Warning that the housing market is contracting again as today’s mortgage rates hover near 8%, Wells Fargo economists wrote in a new analysis that rising borrowing costs “stand to tip the housing sector back into a recession.”

The “ominous” special commentary posted Thursday, according to a Wells Fargo news release, states prospects for a housing rebound are dimming as mortgage rates tighten their grip on the already sharp U.S. housing affordability issues.

Even though the economy has shown “a remarkable degree of resilience” this year — and a strong labor market along with moderating inflation has “raised hopes that the U.S. economy can avoid a recession — the same can’t be said for the real estate market. Unfortunately, not every sector of the economy has been as sturdy in the face of rising debt costs,” the Wells Fargo economic group wrote.

“After generally improving in the first half of 2023, the residential sector now appears to be contracting alongside the recent move higher in mortgage rates,” they continued. “Although mortgage rates may gradually descend once the Federal Reserve begins to ease monetary policy, financing costs are likely to remain elevated relative to recent norms.”

The commentary comes days after Goldman Sachs analysts also issued a downgraded housing forecast, predicting “higher for longer” mortgage rates will continue to squeeze home inventory and yet home prices will stay in the green, though growth will be slight as sales slow even more.

It also comes a day after the Federal Reserve Bank of Atlanta posted an update to its Home Ownership Affordability Monitor, showing housing affordability sank to a “new record low” in August due to still stubbornly high prices and rising interest rates.

In yet another month of declines, the monitor index score sank to 67.3 in August with a national median home price of $377,500, a median income of $76,621, a total median monthly payment of $2,848 and an interest rate of 7.1%. The Atlanta Fed estimated the annual total payment share of median income to be 44.6%, well over the recommended 30% of income for housing costs.

Compare that score to a score of 112.3 in November 2012, when the median home price was $197,333, median income was $52,161, and the interest rate was 3.4%.

This latest affordability reading was back in August, before interest rates inched closer to 8%, hitting that threshold last week before tipping down only slightly, according to Mortgage News Daily.

This “higher for longer” interest rate climate is likely to “not only weigh on demand, but could also constrain supply by reducing new construction and discouraging prospective sellers carrying low mortgage rates from listing their homes for sale,” Wells Fargo economists wrote.

The bank’s analysts also downgraded their home price forecast, though now they expect a “slightly softer pace of home price appreciation in the years ahead.” Because high interest rates are expected to continue to both dampen demand and constrain supply, they predict those dynamics will continue to buoy home prices slightly.

“Higher financing costs are likely to both weigh on demand and constrain supply, which will allow home prices to maintain a positive trajectory,” Wells Fargo economists wrote, predicting the S&P Case-Shiller National Home Price Index to increase 1.8% in 2023 and 2.5% in 2024.

The economic group also predicts a “downshift” in new residential construction starts, with multifamily permits already declining sharply in recent months.

“The recent drop in home builder confidence is evidence that single-family construction may begin to moderate as higher mortgage rates test builders’ ability to offer rate buy-downs to attract new buyers,” they wrote. “That noted, a structural shortfall of single-family supply will likely continue to boost new development.”

With its constant ebbs and flows, real estate demands impeccable timing. There is an intricate art of balancing property transactions, especially in a buyer’s market where there are many opportunities, but with that comes significant risks. Buyers find themselves hesitant, fearing the financial burden of potentially owning two properties, if they can’t sell their current property quickly enough. However, there exists a little-known yet powerful tool: the Sale of Purchaser Property clause, the ace up your sleeve as a buyer in today’s market.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

This strategic provision offers a safeguard against the dual-ownership dilemma, allowing buyers to seize the advantages of a buyer’s market without being shackled by the burden of holding two properties simultaneously. By understanding and effectively utilizing this clause, savvy buyers can navigate the real estate landscape with peace of mind, capitalizing on current market conditions and a favorable upside when playing the long game.

The Power of the Sale of Purchaser Property Clause

A Sale of Purchaser Property clause is a condition the buyer agent includes in the purchase and sale agreement when putting an offer on a home. This clause makes the sale of the new property contingent upon the successful sale of the buyer’s current property.

As a buyer, you essentially get to say: “I’ll buy your property, but only if I can sell my current one first.” The deal may fall through if the buyer’s property doesn’t sell within a specified period, making the new property conditional until the other sale has a firm contract in place. If the buyer successfully sells their property during the conditional period, the condition is waived, and the new home is now also considered legally sold with a binding contract. If you’ve exhausted all options trying to sell your property during that time period, the deal on the property is now void, and the buyer gets their deposit back.

Many buyers and sellers might be more familiar with the terminology of an escape clause; is this any different? An escape clause is included in a purchase agreement so that a seller can continue to market their property and accept new offers from potential buyers even after accepting an offer from a primary buyer. It provides the seller a way to “escape” from the contract if a better offer comes along within a specified time frame. The key difference is that an escape clause primarily benefits the seller. A Sale of Purchaser Property clause benefits the buyer, making their purchase contingent on successfully selling their own property.

Tips for Sellers

Talk to your real estate agent about the escape clause. This allows you to continue to market the property and be aware of further changes in the market (price, interest rates). It’s best to have a short conditional period allowing the buyer to sell their home.

Tips for Buyers

If the inclusion of this clause still keeps you up at night with the concern of owning two properties, you can always consider selling your home first. Typically, in a seller’s market, it takes many unsuccessful offers before firming up on the right home, sometimes taking weeks or even months. However, you can always take your time and work at a pace that is best for you. Take the time to find the right buyer for your property, and include a longer closing period so you have the time you need to find your next home.

With many properties sitting on the market and inventory building up, sellers are feeling the pressure and are eagerly waiting for any offer to be presented. Some stand-out properties are still moving quickly, while others are taking much longer to sell, creating circumstances that favour buyers.

Knowing this condition exists, buyers shouldn’t be afraid to make an offer. If you’re on the fence about a property, the SPP clause gives you security that your purchase can only firm up if you sell your current home. Give us a call today to speak to a real estate agent in your area.

Questions about the real estate market?

Contact us today to talk to a Realtor in your area

McAllen, nestled in Hidalgo County of the southernmost part of Texas, is often recognized for its affordability, burgeoning job market and close ties to Mexico.

This mid-sized city in the Rio Grande Valley attracts a diverse group of residents including retirees, young professionals and families. The question “Is McAllen Texas a good place to live?” often circles the minds of potential relocators. This article unfolds the myriad aspects of living in McAllen to provide a comprehensive outlook.

Cost of living

One of the primary reasons individuals find McAllen appealing is its excellent affordability. The cost of living in McAllen is well below the national average, making it a less expensive area compared to many other cities in Texas and across the country.

Housing costs, which constitute a significant part of living expenses, are remarkably low, with the median home price being much lower than the national average. This reduced price point is often a magnet for buyers and top real estate agents looking to find quality homes at an affordable price.

Amenities

The low cost of living in McAllen extends beyond just housing. Residents find that virtually all basic amenities including food, transportation and health care come at a cost that’s substantially lower than what they might encounter in more expensive areas. The low cost of living isn’t confined to just reduced price tags on goods and services but extends to utilities and other monthly expenditures as well.

Job market

McAllen has witnessed a recent economic boom, thanks to its strategic location near the Mexican border, which has fostered international trade. The city has become a major center for industries such as manufacturing, retail and healthcare. Job opportunities are growing, with many companies choosing to set up shop in the city due to its low operational costs.

Educational landscape

South Texas College is one of the notable educational institutions in McAllen, providing quality higher education to McAllen residents and individuals from the surrounding Rio Grande Valley. Additionally, the presence of other reputable schools and educational programs enriches the city’s educational fabric.

Community and demographics

McAllen is a vibrant city with a diverse population. A significant portion of McAllen’s population is of Mexican descent, reflecting the city’s close cultural and geographical ties with Mexico.

This cultural melting pot creates a unique living experience, albeit with a language barrier as a notable number of residents speak Spanish. Knowing Spanish, while not necessary, can enhance one’s living experience in McAllen.

Location and accessibility

McAllen’s prime location near the Mexican border opens up incredible opportunities for cross-border trade and cultural exchange. Its proximity to South Padre Island and other beautiful coastal areas means residents can easily indulge in outdoor activities. The city’s well-developed metro area facilitates easy commute to downtown McAllen and other bustling areas within and outside the city.

Real estate market

The real estate market in McAllen is thriving, with real estate agents finding a fertile ground for business. The market offers a wide range of housing options ranging from single-family homes to luxury apartments. The affordability of home prices, combined with the expertise of top real estate agents, makes the process of finding a home in McAllen relatively straightforward.

Recreational opportunities

McAllen brims with recreational spots including Archer Park, Fireman’s Park and a burgeoning arts district. The city’s favorable climate, characterized by hot summers and mild winters, is conducive for a variety of outdoor activities. Winter Texans, as the seasonal visitors are known, find McAllen’s mild winter climate particularly appealing.

Weather

The great weather is indeed a significant pull factor. While summers can be hot, the winters are mild with the coldest month of January having an average high that’s considerably warmer compared to many other cities in the U.S.

Safety

McAllen boasts a low crime rate compared to the national average, adding to its attractiveness as a place of residence. The city’s law enforcement agencies work diligently to maintain peace and safety.

Life in McAllen, TX

Living in McAllen Texas presents an array of benefits including a low cost of living, growing job market, and a multicultural community. Its strategic location near the Mexican border enhances its appeal, especially for those involved in international trade or those seeking a bicultural living experience.

While the city has its challenges such as the language barrier for non-Spanish speakers and hot summers, the positives substantially outweigh the negatives, rendering McAllen Texas a good place to live.

Looking for your next casa in McAllen? Check out our apartments and houses for rent here.

Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., August 29, 2023. REUTERS/Brendan McDermid Acquire Licensing Rights

NEW YORK, Oct 19 (Reuters) – Relentless selling of U.S. government bonds has brought Treasury yields to their highest level in more than a decade and a half, roiling everything from stocks to the real estate market.

The yield on the benchmark 10 year Treasury – which moves inversely to prices – briefly hit 5% late Thursday, a level last seen in 2007. Expectations that the Federal Reserve will keep interest rates elevated and mounting U.S. fiscal concerns are among the factors driving the move.

Because the $25-trillion Treasury market is considered the bedrock of the global financial system, soaring yields on U.S. government bonds have had wide-ranging effects. The S&P 500 is down about 7% from its highs of the year, as the promise of guaranteed yields on U.S. government debt draws investors away from equities. Mortgage rates, meanwhile, stand at more than 20-year highs, weighing on real estate prices.

“Investors have to take a very hard look at risky assets,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities in New York. “The longer we remain at higher interest rates, the more likely something is to break.”

Fed Chairman Jerome Powell on Thursday said monetary policy does not feel “too tight,” bolstering the case for those who believe interest rates are likely to stay elevated.

Powell also nodded to the “term premium” as a driver for yields. The term premium is the added compensation investors expect for owning longer-term debt and is measured using financial models. Its rise was recently cited by one Fed president as a reason why the Fed may have less need to raise rates.

Here is a look at some of the ways rising yields have reverberated throughout markets.

Higher Treasury yields can curb investors’ appetite for stocks and other risky assets by tightening financial conditions as they raise the cost of credit for companies and individuals.

Elon Musk warned that high interest rates could sap electric-vehicle demand, which knocked shares of the sector on Thursday. Tesla’s shares closed the day down 9.3%, as some analysts questioned whether the company can maintain the runaway growth that has for years set it apart from other automakers.

With investors gravitating to Treasuries, where some maturities currently offer far above 5% to investors holding the bonds to term, high-dividend paying stocks in sectors such as utilities and real estate have been among the worst hit.

Reuters Graphics

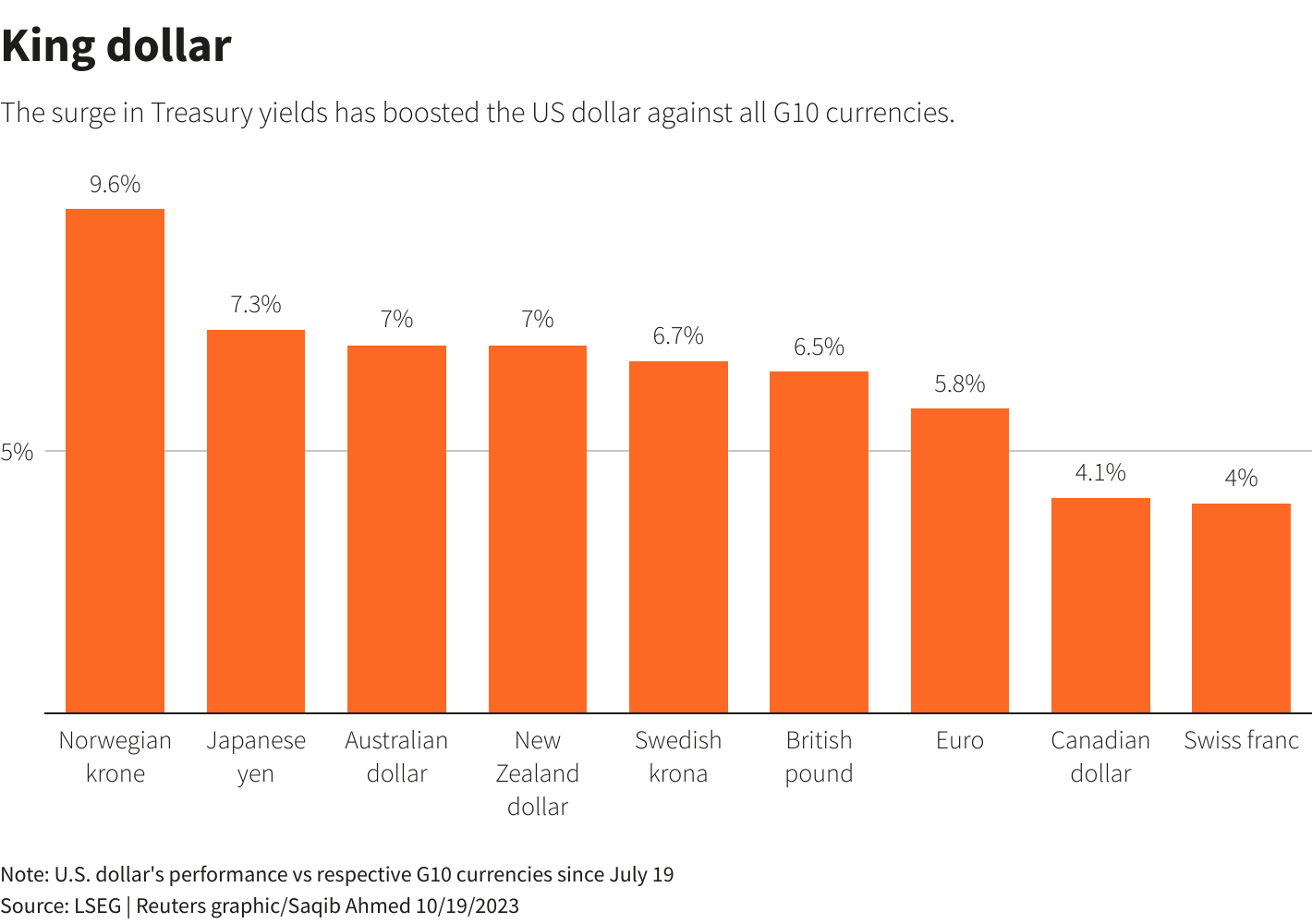

The U.S. dollar has advanced an average of about 6.4% against its G10 peers since the rise in Treasury yields accelerated in mid-July. The dollar index, which measures the buck’s strength against six major currencies, stands near an 11-month high.

A stronger dollar helps tighten financial conditions and can hurt the balance sheets of U.S. exporters and multinationals. Globally, it complicates the efforts of other central banks to tamp down inflation by pushing down their currencies.

For weeks, traders have been watching for a possible intervention by Japanese officials to combat a sustained depreciation in the yen, down 12.5% against the dollar this year.

“The correlation of the USD with rates has been positive and strong during the current policy tightening cycle,” BofA Global Research strategist Athanasios Vamvakidis said in a note on Thursday.

The interest rate on the 30-year fixed-rate mortgage – the most popular U.S. home loan – has shot to the highest since 2000, hurting homebuilder confidence and pressuring mortgage applications.

In an otherwise resilient economy featuring a strong job market and robust consumer spending, the housing market has stood out as the sector most afflicted by the Fed’s aggressive actions to cool demand and undercut inflation.

U.S. existing home sales dropped to a 13-year low in September.

Reuters Graphics

As Treasury yields surge, credit market spreads have widened with investors demanding a higher yield on riskier assets such as corporate bonds. Credit spreads blew out after a banking crisis this year, then they narrowed in subsequent months.

The rise in yields, however, has taken the ICE BofA High Yield Index (.MERH0A0) near a four-month high, adding to funding costs for prospective borrowers.

Volatility in U.S. stocks and bonds has bubbled up in recent weeks as expectations have shifted for Fed policy. Anticipation of a surge in U.S. government deficit spending and debt issuance to cover those expenditures has also unnerved investors.

The MOVE index (.MOVE), measuring expected volatility in U.S. Treasuries, is near its highest in more than four months. Volatility in equities has also picked up, taking the Cboe Volatility Index (.VIX) to a five-month peak.

Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates

Our Standards: The Thomson Reuters Trust Principles.

Find lovely beaches, lush parks and peaceful neighborhoods in Cape Coral.

Is Cape Coral a good place to live? This question has crossed the minds of many prospective residents eyeing the sunny shores of Southwest Florida.

Cape Coral, located near Fort Myers, has a reputation for its lovely beaches, lush parks, and peaceful neighborhoods. In this comprehensive exploration, we dive into the various facets of living in Cape Coral to provide a well-rounded view of what life here truly entails.

Geographical beauty and outdoor fun

Cape Coral is dubbed as the “Waterfront Wonderland” owing to its over 400 miles of navigable waterways. The city’s geographical location by the Caloosahatchee River and Gulf Coast provides numerous avenues for waterfront living.

Residents revel in the close proximity to exotic beaches like Fort Myers Beach and Pine Island. The presence of several parks and natural preserves enhances the appeal for individuals who cherish the great outdoors.

Recreational activities

The city is a hub for a variety of outdoor activities including fishing, boating and hiking. The warm sunny weather, which graces the city year-round, creates a perfect atmosphere for residents to lead an active lifestyle.

The local flora and fauna add to Cape Coral’s charm. The city is known for its burrowing owls, which are not only a sight to behold but also reflect the area’s biodiversity.

Affordability

One of the prominent attractions of living in Cape Coral is its affordability. The city has a cost of living that’s below the national average, making it an enticing location for individuals on a budget.

Real estate

The real estate market in Cape Coral is relatively stable with a variety of housing options ranging from waterfront properties to suburban homes. Home prices are reasonable, providing new residents with a chance to own property in a beautiful city without breaking the bank.

Tax benefits

Florida is known for its friendly tax policies as there is no state income tax, which bodes well for both young adults and senior citizens looking to save on taxes. The lower cost of living extends to utility prices which are also below the national average.

Crime rate and safety

Cape Coral boasts a lower crime rate compared to larger cities in Florida. The lower rates of violent crime and property crime make it a safe community for families and individuals alike.

Economic growth and employment

Cape Coral is experiencing significant growth with a burgeoning economy. The influx of new residents and businesses has led to a robust real estate market and a growing city infrastructure.

The proximity to nearby Fort Myers expands employment opportunities for Cape Coral residents, who can commute for work and still enjoy the peace and tranquility that Cape Coral offers.

Education

Public schools in Cape Coral are part of the Lee County School District, which has a reputation for quality education. Additionally, there are several reputable private schools providing residents with a variety of educational options for their children.

Cultural richness and demographic diversity

Cape Coral hosts various cultural events year-round, providing residents with opportunities to immerse themselves in local and international cultures. The vibrancy of the local arts scene is a testament to the city’s cultural richness.

The city is home to a mix of young adults, families and senior citizens, creating a diverse community. This demographic mix enriches the life in the city and fosters a sense of community among residents.

Cons of Cape Coral life

While there are many benefits to living in Cape Coral, there are drawbacks too. Some residents might find the city to be too quiet, especially when compared to the bustling activity in nearby cities like Miami. The summer months can get exceedingly hot and humid, which might not suit everyone.

Also, the influx of seasonal residents during winter can lead to crowded streets and longer wait times at local establishments.

Living in Cape Coral comes with the reality of facing the hurricane season. The city’s location on the Gulf Coast exposes it to the risk of hurricanes and storm surges, with Hurricane Ian being a notable mention.

Living in Cape Coral

Cape Coral, with its beautiful beaches, affordable living and growing economy, certainly has a lot on offer for prospective residents. While the city has its share of challenges like facing the hurricane season and experiencing seasonal population fluctuations, the positives of living in Cape Coral, FL far outweigh the negatives for the most part.

The city is indeed a great place for individuals and families seeking a serene environment, lower cost of living and a community-centric lifestyle amidst the beauty of Southwest Florida.

Ready to find your Cape Coral rental paradise? Look at apartments for rent here.

Summerville, a picturesque town nestled in the heart of South Carolina, encapsulates a unique blend of southern charm, historic significance and modern convenience.

The overarching question — is Summerville, SC, a good place to live? — becomes easier to answer as one delves into the fabric of this quaint yet burgeoning locale. The aim of this article is to provide a well-rounded view of living in Summerville, the cost of living, employment opportunities and the social and cultural fabric that awaits newcomers and longtime residents alike.

Location, location, location

Summerville’s geographical positioning allows its residents to experience a plethora of sceneries and activities. Charleston Harbor is a mere 24 miles away, offering access to an expansive maritime vista, while a short drive to Folly Beach or Sullivan’s Island opens up a gateway to sun, sand and surf.

Demographic diversity in Summerville

The racial makeup of Summerville, SC, presents a mosaic of cultures, predominantly comprising white, Black, Latine and Asian communities, thus fostering a rich cultural blend. The inclusion of different ethnicities is a part of Summerville’s charm, allowing for a vibrant, multicultural community.

Historic significance

History aficionados would be drawn to Summerville’s rich history, with the town playing host to numerous historically significant sites. The Drayton Hall, Magnolia Plantation and the Aiken Rhett House Museum offer glimpses into the antebellum era and Civil War history.

Weather and natural disasters

While Summerville, SC, does experience hurricanes, the town has a solid infrastructure in place to manage and mitigate the effects of such natural disasters. Its inland location serves as a natural barrier, providing a level of protection against the harshest weather conditions.

Education and employment in Summerville, SC

Charleston Southern University, located a short drive away, is one of many educational institutions offering quality education to Summerville residents. The town also boasts a growing job market with varied employment opportunities, ensuring a stable economic outlook.

Recreational activities

The abundance of walking trails like the Oakbrook Nature Trail, and waterways such as Ashley River, provide ample recreational opportunities. The nearby Jessen Public Boat Landing is a favorite among boating enthusiasts.

Cost of living in Summerville

The cost of living in Summerville, SC, is generally lower than the national average, which is a significant draw for many. Housing, represented by a mix of historic homes, new construction, and Summerville homes in serene neighborhoods, is relatively affordable with the median home price being attractive to both young families and retirees.

Summerville’s real estate market

The real estate market in Summerville, SC is thriving, thanks to a boom in population growth and the subsequent demand for housing. Real estate agents are seeing an upward trend in property values, yet the cost of owning or renting a home remains affordable compared to many other regions in the South.

Culinary scene in Summerville, SC

The culinary palette in Summerville is as diverse as its populace. From smoked chicken to pork belly, ribeye steaks to fried green tomatoes, the food scene is a blend of traditional southern and modern cuisines. Restaurants and food trucks alike offer a wide range of food options, catering to different tastes.

Social aspects

Southern hospitality is alive and well in Summerville. The small town feel, coupled with the friendliness of Summerville residents, creates a welcoming environment. Community events like the Flowertown Festival are a testament to the town’s social cohesion, bringing together people from all walks of life.

Summerville’s growth trend

Summerville’s growth trend is a positive indicator of its viability as a place to live. The influx of more people, bolstered by opening doors of opportunity, is transforming the town while retaining its historic charm.

Conclusion

The blend of affordable living, a robust real estate market, promising job opportunities and a welcoming community makes Summerville, SC a great place to live. Its proximity to beaches, historic downtown Charleston and numerous tourist attractions, like the Folly Beach County Park, add to the allure.

Individuals and families considering moving to Summerville will find a balanced mix of historical essence, modern amenities, and a promising future. If you’re ready to make your move, take a look at our Summerville, SC, apartments for rent.

Nestled in the prestigious Spanish enclave of Son Vida in Palma de Mallorca — dubbed the Beverly Hills of Mallorca — a 21st-century avant-garde residence resembles something straight out of a Hollywood film.

Villa Chameleon is a one-of-a-kind futuristic villa with its own spa and fitness center, but that merely scratches the surface of its long list of unique features.

With an architecturally distinct three-building compound with a massive 35,294 square feet of living space, an illuminated fine crystal facade, and a multi-purpose swimming pool that can convert into a helipad or a state-of-the-art dance floor — the Spanish villa is an experience not to be missed by any 007 die-hard fans.

Especially since it’s the perfect modern-day James Bond villain lair, and we could easily see Ernst Stavro Blofeld, Auric Goldfinger, Raoul Silva or the likes take up residence in this striking abode.

Photo credit: The Agency

Built in 2012 by a Swiss-German consortium, the property first landed on the market in 2014 for a whopping €39.5 million, approximately US$52.2 million based on the exchange rate at the time.

Struggling to find a buyer willing to take over the property in a previously volatile Spanish real estate market, Villa Chameleon was relisted, nine years after its completion.

Now, the futuristic mansion is back on the market. Sporting a new asking price of €33 million (which amounts to a little over US$35 million) and new representation — Alby Euesden of The Agency Mallorca holds the listing — the modern Spanish villa is taking another stab at landing a new owner.

But more on that later. Let’s now take a moment to appreciate this James Bond-worthy residence.

LED lights grace 50% of its facade – one of the many hallmarks of Villa Chameleon

Photo credit: The Agency

With more than half of the building’s facade consisting of beautifully illuminated fine crystals, programmable LED lights, and custom-etched glass balconies, Villa Chameleon is bathed in an assortment of eye-catching colors.

If you haven’t already guessed, the villa takes its name from the mesmerizing lighting effects that transform its ambiance at the touch of a button.

Photo credit: The Agency

And just when you thought it couldn’t get any better, this lavish estate boasts a multi-purpose 1,830 square-foot retractable pool floor that can transform into a helipad or a state-of-the-art dance floor among its boundless amenities.

From entertaining guests alfresco to having a dance night out, the Burmese teak movable pool deck is designed for James Bond-style living — and is perhaps best accompanied with a glass of the obligatory Vodka Martini (shaken, not stirred) — symbolic of how James Bond takes his Martinis.

Even seasoned real estate pros who are somewhat immune to glam amenities and have seen hundreds of million-dollar listings throughout their careers are in awe of this property.

The Agency cofounder and CEO Mauricio Umanky — also familiar to audiences outside of the real estate world as Kyle Richards’ husband on The Real Housewives of Beverly Hills, as one of this season’s most hyped contestants on Dancing with the Stars, and a cast leader on Netflix’s newest docu-series, Buying Beverly Hills — had to travel to Mallorca, Spain to see it for himself.

And he did a little more than that.

Mauricio filmed himself touring the property, and you can see from the footage that even he is taken aback by the villa and its roster of amenities.

[embedded content]

That said, a James Bond-style mansion wouldn’t be complete without its very own five-star amenities, offering modern-day conveniences in all aspects of daily living for those who can afford it.

And this brings us to the inside of the property.

Stepping inside Villa Chameleon – a true Mediterranean oasis

Photo credit: The Agency

With panoramic views stretching from the stunning Mediterranean Sea to the cityscape and port of Palma de Mallorca, Villa Chameleon is a bona fide oasis.

The sprawling estate, perched atop the Son Vida hills in the prestigious Palma de Mallorca — and set just a 10-minute drive from Palma Old Town — has a total of 10 bedrooms and 9 full baths.

Photo credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The Agency

Much like the house’s exteriors, the interiors also change colors come nighttime, creating a mesmerizing effect.

Photo credit: The AgencyPhoto credit: The Agency

It also has 3 swimming pools, an underground five-car garage, a private cinema, an impressive wine cellar, a curated library, a fully-equipped health and wellness retreat, staff quarters and to top it all off, a 2,200 square foot self-contained guest house spread across the 1.61-acre lot.

Photo credit: The AgencyPhoto credit: The Agency

The main building is a three-story residence containing the main living space and master suites. This section of the living space includes a professional-grade kitchen, glass elevator, spacious terrace, and floor-to-ceiling glass walls with direct access to two rooftop pools.

Related: Skyfall, James Bond’s Childhood Home in the Scottish Highlands

The second building, connected by an underground tunnel, is perhaps the key secret to achieving a James Bond-like physique. This health and wellness facility includes a fully equipped gym, sauna, spa and indoor lap pool.

Photo credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The AgencyPhoto credit: The Agency

The guest house is nothing short of stellar — a self-contained, 2,200 square feet living space that comes with a wraparound Mediterranean garden and a private driveway, offering privacy and comfort.

First listed in 2014 for €39.5 million, the James Bond-worthy villa is now on the market for €33 million

The showstopping Mallorca home was initially listed for sale in 2014 for a whopping €39.5 million.

And while it didn’t land a buyer in its first turn on the market, the ultra-luxurious Palma de Mallorca villa is taking another stab at finding its new owner.

With a new listing price (that shaved off a few million $$$ from its former asking price), and new representation — the property is listed with Alby Euesden of The Agency Mallorca — Villa Chameleon is on the market for €33 million.

Photo credit: The Agency

More stories

The Magnificent Palazzo Lija on the Isle of Malta is an Architectural Feat with Modern-Day Amenities

Is the ‘Glass Onion’ house real? Yes, it is, and you’ll find it in Greece

Where Do Your Favorite F1 Drivers Live? 7 Fabulous Houses of Formula 1 Champs

Portland, an East Coast city and the largest city in Maine, offers a blend of old-world charm and modern sophistication.

Nestled amidst a beautiful coastline and lush greenery, this city has seen an uptick in popularity over recent years, drawing people from all walks of life.

But, is Portland Maine a good place to live? This comprehensive look aims to explore the facets of living in Portland from its food scene to housing costs, aiming to provide a holistic view of life in this quaint New England city.

Historical and cultural richness

Portland is steeped in history with its cobbled streets in the Old Port, Victorian architecture in the West End, and a thriving arts district along Congress Street. The city boasts an inclusive community that celebrates local artists during events like First Fridays. The Portland Symphony Orchestra further enhances the rich cultural tapestry of the city.

Nature and outdoor activities

With its proximity to both the Atlantic Ocean and white mountains of New Hampshire, Portland offers a plethora of outdoor activities. Casco Bay invites sailing and kayaking enthusiasts, while the nearby forests and trails are perfect for hiking, cross-country skiing or leisurely walks. Eastern Promenade and Back Cove offer stunning locales for outdoor relaxation and exercise, promoting a healthy lifestyle among Portland residents.

Gastronomic adventure

Dubbed as a ‘Restaurant City’, Portland prides itself on its thriving food scene. The city is synonymous with fresh seafood, especially its famed lobster rolls. Coffee shops, breweries and restaurants line the streets, serving everything from traditional New England fare to international delicacies.

Education

Portland Public Schools provide a solid educational foundation, serving a diverse student population. The city is also close to several reputed colleges and universities, providing a wide range of educational opportunities.

Employment and economic opportunities

Portland has a burgeoning job market, particularly in healthcare, education and the maritime industry. Small businesses also thrive here, supported by both locals and tourists.

Housing and cost of living

The real estate market in Portland can be quite competitive with housing costs being above the national average. While there are affordable housing options in nearby communities, the high demand in Portland has driven up real estate prices within the city limits. However, compared to other larger cities on the East Coast, Portland’s cost of living remains relatively moderate, making it an attractive option for many middle-income earners.

Public transportation

Portland offers a reliable bus system, making it easy to commute within the city and to nearby areas. However, the city’s compact size also makes it highly walkable, especially during the warmer months.

Social aspects

Young professionals, families and retirees find a welcoming community in Portland. The city’s population density allows for a small-city feel, yet it is bustling with activities and social events that provide a sense of a larger city vibrancy.

Pros and cons of living in Portland

Learn what’s most desirable and undesirable about living in this quaint coastal city.

Pros:

Rich Cultural Scene: Portland is a haven for art enthusiasts and those interested in historical architecture.

Outdoor Activities: Easy access to a variety of outdoor activities makes Portland a nature lover’s paradise.

Food Scene: The city is a hotspot for foodies, offering a vast array of culinary delights.

Community Feel: Portland residents enjoy a strong sense of community and friendly neighborhoods.

Educational Opportunities: Quality public schools and nearby higher education institutions are a plus.

Cons:

Cost of Living: The cost of living, particularly housing costs, can be a hurdle for some.

Winter Weather: The long, cold winters might not appeal to everyone.

Sizable Homeless Population: Like many urban areas, Portland faces challenges with homelessness.

Traffic: While not comparable to bigger cities, traffic, especially during rush hour, can be frustrating.

Conclusion: Moving to Portland, Maine?

Portland, Maine, offers a unique living experience with its rich history, cultural activities and beautiful surroundings. While the cost of living and winter weather may deter some, many find the community atmosphere, educational opportunities and the food scene well worth it. Its increasing popularity reflects the city’s appeal, making Portland Maine a very enticing place to consider as a home.

The array of experiences, from strolling down the cobblestone streets of Old Port to enjoying a fresh lobster roll by the bay, encapsulates the essence of living in Portland. For those who value a blend of nature, culture, and culinary delights, alongside a laid-back yet vibrant city life, Portland, Maine, might just be the perfect place to call home.

If you want to make your new home port in Portland, ME, take a look at our available apartments for rent.

US mortgage rates rose for the third week in a row but stayed just under the 7% threshold.

The 30-year fixed-rate mortgage averaged 6.96% in the week ending August 10, up from 6.90% the week before, according to data from Freddie Mac released Thursday. A year ago, the 30-year fixed-rate was 5.22%.

Elevated mortgage rates in the wake of the Federal Reserve’s historic rate-hiking campaign have taken home affordability to its lowest level in several decades. Buying a home is more expensive because of the added cost of financing the mortgage, and homeowners who previously locked in lower rates are reluctant to sell. The combination of low inventory and high costs has squeezed would-be homebuyers.

Rates have been above 6.5% since the end of May, and this week’s average rate matches the highest level since November.

“There is no doubt continued high rates will prolong affordability challenges longer than expected,” said Sam Khater, Freddie Mac’s chief economist. “However, upward pressure on rates is the product of a resilient economy with low unemployment and strong wage growth, which historically has kept purchase demand solid.”

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. The survey includes only borrowers who put 20% down and have excellent credit.

All eyes on employment and inflation data

The rate stayed elevated this week after the Federal Reserve highlighted its reliance on jobs and inflation data in its July monetary policy meeting and in recent comments.

Markets had been waiting for July’s inflation report, released Thursday morning. That report showed inflation rose in July to 3.2% annually, compared to a 3% annual increase in June. That was the first time inflation picked up in a year. The data also showed that shelter costs contributed 90% of the total increase in inflation last month.

“July’s Consumer Price Index holds significant importance for the Fed’s upcoming decisions,” said Jiayi Xu, an economist at Realtor.com.

That faster pace of price increases could support the Fed’s concern that the battle is not over, Xu said. The Fed also will consider the forthcoming August employment and inflation data prior to the next policy meeting, in September.

In addition, the most recent jobs report offered some mixed signals about the labor market, Xu said, including a smaller number of net new jobs added and a dipping unemployment rate.

“While July’s jobs report itself is very unlikely to have a direct impact on the Fed’s upcoming decision, the decline to a 3.5% unemployment rate may imply that more significant slowing is needed to align with the Fed’s projected year-end rate of 4.1%,” she said.

Affordability challenges remain

Borrowing costs will remain elevated until financial markets see an “all clear” signal from the Federal Reserve, accompanied by a stop in interest rate hikes, said George Ratiu, chief economist at Keeping Current Matters, a real estate market insights and content company.

While the Fed does not set the interest rates that borrowers pay on mortgages directly, its actions influence them. Mortgage rates tend to track the yield on 10-year US Treasuries, which move based on a combination of anticipation about the Fed’s actions, what the Fed actually does and investors’ reactions. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

Currently mortgage rates are running higher than they should be in relation to the 10-Year Treasury, given historical trends, he said. The spread between the 30-year fixed rate mortgage and the 10-year Treasury hovers around 300 basis points, Ratiu pointed out, a level seen only a handful of times in the past 50 years and mostly during periods of high inflation and economic turbulence.

“In the absence of the elevated risk premium and hewing closer to a historical average of 172 basis points, today’s 30-year fixed mortgage rate would be around 5.7%,” Ratiu said.

Homebuyers remain sensitive to elevated interest rates, with applications for mortgage rates dropping last week, according to the Mortgage Bankers Association.

“Due to these higher rates, there was a significant pullback in mortgage application activity,” said Bob Broeksmit, MBA president and CEO. “Both prospective buyers and sellers are feeling the squeeze of higher rates as well as low housing inventory, which has prompted a pronounced slowdown in activity this summer.”

While real estate markets are benefiting from more people gaining jobs and better paychecks this year, sales of existing homes have been lagging, said Ratiu.

“The challenge comes mainly from too many buyers chasing not enough available properties,” he said.

Looking to history as a guide, Ratiu said mortgage rates tend to start cooling once inflation abates, with a six-to-eight-month lag.

Shopping for a mortgage has never been easier, thanks to the array of online options. Brick and mortar lenders may still be a viable option, but you may find that an online lender has even more to offer.

Furthermore, exploring online mortgage lenders allows you to compare mortgage rates. You can also receive customized mortgage loan offers in your inbox in minutes. Even better, you’ll have direct access to a loan officer in case you have questions.

Who are the top online mortgage lenders for 2023?

If you’re in the market for a new home and ready to start your search for online lenders, here are some reputable options to choose from.

Best Online Mortgage Lenders of 2023

loanDepot

loanDepot is an online lender, but don’t think that means they are lacking in customer service. They provide over 150 loan stores across the country for customers that prefer in-person service.

The lender is a suitable option for anyone who wants to take out a mortgage with the assistance of a loan officer.

loanDepot offers various mortgage products, including fixed and adjustable-rate mortgages. You can also apply for jumbo loans, VA loans, and FHA loans. You’ll need a minimum credit score of 620 to qualify for a mortgage.

loanDepot ranks high in customer satisfaction and most buyers seem to have a good experience working with them. However, they do charge higher fees than other mortgage lenders.

Quicken Loans

This online lender takes the hassle out of securing a mortgage by letting you complete the entire process online.

You’ll need to provide a few key details about your finances using this form to get started. A Home Loan Expert will review your application and contact you to discuss loan options.

And no need to worry about getting overwhelmed. Quicken Loans offers online tools to help you understand loan options and the home buying process. Plus, the customer service is excellent; a live representative is always standing by.

You can also upload all your documents and monitor the status of your application directly from the portal. This means you never have to pick up the phone if you don’t want to.

And when you’re ready to close, you have the option to schedule the closing when it’s convenient for you.

Better.com

If you’re looking for an online mortgage lender, you should check out Better.com. The company uses technology to simplify the lending process for its customers. Better.com promises a fast and transparent mortgage experience.

The lender is willing to work with all different kinds of buyers, including individuals who are self-employed or have unique job situations.

At least a third of its mortgages are taken out by first-time homebuyers, and over 70% of all buyers pay a down payment that is less than 20%.

Better.com mortgages don’t come with any hidden fees; there are no application or origination fees. To get started, you can visit the company’s website and get pre-approved in just a few minutes.

Rocket Mortgage by Quicken Loans

Rocket Mortgage is a division of Quicken Loans. Their key competitive advantage is the asset importer tool, which takes the guesswork out of determining whether you’re approved.

Instead of uploading documents, importing them from the information provider guarantees the accuracy of the numbers and allows you to receive loan offers using real-time interest rates in a matter of minutes.

And once you’ve selected a loan that works for you or created a custom option, you’ll be able to close in record time. Plus, Rocket Mortgage customer service experts are standing by to assist with questions you may have every step of the way.

NBKC Bank

NBKC Bank is not as widely known as many of the other lenders on this list. But that doesn’t mean you should rule them out as a potential mortgage lender.

There are several features that make the Kansas City-based lender a great option. The bank promises fast home closings and provides exceptional customer service.

NBKC Bank focuses mostly on online mortgages and offers its customers competitive interest rates. It does have several brick-and-mortar locations but focuses mostly on processing online mortgages.

You’ll need a minimum credit score of 620 to qualify for a mortgage, so this is a suitable option for borrowers with fair credit. NBKC Bank offers various mortgage products, as well as personal accounts. This makes them a great option for anyone looking for a full-service lender.

Guaranteed Rate

You can apply for a mortgage in a matter of minutes from the homepage of this digital mortgage provider’s site.

All you have to do is answer a few questions about your desired home, credit, and finances to receive a comprehensive listing of loan types and interest rates you may qualify for.

Guaranteed Rate has plenty of no-down-payment loan options like VA loans and USDA loans. They also offer a knowledge center to help you understand mortgages and how the process works.

Once you decide on a mortgage product that best suits your needs, you’ll work directly with a loan expert to upload and sign documents and finalize the loan. If you prefer to meet with a loan expert, there are 170 Guaranteed Rate branches across the United States.

Truist

Truist is known for its brick-and-mortar presence, but they also have an impressive online mortgage platform. Available in English and Spanish, Truist mortgage offers an array of mortgage solutions to choose from.

You can initiate the application process online or directly from your mobile device through the SMARTGUIDE tool.

You can also call 877-907-1020 to speak with a loan officer or chat online from the website. Or if you wish to meet with a loan officer, use the locator tool to find a Truist branch near you.

You can also take advantage of their Doctor Loan program if you’re a medical professional and meet select income criteria.

SoFi Mortgage

SoFi mortgage is another online lender that stands out from the masses. Although they don’t offer government-backed home loans, SoFi mortgage has programs that require a down payment as low as 10 percent, and they do not assess mortgage insurance.

Customers also enjoy a seamless prequalification and application process, along with no origination fees. Even better, it may be possible to close on your loan in under 30 days.

Penny Mac

If you’re searching for flexibility, Penny Mac may be the ideal lender for you. They offer several options to consumers of varying financial backgrounds. To date, they’ve served over 1 million customers and funded over $5 billion in loans in 2017, alone.

You can request a no-obligation free quote online, chat with an expert, or call (888)870-6229 to get started.

Reali

Crediful’s rating

Reali caters to consumers looking to purchase or refinance their homes. Through their Interactive Loan Dashboard, you can apply, upload any documents needed, and track your loan’s progress at the tap of a fingertip.

You’ll also have access to a Home Loan Advisor 24/7 to address any concerns you may have. And because of their streamlined process and low fees, you can expect to close in record time without spending a fortune.

Unfortunately, Reali does not offer government-backed products, like FHA loans, USDA loans, and VA loans.

This can be a turnoff to first-time, credit-challenged, or cash-strapped buyers.

Another major drawback is that they only operate in Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, Oregon, Pennsylvania, Texas, Virginia, and Washington.

The good news is they plan to expand their offerings to more states soon.

Pros and Cons of Online Mortgage Lenders

The rise of the internet has revolutionized many industries, and the mortgage industry is no exception. Online mortgage lenders have steadily been gaining a more substantial market share due to their distinct advantages. However, as with anything, they come with their own set of disadvantages. Here, we break down the pros and cons of opting for an online mortgage lender.

Pros of Online Mortgage Lenders

1. Lower Costs: Operating primarily online, these lenders often have fewer overhead costs compared to traditional brick and mortar lenders. This can translate into competitive mortgage rates and lower lender fees, making online mortgage lenders potentially cheaper.

2. Convenience: The ability to initiate and complete the entire application process online is a significant advantage. You don’t have to schedule meetings with a loan officer or travel to a bank branch. Instead, you can apply anytime, anywhere, which fits well with busy schedules and modern, on-the-go lifestyles.

3. Range of Loan Products: Online mortgage lenders often offer a broad range of loan products, including FHA and VA loans, USDA loans for rural properties, conventional loans, and jumbo mortgages. These lenders often cater to a diverse demographic, meaning whether you’re a first-time homebuyer seeking down payment assistance, a veteran, or someone with less-than-perfect credit, you can often find an online mortgage product that suits your needs.

Cons of Online Mortgage Lenders

1. Technological Hurdles: Not everyone is tech-savvy. If you’re not comfortable navigating online platforms or don’t have reliable internet access, you may find the online mortgage process daunting. The learning curve associated with digital platforms can be a deterrent for some people.

2. Lack of Personal Interaction: Some people prefer a high-touch, personalized service when dealing with significant transactions like buying a home. With online lenders, face-to-face interaction is usually minimal or non-existent, which can be a downside for those who prefer a more traditional approach to their financial transactions.

3. Negotiability of Fees: While online mortgage lenders are often cheaper, certain costs like origination fees and closing costs may not be as negotiable as they could be with a traditional lender. Also, mortgage insurance may still be required for government-backed loans, like FHA or VA loans, and the requirements for jumbo loans may be stricter.

4. Trustworthiness: The online space can be a breeding ground for scams and unscrupulous practices. Not all online mortgage lenders are trustworthy, making it crucial to do your homework. It’s important to research each online lender thoroughly, checking their reputation, reading customer reviews, and ensuring they are registered with appropriate financial oversight institutions.

Despite these potential downsides, many homebuyers find that the convenience, competitive rates, and the ability to shop around from multiple lenders offered by online mortgage lenders outweigh the cons. But the best online mortgage lender for you ultimately depends on your personal finance needs, comfort level with technology, and unique home loan situation.

Factors to Consider when Choosing an Online Mortgage Lender

Finding the right online mortgage lender for your home-buying journey involves more than just hunting for the lowest interest rate. You need to consider a variety of factors, from loan types to the speed of loan processing. Here’s a breakdown of what to look for:

Interest Rates

As a prospective borrower, interest rates are often one of your first considerations. The interest rate can significantly influence your monthly mortgage payment and the total cost of your loan. Due to their lower overhead costs, online mortgage lenders often advertise competitive rates. However, it’s essential to compare rates across different lenders to ensure you’re getting the best deal.

Fees and Hidden Charges

While interest rates play a crucial role in determining your loan cost, it’s equally important to consider fees and potential hidden charges. This could include origination fees, appraisal fees, closing costs, and other service charges. Some lenders may also charge additional fees for rate locks or early repayments. Always ask for a comprehensive cost breakdown and be wary of lenders who are not transparent about their charges.

Loan Types

Each online mortgage lender may offer a variety of loan types, such as FHA loans, VA loans, conventional loans, and more. Depending on your personal circumstances and needs, you might need specific loan products like USDA loans for rural properties, FHA or VA loans for a low down payment, or jumbo loans for larger properties. Ensure that the lender you choose caters to the type of loan that suits your situation best.

Customer Service and Support

Excellent customer service is crucial when dealing with online lenders as your primary communication methods will be via phone, email, or online chats. Lenders who offer high-quality customer service can significantly streamline the mortgage process, making it less stressful for you. Consider checking customer reviews and ratings for insights into a lender’s customer support.

Speed of Loan Processing

The time it takes for online mortgage lenders to process your loan application and close your loan can vary. If you’re working within a specific timeframe, you may prefer a lender known for quick processing. This is particularly crucial in competitive real estate markets, where being able to close swiftly could make all the difference.

Pre-approval Process

A seamless pre-approval process can signify an efficient online mortgage lender. Pre-approval offers you a rough estimate of how much you can borrow and helps you stand out in competitive property markets. Seek lenders that provide easy pre-approvals, preferably with only a soft credit check to avoid impacting your credit score.

User-friendly Technology

With most of your interaction with online lenders taking place digitally, user-friendly technology becomes paramount. Consider factors such as the simplicity of the application process, online document upload functionality, digital signature capabilities, and the ease of online loan tracking. A lender with a robust, intuitive platform can significantly simplify your online mortgage process.

Tips for Applying for a Mortgage Online

Embarking on the journey of applying for a mortgage online can feel overwhelming, especially if it’s your first time. But don’t worry – we’ve got some helpful tips to guide you through the process.

How to Prepare

Before you start your online mortgage application, it’s important to get your financial house in order. Here’s how:

Check your credit score: Your credit score is one of the main factors that lenders consider when evaluating your loan application. Make sure to check your credit reports for any errors and dispute them if needed. If your score is low, you might want to consider improving it before applying for a mortgage.

Verify your income: You will need to provide proof of income, so gather your recent pay stubs, W-2s, or tax returns. If you’re self-employed, you may need to provide additional documentation, like bank statements or profit and loss statements.

Get your documents in order: Apart from income verification, you’ll need other documentation, like identification, proof of assets, and information about your debts. Having these documents ready can speed up the application process.

Navigating the Application Process

Once you’re ready to apply, keep the following in mind:

Understand the terms: Make sure you understand the terms of the mortgage, like the interest rate, whether it’s fixed or adjustable, the length of the loan, and any fees involved.

Use online tools: Many online lenders offer useful tools like mortgage calculators. These can help you understand what your monthly payments might be based on different interest rates and down payment amounts.

Stay organized: Keep track of where you are in the application process. Most online platforms will save your progress, but it’s good to have your own record too.

Questions to Ask Your Lender

Securing a mortgage can often feel like a daunting process, particularly when applying online. To navigate this path with more confidence, it’s crucial to arm yourself with the right questions when engaging with potential lenders. The responses to these questions will not only give you a clearer idea about the mortgage terms but also about the lender’s transparency and commitment to customer service.

What types of loans do you offer?

The world of mortgages encompasses a variety of loan types designed to cater to different borrower needs. This includes conventional loans, government-backed loans such as FHA, VA, and USDA loans, and jumbo loans for larger mortgages.

Understanding the unique benefits and requirements of each type is important. For example, FHA loans may be suitable for those with lower credit scores, while VA loans are primarily designed for veterans. Your potential lender should be able to provide a comprehensive explanation of each option and help guide you towards the loan type that best fits your unique situation.

What are the interest rates and APR?

While the interest rate of a loan often takes center stage, the Annual Percentage Rate (APR) should not be overlooked. The APR provides a more comprehensive measure of cost as it includes the interest rate, lender fees, and other loan charges, offering a more complete picture of the long-term cost of the loan.

What fees are involved?

Beyond the interest rate, mortgages often involve several other fees that can impact the overall cost of the loan. These include origination fees, appraisal fees, home inspection fees, and potentially prepayment penalties. Some lenders may even charge for rate locks, which secure your interest rate for a specified period. It’s critical to ask for a detailed breakdown of all fees involved to ensure that there are no hidden costs that might surprise you down the line.

What Is the estimated timeline for approval and closing?

Mortgage approval and closing timelines can vary greatly among different lenders. Knowing the expected timeline can be crucial, especially if you’re working with a specific move-in date. In a competitive real estate market, a quick approval and closing process could make all the difference when multiple offers are being considered.

What are your minimum credit score and down payment requirements?

Understanding a lender’s minimum credit score and down payment requirements can help you gauge your chances of approval. These requirements can vary greatly depending on the loan type and the individual lender’s policies.

Do you consider alternative credit data?

For those with a limited credit history, some lenders may consider alternative credit data such as utility bill payments or rent payment history. Asking about these possibilities could potentially help you qualify for a loan even with less conventional credit information.

What is your process for loan servicing?

Understanding whether the lender will service your loan or if they intend to sell it to another company is important. If they plan to sell it, knowing who your point of contact would be for any issues or inquiries is crucial.

Bottom Line

Choosing an online mortgage lender is a significant decision that can impact your financial situation for years to come. Therefore, it’s critical to take the time to carefully evaluate each lender. From comparing interest rates to analyzing the type of customer service they offer, there are many factors to consider in this selection process.

We’ve touched upon some of the best online mortgage lenders available today. These lenders were chosen based on their competitive rates, comprehensive loan options, excellent customer service, and user-friendly platforms. However, remember that the “best” lender will vary depending on individual circumstances, and the top choices for others might not be the best for you.

While online mortgage lenders offer convenience and often competitive rates, they also come with their unique set of challenges. It’s vital to remember that transparency, trustworthiness, and a clear understanding of the terms and conditions are paramount in any financial decision, including choosing a mortgage lender.

We encourage you to conduct your own research and take advantage of online tools and resources that many of these lenders offer. Shopping around and comparing multiple lenders will help you find the best mortgage fit for your specific needs.

Remember, a mortgage is a long-term commitment. The time and effort spent in making a careful, well-researched decision now will pay dividends over the life of your loan. Happy home hunting!