Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults. In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over…

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults.

In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over the years as well.

As the value of certain cards continues to rise, finding the best places to sell your collection of Pokémon cards is more important than ever.

Whether you’re looking to make some extra cash, simply downsize your Pokémon card collection, or if you are decluttering everything you own and find a long lost box of childhood mementos, knowing where and how to sell your Pokémon cards can be important to make the most money.

In this article, I’ll discuss some of the best places to sell Pokémon cards online and locally and provide tips on how to price and present your cards in the best way.

Quick Summary

Identify and evaluate the value of your Pokémon cards before selling. Some cards are worth way more than others. For example, one card may be worth $0.10, and another may be worth over $100,000.

Look at your different selling options to see how you can get the most money.

Learn effective selling tips and strategies for presenting your cards to potential buyers.

How To Sell Pokemon Cards

Selling your Pokémon cards can be an exciting and profitable way to make money, especially if you have rare, holographic, or near-mint-condition cards in your collection.

To help you make the most profit, follow these tips to find the best places to sell your Pokémon cards. Before starting your Pokémon cards selling journey, it’s important to know your cards’ condition, rarity, and type.

Related: How I Made $40,000 In One Year Selling Items

Near-mint cards with no creases, scuffs, or whitening edges tend to have a higher value. Also, rare and holographic cards, like the famous Charizard, are highly wanted by fans, collectors, and trading card game enthusiasts, making them valuable in the Pokémon card market.

To figure out how rare your Pokémon card is, look for the symbols in the bottom right corner of your card and if you have a lot of cards, then you should become familiar with the Pokémon card rarity indicators, as well as the different sets and booster packs in which your cards were released.

For more accurate valuations, you may even look for professional grading services, such as Professional Sports Authenticator (PSA). They evaluate and grade cards based on their condition, ensuring buyers of their authenticity and quality.

If you’re selling Pokémon cards online, make sure to take clear, high-quality pictures that showcase your cards’ condition, as this will give potential buyers a better idea of what they’re purchasing.

By following these tips and tricks, you’ll be prepared to sell your Pokémon cards and get the most amount of money.

Best Places To Sell Pokemon Cards Online

There are many ways to sell Pokémon cards online. Here are some Pokémon selling sites to start with:

1. eBay

eBay is one of the most popular marketplaces for selling Pokémon cards due to its large reach of customers around the world.

I did a quick search on eBay and there are currently over 160,000 Pokémon cards for sale – so they definitely have a huge market!

You can choose to sell your cards through auctions or fixed price listings. When selling on eBay, be mindful of the seller fees and PayPal fees that will be deducted from your earnings. Shipping will also be another cost.

eBay is especially good for selling valuable cards, such as holographic cards or rare Charizard cards. To reach a wider audience and increase the chances of a successful sale, make sure you write detailed descriptions and add high-quality photos of your cards so that people are more likely to click on your listing.

2. Troll and Toad

Troll and Toad is an online store that specializes in collectible card games, such as selling Pokémon cards and they have been around for over 25 years.

They offer a buy list where you can sell your cards for cash or store credit. To sell on Troll and Toad, simply use their search bar to find the cards you want to sell, add them to your cart, checkout, and then ship your cards to them.

This is a great feature of Troll and Toad – the fact that you can see the exact cards they will accept and the exact amount that they will pay you for each Pokémon card. As you will learn below, many of the Pokémon card selling websites have this same feature, which is so helpful!

After you complete the list of cards that you plan on selling to them, you will print out an invoice that they give you, and then choose a payment method. Then, you will ship your box of Pokémon cards to them. Once they receive the package, they will verify the cards that you have sent to make sure they are in the correct condition as you stated. After that, they will pay you.

Troll and Toad also accepts Pokémon cards in bulk.

Keep in mind that they may be selective about the cards they accept, so it’s important to research and determine the value of your cards beforehand.

3. Mercari

Mercari is a site where you can quickly set up an account and start selling your used items, such as Pokémon cards. This site is not dedicated to just Pokémon cards, but they do have many listed and it is an easy option for Pokémon collectors.

There are well over 1,000 Pokémon cards listed on Mercari.

It’s important to create persuasive listings with photos and a relevant, detailed description, and include relevant keywords related to Pokémon cards. (Remember, they don’t just sell Pokémon cards, they also sell clothes and other items, so keywords are important!). Also, Mercari takes a minimum 10% fee from each sale you make on their platform.

4. TCGplayer

TCGplayer is a popular site with card game collectors in the U.S. and Europe.

People love selling on this site because they say it’s easy to use and they have great customer service.

To sell Pokémon cards on TCGplayer, simply list your cards on the TCGplayer marketplace, set your prices, and wait for potential buyers to purchase them. The marketplace handles the transactions, making the selling process easy.

Note: You will have to pay a commission fee of around 12–13% for each sale you make on TCGplayer, and you might also have shipping costs.

Here’s a quick guide on how to sell Pokémon cards on TCGplayer:

Create a seller account – You will need an account to get started selling Pokémon cards.

Set up your inventory – Once your seller account is created, you can start listing your Pokémon cards for sale. Enter details like the card’s name, set, condition, and quantity available.

Pricing your cards – Decide on the prices for your Pokémon cards. You can either manually set the prices or use TCGplayer’s automated pricing tool to match the market rates. TCGplayer has a pricing algorithm to help sellers be competitive and adjust prices based on the market demand.

Shipping options – Decide on the shipping options you will have for buyers.

Receiving payments – TCGplayer usually collects payments from buyers, processes the orders, and then deposits the money into your seller account. From there, you can withdraw your funds.

Maintain your inventory – Keep your inventory up to date. Remove sold items and add new ones to reflect the current availability of your Pokémon cards.

5. Card Cavern

Card Cavern is an online store that specializes in buying and selling Pokémon cards.

They have a straightforward buylist system where you can quickly find the cards they’re interested in and the prices they’re willing to pay.

Then, you ship your cards to them (they recommend purchasing tracking and insurance).

If you choose to sell your cards to Card Cavern, you’ll receive payment through PayPal or receive store credit, depending on your preference.

Their buy rates only apply to near-mint, English, tournament legal cards. You can send as many or as little Pokémon cards as you want to Card Cavern.

6. Dave & Adam’s

Dave & Adam’s is an online store for trading cards, including Pokémon cards, and it has been around for over 30 years.

They offer a buy list where you can see which cards they’re currently interested in purchasing. If your cards match their buy list, you can submit a sell request, ship your cards to them, and receive payment via check, PayPal, or store credit.

If you have a big collection, they will even travel to you.

7. Pokémon Facebook Groups

Pokémon Facebook Groups are communities of Pokémon card collectors and enthusiasts who use the platform to buy, sell, and trade cards. Pokémon Facebook Groups are exactly what you think – Facebook groups for Pokémon card collectors.

This can be a great place to sell your Pokémon cards because these groups are filled with people who are very interested in buying Pokémon cards.

These groups allow you to talk directly with fellow collectors and cater to various interests, such as specific regions, sets, or rarity levels.

To sell your Pokémon cards in these groups, make sure you follow group rules, post clear photos, and respond quickly to potential buyers’ inquiries.

8. CCG Castle

CCG Castle is a website that specializes in games since 2007.

They buy Pokémon cards that you no longer need and have a buy list on their site that will tell you exactly what they are accepting and how much they will pay you for it. They pay in either PayPal cash or store credit.

Best Places To Sell Pokemon Cards Near Me

If you’re looking to sell your collection or particular Pokémon cards, there are several options near you to consider. This section will cover the best local places where you can sell your cards, such as Facebook Marketplace, comic book stores, pawn shops, and Craigslist.

9. Facebook Marketplace

A popular and easy way to sell your Pokémon cards is through Facebook Marketplace. Nearly everyone has a Facebook account, so it can be easy for you to get started, and it allows you to connect with local buyers who might be interested in your cards.

Posting on Facebook Marketplace is simple, and you can include photos, descriptions, and set your price. Also, you can communicate with potential buyers through Facebook Messenger, making it easy to negotiate and set up a meeting location.

There are no listing fees when selling on Facebook Marketplace, which means that you get to keep everything you earn. But, you do have to handle everything yourself.

10. Local comic book stores

Comic book stores, particularly those that specialize in trading cards, card games, and board games, can be a great place to sell your collection.

Many local comic shops are interested in buying Pokémon cards to stock their inventory for other gamers and collectors.

You can visit stores in your local area, ask if they purchase Pokémon cards, and provide the store owner with a list or photos of your cards. They may make an offer on the spot or ask you to come back later. Remember, each comic store is different, so it’s a good idea to try a few stores near you to compare offers and don’t stop at just one.

11. Pawn shops

Another option to consider is pawn shops.

Pawn stores are known for buying various items, including sports cards and collectibles like Pokémon cards. Take your cards to a few pawn shops near you and see if they’re interested in buying your collection.

Keep in mind that pawn shops usually offer lower prices than other options (this is because selling Pokémon cards is not their sole business), but they can be a quick and convenient way to sell more popular cards.

12. Craigslist

Craigslist is a site for buying and selling various items locally – I’m sure you’ve heard of it. You can create a detailed listing for your Pokémon cards, including pictures, descriptions, and asking prices.

Interested buyers in your area can contact you, allowing you to arrange a meetup in a safe and convenient location.

Craigslist is usually a little more difficult to sell Pokémon cards on and that is because this site does not specialize solely in Pokémon cards and is very localized.

Where to Sell Pokemon Cards in Bulk

Selling your Pokémon cards in bulk may be something that you are interested in if you simply don’t have the time to look each one up.

When selling your Pokémon cards in bulk, it’s important to find the right platform. In this section, we’ll focus on three popular options: Full Grip Games, Safari Zone, and Sell2BBNovelties. With their unique offerings and easy-to-sell process, these companies can help you get the most value for your collection if you simply don’t have the time or have too many cards to sort through.

13. Full Grip Games

Full Grip Games is a local game shop in Ohio that buys bulk Pokémon cards online and in person.

At Full Grip Games, they make it easy for you to sell your bulk cards in increments of 100 or 1,000. Also, they accept rares and other card types as well. To make things simpler for you, their website has a bulk buy list that breaks down all the packs and cards they accept along with individual prices.

To get started, follow these easy steps:

Click on the “Buylist Instructions” link on their website.

Choose their full singles buylist or their bulk buylist.

Select the cards in your collection according to the buylist.

Review the pricing and total value of the cards submitted.

Once done, send the cards following their shipping instructions.

Once they receive your bulk cards, it will take them around one week to go through them. For the cards they accept, you can get paid via PayPal, store credit (you will get a 30% bonus if you choose the store credit option), or check via USPS mail.

14. Safari Zone

Safari Zone is another great option to consider for selling your Pokémon cards in bulk. They accept a wide range of cards, but they do need to be in near-mint condition.

Here’s what you should do to sell your cards on Safari Zone:

Create an account on the Safari Zone website.

Review the cards they purchase on their buy list.

Enter the card details.

After submitting the card information, you’ll receive a quote for your collection.

Ship your cards to Safari Zone, and they will process your payment after validating the cards.

Safari Zone only pays via store credit.

15. Sell2BBNovelties

Sell2BBNovelties is a website that has been around since 1999 that specializes in toys and collectibles, such as Pokémon cards.

They have an easy platform to sell your Pokémon cards in bulk and accept various card types, including rares, holographic, and common/uncommon cards.

To sell your Pokémon cards on Sell2BBNovelties, simply:

Go to their website and click on the “Buying Prices” tab.

Select the cards you’re selling according to their buying list.

When you’re ready, submit the form. You’ll receive a confirmation email with the total value of the cards and further instructions.

Ship your cards to Sell2BBNovelties, and they will process your payment upon receiving and verifying your cards.

You can receive payment for the cards they accept in either PayPal cash or store credit.

How to Make a Website to Sell Pokemon Cards

If you have the time and a lot of cards, you may even be interested in starting a website to sell your Pokémon cards.

Creating a website to sell your Pokémon cards is a great idea to reach a wider audience and have lower fees. Of course, there will be more work in this because you will be managing everything yourself.

Choose a platform and create your design – Look for an easy-to-use platform to build your website – my favorite is WordPress. You will want to pick a clean looking design that customers can look at on both computer and phone. Most platforms have a variety of premade themes that you can use. You can also personalize your website by adding your logo, choosing colors that represent your brand, and adding images.

Organize your products – Categorize your Pokémon cards by sets, rarity, or other criteria that make sense for your target audience. Clear product descriptions and high-quality images of each card will help potential buyers too.

Set up payment and shipping – Choose a payment gateway to securely process transactions. Options like PayPal, Stripe, or Square are widely used and reliable. Choose shipping options and rates based on your preferred carriers and shipping destinations.

Create valuable content – In addition to listing your Pokémon cards, consider creating helpful content such as blog posts or videos that add value to your website and attract more readers and buyers. Providing informative content will establish you as an expert in the field and help drive traffic to your site.

Promote your website – Use social media, search engine optimization (SEO), or even paid advertising to increase page views to your website.

Related: How To Start A Website Free Course

Pokemon Card Selling Tips and Strategies

Selling your Pokémon cards can be an exciting way to make extra money, but it’s important to have a little strategy so that you can make the most money and find the most buyers.

Here are some tips for selling your Pokémon cards successfully.

Determine the value of your cards. You should research how rare the card is, the origin, and the condition of your cards, as these factors will affect their worth. Keep an eye out for rare and valuable cards (such as first edition cards and illustrations), as these will attract more interest from collectors. Grading your cards can help with this process – professional grading services can rate the condition of your cards and encapsulate them in a case, increasing their value.

Consider where to sell your cards.There are numerous platforms for selling Pokémon cards online, such as eBay, where you can list your cards as single items or in an auction format. There are also more specialized Pokémon selling websites which are dedicated to trading cards. These sites often have dedicated communities of potential buyers who are very interested in Pokémon cards.

Write clear and accurate descriptions of your cards.You should always be clear and honest about your card’s condition. For example, are there any scratches or bends? Is there a tear or water damage?

Ship your cards carefully.Carefully package your Pokémon cards to protect your cards from damage during transit. You will want to keep your cards waterproof and not use rubber bands (rubber bands can damage the cards). Also, consider offering a tracking number and insurance to your buyer as an additional layer of security. Many of the Pokémon selling sites above have a very exact way they want you to ship the cards to them to prevent any damage, so be sure to see what their rules are.

By following these Pokémon card selling tips and tricks, you can increase the chances of finding the best places to sell your Pokémon cards.

Frequently Asked Questions

Here are answers to common questions about selling Pokémon cards.

How do I know if my Pokemon cards are worth money?

So, how do you know if the Pokémon cards that you have are worth anything? Many people have Pokémon cards, probably stuffed in a box somewhere, or maybe you came across some.

Whatever your reason is, yes, your Pokémon cards may be worth something.

Knowing the value of your Pokémon cards is important before selling, and there are a few key things to think about.

First, look at the rarity symbols on your cards: a circle indicates a common card, a square represents an uncommon card, and a star denotes a rare card. These symbols help you determine the rarity of your cards and their potential worth.

The condition of your cards also plays a big role in their value. Cards in mint condition, meaning they have no visible wear or damage, are worth more than cards with minor imperfections. Holographic cards, especially in mint condition, can be more valuable.

To take it a step further, you could even get your Pokémon cards professionally valued and graded by a reputable company like PSA. Grading involves a professional inspection of your card’s condition, assigning a numerical grade based on factors such as centering, corners, edges, and surface. The higher the graded number, the better the condition and, often, the higher the value.

Keep in mind that while Pokémon cards typically have higher values, other trading card games like Yu-Gi-Oh can also be valuable. Make sure to research the prices of similar cards sold recently, and compare the condition of your cards to decide if they’re worth selling.

How do I sell Pokemon cards for cash?

To sell your Pokémon cards for cash, first organize your cards by set and look for rare ones to see what you have. Once you’ve prepared your collection, follow the selling instructions on your chosen platform.

You can sell your Pokémon cards online, locally near you, and even in bulk.

Where can I find buyers for my Pokemon cards?

You can find buyers for your Pokémon cards on online marketplaces, local card shops, and social media groups. Websites like eBay and TCGplayer are popular places for selling Pokémon cards, as well as community forums and local collector’s events.

What are some reputable websites to sell Pokemon cards?

There are many reputable sites to sell Pokémon cards as we discussed above, such as:

eBay

Troll and Toad

Mercari

TCGplayer

Card Cavern

Dave & Adam’s

Pokémon Facebook Groups

Full Grip Games

Safari Zone

Sell2BBNovelties

Where is the best place to sell Pokemon cards?

The best place to sell your Pokémon cards depends on your preferences. eBay gives you a worldwide market and you are probably already familiar with their platform.

TCGplayer and Troll and Toad specialize in trading card sales and have a lot of Pokémon cards for sale.

Pokémon Facebook Groups are a great way to connect with those interested in Pokémon cards, and there are no listing fees – but you would be dealing with people on your own and handling everything yourself.

Are there any local stores that buy Pokemon cards?

Some local stores, like comic book shops, game stores, and pawn shops, may buy Pokémon cards. You can call local stores to see if they buy cards before bringing your collection in person.

Can you sell Pokemon cards on Etsy?

Etsy is generally geared towards handmade and vintage items, so it’s not an ideal platform for selling Pokémon cards. It’s best to stick with platforms like eBay, TCGplayer, or Troll and Toad for selling trading cards.

I did a search for Pokémon cards on Etsy and it said there were 43,326 results, but I think many of these are for custom art, in that they would be turning a picture of you or your pet into a Pokémon card. So, not the same thing.

Can I sell Pokemon cards on eBay?

Yes, you can sell Pokémon cards on eBay. It is one of the most popular sites for selling Pokémon cards and it gives you control over pricing and listing options.

Can you sell Pokemon cards at GameStop?

GameStop typically does not buy or sell individual Pokémon cards.

Do pawn shops buy Pokemon cards?

Some pawn shops may buy Pokémon cards, especially if they are valuable or rare. Call your local pawn shops or visit them in person to inquire about their interest in buying Pokémon cards. Remember, they do not specialize in Pokémon cards and have a smaller market, so you may not get as much for your Pokémon cards at a pawn store.

What does TCG and CCG mean?

As you’re going through the sites above looking for one of the best places to sell your Pokémon cards, you may come across these two terms. CCG means collectible card game and TCG means trading card game.

How can I determine the value of my Pokemon cards?

Figuring out the value of your Pokémon cards involves considering factors like:

rarity

condition

age

Websites like TCGplayer and Troll and Toad provide price guides and historical sales information to help you estimate the value of your cards.

How do I check the value of my Pokemon cards?

Check the value of your Pokémon cards by researching on websites like TCGplayer, eBay, and Pokémon Price. These platforms can give you a good idea of the current market value for individual cards.

Do you need a license to sell Pokemon cards?

You generally do not need a license to sell Pokémon cards, unless you’re planning to sell them by opening an in-person store. Check your local regulations to make sure you’re following any required guidelines.

How much is Charizard Pokemon card worth?

Charizard cards vary widely in value and can be worth anywhere from $25 to over $50,000. The Charizard Pokémon card that is worth the most is typically a mint condition 1st Edition from the base set.

What Pokemon cards are worth more than $100?

Some Pokémon cards worth more than $100 include rare Pokémon cards, such as first edition holographic cards from the original sets, high-grade cards, misprints, and promotional cards like the Pokémon Illustrator card.

What is the most expensive Pokemon card?

The most expensive Pokémon card varies over time; some examples include the Pokémon Illustrator card, the 1st Edition Charizard, or unique, one-of-a-kind promo cards handed out during official Pokémon events. The rarest Pokémon cards obviously cost more money and sell for more.

According to TCGplayer, the most expensive Pokémon cards include:

Pokémon World Championships No. 2 Trainer Promo

No. 2 Trainer Toshiyuki Yamaguchi (2000)

Neo Genesis 1st Edition Lugia (2000)

Super Secret Battle No. 1 Trainer (1999)

Family Event Trophy Kangaskhan (1998)

Test Print Blastoise Gold Border (1998)

Tsunekazu Ishihara Signed Promo (2017)

Trophy Pikachu No. 3 Trainer Bronze (1997)

Commissioned Presentation Blastoise Galaxy Star Holo (1998)

First Edition Shadowless Holographic Charizard #4 (1999)

Illustrator Pikachu (1998)

These were all sold for over $100,000 each.

Best Places To Sell Pokemon Cards – Summary

I hope you enjoyed this article on the best places to sell Pokémon cards and how to sell Pokémon cards for cash.

If you have Pokémon cards that you no longer want, there are many ways you can sell them. And, they may be worth a lot of money!

To figure out the value of the Pokémon cards that you want to sell, you’ll want to look at their rarity symbols, Pokémon card condition, grading (if applicable), and market comparisons. Understanding these factors will help you decide if your cards are worth selling and where to find the best prices.

Once your cards are sorted and evaluated, it’s now time to choose the best places to sell your Pokémon cards. Here are some popular options:

eBay – This site has millions of Pokémon cards sold every year. It’s a great place to find a worldwide audience, but remember to factor in shipping costs and eBay fees.

Facebook Marketplace and Pokémon Facebook Groups – Connect with local collectors or fans without worrying about shipping fees. This option may mean that you will meet the buyer in person.

Local comic shops – These stores can be an easy place to sell your cards, especially if they specialize in Pokémon cards or trading card games.

TCGplayer – Catering specifically to trading card game fans, this site has a dedicated space for buying and selling Pokémon cards.

Other options include Troll and Toad, Card Cavern, Dave & Adam’s, Sell2BBNovelties, pawn shops, and more.

Good luck selling your Pokémon cards!

What do you think is the best place to sell Pokemon cards for cash?

Homebuilders are to blame for the current housing and mortgage crisis, according to a report released by the Laborers’ International Union of North America (LIUNA).

The group’s report focuses on mortgages originated between 2005 and 2006 in Maricopa County, Arizona by the lending units of three of the nation’s largest homebuilders, including Richmond American, Lennar, and KB Home.

More than one-third of the mortgages originated by these homebuilders in the county are five-year adjustable-rate mortgages expected to reset between 2010 and 2011, and with many of these homeowners now underwater, they could face serious payment shock.

Per the report, in just the last year the value of Lennar homes has declined $61,600, KB Home values have sunk $55,600, and Richmond American Homes are worth $49,500 less.

In the KB Home Santarra Development in Buckeye, Arizona, home values have dropped a staggering $78,800 in the last year, troubling because 55 percent of mortgages held are five-year ARMs, and 63 percent of purchase loans have a second mortgage.

“Former Countrywide-KB Home Loans Regional Vice President Mark Zachary has said in court that KB Home pressured its lending joint venture to engage in systematic mortgage fraud to drive sales, including encouraging inflated appraisals, assisting buyers in supplying false income information, and approving loans without review or documentation,” the release said.

LIUNA, which earlier this year exposed the homebuilder tax break in the Foreclosure Prevention Act, is calling on agencies such as Fannie Mae and Freddie Mac to place greater scrutiny on the mortgages originated by homebuilders and their mortgage lender partners.

At last glance, 30-year fixed mortgage rates were sitting above 7%. Despite this, there are virtually no homes for sale.

One would assume that after such a massive interest rate spike, demand would flounder and supply would flood the market.

Yet here we are, looking at a housing market that has barely any for-sale inventory available.

And when you remove the new home inventory (from home builders) from the equation, it’s even worse.

Let’s explore what’s going on and what it might take to see listings return to the market.

Why There Are No Homes for Sale Right Now?

The housing market is highly unusual at the moment, and has been for quite some time.

In fact, since the pandemic it’s never really been normal. The housing market came to a halt in early 2020 as the world stopped, but then took off like a rocket.

If you recall, the 30-year fixed spent the entire second half of 2020 in the sub-3% range, fueling voracious demand from buyers.

And as Zillow pointed out, the age demographics had already lined up nicely for a surge of demand anyway.

Around that time, some 45 million Americans were expected to hit the typical first-time home buyer age of 34.

When you combined the demographics, the record low mortgage rates, a pandemic (which allowed for increased mobility), and already limited inventory, it didn’t take much to create a frenzy.

At the same time, you had existing homeowners buying up second homes on the cheap, due to those low rates and generous underwriting guidelines.

And let’s not forget investors, who were taking advantage of the very accommodative interest rate environment and the insatiable demand from buyers.

The rise of Airbnb and short-term rentals (STRs) coincided with this low-rate environment, potentially taking additional inventory off the market.

This quickly depleted supply, which was already trending down thanks to a lack of new home building after the prior mortgage crisis.

Home builders got burned in the early 2000s as foreclosures and short sales spiked and prices plummeted. And their excess supply sat on the market.

As a result, they developed cold feet and didn’t build enough in subsequent years to keep up with the growing housing needs of Americans.

Collectively, all of these events led to the massive housing supply shortage.

Low Mortgage Rates Got Buyers in the Door, But Will They Ever Leave?

Low supply aside, another unique issue affecting housing supply is a concept known as mortgage rate lock-in.

In short, there’s an argument that today’s homeowners have such low mortgage rates that they won’t sell. Or can’t sell.

Either they don’t want to give up their low mortgage rate simply because it’s so cheap. Or they are unable to afford a home purchase at today’s rates and prices.

Simply put, most can’t trade in a 3% rate for a 7% rate and purchase a home that’s probably more expensive than theirs was a few years earlier.

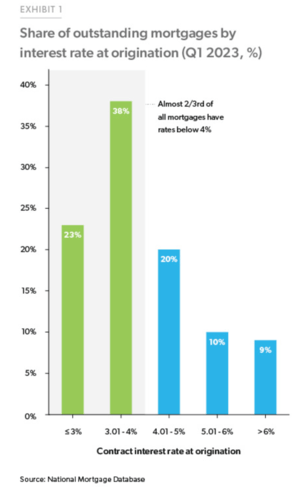

And this isn’t some tiny subset of the population. Per Freddie Mac, nearly two-thirds of all mortgages have an interest rate below 4%.

And nearly a quarter have a mortgage rate below 3%. How on earth will these folks sell and buy a replacement home if prices haven’t come down, but have in fact risen?

The answer is most will not budge, and will continue to enjoy their low, fixed-rate mortgage for many years to come.

This further explains why inventory is so tight and not really improving, despite the Fed’s attack on housing demand via 11 rate hikes.

[Why are home prices not dropping?]

Housing Supply Is at an All-Time Low

Redfin reported that the total number of homes for sale hit a record low in August.

Active listings were down 1.1% month-over-month on a seasonally adjusted basis, and a whopping 20.8% year-over-year.

That’s the biggest annual decrease since June 2021. However, new listings have ticked higher the past two months on a seasonally adjusted basis.

In August, new listings increased 0.8% from a month earlier after increasing the month before that.

But due to nearly a year’s worth of monthly declines prior to that, new listings were still off a big 14.4% year-over-year.

This meant months of supply stood at just two months, well below the 4-5 months usually considered healthy.

Redfin Economics Research Lead Chen Zhao noted that “new listings have likely bottomed out,” arguing that those who are locked in by low rates have already decided not to sell.

That leaves those who must sell their property, due to stuff like divorce or a change in work-from-home policy.

Interestingly, even some WFH homeowners are moving back closer to work, but keeping their homes because they can rent them out.

Because homeowners got in so cheap, it’s not out of the question to keep the old house and go rent or buy another property.

All of this has created a huge dearth of existing home supply, but there is one winner out there.

Home Builders Are Gaining a Ton of Market Share

While existing homes, also known as previously-owned or used homes, are hard to come by, newly-built homes are somewhat plentiful.

In fact, newly built single-family homes for sale were up 4.5% year-over-year in June, per Redfin, while existing homes for sale were down 18%.

And roughly one-third of homes for sale were new builds, up markedly from prior years and well above the norm that might be closer to 10%.

Astonishingly, new homes accounted for more than half (52%) of single-family homes for sale in El Paso, Texas.

Similar market share could be seen in Omaha (46%), Raleigh (42.1%), Oklahoma City (39%), and Boise (38%).

Meanwhile, the National Association of Realtors (NAR) predicts that new home sales will increase 12.3% this year, and 13.9% in 2024.

As for why home builders are seeing a big increase in market share, it’s mostly due to a lack of competition from existing home sellers.

In short, they’re the only game in town, and they don’t need to worry about finding a replacement property if they sell (like existing homeowners)

Additionally, they’re able to tack on huge incentives such as rate buydowns, including temporary and permanent ones, along with lender credits.

This allows them to sell at higher prices but make the monthly payment more palatable for the buyer.

Perhaps more importantly, it allows buyers to still qualify for a mortgage at today’s sky-high prices.

When Will More Homes Hit the Market?

For now, this new reality is expected to be the status quo. After all, those with so-called golden handcuffs have 30-year fixed-rate mortgages.

That means they can continue to take advantage of their dirt-cheap mortgage for the next few decades.

This includes second home owners and investors, who got in cheap when prices were much lower and mortgage rates were also on sale.

Meanwhile, the home builders don’t seem to be going nuts with supply, and even if they ramped up production, it wouldn’t satisfy the market.

Remember, existing home sales typically account for around 85-90% of sales, so builders won’t come close to satisfying demand.

The only real way we get a big influx of supply is via distress, sadly. That could be the result of a bad recession with mass unemployment.

And it could be triggered by the 11 Fed rate hikes already in the books, coupled with a lack of new stimulus and the resumption of things like student loan payments.

Compounding that is sticky inflation, which has made everything more expensive and is quickly depleting the savings accounts of Americans.

But even then, you could argue that a mass loan modification program would be unveiled to at least keep owner-occupied households in their properties.

Considering how cheap their housing payments are, assuming they’ve got a low fixed-rate mortgage, it’d be hard to find them a cheaper alternative, even if renting.

In the early 2000s this wasn’t the case because the typical homeowner held a toxic mortgage, such as an option ARM or an interest-only loan. And many weren’t even properly qualified to begin with.

Read more: Today’s Housing Market Risk Factors: Is Real Estate in Trouble?

Additionally, the mortgage application measure and the pending home sales index are increasingly diverging, reflecting the higher cash share of sales, the ESR group noted.

While the additional downside risk from rate movements to date is minimal, the prospects of a recovery in existing sales in the near future is unlikely given strong mortgage rate “lock-in” effects and stressed affordability.

Going forward, the ESR Group expects new home sales to pull back slightly due to the higher mortgage rate environment and recent decline in homebuilder confidence.

Homebuilder confidence fell six points from July to a reading of 50 in August. It’s the first decline in 2023 reflecting the difficulties of 7% mortgage rates and reduced housing affordability.

The recent rise in mortgage rates will also now test the resiliency of the new home sales market, which showed remarkable strength over the first half of the year.

The lack of existing homes for sale has helped support demand for new homes, including an increasing share of first-time buyers.

To what extent homebuilders will continue to offer generous mortgage rate buydowns to drive sales is a big question that needs to be answered, according to the ESR group.

“When mortgage rates originally jumped to 7% in late 2022, a pullback in homebuilder activity ensued as buying activity slowed. It is uncertain whether this same rate threshold will result in a similar effect this time around or whether buyers and homebuilders have increased their willingness to purchase and subsidize at current rates,” Fannie Mae noted.

Fannie Mae expects Q4 new home sales to average around 691,000 units on an annualized basis, down slightly from the most recent pace of 714,000 in July.

Purchase mortgage origination volume is expected to be $1.3 trillion in 2023 and $1.4 trillion in the following year. Refi volume is forecast to be at around $10 billion in 2023 and $14 billion in 2024.

Fannie Mae’s projection of a mild economic downturn in Q1 2024 remains unchanged.

While the GSE’s initial April 2022 forecast of a mild recession was in the second half of 2023, housing production held up and household savings supported consumer spending longer than Fannie Mae had expected.

“Our current prediction for a mild downturn in the first half of 2024 is predicated on the belief that consumers will begin pausing their spending, in part due to the exhaustion of those funds and having to realign to a more sustainable relationship between spending and incomes,” said Doug Duncan, SVP and chief economist at Fannie Mae.

U.S. home loan applications are the lowest in decades as evidence mounts that rising mortgage rates and home prices are shutting out many aspiring homeowners

ByALEX VEIGA AP business writer

September 7, 2023, 5:50 PM

FILE – A “SOLD” sign decorates the lawn of a new house in Pearl, Miss., Sept. 23, 2021. U.S. home loan applications are at the lowest level in decades, the latest evidence that rising mortgage rates and home prices are shutting out many aspiring homeowners. (AP Photo/Rogelio V. Solis, File)

The Associated Press

LOS ANGELES — U.S. home loan applications are the lowest in decades as evidence mount that rising mortgage rates and home prices are shutting out many aspiring homeowners.

An index that tracks mortgage application volume shows applications for loans to buy a home fell last week to the lowest level in 28 years, according to the Mortgage Bankers Association.

The MBA’s home loan application index shows that home purchase loans fell 2.1% last week from the prior week to a seasonally adjusted reading of 141.9. That’s down about 28% from a year earlier and represents the lowest level for the index since April 1995.

“Both purchase and refinance applications fell, with the purchase index hitting a 28-year low, as prospective buyers remain on the sidelines due to low housing inventory and elevated mortgage rates,” said Joel Kan, the MBA’s deputy chief economist.

Mortgage rates have been climbing in recent weeks, echoing a steady rise in the 10-year Treasury yield, which lenders use as a guide to pricing loans.

The average rate on the benchmark 30-year home loan was 6.48% at the start of this year, falling as low as 6.12% in February, according to mortgage buyer Freddie Mac. Since then, its been hovering around 7%, in-line with the average seen near the turn of the century.

High rates can add hundreds of dollars a month in costs for borrowers, limiting how much they can afford in a market already unaffordable for many Americans. They also discourage homeowners who locked in low rates two years ago from selling, a trend that’s helped keep the inventory of previously occupied U.S. homes on the market at near-record lows.

The lack of housing supply has weighed on sales of previously occupied U.S. homes, which are down 22.3% through the first seven months of the year versus the same stretch in 2022.

The average rate on a 30-year mortgage remains more than double what it was two years ago, when it was just 2.87%. As more homeowners locked in bottom-barrel rates in recent years, demand for home loan refinancing has plunged.

The MBA’s refinance loan index fell to a seasonally adjusted rate of 388.1 last week, down 4.7% from the previous week and 30.3% below a year ago.

It was a tale of two lenders in the first quarter of 2013, according to earnings reports released today by Wells Fargo and Chase.

After crunching the numbers, it appears the two are heading in different directions, though Chase is unlikely to dethrone Wells Fargo anytime soon.

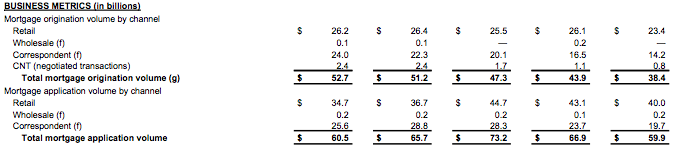

Wells Fargo saw home lending volume dip to $109 billion in the first quarter, down from $125 billion in the fourth quarter and $129 billion a year earlier.

Along with that, the San Francisco-based bank and lender also experienced in decline in mortgage applications, which fell to $140 billion from $152 billion in the fourth quarter and $188 billion in the first quarter of 2012.

As a result, the company’s unclosed mortgage pipeline shrunk to $74 billion, down from $81 billion in the linked quarter and $79 billion a year ago.

Refis and Correspondent Lending Down

If you dig into the numbers, there are a couple of reasons why home loan production is off. For one, refinances as a percentage of total application fell to 65% in the first quarter.

They’re down from 72% in the fourth quarter and 76% a year ago. Long story short, there just aren’t as many potential refinance transactions left, as most predicted.

Most homeowners already refinanced, though there is the possibility for some homeowners to refinance again, seeing that mortgage rates have continued to trickle lower.

Still, refinance activity is expected to drop tremendously this year, and purchase-mortgage activity certainly won’t be able to make up for the entire decline.

Additionally, Wells Fargo saw a big drop in correspondent lending, which actually accounted for much of their quarterly and annual decline.

I’m assuming this isn’t by accident, and could be the result of the bank choosing to focus only on its highest quality business partners.

There’s also an industry-wide push to focus on retail relationships as well, which are valuable from a cross-selling (and loan quality) standpoint.

Chase Growing Larger in the Mortgage Space

While Wells was sputtering, number two was making up for lost time. Chase said it increased mortgage lending by 3% from the fourth quarter and 37% from a year ago.

Total mortgage origination volume for the NYC-based bank increased to $52.7 billion in the first quarter (260,000 mortgages), up from $51.2 billion at year-end and $38.4 billion in the first quarter of 2012.

Chase was also able to increase mortgage application volume slightly, though only by one percent from a year ago. It was off 8% from the fourth quarter.

Contrary to Wells, Chase increased its correspondent mortgage lending significantly from a year earlier.

In fact, it nearly doubled correspondent output (+69%) as the channel accounted for nearly half of overall production. Retail volume increased 12% from a year earlier, but was off one percent from the fourth quarter.

Chase seems to be making a bigger push in home loan lending, as evidenced by these numbers and a recent ad campaign.

The bank is running commercials nationwide promoting its “Chase My New Home” app, which allows potential customers to search and compare homes, calculate monthly mortgage payments, and connect with a Chase Mortgage Banker.

It appears to be their way of saying they want a bigger piece of the purchase market. However, it’s going to take a lot of work to steal the number one spot from Wells Fargo…

If you’re in the market for purchasing a new home or taking on a business loan or personal loan, you’re likely finding it difficult to score the almost-2% APR we saw in 2020. That’s becausethe Federal Reserve has been hiking interest rates since March 2022 in an effort to cool inflation.

“The Fed has two objectives: To keep inflation low, their current obsession, and to keep unemployment low, which is of current lesser concern,” says Amy Hubble, a certified financial planner who has a Ph.D. in consumer economics. “In practice, this means they lower rates to incentivize growth and hiring, and raise rates to combat inflation when the economy gets overextended. This leads to a policy teeter-totter meant to balance out economic activity in the US.”

So the question remains: When will we finally see interest rates start to come down? CNBC Select asked three experts to give their take on what lies ahead for interest rates. Here’s what they had to say.

What we’ll cover

When will interest rates come back down?

Nobody outside of the Federal Open Market Committee (FOMC), the 12 men and women tasked with setting target interest rates, can predict with any certainty what will happen with rates and when. But that hasn’t stoppedeconomists like Preston Caldwell, a senior U.S. economist for Morningstar Research Services LLC, from making their own educated guesses.

“I think rates will start cutting in early 2024,” Caldwell says. “I think inflation will be nearing the Federal Reserve’s 2% target at that phase and the economy will show signs of slowing, but it’s hard to predict.”

Other professionals in the space echo a similar vision. Hubble points to a recent FOMC report that includes committee members’ projections on gross domestic product (GDP) growth, inflation and the unemployment rate — all factors the Fed will weigh when deciding how aggressively to cut rates.

“All FOMC members believe that rates will be stable or higher through 2023 before slowly coming down in 2024–2025 to settle at a comfortable 2.5% for the longer-term,” she says.

Elliot Eisenberg, the Chief Economist at Graphs and Laughs agrees. “There was a belief that once the second half of 2023 came around, rates would’ve been lower than they were at the end of 2022,” he says. “But it hasn’t come down. These things take a long time to work their way through the economy, so sometime in 2024 sounds about right.”

However, he also warns that it’s hard to believe that we’ll see any interest rate cooling in 2023.

Subscribe to the CNBC Select Newsletter!

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here.

What should you do when interest rates go down?

Lower interest rates make borrowing money cheaper. That means all other factors (like your credit score) being equal, you’ll generally pay less in interest on anynewstudent loans, personal loans, business loans and mortgages than you would during today’s high-rate environment. Existing loans with a variable rate may also start charging less interest as the Fed lowers interest rates.

That’s why waiting until interest rates come down beforeborrowing money for alarge purchase — like a home — can be easier on your bank account. The current average mortgage interest rate on a 30-year loan is 7.98% even for borrowers witha credit score between 700 and 719. That’s a tough pill for a first-time homebuyer to swallow month after month as they pay their mortgage.

However, if holding off on getting a mortgage isn’t doable for you, make sure you improve your credit score before applying so you can qualify for an interest rate that’s as low as possible. Also consider choosing a mortgage lender that helps you save money throughout the process. Ally Bank, for instance, doesn’t charge any lender fees. And if you qualify for a Navy Federal Credit Union mortgage, you can get a home loan with no private mortgage insurance (PMI) requirements even if you make a down payment of less than 20%.

Ally Home

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Conventional loans, HomeReady loan and Jumbo loans

Terms

15 – 30 years

Credit needed

Minimum down payment

3% if moving forward with a HomeReady loan

Terms apply.

Navy Federal Credit Union

Annual Percentage Rate (APR)

Apply online for personalized rates

Types of loans

Conventional loans, VA loans, Military Choice loans, Homebuyers Choice loans, adjustable-rate mortgage

Terms

10 – 30 years

Credit needed

Not disclosed but lender is flexible

Minimum down payment

0%; 5% for conventional loan option

You can also refinance your mortgage down the line during a lower interest rate environment so you can score a better rate on your loan. PNC Bank is one of the most accessible lenders because it has locations in all 50 states and customers can apply both online and in-person.

PNC Bank Mortgage Refinance

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Fixed-rate, adjustable-rate, FHA loans, VA loans and jumbo loans

Fixed-rate Terms

10 – 30 years

Adjustable-rate Terms

Available in periods of 7 and 10 years for a fixed rate, followed by an adjustment period when the interest rate may increase or decrease on an annual or semi-annual basis

Credit needed

Not disclosed

Pros

Refinance available for primary and secondary homes, and investment properties

Offers a wide variety of loans to suit an array of customer needs

Offers refinancing for VA and FHA loans

Available in all 50 states

Online and in-person service available

Cons

Doesn’t offer home renovation loans

Lower interest rates can also have an impact on the APY you earn on your high-yield savings account. While buying a house or taking out a personal loan becomes more affordable during lower interest rate environments, you typically can’t earn as high an interest rate from the money in your deposit accounts.

That’s becausebanks use the Fed rate as a benchmark for yields on savings accounts. So when the Fed rate falls, the interest rate on your high-yield savings account will likely also decrease. Right now, some high-yield savings accounts, like the UFB High Yield Savings Account, are offering more than 5% APY on account balances.

UFB High Yield Savings

UFB High Yield Savings is offered by Axos Bank, a Member FDIC.

Annual Percentage Yield (APY)

Earn up to 5.25% APY

Minimum balance

Monthly fee

Maximum transactions

No max number of transactions; max transfer amounts may apply

Excessive transactions fee

Overdraft fee

Overdraft fees may be charged, according to the terms, but a specific amount is not specified; overdraft protection service available

Offer checking account?

Offer ATM card?

Terms apply.

Even though we’re unlikely to see sky-high APYs stick around after the Fed lowers interest rates, it’s still worth keeping your money in a high-yield savings account even in a lower-rate environment. You’ll still grow your money faster in a high-yield account than with most traditional savings accounts, and it provides a safe, FDIC-insured place to keep your emergency fund.

Bottom line

According to experts, we aren’t likely to see significantly lower interest rates this year, but 2024–2025 is likely to see more progress on that front. Lower rates can make life easier for individuals who have been waiting to buy a house or take on other types of loans, even if savers won’t enjoy the high APYs that thrive in a world of high rates.

Meet our experts

At CNBC Select, we work with experts who have specialized knowledge and authority based on relevant training and/or experience. For this story, we interviewed:

Preston Caldwell, a senior U.S. economist for Morningstar Research Services LLC.

Elliot Eisenberg, a chief economist and Graphs and Laughs.

Amy Hubble, a CFP with a Ph.D. in consumer economics.

Why trust CNBC Select?

At CNBC Select, our mission is to provide our readers with high-quality service journalism and comprehensive consumer advice so they can make informed decisions with their money. Every article is based on rigorous reporting by our team of expert writers and editors with extensive knowledge of personal finance. While CNBC Select earns a commission from affiliate partners on many offers and links, we create all our content without input from our commercial team or any outside third parties, and we pride ourselves on our journalistic standards and ethics. See our methodology for more information on how we choose the best mortgage lenders and high-yield savings accounts.

Catch up on CNBC Select’s in-depth coverage of credit cards, banking and money, and follow us on TikTok, Facebook, Instagram and Twitter to stay up to date.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

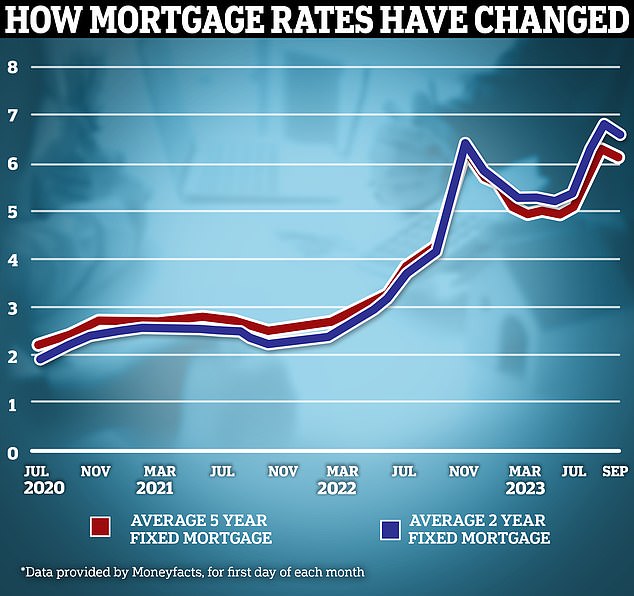

Fixed rate mortgages have dipped below 5 per cent for the first time since early July, offering some hope to struggling homeowners.

Yorkshire Building Society has launched a 4.99 per cent fixed-rate deal which is available to both home buyers and those remortgaging.

It’s available at 75 per cent loan-to-value, meaning eligible customers can apply as long as they either have at least a 25 per cent deposit or 25 per cent equity within their home.

Best rate: Yorkshire Building Society has launched a 4.99 per cent fixed rate deal aimed at both homebuyers and those remortgaging

Someone with a £200,000 mortgage could expect to pay £1,168 a month if repaying over a 25-year term, compared to the market average of £1,249 a month.

The five-year deal comes with a £1,495 fee, however, and a mortgage with a higher rate but a lower fee may be a better deal for some customers.

You can compare rates and fees and work out the true cost of a mortgage using our calculator.

After Yorkshire BS, the next best deal is Virgin Money which has a five-year fix at 5.07 per cent and is available to home buyers purchasing with at least a 35 per cent deposit (65 per cent loan-to-value).

HSBC has a five-year fix at 5.09 per cent for home buyers with at least a 40 per cent deposit (loan-to-value of 60 per cent).

Nationwide also has a 10-year fix available at 5.04 per cent which is available to home buyers with a deposit of 15 per cent or more (85 per cent loan-to-value).

The average five-year fixed mortgage rate is now 5.67 per cent, according to Rightmove.

Rachel Springall, finance expert at Moneyfacts said: ‘It’s great to see such competitive deals launched by Yorkshire Building Society.

‘Borrowers looking for a new low-rate mortgage will find the sub-5 per cent five-year fixed deal is the lowest rate available in its sector.

‘The incentive packages available across all the new deals today may also be popular with borrowers looking to save on the upfront cost of their mortgage.’

Why are mortgage rates going down?

Yorkshire BS’ decision to cut rates, which includes shaving off up to 0.46 percentage points from its 95 per cent loan-to-value deals, is partly due to competition between lenders.

HSBC has also slashed mortgage rates by 0.15 percentage points on average today, alongside rate cuts across its buy-to-let range of up to 0.3 percentage points.

Last week there were also cuts from Coventry BS, Nationwide BS, Accord, Generation Home, Barclays, and Clydesdale Bank.

Past the peak? Fixed mortgage rates appear to be falling back somewhat after a barrage of rate hikes in recent months

Rate cuts have also been encouraged by future market expectations over where interest rates are heading.

Market expectations are reflected in swap rates. These are agreements in which two counter parties, for example banks, agree to exchange a stream of future fixed interest payments for a stream of future variable payments, based on a set amount.

Mortgage lenders enter into these agreements to shield themselves against the interest rate risk involved with lending fixed rate mortgages.

Put more simply, swap rates show what financial institutions think the future holds concerning interest rates.

Five-year swaps are currently at around 4.56 per cent, which is down from 4.74 per cent at the start of this month.

Only as recently as July, five year swaps were above 5 per cent. Similarly, the two-year swap rate is now 5.21 per cent. In July early this was around 6 per cent.

Ben Merritt, director of mortgages at Yorkshire Building Society, said: ‘This week, favourable market swap rates presented just such a window to reduce our mortgage costs, and offer the greatest incentive to those people who typically struggle the most, those with the lowest deposits to put down, including first-time buyers.’

Nicholas Mendes, mortgage technical manager at broker, John Charcol says he wouldn’t rule out a five-year fix at 4.5% by the end of the year

Will mortgages be hiked again if base rate rises?

The Bank of England is widely expected to increase the base rate from 5.25 per cent to 5.5 per cent on Thursday, though some economists are betting on it remaining the same.

The decision will come the day after we learn August’s inflation reading, which many are expecting may go up as a result of higher fuel prices. This may have some bearing on what the Bank of England decides to do with base rate.

If base rate does go up, this will likely increase costs for those on variable rate mortgage deals.

However, it is unlikely to have the same impact on fixed rate products, according to Nicholas Mendes, mortgage technical manager at broker John Charcol. In fact, he expects fixed rate deals to continue falling.

‘The MPC meeting is expected to either hold or rise by 0.25 per cent which will no doubt be the last [rate rise],’ says Mendes.

‘Even in the event there is a rate rise this has already been caked into fixed rate pricing.

‘As a result I expect to see fixed rate pricing on two and five year fixes continue to reduce.

‘While no one can accurately be confident, I wouldn’t rule out a five year fixed at 4.5 per cent by the end of the year based on current pricing trajectory.’

How are mortgage rates affecting the housing market?

While it is good news that mortgage rates are falling, we remain a long way from the low rates enjoyed in previous years.

This time last year, it was possible to secure a fixed rate at 3 per cent and the year before that borrowers were able to secure deals at less than 1 per cent.

The change in mortgage rates has unsurprisingly had an impact on the housing market. Transactions are down by almost 20 per cent, while house prices are also falling.

Last week it was reported that mortgage arrears had hit their highest level for nearly seven years.

The value of outstanding home loans with arrears climbed by 13 per cent to £16.9billion in the second quarter of this year, according to Bank of England figures.

It was the highest level since the third quarter of 2016, and 29 per cent higher than the same period a year ago.

Although there may be less activity across the housing market, Mendes says he isn’t expecting to see a sudden surge in forced sales.

‘Fixed rate mortgages around 5 per cent may dampen purchase demand as prospective home movers postpone their plans, but I still expect to see first-time buyers to continue purchasing,’ he says.

‘With rents continuing to increase, fixed rates at 5 per cent or less could encourage more first time buyers and those in rented accommodation to purchase as a cost-effective alternative.

‘A significant increase in arrears was down to landlords which is understandable in this climate over the past year.

Downwards: Over the past few weeks, mortgages rates have continued to trickle downwards due to competition between lenders and market expectations about interest rates in the future

‘For residential homeowners there are more options to avoid falling into arrears – unless they decide to bury their head in the sand.

‘There is more support from lenders and the Mortgage Charter which allows a grace period of six months which would allow mortgage holders to sell a property before things start to escalate downwards.’

Mark Harris, chief executive of mortgage broker SPF Private Clients, says that falling mortgage rates will result in buyers being able to afford bigger mortgages which should lead to an increase in transactions.

Harris adds: ‘Falling interest may encourage more borrowers to take the plunge and take on a mortgage. However, it is not just about falling mortgage rates but affordability and the underwriting of the loan.

‘Lenders are still required to stress test the borrowing at a minimum of 1 per cent above the reversion rate, with some lenders utilising different lower rates for long/longer term fixes.

‘When these stress rates also start to fall, borrowers will be able to take on bigger mortgages, which may lead to an uptick in transactions and mortgage lending.’

House & Hold: At House & Hold’s Labor Day sale, save up to 20% off brands like Tom Dixon and Four Hands.

IKEA: The Swedish retailer is celebrating 80 years in business with a mega anniversary sale running between now and September 5, where you can shop over a thousand deals all over the store.

Industry West: One of our favorite places for kooky modern furniture is throwing a 25% off Labor Day celebration sitewide. Just use the code “LABORDAY” to partake.

Jayson Home: On Labor Day only, clearance items at Jayson Home will be a whopping 70% off, so strike fast if you see something you like.

Joybird: Plenty of Joybird’s couches-in-a-box are marked-down up to 45% off for Labor Day, along with a rousing 35% off sitewide otherwise.

Sixpenny: Big spenders can take 20% off orders of $1,000 and up at furniture company Sixpenny (where muted linen slipcovers are the name of the game) with the code “WILDFLOWER” at checkout.

Sundays: Take up to 25% off at Sundays’ Labor Day sale, including the GQ Home Award-winning chubby dining room table, cozy boucle beds, and much more.

Wayfair: Wayfair recently dropped a massive Labor Day clearance sale, offering markdowns of up to 70% off furniture, cookware, and bedding.

West Elm: West Elm has also kicked off Labor Day with an up to 60% off sale on thousands of its modern furniture designs.

Urban Outfitters: Don’t sleep on all the furniture and home deals going on over at Urban Outfitters, including stylish velvet seating, carved-out entertainment consoles, Space Age-y shelving and more. They’re not just for teens!

Decor Deals

Saunders

S soy and beeswax candle

Saunders

Lulu & Georgia

shams (set of 2)

Lulu & Georgia

Lulu & Georgia

Nilani Rug

Alabax Medium Surface Mount

ABC Carpet & Home: Whether you’re shopping in-store or online, ABC Carpet & Home’s slashing up to 40% off everything, including plenty of colorful rugs, pillow shams, throws, and more.

Food52: Food52’s having a massive Summer Sendoff event right now where you can take 20% off orders of $250 and over, or 25% off orders over $500. Just use the code “SAVEBIG” at checkout to, ahem, save big.

Jiu Jie: Jiu Jie’s Instagram-famous knot cushions will be marked-down through Labor Day starting today. Take 30% off, no code necessary.

Lumens: Save up to 50% off design-y lighting and fixtures at Lumens’ massive sitewide Labor Day sale.

Little King: One of our favorite small businesses in the upstate New York area is throwing a summer sale, where you can find markdowns on everything from Marimekko towels to tiger rugs.

Lulu & Georgia: Lulu & Georgia’s Labor Day sale has officially dropped, offering 20% off your purchase—including existing clearance deals on on rugs, storage baskets, and pillow shams.

Matches: A small selection of tasteful home goods are marked-down over at Matches’ High Summer sale, including wavy candles, ceramics, and glassware.

Rugs USA: Hunting for a specific kind of Persian or jute rug? The world is your oyster at the online emporium Rugs USA, where everything is an extra 20% off.

HELOC, Manufactured, Technology, Marketing, and Digital Tools; Central Banks and Inflation

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

HELOC, Manufactured, Technology, Marketing, and Digital Tools; Central Banks and Inflation

By: Rob Chrisman

7 Hours, 56 Min ago

If you want something sobering, almost mesmerizing, here’s a short drone video of the flood damage in Libya (at the 15 second mark you can see how it tore through the city). Fortunately not so sobering are some stats out of the United States. The U.S. homeownership rate in 2022 was even higher than before the COVID-19 pandemic at 65.8 percent compared to 64.6 percent in 2019. That rebound was driven largely by those aged 44 and younger. And who says Millennials aren’t buying homes? Homeownership continued to climb from the foreclosure crisis (2004) and Great Recession (2008), when rates dipped as low as 63.4 percent in 2016. Homeownership rates recovered approximately half of the 5.6 percent decrease from 2004 to 2016. In Hawai’i the homeownership rate is 59 percent, I bring up the Aloha State because American Savings Bank, First Hawaiian Bank, and Central Pacific Bank joined Hawaiʻi Community Lending, a Hawaiʻi-based nonprofit community development financial institution, in pledging to provide mortgage forbearances to Maui families impacted by the recent wildfires. (Today’s podcast can be found here and this week’s is sponsored by the Trade-In Mortgage powered by Calque. Homeowners can buy before they sell, make non-contingent offers, and tap their home equity to fund the down payment on their next home. Lenders can help their clients negotiate a lower purchase price, reduce their interest payments, and eliminate PMI. Today’s podcast features Greg Korn and Ben Petit in an interview from the New England Mortgage Bankers Conference.)

Lender and Broker Software, Products, and Services

In an era defined by technological advancements, Dark Matter Technologies LLC emerges as a transformative force in the mortgage origination landscape, marking its evolution from Black Knight Origination Technologies. Under the Perseus Operating Group of Constellation Software Inc., Dark Matter Technologies remains steadfast in its commitment to pioneering innovation. CEO Rich Gagliano aptly sums up the company’s vision: “Dark Matter Technologies is on a mission to revolutionize the mortgage origination business by supporting, growing, and aggressively innovating new and existing products.” With over 1,300 dedicated mortgage technology experts and a portfolio that includes Empower, AIVA, Exchange, and more, Dark Matter Technologies is poised to lead the industry into a new era of unparalleled transformation. Learn more about Dark Matter Technologies and their mission, here.

There is approximately $9T in agency or government MSR outstanding. Billions of dollars are being transacted daily and this volume requires disciplined loan accounting processes to record loans accurately, produce investor reporting, and power business decisions. SBO from SitusAMC is a comprehensive loan accounting and master servicing platform that reconciles daily and monthly servicer cash collections down to the penny, aiding in the discovery of potentially misplaced funds and enhancing the financial integrity of the entire process. Servicers using SBO produce accurate and timely details providing confidence that their investor reporting obligations are being met. Schedule a demo of SBO with SitusAMC’s client-focused experts.

“Did you hear Capacity’s big announcement at TMC Fall? We’ve acquired Denim Social! Together, we’re building a support automation platform that helps you automate support, connect more authentically with your borrowers, and close more loans, faster. Read the press release to learn more! We also gave away a personalized AI Assessment worth $10,000 to help mortgage lenders identify opportunities for improving their business with AI. Plus, our new GSE Search feature pulls accurate, up to date GSE regulations within seconds using generative AI. Want to join the AI in mortgage revolution? Meet the Capacity team today.”

A new era in loan origination has arrived. Mortgage Machine Services, an industry leader in digital origination technology to residential mortgage lenders, announced the launch of its namesake platform Mortgage Machine™, an out-of-the-box, all-in-one LOS designed to accelerate lenders’ operational velocity and support an end-to-end digital origination process. Developed by digital mortgage pioneer and industry veteran Jeff Bode, Mortgage Machine utilizes intelligent automation, configurable business workflows and a cloud-based infrastructure to optimize the entire loan lifecycle and create a seamless lending experience. Key platform features include AI-powered task automation, a scalable cloud-based infrastructure, flexible APIs, pre-configured workflows for retail and TPO channels, integrated document management and POS functionality. Mortgage Machine also offers all-in-one eClosing capabilities, including an eClose room, eNotes, eVault and RON, and utilizes MISMO SMART Doc® data and security standards. Visit here to get started on your digital transformation journey.

Blend Labs continues to be the mortgage industry’s leading technology platform. Core to the platform is Blend’s unique integration with Desktop Underwriter® (DU®) and LPA. These integrations help streamline your approval process for borrowers, with all the conditions lined up for your fulfillment team. Add in intelligent and automated follow-ups and you’ll get to the closing table faster and more efficiently. Putting this information at the loan officer’s fingertips creates a streamlined process and eliminates manual work which equals lower costs, higher pull-through, and increased revenue. See more ways that Blend is committing to innovation and continues to lead the way.

Looking for timely advice on how to capture more loan volume and improve your bottom line in a down market? Now is the time to explore ways to tap into new markets. Expanding your mortgage footprint through new products and channels or by reaching new geographies insulates your business against economic and interest rate volatility by diversifying your sources of volume and revenue. By setting the groundwork to connect with new borrower markets now, you’ll open new revenue possibilities for when the market inevitably recovers, positioning your business to hit the ground running and beat out the competition. Download this informative eBook from mortgage solutions provider Maxwell for actionable advice, including how to create your expansion plan and choose the offerings best suited to the markets you want to pursue. Click here to download Growing Your Mortgage Footprint: How to Launch New Loan Products, Channels & Geographic Expansions.

Broker and Correspondent Products

Build your book with AFR Wholesale® (AFR)! Now, get the chance to listen from and ask questions directly to AFR and Freddie Mac to turn those prospects to active pipeline at the next Why Wait webinar series covering Manufactured Home Financing on Wednesday, September 20th at 1 PM EST. Register here today! Have you and your borrowers looked into Manufactured Housing as an option? With unbeatable affordability, customization options that are very tailored, quick installation and trusted quality, manufactured homes are worth exploring. Especially with a top lending partner in AFR who has been an industry leader for over 25 years. This is a live webinar, and a recording will not be provided so make sure to join and get great insight and have the opportunity to ask questions and listen to scenarios! Visit AFR Wholesale, email [email protected], or dial 1-800-375-6071. AFR Wholesale® – Don’t wait. Register today!

“With Cash-Outs on the decline during this high interest rate environment, it is important to present your borrowers with different cash-out options. That is why Vista Point is announcing a brand new HELOC product coming soon, in addition to our existing Closed-End Second. Our HELOC product is being designed as a complement to our Closed-End Second to provide a full suite of Equity Solutions. Our HELOC will provide a specific solution for borrowers that want the optionality of an interest-only payment, or the ability to draw up and buy down their line during the 5-year draw period with no Appraisals up to $250k. Just like on our Closed-End Second offering, with HELOC loan amounts up to $550K and combined lien amounts up to $2.5M, your borrowers can get the cash they need without sacrificing their advantageous 1st mortgage rate. HELOC will be available for full doc and bank statements on OO and 2nd homes. For more information, reach out to us, or meet us at the Philly MBA to discuss.”

Capital Markets

We learned last week that prices in August rose by the largest monthly percentage in 15 months. However, that month-over-month inflation was widely expected due to a surge in gasoline prices. Underlying oil prices are also pointing towards further increases in September. Meanwhile, core prices were up 0.3 percent and core goods prices declined by 0.1 percent. Over the last three months core prices have increased at an annualized pace of 2.4 percent, the lowest three-month pace since March 2021. Retail sales rose faster than analysts’ expectations in August, also due to higher gas prices. Many analysts expect consumer spending to slow as excess savings built up over the pandemic have materially declined and credit is increasingly costly and difficult to obtain. Additionally, the resumption of student loan payments is expected to cut into discretionary spending. It will take more than expectations of slower spending before the Federal Reserve feels inflation is firmly under control.

What could move mortgage rates this week? The U.S. Federal Reserve, Bank of England, Bank of Japan, and the central banks of Norway, Sweden, and Switzerland are all announcing rate decisions after a spate of recent inflation data shows that price increases are alive and well. The Fed’s Federal Open Market Committee (FOMC), the action arm of “the Fed,” is not expected to raise rates. It’s unlikely that the commentary around the commitment to keep fighting inflation and higher rates for longer will change either, but it could tilt a little more to the hawkish side after a stronger-than-anticipated inflation report for August.