Home is where we spend most of our time, the safe space that welcomes us at the end of a long day, the special place where we raise our families, bond with our loved ones, or retreat to for some well-deserved solitude.

And much like everything else in life, our home needs to be properly taken care of. I’m not talking about property improvements, upgrades or anything fancy.

Today, we just want to go over some general home maintenance aspects that you’re likely well aware of, but we’re hoping that a little reminder will help bring them to the forefront.

There are many things you can do, from doing regular maintenance with proper cleaning products like the ones from HG to taking extra safety measures. When you take care of your home properly, it will be the most comfortable place in the world. Keep reading to learn more about how you can achieve that.

Perform regular maintenance

The first tip to make your home is always in top condition is to perform regular maintenance.

This usually includes inspecting some points in your house, such as pipelines, roofs, ceilings, and HVAC systems. When you find something wrong at one or some of those points, you have to quickly address the issue.

Of course, you can always rely on professionals who are specialized in fixing such problems if you don’t feel like you have the expertise to do it yourself.

Make a regular cleaning schedule

The next tip is to keep your house clean at all times by making a regular cleaning schedule.

You can set the cleaning schedule once a month, twice a month, or even once a week depending on how often your home gets cluttered. Usually, the more people living in the house, the more easily it gets cluttered and accumulates dust.

Photo by Josue Michel on Unsplash

You can adjust your regular cleaning schedule based on how many people live in your house. Besides, you have to stock up on several kinds of cleaning products to make your regular cleaning activities much easier.

Take security measures

Another thing you must not miss when taking care of your home is to take security measures.

This is very important because the safety of your house as well as its inhabitants must be a key priority. And this doesn’t only mean safety from burglars who can break into your house. It also means keeping your home safe from hazards such as fire and potential short circuits.

A few easy ways to achieve this is to ensure your home has all the basic security features like security locks, smoke detectors, and fire extinguishers. It’s also a good idea to install an alarm system and several CCTVs around your home (if your budget can accommodate that) to make it more secure.

Photo by Sebastian Scholz (Nuki) on Unsplash

Perform landscaping and outdoor maintenance regularly

To make your home more comfortable and aesthetically pleasing, you have to perform landscaping and outdoor maintenance regularly.

This is very important because the exterior of your house can change drastically if you don’t tend to it regularly. One of the most important outdoor maintenance activities that you have to do is to mow your lawn due to how fast weeds grow.

You also have to trim bushes and trees if you have any in your yard. You also have to check the drainage to make sure it’s not blocked by dirt.

More stories

7 Top Decorating Ideas for Your Bedroom this Fall: Making Your Room More Cozy & Stylish

Here’s Everything You Need to Set Up a Meditation Corner in Your House

10 Unique Picture Frames and Holders to Create the Perfect Photo Wall

Do you want to learn how to find online typing jobs? There are many online typing jobs that may suit you well, and today’s article will help show you where to look. How to find online typing jobs What are online typing jobs? An online typing job is a job where you simply need an…

Do you want to learn how to find online typing jobs?

There are many online typing jobs that may suit you well, and today’s article will help show you where to look.

How to find online typing jobs

What are online typing jobs?

An online typing job is a job where you simply need an internet connection in order to work. You may be working for yourself as a small business owner or freelancer, or working for a company as an employee.

You can find online typing jobs in many different places, such as job boards, through recruiters, by networking, and more. Some job websites that you may be interested in include Upwork, FlexJobs, Indeed, Monster, and more.

Related content:

How much money can you make with an online typing job?

The amount of money that you can make with an online typing job varies.

This is because there are so many different types of jobs where you are typing online!

From starting your own blog to becoming a proofreader, live chat agent, transcriptionist and more, there are many, many different types of online typing jobs. And, they all pay a different amount of money. You can see below what some of them have for starting pay.

What are the pros and cons of an online typing job?

Pros of online typing jobs include:

If you are a fast typer, then this may be an easy gig for you

You can work from home

You may be able to have a flexible work schedule

You probably already have a laptop or computer, so you probably don’t need much in terms of equipment to get started

Cons of online typing jobs include:

Some online typing jobs may be a little repetitive. While this isn’t always a con, it could be for some

There are some scams out there, so you will need to do your research and make sure it’s a legitimate online typing job that you are looking at

What skills does an online typing job need?

The skills that you need will vary depending on the online typing job that you are interested in. But, some important ones for most will include accuracy in typing and a fast typing speed.

14 Best Online Typing Jobs

Below are the 14 best online typing jobs for beginners.

Blogger

My favorite online typing job is to start your own blog.

I spend most of my working time typing, and I really enjoy it!

Blogging allows me to travel whenever I would like, work from home, have a flexible schedule, earn an income, and more.

I created Making Sense of Cents in 2011, and since then I have earned over $5,000,000 with my blog.

My blog was created on a random day as a way to track my own personal finance progress. And when I first started my own blog, I honestly didn’t even know that people could make money blogging or how to start a successful blog!

I did not create Making Sense of Cents to earn money from home, but after only six months, I began to make money.

Blogging is quite affordable to start too, and you really just need a computer and an internet connection. I spend most of my time typing new blog posts, talking to readers and companies through email, and more.

You can sign up to learn how to start a blog with my free How To Start a Blog Course.

Proofreader

Proofreading is a flexible and detail-oriented job that only requires a laptop or tablet, an internet connection, and a good eye for finding mistakes.

Oh yeah, and accurate typing skills!

Proofreaders look for punctuation mistakes, misspelled words, lack of consistency, and formatting errors.

You might be proofreading books, articles, blog posts, student essays, lessons, scripts, emails, advertising content, medical documents, and more – anything that can be delivered electronically and be proofread on a computer or tablet.

You can learn more at How To Start A Proofreading Business And Make $4,000+ Monthly.

Sell printables on Etsy

Selling printables is an online job where you may be typing, creating graphics, and more.

Making printables on Etsy can be a great way to earn an income because you just need to create one digital file per product, which you can then sell an unlimited number of times.

So, what exactly is a printable?

Printables are digital products that customers can download and print at home. Some ideas for printables include grocery shopping checklists, gift tags, printable quotes for wall art, and more.

You can sign up for this free ebook that helps you figure out where to start when it comes to selling printables on Etsy.

You can also learn more at How I Make Money Selling Printables On Etsy.

Online bookkeeper

A bookkeeper is someone who tracks the finances of a business. As an online bookkeeper, you would be typing from home.

And, yes, you can start this even if you are brand new.

Online bookkeepers are in high demand. If you’ve been wanting to work from home and want to earn $40,000+ each year, bookkeeping could be perfect for you.

As a bookkeeper, you are responsible for helping businesses take care of their finances, such as by tracking receipts and spending.

A bookkeeper is someone who helps manage and track the financial side of a business. They will typically keep track of sales and expenses, and produce financial reports.

Those with virtual bookkeeping jobs work remotely from home, and they do not physically need to go into the office. Bookkeeping is an excellent option for remote work because all of a bookkeeper’s work can be done online or with computer software.

I recommend checking out the free How To Become An Online Bookkeeper Workshop to see if becoming a bookkeeper interests you.

Freelance writer

Freelance writing is a very popular career path, and I think it will only continue to grow!

And, you would be typing all the time. If you like to type, then this may be a great fit for you.

A freelance writer is someone who writes for a number of different clients, such as websites, blogs, magazines, news publications, and more. They don’t work for one specific company, rather they work for themselves and contract out their writing.

If you have a fast typing speed, then you can also write more blog posts and earn a higher income.

Learn more at How I Earn $200,000+ Writing Online Content.

Virtual assistant

As a virtual assistant, you would be typing from home and doing a variety of tasks.

The internet allows us to complete more daily tasks online, and more and more people also have stay-at-home jobs and businesses, such as running a website, social media, real estate, advertising, etc. That’s why virtual assistant jobs are in high demand.

Virtual assistant tasks may include:

Managing social media

Formatting and proofreading content

Scheduling travel and appointments

Managing email

Maintaining spreadsheets

Handling phone calls

And so much more. As a virtual assistant, you can get paid to do any task that needs to be done in someone’s business but doesn’t need to be done by them.

You can learn more at How This Virtual Assistant Earns $10,000 Month From Home as a Virtual Assistant.

Survey taker

Paid online surveys aren’t a full-time job, but if you’re looking for something that just takes up a little bit of your time each month, then this may be one to look into.

As a survey taker, you would mainly be completing surveys online from your laptop. You would be answering questions and simply just giving your feedback. Usually, you are paid via money sent to your PayPal account, gift cards, and free items.

Companies need people to take surveys so that they can see what the public thinks about their product and company, so that they know what to improve.

People typically sign up for as many survey companies as they can, as you usually won’t receive more than just a few surveys from a company each month.

Below are the companies I recommend signing up for:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

PrizeRebel

User Interviews

Book reviewer

As a book reviewer, you can get paid to type from home, as you would be typing reviews for books that you have read!

There are websites that will pay you to review books, or you could even start your own book review blog. Each site varies, but you are typically paid cash via PayPal or bank transfer, or you may receive a free book in exchange for your review.

Here are some of the best websites for online typing jobs that will pay for you to review books:

Online Book Club – With this website, you are only paid with a free book for the first review. After the first review, you will be eligible to be paid for the book review opportunities, plus the books will always be free. With this website, you can get paid around $5 to $60 for each book that you review.

Kirkus – This platform is looking for book reviewers of English and Spanish language books. They need reviews that are about 350 words long, and they are due two weeks after you are assigned to read a book.

Upwork – With Upwork, you would need to create your own profile and make a listing as a book reviewer. This way, clients and authors can find you and hire you directly to read their book and review it. Plus, on Upwork, you can set your own pricing and decide which clients you want to work with.

The US Review of Books – This website uses freelance writers to review books and write reviews that are around 250 to 300 words long.

Reedsy – Here, you can review hundreds of different books before they are published and earn money at the same time. Authors submit their books to Reedsy, specifically to be reviewed by book reviewers. You then get paid by readers (those who buy a book) as a tip for the review. These tips can be $1, $3, or $5.

Booklist – This website pays for reviews that are around 150 to 175 words long that describe the plot, suggest an ideal audience, etc. Booklist pays $15 for each published book review.

Related content: 7 Best Ways To Get Paid To Read Books

Translator

Are you fluent in another language? If so, then you may be able to find an online typing work-from-home job where you translate content, books, articles, and more.

There are lots of places you can find translation jobs, including:

Upwork – On Upwork, you simply create a free profile and apply for translation jobs.

Babelcube – This is a website that sends freelance translation projects to you. You select which books you translate, translate them to one of more than 15 different languages, and partner with published authors.

Guru – Guru is a website that lists freelance writing and translation jobs.

Indeed – Indeed lists translation jobs that they find from job boards, staffing firms, company websites, and more.

FlexJobs – It will cost you to join FlexJobs, but they do list translation jobs, which can be worthwhile.

Today Translations – This is a website that is looking for translators to freelance for them.

Fiverr – Fiverr is an online marketplace where you can find freelance jobs all over the world. You can list your translation services and pricing here.

Ulatus – Ulatus is a website that provides translation services and they hire translators.

As you can see, there are lots of options if you want to put your translation skills to work.

Transcriptionist

Transcription work is when you turn audio or video content into a text document.

There are many businesses looking to fill positions for online transcription jobs since general transcriptionists convert audio files and video to text for virtually any industry. Some examples include marketers, authors, filmmakers, speakers, conferences, legal transcription, and more.

Online transcriptionist jobs can start around $15 an hour to begin with.

You can learn more about becoming a transcriptionist in the interview Make Money At Home By Becoming A Transcriptionist. The interview explains:

What a transcriptionist does

How much you can earn transcribing content

The type of training you need

How to find transcription jobs

And more!

Another online typing job similar to this is captioning, and I know we have all seen captions before. Captioning is when you transcribe a video and synchronize it with the video.

Live chat agent

Many large companies outsource their customer service departments to people who are working at home and they usually pay via an hourly wage.

This means you may be able to find a job as an online chat agent.

Customer service representatives may be responsible for a number of things, like:

Working as an online chat agent

Offering technical support

Providing customer support

A typing job as a customer service representative may be that you respond to help/support requests online, such as through an online live chat, or email support.

Affiliate marketer

I am an affiliate marketer through this blog, Making Sense of Cents, and I spend most of my working hours typing.

I think this can be a great way to earn income if you are interested in finding an online typing career path.

Affiliate marketing is when you earn an income by placing a referral link on your website, blog, Instagram, and so on and have people purchase a product or service through your referral link.

An example would be selling a book and you link to a specific book on your blog and try to get people to purchase the book through your affiliate link.

If you get someone to sign up through your affiliate link, the company (such as Amazon) pays you for sharing the product that they sell through the affiliate link.

If you want to learn more about affiliate marketing, I recommend signing up for Affiliate Marketing Tips For Bloggers – Free eBook.

Scopist

As a scopist, you would be typing from home.

Scoping is when you are editing legal documents for court reporters. This is different from proofreading for court reporters.

Scopists who are working with a court reporter tend to earn around $30,000 to $45,000 each year working around full-time hours.

I interviewed an expert on the topic – Linda from Internet Scoping School. She has been scoping for over 35 years and has taught scoping online for around 20 years.

She has a free course that will introduce you to scoping so that you can decide if it’s one of the online business ideas you want to pursue. You can find the free course by clicking here.

You can learn more at How To Become A Scopist.

Google rater

A search engine evaluator (also known as a Google rater) is a person who rates websites based on their quality and usefulness.

You are rating websites to help Google improve its search engine results.

This can be a great online typing job for beginners because you don’t need experience in this area to start, nor do you have to know what you are doing. This is because Google wants average people rating their sites.

Another great thing – since Google operates in nearly every country around the world, you can work on sites that are in your native language.

Learn more at How To Become a Search Engine Evaluator.

Are online typing jobs legitimate?

Yes, online typing jobs are real and legitimate.

I work online and I know many, many other people who also work online and spend most of their day typing.

Many companies hire online workers, and there are many different kinds of online typing businesses that you can start as well.

There are so many online typing jobs, especially in today’s day and age. I recommend seeing which ones you are most interested in and learning more about them.

Online Typing Jobs – Summary

As you can see, there are many different online typing jobs that may interest you.

Depending on your typing speed, accuracy, skills, whether you are looking for full-time or part-time jobs, if you need entry-level work, and more, there are many different online typing jobs that may interest you.

These may include typist jobs such as:

Blogger

Proofreader

Sell printables on Etsy

Bookkeeper

Freelance writer

Virtual assistant

Survey taker

Book reviewer

Translator

Transcriptionist

Live chat agent

Affiliate marketer

Scopist

Google rater

What do you think are the best online typing jobs?

By waiting for mortgage rates to fall, buyers could risk losing out on their dream home.

Getty Images

As long as inflation is still persistent — and above the Federal Reserve’s 2% goal — interest rates will remain elevated. In fact, after months of cooling inflation actually ticked back up in July. And the benchmark interest rate now sits at a 22-year high.

Mortgage interest rates have also suffered in recent months. After hovering around record lows in 2020 and 2021, rates have risen exponentially and now currently sit around 7.5%. Rates on mortgages are the highest they’ve been in decades, leaving homebuyers with a series of poor options.

That said, even with rates as high as they currently are, there are some compelling reasons why buyers should act now and stop holding out for a better rate environment.

Start by exploring your mortgage rate eligibility here now.

4 reasons why you shouldn’t wait for mortgage rates to drop

Here are four reasons why buyers shouldn’t wait for mortgage rates to fall.

Rates could go higher

Sure, rates are high now, but what happens if they rise even further? Don’t dismiss the possibility of additional rate hikes. Federal Reserve chair Jerome Powell has already implied that additional rate increases could be coming in 2023. If that doesn’t happen this month, then don’t be surprised if it comes around the holidays.

That could be devastating news for those buyers who were planning on timing the market to improve their rate offer. While a 7.5% interest rate isn’t anyone’s idea of a great deal, it could prove to be a desirable one when compared to the prevailing rate in November, December or even January 2024. Just ask those who locked in a “high” 6% rate earlier this year.

Check rates and terms here now to learn more.

You may lose your dream home

Your dream home may only come on the market at one time, and it may not be during the most favorable rate environment. So don’t make perfect the enemy of the good and skip out on the chance to buy the home.

“Date the rate and marry the home,” most experts advise. In other words: The interest rate you secure now is temporary and can (and likely will) be adjusted in the future. But the dream home available now could be gone forever. Adjust your purchase plans accordingly.

You could refinance in the future

Mortgage rates and mortgage refinance rates are both elevated now. But they won’t be forever, at which point you could refinance to a lower rate and, potentially, even better terms.

So don’t feel like you’ll be saddled with a higher rate forever. While experts don’t agree on when rates will come down (and by how much), they all do agree that they will come down at some point — giving you an opportunity to take advantage and pay less.

The rate may not be as bad as it looks

Don’t get discouraged by the rate you find online. There are multiple ways you can secure something lower. This includes (but is not limited to) taking out an adjustable-rate mortgage (which comes with a lower introductory rate before changing over time) or purchasing mortgage points from the lender (to secure a permanently lower rate).

Neither option is ideal and both should be approached cautiously. But both options can save buyers money with a lower rate now. And that extra money could be very helpful to have in today’s economy.

Learn more about your mortgage options here now.

The bottom line

While mortgage rates are high today, buyers should be judicious about their approach. Waiting for them to drop back to pandemic-era lows may not be the wisest move. Instead, buyers should understand that rates could go even higher. And, if they wait for them to stabilize, they may lost the chance to buy their dream home. Plus, they could always refinance to a lower rate in the future — or get a lower one now by applying for an adjustable-rate mortgage or buying mortgage points from their lender.

HousingWire Editor in Chief Sarah Wheeler sat down with John Ashley, chief information officer and chief information security officer at PRMG, to talk about what the company is building versus buying, and how regulators are ramping up privacy and security standards.

Sarah Wheeler: Tell me a little bit about your background and what you’ve done at PRMG.

John Ashley: I’ve collaborated with PRMG since late 2005 and my background was network infrastructure and security. In my career, I’ve swung between enabling technology and securing it at the same time.

Within mortgage, we’ve done everything here at PRMG: multiple lending platform LOS systems, multiple changes of those systems, multiple changes of pricing engines, marketing systems, marketing platforms, CRMs, infrastructure security systems moving to the cloud for most of our infrastructure — I’ve been behind all of that over the last 10 to 15 years.

SW: How many tech people do you guys have?

JA: Within the IT department, we have about 60. So, we’re not little, but we’re not big, like some of these companies with 500 developers. We have smaller teams, but they’re very effective.

SW: At PRMG, do you generally build or buy technology?

JA: We do both. We have a development team and so we have software developers, system analysts, business analysts, quality assurance testers, and people that manage deployments. So, we can and do build stuff, but we tend to try to find solutions just for the speed of getting things up and we find ourselves doing a lot of integration or extending systems that we have.

A great example of this is the Encompass platform, which has been around a long time. And while it’s kind of long in the tooth in many respects, ICE has done a fantastic job in building out their back-end developer, connecting their API and micro services. So now you can extend so much from the Encompass platform. And we’ve taken other products and hooked them to Encompass — we have a pretty innovative work queuing system for our fulfillment people, within operations, that’s all been enabled by using a different third-party product. We tend to lean towards buying and extending, but we do a lot of custom stuff as well.

SW: What’s been the biggest change since you started at PRMG in 2005?

JA: I was going back through some old PRMG stuff and they had “the five tenets of mortgage lending success” and it was: product, pricing, compensation, marketing, and fulfillment. Well, technology is now the sixth tenet, because you can’t do any part of the other ones without the technology and that’s where the big change has happened. People are just clamoring for technology to get an edge, especially now.

The biggest shifts are just in the last two or three years. Back in 2020 and into 2021, you could go out in the parking lot with a net and just catch loans. We put a huge amount of effort into building a fantastic CRM platform, but you couldn’t get anyone to touch it — they were all too busy simply getting loans. And then that changed fast. Now, if you’re in the wholesale business, you need to know what every broker is, what all their people are doing, what kind of loans each of them are doing, and what’s your wallet share with every lender.

Of course, if I had to go back and pick a point in time that really changed mortgage data, it was the 2008 mortgage crisis and the regulations that followed. Now every mortgage that’s recorded has a lender name and it’s got the originator’s NMLS number on every single loan. And that enables just a tremendous amount of data that’s available to be collected and used. That didn’t exist before.

That’s how I can take any lender, any broker shop anywhere in the country, and show you exactly what their mix of business is on different types of loans — purchase or refinance — and what percentage is PRMG. I actually have the data.

SW: Let’s talk about the CRM you mentioned. We know that the time to build is in a slower market, but what does that look like?

JA: Well, within the IT world, we’re just as busy now as we were before, even though the business is slower. Before, we were just trying to hang on and keep the rivets from popping out, just from everything going so fast. But now it’s all into rebuilding. So, there is a lot of work on CRM, marketing platforms, but increasingly quite a bit around compliance, especially around privacy. That’s really become a burden.

But I do agree this is a time to build new capabilities when you have this kind of an opportunity. And we’re looking at changing platforms, looking at new point of sale systems, trying on a lot of technology. I mean, I can’t tell you how many people we talk to, and how many products we look at and ideas that we’ve been getting exposed to.

SW: Is there a type of technology that you’re seeing now, that people are pitching you, that you think is new and really exciting?

JA: One good example is we changed our product and pricing engine. We’ve been using the big common one on the market, Optimal Blue, for so many years, since about 2016 when we changed from another one. We wanted to be able to get more out of our product and pricing engine, so we made a shift this year over to a new platform, which is called Polly X. A pricing engine is something no one ever really wants to have to change because the whole world is tied into that: every product, you’ve got every overlay and everything else. And we’re also looking at changes for our wholesale lending technology to help streamline that.

And when it comes to digital marketing, there’s nothing that’s off limits. I would say search engine optimization and customized websites for loan officers, those are areas where we’ve had some success.

The world of lead generation has really gotten tight, we’ve been looking at new ways to get better data there. We will get lower mortgage rates one day, right? So, we’ve been putting time into building and working on technology for call center tech, things of that sort.

And the CRM — we have our main CRM for retail and a different one for wholesale. But we were looking at actually doing some test implementations on a couple of other ones that are more interesting to really high producing loan officer teams.

And of course, lots of integrations — everywhere where you can build a connection. FinLocker is the company that we’ve been working with an integration to offer that kind of capability, they call it a financial locker for borrowers, where they keep all their data. And consumers can work and use tools to improve their credit and then one day they come back as a borrower or repeat borrower. Another company called Credit Evolve is a really legitimate credit counseling service and we try to move people there who need help.

So, we just try not to leave anything on the table. If somebody would have said two years ago, hey, we could have saved 59 loans out of the kazillion loans that we did, nobody would pay attention. But now it’s like, we could have saved 59 loans if we would have followed this process: it means something. It certainly means something in the pocket of those loan officers who can help those people get into a home.

SW: What do you see on the horizon that you think we should be paying attention to now?

JA: First, privacy is a huge area. In Europe, with GDPR, they’re pretty far ahead of us, but our government is catching up really fast. But the biggest thing is just the web of state regulations. Companies that learn how to navigate the privacy landscape are going to have a really strong competitive advantage. But it’s not an easy landscape to navigate. We wrangle with it every week.

For example, you have to have prior written consent from borrowers to do just about anything with their data. Even if you want to help them in some way — like referring them to a credit counselor or getting a homeowner’s policy — you have to have consent to do that. So, you’ve got to build that infrastructure into your system and then you can reuse that process over and over again on your different platforms.

Secondly, when you get into the security realm, that’s become very much a different world with the FTC — they’ve re-released a whole new set of safeguards, guidelines that fully took effect in June. And there are all kinds of new nationwide requirements for all mortgage lenders that are subject to that rule, things like using multifactor authentication, encrypting all of your data, a whole lot of requirements that I know a lot of smaller lenders are struggling with. We’re doing okay on it. But I know the trouble we’ve gone through to get to where we are, and I know how difficult it is, especially for lenders that maybe don’t have that experience.

SW: How does your background in security inform what you’re doing now at PRMG?

JA: I’d like to say it’s just kind of built into all my decision-making. If I was just a security officer, I would probably be more highly focused just there, but I’m also chief information officer, so we have to get things done and business has to move forward, so you have to find solutions.

There’s no perfection. I mean, if you think wow, I’m secure, all you need to do is go to a cybersecurity conference and listen to these guys get up there and tell you how you’re hosed. So there’s no perfection, there’s just best efforts and making sure that your choices are sound and you can document what you’re doing.

My background has served me well, but it’s a steady, long-term path toward building a secure company. It just doesn’t happen overnight or even in a year. It’s a multiyear plan.

SW: How do smaller companies cope with these kind of issues?

AJ: I think that’s going to be a real test now that the regulations are getting more teeth in them. Everyone’s getting into the game, every regulator, state and federal, and not just that, but all of your counterparties — your warehouse banks and the government sponsored entities, they all have their own audits and their own questionnaires. And they’re all checking the boxes and trying to ensure that everybody’s secure out there. So there is a lot of scrutiny and I think over time, smaller companies are going to remain at a disadvantage there.

SW: With your security background, what keeps you up at night?

JA: Actually, I sleep pretty good. But if I had to pick among the small things that bother me the most in the security world, I think it’s what everyone fears: these ransomware takedowns.

Everybody’s afraid of getting their systems encrypted, having someone get control of their data, and everybody has that same risk. And there are companies in the mortgage industry that have been taken down like that — I assume most of them had to pay the ransom.

And then beyond that is just any kind of large-scale data breach. I don’t see how you can really do business in this space without a strong cyber insurance policy, but I know there are companies out there that don’t have them because they can’t get them. We do. But that market is really tough and if you don’t have a good system, and good controls that you can demonstrate to the insurer, then you’re going to have a tough time getting coverage.

SW: What’s exciting about the future of technology and mortgage?

JA: There’s a lot of promise in artificial intelligence and machine learning. Just about everybody in this country is using that technology already — we have it in our cybersecurity systems. And I think the real promise in lending is what you can do to help speed the process: helping borrowers find the right product and helping underwriters in making decisions faster. I think that’s the exciting, fun part.

Average mortgage rates jumped for all loan terms compared to a week ago, according to data compiled by Bankrate. Rates for 30-year fixed, 15-year fixed, 5/1 ARMs and jumbo loans moved higher.

Mortgage rates have been increasing for some time, with the popular 30-year fixed rate loan breaking through 7 percent this summer. After a stretch of record lows, rates climbed in 2022 thanks to inflation and the Federal Reserve’s response. The Fed last hiked its key interest rate in July, the latest in a tightening cycle that began last year.

The central bank decided to hold firm on another hike at its September meeting, indicating it expects rates to remain elevated in the near term and that it’s not done battling inflation just yet. “Until inflation goes down to the Fed’s target of 2 to 2.5 percent, do not expect rates to move lower,” says Derek Egeberg, a branch manager for Academy Mortgage in Yuma, Arizona.

The increase in mortgage rates comes alongside appreciating home prices, both of which have prevented more homebuyers from entering the market. More than half of home purchase mortgages originated in July had a monthly payment over $2,000, according to Black Knight. Twenty-three percent of originations in July had a payment over $3,000.

Rates as of September 28, 2023.

The rates listed here are averages based on the assumptions here. Actual rates available on-site may vary. This story has been reviewed by Suzanne De Vita. All rate data accurate as of Thursday, September 28th, 2023 at 7:30 a.m.

30-year mortgage rate trends higher, +0.24%

Today’s average 30-year fixed-mortgage rate is 7.83 percent, up 24 basis points since the same time last week. A month ago, the average rate on a 30-year fixed mortgage was lower, at 7.53 percent.

At the current average rate, you’ll pay a combined $721.95 per month in principal and interest for every $100,000 you borrow. That’s $16.56 higher compared with last week.

Standard lending practices defer to the 30-year, fixed-rate mortgage as the go-to for most borrowers buying a home because it allows the borrower to spread payments out over 30 years, keeping their monthly payment lower.

15-year fixed mortgage rate goes up, +0.08%

The average rate for a 15-year fixed mortgage is 6.90 percent, up 8 basis points over the last seven days.

Monthly payments on a 15-year fixed mortgage at that rate will cost around $893 per $100,000 borrowed. That may squeeze your monthly budget than a 30-year mortgage would, but it comes with some big advantages: You’ll save thousands of dollars over the life of the loan in total interest paid and build equity much more rapidly.

5/1 adjustable rate mortgage moves up, +0.12%

The average rate on a 5/1 ARM is 6.63 percent, climbing 12 basis points since the same time last week.

Adjustable-rate mortgages, or ARMs, are home loans that come with a floating interest rate. In other words, the interest rate will change at regular intervals, unlike fixed-rate mortgages. These loan types are best for people who expect to sell or refinance before the first or second adjustment. Rates could be materially higher when the loan first adjusts, and thereafter.

While borrowers shunned ARMs during the pandemic days of super-low rates, this type of loan has made a comeback as mortgage rates have risen.

Monthly payments on a 5/1 ARM at 6.63 percent would cost about $641 for each $100,000 borrowed over the initial five years, but could climb hundreds of dollars higher afterward, depending on the loan’s terms.

Jumbo mortgage interest rate moves higher, +0.24%

The average rate for a jumbo mortgage is 7.86 percent, up 24 basis points from a week ago. A month ago, the average rate was below that, at 7.55 percent.

At today’s average rate, you’ll pay a combined $724.03 per month in principal and interest for every $100,000 you borrow. That’s $16.58 higher compared with last week.

Interested in refinancing? See rates for home refinance

Current 30 year mortgage refinance rate trends upward, +0.20%

The average 30-year fixed-refinance rate is 7.98 percent, up 20 basis points since the same time last week. A month ago, the average rate on a 30-year fixed refinance was lower, at 7.66 percent.

At the current average rate, you’ll pay $732.37 per month in principal and interest for every $100,000 you borrow. That’s an increase of $13.88 over what you would have paid last week.

Where are mortgage rates going?

Economists can’t say for certain where mortgage rates are going from here, according to Bankrate’s latest forecast. Some have speculated the 30-year rate could increase to 8 percent, while others expect rates to cool down by the end of 2023.

30-year fixed mortgage rates mostly follow the 10-year Treasury yield, which shifts continuously as economic conditions dictate, while the cost of variable-rate home loans mirror the Fed’s moves.

“Economic data that is not too hot and not too cold would be helpful to mortgage rates and could get rates back down below 7 percent,” says Greg McBride, chief financial analyst for Bankrate, adding, “but that has to be true for inflation, job growth, wages and consumer spending.”

What current rates mean for you and your mortgage

While mortgage rates move up and down on a daily basis,, there is some consensus that we won’t see rates return to 3 percent for some time. If you’re shopping for a mortgage now, it might be wise to lock your rate when you find an affordable loan. If your house-hunt is taking longer than expected, revisit your budget so you’ll know exactly how much house you can afford at prevailing market rates.

Keep in mind: You could save thousands over the life of your mortgage by getting at least three loan offers, according to Freddie Mac research. You don’t have to stick with your bank or credit union, either. There are many types of mortgage lenders, including online-only and local, smaller shops.

“All too often, some [homebuyers] take the path of least resistance when seeking a mortgage, in part because the process of buying a home can be stressful, complicated and time-consuming,” says Mark Hamrick, senior economic analyst for Bankrate. “But when we’re talking about the potential of saving a lot of money, seeking the best deal on a mortgage has an excellent return on investment. Why leave that money on the table when all it takes is a bit more effort to shop around for the best rate, or lowest cost, on a mortgage?”

More on current mortgage rates

Methodology

Bankrate displays two sets of rate averages that are produced from two surveys we conduct: one daily (“overnight averages”) and the other weekly (“Bankrate Monitor averages”).

The rates on this page represent our overnight averages. For these averages, APRs and rates are based on no existing relationship or automatic payments.

Learn more about Bankrate’s rate averages, editorial guidelines and how we make money.

Cash back benefits are no longer just for credit card users. Learn how to use Discover® Cashback Debit to get the most out of it.

September 29, 2023

Making money for spending money? It might sound too good to be true, but it’s a reality for some debit card holders. Debit cards like the Discover Cashback Debit card now offer a wide range of rewards and benefits to checking account holders, who are enjoying extra money in their pockets, added convenience, and more peace of mind thanks to all the advantages.

Lately, debit card benefits have started to include overdraft protection, receiving your paycheck early,1 online privacy protection, and more. But often the biggest benefit for debit card holders is the cash back they earn on purchases made with their cards.

What does ‘cash back’ mean?

As a debit card benefit, “cash back” refers to money that a bank adds to your checking account in exchange for using the debit card associated with that account. The amount of money you receive thanks to a debit card’s cash back benefit can depend on several factors, such as the financial institution, the type of card, and the type of transaction. For example, some financial institutions will reward customers with a percentage of the amount they spend with their card, while others may give customers a predetermined dollar amount for using the card at particular stores or restaurants. Some financial institutions restrict rewards to certain categories of purchases, such as gas or travel. Each financial institution and card has its own rules for what it considers a qualifying purchase, so make sure you understand the terms.

How does cash back work on debit cards?

Cash back rewards for qualifying purchases made with your debit card will typically appear in your account after the close of each statement period. Depending on your bank, the money could be added into a dedicated section of your online banking portal for you to redeem, or it could be directly deposited into your checking account. Make sure you understand how cash back works for your particular debit card so that you know when you’ll see the funds, how much you’ll receive, if there are any limits, and what types of transactions qualify.

How does Discover cash back work?

The Discover Cashback Bonus for the Discover Cashback Debit card works by providing 1% in cash rewards to customers on qualifying purchases. Discover Cashback Debit card users can earn 1% cash back on up to $3,000 in debit card purchases each month.2 That’s potentially $30 per month—or $360 per year—back in your pocket!

Earn cash back with your debit card

Discover Bank, Member FDIC

When does cash back show up on Discover Cashback Debit Accounts?

Discover Cashback Bonus rewards will post to the Rewards Detail section of your account summary at the end of each month. You can view your Cashback Bonus amount in either the Discover Mobile App or the Online Account Center.

Curious about the best way to redeem Discover Cashback bonus rewards? Well, you’ve got options. Through your account, you can manually transfer your Cashback Bonus into your Discover checking account, Online Savings Account, or Money Market Account. Discover customers are also able to enroll in Auto Redemption, which means Discover will automatically deposit your Cashback Bonus into your Discover Online Savings Account each month. Customers can also manually transfer their bonus to any Discover Credit Card Cashback Bonus® Account.

Ready to open a Discover Cashback Debit Account?

If you’re ready to get the most out of your debit purchases, including 1% in cash rewards2, then it’s time to get Discover Cashback Debit. Not only will you enjoy earning money on your everyday purchases, but you’ll also access amazing benefits like fraud protection, early pay1, and a network of over 60,000 fee-free ATMs.

Ready to get started? Open your Discover Cashback Debit account today.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

1 Early Pay is automatically available to checking, savings (excluding IRA savings), and money market customers who receive qualifying ACH direct deposits. At our discretion, and dependent on the timing of our receipt of the direct deposit instructions, we may make funds from these qualifying direct deposits available to you up to 2 days early. See our Deposit Account Agreement for more information.

2 ATM transactions, the purchase of money orders or other cash equivalents, cash over portions of point-of-sale transactions, Peer-to-Peer (P2P) payments (such as Apple Pay Cash), online sports betting and internet gambling transactions, and loan payments or account funding made with your debit card are not eligible for cash back rewards. In addition, purchases made using third-party payment accounts (services such as Venmo® and PayPal®, who also provide P2P payments) may not be eligible for cash back rewards. Apple Pay® is a trademark of Apple Inc. Venmo and PayPal are registered trademarks of PayPal, Inc. Samsung Pay is a registered trademark of Samsung Electronics Co., Ltd. Google, Google Pay, and Android are trademarks of Google LLC.

Imagine making $1,000 for every $100 you spend on real estate leads. Today’s guest, Joe Herrera of the Joe Taylor Group, does exactly that with a smart, simple Facebook advertising strategy. Listen and learn how to create viral property ads and how to consistently convert the leads that they generate. Plus, you’ll hear how to hold a team of Realtors accountable, what works best for buyer leads in 2023, and why you should not advertise a property’s price.

Listen to today’s show and learn:

About Joe Herrera [0:41]

Why Joe focuses on Facebook for real estate leads [4:43]

How to stop playing Zillow’s game [7:50]

An argument for not listing a property’s price [9:24]

Determining lead spend based on agents’ needs [12:55]

What to expect when you start running ads on Facebook [15:13]

How soon you’ll know whether or not a real estate ad is working [19:29]

How leads come in when running Facebook ads [21:34]

Why Zillow isn’t the right fit for Joe’s real estate business [24:49]

Focusing on the why instead of the what when working buyer leads [27:59]

Building the right relationship with potential clients [29:23]

What the 9-6-6 follow-up schedule looks like [31:50]

Joe’s coaching and lead-gen program for busy real estate agents [33:16]

Common conversion mistakes [36:45]

The difference between customer service and sales [39:51]

How to hold real estate agents accountable [41:40]

Joe’s real estate goals for the next few years [45:41]

The most relevant voice in real estate [49:16]

Joe Herrera

Joe Herrera is a multifaceted individual who seamlessly blends passion and responsibility into his various roles. As a keynote speaker, coach, mentor, lead generator, podcast host, and associate broker of Real Broker, Herrera’s enthusiasm for his work is contagious.

With more than a decade of experience as a lead conversion coach, Herrera has an impressive track record of generating more than 10,000 leads annually. His exceptional team, the Joe Taylor Group, closes an outstanding 1,000 units each year, expanding its presence to seven locations across North America. Notably, Herrera has graced the stage as a featured keynote speaker at prestigious real estate events across the U.S. and Mexico, sharing his expertise and insights.

In addition to his accomplishments in real estate industry, Herrera’s entrepreneurial spirit shines as he owns and operates several businesses specializing in investment and lead generation. His commitment to helping others extends further through his dedicated Velocity coaching business, where he pays it forward by guiding and supporting aspiring professionals.

As a Las Vegas area REALTOR®, Herrera understands the significance of buying or selling a home as a major life event for his clients. Beyond being a salesperson, he embraces his role as a trusted guide, providing unparalleled support and expertise throughout the process.

Outside of his professional pursuits, Herrera remains deeply connected to his community and family. He devotes his time to various acts of service, always ready to give back to those in need. An avid golfer, Herrera enjoys spending quality time with his kids, hitting the links at his favorite golf courses across the country.

Joe Herrera’s story is one of dedication, ambition, and genuine care for others – a testament to his remarkable character and the positive impact he brings to both the real estate industry and his community.

Related Links and Resources:

It might go without saying, but I’m going to say it anyway: We really value listeners like you. We’re constantly working to improve the show, so why not leave us a review? If you love the content and can’t stand the thought of missing the nuggets our Rockstar guests share every week, please subscribe; it’ll get you instant access to our latest episodes and is the best way to support your favorite real estate podcast. Have questions? Suggestions? Want to say hi? Shoot me a message via Twitter, Instagram, Facebook, or Email.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

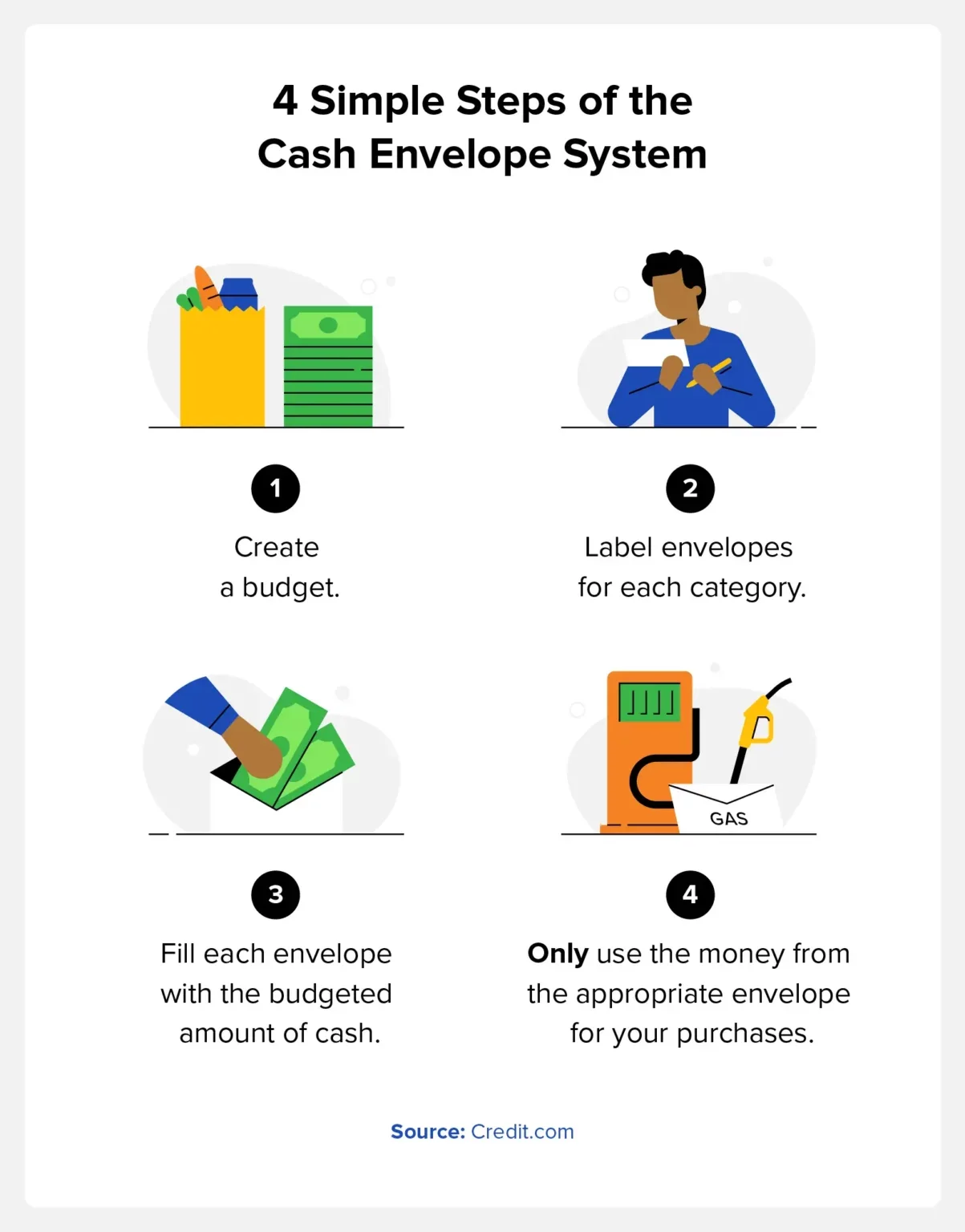

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

This article is part of a series put together by the Total Mortgage marketing team that provides loan officers and other sales professionals with a crash course in marketing and self-promotion. To read other articles in this series, click here.

This article is designed to teach loan officers and other sales professionals how to properly maintain and boost their social media presence. It will hit all the key points such as connecting, managing multiple profiles, engaging with influencers, and what to post.

Want to jump ahead?

LinkedIn

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Facebook

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Twitter

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencer

How and What to Post

Google +

Connecting & following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

LinkedIn

How to Gain/Find Connections

When you first started setting up your LinkedIn account, you were prompted to import your contacts from your email address book. If you clicked yes, you probably already have a few dozen connections. However, once your profile is completed, you will need to search for those connections you didn’t have on your contact list, like loan officers you met at a conference or realtors you haven’t had a chance to work with yet. There are many different ways to go about finding and linking with connections on LinkedIn.

The first way is arguably the easiest way: using the Search box. It can be found on the top of any tab of the LinkedIn interface. There are also many “Advanced Search” options available if you click the “Advanced” text link right next to the search button.

You could also find connections from clicking onto your Profile, scrolling down to your experience and hovering over your business place icon and then clicking onto the icon or your company title, highlighted by the red arrow.

After clicking on your company’s icon, scroll down until you see the “How You’re Connected” on the right side of the screen. Click “See all.”

Now you have the opportunity to see coworkers and contacts who you’re not connected to.

Managing Multiple Profiles

LinkedIn is generally a place where you focus on one personal profile. However, if you run your own business, you will want to create a company page for it. If you need help creating a company page, check out my Social Media Basics post. If you only manage one page, then this section may not be that useful.

If you are on your profile page and you want to switch to your company page, you simply click on the small icon on the top right hand corner of your screen (where the arrow is shown) then on “Company Page.”

This will lead you to this screen.

You’ll now be able manage, change, analyze, and update your company page. If you want to switch back to your profile page, just click on the home tab or profile tab.

Engaging with Influencers

Connecting with influencers—that is, the people who are active, established, and popular in your industry—is a great way to widen your reach. Of course, engaging with influencers on LinkedIn is not something you should do blindly. It takes strategy and time to do correctly.

Do Not:

Do not connect with an influencer without ever interacting with them

Do not like, comment, or share everything they post

Do not post more than 3 times per day

Do:

Do connect if you had previous relations

Do connect if you are connected on other networks

Do connect if you have exchanged emails or contact info

How and What to Post on LinkedIn

Posting on LinkedIn is very straight forward. LinkedIn allows you to share updates, publish a post, upload a photo, share in groups, and post job opportunities. You can access these options in the home tab, except for sharing in groups and posting job opportunities.

Sharing in a Group

Sharing in a group could be a great way to get your content to a broader audience. Joining groups on LinkedIn is very easy. First, click on the “Interests” tab and then click on “Groups” If you are already a member of a group it will appear under the “My Groups” section. If you aren’t a member of any groups, just click on the “Discover” tab and LinkedIn will provide recommendations for groups to join. You have the option to select “not interested,” “ask to join,” or you can ignore and continue to scroll.

Once you ask to join a group, your request must get approved by an admin, which can take a day or two depending on how busy they are. After you’re accepted, you can view what the others in the group are posting. To get started, click on “Start a conversation with your group.” The box will expand and you get the options listed below. At this screen, type in your title and a brief description with a link to the real content. Follow the same process for posting a job opportunity in a group.

If you run a LinkedIn business page, then you have the option of posting a job ad through the “Business Services” tab. Once you hover over “Business Services,” click on “Post a Job” to get to this screen.

After you fill out the appropriate information and click “Start job post,” LinkedIn will walk you through a series of prompts, where you will fill out information like job function, company industry, and job description. Once that’s done, review everything and click submit.

What to Post:

Career status updates

News and events

Articles shared by your connections

Your own articles

What not to Post:

Quotes

Updates trying to sell services/items

Material you deem not appropriate for the workplace

Facebook:

How to Gain Followers:

With more than 1.65 billion monthly active users, Facebook has the potential to connect you to people across the globe. If you’re using Facebook for business purposes, you need to understand how to properly navigate it to connect with others.

There are multiple strategies to take. For example, you can create a personal account, a business page, or both. If you’re in an industry where you need to keep things professional (like, for instance, the mortgage and financial industry), then I recommend creating a business page so you can separate your professional life from your personal life. You have to mindful of whom you invite to like your page, but we’ll touch on that topic a little later.

If you’re completely new to Facebook, prepare to spend some time connecting with people you know. You can manually add friends by clicking in the search box at the top of the screen and typing the name of the person you are trying to find. Eventually Facebook will tailor a carousel of “People You May Know,” which will allow you to click “Add Friend.” Thankfully, Facebook has implemented a few tricks to make it easier to add friends in bulk.

Go to the Friends Request page then to the “Add Personal Contacts,” enter your email and click find friends.

After you enter your email it will take you through to a similar screen. Click “Agree,” then follow the on-screen instructions.

On the Go

You can also import contacts from your mobile device.

Tap

Hit “Find Friends” in the Apps section

Tap “Contacts,” then follow the on-screen instructions

Connecting to Others Via Your Business Page

Click on the triangle in the top right corner of your home page.

Click on the drop down menu and select your business page.

Click on the […] on your cover photo and then click on “Invite Friends.”

Search all friends: click the invite box next to your friends’ names to invite them to like your page—or type their names in the search box.

Managing Multiple Profiles

Facebook does a fantastic job of making it easy to manage as many pages as you want. Their interface organizes your pages so you can easily switch through and manage every single of one of them. Every time you create a new page, Facebook allows you to add that page into your “Favorites” section. I highly recommend doing this, because it keeps all of your pages in easy reach, which you can see in the image below.

You can also switch between pages by clicking the drop-down triangle on the upper right corner of your home page. In that menu, you’ll find a list of three of your pages. Shown below:

If you manage more than 3 pages—like we do here at Total Mortgage—you can just click on “See More…” and it will give you a list of all the Facebook pages that you manage. To switch back to your personal page, you simply just need to hit the “Home” button and it will take you back to your feed.

Properly Engaging with Influencers

Recently, Facebook has changed how you interact with other people or businesses when you’re on your business page. Once, you were able to be on your business profile, click on “Home” and interact with people and businesses that follow your business page. However, that is essentially nonexistent today. Now you really need to be creative if you want to engage with influencers in your community.

To Like a Different Page as Your Business Profile

Go to the page you want to like and click on the […]

Click “Like As Your Page.” Then this screen will pop up and you choose the business account that you want your like to come from. Click “Save.”

Tagging other influencers in your Facebook posts is simple if you know the name of their business page. A lot of influencers have both personal and professional profiles, however, so make sure you know which one you’d like to connect with.

Unfortunately, you can’t tag a personal account from your business profile. If you want to tag a professional account from your business page, you craft your post, then add the appropriate tag at the end. You always want to convey that you got the content from a source and you are using it credibly.

In the picture below, you see that I have crafted a draft of my message and tagged the source I got it from with the tag “via @[name].” Instead of via you could use from, by, thanks to, etc. When possible, try to use a link shortener such as Buffer or Hootsuite to keep things looking tidy.

Once you get the proper etiquette down for interacting with influencers, now it’s time to engage with them. Like I mentioned above, you can like other pages as your page. You are able to do the same for posts. You do that by going to the page you want to like something on and scrolling to the post that you want to interact with. Before you like the post or comment, make sure you switch from your profile to your business profile. You do this by:

1. Clicking on the downwards arrow next to your small Facebook default icon

2. Click on the account you want to like and comment as.

You are now liking and commenting as your business account. This is the best way you can engage with your influencers. There are 3 important things you must always remember to do and don’t do before you start engaging with influencers.

Do Not:

Do not like/comment on everything that they post

Do not ask for a favor like sharing a post right away

Do not reach out to them right away

Do:

Gradually interact with them by liking their page and commenting on a few posts/pictures 1-3 times a week

Share some of their posts 1-2 times a week

Always remember to thank them for sharing information that you find important

Here’s where you use your gut. Once you think you’ve earned yourself a spot on the influencer’s radar, the next step is to reach out personally. This can be done in an open forum through commenting, or it can be done through private message. The eventual goal is to take the conversation “offline” through either phone or email so you can begin building an even more personal relationship.

How and What to Post on Facebook

Posting and sharing on Facebook is very easy. If you have a personal Facebook, you already know the drill. If this is your first time on Facebook or you don’t know how to post to your business page, then keep reading.

Posting on Your Personal Page

Bring your mouse to the top tab and click on your name

Click on the box where it says:

3. Click on the kind of post you want to craft: status, photo/video, or life event. Finish typing it with the appropriate tags (if needed) and click post.

Posting on your Business Page

Make your way over to your business page

Click on the box where it says “status, photo/video, or life event” and create the post you want to send out

When you are finished, click “Publish”

What to Post on Facebook

There are two types of content that you should post on Facebook. The difference depends on what account you plan to post with. For both profiles, you should post content that really resonates with your audience and makes people see you as a credible source (i.e. if you’re a loan officer, try content based around changes in the industry or tips on how to make the mortgage process easier).

Content like this positions you as an authority and encourages your audience to consider using your services if they are shopping for a home or refinancing. Every once in a while, it’s okay to throw in a shameless plug, whether you’re asking for referrals or encouraging people to use your services. Your personal page can have all the other updates—photos of your family, your dog, things you’re passionate about, etc. It is ok to post some business topics on your personal page, but make sure to do so sparingly. Your personal page is meant for personal things.

Twitter:

How to Gain Followers

Twitter is a great place to gain followers based on things that you find interesting. You can use the search box to find other professionals and people in your industry by looking for relevant hashtags, like #realestate.

Top Tips for Gaining Followers

Try finding your connections from other places like Facebook and LinkedIn on Twitter

Follow users who follow your followers

Follow the accounts recommended by Twitter

Join a Twitter chat

Managing Multiple Profiles

Unfortunately, Twitter doesn’t have an interface within itself to switch profiles easily—unless you are on your mobile device or want to use multiple web browsers. However, there are certain tricks, tips and hacks you can use to make managing multiple profiles easier.

Toggling Profiles in the Twitter App for iOS

From the “Me“ tab, tap the people icon

Tap “More options.”

From here you can “Create new account” or “Add an existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the people icon.

Toggling Profiles in the Twitter App for Android:

Tap the overflow icon

Tap “Accounts.”

From here you can “Create new account” or “Add existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the overflow icon, then tapping “Accounts.”

If you’re uninterested in downloading the Twitter app for your mobile device, there are other options. If you manage more than one profile you can easily manage multiple accounts if you use a tool like Tweetdeck, Buffer, or Hootsuite. All of these applications have free versions, so you don’t have to worry about spending money.

These apps make it easy to manage countless amounts of accounts. My personal favorite of the three is Buffer, because the interface is very easy to use and it provides multiple tabs to check out how your account is doing in terms of analytics. It also has a built-in link shortener that automatically shrinks your links when you are adding them to a post. Shown below is a screenshot of my Buffer interface.

Engaging with Influencers

Engaging with influencers on Twitter is a great way to kick-start your influencer marketing strategy. This is where Twitter search comes in handy; you can use it to find the people who tweet regularly in your industry regularly. If you want to stay organized, I recommend creating a spreadsheet that has a list of your influencers, their names, follower count, and what stage of your relationship you’re in. Once you’ve found a handful of them, it’s time to start engaging.

Do not:

Tweet, retweet, or like everything that they tweet

Try to directly reach out to them—it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally tweet, retweet, or like their posts to get on their radar

Appreciate their content by tweeting it out to your audience (and making sure your attribute the author)

Once you established a relationship, make it easy for them to tweet about your service by crafting an email with a few sample tweets that they could send out about your services. Make sure you convey the message that you are willing to reciprocate the favor

How and What to Post:

Posting on Twitter is very simple. If you are on the web browser version of Twitter the tweet box is one of the first things that you see. You can find it by looking for the “What’s happening?” text.

To compose a tweet you just click on this box and type the content you want to share.

Posting a Tweet on a Mobile Device

Tap the compose Tweet icon accessible from your Home timeline, the Notifications tab, or your profile (usually located on the upper right hand of your screen.)

Start typing where it says “What’s happening?”

If you’d like to Tweet an image, tap the camera icon

Tap “Tweet” to post.

What to Post

Just like any other platform, choosing what to post comes down to a few key factors.

Who your audience is

What kind of message are you trying to portray

What kind of content will resonate with that audience

Make sure you don’t forget to utilize the power of hashtags on Twitter. To see how a hashtag is performing simply search the hashtag in the search box before you post the tweet or check it out on Tagboard.

You want to have the appropriate amount of hashtags to text ratio. Most marketers recommend using no more than 3 hashtags per tweet. However, if your tweet only contains 3 words, don’t hashtag them all. Finding the perfect mix of creativity and content is surely a challenge but once you find your niche you will be good to go.

Google Plus

Google+ is one of the most underrated social media platforms, but it could be a great asset to your strategy if used properly.

How to Gain Followers

Make Your Profile Look Good