When it comes to repaying your student loans, you may feel like a deer in the headlights. However, knowing the basics might make you feel more confident in your repayment strategy. Before repaying your student loans, take some time to learn more about your loan’s interest rates, principal, and type to inform your strategy.

Interest rate

The interest rate is the amount you pay your lender for borrowing money. Several factors affect student loan interest rates, including government legislation and the types of loans you choose. The higher the interest rate on a student loan, the more you’ll pay in interest over time. Many borrowers choose to consolidate their loans or pay off the loan with the highest interest rate first.

Principal amount

The principal amount refers to the money you borrow, not including the interest rate or other fees. For example, if you borrow $10,000 at 4.99%, your principal is $10,000. Due to interest, you’ll owe more than just the principal amount, but as you continue to make payments, the principal amount goes down.

Loan type

There’s more than one type of student loan. The two most common types of student loans are federal student loans and private student loans.

What kind of student loans do you have? If you’re not sure, your loan servicer can help you understand your loan types and the repayment options for your particular loan.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content. Communication of SoFi Wealth LLC an SEC Registered Investment Advisor SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

The world’s central banks have unleashed the steepest series of

interest-rate increases in decades during their two-year drive to tame

inflation—and they may not be done yet. Policymakers have raised rates by

about 400 basis points on average in advanced economies since late 2021,

and around 650 basis points in emerging market economies.

Most economies are absorbing this aggressive policy tightening, showing resilience over the past year, but core inflation remains elevated in several

of them, especially the United States and parts of Europe. Major central

banks therefore may need to keep interest rates higher for longer.

In this environment, risks to the world economy remain skewed to the

downside, as we detail in in our Global Financial Stability Report. Though this latest assessment of vulnerabilities is similar to what we

noted in April, the acute stress we saw in some banking systems has since

subsided. However, we now see indications of trouble elsewhere.

One such warning sign is the diminished ability of individual and business

borrowers to service their debt, also known as credit risk. Making debt more

expensive is an intended consequence of tightening monetary policy to

contain inflation. The risk, however, is that borrowers might already be in

precarious positions financially, and the higher interest rates could

amplify these fragilities, leading to a surge of defaults.

Eroding buffers

In the corporate world, many businesses suffered closures during the

pandemic, and others emerged with healthy cash buffers thanks in part to

fiscal support in many countries. Firms were also able to protect their

profit margins even though inflation had picked up. In a higher-for-longer

world, however, many firms are drawing down cash buffers as earnings

moderate and as debt servicing costs rise.

Indeed, the GFSR shows increasing shares of small and mid-sized firms in

both advanced and emerging market economies with barely enough cash to pay

their interest expenses. And defaults are on the rise in the leveraged loan

market, where financially weaker firms borrow. These troubles are likely

going to worsen in the coming year as more than $5.5 trillion of corporate

debt comes due.

Households too have been drawing down their buffers. Excess savings in

advanced economies have steadily declined from peak levels early last year

that were equal to 4 percent to 8 percent of gross domestic product. There

are also signs of rising delinquencies in credit cards and auto loans.

Headwinds also confront real estate. Home mortgages, typically the largest

category of household borrowing, now carry much higher interest rates than

just a year ago, eroding savings and weighing on housing markets. Countries

with predominantly floating rate mortgages have generally experienced

larger home price declines as higher interest rates translate more quickly

into mortgage payment difficulties. Commercial real estate faces similar

strains as higher interest rates have resulted in funding sources drying

up, transactions slowing, and defaults rising.

Higher interest rates also are challenging governments. Frontier and

low-income countries are having a harder time borrowing in hard currencies

like the euro, yen, US dollar and UK pound as foreign investors demand

greater returns. This year, hard currency bond issuances have occurred at much

higher coupon—or interest—rates. But sovereign debt concerns do not only apply to low-income countries, as the recent surge in longer-term interest rates in advanced economies has demonstrated.

By contrast, major emerging economies largely do not face this predicament

given better economic fundamentals and financial health, although the flow

of foreign portfolio investment into these countries has also slowed.

Material amounts of foreign investment have left China in recent months as

mounting troubles in its property sector have dented investor confidence.

Spillover effects

Most investors appear to have shrugged off mounting evidence that borrowers

are having repayment troubles. Along with generally healthy stock and bond

markets, financial conditions have eased as investors appear to expect a

global soft landing, in which higher central bank interest rates contain

inflation without causing a recession.

This optimism creates two problems: relatively easy financial conditions

could continue to

fuel inflation, and rates can tighten sharply if adverse shocks occur—such as an

escalation of the war in Ukraine or an intensification of stress in the

Chinese property market.

A sharp tightening of financial conditions would strain weaker banks

already facing higher credit risks. Surveys from several countries already

point to a slowdown in bank lending, with rising borrower risk cited as a

key reason. Many banks will lose significant amounts of equity capital in a

scenario where high inflation and high interest rates prevail and the

global economy tips into recession, as we explore in a

forthcoming GFSR chapter. Investors and depositors will scrutinize the

prospects of banks if their stock-market capitalization falls below the

value of balance sheet, causing funding problems for the weak bank. Outside

of banking system, fragilities are also present for nonbank financial

intermediaries, such as hedge funds and pension funds, that lend in private

markets.

Reassuringly, policymakers can prevent bad outcomes. Central banks must

remain determined in bringing inflation back to target—sustained economic

growth and financial stability is not possible without price stability. If

financial stability is threatened, policymakers should promptly use

liquidity support facilities and other tools to mitigate acute stress and

restore market confidence. Finally, given the importance of healthy banks

to the global economy, there is a need to further enhance financial sector

regulation and supervision.

Regarding acquiringSpecialized Loan Servicing for a purchase price of approximately $720 million, Nierenberg added that it “helps grow our third-party servicing business and reinforces our position as one of the leading nonbank mortgage servicers in the country.”

The company expects to close the deal in the first quarter of 2024.

To support its acquisitions, Rithm had $1.9 billion of total cash and liquidity at the end of the third quarter.

Challenging origination landscape

Rithm is working on a spin-off in the mortgage business, which includes origination and servicing. Nierenberg said the company “is not giving up on the mortgage company,” but is trying to figure out a cheap way to manufacture more capital.

Rithm, the parent company of Newrez, saw its mortgage business deliver a combined pre-tax income of $412.5 million in the third quarter, compared to $327 million the previous quarter.

Originations delivered only $7 million in profits, compared to $8.7 million in Q2. Mortgage volumes increased to $11 billion in Q3, higher than the $9.9 billion the previous quarter. Gain-on-sale margins improved to 1.28% in Q3, up from 1.23% in Q2.

Analysts at BTIG said the company’s volume in Q3 is comparable to the production at JP Morgan in the period and around half of what they expect from market leader United Wholesale Mortgage (UWM).

“We continue to think it’s likely benefited on the margins from Wells Fargo‘s exit from the correspondent channel this year, although it may be easier to see that appear in earnings if/when mortgage rates fall,” the analysts wrote in a report.

Rithm’s mortgage production is expected to be between $7 billion and $9 billion in Q4. According to the company, market conditions will remain challenging through 2024, and Rithm will continue to evaluate all operational processes to improve efficiencies and cost.

“We’re looking at our expenses; we’re looking at retail, clearly because that business doesn’t make any money right now when you think about volumes and cost to run that business,” Nierenberg said. “But overall, we’re happy with the asset that we have; we just have to figure out a way to generate more capital.”

Expectations for servicing

Loan servicing contributed $444.5 million in profits during Q3, compared to $357.3 million in Q2.

The company’s mortgage servicing rights portfolio (MSRs) totaled $595 billion in unpaid principal balance (UPB) as of Sept. 30, down from $598 billion as of June 30.

The acquisition of Specialized Loan Servicing adds approximately $136 billion in UPB, including $85 billion in third-party servicing.

Nierenberg said that amid the expectation of new rules, banks have to hold more capital against certain assets, which “could create opportunities for us” in the mortgage-servicing rights space.

“I just want to point out, as we think about capital deployment, we do things strategically, where we think we’re gonna have 15% to 20% returns on our capital. If we see a package of MSRs that we think we could achieve those returns, we’ll have a hard look at it.”

The company’s stock traded at $9.35 on Thursday morning, up 4.41% after the earnings report.

Here’s everything you’ll need to know about how to rent a house, including how it’s different from apartment renting.

Maybe you have a growing family or elderly parents moving in. Perhaps you need a dedicated office or you’re craving outdoor space and more privacy than most apartment complexes offer.

If you can’t afford to buy your own home, you can upgrade your living arrangements by renting one. Still wondering how to accomplish this milestone, though? We’ll walk you through it step by step.

How renting a home is different than renting an apartment

While the renting process may be similar, there are large differences that any prospective tenants should be aware of, so their renting process runs smoothly. Navigating the local market is tricky enough, turn to this guide to delve into the must-knows for your home renting experience.

1. Your rent price will look drastically different

Before beginning your hunt for the perfect rental home, you’ll need to figure out what you can afford. Factoring in your income and recurring expenses including any loan payments, check out our helpful tool that will calculate average rents and the cost of living in major cities. You’ll notice upfront, that renting a house may be pricier, due to numerous reasons.

In addition to the monthly rent you’ll be forking over, there are other costs to consider that you may not have had to deal with as an apartment dweller. For example, things like heat, hot water, electricity, internet and satellite TV that are sometimes covered with an apartment rental will likely come straight out of your pocket when you rent a house.

Also, you might be responsible for lawn care, snow removal and other general maintenance, so if you don’t want to take care of those yourself, plan to budget for hiring out those tasks.

You’ll also need to know your credit score to see if you have to get a co-signer or guarantor — someone with good credit who would be liable for your rent if you can’t pay it. This will be added to your lease agreement should this be the case.

2. Your wants and needs will be more extensive

Once you’re clear on your budget, the fun part of researching houses for rent begins. It’s best to start by narrowing down your search to a few choice neighborhoods that offer the amenities you’re looking for, including proximity to work or your children’s schools. Due to the nature of a home (which lacks the built-in amenities an apartment has) your wants and needs for your ideal rental property will be longer.

It’s helpful to make a list of wants vs. needs to help you sort through your thoughts on your dream rental properties:

If you or your family are active or love nature, is the area close to parks and recreation centers?

Do you want a bustling neighborhood packed with restaurants, cafés and boutiques, or would you prefer a quiet, suburban environment?

Is a backyard important to you?

Do you need a garage or dedicated parking space?

Are you looking for a detached home to rent or are you okay with a townhouse?

Does the neighborhood have easy access to public transportation?

3. You’re sure to attend more tours and have more questions

Reading rental listings and taking a good look at the photos is typically not enough to determine whether a rental house might work for you.

While apartment complexes might post floor plans and room sizes online, you might not have advanced information like that with homes for rent. This means you’ll need to ask the landlord, property manager or rental property owner about many things that may not be explicitly listed:

Is the home pet-friendly?

Are appliances included, or would you need to purchase your own?

Is the house furnished? If it is, can you decide what stays or goes?

Are laundry hook-ups in place?

If utilities are not included in the monthly rent, how much can you expect to pay for heat, electricity and hot water?

Can you make decorative changes, such as painting the walls or changing light fixtures?

If there’s a backyard, can you plant a garden?

Is there a home owners association to which you will owe monthly fees?

4. Your neighborhood will be more important than ever

If you like the looks of a house for rent, and the landlord has answered questions to your satisfaction, make sure you also tour the area to get a sense of whether it would be a good fit for you and your family.

Try to speak to some potential neighbors, too: Ask them if it’s safe to walk the streets at night, whether it’s noisy and whether there are other children on the block.

It’s a good idea to visit the street both during the day and in the evening if possible. If the rental home does not have a garage or dedicated parking spot, check out whether street parking is readily available. It’s important to confirm that the right rent price takes into account the neighborhood and what it has to offer potential tenants.

5. There’s additional paperwork, like a home rental application

Paperwork for renting an apartment is a given, however, there tends to be a bit more when it comes to renting a home. Keep in mind, if the property is in a popular neighborhood in a hot real estate market, you won’t want to waste any before time letting the landlord know you’re ready to begin the application process.

Some property managers will charge you a fee between $25 to $100 before opening a file. Supply the following information to help the landlord determine if you are a good candidate to rent the house:

Your personal contact information

Proof of income. If you work full-time, pay stubs are sufficient. If you are self-employed, you can present bank statements or tax returns from the past three years. Retirees can provide proof of pension, 401(k) or bank statements.

Your guarantor’s name and contact information, if applicable

References who can vouch for your reliability and trustworthiness, such as a supervisor or former landlord

6. More rules you’ll have to adhere to

If your rental home has an HOA, you’ll need to check in with them to see if there are any regulations to follow on moving day, such as not leaving empty boxes at the curb when moving. There will likely also be regulations ranging from decorating to construction restrictions that the homeowner, in this case the landlord, will have to adhere to.

The similarities between renting an apartment and a house

There are some steps and parts of the renting process that don’t change even though the type of rental property does. There are similarities beyond the obvious of needing to pay rent and adhering to rental laws.

1. The background check

Landlords want tenants who have a steady income, a good loan repayment track record and a history of paying rent on time. Often, they will conduct a background check to assess whether they want to rent you their house.

During this part of the process, a property manager will likely want to confirm your employment, speak to the references you provided and check your credit report to see how you managed past payments.

2. The required fees such as a security deposit and first month’s rent

Some landlords will require a security deposit equivalent to a month’s rent, which would cover any damage to the property you might cause during the term of the lease. In some cases, you can either be refunded this fee when the lease is up or it goes to the last month’s rent.

You might also have to pay the first month’s rent once you sign a lease, even if you’re not moving in for a while. Sometimes, you’ll be charged a deposit for keys if you require more than one.

3. The moving process

While you won’t have to reserve an elevator to move into your rental home the way you did when you lived in an apartment, there are some things you need to organize before the big move.

For example, before you book a professional moving company, find out from the landlord if you can reserve a parking spot in front of the house where the truck can park, or whether it can back onto part of the property for easier unloading.

Once that’s done, you can concentrate on packing up and getting ready to move into your new home. Don’t forget to advise utility companies, internet and television providers and anyone else who needs to know you’re moving elsewhere.

Make sure to stay on top of details

Taking the time to research rental homes and neighborhoods and asking the right questions will make the transition from apartment living to a home rental go more smoothly.

Being organized with your paperwork and task list for moving day will provide peace of mind and fewer last-minute glitches so that you can celebrate once you’re settled into your new rental home.

And if you’re thinking about renting out your home for some passive income-generating opportunities, take a look at our rent estimator to see how much you could be earning.

Wesley is a Charlotte-based writer with a degree in Mass Communication from the University of South Carolina. Her background includes 6 years in non-profit communication and 4 years in editorial writing. She’s passionate about traveling, volunteering, cooking and drinking her morning iced coffee. When she’s not writing, you can find her relaxing with family or exploring Charlotte with her friends.

Inside: Do you want to claim your partner as a dependent on your taxes? This guide will explain the rules of claiming dependents whether girlfriend or boyfriend and help you take the necessary steps to do so.

Navigating the waters of tax credits can be tricky, especially when it involves claiming an unmarried partner as a dependent.

The Internal Revenue Service (IRS) does permit the declaration of a non-relative adult as a dependent, provided certain conditions are met.

And that is where it gets tricky for the tax novice.

That is where we are going to reference the IRS guidance, so you can determine whether or not you qualify for this deduction.

By pointing you in the right direction, you can understand the specific tests and requirements to avoid any tax-related complications.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Understanding dependency in the context of taxes

The word “dependent” might remind you of a newborn baby or an elderly family member. But in tax terms, the meaning broadens.

In the IRS terms, a “dependent is a person, other than the taxpayer or spouse, who entitles the taxpayer to claim a dependency exemption.” 1

This might be a child, an adult family member, a significant other, or even a close friend. This term “qualifying relative” is crucial in IRS parlance for its implications on your tax dues.

Typically, any person can qualify as a dependent if more than half of their financial support, including living and medical expenses, is taken care of. Also, it’s an opportunity to boost one’s tax return by up to $500 with the Other Dependent Tax Credit.

What qualifies a person as a dependent?

The IRS bases dependents on two categories: “Qualifying children” and “Qualifying relatives.”2 You might think of a qualifying child as your son or daughter. Expanding the scope, a qualifying relative can be a sibling, a parent, or even a significant other.

The essence lies in their financial reliance on you and the nature of your relationship. They ought to:

Be related to you via blood, marriage, or adoption;

You provide over 50% of their financial support including housing, food, medical care, and other expenses

They are U.S. citizen.

The income of the possible dependent.

These nuanced rules might sound overwhelming, but IRS guidance and tax experts like TurboTax can help lighten the load.

Now, let’s address this sticking point: Can you actually claim your partner as a dependent? The following section unravels the mystique.

TurboTax

TurboTax® is the #1 best-selling tax preparation software to file taxes online. Easily file federal and state income tax returns with 100% accuracy.

This is how I have filed my personal taxes for many years.

Get Started

Can I Claim My Partner as a Dependent?

You can claim your partner as a dependent on your tax return, provided they meet certain criteria explained by the IRS, including passing the non-qualifying child test, the citizen or resident test, the joint return test, the income test, and the dependent taxpayer test.

I know this is where it gets difficult to follow for the average person.

So, we are here, to break this terminology down into layman’s terms, as such you can then make the best decision for your tax situation.

If you are still confused, then consult with an online tax software like TurboTax or a tax professional for guidance on your personal taxes.

Basic requirements for claiming your partner as a dependent

This essentially means that your partner should be financially dependent on you, where you bear more than half of their living expenses.

In essence, claiming your partner as a dependent revolves around these fundamentals: 2

Residency: Your partner must have been living with you for the full tax year.

Income limit: Your partner’s gross income should not exceed $4,700 for the year 2023.

Support Requirement: You are the main pillar for your partner’s financial needs by covering over half of their total expenses.

Anyone Else Claiming Them: None else should claim your partner as their dependent.

Unmarried. Your partner must be unmarried legally.

All fulfillment of these criteria moves you a step closer to enjoying some tax relief.

Confirm with an accountant or tax expert as exceptions can exist, such as temporary absences due to illness, education, business, and others.

Common scenarios where you can claim your partner as a dependent

Claiming a partner as a dependent isn’t as fancy as it sounds, but it’s plausible. Here are common scenarios enabling you to do so:

Co-habiting Before Marriage: You and your partner share a home, and you pay more than half of your partner’s living costs. However, your living situation cannot violate local laws, as in some states, “cohabitation” by unmarried people is against the law.

Unemployed Partner: Your partner’s tie with working life is severed (e.g., due to health issues or being laid off), and you bear most of the living expenses.

Supporting Student Partner: Your partner pursues their education, and you shoulder the majority of their expenses.

Take this interactive IRS quiz to determine whom I may claim as a dependent.

How much will I get if I claim my girlfriend as a dependent?

Now the pivotal question: what’s the advantage in dollars and cents?

In essence, claiming your partner as a dependent will slash your taxable income by $500 with the Other Dependent Tax Credit. 3

If you already qualify for Head of Household status with another dependent, then it is possible your deduction may be more. 4

Remember, there’s no one-size-fits-all answer. When tax complexities strike, consult an expert!

Is it better to claim my girlfriend as a dependent?

Honestly, like most tax questions, the answer is: it depends.

If you’re covering your partner’s majority expenses and they’re fulfilling all IRS criteria, then claiming them can bring solid tax savings.

Yet, bear in mind:

If your partner earns substantial income (greater than $4,700), they might lose personal benefits by becoming your dependent.

By claiming your partner, their Social Security or medical benefits may take a hit.

So, assess your partner’s income, benefit entitlements, and your tax situation. Then, tread wisely.

e-file

E-file makes tax season a breeze with its user-friendly interface, ensuring a seamless and stress-free experience for filers.

Simplify your tax journey by choosing E-file.

Start Now

Important Rules to Keep in Mind When Claiming Your Partner

When filing taxes, it’s crucial to understand that both parties are responsible for the accuracy of each other’s tax reporting and liability.

It’s worth noting that tax advantages and disadvantages exist in the scenario of being married and filing jointly, such as potential reductions in your tax bracket and sharing of business losses. So, it may be something to consider.

Can I claim my girlfriend as a dependent if she has no income?

In a nutshell, yes! If your girlfriend had no income in the tax year, you might claim her as a dependent. Given you provide over half of her total support and she lived with you all year, you’re golden.

For 2023, your partner’s gross income should not exceed $4,700.

However, keep in mind that in cases where public assistance or Social Security benefits are her primary financial sources, claiming her could negatively impact those benefits.

Learn the answer to do you have to file taxes if you have no income.

Remember: tax waters are often murky. When in doubt, lean on a tax professional’s shoulder!

Support factors

Answering the support question plays a hefty role in determining who qualifies as a dependent.

You shouldn’t just share the living cost; you should pay more than half of it. Remember, it includes an array of expenses, like food, clothing, education, or medical expenses.

The implication of your partner being claimed by someone else

Here’s a key rule: if someone else is claiming your partner as a dependent, you’re out of the game. The IRS rules say a person can be claimed as a dependent by only one taxpayer in a single tax year.

This could happen if your partner perhaps lives part of the year with someone else like a parent.

Another possibility is if your partner is legally married still, then they would have to file a married, filing separately return.

So, if your partner qualifies as someone else’s dependent, even if they don’t claim them, you can’t claim your partner.

Frequent Situations Where You Can’t Claim Your Partner as a Dependent

Considerations for Non-resident or Non-citizen partners

If your partner isn’t a U.S. citizen, resident, or national, the dependent claiming game changes. Notably, nonresident aliens cannot be claimed as dependents.

However, if your partner is a resident of Canada or Mexico or a U.S. national, you may claim them. But they should be living with you full-time. 2

This rule extends to partners awaiting changes in their residency or citizenship status. In such cases, you must wait until their status changes before claiming them.

When your partner earns more than the stipulated income threshold

When your partner’s income level sails past the IRS limit ($4,700 in 2023), claiming them as a dependent slips off the table. 2

Any part-time job, seasonal work, or income source counts, even those seemingly negligible. As soon as they cross this threshold, regardless of how heavily they rely on you or where they reside, they can’t qualify as your dependent.

Make sure to stay updated on IRS rules. They adjust the income limit for inflation annually, which changes this income ceiling. Keep an eye peeled for those IRS updates!

TurboTax

TurboTax® is the #1 best-selling tax preparation software to file taxes online. Easily file federal and state income tax returns with 100% accuracy.

This is how I have filed my personal taxes for many years.

Get Started

How to Officially Claim Your Partner on Your Taxes

To officially claim your partner as a dependent on your tax return, you will do this when you file your taxes.

Thankfully, this is made easier with online software companies like TurboTax or H&R Block.

The same is true when you are trying to figure out how to file taxes without a W2.

Necessary steps to claim your partner on your taxes

You will first identify them as “other qualifying dependent” or “other qualifying relative”.

Gather the facts first: Confirm your partner’s income, residency, and who has been supporting them for more than half the year.

Document expenses: Keep track of all relevant bills and receipts to demonstrate your majority support.

Use tax software or a professional: Follow prompts about dependents in tax software like TurboTax. They could guide you through the process and specifics.

Complete relevant Tax Forms: Prepare the necessary forms such as Form 1040 and Schedule H and have proof of residency, financial support, gross income information, and certification of your domestic partnership to support your claim.

File your return: Don’t forget to include your partner’s details and tick the correct boxes.

Remember, the devil is in the details. So carefully evaluate your situation to avoid missteps, and consult with a tax professional when in doubt.

Pitfalls to avoid while filing tax returns

While preparing to file your tax returns, beware of these common pitfalls:

Incorrect income calculation: Ensure you tally your partner’s gross income accurately. Reminder: it should not eclipse $4,700 in 2023.

Overlooked Living Qualification: Your partner must have resided with you the entire year. Temporary absences (illness, education) can be exceptions.

Ignoring Other Claimants: If someone else is poised to claim your partner as a dependent – even if they don’t – you can’t claim them.

Emergency Funds Consideration: If your partner taps into their savings for a large expense, this could speak against you providing most of their support.

Forgotten Documents: Maintain a record of bills, receipts, and other expense documents.

The IRS overlooks no mistakes, so take care and stay informed. When in doubt, professional tax help is a button away.

Frequently Asked Questions (FAQ)

Intriguing question! Here’s the short answer: Your partner’s marital status may indeed affect your ability to claim them as a dependent.

For instance, if your partner is married and files a joint tax return with their spouse, you can’t claim them as a dependent.

Remember, tax rules are lock-key specific, and bending them can lead to penalties. Always seek advice from a tax professional.

While you might be able to claim your partner as a dependent, laying claim on their children as dependents is unlikely. IRS rules are clear: you can claim a dependent only if they’re your child or relative.

Since your partner’s children don’t fulfill this requirement, you can’t claim them unless they can be considered your qualifying relative AND you provide more than half of their support.

As always, it’s best to run this by a tax professional for clarity on your unique situation. All we tax-seers can do is guide; the decision falls on your shoulders.

Here’s the hard truth: if your partner didn’t live with you all year, you couldn’t claim them as a dependent. IRS rules are stringent about this: your partner must have the same home as you for the entire year. That is 365 days, no less.

However, IRS grants a green light to temporary separations due to special circumstances like illness, education, military service, or even a holiday. The key lies in their intent to return and, of course, their follow-through.

Stay wise and stay informed, and consult with a tax analyst to seal your decision with assurance.

Get Online Help

Navigating tax rules and regulations doesn’t need to be overwhelming. With the advent of online help, understanding whether you can claim your partner as a dependent becomes considerably more manageable. Here are a few benefits of seeking online help:

Convenience: With online help, you can access the information you need anywhere, anytime. No need to schedule appointments or deal with traffic to get to a tax office. You can get the updates and instructions right from the comfort of your own home.

Accessibility: Some great examples of accessible platforms are TurboTax, e-File, and H&R Block which provide 24/7 support and resources. They offer a wealth of information and experts at your fingertips.

Expertise: Apart from the convenience, these websites employ tax experts who deliver professional analysis and guidance tailored to your specific needs. Specifically, you can use TurboTax Live Full Service for someone to do your taxes from start to finish. Or you can ask questions with TurboTax Live Assisted.

File your own taxes with confidence using TurboTax. This can greatly simplify the process and minimize potential missteps.

Now, Can I Claim my Unmarried Partner as a Dependent is Up to You

As they say, “Ignorance of the law is no excuse”. The same holds true for tax rules.

Falsely claiming a dependent can lead to severe penalties, not just a dinging of your wallet. You’d be sailing the choppy waters of tax evasion, which can bring on hefty fines or even dark days behind bars.

In blatant cases, the IRS could impose a Civil Fraud Penalty. That means a penalty amounting to 75% of the unpaid tax amount resulting from fraud. 5

In short, play by the rules! Accurate and clear tax filing may seem tedious, yet it will steer clear of any legal trouble. Remember, it’s always safer to ask if you are unsure!

Now, are you wondering why do I owe taxes this year?

Source

Internal Revenue Service. “Tax Tutorial.” https://apps.irs.gov/app/understandingTaxes/hows/tax_tutorials/mod04/tt_mod04_glossary.jsp?backPage=tt_mod04_01.jsp#dependent. Accessed October 23, 2023.

Internal Revenue Service. “About Publication 501, Dependents, Standard Deduction, and Filing Information.” https://www.irs.gov/forms-pubs/about-publication-501. Accessed October 23, 2023.

Internal Revenue Service. “About Publication 501, Dependents, Standard DeductionUnderstanding the Credit for Other Dependents.” https://www.irs.gov/newsroom/understanding-the-credit-for-other-dependents. Accessed October 23, 2023.

Intuit TurboTax. “Guide to Filing Taxes as Head of Household.” https://turbotax.intuit.com/tax-tips/family/guide-to-filing-taxes-as-head-of-household/L4Nx6DYu9. Accessed October 23, 2023.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

With the holiday shopping season fast approaching, a simple addition to your catalog can go a long way: gift cards.

Unlike other types of inventory, gift cards are cheap to produce, easy to ship and unlikely to be returned. If you offer digital gift cards, you can’t run out — and you can keep making sales until a few minutes before gifts are exchanged.

“People love giving gift cards,” says Rachel DeCavage, owner and creative director at Cinder + Salt, an eco-friendly clothing company based in New England. “It’s a no-brainer way for them to give someone something that they’re going to love.”

People love getting them, too. In an October survey from the National Retail Federation, 55% of respondents said they hope to get a gift card as a present this year.

Here’s how you can make gift cards part of your holiday strategy, whatever you sell.

1. Create your gift cards

You may be able to order physical cards or offer digital ones through your e-commerce platform or point-of-sale system. Physical cards typically cost less than $2 per card, and digital cards are often free.

Physical cards are more popular gifts for Chicago-based indoor golf facility The Green, says founder and managing partner Connor Ptacin.

During the holidays, Ptacin estimated his team mails out “like 20 gift cards a week” to people who want to give their loved ones something physical.

Digital cards let you keep making sales until the very last minute. DeCavage says she usually sees a rush of gift card orders “like three days before a holiday.”

The right mix of digital and physical cards depends on your customers. If most of your sales take place in person, physical cards may be more popular. But if more of your customers shop online and you tend to ship orders farther away, or if you’re trying to grow your online sales, lean into digital cards.

2. Promote them as gifts

Display gift cards by your register and prominently on your e-commerce website to catch shoppers’ eyes.

“Just pop it right there on the counter and drive the impulse purchase,” says Jay Jaffin, chief marketing officer at Blackhawk Network, which helps retailers create and sell gift cards and other rewards items.

You can use gift cards to encourage other spending. This year, DeCavage is offering gift cards as bonuses to customers who spend more than a certain amount at Cinder + Salt.

“It could be an incentive for them or it could be something they can give to someone else, and it also feels like they’re getting a discount,” DeCavage says.

Make sure your cashiers know how to load gift cards using your point-of-sale system and how to package them. Those transactions give your staff the opportunity to make additional sales, too: DeCavage encourages gift card buyers to add something small, like a sticker, so it’s more exciting for the recipient to open.

“We try to make it a part of the shopping experience for people who are really unsure about what to get,” DeCavage says.

Promote gift cards on social media and via email, too. A well-timed online marketing campaign can remind previous customers that you have gift cards available — especially if you can reach last-minute shoppers at the right moment.

Lastly, Ptacin recommends swapping gift cards with other local businesses that serve similar audiences. That can help you reach new customers who might have just needed a push to visit you.

3. Prepare for redemptions

If you sell enough gift cards, you might reduce the intensity of another post-New Year’s headache: returns.

“A lot of times, what you see is a bunch of returns at the beginning of the year,” Jaffin says. “Sometimes, those gift cards can actually help balance that out — that first-quarter lull.”

Shoppers usually spend more than what’s on their gift cards, Jaffin adds.

DeCavage says gift card shoppers often behave differently. Instead of making a beeline for their desired item, they tend to spend lots of time browsing.

“For small retailers, gift card programs can really be a low-maintenance and affordable way to compete against larger stores,” Jaffin says, “while also helping to acquire new customers and encourage repeat foot traffic.”

Here are some alternatives to no-credit-check loans that are ideal for individuals with little to no credit history.

Search for Lenders Who Take Alternative Credit Backgrounds Into Account

While credit history is typically used to assess a borrower’s risk, some banks will accept alternative data to determine your eligibility such as salary, rent, or utility payment history and bank statements. Remember that most lenders will only accept alternative data for smaller loans like credit cards, personal loans, and auto loans as opposed to larger loans like mortgages.

To find a lender that accepts alternative credit backgrounds, contact financial institutions in your area or apply for loans online. Make sure to have important documents such as bank statements, W-2s, tax returns, and rent payments readily available.

You can also opt to have alternative data reflected in your credit history. For example, you can sign up for a service that reports your rent and utility payments to the three credit bureaus. This is an excellent way to start building your credit.

Credit tip: You may have better luck if you consult with a lender face-to-face rather than over the phone.

Request a Payday Alternative Loan (PAL) Through Your Credit Union

Some credit unions offer payday alternative loans that are typically lower-cost substitutes to pricey payday loans. PALs are small loans granted in amounts ranging from $200 to $1,000, and they have a maximum APR of 28%. To qualify, you must have been a member of a credit union for at least one month.

Credit tip: You can research credit unions to join by visiting MyCreditUnion.gov.

Apply for a Secured Loan

Secured loans involve putting down a valuable asset as collateral. Assets typically used as collateral include cars, houses, or savings accounts. While these types of loans are beneficial because they have less strict credit history requirements, they are risky in the sense that you could potentially lose the asset you put down as collateral if you’re unable to pay the loan back.

Credit tip: Assess whether you can avoid losing the asset before putting it down as collateral.

Borrow Money From Your Retirement Account

If you have a 401(k) plan, you can take out a loan against your account. Most plans allow you to borrow up to 50% of your savings up to $50,000. Since you are essentially borrowing money from yourself, you won’t need to show credit history to take out a 401(k) loan.

While taking this route could cost you in investment earnings, it is generally a better option than other no-credit-check loans that charge high interest rates. Just make sure to repay the loan within five years to avoid paying taxes and penalties.

Credit tip: Avoid taking out a 401(k) loan if you plan on leaving the company, as you may have to pay it off right away.

Find a Trustworthy Cosigner

If you lack credit history, including a trustworthy family member or friend as a cosigner might help you secure a loan. For a cosigner to improve your chances of being approved, they need to have a good credit score and preferably a long credit history.

However, getting someone to agree to cosign may prove to be difficult, because if you miss payments or default, the cosigner’s own credit will be hurt. Note that this could strain your relationship with the cosigner if you get behind on payments.

Credit tip: If someone in your life agrees to cosign, consider scheduling a reminder to make payments on time.

Turn to a Family Member

If you’re in a position where you need money to cover an expense, consider asking a family member or close friend for a loan. While it might be tough to bring it up, this route can help you avoid getting stuck in a situation with a predatory lender.

Credit tip: When borrowing money from family, consider drafting up a contract to ensure everyone is on the same page about the loan amount, repayment timelines, and any interest that may be charged.

How to Get a Loan With No Credit FAQ

Below, we’ve answered some common questions regarding getting a loan with no credit.

Can I Get a Loan With No Credit?

Yes, it’s possible to get a loan with no credit, although it will be more difficult to get approved, and you may incur a higher interest rate.

What Loans Can I Get With No Credit?

Types of loans you can get with no credit include no-credit-check loans, secured loans, online loans, credit union loans, and family loans.

How Much Can I Borrow With No Credit?

The exact amount you can borrow with no credit will depend on the type of credit account you’re approved for. Remember that the higher your credit score, the more money you’ll be able to borrow.

What Is a Good Credit Score to Get a Loan?

While the exact credit score to get a loan varies, borrowers need a FICO® score of at least 670 to fall within the good credit score range.

How to Build Credit

Establishing credit from the ground up can seem daunting. Here are some ways to start building credit so you can get approved for loans more easily in the future:

Become an authorized user: Ask a trusted person in your life to add you as an authorized user to their credit card account so that you can establish credit history.

Apply for a secured credit card: A secured credit card is a type of beginner-friendly card that requires you to put down a refundable deposit. Since these cards pose less risk to the lender, they’re easier to get approved for when first establishing credit.

Report rent or utilities: While most companies don’t report to the credit bureaus, you can sign up for a rent and utility reporting service that reports these payments to build credit faster.

Apply for a credit-builder loan: A credit-builder loan is an installment loan specifically geared to individuals looking to build credit history. When you take out a credit builder loan, the borrowed funds are placed in a secure savings account or certificate of deposit (CD) and held as collateral until you repay the loan.

Ready to start building your credit? ExtraCredit® is a tool that provides complete credit coverage, including rent and utility reporting and other credit profile-building offers. Try it for free today.

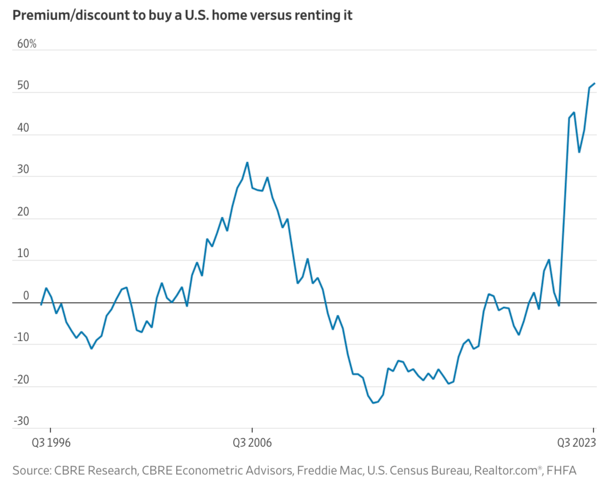

As if you needed more evidence that it’s not a good time to buy a home.

The latest piece comes from the WSJ, which revealed that renting is 50% more expensive than buying.

This comes on top of a recent Fannie Mae survey that said home buyer sentiment matched an all-time survey low, with only 16% indicating it was a good time.

The culprit continues to be mortgage rates, which surpassed 8% last week and continue to erode affordability.

So is it better to hold off and keep renting or continue to house hunt?

It’s Not Always a Good Time to Purchase a Home

First off, it’s not always a good time to purchase a home, or condo for that matter.

Ultimately, there are better times and worse times, at least if we’re framing the question in terms of investment returns.

There’s also the sheer matter of affordability, which could jeopardize the transaction long-term if the buyer isn’t able to keep up with payments.

That’s essentially what transpired in the early 2000s, when home buyers with no business buying homes went through with the transaction regardless.

Often, this involved some creative financing and perhaps some stated income underwriting to get to the finish line.

In the end, while they qualified for the loan and closed on the purchase, they often didn’t make it past the first few mortgage payments before they fell behind.

Today, the situation is different because many of those questionable loan types, like stated income loans and option ARMs, no longer exist.

You can thank the Ability to Repay/Qualified Mortgage rule (ATR/QM Rule), which was born out of the prior mortgage crisis.

It requires lenders to “make a reasonable, good faith determination of a consumer’s ability to repay a residential mortgage loan according to its terms.”

That’s good news because it means fewer unqualified home buyers are getting approved for mortgages.

And more homeowners have safer loan products, such as the 30-year fixed, as opposed to an interest-only loan or something else that’s potentially high-risk.

Affordability Is a Problem No Matter How You Slice It

While the existing stock of homeowners has never been better, thanks to those aforementioned rules and the low, fixed interest rates they hold, it’s a different story for prospective buyers.

Today’s home buyer is looking at an average mortgage payment that is 52% higher than the average apartment rent, per a CBRE analysis.

This is the worst premium since at least 1996, and even well above the prior housing market peak in 2006 when it stood at 33%.

If you look at the chart above, it’s basically all because of the sharp rise in mortgage rates, which increased from sub-3% levels to around 8% today in less than two years.

That’s unprecedented movement, even if rates remain below 1980s mortgage rates. The bigger takeaway is the speed at which rates climbed higher.

We’re talking a near-200% increase in rates in less than 24 months. Meanwhile, home prices haven’t come down, thanks to a dearth of supply.

And a phenomenon known as the mortgage rate lock-in effect, where existing homeowners with 2-3% mortgage rates feel trapped.

Or are simply unwilling to move and take on a much higher interest rate.

Taken together, we have the worst home buying affordability in 30+ years history.

That buy versus rent premium is also up from 51.1% during the second quarter and 45.3% a year ago.

Again, this is largely due to higher mortgage rates, which have continued to climb higher throughout the year thanks to a stronger-than-anticipated economy.

It Now Takes Over a Decade to Break Even on a Home Purchase

Thanks to the big price tag on a home purchase these days, combined with high mortgage rates, it now takes over a decade to break even, per new data from Zillow/Axios.

The typical home buyer who puts down 3% on a $376,000 home purchase with a 7.045% mortgage rate won’t reach this point for 13.5 years.

This assumes a typical increase in home values, 3% closing costs, 1% in home maintenance fees, along with 6% closing costs and 6% agent commissions paid at time of sale.

In other words, you won’t be able to turn a profit until you’ve been in it long enough to whittle down the balance to offset all the associated costs.

Using that same purchase price, the loan balance would be about $285,000 after 13.5 years of regular monthly mortgage payments.

If the mortgage rate was 3%, the balance would be roughly $240,000 at that time because a lot more of each payment goes toward principal.

Someone who puts 20% down on a house can break even a bit sooner, at around 11.3 years, which is still about double the five-year timeline.

What does this say. That maybe it’s not a great time to buy a home, at least from an investment standpoint.

See: Rent vs. buy calculator

Should You Wait to Buy a House?

At this juncture, I don’t think anyone would call you crazy for pumping the brakes on a home purchase, though everyone has different reasons for buying.

And over time when you bought can matter less, assuming you stay the course (ask the 2006 home buyers who still own).

Aside from housing affordability being at multi-decade lows, the available inventory of homes is also quite poor.

Simply put, there isn’t a lot to choose from at the moment, and affordability stinks to boot.

At the moment, there are only about 2.5 months of supply at the existing sales rate, about half the normal 4-5-month level of for-sale inventory, per Redfin.

So despite the horrible lack of affordability, home prices are holding up just fine. In fact, the median sales price is up 1.9% from a year ago.

In other words, if you’re a prospective home buyer today, you might be looking at slim pickings, intense competition from other buyers, and an 8% mortgage rate.

That sure doesn’t sound like favorable home buying conditions.

Those who bought last year and more recently may have been told to marry the house and date the rate.

The argument is the house can be yours forever but the interest rate doesn’t have to be. The problem is mortgage rates have continued to go up.

So that advice hasn’t panned out so well for those who bought banking on refinancing to a lower rate by now.

This means if you do buy a home today, you need to be prepared to pay the mortgage rate you’re given.

Not a temporary buydown rate or a potentially lower rate in the future that may not materialize.

One compromise might be a hybrid adjustable-rate mortgage, which is fixed for the first five or seven years.

By then, hopefully mortgage rates drift over. If you believe the forecasts, they’re actually expected to drop by 2024. But that’s subject to change. And there’s still the question of just how much.

One worry along these lines is lower mortgage rates could be accompanied by lower home prices. And that could make it difficult to refinance if the mortgage is underwater.

In other words, if you buy today, you better be able to afford it. And you better really like the house.

Read more: 10 reasons to buy a house other than for the investment

High-frequency trading (HFT) firms use ultrafast computer algorithms to conduct big trades of stocks, options, and futures in fractions of a second. HFT firms also rely on sophisticated data networks to get price information and detect trends in markets.

A key characteristic of HFT trading — in addition to high speed, high-volume transactions — is the ultra-short time time horizon.

How high-frequency trading impacts markets is a controversial topic. Proponents of HFT say that these firms add liquidity to markets, helping bring down trading costs for everyone. HFT critics argue such firms are an example of how bigger, better-funded players have an advantage over smaller retail investors, and that HFT technology can be used for illegal purposes like front-running and spoofing.

What is High Frequency Trading?

Ultrafast speeds are paramount for high-frequency trading firms. Executing these automated trades at nanoseconds faster can mean the difference between profits and losses for HFT firms.

There are broadly two types of HFT strategies. The first is looking for trading opportunities that depend on market conditions. For instance, HFT firms may try to arbitrage price differences between exchange-traded funds (ETFs) and futures that track the same underlying index.

Futures contracts based on the S&P 500 Index may experience a price change nanoseconds faster than an ETF that tracks the same index. An HFT firm may capitalize on this price difference by using the futures price data to anticipate a price move in the ETF.

Another type of HFT is market making. Not all market makers are HFT firms, but market making is one of the businesses some HFT firms engage in.

A big market-making business for HFT firms is payment for order flow (PFOF). This is when retail brokerage firms send their client orders to HFT firms to execute. The HFT firms then make a payment to the retail brokerage firm. 💡 Quick Tip: Are self-directed brokerage accounts cost efficient? They can be, because they offer the convenience of being able to buy stocks online without using a traditional full-service broker (and the typical broker fees).

How HFT Works and Makes Money

High-frequency trading enables traders to profit from miniscule price fluctuations, and permits institutions to gain significant returns on bid-ask spreads. HFT algorithms can scan exchanges and multiple markets simultaneously, allowing traders to arbitrage slight price differences for the same asset.

Bid-Ask Spreads 101

High-frequency trading firms often profit from bid-ask spreads — the difference between the price at which a security is bought and the price at which it’s sold.

For instance, an HFT may provide a price quote for a stock that looks like this: $5-$5.01, 500×600. That means the HFT firm is willing to buy 500 shares at $5 each — the bid — while offering to sell 600 shares at $5.01 — the ask. The 1 cent difference is how the market maker makes a profit. While this seems small, with millions of trades, the profits can be sizable.

How wide bid-ask spreads are is also a marker of market liquidity. Bigger chunkier spreads are a sign of less liquid assets, while smaller, tighter spreads can indicate higher liquidity.

Recommended: What Is Quantitative Trading?

Payment For Order Flow 101

When it comes to payment for order flow, high-frequency traders can make money by seeing millions of retail trades that are bundled together.

This can be valuable data that gives HFT firms a sense of which way the market is headed in the short-term. HFT firms can trade on that information, taking the other side of the order and make money.

Background on High-Frequency Trading

High-frequency trading became popular when different stock exchanges started offering incentives to firms to add liquidity to the market. Liquidity is the ease with which trades can be done without affecting market prices.

Like momentum trading, the HFT industry grew rapidly as technology in the financial space began to take off in the mid-2000s.

Adding liquidity means being willing to take the other sides of trades and not needing to get trades filled immediately. In other words, you’re willing to sit and wait. Meanwhile, taking liquidity is when you’re seeking to get trades done as soon as possible.

During 2009, about 60% of the market was said to be HFT. Since then, that percentage has declined to about 50% as some HFT firms have struggled to make money due to ever-increasing technology costs and a lack of volatility in some markets. These days the HFT industry is dominated by a handful of trading firms.

Pros and Cons of High-Frequency Trading

HFT comes with certain pros and cons.

Pros of HFT

High-frequency trading is automated and efficient, thanks to its use of complex algorithms to identify and leverage opportunities.

HFT may create some liquidity in the markets.

Cons of HFT

Because high-frequency trades are conducted by institutional investors, like investment banks and hedge funds, these firms and their clientele tend to benefit more than retail investors.

Because high-frequency trades are made in seconds, HFT may only add a kind of “ghost liquidity” to the market.

Some HFT firms may also engage in illegal practices such as front-running or spoofing trades. Spoofing is where traders place market orders and then cancel them before the order is ever fulfilled, simply to create price movements.

The Debate Over High Frequency Trading

High-frequency trading is a controversial topic, and HFT firms have been involved in lawsuits alleging that they create an unfair advantage and potentially create volatility.

Criticism of HFT

One complaint about HFT is that it’s giving institutional investors an advantage because they can afford to develop rapid-speed computer algorithms and purchase extensive data networks.

Critics argue that HFT can add volatility to the market, since algorithms can make quick decisions without the judgment of humans to weigh on different situations that come up in markets.

For instance, after the so-called “Flash Crash” on May 6, 2010, when the S&P 500 dropped dramatically in a matter of minutes, critics argued that HFT firms exacerbated the selloff.

HFT critics also argue that such traders only provide a very temporary kind of liquidity that benefits their own trades, but not retail investors. A December 2020 paper published by the European Central Bank also argued that too much competition in the HFT industry can cause firms to engage in more speculative trading, which can harm market liquidity. 💡 Quick Tip: Before opening any investment account, consider what level of risk you are comfortable with. If you’re not sure, start with more conservative investments, and then adjust your portfolio as you learn more.

Defense of HFT

Defenders of high-frequency trading argue that it has improved liquidity and decreased the cost of trading for small, retail investors. In other words, it made markets more efficient.

This can be particularly important in markets like options trading, where there are thousands of different types of contracts that brokerages may have trouble finding buyers and sellers for. HFT can be helpful liquidity providers in such markets.

When it comes to payment for order flow, defenders of HFT also argue that retail investors have enjoyed price improvement, when they get better prices than they would on a public stock exchange.

The Takeaway

It’s tough to be an investor in many markets today without being affected by high-frequency trading. HFT firms are proprietary trading firms that rely on ultrafast computers and data networks to execute large orders, primarily in the stocks, options, and futures markets.

HFT proponents argue that their participation helps markets be more efficient. Critics argue that they have a big advantage over smaller investors, given how much they pay for information and data networks.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

Is high-frequency trading profitable?

High-frequency trading aims to profit from micro changes in price movements through the use of highly sophisticated, ultrafast technology. That said, HFT investors are subject to losses as well as gains.

Is high-frequency trading illegal?

High-frequency trading has been the subject of lawsuits alleging that HFT firms have an unfair advantage over retail investors, but HFT is still allowed. That said, HFT firms have been linked to illegal practices such as front-running.

What is an example of high-frequency trading?

High-frequency trading can be used with a variety of strategies. One of the most common is arbitrage, which is a way of buying and selling securities to take advantage of (often) miniscule price differences between exchanges. A very simple example could be buying 100 shares of a stock at $75 per share on the Nasdaq stock exchange, and selling those shares on the NYSE for $75.20.

Photo credit: iStock/wacomka

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Imagine your budget allows you to seamlessly fit your student loan repayments into your day-to-day life. Here are a few tips to redo your budget.

Determine your financial goals

How can you budget if you don’t know where you’re going? Setting financial goals can help give your money a purpose. Consider short- and long-term goals, such as paying off loans in a specific period of time, or saving up for a specific purchase or life event.

Calculate your income

How much do you make after taxes? All you have to do is look at a paystub and any other income, such as from a side hustle. You might have investments that pay you dividends or other forms of income. Whatever you have, add it all up!

Review your expenses

How much money flows out of your checking account every month? Look at loan payments, insurance costs, mortgage payments or rent, utilities, food, childcare, healthcare, IRA deductions, and everything else that belongs in the category of expenses.

Make adjustments

Consider where you can make adjustments based on your income and expenses so your student loans nestle right into your budget.

What percent should go toward student loans? Keep the 50/30/20 budgeting rule in mind:

• 50% toward needs

• 30% toward wants and discretionary expenses

• 20% toward savings and paying off debt

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content. Communication of SoFi Wealth LLC an SEC Registered Investment Advisor SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.