Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Disclosure regarding our editorial content standards.

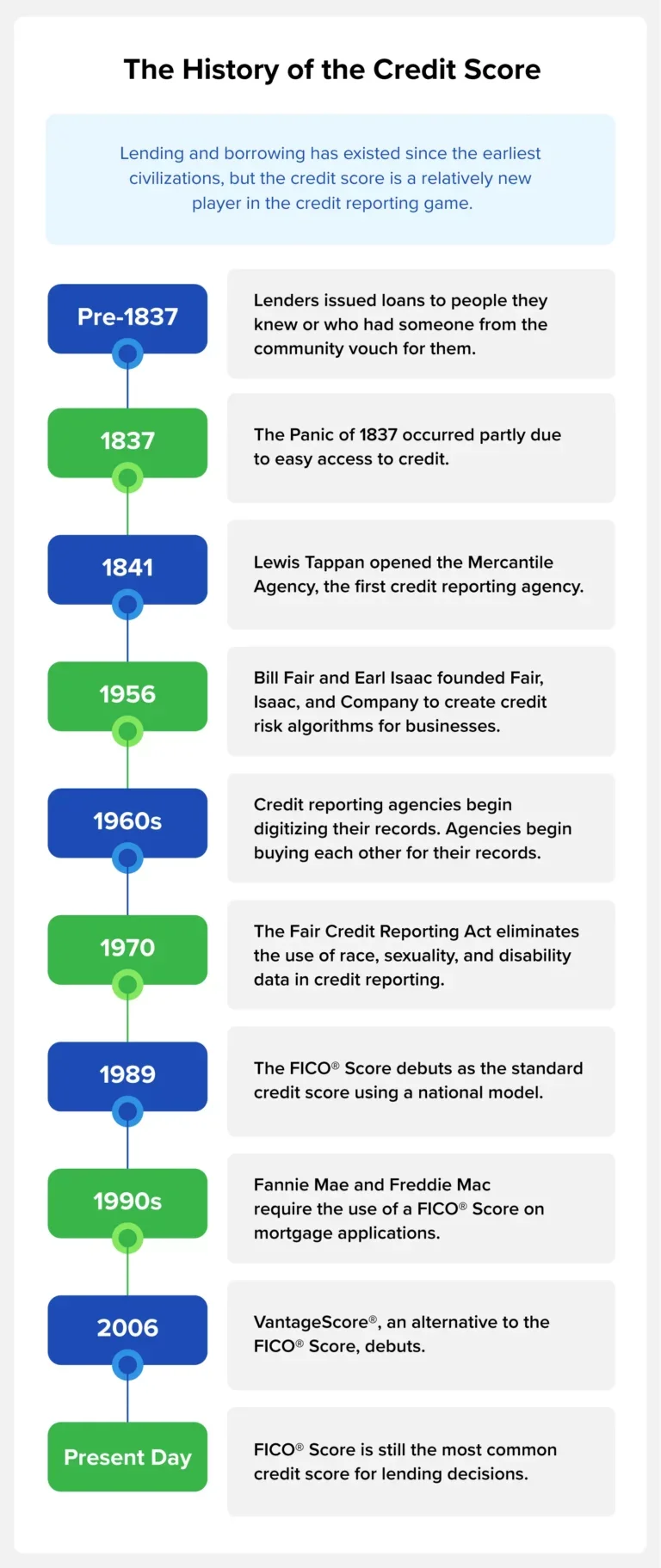

The credit score was invented in 1989 to make credit reports more actionable for lenders.

Credit scores affect many parts our lives: whether we qualify for a loan, what interest rate we pay, even where we can rent or whether we get our dream job. But that three-digit number is a relatively new invention—the credit score was invented in 1989, less than 50 years ago.

Understanding the origins of the credit score can help you better comprehend why lenders use it and how to improve your financial situation.

When Credit Scores Were Invented

People have borrowed and lent money for centuries. In the early days, storekeepers and lenders only extended credit to people they knew, or they would ask people they respected in town for their views on a person’s credit risk. This informal credit reporting system was highly localized and incredibly subjective.

But as credit became more critical to daily life and people began to move around more, the need for a more widespread credit reporting method arose.

The 1800s: The Rise of Credit Reporting Agencies

After the Panic of 1837 (partly caused by easy access to credit), Lewis Tappan recognized that businesses might benefit from a better understanding of who to issue credit to. In 1841, he formed Tappan’s Mercantile Agency, the first credit reporting agency in America, to meet this need.

His company hired “correspondents,” reliable men (often attorneys and ministers) who would investigate people’s standing in their communities and report it to the central office. They would then add the information to a central ledger in New York City. Many businesses subscribed to the Mercantile Agency to view these reports before issuing credit.

Tappan was a strict abolitionist, so he only worked with businesses in free states, so other credit reporting agencies began to spring up to work with businesses in the South. Hundreds of these credit reporting agencies existed all over the country by the end of the Civil War, but the system had a few problems:

Each agency had different information based on who they hired as correspondents.

Information was highly subjective and included information about a person’s race, gender, and overall moral character, which allowed bias to play a role in lending decisions.

Lenders didn’t know how to interpret the information in the credit reports because they were so subjective, and lenders often didn’t know the person applying for credit.

As more people began to access credit to purchase items like cars and homes in the late 1880s and early 1900s, these credit reporting agencies continued to thrive.

1950s and 1960s: Digitizing Credit Reports

This system was still in place in the 1950s when the ability to digitize records meant that some standardization could occur. Larger agencies started buying their smaller counterparts for additional data they could add to their reports, and national credit bureaus began to form.

In 1956, Bill Fair and Earl Isaac created Fair, Isaac, and Company to make credit reports more actionable for lenders. They used the data in a credit report to perform a statistical analysis that would inform a lender of a person’s credit risk. What resulted was a more analytical approach to interpreting credit reports, but each business or lender had its own algorithm based on the factors they prioritized.

As records continued to be digitized, many people became concerned about the surveillance being done to gather credit information and discriminatory practices in credit reporting. People also realized that credit mistakes would be available forever and could potentially hurt people’s ability to borrow for their entire lifetimes. The Fair Credit Reporting Act of 1970 put several protections into place, including:

Removing data related to race, sexuality, and disability from credit reports

Requiring credit reporting agencies to delete information after seven to 10 years, depending on the type of data

1989: The FICO Credit Score

While more effective for lenders than the previous system, scores varied widely based on a company’s priorities.

The credit reporting bureaus wanted something more standardized, so they partnered with Fair, Isaac, and Company (now known as FICO®) to create the FICO Score, a national scoring model for everyone. The FICO Score debuted in 1989 and quickly became popular with lenders, who no longer needed to hire companies to create their own algorithms. Consumers, who could now know their credit score before applying for a loan, also appreciated the FICO Score.

In the 1990s, the FICO Score cemented itself as part of the lending landscape when Fannie Mae and Freddie Mac began requiring the score as part of mortgage applications.

VantageScore and Other Credit Scores

In 2006, the three major credit reporting bureaus—Equifax®, Experian®, and TransUnion®—launched the VantageScore®, an alternative to the FICO score. There have been four iterations of the VantageScore since 2006, and the latest version incorporates trended credit data, which includes monthly data points over 24 months. It also utilizes machine learning and does not factor medical debt into its algorithms.

Each major credit reporting bureau also has its own proprietary scoring models that lenders may also consider:

Equifax Credit Score

Experian PLUS Score

TransUnion CreditVision New Account score

Despite these options, most top lenders use the FICO Score.

Why Credit Scores Were Invented

Before the credit score, lenders determined a person’s credit risk based on credit reports, which include:

Personal information

Account information

Hard inquiries into your credit

Public financial records such as liens or bankruptcies

Often, lenders weren’t sure how to interpret your credit report, which led to bias in lending decisions and general confusion for consumers regarding whether they would be approved for a loan when they applied.

The credit score was invented to standardize the lending process to make it faster and more equitable. It prevented lenders from using racial, gender, and class bias when determining someone’s credit risk.

Problems With Modern Credit Scoring

While credit scores eliminated the problems of previous credit reporting systems, they aren’t perfect. Here are a few issues with modern credit scoring:

Inappropriate use of credit scores. When the credit score was originally invented, its sole purpose was to determine credit risk for loans. Now, lenders, landlords, and employers often use it to determine a person’s level of responsibility, which can influence car insurance rates and hiring decisions.

Upholding social hierarchies: People with low credit scores, or the roughly 10% of Americans with no credit history, are often denied access to loans or credit cards. When they receive a loan, they often have to make a larger down payment and pay more in interest.

Racial disparities: While the Fair Credit Reporting Act of 1970 removed the use of race as an explicit factor in one’s credit, institutional racism may still impact the remaining factors. For example, redlining continues to prohibit many Black Americans from purchasing a home, preventing them from building wealth through homeownership. As a result, their credit length and payment history, two factors that impact your credit score, may be shorter. This may explain why multiple studies have shown that racial minorities have lower credit scores than white people.

Inaccurate information: A recent study found that 34% of people have at least one error on their credit report. These errors can lower your credit score, resulting in you paying more in interest. While you can dispute errors on your credit report, it may take time to see an increase in your credit score.

These problems could result in you paying more in interest for a loan or being denied the loan altogether.

The Future of Credit Scores

Credit scores have changed since they were invented and will continue to do so as consumer spending and technology change. Here are a few trends that may impact how credit bureaus determine your credit score in the near future:

Buy Now, Pay Later (BNPL): Also called point-of-sale (POS) installment loans, BNPL plans allow you to divide purchases into lower monthly payments, often without interest. Currently, these short-term loans aren’t reported to a credit bureau unless you don’t make your payments, but that may change as technology advances to allow real-time data and these become more popular with consumers.

AI and Machine Learning: Experts are currently debating the use of AI and machine learning to automate and improve credit scoring. Some parties claim it will result in more accurate credit risk assessments and allow credit reporting to occur in real time, making it more accurate. Others are concerned about the potential invasion of privacy and the ethical use of data since AI is only as good as the data it is fed.

Inclusion of alternative data: Nearly 37 million Americans are credit underserved, meaning they have little to no credit history. As a result, they are unable to get access to credit. To help the credit invisible gain credit, credit reporting companies have begun considering alternative data, called consumer-permissioned data, including bank account information and monthly payments like rent, utilities, and streaming subscriptions. Currently, consumers can choose to share this information with lenders and then retract access once they’ve built credit, but this information could begin factoring into everyone’s credit score since AI can make this data easier to use.

Track Your Credit Score With Credit.com

Your credit score is one of the most important numbers in your life. Understanding the history of the credit score and its challenges can help you in your journey to improve your credit. As technology continues to advance, stay informed on the latest updates to credit scoring and take proactive steps to manage your credit with Credit.com.

Rates were already high coming into this week. As of last Friday, that meant an average 30yr fixed rate just under 7.5%. As of this Friday, we’re closer to 8%.

Certain lenders may be quoting lower rates, but that often involves the presence of discount points. The Freddie Mac survey (orange line above) doesn’t account for discount points. It’s also a weekly average and has not yet counted the rates seen on Thursday or Friday.

Friday brought a sharp rise to the highest levels in 23 years. The most obvious culprit was the big monthly jobs report which showed job creation (nonfarm payrolls) increasing far faster than economists predicted. It was one of only a handful of months in the past few years that came in higher than the 12 month trailing average.

Perhaps just as importantly, this is a level of job growth (336k) that falls at the upper edge of the pre-pandemic range.

Most economists thought we wouldn’t be breaking back above 300k after averaging less than 200k for the past 3 months. In a world where the Fed constantly reiterates “data dependence,” this was a blow for rates. 10yr Treasury yields–the most ubiquitous long-term rate benchmark–left no doubts as to the bond market’s response.

It’s easy enough to see the vertical line after the jobs data, but what’s up with the fairly big recovery later in the day? If bonds are freaked out about data, why would they erase a majority of the losses?

There are a few reasons. The best one is actually the most esoteric as it has to do with the tendency for traders to close out trading positions on Fridays and especially on the Fridays before 3-day weekends. If traders were betting on higher rates (and they were!), the closing of those positions would bring rates back down a bit.

Ultimately, that position closing doesn’t really change the bigger picture. In fact, the jobs report reaction barely sticks out on a longer term chart. What DOES stick out is the shift in momentum that began after the last Fed day–the one we’ve discussed a few times now as the market’s way of repricing toward a “higher for longer” rate trajectory.

It continues to be the case that economic data needs to be substantially more downbeat on a consistent basis (2-3 months) in order for the Fed to acknowledge that a true shift is taking place and that the end of their “higher for longer” policy stance is up for discussion. Only then would rates have a chance to meaningfully decline.

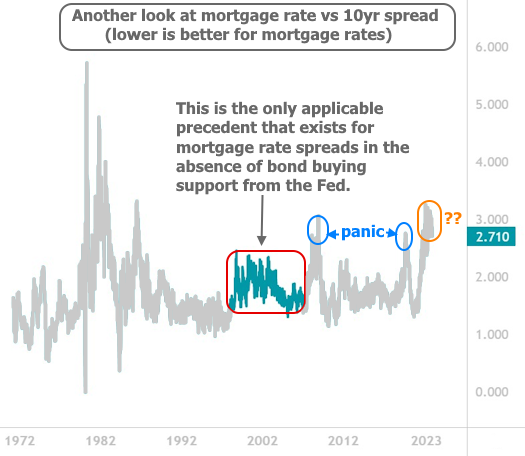

Still, there’s lots of hope out there that rates could/should decline for other reasons. One observation that’s become quite popular is the wide spread between mortgage rates and 10yr Treasury yields. For some reason, people think if spreads could only be a bit more narrow, mortgage rates could be more tolerable without the need for any major change in the broader bond market.

The following chart shows mortgage rates and 10yr yields on the same axis. It’s hard to track spreads with a chart like this, but it’s easy to see why the 10yr is used as a benchmark for mortgages!

The next chart makes the change in spreads easier to track. It is quite simply the value of the blue line above minus the value of the orange line. It shows that people might not be too crazy to hope for a return to a more normal spread range. After all, if we’re near 3% right now, a move down to 2% would put the average mortgage lender back in the high 6% range for a 30yr fixed.

A 2% spread is probably something that can be reasonably entertained, but some pundits are talking about spreads in the 1 to 1.5% range. A tightening of that magnitude is highly unlikely in the short term and possibly even “ever.” To talk about why, we first need a quick refresher on the Fed’s role in the mortgage market.

In order to prevent more catastrophic outcomes from the Great Financial Crisis, the Fed began buying large amounts of mortgage-backed securities (MBS) in 2009. In conjunction with the Fannie/Freddie conservatorship, this calmed investors and brought spreads down (mortgage buyers demand higher yields/rates when mortgage debt is perceived as more risky, thus inflating spreads).

Over the next decade, the Fed would not be able to stop buying MBS for long without spreads blowing out. Notably, there was only about a year of time before covid that the Fed was actually decreasing the amount of MBS it owned. That year coincided with broadly lower rates due to the trade war, and a lower rate trend helps spreads stay more narrow than they otherwise would be.

Why can’t we use the time before the financial crisis as a spread baseline? We can, to some extent, but nothing before the housing reforms of the mid 90s which expanded accessibility to mortgage financing and made the landscape riskier for investors. There is a very obvious bump in spreads at that time, and that marks the only real baseline that matters. Here’s the same chart, but with that time frame highlighted.

Since covid, we’ve had two instances of panic. The first was addressed with the most massive glut of Fed bond buying in the history of Fed bond buying. It crushed spreads and set us up for the world of pain we’re in now. As the Fed once again began shrinking its mortgage holdings in 2022, spreads blew out again. Combined with the surge higher in benchmark rates and the overall volatility (both things that hurt mortgage spreads) we saw even higher levels at the end of 2022.

But now, miraculously, without any Fed intervention, spreads have been grinding to slightly narrower levels. Sure, they’re still very wide, historically, but the Fed will definitely not be riding to the rescue this time around. Moreover, policymakers won’t likely be concerned enough to do anything about it until and unless a broader interest rate correction fails to help mortgage rate spreads come in a bit. Fortunately, a broader interest rate correction will almost certainly do just that. Just don’t expect it to restore the 1.0-1.5% spread level any time soon.

Think of it more like this: if 10yr yields find a scenario where they can rally down to 3.5% and spreads can return to 2.0%, that puts a 30yr fixed mortgage rate at 5.5%. At that level, the conversations about the weird things that need to happen to save the mortgage market would be very different, or altogether unnecessary.

Inside: Looking for the best travel essentials? Look no further! This guide has everything you need to pack for a trip.

There’s no feeling quite like the thrill of embarking on a new adventure, and with these top-notch travel essentials, your journey is set to be an absolute blast!

These travel essentials play a crucial role in not just enhancing your travel experience but also in keeping your trip organized, efficient, and absolutely “funner”!

Prepare to soar into hassle-free travel filled with joy, convenience, and unforgettable moments.

Many of my readers diligently save for their vacation and sometimes forget the small details like – travel essentials.

Traveling can transform from a stressful ordeal into an exciting escapade when armed with these must-haves that smart travelers swear by.

So, buckle up for an exhilarating journey ahead, knowing you’re perfectly prepared to take on the world. Let the adventures begin!

What are Travel Essentials?

Getting back to travel? Isn’t it just lovely!

Well, travel essentials are your new best friend! Waves of seasoned globetrotters have prepared this special guide for your benefit.

These items qualify as essentials because they streamline the packing process, afford comfort while traveling, and add a dash of fun to your adventures.

Also, there are so many cool gadgets available now that make traveling seamless.

What things are essential for Travelling?

Before you head off on the trip of your dreams, pack the right travel essentials to maximize your fun!

Meds: Don’t forget your prescriptions and common medicines for allergies or pain. Remember, health first!

Travel Insurance: Give yourself peace of mind by buying travel insurance – especially if you are traveling internationally.

Travel Credit Card: Credit cards are a simple way to pay when traveling. Make sure you have no foreign transaction fees!

Document Copies: Keep digital copies of essential documents to minimize panic and ensure quick verification in case of loss. And share this with someone in case you lose your phone!

Joyous journeys come from well-prepared travelers!

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What are 3 items to take on vacation?

Embrace the exhilarating aura of preparing for your much-awaited vacation!

Tuning into your needs and wants as a traveler, three crucial items stand out as top priority:

Anti-Theft Bag: This is an ideal travel companion – it comes with built-in security features that keep your belongings secure, reducing the risk of theft during your travels. With advancements in fashion, you can now find stylish options with exceptional functionality, making them perfect for vacations where style and security are priorities.

eReader: like the Kindle Paperwhite, makes the perfect vacation companion as it combines the portability and weightlessness of a single book while providing the capacity to store thousands of novels for entertainment. Moreover, its adjustable light settings and long battery life facilitate reading during transit, whether it’s mid-flight or at night, without disturbing others – a luxury traditional books can’t offer.

Tech Organizer Case: ensures all essential tech accessories like cables, adapters, and devices are neatly organized and easily accessible. This not only eliminates the hassle of rummaging through your bag for a tangled cord but also helps to maximize the efficient use of space within the bag.

Remember, the key is to pack smart and embrace savvy travel essentials that optimize comfort and convenience!

Best Travel Essentials Everyone Wants

Planning for a trip often entails the excitement-charged task of selecting the right essentials to pack.

This section highlights the best travel essentials that everyone craves, from the appropriate attire to tech gadgets, that go a long way in enhancing convenience during your journey.

These items, carefully curated by experienced travelers, promise to make every trip, whether short or long, a hassle-free experience.

1. Apple AirTags

Get ready for your next adventure with a travel essential that’s as smart as it is useful – the Apple AirTag.

This tiny gadget can make your trips stress-free by preventing the harrowing instances of lost luggage.

As a modern-day traveler, you’ll love the security it brings to your journeys. Simply sync the AirTag with your ‘Find My map’ and place it in your luggage to keep track of your belongings from point A to point B.

Lost luggage is increasingly common, but with an Apple AirTag, you’re covered.

Don’t forget these handy AirTag holders!

2. Travel Backpack

A travel backpack is your next must-have travel essential!

It’s an easy and convenient way to keep all your essentials – think wallet, phone, keys, passport – in one place, and with some even featuring a built-in USB port, you’ll never run out of battery on the move.

Its versatility and functionality, such as several compartments for organization and a separate section for shoes, are just unbeatable. Seriously, these travel backpacks are way cooler than your backpack from high school!

3. Luggage Scale

Traveling soon? Don’t even think about neglecting the trusty luggage scale!

This small but mighty tool, loved by frequent travelers like us, is your ticket to a stress-free journey.

With this compact gadget, say goodbye to dreaded overweight baggage fees.

Pack it in your carry-on for on-the-go convenience and weigh it with precision every time. One of my best gifts ever!

4. Anti-Theft Bag

An Anti-Theft Bag offers peace of mind when traveling, with built-in safety features deterring theft. These bags aren’t just secure but also fashionable, which is perfect!

The locking zippers act as a deterrent against potential theft as they add an additional barrier of protection.

Moreover, the incorporation of RFID blocking technology in these bags ensures your valuable information stays protected. This technology prevents identity theft by safeguarding any object with an RFID chip, such as passports issued after 2006 and credit/debit cards, from being read through your bag.

While traditionally, anti-theft bags have been seen as lacking in style, new versions of these bags are coming up in several fashionable options. As stated, they are now available in various colors like navy, charcoal, merlot, and blush apart from the usual black.

5. Underwater Action Camera

As a travel essentials superstar, the Underwater Action Camera ensures you never miss capturing a thrilling aquatic adventure. Turning ordinary snapshots into extraordinary keepsakes, this camera becomes a must-have for wanderlust souls.

Remarkably sealed, this camera captures stunning photos even from underwater.

Perfect for beachy holidays, and even more beneficial for snorkelers and swimmers.

Get for a tech-free vacation!

Pro tip: Master using this camera during daylight for better results.

6. Bluetooth Earbud Transmitter – Perfect to Use Your Airpods Pro

Head off on your next adventure armed with the Twelve South Bluetooth Audio Transmitter. This coveted travel essential turns your flight into a personal cinema!

Its superb features include high-quality sound transmission, pairing capabilities with airplane TVs, and functioning as a headphone splitter.

Ideal for tech-savvy travelers and those who love using their own headphones.

7. External Portable Charger

Don’t forget your portable charger – it’s a true travel hero! Imagine never running out of battery while navigating unfamiliar territories or capturing memorable moments.

This external power bank ensures your devices always stay juiced up.

Lightweight and compact size

Fast-charging capability

Can charge multiple devices at once.

Expert tip: Choose a charger that can power your device type at least 4x from zero battery.

8. Lightweight Luggage

Investing in lightweight luggage helps travelers avoid excessive baggage fees.

This is what we did over ten years ago and I can truly say we have saved thousands of dollars.

Look for luggage that weighs less than ten pounds. With most airlines capping luggage weight between 40-50 pounds that gives you 30-40 pounds of your stuff that you can pack.

While it is an upfront investment in new luggage, you will significantly reduce the risk of incurring additional fees.

9. Travel Wallet

This is something I picked up right before my last flight (teal of course)! I loved it because it was lightweight and compact size for easy carrying. Even in my yoga pant pocket!

Heald exactly what I needed with organized compartments for ID, cash, and credit cards

Sleek design that suits any style

RFID protection to keep your information safe

Travel wallets are perfect for minimalist travelers who love simplicity and security.

Learn how much cash can you fly with. It is more than your travel wallet!

10. Passport Holder

A passport holder: the travel essential you never knew you needed.

It’s the perfect companion for safeguarding your most priceless travel accessory – your passport.

Super convenient, passport holders come equipped with slots for important IDs, boarding passes, and even stashed currency.

The RFiD-blocking feature ensures your personal details remain secure from potential scams.

If you are traveling internationally, then this is something you want to seriously consider.

11. Tech Organizer Case

It’s a must-have to neatly stash all your tech essentials. Never be frazzled by tangled cords or lost chargers again.

The Tech Organizer Case, like the top pick FYY Electronic Organizer, is your ultimate travel buddy ensuring a clutter-free trip.

Ample space for multiple chargers, durable, and easy-to-use zippered compartments.

Be the organized traveler everyone envies!

12. Portable Door Lock

You mustn’t miss out on the Portable Door Lock when packing your travel essentials! This compact lock adds top-notch security and peace of mind to your trips.

Portable door locks are hot on the list of travel essentials because of their simplicity – easy to use, install, and pack in your luggage.

Best for solo travelers and Airbnb guests, this device prevents unexpected entrance even with a key.

Pro tip: Always test the lock right after installation for foolproof safety.

13. Carry-On Rolling Luggage

With precise packing, it is feasible to fit everything you need into this one carry-on, thereby ensuring a seamless travel experience.

Picking the best carry-on rolling luggage for your needs requires careful consideration. Rolling luggage with 4-wheels can be ideal as it takes the weight off your wrist and can be rolled effortlessly by your side.

Spacious enough to accommodate all your travel essentials like laptop, shoes, etc.

Opt for brands that offer a good warranty to ensure the durability of your luggage.

If your travel involves different types of terrain or switching from airports to cobblestones, you might want to consider a wheeled backpack which can be rolled or carried as needed. Lastly, always ensure that your chosen luggage is lightweight, versatile, and

These suitcases not only provide convenience due to their mobility but also allow the freedom to avoid checked luggage.

14. Toiletry Bag

Toiletry bags have become an essential part of smart packing for travel.

Hanging toiletry bags, like the Bagsmart option, represent a game changer, contributing significantly to an organized, convenient, and hassle-free travel experience.

Pick one that has the ability to accommodate a week’s worth of travel-size toiletries.

15. Travel Duffel Bag

Whether it’s a long adventure or a weekend getaway, a travel duffel bag is incredibly useful.

It holds your essentials—clothes, tech gadgets, toiletry bag, keys, phone—safely and conveniently.

Remember the thrill of keeping all your belongings organized? You get that with the multiple compartments.

Also, let’s not forget about that separate section for shoe storage—talk about clutch!

Best feature? Some come with a built-in USB port to ensure your devices are always charged.

Expert tip: Look for a bag that’s airline-compliant, lightweight, and durable.

16. Travel Pillow

Ready for your next adventure? Don’t forget your travel pillow – it’s your key to ultimate comfort!

Many popular Travel Pillows offer tailor-made support for your head and neck, especially on those long-haul flights. It’s lightweight and packs easily, meaning less hassle for you.

Best for those who value a peaceful in-flight snooze, this game-changing essential comes with a memory-foam wall offering unmatched comfort.

Pro Tip: Pair it with the EverSnug travel blanket, It doesn’t just keep you cozy but doubles as a compact cushion too! Now, that’s travel made comfy and convenient!

17. Sunglasses Case

Off to a sun-soaked adventure, you need a nifty sunglasses case! It’s a must-have to safeguard your shades from damage while in transit.

Perfect for those eyeing to pack multiple pairs of sunglasses, you’d love this.

Expert tip – Choose a case that securely holds your glasses snugly, ensuring no damage takes place during the journey.

18. Contact Lens Case Kit

After my last late night flight, I was determined to find a better system for my contact. Enter the Contact Lens Case Kit.

Perfect for maintaining your vision care away from home, this kit boasts a mirror, mini solution bottle for your contacts, lens case, tweezer, and remover tool.

You can also get a contact lens and glasses case combo travel kit!

This handy, compact kit is an asset to anyone wearing contacts. Not only will it make your travel simpler, but it’s also affordable, priced under $10.

19. Reusable Water Bottle

Set off on your travels with the ultimate companion, a reusable water bottle!

Refill at any airport water fountain and save on plastic and expenditure – a savvy choice for our planet and wallet!

Plus this is a frugal green item with less plastic waste and sustainable hydration.

Expert Tip: Pack Liquid IV or Nuun tabs to make your drink a fun experience!

20. Packing Cubes

Say goodbye to disorganized luggage with packing cubes—your best travel buddy!

They’re a lifesaver for the frequent flyer seeking an organized and hassle-free travel experience. Especially those traveling with kids!

With features like shoe sleeves and compressibility, they’re ideal for chronic over-packers or shared-luggage travelers. I cannot say how helpful packing cubes are for trips!

21. Luggage Straps

Luggage straps are a travel essential you shouldn’t overlook! These handy accessories offer added security and ease for every traveler.

Designed with durability and convenience in mind, luggage straps, such as the TSA-approved luggage nylon straps, keep your checked bags secure during long flights. You’ll also love their visibility feature – bright neon colors that make your suitcase easily identifiable!

Ideal for people frequently on the go, they’ve garnered solid endorsements from seasoned travelers.

22. Travel Pill Box

Say goodbye to loose pills and experience medication portability at its finest with the Travel Pill Box – a real game changer for travel essentials!

The sheer convenience it offers makes it a must-have for every traveler.

The Travel Pill Box keeps your medications organized with multiple compartments that can be labeled as you wish.

Ideal for people on the go, it eliminates the need for bulky pill boxes and plastic bags.

Expert Tip: Allocate distinct sections for different medications and times of the day to ensure regularity even when your travel schedule is unpredictable.

23. Universal Travel Adapter

This top-quality adapter is a jet-setter’s delight, ensuring you’re always powered up on your globe-trotting adventures.

A travel adapter is a useful device that allows travelers to use their electronic devices in countries where different plug standards are used. It provides a hassle-free way to keep electronic devices like laptops, phones, or cameras powered up, vital for staying connected and entertained during international travels.

With its functionality in over 150 countries and capacity to charge six devices simultaneously, it’s perfect for the tech-savvy traveler.

Remember, it’s not a voltage converter, so ensure your devices are dual-voltage. If not, pack an adapter that converts voltage.

24. TSA Approved Luggage Lock

Secure your luggage with the TSA Approved Luggage Lock, an absolute must-have for every savvy traveler.

With this lock, enjoy peace of mind on your journeys, assured your luggage is safe and no one has been through your stuff!

Featuring easy-to-read dials, an inspection indicator, and a durable zinc alloy design, it’s perfect for frequent flyers and security-conscious travelers.

Expert Tip – Always lock your suitcase when unattended to deter theft. And carry an extra in case yours is lost.

25. TSA Approved Travel Bottles

These TSA Approved Travel Bottles are magnificent game-changers for any frequent flier.

They’re precisely designed, with an easy dispensing mechanism, and leak-proof tops, plus conform to TSA size limits.

A supreme choice for savvy travelers, they’re reusable, eco-friendly, and wallet-friendly.

26. Luggage Cup Holder

The Luggage Cup Holder is about to be your new jet-setting best friend. (In fact, I’m buying this for my son for Christmas.)

This genius accessory deftly holds your coffee or water bottle, freeing you up to maneuver through busy airports effortlessly.

Even better, it features a handy pouch for storing essentials like ID’s or credit cards.

Juggle less and travel more, with this brilliant travel necessity!

27. Compression Socks

Long-haul flights call for compression socks! They increase blood flow while reducing swelling and the risk of blood clotting which may occur due to prolonged periods of sitting, such as during long flights.

Thankfully, they are way more stylish than the traditional hospital-issued white compression socks. This has caused their popularity to soar, providing pressure from the ankle upwards, making them essential for flights.

These socks provide graduated compression especially high at the ankles and reduce upwards towards the knee, facilitating increased blood flow.

Moreover, they are not only meant for those with medical conditions, but also beneficial for travelers, athletes, and those who stand for long hours at work. They enhance overall leg health by minimizing swelling, fatigue, and discomfort, thus improving the quality of your daily activities and sleep.

28. Cruise Luggage Tags

Get ready to sail in style and convenience with one indispensable travel essential – cruise luggage tags.

It’s that little gadget you never knew you needed until you’ve used one and seen its magic.

Here’s why: These tags make your bags unmistakable, reducing the risk of losing them amidst a sea of sameness. It’s a godsend for frequent cruisers as your company-issued tags won’t fall off.

Go for brightly-colored, durable tags. A simple trick, but could save you from a world of lost luggage stress.

29. Laundry soap sheets

One of the best ways to pack less is to run a quick load of luggage on your trip. So, these laundry soap sheets come in handy! We also pack two dryer balls as well.

Ready to pack for your next adventure? Don’t forget laundry soap sheets, a travel game-changer! –

They’re lightweight and occupy minimal space. This is great when packing a minimalist capsule wardrobe.

No time to find a laundromat? Then, use SinkSuds which can be used anywhere!

30. Security Cameras at Home

Securing your home with surveillance cameras while traveling is a crucial precaution.

The peace of mind offered by a vigilant “electronic eye” is incomparable. These cameras capture real-time footage, aiding in deterring burglaries and providing evidence if needed. Perfect for frequent travelers, it assures your abode’s safety from afar.

When we travel, we install one inside our house with an instant notification on our phones. As motion is detected, a siren noise goes off, which I’m sure would terrify any intruder!

Expert tip: Opt for cameras with remote-access features, so you’re always a glance away from your home.

What are the five most important items you need for these vacations?

Setting off for your much-anticipated vacation?

Here are the top five must-have travel essentials for an easy-going and memorable adventure.

Travel Planner and Journal: This bundle is essential for planning your trip and keeping track of your daily activities. The planner helps organize your itinerary, while the journal provides a wonderful means to record memories and experiences from your trip.

Multipurpose Clothing: Items like versatile shoes or pants that are ideal for multiple activities such as hiking and sightseeing are crucial to pack. Such items can save you space in your baggage, simplify your travel outfits, and cover a variety of travel occasions or activities.

All-in-One Travel Bag: A multipurpose bag, like a fanny pack or backpack, is an important versatile travel essential. This item keeps your essentials within easy reach, aids organization, and can adapt to a variety of travel situations.

Personal Care Essentials: Depending on your destination and planned activities, personal care items may include sunblock, moisturizer, or insect repellant. They ensure you are prepared for the environmental conditions you may face and can greatly enhance your overall comfort and well-being during your travels.

Travel Luggage: This trendy luggage piece thrills travelers with its durability and sleek design. Make sure your suitcases are lightweight!

Remember, a well-prepared traveler is a happy traveler. Aim for comfort, protection, and convenience!

Which Essentials for Travelling are your Next Purchase?

Ready to embark on your next adventure?

Don’t let unexpected situations curb your enthusiasm – it all starts with being prepared.

Remember, travel isn’t just about the destination but the journey, and the journey includes packing well!

With these travel essentials ideas, you can load up your bags with high-quality travel gear, ensuring comfort and stress-free experiences during your trip and beyond. Many of which are actually Amazon travel must haves.

Investing in essentials now will not just save you money down the line, but also help avoid irritating travel hitches.

Whether it’s tangle-free cords, smart luggage, or convenient packing tools – each item on our list has earned its spot by proving its worth on countless journeys for me.

So, next time you’re planning a trip, remember to refer back to this list. Good preparation equals to great journeys!

Know someone else that needs this, too? Then, please share!!

A bear market is defined as a broad market decline of 20% or more from recent highs, which lasts for at least two months. Although bear markets make for dramatic headlines, the truth is that bull markets tend to last much longer — the average bear market typically ends within a year.

While most investors know the difference between a bull and a bear market, it’s important to know some of the characteristics of bear markets in order to understand how different market conditions may impact your portfolio and your investment choices.

What Is a Bear Market?

Investors and market watchers generally define a bear market as a drop of 20% or more from market highs. So when investors refer to a bear market, it usually means that multiple broad market indexes, such as the Standard & Poors 500 Index (S&P 500), Dow Jones Industrial Average (DJIA), and others, fell by 20% or more over at least two months.

To be sure, 20% is a somewhat arbitrary barometer, but it’s a common enough standard throughout the financial world.

The term bear market can also be used to describe a specific security. For example, when a particular stock drops 20% in a short time, it can be said that the stock has entered a bear market.

Bear markets are usually associated with economic recessions, although this isn’t always the case. As economic activity slows, people lose jobs, consumer spending falls, and business earnings decline. As a result, many companies may see their share prices tumble or stagnate as investors pull back.

Why Is It Called a Bear Market?

There are a variety of explanations for why “bear” and “bull” have come to describe specific market conditions. Some say a market slump is like a bear going into hibernation, versus a bull market that keeps charging upward.

The origins of the term bear market may also have come from the so-called bearskin market in the 18th century or earlier. There was a proverb that said it is unwise to sell a bear’s skin before one has caught the bear. Over time the term bearskin, and then bear, became used to describe the selling of assets.

Characteristics of a Bear Market

There are two different types of bear markets:

• Regular bear market or cyclical bear market: The market declines and takes a few months to a year to recover.

• Secular bear market: This type of bear market lasts longer and is driven more by long-term market trends than short-term consumer sentiment. A cyclical bear market can happen within a secular bear market.

History of Bear Markets

The most recent U.S. bear market began in June 2022, largely sparked by rising interest rates and inflation. The bear market officially ended on June 8, 2023, lasting about 248 trading days, according to Dow Jones Market Data, and resulting in a market drop of about 25.4%.

Including the most recent bear market, the S&P 500 Index posted 12 declines of more than 20% since World War II. The table below shows the S&P 500’s returns from the highest point to the lowest point in a downturn. Bear markets average a decline of 34%, and generally last a little more than a year: about 400 days.

Recommended: What Is a Financial Crisis?

Bear markets have occurred as close together as two years and as far apart as nearly 12 years. A secular bear market refers to a longer period of lower-than-average returns; this could last 10 years or more. A secular bear market may include minor rallies, but these don’t take hold.

A cyclical bear market is more likely to last a few weeks to a few months and is more a function of market volatility.

Peak (Start)

Trough (End)

Return

Length (in days)

May 29, 1946

May 17, 1947

-28.78%

353

June 15, 1948

June 13, 1949

-20.57%

363

August 2, 1956

October 22, 1957

-21.63%

446

December 12, 1961

June 26, 1962

-27.97%

196

February 9, 1966

October 7, 1966

-22.18%

240

November 29, 1968

May 26, 1970

-36.06%

543

January 11, 1973

October 3, 1974

-48.20%

630

November 28, 1980

August 12, 1982

-27.11%

622

August 25, 1987

December 4, 1987

-33.51%

101

March 27, 2000

Sept. 21, 2001

-36.77%

545

Jan. 4, 2002

Oct. 9, 2002

-33.75%

278

October 9, 2007

Nov. 10, 2008

-51.93%

408

Jan. 6, 2009

March 9, 2009

-27.62%

62

February 19, 2020

March 23, 2020

-34%

33

June 2022

June 8, 2023

-25%

248

Average

-34%

401

Source: Seeking Alpha/Dow Jones Market Data as of June 8, 2023.

What Causes a Bear Market?

Usually bear markets are caused by a loss of consumer, investor, and business confidence. Various factors can contribute to the loss of consumer confidence, such as changes to interest rates, global events, falling housing prices, or changes in the economy.

When the market reaches a high, people may feel that certain assets are overvalued. In that instance, people are less likely to buy those assets and more likely to start selling them, which can make prices fall.

When other investors see that prices are falling, they may anticipate that the market has reached a peak and will start declining, so they may also sell off their assets to try and profit on them before the decline. In some cases panic can set in, leading to a mass sell-off and a stock market crash (but this is rare).

Is a Recession the Same as a Bear Market?

No. Bear market conditions can lead to recessions if the market slump lasts long enough. But this isn’t always the case. According to the National Bureau of Economic Research as reported in The New York Times, the U.S. has been in a recession only 14% of the time since World War II.

What Is a Bear Market Rally

Things can get tricky if there is a bear market rally. This happens when the market goes back up for a number of days or weeks, but the rise is only temporary. Investors may think that the market decline has ended and start buying, but it may in fact continue to decline after the rally. Sometimes the market does recover and go back into a bull market, but this is hard to predict.

If the bear market continues on long enough then it becomes a recession, which can go on for months or years. That said, it’s not always the case that a bear market means there will be a recession.

Once asset prices have decreased as much as they possibly can, consumer confidence begins to rise again, and people start buying. This reverses the bear market trend into a bull market, and the market starts to recover and grow again.

Example of a Bear Market

The most recent bear market occurred in June of 2022, when the S&P 500 closed 21.8% lower than its high on Jan. 3, 2022.

While the Nasdaq and the Dow showed a similar pattern in early 2022, the decline of those markets didn’t cross the 20% mark that signals official bear market territory.

Bear Market vs Bull Market

A bull market is essentially the opposite of a bear market. As consumer confidence increases, money goes into the markets and they go up.

A bull market is defined as a 20% rise from the low that the market hit in a bear market. However, the parameters of a bull market are not as clearly defined as they are for a bear market. Once the bottom of the bear market has been reached, people generally feel that a bull market has started.

Investing Tips During a Bear Market

There are a few different bear market investing strategies one can use to both prepare for a bear market and navigate through one.

1. Reduce Risky Investments

When preparing for a bear market, it’s a good idea to reduce riskier holdings such as growth stocks and speculative assets. One can move money into cash, gold, bonds, or other ‘safe’ investments to reduce the risk of losses if the market goes down.

These safe investments tend to perform better than stocks during a bear market. Types of stocks that tend to weather bear markets well include consumer staples and healthcare companies.

2. Diversify

Another investing strategy is diversification. Rather than having all of one’s money in stocks, distribute your investments across asset classes, e.g. precious metals, bonds, crypto, real estate, or other types of investments.

This way, if one type of asset goes down a lot, the others might not go down as much. Similarly, one asset may increase a lot in value, but it’s hard to predict which one, so diversifying increases the chances that one will be exposed to the upward trend, and you’ll see a gain.

3. Save Capital and Reduce Losses

During a bear market, a common strategy is to shift from growing capital into saving it and reducing losses. It may be tempting to try and pick where the market has hit the bottom and start buying growth assets again, but this is very hard to do. It’s safer to invest small amounts of money over time using a dollar-cost averaging strategy so that one’s investments all average out, rather than trying to predict market highs and lows.

4. Find Opportunities for Future Growth

However, in a broad sense if the market is at a high and assets are clearly overvalued, this may not be the best time to buy. And vice versa if assets are clearly undervalued it may be a good time to buy and grow one’s portfolio. A bear market can be a good time to identify assets that might grow in the next bull market and start investing in them.

5. Short Selling

A very risky strategy that some investors take is short selling in anticipation of a bear market. This involves borrowing shares and selling them, then hoping to buy them back at a lower price. It’s risky because there is no guarantee that the price of the shares will fall, and since the shares are borrowed, typically using a margin account, they may end up owing the broker money if their trade doesn’t work out as they hope.

Overall, it’s best to create a long-term investing strategy rather than focusing on short-term trends and making reactive decisions to market changes. It can be scary to watch one’s portfolio go down, especially if it happens fast, but selling off assets because the market is crashing generally doesn’t turn out well for investors.

The Takeaway

Bear markets can be scary times for investors, but even a prolonged drop of 20% or more isn’t likely to last more than a few months, according to historical data. In some cases, bear markets present opportunities to buy stocks at a discount (meaning, when prices are low), in the hope they might rise.

Also there are strategies you can use to reduce losses and prepare for the next bull market, including different types of asset allocation. The point is that whether the markets are considered bearish or bullish, any time can be a good time to invest.

If you’re looking to build a portfolio, no matter what the market, it’s easy when you set up an Active Invest account with SoFi Invest. The secure investing app lets you research, track, buy and sell stocks, ETFs, crypto, and other assets right from your phone or computer. You can easily move between different types of assets and you can set automated recurring investments if you want to put in a certain dollar amount each week or month. All you need is a few dollars to get started.

Start building a portfolio today.

FAQ

How long do bear markets last?

Bear markets may last a few months to a year or more, but most bear markets end within a year’s time. If they go on longer than that they typically become recessions. And while a bear market can end in a few months, it can take longer for the market to regain lost ground.

When was the last bear market?

The most recent bear market started in June of 2022, when the S&P 500 fell from record highs in January for more than two months.

Photo credit: iStock/Morsa Images

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

The other day, a friend and I went down to Indymac to close out his savings account, as the massive bank run line had now substantially subsided.

When we arrived, we were greeted by a man in a vest with a clipboard who asked if we were there to make a withdrawal.

Once my friend explained that he was indeed there to withdraw his savings, he was put on a short waiting list and told to sit in a specific area within the bank.

I suppose they wanted to create some semblance of calm that all was well at the failed bank and mortgage lender, despite the panic that had ensued in earlier days.

After withdrawing the cash, we walked about 20 feet and came across First Bank, which had the sign you see above in front of their building, luring ex-customers to quickly redeposit their newly homeless funds.

This seemed to be quite a reversal to what we had been hearing days earlier, that banks such as Washington Mutual and Wells Fargo were placing holds on checks or perhaps not even honoring them.

While this likely created a second wave of panic, supposedly these banks have been placing longer holds on Indymac checks as a measure designed to catch fraudulent activity.

Obviously there will be some winners and losers that emerge from this unprecedented mortgage crisis.

What should you do if your mortgage company didn’t pay your property taxes? First, don’t panic, but do take immediate action. Start by contacting your lender, tax authority, and even your lawyer if necessary.

Getting an unpaid tax notice in the mail can be scary, especially when you know you have an escrow account and your mortgage payments are up to date. The important thing is to remain calm. Then, take the necessary steps to resolve the issue.

This article provides more information about how escrow accounts work and what steps you should take if you receive a tax notice in the mail.

In This Piece

How Do Escrow Accounts Work?

Many lenders today require homebuyers to set up escrow accounts prior to closing. The lender uses this escrow account to store money to cover fees above and beyond your mortgage payments, such as property taxes, homeowners’ insurance, and HOA fees. You pay these extra fees right along with your mortgage payments each month. Your lender takes its share of your payment and then puts the rest into this escrow account.

Bills for your property taxes, insurance, and HOA fees should go directly to your lender, who then pays these fees right from your escrow account. In turn, you should receive a notice on your mortgage statements when each of these bills is paid. If you received a tax notice in the mail, something went wrong with this process. It’s critical to take immediate steps to resolve this issue.

It’s also important to understand this connection between your property taxes and your mortgage payment. In fact, knowing how an escrow account works can help you better compare mortgage rates when searching for a home and determining exactly how much you can afford to pay each month.

Get matched with a personal

loan that’s right for you today.

Learn

more

What If You Learn Your Mortgage Servicer Didn’t Pay Your Taxes?

There are several reasons your mortgage servicer might not have paid your taxes, such as:

Clerical error. It’s not unheard of for local and state tax authorities, and even loan servicing companies, to make clerical errors that result in unpaid property taxes. For example, maybe the local tax authority sent the bill to your address instead of to the mortgage servicer.

Change in loan servicing company. Another common reason for unpaid property taxes is a change in loan servicing companies. It’s possible your lender sold your loan or changed mortgage servicers. In this case, your tax bill may have been sent to the old company rather than the new one.

Late mortgage payments. If you’re behind on your mortgage payments by more than 30 days, the lender isn’t required to pay your property taxes. However, if there’s still money in your escrow account, most lenders will make these payments.

If you find out your mortgage servicer didn’t pay your taxes, don’t assume anything. Instead, it’s crucial that you act fast. The first step is to contact all related parties.

Contact Your Lender

The first person you want to contact is your lender. Explain the situation and ask it to check on your escrow account immediately. In fact, you can request a copy of your escrow account activity at any time. In most cases, the lender will walk you through what steps you must take to resolve the issue.

However, if you’re not satisfied with the results of this call, you can file a dispute by sending a letter to your lender. In this letter, provide your name, contact information, account details, and a description of the error along with copies of your tax notice. Don’t send this letter with your standard mortgage payment. Instead, send it in a separate letter directly to your mortgage servicer.

Keep in mind that your lender is required by law to pay these fees out of your escrow account prior to the due date. Clerical errors do occur sometimes, so give your lender time to fix the error. Once you send a dispute letter, it only has 30 days to reply. However, it can state in writing that it needs an additional 15 days to investigate the issue.

Contact Your Tax Authority

You also want to contact your tax authority to discuss the issue. Even if you worked things out with the lender, you still want to update the tax authority on the status of your tax payments.

However, if your lender states that it didn’t receive your tax bill, you need to make sure the tax authority has the correct records. Start by explaining to the agency that your taxes are in escrow and your lender makes the payments. Then, have it check its records to make sure it has the right mortgage servicer listed.

If your lender states that it paid your taxes, ask the tax authority to recheck its records. If the agency’s records still show unpaid tax records, provide it with payment information from your lender and ask it to recheck. You may have to call your lender back if the agency is unable to find the payment.

Contact an Attorney

If after sending a letter to your mortgage servicer or providing the tax authority with the necessary documentation you still haven’t resolved the issue, it may be time to seek legal assistance. Contacting a lawyer can help you learn more about your legal rights pertaining to escrow accounts. It’s likely your attorney can resolve the issue quickly or guide you through the next steps.

Stay on Top of Your Mortgage Payments

Unpaid taxes could result in a lien against your property, which can be difficult to remove. Unpaid taxes don’t directly impact your credit score. However, if you have to use your credit card or take out a personal loan to cover these costs, your credit score could drop.

The most important step is to follow through and make sure your taxes were paid in full. Ask for a full report of your escrow account where it shows payment. You also want to double-check with the tax authority to make sure your tax bill was paid.

If you’re in the market for a new home or considering refinancing your current home, you want to make sure your credit score is in good standing before applying for a new loan. Try Credit.com’s ExtraCredit program to build, guard, track, reward, and restore your credit. Sign up for ExtraCredit today.

According to IBM’s annual Cost of a Data Breach report, the average cost of a data breach to an organization in 2021 was 4.24 million dollars. That’s the highest average figure in its 17-year history. Most of these breaches were the result of compromised user credentials (where an attacker is able to gain unauthorized access to an account) and are often more costly where remote working is involved.

cyber attack

These breaches aren’t just costly for large enterprises, though. Many small organizations fail to recover from a serious data breach (where the average cost is just under $700,000), with 60% of them going out of business within 6 months of an attack.

But of course, we can also fall victim to cyber attacks as individuals, and the cost to us can be significant, too. If you’ve been unlucky enough to have been a victim of a data breach, or (worse), identity theft, you’ll know that you can lose eye-watering and potentially crippling sums: this hacking victim lost over $13k in 2020.

But when we talk about the cost of a cyber attack to an individual, we’re not talking simply about financial losses.

How to Avoid a Cyber Attack

Psychologically, the after-effects of a cyber attack can be damaging. The feeling that you’ve been manipulated by a stranger (and your personal data has been ‘invaded’) can be deeply unsettling. It can lead to a serious loss of confidence, and make you increasingly wary of trusting others. It can cause embarrassment, too, as a victim of a hack can be made to feel as if it’s their fault.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

In the most extreme cases (where a cyber attack has led to a significant loss of funds or even the loss of a job) the effect can be even more harmful, leading to stress, anxiety and even depression. Whatever the financial cost of an attack, the emotional cost is often far more significant in the long run.

Fortunately, there are a number of steps you can take to secure your data and ensure you’re aware of the threats you might face while online.

Check If Your data Is at Risk

Without knowing it, your data might have already been involved in a breach. A breach usually occurs when a hacker gains access to the database of a service or company which contains users’ private information, including (but not limited to) usernames, passwords, email addresses and, in the worst cases, bank account details. If you’ve been involved in a data breach, some of your personal information might have been made public without you realizing, which could put you at risk of identity theft.

But don’t panic. You can check if your email address or phone number has been exposed in a data breach by going to Have I Been Pwned. If any of your accounts may have been compromised, change those passwords immediately, and make sure you’re not reusing the same passwords across multiple accounts.

Use Strong Passwords

Speaking of passwords, nearly a quarter of Americans have admitted to using a password like “password” or “123456”. These should clearly be avoided, as they’re easily guessable and won’t take long for a hacker to crack. The longer and more complex a password is, the stronger it is. You can check the strength of your passwords at Security.org.

Using a “passphrase” (a series of unrelated words with spaces in between) is often more effective than using a simple combination of letters and numbers, as these can be harder to crack. This can help to protect your accounts from threats like brute-force attacks, in which attackers will submit vast numbers of possible passwords in an effort to guess correctly.

Protect Your Website(s)

This action may not apply to you, of course — but if you happen to run a website (for a small business, perhaps, or even just a hobby such as blogging) then your personal information is inextricably linked to it, and it can be a huge point of vulnerability. If someone gains access to it through a CMS exploit or a comparable weakness, they can learn your passwords, uncover private information, or even hold the site hostage in an effort to extort you.

Keeping extortion efforts at bay is largely a matter of investing in technical safeguards. Top managed hosting platforms are particularly good at keeping ahead of potential attackers, and some (e.g. Cloudways with its 2022-launched Cloudflare CDN integration) are investing in native features that make it all but impossible for run-of-the-mill hackers to gain access. Overall, though, the biggest thing you can do is refrain from storing any sensitive information on your website. Anything intended for public viewing inevitably makes a bad storage vault.

Beware of Suspicious Emails

One of the most common ways individuals fall victim to cyber crime is through phishing attacks, a type of ‘social engineering’ where an attacker sends a fraudulent email to an intended victim enticing them to click a suspicious link or hand over personal information. Phishing emails often appear as though they’re from a legitimate organization (like your bank, for example) but there are some classic signs to look out for.

Check the email domain (the bit after the @ symbol) to see if it looks legitimate. If it’s misspelled (or a public domain like gmail.com) it could be a scam. Next, check for poor spelling and grammar in the body of the email, as phishing attempts are often shoddily written. If you have the slightest suspicion that the email may not be legitimate, do not respond or click any links in the email. To ensure you’re aware of the telltale signs, IT Governance has produced a handy guide on the ways to detect a phishing email.

Update Your Software

Cyber threats are constantly evolving, with hackers developing newer, more sophisticated ways to gain access to our devices and our personal data. That’s why it’s so important that our operating systems and software programs are always updated to the latest available versions. These newer versions will fix previously discovered vulnerabilities and offer greater protection against emerging threats.

If you’re still using an outdated operating system, for example, it may contain weaknesses that can quite easily be exposed by an attacker, especially if those weaknesses are public knowledge. Use a tool like Soft4Boost to check for out-of-date and potentially vulnerable software, and update to the latest supported versions where necessary.

Secure Your Devices

It’s also important to protect our physical devices, as a lost or stolen device could present an easy opportunity for an attacker to gain access to your personal data. Ensure a password or PIN is always required to access the device (and don’t use anything easily guessable like 0000 or 1234). Many devices now enable facial recognition or fingerprint access, so enable these functions where possible. When you’re not using your device, make sure it’s locked.

Backing up your data is essential, too, so that it can be recovered in the event of a data breach. Most computers will include a backup facility, while mobile phone data can usually be backed up using cloud storage. Finally, beware of unsecured public Wi-Fi networks (where no password is required for access) as these are often prime targets for an attacker, and disable your Bluetooth function when you’re not using it.

A limit order allows investors to buy or sell securities at a price they specify or better, providing some price protection on trades.

When you set a buy limit order, for example, the trade will only be executed at that price or lower. For sell limit orders, the order will be executed at the price you set or higher. By using certain types of orders, traders can potentially reduce their risk of losses and avoid unpredictable swings in the market.

Table of Contents

How do Limit Orders Work?

In the simplest terms, limit orders work as a sort of restriction that an investor can choose (to either buy or sell) with “limits” on a minimum or maximum price. An investor places an order to buy a stock at a minimum price, for instance, or places an order to sell at a maximum price, in an effort to maximize their returns.

There are two types of limit orders investors can execute: buy limit orders and limit sell orders. An important thing to know is that while a limit order specifies a desired price, it doesn’t guarantee the trade will occur at that price — or at all.

When you set a limit order, the trade will only be executed if and when the security meets the terms of the order — which may or may not happen, depending on the overall market conditions. So, when an investor sets a limit order, it’s possible to miss out on other investing opportunities.

Types of Limit Orders

As mentioned, there are two types of limit orders investors can execute: buy limit orders and limit sell orders.

For buy limit orders, you’re essentially setting a ceiling for the trade — i.e. the highest price you’d be willing to pay for each share. For sell limit orders, you’re setting a price floor — i.e. the lowest amount you’d be willing to accept per share.

• What is limit order to buy? If a trader places a buy limit order, the intention is to buy shares of stock. The order will be triggered when the stock hits the limit price or lower.

For example, you may want to buy shares of XYZ stock at $15 each. You could place a buy limit order that would allow the trade to be carried out automatically if the stock reaches that purchase price or better.

• What is limit order to sell? If a trader places a limit order to sell, the order will be triggered when the stock hits the limit price or higher. So you could set a sell limit order to sell XYZ stock once its share price hits $20 or higher.

As noted above, the main upside of using limit orders is that traders get to name a desired price; they generally end up paying a price they expect; and they can set an order to execute a trade that can be executed even if they are doing other things.

In this way, setting limit orders can help traders seize opportunities they might otherwise miss because limit orders can stay open for months or in some cases indefinitely (the industry term is “good ‘til canceled,’ or GTC). The limit order will still execute the trade once the terms are met.

Limit Order vs Market Order

Limit orders differ from market orders, which are, essentially, orders to buy a security immediately at its given price. These are the most common types of orders. So, while a market order is executed immediately regardless of terms, limit orders only execute under certain circumstances.

Limit orders can also be set for pre-market and after-hours trading sessions. Market orders, by contrast, are limited to standard trading hours (9:30am to 4pm ET).

Remember: Even though limit orders are geared to a specific price, that price isn’t guaranteed. First, limit orders are generally executed on a first-come-first-served basis. So there may be orders ahead of yours that eliminate the availability of shares at your limit price.

And it bears repeating again: There is also the potential for missed opportunities: The limit order you set could trigger a trade. But then the stock or other security might hit an even better price.

In other words, time is a factor. In today’s market, computer algorithms execute the majority of stock market trades. In this high-tech trading environment, it can be hard as an individual trader to know when to buy and sell. By using certain types of orders, like limit orders, traders can potentially limit their losses, lock in gains, and avoid swings in the market.

Though limit orders are commonly used as a part of day trading strategies, they can be useful for any investor who wants some price protection around their trades. For example, if you think a stock is currently undervalued, you could purchase it at the current market price, then set a sell limit order to automatically sell it when the price goes up. Again, the limit order can stay open until the security meets your desired price — or you cancel the order.

However, speculating in the market can be risky and having experience can be helpful when deciding how and when to set limit orders. 💡 Quick Tip: Did you know that opening a brokerage account typically doesn’t come with any setup costs? Often, the only requirement to open a brokerage account — aside from providing personal details — is making an initial deposit.

Limit Orders vs Stop Orders

There is another type of order that can come into play when you’re trying to control the price of a trade: a stop order. A stop order is similar to a limit order in that you set your desired price for a stock, say, and once the stock hits that price or goes past it, a market order is triggered to execute the purchase or sale.

The terms of a limit order are different in that a trade will be executed if the stock hits the specified price or better. So if you want to sell XYZ stock for $50 a share, a sell limit order will be triggered once the stock hits $50 or higher.

A stop order triggers a market order once XYZ stock hits $50, period. By the time the order is executed, the actual stock price could be higher or lower.

Thus with a stop order there’s also no guarantee that you’ll get the specified price. A market order is submitted once the stop price is hit, but in fast-moving markets the actual price you pay might end up being higher or lower.

Stop orders are generally used to exit a position and to minimize losses, whereas limit orders are used to capture gains. But two can also be used in conjunction with each other with something called a stop-limit order.

Stop-Limit Orders

A stop-limit order is a combination of a stop order and a limit order. Stop-limit orders involve setting two prices. For example: A stock is currently priced at $30 and a trader believes it’s going to go up in value, so they set a buy stop order of $33.

When the stock hits $33, a market order to buy will be triggered. But with a stop-limit order, the trader can also set a limit price, meaning the highest price they’re willing to pay per share — say, $35 per share. Using a stop-limit order gives traders an additional level of control.

Stop-limit orders can also help traders make sure they sell stocks before they go down significantly in value. Let’s say a trader purchased stock XYZ at $40 per share, and now anticipates the price will drop. The trader doesn’t want to lose more than $5 per share, so they set a stop order for $35.

If the stock hits $35 — the stop price — the stock will be triggered to sell. However, the price could continue to drop before the trade is fully executed. To prevent selling at a much lower price than $35, the trader can set a limit order to only sell between $32 and $35.

When a Trader Might Use a Limit Order

There are several reasons why you might want to use a limit order.

• Price protection. When a stock is experiencing volatility, you may not want to risk placing a market order and getting a bad price. Although it’s unlikely that the price will change drastically within a few seconds or minutes after placing an order, it can happen, and setting a limit order can set a floor or a ceiling for the price you want.

• Convenience. Another occasion to use a limit order might be when you’re interested in buying or selling a stock but you don’t want to keep a constant eye on the price. By setting a limit order, you can walk away and wait for it to be executed. This might also be a good choice for longer-term positions, since in some cases traders can place a limit order with no expiration date.

• Volatility. Third, an investor may choose to set a limit order if they are buying or selling at the end of the market day or after the stock market has closed. Company or world news could be announced while the market is closed, which could affect the stock’s price when the market reopens. If the investor isn’t able to cancel a market order while the market is still closed, they may not be happy with the results of the trade. A limit order can help prevent that.

Limit orders can also be useful when the stock being traded doesn’t have a lot of liquidity. If there aren’t many people trading the stock, one order could affect the price. When entering a market order, that trade could cause the price to go up or down significantly, and a trader could end up with a different price than intended.

Get up to $1,000 in stock when you fund a new Active Invest account.**