Outspoken FDIC Chairman Sheila Bair today announced a loan modification plan for troubled Indymac borrowers who are currently behind on their mortgage payments.

The aim of the program is help struggling borrowers get back on track with affordable mortgages while increasing the value of Indymac’s mortgage portfolio for the sake of its outstanding creditors (what is a loan modification program?).

“I have long supported a systematic and streamlined approach to loan modifications to put borrowers into long-term, sustainable mortgages—achieving an improved return for bankers and investors compared to foreclosure,” said Chairman Bair.

“The program we are announcing today will provide affordable mortgages for eligible borrowers primarily in the so-called ‘Alt-A‘ market. It provides a systematic approach for modifying troubled loans with payment resets due to negative amortization and other resets — a market where we are seeing growing defaults and foreclosures.”

Under the Indymac Federal Bank loan modification program, eligible mortgages will be modified into fixed mortgages capped at the current Freddie Mac survey rate for conforming mortgages.

Monthly mortgage payments will be designed to achieve a sustainable debt-to-income ratio of 38 percent (income must be verified), which may involve interest rate reductions, extended amortization, and principal forbearance.

Mortgage rates below the current Freddie Mac surveyed rate may be made for up to five years if necessary to keep the DTI at acceptable levels, with annual interest rate caps of no more than one percent, up until the current survey rate.

Indymac will only provide loan modifications to borrowers when doing so will benefit Indymac Federal or its investors.

An estimated 4,000 modification proposals will be sent to borrowers this week, with those most severely delinquent or in default served first.

“Our goal is to get the greatest recovery possible on loans in default or in danger of default, while helping troubled borrowers remain in their homes. I believe we achieve that with this framework,” Bair concluded.

Several years ago, when the mortgage crisis first materialized, an interest rate reset chart from Credit Suisse began circulating on the Internet.

The picture said more than a thousand words – it essentially foretold disaster for the housing market, and it largely delivered.

Fast forward to 2013, and you’d think we’d be out of the woods, seeing that the chart was from all the way back in 2007.

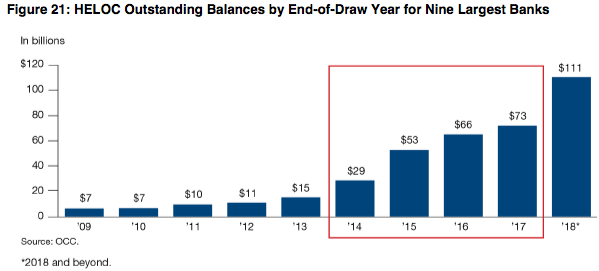

But there is yet another wave of resets on the horizon, and this time it’s home equity lines of credit (HELOCs).

More 10-Year Draw Periods End in 2014

Most HELOCs are designed so a homeowner can draw from the line of credit for the first 10 years, and then pay back the balance during the following 15 years.

To further accommodate homeowners, the initial 10-year draw period allows for interest-only payments. And people tend to like to make smaller payments.

Per a new report from Fitch Ratings titled, “U.S. Banks – Home Equity ReSet Risk Hitting the ReSet Button in 2014,” home equity lending surged in 2004 as credit conditions eased and home prices shot higher.

The screenshot above from the OCC’s Fall 2012 Semiannual Risk Perspective illustrates that (it actually gets worse in later years).

According to Fitch, HELOCs outstanding increased 42% in 2004, and home prices still aren’t back to 2004 levels in many areas of the country.

In other words, most borrowers who still have their HELOCs will have a difficult time refinancing out of them.

And borrowers are essentially hit with two payment increases. For one, they must make principal and interest payments, as opposed to paying interest-only.

Additionally, the amortization period drops to just 15 years. So if you only paid interest for the entire draw period, you’d have a full balance to pay off in just 15 years.

Clearly this could increase monthly mortgage payments significantly, especially for those who took out large HELOCs.

During the boom, there were plenty of homeowners who used HELOCs as second mortgages to finance their hefty purchases. We’re talking $200,000+ loan amounts and higher in California and other pricey states.

For these folks, the payment increase will be nothing to sneeze at.

And Fitch believes individual bank disclosure on the risk of home equity payment resets is “generally inadequate.” So are banks not being upfront about their increased default risk on HELOCs?

It May Not Be That Bad

Fitch noted that only a “handful of rated banks” made disclosures about their home equity loan situation, meaning they could be holding out on the truth.

But there are a number of good things happening that should offset this anticipated payment shock.

For one, a decent amount of these loans were probably already paid off, refinanced, or extinguished when associated properties sold or were lost to foreclosure or short sale.

Secondly, many distressed homeowners have taken advantage of HAMP or HARP and other programs for those with negative equity.

As a result, their total monthly mortgage payments have been greatly reduced, even if a reset is coming on their second mortgage.

In fact, if homeowners are saving several hundred dollars a month on their first mortgages thanks to a massive interest rate reduction, it should be more than enough to offset a payment increase on the HELOC.

If anything, they can take their savings on the first mortgage and apply it to the HELOC, and probably still wind up with money left over.

Additionally, home prices are on the rise, meaning many of these homeowners are getting back above water, or even lowering loan-to-value ratios to levels where a traditional refinance is possible.

Lastly, the prime rate, which dictates what a borrower will pay on a HELOC, is as low as it can go, at just 3.25%.

Before the crisis, the prime rate was as high as 8.25%, so rates on HELOCs are rock bottom as well.

In other words, we probably don’t have too much to worry about collectively, though certain homeowners will definitely be affected.

And that could mean more payment defaults and foreclosures, and more losses for the big banks that hold all these loans.

Today’s Fed announcement was largely as expected: no rate hike, “data dependent,” and “higher for longer” communicated via the dots. The direction of the change in the dot plot is no surprise, but the magnitude was. The median Fed member moved their forecast up by 0.50% through both 2024 and 2025. Granted, those forecasts have a poor track record of predicting the future, but they speak to the Fed’s will to continue hiking if the data remains resilient. Bonds held their ground reasonably well at first, but late day position squaring resulted in a break to new long term yield highs.

Fed Dot Plot Changes

2023

5.625% (range 5.375% to 5.625%); prior 5.625%

2024

5.125% (range 4.375% to 6.125%); prior 4.625

2025

3.875% (range 2.625% to 5.625%); prior 3.375%

2026

2.875% (range 2.375% to 4.875%)

09:24 AM

gradually but modestly stronger throughout the overnight session. MBS up 6 ticks (.19). 10yr down 3.4bps at 4.329.

01:24 PM

10yr down 4.6bps, near best levels at 4.317. MBS up 6 ticks (.19) again after some AM volatility.

02:05 PM

Sharply weaker after Fed announcement. MBS down 3 ticks (.09) and 10yr up to 4.359

03:22 PM

Volatile 2-way trading since Fed. Powell press conference is over. MBS down 7 ticks during moments of illiquidity (-0.22) but only 1-2 ticks otherwise (0.03-0.06). 10yr down 1bp on the day at 4.353.

04:41 PM

Weakest levels of the day. MBS down 9 ticks (.28) and 10yr up 3.4bps at 4.397.

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.

In the week leading up to the Federal Open Market Committee meeting, mortgage applications finally ticked up.

For the week that ended Sept. 15, mortgage applications rose 5.4% from the prior week, according to data from the Mortgage Bankers Association.

Last week, purchase applications increased for both conventional and FHA loans but remained 26% lower than the same week a year ago. Meanwhile, refinance applications also increased but are still about 30% lower than the same week last year.

“Mortgage applications increased last week, despite the 30-year fixed rate edging back up to 7.31%, its highest level in four weeks,” Joel Kan, MBA’s vice president and deputy chief economist said.

Also noteworthy, the average loan size on a purchase application was $416,800, the highest level in six weeks.

“Home prices in many markets have been supported by low inventory and resilient housing demand for available homes,” Kan added.

The refinance share of mortgage activity increased to 31.6% of total applications from 29.1% the previous week. Meanwhile, the adjustable-rate mortgage (ARM) share of activity decreased to 7.2% of total applications from 7.5% last week.

The 30-year fixed mortgage rate increased to 7.31% last week, according to Kan. At HousingWire’s Mortgage Rates Center, Optimal Blue had 30-year fixed-rate mortgage at 7.19% on Sunday. At Mortgage News Daily, 30-year fixed-rate mortgage rates were at 7.30% on Tuesday.

The Federal Housing Administration loans’ share remained unchanged at 14.2%. As homebuyers continue to face higher rates and limited for-sale inventory, purchase conditions are becoming more challenging for buyers. The U.S. Department of Veteran Affairs loans’ share decreased to 11% from 11.3% the week prior. Lastly, the U.S. Department of Agriculture loans’ share remained unchanged at 0.4%.

The average contract interest rate for 5/1 ARMs dropped to 6.42% from 6.59% a week prior.

The FOMC is expected to hold rates steady on Wednesday, though analysts believe one more rate hike remains in the cards this year.

As mortgage rates began to spike last year, homebuilders across much of the country began to reduce their profit margins—which had grown to record levels during the boom—to do things that would entice buyers back into the market. For some builders, that meant offering aggressive rate buydowns, which in some cases lowered buyers’ mortgage rate below 5%. In some communities, it required cutting prices by 5%, 10%, or even 15%.

Many of the best builder deals disappeared earlier this year as the U.S. housing market started to show signs of life amid the seasonally stronger spring and summer windows.

However, the fact that the mortgage rate shock has regained bite just as the housing market entered into the seasonality softer fall window has translated into many homebuilders once again rolling out juicer incentives.

Look no further than Lennar, a homebuilder ranked No. 119 on the Fortune 500, which is presently promoting a “fixed [mortgage] rate of 4.25%” in Colorado for buyers who “sign a purchase agreement on a select move-in ready home in Colorado between 09/18/23 and 09/25/23 and close by 10/31/23.” That’s quite the mortgage rate buydown considering that on Tuesday the average 30-year fixed mortgage rate sat at 7.30%.

The fact that big homebuilders, including Lennar, still have profit margins that are well above pre-pandemic levels gives them wiggle room to offer aggressive buydowns when needed.

But just because Lennar is offering a 4.25% mortgage rate buydown in Colorado doesn’t mean buyers across the country can find that level of a buydown in their home market.

Among U.S. housing markets, Colorado markets have seen greater softening as a result of strained fundamentals.

“In normal times, we’ll have a 10% to 15% premium over resale [prices] in that zip code, it’s that localized. When the market was running prior to Fed rates going up, and mortgage rates going up, in some locations our premium got as high as 30% over resales in certain areas. So then you’re out of whack with your biggest competition, which is resale. You can do it as long as it works, but once the market starts to normalize, you have to come down. Over time it tends to revert to the means, which is a 10% to 15% premium over resale,” KB Home’s CEO Jeff Mezger recently told Fortune.

Mezger says that Denver—where Lennar is offering its 4.25% mortgage rate buydown—is still their weakest housing market.

“The [housing] market where the premium to resale got too far out there, and the market has been correcting, and it has been difficult for the industry, would be Denver. Where prices just moved very quickly, and moved away from affordability, and we’re continuing to adjust there, and demand remains a little more sluggish than average,” Mezger says.

Want to stay updated on the housing market? Follow me on Twitter at @NewsLambert.

Subscribe to Well Adjusted, our newsletter full of simple strategies to work smarter and live better, from the Fortune Well team. Sign up today.

One interesting aspect of the home loan process is the sheer number of individuals you’ll work with along the way.

You don’t just speak to a salesperson and call it a day. Lots of people are involved in what is a very complex transaction.

Aside from salespeople, there are loan underwriters, processors, appraisers, escrow officers, real estate attorneys, and more.

Let’s discuss the roles these people hold to help you better understand what it takes to get a mortgage.

Remember, you’re asking to borrow a large sum of money, so it’s going to take time and energy (and lots of people) to get to the finish line.

The Sales Rep/Loan Officer/Mortgage Broker

The first step in the home loan process typically involves a sales person, which can be a banker at your local branch or credit union, a loan officer, or a mortgage broker.

If we’re talking about a purchase, this may come before/during your home search or after you’ve found your property with the assistance of a real estate agent.

If it’s a mortgage refinance, you’d simply jump right to this step to rework the details of your existing home loan if you wanted a rate and term refinance or a cash out refi.

You might be referred to an individual/company, or you might do your own discovery to find a suitable partner. Either way, always look beyond the referral you were given.

Your real estate agent might know a great lender, but you your own research as well.

It’s important to gather multiple quotes from different companies to ensure you get the best deal.

Now, this individual will be your main point of contact during the loan process, and perhaps most importantly, will provide you with pricing.

Bankers and loan officers work at the retail level, while mortgage brokers offer wholesale rates from their lender partners.

You can read more about the differences (banks vs. brokers) but either way they’ll likely be the person you speak with most.

Aside from providing pricing, these individuals can help get you pre-qualified or pre-approved for a mortgage, discuss different loan scenarios, and guide you on loan choice.

If you have mortgage questions, they should be able to provide answers and give you guidance.

They may make certain recommendations, such as down payment amount, loan type, or provide an opinion about paying discount points or when to lock your rate.

This individual will be with you from start to finish, but doesn’t work alone. They’ve got an entire team to help you close your loan in a timely fashion.

FYI, you may also come across a “mortgage planner,” which is an individual who may assist a busy senior loan officer.

They can communicate loan status, provide follow-up, collect conditions, and perform other tasks if the LO is unavailable or simply needs a hand.

The Loan Processor

Once you’ve spoken to a sales representative (or LO/broker) and have decided to move forward, you’ll be in put in touch with a loan processor.

The main goal of the processor is to put together a clean loan file that can be submitted to the underwriting department.

This means collecting key documents, ensuring there are no red flags, double-checking everything, and making any necessary corrections.

The processor may also reach out after the loan is approved to collect additional documents to satisfy any outstanding conditions.

They will also provide updates to the loan officer or broker, who will then keep you in the loop about where you’re at in the process.

The processor essentially acts as a liaison between the underwriter and sales rep/LO/broker.

This ensures things move along smoothly and any hiccups can be resolved quickly without delay.

The Loan Underwriter

The loan underwriter probably holds the most important role in the home loan process.

They decide if the mortgage is approved, declined, or potentially suspended pending further explanation.

It’s for this reason that the loan processor only sends the loan package to the underwriter once everything has been thoroughly checked.

You only get one chance to make a first impression, so it’s imperative to get it right. Otherwise you could face delays or simply get flat out denied.

Aside from approving the loan, the underwriter will also provide a list of conditions needed to close the loan.

Most mortgage approvals are conditional, meaning you might need to furnish additional information or documentation to obtain your final approval.

Once these documents are provided, whether it’s another bank statement or letter of explanation, the underwriter will clear the outstanding conditions and move the loan to the funding department.

The Home Appraiser

While your loan is being reviewed by the underwriter, an appraisal will be ordered to determine the value of the underlying property.

Remember, aside from determining your ability to repay the loan, the bank also needs to ensure the collateral for the loan is valued properly.

This individual will visit the property to assess its condition, take photographs, and determine recent sales comparisons.

They will formulate a valuation based on the property details, such as number of bedrooms and bathrooms, square footage, amenities, location, lot size, condition, and so on.

The value they come up with, known as the appraised value, is used as the basis for the loan-to-value ratio.

Generally, the goal is for the appraiser to support the purchase price of the property or the value declared for a refinance.

If the value is lower, the details of the loan may need to be reworked, such as a higher down payment.

For certain types of loans, such as FHA loans and VA loans, the home appraiser will also ensure that certain Minimum Property Requirements (MPRs) are met.

This ensures the property is safe for the occupants, that there are adequate living conditions, and no major hazards, such as lead paint or termites.

The Home Inspector

If we’re discussing a home purchase, you’ll want to get an inspection done. And you’ll want to do it ASAP while any contingencies are still in place.

While a home inspection typically isn’t required, they’re generally a good idea.

Aside from finding out what’s potentially wrong with the property, you can ask for credits from the seller if the inspector finds any significant issues.

As the name suggests, a home inspector will come out to the property and assess the condition of the structure itself, the foundation, the interior, the roof, the electrical, HVAC, and more.

Some may also inspect the pool and spa, if one exists, though you could be charged extra.

They’ll make notes as they survey the property and issue a formal report afterwards. This can be used to negotiate with the seller if anything material comes up.

The Notary Public

Once it’s time to sign your loan documents, you’ll need to make an appointment with a notary public.

This individual serves “as an impartial witness” when signing important documents, such as those related to a home purchase or mortgage loan.

Your settlement agent should organize a time to meet with this individual to conduct your signing.

The notary may come to your home or meet you somewhere else to review and sign documents.

The main job of the notary is to verify the identity of the signer and ensure they are willing to sign the documents “without duress or intimidation.”

This requires you to furnish identification, such as a driver’s license, during the signing appointment.

The Escrow Officer

Another very important individual in the transaction is the escrow officer, a third-party who facilitates the loan closing and collects/disburses funds to the appropriate parties.

Some of their key roles include preparing final statements for the buyer, such as cash required to close, and determining costs such as property taxes, insurance, prepaid interest, and loan payoffs.

The escrow officer will send you a settlement statement that lists all the fees and closing costs associated with your loan, along with any lender credits and loan payoffs and funds required.

They will also liaise with a title company and forward necessary documents for loan recording.

Importantly, they’ll provide wiring instructions to all parties, including the buyer, so you know where to send funds (cash to close).

If you have questions about things like prepaid items, mortgage impounds, and loan payoffs, they can be particularly helpful.

The Title Agent

To ensure the property is free of any liens, encumbrances, or defects, a title insurance policy is usually required in order to take out a mortgage.

A title agent is the individual who conducts a title search, orders a preliminary title report, and eventually issues title insurance on the subject property. This makes them a licensed insurance agent

They are also in charge of recording the deed and loan documents with the county once the loan has funded.

You might hear the words title and escrow used interchangeably, but title has to do with property ownership/lien history, while escrow is about the calculation, collection, and disbursement of funds.

However, they may perform other settlement tasks beyond just title depending on the state where they’re located.

The Loan Closer/Funder

If you’ve made it this far, it means the loan is almost funded. But there’s still work to be done.

The loan closer/funder has to review the file to ensure everything is accurate and complete, and if not, address and fix any errors or outstanding issues.

They must ensure all prior to funding (PTF) conditions are satisfied and work with the settlement agent to prepare funding figures and timing of disbursement.

This includes the review of signed closing documents and items like hazard insurance and the preliminary title report.

And if everything looks good, request the wire instructions from escrow after a thorough review.

The Real Estate Attorney

Note that in certain states, a real estate attorney could be required to prepare certain documents and/or to conduct the loan closing.

This individual may order and certify a title report, review loan documents, and advise you if necessary.

Beyond that, they can ensure the interests of all parties are protected, and handle any legal issues or disputes that may come up.

One last thing. You may find that there is some overlap with a title company and escrow company, as the former can also provide escrow and notary services as well.

So depending on where you live, you could have one company or individual handle several tasks.

As you can see, there are quite a few people involved in the funding of a home loan, which explains why they take a month or longer to close.

Once you know more about each person’s role, it should be easier to navigate the home loan process and make better sense of it all.

And perhaps adjust your expectations that there isn’t a same-day mortgage and likely won’t be for the foreseeable future.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.

Furnished Finder is where we decided to list our room, which started out as a platform for traveling nurses to find furnished housing. It is now used heavily by many healthcare professionals, students, and professionals in other fields.

Travelers reach out to us through the Furnished Finder website and if the dates work out, we move forward with scheduling a video interview. It’s important for us to be able to talk to the person, even if it’s just over video, and we want them to see our faces and home in real time as well.

For the lease agreement, we used ez Landlord Forms, because they have leases for each state with specific information on what’s required to include.

We don’t ask for anything major from tenants. The most important things to us are that they are respectful of our space, don’t smoke in the house, and pay their rent on time. We also added a page at the end for tenants to add two emergency contacts in case we need to call someone on their behalf.

We have had 4 renters so far with the room being occupied for 13 out of the last 14 months. It has really helped us with our debt payoff goals and we have also met some awesome people through the process! We plan to continue renting it out for the foreseeable future.

Applied for in-state student loan help

My state offered a program called the Oregon Behavioral Health Loan Repayment Program where they help minorities in the behavioral health field, or those who serve them, pay back their student loans.

This program is funded by The Behavioral Health Workforce Initiative which has the goal of recruiting and retaining behavioral health providers who, “Are people of color, tribal members, or residents of rural areas of Oregon, and can provide culturally responsive care for diverse communities.”

To apply, I had to show I was employed and actively providing behavioral health services and give them detailed documentation about my student loans. I also had to answer two essay questions related to being a part of and/or working with communities who are underserved and how my training has equipped me with supporting these communities.

I applied last year and was a recipient of an award!

As a recipient, there is a two-year service commitment which means I have to continue providing some sort of behavioral health service during that time frame (which I planned to). Over the next two years, I will be getting ~$88,000 in quarterly disbursements to put towards my student loans. So far this year, I have received ~$11,000, and it’s been life changing to say the least!

Alongside this support, I am also pursuing Public Service Loan Forgiveness (PSLF) for additional student loan relief.

Managing our mental health while paying off debt

Since I am a social worker, I often think about how money and debt affect individuals’ mental health. It’s one of the reasons why I started my blog in the first place.

I realized managing money is a universal task and many of us don’t know what we are doing because talking about money is taboo. And when you have financial stress, it can really take a toll on your mental health. So, I wanted to share our journey in hopes of helping others.

Bret and I aren’t those individuals who want to avoid eating out and fun experiences until we are debt free. And, we are also privileged to not have to take those extreme measures either. It has been important for us to make this journey sustainable and not deprive ourselves of experiences while we are going through it.

Here’s how we are making our journey sustainable:

Still going out to eat

Budgeting for personal spending money, aka fun

Setting realistic debt payoff goals

Putting aside money for travel

Not comparing and thinking other people are better than us because they’re able to pay off their debt quicker

Tracking our debt payoff progress (we use Excel). With so much debt left to pay off, being able to see our progress is really motivating

Openly talking about our debt. Avoidance is a coping mechanism for many, for us, acknowledging and addressing it has been so freeing (but it wasn’t always this way).

Talking about our dreams and reminding ourselves why we want to do this in the first place

We know that if we eliminated going out to eat, budgeting for fun, or both, we could be paying off our debt much quicker. However, that sounds miserable to us. It’s worth it to still go out to dinner, travel, or buy plants (in my case) than to deprive ourselves of the joy these things bring.

We are making great progress and we know in time, we will be debt free.

Our debt payoff journey is not linear

A few months ago, we decided to take out $6,000 of student loans. Bret currently has a full tuition scholarship, so we are tremendously lucky in that regard, but he just learned about some conferences that would be really helpful to his professional growth. We have gotten $1,500 of this loan money already which is included in our current debt balance, but we haven’t received all of it yet.

We could have pinched and saved to avoid taking on any of this debt, but that would have caused me to work more than I currently am. Again, not in line with our current goal of making this journey sustainable!

We were very intentional about how much to take out. We estimated how much he would need for a few conferences and declined the rest. We even opened a separate savings account for the money to make sure it didn’t get accidentally spent on anything.

I’m SO proud of us for that!

The goal here is progress not perfection. So cliche, I know. But we are learning how to think critically about our money, spend thoughtfully, use our money as a tool to reach our goals, and enjoy our life along the way. And right now, that meant taking on a little more debt.

We are moving in the right direction, and we know when he starts working, that will really accelerate our debt payoff journey since we have proven to ourselves we can live on my income alone.

Our plan going forward

Bret is still in school which means his loans are on deferment, so we currently have his on the back burner.

With the loan payment assistance I am receiving, it’s allowing us to put any extra money we have each month towards our savings. Our priority right now is building up a good emergency fund of about $16,000 (~4 months’ worth of expenses).

This has been difficult because of inflation and just little emergencies that keep popping up, but we are slowly making progress.

I am also prioritizing investing in my employer retirement plan, but only up to the amount that gets me my employer match which is 6% of my income.

Bret will be graduating in 2025, so at that time, we will pivot to incorporating his loans into our budget. Our goal is to be debt free by 2028.

It will take a lot of discipline and persistence, but I think we can do it. I am manifesting it!

We want to continue to learn, implement, and grow. We want to keep having transparent discussions about money and building our money foundations. And I personally want to continue sharing our journey with hopes of inspiring, encouraging and educating others. Here’s to sharing the wealth.

Do you have debt? What are you doing to pay it off?

Taylor is a social worker and personal finance blogger at Social Work to Wealth where she shares tips, resources, and lessons learned on her family’s journey to paying off $277,000 of debt and retiring early. She hopes to inspire and empower social workers with financial education so they can have a better relationship with their money. When she’s not working or blogging, you can find her traveling, gardening, trying a new restaurant, or buying too many plants.

The mortgage market faces a turning point, experts say, asnew fixed mortgage rates have stayed below variable rates for several months and predictions grow that the cash rate has peaked.

National Australia Bank and Westpac last week became the latest banks to reduce some of their fixed rates, with both lenders dropping certain two-year rates, following cuts from the Commonwealth Bank in August.

For the first time since January last year, the average fixed rate dipped below the average variable rate in May.Credit: AFR

Chief executive of mortgage broker Finspo, Angus Gilfillan, said new fixed interest rates had crossed a pivotal threshold, dipping below new variable rates for the first time since January 2022.

“The current situation suggests an inflection point, where the market no longer expects interest rate rises to occur in the medium term,” he said.

While the average new variable rate has increased 2.5 percentage points to 5.95 per cent over the past year – exceeding the 1.75 percentage point increase in the Reserve Bank cash rate over the same period – Gilfillan said average new fixed rates increased by a more modest 1.7 percentage points to 5.8 per cent.

Fixed rates, which have traditionally played a small part in Australia’s home loan market, tend to reflect the money market’s view on the future path of the cash rate.

“Fixed rates are historically higher than variable rates when rate hikes are expected on the horizon,” Gilfillan said.

Some economists have called a peak in the Reserve Bank’s cash rate, forecasting a fall as early as March. While some fixed rates have fallen lately, RateCity figures still show the majority of recent fixed-rate changes have been increases.

Advertisement

RateCity research director Sally Tindall said the major banks’ reductions recently could be an early sign some fixed rates are on their way down. At the same time, banks have been trying to rein in some of the more aggressive discounts they are offering on variable-rate loans, and Tindall said none of the big four banks had an advertised variable rate under 6 per cent.

Westpac last week raised one of its advertised variable rates for new customers, and Tindall said this was the 22nd rise to new customer rates from a big four bank since March. She said this trend showed “a strategic move to walk away from the cut-throat competition in the home loan market”.

She said it was unlikely that variable rates among the big four would return below 6 per cent until the Reserve Bank began cutting the cash rate.

As banks raised their variable rates, the number of customers choosing to fix their home loans has risen, albeit from low levels. Gilfillan said the proportion of customers choosing fixed rates had doubled over the past three months to 9.4 per cent in July, although it remains below the peak of 46 per cent in July 2021 when banks were offering ultra-low fixed rates.

Morningstar analyst Nathan Zaia said banks may have lowered their fixed rates recently to attract customers who were coming to the end of their previous fixed-rate contracts.

“The banks are probably looking for a way to lock their customers in, at least for a few years,” he said, as the mortgage rate cliff plays out.

Banks have signalled their intentions to walk away from cut-throat competition in the past few months in an effort to protect their margins, and have been less generous in some of the discounts they are offering customers on variable-rate loans.

“The banks are still offering very competitive pricing, but they’re not competing as hard,” Zaia said.

Once banks have made their repayments to a pandemic-era RBA funding program called the term funding facility (TFF), Zaia said the intensity of competition would probably fade.

“If the cash rate starts falling, they may not pass all the decreases on to borrowers,” he said. “Once they’re past the TFF repayments, banks will have more flexibility and there’s really little incentive for them to compete hard.”

The Business Briefing newsletter delivers major stories, exclusive coverage and expert opinion. Sign up to get it every weekday morning.

Millie Muroi is a business reporter at The Sydney Morning Herald covering banks, financial services and markets.Connect via Twitter or email.

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults. In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over…

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults.

In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over the years as well.

As the value of certain cards continues to rise, finding the best places to sell your collection of Pokémon cards is more important than ever.

Whether you’re looking to make some extra cash, simply downsize your Pokémon card collection, or if you are decluttering everything you own and find a long lost box of childhood mementos, knowing where and how to sell your Pokémon cards can be important to make the most money.

In this article, I’ll discuss some of the best places to sell Pokémon cards online and locally and provide tips on how to price and present your cards in the best way.

Quick Summary

Identify and evaluate the value of your Pokémon cards before selling. Some cards are worth way more than others. For example, one card may be worth $0.10, and another may be worth over $100,000.

Look at your different selling options to see how you can get the most money.

Learn effective selling tips and strategies for presenting your cards to potential buyers.

How To Sell Pokemon Cards

Selling your Pokémon cards can be an exciting and profitable way to make money, especially if you have rare, holographic, or near-mint-condition cards in your collection.

To help you make the most profit, follow these tips to find the best places to sell your Pokémon cards. Before starting your Pokémon cards selling journey, it’s important to know your cards’ condition, rarity, and type.

Related: How I Made $40,000 In One Year Selling Items

Near-mint cards with no creases, scuffs, or whitening edges tend to have a higher value. Also, rare and holographic cards, like the famous Charizard, are highly wanted by fans, collectors, and trading card game enthusiasts, making them valuable in the Pokémon card market.

To figure out how rare your Pokémon card is, look for the symbols in the bottom right corner of your card and if you have a lot of cards, then you should become familiar with the Pokémon card rarity indicators, as well as the different sets and booster packs in which your cards were released.

For more accurate valuations, you may even look for professional grading services, such as Professional Sports Authenticator (PSA). They evaluate and grade cards based on their condition, ensuring buyers of their authenticity and quality.

If you’re selling Pokémon cards online, make sure to take clear, high-quality pictures that showcase your cards’ condition, as this will give potential buyers a better idea of what they’re purchasing.

By following these tips and tricks, you’ll be prepared to sell your Pokémon cards and get the most amount of money.

Best Places To Sell Pokemon Cards Online

There are many ways to sell Pokémon cards online. Here are some Pokémon selling sites to start with:

1. eBay

eBay is one of the most popular marketplaces for selling Pokémon cards due to its large reach of customers around the world.

I did a quick search on eBay and there are currently over 160,000 Pokémon cards for sale – so they definitely have a huge market!

You can choose to sell your cards through auctions or fixed price listings. When selling on eBay, be mindful of the seller fees and PayPal fees that will be deducted from your earnings. Shipping will also be another cost.

eBay is especially good for selling valuable cards, such as holographic cards or rare Charizard cards. To reach a wider audience and increase the chances of a successful sale, make sure you write detailed descriptions and add high-quality photos of your cards so that people are more likely to click on your listing.

2. Troll and Toad

Troll and Toad is an online store that specializes in collectible card games, such as selling Pokémon cards and they have been around for over 25 years.

They offer a buy list where you can sell your cards for cash or store credit. To sell on Troll and Toad, simply use their search bar to find the cards you want to sell, add them to your cart, checkout, and then ship your cards to them.

This is a great feature of Troll and Toad – the fact that you can see the exact cards they will accept and the exact amount that they will pay you for each Pokémon card. As you will learn below, many of the Pokémon card selling websites have this same feature, which is so helpful!

After you complete the list of cards that you plan on selling to them, you will print out an invoice that they give you, and then choose a payment method. Then, you will ship your box of Pokémon cards to them. Once they receive the package, they will verify the cards that you have sent to make sure they are in the correct condition as you stated. After that, they will pay you.

Troll and Toad also accepts Pokémon cards in bulk.

Keep in mind that they may be selective about the cards they accept, so it’s important to research and determine the value of your cards beforehand.

3. Mercari

Mercari is a site where you can quickly set up an account and start selling your used items, such as Pokémon cards. This site is not dedicated to just Pokémon cards, but they do have many listed and it is an easy option for Pokémon collectors.

There are well over 1,000 Pokémon cards listed on Mercari.

It’s important to create persuasive listings with photos and a relevant, detailed description, and include relevant keywords related to Pokémon cards. (Remember, they don’t just sell Pokémon cards, they also sell clothes and other items, so keywords are important!). Also, Mercari takes a minimum 10% fee from each sale you make on their platform.

4. TCGplayer

TCGplayer is a popular site with card game collectors in the U.S. and Europe.

People love selling on this site because they say it’s easy to use and they have great customer service.

To sell Pokémon cards on TCGplayer, simply list your cards on the TCGplayer marketplace, set your prices, and wait for potential buyers to purchase them. The marketplace handles the transactions, making the selling process easy.

Note: You will have to pay a commission fee of around 12–13% for each sale you make on TCGplayer, and you might also have shipping costs.

Here’s a quick guide on how to sell Pokémon cards on TCGplayer:

Create a seller account – You will need an account to get started selling Pokémon cards.

Set up your inventory – Once your seller account is created, you can start listing your Pokémon cards for sale. Enter details like the card’s name, set, condition, and quantity available.

Pricing your cards – Decide on the prices for your Pokémon cards. You can either manually set the prices or use TCGplayer’s automated pricing tool to match the market rates. TCGplayer has a pricing algorithm to help sellers be competitive and adjust prices based on the market demand.

Shipping options – Decide on the shipping options you will have for buyers.

Receiving payments – TCGplayer usually collects payments from buyers, processes the orders, and then deposits the money into your seller account. From there, you can withdraw your funds.

Maintain your inventory – Keep your inventory up to date. Remove sold items and add new ones to reflect the current availability of your Pokémon cards.

5. Card Cavern

Card Cavern is an online store that specializes in buying and selling Pokémon cards.

They have a straightforward buylist system where you can quickly find the cards they’re interested in and the prices they’re willing to pay.

Then, you ship your cards to them (they recommend purchasing tracking and insurance).

If you choose to sell your cards to Card Cavern, you’ll receive payment through PayPal or receive store credit, depending on your preference.

Their buy rates only apply to near-mint, English, tournament legal cards. You can send as many or as little Pokémon cards as you want to Card Cavern.

6. Dave & Adam’s

Dave & Adam’s is an online store for trading cards, including Pokémon cards, and it has been around for over 30 years.

They offer a buy list where you can see which cards they’re currently interested in purchasing. If your cards match their buy list, you can submit a sell request, ship your cards to them, and receive payment via check, PayPal, or store credit.

If you have a big collection, they will even travel to you.

7. Pokémon Facebook Groups

Pokémon Facebook Groups are communities of Pokémon card collectors and enthusiasts who use the platform to buy, sell, and trade cards. Pokémon Facebook Groups are exactly what you think – Facebook groups for Pokémon card collectors.

This can be a great place to sell your Pokémon cards because these groups are filled with people who are very interested in buying Pokémon cards.

These groups allow you to talk directly with fellow collectors and cater to various interests, such as specific regions, sets, or rarity levels.

To sell your Pokémon cards in these groups, make sure you follow group rules, post clear photos, and respond quickly to potential buyers’ inquiries.

8. CCG Castle

CCG Castle is a website that specializes in games since 2007.

They buy Pokémon cards that you no longer need and have a buy list on their site that will tell you exactly what they are accepting and how much they will pay you for it. They pay in either PayPal cash or store credit.

Best Places To Sell Pokemon Cards Near Me

If you’re looking to sell your collection or particular Pokémon cards, there are several options near you to consider. This section will cover the best local places where you can sell your cards, such as Facebook Marketplace, comic book stores, pawn shops, and Craigslist.

9. Facebook Marketplace

A popular and easy way to sell your Pokémon cards is through Facebook Marketplace. Nearly everyone has a Facebook account, so it can be easy for you to get started, and it allows you to connect with local buyers who might be interested in your cards.

Posting on Facebook Marketplace is simple, and you can include photos, descriptions, and set your price. Also, you can communicate with potential buyers through Facebook Messenger, making it easy to negotiate and set up a meeting location.

There are no listing fees when selling on Facebook Marketplace, which means that you get to keep everything you earn. But, you do have to handle everything yourself.

10. Local comic book stores

Comic book stores, particularly those that specialize in trading cards, card games, and board games, can be a great place to sell your collection.

Many local comic shops are interested in buying Pokémon cards to stock their inventory for other gamers and collectors.

You can visit stores in your local area, ask if they purchase Pokémon cards, and provide the store owner with a list or photos of your cards. They may make an offer on the spot or ask you to come back later. Remember, each comic store is different, so it’s a good idea to try a few stores near you to compare offers and don’t stop at just one.

11. Pawn shops

Another option to consider is pawn shops.

Pawn stores are known for buying various items, including sports cards and collectibles like Pokémon cards. Take your cards to a few pawn shops near you and see if they’re interested in buying your collection.

Keep in mind that pawn shops usually offer lower prices than other options (this is because selling Pokémon cards is not their sole business), but they can be a quick and convenient way to sell more popular cards.

12. Craigslist

Craigslist is a site for buying and selling various items locally – I’m sure you’ve heard of it. You can create a detailed listing for your Pokémon cards, including pictures, descriptions, and asking prices.

Interested buyers in your area can contact you, allowing you to arrange a meetup in a safe and convenient location.

Craigslist is usually a little more difficult to sell Pokémon cards on and that is because this site does not specialize solely in Pokémon cards and is very localized.

Where to Sell Pokemon Cards in Bulk

Selling your Pokémon cards in bulk may be something that you are interested in if you simply don’t have the time to look each one up.

When selling your Pokémon cards in bulk, it’s important to find the right platform. In this section, we’ll focus on three popular options: Full Grip Games, Safari Zone, and Sell2BBNovelties. With their unique offerings and easy-to-sell process, these companies can help you get the most value for your collection if you simply don’t have the time or have too many cards to sort through.

13. Full Grip Games

Full Grip Games is a local game shop in Ohio that buys bulk Pokémon cards online and in person.

At Full Grip Games, they make it easy for you to sell your bulk cards in increments of 100 or 1,000. Also, they accept rares and other card types as well. To make things simpler for you, their website has a bulk buy list that breaks down all the packs and cards they accept along with individual prices.

To get started, follow these easy steps:

Click on the “Buylist Instructions” link on their website.

Choose their full singles buylist or their bulk buylist.

Select the cards in your collection according to the buylist.

Review the pricing and total value of the cards submitted.

Once done, send the cards following their shipping instructions.

Once they receive your bulk cards, it will take them around one week to go through them. For the cards they accept, you can get paid via PayPal, store credit (you will get a 30% bonus if you choose the store credit option), or check via USPS mail.

14. Safari Zone

Safari Zone is another great option to consider for selling your Pokémon cards in bulk. They accept a wide range of cards, but they do need to be in near-mint condition.

Here’s what you should do to sell your cards on Safari Zone:

Create an account on the Safari Zone website.

Review the cards they purchase on their buy list.

Enter the card details.

After submitting the card information, you’ll receive a quote for your collection.

Ship your cards to Safari Zone, and they will process your payment after validating the cards.

Safari Zone only pays via store credit.

15. Sell2BBNovelties

Sell2BBNovelties is a website that has been around since 1999 that specializes in toys and collectibles, such as Pokémon cards.

They have an easy platform to sell your Pokémon cards in bulk and accept various card types, including rares, holographic, and common/uncommon cards.

To sell your Pokémon cards on Sell2BBNovelties, simply:

Go to their website and click on the “Buying Prices” tab.

Select the cards you’re selling according to their buying list.

When you’re ready, submit the form. You’ll receive a confirmation email with the total value of the cards and further instructions.

Ship your cards to Sell2BBNovelties, and they will process your payment upon receiving and verifying your cards.

You can receive payment for the cards they accept in either PayPal cash or store credit.

How to Make a Website to Sell Pokemon Cards

If you have the time and a lot of cards, you may even be interested in starting a website to sell your Pokémon cards.

Creating a website to sell your Pokémon cards is a great idea to reach a wider audience and have lower fees. Of course, there will be more work in this because you will be managing everything yourself.

Choose a platform and create your design – Look for an easy-to-use platform to build your website – my favorite is WordPress. You will want to pick a clean looking design that customers can look at on both computer and phone. Most platforms have a variety of premade themes that you can use. You can also personalize your website by adding your logo, choosing colors that represent your brand, and adding images.

Organize your products – Categorize your Pokémon cards by sets, rarity, or other criteria that make sense for your target audience. Clear product descriptions and high-quality images of each card will help potential buyers too.

Set up payment and shipping – Choose a payment gateway to securely process transactions. Options like PayPal, Stripe, or Square are widely used and reliable. Choose shipping options and rates based on your preferred carriers and shipping destinations.

Create valuable content – In addition to listing your Pokémon cards, consider creating helpful content such as blog posts or videos that add value to your website and attract more readers and buyers. Providing informative content will establish you as an expert in the field and help drive traffic to your site.

Promote your website – Use social media, search engine optimization (SEO), or even paid advertising to increase page views to your website.

Related: How To Start A Website Free Course

Pokemon Card Selling Tips and Strategies

Selling your Pokémon cards can be an exciting way to make extra money, but it’s important to have a little strategy so that you can make the most money and find the most buyers.

Here are some tips for selling your Pokémon cards successfully.

Determine the value of your cards. You should research how rare the card is, the origin, and the condition of your cards, as these factors will affect their worth. Keep an eye out for rare and valuable cards (such as first edition cards and illustrations), as these will attract more interest from collectors. Grading your cards can help with this process – professional grading services can rate the condition of your cards and encapsulate them in a case, increasing their value.

Consider where to sell your cards.There are numerous platforms for selling Pokémon cards online, such as eBay, where you can list your cards as single items or in an auction format. There are also more specialized Pokémon selling websites which are dedicated to trading cards. These sites often have dedicated communities of potential buyers who are very interested in Pokémon cards.

Write clear and accurate descriptions of your cards.You should always be clear and honest about your card’s condition. For example, are there any scratches or bends? Is there a tear or water damage?

Ship your cards carefully.Carefully package your Pokémon cards to protect your cards from damage during transit. You will want to keep your cards waterproof and not use rubber bands (rubber bands can damage the cards). Also, consider offering a tracking number and insurance to your buyer as an additional layer of security. Many of the Pokémon selling sites above have a very exact way they want you to ship the cards to them to prevent any damage, so be sure to see what their rules are.

By following these Pokémon card selling tips and tricks, you can increase the chances of finding the best places to sell your Pokémon cards.

Frequently Asked Questions

Here are answers to common questions about selling Pokémon cards.

How do I know if my Pokemon cards are worth money?

So, how do you know if the Pokémon cards that you have are worth anything? Many people have Pokémon cards, probably stuffed in a box somewhere, or maybe you came across some.

Whatever your reason is, yes, your Pokémon cards may be worth something.

Knowing the value of your Pokémon cards is important before selling, and there are a few key things to think about.

First, look at the rarity symbols on your cards: a circle indicates a common card, a square represents an uncommon card, and a star denotes a rare card. These symbols help you determine the rarity of your cards and their potential worth.

The condition of your cards also plays a big role in their value. Cards in mint condition, meaning they have no visible wear or damage, are worth more than cards with minor imperfections. Holographic cards, especially in mint condition, can be more valuable.

To take it a step further, you could even get your Pokémon cards professionally valued and graded by a reputable company like PSA. Grading involves a professional inspection of your card’s condition, assigning a numerical grade based on factors such as centering, corners, edges, and surface. The higher the graded number, the better the condition and, often, the higher the value.

Keep in mind that while Pokémon cards typically have higher values, other trading card games like Yu-Gi-Oh can also be valuable. Make sure to research the prices of similar cards sold recently, and compare the condition of your cards to decide if they’re worth selling.

How do I sell Pokemon cards for cash?

To sell your Pokémon cards for cash, first organize your cards by set and look for rare ones to see what you have. Once you’ve prepared your collection, follow the selling instructions on your chosen platform.

You can sell your Pokémon cards online, locally near you, and even in bulk.

Where can I find buyers for my Pokemon cards?

You can find buyers for your Pokémon cards on online marketplaces, local card shops, and social media groups. Websites like eBay and TCGplayer are popular places for selling Pokémon cards, as well as community forums and local collector’s events.

What are some reputable websites to sell Pokemon cards?

There are many reputable sites to sell Pokémon cards as we discussed above, such as:

eBay

Troll and Toad

Mercari

TCGplayer

Card Cavern

Dave & Adam’s

Pokémon Facebook Groups

Full Grip Games

Safari Zone

Sell2BBNovelties

Where is the best place to sell Pokemon cards?

The best place to sell your Pokémon cards depends on your preferences. eBay gives you a worldwide market and you are probably already familiar with their platform.

TCGplayer and Troll and Toad specialize in trading card sales and have a lot of Pokémon cards for sale.

Pokémon Facebook Groups are a great way to connect with those interested in Pokémon cards, and there are no listing fees – but you would be dealing with people on your own and handling everything yourself.

Are there any local stores that buy Pokemon cards?

Some local stores, like comic book shops, game stores, and pawn shops, may buy Pokémon cards. You can call local stores to see if they buy cards before bringing your collection in person.

Can you sell Pokemon cards on Etsy?

Etsy is generally geared towards handmade and vintage items, so it’s not an ideal platform for selling Pokémon cards. It’s best to stick with platforms like eBay, TCGplayer, or Troll and Toad for selling trading cards.

I did a search for Pokémon cards on Etsy and it said there were 43,326 results, but I think many of these are for custom art, in that they would be turning a picture of you or your pet into a Pokémon card. So, not the same thing.

Can I sell Pokemon cards on eBay?

Yes, you can sell Pokémon cards on eBay. It is one of the most popular sites for selling Pokémon cards and it gives you control over pricing and listing options.

Can you sell Pokemon cards at GameStop?

GameStop typically does not buy or sell individual Pokémon cards.

Do pawn shops buy Pokemon cards?

Some pawn shops may buy Pokémon cards, especially if they are valuable or rare. Call your local pawn shops or visit them in person to inquire about their interest in buying Pokémon cards. Remember, they do not specialize in Pokémon cards and have a smaller market, so you may not get as much for your Pokémon cards at a pawn store.

What does TCG and CCG mean?

As you’re going through the sites above looking for one of the best places to sell your Pokémon cards, you may come across these two terms. CCG means collectible card game and TCG means trading card game.

How can I determine the value of my Pokemon cards?

Figuring out the value of your Pokémon cards involves considering factors like:

rarity

condition

age

Websites like TCGplayer and Troll and Toad provide price guides and historical sales information to help you estimate the value of your cards.

How do I check the value of my Pokemon cards?

Check the value of your Pokémon cards by researching on websites like TCGplayer, eBay, and Pokémon Price. These platforms can give you a good idea of the current market value for individual cards.

Do you need a license to sell Pokemon cards?

You generally do not need a license to sell Pokémon cards, unless you’re planning to sell them by opening an in-person store. Check your local regulations to make sure you’re following any required guidelines.

How much is Charizard Pokemon card worth?

Charizard cards vary widely in value and can be worth anywhere from $25 to over $50,000. The Charizard Pokémon card that is worth the most is typically a mint condition 1st Edition from the base set.

What Pokemon cards are worth more than $100?

Some Pokémon cards worth more than $100 include rare Pokémon cards, such as first edition holographic cards from the original sets, high-grade cards, misprints, and promotional cards like the Pokémon Illustrator card.

What is the most expensive Pokemon card?

The most expensive Pokémon card varies over time; some examples include the Pokémon Illustrator card, the 1st Edition Charizard, or unique, one-of-a-kind promo cards handed out during official Pokémon events. The rarest Pokémon cards obviously cost more money and sell for more.

According to TCGplayer, the most expensive Pokémon cards include:

Pokémon World Championships No. 2 Trainer Promo

No. 2 Trainer Toshiyuki Yamaguchi (2000)

Neo Genesis 1st Edition Lugia (2000)

Super Secret Battle No. 1 Trainer (1999)

Family Event Trophy Kangaskhan (1998)

Test Print Blastoise Gold Border (1998)

Tsunekazu Ishihara Signed Promo (2017)

Trophy Pikachu No. 3 Trainer Bronze (1997)

Commissioned Presentation Blastoise Galaxy Star Holo (1998)

First Edition Shadowless Holographic Charizard #4 (1999)

Illustrator Pikachu (1998)