This article is part of a series put together by the Total Mortgage marketing team that provides loan officers and other sales professionals with a crash course in marketing and self-promotion. To read other articles in this series, click here.

This article is designed to teach loan officers and other sales professionals how to properly maintain and boost their social media presence. It will hit all the key points such as connecting, managing multiple profiles, engaging with influencers, and what to post.

Want to jump ahead?

LinkedIn

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Facebook

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Twitter

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencer

How and What to Post

Google +

Connecting & following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

LinkedIn

How to Gain/Find Connections

When you first started setting up your LinkedIn account, you were prompted to import your contacts from your email address book. If you clicked yes, you probably already have a few dozen connections. However, once your profile is completed, you will need to search for those connections you didn’t have on your contact list, like loan officers you met at a conference or realtors you haven’t had a chance to work with yet. There are many different ways to go about finding and linking with connections on LinkedIn.

The first way is arguably the easiest way: using the Search box. It can be found on the top of any tab of the LinkedIn interface. There are also many “Advanced Search” options available if you click the “Advanced” text link right next to the search button.

You could also find connections from clicking onto your Profile, scrolling down to your experience and hovering over your business place icon and then clicking onto the icon or your company title, highlighted by the red arrow.

After clicking on your company’s icon, scroll down until you see the “How You’re Connected” on the right side of the screen. Click “See all.”

Now you have the opportunity to see coworkers and contacts who you’re not connected to.

Managing Multiple Profiles

LinkedIn is generally a place where you focus on one personal profile. However, if you run your own business, you will want to create a company page for it. If you need help creating a company page, check out my Social Media Basics post. If you only manage one page, then this section may not be that useful.

If you are on your profile page and you want to switch to your company page, you simply click on the small icon on the top right hand corner of your screen (where the arrow is shown) then on “Company Page.”

This will lead you to this screen.

You’ll now be able manage, change, analyze, and update your company page. If you want to switch back to your profile page, just click on the home tab or profile tab.

Engaging with Influencers

Connecting with influencers—that is, the people who are active, established, and popular in your industry—is a great way to widen your reach. Of course, engaging with influencers on LinkedIn is not something you should do blindly. It takes strategy and time to do correctly.

Do Not:

Do not connect with an influencer without ever interacting with them

Do not like, comment, or share everything they post

Do not post more than 3 times per day

Do:

Do connect if you had previous relations

Do connect if you are connected on other networks

Do connect if you have exchanged emails or contact info

How and What to Post on LinkedIn

Posting on LinkedIn is very straight forward. LinkedIn allows you to share updates, publish a post, upload a photo, share in groups, and post job opportunities. You can access these options in the home tab, except for sharing in groups and posting job opportunities.

Sharing in a Group

Sharing in a group could be a great way to get your content to a broader audience. Joining groups on LinkedIn is very easy. First, click on the “Interests” tab and then click on “Groups” If you are already a member of a group it will appear under the “My Groups” section. If you aren’t a member of any groups, just click on the “Discover” tab and LinkedIn will provide recommendations for groups to join. You have the option to select “not interested,” “ask to join,” or you can ignore and continue to scroll.

Once you ask to join a group, your request must get approved by an admin, which can take a day or two depending on how busy they are. After you’re accepted, you can view what the others in the group are posting. To get started, click on “Start a conversation with your group.” The box will expand and you get the options listed below. At this screen, type in your title and a brief description with a link to the real content. Follow the same process for posting a job opportunity in a group.

If you run a LinkedIn business page, then you have the option of posting a job ad through the “Business Services” tab. Once you hover over “Business Services,” click on “Post a Job” to get to this screen.

After you fill out the appropriate information and click “Start job post,” LinkedIn will walk you through a series of prompts, where you will fill out information like job function, company industry, and job description. Once that’s done, review everything and click submit.

What to Post:

Career status updates

News and events

Articles shared by your connections

Your own articles

What not to Post:

Quotes

Updates trying to sell services/items

Material you deem not appropriate for the workplace

Facebook:

How to Gain Followers:

With more than 1.65 billion monthly active users, Facebook has the potential to connect you to people across the globe. If you’re using Facebook for business purposes, you need to understand how to properly navigate it to connect with others.

There are multiple strategies to take. For example, you can create a personal account, a business page, or both. If you’re in an industry where you need to keep things professional (like, for instance, the mortgage and financial industry), then I recommend creating a business page so you can separate your professional life from your personal life. You have to mindful of whom you invite to like your page, but we’ll touch on that topic a little later.

If you’re completely new to Facebook, prepare to spend some time connecting with people you know. You can manually add friends by clicking in the search box at the top of the screen and typing the name of the person you are trying to find. Eventually Facebook will tailor a carousel of “People You May Know,” which will allow you to click “Add Friend.” Thankfully, Facebook has implemented a few tricks to make it easier to add friends in bulk.

Go to the Friends Request page then to the “Add Personal Contacts,” enter your email and click find friends.

After you enter your email it will take you through to a similar screen. Click “Agree,” then follow the on-screen instructions.

On the Go

You can also import contacts from your mobile device.

Tap

Hit “Find Friends” in the Apps section

Tap “Contacts,” then follow the on-screen instructions

Connecting to Others Via Your Business Page

Click on the triangle in the top right corner of your home page.

Click on the drop down menu and select your business page.

Click on the […] on your cover photo and then click on “Invite Friends.”

Search all friends: click the invite box next to your friends’ names to invite them to like your page—or type their names in the search box.

Managing Multiple Profiles

Facebook does a fantastic job of making it easy to manage as many pages as you want. Their interface organizes your pages so you can easily switch through and manage every single of one of them. Every time you create a new page, Facebook allows you to add that page into your “Favorites” section. I highly recommend doing this, because it keeps all of your pages in easy reach, which you can see in the image below.

You can also switch between pages by clicking the drop-down triangle on the upper right corner of your home page. In that menu, you’ll find a list of three of your pages. Shown below:

If you manage more than 3 pages—like we do here at Total Mortgage—you can just click on “See More…” and it will give you a list of all the Facebook pages that you manage. To switch back to your personal page, you simply just need to hit the “Home” button and it will take you back to your feed.

Properly Engaging with Influencers

Recently, Facebook has changed how you interact with other people or businesses when you’re on your business page. Once, you were able to be on your business profile, click on “Home” and interact with people and businesses that follow your business page. However, that is essentially nonexistent today. Now you really need to be creative if you want to engage with influencers in your community.

To Like a Different Page as Your Business Profile

Go to the page you want to like and click on the […]

Click “Like As Your Page.” Then this screen will pop up and you choose the business account that you want your like to come from. Click “Save.”

Tagging other influencers in your Facebook posts is simple if you know the name of their business page. A lot of influencers have both personal and professional profiles, however, so make sure you know which one you’d like to connect with.

Unfortunately, you can’t tag a personal account from your business profile. If you want to tag a professional account from your business page, you craft your post, then add the appropriate tag at the end. You always want to convey that you got the content from a source and you are using it credibly.

In the picture below, you see that I have crafted a draft of my message and tagged the source I got it from with the tag “via @[name].” Instead of via you could use from, by, thanks to, etc. When possible, try to use a link shortener such as Buffer or Hootsuite to keep things looking tidy.

Once you get the proper etiquette down for interacting with influencers, now it’s time to engage with them. Like I mentioned above, you can like other pages as your page. You are able to do the same for posts. You do that by going to the page you want to like something on and scrolling to the post that you want to interact with. Before you like the post or comment, make sure you switch from your profile to your business profile. You do this by:

1. Clicking on the downwards arrow next to your small Facebook default icon

2. Click on the account you want to like and comment as.

You are now liking and commenting as your business account. This is the best way you can engage with your influencers. There are 3 important things you must always remember to do and don’t do before you start engaging with influencers.

Do Not:

Do not like/comment on everything that they post

Do not ask for a favor like sharing a post right away

Do not reach out to them right away

Do:

Gradually interact with them by liking their page and commenting on a few posts/pictures 1-3 times a week

Share some of their posts 1-2 times a week

Always remember to thank them for sharing information that you find important

Here’s where you use your gut. Once you think you’ve earned yourself a spot on the influencer’s radar, the next step is to reach out personally. This can be done in an open forum through commenting, or it can be done through private message. The eventual goal is to take the conversation “offline” through either phone or email so you can begin building an even more personal relationship.

How and What to Post on Facebook

Posting and sharing on Facebook is very easy. If you have a personal Facebook, you already know the drill. If this is your first time on Facebook or you don’t know how to post to your business page, then keep reading.

Posting on Your Personal Page

Bring your mouse to the top tab and click on your name

Click on the box where it says:

3. Click on the kind of post you want to craft: status, photo/video, or life event. Finish typing it with the appropriate tags (if needed) and click post.

Posting on your Business Page

Make your way over to your business page

Click on the box where it says “status, photo/video, or life event” and create the post you want to send out

When you are finished, click “Publish”

What to Post on Facebook

There are two types of content that you should post on Facebook. The difference depends on what account you plan to post with. For both profiles, you should post content that really resonates with your audience and makes people see you as a credible source (i.e. if you’re a loan officer, try content based around changes in the industry or tips on how to make the mortgage process easier).

Content like this positions you as an authority and encourages your audience to consider using your services if they are shopping for a home or refinancing. Every once in a while, it’s okay to throw in a shameless plug, whether you’re asking for referrals or encouraging people to use your services. Your personal page can have all the other updates—photos of your family, your dog, things you’re passionate about, etc. It is ok to post some business topics on your personal page, but make sure to do so sparingly. Your personal page is meant for personal things.

Twitter:

How to Gain Followers

Twitter is a great place to gain followers based on things that you find interesting. You can use the search box to find other professionals and people in your industry by looking for relevant hashtags, like #realestate.

Top Tips for Gaining Followers

Try finding your connections from other places like Facebook and LinkedIn on Twitter

Follow users who follow your followers

Follow the accounts recommended by Twitter

Join a Twitter chat

Managing Multiple Profiles

Unfortunately, Twitter doesn’t have an interface within itself to switch profiles easily—unless you are on your mobile device or want to use multiple web browsers. However, there are certain tricks, tips and hacks you can use to make managing multiple profiles easier.

Toggling Profiles in the Twitter App for iOS

From the “Me“ tab, tap the people icon

Tap “More options.”

From here you can “Create new account” or “Add an existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the people icon.

Toggling Profiles in the Twitter App for Android:

Tap the overflow icon

Tap “Accounts.”

From here you can “Create new account” or “Add existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the overflow icon, then tapping “Accounts.”

If you’re uninterested in downloading the Twitter app for your mobile device, there are other options. If you manage more than one profile you can easily manage multiple accounts if you use a tool like Tweetdeck, Buffer, or Hootsuite. All of these applications have free versions, so you don’t have to worry about spending money.

These apps make it easy to manage countless amounts of accounts. My personal favorite of the three is Buffer, because the interface is very easy to use and it provides multiple tabs to check out how your account is doing in terms of analytics. It also has a built-in link shortener that automatically shrinks your links when you are adding them to a post. Shown below is a screenshot of my Buffer interface.

Engaging with Influencers

Engaging with influencers on Twitter is a great way to kick-start your influencer marketing strategy. This is where Twitter search comes in handy; you can use it to find the people who tweet regularly in your industry regularly. If you want to stay organized, I recommend creating a spreadsheet that has a list of your influencers, their names, follower count, and what stage of your relationship you’re in. Once you’ve found a handful of them, it’s time to start engaging.

Do not:

Tweet, retweet, or like everything that they tweet

Try to directly reach out to them—it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally tweet, retweet, or like their posts to get on their radar

Appreciate their content by tweeting it out to your audience (and making sure your attribute the author)

Once you established a relationship, make it easy for them to tweet about your service by crafting an email with a few sample tweets that they could send out about your services. Make sure you convey the message that you are willing to reciprocate the favor

How and What to Post:

Posting on Twitter is very simple. If you are on the web browser version of Twitter the tweet box is one of the first things that you see. You can find it by looking for the “What’s happening?” text.

To compose a tweet you just click on this box and type the content you want to share.

Posting a Tweet on a Mobile Device

Tap the compose Tweet icon accessible from your Home timeline, the Notifications tab, or your profile (usually located on the upper right hand of your screen.)

Start typing where it says “What’s happening?”

If you’d like to Tweet an image, tap the camera icon

Tap “Tweet” to post.

What to Post

Just like any other platform, choosing what to post comes down to a few key factors.

Who your audience is

What kind of message are you trying to portray

What kind of content will resonate with that audience

Make sure you don’t forget to utilize the power of hashtags on Twitter. To see how a hashtag is performing simply search the hashtag in the search box before you post the tweet or check it out on Tagboard.

You want to have the appropriate amount of hashtags to text ratio. Most marketers recommend using no more than 3 hashtags per tweet. However, if your tweet only contains 3 words, don’t hashtag them all. Finding the perfect mix of creativity and content is surely a challenge but once you find your niche you will be good to go.

Google Plus

Google+ is one of the most underrated social media platforms, but it could be a great asset to your strategy if used properly.

How to Gain Followers

Make Your Profile Look Good

I know, it sounds obvious, but a lot of people just use the default graphics that Google supplies. Make sure your profile looks good and is customized so you reach people in your niche.

Follow other Google Plus People

Just like other social platforms, you’ll need to work for your followers. You do this by following as many people as possible. There are multiple ways of doing this. If you are looking for people to connect with , search for something relevant to your industry like, for example, “Real Estate.” A list like below will pop up and you will be able to decide who what you want to follow, whether it be collections, communities, people & pages, or if you just want to view posts.

You can also follow people manually:

Click the People Icon on the left side of the screen

You should see a “Find People” option. Click on that

Go through the list of people and see who you want to add

You can add them to just your follower base or you can add them to relevant circles, such as “Realtors”

Join Communities

If you’re looking for the fast track way of getting your name in front of dozens, even hundreds of people at once, then you’re looking for communities. When you join a community, you are part of a much larger group of people who are interested in a certain topic. This is how you engage the right kind of followers.

Utilize Hashtags

With Google Plus know you can search content by words, phrases, and hashtags. Even though hashtags are more popular on Twitter, they work the same way on Google+.

Let’s say you hashtag a word or phrase in your post, i.e. #RealEstate. Thanks to that hashtag, your post enters a stream with hundreds of other posts with that same hashtag. Meaning, anyone watching that stream or looking for specific information centered on that topic will easily find your post.

Add a Google+ Badge to Your Website

If you have your own website, it’s a sin in 2016 to not have visible social widgets. These are clickable icons that take you right to your social media pages. They take the hassle out of finding your social pages, making it easier to gain followers.

Managing Multiple Profiles

Managing multiple profiles on Google+ is very simple if you add all your accounts to one email address. Once you associate all your different profiles to that one email address it becomes very easy to switch back and forth between the different profiles from the Google+ interface. Don’t forget—you can always use a social media management tool like Buffer to switch profiles simultaneously.

Switching Profiles:

Click the icon on the upper right hand corner (Note: Your icon will be different from ours)

Once you click on that icon it will release a drop down menu of all the other profiles you have connected to your account

Now you are free to switch through whichever profile you deem necessary

Properly Engaging with Influencers

Engaging with influencers is a lot like engaging with influencers on any other platform—you need a strategy and you need to find the right influencers.

Do not:

Plus one (+1) everything they share

Try to directly reach out to them–it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally +1, comment, and share their posts

Appreciate their content by sharing it in your communities

Share some of their posts 1-2 times a week

Thank them for sharing information that you find important

How and What to Post

Posting on Google+ seems a lot more complicated than it really is. Just keep in mind that you can post publicly, in a community, or in a group. To post you simply go to the page, community or group you want to post to.

Click on the pencil icon on the bottom right hand corner

Which will bring you to this screen

Here you type in the text of the message you want to draft in the ‘What’s new with you?’ section. If you are adding a link, click on the. If you want to add a picture (recommended) click on the camera icon. You can also add your location by clicking on the location pin.

What to Post

Just like any other network, you need to find your niche before posting blindly. Finding content that really resonates with your audience is half the battle. Like I said previously, try testing a few types of content to see what works best.

Don’t be afraid to use content with a lot of pictures like infographics. The more pictures the better. A very good post is a combination of clever content, great pictures and captive CTA’s (call to actions.) Once you find this balance roll with it and optimize your Google+ account to its full potential.

Thinking About Your Next Steps?

All of these social media platforms are great for connecting and getting your content out there. Each platform is a little different from the next, so don’t try to implement the same strategy throughout all of them. Finding your groove might take some time, but keep working towards it and tweaking your strategy to see what gives you the best results. Once you hit that sweet spot, roll with it.

You can learn more about what the Total Mortgage marketing team does for our loan officers by checking out other articles in this series, or by visiting our career portal.

Carter Wessman

Carter Wessman is originally from the charming town of Norfolk, Massachusetts. When he isn’t busy writing about mortgage related topics, you can find him playing table tennis, or jamming on his bass guitar.

Inside: Are you looking for a way to help your kids learn about money? If so, Cash App for kids is the ideal answer. This guide will teach you how to manage money simply by using apps.

Ever wondered why it’s crucial for your kids and teens to have a cashless payment option?

In this digital age, teaching money management skills early to our younger generation is vital.

Having features likeCash App for kids is a great way to introduce them to responsible spending. Not only does it provide a secure method for purchases without the need for carrying physical money, but it also serves as an excellent tool for setting spending limits and tracking budgeting habits.

Plus, it’s a win-win for parents and teens as you can visually monitor transactions while they enjoy a sense of financial independence.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is Cash App?

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

It offers a range of services including a free custom Visa debit card and the option to receive paychecks up to two days earlier.

Additionally, with the Cash App, users can instantly buy and sell stocks commission-free and even trade in bitcoin.

Can a child have Cash App?

Yes, a child can have a Cash App account if they are 13 years old or older. However, it requires parental approval.

Remember, this gives your child the opportunity to learn money management, but it also comes with the responsibility of overseeing their spending.

Why would kids need Cash App?

Well, we are moving to a cashless world. There are thousands of stores and restaurants that only offer cash. We learned this when our son went to an MLB baseball game with his middle school. No cash. Only debit or credit cards were accepted as well as Visa gift cards.

So, we needed to give our kids an introduction to modern, simple, and secure ways of money management.

Cash App might be the perfect solution. Another great option is Greenlight for kids.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

What are the benefits of using Cash App for kids?

Education: Cash App can be an effective way to teach your children about responsible money handling and the dynamics of a digital economy.

Control: You have the flexibility to set spending limits and disable certain features, ensuring responsible use of the application.

Security: Cash App’s encrypted connection adds an extra layer of security, keeping your kid’s transactions and personal data secure.

Emergencies and convenience: It’s an incredibly handy tool for sending cash to your kid during emergencies. No need to rush, just a tap on your phone, and you can send money.

What cash apps can 13 year olds use?

In today’s cashless society, it’s more important than ever for kids to learn how to manage money digitally.

Below are some alternatives to Cash App that serve well for 13-year-olds:

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

No bank account needed.

No fancy phone needed.

Affordable for all! Plus free trial!

Mobile setup is not user friendly.

No investing option.

$5.99 month or $3.33/month for 12 months

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Only able to spend what is loaded on Card.

Free CashApp debit card.

No maintenance or annual fees.

Not FDIC insured.

No parental controls.

Remember, each app has its own unique strengths and weaknesses. Do some research and try out a few to see which one best suits your teen’s financial needs.

How do I create a Cash App account for my child?

Teaching kids about money management is vital for their financial future.

One excellent way to do this effectively is by setting up a Cash App account for children, giving them practical experience in handling finances while under a parent’s supervision. Also, known as a sponsored account.

This guide will walk you through the process of creating a Cash App account for your child and highlight the numerous benefits it offers.

Step 1: Download Cash App

To download Cash App, click this Cash App link to make sure you are in the right spot. Both you and your teen will need to do this step.

It’s easily recognizable – look for the white dollar sign on a green background. Once you’ve found it, simply hit ‘Install’ and sit back while your phone does the work.

Remember, this green goodness is only accessible to users in the United States.

When learning which payment type is best when trying to stick to a budget, you will be pleasantly surprised at how well Cash App works.

Step 2: Create an Account

This is a simple process. Both the teen and the adult will need to do this step separately. If as the parent you don’t have a Cash App account, then you will need to do this step.

To create a Cash App account, follow these steps:

Once installed, open the application and follow the on-screen instructions to set up your account.

You will have to enter your phone number or email address.

For security certification, the Cash App will send you a secret code to verify you. Enter it.

Select a $cashtag, which is a unique username to send and receive money (similar to Venmo)

Step 3: Connect a Bank Account

For the parent account, you need to complete this step and the teen will need to wait.

Remember, in “My Cash” you’ll spot the “Add Money” option for funding.

Open Cash App; it’s the icon with a white dollar sign on a green background.

Tap the top-right profile icon.

Navigate to “My Cash” – it’s a tab on the home screen.

Click “Link a Bank,” nestled within the options.

Follow the prompts to add your bank account or debit card info.

Once your card is linked, you’re all set.

Learn where can I load my Cash App card.

Step 4: Authorization Request of a Family or Sponsor Account

Now, you must link the two accounts together. Cash App calls this a sponsored account. There are one of two ways to accomplish this.

Option #1 – Parents Initiate the Request

To invite someone 13-17, then open the app:

Tap the Profile Icon on your Cash App home screen

Select Family

Tap Invite a teen

Follow prompts to share links using text or email

Option #2 – By the Teen

On the Home Screen, tap the Cash App profile icon.

Proceed to Family Accounts and choose the option “I’m a Teen”.

Complete the Cash App for Kids application form with your details including your name and birthday.

Hit the Request Approval button.

Enter the name, email, phone number, or $CashTag of your parent/guardian.

Lastly, tap Send. This will send an authorization request to your parent or guardian’s Cash App account. They need to approve this request before you can start using the app.

Note: You can’t add funds, send payment, or request a Cash Card until this authorization is approved.

Step 5: Have Your Child Design and Order a Free Cash Card

Now, the fun part! Ordering your own Cash App Card.

Designing and ordering your Cash Card is packed with creativity and ease.

Customize your card to represent your unique personality, with choices ranging from the material, font size, and base design, to text lines.

You can seek inspiration from an array of cool Cash App Card design ideas. Notably, the glow-in-the-dark cards are quite popular among minors.

The whole process is about making your debit card unmistakably yours.

Step 6: Limitations on Certain Features

Certain financial apps cater to teens by setting limits on transactions.

For example, a teen on Cash App can send and receive up to $1,000 every 30 days. This safeguard is designed to prevent overspending and encourage smart budgeting practices.

Furthermore, parents and guardians have the option to impose their own customized spending limits through the app according to their teen’s financial maturity. However, it’s essential to keep in mind, that these apps are not recommended to be used by teens just like regular accounts due to the risks of misspending and overspending.

Be aware that certain transactions are blocked, including bars, dating services, and rental car services

Encourage your kids to use robust, unique passwords and activate features like PIN lock and facial ID to enhance security.

You can ensure safety by setting a PIN, turning on notifications, and limiting money requests to ‘contacts only’.

This is similar to understanding the advantages of mobile phones for kids.

Step 7: Pick a unique $Cashtag

Tell your child to select a unique and fun $Cashtag for their Cash App account. It’s like a username and can be used in transactions.

Emphasize the originality of the $Cashtag as it needs to be unique.

Expert Tip: To secure their $Cashtag, avoid using personal information like birthdate or social security number. Instead, opt for quirky, fun, and uncommon word combinations.

Step 8: Send & receive money

Cash App provides an easy-to-use platform for instantly transferring money between friends and family at no cost.

A few quick taps allow users to request, receive, or send money, presenting a convenient method for paying a dinner, settling rent with roommates, or any other financial interactions.

In addition, users get a free custom Visa debit card, which they can order directly from the Cash App for both virtual and physical use. The card enables users to make purchases from any merchant accepting Visa cards.

Plus, with the Cash Boost feature, users gain from immediate discounts at select restaurants, stores, applications, and websites when they use their Cash App card.

An Alternative – Use Greenlight Debit Card for Kids

Looking for an all-in-one alternative to the Cash App for your kids?

Explore the Greenlight Debit Card for kids – a superb choice for money management and financial education.

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track their child’s spending and saving habits.

Plus it offers 1% cash back on all purchases and up to 2% interest on savings, this card is accepted anywhere MasterCard is used and comes with built-in features that include educational programming and real-time notifications for every transaction.

Greenlight

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Pros:

Offers a comprehensive financial education pathway

Broad acceptance due to affiliation with Mastercard

Parents retain control over spending limits

Real-time notifications improve security

Cashback rewards are an added bonus

Cons:

Greenlight charges a monthly fee starting from $4.99

Limitations on direct deposits

No possibility for payments from Paypal, Venmo or Apple Cash

Kids under 13 require parental access

Some transaction types are blocked

It’s an innovative and secure financial platform for kids, with plans starting at $4.99 a month.

Safety Measures for Using Cash App for Kids

Educating children about safety measures while using cash apps and debit cards is crucial in today’s digital age.

With increased online scams, it’s important that kids understand the equivalence of digital cash to real money and how to protect their accounts.

This brief overview will highlight key practices to ensure your child’s safety when handling digital transactions.

1. Know the App’s Safety Features

Knowing the app’s safety features is crucial for maintaining security while using cash apps.

These features can include password protection, two-step verification, and biometric scans such as fingerprint or facial ID. Many apps also offer robust encryption to secure data and transactions.

Keeping abreast of the app’s safety protocols not only helps safeguard against potential scams but also instills a better understanding of digital literacy. Understanding these safety measures and functionalities can greatly lessen the likelihood of falling victim to fraudulent activities.

Make sure they don’t learn how to unlock borrow on CashApp!

2. Talk to Your Kids About Money

It is essential to talk to your children about financial literacy from an early age especially if your parents never spoke about money.

Start by making them aware of the concept of saving by using tools like a piggy bank and elucidate the value of delayed gratification.

As they mature, introduce them to the functionalities of debit cards and apps like Cash App that provide hands-on experience in managing finances. Teach them about budgeting, saving, and investing in an age-appropriate manner.

Above all, impart the message that money doesn’t just grow on trees and that every purchase needs to be evaluated against future needs and plans.

3. Use Account Alerts to Stay Up to Date

Account alerts on Cash App are not only handy but critical to your kid’s financial safety. Setting them up is a breeze.

Firstly, head to the “Notification” tab in your app settings.

Thereafter, opt for “Account alerts” and switch it on. This will ensure you’re notified of all transactions.

For an added layer of security, enable “Suspicious activity” alerts; this helps to flag any odd movements swiftly.

4. Set Up a Strong Account Passwords

It is crucial to ensure that your online accounts are secured with robust and unique passwords.

Complex passwords that incorporate a mix of uppercase and lowercase letters, numbers, and special characters can provide a strong line of defense against unauthorized access. Also, you should look at changing these passwords regularly, which further enhances security.

Using a password manager, either online or paper-based, can assist in maintaining and keeping track of different account credentials, maximizing security while minimizing the risk of forgetting passwords.

However, if opting for a paper-based version, it is crucial to store it in a secure and confidential location to prevent unauthorized access.

5. Have a Conversation About Scams and Fraud

The proliferation of digital transactions and cash transfer apps has given rise to numerous scams, making it critical for users to look out for fraud.

Online scams can result in financial loss, with cash apps often not assisting in the recovery of misdirected funds due to errors or fraudulent activities.

Additionally, cybercriminals use these scams to steal personal data, leading to issues like identity theft and fraudulent transactions. Furthermore, the anonymity of digital platforms enables scammers to disappear without a trace after executing a scam, sometimes befriending and exploiting minors.

Therefore, everyone must stay vigilant about potential scams to protect their money, personal information, and overall digital safety.

Key Tips to Watch for:

Discuss current scams happening. Use reliable resources to educate them about how fraud works and precautions to take.

Teach them to *slow down* during transactions to avoid sending money to the wrong contacts.

Advise against sending money to strangers to avoid being scammed.

6. Check Bank Accounts for Any Unauthorized Payments

As a parent, it is essential to regularly check your teen’s checking accounts linked to their mobile wallet for unauthorized payments.

By staying vigilant, you can detect suspicious activity early and prevent possible instances of fraud.

Tracking their spending patterns also helps you understand if they are managing their digital money wisely or if there are sudden changes in their spending habits.

Remember, it is better to be proactive in monitoring these accounts, as most money transfer app funds are not FDIC insured, making the recovery of accidental transfers or payments a challenging task.

7. Ability to Give Your Kids an Allowance

If you choose to do so, giving your kids an allowance on Cash App is a safe and effective way to teach them about responsible money management. It provides hands-on experience while putting the power of monitoring in your hands.

To set this up, simply create an account for your minor and periodically send money to it as an allowance. They can spend or save it, while you observe their spending habits.

This is a simple way for kids and teens to start managing a small amount of money.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Which cash app will you choose for your kids

To sum it up, equipping your kids with financial responsibility via Cash App or Greenlight is an intelligent move.

These apps provide a platform for learning about savings, investments, and the value of money.

Although risk exists its potential scams, with proper guidance, your teen can safely navigate this. The added perks of trading, direct cash exchanges, and options like BusyKid and Bankaroo can further enrich their financial literacy journey.

So, which digital wallet will you pick for your kid’s first leap into financial independence?

Know someone else that needs this, too? Then, please share!!

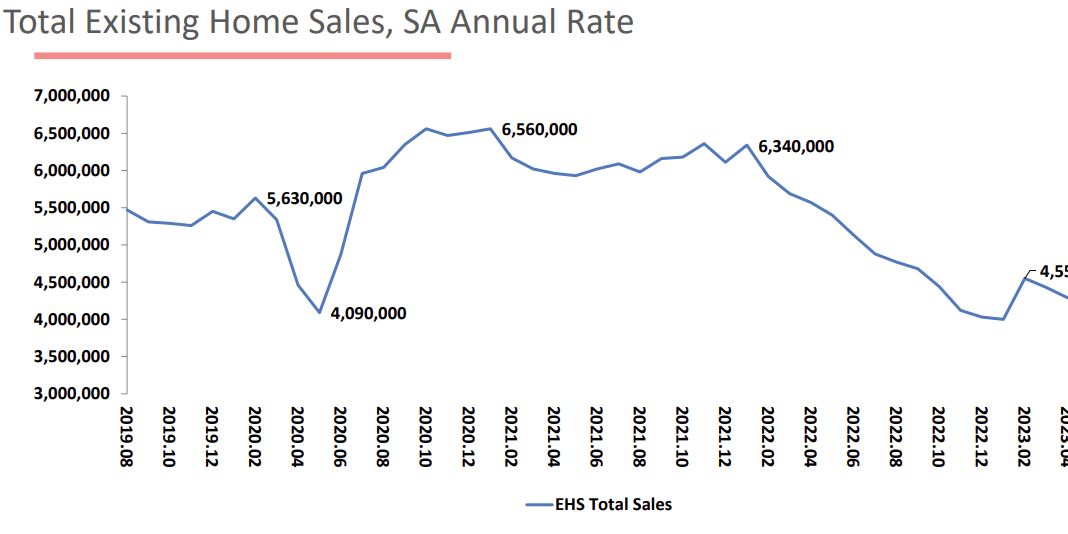

Existing home sales fell 0.7% in August from the prior month as higher mortgage rates lead to limited supply of homes for sale.

Sales fell to an annualized rate of 4.04 million units, below the pandemic low of 4.09 million.

“Home prices continue to march higher despite lower home sales. Supply needs to essentially double to moderate home price gains,” NAR economist Lawrence Yun said.

Loading

Something is loading.

National Association of Realtors, which shows that the post-pandemic rebound of home sales has been completely wiped out amid a period of elevated mortgage rates.

Existing home sales fell 0.7% in August from the prior month to an annualized rate of 4.04 million, below economist forecasts of 4.10 million and below the pandemic-era low of 4.09 million.

The ongoing decline in US existing home sales began in 2022, when the Federal Reserve started to aggressively hike interest rates in its quest to tame inflation.

Since early 2022, total existing home sales in the US fell 36% from 6.34 million to last month’s reading of 4.04 million. The decline accelerated as the average 30-year fixed mortgage rates steadily climbed above 7%, making the prospect of buying a home much less affordable.

Advertisement

Advertisement

But despite the decline in home sales, home prices are rising because of a limited supply of homes available for sale.

The National Association of Realtors said the median price of existing homes in August jumped 3.9% year over year to $407,100. Meanwhile, the inventory of unsold existing homes fell 0.9% to 1.1 million, which is equivalent to just 3.3 months of supply at the current pace of monthly home sales.

And the home price gains could keep accelerating as long as supply remains limited and buyers don’t balk at too-high mortgage rates.

“Home prices continue to march higher despite lower home sales. Supply needs to essentially double to moderate home price gains,” National Association of Realtors’ chief economist Lawrence Yun said.

Advertisement

Advertisement

The decline in existing home sales comes as homebuilder sentiment and US housing starts continue to decline. And with no Fed interest rate cuts on the immediate horizon, these trends could continue.

Home prices won’t drop, and could surge 15% once mortgage rates fall, Barbara Corcoran says.

There’s a shortage of homes for sale as people don’t want to give up their cheap mortgage rates.

The housing market is in good shape, and buyers will pounce once rates drop, Corcoran says.

Loading

Something is loading.

Good Morning America” this week.

In response to a massive inflation spike last year, the Federal Reserve has raised interest rates from almost zero to more than 5% since last spring. As a result, the average 30-year mortgage rate has surged from about 3% at the start of 2022 to 7.3% – the highest level since 2000.

Steeper interest rates encourage saving over spending and increase borrowing costs, meaning they typically pull down the prices of assets such as houses. However, home prices were down just 1% in May from their peak last June, the S&P Case-Shiller index shows.

Advertisement

Advertisement

Prices have been shored up by a shortage of homes on the market, in part because many owners are reluctant to sell and give up the low, fixed mortgage rates they’ve locked in.

Corcoran started to say that “all hell’s going to break loose” once the Fed cuts rates and mortgages get cheaper.

“Every buyer on the sideline is going to jump into the market as long as the interest rates come down to 5% or 4%, and houses are going to go up in price all over again,” she said. “I wouldn’t be surprised if they go up by as much as 10% or 15% when that happens.”

The Corcoran Group founder also said a lack of inventory has resulted in a third of homes selling above the asking price, and the average home being listed for only 20 days before it’s snapped up.

Advertisement

Advertisement

“The housing market is as strong as ever,” she said, although she noted it would be wise to wait until next year to sell.

“When all the buyers come off the sidelines, when interest rates come down, I’m going to get a lot more from my house than I would get right now,” Corcoran said.

The investor’s touted the health of the housing market before. In June, she suggested home prices could jump as much as 20% once interest rates drop by two percentage points.

She also dismissed concerns of a housing bubble in southern states such as Florida, arguing that people are speculating less and using more cash than debt compared to the mid-20 00s housing mania.

This morning (Europe time), I heard the sad news that my friend and former boss, Jim Marks, passed away. I was aware he was battling health issues the past few years, but had no idea it had gotten this bad. After meeting him during the #rebarcamp over a decade ago, his genuineness, intelligence, and warmth quickly won me over. After moving on from Zillow, I ended up joining him as Director of Marketing following my (nearly) year abroad. If there was one thing he was big on, it was the power of doing the work. As genuine and warm as they come, he epitomized caring. In fact, so much so that it became VR’s core differentiator–we cared more than the competition. And, it wasn’t a marketing charade.

Jim was a marketing legend in my book. Virtual Results (now owned/operated by Ryan Rockwood) was the first real estate website and marketing agency that built its company, brand, and reputation with performance-based results. At least that I’m aware of. The “measure (and prove) your results” mindset so many agents and brokers operate with today was a movement propelled forward by Jim.

I’ve worked for multiple owners/founders who are perfectionists; Jim was one of them. While I can’t say we saw eye to eye on absolutely everything, we did agree that striving for excellence was worth the fight and tradeoffs required to pull it off. From a 2011 blog post:

Reading [Steve Jobs biography] made me better understand Jim’s perfectionist nature when it comes to products. There are times where we’ll show him something, and his immediate reaction is “that’s crap” (not unlike Steve Jobs’ reaction to many early products shown to him by the Apple team). He doesn’t mean it’s literally crap, he means it can be better…and that we need to spend the time it takes to make it perfect. There are certainly tradeoffs; operating to perfection takes longer to ship and costs more money. But we believe it’s worth it.

On a personal level, I spent quite a considerable amount of time with Jim, his wife Lorraine, and their two vizslas at their gorgeous home on Top of the World overlooking Laguna Beach; the #marksshack he called it–as well as a couple trips out on their sailboat. He was a man of many talents, also a divemaster and expert racecar driver. I am so appreciative of having the chance to be part of their lives and thankful for their willingness to share it. My thoughts and prayers go out to Lorraine and family.

RIP, Jim. You warmed the hearts of so many and will be deeply missed.

The Federal Reserve’s recent interest-rate hikes may be affecting your wallet more than you think.

The Fed funds rate influences mortgage, credit-card, and auto-loan rates.

This means when the bank hikes rates, it becomes pricier to get a car loan or pay off credit cards.

Loading

Something is loading.

waged a war on inflation for over a year, and while price growth has been slowing amid the central bank’s interest-rate hikes, those hikes could be hitting your wallet.

Michelle Bowman, a Federal Reserve governor, recently said that multiple interest-rate hikes might be in store to bring inflation down to target levels, after 11 hikes in the past 12 meetings. But for many Americans, what do these rate hikes even mean, and how do they affect adults buying a home or paying off credit-card bills?

The Fed funds rate, with a target range now at 5.25% to 5.5%, is the rate at which banks and credit unions borrow and lend excess reserves to one another overnight, set by the Federal Open Market Committee. While the Fed rate itself is mostly directly relevant to banks, it acts as a benchmark for most interest rates that matter to consumers and businesses, including mortgage and credit-card rates.

From April 2020 to March 2022, the Fed funds rate was in the 0% to 0.25% range, which was implemented to stimulate economic growth and inflation after the start of the pandemic.

But to get the economy in a stabler position after inflation began to take off in 2021, the Fed hiked rates to increase the cost of credit, making loans more expensive. With higher borrowing costs, banks, consumers, and businesses may borrow less money. Because less money circulates throughout the economy, inflation — and the economy at large — tends to cool.

The rate also influences the market, as hikes often lead to drops in the stock market as investors become wary about businesses’ ability to expand profitably in an era when loans are more expensive.

Bank prime loan rates, the interest rates banks charge creditworthy customers, are typically about 3 percentage points higher than the Fed funds rate. The prime rate is the basis for mortgages, personal loans, and other major consumer loans.

Take auto loans as an example. Interest rates for two-year auto loans tend to be slightly higher than the prime rate, meaning auto loans have been between 3 and 5 percentage points above the Fed funds rate. As the Fed hiked interest rates, auto loans jumped from a pandemic low of 4.6% in October 2021 to a 2023 high of 7.5%. More than 14% of drivers couldn’t secure a car loan in June, according to the Federal Reserve, as lenders worried about rising balances and higher delinquency rates — while high interest rates and monthly car payments hurt consumers’ wallets.

Auto loans are now at about their highest point since 2007, in line with the Fed funds rate. They also remained rather stagnant during the Fed’s zero-interest-rate policy.

Credit-card rates, though much higher than the prime rate, have a similar shape. Amid the Fed’s rate hikes, credit-card rates have increased roughly 6% since January 2022, while the Fed funds rate has risen over 5%. Likewise, as the Fed kept rates near 0% at the start of the pandemic, credit-card rates stayed roughly constant. An analysis by WalletHub found the most recent 25-basis-point rate hike could cost credit-card users about $1.72 billion in additional interest charges over the next year.

In the short term, the Fed funds rate also affects Treasury yields, or the interest rate the government pays on its debt obligations. These yields influence how much consumers pay on real estate and equipment, as they set a baseline for other interest rates. These yields are determined by economic stability, interest rates, and geopolitical conditions.

The two-year Treasury yield is nearly identical to the Fed funds rate. During the height of the pandemic, both curves had a similar shape, with the Fed funds rate lagging slightly.

The 10-year Treasury yield less closely parallels the Fed funds rate but still has a relatively similar pattern. Over the past few years, the 10-year Treasury yield fell and rose roughly in line with the Fed funds rate, which suggests the long-term economic outlook is more or less improving.

Ten-year Treasury yields serve as a proxy for fixed-rate mortgages, which have trended about 2% to 4% higher than the Fed funds rate over the past decade. Mortgage rates typically move with shifts in 10-year Treasury yields. The 30-year fixed mortgage rate also changes with inflation — Fed rate hikes are done to slow inflation.

This means if you’re looking to purchase a home, a rise in the Fed funds rate indirectly pushes mortgage rates up, as the 30-year fixed mortgage rate hovers just below 7%. Those looking for a new home now have less purchasing power because of the Fed decisions and inflation. A WalletHub analysis found homebuyers with a 30-year fixed-rate mortgage would pay $11,160 more over the course of the loan than if they secured the loan before July, under the condition that the average home loan is $426,100.

For those looking to save money, certificate-of-deposit rates are another metric closely tied to the Fed funds rate. Ninety-day CD rates track almost identically to the Fed funds rate, meaning these CDs have paid higher interest rates as the Fed hikes rates.

Large corporations also are directly affected by higher interest rates, as the cost of borrowing money also follows the Fed funds rate. The yield on corporate bonds, which are issued by corporations to raise financing, has somewhat mirrored the dips and spikes of the Fed funds rate, particularly with companies that have the highest credit rating from Moody’s. This suggests that as the Fed raises rates, investors get bigger returns on corporate bonds. However, those higher rates for corporate borrowing could lead businesses to curtail investments in their operations.

All this is to say, the Fed’s decision to hike rates 11 times in the past 12 meetings may not yet show up at the grocery checkout, though such hikes have major effects on paying off credit-card debt, buying a home, and purchasing a new car.

A city that needs no introduction, Las Vegas is a glittering oasis in the heart of the Nevada desert. From its inception as a humble railroad stopover to becoming a global entertainment icon, Las Vegas has etched its name into the annals of history. Instantly recognizable for its neon-lit skyline, iconic resort casinos, and high energy, Las Vegas is where fantasy becomes reality. But what exactly is Las Vegas known for? Whether you’re looking to rent an apartment in Las Vegas or purchase a home in the area, prepare to uncover what makes this beautiful city what it is today.

World-class casinos

Las Vegas boasts several famous casinos that have become synonymous with luxury, excitement, and indulgence. From the Flamingo, the first major resort on the Strip, to the Bellagio with its famous dancing fountains, these casinos offer numerous gaming options, from slot machines and table games to poker rooms and sports betting. Each casino has its unique theme and atmosphere, transporting visitors to different corners of the world. Not to mention, the architecture, interior designs, and entertainment options, including live performances and celebrity chef restaurants, make Las Vegas casinos a haven for those seeking a one-of-a-kind entertainment experience.

Being a global entertainment epicenter

From residency shows featuring artists like Kelly Clarkson, Elton John, Adele, and Luke Bryan, to Cirque du Soleil productions such as “O” and “Mystère,” the city’s theaters and venues offer many different types of live entertainment. Beyond music and theater, Las Vegas has many attractions along or close to the strip, including the Bellagio Fountains, the High Roller observation wheel, and the Mirage Volcano. The city’s nightlife is equally renowned, with its vibrant nightclubs and bars drawing international DJs and partygoers.

Thrilling outdoor adventures

Las Vegas offers exhilarating outdoor adventures for those exploring the surrounding region. Within a short distance, visitors can go on desert excursions, such as off-roading adventures in rugged terrains, guided ATV tours through Red Rock Canyon’s stunning landscapes, or even dune buggy rides across the sand dunes of the Mojave Desert. For the more adventurous, opportunities for rock climbing, hiking, and rappelling in nearby canyons like the picturesque Valley of Fire provide a unique blend of adrenaline and breathtaking scenery. Additionally, the nearby Colorado River invites visitors to engage in activities like kayaking, paddleboarding, and even white-water rafting.

The Las Vegas Strip

The Las Vegas Strip is a world-famous thoroughfare stretching approximately 4.2 miles along Las Vegas Boulevard South. This iconic street features resort casinos, dazzling neon lights, and bustling crowds. Each resort along the Strip has its own unique theme, from the elegant Venetian with its intricate replica of Venice’s canals to the pyramid-shaped Luxor and the extravagant Paris Las Vegas. The Strip is not only a hub of gambling and gaming, but it also offers entertainment, from mesmerizing theatrical productions to world-class concerts by renowned artists.

Unique landmarks

Las Vegas has unique landmarks that contribute to its distinctive and iconic character. The famed Las Vegas Strip is a remarkable landmark, but there are many other attractions to check out. Some of which include the Neon Boneyard (which showcases a dazzling collection of vintage neon signs), the “Pawn Stars” Gold & Silver Pawn Shop, and the unconventional and artistic Container Park.

Fine dining

Las Vegas has established itself as a global culinary destination, offering an exquisite array of fine dining experiences. Renowned for celebrity chef restaurants, the city boasts a culinary landscape where innovation meets luxury. From the elegant and contemporary ambiance of Joël Robuchon at the MGM Grand to the sophisticated Italian cuisine of Carbone at ARIA, these establishments elevate dining to an art form. Notably, the Wynn and Encore resorts house a collection of fine dining gems, including SW Steakhouse and Wing Lei, the first Chinese restaurant in the U.S. to earn a Michelin star.

Fremont Street

Often referred to as the “original Las Vegas,” Fremont Street boasts a rich history dating back to the city’s early days, lined with vintage casinos, neon signs, and a distinctive retro charm. The renowned Fremont Street Experience, a massive canopy of LED lights, hosts dazzling light shows and concerts, immersing visitors in a visual display. The street is also home to some of Las Vegas’s oldest and most iconic casinos, including the Golden Nugget and Binion’s. Street performers and live music are common throughout all parts of the day.

Have you ever wondered what a 9-figure amount looks like? It’s a sum of money too big to ignore, with a whopping total of 100 million to less than 1 billion. Discover more about this colossal figure and the wealth it represents

When we mention nine-figure sums, we’re talking about a truly astronomical level of wealth. To put it in perspective, nine figures represent anything from $100,000,000 all the way up to $999,999,999.

This figure surpasses the GDP of several small nations. For instance, Samoa reported a GDP of approximately 843.8 million USD in 2021.

Or consider that according to Investopedia, 7-figure wealth is what puts you among the top 0.1% of the wealthiest people on the planet. This means that having nine figures puts someone at an even more elite level, one whose luxury extends far beyond mere financial freedom.

Only a small fraction of individuals or companies globally can boast such immense wealth. However, it is not an unattainable goal. Let’s take a look at some of the strategies you can employ to accumulate substantial wealth while also examining the lifestyles and pursuits of those who have successfully achieved it.

How Much Is a 9-figure Salary?

Table of Contents

A nine-figure income signifies any earnings that flaunt nine digits, starting from $100,000,000 and soaring upwards. To put it into words, we’re discussing one hundred million dollars.

Quite a mind-boggling figure, isn’t it?

It’s like being handed the keys to a kingdom of unimaginable wealth. But remember, this is a sphere occupied by only a select few worldwide.

Their playgrounds? Often, you’ll find them in the tech sector, inheriting vast wealth or expanding an already thriving family business.

Now, let’s delve a bit deeper, shall we?

When we speak of nine figures, are we referring to the lower end close to one hundred million, the middle ground around 550,000,000, or the staggering high end nearing 999,999,999?

So, the next time you find yourself daydreaming about a nine-figure salary, remember this: It’s not just a number; it’s a lifestyle, a testament to extraordinary achievements, and a beacon of exceptional success.

And who knows? With the right mix of passion, dedication, and a sprinkle of luck, you might just find yourself joining this elite club.

After all, isn’t the sky the limit when it comes to chasing our dreams?

Examples of People Who Earn 9-Figure Incomes

Cristiano Ronaldo: A Sports Icon – With an astonishing income of $105,000,000, this celebrated athlete is not just a football superstar but also a nine-figure earner.

Safra A. Catz: Leading Oracle – As the CEO of Oracle, Safra A. Catz’s leadership prowess is reflected in her staggering earnings of $108,200,000.

David Zaslav: The Discovery Dynamo – Captaining Discovery as its CEO, David Zaslav, commands a whopping $129,500,000.

Nikesh Arora: The Palo Alto Networks Powerhouse – As the CEO of Palo Alto Networks, Nikesh Arora’s genius is rewarded with a hefty paycheck of $125,000,000.

Roger Federer: Tennis Titan – This globally recognized athlete proves that sports can indeed yield nine-figure incomes, as evidenced by his impressive earnings of $106,300,000.

Case Study: What Does A 9-Figure Earning Look Like?

Understanding the intricacies of nine-figure earnings can be a complex undertaking due to the lack of universally defined parameters. For the context of this case study, we will consider an annual income of at least $432K as the lower limit for this category. It is worth noting that any figure below this threshold would classify one into the realm of billionaires.

Renowned business magnates such as Warren Buffet and Mark Zuckerberg exemplify this earnings bracket, with annual incomes reported around $51M and marginally less than $50M, respectively.

Reaching the stature of a nine-figure income earner typically necessitates either a substantial inheritance or proprietorship of a prosperous company with diverse revenue channels. The case of Elon Musk serves as a prime example, with his considerable income derived from two distinct sources – Tesla and SpaceX.

Aspiring for this scale of income undoubtedly sets a high bar. However, with the appropriate strategy and relentless determination, it is not beyond reach. Be prepared to tread a path akin to those who have already achieved this feat.

What Is the Potential Monthly, Weekly, Daily, or Hourly Income in the 9-Figure Range?

How Much Is 9 Figures Monthly?

To figure out the monthly income from a massive annual salary, just divide the yearly amount by 12. Keep in mind that this will give you a range of values. But if you want to earn a nine-figure salary, the smallest monthly income would be $8,333,333.33.

$100,000,000 per year / 12 months

= $8,333,333.33 per month

This question might take a different perspective if you’re raking in 9 figures every month. That means your annual income would be at least $1,200,000,000 or even more.

How Much Is 9 Figures a Week?

If we were to divide the 9-figure annual salary by 52 weeks, we’d be looking at a minimum weekly income that could make anyone’s head spin – a cool $1,923,076.9! 💸💼.

$100,000,000 per year / 52 weeks

= $1,923,076.9 per week

While you’re at it, if you manage to rake in a solid 9-figure sum every week, your annual income will soar to a minimum of £52,000,000,00 or maybe even more.

How Much Is 9 Figures a Day?

Want to know how much you can earn daily from a nine-figure income? Just divide it by 365! If you make money every day, your minimum daily earnings would be $273,972.6. That’s your ticket to the nine-figure club!

Here’s the breakdown:

$100,000,000 per year / 365 days

= $273,972.6 per day

Now, let’s say you take weekends and U.S. holidays off. In that case, you’d need to earn around $381,679.3 per day to make $100,000,000 per year. It’s a good goal to aim for if you want that nine-figure salary without burning yourself out.

How Much Is 9 Figures an Hour?

If you’re seeking a nine-figure income from hourly wages, the calculations are slightly different. Just divide your per day salary by 8 hours, and voilà! The minimum number is $47,709.90per hour. This calculation is based on working days – usually 262 days per year in the US.

How Much Is 9 Figures After Taxes?

Achieving a 9-figure income is quite an extraordinary feat, one that is typically reserved for the most successful entrepreneurs, athletes, and entertainers in our society. It’s almost impossible to reach that level through a single salary alone.

Instead, individuals in this income bracket often have multiple income streams, such as investments, business ventures, and other revenue-generating activities.

Calculating the exact tax on a 9-figure income can be a challenging endeavor. Taxes can vary greatly depending on many factors, including location, type of income, applicable deductions, and more. However, it’s safe to say that anyone earning in the 9-figure range will face a significant tax bill.

What Is the Pathway To Achieving a 9-Figures Income?

If you are in pursuit of a 9-figure income, it is essential to have an understanding of the components that fuel this elusive status. What sets apart these high-net-worth individuals from the rest is their capacity to create multiple streams of passive income and capitalize on them.

Here are some tips to help you achieve this milestone:

Acquire Valuable Skills and Experience

The first step towards achieving a 9-figure income is building a solid foundation of high income skills and experience in a high-value field. This could be anything from technology and finance to entertainment and sports. The key is to become exceptionally good at what you do, often necessitating years of dedication, learning, and practical application.

Build or Join a High-Growth Venture

Next, it’s super important to either build or get involved in a high-growth venture. This could mean starting a business with a game-changing idea or joining a rapidly expanding company in a leadership position. The aim here is to use your unique skills and experiences to create substantial value and wealth, which could potentially lead to a massive income if the venture becomes incredibly successful.

Invest Wisely and Diversify Your Income Streams

Who said you can’t have your cake and eat it too? Investing in the stock market, real estate, bonds, and other alternative investments is another way to generate a 9-figure income. It’s important to diversify your portfolio across multiple strategies so that you’re not overly exposed to any one asset class.

Let’s give you an example.

If you’re already running a successful business, consider investing in cryptocurrency or another digital asset class to increase your income streams. This could provide an additional source of passive income that can help solidify your journey to a 9-figure salary.

Equities and Derivatives Trading

The stock market is an incredibly powerful tool that can help you to achieve a 9-figure income. Through equity and derivatives trading, you can tap into the world’s most lucrative markets and make substantial returns on your investments in a short amount of time.

Learning how to navigate this complex ecosystem of risk and reward requires patience, dedication, and a lot of practice. Start by investing in the stock market or trading on a simulated platform to get comfortable with the process before taking it to the next level.

Leverage Networks and Opportunities

Networking is a critical component of achieving a 9-figure income. By cultivating meaningful relationships with influential people in your industry, you can open doors to opportunities that might otherwise remain closed. These could include partnerships, investments, or high-profile job offers that can significantly boost your income.

Jobs That Pay 9 Figures

Earning a nine-figure salary is an incredibly rare achievement reserved for the top echelons of various lucrative industries. Here are some of the highest-paying jobs and industries that can bring in nine-figure salaries.

Tech Company Bosses

Tech company bosses, particularly those at the helm of companies like Amazon, Facebook, and Tesla, are among the highest earners globally. Their compensation often comes in the form of stock options, which can value in the hundreds of millions or even billions when their companies perform well.

Examples include:

Elon Musk, CEO of Tesla ($242.4 billion)

Jeff Bezos, CEO of Amazon ($151.5 billion)

Mark Zuckerberg, CEO of Facebook ($103.4 billion)

Professional Athletes

In the world of professional sports, athletes like Cristiano Ronaldo, Lionel Messi, and LeBron James have managed to secure contracts and endorsement deals that push their annual incomes into the nine-figure realm. These athletes excel in their respective sports and have built strong personal brands, attracting lucrative sponsorship deals.

According to reports, these athletes earned more than $100 million in a single year:

Hollywood Celebrities

Hollywood is no stranger to nine-figure earners. Actors like Dwayne Johnson and Robert Downey Jr., thanks to their roles in blockbuster franchises, command massive salaries. Additionally, they earn significantly from endorsements, producing roles, and profit participation deals.

Media Stars

Media stars, especially those with a strong presence on digital platforms, can earn nine figures. For instance, YouTubers and influencers with millions of followers can generate substantial income from ad revenue, brand partnerships, and merchandise sales.

Hedge Funds & Investment Bankers

Investment bankers and hedge fund managers are some of the highest earners in the financial sector due to their expertise. Some notable examples include:

Ray Dalio, founder of Bridgewater Associates ($19.1 billion)

David Tepper, hedge fund manager ($18.5 billion)

Carl Icahn, founder of Icahn Enterprises ($10.1 billion)

Pop Superstars

The music industry has always been a lucrative field for successful artists. Pop superstars like Taylor Swift and Beyoncé have made fortunes from their music sales, concert tours, and endorsement deals. These musicians not only create hit songs but also build powerful brands that amplify their earnings.

Entertainment (actors, singers, dancers, etc.)

Performers in the entertainment industry, including actors, singers, and dancers, can achieve nine-figure incomes. Successful film actors can earn millions per movie while top-charting musicians make a significant portion of their income from touring. Broadway performers and dancers in high-demand shows can also command high salaries.

Top-notch Business Owners

Business owners, especially those who own large corporations or successful startups, can earn nine figures. This income comes from their business profits and, in some cases, from selling their businesses. Entrepreneurs like Elon Musk and Jeff Bezos have made billions from their ventures.

These careers represent the pinnacle of earning potential in their respective fields. However, it’s essential to note that reaching this income level requires exceptional talent, hard work, and often a good dose of luck.

Are 9-Figures Rich?

When we talk about money, figures, and digits start dancing in our heads. Six figures? That’s quite impressive. Seven figures? Now you’re playing with the big boys. But when we leap into the world of nine-figure incomes, we’re talking about a whole different ball game. It’s like comparing a kiddie pool to the Pacific Ocean!

A nine-figure income means someone is raking in between $100,000,000 and $999,999,999 annually. That’s right. There are more zeros in that figure than in a beginner’s Sudoku puzzle! This income bracket places individuals among the financial titans of the world. To put it plainly, if you’re earning nine figures, you’re not just rich—you’re Scrooge McDuck swimming in a vault of gold-level wealth.

But let’s be real, nine-figure incomes are as rare as a unicorn at a donkey convention. Even some of the world’s wealthiest individuals, like Bill Gates and Warren Buffet, didn’t make their billion-dollar fortunes overnight. It took years of smart decisions, a bit of luck, and probably a few sleepless nights.

And don’t forget, these ultra-wealthy folks aren’t waiting for a paycheck every month. Their wealth comes from various sources, including investments, real estate, and businesses3. They’ve got their fingers in so many pies; they could open a bakery!

What Does a 9-Figure Lifestyle Entail?

Living a 9-figure lifestyle is beyond the realm of what most people could even imagine. It involves not just extraordinary wealth but also the responsibilities and opportunities that come with it. Here’s a detailed look at what such a lifestyle might entail:

Extreme Luxury

A 9-figure lifestyle allows for some of the most opulent luxuries in the world. For instance, consider real estate: billionaires often own multiple properties around the globe. According to a report by Economics Times, the average billionaire owns 4 homes, with each worth nearly $20 million.

Traveling is another area where this wealth is evident. Private jet travel is commonplace among this group. The cost of owning a private jet can range from $3 million to over $90 million, not including the ongoing costs of maintenance, fuel, and crew salaries.

Philanthropy

Philanthropy is a significant aspect of a 9-figure lifestyle. Many ultra-wealthy individuals are committed to giving back to society. For example, Warren Buffett, one of the richest people in the world, pledged to give away 99% of his wealth to philanthropic causes.

The Giving Pledge is another example of this. Initiated by Bill Gates and Warren Buffet, it’s a commitment by some of the world’s wealthiest individuals and families to give away more than half of their wealth to solve societal problems.

Investments