Home builder confidence took a hit in September as average mortgage rates for a 30-year fixed-rate loan stayed above 7%.

Builder confidence in the market for newly built single-family homes in September fell five points to 45, according to the National Association of Home Builders / Wells Fargo Housing Market Index released Monday. This follows a six-point drop in August.

The monthly index looks at current sales, buyer traffic and the outlook for sales of new-construction homes over the next six months. September’s reading is the first time in five months that overall builder sentiment levels dropped below the break-even measure of 50.

“The two-month decline in builder sentiment coincides with when mortgage rates jumped above 7% and significantly eroded buyer purchasing power,” said Alicia Huey of the NAHB.

Home builder sentiment had been rising earlier this year, riding the wave of demand caused by lack of inventory in the existing home market. But confidence dropped for the first time this year in August, as rates climbed.

In addition, builders continue to grapple with a shortage of construction workers and buildable lots, which is further adding to housing affordability challenges, said Huey.

All three dimensions of the new housing market evaluated saw declines in September: The index gauging current sales conditions fell six points to 51. The component charting sales expectations in the next six months also declined six points to 49. And the gauge measuring traffic of prospective buyers dropped five points to 30.

“High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower,” said Robert Dietz, NAHB Chief Economist. “Putting into place policies that will allow builders to increase the housing supply is the best remedy to ease the nation’s housing affordability crisis and curb shelter inflation. Shelter inflation posted a 7.3% year-over-year gain in August, compared to an overall 3.7% consumer inflation reading.”

New homes have become an attractive alternative for buyers frustrated by extraordinarily low inventory of existing homes as homeowners hunker down with their ultra-low mortgage rates of 2%, 3%, 4% rather than selling and becoming a buyer at a 7% rate.

As mortgage rates stayed above 7% over the last month, more builders cut prices to boost sales, according to NAHB.

In September, 32% of builders reported dropping home prices, compared to 25% in August. That’s the largest share of builders cutting prices since last December. The average price discount is 6%.

Meanwhile, 59% of builders provided sales incentives of all forms in September, more than any month since April.

This available inventory and price flexibility has gotten the attention of first-time homebuyers.

According to the NAHB, 42% of new single family home buyers were first time buyers so far this year. That’s significantly higher than the 27% of first time buyers purchasing new construction homes during the same time period in 2018, when the market was more typical.

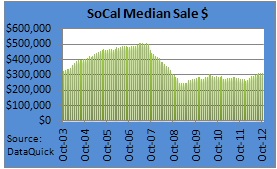

Are foreclosures going the way of the dodo? Not quite, but they certainly aren’t as common as they once were, if a new report from DataQuick is any judge.

The company, which tracks home purchases nationally and in many large metros across the country, noted that foreclosures accounted for just 16.3% of the Southland resale market in October.

While still a sizable chunk of home sales in the hard-hit area, it’s nowhere close to the 32.8% share seen a year earlier.

In fact, last month’s level was the lowest since October 2007, just after the housing boom went bust.

The highest monthly percentage total recorded was a staggering 56.7%, seen back in February 2009. The word “yikes” comes to mind.

Yes, more than one in every two resales used to be a foreclosure in SoCal, which explains the rapid decline in home prices.

But now that foreclosures are becoming less and less common, home prices are marching higher, and are now at levels not seen since August 2008.

We’ve still got a long way to go to hit those insane 2006 and 2007 numbers, but things appear to be on the mend. Even home flipping is up, rising from 3.7% last year to 6.1% last month. Watch out for bad granite countertops, laminate floors, and cheesy fixtures.

The median price paid for a home in the Southland last month was $315,000, steady compared to September, but up 16.7% from October 2011.

DataQuick attributed the rise to highly favorable mortgage rates, along with a change in the mix of homes selling.

In short, heavily discounted foreclosures are being replaced by a larger share of move-up home sales, which pushes the median higher.

Home sales in the $300,000 to $800,000 range have jumped 41.5% annually, while sales above $500,000 are up 55.2%.

And last month, home sales over $500,000 accounted for 23.3% of all SoCal sales, up from 17.9% a year ago.

Short Sales and Foreclosures Still Hold a Large Share

Overall, it’s still not very pretty. Short sales still hold more than a quarter of the resale market (26%), down slightly from 25.4% a year ago.

So combined with foreclosures, distressed sales make up nearly half the entire market, which clearly does not exude “healthy.”

The word “recovering” is probably more appropriate. But it certainly beats “declining.”

The good news is that investors seem to be on-board, despite the rise in home prices. Absentee buyers, which purchase both investment properties and second homes, bought 28% of Southland homes in October.

That number is up from 27.7% in September and 25.4% in October 2011. The record was set earlier this year when absentee buyers snatched up 29.9% of sales in February.

Seeing that the monthly average is 17.6% going back to the year 2000, there are clearly some deals to be had out there still.

Cash Is King

Unfortunately, for everyday homebuyers, the investors are making it increasingly difficult to snag a property on the cheap, or at all for that matter.

About a third of all purchases in October were paid for with greenbacks (32.1%), up from 30% last year, and not far from the record of 33.7% set in February of this year.

Cash offers easily trump those looking to finance a deal with a mortgage, which explains why buyers are having to come in with sizable down payments if they want to be considered.

It’s clear if you look at the FHA loan numbers – last month, they accounted for just 25.2% of all purchase mortgages, down from 31.9% a year ago.

The FHA-share is now at its lowest point since July 2008, because let’s face it; a 3.5% down payment doesn’t beat a 100% down payment.

Put simply, if you want a house in a desirable area, be prepared for a bidding war.

Nestled in Hidalgo County, the small city of Alamo, Texas, often emerges as a discussion point among people on a quest for a serene yet promising locale to call home.

The quaint charm often associated with smaller cities can sometimes transcend beyond the picturesque to also offer a quality of life that rivals, or in some instances, surpasses the bustling allure of much larger cities.

This comprehensive assessment dives into the various factors that encapsulate living in Alamo, Texas, with a thorough examination of its cost of living, demographics, amenities and proximity to other significant Texan hubs, ultimately aiming to answer the burning question: “Is Alamo, Texas, a good place to live?”

Demographics and community

The community within Alamo, TX is a reflection of the broader Rio Grande Valley’s demographic composition. With a population that hovers around the 19,000 mark, the town hosts a predominantly Hispanic populace. This cultural backdrop lends Alamo a unique blend of Texan and Mexican traditions, which not only enriches the social fabric but also manifests in the culinary, cultural and artistic offerings of this small city.

Economy and employment

A scrutiny of Alamo’s economic landscape reveals an unemployment rate slightly above the national average. However, this metric has been on a downward trajectory, thanks to burgeoning local businesses and the spillover of economic activities from neighboring cities. The median income in Alamo resonates with the laidback and modest lifestyle it champions.

Cost of living

One of the enticing facets of living in Alamo, Texas, is undoubtedly its cost of living. Statistically, Alamo’s cost of living indices fall below the national average, making it an affordable place especially when pitted against other cities in Texas.

The low cost of living can be largely attributed to the affordable housing market in the city, with the median home value significantly less than the state and national averages. Alamo’s cost of housing and overall living expenses are arguably its biggest selling point to prospective residents on a budget.

Housing market

In Alamo, the median home value stands as a testament to its affordability. Housing here is not only accessible but offers a variety of choices for different income levels. Whether you are looking to rent or buy, the market in Alamo is conducive for families, retirees and even single individuals. The median home value is appreciably lower compared to other cities, making homeownership a feasible dream for many.

Education

Education is a pivotal concern for families contemplating a move to Alamo, TX. The city hosts several public and private schools, delivering a standard of education that aligns with the state’s benchmarks. The proximity to universities and colleges in nearby cities also broadens the educational horizon for residents.

Healthcare and services

Quality healthcare services are within reach, with a number of healthcare facilities located in and around Alamo. The nearby city of McAllen, for instance, has a wider array of medical facilities, ensuring residents have access to specialized medical care whenever necessary.

Proximity to major cities

Nestled strategically in the Rio Grande Valley, Alamo’s location is within a convenient distance from major cities like McAllen and Edinburg. This proximity not only opens up a world of additional amenities and services but also employment opportunities for the residents of Alamo. Moreover, the accessibility to international borders with Mexico enhances the city’s appeal to a more global-minded populace.

Recreation and lifestyle

The lifestyle in Alamo leans towards the tranquil and family-oriented. Numerous parks, recreational facilities and community events held throughout the year contribute to a sense of belonging among residents. The close-knit community vibe is often cited in reviews as one of the endearing qualities of living in Alamo.

Crime and safety

The crime rate in Alamo is comparable to other small towns in Texas. The local law enforcement agencies are active and the community itself is known for its neighborly ethos, which contributes to the overall safety and peaceful living conditions in the city.

Conclusion

The allure of Alamo, Texas lies in its simplistic yet fulfilling lifestyle, far removed from the hustle and bustle synonymous with bigger cities. While it might lack some of the flashy amenities, its affordability, community-centric lifestyle and the promise of a serene living environment make it a compelling choice for individuals seeking a harmonious work-life balance.

However, as with any city, prospective residents should be aware of the economic conditions and be prepared for a lifestyle more serene and traditional compared to urban hubs like Austin or Houston. Looking for your Alamo dream home? Take a look at our available apartments for rent here.

Why Your Checking Account Should Contain as Little Money as Possible

By: Natasha Etzel |

Updated

Oct. 4, 2023 – First published on Oct. 4, 2023

A bank account is an excellent place to keep your money so it’s organized and readily available when needed. Many people keep their cash in a checking account. But, while you want to stash enough money in your checking account to cover your bills and everyday expenses, you want to avoid keeping all of your cash there. I’ll explain why here, and suggest a better place to stash your extra savings.Don’t miss out on interestThe average checking account doesn’t accrue interest. That means you won’t get rewarded for keeping money in your bank account. Instead of keeping all your cash in your checking account, you should only keep enough to cover your monthly expenses. You may want to keep a bit more than just enough to cover your bills. That way, you’ll be covered if you have an unexpected charge or a more costly bill than anticipated. How much extra should you have? It depends. For some people, a couple hundred extra dollars may be ideal. But for others, it may be a good idea to include a few hundred or up to an extra $1,000 in their checking accounts for extra wiggle room.But don’t keep every last dollar you have in your checking account. If you do, you’ll miss out on interest. Instead, move your extra savings into a bank account that accrues interest. With an interest-earning bank account, you’ll get rewarded as your cash sits in the bank. You could earn money with a savings accountMany people keep extra cash in a savings account. Review the bank’s annual percentage yield (APY) when considering a new savings account. This rate is the amount of money or interest you’ll earn over a year. The higher the APY, the more money you can make. You can take advantage of an attractive interest rate by opening a high-yield savings account. At the time of writing, the bank accounts on our best high-yield savings accounts list offer APYs ranging from 4.30% to 5.26%. If you have a significant amount of extra cash and keep it in an account like this, you can earn money without doing extra work. $5,000 in savings accumulates this much interest To determine how much interest you can earn by moving your extra cash to a savings account, multiply your initial deposit by the APY your bank account offers. This will show you how much interest you can earn by keeping your money in the bank for a year. Let’s imagine you have $5,000 extra sitting in your checking account right now. If you instead move that money to a high-yield savings account with an APY of 5% and you keep it in the bank for an entire year (and your APY doesn’t change; note that banks can raise or lower APYs at any time), you’ll earn $250. That’s much better than making $0 by keeping your savings in a checking account that doesn’t accrue interest. Now you can see why it pays to avoid keeping all your money in a checking account. You can earn extra money from interest by keeping your spare cash in a savings account that offers interest. For additional tips like this, check out our free personal finance resources.

3 Reasons I Don’t Like Aldi as Much as I Used To

By: Maurie Backman |

Updated

Sept. 13, 2023 – First published on Sept. 13, 2023

At some point in 2022, I discovered Aldi and began shopping there weekly. I found that I was able to save money on my grocery bill by purchasing certain produce items there. And since I happen to have an Aldi adjacent to my local Costco, it wasn’t particularly out of my way.But over the past few months, I’ve become less enamored with Aldi. Here’s why.1. The selection is just too limitedAldi — at least near me — is a minimally stocked grocery store. The shelves aren’t loaded the way they are at my nearby ShopRite and Stop & Shop.To be fair, this was the case when I first started shopping there. But because there’s just not a lot of selection, I’m generally limited to only buying a few items when I pop into Aldi.Not so long ago, I was running into Aldi for some fruit, which I usually buy there, and I needed to grab shredded cheddar cheese. Normally, I get that at Costco, but I didn’t want to run next door to Costco and wait in a line for cheese alone. Unfortunately, though, Aldi didn’t have the cheese I needed, so I had to make an extra stop anyway.2. The inventory is too inconsistentNot only is there a limited selection of food items I can buy at Aldi, but sometimes, I can’t even find the five or six things I’m looking for. Aldi was once my go-to source for avocados, since it’s an expensive purchase and Aldi tends to sell them for less than Costco (at least in my area). But the last few times I stopped at Aldi, avocados weren’t in stock.And that’s happened to me with other things, too. Over the past several months, I’ve struggled to find everything from cucumbers to strawberries at Aldi as well.3. What the store saves me on groceries, I lose via lost working hoursShopping at Aldi still has the potential to save me a little money on groceries. At a time when supermarket prices are up 3.6% on an annual basis, that helps.The problem, however, is that even though Aldi is right near Costco in my neighborhood, thereby allowing me to combine those trips, it still takes time to visit an extra supermarket. I have to find parking, wait in a checkout line, and spend time searching the shelves.While it’s nice to save $2 here and $3 there, the reality is that a stop at Aldi might cost me 20 or more minutes of work — especially when I don’t manage to find the things I need. And losing out on that work time often means forgoing more than $2 or $3 of income. So from a time perspective, it’s just not worth it.Shopping at Aldi could make sense for a lot of people. If you’re someone with flexibility in your schedule and grocery list, and you’re not so picky about the brands you bring home, then it could pay to spend the time visiting Aldi, even if you don’t always manage to find all the things you need. But I’ve reached the point where shopping at Aldi makes less and less sense for me, so I’ll most likely stop going there unless it’s a one-off basis.

7 Little-Known Gift Cards You Should Always Buy at Costco

By: Steven Porrello |

Updated

Sept. 29, 2023 – First published on Sept. 29, 2023

Costco gift cards are one of the warehouse’s best deals. Costco often will add 10% to 30% of value when you buy its gift cards in a bundle. It would be one thing if the gift cards were for places you’d never shop, like Bed, Bath, and Beyond (R.I.P.). But Costco gift cards are surprisingly varied and include many restaurants and retailers you’re probably already spending money with.So if you, like me, pinch pennies for your finances, here are seven gift cards you should always buy at Costco.1. Jiffy LubeCostco will add 25% of value when you buy a set of two $50 Jiffy Lube eGift cards for $74.99. While Jiffy Lube doesn’t offer the cheapest oil change on the market (Walmart will likely take the gold for that), its technicians do go through rigorous training via the Jiffy Lube University to ensure no accidental damage is done to your vehicle. If quality trumps price for your vehicle, this deal will save you $25 off your next oil change (limit of five per membership).2. Alaska AirlinesPacific Northwesterners will appreciate this deal — Costco will give you a $500 eCertificate to Alaska Airlines for $449.99. That comes to 10% off your next Alaska Airlines flight (limit of four per membership).3. Southwest AirlinesIf that was the first time you’d heard of Alaska Airlines, here’s a gift card package with a more familiar airline: Southwest. Costco will add 10% of value when you buy $500 of Southwest Airlines gift cards for only $449.99.4. Cinemark TheatresIn a great deal for moviegoers, you can buy a $50 Cinemark Theatres eGift card for only $39.99 at Costco. That’s an extra 20% of value that you can use for movie tickets, food, drinks, or merchandise (limit of 10 per membership).5. Miller PaintPainting your house ain’t cheap. Interior paint jobs will cost about $2 to $6 per square foot, according to the home improvement site HomeAdvisor, while exterior paint jobs can cost about $1.50 to $4 per square foot. To ease those costs, Costco will sell you $100 of Miller Paint gift cards for $69.99 — a whopping 30% of extra value.6. SpafinderIf you thought the cost of painting your house was bad, imagine how your back will feel after hours of painting walls. To ease that pain, Costco has an irresistible gift card deal: two $50 eGift cards for $79.99 to be used at thousands of spas and salons across the country. You can also use them at participating yoga and fitness studios (limit of 10 per membership).7. Synergy RestaurantsOne of the more interesting gift card packages I’ve come across, this extremely lucrative deal — two $50 eGift cards for a sticker price of $69.99 — will help you foot the bill at hundreds of local restaurants in numerous cities across Arizona, California, Colorado, Nevada, New Mexico, and Texas. This is perhaps one of the best deals I’ve seen and can be perfect for locals in those states and travelers who are visiting them.Most members don’t realize how many gift cards Costco actually sells. In fact, these seven packages only scratch the surface. Next time you’re at your local Costco warehouse, be on the lookout for gift card packages, which are often found at the ends of aisles. You might find a deal you can’t get anywhere else.

5 Amazing Costco Buys for Less Than $10

Costco is a favorite among bargain hunters. But because it’s a place where you typically buy in bulk, it’s often not great when you only want to spend a few bucks. Believe it or not, though, there are some deals at Costco for $10 or less. Here are five amazing Costco finds that will set you back no more than $10.1. Rotisserie chickenNot surprisingly, the $4.99 rotisserie chicken tops this list. Costco debuted its famed bird for $4.99 way back in 1994. It briefly raised the price by $1 during the Great Recession in 2008, then knocked it back down to $4.99 one year later. Had Costco raised its prices to keep up with inflation since 1994, that chicken would cost $10.48 today.Costco’s rotisserie chicken will always be a fan favorite for those looking for an effortless dinner. Just be aware: Costco keeps the prices low because its rotisserie chicken is what’s called a loss leader. The warehouse giant is willing to lose money selling them because it knows it can get customers into stores, where they’ll probably buy more than just a chicken.2. Hot dog and soda comboCostco has raised the prices of many of its food court items in recent years, but the price of one perennial favorite shows no signs of budging: the hot dog and soda combo, which has cost $1.50 since it debuted in 1985. Adjusted for inflation, the hot dog and soda combo should cost $4.28. Last year, during a quarterly earnings call, Costco chief financial officer Richard Galanti said the warehouse giant could keep the $1.50 price point “forever.”3. Kirkland Signature Creamy Almond ButterYou can use almond butter as a salad dressing ingredient, slather it on toast, put it in baked goods, or just eat it straight from the jar. If you’re the type who likes to devour almond butter by the spoonful, you don’t want to pass up a 27-ounce jar of Kirkland Signature Creamy Almond Butter, available for just $7.99. That works out to less than $0.30 per ounce. By comparison, a 16-ounce jar of Trader Joe’s Creamy Almond Butter Salted costs $6.99.4. Olde Thompson Kosher Sea Salt, 5 lbsSea salt has plenty of uses that go beyond cooking. You can use it for cleaning, as an exfoliant for your skin, and sprinkle it around your garden to keep unwanted bugs away. For just $5.99, you can score a 5-pound jar of Olde Thompson Kosher Sea Salt and keep it handy for all your household and kitchen needs.5. Bisquick Pancake & Baking Mix, 96 OuncesBisquick is another one of those things that’s handy to keep in your pantry. You can use it to whip up a quick batch of pancakes or waffles for breakfast or keep it on hand for a variety of baked good recipes. A 96-ounce box of Bisquick is available at Costco for $8.89. It’s normally priced at $10.99, but there’s a $2.10 manufacturer’s discount that’s good through Oct. 8, 2023.What are the best deals at Costco?Since Costco tends to sell large quantities, you’ll typically find that a lot of the best deals cost well above $10. Regardless of the exact price, it usually makes sense to buy products at Costco that have a long shelf life. For example, even if you find great deals on fresh produce and milk, you probably don’t want to load up on these items unless you’re feeding a large crowd, as they’ll go bad quickly.Also, make sure you look beyond the grocery department for savings. For example, getting your prescriptions from Costco Pharmacy or using Costco to fill up your gas tank could also save you money.If you want to maximize the benefits of your membership, try shopping with a Visa credit card that offers rewards. (Costco only accepts Visa credit cards.) That way you can earn travel rewards or cash back when you load up on groceries and other necessities.

5 Ways to Turn $100 Into Passive Income

By: Chris Neiger |

Updated

Oct. 1, 2023 – First published on Oct. 1, 2023

Creating passive income is one of the best ways to build wealth and protect your personal finances from an emergency, like losing a job or having your salary cut. According to U.S. Census Bureau data, about 20% of Americans have some level of passive income, with the average amount earned from passive income being $4,200 annually.Passive income strategies aren’t get-rich-quick schemes, and many initially require a significant time investment. The good news is that many can be started with $100 or less. Here are a few inexpensive ways you can start generating passive income.1. Buy stocksSome people think that owning stocks is only for rich people. It’s not. In fact, 61% of Americans own stocks, according to Gallup. And while you won’t get rich investing $100, you do have the potential to easily make money.You can open an online brokerage account for free and typically buy stocks for either little or no fees these days. The hard part is figuring out what company you think will do well over the long term so that you get the largest return.Let’s look at one popular company that many people own stock in: Apple. Let’s say you invested $100 annually over the past 10 years to buy Apple’s stock and reinvested any dividends you received to buy more shares. Thanks to Apple’s phenomenal growth over the past decade, your stock would be worth $4,848 — a 385% return on your investment.Of course, picking stocks can be difficult. If you want to potentially earn passive income in the market without picking specific stocks, you may want to buy shares of an exchange-traded fund (ETF). These funds follow market indices and can be purchased for as little as $1, thanks to online platforms that allow you to purchase fractional shares.2. Rent out an extra roomThis one is super easy and might cost you $0 if you already have the extra space. The latest Census Bureau data shows that 27.6% of Americans live alone. This means that many Americans may have a spare room in their home that could be transformed into a passive income stream.While it’s not for everyone, renting out a room in your home could be one of the easiest ways to generate passive income because you’re already in the space — either renting or as a homeowner — so all you need to do is find a roommate and collect their rent payments.This could be a very lucrative way to boost your income, considering that rent prices have skyrocketed over the past few years.3. Rent out your carWith 13% of full-time Americans working from home right now and 28% on hybrid schedules, many cars are sitting unused throughout the work week. With some planning and effort, your vehicle could quickly begin generating income through car-sharing websites like Turo.You can list your vehicle on the site for free and pay Turo a fee when you’ve rented out the vehicle. Turo says the average annual income for one car on its site is $10,516. Of course, some work is required to keep the vehicle clean and coordinate pick-up and drop-off. Still, renting out your vehicle could be a low-cost way to earn semi-passive income.4. Create an online courseMany people have accumulated many skills through jobs and even hobbies. You likely know how to get certain things done that someone else would find very useful — and pay for.There are many online platforms — including Udemy, Skillshare, and Thinkific — where you can create your own professional course and then sell it to an established online audience.You’ll need to do a fair amount of work upfront creating your course — including planning the sessions, recording videos, and making other content — but once you have it up and running, you can earn passive income from your hard work.Some course-creating platforms charge a monthly fee, while others may take a percentage of each sale you make. But while this option isn’t free, it’s certainly inexpensive.5. Start a dropshipping businessThere are many different businesses that fall under the dropshipping category, including selling T-shirts online or print-on-demand content like notebooks and journals.The startup cost for dropshipping businesses is low because you don’t buy any inventory and don’t have to rent an office or retail space. Instead, you’ll spend money setting up a website and potentially selling ads to market your products. You can even become a seller on Amazon and sell products without investing in your own online shop.You’ll have to invest significant time on the front end to build your business. Still, once you’ve found a niche and have established the relevant products, dropshipping allows you to spend minimal time keeping up the business while still making online sales.Keep these things in mindWhile all of these ideas will cost you little money and have the potential to generate passive income, you’ll still need to invest time and mental energy in setting them up. For example, you may need to do a lot of research before setting up a dropshipping business or launching an online course.Like anything worthwhile, be patient and take small steps to get started. You likely won’t be an overnight success, but making any progress toward generating passive income will move you further toward your personal financial goals.

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience. There are many ways to make money online, and as a teenager, you may be interested in learning how you can as…

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience.

There are many ways to make money online, and as a teenager, you may be interested in learning how you can as well.

Whether you are 13 years old or 19 years old, there are many different legitimate online jobs for teens that you may be interested in learning more about.

Related content:

Online Jobs For Teens

There are many online jobs for teens listed below. If you want to skip the list, here are some virtual jobs for teens that you may want to start learning more about first:

Start a website

While I was around 21 years old when I started my blog, I know of a few people who started theirs as teenagers.

A blog can be a great online job to start when you’re young, as you can decide how to build your blog, how you earn an income, and the schedule you put toward it.

Blogging has allowed me to travel full-time, work from home, have a flexible schedule, earn a high income, and love what I do.

You can easily learn how to start a blog with my free How To Create a Blog Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog today

Day 2: What topic to blog about

Day 3: Tutorial on how to start a blog on WordPress

Day 4: How to make money with your blog

Day 5: How to make passive income on your blog

Day 6: How to get pageviews to your blog

Day 7: Tips to see success with your blog

Out of all of these online jobs for teens, blogging is by far my favorite. It does take a little more time to start making money, but it’s very flexible and fits with any kind of schedule.

Create a TikTok account

You have most likely heard of TikTok.

There are over 1.5 billion users on TikTok, and many people are able to earn an income on this social media platform doing many different things.

From personal finance tips to comedy, day in the life to travel, and more, there are many different topics you can cover on your own TikTok account through making social media content.

If you want to learn how to make money online for teens, this is a fun one.

You can learn more at How I Make Money On TikTok – How I Grew To 350,000 Followers and Made $60,000 In 6 Weeks.

Begin a YouTube channel

Everyone has heard of YouTube, and pretty much everyone has watched at least one YouTube video in their life.

In fact, according to YouTube, there are over 2 billion people who watch at least one video on YouTube each month.

Many people have goals of starting a YouTube channel and making money, but not many people ever actually start.

You can learn more at How I Grew From 0 Subscribers To Over $100,000 On YouTube In Less Than One Year.

Resell items online

If you are looking for a flexible job as a teenager, one to look into may be reselling items online, such as on Craigslist, eBay, or Facebook Marketplace. There are many other online marketplaces as well.

Plus, it’s something that anyone can start because many of us own things that we could probably sell.

And, there are always things that you can buy for a low price and possibly resell for a profit. Or, you may even be able to find free things that people are throwing away and sell that as well.

This is such a profitable idea that my friend was able to make $133,000 in one year through buy-and-sell flipping and with working only 10-20 hours per week.

Since then, they have turned this into an even bigger and more profitable business!

Some of the best items that they’ve resold include:

Something they bought for $10 and flipped for $200 just 6 minutes later

A security tower they bought for $6,200 and flipped for $25,000 just one month later

A prosthetic leg that they bought for $30 at a flea market and sold for $1,000 on eBay the very next day

A lift that they found in the trash (and asked the owner for permission to take) that they sold online for $7,500

You can learn more at How I Made $40,000 In One Year Flipping Items.

They also have a helpful free webinar, Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business In As Little As 14 Days. I recommend checking it out.

Sell printables on Etsy

If you are looking for a way to make money at home and be your own boss, then creating printables may be for you.

A printable is a digital product that can be downloaded and printed at home. You make them once and then sell them on a website such as Etsy for people to buy. You wouldn’t have to print anything, instead, you are simply selling the download.

Items such as grocery shopping checklists, weekly meal plans that someone puts on their fridge, gift tags, and quotes to be framed are all printables.

This can be a great way to make money at home as a teenager because you create one digital file download per product, and you can then sell them an unlimited amount of times.

You can sign up for this free ebook that helps you figure out where to start when it comes to selling printables on Etsy.

I recommend reading about this further at How I Make Money Selling Printables On Etsy to learn more about one of the best jobs for stay-at-home moms.

Note: Etsy account owners must be at least 18 years of age to sell on Etsy. If you are between the ages of 13 and 17, you can sell on Etsy if you have the appropriate permission and direct supervision of your parent or legal guardian. Your Etsy account must be registered with the parent or legal guardian’s information.

Create and sell stickers

Another fun way to make money online as a teenager is to sell stickers.

My friend started with no graphic design skills and didn’t even know how to create stickers when she first started. It’s something she learned as she went, and she now earns over $100,000 each year with her sticker business.

I interviewed her here on Making Sense of Cents and she answered questions such as:

Do I need to be a graphic designer to make and sell stickers?

Why do people buy stickers online?

Do stickers sell well online?

How much money can I make selling stickers as a small business idea?

You can head over to How To Make $1,000+ A Month Selling Stickers Online to read more.

Make Canva templates

Canva is an online graphic design website. On Canva, you can sell premade designs to other Canva users so that they can edit and customize them.

Some examples of Canva templates include ebooks, workbooks, Pinterest pins, and more.

Creating Canva templates can be a great way to make extra money because you just need to create them once, and you can sell them an unlimited amount of times.

People all around the world use Canva to help with the graphic design side of their business, and templates make their lives so much easier.

Working just a few hours a week, I know someone who is able to earn $2,000 each month from selling Canva templates from home.

Do you have questions such as:

What is a Canva template and what is Canva?

Why would someone buy Canva templates? What is the benefit?

I have no tech skills, can I still create and sell Canva templates?

You can head to this article to learn more at How I Make $2,000+ Monthly Selling Canva Templates.

Voice over acting

Voice-over actors are of all ages, and you probably hear them all the time!

A voice-over actor is the person you hear but usually do not see on radio ads, YouTube videos, documentaries, e-learning courses, audiobooks, TV commercials, video games, movies, and cartoons.

This job doesn’t require previous experience or special skills – you just need to have the voice the company is looking for.

You can learn more about how to become a voice-over actor at How To Become A Voice Over Actor.

Answer online surveys

Not too long ago, one of the ways I made extra money to pay off my student loan debt was by answering paid online surveys.

You will not get rich from taking surveys, but it can help you to earn a little bit of extra money in some of the spare minutes that you may have throughout the day. Plus, you may get free items occasionally to review as well.

Companies will pay you to take surveys because they want to see what people think of their product and their company. They seek out real opinions from real people.

Here are some of the survey companies that are open to teenagers (along with their minimum age requirements):

American Consumer Opinion – Age minimum – 14 years old

Survey Junkie – Age minimum – 12 years old

MyPoints – Age minimum – 13 years old

Branded Surveys – Age minimum – 16 years old

Swagbucks – Age minimum – 13 years old

InboxDollars – Age minimum – 12 years old

Pinecone Research – Age minimum – 18 years old

User Interviews – Age minimum – 16 years old

Some of the above will even pay you to review music, play video games, or test mobile apps as a part of their research.

Sell items on Amazon

We have all heard of Amazon.

It is a website full of items sold by people like you and me.

In the first year that my friend Jessica’s family ran their Amazon FBA business together, working less than 20 hours a week total, they made over $100,000 profit!

You can learn more by reading How To Make Money From Home Selling On Amazon, such as answers to questions like:

How Jessica started selling on Amazon FBA

What exactly Amazon FBA is

How to choose what to buy and sell

How much a person can expect to earn

The positives of selling on Amazon, and more

Customer service support

If you are looking for a more traditional style of online job, such as working for someone else, then finding a customer service representative job may be something to look into. This way, you can start earning money right away, right after you get hired, instead of attempting to build a business.

There are many companies that hire for customer service support at home, even if you are young. Most will want you to be at least 16 years old or 18 years old to start.

As a customer service representative, you may be responsible for tasks such as:

Answering questions from customers about a product

Troubleshooting and helping with issues that a customer may have with a product

Processing orders

Assisting with returns

Handling feedback and customer complaints

And so much more.

Virtual assistant

As a virtual assistant, you would be helping a person or small business owner with administrative and business tasks. You would be their assistant but working in your own home instead.

I have been a virtual assistant in the past, and I now have virtual assistants of my own. They are lifesavers!

You do not need to have previous experience in order to start as a virtual assistant, instead, you need to be willing to learn so that you can help a business run more smoothly.

Many, many people and companies are looking for virtual assistants, as they play such an important role.

As a virtual assistant, you may be able to start at around $15-$20 an hour, or even much more. This will depend on the type of work you are providing, the experience that you have, the field you will be working in, and more. As a full-time virtual assistant, you may be able to earn over $10,000 a month once you gain experience.

As a virtual assistant, you may be doing tasks such as:

Managing a company’s social media accounts, such as by being their social media manager

Managing a person or company’s calendar

Scheduling appointments or travel

Creating or assisting with slideshows or presentations

Email management

Communicating with clients or customers

And so much more.

Different companies and employers will need different work to be done – it simply depends on who you will be working for and what they need to be completed.

You can learn more at How I Earn $10,000 Per Month From Home as a Virtual Assistant.

Start an online store

I feel like so many young adults are starting online stores, and it completely makes sense.

It’s something you can do from home, and there are ways to do it that don’t involve storing inventory or taking up a large amount of your valuable time.

Plus, you can make extra cash or even a full-time income.

And, there are so many different things that you can sell online.

From pet items, skincare, fitness products, subscription boxes, and accessories, to clothing, crafts, and more, the list is endless.

You can learn more about this topic at How I Make Over $10,000 Monthly With My Online Store In Less Than 10 Hours Per Week.

Write an ebook

Yes, you may be able to make extra money as a teenager by writing an ebook, and you can do it all from your home.

Anyone can write an ebook, no matter how young you may be.

There are many different genres that you can choose from, such as fantasy, fiction, nonfiction, mystery, and more.

If this is one of the online jobs for teens you’d like to learn more about, read How I Make $200 Each Day In Book Sales.

Find online tutoring jobs

Are you looking for a flexible side hustle as an online tutor?

If there is a subject that you are knowledgeable in, such as math, English, science, etc., then you may want to see if you can find students that you can tutor.

To become an online tutor, you can simply create a tutor profile on a tutoring platform, create a listing on Fiverr, reach out to people that you know, and more.

Learn more at The Best Online Tutoring Jobs – A Flexible Way To Make More Money.

Freelance write

Becoming a freelance writer can be a great online job for teens because there is a growing number of jobs out there for freelance writers, and many people start with no previous experience.

A freelance writer is someone who writes for a number of different clients, such as a website, blog, magazine, and more.

You can learn more in the article How To Become A Freelance Writer.

Proofread

If you have a passion for reading and often find mistakes in written content, then you may want to learn how to become a proofreader.

Freelance proofreading is a flexible and detail-oriented job that only requires a laptop or tablet, an internet connection, grammar skills, and a good eye for finding mistakes.

Proofreaders look for punctuation mistakes, grammar, misspelled words, lack of consistency, and formatting errors.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

Tips for online jobs for teens

Below, I want to share some tips for you on how to manage an online job for high schoolers. Having an online job as a teenager means that you may have some questions, such as how to avoid scams, how to balance school and work, how to open a PayPal account when you are underage, and more.

How to avoid online job scams

While there are many, many legitimate online jobs for teens, there are scams as well. Due to that, I want to share my best tips so that you can avoid scams but still find an online gig.

Some of my tips to avoid scams:

Research the company and the position to make sure they are real and a company that you would like to work for.

Search on the Better Business Bureau to learn more about the company and read their reviews.

Research the company online to see if there are any mentions of it being a scam. I like to type in “Company name + Scam” into a search engine and see what pops up.

Always be careful if the company asks you to pay money.

Before you give out any personal information, such as your social security number, you should make sure it is a real job that they are offering you.

Search the Federal Trade Commission and see if they have any press releases or articles about work-from-home job scams that they may have found.

Never click on any links or download anything in a suspicious email.

And, always trust your instincts! If something seems fishy, then trust yourself. There are always other jobs out there – do not feel like you have to take one that you are unsure about.

Simply move on and look for another opportunity that fits you.

Frequently Asked Questions About Online Jobs for teenagers

Below are common questions about online jobs for high schoolers.

How can a student work from home?

If you are a teenager, then you may still be in school. If you are trying to manage school and find a way to make money, then I do want to share some of my best tips.

After all, I have been in your shoes!

Working and going to school can be tough to manage.

Below is my advice for balancing both:

Realize what your motivation is for balancing both school and having a job. This is important because at times it will be hard to manage both, and thinking about why you are making yourself so busy can help to keep you motivated. You may even want to create a vision board so that you can look at it whenever things are tough so that you can easily remember what you are working towards.

Carefully plan out your school and work schedule. To balance school and work, then I recommend creating a carefully planned out schedule. This mainly only applies if you are in college or if you have control over the hours in your school day. This may include researching when the classes you need are offered and start trying to eliminate any gaps that may fall between your classes. Having an hour or two break between each class can quickly add up.

Bulk up your class days. If you think you can do it without overtiring yourself, then you may want to have as many classes together as possible in one day so that you are not constantly having to drive back and forth between school, work, and home.

Have a to-do list. I live and breathe by my to-do list. It helps me to not forget anything and to quickly realize that I have something to do (so I should stop procrastinating!).

Please head to 9 Ways To Successfully Balance School And Work to learn more.

How to open a PayPal account when you are a teenager?

If you are under the age of 18, then you will need a parent or a legal guardian to open a PayPal account. They would be the primary account holder, and you would simply be doing transactions through their account.

So, this means that you want to choose someone that you trust as they will have full access to the money that you are earning and is being transferred to your PayPal account.

How old do you have to be to work an online job? Can I work from home at 15? How can I make money at 17 without a job?

The age will vary depending on the job that you are looking to get.

How do you get paid with an online job for teens?

The way that you will get paid will depend on what you are doing.

If you are taking paid online surveys, for example, then you may get paid in rewards, a gift card, or even PayPal or check.

For more traditional jobs and gigs, you may be getting a paycheck every two weeks. If you are working for yourself, then you may be getting paid directly to your bank account.

How can I make money online as a teenager?

There are many ways to make money as a teenager, as you learned above. These include:

Blogging

TikTok creator

YouTuber

Reseller

Printables creator

Sticker maker

Canva templates designer

Voice-over actor

Survey taker

Amazon seller

Customer service representative

Virtual assistant

Online store owner

Author

Tutor

Freelance writer

Proofreader

And the list goes on and on!

Whether you are looking to make extra cash or if you are looking for a full-time job, there are many ways for you to earn money as a teenager.

Lastly, my final piece of advice is to make sure that your parents are informed of what you are doing. For your safety, I highly recommend telling your parents about your online job and keeping them updated about what is going on and if there are any changes.

Are you looking for the best online jobs for teens?

The average mortgage lender is quoting a top tier 30yr fixed mortgage rate that is nearly a quarter of a percent lower than the same scenario last Friday. Granted, big moves like this are more common after hitting multi-decade highs, but today’s example has other motivations.

Specifically, the outbreak of the Israel-Gaza conflict prompted some excess demand for safer haven assets like US Treasuries and mortgage-backed securities. Perhaps more importantly the conflict creates geopolitical uncertainty that is seen as one more reason for the Fed to “wait and see” when it comes time to decide whether to hike rates one more time in 2023 or not.

Last but not least, today’s rate movement was bigger than it otherwise might have been due to the bond market holiday. Most mortgage lenders did not update their rate offerings yesterday, thus facing the need to account for an additional day of global events. Frequently, this wouldn’t matter, but things are different when global events are having a big impact.

Regardless of the new motivations behind today’s rate rally, old motivations are still important. Specifically, if economic data falls far from expectations in the coming days, rates would likely react–especially for Thursday’s Consumer Price Index (CPI).

Downsizing from a big house to a smaller dwelling is a rite of passage for retirees hoping to simplify their lives and shore up their nest eggs. But it might no longer result in savings in today’s housing market.

Industry-leading lender Movement Mortgage will become an “early adopter” of FICO Score 10 T, the updated credit scoring model designed to take advantage of trended data information to help expand mortgage approval rates.

Movement will employ FICO 10 T “to analyze their non-conforming loans, in conjunction with the classic FICO Scores,” the company said in a joint announcement with FICO.

“As a first-in-market user of FICO Score 10 T, Movement Mortgage and FICO will work together to share early-use insights for non-conforming products to help the mortgage industry understand the benefits of the most predictive credit score in the space.”

FICO originally released 10 T in 2020, saying that the new model allowed for lenders to have greater precision in making lending decisions through the incorporation of trended credit bureau data. The word “trended” is the source of the “T” in the 10 T name.

FICO claims that the 10 T model can “expand mortgage approval rates by up to 5% relative to versions most commonly in use today, without adding incremental risk.”

“Movement Mortgage’s adoption of our new credit score model is an industry-leading first step to showcasing the comparisons between classic FICO Scores and FICO Score 10 T for optimizing mortgage originations,” said Jim Wehmann, EVP for scores at FICO.

Jason Stenger, COO at Movement Mortgage, said in a statement: “We are looking forward to implementing FICO Score 10 T for non-conforming loans and are eager to work with FICO to help more consumers qualify for mortgages, while highlighting the advanced credit risk capabilities of the new scoring model to the entire lending ecosystem.”

In late 2022, the Federal Housing Finance Agency announced that it would replace the Classic FICO credit model, which Fannie Mae and Freddie Mac have relied on for nearly 20 years, with the FICO 10 T and VantageScore 4.0, a competing model that also incorporates trended credit bureau data.

The original implementation timeline for FHFA to incorporate the updated models was for FHFA to gather industry feedback in the second quarter of 2023, publish Classic FICO data to support the credit report update in the fourth quarter of 2023 and ultimately move to a bi-merge system from a tri-merge system in the first quarter of 2024.

Earlier this month, however, FHFA delayed the transition to a bi-merge system due to concerns expressed by stakeholders and members of the U.S. Congress. Instead, it will offer additional opportunities for public engagement as it considers the transition to updated credit score models and credit report requirements for loans acquired by government-sponsored enterprises (GSEs).

Mortgage financiers Fannie Mae and Freddie Mac were deemed “adequately capitalized” as of March 31, according to a statement released by the Office of Federal Housing Enterprise Oversight today.

However, it should be noted that the OFHEO recently lowered the capital surplus requirement from 30 percent to 20 percent, reflecting the pair’s remediation efforts and capital raising measures.

As of the end of the first quarter, Fannie Mae’s surplus over the newly designated capital requirement was 13.5 percent, up from 9.3 percent as of the end of 2007.

But taking into account the 10 percent decrease in the OFHEO-directed requirement, Fannie’s capital surplus actually declined, which the regulator attributed to credit-related losses.

Freddie Mac’s surplus based on the new capital requirement stood at 18.5 percent above the limit, up from 10 percent at year-end.

Fannie Mae’s core capital of $42.7 billion exceeded the OFHEO-directed minimum requirement by $5.1 billion, while Freddie’s $38.3 billion was $6 billion in excess of the new requirement.

Because Fannie Mae raised roughly $7.4 billion in fresh capital on May 19, the OFHEO has further reduced its capital requirement to just a 15 percent surplus.

The same will be true for brother Freddie Mac following its announced $5.5 billion capital raise, assuming no safety or soundness issues abound.

“The efforts by both Fannie Mae and Freddie Mac to raise new capital, their commitments to maintain overall capital levels well in excess of the requirements, and appropriately reserve for credit risks, positions them to fulfill their mission and support the mortgage market during these stressful times,” the OFHEO said in a statement.

The two companies are classified by the OFHEO as adequately capitalized, undercapitalized, significantly undercapitalized or critically undercapitalized.

Shares of Fannie were off $2.20, or 8.56%, to $23.51, while Freddie shares slipped $1.76, or 7.35%, to $22.20 in late trading Monday.

Well, the U.S. Department of Housing and Urban Development (HUD) finally released its long anticipated annual report to Congress today, revealing the need for more changes to stay financially independent.

The actuarial study found that the capital reserve fund, which supports the FHA’s single family mortgage and reverse mortgage insurance programs, fell below zero, to -1.44%, representing a negative economic value of $16.3 billion.

The FHA continues to be hurt by seller downpayment assistance loans, which allowed borrowers to buy homes with nothing down, and really, nothing at all out-of-pocket. We’re talking no costs loans on steroids.

Clearly this was a terrible and completely irresponsible way of doing lending, and it has rattled the FHA’s finances year after year.

These loans, which were originated between fiscal years 2007 and 2009, have resulted in about $70 billion in losses for the FHA.

Additionally, the low mortgage rates are also hurting the FHA because of the rapid rate of refinancing among FHA borrowers, though only on a short-term basis.

Essentially, it costs the FHA money when borrowers refinance their mortgages to lower market rates, at least in the near term. However, over time this should help their expected default rate as borrowers will have more manageable payments.

Along with that, FHA borrowers who aren’t able to refinance to today’s extraordinarily low rates will be more inclined to default, thereby increasing losses from projected foreclosures.

The FHA also blamed less favorable home-price appreciation forecasts used for this latest study, and noted that their methodology for predicting losses also hurt the economic value of the insurance fund.

No Treasury Draw Needed, Yet

Despite all this, HUD said it doesn’t need to call on the Treasury for a bailout just yet.

The need for a draw will be determined in the President’s fiscal year 2014 budget proposal, which will be released in February.

And in the meantime, the actuary behind the study believes the FHA’s fiscal year 2013 book of business will add $11 billion in capital accumulation.

Long story short, the FHA cleaned up its act a lot in recent years, and most of the loans it originates are of much higher quality.

This is partially because of a shift in borrower demographics, as more creditworthy borrowers turned to the FHA after conventional lending became more stringent and harder to come by.

Still, the FHA endorsed roughly 734,000 purchase mortgages over the past year, including 78% to first-time homebuyers.

Additionally, the FHA insured about half of all home purchase mortgages to African American and Hispanic/Latino borrowers.

More Expensive FHA Loans in 2013

And now the bad news, for prospective homeowners. Beginning in 2013, the FHA will raise the annual insurance premium paid by borrowers on new FHA loans by 0.10%.

It’s not a lot, but it will add an additional $13 per month to the average borrower’s mortgage payment. And premiums have already increased several times in the past year or so.

In other words, new borrowers will continue to pay for the irresponsibility of past years, but if you want to put down just 3.5%, they’re the only game in town.

On top of that, the FHA plans to reverse a rule that allows borrowers to cancel mortgage insurance premiums after only five years, despite the fact that the underlying loans are still insured for the full term of 30 years.

The agency will also shore up losses by continuing to sell pools of defaulted mortgages, those sailing toward foreclosure, with a commitment to sell at least 10,000 per quarter next year.

They will also expand the use of short sales and revise their loss mitigation program to “target deeper levels of payment relief.”