I had a conversation with a friend the other day about his current housing situation.

In a nutshell, the home he resides in isn’t large enough for his family, nor does it have certain amenities like a swimming pool.

At the same time, he loves his home and the very cheap mortgage attached. Like millions of other Americans, he’s got a 30-year fixed in the low 3% range.

This has created a dilemma for him and many others, who want to move, but can’t make it pencil at today’s rates and asking prices.

But one thought is to rent out his current home and then rent another, as opposed to buying. Or selling for that matter.

It’s Possible to Rent Out Your Current Home and Rent Yourself

One trend that has emerged of late is the ‘rent out and rent’ scheme.

The way it works is relatively simple. If you’re an existing homeowner, you simply rent out your property to someone else and then go rent a different home.

This allows you to keep your low-rate mortgage intact, and it allows you to rent for less than what a new mortgage would cost.

It works because the PITI on the old house is so low, and asking rents are pretty attractive in many markets nationwide.

Sure, there might be a premium for rent on the new property, but it can still be the cheaper option relative to buying a home.

And the homeowner doesn’t need to worry about a large down payment, or losing their original home, which could now be seen as an investment property.

Let’s Look at an Example of Rent Out and Rent

Current monthly PITI: $3,500 per month

Potential rent for existing home: $6,000 per month

Cost to rent a larger home: $7,500 per month

Cost to buy a larger home: $10,000 per month plus $300k down

Cost to rent out and rent: $1,500 per month

As noted, I’ve got a friend considering a rent and rent out arrangement. Somewhat incredibly, the property he has his eye on is literally across the street.

This makes it easier, at least from a moving point of view. He can probably just lug his stuff over on his own, if he’s up for it.

It also allows him to keep an eye on his old property, which can be helpful but also perhaps a bit awkward.

Anyway, the house across the street is larger, has a view, and has a swimming pool. These are all wants and needs.

However, the price tag is a bit higher, we’ll call it $7,500 per month to rent. The good news is his current mortgage payment (full PITI) is just $3,500 a month.

And he can potentially rent his place for $6,000 per month because he got in cheap about a decade ago with that ultra-cheap mortgage rate.

If we do the math, it would cost $1,500 more per month to rent the larger home, using the cash flow on his existing property to offset the increased rent.

But he gets the larger space, the nicer home, the pool, the view, etc.

Perhaps more importantly, he doesn’t need to buy a home at today’s lofty prices and come in with a massive down payment.

Assuming they purchased a similar property, they’d need a $300,000 down payment and the mortgage rate would likely be 6-7% versus their current 3% rate. Ouch!

This Works When Home Prices Are High and Your Existing Payment Is Low

The reason this strategy works right now is because it’s more expensive to buy a home than rent in many places.

You can thank both high mortgage rates and high home prices, which have moved higher in tandem.

As I always say, there isn’t an inverse relationship between home prices and mortgage rates.

They can both go up together, go down together, or sometimes diverge.

This plan also works because many homeowners like my friend got into their current homes when prices and rates were low.

So they essentially have a lot of wiggle room to cash flow if renting out their existing properties, which can then be used toward a new home.

But instead of buying, they can simply pay a little extra in rent to get what they want, while continuing to enjoy appreciation on the old property.

At the same time, any improvements made on the old home benefit them as well. And they can always move back in the future.

For the record, this strategy can also be employed with downsizing. So a pair of empty nesters can rent out their larger home and go rent a smaller one.

In their case, we’re talking lower rent, potentially leading to some additional cash flow without having to commit to a new home purchase.

There Are Pros and Cons to Renting Out and Renting

It’s not without its risks though. When you rent, you’re at the mercy of your landlord. They might want to sell at some point, at which time you’d need to move.

You could also be limited in terms of making improvements or changes to the property.

In addition, you’re now a landlord yourself, which isn’t always a passive job. And the tenants present new risks, such as failure to pay rent.

It’s also possible to find your old home vacant for a month if you’re unable to find a tenant.

So you could be in a situation where you have to float two monthly housing payments. If you’re unable to, well, you’ve got a problem.

But the advantages are there too. You get the property you want/need for a lot less than what it might cost to buy.

And you get to keep your old home, which could be an incredible investment opportunity.

You’ve also got optionality. You can rent for a while then go back to your old home. Or decide after a while to buy something.

You aren’t necessarily locked in beyond the initial rental contracts in place, which might last a year.

It gives you time to determine your next move, assuming you’re not quite sure what you want to do.

Unfortunately, this also speaks to the dearth of for-sale inventory available in the housing market today.

And the incredible position many homeowners are in, thanks to their low-rate fixed mortgages.

Back in August 2020, the Aspen Institute analyzed U.S. Census data to calculate that without “swift intervention” there might be an estimated 30 to 40 million people in America at risk for eviction, with 29 to 43 percent of renter households at risk of eviction by the end of 2020.

Here we are in early 2021, and some “swift intervention” has arrived in the form of an extension of a Centers for Disease Control and Prevention nationwide ban on “certain residential evictions.” The CDC order, which defines a temporary halt to residential evictions to prevent the further spread of COVID-19, went into effect on Sept. 4 and was to end on Dec. 31, 2020. It’s now in effect until March 31.

Aside from any federal rules, many states have put their own eviction bans in place. The NOLO legal information website has a list of state eviction protections. Princeton University’s Eviction Lab monitors weekly reports through its Eviction Tracking System with nearly real-time updates on states’ moratoria. For more updates, check with a legal aid organization where you live.

All good news but cold comfort if you’re one of the people who has already been evicted. Although it’s never a good time to leave your place of residence, to have to do so during a global pandemic adds an extra layer of fear and uncertainty. Aside from health worries, how do you get an apartment with an eviction? What happens to your credit? Will you be able to rent again?

What are the reasons for an eviction?

The following are some reasons you might face eviction:

Behind in rent

Won’t leave the property after the lease is up

Violated the terms of the lease

Engaged in illegal activity

Damaged the property

What does an eviction mean?

Landlords have to follow a series of legal steps before they can put you out. They can’t just change the locks while you’re not home.

Usually, but depending on local laws, the landlord has 30 days to notify you in writing that they’re terminating your lease. They must attend a hearing and make a case for why you, the renter, need to leave. If the landlord wins the case, and you don’t leave or make changes — by paying the back rent, for example — they will then contact law enforcement and schedule an eviction date. A sheriff or marshal will give you notice that law enforcement will arrive a few days hence to escort you off the premises.

You can, of course, defend yourself against an eviction if you believe it’s wrongful — a landlord’s illegal activity, the property is uninhabitable, the landlord is retaliating against you for demanding repairs.

Will eviction affect your credit?

An eviction shows up on your legal record, which future landlords will be able to access, and remains there for seven years. The eviction will not show up on your credit report, but it may affect your credit in these ways:

Your landlord may have sent unpaid rent information to a collections agency

If your landlord sues you in court for unpaid rent and wins, you’ll have a civil judgment against you. That civil judgment will show up on your credit history.

You can petition the court to expunge the eviction from your legal record. You can then contact the credit reporting agencies to remove the civil judgment from your credit report. Getting rid of the collections agency from your credit report will be more difficult.

If unpaid rent was the reason for your eviction, do all you can to make amends with your previous landlord or the collections agency. That includes paying back what you owe.

What steps can you take to rent again?

You may have trouble finding apartments that accept evictions. For one thing, many property owners require a background check, but it’s possible to find some private owners who ask only for reference letters or apartments with eviction forgiveness. So, check upfront about how they will vet you.

While you’re looking for an apartment that accepts evictions, spend time rebuilding your own personal portfolio to show future landlords you’re worth any perceived risk:

1. Rebuild your credit

If you were delinquent in rent and got backed up on other bills, you’ll have dings on your credit report. You may want to engage a credit counselor to help in consolidating debt and creating a debt-management plan. (Check the Federal Trade Commission website for information on credit counselors.)

Ultimately, you’ll need to make a commitment — and stick to it — to pay all bills on time every time. Reduce your credit card balances and don’t apply for new credit cards. Keep in mind, rebuilding your credit will take time.

2. Write a letter of credit

You’ve got to convince a new landlord that you’re creditworthy. Be transparent and honest about your credit history and let a prospective landlord know that you’ve learned from past mistakes and will move forward responsibly.

You can do this by phone or by writing a letter in which you explain your circumstances. Offer details about how those have changed, e.g. you now have a higher paying job and define how you’re working to rebuild your credit. Back up your claims with pay stubs and reference letters.

3. Have references ready

Perhaps you have previous rental experience in which you were never late on payments. Get that landlord to write a letter attesting to that. You can also get employers, business partners, family and friends to write letters on your behalf.

4. Sweeten the deal

If you can afford it, offer to pay upfront more than what might be asked of you. Perhaps you can swing first and last month’s rent. Or, offer to pay a higher security deposit. Have a co-signer ready to help back your lease agreement. This makes you less of a risk.

You can find apartments that accept evictions

You want to make a good impression when you meet a prospective landlord to make your case. Dress neatly, stay calm, be honest and focus on your positive attributes. Although it might seem like it, an eviction is not the end of the world. Stay positive and spend time researching and preparing for how to get an apartment with an eviction.

Stacey Freed is an award-winning writer and former senior editor for Remodeling, a trade publication focused on the business of the remodeling and construction industry. As an independent writer, she continues to write about the building, design, architecture and housing industries. Her work has appeared in Better Homes and Gardens and USA Today special interest publications, Realtor magazine, This Old House, Professional Builder and online at AARP, Forbes.com, House Logic and Sweeten.com among other places.

Seems like a simple thing — to measure the square footage of a house. Just multiply the length by the width of each room and add up all your numbers. Not so fast. First of all, what’s a “room”? Do closets count? Basements? And why does accurate measuring even matter? There’s a lot to unpack.

What’s so important about getting square footage right?

If you’re moving into a new home and you want to know if your California king is going to fit into the primary bedroom, it’s nice to know the room’s square footage.

But there’s more riding on how to calculate the square footage of a house than just being able to fit your stuff. The square footage of a house determines its value. Lenders rely on square footage for mortgage calculations, tax assessors rely on square footage for assessments.

So, if you’re renting a house now but thinking of buying, it’s important to understand your current square footage so you can make a good comparison when house hunting.

What’s included in a house’s square footage?

There are several different answers to this question. First, here are a few terms to understand:

GLA (gross living area) is a home’s finished livable space above ground. And, if any part of the finished space is below grade, the entire area is typically known as below grade. GLA calculates when appraisers measure the home’s exterior. It goes in public records and is often important for tax purposes.

TLA (total living area) is like GLA but it includes finished basement space or possibly an accessory dwelling unit (ADU).

Living space is determined by American National Standards Institute (ANSI) Z765, which is a voluntary guideline for describing, measuring, calculating and reporting area for single-family homes.

Living space generally refers to “anything that is under the roof, within the house that is finished and heated — space heaters don’t count,” said Bryan Reynolds, a Certified General appraiser in Kentucky and Tennessee and president of the National Association of Appraisers.

Rooms to measure when calculating the square footage of a house

You might be surprised by which rooms are included — and which are not — when determining how to figure out square footage:

Bedrooms

Bathrooms

Kitchens

Hallways

Finished closets

Areas that don’t count towards the square footage of a house

There are plenty of rooms or spaces in your home that would qualify as “living space,” but don’t get counted in the total square foot calculation:

Finished basement: Say you have a ranch home with 1,000 square feet above ground and a 1,000-square-foot finished basement. An appraiser would say it’s 1,000 square feet of above-grade space and 1,000 square feet below grade. A real estate agent might say that there are 2,000 total square feet.

Enclosed porch: “If it’s unheated or used seasonally and there’s a separate door to the livable area, then it’s not included,” Reynolds said. But “if it’s finished in similar quality to the rest of the home, functional in design and has a heat source that is permanent in nature, then it can be included.”

Garage: The normal garage storage space doesn’t count. However, a bonus room above the garage might count. Only if it’s heated and 100 percent finished to a similar quality as the house. And, if it’s directly accessible from the inside of the house though.

Accessory Dwelling Unit: Unless it’s actually part of the house, it’s considered a separate entity.

Then, if you want to really get into the weeds, what about the sort of dead space under the stairs? According to Reynolds, ANSI says to include it, but AMS (American Measurement Standard) allows you to remove it from the square footage equation.

And, if you’ve got a bay window with a bench under it, one could argue that if you were to take the bench away, there would be useable floor space and that should come with the square footage.

How to figure out the square footage

Now that you know what to measure, here’s how to measure. But first, remember the aforementioned ANSI Z765?

For a room to make it in a home’s total square footage, the ceiling must hit a certain height — seven feet or higher or six feet four inches if there are beams or soffits. Plus, no portion of the finished area can have a ceiling height of less than 5 feet.

Let’s say you’ve got a Cape Cod with a sloped ceiling and knee walls. That portion under the sloped ceiling (if it’s five feet or less) is not counted in the square footage (see image). In addition, the rest of the ceiling must hit at least seven feet for at least half of the room’s floor area.

Photo source: AccurateHomeMeasuring.com

Keep in mind that an appraiser will, hopefully, look around inside the house but will measure the house from the exterior — unless there’s that pesky sloped ceiling situation, in which case they will have to go inside or the square footage will be off.

According to Hamp Thomas, certified residential appraiser and author of “How to Measure a House Using the ANSI Standard,” the pros use a 100-foot tape measure to do their job. Certainly, a shorter tape measure would work. However, there is a lot of stopping, starting and adding that can lead to inaccuracies.

Measure around the outside of the house above the foundation. Multiply the length by the width of each rectangular space. If you’ve got a second story and can’t reach a corner on the exterior, for example, measure from the inside and then add the width of the exterior walls.

Know why you’re measuring

It’s likely that, if you’re reading this, you’re not a professional appraiser. If you’re interested in getting a general sense of how much footage you have in your house, grab a measuring tape and measure each room’s length and width and multiply those numbers. Then add all the square footages together. “Don’t forget to include any outside walls thickness, or just measure from the exterior,” Reynolds said.

If a room isn’t a nice rectangular shape and has jogs and bumps, create rectangles, measure and multiply the length by width. Then, add up all the bits and pieces.

And if old-school tape measures aren’t your thing, there are lots of free measurement apps that you can download to your phone. You can also put the information into Calculator Soup’s square footage calculator, which can help you figure out the square footage of differently shaped rooms.

Measure on.

Stacey Freed is an award-winning writer and former senior editor for Remodeling, a trade publication focused on the business of the remodeling and construction industry. As an independent writer, she continues to write about the building, design, architecture and housing industries. Her work has appeared in Better Homes and Gardens and USA Today special interest publications, Realtor magazine, This Old House, Professional Builder and online at AARP, Forbes.com, House Logic and Sweeten.com among other places.

The holidays are upon us, and our thoughts turn to shopping, eating and decorating. But safety is never far from our minds. Keeping the holidays fun and safe takes a little prepping and planning. Here are eight holiday safety tips to keep you and yours healthy and safe as you head into the jolliest of seasons.

1. Avoid delivery dramas

The holidays are prime time for thieves. The USPS delivers more than 28 million packages per day for the 10 days before Christmas. Here are a few holiday safety tips to keep your packages secure:

Install a safety camera or video doorbell

If there’s not one in your building, talk with your landlord or property manager about creating a dedicated package room with a door

Get to know your neighbors as a lot of folks are working remotely. They could keep an eye out for deliveries.

Add delivery instructions to packages such as leaving them in a spot where no one will notice them

Employ one or more of these tactics to keep your holiday goodies safe and out of the hands of would-be thieves.

2. Don’t fan the flames

Candles and fireplaces are romantic but can also become problems if you don’t take precautions. Keep children and pets away from burning candles and lit fires and always remember to snuff out candles before going to bed. If you do have little ones, consider using battery-operated candles and flameless tea lights for that warm glow.

If you want to make a fire, ensure your fireplace flue is open and keep the damper open until the fire is out. Clear away any flammable clutter — books, magazines, draperies, furniture — before lighting the fire. Keep a screen in front of the fireplace at all times. Make sure the fire is completely out before you go to bed or leave the house.

While the risk of fire attributed to Christmas trees is small — about 160 fires (out of roughly 358,500 home fires) according to the National Fire Protection Association (NFPA) — it’s still something you should consider. Most of those fires involve real trees, which is why many apartment buildings do not allow tenants to use living trees for the holiday (check your lease agreement or with your property manager or landlord before dragging home a tree from the local scouts).

Keep your Christmas tree at least three feet from fireplaces, radiators and other heat sources. Make sure you keep up with the watering. There’s nothing worse than stepping with your bare feet on dry, spiky needles — except those dry, spiky needles catching on fire.

Unplug the lights if you leave the house and before you go to sleep. If you purchase an artificial tree, make sure it has a fire-retardant label. And if you have a metallic tree, never decorate it with electric lights. If the lights are faulty, the tree can become charged and anyone touching it could be electrocuted.

And this might be the biggest holiday safety tip of them all: Once the holidays are over, don’t wait too long to take down your tree and lights. Not only will it be safer, but it will make your neighbors happy.

3. Tame your travel troubles

If you’re heading out of town for the holidays, there’s a lot to think about beyond directions for getting over the river and through the woods.

Make sure your car has a roadside emergency kit that includes items such as blankets, a first aid kit, a tool kit, a small shovel, a flashlight and extra batteries. Keep a few gallons of water on hand.

Holiday gatherings are what the holidays are all about, and they often involve alcohol. Seems like this holiday safety tip should be a no-brainer, but, always name a designated driver or take an Uber, Lyft or taxi home.

We’re still facing the effects of the pandemic. When you stop at roadside facilities, wear masks and avoid crowds. The CDC still recommends staying at least six feet from people who are not traveling with you. Wash your hands often.

4. Ditch your decorating dilemmas

From fires to choking to cuts and poisoning, decorating your home for the holidays is a minefield of potential hazards.

That box of old decorations may no longer be safe: broken lights and wires are an electrical hazard; older tinsel might be lead-based; aging angel hair is abrasive to your skin. And breathing in spray-on artificial snow can cause everything from a headache and nausea to difficulty walking and heart palpitations.

Read the labels for proper use of these products or update your box of decorations with some newer products that have safety labels from an independent testing laboratory.

Take extra precautions if there will be children around. To you it’s a decoration, but to them, the colorful baubles look like candy. Keep trimmings out of reach and avoid those that are easily breakable or sharp.

And take care when decorating. Remember that chairs are not ladders. There are about 200 decorating-related injuries every holiday season — usually involving a fall.

5. Lose lighting liabilities

With its tangle of wires, peering into your holiday decorating box is like looking into a snake pit. The U.S. Consumer Product Safety Commission suggests you check light strings for broken bulbs, frayed wires, cracked sockets and loose connections. Replace damaged ones and don’t use more than three standard-size sets of lights for each extension cord. Keep “bubbling” lights away from children. These lights have a chemical that’s hazardous if ingested.

Here’s a simple holiday safety tip for your lights: If you’re hanging lights outside, make sure they’re securely fastened to the house, trees or walls to protect them from wind damage.

6. Set shopping safeguards

Don’t forget that thieves also have holiday wish lists, and they don’t go on vacation between Christmas and New Year. (Although they are less active on Thanksgiving.) You don’t want to make it easy for them, so keep these holiday safety tips in mind when you’re shopping.

If you’re out with your car, park in a well-lit area and stow any purchases in the trunk. Pay attention to your surroundings. Thieves often troll parking lots and wait for the right moment — like after you’ve unloaded your packages and you head back into the mall. Be sure to lock your car and don’t leave your fob behind.

Use electronic payments as much as possible, and don’t carry around too much cash. Check your bank statements regularly to make sure your purchases and only your purchases are accurately recorded.

If you’re shopping online, be alert for scams. Make sure you’re on a reputable site before you hand over your credit card number. (And, if you can, use a credit card that’s designated for your online purchases.) This holiday safety tip should be followed all year round: When you get emails announcing great deals, don’t click on any links. Check out sites separately and never through an unsolicited email.

7. Cut out cooking calamities

Cooking fires top the list of residential fires, and according to the Consumer Product Safety Commission, three times the average number of daily cooking fires occur on Thanksgiving Day (about 1,700 each year). For fire safety, always have a fire extinguisher on hand and use it to smother flames (don’t use flour or water). Remember to turn pot handles toward the back of the stove, and don’t wear loose clothing while you cook.

Frying turkeys has become increasingly popular at holiday time. The NFPA reports that these deep fryers cause an average of five deaths, 60 injuries and more than $15 million in property damage each year. If you use one, don’t leave it unattended and don’t overfill it. Wear safety goggles, closed-toed shoes and use the fryer outdoors, making sure it’s far from flammable materials.

Practice good food safety. Wash your hands often, separate raw meat from produce, cook all meat to the right temperature and refrigerate leftovers within two hours of serving.

8. Consider holiday safety tips for pets

The holidays are exciting but dangerous for pets. They love shiny objects. Lots of guests “accidentally” share food with them. Beware of the following, especially:

Tinsel: It’s not poisonous, but if your dog or cat eats it, the tinsel can get stuck in their teeth or stomach. It may cut or bunch up in their intestines. If you think your pet had a tousle with tinsel, get your pet to the vet’s office right away.

Toxic foods: Chocolate, grapes, raisins, currants and macadamia nuts can all be toxic to both cats and dogs. The iKibble app offers information on what foods are toxic for dogs, as well as the general healthiness of foods.

Mistletoe and holly: If your pet eats these, they may get diarrhea and vomit. Never a good look on Christmas morning. Feature these plants in places your animals can’t reach.

“Adult” party substances: A jolly night for you and your friends is downright dangerous to your pets. Keep alcoholic beverages and marijuana (now legal for recreational use in 19 states) stowed away. Clean up anything that might have hit the floor. No one likes a hangover, and you certainly don’t want to spend precious holiday time off at the emergency vet’s office.

Keep your furry friends in mind as you set up your holiday decorations. They want happiness and healthiness this year, too.

Take extra precautions by following these holiday safety tips

With COVID still an issue, you’ve got an additional layer of concern this year. We’re all looking forward to gathering in person, but we still need to be cautious. Schedule smaller gatherings. Ask people about their vaccination status and determine what works for you. Wear a mask when you’re in a crowd and shop online if you’re uncomfortable being among the throngs of shoppers.

Be healthy, be safe and happy holidays to all.

Stacey Freed is an award-winning writer and former senior editor for Remodeling, a trade publication focused on the business of the remodeling and construction industry. As an independent writer, she continues to write about the building, design, architecture and housing industries. Her work has appeared in Better Homes and Gardens and USA Today special interest publications, Realtor magazine, This Old House, Professional Builder and online at AARP, Forbes.com, House Logic and Sweeten.com among other places.

Whether you’re selling your home to begin a new adventure or refinancing your existing home, getting an appraisal with the value you want is an important hurdle to clear. You may feel that the appraisal process is out of your control, but there are many easy and inexpensive ways to get both yourself and your home ready.

We put together a checklist of our top tips below. But first, let’s quickly cover the basics of home appraisals.

What Is a Home Appraisal and Why Is It Important?

A home appraisal is an unbiased report on the value of your home performed by a trained and state-licensed individual. Appraisals are an essential part of the home financing process, ensuring the homebuyer, seller and mortgage lender each have an impartial, consistent and accurate assessment of the value of the property under consideration.

The lender is responsible for ensuring that your home provides adequate collateral for the mortgage. For most loans, the lender obtains a signed and completed appraisal report that accurately reflects the market value, condition and marketability of the property.

It’s the appraiser’s job to provide a factual, unbiased and detailed description of the property and the neighborhood. They must take into account all factors that influence a home’s value when developing the market value opinion in the appraisal report.

Home Appraisal Cost

While home appraisal costs can vary by state and property size, the fee can range between $300 and $1,200. Most fall somewhere around $600-$1,000, with costs based primarily on the geographical area of the home.

How Long Does a Home Appraisal Take?

From start to finish, the home appraisal process usually takes approximately 7-10 days to complete.

The required in-person visit by a home appraiser can take over an hour, depending on the size of your home. However, several other steps are involved in making an unbiased and professional assessment of your home’s value. Your appraiser will research trends, local county records and recently closed comparable homes in your area, known in the industry as “comps.”

Once your appraiser compiles and analyzes all the information and data, they will present a final report of your home’s value.

What Do Home Appraisers Look For?

A home appraiser uses several sources of information to determine a property’s value. As part of the assessment, the appraiser will visit the property in person and review recently completed sales of comparable homes. Common factors examined during home appraisals include:

Property size. In real estate appraisals, size significantly affects the final number. In general, the higher the square footage of a home, the higher its value. An appraiser will also look at the kitchen, number of bedrooms, bathrooms and closets.

Exterior condition. When assigning a value to your property, the appraiser will consider not only the exterior appearance of your home but also its condition. They will check the following:

The condition of the roof, foundation, siding, gutters, chimney and walls, looking for signs of leaks, mold and other safety hazards

Lot size, including front and backyard square footage

Pool, outdoor kitchen, deck, porch and other amenities

Interior condition. Again, this refers not only to the appearance of the interior but also to the working condition of standard household assets such as:

Plumbing

Electrical and HVAC systems

Doors and windows

Light fixtures

Any kitchen appliances to be included in the sale

Attic, basement and foundation. A finished basement or attic may impact a home’s value, but these areas must meet specific requirements to be considered part of the Gross Living Area (GLA). An appraiser will also evaluate your home’s foundation and its condition.

Home improvements and renovations. Tell your appraiser about any work or upgrades you have done to spruce up your home. This can include anything from the central air system you installed 10 years ago to the kitchen flooring and countertops you just renovated (along with the new oven and fridge to match, of course).

What Hurts a Home Appraisal?

If an appraisal is in your future, it’s essential to understand the factors that could negatively impact it, such as the following:

Low-value comps and decreasing neighborhood property values

Poorly maintained interior or exterior

Age of the home

Location, such as a flood zone or busy road

Signs of mold, insect infestation, leaks or other safety concerns

Issues with the home’s systems, such as plumbing, electric or HVAC

Lack of parking

Hazardous construction materials like lead paint or asbestos tile

Outdated or faulty plumbing, electrical and heating systems

Some issues are in your control and some may not be. Whether you choose to address the correctable concerns or not, being aware of crucial appraisal criteria can help you avoid the potential unwelcome surprise of a lower-than-expected home value.

Top 7 Tips Home Appraisal Checklist

How does one best prepare for a home appraisal? We put together a checklist of common (and not-so-common) tips to help you get a high valuation from your appraiser.

1. Do Your Own Appraisal

Imagine that you are the appraiser. Walk around your home’s interior and exterior and really scrutinize it as if you were going to complete the appraisal report yourself. Take note of any obvious damage or deferred maintenance that needs your attention. Leaks, broken systems and damaged surfaces should all go on your list of things to repair.

Thoroughly inspect safety equipment like smoke alarms, carbon monoxide alarms and home security systems. Are they all functioning, or do parts or entire systems need to be replaced? Make a plan to repair these issues and clean up any cosmetic issues that may have occurred as a result.

2. Investigate Comps

Check out recent home sales in your neighborhood. What has the price range been for homes with features and updates similar to yours? The values of these comparable homes should be similar to what your home will appraise for. This information can help you know where to focus your time, efforts and funds.

If you know a neighbor (or real estate agent) who recently sold a home in your area, contact them to find out if there were any appraisal issues or insights that they can share.

If you’re working with a real estate agent, you can request that they collect some comps for you and your appraiser to review. Particularly if your home has unique or uncommon features, your agent may need to get creative while staying within the guidelines for selecting comps.

A quick way to get a rough idea of how much your home is worth is to use a home value estimator calculator. Add some basic information to gauge your home’s current value and view recent home sales in your area.

3. Get Superficial

Clean your house from top to bottom and remove extra clutter. Once you’ve scrubbed and straightened up everything possible, consider making some easy, low-cost cosmetic updates that can have a big impact, like the following:

Paint or touch up existing paint

Hang updated window treatments

Replace worn faucets, doorknobs and cabinet hardware

If you’ve been planning to update your decor after you move, consider bringing in a few of the newer pieces to make the old house look fresh and modern. Downsizing or packing for a long-distance move? Ask your real estate agent if they have staging furnishings you can borrow or recommendations for a service you can use.

4. Make Your Outdoor Areas Truly Great

Now that your home’s interior looks fantastic, it’s time to pay attention to the exterior. Make sure that your landscaping is looking its best by doing the following:

Mow your lawn, trim your trees and bushes

Remove weeds and dead vegetation

Add color with inexpensive, seasonal flowers in the spring, summer or fall, and ensure that snow removal is neat and tidy in the winter

You’ll also want to:

Remove outdoor clutter, like yard tools and stray toys, from everywhere on the property

Consider staging any outdoor living spaces with new furniture or accessories

Power wash your home’s exterior, as well as your driveway and any deck or patio surfaces

Ensure your pool is well-maintained and in safe operating condition

Most of this can be accomplished in a weekend, and the increased curb appeal will be worth it.

Check out expert tips for outdoor home renovations — you may find just the right improvement to increase your value!

5. Be Sure To Share Your Upgrades

Tell your home appraiser about the improvements you’ve made to your home. Inform them of upgrades like the following that will positively impact your appraisal value:

New features that you have added, like a security system

Updated HVAC units

Exterior improvements like siding, gutters or a new roof

High-value room remodels like kitchens and bathrooms

An easy way to make sure that your appraiser remembers all of these improvements is to create and share a short, one-page list detailing each. You should have this list ready in advance and include any applicable permit information.

6. Know Your Neighborhood

Make your appraiser aware of any recent improvements in your overall neighborhood. It’s worth mentioning things like:

New or highly rated schools

Parks

Transportation enhancements

Shopping

Other beneficial amenities

These kinds of changes can add significant value to your home, and if your appraiser is not a local resident, they may not be aware of them. Appraisers are often familiar with the general area, but you probably know your specific neighborhood better than they do.

7. Stay Focused

While you are working your way through the tasks and updates listed above, it’s important to remember not to go overboard and take on too many projects. Invest your time, money and effort only on issues that clearly need attention. If you’re getting an appraisal for a home you’re selling, you most likely already have a buyer who liked your home enough in its current state to make an offer on it. Making unnecessary major changes could end up being a waste of your time and resources.

Your home’s selling price is affected by much more than just the appraisal! Find out how the time of year can increase your sale price.

Although it’s not possible to change your bungalow into a country estate overnight, taking the time to tackle a few strategic projects before your appraisal can help put you in a better position to get the outcome you want. If you’re ready to move or refinance the home you love living in, get a custom mortgage rate quote from Pennymac today. Our Loan Experts can answer your questions and help guide you through the mortgage loan process.

Share

Categories

buying a home selling a home appraisal fundamentals

At last glance, 30-year fixed mortgage rates were sitting above 7%. Despite this, there are virtually no homes for sale.

One would assume that after such a massive interest rate spike, demand would flounder and supply would flood the market.

Yet here we are, looking at a housing market that has barely any for-sale inventory available.

And when you remove the new home inventory (from home builders) from the equation, it’s even worse.

Let’s explore what’s going on and what it might take to see listings return to the market.

Why There Are No Homes for Sale Right Now?

The housing market is highly unusual at the moment, and has been for quite some time.

In fact, since the pandemic it’s never really been normal. The housing market came to a halt in early 2020 as the world stopped, but then took off like a rocket.

If you recall, the 30-year fixed spent the entire second half of 2020 in the sub-3% range, fueling voracious demand from buyers.

And as Zillow pointed out, the age demographics had already lined up nicely for a surge of demand anyway.

Around that time, some 45 million Americans were expected to hit the typical first-time home buyer age of 34.

When you combined the demographics, the record low mortgage rates, a pandemic (which allowed for increased mobility), and already limited inventory, it didn’t take much to create a frenzy.

At the same time, you had existing homeowners buying up second homes on the cheap, due to those low rates and generous underwriting guidelines.

And let’s not forget investors, who were taking advantage of the very accommodative interest rate environment and the insatiable demand from buyers.

The rise of Airbnb and short-term rentals (STRs) coincided with this low-rate environment, potentially taking additional inventory off the market.

This quickly depleted supply, which was already trending down thanks to a lack of new home building after the prior mortgage crisis.

Home builders got burned in the early 2000s as foreclosures and short sales spiked and prices plummeted. And their excess supply sat on the market.

As a result, they developed cold feet and didn’t build enough in subsequent years to keep up with the growing housing needs of Americans.

Collectively, all of these events led to the massive housing supply shortage.

Low Mortgage Rates Got Buyers in the Door, But Will They Ever Leave?

Low supply aside, another unique issue affecting housing supply is a concept known as mortgage rate lock-in.

In short, there’s an argument that today’s homeowners have such low mortgage rates that they won’t sell. Or can’t sell.

Either they don’t want to give up their low mortgage rate simply because it’s so cheap. Or they are unable to afford a home purchase at today’s rates and prices.

Simply put, most can’t trade in a 3% rate for a 7% rate and purchase a home that’s probably more expensive than theirs was a few years earlier.

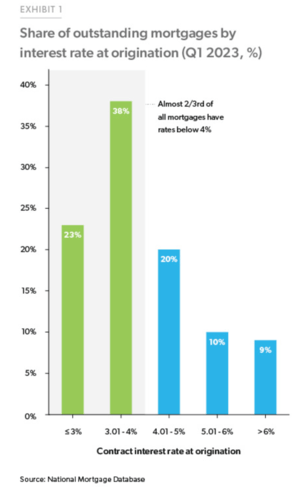

And this isn’t some tiny subset of the population. Per Freddie Mac, nearly two-thirds of all mortgages have an interest rate below 4%.

And nearly a quarter have a mortgage rate below 3%. How on earth will these folks sell and buy a replacement home if prices haven’t come down, but have in fact risen?

The answer is most will not budge, and will continue to enjoy their low, fixed-rate mortgage for many years to come.

This further explains why inventory is so tight and not really improving, despite the Fed’s attack on housing demand via 11 rate hikes.

[Why are home prices not dropping?]

Housing Supply Is at an All-Time Low

Redfin reported that the total number of homes for sale hit a record low in August.

Active listings were down 1.1% month-over-month on a seasonally adjusted basis, and a whopping 20.8% year-over-year.

That’s the biggest annual decrease since June 2021. However, new listings have ticked higher the past two months on a seasonally adjusted basis.

In August, new listings increased 0.8% from a month earlier after increasing the month before that.

But due to nearly a year’s worth of monthly declines prior to that, new listings were still off a big 14.4% year-over-year.

This meant months of supply stood at just two months, well below the 4-5 months usually considered healthy.

Redfin Economics Research Lead Chen Zhao noted that “new listings have likely bottomed out,” arguing that those who are locked in by low rates have already decided not to sell.

That leaves those who must sell their property, due to stuff like divorce or a change in work-from-home policy.

Interestingly, even some WFH homeowners are moving back closer to work, but keeping their homes because they can rent them out.

Because homeowners got in so cheap, it’s not out of the question to keep the old house and go rent or buy another property.

All of this has created a huge dearth of existing home supply, but there is one winner out there.

Home Builders Are Gaining a Ton of Market Share

While existing homes, also known as previously-owned or used homes, are hard to come by, newly-built homes are somewhat plentiful.

In fact, newly built single-family homes for sale were up 4.5% year-over-year in June, per Redfin, while existing homes for sale were down 18%.

And roughly one-third of homes for sale were new builds, up markedly from prior years and well above the norm that might be closer to 10%.

Astonishingly, new homes accounted for more than half (52%) of single-family homes for sale in El Paso, Texas.

Similar market share could be seen in Omaha (46%), Raleigh (42.1%), Oklahoma City (39%), and Boise (38%).

Meanwhile, the National Association of Realtors (NAR) predicts that new home sales will increase 12.3% this year, and 13.9% in 2024.

As for why home builders are seeing a big increase in market share, it’s mostly due to a lack of competition from existing home sellers.

In short, they’re the only game in town, and they don’t need to worry about finding a replacement property if they sell (like existing homeowners)

Additionally, they’re able to tack on huge incentives such as rate buydowns, including temporary and permanent ones, along with lender credits.

This allows them to sell at higher prices but make the monthly payment more palatable for the buyer.

Perhaps more importantly, it allows buyers to still qualify for a mortgage at today’s sky-high prices.

When Will More Homes Hit the Market?

For now, this new reality is expected to be the status quo. After all, those with so-called golden handcuffs have 30-year fixed-rate mortgages.

That means they can continue to take advantage of their dirt-cheap mortgage for the next few decades.

This includes second home owners and investors, who got in cheap when prices were much lower and mortgage rates were also on sale.

Meanwhile, the home builders don’t seem to be going nuts with supply, and even if they ramped up production, it wouldn’t satisfy the market.

Remember, existing home sales typically account for around 85-90% of sales, so builders won’t come close to satisfying demand.

The only real way we get a big influx of supply is via distress, sadly. That could be the result of a bad recession with mass unemployment.

And it could be triggered by the 11 Fed rate hikes already in the books, coupled with a lack of new stimulus and the resumption of things like student loan payments.

Compounding that is sticky inflation, which has made everything more expensive and is quickly depleting the savings accounts of Americans.

But even then, you could argue that a mass loan modification program would be unveiled to at least keep owner-occupied households in their properties.

Considering how cheap their housing payments are, assuming they’ve got a low fixed-rate mortgage, it’d be hard to find them a cheaper alternative, even if renting.

In the early 2000s this wasn’t the case because the typical homeowner held a toxic mortgage, such as an option ARM or an interest-only loan. And many weren’t even properly qualified to begin with.

Read more: Today’s Housing Market Risk Factors: Is Real Estate in Trouble?

One of the most stressful parts of buying a new home is the move-in. If you’re not careful, it can make getting a mortgage look like the easy part. There are two ways to go about moving into a new place. You can either hire a moving company, or do it yourself.

Both options have pros and cons, and depending on your situation, there is a better choice for you. Use these few factors when making the choice between having someone move your stuff for you and doing it on your own.

1. Distance

One of the biggest factors when deciding if you want to take on moving yourself is how far you are going. If you are just moving to the other side of town, it is probably worth it to try moving yourself. You can rent a U Haul and make multiple trips. Multiple trips means that you don’t have to cram everything in at once like a professional packer.

If you’re moving across the country, however, it is probably in your best interest to hire movers. If things are not packed correctly for a long drive, they can get seriously damaged. And if things break with a moving company, their insurance should cover it.

2. Price

Although the easiest answer might be to hire movers, it for sure is not the most cost effective. If you want someone to move you in from start to finish, it is going to cost you—a lot. Moving companies are not cheap, but renting a truck and buying boxes are, and may fall better in your price range.

However, there are options out there where you can have movers do some of the work. Many companies will do part of the job for a lot less money. Perhaps you pack everything up, and they just deliver everything to your house. There are many combinations for you to pick from to benefit you best.

3. Help

Another key factor to consider when deciding how to move is if you can get the help. Can you sucker a few friends and/or family members to help you move for a few days? Moving an entire house by yourself is an impossible task, so if you have no one who can help you out, hiring movers is probably the way to go for you.

4. Amount of Stuff

To see if it is worth paying for a moving company, ask yourself “how much stuff do I really have?” Are you moving out of a studio apartment or a four bedroom house? If you do not have too much stuff to move, there is no point wasting your money on a job that would only take you half a day.

However, if you are moving out of a large house with a lot of large objects and furniture, it is beneficial to spend the money for a mover. With large objects, you are also at greater risk to hurt yourself so let people who are professionals at lifting things take the weight.

5. Time

Moving is no quick task. It takes a lot of time, especially if you are moving a lot of stuff or far away. If you have a fulltime job, or a crazy life schedule, it may be hard to find the time to move yourself. This would be a good time to call a moving company. However, if you have a free weekend, or can afford to take a few days off of work, you could tackle this process by yourself.

However, don’t make the mistake of trying to cram moving into a small window of time. That’s how things become too stressful and mistakes get made.

Final Thoughts

When it comes from moving to your old house to a new one, use these tips to properly decide whether it is beneficial for you to do it all yourself or spend the money to hire a moving company. For more tips on the moving process, visit Top Moving Tips On How To Move Smoothly.

Carter Wessman

Carter Wessman is originally from the charming town of Norfolk, Massachusetts. When he isn’t busy writing about mortgage related topics, you can find him playing table tennis, or jamming on his bass guitar.

An abrupt change of plans A major renovation to the place turned it into a reproduction of the historic home of George and Martha Washington, where her parents also lived with her and her husband. “We couldn’t find an old house to renovate,” she said. “We ended up building a replica of Mt. Vernon and … [Read more…]

Whoa, have you seen what just happened to interest rates!?

Suddenly, after at least fourteen years of our financial world being mostly the same, somebody flipped over the table and now things are quite different.

Interest rates, which have been gliding along at close to zero since before the Dawn of Mustachianism in 2011, have suddenly shot back up to 20-year highs.

–

Which brings up a few questions about whether we need to worry, or do anything about this new development.

Is the stock market (index funds, of course) still the right place for my money?

What if I want to buy a house?

What about my current house – should I hang onto it forever because of the solid-gold 3% mortgage I have locked in for the next 30 years?

Will interest rates keep going up?

And will they ever go back down?

These questions are on everybody’s mind these days, and I’ve been ruminating on them myself. But while I’ve seen a lot of play-by-play stories about each little interest rate increase in the financial newspapers, none of them seem to get into the important part, which is,

“Yeah, interest rates are way up, butwhat should I do about it?”

So let’s talk about strategy.

Why Is This Happening, and What Got Us Here?

*

Interest rates are like a giant gas pedal that revs the engine of our economy, with the polished black dress shoe of Federal Reserve Chairman Jerome Powell pressed upon it.

For most of the past two decades, Jerome’s team and their predecessors have kept the pedal to the metal, firing a highly combustible stream of easy money into the system in the form of near-zero rates. This made mortgages more affordable, so everyone stretched to buy houses, which drove demand for new construction.

It also had a similar effect on business investment: borrowed money and venture capital was cheap, so lots of entrepreneurs borrowed lots of money and started new companies. These companies then rented offices and built factories and hired employees – who circled back to buy more houses, cars, fridges, iPhones, and all the other luxurious amenities of modern life.

This was a great party and it led to lots of good things, because we had two decades of prosperity, growth, raising our children, inventing new things and all the other good things that happen in a successful rich country economy.

Until it went too far and we ended up with too much money chasing too few goods – especially houses. That led to a trend of unacceptably fast Inflation, which we already covered in a recent article.

–

So eventually, Jay-P noticed this and eased his foot back off of the Easy Money Gas Pedal. And of course when interest rates get jacked up, almost everything else in the economy slows down.

And that’s what is happening right now: mortgages are suddenly way more expensive, so people are putting off their plans to buy houses. Companies find that borrowing money is costly, so they are scaling back their plans to build new factories, and cutting back on their hiring. Facebook laid off 10,000 people and Amazon shed 27,000.

We even had a miniature banking crisis where some significant mid-sized banks folded and gave the financial world fears that a much bigger set of dominoes would fall.

All of these things sound kinda bad, and if you make the mistake of checking the news, you’ll see there is a big dumb battle raging as usual on every media outlet. Leftists, Right-wingers, and anarchists all have a different take on it:

It’s the President’s fault for printing all that money and running up the debt! We should have Fiscal Discipline!

No, it’s the opposite! The Fed is ruining the economy with all these rate rises, we need to drop them back down because our poor middle class is suffering!

What are you two sheeple talking about? The whole system is a bunch of corrupt cronies and we shouldn’t even have a central bank. All hail the true world currency of Bitcoin!!!

The one thing all sides seem to agree on is that we are “experiencing hard economic times” and that “the country is headed in the wrong way”.

Which, ironically, is completely wrong as well – our unemployment rate has dropped to 50-year lows and the economy is at the absolute best it has ever been, a surprise to even the most grounded economists.

The reality? We’re just putting the lid back onto the ice cream carton until the economy can digest all the sugar it just wolfed down. This is normal, it happens every decade or two and it’s no big deal.

Okay, but should I take my money out of the stock market because it’s going to crash?

This answer never changes, so you’ll see it every time we talk about stock investing: Holy Shit NO!!!

The stock market always goes up in the long run, although with plenty of unpredictable bumps along the way. Since you can’t predict those bumps until after they happen, there is no point in trying to dance in and out of it.

But since we do have the benefit of hindsight, there are a few things that have changed slightly: From its peak at the beginning of 2022 until right now (August 2023 as I write this), the overall US market is down about 10%. Or to view it another way, it is roughly flat since June 2021, so we’ve seen two years with no gains aside from total dividends of about 3%.

Since the future is always the same, unknowable thing, this means I am about 10% more excited about buying my monthly slice of index funds today than it was at the peak.

Should I start putting money into savings accounts instead because they are paying 4.5%?

This is a slightly trickier question, because in theory we should invest in a logical, unbiased way into the thing with the highest expected return over time.

When interest rates were under 1%, this was an easy decision: stocks will always return far more than 1% over time – consider the fact that the annual dividend payments alone are 1.5%!

But there has to be some interest rate at which you’d be willing to stop buying stocks and prefer to just stash it into the stable, rewarding environment of a money market fund or long-term bonds or something else similar. Right now, if a reputable bank offered me, say, 12% I would probably just start loading up.

But remember that the stock market is also currently running a 10% off sale. When the market eventually reawakens and starts setting new highs (which it will someday), any shares I buy right now will be worth 10% more. And then will continue going up from there. Which quickly becomes an even bigger number than 12%.

In other words, the cheaper the stocks get, the more excited we should be about buying them rather than chasing high interest rates.

As you can see, there is no easy answer here, but I have taken a middle ground:

I’m holding onto all the stocks I already own, of course

BUT since I currently have an outstanding margin loan balance for a house I helped to buy with several friends (yes this is #3 in the last few years!), I am paying over 6% on that balance. So I am directing all new income towards paying down that balance for now, just for peace of mind and because 6% is a reasonable guaranteed return.

Technically, I know I would probably make a bit more if I let the balance just stay outstanding, kept putting more money into index funds, and paid the interest forever, but this feels like a nice compromise to me

What if I want to Buy a House?

–

For most of us, the biggest thing that interest rates affect is our decisions around buying and selling houses. Financing a home with a mortgage is suddenly way more expensive, any potential rental house investments are suddenly far less profitable, and keeping our old house with a locked-in 3% mortgage is suddenly far more tempting.

Consider these shocking changes just over the past two years as typical rates have gone from about 3% to 7.5%.

Assuming a buyer comes up with the average 10% down payment:

The monthly mortgage payment on a $400k house has gone from about $1500 at the beginning of 2022 last year to roughly $2500 today. Even scarier, the interest portion of that monthly bill has more than doubled, from $900 to $2250!

For a home buyer with a monthly mortgage budget of $2000, their old maximum house price was about $500,000. With today’s interest rates however, that figure has dropped to about $325,000

Similarly, as a landlord in 2022 you might have been willing to pay $500k for a duplex which brought in $4000 per month of gross rent. Today, you’d need to get that same property for $325,000 to have a similar net cash flow (or try to rent each unit for a $500 more per month) because the interest cost is so much higher.

And finally, if you’re already living in a $400k house with a 3% mortgage locked in, you are effectively being subsidized to the tune of $1000 per month by that good fortune. In other words, you now have a $12,000 per year disincentive to ever sell that house if you’ll need to borrow money to buy a new one. And you have a potential goldmine rental property, because your carrying costs remain low while rents keep going up.

This all sounds kind of bleak, but unfortunately it’s the way things are supposed to work – the tough medicine of higher interest rates is supposed to make the following things happen:

House buyers will end up placing lower bids which fit within their budgets.

Landlords will have to be more discerning about which properties to buy up as rentals, lowering their own bids as well.

Meanwhile, the current still-sky-high prices of housing should continue to entice more builders to create new homes and redevelop and upgrade old buildings and underused land, because high prices mean good profits. Then they’ll have to compete for a thinner supply of home buyers.

The net effect of all this is that prices should stop going up, and ideally fall back down in many areas.

When Will House Prices Go Back Down?

This is a tricky one because the real “value” of a house depends entirely on supply and demand. The right price is whatever you can sell it for. However, there are a few fundamentals which influence this price over the long run because they determine the supply of housing.

The actual cost of building a house (materials plus labor), which tends to just stay pretty flat – it might not even keep up with inflation.

The value of the underlying land, which should also follow inflation on average, although with hot and cold spots depending on which cities are popular at the time.

The amount of bullshit which residents and their city councils impose upon house builders, preventing them from producing the new housing that people want to buy.

NIMBYS in my own area, damaging the housing market.

The first item (construction cost) is pretty interesting because it is subject to the magic of technological progress. Just as TVs and computers get cheaper over time, house components get cheaper too as things like computerized manufacturing and global trade make us more efficient. I remember paying $600 for a fancy-at-the-time undermount sink and $400 for a faucet for my first kitchen remodel in the year 2001. Today, you can get a nicer sink on Amazon for about $250 and the faucet is a flat hundred. Similarly, nailguns and cordless tools and easy-to-install PEX plumbing make the process of building faster and easier than ever.

On the other hand, the last item (bullshit restrictions) has been very inflationary in recent times. I’ve noticed that every year another layer of red tape and complicated codes and onerous zoning and approval processes gets layered into the local book of rules, and as a result I just gave up on building new houses because it wasn’t worth the hassle. Other builders with more patience will continue to plow through the murk, but they will have less competition, fewer permits will be granted, and thus the shortage of housing will continue to grow, which raises prices on average.

Thankfully, every city is different and some have chosen to make it easier to build new houses rather than more difficult. Even better, places like Tempe Arizona are allowing good housing to be built around people rather than cars, which is even more affordable to construct.

But overall, since overall US house prices adjusted for inflation are just about at an all-time high, I think there’s a chance that they might ease back down another 25% (to 2020 levels). But who knows: my guess could prove totally wrong, or the “fall” could just come in the form of flat prices for a decade that don’t keep up with inflation, meaning that they just feel 25% cheaper relative to our higher future salaries.

–

When Will Interest Rates Go Back Down?

The funny part about our current “high” interest rates is that they are not actually high at all. They’re right around average.So they might not go down at all for a long time.

Remember that graph at the beginning of this article? I deliberately cropped it to show only the years since 2009 – the long recent period of low interest rates. But if you zoom out to cover the last seventy years instead, you can see that we’re still in a very normal range.

–

But a better answer is this one: Interest rates will go down whenever Jerome Powell or one of his successors determines that our economy is slowing down too much and needs another hit from the gas pedal. In other words, whenever we start to slip into a genuine recession.

In order to do that however, we need to see low inflation, growing unemployment, and other signs of an economy that’s not too hot. And right now, those things keep not showing up in the weekly economic data.

You can get one reasonable prediction of the future of interest rates by looking at something called the US Treasury Yield Curve. It typically looks like this:

–

What the graph is telling you is that as a lender you get a bigger reward in exchange for locking up your money for a longer time period. And way back in 2018, the people who make these loans expected that interest rates would average about 3.0 percent over the next 30 years.

Today, we have a very strange opposite yield curve:

–

If you want to lend money for a year or less, you’ll be rewarded with a juicy 5.4 percent interest rate. But for two years, the rate drops to 4.92%. And then ten-year bond pays only 4.05 percent.

This situation is weird, and it’s called an inverted yield curve. And what it means is that the buyers of bonds currently believe that interest rates will almost certainly drop in the future – starting a little over a year from now.

And if you recall our earlier discussion about why interest rates drop, this means that investors are forecasting an economic slowdown in the fairly near future. And their intuition in this department has been pretty good: an inverted yield curve like this has only happened 11 times in the past 75 years, and in ten of those cases it accurately predicted a recession.

So the short answer is: nobody really knows, but we’ll probably see interest rates start to drop within 18-24 months, and the event may be accompanied by some sort of recession as well.

The Ultimate Interest Rate Strategy Hack

–

I like to read and write about all this stuff because I’m still a finance nerd at heart. But when it comes down to it, interest rates don’t really affect long-retired people like many of us MMM readers, because we are mostly done with borrowing. I like the simplicity of owning just one house and one car, mortgage-free.

With the current overheated housing market here in Colorado, I’m not tempted to even look at other properties, but someday that may change. And the great thing about having actual savings rather than just a high income that lets you qualify for a loan, is that you can be ready to pounce on a good deal on short notice.

Maybe the entire housing market will go on sale as we saw in the early 2010s, or perhaps just one perfect property in the mountains will come up at the right time. The point is that when you have enough cash to buy the thing you want, the interest rates that other people are charging don’t matter. It’s a nice position of strength instead of stress. And you can still decide to take out a mortgage if you do find the rates are worthwhile for your own goals.

So to tie a bow on this whole lesson: keep your lifestyle lean and happy and don’t lose too much sweat over today’s interest rates or house prices. They will probably both come down over time, but those things aren’t in your control. Much more important are your own choices about earning, saving, healthy living and where you choose to live.

With these big sails of your life properly in place and pulling you ahead, the smaller issues of interest rates and whatever else they write about in the financial news will gradually shrink down to become just ripples on the surface of the lake.

In the comments:what have you been thinking about interest rates recently? Have they changed your decisions, increased, or perhaps even decreased your stress levels around money and housing?

—

* Photo credit: Mr. Money Mustache, and Rustoleum Ultra Cover semi gloss black spraypaint. I originally polled some local friends to see if anyone owned dress shoes and a suit so I could get this picture, with no luck. So I painted up my old semi-dressy shoes and found some clean-ish black socks and pants and vacuumed out my car a bit before taking this picture. I’m kinda proud of the results and it saved me from hiring Jerome Powell himself for the shoot.

With record-low inventory nationwide, real estate agents seem to be hearing the same thing day in and day out: “I’d list my home, but where would I move?”For most agents, that’s the end of the conversation, ending the possibility of taking a new listing as well as facilitating the buyer side. Nationwide, inventory is at all-time lows. According to Altos Research, this week there are only 465,000 active listings. We are still at least a million listings shy of being a balanced market, so this excuse is not going to subside anytime soon.

Stop answering clients’ concerns by saying, “Yeah, there’s really nothing on the market, I mean everything in the MLS is already pending.I’ll put you into my search widget and we’ll watch for something to pop up together.”

While that’s onemethod of finding a home for your would-be sellers to buy, you can’t end the conversation there and expect to do any business this year. The key is to set up the ‘drip system,’ then move the conversation forward by being a problem solver. How does someone list and buy at the same time successfully in a market like this?

Here are 10 solutions for sellers who what to buy that go beyond waiting and watching for magic inventory to appear.

Build a home instead of chasing after the scarce resale inventory

30% of available homes are new construction, so there are several advantages to this option. First, many builders are buying down interest rates using their in-house financing. Builders are closing loans in the 4.5 to 5.5% range currently! Next, the house is new. No rehab for them and no inspection woes for you. Your client can get their home on the market a few months before construction is complete and not have to move twice. Finally, when your client builds, they don’t have to compete in a bidding war.

Buy first, close and then list the previous home

Don’t assume your clients won’t or can’t utilize this option. They may have a downpayment saved that isn’t their home equity. They might use a bridge loan to borrow their equity, close on the next home and then sell the old one. You don’t know if you don’t ask. The advantage here is that your client can make a non-contingent offer, secure their next home and deal with their old house later. Make sure you know lenders who offer bridge loans and understand how to explain this option.

Sell first, rent for a while and take the time to look for the right home

The advantage here is the seller has cashed out their equity and is ready to pounce on the right home, but without the pressure of scheduling closing and possession dates. Who are your go-to leasing agents? Maybe youare a leasing agent. Consider both traditional rentals, short-term vacation rentals, as well as apartment complexes. Many have some great amenities which could work for a short to longer-term lease while you help your client find the right home to buy.

Offer acceptance contingent on seller finding suitable housing

The buyer will probably want a specific time frame, but you can usually get 90 to 120 days to secure the next home. Many buyers in today’s market are simply anxious to find the right home, so they will be flexible with the seller’s situation. It’s still a seller’s market. The advantage to your client is they won’t have to move twice and you’ve built in enough time to look for the next place.

Convert the previous home into a rental

You can handle the lease yourself or refer it to your favorite leasing agent. The home stays an asset for your client and they can keep their low-interest rate mortgage. Don’t assume that this isn’t an option. You have to ask! Remember that Americans currently have record-high credit scores. They may be more comfortable taking this option than you think. In some markets, keeping the home and turning it into a short-term rental can be very profitable. It might be the best option for your client. You can always run the numbers and see if it makes sense, at least in the short term.

Leasing back the home

In this scenario, the buyer is happy because they secured the house, and your seller is happy because they have both time and money coming in to facilitate their move to the next place. Once the home has been purchased by the new owners, your clients would essentially pay rent to stay while they house hunt.

Buying an RV, a houseboat or a sailboat

There are endless examples of sellers who cashed out their homes, bought a recreational home and traveled for a while. You might be surprised that it’s not just baby boomers or retirees who are doing this! Another version of this option involves sellers cashing out and renting a series of short-term rentals in different areas of the country or the world, trying out new possibilities before they decide where to land.

Find your would-be seller an off-market home to purchase where that seller has flexibility

In this scenario, you are in complete control of both sides of the transaction, and you may pick up yet another client when the off-market seller also needs to buy. Refer to our podcast series and HousingWire articles about how to find inventory that’s not in the MLS.

Moving into an assisted living care facility

Many of the homes that are coming onto the market right now are in 55 and over communities. There is also inventory from families downsizing, new empty-nesters moving and the like. Are you prospecting in those neighborhoods?

Moving in with relatives

Whether that’s moving in with parents, kids or cousins somewhere else, it can be a short-term solution for sellers who don’t have another property in mind yet.

Bottom line? You can’t just wait around for listings to appear for your sellers! Stop relying on your ‘drip system.’ Be proactive with different solutions that could work for them. You’ll have more transactions and they’ll value your expertise, netting you both current business as well as future repeat and referrals.

Tim and Julie Harris host the nation’s #1 podcast for real estate professionals. https://timandjulieharris.com/category/podcast has new podcasts every day. Tim and Julie have been real estate coaches for more than two decades, coaching the top agents in the country through different types of markets. https://PremierCoaching.com to get started for FREE today.