New York-based Rithm Capital, the parent company of Newrez, announced on Friday it completed the acquisition of Sculptor Capital Management for $719.8 million.

The deal was made public four months ago and created a dispute among investors to take the firm, leading Rithm to increase its price by 14% compared to the original bid. The transaction also created legal battles with Sculptor’s shareholders and founders, including Daniel S. Och, but the parties settled the cases in court.

In a special meeting on Thursday, Sculptor’s stockholders of 89% of the Class A common stock and 97% of Class B common stock voted in favor of the agreement with Rithm. They also approved the compensation to directors to consolidate the deal. As a result, Sculptor will be delisted from the New York Stock Exchange.

Michael Nierenberg, chairman, CEO and president of Rithm, said in a statement that the company plans to “create a superior global asset management business focused on delivering significant, long-term value for our shareholders and fund investors.”

Rithm announced on July 24 its plans to acquire Sculptor for $11.15 per share. After the deal was public, Rithm faced competition from a group of investors, including Boaz Weinstein, Bill Ackman, Marc Lasry and Jeff Yass. They offered $13.50 per share.

It resulted in Och and other founders filing lawsuits opposing the deal, saying it aimed to protect current CEO Jimmy Levin rather than maximize shareholder value.

Rithm only received the blessing of Sculptor’s founder at the end of October after increasing its price to $12.70 per share. It had previously increased to $12 per share without success.

Rithm reported a $194 million GAAP net income in the third quarter of 2023 — lower than the $357.4 million the prior quarter. The company targets transitioning from a real estate investment trust to a global asset manager.

Sculptor is relevant to this plan because it will bring to Rithm $34 billion of assets under management, including real estate, credit and multi-strategy investing spectrum.

Citi acted as the exclusive financial advisor to Rithm. PJT Partners was the financial advisor to the Sculptor’s special committee. The sculptor’s financial advisor was JP Morgan Securities LLC.

Since investors don’t have (functional) crystal balls, figuring out how to know when to buy a stock, in an effort to time the market and generate the biggest return, is difficult. While you shouldn’t necessarily try to time the market, if you are trading and incorporating some knowledge and tactics around when to buy a stock as a part of your larger financial plan, you’ll want to do what you can to fine-tune your strategy.

Trading stocks, of course, is fairly risky, and investors will want to keep that in mind. But with some practice and knowledge, you may be able to figure out the best time to buy stocks, and other variables, to help you try to boost your portfolio.

The Best Times to Buy Stocks

As noted, it’s generally not a good idea to try and time the market. But that’s not to say that there are larger market forces at work that result in certain trends. With that in mind, there can be good times of the day, days of the week, and even months to buy stocks that could generate bigger returns – though nothing is guaranteed.

The Best Time of Day to Buy Stocks

First and foremost, remember when the stock market is open and when trading is occurring. The New York Stock Exchange and Nasdaq, two of the largest and most active stock exchanges, are open 9:30 a.m. to 4:30 p.m. ET, Monday through Friday.

With that, the best time of the day, in terms of price action, is usually in the morning, in the hours immediately after the market opens up until around 11:30 a.m. ET, or so. That’s generally when most trading happens, leading to the biggest price fluctuations and chances for investors to take advantage.

The Best Day of the Week to Buy Stocks

If investors are aiming to trade during times of relative volatility, then they’ll want to utilize a trading strategy that aims to crowd their activity near the beginning and end of the week. Monday is probably the best day to trade stocks, since there is likely considerable volatility pent up over the weekend.

That said, Friday can also be a good day to trade, as investors make moves to prepare their portfolios for a couple of days off. The middle of the week tends to be the least volatile.

The Best Month to Buy Stocks

When thinking about the best months to buy stocks, examining historic performance can be helpful. For instance, looking at monthly returns from 2000 to 2020, the best months to buy are usually April, October, and November. Conversely, the month with the worst historic performance is September.

Again, these “best times to buy stocks” in terms of times, days, and months aren’t guarantees of anything, but are merely based on historical performance. That can be good to keep in mind.

Get up to $1,000 in stock when you fund a new Active Invest account.**

Access stock trading, options, auto investing, IRAs, and more. Get started in just a few minutes.

**Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

When Should You Buy Stocks

There’s a difference between “can” and “should” – and investors trying to discern when they should buy stocks should really consider their personal preferences, risk tolerance, and investment strategies. The right time to buy a stock is when an investor has done their research and feels confident that a stock price will rise in the short or long term, and that they’re willing to hold onto it until it does.

It helps to be informed when considering whether to buy stocks, and one way to do that is to learn about the company itself. Interested investors can find many company’s financial reports and earnings reports from government databases or private company research reports.

While ultimately it may be a good idea to buy stocks across different industries in order to diversify, it sometimes helps to start with a business or industry one is familiar with. Knowing about the company can help put the earnings reports into context.

Understanding the value of stocks is often, if not always tied to understanding the business those stocks represent a share in. Is the company a good investment? Does it have sound financials and growth potential? Here are helpful questions to consider when contemplating buying a stock:

What is the price range at which you’re willing to buy? If an investor has a company in mind, setting a price range at which they would want to buy stock in that company may help inform their decision. One can do this through analysts’ reports and consensus price targets, which average all analyst opinions.

Does the stock appear undervalued? There are different ways to determine value. The most common valuation metric is a price-earnings ratio (or P/E), which takes the price per share and divides it by earnings per share. The lower the number, the less the value. Generally for U.S. companies, a P/E below 15 is considered a good value and a P/E over 20 is considered a bad value. You can also compare the company’s P/E to others in the industry.

Another way to look at value is a discounted cash flow (DCF) analysis, which takes projected cash values and discounts them back to the present. This ultimately gives an investor a theoretical price target; if the actual price is below the target, then in theory, it’s undervalued and a good buy. 💡 Quick Tip: Did you know that opening a brokerage account typically doesn’t come with any setup costs? Often, the only requirement to open a brokerage account — aside from providing personal details — is making an initial deposit.

When Is the Worst Time to Buy Stocks?

Just as there are the purported best times to buy stocks, there are also the worst times to buy stocks, too. Given that investors may be looking for relatively volatile times in the market to buy stocks, relatively calm periods during the trading day may be the worst times to buy. Those hours would be during the middle of the day, perhaps from 11:30 a.m. ET until 3 p.m. ET.

In terms of days of the week? Tuesdays, Wednesdays, and Thursdays may be worse than Mondays or Fridays, barring any market-moving news or other volatility-inducing events. Finally, September, February, and May tend to be the weakest-performing months for the stock market, dating back nearly a century. 💡 Quick Tip: How do you decide if a certain trading platform or app is right for you? Ideally, the investment platform you choose offers the features that you need for your investment goals or strategy, e.g., an easy-to-use interface, data analysis, educational tools.

How Do You Know When to Hold Stocks?

Knowing when to hold a stock often comes down to one’s investment strategy. With a passive investment approach, investors invest in various stocks with the intention of holding them for an indefinite amount of time. This is also known as a buy and hold investment strategy.

With this type of investing, investors attempt to match a market index such as the S&P 500 and the Dow Jones Industrial Average. So, they select stocks in that market index coinciding with the same percentages in that index.

One benefit of the buy and hold strategy is that the tax rate on long-term capital gains (from stocks that an investor has owned for more than one year) are much lower than that of short-term capital gains.

For many, if not most investors, if you’re going to buy a stock, it may be a good strategy to hold onto it for a while. When an investor buys an undervalued stock, it could take a few years for it to reach its “correct” valuation. And of course, there’s always a risk it will never reach what the investor has determined is the correct valuation.

Not everyone holds onto their stocks for a long time, but there are risks to day trading that may inspire some to become buy-and-holders.

How Do You Know When to Sell a Stock?

Just like how a decision to hold a stock largely depends on an individual investor’s specific strategy, so does the choice as to whether or not to sell.

Some investors rely on a rule of thumb that states that the stock market reaches a high point in May or June and then goes down over the summer until September or October. While that can sometimes be observed in overall market behavior — partially because traders (just like lots of people) go on vacation in the summer and partially because it’s a bit of a self-fulfilling prophecy — it doesn’t mean an individual stock will definitely go down over the summer.

Taking this advice, however, — and other, similar types of advice – should be taken with a grain of salt. Again, the choice of whether to sell a stock is up to you, and the research you’ve put into making the decision.

The Takeaway

Knowing when to buy, sell, and hold stocks can be less confusing when an investor does the research into company health, overall market conditions, and their own financial needs as relates to personal short-term and long-term goals.

One of the easiest ways to buy and sell stocks or manage any investment portfolio is to open an online taxable brokerage account. This is often appealing to investors who want to take more of an active investing approach and buy and sell stocks. Investors would typically pay fees based on the account and the number of trades they make.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

FAQ

Is it best to buy stocks when they are down?

The best time to buy a stock is when an investor has done their research and due diligence, and decided that the investment fits their overall strategy. With that in mind, buying a stock when it is down may be a good idea – and better than buying a stock when it is high. But there are always risks to take into consideration.

Should I buy stocks at night?

Investors can engage in after-hours trading, but there are unique risks to doing so, and orders won’t execute until the market opens. Interested investors may want to try after-hours trading to get a feel for it before fully incorporating it into their strategy.

What are the worst months for the stock market?

Based on past performance, the worst months for the stock market tend to be in the early fall and summer. September is usually the worst, but October, June, and August can be bad as well.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

TheStreet’s J.D. Durkin brings the latest business headlines from the floor of the New York Stock Exchange as markets close for trading Friday, November 10.

Full Video Transcript Below:

This page requires Javascript.

Javascript is required for you to be able to read premium content. Please enable it in your browser settings.

A version of this story first appeared in CNN Business’ Before the Bell newsletter. Not a subscriber? You can sign up right here. You can listen to an audio version of the newsletter by clicking the same link.

New York CNN

—

Policymakers at the Federal Reserve are feeling optimistic that a rise in long-term Treasury yields could finally put an end to the past 19 months of historic interest rate hikes meant to tamp down inflation.

Wall Street is also feeling hopeful that there won’t be further tighteningof monetary policy. The odds of another interest rate hike by the Fed in November are falling, according to the CME FedWatch Tool.

Financial markets currently see a nearly 90% chance the US central bank will keep rates unchanged at its next policy meeting to be held on October 31 through November 1. Just a month ago, markets had those odds at just 57%.

The majority of traders are betting that there will be no more hikes and that the Fed will hold rates steady through June 2024 before loosening policy, the CME tool shows.

What’s happening: US Treasury rates are white hot — 10-year Treasury yields are near their highest levels since 2007. That’s bad news for the economy,but those yields could be doing the Fed’s job for it.

For American consumers, an elevated 10-year Treasury return means more costly car loans, credit card rates and even student debt.

It also means more expensive mortgage rates. Mortgage rates tend to track the yield on 10-year US Treasuries. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

US mortgage rates are at 23 year-highs, and home affordability is at its lowest level since 1984.

That means consumers are beginning to sweat. Americans haven’t been this worried about missing a minimum debt payment since the early weeks of the pandemic, according to consumer survey data released Tuesday by the New York Federal Reserve.

The average perceived probability of not making a minimum debt payment in the next three months increased 1.4 percentage points to 12.5% in September, according to the Federal Reserve Bank of New York’s latest Survey of Consumer Expectations. That’s the highest rate since May 2020.

But what’s bad for the economy tends to be good for bringing prices down. And some Fed officials indicated this week that rates are now high enough to lower inflation to their target goal of 2%.

Philip Jefferson, the number two official at the Fed, said in a speech on Monday that he would “remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

That’s Fed speak for: I’m paying attention to the fact that borrowing money is more expensive and I’ll keep that in mind when deciding what actions the Fed should take in the future.

Dallas Fed President Lorie Logan also suggested on Monday that higher yields mean there’s not as much need for future rate hikes.

On Tuesday, Federal Reserve Bank of Atlanta President Raphael Bostic said barring unforeseen economic events, he didn’t see the need to raise interest rates any higher.

“I think that our policy rate is at a sufficiently restrictive position to get inflation down to 2%,” he said at the annual convention for the American Bankers Association. “I actually don’t think we need to increase rates anymore.”

Bostic, who does not vote on policy decisions, said that Treasury yields showed rates were “clearly” restrictive and slowing the economy.

Last week, San Francisco Fed President Mary Daly said that the increases in Treasury yields since the Fed’s last meeting in September were equivalent to another quarter percentage point interest rate hike. If financial conditions remain tight, she said, “the need for us to take further action is diminished.”

What about markets: In a twist, the prospect of a steady Fed policy buoyed markets and sent Treasury yields lower on Tuesday. Bonds compete with stocks for investors’ dollars, so when equities go up, yields often go down.

The 2-year Treasury yield fell to 4.96% on Tuesday and the 10-year Treasury yield dropped to 4.65%, but both still sit near recent highs.

What’s next: Investors will pay attention to the Producer Price Index (PPI), which tracks the average change in prices that businesses pay to suppliers, due out Wednesday and the Consumer Price Index (CPI), a closely watched inflation gauge, on Thursday for furtherclues about the Fed’s next move.

PPI for September is expected to be unchanged for the year at 1.6% and lower for the month at 0.3% versus 0.7% in August, according to Refinitiv estimates.

Inflation as measured by CPI, meanwhile, is expected to have slowed month-over-month to 0.3% from 0.7% in August.

Birkenstock is now an $8 billion company

It’s official. Birkenstock will be making its debut on the New York Stock Exchange Wednesday under the ticker symbol BIRK.

The beloved cork-soled shoemaker priced its initial public offering at $46 a share, making Birkenstock an $8.6 billion company, reports my colleague Elisabeth Buchwald.

That would make Birkenstock one of the 5 largest consumer discretionary IPOs of the past 20 years, according to data from Renaissance Capital.

It also means that the company is valued at about 37 times its earnings. That’s a signal of confidence in the market despite an “ongoing IPO market slump,” said Megan Penick, public securities chair and partner at law firm Michelman & Robinson.

The climate crisis is coming for your hoppy beer

Hops in major beer-producing European countries like Germany, Czech Republic and Slovenia are ripening earlier and producing less since 1994, scientists found. And, perhaps most alarmingly for the IPA lovers of the world, they are starting to lose their critical bitter component, reports my colleague Rachel Ramirez.

It’s going to get worse, researchers say. Hop yields could decline by as much as 18% by 2050, and their alpha acid content — which makes beer bitter — could decrease by up to 31% due to hotter and drier conditions, according to a study published Tuesday in the journal Nature Communications.

Scorching temperatures have already shifted the start of hop growing season by 13 days from 1970 to 2018, according to the study. The growth of new shoots from the hop plant typically occurs during the spring, but since 1995, the researchers found it’s happening earlier in the regions analyzed than years prior.

In recent years, more consumers are preferring beer aromas and flavors that require higher-quality hops, according to the study. Since these hops are only grown in smaller regions, researchers say they’re put at even higher risk from climate change-fueled heat waves and droughts.

Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., August 29, 2023. REUTERS/Brendan McDermid Acquire Licensing Rights

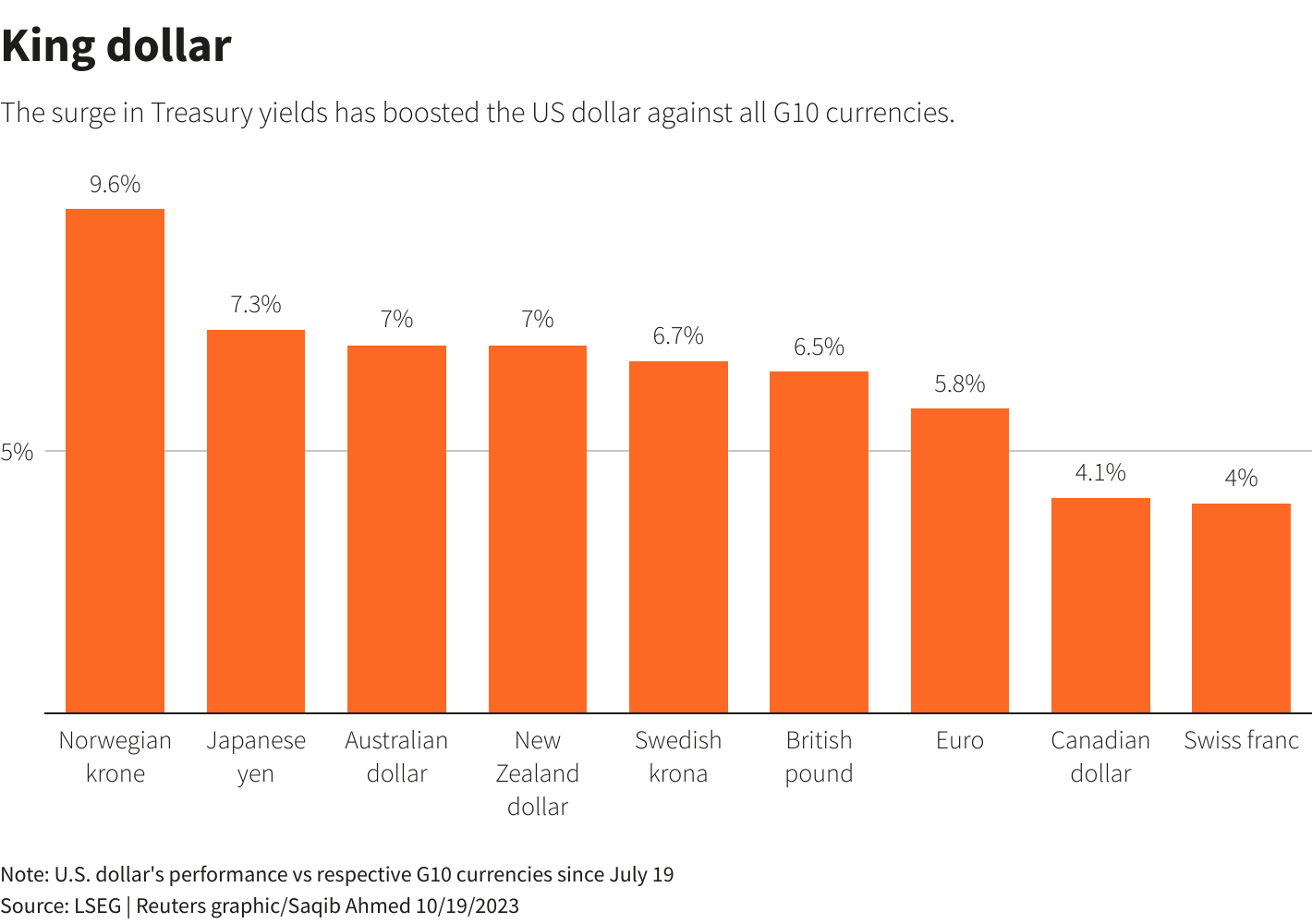

NEW YORK, Oct 19 (Reuters) – Relentless selling of U.S. government bonds has brought Treasury yields to their highest level in more than a decade and a half, roiling everything from stocks to the real estate market.

The yield on the benchmark 10 year Treasury – which moves inversely to prices – briefly hit 5% late Thursday, a level last seen in 2007. Expectations that the Federal Reserve will keep interest rates elevated and mounting U.S. fiscal concerns are among the factors driving the move.

Because the $25-trillion Treasury market is considered the bedrock of the global financial system, soaring yields on U.S. government bonds have had wide-ranging effects. The S&P 500 is down about 7% from its highs of the year, as the promise of guaranteed yields on U.S. government debt draws investors away from equities. Mortgage rates, meanwhile, stand at more than 20-year highs, weighing on real estate prices.

“Investors have to take a very hard look at risky assets,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities in New York. “The longer we remain at higher interest rates, the more likely something is to break.”

Fed Chairman Jerome Powell on Thursday said monetary policy does not feel “too tight,” bolstering the case for those who believe interest rates are likely to stay elevated.

Powell also nodded to the “term premium” as a driver for yields. The term premium is the added compensation investors expect for owning longer-term debt and is measured using financial models. Its rise was recently cited by one Fed president as a reason why the Fed may have less need to raise rates.

Here is a look at some of the ways rising yields have reverberated throughout markets.

Higher Treasury yields can curb investors’ appetite for stocks and other risky assets by tightening financial conditions as they raise the cost of credit for companies and individuals.

Elon Musk warned that high interest rates could sap electric-vehicle demand, which knocked shares of the sector on Thursday. Tesla’s shares closed the day down 9.3%, as some analysts questioned whether the company can maintain the runaway growth that has for years set it apart from other automakers.

With investors gravitating to Treasuries, where some maturities currently offer far above 5% to investors holding the bonds to term, high-dividend paying stocks in sectors such as utilities and real estate have been among the worst hit.

Reuters Graphics

The U.S. dollar has advanced an average of about 6.4% against its G10 peers since the rise in Treasury yields accelerated in mid-July. The dollar index, which measures the buck’s strength against six major currencies, stands near an 11-month high.

A stronger dollar helps tighten financial conditions and can hurt the balance sheets of U.S. exporters and multinationals. Globally, it complicates the efforts of other central banks to tamp down inflation by pushing down their currencies.

For weeks, traders have been watching for a possible intervention by Japanese officials to combat a sustained depreciation in the yen, down 12.5% against the dollar this year.

“The correlation of the USD with rates has been positive and strong during the current policy tightening cycle,” BofA Global Research strategist Athanasios Vamvakidis said in a note on Thursday.

The interest rate on the 30-year fixed-rate mortgage – the most popular U.S. home loan – has shot to the highest since 2000, hurting homebuilder confidence and pressuring mortgage applications.

In an otherwise resilient economy featuring a strong job market and robust consumer spending, the housing market has stood out as the sector most afflicted by the Fed’s aggressive actions to cool demand and undercut inflation.

U.S. existing home sales dropped to a 13-year low in September.

Reuters Graphics

As Treasury yields surge, credit market spreads have widened with investors demanding a higher yield on riskier assets such as corporate bonds. Credit spreads blew out after a banking crisis this year, then they narrowed in subsequent months.

The rise in yields, however, has taken the ICE BofA High Yield Index (.MERH0A0) near a four-month high, adding to funding costs for prospective borrowers.

Volatility in U.S. stocks and bonds has bubbled up in recent weeks as expectations have shifted for Fed policy. Anticipation of a surge in U.S. government deficit spending and debt issuance to cover those expenditures has also unnerved investors.

The MOVE index (.MOVE), measuring expected volatility in U.S. Treasuries, is near its highest in more than four months. Volatility in equities has also picked up, taking the Cboe Volatility Index (.VIX) to a five-month peak.

Reporting by Saqib Iqbal Ahmed; Writing by Ira Iosebashvili; Editing by Stephen Coates

Our Standards: The Thomson Reuters Trust Principles.

The nation’s largest home builder, D.R. Horton, also has its own affiliated mortgage lender known as “DHI Mortgage.”

Recently, new home sales have surged in popularity due to the mortgage rate lock-in effect.

Essentially, existing homeowners aren’t selling their properties because they’ve got ultra-low fixed interest rates on their home loans.

At the same time, mortgage rates have surged higher, resulting in big financing incentives from home builders to move their newly-built home inventory.

Let’s take a hard look at what DHI Mortgage has to offer and whether an in-house lender is the way to go.

DHI Mortgage Fast Facts

Full service mortgage lender offering home purchase loans and refis

Founded in 1997, headquartered in Austin, Texas

Parent company D.R. Horton is the nation’s largest home builder

Publicly traded company (NYSE: DHI)

Also operate DHI Title and D.R. Horton Home Insurance Agency

Aim to be a one-stop shop for newly-built home buyers

Funded roughly $20 billion in home loans during 2022

Most active in the states of Texas, Florida, and California

Licensed to do business in 34 states

DHI Mortgage is a full-service mortgage lender owned by parent company D.R. Horton.

They were founded in 1997 and are headquartered in Austin, Texas.

D.R. Horton is the largest home builder in the United States, slightly bigger than competitor Lennar, which also has a captive mortgage company called Lennar Mortgage.

The home builder got its start back in 1978 when Don R. Horton built his first home in Fort Worth, Texas.

Since then, the company has grown into a near-$35 billion dollar company that is publicly-traded on the New York Stock Exchange (NYSE: DHI).

The company’s shares are owned by legendary investor Warren Buffett, who sees strength in home building given the lack of existing home supply.

Aside from operating their in-house mortgage lender DHI Mortgage, they also run an affiliated title company and insurance agency.

This means home shoppers can use DHI Title for their title insurance needs and D.R. Horton Home Insurance Agency for their homeowners insurance, assuming it’s competitively priced.

The goal is to create a one-stop shopping experience for home buyers and streamline what is often a daunting process.

Last year, they funded about $20 billion in homes, with nearly 30% of overall volume coming their home state of Texas, per HMDA data.

They are also quite active in Florida, California, Arizona, Georgia, Nevada, and The Carolinas.

How to Apply with DHI Mortgage

While you can get pre-qualified for a mortgage online via the DHI Mortgage website, they say to get in touch with your mortgage loan originator to submit a full loan application.

It’s unclear if this means you can still apply electronically after speaking with a loan officer, or if you have to apply in-person.

They do have branch locations and sales offices at their home builder developments, which could facilitate this process.

Unfortunately, their website is a bit limited when it comes to information, so you’ll probably need to speak with a human before proceeding to an application.

Their online system, powered by fintech company Blend, does seem to allow for online refinance applications along with the pre-qualifications.

If you visit their website, it’s also possible to search for a local loan originator by state, branch, or by name.

They say they have digital options for buyers, but don’t make clear what those are. My assumption is they do offer some sort of online loan submission process.

And likely the ability to complete tasks electronically, whether it’s satisfying loan conditions or checking loan status.

However, I would like to see more information in this department.

Loan Programs Offered by DHI Mortgage

Home purchase loans

Refinance loans

Conventional loans including Fannie/Freddie 3% down

FHA loans

VA loans

USDA loans

Fixed-rate and adjustable-rate options

Temporary buydowns

Affordable housing loans

DHI Mortgage offers the most popular loan options out there, whether it’s 3% down conforming loan backed by Fannie Mae or Freddie Mac or an FHA loan.

You can get both a home purchase loan or a mortgage refinance, though I doubt many existing homeowners would use them for a refinance unless mortgage rates were ultra-competitive.

The full menu of government-backed mortgages is offered, including FHA loans, VA loans, and USDA loans.

And both fixed-rate and adjustable-rate options are available, including the 30-year fixed, 15-year fixed, 7/1 ARM, and 5/1 ARM.

They also appear to offer jumbo loans that exceed the conforming loan limit in pricier regions of the country.

However, they don’t appear to offer any second mortgages, such as HELOCs or home equity loans.

But temporary buydowns, such as 2-1 buydown, are offered, as well as other affordable housing loans if buying in specific locations or with low-to-moderate income.

DHI Mortgage Rates

Speaking of mortgage rates, DHI Mortgage doesn’t have a page on their website dedicated to rates or lender fees for that matter.

So you’ll be a little bit in the dark there. Be sure to ask your loan originator what fees they charge, such as loan origination fees, application fees, processing and underwriting, etc.

The good news is I did see special interest rate offers on the D.R. Horton website, which is typical of home builders.

They often offer special incentives to their home buyers who also use their affiliated lender.

In this case, I saw a 5.50% fixed rate FHA loan offer, which was also available on VA and USDA loans.

And a 5.75% fixed rate conventional loan offer that only required a five percent down payment.

So chances are they can offer some pretty competitive rates if you buy a D.R. Horton property and use DHI Mortgage.

DHI Mortgage Home Buyers Club

Those with imperfect credit can take advantage of the “DHI Mortgage Home Buyers Club.”

It pairs in-house credit consultants with prospective home buyers to prepare them for homeownership.

While it doesn’t guarantee loan approval or improved credit scores, they will work with you to boost your overall credit profile.

They’ll also ask you to complete a HUD-approved homebuyer education course while your credit consultant comes up with a credit profile improvement strategy.

This might entail removing inaccurate items on your credit report, paying down high balances, and getting current on any past due accounts.

The goal is to clean up your credit history and improve chances of mortgage approval, and potentially snag a lower mortgage rate depending on credit score improvement.

DHI Mortgage Reviews

As always, I try to track down customer reviews online to see what past customers think of the lender in question.

And they don’t appear to be great, based on what I could find. Their headquarters in Austin has a 2.6/5 rating from about 40 Google reviews.

Over at WalletHub, it’s a similar 2.6/5 rating from just over 30 reviews, with some customers citing poor communication and delays.

You can also find reviews for individual loan officers if you go on Zillow and search by name or location.

DHI Mortgage currently has a ‘B+’ rating with the Better Business Bureau (BBB), which isn’t fantastic and likely due to customer complaints.

They also have a 1.14/5 rating on the BBB website based on customer reviews.

To sum things up, their website could do with improving and their mixed reviews raise some questions about customer service.

On the bright side, they offer a good amount of loan programs and might have financing specials that beat out the competition.

Ultimately, it would probably come down to price if deciding between them and a different lender.

Though I assume most DHI Mortgage customers are also likely D.R. Horton home buyers, so there will likely be a big push to stay in-house.

Just be sure to speak with other mortgage companies, independent mortgage brokers, and so on to weigh your options.

Convenience is great, but not at the price of higher closing costs and/or interest rates. So definitely shop around.

Lastly, note that DHI Mortgage sells most of the loans it originates, meaning it’s likely your loan will be sold and transferred to a new loan servicer shortly after closing.

DHI Mortgage Pros and Cons

The Good

Special financing incentives to D.R. Horton home buyers

Might be a quicker/easier home buying process using affiliated companies

Branch locations allow borrowers to work with in-person if preferred

DHI Mortgage Home Buyers Club helps credit challenged buyers

Free mortgage calculator and homebuyer education resources online

Lots of loan programs to choose from including fixed-rate loans and ARMs

The Perhaps Not

Only licensed in 34 states

No mention of mortgage rates or lender fees online

Clunky website with limited information

Don’t seem to able to apply for a home loan electronically

Do not offer second mortgages or home equity products

Investing in the stock market has never been more accessible than it is today. Thanks to a wide array of online brokers, you can now trade stocks, ETFs, and other securities right from the comfort of your own home or even on the go. But with so many options available, how do you choose the right one?

We’ve broken down the top online brokers for stock trading, considering factors such as cost, user interface, customer service, and the range of available investments.

Whether you’re a seasoned investor or a beginner just looking to dip your toes into the financial markets, our guide will help you navigate this essential decision. Let’s get started!

7 Best Online Brokers

Check out our list of 2023‘s best stock trading platforms. You’ll find all the details you need in this accessible guide so you can get right to the good part: starting your trades.

Robinhood

Robinhood is a trading app that provides commission-free options, ETF, and cryptocurrency trades. For a long time, the company stood out as one of the few online stockbrokers offering commission-free trades, but it has become more common in the past year.

Robinhood is still one of the best online brokers for anyone looking to get started with investing. And it’s still one of the few apps that allows you to trade cryptocurrency.

Many people like Robinhood for its simplicity. There is no account minimum to get started and no annual fees. In addition, the company offers a web-based and mobile app and customer support options.

However, a common complaint about Robinhood is that the company’s offerings are very light on the research. And while the app is easy to use, there is very little offered in customizations.

Learn more by reading our full Robinhood review.

Charles Schwab

Charles Schwab requires you to start with a bit of skin in the game, with a minimum opening deposit of $1,000.

You can, however, check for promotions that often allow you to waive the minimum if you sign up for monthly $100 deposits. It’s an easy entry point for beginning trade enthusiasts.

When you’re ready to start trading with Charles Schwab, you can enjoy lower costs of just $4.95 per trade and $4.95 plus $0.65 per contract for options trading.

ETF lovers will appreciate the 200+ commission-free funds in addition to 3,000+ mutual funds with no transaction fees. In addition, you get to skip any kind of annual or inactivity fee on your account, but it’s $50 if you ever decide to close your account.

While you can choose from two different trading platforms, StreetSmart Edge is the more sophisticated version for frequent stock traders.

Don’t let the easy customization fool you. You can perform in-depth research and monitor your stocks with features like streaming market data and your account buying power.

Additionally, they provide countless reports, from its own equity ratings to third-party data from industry stalwarts like Morningstar, Market Edge, Capital IQ, and more.

For access to all of this at your fingertips anytime, anywhere, the mobile app carries just about all the same features as the web version.

Data-centric traders could definitely gain many insights by choosing Schwab for their online stock trading.

Fidelity

Fidelity may require a rather hefty minimum deposit of $2,500 but makes up for it with its attractive commissions.

It’s just $4.95 for each trade and the same amount for options, plus $0.65 per contract. This is a recent drop, so if you previously discounted Fidelity, it’s time to take a second look.

Do you want extensive NTF mutual funds? You’ll find about 3,600 with Fidelity. There are also about 91 commission-free ETFs, which is certainly encouraging but not the most we’ve seen.

One interesting feature with Fidelity is that you can do forex trading along with more standard securities. Like many of the brokerages we’ve reviewed, there are no account fees or inactivity fees.

Looking for a robust trading platform?

Check out Fidelity’s Active Trader Pro. To get access, you will need to make at least 36 trades in a 12-month period. If you fit the bill, you’ll get a fully customizable account with real-time streaming and market updates.

You can also look at historical trends and use the Strategy Ideas tool. It can even help you craft an exit strategy when the time comes.

In terms of additional research, Fidelity actually gets its research from over 20 firms, such as Recognia, McLean Capital Management, and Ned Davis. You can even get an aggregate picture from all the data available through Fidelity’s Equity Summary Score on each stock quote page.

Merrill Edge

Owned by parent company Bank of America, you can actually access all of your accounts from the same login if you’re a B of A customer.

This can be a huge draw for some, but Merrill Edge comes with both pros and cons, just like any other trading platform.

Let’s take a look.

First, Merrill Edge has excellent customer service and powerful research and trading tools.

Commissions are somewhat high, coming in at $6.95 for stock trades plus an extra $0.75 per contract for options. They offer 2,000+ NTF mutual funds, but unfortunately, don’t have any commission-free ETFs. This may be a deal-breaker for some traders.

You can, however, qualify for 30 commission-free trades on individual stocks or ETFs each month by meeting a balance minimum.

You can qualify if you have at least $25,000 in either a Merrill Edge self-directed account or a Bank of America cash deposit account.

E-Trade

You will need at least $500 to open up an E-Trade account, but many traders agree that the volume discounts and easy-to-use platforms are well worth it.

In fact, each platform appeals to two types of investors: beginners and more seasoned pros. So, it’s a great place to start with a bit of cash, which also allows you to take advantage of more sophisticated tools as needed.

But, there is a catch.

To upgrade from the basic E-Trade Web platform to the E-Trade Pro platform, you’ll need either a large account or an active trade history.

So, you’ll either need a minimum of $250,000 in your account or make 30 or more trades per quarter. If you do make that amount of quarterly trades, you can still qualify for some other benefits as well — including discounted commissions.

Just how much?

For stock trades, your commission per trade will drop from $6.95 to $4.95. For options trading, it’s typically $6.95 plus $0.75 per contract, but for active traders, your fee drops to $0.50.

And while you’ll enjoy 100+ commission-free ETFs and 2,500 no-transaction-fee mutual funds, any others cost $19.99.

Ally Invest

Known for their great customer service that’s available 24/7, Ally Invest is one of the best online brokers providing low barriers to entry in the trading game.

There are no account minimums and low commission fees. Not only are stock and ETF trades just $4.95 each, but you can also receive a discount when trading in volume.

The bottom line for getting cheaper trades?

Make either 30+ trades per quarter or keep a minimum of $100,000 in your brokerage account. That drops the commission fee to just $3.95 per equity trade. The standard options trade of $4.95 plus $0.65 per contract drops to $3.95 plus $0.50 per contract for active traders.

In addition to the traditional securities found at most online brokers, Ally Invest also offers forex and futures trading.

You can take advantage of free data if you make at least one forex trade within a 90-day period. Instead of paying a trade commission, you’ll instead be charged on your forex trades based on the spread markup.

What kind of platform can you expect from Ally?

There’s just one web-based trading platform, so you can log in from any device. Like most other online trading platforms, Ally’s gives you live-streaming of quotes and data plus a dashboard you can completely customize.

You can also access your brokerage account through their iPhone or Android mobile app.

Ally also shines when it comes to investing tools. Options traders, for example, can utilize the pricing calculator to compare current prices to forecasts.

You can also pick your own criteria within the strategy scanner to help identify various options strategies.

Interactive Brokers

Beginners beware: Interactive Brokers is an advanced online broker with a high account minimum to the tune of $10,000, so don’t jump into this one until you’re ready.

But if you’re 25 or younger, you can open an account with just $3,000. Still, you need to know what you’re doing because Interactive Brokers doesn’t house a huge resource pool for beginners.

Unlike most other online stock brokers on this list, Interactive Brokers charges commissions per share rather than per trade. So while you can get a volume discount, the standard stock trade costs are $0.005 per share.

There’s a minimum charge of $1 and a maximum of 0.5% of your trade value. Options trades also carry a $1 minimum and charge $0.70 per contract.

You may also be charged fees for certain situations. For example, if you have an IRA, you’ll be charged a quarterly fee of $7.50. If you’re inactive in your account, you may be charged a fee between $3 and $20.

Interactive Brokers has about 30 ETFs to choose from that you won’t pay commissions on. There are, however, almost 3,000 NTF mutual funds available for trading. They also offer forex trading, but you’ll need at least $10 million in assets to access this feature.

Best Online Stock Trading Platforms FAQ

How much do online brokerage firms charge?

For active traders who want to minimize costs, an online stockbroker can save you a lot compared to a traditional brokerage. When you go with a full-service brokerage, you’re usually charged a percentage of the trade amount. With a discount brokerage account, you pay a low commission on every trade.

But with an online brokerage account, you typically get charged a flat fee for each trade, which can save you a lot over the long run. Depending on the type of transaction, you can expect to pay anywhere between $5 and $20 per trade.

What is the best stockbroker for beginners?

Most beginner traders incur losses because of several factors, including choosing an unsuitable online broker. Consequently, it is advisable to start with a platform designed to make trading easier. Some factors to consider when choosing an ideal platform for beginners may include:

Dedicated advisers to help you make better decisions through comprehensive analysis and one-on-one guidance.

A demo account with which you can practice as you learn and prepare for real-life trading.

A dedicated customer support desk to help you overcome complications with the platform or the markets.

Learning materials to familiarize you with the platform and the markets (fortunately, most offer updated learning materials).

A diverse range of trading options.

An easy-to-use trading interface.

Affordable fees and account minimums.

This guide includes excellent online brokers for beginners, such as Robinhood and Charles Schwab. However, don’t be afraid to cast your net further as you look for the ideal platform for your needs.

Which online trading platform is best?

All online trading platforms advertise themselves as the best. However, some offer better trading options and overall superior quality of services than others. Additionally, you will find that some platforms suit your investment needs and preferences better than others.

Consequently, it is advisable to consider what each platform offers based on your needs. Some questions to ponder when choosing an ideal online brokerage platform may include:

What do I know about online trading?

Will I need someone to guide me through some (or all) of my trades?

How much money do I need to invest?

Can I trust the platform with my money?

For example, you will need a beginner-friendly online broker if you are new to trading. Additionally, a platform that requires a high account minimum may not be right for you if you don’t have a lot of money to start with. You will also benefit from our guide on choosing a suitable online broker as you continue reading.

What is the most profitable trading platform?

It is true that some trading platforms offer better investment options and terms than others. However, it is a common misconception that some platforms can make you more money than others. While some platforms can save you money, but they will not automatically make you more money.

How much money you make on any trading platform depends on your overall trading strategy and accuracy. Online brokers don’t influence market directions—the markets do!

Here are some tips on how to develop a winning and profitable trading strategy:

Take classes about stock trading (and investment in general) before diving in with the sharks. You want to continue to learn throughout your trading career.

Always have a trading plan, including comprehensive money management criteria for every trade. It is also a general rule of thumb never to trade more than you can afford to lose.

Leave emotions out of trading and treat it like a business (one that can change your life if managed well).

Take advantage of trading tools and other technologies to improve your accuracy and timing.

Know when to stop trading and always use a stop loss.

This FAQ includes a comprehensive guide on choosing an ideal online trading platform. Fortunately, there are hundreds of high-quality online brokerage platforms.

Which online broker has the lowest fees?

Some online brokers charge exorbitant fees, while others charge pennies. To this end, you can save thousands of dollars per year by choosing an online broker that offers affordable fees.

With such variation, it is critical to identify your broker’s fees for different services and do the math. Most people focus on commissions. However, it’s also important to consider charges such as margin rates, finance rates, spreads, and conversion fees.

Traders looking to work with online brokers charging minimum fees may be interested in discount brokers. This is because a discount broker executes orders at a fraction of what other stockbrokers charge. As a result, discount brokers are wildly popular and constitute a considerable portion of the fintech industry.

However, it is worth noting that discount brokers don’t offer a full range of services. Most notably, they don’t provide investment advice, unlike full-service brokers. Consequently, the cost savings may not be worth it unless you are an excellent trader with a winning strategy.

What does a stockbroker do?

A stockbroker executes orders in the stock market on behalf of clients like yourself. Stockbrokers also offer their clients sound financial advice, but they are obligated to follow their clients’ directions. They are also commonly called investment advisors or registered representatives.

You must be fully qualified and licensed to work as a stockbroker. Additionally, you must be a member of a stock exchange (such as the New York Stock Exchange) to buy or sell on their platforms. Consequently, not everyone can buy or sell directly from the platform. Stockbrokers function as the go-between as their license automatically qualifies them as members.

Interestingly, many stockbrokers today mainly specialize in financial advisory and planning, thanks mostly to the rise of online stockbrokerage platforms. These platforms have eased access to the stock markets. Essentially, anyone with access to the internet and genuine interest in the markets (and some capital) can start trading in minutes.

Should I hire a stockbroker?

Trading stocks and other securities has never been easier, thanks mainly to the rise of online brokerage platforms. To this end, it is common for many people to view stockbrokers as redundant. However, they are not. Even experienced traders ensure that they always have a stockbroker on speed dial.

So, why should you hire a stockbroker? Here is an overview of three irrefutable reasons why a stockbroker could be invaluable:

First, stockbrokers can read the markets with accuracy. They can also give you tips on profitable trades before the rest of the market can dilute the trend.

Second, stockbrokers can manage all of your investments if you don’t have the time to do it yourself. This allows you to facilitate a passive investing strategy and potentially lucrative passive income.

Finally, stockbrokers can give you deep financial advice that extends beyond investing. This can help you better manage your personal and business finances.

Ultimately, a stockbroker’s services pay their fees several times over if you put their advice to good use. However, it is prudent to pick a competent and intelligent stockbroker to ensure that you get sound investment and financial advice.

How do I choose an online brokerage?

Online brokerage platforms make it easy and affordable for anyone to trade stocks and other securities. There are hundreds of online brokers, and some offer better terms and services than others. Hence, it is advisable to choose your online brokerage platform wisely. Here is an overview of three factors to consider when choosing one:

Account Fees & Minimums

All online brokers charge fees to use their platforms, just like you would pay a stockbroker. Additionally, many online brokerage firms require their clients to maintain a minimum amount of money in their accounts. Therefore, it is advisable to ensure that the amounts in both cases are low and affordable.

Investment Options

It is always advisable to diversify your investments across multiple securities and other investment options to spread (and minimize) risks. Consequently, it is vital to ensure that your chosen online broker provides access to as many securities as you need. Some of the main investment options include stocks, mutual funds, ETFs, bonds, and cryptocurrencies.

Support

Trading stocks can prove complicated, and most people find themselves wishing that they had a professional to guide them. Fortunately, many online stockbrokers offer access to individual stockbrokers for one-on-one investment and financial advice.

Stock Trading Fees Explained

You have to pay to play in the stock market, metaphorically speaking. You pay for the services provided by online brokers or brokerage platforms when you trade stocks. Stock trading fees come in varying types, and some of the most notable ones include:

Commission

Most brokerage platforms charge a commission for every trade, which is usually a dismal fraction of the trade’s cost. The commission can be charged as a flat fee or based on the volume of your trades. However, it is worth noting that more and more online brokers are eliminating commissions.

Spread

The spread is the difference between the bid and ask prices. Ideally, you would incur a loss if you bought and sold a trade simultaneously. This loss depends on the difference between the sell and buy prices.

Finance Rate

A finance rate refers to the cost incurred when you hold a leveraged position for longer than 24 hours. A leveraged position essentially is borrowed money, and your broker will charge you interest for this loan in the form of a finance rate.

Margin Rate

Trading on margin entails trading using money borrowed from the broker. The broker will also charge interest on this money in the form of a margin rate.

Conversion Fee

Do you need to convert your money to another currency to start trading? The broker will charge you a small conversion fee every time you convert currency for deposits or withdrawals.

How much money do you need to start investing?

It is easier than ever for folks to start investing, and often you can start with as little as $500. Some online stock brokers don’t require any account minimums at all. Where they do, the minimum investment amount will depend on your broker and the type of investment.

For example, most mutual funds have minimum investments of around $1,000, so if mutual fund trades are a priority for you, keep that in mind.

Is Stock Trading Safe?

While it is generally safe to trade stocks, that doesn’t mean there aren’t risks involved. The best trading platforms will work hard to keep you informed and minimize those risks.

As an online trader, it is also your responsibility to practice good security habits. Use the same security steps with a brokerage account that you would with your bank account. Additionally, always use common sense when trading.

What Are the Risks of Online Trading Platforms?

By virtue of being an online activity, there are several risks involved when you trade with online stock brokers. Let’s take a look at the most common risks:

Identity theft: As is the case for any online account you use, it is possible for your brokerage account to be hacked by scammers who obtain your personal identifying information. This is why it’s always vital to keep your passwords secure. You should also use two-factor authentication wherever possible to protect your accounts.

Computer viruses and malware: It’s important to ensure that the computer you use to access your brokerage account is always clean, secure, and free of malware. Hackers can use spyware to gain access to your passwords and personal information. So, protecting yourself means using a quality anti-virus program and performing routine checks.

Data breaches: Data breaches are a major risk for companies and customers alike, and unfortunately, they seem to be on the increase. As a customer, the most critical step you can take to protect yourself here is to only do business with reputable companies. Ideally, you want to choose one that has never had a previous data leak.

Phishing schemes: This often comes in the form of an email or text message which claims to be from your brokerage firm, but is actually an elaborate scam. Always pay close attention to the details in any communication you receive from your online stock broker. Never click on any links until you are certain the sender is legitimate.

Bottom Line

Your online stock broker is your gateway to investing, so it’s not a decision to take lightly. When searching for an online stock broker, it’s important to consider your unique investment needs.

You’ll need to compare costs, available investment options, account types, and how well the stock broker works for your investment style. Any of the online stock brokers above could be a great fit for your investing and trading goals.

In your search for online brokers for stock trading, make sure you take the time to figure out your priorities. Then, you can find a brokerage account that truly serves you. There are a lot of great online stock brokers out there, but being clear about your goals will make it easier to choose.

Today we’ll check out “Lennar Mortgage,” which is the financing division of parent company Lennar Corp.

If you weren’t aware, Lennar is one of the nation’s largest home builders, and is also nearly 70-years old.

Like many large builders, they have an in-house mortgage company that facilitates their new home sales.

Instead of outsourcing home loan lending to a third-party company, they’re able to provide the customer with a streamlined process from end to end.

Read on to learn more about their history and what types of loan offerings they have available, including special incentives you won’t find elsewhere.

Lennar Mortgage Fast Facts

The home loan division of parent company Lennar Corp.

Lennar is the nation’s second largest home builder, founded in 1954

Formerly known as Eagle Home Mortgage before a name change in 2020

Headquartered in Miami, FL, founded in 1981

Currently have building operations in 26 states nationally

Primarily utilized by home buyers who purchase a Lennar property

Funded over $14 billion in home loans in 2022

Known for offering big mortgage rate buydowns

As noted, Lennar Mortgage is the financing unit of its parent company, Lennar Corp.

While the parent company is nearly 70 years old, Lennar Mortgage is a lot younger.

In fact, they were acquired by Lennar back in 1999, at the time known as “Eagle Home Mortgage.” That company had been around since 1981.

As of December 5th, 2020, they were renamed Lennar Mortgage to make it clearer to customers that the company was part of the Lennar family.

At the moment, they have building operations in 26 states, meaning Lennar Mortgage is essentially available to customers in roughly half the country.

They primarily operate in the states of California, Florida, and Texas, along with the Mountain West and Mid-Atlantic states.

Last year, the company funded over $14 billion in home loans, with about 75% being conventional loans, 15% FHA loans, and 12% VA loans, per HMDA data.

While their website indicates that they offer refinance loans, they primarily serve their own home buyer customers with purchase loans.

Aside from operating a mortgage unit, Lennar also has Lennar Title and Lennar Insurance Agency, which allows them to streamline the home buying process.

They have physical branches throughout the country (where new home communities exist) and roughly 1,200 lending associates.

How to Apply with Lennar Mortgage

To get started, you can visit their website and get pre-qualified for a mortgage, or simply coordinate with your home buying rep after visiting a new home community.

They’ve got local loan officers throughout the country and physical branches in the states where they build homes.

Their new home communities may also have sales offices with lending representatives present.

Like other mortgage lenders, Lennar Mortgage offers a digital home loan experience that is mostly paperless.

It appears to be backed by ICE Mortgage Technology, one of the leading fintech companies in the mortgage space.

Customers can apply from any device and auto-save their loan application to pick up where they left off.

And automatically connect bank statements, tax returns, and income documentation within minutes, with bank-level encryption to provide peace of mind.

On-demand digital mortgage support is also available for those who need help along the way, though most tasks can be completed without the need for human interaction if that’s a preference.

All in all, it appears they offer a good combination of human support, if needed, along with the latest technology for convenience.

Loan Options Available at Lennar Mortgage

Home purchase loans (and mortgage refinances)

Conforming and jumbo loans

FHA/VA/USDA loan options

Fixed-rate and adjustable-rate loans available

They lend on single-family homes and townhomes

As noted, most Lennar Mortgage customers will use the company for a home purchase mortgage.

While they do offer refinance loans, their primary objective is getting their parent company’s home buyers a mortgage.

The good news is they offer all the major home loan types a home buyer would need, whether it’s a conforming loan or a jumbo loan.

Or a fixed-rate mortgage or adjustable-rate mortgage, including the popular 7/1 ARM.

They also offer the complete suite of government-back loans, including FHA, VA, and USDA loans.

Down payments can be as low as zero on the government loan options, or just 3% for the conventional loan options.

They offer financing on primary residences, second homes, and investment properties.

Lennar Mortgage Rates

Once huge advantage to using Lennar Mortgage is their mortgage rate buydowns, which are pretty hard to beat.

Since mortgage rates surged higher, from around 3% in early 2022 to nearly 8%, companies like Lennar Mortgage have been offering large rate buydowns to their own customers.

So those who use the company to purchase a Lennar home can take advantage of big interest rate reductions they likely won’t find elsewhere.

For example, you might see an advertised mortgage rate special of 4.99%, despite the 30-year fixed currently averaging 7.50% or higher.

Or a big dollar amount in incentives, which can be used like a lender credit to cover closing costs or apply toward a rate buydown.

This is their big advantage as a home builder’s captive financing unit. They’re able to offer special deals that can boost affordability, even if market rates are high.

In terms of advertising their rates, you won’t find a page dedicated to mortgage rates on their website.

And these rate specials will vary from community to community nationwide, depending on supply and demand of newly-built homes.

Is Lennar Mortgage Legit?

Yes, they are the official financing division of Lennar, one of the largest home builders in the United States.

In fact, Lennar Corp. was reportedly the second largest home builder in the nation as of 2023, trailing only D.R. Horton.

The company is also publicly traded on the New York Stock Exchange (NYSE: LEN) and is valued at over $34 billion at last glance.

They are a Fortune 500 company as well and date back to the 1950s, which is older than most mortgage companies in existence today.

Lennar Mortgage also has a 4.89/5 star rating on Zillow from over 2,100 customer reviews and holds an ‘A+’ Better Business Bureau (BBB) rating.

Keep in mind that you don’t need to use Lennar Mortgage just because you’re purchasing a Lennar home.

It’s perfectly acceptable to use a third-party lender, though it may be difficult for them to match the pricing incentives offered.

At the end of the day, Lennar Mortgage will likely have a huge leg up compared to other lenders thanks to their ability to structure pricing and rates in-house to boost affordability.

And because they offer a wide range of loan options and a digital mortgage experience, it’ll likely be a challenge for outside lenders to compete.

That being said, always take the time to gather other mortgage quotes and be sure to negotiate with the company.

Simply letting them know you are looking into other financing alternatives could result in more leverage and/or a better deal.

But when it comes time to refinance your loan, they likely won’t be nearly as competitive on pricing. At that stage, you’d probably be better off finding a new mortgage company to work with.

Lennar Mortgage Pros and Cons

The Good

Can apply for a home loan online or at a physical branch

Offer a paperless digital mortgage experience

Integrated title and homeowners insurance companies

Lots of loan options including fixed rates and ARMs

Offer big incentive to home buyers including rate buydown and lender credits

Free credit guidance to those who need to boost their FICO scores

Access to mortgage calculators and learning center online

Excellent reviews from past customers

The Maybe Not

Do not advertise their daily mortgage rates online

GuideWell Mutual Holding Corp., the parent company of health insurer Florida Blue, is the biggest company headquartered in Jacksonville.

But as a mutual holding company that doesn’t publicly report financial results, we don’t often have a chance to know how big it is.

However, as the company announced the appointment of a new chief financial officer Sept. 27, its news release indicated GuideWell has grown significantly in just the last two years.

Jeffrey Goddard, executive vice president and chief financial officer, GuideWell

The announcement of Jeffrey Goddard’s appointment said GuideWell has grown into a “health solutions enterprise” with annual revenue of $30 billion.

That would make GuideWell one of the 150 largest U.S. companies, based on Fortune 500 data. But Fortune magazine’s annual list of largest companies doesn’t include businesses that don’t publicly report data.

Just two years ago, GuideWell was saying annual revenue was at $20 billion.

The company did expand in February 2022 with the acquisition of Triple-S Management Corp., licensee of the Blue Cross Blue Shield insurance brand in Puerto Rico, adding about $4 billion in revenue.

Besides Florida Blue and Triple-S, GuideWell said it owns or has significant interests in several other health care businesses.

GuideWell is about double the size of the largest Jacksonville-based company in the Fortune 500.

Railroad company CSX Corp. ranked 279th with 2022 revenue of $14.86 billion.

GuideWell said Goddard joined the company as executive vice president and CFO, succeeding Thurman Justice, who took over leadership of the managed care business at Triple-S.

Goddard was most recently senior vice president and CFO for CVS Caremark.

ICE: Black Knight deal helps mortgage ‘ecosystem’

After Intercontinental Exchange Inc. agreed in May 2022 to acquire Jacksonville-based mortgage technology firm Black Knight Inc., antitrust officials were concerned the deal would give ICE too much control over mortgage technology in the U.S.

Now that the deal is completed, ICE officials said in a Sept. 28 conference call the merged businesses will benefit everyone involved in the mortgage process.

Ben Jackson, president of ICE’s mortgage technology business

Ben Jackson, president of ICE’s mortgage technology business, said the company was convinced when it agreed to buy Black Knight that the deal would result in an improved mortgage workflow.

“Over the last 16 months, our confidence in that strategic vision has only increased,” he said.

ICE’s technology will be able to handle mortgage loans from origination to final settlement “in one digital ecosystem,” Jackson said.

Black Knight dominated the market for technology for servicing existing home loans, handling processing for nearly two-thirds of all first mortgage loans.

ICE is the market leader in technology for originating mortgage loans.

“The breadth and depth of what we have assembled touches nearly every home mortgage in the United States and is a platform that we believe will enable us to provide the foundation for improving risk management in this major consumer credit market,” ICE Chief Executive Jeff Sprecher said in the conference call.

“Together with Black Knight, ICE is well positioned to improve the execution and subsequent settlement and servicing of U.S. home mortgages, the major credit exposure for most U.S. consumers,” he said.

To satisfy antitrust concerns and gain Federal Trade Commission approval for the merger, the companies agreed to sell off Black Knight’s loan origination technology business called Empower and its data subsidiary Optimal Blue.

ICE Chief Executive Jeff Sprecher

However, the deals to sell those units to Constellation Software Inc. included an agreement that will give ICE mortgage technology clients access to Optimal Blue’s data services under its new ownership.

While ICE’s mortgage technology operations serve business customers, Sprecher said the merged company will be able to provide data that will help its clients deal with consumers.

“With Black Knight, we are now in a position to see data and micro trends that give us valuable insight into existing homeowners and prospective homeowners in the United States,” he said.

Black Knight is a successor to a long line of Jacksonville-based companies that have provided mortgage technology services since the 1960s.

ICE has not announced any specific plans for Black Knight’s Jacksonville operations after the merger.

A company spokesperson said in an emailed statement Oct. 3: “With about two thousand people already in Jacksonville, and room to grow, it will quickly become an important part of ICE’s operations.”

Atlanta-based ICE provides financial technology in a number of areas and is best known as operator of the New York Stock Exchange.

Jackson said in the conference call that with Black Knight added to the company, the mortgage technology business will increase from 14% of ICE’s total revenue to 25%.

St. Joe gains help chairman’s fund

Reuters news service reported that a strong third-quarter stock performance for The St. Joe Co. helped its chairman’s mutual fund produce some of the best returns for the quarter.

St. Joe Chairman Bruce Berkowitz’s Fairholme Fund controls about 34% of the company’s stock, according to its latest Securities and Exchange Commission filings, and Reuters said the fund has more than 80% of its assets in St. Joe stock.

As the overall market fell in the third quarter, St. Joe’s stock rose 14%, with a big gain in late July after the real estate development company reported strong third-quarter earnings.

As a result, Fairholme rose 17% in the quarter while another fund with a large stake in St. Joe, the Schwartz Value Focused Fund, rose nearly 15%, Reuters said.

Meanwhile, the Dow Jones Industrial Average fell 2.6% and the S&P 500 fell 3.6% in the quarter.

Panama City Beach-based St. Joe was a long-time conglomerate headquartered in Jacksonville before selling off its other businesses to focus on real estate development.

The company moved the headquarters to the Florida Panhandle in 2010 to be closer to its real estate holdings.

High rates affect Dream Finders, other homebuilders

Dream Finders Homes Inc. was the best-performing stock among Jacksonville-based companies in the first half of 2023, nearly tripling in price.

However, continued high interest rates are hurting the homebuilder sector, and Dream Finders’ stock has dropped sharply since peaking in early August.

The stock ended the third quarter at $22.23, down nearly 30% from its Aug. 7 peak of $31.60 and down nearly 10% for the entire third quarter.

However, Dream Finders still had a net gain of more than 150% for the first nine months of the year.

FPL parent’s stock drops sharply

NextEra Energy Inc.’s stock dropped sharply after a related business said it was cutting its growth expectations.

Juno Beach-based NextEra is the parent company of Florida Power & Light, which provides electricity to 5.8 million Florida customers. It serves most of the state’s East Coast outside of Jacksonville.

NextEra formed a limited partnership in 2014 called NextEra Energy Partners, or NEP, to own and manage clean energy projects.

The limited partnership announced Sept. 27 it was cutting the expected growth rates for distributions to its shareholders to 5% to 8%, with a target growth rate of 6%, down from the previous level of 12% to 15%.

NEP cited tighter monetary policy and higher interest rates for the cut.

That caused NEP units to lose more than half their value, falling from about $50 two weeks earlier to a low of $24.25 on Oct. 2.

NextEra’s stock fell from the upper $60s to a low of $50.18 on Oct. 2.

Wells Fargo analyst Neil Kalton cut his rating on NEP from “overweight” to “equal weight” Oct. 2 and cut his price target from $80 to $33.

“Despite a still strong secular backdrop for renewables and a high quality sponsor (NEE), NEP’s existing cost of capital raises questions about the partnership’s ability to execute on growth initiatives,” Kalton said in his research note.

In a Sept. 28 note, J.P. Morgan analyst Jeremy Tonet said he was maintaining his “overweight” rating on NextEra Energy Inc., or NEE, after the NEP announcement.

“While these concerns and sharp NEP weakness could weigh on NEE in the near-term, we see the sell off as overdone. We still see FPL as one of the best utilities in the country (benefiting from a constructive regulatory backdrop and favorable economic trends),” Tonet said.

FEC Railway expanding intermodal services

The Jacksonville-based Florida East Coast Railway announced a deal Sept. 27 that will expand its intermodal business.

FEC, which operates a 351-mile railroad from Jacksonville to Miami, said it agreed with Norfolk Southern Corp. to provide intermodal service at FEC terminals in Fort Pierce and Fort Lauderdale.

Norfolk Southern was already providing services at FEC terminals in Miami and Titusville, it said.

Atlanta-based Norfolk Southern is the main competitor of CSX, providing railroad services in much of the Eastern U.S.

Its railroad connects to FEC’s rail line in Jacksonville.

FEC said the new agreements will help it offer services for freight customers to more U.S. cities outside of Florida.

FEC is owned by GMXT, the transportation subsidiary of Mexico City-based Grupo Mexico.

GMXT acquired the Florida railroad in 2017.

Safe & Green Holdings spinoff completed

Safe & Green Holdings Corp. completed the spinoff of its real estate development subsidiary into a separate company on Sept. 28, and Safe and Green Development Corp. is now trading on Nasdaq under the ticker symbol “SGD.”

Safe & Green Holdings continues to trade under the ticker “SGBX.”

The company’s main business is converting cargo shipping containers into buildings, and it announced its plan to spin off its real estate development company in December 2022.

The company was formerly known as SG Blocks and was headquartered in Jacksonville, but it moved its offices to Miami in early 2023.

A financial instrument is simply a contract between entities that represents the exchange of money for a certain asset. Financial instruments include most types of investments: cash, stocks, bonds, mutual funds, exchange-traded funds (ETFs), certificates of deposit (CDs), loans, derivatives, and more.

Financial instruments facilitate the movement of capital through the markets and the broader economic system. While this may take different forms, the flow of capital remains a central feature.

What Is a Financial Instrument?