Do you know who your neighbors are? According to the Pew Research Center, 57 percent of Americans say they know some of their neighbors. Whether you frequently talk to your upstairs neighbor or you only see your next-door neighbor on occasion, being a good neighbor is important in establishing yourself as part of the neighborhood and community.

1. Learn the three-step rule

“Our best tip to be a good neighbor is a simple three-step rule: Respect, communication and responsible pet ownership!” says 10 Stars Property Management. “In almost any situation respecting others’ space is a good base for any relationship. Especially with someone living right next door. Just be social and communicate with your neighbors — even just a smile goes a long way! Finally, always be conscious of your pets and their actions. No one wants to step into poop!”

2. Consideration goes a long way

“Being a good neighbor means being considerate of people,” says Nick Slagle of HomeRootsPM.com. “They take care of the appearance of their home and simultaneously are willing to help those in their neighborhood. Good neighbors are friendly and welcoming without being intrusive.”

3. Introduce yourself

“The best way to build into a good neighbor? Introduce yourself!” says Jim Shonts, real estate broker and owner of PMI Elevation. “Neighborhoods can thrive on a sense of community, and getting to know your neighbors soon after moving can help you settle in. And, since not all people are outgoing, those early introductions can give insight on how to respect their personal space.”

4. Show interest

“Whether you are moving in or welcoming a new neighbor, show interest in them by allowing the interruption in your day to greet each other when the opportunity arises,” says Sallie Plass from Etiquette Enrichment. “Ask for or suggest ways to get involved in the neighborhood or community. Intentionally smile, exchange names and phone numbers.”

5. Stay kind

Dr. Lew Bayer, CEO of Civility Experts Inc. suggests that a good neighbor should try to “ease the experience” of the others. “This means try to reduce stress and offer support versus causing stress, e.g. if the neighbor leaves the garage door open, let them know. If the neighbor’s dog barking bothers you, ask if you can give the dog a toy or bone. Turn your music down when you see your neighbor come home. Shovel the neighbor’s walk when you shovel yours. Just do what you can to stay kind…everyone is busy and tired and sometimes struggling. Try to assume the best of people and try to make their life easier versus harder.”

6. Treat your neighbor

“A few days after the new neighbors move in, knock on the door to meet them and include a small plate of homemade cookies or muffins or a seasonal plant (for example, a potted chrysanthemum in the fall) and a sticky note with your name and phone number if they need anything,” says Rachel from the Etiquette Trainer. “Additionally, if there’s a neighborhood Facebook page, let them know about it and encourage them to contact you if they need to borrow anything while settling in, such as a ladder or hand tools.”

7. Prioritize respect

“The adage, ‘Good fences make good neighbors’ still holds true,’” says Diane Gottsman, a national etiquette expert from The Protocol School of Texas, “It’s important to be respectful of each other, especially when sharing a fence, trees hanging over the roof, drainage coming into the other person’s lawn and an assortment of dilemmas. If you are experiencing an issue, reach out in person, and address the issue in a pleasant tone of voice with an open attitude and collaborative spirit. People are much more willing to work with someone who has a smile on their face and shows an effort to get along.”

“If there is a problem that cannot be dealt with neighbor-to-neighbor, the HOA may need to get involved. When renting, talk to the landlord first before going over their head. A good neighbor respects each other’s property, pets and privacy.”

8. Just say hi

“I think being a good neighbor starts by knowing your neighbors. I make sure to say hello every day. Whether it’s a good day, bad day or if I’m in a rush, I believe acknowledgment goes a long way and eventually, that helps cultivate a deeper and better neighbor relationship,” says Pamela Syvertson, broker and owner of Verandah Properties.

9. Model how you’d like to connect with your neighbors

“Challenge yourself to reach out to a neighbor you wouldn’t normally connect with and set the tone in how you want to connect with them,” says Daniel McArdle-Jaimes, the Strategic Communications Officer for the Office of Community & Civic Life in Portland, OR. “Maybe your neighbor is from another country or is a different age than you. Start by introducing yourself and developing a relationship to help make your block a more welcoming place for all. And who knows? You might make a new friend or regular lunch buddy!”

“Also — during and after an emergency, neighbors offer a powerful source of help. Organizing a neighborhood meeting or training through an organization to discuss emergency plans and personal safety is a wonderful way to build community. Many cities offer free resources, like the City of Portland’s Neighbors Together training, which help to start and host these important safety conversations.”

10. Remember empathy

“In addition to following the rules of your community, being a good neighbor requires empathy,” says Stayce Wagner, founder and CEO of Spencer Crane Etiquette. “The ability to see things from your neighbor’s perspective helps you behave with kindness, consideration and respect. A good neighbor cleans up their dog’s poop, doesn’t blast music in the middle of the night and never parks in a neighbor’s assigned space without permission.”

“Additionally, if making small talk with people in your neighborhood is outside your comfort zone, start with a smile, eye contact and a friendly hello. When you feel more comfortable, introduce yourself to the neighbors you see regularly and let things develop naturally. Every introduction won’t lead to a close friendship, but you’ll have established friendly contact.”

11. Talk like adults

“The best advice we can give as a management company is that if you have an issue with a neighbor, you go visit them directly and discuss it in an adult manner. Try this approach first before contacting law enforcement, HOA’s or management companies,” says David Peschio, owner and principal broker at PMI Richmond. “It usually can be resolved without escalation and helps maintain good relationships moving forward.”

12. Remember their name

“Being a good neighbor isn’t difficult, but you need to put a little effort into it to have happy neighborly relations,” says Arden Clise, President of Clise Etiquette and author of Spinach in Your Boss’s Teeth: Essential Etiquette for Professional Success. “When a new neighbor moves in, drop by with some cookies, a plant or some small gift to introduce yourself and welcome them to the neighborhood. Be thoughtful. If you’re shoveling your walk of snow, clear your neighbor’s walk, as well. If you have a neighbor who is elderly, sick or struggling in some way, check in on them and see how you can be helpful. At the very least, make an effort to remember their name and say hello when you see them.”

13. When in doubt, act neighborly

“Remember — be kind. To yourself, to your neighbor, their kids, their pets and their plants and trees,” says Felipe Quintana from Charter for Compassion. “Be forgiving: We all make mistakes — aim to be the best version of yourself. Allow everyone their space but stay there for them on the sidelines if they need a friend. It all comes back in the end!”

14. Keep it friendly

“Being a good neighbor means being friendly and helpful, without being intrusive. Giving a wave and a hello with sincerity is felt and appreciated,” says Mary Ann Brennan, the Director of Rental Services for Del Val Realty & Property Management.

“Love your neighbor as yourself, but don’t take down the fence.” — Carl Sandburg

When you’re looking for a new place to live, make sure to ask your future landlord or property management company about the local community. While you can’t pick who your neighbors are, you can ask questions to get a sense of who could be living next door.

Charlsie Niemiec has spent the last 10 years working as a content marketing and social media editor and strategist. With in-house experience ranging from The Elf on the Shelf to CNN to Piedmont Healthcare, Charlsie has freelanced for the last four years with clients ranging from ESPN to the Atlanta Beltline. When she’s not copyediting or scrolling on Twitter, she is walking her very scruffy wirehaired terriers mixes Leonard and Biscuit or probably watering one of her 54 houseplants.

By Evlin DuBose · Tuesday, 19 September 2023

· 3 min read

Fact Checked

Advertiser disclosure

House prices in Australia have been daunting for a while, but while soaring values are good for investors and owners building home equity, they’re bad news for first-home buyers.

According to Mozo’s analysis, Australians nationwide now need at least six figures in savings to afford the 20% home loan deposit required for the average mortgage. For many home buyers, this could mean saving two and a half times their yearly income.

“Despite rising interest rates historically leading to a drop in housing prices, the cost of buying a home in Australia is becoming increasingly unaffordable,” says Mozo banking and rates expert Peter Marshall.

“Borrowers are now searching for more than $100,000 to cover a 20% deposit.”

So what’s the average deposit size in Australian states and territories? And is buying with a small deposit worth it?

Average home loan deposit size by Australian state and territory

Unsurprisingly, New South Wales has the steepest home loan deposit costs. Housing markets like Sydney have significantly skewed the savings needed just to get in, and now NSW buyers need $233,500 in savings to afford a 20% deposit.

According to data from the Australian Bureau of Statistics, a deposit of this size is 245% of the average NSW annual income.

State

Average dwelling value

20% home loan deposit

Average annual income

% Average annual income

NSW

$1,167,500

$233,500

$95,259

245%

VIC

$904,800

$180,960

$95,311

189%

QLD

$781,600

$156,320

$93,132

168%

SA

$684,700

$136,940

$87,246

157%

WA

$671,000

$134,200

$106,044

127%

TAS

$662,200

$132,440

$84,204

157%

NT

$521,700

$104,340

$92,347

113%

ACT

$947,900

$189,580

$105,191

180%

But the place with the cheapest property, the Northern Territory, isn’t much better. The average property price in NT is $521,700, meaning a 20% deposit is $104,340, which is still over 110% of the average yearly earnings in the territory.

Why is the standard home loan deposit 20%?

The purpose of a 20% home loan deposit is to establish your loan-to-value ratio (LVR) and give you a financial stake in your home. The deposit pays part of the upfront property price.

If you have a 20% deposit, you own 20% of your home. A home loan covers the remainder, giving you 80% LVR.

This LVR tier is where borrowers get the most competitive interest rates. An LVR higher than 80% is financially risky in the lender’s eyes since the borrower could struggle to afford their home loan repayments.

To offset the financial risk, lenders slap buyers with smaller deposits with additional fees, such as higher interest rates and Lenders Mortgage Insurance (LMI), which can add thousands of dollars to mortgage repayments.

Lower LVRs, on the other hand, receive lower interest rates because the risk to the lender is smaller. They also don’t have to pay LMI.

You can see this play out in the latest averages for owner-occupied home loans tracked in the Mozo database. The difference below 80% is less severe. Above 80%? The interest rate skyrockets.

Average home loan interest rate by LVR tier – (19 September 2023)

LVR Tier

Average interest rate

60%

6.52% p.a.

70%

6.57% p.a.

80%

6.60% p.a.

90%

6.92% p.a.

95%

7.16% p.a.

Borrowers buying with a small deposit (< 20%) could just decide to pay the higher interest rates. However, their home loan applications will be run through serviceability tests, meaning lenders will see if they can afford principal & interest repayments at a rate up to 3% higher than the one they apply for. A 7% interest rate may be fine, but could you theoretically afford a 10% one?

Given that saving for the deposit can be a stretch, this interest rate may be a tall order – especially with average Australian incomes only ranging between $84k and $106k.

Is it a good idea to buy with a small home loan deposit?

Government schemes such as the Family Home Guarantee can help bridge the deposit gap for a select few borrowers, usually first-home buyers.

There are other options available for buying with a smaller deposit, too, such as:

Having a guarantor.

Accepting the deposit from a family or friend as a cash gift.

Using a deposit boost loan, such as through OwnHome.

The viability of these pathways will depend on your financial situation. However, there are risks to consider with each, warns Marshall.

“A [small] deposit may seem enticing, but a loan with a lower deposit will cost more in interest over the term of the loan,” Marshall explains.

“With smaller deposits, it’s also very easy for a negative equity situation to arise, so it’s crucial to get professional advice from a broker before being enticed by the low deposit amount.”

Until then, housing affordability will require governmental reform.

Can you afford a $600,000 or $750,000 home? How about $900,000? Crunch the numbers with Mozo’s home loan calculators.

Compare low-deposit home loans in the table below.

Compare low deposit home loans – last updated 19 September 2023

Search promoted home loans below or do a full Mozo database search . Advertiser disclosure

Featured Product

Unloan Variable

Owner Occupier, Refinance Only, LVR <80%

interest rate

comparison rate

Initial monthly repayment

5.74% p.a.variable

5.65% p.a.

For refinancers only. Built by CommBank, the Unloan is the first home loan with an increasing discount (conditions apply) for borrowers. No application or banking fees. No monthly account keeping or early exit fees. Apply in as little as 10 minutes.

Compare

Compare

Details Close

Unloan Variable

For refinancers only. Built by CommBank, the Unloan is the first home loan with an increasing discount (conditions apply) for borrowers. No application or banking fees. No monthly account keeping or early exit fees. Apply in as little as 10 minutes.

interest rate

5.74% p.a.variable

comparison rate

5.65% p.a.

Ongoing fees

$0.00

Discharge Fee

$0.00

Extra repayments

yes – free

Redraw facility

yes – free

Offset account

no

Maximum loan to value ratio

80.00%

minimum borrowing amount

$10,000

maximum borrowing amount

$10,000,000

type of mortgage

Variable

Repayment types

Principal & Interest

Availability

Owner Occupier

Repayment options

Weekly, Fortnightly, Monthly

Special Offers

–

Own Home Loan

Owner Occupier, Principal & Interest, LVR <80%

interest rate

comparison rate

Initial monthly repayment

5.94% p.a.variable

6.18% p.a.

Competitive variable rate. Multiple offset accounts available. Borrowers can also make extra repayments. Redraw facility available. Simple online application process.

Compare

Compare

Details Close

Own Home Loan

Competitive variable rate. Multiple offset accounts available. Borrowers can also make extra repayments. Redraw facility available. Simple online application process.

interest rate

5.94% p.a.variable

comparison rate

6.18% p.a.

Ongoing fees

$250.00 yearly

Discharge Fee

$300.00

Extra repayments

yes – free

Redraw facility

yes – free

Offset account

yes

Maximum loan to value ratio

80.00%

minimum borrowing amount

–

maximum borrowing amount

–

type of mortgage

Variable

Repayment types

Principal & Interest

Availability

Owner Occupier

Repayment options

Weekly, Fortnightly, Monthly

Special Offers

–

Express Home Loan

Owner Occupier, Principal & Interest, LVR <90%

interest rate

comparison rate

Initial monthly repayment

5.72% p.a.variable

5.87% p.a.

Get fast online approval from the award-winning Bendigo Bank Express Home Loan. Multiple offset accounts and redraw available. 100% offset on variable rate loans and partial offset on fixed rate. Flexible repayment options. New home loans only.

Compare

Compare

Details Close

Express Home Loan

Get fast online approval from the award-winning Bendigo Bank Express Home Loan. Multiple offset accounts and redraw available. 100% offset on variable rate loans and partial offset on fixed rate. Flexible repayment options. New home loans only.

interest rate

5.72% p.a.variable

comparison rate

5.87% p.a.

Ongoing fees

$10.00 monthly

Discharge Fee

$350.00

Extra repayments

yes – free

Redraw facility

yes – free

Offset account

yes

Maximum loan to value ratio

90.00%

minimum borrowing amount

$5,000

maximum borrowing amount

$3,000,000

type of mortgage

Variable

Repayment types

Principal & Interest

Availability

Owner Occupier

Repayment options

Weekly, Fortnightly, Monthly

Special Offers

–

Variable Home Loan 90

Principal and Interest, LVR <90%

interest rate

comparison rate

Initial monthly repayment

5.79% p.a.variable

5.81% p.a.

Affordable home loan rate for buyers or refinancers.. No monthly or ongoing fees. Option to add an offset for 0.10%. Access to savings with unlimited redraws available. Minimum 10% deposit required.

Compare

Compare

Details Close

Variable Home Loan 90

Affordable home loan rate for buyers or refinancers.. No monthly or ongoing fees. Option to add an offset for 0.10%. Access to savings with unlimited redraws available. Minimum 10% deposit required.

interest rate

5.79% p.a.variable

comparison rate

5.81% p.a.

Ongoing fees

$0.00

Discharge Fee

$0.00

Extra repayments

yes – free

Redraw facility

yes – free

Offset account

yes

Maximum loan to value ratio

90.00%

minimum borrowing amount

$50,000

maximum borrowing amount

$2,000,000

type of mortgage

Variable

Repayment types

Principal & Interest

Availability

Owner Occupier

Repayment options

Weekly, Fortnightly, Monthly

Special Offers

–

Home Variable Rate

Owner Occupier, Principal & Interest, Refinance Only

interest rate

comparison rate

Initial monthly repayment

5.90% p.a.variable

5.90% p.a.

Enjoy a competitive variable interest rate from Up. No application, monthly, annual, redraw, or discharge fees to pay. Up to 50 free offset accounts available. Up home loans are only available to owner-occupiers buying or refinancing in major Australian cities. Up is 100% owned by Bendigo Bank. New joiners get $10 by signing up to the app using code UPHOMEMOZO. (T&Cs apply) Mozo Experts Choice award winner.

Compare

Compare

Details Close

Home Variable Rate

Enjoy a competitive variable interest rate from Up. No application, monthly, annual, redraw, or discharge fees to pay. Up to 50 free offset accounts available. Up home loans are only available to owner-occupiers buying or refinancing in major Australian cities. Up is 100% owned by Bendigo Bank. New joiners get $10 by signing up to the app using code UPHOMEMOZO. (T&Cs apply) Mozo Experts Choice award winner.

interest rate

5.90% p.a.variable

comparison rate

5.90% p.a.

Ongoing fees

$0.00

Discharge Fee

$0.00

Extra repayments

yes – up to $30,000

Redraw facility

yes – free

Offset account

yes

Maximum loan to value ratio

90.00%

minimum borrowing amount

$50,000

maximum borrowing amount

$10,000,000

type of mortgage

Variable

Repayment types

Principal & Interest

Availability

Owner Occupier

Repayment options

Monthly

Special Offers

–

*

WARNING: This comparison rate applies only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan. The comparison rate displayed is for a secured loan with monthly principal and interest repayments for $150,000 over 25 years.

**

Initial monthly repayment figures are estimates only, based on the advertised rate. You can change the loan amount and term in the input boxes at the top of this table. Rates, fees and charges and therefore the total cost of the loan may vary depending on your loan amount, loan term, and credit history. Actual repayments will depend on your individual circumstances and interest rate changes.

^See information about the Mozo Experts Choice Home Loan Awards

Mozo provides general product information. We don’t consider your personal objectives, financial situation or needs and we aren’t recommending any specific product to you. You should make your own decision after reading the PDS or offer documentation, or seeking independent advice.

While we pride ourselves on covering a wide range of products, we don’t cover every product in the market. If you decide to apply for a product through our website, you will be dealing directly with the provider of that product and not with Mozo.

Buying insurance coverage helps keep you protected from the full financial fallout of an accident or injury. But even with insurance, you’ll probably still be responsible for some costs when you file a claim.

An insurance deductible is the amount of money the insured party is responsible for at the time of loss or damage: it’s the cost you have to pay before the insurance company pays out its share.

Here’s what you need to know about the different types of insurance deductibles and other insurance-related costs you may face.

What Is a Deductible?

When you buy insurance, you’ll encounter several different costs depending on the type of coverage you’re purchasing. These may include monthly premiums, copays, out-of-pocket maximums, and possibly others.

The vast majority of insurance policies, whether they’re auto, health, or homeowners, carry a deductible. So what is a deductible, and how does it work?

The deductible is a sum of money you, as the insured party, are expected to pay toward a loss. Another way to think about it: It’s the amount the insurance company deducts from the total claim and asks you to pay.

For instance, say you get into a car accident in which you sustain $8,000 worth of damage and you have a $1,000 deductible. When you file your claim, you’ll pay $1,000 toward repairs and the insurance company will cover the remaining $7,000 (or up to whatever limits are laid out in your insurance contract).

Your deductible can be a fixed dollar amount or a percentage, depending on your individual plan and the kind of insurance policy you’re talking about. Homeowners insurance, for instance, is commonly offered with deductibles calculated as a percentage of the property’s total insured value.

It’s important to understand that your deductible is separate from your premium, which is the amount of money you pay each month in order to keep your insurance policy active.

Also remember that you may also be responsible for other insurance-related expenses, like copays or coinsurance, so always read the fine print carefully. 💡 Quick Tip: If you have a mortgage, a homeowners policy may be required by your lender. Surprisingly, unlike auto insurance, there is no legal mandate to carry insurance on your home.

Copay vs Deductible

With certain types of insurance — primarily health insurance products — you may be required to pay a copay each time you go to the doctor’s office or receive a covered service. This copay is separate from your deductible, and, generally, your copay doesn’t count toward your deductible amount.

As with other types of insurance, the health insurance deductible must be paid by the insured person before the insurance company begins its coverage. However, individual health plans may cover certain services, such as regular check-ups, even before the deductible is paid in full.

Here’s an example: Say you twist your ankle and visit your doctor, who orders an MRI. If your copay is $25, you’ll pay $25 at the office before or after you see your physician. If the total cost of the doctor’s care and imaging services is $1,000 and you have a $500 deductible, you may still be responsible for the full $500. Any copays you’ve paid along the way won’t be subtracted from your deductible.

Some plans may carry a coinsurance cost rather than a copay. The two are similar, but not identical. Coinsurance is an amount you pay when you receive a medical service, separate from your deductible. Unlike copays, which are charged at a fixed dollar amount, coinsurance is calculated as a percentage of the total cost of the service. Your plan might even include both copays and coinsurance.

All insurance policies are different, and your individual costs and experience may vary depending on the services you’ve received and the specific coverage you have. You can consult your insurance paperwork or contact your insurer for full details on what’s covered in your plan.

Out-of-Pocket Maximums

Health insurance policies in particular are subject to federally mandated out-of-pocket maximums. This is the highest total dollar amount you’ll have to pay toward covered healthcare over the course of a single year, including both deductibles and copays.

The out-of-pocket maximum does not include the amount you pay toward your monthly premium, however. Nor does it include out-of-network services or services that your plan expressly does not cover.

For 2023, the out-of-pocket maximum for a Marketplace plan can’t be more than $9,100 for an individual or $18,200 for a family. In 2024, that limit rises to $9,450 for an individual or $18,900 for a family. (The maximum is allowed to be lower, however, so consult your plan paperwork for full details.)

Do You Want a High or Low Deductible?

When shopping for insurance coverage, you’ll likely have a range of options to consider, including varying deductible costs. And when it comes to figuring out whether you want a high or low deductible, the answer is: It depends.

Generally speaking, the lower your deductible, the higher your premium will be and vice versa. This makes sense when you think about it. If you have a low deductible, the insurer will have to pay out a higher amount when you incur a loss. So in exchange for the promise of covering most of the costs when a claim is filed, the company expects you to pay more up front in the form of a higher premium.

While choosing a higher deductible can help you save money over time since your monthly premiums will be lower, it also means you’re assuming more risk. If something happens and costs are incurred, you’ll be responsible for a larger share of those expenses.

On the other hand, choosing a lower deductible means you’ll likely pay a higher premium each month. But you’ll also have less to worry about if you do need to file a claim, since the insurance company will cover more of the costs (assuming that all the damages and expenses are covered under your policy).

As with so many other financial matters, what’s right for you comes down to a number of factors, including your risk tolerance, budget, and even your lifestyle. If you participate in extreme sports, for instance, and are at risk for catastrophic injuries, you might want to pick a health insurance policy with a lower deductible and higher premiums.

Recommended: How Much Is Homeowners Insurance?

Zero-Deductible Insurance: Is It a Thing?

You may see ads for zero-deductible insurance policies and wonder if they’re too good to be true. While zero-deductible insurance policies do exist, they usually carry higher premiums than policies that do carry deductibles, and you may also be responsible for a one-time no-deductible fee or waiver.

Furthermore, some insurance coverages are required by state law to carry a minimum deductible, particularly when it comes to auto insurance.

Before you sign up for any kind of insurance coverage, be sure to read the contract thoroughly to ensure you understand what costs you’re responsible for.

Recommended: What Does Auto Insurance Cover?

Types of Deductibles

There are many different types of insurance policies with deductibles on the market. Common ones include:

• Health insurance deductibles

• Auto insurance deductibles

• Homeowners insurance deductibles

• Renters insurance deductibles

• Life insurance deductibles

The deductible amount varies by type of insurance, company, and plan, among other factors. 💡 Quick Tip: Online insurance tools allow you to personalize your coverage for homeowners, renters, auto, and life insurance — all with zero paperwork.

The Takeaway

Purchasing insurance is an important — and sometimes legally mandated — step toward protecting yourself from the high costs of personal accidents, property damages, and medical bills. But most policies involve set costs, including deductibles. This is the portion of the claim the insured party is responsible for paying.

Whether you’re comparison shopping or switching from your current plan, it’s important to understand what your deductible will be. Having a full picture of all the costs involved can help you find coverage that fits your life and finances.

When the unexpected happens, it’s good to know you have a plan to protect your loved ones and your finances. SoFi has teamed up with some of the best insurance companies in the industry to provide members with fast, easy, and reliable insurance.

Find affordable auto, life, homeowners, and renters insurance with SoFi Protect.

Insurance not available in all states. Experian is a registered service mark of Experian Personal Insurance Agency, Inc. Social Finance, Inc. (“SoFi”) is compensated by Experian for each customer who purchases a policy through Experian from the site.

Coverage and pricing is subject to eligibility and underwriting criteria.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers- for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products.

Ladder, SoFi and SoFi Agency are separate, independent entities and are not responsible for the financial condition, business, or legal obligations of the other, Social Finance. Inc. (SoFi) and Social Finance Life Insurance Agency, LLC (SoFi Agency) do not issue, underwrite insurance or pay claims under Ladder Life™ policies. SoFi is compensated by Ladder for each issued term life policy.

SoFi Agency and its affiliates do not guarantee the services of any insurance company.

All services from Ladder Insurance Services, LLC are their own. Once you reach Ladder, SoFi is not involved and has no control over the products or services involved. The Ladder service is limited to documents and does not provide legal advice. Individual circumstances are unique and using documents provided is not a substitute for obtaining legal advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.

Furnished Finder is where we decided to list our room, which started out as a platform for traveling nurses to find furnished housing. It is now used heavily by many healthcare professionals, students, and professionals in other fields.

Travelers reach out to us through the Furnished Finder website and if the dates work out, we move forward with scheduling a video interview. It’s important for us to be able to talk to the person, even if it’s just over video, and we want them to see our faces and home in real time as well.

For the lease agreement, we used ez Landlord Forms, because they have leases for each state with specific information on what’s required to include.

We don’t ask for anything major from tenants. The most important things to us are that they are respectful of our space, don’t smoke in the house, and pay their rent on time. We also added a page at the end for tenants to add two emergency contacts in case we need to call someone on their behalf.

We have had 4 renters so far with the room being occupied for 13 out of the last 14 months. It has really helped us with our debt payoff goals and we have also met some awesome people through the process! We plan to continue renting it out for the foreseeable future.

Applied for in-state student loan help

My state offered a program called the Oregon Behavioral Health Loan Repayment Program where they help minorities in the behavioral health field, or those who serve them, pay back their student loans.

This program is funded by The Behavioral Health Workforce Initiative which has the goal of recruiting and retaining behavioral health providers who, “Are people of color, tribal members, or residents of rural areas of Oregon, and can provide culturally responsive care for diverse communities.”

To apply, I had to show I was employed and actively providing behavioral health services and give them detailed documentation about my student loans. I also had to answer two essay questions related to being a part of and/or working with communities who are underserved and how my training has equipped me with supporting these communities.

I applied last year and was a recipient of an award!

As a recipient, there is a two-year service commitment which means I have to continue providing some sort of behavioral health service during that time frame (which I planned to). Over the next two years, I will be getting ~$88,000 in quarterly disbursements to put towards my student loans. So far this year, I have received ~$11,000, and it’s been life changing to say the least!

Alongside this support, I am also pursuing Public Service Loan Forgiveness (PSLF) for additional student loan relief.

Managing our mental health while paying off debt

Since I am a social worker, I often think about how money and debt affect individuals’ mental health. It’s one of the reasons why I started my blog in the first place.

I realized managing money is a universal task and many of us don’t know what we are doing because talking about money is taboo. And when you have financial stress, it can really take a toll on your mental health. So, I wanted to share our journey in hopes of helping others.

Bret and I aren’t those individuals who want to avoid eating out and fun experiences until we are debt free. And, we are also privileged to not have to take those extreme measures either. It has been important for us to make this journey sustainable and not deprive ourselves of experiences while we are going through it.

Here’s how we are making our journey sustainable:

Still going out to eat

Budgeting for personal spending money, aka fun

Setting realistic debt payoff goals

Putting aside money for travel

Not comparing and thinking other people are better than us because they’re able to pay off their debt quicker

Tracking our debt payoff progress (we use Excel). With so much debt left to pay off, being able to see our progress is really motivating

Openly talking about our debt. Avoidance is a coping mechanism for many, for us, acknowledging and addressing it has been so freeing (but it wasn’t always this way).

Talking about our dreams and reminding ourselves why we want to do this in the first place

We know that if we eliminated going out to eat, budgeting for fun, or both, we could be paying off our debt much quicker. However, that sounds miserable to us. It’s worth it to still go out to dinner, travel, or buy plants (in my case) than to deprive ourselves of the joy these things bring.

We are making great progress and we know in time, we will be debt free.

Our debt payoff journey is not linear

A few months ago, we decided to take out $6,000 of student loans. Bret currently has a full tuition scholarship, so we are tremendously lucky in that regard, but he just learned about some conferences that would be really helpful to his professional growth. We have gotten $1,500 of this loan money already which is included in our current debt balance, but we haven’t received all of it yet.

We could have pinched and saved to avoid taking on any of this debt, but that would have caused me to work more than I currently am. Again, not in line with our current goal of making this journey sustainable!

We were very intentional about how much to take out. We estimated how much he would need for a few conferences and declined the rest. We even opened a separate savings account for the money to make sure it didn’t get accidentally spent on anything.

I’m SO proud of us for that!

The goal here is progress not perfection. So cliche, I know. But we are learning how to think critically about our money, spend thoughtfully, use our money as a tool to reach our goals, and enjoy our life along the way. And right now, that meant taking on a little more debt.

We are moving in the right direction, and we know when he starts working, that will really accelerate our debt payoff journey since we have proven to ourselves we can live on my income alone.

Our plan going forward

Bret is still in school which means his loans are on deferment, so we currently have his on the back burner.

With the loan payment assistance I am receiving, it’s allowing us to put any extra money we have each month towards our savings. Our priority right now is building up a good emergency fund of about $16,000 (~4 months’ worth of expenses).

This has been difficult because of inflation and just little emergencies that keep popping up, but we are slowly making progress.

I am also prioritizing investing in my employer retirement plan, but only up to the amount that gets me my employer match which is 6% of my income.

Bret will be graduating in 2025, so at that time, we will pivot to incorporating his loans into our budget. Our goal is to be debt free by 2028.

It will take a lot of discipline and persistence, but I think we can do it. I am manifesting it!

We want to continue to learn, implement, and grow. We want to keep having transparent discussions about money and building our money foundations. And I personally want to continue sharing our journey with hopes of inspiring, encouraging and educating others. Here’s to sharing the wealth.

Do you have debt? What are you doing to pay it off?

Taylor is a social worker and personal finance blogger at Social Work to Wealth where she shares tips, resources, and lessons learned on her family’s journey to paying off $277,000 of debt and retiring early. She hopes to inspire and empower social workers with financial education so they can have a better relationship with their money. When she’s not working or blogging, you can find her traveling, gardening, trying a new restaurant, or buying too many plants.

In the world of real estate, where property expertise reigns supreme, it comes as little surprise that the most successful real estate agents own some of the most remarkable and envy-inducing residences.

With their extensive knowledge of market trends and investment potential — not to mention their keenly trained eye for luxury living — real estate pros are the first to spot desirable properties, often before they are even listed for the general public to see.

They then leverage their design expertise and Rolodex of industry connections to turn their homes into personal sanctuaries that serve as living testaments to their industry acumen and discerning tastes.

Such is the case of Billy Rose, realtor to the stars and co-founder of luxury real estate brokerage, The Agency.

Rose, rated as one of the best real estate agents in Los Angeles (and the entire country, once being named the Number 10 real estate agent in the U.S. by The Wall Street Journal), owns an architecturally distinct home in one of Los Angeles’ best areas, which he’s now bringing to market.

Priced at $5,895,000, the elegant abode has served as Billy Rose’s personal residence for 20 years.

Located in the sought-after Westword neighborhood, the property sits on the “first lot bought in highly coveted Westwood Hills”, per the listing, and is known as the Murrow Residence, named after its original owners.

Rose himself provided a little bit of background on the home’s history.

“The Murrows considered the lot to be the trophy of Westwood Hills,” Billy Rose tells us. “Mr. Murrow, for whom the home was built, was (as I understand it) a bit of a “mucky muck” at the Rand Corporation. He had rigged the front door such that he could attach a 35mm projector to the door and project through to the living room.“

But it’s not just the location that appealed to The Agency co-founder.

The home’s distinct design played a big role too. The 1940-built residence is an outstanding example of International Style architecture (post Deco and pre Mid-Century Modern).

Photo credit: The Agency

“I find International Style architecture to be sublime,” Billy Rose shared in an exclusive comment for Fancy Pants Homes. “The style is best described as stripped of all unnecessary ornamentation and about accentuating the strengths of the home (the view, the layout, the light, the circulation, the air flow). Le Corbusier (one of the pioneers of what is now regarded as modern architecture) summed it up best when he called a house a “machine for living”.“

Vintage and collectible lighting, designer finishes, and terrazzo and custom-milled walnut floors complement the home’s unique style, while broad expanses of glass in every direction bring the outdoors in.

Photo credit: The AgencyPhoto credit: The AgencyPhoto credit: The Agency

The house has a total of 5 bedrooms — all suites — with the primary being touted as “one of the best primary suites in its class with extremely generous dual closets and baths”, per the listing.

Photo credit: The AgencyPhoto credit: The AgencyPhoto credit: The Agency

The inviting chef’s kitchen has its own claim to fame.

“My wife is a chef and she filmed her show “Taste of Melrose” from there,” shared Rose whose wife, model-turned-chef Melissa Rose, has been filming her cooking show in their camera-ready kitchen for years.“It was not only a great exhibition kitchen, but it served us well for our numerous dinner parties.”

Photo credit: The AgencyPhoto credit: The AgencyPhoto credit: The Agency

When prompted to pick his favorite area of the house, The Agency co-founder signaled out the primary bedroom suite, along with “the original stairway, with its two-story Torrance steel window system“, which he says was one of the things that drew him to the property.

Photo credit: The Agency

Heading outside, we find a secluded backyard oasis with a cascading pool, spa, fire pit, grassy yard, dining and lounging areas, with mature landscaping, tall hedges, and privacy walls shielding it from prying eyes.

Photo credit: The AgencyPhoto credit: The Agency

Unsurprisingly, Billy Rose holds the listing along with Stefan Pommepuy, also with The Agency.

And while Rose hasn’t yet been part of the cast of Buying Beverly Hills, the Netflix series starring agents from the luxury real estate brokerage he co-founded alongside Mauricio Umansky, we’re hoping his house will — and that the second season of the show will give us a better look inside his inviting abode.

More stories

This charming storybook cottage nestled under the iconic Hollywood sign will take you back to the early days of Hollywoodland

Home of the Week: Architect Harry Gesner’s personal home, the $22.5M Sandcastle House

An artist’s escape: Donald (@drawbertson) Robertson’s picture-perfect house in Montecito

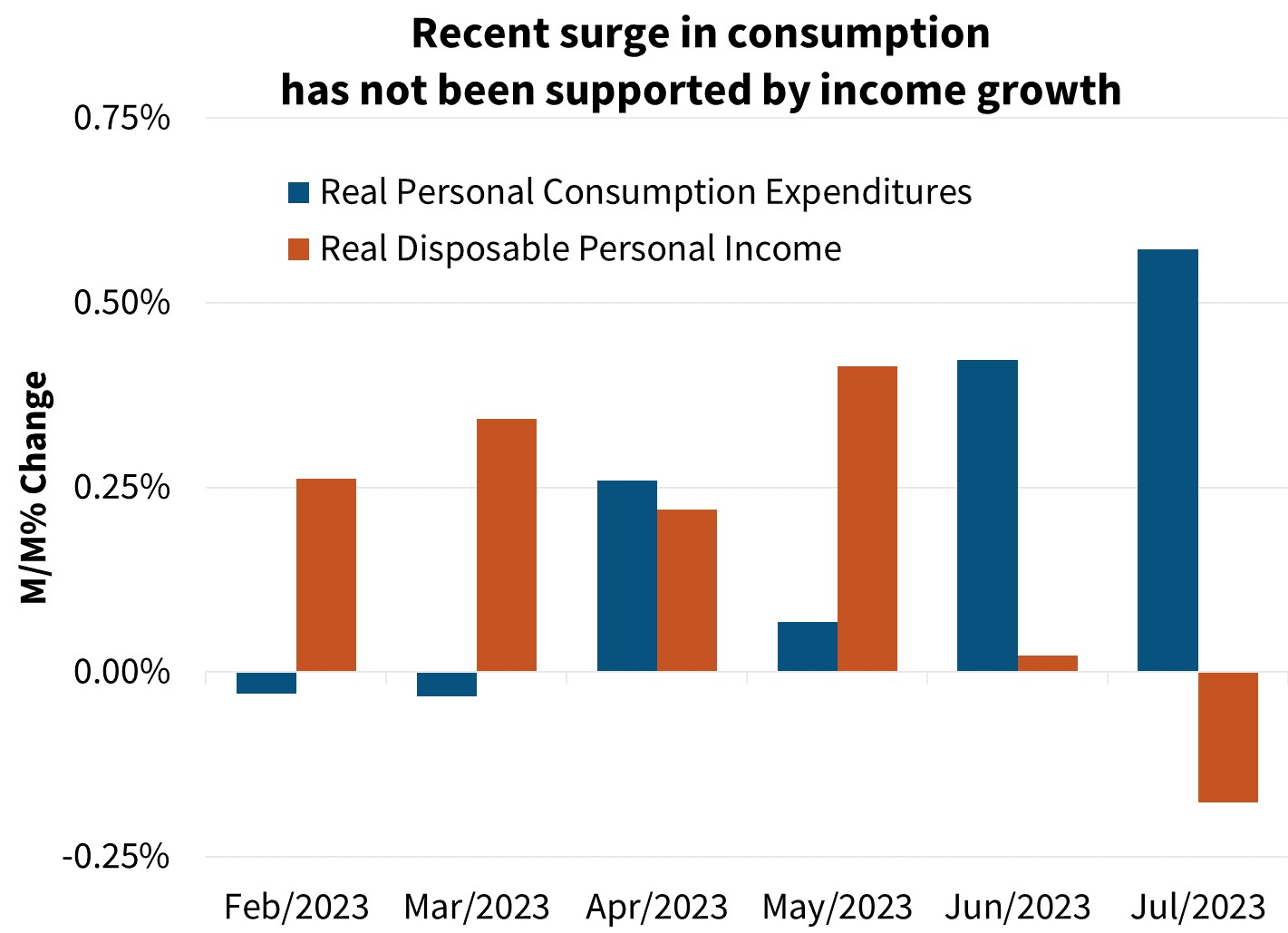

We maintain our forecast for a modest economic contraction in the first half of 2024. Fundamentally, personal consumption remains at what we believe to be an unsustainable level relative to incomes, and the full effects of monetary policy tightening are still working through the economy. We have upgraded our 2023 real GDP growth outlook to 2.2 percent from 1.9 percent on a Q4/Q4 basis largely due to incoming July data, while our forecast for growth in 2024 is unchanged. Meanwhile, we forecast the topline and core measures of the Consumer Price Index (CPI) to end the year around 3.1 percent and 4.0 percent in 2023, respectively, slowing further in 2024 to 2.4 percent and 2.5 percent.

With the jump in mortgage rates to above 7 percent, the housing market faces renewed headwinds. Mortgage origination activity has slowed further in recent weeks and total home sales remain at levels not seen since 2011. The new home market, which showed surprising strength over the first half of 2023, due in part to a limited inventory of existing homes for sale, may now be taking a breather. We forecast total home sales to be around 4.8 million in 2023, which would be the slowest annual pace since 2011 and 4.9 million in 2024. Similarly, our expectation for 2023 mortgage originations was downgraded from $1.60 trillion to $1.56 trillion in 2023 and from $1.92 trillion to $1.88 trillion in 2024.

Q3 GDP Growth Poised to Accelerate, but Strength is Likely Temporary The third quarter started off on a strong note, with real personal consumption jumping 0.6 percent month over month in July, pointing to a stronger Q3 2023 GDP growth figure than previously anticipated. Even if personal consumption expenditures were to remain flat over the next two months, July’s growth alone would translate into a pace of personal consumption over the quarter of around 3.8 percent annualized. However, this surge in spending is likely unsustainable and our outlook is for decelerating activity. We believe much of the July consumption was the result of pulling forward future spending in part due to a combination of the release of popular movies and concerts as well as an increase in spending on energy during the July heat waves, and perhaps due to seasonal timing related to online retailer sales. Both recent credit card transaction data and auto sales data point to a likely pullback in consumption in August, with auto sales falling 4.6 percent month over month. August nominal retail sales jumped by 0.6 percent, but this was almost entirely due to price increases in gasoline. Control group retail sales, which feed into the GDP report, rose by only 0.1 percent in nominal terms, suggesting flat or slightly declining real sales. Furthermore, the 0.6 percent pop in real consumption in July came despite a decline of 0.2 percent in real disposable income, increasing the divergence between the two series. Recent spending growth has come via a further reduction in the already below-trend personal saving rate to 3.5 percent in July. This was down from 4.3 percent in June and around an average of 8.0 percent from 2017 to 2019. Especially when accounting for an expected deceleration in wage growth, we expect more modest consumer spending growth in coming quarters.

Refinance Application-Level Index (RALI), remains depressed given that mortgage rates remain above the 7 percent level.

Economic & Strategic Research (ESR) Group September 14, 2023 For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR’s Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Mortgage Bankers Association, National Association of REALTORS®, Fannie Mae

Opinions, analyses, estimates, forecasts and other views of Fannie Mae’s Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae’s business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

Student loans can help you finance your college education without paying much interest. However, you don’t want to take on more debt than you can comfortably pay back after you graduate. As of June, 2023, student borrowers owe 1.76 trillion in student loan debt, including federal and private student loans, according to the Federal Reserve.

High school can be a great time to start learning about the types of student loans available to you, how interest accrues, and what you can expect when it comes time to repay any student loans you take out. Read on to learn some of the ABCs of student loans, and how to not let them weigh down your financial future.

Student Loan Types

There are two main categories for student loans: federal and private student loans.

Federal Student Loans

Federal student loans are funded by the federal government. Interest rates are fixed (and comparatively fair) and are set annually by Congress every July. Federal student loans also come with protections like income-driven repayment plans and deferment or forbearance options in the case of life changes, such as sudden loss of a job or other roadblocks to repayment.

The following are the federal student loan options offered:

• Direct Subsidized Loans These are available to eligible undergraduates with a proven financial need. The government subsidizes (meaning it pays for) the interest that accrues on these loans while the student borrower is enrolled in school at least half-time and during the loan’s grace period (more on that below), and other qualifying periods of deferment.

• Direct Unsubsidized Loans These are available to eligible undergraduates and graduate students regardless of financial need. Student borrowers are responsible for paying all of the accrued interest on unsubsidized student loans.

• Direct PLUS Loans These are available to eligible parents of undergraduate students and to graduate or professional students. They are not subsidized by the government.

Private Student Loans

Private student loans are issued by non-government institutions, such as banks, credit unions, and online lenders. The requirements for applying for these types of loans may be more stringent.

Lenders will typically look at the student’s or their cosigner’s credit history, income, and other financial information. Some lenders require you to begin making payments while you are in school, while others allow you to wait until six months after you graduate. Either way, interest typically begins to accrue as soon as the funds are disbursed.

How to Apply for a Student Loan

The process for applying for student loans varies based on whether the loan is private or federal.

Applying for a Federal Student Loan

To apply for a federal student loan, you need to fill out and submit the Free Application for Federal Student Aid (FAFSA®) . Even if you don’t think you’ll be approved for financial aid, it can be worth submitting the FAFSA. The application is free and you may qualify despite your circumstances. The FAFSA also gives you access to federal student loans.

Every year, the FAFSA form usually becomes available online as of October 1 for the next school year. (Note that the FAFSA for 2024-25 academic year won’t be available until December 2023 due to the roll out of a new, more simplified form.)

You can easily apply online (see the link above). Completing the FAFSA determines the combination of federal loans, grants, and work-study you’re eligible for. Some colleges and universities also use information from the FAFSA to determine if you qualify for school-specific financial aid.

Applying for a Private Student Loan

It’s important to take the time to do some research and find a lender with a good reputation that offers competitive rates and terms. Ideally, you want a lender that offers flexible repayment options, reasonable (or no) fees, and will provide helpful customer support if you find yourself having any issues with your student loan payments.

If you decide to apply for a private student loan, you will more than likely have to reveal personal financial details, like your credit history. Since students typically don’t have much, or any, credit history, they often need to apply with a cosigner. That’s someone who will share the responsibility with you of paying back the loan.

In many cases, that cosigner would be a parent or an adult with whom you have a close relationship. Getting a cosigner may increase your chances of getting a better interest rate, which could help you spend less in interest over the life of the loan.

[embedded content]

Types of Student Loan Interest Rates

The interest rate on your student loans could have a lasting impact on your future finances. The interest charged is a percentage of your unpaid loan principal — that is, the amount you borrowed. Interest is paid to the lender in exchange for the opportunity to borrow money from them.

You can typically choose from between two types of interest rates: fixed-rate and variable rates.

Fixed-rate student loans: These types of loans offer an interest rate that remains the same throughout the life of the loan. This could give you peace of mind, knowing that the rate won’t change, even if the state of the economy does. Interest rates could fluctuate wildly during the course of your loan, but a fixed-rate won’t be affected. As previously mentioned, federal student loans have a fixed interest rate. Some private lenders also offer student loans with a fixed interest rate.

Variable-rate loans: These types of loans come with an interest rate that can increase or decrease based on market fluctuations. Some private lenders offer student loans with variable interest rates. These are also sometimes called floating-rate loans, because the interest rate can change during the life of the loan.

A variable-rate school loan might start with a lower rate than a fixed-rate loan but keep in mind that your interest rate — and monthly payment — could rise later on. A variable- rate loan can make sense if you plan to pay off your student loan early before rates have a chance to rise too much, expect rates to fall in the future, or you have some wiggle room in your budget in case of rising interest rates.

Student Loan Mistakes to Avoid.

1. Failing to Research Your Loans

With any type of student loan, it’s key to understand what you are agreeing to. You’ll want to make sure you understand what the interest rate will be, what your monthly payment will be, when you’ll need to start repayment, and how you plan to cover that obligation.

2. Borrowing Too Many Loans

It’s nice to be approved and accepted, but too many loans (borrowing more money than you actually need) can lead to a heavy financial burden after graduation. Generally, you’ll want to use any college savings, financial aid, and federal student loans before looking to private student loans (which tend to come with higher interest rates than federal student loans). If you’ll need to take on significant debt to attend a certain school, you might consider choosing a less expensive institution.

3. Not Having a Plan

Life can be unpredictable. The one thing you could have power over is your school loan repayment plan. It’s important that you know exactly when your student loan repayment plan starts (in some cases, that could be before you graduate), and exactly what your monthly payment will be.

It can also be helpful to set up a budget that accounts for all of your college costs, including tuition, books, room and board, food expenses, and anything else related directly to your education. If you budget for it ahead of time, you can help make it easier to use your student loan money wisely.

4. Not Realizing That Interest Continues Accruing

Understanding how and when interest accrues on your student loans is critical. For many student loans, interest will accrue while you are in school and during your grace periods. (A grace period is the period of time after you graduate or drop down below half-time attendance, during which you are not required to make payments.)

With the exception of subsidized federal student loans, interest will continue to accrue even if you are not making payments on your student loan. It will then typically be capitalized. Capitalization occurs when the accrued interest is added to the principal balance of the loan (the original amount borrowed). This new value becomes the balance on which interest is calculated moving forward.

Recommended: Understanding Capitalized Interest on Student Loans

Repaying Your Student Loan

Another important factor is understanding what repayment plans are available to you based on the type of loan you borrowed.

Repaying Federal Loans

For Direct Subsidized and Unsubsidized Federal Loans, students who are enrolled in school at least half-time aren’t required to make payments on their student loans. On these loans, repayments officially begin after the loan’s grace period.

Federal loans typically have a six-month grace period after graduation, which allows you time before you have to start repaying your loans. It’s important to note that even though you may be granted a grace period, depending on the loan you have, you may still be responsible for paying the interest on the loan during the time you are not making payments.

Note that PLUS Loans, which are available to parents of students and graduate or professional students, require repayments as soon as the loan is disbursed (or paid out).

Borrowers with federal loans are able to choose one of the federal repayment plans . These include:

• Standard Repayment Plan On this plan, monthly payments are a fixed amount and repayment is set over a 10-year period.

• Graduated Repayment Plan On this plan, payments start out on the lower end and then gradually increase as repayment continues. Loans are generally paid off over a 10-year period.

• Extended Repayment Plan Payments may be either fixed or may gradually increase over the loan term. Loans are paid off within 25 years.

• Income-Driven Repayment Plans There are four income-driven repayment plans. These tie payments to the borrower’s discretionary income. The percentage and repayment term may vary depending on the type of income-driven repayment plan the borrower is enrolled in.

With private student loans, the repayment terms are determined by the lender. That schedule will tell you exactly when your first payment is due and how much you will owe.

Unlike federal loans, many private loans have to be paid back before you graduate, so be sure to review your agreement closely and know exactly what you are going to need to do. Contact the lender directly if you have any questions.

Recommended: How to Pay Off College Loans

Named a Best Private Student Loans Company by U.S. News & World Report.

If Repaying Loans Becomes a Problem

Nobody plans on not paying back their student loans, but sometimes life can throw a few financial punches that you weren’t expecting. A smart strategy if this were to happen to you: face the problem head-on.

Options for Federal Student Loans

If a borrower is struggling to make payments on their federal student loans, they may consider changing their repayment plan. Federal loans, as mentioned, offer income-driven repayment options which tie the monthly payments to the borrower’s income. This can help make monthly payments more manageable for borrowers.

In cases when even income-driven repayments are too much, borrowers may be able to apply for deferment or forbearance. These allow borrowers to pause their loan payments. Depending on the loan type, you may or may not accrue interest during periods of deferment or forbearance.

Options for Private Student Loans

Private lenders are not required to offer the same repayment plans or borrower protections (like deferment and forbearance, mentioned above) as federal student loans. Some private lenders may be willing to work with you during times of financial difficulty so that you can continue making payments. Check in directly with your lender to see what payment plans or options they may have available to you.

A Note on Student Loan Default

After a certain number of missed payments (which can vary depending on whether you have borrowed a federal or private student loan), your loan may enter default. That can have serious financial consequences, such as impacting your credit score.