For the first time in about 15 months, the number of homes listed for sale increased on an annual basis — albeit by a very small amount, Redfin reported.

New listings rose by 0.3% for the four weeks ended Oct. 22 compared with the same time frame one year ago; this is the first rise since July 2022.

With the 30-year fixed rate mortgage averaging close to 8% last week, many potential sellers have decided those are unlikely to decline by a significant amount anytime soon, Redfin said. Another factor might be the impact on prices.

“Some people are selling right now because they’re concerned home values will go down, though that’s definitely not a foregone conclusion,” said Ali Mafi, a Redfin agent in San Francisco, in a press release. “Others are noticing an uptick in demand and testing the waters.”

Pending home sales increased unexpectedly in September, a report from the National Association of Realtors noted.

However, those now moving to list need to be realistic about pricing. “Even though there are a few more buyers out there, this isn’t 2021,” Mafi said.

Approximately 6.8% of properties for sale reported a price drop during the four weeks ending Oct. 22, the highest share on record, Redfin claimed.

Still for the period, the median sales price was $369,975, up 3.1% over the prior year, while the median asking price rose 5.4% — the biggest increase in a year — to $384,375.

“Prices are up partly because elevated mortgage rates were hampering prices during this time last year,” the Redfin press release said.

While active listings declined 12% from one year ago, to 841,697, this is the smallest annual drop since July.

The supply of homes for sale was 3.5 months, a 0.2 percentage point gain to the highest level since February, Redfin said.

The median time a home spent on the market was 33 days, a decline of 3 days, while the share of homes sold above list price 29.8%, up from 28% in August 2022.

Everyone was calling a housing bottom about a month ago, and there’s finally some data to back up the claims.

A new report from Zillow revealed that national U.S. home prices increased year-over-year for the first time since 2007.

Of course, the rise wasn’t all that mind-blowing at a paltry 0.2%, but the housing market wasn’t able to pull off such a seemingly small feat for five years.

So it means something, maybe.

Is It a Blip or Meaningful?

The data is based on home values from the second quarter of 2011 to the second quarter of 2012, and if the recent surge in home buying is any indication, the third quarter numbers should be even better.

In a press release, Zillow Chief Economist Dr. Stan Humphries said, “it seems clear that the country has hit a bottom in home values,” thanks to four months of solid gains.

During the second quarter, national home prices jumped 2.1%, with Phoenix leading the country with an impressive, if not troubling, 6% gain.

In fact, home prices are up 12.1% in Phoenix since the second quarter of 2011!

Other winners include the Miami-Ft. Lauderdale metro, which saw a 4.7% gain, and San Jose, where home prices increased 3.7%.

So it looks as if a lot of the hardest hit regions of the country are finally bouncing back to some degree. Even Las Vegas saw prices rise 2.5%, though they are still down 2% year-over-year.

However, one major metro, Philadelphia, still hasn’t bottomed, though it is expected to by year-end.

Aside from Zillow, a lot of big pundits and investment bankers are getting on the housing train as well, so could it be for real this time?

Still Lots of Risk to Housing Market

Humphries warned that there is lingering risk, thanks to foreclosures picking up steam and increasing inventory, which currently remains very tight in highly-sought after regions of the country.

Still, he expects most of the new inventory to get absorbed, thanks to more positive sentiment from consumers regarding housing.

But the big question remains whether there are enough qualified buyers (those who can actually obtain financing) to scoop up the homes as they come on the market.

Clearly there are a ton of former homeowners who aren’t eligible, thanks to their newly damaged credit. And then there are the many unemployed, who also can’t qualify.

This should subdue any tremendous gains in the near future, pointing to a slow, if not choppy, housing recovery.

There’s also the economy at large, which took another turn for the worse this week as European fears grew stronger. There’s even talk of another recession. Yes, it’s ugly out there.

So don’t expect to make millions in housing overnight. In fact, you might even see your new home purchase fall in value if this recent rally doesn’t hold, which makes you wonder if the low mortgage rates are a home buyer trap. But if you buy and hold, and exercise patience, you should be rewarded.

Read more: Is a 30-year fixed in 2% range possible?

A very large majority of home appraisers are being pressured to inflate property values, according to a survey conducted by Valufinders, a national provider of valuation services.

The company said 91 percent of those surveyed said they’ve been asked to pump up the value of the homes they appraise, while 81 percent worried they’d lose repeat business if they failed to bring in the desired result.

Some of the appraisers polled even expressed concern about losing a job if they didn’t provide a value to the client upfront, before the appraisal was ordered.

Nearly two-thirds (65 percent) said they were affected by the pressure to overvalue a property, indicating that integrity was undermined as a result of the constant competition.

“We’ve all been pressured to inflate values and loan officers are often ‘fishing for value’ with their ‘comp check’ requests,” said one appraiser who was surveyed.

At the same time, another appraiser expressed that he takes an “impartial approach,” and has no trouble telling borrowers the value of their home, good or bad.

Asked if their workload would be less burdensome if the mortgage industry adopted a facilitated appraisal process, just over half (52 percent) of respondents said yes.

In early March, the OFHEO unveiled the Home Valuation Code of Conduct, which would eliminate broker-ordered appraisals, prohibit appraiser coercion, and reduce the use of in-house appraisals come 2009.

As if you needed more evidence that it’s not a good time to buy a home.

The latest piece comes from the WSJ, which revealed that renting is 50% more expensive than buying.

This comes on top of a recent Fannie Mae survey that said home buyer sentiment matched an all-time survey low, with only 16% indicating it was a good time.

The culprit continues to be mortgage rates, which surpassed 8% last week and continue to erode affordability.

So is it better to hold off and keep renting or continue to house hunt?

It’s Not Always a Good Time to Purchase a Home

First off, it’s not always a good time to purchase a home, or condo for that matter.

Ultimately, there are better times and worse times, at least if we’re framing the question in terms of investment returns.

There’s also the sheer matter of affordability, which could jeopardize the transaction long-term if the buyer isn’t able to keep up with payments.

That’s essentially what transpired in the early 2000s, when home buyers with no business buying homes went through with the transaction regardless.

Often, this involved some creative financing and perhaps some stated income underwriting to get to the finish line.

In the end, while they qualified for the loan and closed on the purchase, they often didn’t make it past the first few mortgage payments before they fell behind.

Today, the situation is different because many of those questionable loan types, like stated income loans and option ARMs, no longer exist.

You can thank the Ability to Repay/Qualified Mortgage rule (ATR/QM Rule), which was born out of the prior mortgage crisis.

It requires lenders to “make a reasonable, good faith determination of a consumer’s ability to repay a residential mortgage loan according to its terms.”

That’s good news because it means fewer unqualified home buyers are getting approved for mortgages.

And more homeowners have safer loan products, such as the 30-year fixed, as opposed to an interest-only loan or something else that’s potentially high-risk.

Affordability Is a Problem No Matter How You Slice It

While the existing stock of homeowners has never been better, thanks to those aforementioned rules and the low, fixed interest rates they hold, it’s a different story for prospective buyers.

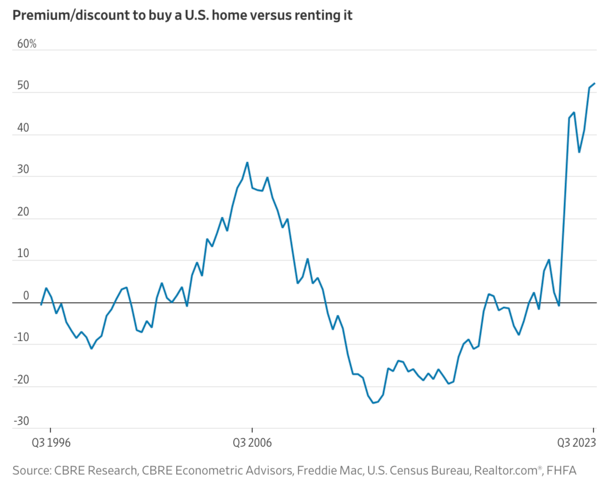

Today’s home buyer is looking at an average mortgage payment that is 52% higher than the average apartment rent, per a CBRE analysis.

This is the worst premium since at least 1996, and even well above the prior housing market peak in 2006 when it stood at 33%.

If you look at the chart above, it’s basically all because of the sharp rise in mortgage rates, which increased from sub-3% levels to around 8% today in less than two years.

That’s unprecedented movement, even if rates remain below 1980s mortgage rates. The bigger takeaway is the speed at which rates climbed higher.

We’re talking a near-200% increase in rates in less than 24 months. Meanwhile, home prices haven’t come down, thanks to a dearth of supply.

And a phenomenon known as the mortgage rate lock-in effect, where existing homeowners with 2-3% mortgage rates feel trapped.

Or are simply unwilling to move and take on a much higher interest rate.

Taken together, we have the worst home buying affordability in 30+ years history.

That buy versus rent premium is also up from 51.1% during the second quarter and 45.3% a year ago.

Again, this is largely due to higher mortgage rates, which have continued to climb higher throughout the year thanks to a stronger-than-anticipated economy.

It Now Takes Over a Decade to Break Even on a Home Purchase

Thanks to the big price tag on a home purchase these days, combined with high mortgage rates, it now takes over a decade to break even, per new data from Zillow/Axios.

The typical home buyer who puts down 3% on a $376,000 home purchase with a 7.045% mortgage rate won’t reach this point for 13.5 years.

This assumes a typical increase in home values, 3% closing costs, 1% in home maintenance fees, along with 6% closing costs and 6% agent commissions paid at time of sale.

In other words, you won’t be able to turn a profit until you’ve been in it long enough to whittle down the balance to offset all the associated costs.

Using that same purchase price, the loan balance would be about $285,000 after 13.5 years of regular monthly mortgage payments.

If the mortgage rate was 3%, the balance would be roughly $240,000 at that time because a lot more of each payment goes toward principal.

Someone who puts 20% down on a house can break even a bit sooner, at around 11.3 years, which is still about double the five-year timeline.

What does this say. That maybe it’s not a great time to buy a home, at least from an investment standpoint.

See: Rent vs. buy calculator

Should You Wait to Buy a House?

At this juncture, I don’t think anyone would call you crazy for pumping the brakes on a home purchase, though everyone has different reasons for buying.

And over time when you bought can matter less, assuming you stay the course (ask the 2006 home buyers who still own).

Aside from housing affordability being at multi-decade lows, the available inventory of homes is also quite poor.

Simply put, there isn’t a lot to choose from at the moment, and affordability stinks to boot.

At the moment, there are only about 2.5 months of supply at the existing sales rate, about half the normal 4-5-month level of for-sale inventory, per Redfin.

So despite the horrible lack of affordability, home prices are holding up just fine. In fact, the median sales price is up 1.9% from a year ago.

In other words, if you’re a prospective home buyer today, you might be looking at slim pickings, intense competition from other buyers, and an 8% mortgage rate.

That sure doesn’t sound like favorable home buying conditions.

Those who bought last year and more recently may have been told to marry the house and date the rate.

The argument is the house can be yours forever but the interest rate doesn’t have to be. The problem is mortgage rates have continued to go up.

So that advice hasn’t panned out so well for those who bought banking on refinancing to a lower rate by now.

This means if you do buy a home today, you need to be prepared to pay the mortgage rate you’re given.

Not a temporary buydown rate or a potentially lower rate in the future that may not materialize.

One compromise might be a hybrid adjustable-rate mortgage, which is fixed for the first five or seven years.

By then, hopefully mortgage rates drift over. If you believe the forecasts, they’re actually expected to drop by 2024. But that’s subject to change. And there’s still the question of just how much.

One worry along these lines is lower mortgage rates could be accompanied by lower home prices. And that could make it difficult to refinance if the mortgage is underwater.

In other words, if you buy today, you better be able to afford it. And you better really like the house.

Read more: 10 reasons to buy a house other than for the investment

High home prices and interest rates have created many challenges for young Americans.

But the boomer generation has fewer reasons to complain.

Many have benefited from high home prices and bond yields and are less hurt by the economy’s cons.

Loading

Something is loading.

less affordable than it’s been in decades, but many older Americans are benefiting from the economic environment.

According to the National Association of Realtors, US mortgage affordability is at the lowest level since at least 1989. As of June, the median American had to spend over 43% of their income to meet a mortgage payment on the typical US home, according to the Atlanta Fed, the third-highest monthly figure since 2006.

These trends have been driven by the combination of high home prices and interest rates. This month, the median US monthly mortgage payment hit a record high of over $2,600. In the second quarter of this year, over half of the US housing market saw record price increases. At the same time, the 30-year fixed mortgage rate is near a two-decade high, in part due to the Federal Reserve’s campaign to raise interest rates and cool inflation.

If you’re a young, aspiring first-time homebuyer, these developments may sound dismal. But if you’re a member of the baby-boom generation, the youngest members being about 60 years old, there’s a good chance you have fewer complaints about high home prices and interest rates.

Advertisement

Advertisement

Of course, many older Americans are also struggling in today’s economy, but high prices and rates are generally more advantageous to them than to younger generations. Insider breaks down the reasons below.

Rising home prices increase the wealth of existing homeowners

For the roughly 70% of US 18- to 29-year-olds who didn’t own a home as of 2021, per the Federal Reserve, high prices might’ve made homeownership feel unattainable. First-time buyers accounted for just 26% of US home purchases last year, according to the National Association of Realtors, the lowest share since data collection began in 1981. By pushing up the number of renters, high home prices help keep young Americans’ rent prices high.

For many older Americans, however, high home prices have been a boon to their finances.

As of 2021, 84% of Americans ages 60 and older owned their home. The rise in housing prices over the past few decades — and especially the past few years — has helped boomers accumulate more real-estate wealth than any other generation, a New York Time analysis of Fed data found.

Advertisement

Advertisement

As of the first quarter of this year, boomers held about 53% of total US household wealth, the Fed said. While many Gen Xers and millennials have bought homes over the past decade, they held only 28% and 6%, respectively — partly because they haven’t had as much time to see their home values grow.

Rising interest rates affect you less if you’ve already been locked in a loan payment

Boomers historically faced significant housing-affordability challenges of their own, but many were able to refinance at lower rates over the years. And with their fixed mortgage rates now locked in, the recent spike isn’t a problem for those still paying off their mortgages.

For young Americans, there’s not a whole lot to like about high interest rates.

Elevated rates not only contribute to the high mortgage rates that have helped make homeownership so expensive but also make credit-card debt all the more costly. Americans could pay an extra $45 billion in credit-card interest this year because of the increase in rates alone.

Advertisement

Advertisement

Students who took out federal student loans this fallwere strapped with the highest interest rates in at least a decade. Those with variable-rate student loans from private lenders could see their borrowing costs rise as well.

Meanwhile, the average monthly car payment in the US reached a record high of $733 in the second quarter of this year, driven in part by elevated interest rates.

Older Americans aren’t immune to credit-card debt, but few are taking out student loans at this point in their lives. While some are purchasing new vehicles, many locked in a lower car payment years ago.

High interest rates boost low-risk investments for retired boomers

One of the most common pieces of investing advice for older Americans and retirees is to shift at least some savings away from lucrative but risky investments in the volatile stock market into more-stable but typically lower-yielding bonds.

Advertisement

Advertisement

Generally, investors are forced to accept a much lower return in exchange for bonds’ lower risk, but in today’s high-interest environment, many boomers have been able to have something close to the best of both worlds.

On Wednesday, yields on US government Treasury bonds reached the highest level since 2007. The rate of 10-year Treasurys was about 4.36%, up from a low of 0.32% in early 2020.

For younger investors eager to ride the stock-market roller coaster and grow their wealth over time, bonds are less attractive. Elevated interest rates, however, are weighing on the stock market because high Treasury bond yields have made investors less likely to dump money into stocks.

In the near term, US home prices are likely to continue frustrating young Americans and boosting the net worths of many boomers. High interest rates, meanwhile, are expected to persist, though experts say the Fed could begin cutting rates next year.

A home for sale in the Ashby Acres community in Phoenix on Sept. 6, 2023. (Photo by Kevinjonah Paguio/Cronkite News)

PHOENIX – High home sales prices and mortgage interest rates are squeezing out first-time home buyers from entering the market, especially as incomes have not kept up, housing experts say.

In 2020, the housing market was in a frenzy. High numbers of homes were selling, agents’ inventories were low and offers were frequently being made over list prices, said Jason Giarrizzo, a realtor with West USA Realty, who has been in the industry for 31 years.

Coming out of 2020, during the COVID-19 pandemic, the market continued to surge as people began buying real estate, Giarrizzo said. “We weren’t sure where the market was going to go, (if) it (was) going to plummet because of you know, the shutdown and everything, but it was quite the opposite.”

A balanced market in the Phoenix metropolitan area would have inventory levels of about 30,000 properties, Giarrizzo said, but by the end of 2021 inventory began to shrink to about 4,400 properties in the area.

Then, home prices hit a high and interest rates began to climb as the Federal Reserve started raising rates in an attempt to head off inflation. “In all my years of real estate, I don’t think I saw the inventory spike to the level that it did in such a short period of time. We went from 4,400 properties just coming into spring to almost 20,000 properties for sale by summer,” Giarrizzo said.

The downtown Phoenix skyline overlooks homes in the Willo Historic District in Phoenix on Sept. 6, 2023. (Photo by Kevinjonah Paguio/Cronkite News)

Now, the inventory is at about 13,000, which is still half of what a balanced inventory is for the Phoenix metropolitan area, Giarrizzo said.

As mortgage loan interest rates have risen, that frenzy has subsided, especially for the first-time buyers market, Giarrizzo said.

Mortgage loan interest rates vary widely based on factors such as the individual market, credit score of the buyer, price of the home, down payment, rate type, loan term and type.

The current average rate for a conventional 30-year fixed mortgage is at or below 8.063% for a $430,000 home in Arizona for a buyer with a credit score of 700-719 who puts 10% down, according to the Consumer Financial Protection Bureau.

Chris Giarrizzo, a mortgage loan officer at Lennar Mortgage, who has been in the industry for over 23 years and is married to Jason Giarrizzo, said many hourly workers are struggling to afford housing, whether it’s a home purchase, or even rent.

The median home sale price in the Phoenix metropolitan area in September 2023 was $435,700, according to Redfin, a real estate firm that tracks prices and trends.

“I actually wouldn’t say necessarily it’s a bad time to buy a home, it’s just a challenging time to buy a home,” Chris Giarrizzo said.

Although mortgage loan rates have been this high before, high sales prices are providing little relief to buyers, she said, and there’s no relief anticipated until possibly sometime next year.

The last time 30-year fixed mortgage loan rates reached 8% was in 2000.

It was a combination of people who moved to the state and people who had more disposable income following the pandemic shutdown that drove the market takeoff in the Phoenix metropolitan area in 2020, Chris Giarrizzo said.

“We weren’t out shopping and weren’t traveling, and so I’ll be honest, not only in my industry, but in several industries, people had said that they had never been as busy. … We were all working a lot of hours,” Chris Giarrizzo said.

A “perfect storm” of high demand, low interest rates and not enough inventory drove home values up, creating the frenzy of people paying over list price because there was so much competition, she said.

First-time homebuyers in the market

“You’ve got a lot of people that are just sitting on the sidelines right now, eager to jump in and buy their first home,” Chris Giarrizzo said.

Many people locked in low interest rates years ago, so even if it makes sense to move or downsize, they don’t, because they’ll be looking at interest rates of over 7%, Jason Giarrizzo said.

A February Realtor.com survey found that 82% of homeowners with existing low-rate mortgages feel “locked in.”

“Even though the frenzy is over, I don’t see a plummet in home values,” Jason Giarrizzo said. “We’re not going to see big spikes in inventory, I think, due to those people that have locked in on those low rates.”

Related story

Interest rates will eventually fall, but when and by how much is hard to predict, Chris Giarrizzo said, noting rates under 3% were largely pandemic-driven and will probably not be seen again.

In August 2021, the 30-year mortgage rate hovered around 2.8%, according to data from the Arizona Regional Multiple Listing Service.

“If we can get rates back into the fours or fives (percent), I think we’ll see a start to return to a more balanced market,” Chris Giarrizzo said.

In northern Arizona, where Jason Giarrizzo also sells real estate, the properties are being sold more quickly and at much higher prices, although there is still low inventory. “I’ve been working more in that $1 million to $2.5 million range, and actually I’m seeing a lot of those deals go in cash,” he said.

But in Payson, and other nonluxury home markets in northern Arizona, the same housing squeeze is being felt, where the housing is largely unaffordable due to the combination of rates and list prices, Chris Giarrizzo said.

J Cruz, a 46-year-old Phoenix park ranger, started his home search two months ago and does not see a light at the end of the tunnel.

“Trying to find a good deal – that’s been very hard and challenging,” Cruz said. “Monthly mortgage payments are way too high for what I want, and it’s not feasible to pay that every month.”

He fixed his credit score, saved for a down payment and recently started the process of getting a home loan.

But mortgage interest rates are one of the things holding Cruz back. “I don’t want to get into a home that I can afford for a few months and not be able to afford two years from now,” he said.

Cruz is in search of a three-bedroom home in Phoenix, Peoria or Glendale, and even though he is a full-time city employee and has good benefits, he and many of his co-workers have part-time jobs to make ends meet.

“Even though we have a full-time job with the city, you know, in today’s economy it is still a little bit hard,” Cruz said.

New-build financing at interest rates lower than market rate is probably the best route for a lot of first-time buyers, especially if they are struggling to qualify, Chris Giarrizzo said.

Federal Housing Administration loans are available for first-time homebuyers, with down-payment options as low as 3.5%.

Zillow Home Loans is offering a 1% down payment incentive to buyers in Arizona to reduce the amount of time that it takes for eligible buyers to save.

The program is intended for buyers who have kept up with high monthly rent payments but have not been able to save for a down payment.

“I would just advise borrowers that the less down you’re putting, the higher your (monthly) payments are going to be,” Chris Giarrizzo said.

This program can reduce the time needed to save for a down payment and provide another option for those who are otherwise ready to take on a mortgage payment

SEATTLE, Aug. 24, 2023 /PRNewswire/ — Zillow Home Loans announced its 1% Down Payment program to allow eligible home buyers to pay as little as 1% down on their next home purchase. This program is initially being offered on properties located in Arizona, with plans to expand to additional markets. With the 1% Down Payment program, borrowers who qualify can now save just 1% to cover their portion of the down payment and Zillow Home Loans will contribute an additional 2% at closing. The 1% Down Payment program can reduce the time eligible home buyers need to save and open homeownership to those who are otherwise ready to take on a mortgage.

Most markets are in the midst of an affordability crisis, and saving for a down payment remains one of the biggest barriers for many potential home buyers. This is especially true for first-time buyers, who are often paying high rents. Typical asking rent nationwide is $2,062, or 3.6% higher than one year ago and up 31% since the start of the pandemic. (The typical rent in the U.S. in February 2020 was $1,597.) The combination of record-breaking home price appreciation and rising interest rates means a majority of first-time buyers (64%) are putting down less than 20%, and one-quarter of first-time buyers are putting down 5% or less.

Zillow Home Loans’ 1% Down Payment program lowers the down payment barrier and increases access to the housing market for eligible borrowers. An analysis by Zillow Home Loans’ shows that by reducing the down payment burden to 1% of the purchase price, a home buyer looking to purchase a $275,000 home in Phoenix, Arizona, who makes 80% of their area’s median income and saves 5% of their income would need only 11 months to save for the down payment. By comparison, the same buyer who needed to save 3% of the purchase price would require two and half years (31 months) to save that amount.

“For those who can afford higher rent payments but have been held back by the upfront costs associated with homeownership, down payment assistance can help to lower the barrier to entry and make the dream of owning a home a reality,” said Zillow Home Loans’ senior macroeconomist Orphe Divounguy. “The rapid rise in rents and home values means many renters who are already paying high monthly housing costs may not have enough saved up for a large down payment, and these types of programs are welcome innovations in lowering the potential barriers to homeownership for those who qualify.”

Home buyers looking to purchase in the next year should take steps to research and prepare for getting a mortgage as they start on their home-financing journey. Among those steps:

Understand your credit profile: Credit scores are key to getting approved for a mortgage, but for many home buyers, understanding credit is complex.

Improve your credit score: Once buyers familiarize themselves with what’s in their credit report, they can take steps to pay down existing debts, pay bills on time, and review their credit report and dispute possible errors.

Avoid closing accounts: Don’t close an account to remove it from your report. Those accounts aren’t automatically removed and will continue to show up on your report.

Hold off on financing large new purchases: Wait to make purchases that need to be financed, such as a car, until after you close on a home. This type of purchase will impact your debt-to-income ratio, which will negatively affect the amount of home loan you qualify for.

Determine what affordability looks like: Once buyers have a good understanding of their credit report and their credit score is at least 620 (generally the lowest score accepted by mortgage lenders) it’s time to understand how much home they can afford. Use Zillow’s mortgage affordability calculator to customize payment details.

Zillow Home Loans’ 1% Down Payment program is currently available to eligible borrowers in Arizona, with plans to expand. Through the 1% Down Payment program, Zillow Home Loans will pay 2% of the down payment for eligible borrowers. The 2% is paid through closing and not as a payment to the borrower. Interested applicants should call 1-833-372-1449 to speak with a Zillow Home Loans representative to learn more about the program and determine if it’s the right fit for their circumstances.

About Zillow Group Zillow Group, Inc. (NASDAQ: Z and ZG) is reimagining real estate to make it easier to unlock life’s next chapter. As the most visited real estate website in the United States, Zillow® and its affiliates offer customers an on-demand experience for selling, buying, renting, or financing with transparency and ease.

Zillow Group’s affiliates and subsidiaries include Zillow®; Zillow Premier Agent®; Zillow Home Loans™; Trulia®; Out East®; StreetEasy®; HotPads®; and ShowingTime+™, which houses ShowingTime®, Bridge Interactive®, and dotloop®. Zillow Home Loans, LLC is an Equal Housing Lender, NMLS #10287 (www.nmlsconsumeraccess.org).

SOURCE Zillow Home Loans

For further information: Media contact: Jessica Drum, Zillow Home Loans, [email protected]

When the housing market was searing hot, buyers faced intense competition — bidding wars, cash investors, and buy/sell decisions made on rapid deadlines. Now that real estate has cooled, there are fewer homes for sale, two-decade-high interest rates, and stubbornly elevated house values.

It’s rarely easy to buy a home. And if you can find a house you love, the question becomes: Is now a good time to buy?

The 2023 housing market

Looking for the perfect time to buy? Fewer than one in five consumers surveyed by Fannie Mae in July 2023 thought that it was a good time to buy a home. Yet, timing the housing market is more complicated than timing the stock market. Which is impossible. There are few “just right” Goldilocks real estate markets.

But you’re not buying the market. You’re buying a house in a city, neighborhood, and block where you want to live. Hopefully, for quite a while.

Mortgage rates

We all know this story. Interest rates have risen — and mortgage rates are no exception. The Federal Reserve has been raising short-term interest rates for well over a year in an effort to shrink inflation — the rise in consumer prices. Not only do the Fed’s rate increases immediately lift short-term mortgage rates such as variable-rate loans, but they also tend to influence long-term mortgage rates upwards as well eventually.

And though we don’t live in a 2%-3% world these days, mortgage rates are near their 52-year historical average.

Since April 1971, the 30-year mortgage rate has averaged 7.74%, based on data collected by Freddie Mac.

Of course, that’s little comfort to homebuyers today who remember when rates were under 3% for much of 2021. Conversely, the highest rate on record was a whopping 18.63% in October 1981.

According to Zillow research, the trend of mortgage rates — whether interest rates are generally rising or falling — may influence whether existing homeowners would consider selling their existing house to move into another. With so many existing homeowners paying a much lower mortgage rate, the study found it would take rates to fall somewhere to between 4% and 5% before they would sell the home they’re in and buy another.

This rate gridlock is contributing to the lack of existing homes for sale.

Take action: Consider the interest rate strategies below until (and if) mortgage rates fall significantly lower for an opportunity to refinance.

Home values

There is a little good news, though. Higher mortgage rates have softened the real estate market, and the increase in home prices is moderating.

The rise in existing home values is slowing. Home values are lower year-over-year in almost half (23) of the 50 largest metro areas, according to a Zillow analysis.

Take action: Look for homes with price reductions where you want to live. Then negotiate even harder.

But listings for existing homes are far fewer. For more than 12 months, new listings have been down year-over-year. The number of new listings of homes for sale is down more than 20% from pre-pandemic levels, according to Realtor.com.

Take action: Consider expanding your search to more affordable areas close to your favorite neighborhood if it’s too pricey.

New home inventory is rising. Construction of new homes is showing promise of growth, according to the U.S. Census Bureau. However, builders are still wary of oversupplying the market, concerned that consumer demand could sag as potential buyers shy away from rising mortgage rates.

Take action: If you want to buy a house now, consider new construction. You may be able to choose some finishes or make an even better deal on a spec home that’s been on the market for a while.

When is a good time to buy a house?

Buying a home is more than considering macroeconomic factors. It’s an important life decision based on your personal and financial situation.

Where do you want to be in 5 years?

When you rent, the decision to move is broken down into six months, or a year or two at a time, as your lease renews. But every dollar-related detail makes a home purchase a medium- to long-term investment. Buying a house includes various costs: the down payment, closing costs, and financing fees, moving expenses, property taxes, and perhaps selling your existing place.

Homeownership requires a years-long timeline. How you make a living, your friends, family, and even community amenities all come into play.

Your income

A primary consideration: your job. Will it require a location change anytime soon, or can you live where you please? Is your income steady and all but assured?

Your credit score

One of the significant factors that will qualify you for a home loan is your credit score. It’s important to know it before applying for a mortgage.

For the most common loan, a conventional mortgage not backed by a government agency, you generally need a FICO score of 620 or better.

FHA loans can allow a credit score as low as 580 with 3.5% down. VA loans issued to qualified military service members and veterans don’t officially have a minimum credit score, though some lenders will require a FICO score of 620.

As a benchmark to where you stand, the median credit score on a new mortgage in the second quarter of 2023 was 769, according to the New York Federal Reserve.

Of course, minimum scores are the entry-level to qualifying; the higher your score, the better the loan terms you’ll be offered. Most importantly, that can mean you’ll pay a lower annual percentage rate over the life of the loan. You may also have more room to negotiate on fees.

Your current debt load

A primary financial metric lenders will use to determine your creditworthiness is your debt-to-income ratio.

Fannie Mae, a government-sponsored entity that provides liquidity to the home loan market, looks for a maximum total DTI ratio of 36% of “the borrower’s stable monthly income.” Exceptions can allow for total DTIs up to 50%, but it’s usually best to avoid working on the edges of qualification if you can.

You can calculate your DTI by dividing your total recurring monthly debt by your gross (before taxes and other deductions) monthly income.

Include debt such as monthly mortgage payments (or rent), real estate taxes, and homeowner’s insurance. Also, add any car payments, student loans, and the monthly minimum due on credit cards. Remember any personal loan payments and child support or alimony.

Do not include debt such as monthly utilities — like electricity, water, garbage, or gas bills — or car insurance, television streaming subscriptions, or cell phone bills. You can also exclude health insurance costs and miscellaneous expenses such as groceries or entertainment.

Your savings

Having a cash cushion in the form of emergency savings shows lenders that you are prepared for the unexpected. Of course, that savings account should also include …

Your down payment

A large chunk of your savings account should be dedicated to the down payment. A minimum of 3% down is required in order to qualify for a conventional loan targeted to first-time homebuyers — or ideally, 20% to avoid private mortgage insurance. Yes, zero-down options exist if you are eligible for a VA- or USDA-backed loan.

According to Realtor.com, the average down payment in the first quarter of 2023 was 13%.

4 rate-relief strategies to consider

Buying a house when interest rates are high can require some financial finesse to enhance affordability.

1. Buying discount points

Prepaying interest in order to lower your ongoing mortgage rate is called buying discount points. One point is equal to 1% of the loan amount. However, lenders sometimes add a point or two to a mortgage proposal to make their loan offer appear more enticing. But you’re actually paying for the discount with an upfront fee.

When shopping for a loan, compare loan offers with zero points. Then, you can decide whether to buy points to lower your interest rate. It is important to note that buying one point (paying 1% of the loan amount upfront) will generally reduce your interest rate by only one-quarter of a percentage point.

2. An interest rate buydown

Borrowers can lower their mortgage interest rate for the first few years at the beginning of the loan term with a buydown. Home builders, sellers, and some lenders sometimes offer an interest rate buydown to boost sales.

While you get a short-term break on the interest rate, your payments and total interest may actually be higher. It’s a strategy that requires running the numbers on the long-term benefits.

If you’re paying for the buydown, compare a mortgage both with and without a buydown. By the way, lenders will qualify you based on the permanent interest rate, not the temporary buydown rate.

3.An adjustable-rate mortgage

A mortgage product that increases in popularity whenever rates begin to rise is back: the adjustable-rate mortgage.

ARMs have a fixed interest rate for an introductory period, often five to 10 years, and then the rate changes regularly, usually once or twice a year. Tips when shopping for an ARM:

Look for an introductory rate that is lower than a fixed-rate mortgage.

Choose a term you feel comfortable with, perhaps in line with how long you plan to stay in the home.

Make sure you budget for possible increases in your monthly payment if the interest rate moves higher after the end of the introductory rate period.

4. A shorter-term mortgage

Are you more comfortable with an interest rate that never changes, even if your monthly payment is slightly higher than you’d like? Consider a shorter-term loan. Mortgages with 20- or 15-year fixed terms, as opposed to the traditional 30-year term, typically come with lower interest rates. The lower rate and shorter term combination means you’ll gain equity in your home faster, too.

Your next move

Buy smart and shop a lot. Relentlessly shop mortgage rates and lenders for the best loan offers and justified fees. Get a written preapproval from your lender, then shop for a house you can love and can afford. Your home buying competition is.

According to Zillow, when it comes to first-time buyers versus repeat buyers, first-timers are more likely to reach out to at least three lenders and three real estate agents.

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Mortgage rates remain at jarringly lofty levels. In late September, the average rate on a 30-year home loan surged past 7.5 percent for the first time since November 2000, according to Bankrate data.

For October, experts don’t expect rates to depart much from that high point.

The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event. Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.

— Greg McBride, Bankrate chief financial analyst

Fed’s ‘higher for longer’ keeps pressure on mortgages

Mortgage rates broke through 7 percent faster than anticipated. The average rate on a 30-year home loan was 7.42 percent as of early September, according to Bankrate’s weekly national survey of lenders. That figure surged all the way to 7.55 percent in Bankrate’s final survey of the month.

For a 30-year loan at that rate, you’d pay $702 per month for every $100,000 borrowed. At the current median national price of $407,100, that equates to about $2,775 per month, assuming you’re making a 3 percent down payment.

Not long ago, experts thought rates might fall to 5 percent this year.

At its September meeting, the Federal Reserve declined to boost its policy rate again, but did signal it doesn’t expect to cut rates any time soon.

That new outlook led to a spike in 10-year Treasury yields, which are correlated with 30-year mortgage rates.

“Higher for longer seems to be the mentality of the Fed right now,” says Scott Haymore, head of Capital Markets and Mortgage Pricing at TD Bank. “They pushed out any decrease in rates until Q2 2024.”

For months, the major mortgage rate driver was inflation and the Fed’s response. While the policymaker doesn’t directly control mortgage rates, its moves set the overall tone for borrowing costs.

Outlook hazy for the rest of the year

Economists agree that the pandemic-era 3 percent rates aren’t coming back. The question now is how much higher they’ll go.

“The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event,” says Greg McBride, chief financial analyst for Bankrate. “Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.”

Some are optimistic. The Mortgage Bankers Association (MBA) predicts rates will drop to 6.3 percent by the end of 2023.

Haymore, of TD Bank, sees little change in rates in the near future.

“I think over the remainder of the year, we’ll be within a quarter point of where we are now,” says Haymore. “I don’t think we’ll see 8 percent.”

Lawrence Yun, chief economist at the National Association of Realtors, says that threshold is very much in the realm of possibility.

“In the short run, it’s possible mortgage rates may go to 8 percent,” says Yun.

More forecasts

A roadblock in more ways than one

Despite rising mortgage rates, home price appreciation hasn’t slowed and listings are still moving quickly. As the height of homebuying season fades, buyers are now weighing whether to take a higher rate — in hopes of refinancing later — or, perhaps more frustrating, wait things out.

If your aim is to close by the end of 2023, don’t delay, and carefully consider a rate lock.

“The trend has not been our friend and rates continue to get worse than I had expected based on recent data,” says James Sahnger of C2 Financial Corporation in Jupiter, Florida, adding “until we receive additional data to indicate a decidedly weaker economy, take a defensive posture when locking your rate.”

Rates above 7 percent are as much a psychological barrier as a financial one, says Lisa Sturtevant, chief economist at Bright MLS, a listing service in the Mid-Atlantic region.

“For many would-be homebuyers, a mortgage rate above 7 percent simply means that the numbers do not work for them,” says Sturtevant. “Consumer confidence has started to stumble as individuals and households are becoming more anxious about the economy.”

Indeed, 42 percent of respondents to a recent Bankrate survey cited paying for housing, either a mortgage or rent, as a negative influence on their mental health.

Still, American homeowners have proven their ability to adapt. In the 1980s, mortgage rates averaged 12 percent, but we kept buying homes.

Of course, home values weren’t nearly as high then. Add those two things together, Sturtevant says, and “the seemingly unstoppable housing market may be about to finally and truly stall out.”