread of 200 bps puts the 30-year fixed back to 6.50%.

That would spell relief for many prospective home buyers, who might be facing mortgage rates as high as 8% depending on their individual loan attributes.

Factor in paying mortgage points at closing, and it’s possible home buyers could obtain mortgage rates back in the high-5% range.

That would likely be good enough for now to get transactions flowing again, and potentially unlock some existing homeowners trapped by so-called mortgage rate lock-in.

Just beware that the trend has not been friendly to mortgage rates for a long time, and things can easily reverse course again depending on what transpires.

While it might signal a turning point, mortgage rates can also remain stubborn at these levels without significant economic data pointing to lower inflation.

And tomorrow’s CPI report alone could completely reverse the big move lower over the past couple days.

So while we’ve gotten some relief over the past few days, this so-called mortgage rate plunge may easily unwind if more hot economic data comes in. Or if global tensions ease.

Nestled in Hidalgo County, the small city of Alamo, Texas, often emerges as a discussion point among people on a quest for a serene yet promising locale to call home.

The quaint charm often associated with smaller cities can sometimes transcend beyond the picturesque to also offer a quality of life that rivals, or in some instances, surpasses the bustling allure of much larger cities.

This comprehensive assessment dives into the various factors that encapsulate living in Alamo, Texas, with a thorough examination of its cost of living, demographics, amenities and proximity to other significant Texan hubs, ultimately aiming to answer the burning question: “Is Alamo, Texas, a good place to live?”

Demographics and community

The community within Alamo, TX is a reflection of the broader Rio Grande Valley’s demographic composition. With a population that hovers around the 19,000 mark, the town hosts a predominantly Hispanic populace. This cultural backdrop lends Alamo a unique blend of Texan and Mexican traditions, which not only enriches the social fabric but also manifests in the culinary, cultural and artistic offerings of this small city.

Economy and employment

A scrutiny of Alamo’s economic landscape reveals an unemployment rate slightly above the national average. However, this metric has been on a downward trajectory, thanks to burgeoning local businesses and the spillover of economic activities from neighboring cities. The median income in Alamo resonates with the laidback and modest lifestyle it champions.

Cost of living

One of the enticing facets of living in Alamo, Texas, is undoubtedly its cost of living. Statistically, Alamo’s cost of living indices fall below the national average, making it an affordable place especially when pitted against other cities in Texas.

The low cost of living can be largely attributed to the affordable housing market in the city, with the median home value significantly less than the state and national averages. Alamo’s cost of housing and overall living expenses are arguably its biggest selling point to prospective residents on a budget.

Housing market

In Alamo, the median home value stands as a testament to its affordability. Housing here is not only accessible but offers a variety of choices for different income levels. Whether you are looking to rent or buy, the market in Alamo is conducive for families, retirees and even single individuals. The median home value is appreciably lower compared to other cities, making homeownership a feasible dream for many.

Education

Education is a pivotal concern for families contemplating a move to Alamo, TX. The city hosts several public and private schools, delivering a standard of education that aligns with the state’s benchmarks. The proximity to universities and colleges in nearby cities also broadens the educational horizon for residents.

Healthcare and services

Quality healthcare services are within reach, with a number of healthcare facilities located in and around Alamo. The nearby city of McAllen, for instance, has a wider array of medical facilities, ensuring residents have access to specialized medical care whenever necessary.

Proximity to major cities

Nestled strategically in the Rio Grande Valley, Alamo’s location is within a convenient distance from major cities like McAllen and Edinburg. This proximity not only opens up a world of additional amenities and services but also employment opportunities for the residents of Alamo. Moreover, the accessibility to international borders with Mexico enhances the city’s appeal to a more global-minded populace.

Recreation and lifestyle

The lifestyle in Alamo leans towards the tranquil and family-oriented. Numerous parks, recreational facilities and community events held throughout the year contribute to a sense of belonging among residents. The close-knit community vibe is often cited in reviews as one of the endearing qualities of living in Alamo.

Crime and safety

The crime rate in Alamo is comparable to other small towns in Texas. The local law enforcement agencies are active and the community itself is known for its neighborly ethos, which contributes to the overall safety and peaceful living conditions in the city.

Conclusion

The allure of Alamo, Texas lies in its simplistic yet fulfilling lifestyle, far removed from the hustle and bustle synonymous with bigger cities. While it might lack some of the flashy amenities, its affordability, community-centric lifestyle and the promise of a serene living environment make it a compelling choice for individuals seeking a harmonious work-life balance.

However, as with any city, prospective residents should be aware of the economic conditions and be prepared for a lifestyle more serene and traditional compared to urban hubs like Austin or Houston. Looking for your Alamo dream home? Take a look at our available apartments for rent here.

Why Your Checking Account Should Contain as Little Money as Possible

By: Natasha Etzel |

Updated

Oct. 4, 2023 – First published on Oct. 4, 2023

A bank account is an excellent place to keep your money so it’s organized and readily available when needed. Many people keep their cash in a checking account. But, while you want to stash enough money in your checking account to cover your bills and everyday expenses, you want to avoid keeping all of your cash there. I’ll explain why here, and suggest a better place to stash your extra savings.Don’t miss out on interestThe average checking account doesn’t accrue interest. That means you won’t get rewarded for keeping money in your bank account. Instead of keeping all your cash in your checking account, you should only keep enough to cover your monthly expenses. You may want to keep a bit more than just enough to cover your bills. That way, you’ll be covered if you have an unexpected charge or a more costly bill than anticipated. How much extra should you have? It depends. For some people, a couple hundred extra dollars may be ideal. But for others, it may be a good idea to include a few hundred or up to an extra $1,000 in their checking accounts for extra wiggle room.But don’t keep every last dollar you have in your checking account. If you do, you’ll miss out on interest. Instead, move your extra savings into a bank account that accrues interest. With an interest-earning bank account, you’ll get rewarded as your cash sits in the bank. You could earn money with a savings accountMany people keep extra cash in a savings account. Review the bank’s annual percentage yield (APY) when considering a new savings account. This rate is the amount of money or interest you’ll earn over a year. The higher the APY, the more money you can make. You can take advantage of an attractive interest rate by opening a high-yield savings account. At the time of writing, the bank accounts on our best high-yield savings accounts list offer APYs ranging from 4.30% to 5.26%. If you have a significant amount of extra cash and keep it in an account like this, you can earn money without doing extra work. $5,000 in savings accumulates this much interest To determine how much interest you can earn by moving your extra cash to a savings account, multiply your initial deposit by the APY your bank account offers. This will show you how much interest you can earn by keeping your money in the bank for a year. Let’s imagine you have $5,000 extra sitting in your checking account right now. If you instead move that money to a high-yield savings account with an APY of 5% and you keep it in the bank for an entire year (and your APY doesn’t change; note that banks can raise or lower APYs at any time), you’ll earn $250. That’s much better than making $0 by keeping your savings in a checking account that doesn’t accrue interest. Now you can see why it pays to avoid keeping all your money in a checking account. You can earn extra money from interest by keeping your spare cash in a savings account that offers interest. For additional tips like this, check out our free personal finance resources.

3 Reasons I Don’t Like Aldi as Much as I Used To

By: Maurie Backman |

Updated

Sept. 13, 2023 – First published on Sept. 13, 2023

At some point in 2022, I discovered Aldi and began shopping there weekly. I found that I was able to save money on my grocery bill by purchasing certain produce items there. And since I happen to have an Aldi adjacent to my local Costco, it wasn’t particularly out of my way.But over the past few months, I’ve become less enamored with Aldi. Here’s why.1. The selection is just too limitedAldi — at least near me — is a minimally stocked grocery store. The shelves aren’t loaded the way they are at my nearby ShopRite and Stop & Shop.To be fair, this was the case when I first started shopping there. But because there’s just not a lot of selection, I’m generally limited to only buying a few items when I pop into Aldi.Not so long ago, I was running into Aldi for some fruit, which I usually buy there, and I needed to grab shredded cheddar cheese. Normally, I get that at Costco, but I didn’t want to run next door to Costco and wait in a line for cheese alone. Unfortunately, though, Aldi didn’t have the cheese I needed, so I had to make an extra stop anyway.2. The inventory is too inconsistentNot only is there a limited selection of food items I can buy at Aldi, but sometimes, I can’t even find the five or six things I’m looking for. Aldi was once my go-to source for avocados, since it’s an expensive purchase and Aldi tends to sell them for less than Costco (at least in my area). But the last few times I stopped at Aldi, avocados weren’t in stock.And that’s happened to me with other things, too. Over the past several months, I’ve struggled to find everything from cucumbers to strawberries at Aldi as well.3. What the store saves me on groceries, I lose via lost working hoursShopping at Aldi still has the potential to save me a little money on groceries. At a time when supermarket prices are up 3.6% on an annual basis, that helps.The problem, however, is that even though Aldi is right near Costco in my neighborhood, thereby allowing me to combine those trips, it still takes time to visit an extra supermarket. I have to find parking, wait in a checkout line, and spend time searching the shelves.While it’s nice to save $2 here and $3 there, the reality is that a stop at Aldi might cost me 20 or more minutes of work — especially when I don’t manage to find the things I need. And losing out on that work time often means forgoing more than $2 or $3 of income. So from a time perspective, it’s just not worth it.Shopping at Aldi could make sense for a lot of people. If you’re someone with flexibility in your schedule and grocery list, and you’re not so picky about the brands you bring home, then it could pay to spend the time visiting Aldi, even if you don’t always manage to find all the things you need. But I’ve reached the point where shopping at Aldi makes less and less sense for me, so I’ll most likely stop going there unless it’s a one-off basis.

7 Little-Known Gift Cards You Should Always Buy at Costco

By: Steven Porrello |

Updated

Sept. 29, 2023 – First published on Sept. 29, 2023

Costco gift cards are one of the warehouse’s best deals. Costco often will add 10% to 30% of value when you buy its gift cards in a bundle. It would be one thing if the gift cards were for places you’d never shop, like Bed, Bath, and Beyond (R.I.P.). But Costco gift cards are surprisingly varied and include many restaurants and retailers you’re probably already spending money with.So if you, like me, pinch pennies for your finances, here are seven gift cards you should always buy at Costco.1. Jiffy LubeCostco will add 25% of value when you buy a set of two $50 Jiffy Lube eGift cards for $74.99. While Jiffy Lube doesn’t offer the cheapest oil change on the market (Walmart will likely take the gold for that), its technicians do go through rigorous training via the Jiffy Lube University to ensure no accidental damage is done to your vehicle. If quality trumps price for your vehicle, this deal will save you $25 off your next oil change (limit of five per membership).2. Alaska AirlinesPacific Northwesterners will appreciate this deal — Costco will give you a $500 eCertificate to Alaska Airlines for $449.99. That comes to 10% off your next Alaska Airlines flight (limit of four per membership).3. Southwest AirlinesIf that was the first time you’d heard of Alaska Airlines, here’s a gift card package with a more familiar airline: Southwest. Costco will add 10% of value when you buy $500 of Southwest Airlines gift cards for only $449.99.4. Cinemark TheatresIn a great deal for moviegoers, you can buy a $50 Cinemark Theatres eGift card for only $39.99 at Costco. That’s an extra 20% of value that you can use for movie tickets, food, drinks, or merchandise (limit of 10 per membership).5. Miller PaintPainting your house ain’t cheap. Interior paint jobs will cost about $2 to $6 per square foot, according to the home improvement site HomeAdvisor, while exterior paint jobs can cost about $1.50 to $4 per square foot. To ease those costs, Costco will sell you $100 of Miller Paint gift cards for $69.99 — a whopping 30% of extra value.6. SpafinderIf you thought the cost of painting your house was bad, imagine how your back will feel after hours of painting walls. To ease that pain, Costco has an irresistible gift card deal: two $50 eGift cards for $79.99 to be used at thousands of spas and salons across the country. You can also use them at participating yoga and fitness studios (limit of 10 per membership).7. Synergy RestaurantsOne of the more interesting gift card packages I’ve come across, this extremely lucrative deal — two $50 eGift cards for a sticker price of $69.99 — will help you foot the bill at hundreds of local restaurants in numerous cities across Arizona, California, Colorado, Nevada, New Mexico, and Texas. This is perhaps one of the best deals I’ve seen and can be perfect for locals in those states and travelers who are visiting them.Most members don’t realize how many gift cards Costco actually sells. In fact, these seven packages only scratch the surface. Next time you’re at your local Costco warehouse, be on the lookout for gift card packages, which are often found at the ends of aisles. You might find a deal you can’t get anywhere else.

5 Amazing Costco Buys for Less Than $10

Costco is a favorite among bargain hunters. But because it’s a place where you typically buy in bulk, it’s often not great when you only want to spend a few bucks. Believe it or not, though, there are some deals at Costco for $10 or less. Here are five amazing Costco finds that will set you back no more than $10.1. Rotisserie chickenNot surprisingly, the $4.99 rotisserie chicken tops this list. Costco debuted its famed bird for $4.99 way back in 1994. It briefly raised the price by $1 during the Great Recession in 2008, then knocked it back down to $4.99 one year later. Had Costco raised its prices to keep up with inflation since 1994, that chicken would cost $10.48 today.Costco’s rotisserie chicken will always be a fan favorite for those looking for an effortless dinner. Just be aware: Costco keeps the prices low because its rotisserie chicken is what’s called a loss leader. The warehouse giant is willing to lose money selling them because it knows it can get customers into stores, where they’ll probably buy more than just a chicken.2. Hot dog and soda comboCostco has raised the prices of many of its food court items in recent years, but the price of one perennial favorite shows no signs of budging: the hot dog and soda combo, which has cost $1.50 since it debuted in 1985. Adjusted for inflation, the hot dog and soda combo should cost $4.28. Last year, during a quarterly earnings call, Costco chief financial officer Richard Galanti said the warehouse giant could keep the $1.50 price point “forever.”3. Kirkland Signature Creamy Almond ButterYou can use almond butter as a salad dressing ingredient, slather it on toast, put it in baked goods, or just eat it straight from the jar. If you’re the type who likes to devour almond butter by the spoonful, you don’t want to pass up a 27-ounce jar of Kirkland Signature Creamy Almond Butter, available for just $7.99. That works out to less than $0.30 per ounce. By comparison, a 16-ounce jar of Trader Joe’s Creamy Almond Butter Salted costs $6.99.4. Olde Thompson Kosher Sea Salt, 5 lbsSea salt has plenty of uses that go beyond cooking. You can use it for cleaning, as an exfoliant for your skin, and sprinkle it around your garden to keep unwanted bugs away. For just $5.99, you can score a 5-pound jar of Olde Thompson Kosher Sea Salt and keep it handy for all your household and kitchen needs.5. Bisquick Pancake & Baking Mix, 96 OuncesBisquick is another one of those things that’s handy to keep in your pantry. You can use it to whip up a quick batch of pancakes or waffles for breakfast or keep it on hand for a variety of baked good recipes. A 96-ounce box of Bisquick is available at Costco for $8.89. It’s normally priced at $10.99, but there’s a $2.10 manufacturer’s discount that’s good through Oct. 8, 2023.What are the best deals at Costco?Since Costco tends to sell large quantities, you’ll typically find that a lot of the best deals cost well above $10. Regardless of the exact price, it usually makes sense to buy products at Costco that have a long shelf life. For example, even if you find great deals on fresh produce and milk, you probably don’t want to load up on these items unless you’re feeding a large crowd, as they’ll go bad quickly.Also, make sure you look beyond the grocery department for savings. For example, getting your prescriptions from Costco Pharmacy or using Costco to fill up your gas tank could also save you money.If you want to maximize the benefits of your membership, try shopping with a Visa credit card that offers rewards. (Costco only accepts Visa credit cards.) That way you can earn travel rewards or cash back when you load up on groceries and other necessities.

5 Ways to Turn $100 Into Passive Income

By: Chris Neiger |

Updated

Oct. 1, 2023 – First published on Oct. 1, 2023

Creating passive income is one of the best ways to build wealth and protect your personal finances from an emergency, like losing a job or having your salary cut. According to U.S. Census Bureau data, about 20% of Americans have some level of passive income, with the average amount earned from passive income being $4,200 annually.Passive income strategies aren’t get-rich-quick schemes, and many initially require a significant time investment. The good news is that many can be started with $100 or less. Here are a few inexpensive ways you can start generating passive income.1. Buy stocksSome people think that owning stocks is only for rich people. It’s not. In fact, 61% of Americans own stocks, according to Gallup. And while you won’t get rich investing $100, you do have the potential to easily make money.You can open an online brokerage account for free and typically buy stocks for either little or no fees these days. The hard part is figuring out what company you think will do well over the long term so that you get the largest return.Let’s look at one popular company that many people own stock in: Apple. Let’s say you invested $100 annually over the past 10 years to buy Apple’s stock and reinvested any dividends you received to buy more shares. Thanks to Apple’s phenomenal growth over the past decade, your stock would be worth $4,848 — a 385% return on your investment.Of course, picking stocks can be difficult. If you want to potentially earn passive income in the market without picking specific stocks, you may want to buy shares of an exchange-traded fund (ETF). These funds follow market indices and can be purchased for as little as $1, thanks to online platforms that allow you to purchase fractional shares.2. Rent out an extra roomThis one is super easy and might cost you $0 if you already have the extra space. The latest Census Bureau data shows that 27.6% of Americans live alone. This means that many Americans may have a spare room in their home that could be transformed into a passive income stream.While it’s not for everyone, renting out a room in your home could be one of the easiest ways to generate passive income because you’re already in the space — either renting or as a homeowner — so all you need to do is find a roommate and collect their rent payments.This could be a very lucrative way to boost your income, considering that rent prices have skyrocketed over the past few years.3. Rent out your carWith 13% of full-time Americans working from home right now and 28% on hybrid schedules, many cars are sitting unused throughout the work week. With some planning and effort, your vehicle could quickly begin generating income through car-sharing websites like Turo.You can list your vehicle on the site for free and pay Turo a fee when you’ve rented out the vehicle. Turo says the average annual income for one car on its site is $10,516. Of course, some work is required to keep the vehicle clean and coordinate pick-up and drop-off. Still, renting out your vehicle could be a low-cost way to earn semi-passive income.4. Create an online courseMany people have accumulated many skills through jobs and even hobbies. You likely know how to get certain things done that someone else would find very useful — and pay for.There are many online platforms — including Udemy, Skillshare, and Thinkific — where you can create your own professional course and then sell it to an established online audience.You’ll need to do a fair amount of work upfront creating your course — including planning the sessions, recording videos, and making other content — but once you have it up and running, you can earn passive income from your hard work.Some course-creating platforms charge a monthly fee, while others may take a percentage of each sale you make. But while this option isn’t free, it’s certainly inexpensive.5. Start a dropshipping businessThere are many different businesses that fall under the dropshipping category, including selling T-shirts online or print-on-demand content like notebooks and journals.The startup cost for dropshipping businesses is low because you don’t buy any inventory and don’t have to rent an office or retail space. Instead, you’ll spend money setting up a website and potentially selling ads to market your products. You can even become a seller on Amazon and sell products without investing in your own online shop.You’ll have to invest significant time on the front end to build your business. Still, once you’ve found a niche and have established the relevant products, dropshipping allows you to spend minimal time keeping up the business while still making online sales.Keep these things in mindWhile all of these ideas will cost you little money and have the potential to generate passive income, you’ll still need to invest time and mental energy in setting them up. For example, you may need to do a lot of research before setting up a dropshipping business or launching an online course.Like anything worthwhile, be patient and take small steps to get started. You likely won’t be an overnight success, but making any progress toward generating passive income will move you further toward your personal financial goals.

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience. There are many ways to make money online, and as a teenager, you may be interested in learning how you can as…

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience.

There are many ways to make money online, and as a teenager, you may be interested in learning how you can as well.

Whether you are 13 years old or 19 years old, there are many different legitimate online jobs for teens that you may be interested in learning more about.

Related content:

Online Jobs For Teens

There are many online jobs for teens listed below. If you want to skip the list, here are some virtual jobs for teens that you may want to start learning more about first:

Start a website

While I was around 21 years old when I started my blog, I know of a few people who started theirs as teenagers.

A blog can be a great online job to start when you’re young, as you can decide how to build your blog, how you earn an income, and the schedule you put toward it.

Blogging has allowed me to travel full-time, work from home, have a flexible schedule, earn a high income, and love what I do.

You can easily learn how to start a blog with my free How To Create a Blog Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog today

Day 2: What topic to blog about

Day 3: Tutorial on how to start a blog on WordPress

Day 4: How to make money with your blog

Day 5: How to make passive income on your blog

Day 6: How to get pageviews to your blog

Day 7: Tips to see success with your blog

Out of all of these online jobs for teens, blogging is by far my favorite. It does take a little more time to start making money, but it’s very flexible and fits with any kind of schedule.

Create a TikTok account

You have most likely heard of TikTok.

There are over 1.5 billion users on TikTok, and many people are able to earn an income on this social media platform doing many different things.

From personal finance tips to comedy, day in the life to travel, and more, there are many different topics you can cover on your own TikTok account through making social media content.

If you want to learn how to make money online for teens, this is a fun one.

You can learn more at How I Make Money On TikTok – How I Grew To 350,000 Followers and Made $60,000 In 6 Weeks.

Begin a YouTube channel

Everyone has heard of YouTube, and pretty much everyone has watched at least one YouTube video in their life.

In fact, according to YouTube, there are over 2 billion people who watch at least one video on YouTube each month.

Many people have goals of starting a YouTube channel and making money, but not many people ever actually start.

You can learn more at How I Grew From 0 Subscribers To Over $100,000 On YouTube In Less Than One Year.

Resell items online

If you are looking for a flexible job as a teenager, one to look into may be reselling items online, such as on Craigslist, eBay, or Facebook Marketplace. There are many other online marketplaces as well.

Plus, it’s something that anyone can start because many of us own things that we could probably sell.

And, there are always things that you can buy for a low price and possibly resell for a profit. Or, you may even be able to find free things that people are throwing away and sell that as well.

This is such a profitable idea that my friend was able to make $133,000 in one year through buy-and-sell flipping and with working only 10-20 hours per week.

Since then, they have turned this into an even bigger and more profitable business!

Some of the best items that they’ve resold include:

Something they bought for $10 and flipped for $200 just 6 minutes later

A security tower they bought for $6,200 and flipped for $25,000 just one month later

A prosthetic leg that they bought for $30 at a flea market and sold for $1,000 on eBay the very next day

A lift that they found in the trash (and asked the owner for permission to take) that they sold online for $7,500

You can learn more at How I Made $40,000 In One Year Flipping Items.

They also have a helpful free webinar, Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business In As Little As 14 Days. I recommend checking it out.

Sell printables on Etsy

If you are looking for a way to make money at home and be your own boss, then creating printables may be for you.

A printable is a digital product that can be downloaded and printed at home. You make them once and then sell them on a website such as Etsy for people to buy. You wouldn’t have to print anything, instead, you are simply selling the download.

Items such as grocery shopping checklists, weekly meal plans that someone puts on their fridge, gift tags, and quotes to be framed are all printables.

This can be a great way to make money at home as a teenager because you create one digital file download per product, and you can then sell them an unlimited amount of times.

You can sign up for this free ebook that helps you figure out where to start when it comes to selling printables on Etsy.

I recommend reading about this further at How I Make Money Selling Printables On Etsy to learn more about one of the best jobs for stay-at-home moms.

Note: Etsy account owners must be at least 18 years of age to sell on Etsy. If you are between the ages of 13 and 17, you can sell on Etsy if you have the appropriate permission and direct supervision of your parent or legal guardian. Your Etsy account must be registered with the parent or legal guardian’s information.

Create and sell stickers

Another fun way to make money online as a teenager is to sell stickers.

My friend started with no graphic design skills and didn’t even know how to create stickers when she first started. It’s something she learned as she went, and she now earns over $100,000 each year with her sticker business.

I interviewed her here on Making Sense of Cents and she answered questions such as:

Do I need to be a graphic designer to make and sell stickers?

Why do people buy stickers online?

Do stickers sell well online?

How much money can I make selling stickers as a small business idea?

You can head over to How To Make $1,000+ A Month Selling Stickers Online to read more.

Make Canva templates

Canva is an online graphic design website. On Canva, you can sell premade designs to other Canva users so that they can edit and customize them.

Some examples of Canva templates include ebooks, workbooks, Pinterest pins, and more.

Creating Canva templates can be a great way to make extra money because you just need to create them once, and you can sell them an unlimited amount of times.

People all around the world use Canva to help with the graphic design side of their business, and templates make their lives so much easier.

Working just a few hours a week, I know someone who is able to earn $2,000 each month from selling Canva templates from home.

Do you have questions such as:

What is a Canva template and what is Canva?

Why would someone buy Canva templates? What is the benefit?

I have no tech skills, can I still create and sell Canva templates?

You can head to this article to learn more at How I Make $2,000+ Monthly Selling Canva Templates.

Voice over acting

Voice-over actors are of all ages, and you probably hear them all the time!

A voice-over actor is the person you hear but usually do not see on radio ads, YouTube videos, documentaries, e-learning courses, audiobooks, TV commercials, video games, movies, and cartoons.

This job doesn’t require previous experience or special skills – you just need to have the voice the company is looking for.

You can learn more about how to become a voice-over actor at How To Become A Voice Over Actor.

Answer online surveys

Not too long ago, one of the ways I made extra money to pay off my student loan debt was by answering paid online surveys.

You will not get rich from taking surveys, but it can help you to earn a little bit of extra money in some of the spare minutes that you may have throughout the day. Plus, you may get free items occasionally to review as well.

Companies will pay you to take surveys because they want to see what people think of their product and their company. They seek out real opinions from real people.

Here are some of the survey companies that are open to teenagers (along with their minimum age requirements):

American Consumer Opinion – Age minimum – 14 years old

Survey Junkie – Age minimum – 12 years old

MyPoints – Age minimum – 13 years old

Branded Surveys – Age minimum – 16 years old

Swagbucks – Age minimum – 13 years old

InboxDollars – Age minimum – 12 years old

Pinecone Research – Age minimum – 18 years old

User Interviews – Age minimum – 16 years old

Some of the above will even pay you to review music, play video games, or test mobile apps as a part of their research.

Sell items on Amazon

We have all heard of Amazon.

It is a website full of items sold by people like you and me.

In the first year that my friend Jessica’s family ran their Amazon FBA business together, working less than 20 hours a week total, they made over $100,000 profit!

You can learn more by reading How To Make Money From Home Selling On Amazon, such as answers to questions like:

How Jessica started selling on Amazon FBA

What exactly Amazon FBA is

How to choose what to buy and sell

How much a person can expect to earn

The positives of selling on Amazon, and more

Customer service support

If you are looking for a more traditional style of online job, such as working for someone else, then finding a customer service representative job may be something to look into. This way, you can start earning money right away, right after you get hired, instead of attempting to build a business.

There are many companies that hire for customer service support at home, even if you are young. Most will want you to be at least 16 years old or 18 years old to start.

As a customer service representative, you may be responsible for tasks such as:

Answering questions from customers about a product

Troubleshooting and helping with issues that a customer may have with a product

Processing orders

Assisting with returns

Handling feedback and customer complaints

And so much more.

Virtual assistant

As a virtual assistant, you would be helping a person or small business owner with administrative and business tasks. You would be their assistant but working in your own home instead.

I have been a virtual assistant in the past, and I now have virtual assistants of my own. They are lifesavers!

You do not need to have previous experience in order to start as a virtual assistant, instead, you need to be willing to learn so that you can help a business run more smoothly.

Many, many people and companies are looking for virtual assistants, as they play such an important role.

As a virtual assistant, you may be able to start at around $15-$20 an hour, or even much more. This will depend on the type of work you are providing, the experience that you have, the field you will be working in, and more. As a full-time virtual assistant, you may be able to earn over $10,000 a month once you gain experience.

As a virtual assistant, you may be doing tasks such as:

Managing a company’s social media accounts, such as by being their social media manager

Managing a person or company’s calendar

Scheduling appointments or travel

Creating or assisting with slideshows or presentations

Email management

Communicating with clients or customers

And so much more.

Different companies and employers will need different work to be done – it simply depends on who you will be working for and what they need to be completed.

You can learn more at How I Earn $10,000 Per Month From Home as a Virtual Assistant.

Start an online store

I feel like so many young adults are starting online stores, and it completely makes sense.

It’s something you can do from home, and there are ways to do it that don’t involve storing inventory or taking up a large amount of your valuable time.

Plus, you can make extra cash or even a full-time income.

And, there are so many different things that you can sell online.

From pet items, skincare, fitness products, subscription boxes, and accessories, to clothing, crafts, and more, the list is endless.

You can learn more about this topic at How I Make Over $10,000 Monthly With My Online Store In Less Than 10 Hours Per Week.

Write an ebook

Yes, you may be able to make extra money as a teenager by writing an ebook, and you can do it all from your home.

Anyone can write an ebook, no matter how young you may be.

There are many different genres that you can choose from, such as fantasy, fiction, nonfiction, mystery, and more.

If this is one of the online jobs for teens you’d like to learn more about, read How I Make $200 Each Day In Book Sales.

Find online tutoring jobs

Are you looking for a flexible side hustle as an online tutor?

If there is a subject that you are knowledgeable in, such as math, English, science, etc., then you may want to see if you can find students that you can tutor.

To become an online tutor, you can simply create a tutor profile on a tutoring platform, create a listing on Fiverr, reach out to people that you know, and more.

Learn more at The Best Online Tutoring Jobs – A Flexible Way To Make More Money.

Freelance write

Becoming a freelance writer can be a great online job for teens because there is a growing number of jobs out there for freelance writers, and many people start with no previous experience.

A freelance writer is someone who writes for a number of different clients, such as a website, blog, magazine, and more.

You can learn more in the article How To Become A Freelance Writer.

Proofread

If you have a passion for reading and often find mistakes in written content, then you may want to learn how to become a proofreader.

Freelance proofreading is a flexible and detail-oriented job that only requires a laptop or tablet, an internet connection, grammar skills, and a good eye for finding mistakes.

Proofreaders look for punctuation mistakes, grammar, misspelled words, lack of consistency, and formatting errors.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

Tips for online jobs for teens

Below, I want to share some tips for you on how to manage an online job for high schoolers. Having an online job as a teenager means that you may have some questions, such as how to avoid scams, how to balance school and work, how to open a PayPal account when you are underage, and more.

How to avoid online job scams

While there are many, many legitimate online jobs for teens, there are scams as well. Due to that, I want to share my best tips so that you can avoid scams but still find an online gig.

Some of my tips to avoid scams:

Research the company and the position to make sure they are real and a company that you would like to work for.

Search on the Better Business Bureau to learn more about the company and read their reviews.

Research the company online to see if there are any mentions of it being a scam. I like to type in “Company name + Scam” into a search engine and see what pops up.

Always be careful if the company asks you to pay money.

Before you give out any personal information, such as your social security number, you should make sure it is a real job that they are offering you.

Search the Federal Trade Commission and see if they have any press releases or articles about work-from-home job scams that they may have found.

Never click on any links or download anything in a suspicious email.

And, always trust your instincts! If something seems fishy, then trust yourself. There are always other jobs out there – do not feel like you have to take one that you are unsure about.

Simply move on and look for another opportunity that fits you.

Frequently Asked Questions About Online Jobs for teenagers

Below are common questions about online jobs for high schoolers.

How can a student work from home?

If you are a teenager, then you may still be in school. If you are trying to manage school and find a way to make money, then I do want to share some of my best tips.

After all, I have been in your shoes!

Working and going to school can be tough to manage.

Below is my advice for balancing both:

Realize what your motivation is for balancing both school and having a job. This is important because at times it will be hard to manage both, and thinking about why you are making yourself so busy can help to keep you motivated. You may even want to create a vision board so that you can look at it whenever things are tough so that you can easily remember what you are working towards.

Carefully plan out your school and work schedule. To balance school and work, then I recommend creating a carefully planned out schedule. This mainly only applies if you are in college or if you have control over the hours in your school day. This may include researching when the classes you need are offered and start trying to eliminate any gaps that may fall between your classes. Having an hour or two break between each class can quickly add up.

Bulk up your class days. If you think you can do it without overtiring yourself, then you may want to have as many classes together as possible in one day so that you are not constantly having to drive back and forth between school, work, and home.

Have a to-do list. I live and breathe by my to-do list. It helps me to not forget anything and to quickly realize that I have something to do (so I should stop procrastinating!).

Please head to 9 Ways To Successfully Balance School And Work to learn more.

How to open a PayPal account when you are a teenager?

If you are under the age of 18, then you will need a parent or a legal guardian to open a PayPal account. They would be the primary account holder, and you would simply be doing transactions through their account.

So, this means that you want to choose someone that you trust as they will have full access to the money that you are earning and is being transferred to your PayPal account.

How old do you have to be to work an online job? Can I work from home at 15? How can I make money at 17 without a job?

The age will vary depending on the job that you are looking to get.

How do you get paid with an online job for teens?

The way that you will get paid will depend on what you are doing.

If you are taking paid online surveys, for example, then you may get paid in rewards, a gift card, or even PayPal or check.

For more traditional jobs and gigs, you may be getting a paycheck every two weeks. If you are working for yourself, then you may be getting paid directly to your bank account.

How can I make money online as a teenager?

There are many ways to make money as a teenager, as you learned above. These include:

Blogging

TikTok creator

YouTuber

Reseller

Printables creator

Sticker maker

Canva templates designer

Voice-over actor

Survey taker

Amazon seller

Customer service representative

Virtual assistant

Online store owner

Author

Tutor

Freelance writer

Proofreader

And the list goes on and on!

Whether you are looking to make extra cash or if you are looking for a full-time job, there are many ways for you to earn money as a teenager.

Lastly, my final piece of advice is to make sure that your parents are informed of what you are doing. For your safety, I highly recommend telling your parents about your online job and keeping them updated about what is going on and if there are any changes.

Are you looking for the best online jobs for teens?

With a three-dimensional cubist design, the Ezra natural rye wood bar cabinet is a functional piece of art. $2,299 at Crate & Barrel, 4820 Massachusetts Ave. NW, Washington, D.C.; 202-364-6100; crateandbarrel.com

Credit: Courtesy photo

Blanket Statement

Snuggle up on a chilly fall evening with this handwoven corded throw. $60 to $65 at West Elm, 951 Rose Ave. (Pike & Rose), North Bethesda; 301-230-7630; westelm.com

Credit: Courtesy photo

Bowled Over

Handcrafted and hand glazed, the ceramic Frasier bowl adds an organic element to a coffee table, nightstand or side table. $129 at Pottery Barn, 4750 Bethesda Ave., Bethesda; 301-654-1598; potterybarn.com

arhaus.com

Credit: Courtesy photo

Up Against The Wall

Textured wallpaper—and natural grass cloth-inspired designs in particular—have made a big comeback in recent years. York Wallcoverings’ Line Stripe, from the New Origins collection, features a metallic thread in a horizontal design. $130 per double roll through Sherwin-Williams, 4809 Auburn Ave., Bethesda; 301-654-7955; sherwinwilliams.com

Credit: Courtesy photo

Soft Slumber

Cozy velvet bedding is a fantastic seasonal switch for fall. Rich in texture and color, the Delwood quilt is made from washed cotton velvet with channel quilting and features a lightweight linen backing. $348 to $448 at Serena & Lily, 7121 Bethesda Ave., Bethesda; 240-531-1839; serenaandlily.com

Advertisement

This story appears in the September/October issue of Bethesda Magazine.

If you’ve got a home equity line of credit (HELOC), you’ve likely seen your interest rate rise significantly over the past year and change.

The reason being is HELOCs are tied to the prime rate, which moves in lockstep with the fed funds rate.

Since early 2022, the Federal Reserve has raised its target rate 11 times, pushing the prime rate up from 3.25% to 8.50%.

This means homeowners with HELOCs have seen their rates increase 5.25% in just over a year.

But here’s the good news; we could already be looking at peak HELOC rates and relief as soon as early 2024.

The Odds of Another Fed Rate Hike Are Now Lower Than a Fed Rate Cut

While the financial markets are dynamic and always subject to change, data is now signaling that the Fed rate hikes are done.

And even better, that a rate cut is on the horizon in early 2024.

The CME FedWatch Tool, which tracks the likelihood that the Fed will change its target rate at upcoming FOMC meetings, no longer has additional rate hikes as odds-on favorites.

Instead, it has a rate cut as the most probable next move slated for the June 2024 Fed meeting.

In the meantime, rates are largely expected to remain unchanged, though a rate cut could arrive even sooner.

These percentage probabilities are based on interest rate trades by major brokers in the market for overnight unsecured loans between depository institutions.

As noted, the forecasts are subject to change (and do change constantly), but the data appears to be tipping more and more in favor of rate cuts instead of hikes.

In the chart above, you can see that rates are expected to be unchanged during the next five Fed meetings (light blue boxes).

But in June 2024, the odds are now on a 0.25% rate cut, with a 38.7% likelihood, versus them holding steady at 24.5%.

Interestingly, even a .50% rate cut has higher odds at 24.8%, meaning the odds of a cut are pretty strong by then.

Depending on how things pan out, a rate cut could come even sooner, with a 0.25% cut holding odds of 38.5% in May vs. holding steady at 38.9%.

If we look at total probabilities, there’s a better chance of rates easing vs. hiking by the March 2024 meeting.

And it continues to get rosier and rosier for interest rate cuts through the end of 2024.

HELOC Rates Could Be 0.75% Lower by Late 2024

All said, the fed funds rate could end 2024 in a range of 4.50% to 4.75%, which would be nearly 1% below the current range of 5.25% to 5.50%.

Because the prime rate is dictated by the Fed’s hikes and cuts, that would push HELOC rates down by the same amount, so 0.75% if these odds come to fruition.

It might not spell major relief, but it would be some relief. And monthly payments would begin falling for the many homeowners holding these adjustable-rate second mortgages.

HELOC rates are determined by combining a pre-set fixed margin and the prime rate, which we know can adjust up or down.

So a hypothetical borrower with a margin of 1% currently has a HELOC rate of 9.50%, factoring in the current prime rate of 8.50%.

If these rate cuts do materialize, and the prime rate falls to 7.75%, they’d eventually have a rate of 8.75%.

This would result in a lower monthly payment and less interest due, and perhaps peace of mind seeing their rate fall as opposed to rise for a 12th time in less than two years.

What About Mortgage Rates and Fed Rate Cuts?

While the fed funds rate does not dictate mortgage rates, it can play an indirect role.

Simply put, if the fed funds rate starts falling because the economy is slowing, it could signal lower long-term rates over time.

That would result in lower mortgage rates as well, as a cooler economy and lower inflation can bring down bond yields.

Additionally, more certainty from the Fed could also result in a narrower mortgage rate spreads, which have nearly doubled in recent years.

So we might also conclude that first mortgage rates, along with HELOC rates, are nearing or at their peak too.

Of course, mortgage rates might take some time to come down and could remain “sticky” at these new higher levels.

Still, any relief is welcomed at this time with 30-year fixed mortgage rates approaching 8% levels.

The good news is we might be finally seeing peak interest rates this cycle, though there’s still reason to be cautious as economic data continues to flow in.

Any surprises could derail these current estimates, though they do seem to be finally moving more decisively in the right direction.

The return of the sub-5 per cent five-year residential fixed rate is “now looking imminent” Coreco managing director, Andrew Montlake, has argued.

Montlake explained that, with mortgage lenders “battling” for market share “we can expect to see continued rate and criteria improvements over the next quarter”.

It comes as The Mortgages Works announced a five-year fixed rate deal at 4.99 per cent, with a 3 per cent fee.

This is the first sub-5 per cent deal brokers have seen for months and is consistent with falling Swap rates.

Montlake added that the market could be about to “scale the peak of the recent interest rate cycle”, with one more rate rise to 5.5 per cent already “hard-baked” into mortgage pricing, therefore having little impact on rates.

This should be good news for borrowers of all kinds as we head into 2024Blue Fish Mortgage Solutions owner, Ross McMillian

However, Montlake acknowledged that “much now rests on the next inflation report” and “we can only hope that the Monetary Policy Committee opts to pause, or at most raise by 0.25 per cent.”

A similar sentiment was shared by other brokers such as KAG Financial director, Kylie-Ann Gatecliffe, who added: “With Swap rates reducing and the completion between lenders heating up, I believe we will continue to see rates fall.

She additionally stated that this would be the case even if the bank rate increases by 0.25 percentage points, which she described as “great news for the market”.

Inflation is key

R3 Mortgages director, Riz Malik, also predicted that mortgage rates will continue to fall even with a 25 basis point increase at the next Monetary Policy Committee meeting, so long as there are “no nasty surprises in the inflation print”.

He explained that a “hold” decision would shake the market and result in “substantial” cuts.

Blue Fish Mortgage Solutions owner, Ross McMillian, also highlighted the importance of the next inflation report stating: “Inflation remains the key measurement.”

He added that as long as this maintains or improves on the downward trend seen last month then confidence that “we are over the peak of the rate mountain should gain momentum”.

As a result of this, McMillian suggested that lenders are likely to “really begin to fight” for their share of the “diminishing” market.

“This should be good news for borrowers of all kinds as we head into 2024,” he predicted.

This sentiment was shared by EHF Mortgages founder, Justin Moy, who said: “Even if the base rate were to increase by 0.25 per cent, mortgage lenders would look to continue to make small cuts, if only to attract more applications.”

Moy added that “this is especially the case in the buy-to-let market.”

It’s the most wonderful time of the year. Make it even more memorable with these holiday party ideas.

The minute the leaves begin to change color, we all feel a slight shift towards the holidays. The crisp, cool air combined with the anticipation for the upcoming holidays brings an unmistakable cheer.

With so much to look forward to between the holiday festivities, gifts and delicious fall and winter food and drinks, it’s easy to fall into your typical holiday party patterns. If you’re hosting a party or yearning to step into the role of host this year, ensure your soiree doesn’t lack originality. Here are a few themes to try and how to pull each one off seamlessly.

8 creative party themes for the perfect holiday celebration

The best way to spread holiday cheer is by partying loudly for all to hear. These party ideas are sure to elevate your holiday gatherings and make your celebrations unforgettable. You may even start some new traditions along the way!

DIY craft night

Some of the most memorable nights are small, casual get-togethers where crafting takes place. Hosting a holiday-themed DIY craft night sets the stage for great memories to be had and fun creations to be made. Provide supplies for guests to make their own holiday decorations, ornaments or wreaths.

For the more experienced crafters, you can even dare to try making scented candles. This theme is perfect for those who enjoy getting creative and taking home a handmade keepsake.

Gatsby-inspired glam holiday party

The holiday season is a fabulous excuse for people to dress up, especially for a themed party. A Gatsby-inspired glam party challenges guests to channel the aesthetic and fashion of the roaring ’20s.

The combination of jazz music, art Deco-inspired decorations, prohibition-themed cocktails and a strict 1920s dress code is sure to transport your guests back in time. Due to the glitz and glam that naturally surrounds the fashion and influence of this era, this theme would make for a perfect New Year’s Eve soiree.

Ugly sweater party

This party theme is a holiday favorite, and for good reason. Guests are instructed to dig up their cheesiest holiday sweaters and prepare for a fun night of catching up with friends, drinking holiday-themed cocktails and snacking on their favorite appetizers. Adding board games into the mix will only enhance the merriment. Encourage guests to bring a dish to share and their best-judging hat, as the guests will determine the tackiest sweater of the night.

Cocktail holiday party extravaganza

A craft cocktail party is a timeless gathering, but for the purpose of this list, add a seasonal twist. Guests invited must bring a winter-themed cocktail like spiced rum punch, sugar cookie martini, white Christmas margaritas or jingle juice, just to list a few.

Offer guests two choices for participation: they can either craft their cocktails on-site during the party or bring a larger batch of their signature cocktail to share with everyone, ensuring that all can savor and appreciate each cocktail.

Disney holiday movie madness

The Disney universe has a plethora of holiday movies that are sure to get even the grinches of the world in the holiday spirit. Think movies like “Full-Court Miracle,” “Frozen,” “The Nightmare Before Christmas,” “CoCo” and “Home Alone.”