Moving is part of most people’s lives. Maybe you’re heading to grad school a couple of towns away. Or perhaps you have a job offer hundreds of miles away that you’re excited to accept.

Whatever the reason, the logistics of getting your stuff from the old place to the new one will need wrangling. Here, you’ll learn more about your options for moving, how much it may cost (from a couple of hundred dollars to thousands), and how to afford the expense.

DIY Moving Costs

Yes, you could move yourself. This could be a smart move for a small, local move, and it can help keep costs within your budget.

Exactly how much this might cost will be based on several factors:

• Cost of transportation (can you borrow a friend’s van or do you need to rent one)?

• Cost of the packing materials you use (recycled boxes and old newspapers vs. the pros’ higher-end and job-specific supplies

• How much stuff you’re moving (and if you need to figure out insurance for any pricey items)

• How far you’re going

• Whether you need to store some things temporarily.

As you might guess, packing up the contents of a dorm room and moving it half a mile away to the apartment you’re renting with friends will cost one amount. Supplies might cost, say, $65.

Loading up the contents of the sweet bungalow you’ve been living in for a couple of years and depositing your worldly possessions at a new place 1,000 miles away will be a much more involved and expensive undertaking. Packing materials alone could be a few or several hundred dollars, and renting a moving truck could be anywhere from $20 to $100 per day, depending on your local cost of living. Also, you will likely have to pay to stay somewhere overnight and also spend at least a couple of hundred dollars on gas, dollies, and insurance. 💡 Quick Tip: Some personal loan lenders can release your funds as quickly as the same day your loan is approved.

Full Service Moving Costs

If you decide a full-service move best meets your needs, you’re probably going to want to gather some estimates, so you can nail down the details and be ready when it’s time to go. Some pointers as you do so:

• Also, do check ratings and references carefully. There are plenty of instances of fraud and scams in this realm, and it’s wise to protect yourself.

• Booking your truck four to eight weeks in advance is typically a good rule of thumb — maybe even further out if you’re moving in the busy summer months.

• Professional moving companies can give you an estimate based largely on how many rooms of furniture you have. Most have websites, so you can often get a quick estimate online. A typical local (or fairly local, not long-haul) move for a three-bedroom home is about $2,100.

The average moving costs if you relocate cross-country can easily be twice that, or $4,300 for a distance of about 1,225 miles. Keep in mind, specifics will vary. Oversized or extremely heavy items might cost you extra — as could lots of stairs, or things that need to be taken apart and put back together.

Recommended: Average Personal Loan Rates

Extra Moving Costs to Think About

Then there are the extras that go along with getting out of one place and into another.

• Transportation: If you’re taking your car across the country, you’ll probably want to get a tune-up before you go. And then there’s gas, hotel stays, and eating on the road. Having a car transported instead of driving it yourself could cost anywhere from $700 to $2,000.

If you’re in a hurry and decide to fly, that’s another expense. And if you’re taking a pet, you may have to add a little bit more to your overall bill, depending on the mode of transportation you choose for your furry friend.

• Getting into your new home: Don’t forget about deposits you might have to make at your new location. That could be anything from first and last month’s rent and a pet deposit at a new apartment, to utility deposits at a new house.

• Home repairs and cleaning: Be ready to pay for some home repairs on both ends of your move. You may have to make some quick fixes to get out of your rental without losing the deposit or maybe even major repairs if you’re selling a home. When you get to your new location, you could find some unexpected problems. Or you may just want to hire someone to come in and clean so you can cross that off your ever-growing moving to-do list.

• Starting out fresh: You’ll probably need to buy some things at your new home (like curtains, curtain rods, hangers, bedding, etc.) that are easily overlooked. Then there’s that fridge to fill. All those little costs can add up.

• Cash for tips: You will likely need to withdraw money from an ATM to thank people for their help when you move. Tips for the movers. Tips for the handyman or housekeeper who helps you get things in shape. Tips at your hotel. Tips for waitstaff at the restaurants you’ll be eating at until you get your new place up and running—or at the very least, tips for the pizza delivery guy.

Recommended: Typical Personal Loan Requirements Needed for Approval

Financing Your Move

If you have enough room on multiple credit cards, you could go that route, but should you? Interest rates can be considerable.

Or would a personal loan make more sense for you to cover all those costs, big and small?

Remember, even if you’ll be reimbursed by your employer or plan to take some moving deductions when you file your tax return, it’s very likely you’ll be paying at least some moving costs up front. And the longer those expenses sit on a credit card, the more interest racks up.

The Takeaway

Even if you have a small amount of stuff and aren’t moving very far, moving takes time, energy, organization, and money. With the average professional move costing a couple of thousand dollars, you may want to plan carefully for this expense. It’s likely not a good reason to dip into your emergency fund, so you may want to save in advance or consider a personal loan. If you qualify for a personal loan, your interest rate may be lower than a credit card, which can free up some cash and reduce your money stress.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

If you own a home, you probably always have a list of improvements you’re considering. Maybe you desperately want to replace those dated kitchen appliances that scream year 2000, or you want to focus on ways to lower your energy bills, whether that means some strategic air sealing or adding solar panels.

Chances are, you also want any upgrades you pay for to increase the value of your home. You want to know that if and when it comes time to sell your place, you’ll recoup a good percentage of what you invested.

So, whether you have the cash saved up for home investment or you are looking to borrow for your next home project, consider these wise investments.

1. Improve Your Attic Insulation

We get it: You’re not going to invite friends over to see your new attic insulation.But it’s one of the best ways to increase your home’s energy efficiency.

You’ll not only profit when it’s time to sell, but you’ll also see immediate savings from the ongoing energy efficiency this upgrade provides. A properly insulated attic, combined with sealing air leaks throughout your home, cuts an average of 15% off your heating and cooling costs, allowing you to pocket the savings month after month. And who doesn’t want a lower energy bill?

Cost: $600 to $1,200 for blown-in insulation for a 1,000-square-foot attic. You may also need to rent the machine that blows in the fiberglass if you’re a DIY type. If you hire a pro, labor will run about $40 to $70 an hour. 💡 Quick Tip: Before choosing a personal loan, ask about the lender’s fees: origination, prepayment, late fees, etc. SoFi personal loans come with no-fee options, and no surprises.

2. Treat Yourself to New Windows

New windows can do double duty. Not only do they update a room’s tired appearance, they can also have energy-efficiency benefits. Depending on how many windows you replace, this can be a very big-ticket item. The average cost for a vinyl window replacement is $850, and a whole-home job can ring in at $20,091, according to Remodeling magazine. (Wood windows are pricier still.)

But here’s some good news: Replacing those windows adds value to your home. Typically, to the tune of 69% of the cost of the window-replacement project.

Cost: Anywhere from $850 per vinyl window to $20,000+ for the whole house. Again, if you go for wood vs. vinyl windows or need custom size ones (or several French doors), the price can ratchet up significantly. In that case, you might want to look at home improvement loan options.

3. Build a Deck

You and likely anyone who might buy your home in the future will love what a deck can do, lifestyle-wise. Weather permitting, you can have your AM coffee there, type away on your laptop during the day, and host friends, read, or just listen to the birdsong during off-hours. Here’s another nice thing about adding a deck: Your ROI is typically around 68% of the money you pay.

Cost: A new wood deck will cost on average $16,766. A composite one can cost more; on average, these are $22,426.

Read Next: How to Create a Renovation Plan to Match Your Budget

4. Refresh Your Bathroom

Who doesn’t love a beautiful new bathroom, whether your style is sleek and all white or if you prefer a warmer country cottage vibe? A bath remodel will cost, on average, between $6,627 and $17,494, according to Angi, the home renovation site. While an updated bath can definitely add to your home’s value, keep in mind that the sky’s the limit with the price tag. If you move the fixtures around and add one of those egg-shaped soaking tubs or a spa shower that has half-a-dozen mist settings, you may go well beyond the average range of costs.

Also, keep in mind that if you do something really singular (say, you pick tile in a super-bright shade), it may be harder to get your money out if and when you sell your property.

Cost: The average cost is $11,944, with cabinets and shelving accounting for 25% of the total, the shower and tub eating up 22% of costs, and your contractor’s fees usually being about 13% of your total expense. Of course, you can do a small bathroom remodel, perhaps repainting, adding some new artwork and a fresh shower curtain. 💡 Quick Tip: Home improvement loans typically offer lower interest rates than credit cards. Consider a loan to fund your next renovation.

5. Cook up a Cooler Kitchen

If you’re stuck with outdated appliances or hideous cabinets, a kitchen remodel is likely high on your list of improvements. It’s a great way to refresh your kitchen’s style and function.

But increasing home value with a new kitchen can fry your bank account: A remodel typically runs $14,612 and $41,392 according to Angi, but can cost much more if you move appliances’ position, opt for marble countertops, or fall in love with custom cabinetry. On average, you’ll recoup about 60% in ROI.

To update for less and wow your kitchen in a weekend, make some wallet-friendly upgrades: fresh paint, a new faucet, updated lighting (pendant lights are a good choice), and new cabinet pulls.

Cost: While you could just swap out cabinet pulls, which start at about $2 each, and repaint (plan on around $200), a larger kitchen remodel averages $26,849. Again, however, it’s worth noting you could spend multiples of that, depending on how large a project, how luxe the details, and where you live (cost of living can impact the price of goods and services in your area).

Recommended: Secured vs. Unsecured Personal Loans

The Easy Way to Finance HGTV-Worthy Upgrades

Even budget-friendly home improvements can set you back quite a bit. If you haven’t set aside the budget to bring more value to your home, you don’t necessarily have to dip into your retirement account or pay less on your student loans each month. You might want to consider a personal loan.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Federal Reserve left its key short-term interest rate unchanged again Wednesday, hinted that rate hikes are likely over and forecast three cuts next year amid falling inflation and a cooling economy.

That’s more rate cuts than many economists expected.

The decision leaves the Fed’s benchmark short-term rate at a 22-year high of 5.25% to 5.5% following a flurry of rate increases aimed at subduing the nation’s sharpest inflation spike in four decades. The central bank has now held its key rate steady for three straight meetings since July.

That provides another reprieve for consumers who have faced higher borrowing costs for credit cards, adjustable-rate mortgages and other loans as a result of the Fed’s moves. Yet Americans, especially seniors, are finally reaping healthy bank savings yields after years of paltry returns.

Best high-yield savings accounts of 2023

401(k) boon:Stocks surge, Dow Jones hits all-time high at close after Fed forecasts lower rates

Leaving savings behind:Many Americans are missing out on high-interest savings accounts. Don’t be one of them

Is a soft landing in sight? What the Fed funds rate and mortgage rates are hinting at

Will the Fed raise interest rates again?

The central bank didn’t rule out another rate increase as it downgraded its economic outlook for next year while lowering its inflation forecast. In a statement after a two-day meeting, it repeated that it would assess the economy and financial developments, among other factors, to determine “the extent of any additional (rate hikes) that may be appropriate to return inflation to 2% over time.”

Fed Chair Jerome Powell said at a news conference, noting the Fed’s key rate is “at or near its peak.”

while the Dow Jones Industrial Average closed at a record high after rising 1.4% following the Fed’s signals that it’s probably done lifting rates and is forecasting three cuts next year. The 10-year Treasury was down to about 4% from 4.21% on Tuesday.

Last month, Powell said high Treasury yields, if persistent, likely would constrain the economy and require fewer Fed rate increases,

In its statement Wednesday, however, the central bank didn’t acknowledge the recent decline in Treasury yields, suggesting yields are still relatively high and could spike again, crimping the economy.

“Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring and inflation,” the Fed said, repeating the language of its previous statement.

Is inflation really slowing down?

The Fed’s middle-ground approach may have been cemented Tuesday by a mixed report on the consumer price index. The good news was that overall inflation barely budged in November amid falling gasoline prices, pushing down annual price gains to 3.1% from 3.2%, still well above the Fed’s 2% goal.

The Federal Reserve System is the U.S.’s central bank.

When does the Fed meet again?

The first Federal Reserve meeting of the new year will be from Jan. 30 through 31.

Federal reserve calendar

Jan. 30-31

March 19-20

April 30- May 1

June 11-12

July 30-31

Sept. 17-18

Nov. 6-7

Dec. 17-18

The U.S. economy was strong in the third quarter as consumers continued to spend despite high interest rates and inflation.

The value of all services and products generated in the U.S., or GDP, rose at a seasonally adjusted 4.9% for the year in the months spanning July to September, according to the Commerce Department. That was more than twice the 2.1% increase in the previous quarter and the most aggressive pace of growth since the end of 2021 when the economy surged back from a recession sparked by the pandemic.

a recession over the next year, down from the 61% odds forecast in May.

Barclays predicted a loss of roughly 375,000 jobs by the middle of next year. But consumer spending remains robust despite high inflation and interest rates that are making credit card use and consumer loans more expensive. And that may help stave off a recession, says Barclays economist Jonathan Millar.

What does FOMC stand for?

The FOMC is the Federal Open Market Committee, the voting body responsible for setting interest rates. The 12-member committee includes seven members of the Board of Governors and five of the 12 Reserve Bank presidents.

What causes inflation?

Inflation can have many roots. Typically, it’s caused by “a macroeconomic excess of spending over the economy’s relative ability to produce goods and services,” said Josh Bivens, the director of research at the Economic Policy Institute, a left-leaning think tank based in Washington D.C.

That means more people are wanting items and services than there is adequate supply, leading producers to raise prices.

“If everyone in the economy, tomorrow, decided they weren’t going to save any money from their paychecks, and they’re just going to spend every last dollar out of the blue, they would all run to the stores and try to buy things,” Bivens said. “But, producers haven’t produced enough to accommodate that big surge of across-the-board spending. So, you would see prices bid up.”

Inflation can also happen when there are too few producers, or there aren’t enough employees to provide the coveted products and services, Bivens said.

Finally, economies also have some “built-in inflation” to help keep inflation in check. In the U.S., that target is 2%, meaning businesses can raise prices 2% annually year and that shouldn’t overburden consumers. That’s also the typical cost of living raise offered by employers.

Inflation meaning

Inflation is the term for a “generalized rise in prices,” according to Josh Bivens, head of research at the Economic Policy Institute, a left-leaning think tank based in Washington D.C.

Everything from food to rent can become costlier due to inflation. But it is the overall impact that determines what the inflation rate actually is.

“Inflation, though, really is meant to only refer to all goods and services, together, rising in price by some common amount,” Bivens said. The Federal Reserve’s inflation goal is 2%, which means businesses can hike prices by 2% a year and that shouldn’t cause consumers financial distress. Cost of living increases to workers’ pay are also expected to meet that target to ensure consumers can adequately deal with the rising costs of goods and services.

What is CPI?

In November, the Consumer Price Index (CPI) ‒ a measure of the average shift in prices for different products and services ‒ was 3.1%, down slightly from the month before.

Annual inflation is down dramatically from the 9.1% in June 2022 that marked a 40-year high but remains above the 2% target the Fed sees as the level that signals the rate of price increases is under control.

Why is CPI important?

The Federal Reserve watches two key aspects of the economy, price stability and maximum employment, and those are the main factors it takes into account for its interest rate decisions. The CPI is a primary measure the Fed looks at to help determine if prices are “stable.’’

What is the difference between CPI and core CPI?

Core prices don’t count the volatile costs of food and energy items, giving a more accurate window into longer-term trends.

Are wages going up in 2024?

If you’re deemed a top performer at a company that is offering raises, you’ve got a pretty good chance of getting a pay boost next year.

About 3 out of four business leaders told ResumeBuilder.com they intended to give raises. But half of those company executives said only 50% or less of their staff members would see a pay hike, and 82% of the raises would hinge on performance. For those who do manage to get the salary boost, 79% of employers said the pay hikes would be greater than those given in recent years.

Are U.S. Treasury yields rising?

Not recently.

The 10-year Treasury yield was above 5% in November when the Fed kept rates steady for the second consecutive month the first time it had left the key rate unchanged two months in a row in almost two years.

That led to mortgage rates spiking to almost 8% and pushed up other borrowing costs for consumers and businesses. Stocks meanwhile sank close to a recent low, leading Fed Chair Jerome Powell to say such financial pressures could achieve the same cooling effect on the economy as additional rate hikes.

But in the following weeks, 10-year Treasury yields dipped to 4.2% and stocks rebounded. That might make the Fed resist rate cuts in case the economy heats up and causes the broader dip in prices “to stall at an uncomfortably elevated level,” Barclays says.

Barclays and Goldman Sachs forecast that rate cuts won’t happen until the spring, and that there will be only two, to a range of 4.75% to 5%, with more cuts implemented in the next two years.

When will inflation go back to normal?

It may take a little while.

Inflation’s decline likely “won’t show much progress in coming months,” Barclays wrote in a research note.

Overall price hikes have eased significantly since peaking at 9.1% in June 2022, a four-decade high. And in October, broader inflation as well as core prices experienced a dip, leading to a lower 10-year Treasury yield.

But core prices, which exclude the volatile costs of food and energy, will probably rise 0.3% each of the next three months, Goldman Sachs says. Used cars and furniture have been getting cheaper as the supply-chain shortages of the pandemic end. Meanwhile, health care, auto repairs, car insurance and rent continue to get more expensive, as employers pay higher wages to attract workers amid a labor shortage lingering from the global health crisis.

What is core inflation right now?

Core prices, which leave out the more volatile costs of food and energy, bumped up 0.3% in November, slightly more than the 0.2% uptick seen the previous month. That kept the yearly increase at 4%, the lowest rate since September 2021.

New inflation tax brackets

Inflation may also impact the amount of taxes you have to pay.

The Internal Revenue Service said in its annual inflation adjustments report that there will be a 5.4% bump in income thresholds to reach each new level in next year’s tax season.

In 2024, the lowest rate of 10% will apply to individuals with taxable income up to $11,600 and joint filers up to $23,200. The top rate of 37% will apply to individuals earning over $609,350, and married couples filing jointly who make at least $731,200 a year.

The IRS makes these adjustments annually, using a formula based on the consumer price index to account for inflation and stave off “bracket creep,” which happens when inflation shifts taxpayers into a higher bracket though they’re not seeing any real rise in pay or purchasing power.

The 2024/25 increase is less than last year’s 7% increase, but much more than recent years when inflation was below the current 3.1% inflation rate.

Will Social Security get a raise because of inflation?

Yes, but it will be a lot less than what recipients received in 2023.

The cost-of-living adjustment, or COLA, to Social Security benefits will be 3.2% next year. That’s roughly one-third of the 8.7% increase given in 2023, which marked a forty-year high.

The 2024 COLA hike is above the average 2.6% raise recipients have received over the past two decades, but seniors remain concerned about being able to pay their expenses as well as the increasing possibility Social Security benefits will be reduced in coming years, according to a retirement survey of 2,258 people by The Senior Citizens League, a nonprofit seniors group.

How does raising rates lower inflation?

The federal funds rate is what banks pay each other to borrow overnight. If that rate increases, banks usually pass along that extra cost, meaning it becomes more expensive for businesses and consumers to borrow as rates rise on credit cards, adjustable rate mortgages and other loans. That’s why the funds rate is the key mechanism used by the Federal Reserve to calm inflation.

Simply put, companies and consumers don’t borrow as much when loans cost them more, and that means an overheated economy can cool and inflation may dip.

Will credit card interest rates continue to rise this holiday season?

The Fed’s string of rate hikes, aimed at easing the highest inflation in four decades, are a big reason credit card interest rates have reached record highs just in time for the holiday season.

Some retail credit cards now charge more than 33% interest, topping a 30% threshold that stores and banks were previously able to bypass but seldom did – until now.

“They can charge that much,” said Chi Chi Wu, a senior attorney at the nonprofit National Consumer Law Center. “Credit cards can actually charge whatever they want. It’s a little-known fact.”

The domino effect of a high benchmark rate and soaring credit card interest could put many Americans in financial straits this holiday season.

Though some consumers are paring back to deal with high prices, rising debt and shrinking savings, the average shopper expects to spend $1,652 this year on holiday purchases, according to the consultancy Deloitte, more than was typically spent in the last three years.

A lot of the buying will be done with credit cards. In an October poll of 1,036 shoppers by CardRates.com, nearly 4 in 10 respondents said they intend to have holiday credit card debt in the new year.

The nation’s collective credit card debt was $1.08 trillion, at the end of September, a record high. And the average interest rate was 21%, the highest ever documented by the Federal Reserve.

Savings account impact of high rates

The upside to the Fed’s string of rate hikes has been that consumers were able to earn good interest on their savings for the first time in years. Even when the Fed leaves interest rates unchanged, savers can do well.

Unfortunately, most account holders aren’t making the most of that potential opportunity.

Roughly one-fifth of Americans who have savings accounts don’t know how much interest they’re earning, according to a quarterly Paths to Prosperity study by Santander US, part of the global bank Santander. Among those who did know their account’s interest rate, most were earning less than 3%.

But consumers have time to make a change that could enable them to make more from their savings.

“We’re still a long way from (the Fed) beginning to cut rates,” said Greg McBride, chief financial analyst at financial services platform Bankrate. “This is great news for savers, who will continue to enjoy inflation-beating returns in the top-yielding, federally insured online savings accounts and certificates of deposit. For borrowers, interest rates staying higher for a longer period underscores the urgency to pay down and pay off costly credit card debt and home equity lines.”

The string of Fed rate hikes that began in March 2022 has made it costlier for consumers to borrow as interest rates on credit cards and other loans increased dramatically.

At the same time, inflation has made daily needs more expensive, pushing more Americans to lean on credit cards to get by. But lenders have become more reluctant to issue new cards, so in the midst of the holiday season, more shoppers are seeking higher credit limits, experts say.

In October, the application rate for higher limits rose to 17.8% from 11.2% in the same month the previous year, and from 12.0% in 2019, New York Fed data showed.

For some consumers, a higher limit on a card they already have is about their only option.

“After COVID, inflation and interest rates went out of control … people have less emergency funds for car repairs or buying presents,” said Brandon Robinson, president and founder of JBR Associates, which specializes in retirement strategies. “What they’re doing is using more credit card utilization – over 30% or well over 50% of their credit card allowance – and then can’t get approved for another card because their credit rating is down.”

Inflation is leading more Americans to work multiple jobs

The number of Americans working at least two jobs is at its highest peak since before the COVID-19 pandemic, according to federal data, an uptick that may reflect the financial pressure people are feeling amid high inflation.

Almost 8.4 million people had multiple jobs in October, the Labor Department said, a figure that represents 5.2% of the laborforce, the highest percentage since January 2020.

“Paying for necessities has become more of a challenge, and affording luxuries and discretionary items has become more difficult, if not impossible for some, particularly those at the lower ends of the income and wealth spectrums,” Mark Hamrick, senior economic analyst at Bankrate, told USA TODAY in an email.

People may also be moonlighting to sock away cash in case they’re laid off since job cuts typically peak at the start of a new year.

What is the Federal Reserve’s 2024 meeting schedule? Here is when the Fed will meet again.

What is the mortgage interest rate today?

Mortgage rates are falling, so is it time to buy?

It depends.

First of all, the Fed doesn’t directly set mortgage rates, but its actions have an impact. For instance, when the central bank was steadily boosting its key rate, the yield on the 10-year treasury bond went up as well. Because those bonds are a gauge for the interest applied to an average 30-year loan, mortgage rates increased.

But over the past six weeks, mortgage rates have been declining, averaging 7% for a 30-year fixed mortgage. That’s down from almost 7.8% at the end of October, according to data released by Freddie Mac on Dec. 7.

That may be giving some wannabe homeowners the confidence to start house hunting. For the week ending Dec. 1, mortgage applications rose 2.8% from the prior week, according to the Mortgage Bankers Association.

“However, in the big picture, mortgage rates remain pretty high,” says Danielle Hale, senior economist for Realtor.com. “The typical mortgage rate according to Freddie Mac data is roughly in line with what we saw in August and early to mid-September, which were then 20 plus year highs.”

So, many potential buyers may still need to sit on the sidelines, waiting for rates to drop further, says Sam Khater, chief economist for Freddie Mac. Hale and many other experts believe mortgage rates will dip next year.

Interest rate projection 2024

The Fed is expected to cut interest rates next year, though markets and economists disagree about how many rate cuts there will be.

Futures markets forecast there will be four or five rate cuts in 2024, amounting to a quarter of a percentage point each. The cuts, they predict, should start by spring, and ultimately drop interest rates as low as 4% to 4.25%.

But core prices, which leave out the volatile costs of food and energy and are the metric followed more closely by the Fed, ticked up 0.3% in November, higher than the 0.2% increase the month before. That might make the Fed more hesitant to nip rates in the immediate future.

Goldman Sachs and Barclays expect there to be only two rate decreases in 2024. And Fed Chair Jerome Powell has cautioned in recent public remarks that it was “premature” to talk about rate cuts.

November inflation report

Inflation dipped slightly last month, with falling gas prices mitigating the impact of rising rents.

Consumer prices overall increased 3.1% from a year earlier, slightly below the 3.2% rise in October, according to the Labor Department’s consumer price index. That slower pace moves the inflation rate nearer to the level, reached in June, that was the lowest in over two years. Month over month, prices increased a slight 0.1%.

Core prices, however, which leave out the more erratic costs of food and energy and which are more closely monitored by the Fed, increased 0.3% in November after rising 0.2% the previous month. That means core inflation’s yearly increase remained at 4%, though it’s the lowest level since September 2021.

Nursing can be a rewarding career in a couple of important ways. It involves caring for the health of others and helping them through what can be a challenging moment in their lives, which can be satisfying. A nursing degree can mean job stability as well. According to the Bureau of Labor Statistics, demand for nurses will increase at 6% per year, faster than the average career growth. And here’s one other important fact: The average registered nurse salary is at a median of $81,220 per year. Compare that with the median US salary for the same period of $54,132, and you can see that nursing can be a lucrative career, too.

The average nursing salary will vary depending on the type of nursing you do. For instance, there’s the average nurse salary vs. the average registered nurse salary vs. the average nurse practitioner salary. Qualifications and other factors will determine how much you make as a nurse.

Read on to learn more about this important topic. The information that follows can help you decide if nursing is the right career path for you, and, if so, which type of nursing you want to pursue.

Average Salaries for Different Types of Nurses

Wondering, “How much do nurses make?” First, understand that when considering nursing as a career, it’s vital to know about the different types of nurses. Each has its own education and certification requirements.

• A licensed vocational nurse (LVN) or licensed practical nurse (LPN) is one of the lowest-paid jobs within the nursing field. Job responsibilities are typically similar for LVN and LPNs. California and Texas use the term LVN, while the rest of the country uses the designation LPN. These positions also have the lowest educational requirements.

While LVN/LPN roles don’t always require a college education, there are usually state-approved training certification programs. Most of these courses take aspiring LVN/LPNs one year to complete, and then they must pass the NCLEX-PN examination for state licensing. How much does a nurse make a year with this kind of credential? The average salary for LVN/LPNs as of 2023 was about $50,580 annually.

• Aspiring registered nurses (RN) typically need a bachelor’s or associate’s degree from an accredited program. There are also some accelerated programs available and some second degree programs for students who already have a bachelor’s degree in another field.

After successfully completing their chosen coursework, nursing students must then pass the NCLEX-RN exam in order to become a certified RN. In addition, RNs usually must obtain a state license after passing the NCLEX-RN exam.

To drill down on the details here, know that each state has its own licensing board. You may want to research the specific requirements in the state where you plan to practice. How much do RNs make? The average RN salary as of 2023, as noted above, was approximately $88,220 per year. (Below you will find state-by-stage nursing salaries, though not specifically for RNs.)

Next, consider the career of a Clinical Nurse Specialists (CNS). This type of nurse has gone a step beyond RN and pursued additional education. At a minimum, you must have a master of science in nursing (MSN) to become a CNS.

A CNS typically trains extensively in a specialty area, such as emergency medicine, oncology, or women’s health. At the end of 2023, the average salary for a CNS was $99,148 annually, which is higher than the RN salary, reflecting the additional education and skills.

• A Nurse Practitioner (NP) holds an advanced degree, but their responsibilities vary slightly when compared with a CNS. For example, in most states, a nurse practitioner is able to prescribe medication, while a CNS is not. The average nurse practitioner salary at the end of 2023 was $124,680 annually. 💡 Quick Tip: Ready to refinance your student loan? With SoFi’s no-fee loans, you could save thousands.

Average Salaries and Location

Here’s another factor that can impact the average nurse’s salary: location. After all, wages and overall cost of living can vary dramatically depending on whether you live in, say, a small town or close to a pricey urban center.

Check this chart to see how average nurse salaries compare state by state. Note that these figures reflect LPN salaries, which are at the lower end of the spectrum, but they can give you an idea of how much nurses make by location. This could be good information to consider when deciding where to practice.

State

Mean Annual Nurse Salary

Alabama

$45,260

Alaska

$66,710

Arizona

$61,920

Arkansas

$45,990

California

$69,930

Colorado

$60,310

Connecticut

$62,620

Delaware

$57,360

District of Columbia

$62,010

Florida

$53,780

Georgia

$50,830

Hawaii

$55,730

Idaho

$54,710

Illinois

$58,840

Indiana

$55,850

Iowa

$51,400

Kansas

$51,700

Kentucky

$49,570

Louisiana

$47,430

Maine

$55,830

Maryland

$60,180

Massachusetts

$68,170

Michigan

$57,180

Minnesota

$54,870

Mississippi

$45,020

Missouri

$49,500

Montana

$52,420

Nebraska

$52,080

Nevada

$63,910

New Hampshire

$63,550

New Jersey

$61,990

New Mexico

$59,400

New York

$57,560

North Carolina

$53,010

North Dakota

$53,080

Ohio

$52,330

Oklahoma

$48,090

Oregon

$66,190

Pennsylvania

$54,520

Rhode Island

$66,770

South Carolina

$51,060

South Dakota

$46,000

Tennessee

$46,540

Texas

$52,850

Utah

$55,790

Vermont

$57,150

Virginia

$52,790

Washington

$69,950

West Virginia

$45,530

Wisconsin

$52,610

Wyoming

$54,880

How Much Does it Cost to Get a Nursing Degree?

The cost of getting a nursing degree varies based on the type of nursing program you choose. Each of the nursing positions listed above requires different degrees and certification.

• The process to become an LVN/LPN generally costs between $1,000 and $5,000.

• Taking an RN two-year associate’s program can cost $3,500 per year at public institutions; $15,470 per year at private schools.

• An alternative is to become an RN through a four-year bachelor’s program. This process works similarly to most other bachelor’s degree programs and typically costs the same as a four-year college or university.

• In addition to having already been an RN, both CNS and NP careers require advanced degrees. Typically, a masters of science in nursing (MSN) is required for both positions, which can cost between $18,000 to $57,000 in total.

• Some choose to further their education, becoming a Doctor of Nursing Practice (DNP). These degrees can be expensive but also have the potential to increase a nurse’s salary. After a master’s degree, expect to pay an additional $20,000 to $40,000, but your nursing salary is likely to rise, too.

There are usually costs beyond nursing school tuition. You’ll likely have to buy textbooks and supplies like a lab coat, scrubs, and a stethoscope. Many programs also charge additional lab fees each semester. Many schools will require nursing students to take out liability insurance and get some mandatory immunizations.

After graduating from your chosen program(s), you’ll also likely want to factor in the cost of licensing and exam fees as you enter the job market. 💡 Quick Tip: When refinancing a student loan, you may shorten or extend the loan term. Shortening your loan term may result in higher monthly payments but significantly less total interest paid. A longer loan term typically results in lower monthly payments but more total interest paid.

Paying for Your Nursing Degree

Becoming a nurse can be a pricey process, depending on the path you choose. But there are options available to help students pay for their nursing degree. The American Association of Colleges of Nursing has a database of scholarships for nursing schools. As you may know, scholarships don’t need to be repaid. This can make them an especially valuable resource in making ends meet as a nursing student.

In addition, federal aid, including grants, scholarships, work-study, and federal student loans could provide some relief. To apply, students must fill out the Free Application for Federal Student Aid (FAFSA) each year.

Student Loan Forgiveness Options for Nurses

There are a number of student loan forgiveness programs available to nurses. Keep in mind that each typically has its own program requirements, so it’s helpful to review them closely to determine whether you qualify.

• Public Service Loan Forgiveness (PSLF) forgives certain federal Direct loans after 10 years of qualifying, on-time payments. This program is open to borrowers who work for a qualifying organization. You can find details online about qualifying for the PSLF program to see if you could benefit from it.

• The NURSE Corps Loan Repayment Program will repay a portion of a nurse’s eligible student loans when they work full time at a Critical Shortage Facility or as a faculty member at a qualifying nursing school. Those accepted by the program are eligible to have 85% of their outstanding loan balances forgiven over a two-year commitment.

• The National Health Service Corps Loan Repayment Program provides loan forgiveness to qualifying nurses who commit to working for two years in clinical practice at a National Health Service Corps site.

Repaying Student Loans after Nursing School

If you borrowed federal or private student loans to help you pay for nursing school, developing a repayment strategy can be valuable. Not only will it set you on a path to repaying your debt, it can teach you valuable budgeting skills as well.

If you don’t qualify for any of the available loan forgiveness options, federal student loans come with a few different student loan repayment plans so you can find the option that works best for your budget.

If you relied on private student loans to help you pay for your tuition at nursing school, you may want to review your repayment terms. Each lender will determine their own terms and conditions for the loans they lend.

As you develop a game plan to help you repay your student loans, one option to consider is student loan refinancing.

When you refinance a loan, you take out a new loan with new terms. This loan can then be used to repay your existing loans. If you borrowed multiple loans, that means you could have the option to consolidate them into one single monthly payment — potentially with a lower interest rate.

However, it’s important to keep in mind a couple of factors:

• You may pay more interest over the life of the loan if you refinance with a longer term.

• If you are considering refinancing federal student loans, know that they come with an array of benefits and protections that are forfeited if you refinance.

To see how refinancing could impact your student loan, you can take a look at this student loan refinancing calculator.

The Takeaway

Nursing can be a challenging but rewarding profession, and the average nurse salary could provide a well-paying career. How much do RNs make? The typical salary currently tops $88,000. There are different kinds of nursing degrees and positions, so it’s wise to do your research to understand what each one requires and which might best suit your needs. Also, financing your education as a nurse can also need research to understand the obligation and how you might fund it.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

SoFi Student Loan Refinance If you are a federal student loan borrower, you should consider all of your repayment opportunities including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. Please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans or extended repayment plans.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Homeowners usually refinance to save money. If you can reduce your interest rate by 1% or more, that could be enough incentive to refinance. Yet given elevated rates, you probably won’t be able to secure a significantly lower rate than your current one. That doesn’t mean a refi isn’t a good idea for other reasons, like changing your term length or home loan type.

Both 15-year fixed and 30-year fixed refinances saw their mean rates trail off this week. The average rate on 10-year fixed refinance also slumped.

Millions of homeowners refinanced when mortgage rates hit record lows at the start of the pandemic. However, in today’s high-rate environment, most refinance demand is for cash-out refinances to help consolidate debt or fund other major expenses, according to Matt Graham of Mortgage News Daily. For those considering a refinance, Graham recommends getting in touch with a loan originator, keeping an eye on daily rate changes and making a game plan to capitalize on the next big drop in rates.

About these rates: Like CNET, Bankrate is owned by Red Ventures. This tool features partner rates from lenders that you can use when comparing multiple mortgage rates.

Refinance rates for homeowners

Many homeowners are facing the same disadvantages as everyone else in the housing market right now: elevated mortgage rates, limited available inventory and expensive homes.

If you decide to refinance, make sure to compare rates, fees and the annual percentage rate — which reflects the total cost of borrowing — from different lenders to find the best deal. Here’s a table with the average refinance rates reported by lenders across the country. We track refinance rate trends using information collected by Bankrate:

Today’s refinance interest rates

Product

Rate

A week ago

Change

30-year fixed refi

7.69%

7.74%

-0.05

15-year fixed refi

6.95%

7.05%

-0.10

10-year fixed refi

6.97%

7.11%

-0.14

Rates as of Dec. 1, 2023.

Where refinance rates are headed

In early November, a dip in mortgage rates motivated some prospective buyers to come off the sidelines and apply for home loans. Refinance applications also picked up slightly over the last few weeks, but they still remain well below historical averages, according to the Mortgage Bankers Association. Experts predict that both purchasing and refinancing activity won’t come back into full swing for a while.

“High interest rates and house prices have dampened demand, particularly in the refinancing market, which is currently at a standstill,” said Carlos Garriga, senior vice president and research director at the St. Louis Federal Reserve.

Mortgage rates surged steadily throughout much of 2022 and 2023 as the Federal Reserve carried out aggressive interest rate hikes to slow inflation. With inflation now going down, the Fed has held off on further rate hikes to evaluate the impact on price growth and the labor market.

It’s widely expected the Fed will hold interest rates steady until mid-2024, which can help mortgage rates stabilize. Once the central bank begins to actually cut rates, there should be more sustained downward movement.

“It’s very difficult to forecast movements in the mortgage rate, but we expect significantly less rate volatility in the coming year relative to 2022,” said Matthew Walsh, housing economist for Moody’s Analytics.

Even if rates return to 7% — a considerable decline from recent peaks — it could still be hard for homeowners to find many compelling or profitable reasons to refinance, said Keith Gumbinger, vice president of the mortgage site HSH.com.

Instead of a traditional rate-and-term refinance, homeowners might instead opt for a cash-out refinance, which allows them to tap into their home equity with a lower interest rate than other types of borrowing, according to Logan Mohtashami, lead analyst at HousingWire. “This would make sense only if it benefits the homeowner with a lower total cost of living because credit card interest rates are so high,” said Mohtashami.

How to find personalized refinance rates

The rates advertised online often require specific conditions for eligibility. Your personal interest rate will be influenced by market conditions as well as your specific credit history, financial profile and application. Having a high credit score, a low credit utilization ratio and a history of consistent and on-time payments will generally help you get the best interest rates. To get the best refinance rates, make your application as strong as possible by getting your finances in order, using credit responsibly and monitoring your credit regularly. And don’t forget to speak with multiple lenders and shop around.

Refinancing can be a great move if you get a good rate or can pay off your loan sooner, but consider whether it’s the right choice for you at the moment.

30-year fixed-rate refinance

The average 30-year fixed refinance rate right now is 7.69%, a decrease of 5 basis points compared to one week ago. (A basis point is equivalent to 0.01%.) A 30-year fixed refinance will typically have lower monthly payments than a 15-year or 10-year refinance so it can be a good option if you’re having trouble making your monthly payments. However, a 30-year refinance loan will take you longer to pay off and will typically cost you more in interest over the long term.

15-year fixed-rate refinance

For 15-year fixed refinances, the average rate is currently at 6.95%, a decrease of 10 basis points compared to one week ago. Though a 15-year fixed refinance will most likely raise your monthly payment compared to a 30-year loan, you’ll save more money over time because you’re paying off your loan quicker. Also, 15-year refinance rates are typically lower than 30-year refinance rates, which will help you save more in the long run.

10-year fixed-rate refinance

The current average interest rate for a 10-year refinance is 6.97%, a decrease of 14 basis points compared to one week ago. A 10-year refinance typically has the lowest interest rate but the highest monthly payment of all refinance terms. A 10-year refinance can help you pay off your house much quicker and save on interest, but make sure you can afford the steeper monthly payment.

Is now a good time to refinance?

Generally, it’s a good idea to refinance if you can get a lower interest rate than your current interest rate, or if you need to change your loan term. When deciding whether to refinance, consider other factors, including how long you plan to stay in your current home, the length of your loan and the amount of your monthly payment. And don’t forget to factor in fees and closing costs, which can add up.

With mortgage refinance rates at current heights, the number of refinancing applicants has shrunk. If you bought your house when interest rates were lower than today, there is little financial benefit to refinancing your mortgage. However, homeowners can’t time the market. Regardless of where rates are headed, decide if refinancing makes sense based on your financial situation and goals.

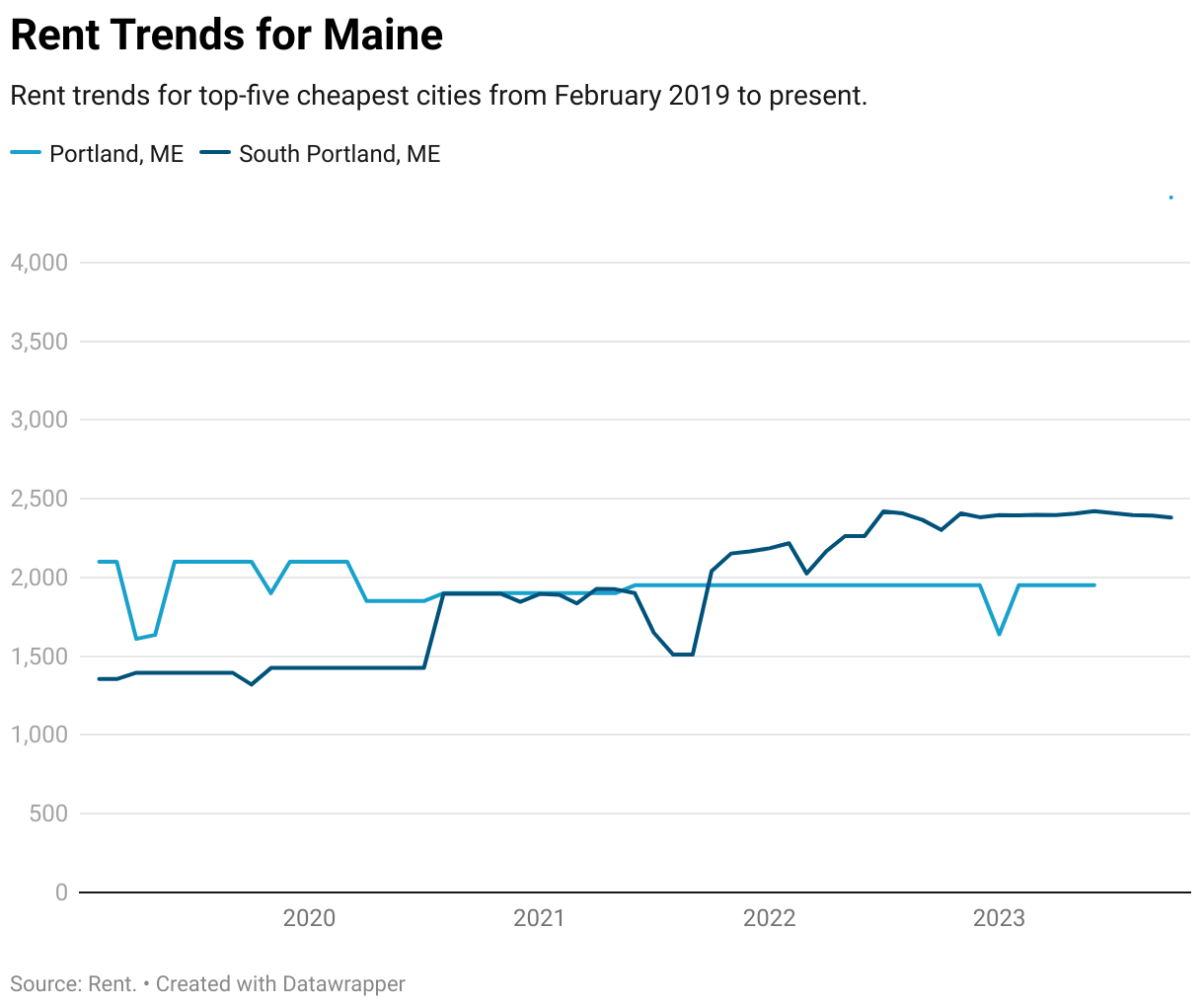

Maine, known for its picturesque landscapes and serene environment, is quickly becoming a hot spot for renters due to its affordability. As the Pine Tree State flourishes with opportunities, it provides affordable living for individuals from all walks of life. Rental prices vary greatly across the state, yet Maine sustains an appealing cost of living for many. Particularly, three cities have marked their places as the cheapest for renters; South Portland, Portland, and Yarmouth. These cities not only offer affordable rent but also present a high quality of living with their unique characteristics.

South Portland, ME

With a population of 25,665, South Portland is not just an affordable city but also a great place to live. The city offers a median income of $67,198 and a median home value of $276,100. Life in South Portland comes with more than just affordable living, it’s a city that thrives on its local community and stunning coastal views. You’re never far from a stunning view, with the city’s unique location on the coast of Maine. The city also has plenty of green spaces, including Mill Creek Park and Willard Beach, providing the perfect backdrop for a Maine lifestyle.

Portland, ME

As the most populous city in Maine with 66,706 residents, Portland offers a balance between an affordable cost of living and a vibrant city life. The city has a median income of $61,695, and a median home value of $302,700. Of note to renters, the asking price for a 2-bedroom is around $4,412. Portland’s Old Port district, with its cobblestone streets, 19th-century brick buildings, and fishing piers, is a hub of activity. Plus, there are numerous recreational areas in the city, including East End Beach and the Eastern Promenade.

Yarmouth, ME

Although smaller with a population of 5,752, Yarmouth is a charming town that offers an affordable lifestyle. Here, the median income stands at $69,576 with a median home value of $347,300. Renters can find a 2-bedroom place for an asking price of around $2,915. Yarmouth’s Main Street is a testament to its historical charm, while Royal River Park provides a great outdoor experience for residents. Yarmouth also hosts the famous annual Clam Festival, which offers a glimpse into the friendly community spirit of the town.

Methodology

The cheapest cities in each state were ranked based on its median home price and median asking rents for studio, one-, two-, and three-bedroom units. Prior to ranking, inputs were normalized, and weights were applied using a 1.25:1 ratio of asking rents to home prices. Data on home prices are from the U.S. Census 2016-2020 American Community Survey 5-year estimates. Data on asking rents are from Rent. Cities without data for one- or two-bedroom asking rents or a population of less than 10,000 were removed from this ranking. Any other missing values were zeroed and did not impact the final score.

Saving up for a down payment is a common challenge for many prospective homebuyers. FHA loans allow qualifying borrowers to put as little as 3.5% down on a property, helping lower the barriers to homeownership for many.

With an FHA loan, borrowers may also be eligible for down payment assistance. But there are other out-of-pocket expenses to keep in mind when considering an FHA loan. Let’s take a closer look at FHA loan down payment requirements and how much money you’ll need to get to the closing table.

What Is an FHA Loan?

An FHA loan is a type of mortgage that’s issued by a lender, such as a bank or credit union, but insured by the Federal Housing Administration (FHA). The purpose of the FHA mortgage program is to make homeownership more affordable for low- to moderate-income buyers.

Since FHA loans are government-insured, they offer more flexible eligibility requirements for borrowers who might not qualify for a conventional home loan. FHA loans have lower minimum down payment and credit score requirements, making them popular with first-time homebuyers and applicants with limited savings or poor credit. Compared to conventional mortgages, FHA loan interest rates are typically lower, but will vary depending on the lender and on the borrower’s credit score and finances. 💡 Quick Tip: Buying a home shouldn’t be aggravating. SoFi’s online mortgage application is quick and simple, with dedicated Mortgage Loan Officers to guide you through the process.

First-time homebuyers can prequalify for a SoFi mortgage loan, with as little as 3% down.

FHA Loan Income Requirements

There aren’t any minimum or maximum income requirements to qualify for an FHA loan. However, there may be income limits for borrowers receiving down payment assistance through a state or local program.

In any case, lenders will look at an applicant’s ability to manage monthly mortgage payments and ultimately repay the FHA loan. Besides savings and assets, lenders assess an applicant’s debt-to-income (DTI) ratio, which measures the percentage of monthly income that goes toward debt payments. A lower DTI ratio is typically viewed as favorable. Depending on the lender, borrowers can get an FHA loan with a DTI ratio of up to 50%. In comparison, conventional loans typically require a DTI ratio of 43% or less.

Recommended: How Much is a Down Payment?

What Is the Down Payment Required for an FHA Loan?

Down payments are calculated as a percentage of the home purchase price. Historically, lenders looked for buyers to put down one-fifth of a home’s purchase price upfront. But you no longer always need to put down 20% on a house. The minimum down payment percentage for FHA loans depends on a borrower’s credit score.

The average down payment on a house in the U.S. was 13% in 2022. But with an FHA loan, borrowers with a credit score of 580 or more may qualify for a down payment of 3.5% of the home purchase price. Those with credit scores between 500 and 579 will need to put 10% of the home price towards a down payment. For a $400,000 house, this translates to $14,000 for a 3.5% down payment and $40,000 for a 10% down payment. 💡 Quick Tip: Generally, the lower your debt-to-income ratio, the better loan terms you’ll be offered. One way to improve your ratio is to increase your income (hello, side hustle!). Another way is to consolidate your debt and lower your monthly debt payments.

What Other Cash Will I Need to Close?

Besides the down payment, the remaining amount you need to close on a house will depend mainly on the home’s purchase price. Taking out an FHA loan requires paying an upfront mortgage insurance premium (MIP) of 1.75% of the loan total. It may be possible to roll this cost into the loan, which would increase the loan principal and monthly payment amount.

Buyers will also be on the hook for FHA loan closing costs, which typically range from 2% to 5% of the home’s purchase price. Borrowers can potentially avoid the upfront expense by rolling closing costs into an FHA loan. By financing closing costs, borrowers will pay a portion of the costs each month, plus interest. Note that financing closing costs can increase a borrower’s DTI ratio and potentially impact their ability to qualify for an FHA loan.

An alternative option to cover closing costs would be to ask for seller concessions. FHA loans allow the seller to contribute up to 6% of the home value for closing costs as a seller concession.

Recommended: What Do You Need to Buy a House?

How to Save for an FHA Loan Down Payment

Understanding how much house you can afford is a useful place to start to determine your housing budget and savings goal. Using an FHA loan mortgage calculator can help crunch the numbers to determine your down payment and monthly payment based on different loan terms. Not sure you will choose an FHA loan? Use a home affordability calculator to determine how much house you can afford.

With a savings goal in mind, calculate how much you can set aside each month after paying for debts and expenses. Consider cutting discretionary spending, such as dining out and travel, to increase monthly savings.

Buyers can also get the money they need for an FHA down payment in the form of a gift from family, friends, employer, charitable organization, or government program. Gifted funds need to be accompanied by a gift letter to show the lender that the money is going toward the down payment and doesn’t need to be repaid.

Is Down Payment Assistance Available for FHA Loans?

Borrowers who can’t afford a down payment on an FHA loan may be eligible for financial assistance. Down payment assistance can come in several forms, including grants and forgivable loans. These programs are available through local, state, and federal government programs, as well as nonprofit organizations.

Most down payment assistance programs are geared towards first-time buyers. They may include additional eligibility requirements, such as income limits and participation in homebuyer education courses. Consult a list of first-time homebuyer programs and loans to see what you might be eligible for. If it has been more than three years since you have owned a home, you may qualify for first-time homebuyer status.

Additional Cost Considerations for FHA Loans

In addition to the upfront costs of a down payment, closing costs, and MIP, there are other expenses to plan for.

The MIP includes an additional annual fee besides the 1.75% that’s required for closing. Annual payments range from 0.15% to 0.75% depending on the loan terms and loan-to-value ratio. The total annual cost is divided by 12 and spread out across the monthly payments in a given year. Note that MIP usually spans the life of the FHA loan unless a borrower refinances.

Depending on the property location, borrowers may also need to pay for flood insurance to get an FHA loan.

Pros and Cons of an FHA Loan

FHA loans are popular for their lower down payment mortgage requirements, but they’re not for everyone. Here are some advantages and drawbacks to consider when comparing home mortgage loan options.

Pros:

• Smaller down payments

• More lenient credit score requirements

• No income limits

• Can finance closing costs

Cons:

• Required to pass an inspection and appraisal

• Must be used for a primary residence.

• Loan limits of $472,030 to $1,089,300 for a single-family home, depending on the cost of living by state.

• Can require an inspection and stricter standards for the condition of the property.

The Takeaway

What is the minimum down payment for an FHA loan? Borrowers with credit scores of 580 or more can put just 3.5% down, while those with scores between 500 to 579 need to put 10% toward a down payment. The combination of lower minimum credit score and low down payment make FHA loans one attractive option for first-time homebuyers.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

FAQ

What is the lowest down payment for an FHA loan?

The lowest down payment for an FHA loan is 3.5% of the loan amount. Borrowers can explore down payment assistance programs to help cover the cost.

What is the down payment for an FHA loan 2023?

The down payment for an FHA loan in 2023 ranges from 3.5% to 10% depending on the borrower’s credit score.

What will disqualify you from an FHA loan?

Borrowers could be disqualified from an FHA loan based on a high debt-to-income ratio, poor credit, or insufficient funds to pay for the down payment, closing costs, and monthly mortgage payment.

Photo credit: iStock/Edwin Tan

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Mortgages Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility for more information.

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

In this brief exploration of the cheapest places to live in Indiana, we delve into the unique aspects that make certain cities stand out as ideal havens for those on a tight budget. From accessible housing markets to economic diversity, each city on this list presents distinctive features that contribute to a cost-effective and comfortable lifestyle.

Join us as we uncover the hidden gems and economic advantages that make these places not only the most affordable cities, but also enriching for residents seeking financial stability.

Bloomington stands out among the most economical towns to call home in Indiana. Its cost-effective appeal is anchored in several key factors. Firstly, the city maintains a relatively low overall cost of living, encompassing affordable housing options and reasonable utility expenses. Beyond that, Bloomington offers accessible public transportation, minimizing commuting costs for residents on a budget.

The presence of Indiana University contributes to the city’s economic dynamic, fostering a competitive job market with opportunities for part-time and entry-level positions in the university itself. This aspect can be particularly advantageous for individuals seeking employment without compromising their financial constraints.

Grocery and everyday necessities are reasonably priced in Bloomington, allowing residents to manage their budgets more effectively. Additionally, the city’s commitment to green spaces and outdoor activities provides affordable recreational options, promoting an active lifestyle without significant expenses.

Fort Wayne offers affordable housing options, ensuring that individuals and families can find the best home price and right spot that aligns with their financial situation. The cost of living in Fort Wayne is notably reasonable considering the amenities that the city provides.

Ample job opportunities in Fort Wayne contribute to the income ratio and significantly to its affordability. The city boasts a diverse employment landscape with a range of industries, providing residents with various options for securing a comfortable income.

Furthermore, Fort Wayne prioritizes accessible and budget-friendly community facilities. The city’s commitment to parks and open spaces allows residents to enjoy outdoor activities without incurring significant expenses.

Hammond’s housing market is characterized by reasonable prices, ensuring that individuals and families can find cost-effective living arrangements that meet their financial needs.

One notable advantage of living in Hammond is its strategic location, providing easy access to neighboring cities and employment opportunities. This accessibility enhances the potential for securing affordable employment options, contributing to residents’ financial stability.

Additionally, Hammond’s strong food scene is full of affordable dining options, allowing residents to explore the world of various cuisines without breaking the bank. This culinary diversity adds a unique flavor to the city, providing residents with plenty of budget and family-friendly dining experiences.

One distinct advantage of affordable living here in Lafayette is its proximity to educational institutions and attractions. The presence of Purdue University provides opportunities for budget-friendly educational and cultural experiences, including lectures, events and performances that enhance overall quality of life for residents on a tight budget.

The city’s commitment to green spaces and outdoor activities is another notable aspect. Lafayette boasts well-maintained parks and communal spacess that are not only easily accessible but also contribute to a healthy and active lifestyle without significant expenses.

Lafayette’s local economy, supported by a mix of industries, presents residents with varied job opportunities, promoting financial stability for those seeking employment within their budget constraints.

One distinctive advantage of renting in South Bend is the city’s commitment to supporting a healthy lifestyle. Well-maintained parks and outdoor facilities not only provide residents with affordable leisure options but also contribute to a more active lifestyle without additional costs.

South Bend’s proximity to the University of Notre Dame is a notable aspect, offering potential renters access to educational and community resources without straining their budgets. The university’s presence enriches the local atmosphere and provides opportunities for affordable entertainment and intellectual experiences.

The city’s transportation infrastructure is another cost-effective aspect for renters. South Bend’s accessible public transportation system minimizes commuting expenses, allowing residents to navigate the city conveniently without a significant financial burden.

One notable advantage for renters in Evansville is the city’s affordable utilities and lowest cost of living expenses. Lower utility costs contribute significantly to the overall affordability of renting in the area, allowing residents to manage their monthly expenses more effectively.

Evansville’s commitment to community services and rec facilities is another key aspect. The city is home to a number of parks, affordable outdoor activities and open green spaces that contribute to a high quality of life for renters seeking budget-friendly leisure options.

The local job market in Evansville is full of employment opportunities, ensuring renters have access to a range of options that align with their skills and qualifications. This economic diversity supports financial stability for individuals seeking employment within their budget constraints.

One distinctive advantage for renters in Kokomo is the city center’s affordable cost of living. Lower living expenses, including utilities and everyday necessities, make it a particularly attractive and affordable place for those seeking to manage their monthly budgets effectively while renting.

Kokomo’s community focus is another noteworthy aspect, as the city prioritizes local events and affordable activities. Residents have access to safe parks, community spaces and budget-friendly entertainment options.

The city’s strategic location and ease of transportation contribute to its appeal for budget-conscious renters. Kokomo’s accessible transportation infrastructure minimizes commuting costs and enhances convenience for residents navigating the city on a budget.

Muncie is home to Ball State University, providing renters with access to affordable educational and cultural experiences. Renters on a budget can attend events, lectures and performances at ball state university without significant financial strain.

Muncie has a great secondhand market scene, from thrift stores to community markets. This allows budget-conscious renters to furnish their homes, update their wardrobes and meet their daily needs at a fraction of the cost compared to new items, contributing to significant savings.

Muncie boasts a variety of budget-friendly local eateries and diners. Residents can enjoy unique culinary experiences without breaking the bank, thanks to the city’s affordable dining options that cater to various tastes and preferences.

One noteworthy advantage for renters in Gary is the city’s strategic location. Positioned near major highways and transportation hubs, Gary facilitates easy access to neighboring cities, providing residents with diverse employment opportunities. This accessibility enhances the potential for renters to find jobs that align with their skills and financial needs.

Gary’s commitment to green spaces is another unique aspect that caters to individuals on tight budgets. The small city also maintains well-kept parks and outdoor areas around town that not only provide residents with affordable recreational options but also contribute to a healthier lifestyle without the need for expensive memberships or facilities.

Moreover, Gary’s local initiatives for affordable community services, like healthcare clinics and assistance programs, help renters manage their basic needs without incurring significant costs. This focus on community support services contributes to an overall more sustainable and budget-friendly living experience.

One distinctive advantage for renters in Terre Haute lies in the city’s commitment to green spaces and outdoor activities. With a ton of parks, hiking nature trails and public use areas, residents can do as they please in the great outdoors.

The city’s proximity to Indiana State University adds a unique dimension for Terre Haute renters on a budget. Access to the university’s educational resources, including libraries and events, provides affordable opportunities for personal enrichment, further enhancing the overall living experience.

Find your affordable Indiana apartment today