Here are the steps landlords and property managers can take to evict a tenant whose lease has ended.

When a tenant’s lease agreement ends, you expect that they’ll either renew the lease and keep living in the unit or inform you that they’re moving out. But what if a tenant doesn’t take either action? That’s when they become a holdover tenant.

These tenants don’t sign a new lease but continue to live in the rental. And there are several options for handling the situation, including eviction. Here’s a look at what to do about a holdover tenant.

What is a holdover tenant?

A holdover tenant is a renter who doesn’t vacate the home at the end of a lease term and keeps living in the property without permission from a property owner or manager. They often even continue paying rent.

Tenants can actually go on living in the home without a lease, until the property manager goes through a formal process to remove them. So, the holdover period officially starts when a lease concludes and ends when the tenant is given a written notice to leave.

What to do about a holdover tenant?

Landlord-tenant laws vary drastically by state and city, so you must read up on your local area’s regulations regarding holdover tenants. In some cases, if a property manager accepts rent, it resets the lease term and you can’t evict them. In other areas, accepting rent enacts a month-to-month lease.

When drafting your lease agreement, include details about what happens once a lease agreement expires to prevent having holdover tenants. Specify a timeframe when you’ll take action if someone doesn’t move out of the home after the lease term and what that action will be.

Since rental laws vary so much, how to best handle a holdover tenant depends on where you live. The first step is to discuss the situation with the tenant to get a sense of their intentions and what might work best for everyone. Often, finding a way to keep a good tenant in your unit is best. Advertising the home and finding new tenants is time-consuming and costly.

Eviction is often one option for dealing with a holdover tenant. You can also convert them to a month-to-month lease, especially if they’re still paying rent. Include terms for how they notify you when they want to move out and how you’ll inform them when you want to end the lease. And, of course, make sure everyone signs the new lease.

How to evict a holdover tenant

If you decide eviction is the best way to deal with a holdover tenant, there are several steps to take. Keep in mind that evictions can take time and usually come with hefty expenses. Here’s how to evict a holdover tenant:

Know the law

Eviction laws differ from state to state, so start by researching local laws. The laws are complex, so hiring an attorney is the best way to ensure you do the eviction by the book. Also, double-check that there are no local eviction moratoria in your area.

Establish grounds for eviction

Before you begin the official eviction, make sure you have a good reason. Staying past a lease term without permission is often grounds for eviction — but you must know for sure. And, if you’ve been accepting rent payments, that could complicate your ability to evict. That’s why consulting with an attorney is crucial.

If the tenant isn’t paying rent, has caused damage to the property or has violated the lease agreement in other ways, that’s adequate grounds for eviction. You’ll most likely need to prove your case if the eviction goes to court. So, hang onto any emails or letters about the end of the lease, late rent or any other issue that has come up.

Ask the tenant to leave

Simply asking the holdover tenant to leave the property can save you both a lot of time and money. If you have a good relationship with your renter, you can explain that the lease term has ended and that they’ll need to sign a new lease to continue living in the unit. Otherwise, you’ll have to evict them.

Mention that the eviction will take time, likely cost them money and could harm their credit, which might affect their ability to rent a home in the future. Working out a solution is better for everyone involved.

But, never take matters into your own hands. Avoid removing a tenant’s belongings from the home or changing the locks. If you can’t persuade the tenant to leave, that’s when you should send a formal eviction notice.

Provide the holdover tenant with a formal notice

To officially start the eviction process, you must send a formal eviction notice to the holdover tenant. The notice tells the tenant that they must vacate the property by a specific date or you’ll proceed with the eviction through the court system.

The eviction notice should include the following elements:

Rental property address

Date when the tenant must move out

A detailed description of the situation, including the reason for the eviction

An explanation of why the holdover status violates the lease agreement

Deliver the eviction notice in person or send via certified mail or a read receipt email, so you have proof they received it. Deliver the notice within a certain number of days before filing with the courts, usually 30 or 60 days but it depends on local eviction laws.

File the eviction with the court

If the tenant doesn’t respond to the eviction notice or move out of the unit, file it with the court. The specific process for filing evictions with the courts is different from place to place, so contact your courthouse for the details.

Usually, the process goes something like this:

File the paperwork in person at your local courthouse

Pay a fee

Show proof that you provided a formal eviction notice to the tenant

Receive a scheduled hearing date

The court will inform the tenant of the eviction filing and hearing.

On the hearing date, be sure to attend and make your case for removing the tenant. You have the option to hire an attorney or represent yourself. And, you’ll want to bring evidence, such as the original lease agreement, records of communication with the tenant, the formal eviction notice and proof that the tenant received the notice.

Go through with evicting the holdover tenant

If the court sides with you, the holdover tenant will be given a move-out date. The exact timeframe they’ll have to move out depends on local laws.

Hopefully, they’ll go peacefully. If not, you have the right to contact local law enforcement, citing the court’s judgment in your favor. A police officer will tell the tenant to move out in a day or two or escort them off the property.

If the tenant owes back rent, you can file a small claims lawsuit to collect it. You’ll receive a court order to garnish the renter’s wages and repay the owed rent.

Evicting a holdover tenant from your rental

A holdover tenant isn’t something most property managers or owners expect, but it happens. The best way to handle it is to prepare and include provisions for holdover tenants in the lease agreement. In the worst-case scenario, you can use these tips to evict the tenant. When you list your rental at Rent., you can get in front of millions of potential renters, screen tenants and collect rent online.

Erica Sweeney covers real estate, business, health, wellness and many other topics. Her work has appeared in The New York Times, The Guardian, Good Housekeeping, HuffPost, Parade, Money, Business Insider, Realtor.com and lots more.

UK ‘mortgage meltdown’ looms amid ‘terrifying’ growth in arrears

Jump in borrowers unable to make payments with landlords particularly hit and ‘worse to come’

Analysis: will the Bank listen to business and halt rate rises?

Mortgage balances with arrears jumped by 13% in the second quarter of the year to the highest level since 2016, according to Bank of England figures that underscore the stress in the UK mortgage market.

Rising interest rates and unemployment over recent months have put pressure on household disposable incomes, forcing some families to cut or suspend their monthly mortgage payments.

Buy-to-let mortgage payers have also come under pressure in parts of the country where tenants are struggling with the cost of living crisis.

The Bank of England said the total value of mortgage balances which had some arrears rose to £16.9bn, up by 29% on the previous year and the highest since the third quarter of 2016.

Mortgage arrears are based on figures showing the number of borrowers failing to make payments equivalent to at least 1.5% of the outstanding mortgage balance or where the property is in possession.

Mortgage lending was also hit in the second quarter with gross advances falling by £6.3bn to £52.4bn. Year on year, mortgage lending slumped by almost a third, to the lowest level since the worst of the Covid-19 collapse in lending in the second quarter of 2020.

Lewis Shaw, founder of Mansfield-based Shaw Financial Services, told the news agency Newspage a “mortgage meltdown” is approaching, unless the Bank of England changes its approach.

Shaw said: “The speed at which mortgage arrears are increasing is terrifying and should give cause to pause at the next Bank of England interest rate meeting. This is dire data, and we know that it’s about to get an awful lot worse with 1.6m mortgage holders due to renew over the next 12 months at significantly higher rates than anyone has been used to for well over a decade.”

Simon Gammon, managing partner at the finance arm of estate agents Knight Frank, said the proportion of mortgage payers falling behind with payments remained low at just 1%, despite the “sizeable jump in arrears”.

He said: “That’s because the vast majority of outstanding mortgages were issued under the post-global financial crisis regime, which was much more stringent when it comes to affordability.”

However, while homeowners were more likely to make cuts to other spending before falling behind with mortgage payments, buy-to-let landlords may take a different view, he said.

“We are more likely to see arrears in the buy-to-let sector, where landlords face a unique set of challenges. If a landlord finds their mortgage is no longer affordable, or the rent no longer covers their outgoings, they only have two choices – sell or default. If they opt to sell, they may have to wait up to a year for the tenancy to end, unless they are willing to sell with a tenancy in place, which is more difficult.

“Landlords are also more likely to opt to default than those struggling with a mortgage secured against their main residence, so this is an area to watch,” he added.

Incoming Bank of England deputy governor Sarah Breeden said she agreed with her future colleagues on the monetary policy committee (MPC), which sets UK interest rates, that inflation may fall at a slower pace next year than expected, forcing the central bank to keep the cost of borrowing higher for longer than expected.

Breeden, who will replace Jon Cunliffe as the Bank’s deputy governor for financial stability after the MPC’s meeting next week, said there was also a risk that growth and unemployment will worsen.

skip past newsletter promotion

after newsletter promotion

“I will, after November, be very careful in balancing those two factors: the risk of inflation becoming embedded through more persistent, second-round effects, as well as the impact of tightening coming through,” she told parliament’s Treasury Committee in a hearing convened to approve to her appointment.

“The challenge right now is that wages are high and rising and there is a real risk that second-round effects means that this inflation becomes embedded,” she said, adding that in keeping a lid on inflation, “it is not our intention to cause a recession”.

The MPC is expected to raise interest rates by a quarter point to 5.5% on 21 September, raising the average mortgage payments by £3,000 a year for a household that refinances a 2-year fixed product.

Breeden said she expected inflation to be “around the [Bank of England’s] 2% target in two years’ time”.

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

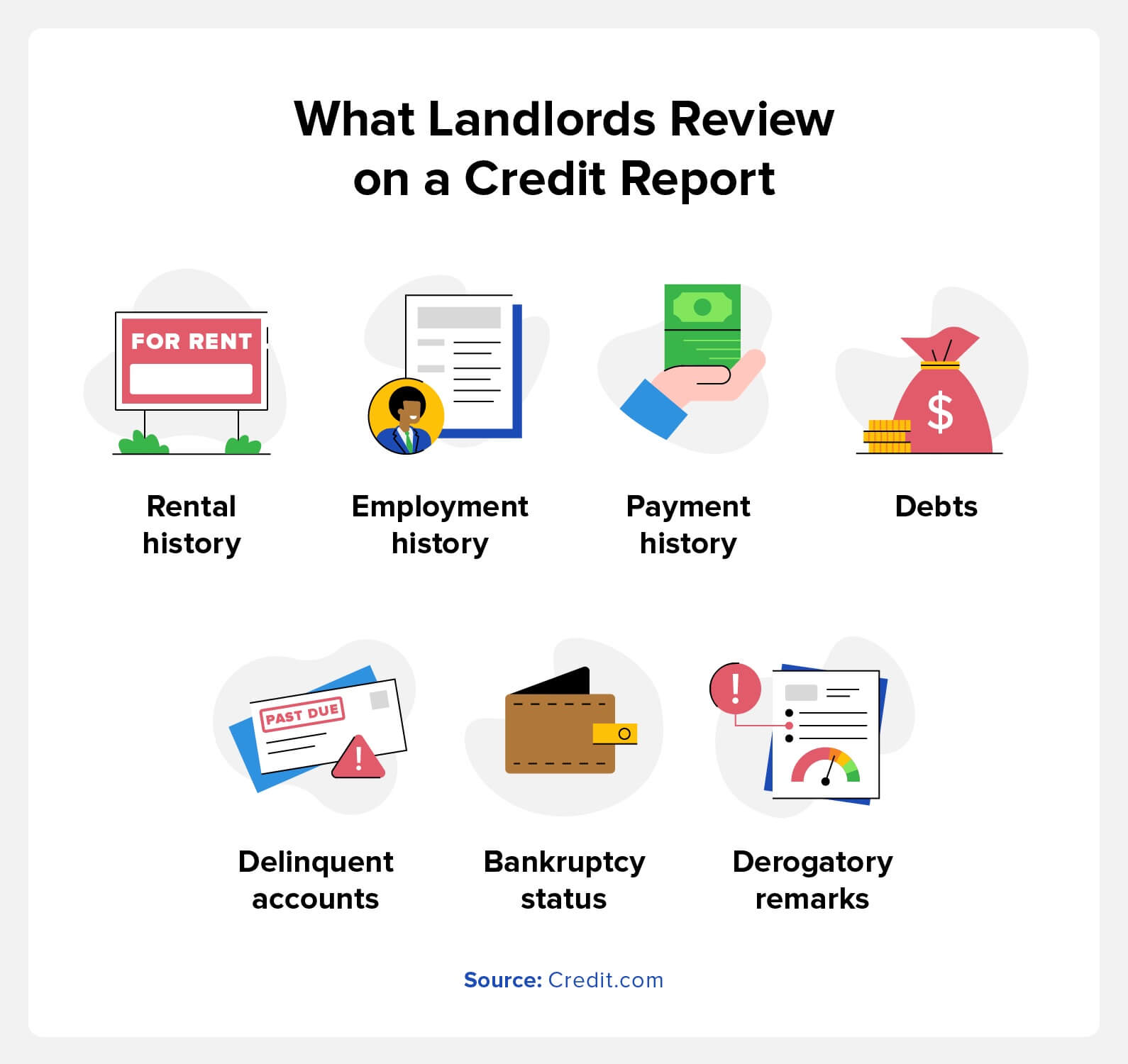

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.

Employment history: Current or past employers may show up on a credit report. Typically, they only appear if you listed them on a credit card application or loan.

Payment history: Credit reports show your history of payments to lenders. Late or missing payments will lower your score and work against your rental application.

Debts: Current and past debts show up on your credit report. By providing payslips, landlords can calculate your debt-to-income ratio. If you make enough to repay your debts responsibly, that improves your application.

Delinquent or collections accounts: An account is delinquent if you miss a payment due date. If you miss enough payments for lenders to transfer your account to a collection agency or sell it to a debt buyer, it becomes a collections account. Both of these hurt your credit score.

Bankruptcy status: Bankruptcy filings will affect your credit score. Landlords may take recent bankruptcies as a sign that you’re a high-risk tenant.

Derogatory remarks: These remarks refer to negative items on your credit report. They include auto repossessions or foreclosures. They hurt your score and hamper a rental application.

Landlords gauge the risk they pose by looking at how applicants spend their money. Someone with a high income but a history of late payments may not make the cut. On the other hand, someone who filed for bankruptcy years ago may be more responsible now.

How to Get an Apartment with Bad Credit

While a low score sets you back, you can learn how to get approved for an apartment with low credit. By following these methods, you can get a leg up in rental applications:

Make an Upfront Payment

Putting down more money upfront can give you an edge on rental applications. Landlords will usually request a security deposit or the first and last month’s rent upfront. To sway a landlord’s opinion, offer the first three months’ rent or put down a higher security deposit.

At the end of the day, renting is an investment. If you can show your landlord that you’ll give them a reliable ROI, it’s all the more likely they’ll accept you. As a bonus, paying more in advance saves you a financial burden for the next few months.

Find a Guarantor or Cosigner for Your Apartment

If a landlord can’t trust you to make payments, you can get someone to sign your lease with you. Someone with a great credit score who signs on with you can assuage a property manager’s worries. However, remember that the person who helps you takes on financial risk. You have two options for this approach:

Cosignerssign a rental agreement with you and share the financial responsibility for it. They must do so on your behalf if you can’t or won’t pay rent.

Guarantors share cosigners’ responsibilities, but they have fewer rights. More specifically, they vouch for you and can make payments on your behalf. However, they aren’t entitled to reside in your unit.

Offer References and Supporting Documents

While credit reports outline your financial history, you aren’t the sum of your spending decisions. You can offer other documents to show your responsibility in an apartment application. Additionally, these documents can prove you can pay rent each month. Some examples of supporting documents include:

Payslips: Offer pay stubs that show you make enough money to pay rent each month.

Letters of recommendation: Reference letters from a friend or employer can attest to your character and responsibility.

Proof of reliable rental history: Account statements and landlord testimonials can prove you always pay rent on time.

A snapshot of your savings account: If all else fails, you can show landlords you have the money to make rent. Be sure to censor sensitive information on your snapshot.

Utility payments: A history of on-time utility payments shows your trustworthiness.

Find Apartments to Rent with No Credit Check

While credit checks are common, not all landlords require one. While these properties aren’t the most competitive, that isn’t always a problem. Apartments with no credit check tend to cost less than ones with one.

If you’re looking for another option, some landlords advertise units with low credit requirements. Again, these properties set a low credit requirement for a reason. That said, if you inspect the unit and it looks good, this route can save you a headache. As you live in low-credit apartments, you can build your score for future applications.

Adjust Your Expectations

If you can’t get around a credit check, reassess the kinds of apartments you can apply for. This isn’t to say you should only apply to units in poor condition. Instead, consider what you’re willing to compromise on. You may have an easier time qualifying for an apartment:

Farther away from your work or downtown area

Without amenities like a gym or pool

That doesn’t include parking

With less square footage than you’d prefer

If you apply with a roommate

Bear in mind that compromising on these points means the apartment may cost less. While living in a less-than-ideal unit, you can save and rebuild your credit while renting. When it comes time to look for a new apartment, you’ll have better odds of getting the one you want.

Tips to Raise Your Credit Before Renting an Apartment

If you plan to send rental applications down the line, you should work to improve your credit. Bear in mind that increasing your credit score takes time. To see a major change, expect months or even a year of work. In that time, follow these tips to improve your credit:

Pay Your Bills on Time

A person’s payment history can make or break their credit score. Central to that payment history: whether you paid your bills on time. Making timely and consistent payments plays a big role in improving your credit score. On top of that, timely payments prove your reliability to a landlord, boosting your chance of getting approved.

Pay Down Any Debt

Paying down debts is one of the best ways to improve your credit score. For this reason, someone who takes on and pays off debt won’t get punished for the debt they take on. Paying off debts shows your fiscal responsibility and proves your finances are on an upward trajectory.

Paying off any kind of debt can improve your score. The main ones to look out for include:

Credit card debt

Student loans

Medical debt

Auto loans

Become an Authorized User for Credit Piggybacking

If you don’t have the resources to boost your credit alone, you can try credit piggybacking. Credit piggybacking lets you benefit from a friend or family member who pays down their debts. By becoming an authorized user on their account, your credit report reflects their payoffs.

You can break the process into a few steps:

Find a friend or family member you trust to spend responsibly.

Become an authorized user on one of their credit cards or lines of credit.

As they pay down their debts, this will show up on your credit report.

By piggybacking on their credit payoffs, your score will improve.

Dispute Credit Report Errors

Sometimes, a low credit score isn’t your fault. Credit reporting errors can come from major credit reporting agencies or the companies giving them information. Credit reporting errors aren’t uncommon, so you should review your report for issues.

Credit reports may contain errors related to:

Accounts held by another person with a similar name to you

Accounts opened by fraudsters who committed identity theft

Closed accounts that still read as open

Accounts incorrectly labeled as delinquent or in collections

Payments that don’t get reflected in your report

Multiple listings of the same debt

Accounts with inaccurate balances or credit limits

To dispute credit report errors, contact the credit bureaus and the company that reported inaccurate information to them. You want to provide supporting documentation that proves the report contains errors. While you can send a dispute by phone, this doesn’t leave a paper trail. Instead, mail a dispute letter or use an online form.

FAQs on Renting an Apartment with Bad Credit

You may still have questions about getting approved for an apartment. To help you out, we’ve answered FAQs on renting apartments with bad credit.

Is 500 a High Enough Credit Score for an Apartment?

You can rent an apartment with a credit score of 500. While it might take you out of the running for expensive units, you should still have a good chance of renting:

Apartments with low credit requirements

Apartments with no credit requirements

Apartments you apply to with a cosigner or roommate.

Can I Reapply for an Apartment After I Get Denied for Bad Credit?

You can apply for the same apartment after getting denied on your first attempt. That said, some renters may throw out your application or ignore it. If you reapply, try to improve your credit and finances between applications.

Do Landlords Need Permission to Run a Credit Check?

Landlords need your permission to run a credit check. The Fair Credit Reporting Act calls rental applications a “permissible purpose.” This gives them the right to view your credit. However, that doesn’t mean landlords can check your score without your consent.

Improve Your Credit for an Apartment with Credit.com

Managing apartment applications is hard enough, even without a low credit score. However, you can get an apartment with bad credit by following the right steps. You’ll see more housing opportunities by learning how credit works, reviewing strategies for getting an apartment with low credit, and following tips to boost your score.

If you’d like a way to streamline raising your credit for rental applications, Credit.com can help. Our rent and utility reporting services ensure that your on-time payment gets reflected on your report. Even if your landlord doesn’t report payments, our tool helps build your credit with every rent payment reported.

After you’ve debated the pros and cons of living with someone and decided to have a roommate, the next challenge is figuring out how to find one. If you don’t already have a potential roommate in mind, you’ll need to start looking for one, which is its own challenge. Here are tips on how to find a roommate who will be compatible with your lifestyle.

Ask around

You can ask your family, friends and other acquaintances if they know anyone looking for a place to live. At the very least, you can let others know you’re seeking a roommate, so they can pass along the word to their friends and family. There’s a good chance that your contacts know someone who needs a place to live.

Furthermore, you’ll have the benefit of a reference you know already. You can ask your friends and family about the potential roommates and what they think of them. If a friend says their old roommate is looking to move, you can get great insights on if the potential roommate is clean, easy to live with, etc., from your friend, rath

er than relying on unknown references provided to you by that potential roommate.

Leverage social media

This can be a farther-reaching method of asking friends and family if they know anyone looking for a place to live. You can make a post with details, such as the area you’ll be living in, how much rent will be and how many other people will be living in the apartment. Make sure that your post is shareable, then ask everyone to share your post to get the word out!

You can also do some searching on socials to see if others from your city are posting about looking for an apartment. Reach out to those individuals and let them know what your apartment and the living situation would offer!

Some social media platforms like Facebook have groups specifically for housing in certain cities or areas. You can post in these groups that you’re looking for a roommate and it will be seen by plenty of others.

Place ads and listings

There’s no shame in using platforms like Craigslist and Facebook Marketplace to find a roommate. It’s easy and usually free to create a listing and it’s searchable by location, so those who are actively seeking to live in your area will quickly find your listing. Many local or state news networks will have a place for classified listings and rentals, so check to see if your city has one where you can post your apartment.

Try an app

Using apps is one of the best ways to find a roommate. There are plenty to choose from, but some of the most popular are Cirtu, Roomster, Roomi and SpareRoom. Such apps often allow for a more personalized search where you can specify what qualities you want in a roommate (quiet and keeps to themselves, extroverted and likes to socialize, clean, etc.). They also often require background checks or multi-step verification for users, so it can be safer for you to use.

You’ve found a roommate, now what?

As much as you want to find a roommate, your personal safety, credit history and even your reputation matter. So, make sure you research every potential roommate thoroughly.

1. Review references

Ask applicants for references from employers and previous landlords. Even notes from friends, clergy, professors and former roommates can help you get a sense of their character and habits.

Search each potential roommate’s social media pages to see if they’re respectful in their interactions with others and if they show good judgment in what they post publicly. If you see evidence of illegal activity, angry messages from friends or hostile, hateful, racist or sexist posts from your potential roommate, cross them off the list.

2. Check their criminal background

Search each applicant’s name and look for arrest records. Some states also have circuit court access websites available for your reference. People with common names are sometimes mixed up, so make sure you’re researching the right individual by cross-referencing details like photos and location.

If you find something questionable, you can reach out to the police department that made an arrest. They can offer clarification while still preserving privacy.

3. Do a financial check

Of all the questions to ask potential roommates, financial questions are among the most important. You’ll be paying bills with this person, so their bad credit and financial habits could affect you.

You can request a credit check from a potential roommate to make sure they have a solid payment history and ask about their job. Someone with a steady full-time job is likely more stable than someone who works sporadically or changes jobs frequently. You can ask for pay stubs as proof if you’re concerned.

Keep in mind that a potential roommate might have alternative sources of income, like alimony, savings, stipends and investments. Or, if they’re a student, they can typically get extra help via student loans or grants.

Other questions to ask potential roommates

Once you’ve narrowed down your list of candidates, it’s time to go a little deeper by discussing your personalities and habits to find the best fit.

Consider creating a rough outline of a roommate agreement and using it as a conversational guide. If you hit it off, you and your future roommate can edit it together before they move in.

1. Additional financial questions

You don’t have to be best friends to be successful roommates. But you do have to cooperate and be good financial partners.

Ask your roommate what they can spend on rent and utilities and how much they can contribute to the security deposit. Discuss how and when you’ll pay bills and what will happen if someone comes up short.

2. Chores and responsibilities

The bills aren’t the only thing you’ll be dividing — roommates need to split the chores, as well. Be honest about how often you plan to clean, which chores you’d like to handle and if you’re tidy or messy. If you’re on opposite sides of the spectrum, you could face an uphill battle.

Shopping, deep cleaning and other household management tasks like corresponding with your landlord also fall under this category. Hash out how you’ll allocate these tasks and figure out a system that will work for both of you.

3. Personalities and habits

An introvert and an extrovert can live together quite happily, as long as they establish ground rules. Figure out a communication style that works for both of you.

Little disagreements can cause big drama, so chat about seemingly insignificant things like how warm you like the apartment and what you consider a “normal” volume level before you move in. If your views on habits like drugs, alcohol and smoking don’t line up, that’s probably a deal-breaker.

4. Schedules

Get an idea of how often your potential roommate will be at home. A traveling sales rep has a very different schedule than someone who works and socializes on a laptop in their bedroom.

It’s also smart to talk about how they plan to use your joint living spaces. If they cook three-course dinners every evening, like to throw parties or plan movie marathons every weekend, find ways to make sure their activities don’t interfere with your at-home workout sessions or meditation time.

5. Personal relationships

How do you feel about friends and family members coming over or spending the night? What happens if you both want company at the same time? If they’re dating someone, discuss how often their partner will be in the apartment and expectations around what privacy will look like.

Pets are like family, so make sure you know the details about your potential roommate’s pets. Discuss how they’ll share the space with yours and brainstorm how you might split pet-related chores. If one of you is allergic to animals — or if pets aren’t allowed in the building — move on.

The best way to find a roommate

Once you’ve done your homework, it’s time to make your future roommate an offer. Eliminate anyone who gave you a bad feeling or people with whom you just didn’t click. Basic respect and good communication are the building blocks of a solid roommate partnership.

Figuring out how to find a roommate can be challenging. But it doesn’t have to be complicated. Ask smart questions, leverage your personal networks and use tools available to help you find someone with similar goals who will be a good fit.

Many believe that the policies of their landlords will cover them. Some also believe that tenant’s insurance is simply a waste of time and money.

It should be noted that a landlord’s policy will cover things like appliances, structural problems, as well as pipes. However, their policy likely won’t cover your most valuable assets, which may include money, gold, jewelry, and electronics. Damage to such items won’t be covered even in a natural disaster, such as a flood, fire, or earthquake. Your belongings will also not be covered if they’re stolen or vandalized.

The costs of displacement will also typically not be covered by your landlord’s insurance policy, nor will they be held liable if someone is injured in your apartment.

As can be seen, tenant insurance companies have many benefits that many renters are not aware of. Here are the ways tenant insurance helps keep you and your valuables safe and more reasons why it’s important for renters.

What Is Tenant Insurance?

Tenant insurance is also referred to as renter’s insurance. It intends to provide tenants with financial security if their property is destroyed or severely damaged due to an insurable event.

Examples include vandalism, theft, flooding, fires, hurricanes, tornadoes, and earthquakes.

What Does Tenant Insurance Cover?

Tenant insurance can be broken down into three distinct categories in terms of coverage. Each category provides its own set of protections against numerous perils.

Personal property coverage: covers the costs required to replace your personal belongings. Examples include home appliances, computer accessories, electronic gadgets, furniture, and jewelry.

Basic tenant insurance provides personal property coverage in the event of steam or water leakage or overflow. It’ll also provide coverage in the event of lightning, explosions, fire, aircraft damage, hail, and windstorms.

Personal liability coverage and medical expenses: you’re provided with personal liability coverage in the event that you accidentally damage or destroy something while at someone else’s home. Also, if someone accidentally slips and falls while at your apartment, their medical bills will be covered by your insurance, even if you’re deemed responsible. In sum, you’ll be protected, regardless of whether or not you’re the victim or the one responsible for the damage or injuries incurred.

Loss of use coverage: if your home is inhabitable for a prolonged period of time due to extensive water or fire damage, the costs required to stay at a hotel will be covered by your tenant insurance. However, loss of use coverage is temporary, meaning it should only be seen as a short-term solution.

Key Reasons to Have Tenant Insurance

You won’t be legally obligated to have tenant’s insurance in most rental situations, but it’s highly recommended. Some renters mistakenly assume that they will be completely covered under their landlord’s policy or too expensive.

In truth, it should be one of your top priorities while you’re looking for a new apartment. When looking for a tenant’s policy, consider the following to find one that’ll cover you in these situations.

Personal Property Coverage: under your landlord’s policy, only major appliances that came with the apartment will be covered along with the physical structure. As for tenant’s insurance, it’ll cover most, if not all, of your belongings, including clothes, furniture and electronics.

Personal Property Coverage While Traveling: if your belongings are stolen or damaged while you’re away, they’ll be covered. They’ll also be covered if you travel with them and they’re stolen or damaged.

Protection for damages that you cause to someone else’s property: if you damage someone else’s property with your car or accidentally start a fire in someone else’s apartment, you’ll be protected.

Liability Coverage: if you accidentally injure someone while they’re on your property or they injure themselves (i.e., slip and fall on your snowy driveway), then you’ll be protected. You won’t have to worry about paying for any legal and/or medical expenses that arise from injuries to others.

Additional Living Expenses Coverage: if your home is damaged in a flood or fire, then your insurance may cover food, lodging, and other expenses while you’re living in another temporary domicile.

Conclusion

It’s important to note that tenant insurance is usually not mandatory in most cases for those who wish to rent an apartment. However, landlords are legally obligated to obtain it from prospective tenants before an agreement is signed.

All tenant insurance policies are also not the same, so you may want to compare and contrast offers from different companies. The peace of mind and protection you’ll obtain from the ideal insurance package shouldn’t be taken for granted.

Do you know who your neighbors are? According to the Pew Research Center, 57 percent of Americans say they know some of their neighbors. Whether you frequently talk to your upstairs neighbor or you only see your next-door neighbor on occasion, being a good neighbor is important in establishing yourself as part of the neighborhood and community.

1. Learn the three-step rule

“Our best tip to be a good neighbor is a simple three-step rule: Respect, communication and responsible pet ownership!” says 10 Stars Property Management. “In almost any situation respecting others’ space is a good base for any relationship. Especially with someone living right next door. Just be social and communicate with your neighbors — even just a smile goes a long way! Finally, always be conscious of your pets and their actions. No one wants to step into poop!”

2. Consideration goes a long way

“Being a good neighbor means being considerate of people,” says Nick Slagle of HomeRootsPM.com. “They take care of the appearance of their home and simultaneously are willing to help those in their neighborhood. Good neighbors are friendly and welcoming without being intrusive.”

3. Introduce yourself

“The best way to build into a good neighbor? Introduce yourself!” says Jim Shonts, real estate broker and owner of PMI Elevation. “Neighborhoods can thrive on a sense of community, and getting to know your neighbors soon after moving can help you settle in. And, since not all people are outgoing, those early introductions can give insight on how to respect their personal space.”

4. Show interest

“Whether you are moving in or welcoming a new neighbor, show interest in them by allowing the interruption in your day to greet each other when the opportunity arises,” says Sallie Plass from Etiquette Enrichment. “Ask for or suggest ways to get involved in the neighborhood or community. Intentionally smile, exchange names and phone numbers.”

5. Stay kind

Dr. Lew Bayer, CEO of Civility Experts Inc. suggests that a good neighbor should try to “ease the experience” of the others. “This means try to reduce stress and offer support versus causing stress, e.g. if the neighbor leaves the garage door open, let them know. If the neighbor’s dog barking bothers you, ask if you can give the dog a toy or bone. Turn your music down when you see your neighbor come home. Shovel the neighbor’s walk when you shovel yours. Just do what you can to stay kind…everyone is busy and tired and sometimes struggling. Try to assume the best of people and try to make their life easier versus harder.”

6. Treat your neighbor

“A few days after the new neighbors move in, knock on the door to meet them and include a small plate of homemade cookies or muffins or a seasonal plant (for example, a potted chrysanthemum in the fall) and a sticky note with your name and phone number if they need anything,” says Rachel from the Etiquette Trainer. “Additionally, if there’s a neighborhood Facebook page, let them know about it and encourage them to contact you if they need to borrow anything while settling in, such as a ladder or hand tools.”

7. Prioritize respect

“The adage, ‘Good fences make good neighbors’ still holds true,’” says Diane Gottsman, a national etiquette expert from The Protocol School of Texas, “It’s important to be respectful of each other, especially when sharing a fence, trees hanging over the roof, drainage coming into the other person’s lawn and an assortment of dilemmas. If you are experiencing an issue, reach out in person, and address the issue in a pleasant tone of voice with an open attitude and collaborative spirit. People are much more willing to work with someone who has a smile on their face and shows an effort to get along.”

“If there is a problem that cannot be dealt with neighbor-to-neighbor, the HOA may need to get involved. When renting, talk to the landlord first before going over their head. A good neighbor respects each other’s property, pets and privacy.”

8. Just say hi

“I think being a good neighbor starts by knowing your neighbors. I make sure to say hello every day. Whether it’s a good day, bad day or if I’m in a rush, I believe acknowledgment goes a long way and eventually, that helps cultivate a deeper and better neighbor relationship,” says Pamela Syvertson, broker and owner of Verandah Properties.

9. Model how you’d like to connect with your neighbors

“Challenge yourself to reach out to a neighbor you wouldn’t normally connect with and set the tone in how you want to connect with them,” says Daniel McArdle-Jaimes, the Strategic Communications Officer for the Office of Community & Civic Life in Portland, OR. “Maybe your neighbor is from another country or is a different age than you. Start by introducing yourself and developing a relationship to help make your block a more welcoming place for all. And who knows? You might make a new friend or regular lunch buddy!”

“Also — during and after an emergency, neighbors offer a powerful source of help. Organizing a neighborhood meeting or training through an organization to discuss emergency plans and personal safety is a wonderful way to build community. Many cities offer free resources, like the City of Portland’s Neighbors Together training, which help to start and host these important safety conversations.”

10. Remember empathy

“In addition to following the rules of your community, being a good neighbor requires empathy,” says Stayce Wagner, founder and CEO of Spencer Crane Etiquette. “The ability to see things from your neighbor’s perspective helps you behave with kindness, consideration and respect. A good neighbor cleans up their dog’s poop, doesn’t blast music in the middle of the night and never parks in a neighbor’s assigned space without permission.”

“Additionally, if making small talk with people in your neighborhood is outside your comfort zone, start with a smile, eye contact and a friendly hello. When you feel more comfortable, introduce yourself to the neighbors you see regularly and let things develop naturally. Every introduction won’t lead to a close friendship, but you’ll have established friendly contact.”

11. Talk like adults

“The best advice we can give as a management company is that if you have an issue with a neighbor, you go visit them directly and discuss it in an adult manner. Try this approach first before contacting law enforcement, HOA’s or management companies,” says David Peschio, owner and principal broker at PMI Richmond. “It usually can be resolved without escalation and helps maintain good relationships moving forward.”

12. Remember their name

“Being a good neighbor isn’t difficult, but you need to put a little effort into it to have happy neighborly relations,” says Arden Clise, President of Clise Etiquette and author of Spinach in Your Boss’s Teeth: Essential Etiquette for Professional Success. “When a new neighbor moves in, drop by with some cookies, a plant or some small gift to introduce yourself and welcome them to the neighborhood. Be thoughtful. If you’re shoveling your walk of snow, clear your neighbor’s walk, as well. If you have a neighbor who is elderly, sick or struggling in some way, check in on them and see how you can be helpful. At the very least, make an effort to remember their name and say hello when you see them.”

13. When in doubt, act neighborly

“Remember — be kind. To yourself, to your neighbor, their kids, their pets and their plants and trees,” says Felipe Quintana from Charter for Compassion. “Be forgiving: We all make mistakes — aim to be the best version of yourself. Allow everyone their space but stay there for them on the sidelines if they need a friend. It all comes back in the end!”

14. Keep it friendly

“Being a good neighbor means being friendly and helpful, without being intrusive. Giving a wave and a hello with sincerity is felt and appreciated,” says Mary Ann Brennan, the Director of Rental Services for Del Val Realty & Property Management.

“Love your neighbor as yourself, but don’t take down the fence.” — Carl Sandburg

When you’re looking for a new place to live, make sure to ask your future landlord or property management company about the local community. While you can’t pick who your neighbors are, you can ask questions to get a sense of who could be living next door.

Charlsie Niemiec has spent the last 10 years working as a content marketing and social media editor and strategist. With in-house experience ranging from The Elf on the Shelf to CNN to Piedmont Healthcare, Charlsie has freelanced for the last four years with clients ranging from ESPN to the Atlanta Beltline. When she’s not copyediting or scrolling on Twitter, she is walking her very scruffy wirehaired terriers mixes Leonard and Biscuit or probably watering one of her 54 houseplants.

According to the Lost & Found survey by Pixie, nearly one in four Americans misplace their house or car keys twice a week. Having a spare key is quite handy if you find yourself locked out of your apartment.

Where do you hide a spare key when you live in an apartment?

Hiding a spare key in your car or at a house is typically pretty easy, but knowing where to hide a spare key for an apartment is trickier. After all, there aren’t as many nooks and crannies where a spare key can go. Plus, you want to make it easy to find but not obvious to anyone who might be looking for it. However, with a little creativity, there are some great spots where you can hide a spare key for your apartment.

1. Tuck it in your décor

If you routinely decorate your apartment entrance, this could provide an ideal hiding place for your spare key. For instance, you could tape it inside your door knocker or attach it to your wind chimes. If you change out your décor to reflect the season or holidays and tucked your spare key in a wreath or other item, don’t forget to move it from the old décor and place it in the new.

2. Put it in a fake rock along the walkway

Fake rocks are a great option for hiding a spare key for your apartment. However, you shouldn’t place those fake rocks just anywhere — you don’t want to set one near your doorway because it will look out of place, immediately grabbing the attention of would-be thieves. A better location is the landscaping along the walkway to your building or alongside the building. Placing it on the ground among other rocks or under shrubs will camouflage your container. The goal is to make sure it looks natural wherever you place it.

3. Slip it in a magnetic key box under a staircase

Many people often slip a spare car key into a magnetic key box and hide that box somewhere in their car. You can use this same technique by putting your spare apartment key in a magnetic box and hiding it under a metal staircase. Or, you could attach it to the back of a light along the lighted corridor. Another good spot is on the rear of a metal gutter. Essentially, any magnetic surface will work, but make sure it’s not a spot that others may access often. For instance, don’t put it near electrical boxes that may require routine maintenance.

4. Hide it among your outdoor furniture

If you have a patio that’s easily accessible from the exterior of your apartment, you could hide a spare key on the furniture. Tape it under a chair or under your storage box for cushions. Another option is taping it to the underside of your barbecue grill. If you do, check the adhesive on the tape periodically to make sure it’s still securely taped to the grill. A birdhouse is another good hiding spot. Slip your key in there for when you need it, but make sure it’s easy to get out. Just skip the obvious places like under a potted plant or doormat.

5. Stash it under a balcony or deck

For apartment buildings with balconies or decks, you can stash a key in the nooks and crannies underneath the structures. When placing a spare key, check to make sure it won’t fall out easily or get washed away when it rains. Depending on the structure, you might be able to drive a nail into one of the wood posts and hang the key on it.

6. Leave a spare key with your neighbor

If you have a neighbor you know and trust, ask them to keep a spare key to your apartment. Not only will this be handy if you actually lock yourself out of your apartment, but they can help you out if you need someone to put a delivery in your apartment or check on your pets while you’re gone.

Where not to put a spare key for your apartment

When hiding a spare key for your apartment, skip the obvious spots that a would-be burglar may check. These include under the doormat, in or under a potted plant near the door or along the door jam. Although your apartment key would be out of sight, it likely wouldn’t be out of mind for someone trying to gain access to your apartment.

Also, while a fake wall socket or fake clock with a safe can provide a great hiding place, you need to install them in the wall, meaning you’ll need to cut a hole in the wall to place it. If you want to try this option, make sure you talk to your landlord before you make permanent cuts.

The right spot for the spare key for your apartment

Figuring out where to hide a spare key to your apartment might seem difficult at first, but it might be easier than you think. Take a look around your apartment and building and see what good hiding spots you can find. From a metal staircase to a flowerbed to the lights in your hallway, you’ll be surprised at how many places you can find to hide a spare apartment key.

An experienced freelance writer, Karon Warren has covered home and real estate topics for more than 20 years for such outlets as Curbed Atlanta, Apartment Therapy, RealTrends and HotPads.com. She is a member of the American Society of Journalists & Authors.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.

Furnished Finder is where we decided to list our room, which started out as a platform for traveling nurses to find furnished housing. It is now used heavily by many healthcare professionals, students, and professionals in other fields.

Travelers reach out to us through the Furnished Finder website and if the dates work out, we move forward with scheduling a video interview. It’s important for us to be able to talk to the person, even if it’s just over video, and we want them to see our faces and home in real time as well.

For the lease agreement, we used ez Landlord Forms, because they have leases for each state with specific information on what’s required to include.

We don’t ask for anything major from tenants. The most important things to us are that they are respectful of our space, don’t smoke in the house, and pay their rent on time. We also added a page at the end for tenants to add two emergency contacts in case we need to call someone on their behalf.

We have had 4 renters so far with the room being occupied for 13 out of the last 14 months. It has really helped us with our debt payoff goals and we have also met some awesome people through the process! We plan to continue renting it out for the foreseeable future.

Applied for in-state student loan help

My state offered a program called the Oregon Behavioral Health Loan Repayment Program where they help minorities in the behavioral health field, or those who serve them, pay back their student loans.

This program is funded by The Behavioral Health Workforce Initiative which has the goal of recruiting and retaining behavioral health providers who, “Are people of color, tribal members, or residents of rural areas of Oregon, and can provide culturally responsive care for diverse communities.”

To apply, I had to show I was employed and actively providing behavioral health services and give them detailed documentation about my student loans. I also had to answer two essay questions related to being a part of and/or working with communities who are underserved and how my training has equipped me with supporting these communities.

I applied last year and was a recipient of an award!

As a recipient, there is a two-year service commitment which means I have to continue providing some sort of behavioral health service during that time frame (which I planned to). Over the next two years, I will be getting ~$88,000 in quarterly disbursements to put towards my student loans. So far this year, I have received ~$11,000, and it’s been life changing to say the least!

Alongside this support, I am also pursuing Public Service Loan Forgiveness (PSLF) for additional student loan relief.

Managing our mental health while paying off debt

Since I am a social worker, I often think about how money and debt affect individuals’ mental health. It’s one of the reasons why I started my blog in the first place.

I realized managing money is a universal task and many of us don’t know what we are doing because talking about money is taboo. And when you have financial stress, it can really take a toll on your mental health. So, I wanted to share our journey in hopes of helping others.

Bret and I aren’t those individuals who want to avoid eating out and fun experiences until we are debt free. And, we are also privileged to not have to take those extreme measures either. It has been important for us to make this journey sustainable and not deprive ourselves of experiences while we are going through it.

Here’s how we are making our journey sustainable:

Still going out to eat

Budgeting for personal spending money, aka fun

Setting realistic debt payoff goals

Putting aside money for travel

Not comparing and thinking other people are better than us because they’re able to pay off their debt quicker

Tracking our debt payoff progress (we use Excel). With so much debt left to pay off, being able to see our progress is really motivating

Openly talking about our debt. Avoidance is a coping mechanism for many, for us, acknowledging and addressing it has been so freeing (but it wasn’t always this way).

Talking about our dreams and reminding ourselves why we want to do this in the first place

We know that if we eliminated going out to eat, budgeting for fun, or both, we could be paying off our debt much quicker. However, that sounds miserable to us. It’s worth it to still go out to dinner, travel, or buy plants (in my case) than to deprive ourselves of the joy these things bring.

We are making great progress and we know in time, we will be debt free.

Our debt payoff journey is not linear

A few months ago, we decided to take out $6,000 of student loans. Bret currently has a full tuition scholarship, so we are tremendously lucky in that regard, but he just learned about some conferences that would be really helpful to his professional growth. We have gotten $1,500 of this loan money already which is included in our current debt balance, but we haven’t received all of it yet.

We could have pinched and saved to avoid taking on any of this debt, but that would have caused me to work more than I currently am. Again, not in line with our current goal of making this journey sustainable!

We were very intentional about how much to take out. We estimated how much he would need for a few conferences and declined the rest. We even opened a separate savings account for the money to make sure it didn’t get accidentally spent on anything.

I’m SO proud of us for that!

The goal here is progress not perfection. So cliche, I know. But we are learning how to think critically about our money, spend thoughtfully, use our money as a tool to reach our goals, and enjoy our life along the way. And right now, that meant taking on a little more debt.

We are moving in the right direction, and we know when he starts working, that will really accelerate our debt payoff journey since we have proven to ourselves we can live on my income alone.

Our plan going forward

Bret is still in school which means his loans are on deferment, so we currently have his on the back burner.

With the loan payment assistance I am receiving, it’s allowing us to put any extra money we have each month towards our savings. Our priority right now is building up a good emergency fund of about $16,000 (~4 months’ worth of expenses).

This has been difficult because of inflation and just little emergencies that keep popping up, but we are slowly making progress.

I am also prioritizing investing in my employer retirement plan, but only up to the amount that gets me my employer match which is 6% of my income.

Bret will be graduating in 2025, so at that time, we will pivot to incorporating his loans into our budget. Our goal is to be debt free by 2028.

It will take a lot of discipline and persistence, but I think we can do it. I am manifesting it!

We want to continue to learn, implement, and grow. We want to keep having transparent discussions about money and building our money foundations. And I personally want to continue sharing our journey with hopes of inspiring, encouraging and educating others. Here’s to sharing the wealth.

Do you have debt? What are you doing to pay it off?

Taylor is a social worker and personal finance blogger at Social Work to Wealth where she shares tips, resources, and lessons learned on her family’s journey to paying off $277,000 of debt and retiring early. She hopes to inspire and empower social workers with financial education so they can have a better relationship with their money. When she’s not working or blogging, you can find her traveling, gardening, trying a new restaurant, or buying too many plants.

More than seven in 10 landlords (71%) say they are unlikely to buy a property which has an EPC rating of less than C, according to the latest BVA BDRC landlord research for quarter two 2023.

Asked to what extent the EPC rating of a property now impacted on their purchasing decision, the vast majority of respondents said they were increasingly unlikely to purchase a rental property if it wasn’t already at a C level – which is likely to be the future minimum standard.

The more properties the landlord had within their portfolio, the less likely they were to buy below C, with 74% of those with six to 10 and 11-19 properties, saying this, and 78% of those with over 20 properties. Only 18% of landlords said the EPC level would make no difference.

The research, comprised of 983 online interviews with landlords, was undertaken on behalf of Foundation Home Loans, the intermediary-only specialist lender, between the first three weeks of July this year.

Landlords also had a strong awareness of the likelihood of future legislation around a minimum EPC level of C being introduced for all private rental sector (PRS) properties. 71% said they were aware and fully understood the details, 24% were aware but did not understand the details, and just 4% had no awareness.

Given that, according to the research, the average landlord has 3.3 properties rated EPC D or below, with this rising to 9.5 for landlords with more than 11 properties, Foundation said it was not surprising to see strong awareness of future minimum EPC standards for PRS properties and landlords being less inclined to add below-Level C EPC properties to their portfolios.

In terms of the work landlords intended to carry out on below-Level C properties, 37% said they would carry out the works at the minimum cost required to comply, while nearly one in five (20%) said they would carry out works to maximise the long-term value of their property. However, a quarter said they would not carry out any works and would either sell the property or not re-let it.

Landlords anticipate it will cost just over £10k per property to carry out the works required to reach EPC Level C, with this rising to over £11.5k for those with larger portfolio sizes.

57% said they would fund the works via savings (down from 76% last quarter), 33% said they would increase the rent (up from 26%), 18% would access Government grants or funding (previously 19%), while 19% said they would either take a further advance from their lender or take out a loan (down from 20%).

Foundation Home Loans offers a range of specialist buy-to-let mortgages available to individual and portfolio landlords as well as limited companies. The lender allows capital raising for a very broad range of purposes on its core buy-to-let range, and specialises in portfolio underwriting. It also offers a specific range of Green products available for any property with an A-C EPC rating.

Foundation’s current service levels continue to average turnaround times of one day for DIP referral, application and underwriter review for all cases.

Grant Hendry, Director of Sales at Foundation Home Loans, said:

“While we still might be waiting for certainty and clarity over when the Government is likely to introduce its minimum EPC Level legislation for the private rental sector, it’s clear from this research that landlords are aware of what is likely to be coming, and are thinking seriously about their existing portfolios, how they might fund improvements, and what their plans might be when this is introduced.