Real estate investment trust Rithm Capital Corp has entered into a definitive agreement to acquire Computershare Mortgage Services Inc. for about $720 million, the companies announced Monday. The deal includes the purchase of Specialized Loan Servicing LLC.

The deal represents the second major acquisition that New York-based Rithm, which operates NewRez, Caliberand other businesses, has announced in the past three months. In July, the company struck a deal to acquire Sculptor Capital Management Inc. for $639 million, leading to a dispute among the shareholders at the asset management firm.

Rithm’s deal with Computershare will add a mortgage servicing rights (MSR) portfolio of about $136 billion in unpaid principal balance (UPB) to the company. It includes $85 billion in third-party servicing and the Specialized Loan Servicing’s MSR portfolio.

“Our track record of acquisitions in the mortgage servicing space continues to deliver value not only for our shareholders but also for the millions of consumers we serve,” Michael Nierenberg, chairman, CEO and president of Rithm Capital, said in a statement.

Rithm expects to conclude the acquisition in the first half of 2024.

Following the deal’s closing, Specialized Loan Servicing portfolio and operations will be under Newrez, the 8th largest U.S. mortgage lender in the first six months of 2023, with a production of $17 billion in loans, per Inside Mortgage Finance data.

Newrez was also the fifth largest company in owned mortgage servicing in the second quarter, with a $540 billion MSR portfolio. Computershare Loan Services was No. 36, with $53 billion in total, according to the IMF data.

Rithm intends to use a mix of existing cash, available liquidity on the balance sheet and additional MSR financing to close the Computershare deal.

Rithm had 1.8 billion of total cash and liquidity to support its acquisitions at the end of the second quarter. From April to June, Rithm delivered a $357.4 million GAAP net income — higher than the $68.9 million the prior quarter.

So far this year, the company has also invested $145 million to purchase $1.4 billion of consumer loans from Goldman Sachs and purchased 371 newly built single-family rental properties from Lennar.

Are you a property manager looking to attract future residents, or a private owner aiming to showcase your rental online? The secret to success is apartment staging. Transforming your space into a welcoming and visually appealing environment can make all the difference in capturing potential tenants’ attention.

In this Redfin article, we’ll delve into expert apartment staging tips and rental staging techniques to help you shine in the competitive rental market, whether you’re in bustling cities like New York and Los Angeles or thriving rental markets such as Austin and Seattle. Let’s get started.

1. Curb appeal matters

Curb appeal isn’t just for homeowners; it’s equally vital when staging a rental property. Before potential tenants even step inside your rental property, they’ll form their first impression based on its exterior.

Whether it’s refreshing the paint on the front door, adding potted plants to the entryway, or ensuring the walkway is clean and well-lit, small enhancements to the property’s exterior can make a significant difference. Remember, the goal is to make prospective renters envision themselves coming home to that space every day.

2. Start with a clean slate

Before staging, ensure your rental is spotless. Clean every nook and cranny, including carpets, windows, and appliances. A clean space feels more inviting and allows potential tenants to envision themselves living there.

Expert tip: ”To successfully stage your rental home or apartment, the first step is organizing and decluttering your belongings,” shares professionals Cut the Clutter RVA. “It’s essential to edit your possessions. This means assessing what you actually use and removing items that no longer serve a purpose – a critical step, particularly in smaller spaces prone to clutter. A well-organized and clutter-free environment creates the illusion of more space and enhances the appeal of your rental property to potential tenants.”

3. Focus on your audience when staging

Whether it’s a home or a rental, your first step should always be to consider your potential tenant. It’s not just about making it look nice; it’s about ensuring it resonates with those who might call it home.

Expert tip: “When staging a property, whether it’s a home or rental, the first step is to consider your potential buyer,” recommends international media group Inspired Spaces. “Identify your audience – young families, singles, retirees, professionals – and adapt the style, room arrangements, and color palette accordingly. For instance, if your target is young professionals, a secondary bedroom could serve as an office. But for a young family, that same room is best as a child’s bedroom. Focus on neutral, yet inviting color palettes in each space. This appeals to a wider range of buyers, aiming for sophistication that remains relatable.”

4. Use a neutral color palette

Opt for a neutral color scheme when painting walls and selecting furnishings. Neutral tones create a blank canvas that appeals to a broader audience and allows renters to add their personal touches with ease.

Expert tip: Broker Corrie Hayes emphasizes the importance of cohesive decor in creating a balanced room. “Have you ever thought, ‘something is off?’ in a room, but you can’t put your finger on it? Your space can unintentionally feel like it’s having an identity crisis. Whether it’s shabby chic, industrial, rustic farmhouse, or modern sleek, creating harmony in your decor is key. Mixing contrasting styles can lead to visual confusion, but it can be resolved with purposeful choices like coordinating grey couches with beige or cream throws, wall art featuring a mix of complementary colors, and bedding that combines various neutral tones. The result is an inviting space that appeals to a broad range of individuals.”

5. Choose furniture that fits the space

When selecting furniture, consider the size of the space. Avoid overcrowding rooms; instead, opt for appropriately sized furniture that complements the room’s layout. Don’t forget comfortable seating in common areas to highlight a cozy atmosphere.

Expert tip: According to Southern Maryland interior designers at Chesapeake Staging & Interiors, LLC, there are key logistics to consider when staging a rental property or unit. “The first is whether or not the property or unit will be listed as furnished. If not, you’ll need to state that it is an unfurnished unit to avoid confusing potential renters. If it is furnished, you’ll need to stage it with quality furniture that can withstand a renter’s use.”

6. Focus on lighting

Natural light is a key selling point. Open curtains or blinds to let in sunlight and add floor or table lamps where needed, to create a warm and well-lit environment. Adequate lighting enhances the overall ambiance.

Expert tip: According to Aspect Staging, “Lighting plays a vital role in enhancing your rental property’s appeal. To create a warm and inviting atmosphere, strategically illuminate key areas like the living room and bedroom. Use modern floor lamps to brighten dark corners, and consider matching bedside table lamps for a cozy ambiance. Opt for soft white light bulbs with a color temperature between 3000k and 3500k lumens to strike the perfect balance between warm and cool lighting, making your space feel spacious and inviting.”

7. Emphasize storage possibilities

Highlight the storage options in your rental property, as it’s a top priority for many renters. Keep closets and cabinets organized and clutter-free, allowing tenants to envision their belongings neatly stored. Well-arranged storage spaces make your property appear spacious and cater to practical needs, enhancing its appeal.

8. Use staging to define spaces within your rental

If your rental space lacks distinct areas, create them with furniture placement and rugs. Clearly defined living, dining, and sleeping areas can help renters visualize the functionality of the space.

Expert tip: Birgit Anich, CEO and Creative Director at BA Staging & Interiors, emphasizes that staging a rental property parallels staging one for sale. “Given that rental apartments often have limited space, a clear definition of how each area is used is key. The level of sophistication in staging should align with the rental price. A deliberate design that incorporates the renter’s lifestyle and aspirations into the details can evoke emotions and foster a connection with the space, making it more enticing.”

9. Accessorize your rental thoughtfully

Incorporate tasteful accessories such as throw pillows, artwork, and decorative items. These personal touches add character to the space and help renters connect emotionally with the property.

Expert tip: Professional real estate photographer Cynthia James Photography advises that, “When selecting a rental property, it’s crucial to create a welcoming home-like ambiance. In urban areas, consider faux plants for a touch of nature. Enhance the kitchen’s charm with decorative canisters, a recipe book holder, draped kitchen towels, and fresh flowers. In the owner’s bedroom, a queen-size bed with neutral bedding, layered pillows, a quilt, and blankets add comfort. Transform the bathroom into a serene spa with a small rug, neatly arranged soaps, and folded white towels. At the entrance, a welcoming doormat and decorative items like a wreath or home sign can make your rental feel like a comfortable long-term home.”

10. Be creative while staging

In the world of rental property staging, creativity can be your secret weapon. When it comes to making your space more appealing to potential tenants, a dash of innovation can transform ordinary into extraordinary.

Expert tip: For renters looking to make their space more appealing, Florida interior designers TOSCANO INTERIORS recommend creative staging techniques. They suggest, “Converting underutilized spaces and incorporating local art and craftsmanship to add authenticity. The key is to strike a balance between uniqueness and broad appeal, ensuring that unique touches enhance the space. This helps renters create a compelling narrative in their home through furniture, decor, and color choices.”

11. Use fresh flowers and greenery throughout your space

Adding a touch of nature to your staging can work wonders. Fresh flowers and potted plants breathe life into your rental space, infusing it with vitality and freshness. Fresh flowers bring color and a welcoming fragrance, while greenery introduces a calming presence. They are versatile, complement various interior styles, and require minimal maintenance. These natural elements make your property feel like a vibrant and inviting home, leaving a lasting impression on potential tenants.

12. Make sure the rental is clean and smells nice

Before each showing or photoshoot, ensure the space is clean and well-maintained. A final walkthrough is crucial to catch any last-minute details that need attention.

Expert tip: “Don’t underestimate the impact of odors on potential buyers,” says CC Staging & Design. “Unpleasant smells, whether from pets, cooking, or other sources, can quickly deter them. Take proactive steps to ensure your home exudes a fresh and clean scent. Deep-clean carpets, introduce air purifiers for a crisp ambiance, and opt for subtle, pleasant scents rather than overpowering air fresheners. Elevate your home’s appeal with an inviting and refreshing fragrance.”

13. Hire a photographer

Invest in professional photography for your rental property. High-quality images make your online listing stand out and attract more potential tenants. Make sure the photographer captures the best angles and showcases the key selling points.

Expert tip: AV Home Staging brings attention to the advantages of staging in your rental property marketing strategy. Their tip, “Marketing increases more viewings and showings. With a vast number of renters starting their search online, professionally staged photos create a lasting impact, piquing interest and yielding a larger pool of potential applicants – a win-win for any rental property owner.”

14. Be ready to show your rental

In the competitive rental market, readiness is essential. Whether it’s in-person tours or virtual viewings, your ability to promptly and flexibly present the property is crucial. Be flexible with showing schedules, maintain the property’s condition, have the necessary technology for virtual viewings, be well-informed, follow protocols, and prioritize prompt communication to make your rental more appealing to prospective tenants.

A final note on staging a rental

By following these expert apartment staging tips and rental staging techniques, you’ll increase your chances of attracting the right tenants and securing your rental property’s success. Remember, the goal is to create a space that feels like home from the moment potential tenants step inside or view it online. Happy staging!

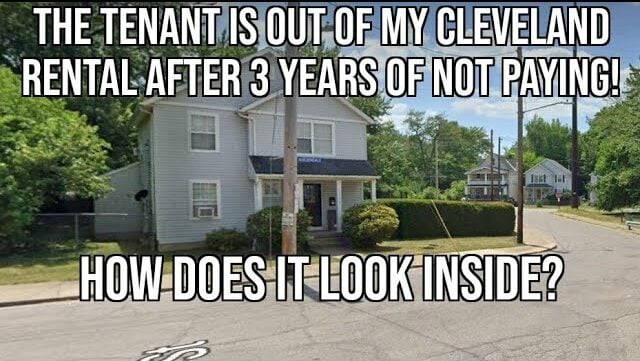

I own one rental property out of my area in Cleveland Ohio and we just got that tenant out after she did not pay rent for three years! All of my other rentals are in Colorado and I usually have no problems with evictions or getting tenants out, yes even during the Covid year. However, I learned that some cities and states can be a nightmare and do everything they can to make life difficult for landlords, especially out-of-state landlords. If you are going to invest in real estate in other areas make sure you do your due diligence!

Why did it take so long for me to get a non-paying tenant out of my rental?

I bought this turn-key rental in 2015 in my IRA. I have many other rentals in Colorado that I bought in a more traditional way but this house was sold to me by a friend, or so I thought, for $45k. It was supposed to be rented and managed but that’s another story. The rental was fine until COVID came along and the city started to pay rent for tenants. My tenant stopped paying rent and when the City of Cleveland stopped paying landlords the tenant never paid rent again.

I had a property management company that was mostly worthless and incompetent. I won’t mention their name, actually, I will, Monument Real Estate. I told Monument to evict and months went by with nothing happening. At first, Monument said I could not evict because the property needed to be certified lead-based paint-free which the City of Cleveland requires on all rentals built prior to 1978. However, my property was exempt because it was built in 2005. I told Monument this for months before they understood.

After we got that figured out, Monument said I could not evict because my IRA needed to be registered in Ohio for the Cleveland courts to hear the eviction case. The company that I used said they would not register in Ohio. I talked to multiple lawyers and they all said I was pretty much screwed because an IRA is not a corporation and you can’t register it. This went on for months more and eventually I had some help from commenters on my YouTube videos. They told me to try different lawyers and one told me to try a property management company that had helped them in difficult situations.

After the tenant not paying rent during COVID, the months the property management company argued with me over lead-based paint, and trying to figure out the registering my IRA, it had been close to three years, and the tenant never paid a dime.

How was I able to finally get the tenant out?

While this was happening I asked the property management companies to offer cash for keys. Cash for keys is when you pay someone to leave a house. The tenant never responded to any notes or calls. I switched property management companies and the new one also tried cash for keys with no success. The new property management company did help me get my IRA registered. They told me to register as a corporation with the Secretary of State (SOS) in Ohio. I told them the lawyers said that wouldn’t work but they told me to try anyway.

I tried to register as a corporation and it didn’t work. The SOS said an IRA is not a corporation and can’t be registered as one, but they were very helpful and worked with me to find a solution. Eventually, the SOS helped me to register the IRA name as an entity doing business in Ohio. It took some time but we got it done and with that registration, the courts agreed to hear the case!

At the first hearing, nothing was done except to schedule another hearing. The tenant was given a free attorney by Cleveland to help fight the eviction. My property manager told me we should offer cash for keys in court because the judge will see we are trying and the tenant has to respond. I agreed to offer $2,000. The rent on the property was less than $800.

While all of this was happening the property management company said the tenant was suing them for $35k! I could not believe it until I got a package in the mail from the tenant and they wanted $35,000 from me as well! They said they needed $10,000 for cash for keys to move out and $25,000 for emotional distress from the notes and calls my property management companies made trying to offer cash for keys.

I was not hopeful she would accept the cash for keys in court, but she did! She had to move out in about 30 days and if she did not we could file for an immediate eviction. The tenant moved out and I have my house back.

The YouTube video below goes over the story and shows the house

[embedded content]

How could I have avoided this nightmare rental?

I take full blame for this situation as I should have known better. I made a few mistakes:

I trusted someone too much: I trusted someone who said they knew the area and that this was a good deal. None of that was true and if I had had a third party check out the property I would have known never to buy it.

I trusted the property management company given to me: That person also recommended a property management company that stopped doing rentals and then they recommended Monument and I never checked them out myself. I should have done way more due diligence.

I didn’t fire a bad property management company as soon as I knew there were issues: I knew Monument was bad since they messed up my accounting before, and kept making mistakes, not communicating, and were flat-out rude. I was lazy and waited too long to hire a new one.

How to buy out-of-state rentals the right way.

Conclusion

If I were to buy out of my area again, I would do way more due diligence and most likely not use a turn-key company. I would find an agent, and property manager and use them to find a great deal wherever I wanted to invest. I would have a third party checking things out and not trust people as much as I did. I can handle the nightmare this became because my other rentals have done very well but a new investor without other investments could have huge problems in the same situation.

When it comes to the topic of real estate in America, the Las Vegas housing market often emerges as a point of discussion. Known for its neon lights, bustling casinos and luxury hotels, Las Vegas also presents a residential backdrop that is just as dynamic and ever-changing. From market trends to environmental risks, let’s take a comprehensive look at what the Las Vegas housing market has in store for potential buyers, sellers and investors.

The Las Vegas housing market today

First, let’s talk numbers. Currently, the Las Vegas housing market sits in a somewhat competitive niche, making it an interesting ground for buyers and sellers. Homes here are generally on the market for around 35 days, a noticeable increase from 23 days last year. They receive around two offers before the ink dries on the dotted line.

What’s striking is that the median sale price for homes in the Las Vegas housing market is $415,000 — a 2.4% decrease when compared to last year’s figures. However, it’s worth mentioning that the number of homes sold actually inched up by 1.3%, from 934 to 946 homes.

Affordability

A closer look at the numbers reveals that the median sale price per square foot stands at $247, which is a slight 1.6% decrease from last year. For those eyeing the Las Vegas housing market for potential investment, this could mean that now might be a reasonable time to step in.

Homes are selling for about 1% below the list price, giving a little wiggle room for negotiation. The sale-to-list price ratio sits at a solid 98.8%, a minor but interesting 0.48-point drop from the previous year.

Climate impacts on the Las Vegas housing market

Let’s switch gears and discuss something increasingly important in real estate — climate. Las Vegas isn’t just about arid desert landscapes. Las Vegas has some substantial environmental challenges that homeowners need to consider.

According to the First Street Foundation, 5% of properties are at risk of flooding over the next three decades. A substantial 27% face wildfire risks, which can’t be taken lightly given the global uptick in extreme weather events. Astonishingly, a staggering 95% of properties in the Las Vegas housing market are at severe risk due to heat. If you’re eyeing a long-term investment, these aren’t just numbers; these are lifestyle factors that could impact the future value of homes in Las Vegas.

Transportation

Another point to consider is the city’s transportation infrastructure. Walkability and availability/reach of public transport can significantly influence the attractiveness of a residential area.

Las Vegas scores 42 out of 100 on the Walk Score®, showcasing a largely car-dependent environment. Its Transit Score® is just 36, making public transportation a less convenient option for daily commuting. The Bike Score® stands at 46, indicating that the city is only somewhat bike-friendly.

Las Vegas housing market compared to national trends

Zooming out for a bit, the median sale price in the Las Vegas housing market is about 2% lower than the national average. The overall cost of living in the city is also 1% lower than what you would expect to see nationwide.

The Las Vegas housing market is worth your attention

The Las Vegas housing market presents a mixed bag of opportunities and challenges. While prices per home and per square foot are on a minor decline, the number of homes sold has seen a slight upswing.

It’s clear that the Las Vegas housing market is at an interesting juncture. Whether you’re an eager buyer, a potential seller or an observant investor, staying tuned to these trends could be the key to making savvy decisions in a fluctuating market. Just like a night at the casino, the Las Vegas housing market can offer high stakes and big wins — but you need to play your cards right, and it pays to keep an eye on the ever-changing landscape.

The rental market in Las Vegas

Just as the Las Vegas housing market offers tons of opportunities for buyers and sellers, the rental market in Las Vegas paints its own fascinating portrait. For renters contemplating a move to the Entertainment Capital of the World, or for investors considering the potential for income-generating properties, understanding the nuances of this rental market is key.

The current state of Las Vegas rental prices

As of September 2023, the average rent for apartments in Las Vegas ranges from $874 for a studio to $1,462 for a two-bedroom apartment. Interestingly, there is a downward trend in rental prices; the average rent for a studio apartment has declined by 1% to $874, while one-bedroom and two-bedroom apartments have seen more significant decreases of 8% and 11%, respectively.

These declines raise interesting questions about the rental market. It could signify that more people are opting for home ownership, reflecting trends in the Las Vegas housing market where home prices have slightly decreased. Alternatively, it may indicate an increased supply of rental properties, which puts downward pressure on rental costs.

Neighborhood trends in the Las Vegas rental market

Different neighborhoods offer diverse rental options. For instance, in Centennial Hills and Lone Mountain, the average rent for a studio apartment hovers around a steep $1,646 but has decreased by 3% over the year. Contrastingly, in Northern Strip Gateway, the average studio rent is a far more affordable $550.

Comparing Las Vegas to nearby cities

When we compare the Las Vegas rental market to neighboring cities, it’s evident that Las Vegas provides a middle-ground option in terms of rental costs. For example, Henderson, a nearby city, has an average studio rent of $1,442, which is considerably higher than the Las Vegas average.

Apartment price ranges: Where does demand lie?

Further dissecting the rental landscape, the highest proportion of apartments — 45% — falls in the $2,101 and above range. Apartments ranging from $1,501 to $2,100 make up 32%, and those priced between $1,001 and $1,500 contribute to 17% of the market. Interestingly, only 7% of apartments are in the $701 to $1,000 range, and virtually none are available for $500-$700.

Affordability in the Las Vegas rental market

When it comes to affordability, Northern Strip Gateway, Downtown and Huntridge stand out as the most budget-friendly neighborhoods, with average one-bedroom rents at $800, $925 and $950 respectively. This contrasts sharply with the city average of $1,340 for a one-bedroom apartment, offering cost-effective options for those willing to compromise on location.

The Las Vegas rental market at a glance

The rental market in Las Vegas offers a range of options for various budgets and lifestyle needs, aligning well with the trends seen in the broader Las Vegas housing market.

Whether you are an aspiring tenant or an investor looking to dive into the rental market, Las Vegas has a ton of opportunities. As with home ownership, understanding the nuances in rental trends — from neighborhood variances to overarching annual changes — can be the key to making a savvy move in the dynamic landscape of the Las Vegas rental market.

A native of the northern suburbs of Chicago, Carson made his way to the South to attend Wofford College where he received his BA in English. After working as a copywriter for a couple of boutique marketing agencies in South Carolina, he made the move to Atlanta and quickly joined the Rent. team as a content marketing coordinator. When he’s off the clock, you can find Carson reading in a park, hunting down a great cup of coffee or hanging out with his dogs.

The U.S. housing market is short by at least 6.5 million homes. After more than a decade of under-building relative to population growth, there are simply not enough affordable entry-level and first-time move-up options available for buyers. Renters are finding themselves priced out of areas within a reasonable commuting distance to work.

The scarcity of housing has driven home prices and rents prices to an all-time high and pushed affordability to a multi-decade low. Over the next decade, there will be more than two million adults added annually to the U.S. population, due to a combination of aging and immigration. This shift will drive a voracious need for more housing, especially among entry-level and first-time move-up homes at lower price points given structural affordability challenges.

Reasons for the housing shortage plentiful

Housing has been materially unbuilt for the past 15 years. Most production builders have focused on ever larger and more expensive new homes, and relatively few new homes have been built that cater to lower-income households and entry-level buyers, especially in high-cost coastal markets.

Most recently, rising interest rates have intensified the fight for housing. From February 2011 to April 2022, mortgage rates never rose above 5%, making the cost to borrow money and buy a home very cheap. However, since 2022, there has been a rapid rise in rates that has created a “lock-in effect” and stalled many families who would have otherwise considered moving. Homeowners who “locked-in” a mortgage rate of 3-4% during the pandemic are unwilling to buy a home at a 7%+ on a new mortgage, which means even fewer homes are going on the market as existing homeowners choose to stay put.

For those hoping to buy a home for the first time, the rise in rates means that monthly payments are effectively double what they would have been a year ago, a reality that has priced many people out of buying. Couple that with rising costs of home insurance and the general price inflation, and there is a massive housing affordability problem facing the majority of the country.

A need for alternatives

This persistent housing shortage has generated a pressing need for alternatives that can bridge the gap between demand and supply, while accounting for a limited availability of land in top areas.

Enter the Accessory Dwelling Unit, commonly known as an ADU, or more informally called an in-law suite, granny flat or backyard home. ADUs are small, self-sufficient structures that usually have one to three bedrooms, a private entrance, and all the amenities that a resident would require including kitchens and bathrooms. ADUs are one of the most effective ways to add density and rental properties in a higher cost market. These generally detached structures can be built in less than a year and cost far less to build than primary homes. Depending on where you live, there are also various state-run programs such as the CalHFA ADU Grant in California that can bring down building costs tremendously.

For homeowners, ADUs offer an opportunity to provide affordable housing on the rental market or house relatives that would otherwise be unable to afford the neighborhood. These structures can generate rental income to offset rising mortgage payments, and create more long-term rental supply, ultimately lowering the average rental cost for tenants. For local governments, ADUs can increase the number of tenants in areas where high-rise dwellings are not a desirable option. ADUs also offer a compelling option for multi-generational living, which can be a tremendous help with families that want to reduce burdens of childcare and senior care.

Changing policies good for ADUs

Fortunately, we are seeing many government authorities focusing on changing housing policies and zoning codes to make ADUs a more actionable solution. It’s a rare example of government housing policies driving the private market to solve a critical problem. For example, California’s changes in laws and regulations have made ADUs much easier to build. The momentum from these regulations has resulted in a large increase in ADU construction activity: permits for ADUs in California have increased nearly 22x from around 1,100 in 2015 to nearly 24,000 in 2022 and roughly 68,000 ADUs were built across California between 2017-2021. As a result, there are a large number of new housing units that have been added to high-cost locations where people hope to live and work.

Nationwide, many local and state governments are starting to follow the California example. Washington, Oregon, Florida, and Colorado, to name a few states, are starting to make ADUs a more prevalent part of solving the housing affordability issue. Ultimately, ADUs alone won’t solve decades of housing issues. But they can close the gap between the number of people looking for affordable housing and the number of homes available for rent or purchase.

Sean Roberts is CEO of Villa, an ADU builder in California.

This column does not necessarily reflect the opinion of RealTrends’ editorial department and its owners.

To contact the author of this story: Sean Roberts at [email protected]

To contact the editor responsible for this story: Tracey Velt at [email protected]

Looking to build wealth with the best income-generating assets? As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life. This is because you can invest in assets that will generate you income, earning you more passive income. Today’s article will introduce you to…

Looking to build wealth with the best income-generating assets?

As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life.

This is because you can invest in assets that will generate you income, earning you more passive income.

Today’s article will introduce you to a range of assets that reliably bring in cash, giving you peace of mind and the freedom to live life on your own terms.

From traditional investments like stocks and bonds to more creative options like peer-to-peer lending or real estate, income-generating assets give you the power to diversify your portfolio and build wealth over time.

Related content:

What are income generating assets?

Before we begin, I want to talk about the basics on income-generating assets, in case you are new to the subject or if you want a background first.

Income-generating assets are investments that, as the name suggests, generate income for you. These are assets that provide you with a steady cash flow, allowing you to earn passive income and build your wealth over time.

Examples include rental real estate and dividend-paying stocks (we will go over 17 different types of income-generating assets below in more detail).

There are several benefits of the best income-generating assets such as:

Passive income: You earn money without actively working, and this can provide financial freedom and the ability to focus on other things in life. You can earn money in your sleep, while on vacation, making dinner, and more.

Diversification: You can diversify your investments so that all of your income is not coming from just one source.

Wealth building: Earning income and generating a steady cash flow can help you build your wealth over time.

Note: Please keep in mind that there is no one-size-fits-all approach when investing in any of these income-producing assets. Everyone is different and while one asset may work great for someone, it may not be the right asset for you. I recommend doing as much research as you can if you are interested in one of the asset investments I talk about below.

Types Of Income Generating Assets

There are many types of income-generating assets. Some may be more traditional such as dividend-paying stocks, and others may be more alternative income-generating assets, such as selling stock photos, and even renting out your driveway.

Today, I will talk about 17 different types of income-generating assets, but this is not a full list of the best income-producing assets. There are many, many more!

The different types of income-generating assets that I will talk about today include:

1. Dividend-paying stocks

One of the best assets to invest in are dividend-paying stocks.

Dividends are simply a payment in cash or stock that public companies distribute to their shareholders.

The amount of a dividend is determined by a company’s board of directors, and they are given as a way to reward those who have stock in their company. Both private and public companies pay dividends, but not all companies pay dividends.

How do dividends work? If you own shares of a dividend-paying stock, then a dividend is paid per share of that stock. So, if you have 10 shares in Company ABC, and they pay $5 in cash dividends each year, then you will get $50 in dividends that year. While dividends can be paid on a monthly, quarterly, or yearly basis, they are most commonly paid out quarterly — so, four times a year. In this example, the $5 in cash dividends the company pays each year will most likely be distributed as $1.25 per quarter for each share of stock.

The most common type of dividends are cash dividends. Shareholders may choose to get this deposited right into their brokerage account. Stock dividends are another common type of dividend. In this case, shareholders get extra shares of stock instead of cash.

Both cash dividends and stock dividends are great income-generating assets that will earn more money for you.

As a shareholder, you can earn income when companies distribute profits to their shareholders. Look for stocks with a history of consistent dividend payouts and a high dividend yield. Keep in mind that dividend stocks are still subject to market fluctuations, and just because a company has paid a dividend in the past does not mean that they always will in the future.

Related content:

2. High-yield savings accounts and CDs

High-yield savings accounts and CDs are a great way to grow your savings, but most people have their money in accounts with low rates. Unfortunately, that means many of you are losing out on some easy money.

Savings accounts at brick-and-mortar banks are known for having really low interest rates. That’s because they have a much higher overhead — paying for the building, paying the tellers to help you in person at the bank, etc.

High-yield savings accounts offer an easy option for earning interest on your cash. Online banks often offer higher interest rates than traditional banks. As of the writing of this blog post, you can easily find high-yield savings accounts that can earn you above 4.00%.

Certificates of Deposit (CDs), another form of income-generating assets, are FDIC insured and provide a guaranteed interest rate over a specific term. Remember that access to your money is limited during the term of the CD. You will agree upon the term before putting your money in the CD. The terms typically vary in length from around 3 months to 5 years.

Money market accounts are also offered by banks and often with a higher yield than other types of savings accounts.

3. Real estate

Real estate is one of the most common income-generating assets that people think of.

Investing in rental properties is a popular way to generate steady cash flow. You can earn rental income from tenants, and properties typically appreciate in value over time.

Location and property management are important factors that can impact your return on investment.

By investing in real estate, you may be investing in residential properties, commercial real estate, short-term rentals, REITs, and more.

Recommended reading: How This Woman In Her 30s Owns 7 Rental Homes

4. Real estate investment trusts (REITs)

An REIT is a company that owns and manages income-producing real estate. They then sell shares to investors like stock.

By investing in REITs, you can make money in the real estate market without actually owning real estate.

So, if you don’t want to be a landlord, then this may be something for you to look into. This makes it much more passive than actually owning real estate and having to manage it.

You can even diversify your income stream with REITs by investing in different property types, such as residential homes, commercial office space, industrial, and retail store properties.

5. Bonds

Bonds are fixed-income investments that are issued by governments and companies. If you own a bond, you receive interest payments from borrowers on a regular basis.

An easy way to explain this is: When you buy a bond, you are giving someone a loan and they are agreeing to pay you back with interest.

Bonds with higher credit ratings are generally a safer investment but may offer lower interest rates.

6. Mutual funds

Mutual funds gather funds from investors to invest in stocks, bonds, or other securities. Basically, the funds are pooled together and there’s a fund manager who chooses the best investments.

Income-generating assets like this have multiple types of mutual funds available for multiple types of investors. Some of these fund types include bond funds, stock funds, balanced funds, and index funds.

Mutual funds typically have higher fees because they have fund managers who are actively trying to beat the market.

With a mutual fund, you get diversification because the fund manager mixes the assets in it.

7. Index funds and exchange-traded funds (ETFs)

ETFs and index funds are popular options for those who are looking to diversify their portfolio of income-generating assets.

This is because index funds and ETFs track a specific market index and invest in a wide range of stocks or other assets, instead of picking and choosing stocks in an attempt to beat the market. This is what makes them different from mutual funds.

They often have lower fees and higher diversification compared to actively managed funds.

8. Annuities

Annuities are long-term investments offered by insurance companies that give you a guaranteed income stream to build wealth. In exchange for a lump-sum payment or periodic contributions (such as monthly or annually), you’ll receive steady payments in the future.

The way it works is you pay premiums into the annuity for a set amount of time. Later, you stop paying premiums, and the annuity starts sending regular payments to you. Some are even set up to pay you back with a lump sum.

Annuities can be fixed or variable. A fixed annuity offers a guaranteed payment amount — which means a predictable income for you. As for a variable annuity, the payment amount does vary, depending on how the market is doing.

9. Websites and blogs

Starting a website can generate income through the money-making assets of advertising, affiliate marketing, or the sale of products and services.

Since I started Making Sense of Cents, I have earned over $5,000,000 from my blog through affiliate marketing, sponsored partnerships, display advertising, and online courses. These income-generating assets make sense for building wealth.

Blogging allows me to travel as much as I want, have a flexible schedule — and I earn a great income doing it.

Now, it’s not entirely passive, but I do earn semi-passive income from my blog.

You can learn how to start a blog in my How To Start a Blog FREE Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog

Day 2: How to decide what to write about (your blog niche!)

Day 3: How to create your blog (in this lesson, you will learn how to start a blog on WordPress)

Day 4: The different ways to make money with your blog

Day 5: My advice for making passive income with your blog

Day 6: How to get pageviews

Day 7: Other blogging tips to help you see success

Recommended reading: The 25 Most-Asked Blogging Questions To Get You Started Today

10. Royalties and intellectual property

Intellectual property, such as patents, copyrights, and trademarks, can generate income through licensing fees or royalties. This particular option is good for creative professionals, such as authors, musicians, and inventors, who are looking for income-generating assets.

Royalties are a way to earn income from your creative work or intellectual property. By granting others permission to use or distribute your intellectual property, you can receive ongoing payments known as royalties.

Whether you’re a musician, author, inventor, or artist, royalties offer a passive income stream as your creations continue to generate revenue over time.

Royalties can be paid out periodically or as a lump sum on these passive income assets, depending on your agreement with the licensee.

11. Stock photos

If you have a talent for photography, you can monetize your skills by selling stock photos on platforms such as Shutterstock or Adobe Stock. The more high-quality images you upload, the more potential passive income you can generate.

With stock photography, you simply upload photos that you have taken to a platform such as DepositPhotos, turning your pictures into income-generating assets. Then, you will receive a commission whenever someone buys one of your stock photos.

Stock photos are used for all sorts of reasons by websites, companies, blogs, and more. Businesses need stock photos because they are not usually in the business of taking photos of everything that they need. Instead, they can use stock photos to make their content, website, or business more visually appealing.

Some examples of stock photography include pictures of:

Travel, vacations, landmarks, outdoor adventures

Family members, such as parents, children, family gatherings

Food and drink

Cars, boats, RVs

Businesses, pictures of people in meetings, in an office.

Sports, professional events

Animals, such as household pets or wildlife

The photo possibilities are almost endless for this type of income-generating asset.

Recommended reading: 18 Ways You Can Get Paid To Take Pictures

12. Crowdfunding and peer-to-peer lending

Crowdfunding platforms enable you to invest in real estate deals with a smaller amount of money than buying real estate up front, giving you a passive income through rental income or even a property increasing in value.

Peer-to-peer lending platforms allow you to lend money directly to borrowers. Typically you can earn higher returns than traditional savings accounts, though there’s always the risk of a borrower not paying you back.

Both of these types of assets — crowdfunding and peer-to-peer lending — use technology to connect investors with those looking for funding.

13. Renting out storage space

If you own unused land or unused space in your home, renting it out for storage can be a simple way to generate passive income.

You can offer storage solutions for vehicles or boats. If you have a smaller space, then offer it to store personal belongings. You can rent out your driveway, closet, basement, attic, and more. You can even rent out a shelf.

A website where you can list your storage space is Neighbor. You can earn $100 to $400+ each month on this platform. This depends on the demand in your area and the type of income-generating assets you are renting out. And, you can choose who, what, and when — who to rent to, what things are stored, and when it will happen.

You can learn more at Neighbor Review: Make Money Renting Your Storage Space.

14. Short-term rentals

Short-term rentals can be a lucrative income-generating asset if you own properties in popular tourist destinations or business hubs.

Websites like Airbnb provide a platform to rent out your property to travelers for short periods, potentially generating higher returns than traditional long-term leases.

Furnished Finder is another website for short-term rentals. This is a way to connect with travel nurses in need of short-term housing.

Keep in mind that rental income can be affected by local regulations, potential vacancies, or seasonal fluctuations.

15. Car rentals

Car rental platforms like Turo allow you to rent out your car when you’re not using it. Assets that generate cash flow include your own wheels, and that means no significant initial investment besides the cost of the car you already own.

Be mindful of risks such as wear and tear, insurance, and potential damage caused by renters.

It’s an affordable alternative to traditional rental car companies for customers, and it’s a good way to make money if you’re already working from home and don’t need your car, or are a two-car household.

Turo is one of a few different places to rent out your car, turning your vehicle into one of your income-generating assets. Your car is covered by Turo with up to a $1 million insurance policy. You can also pick the dates for when your car is available and set your rates.

Turo says you can earn an average of $706 per month by listing your car on their site.

16. RV rentals

Similarly to car rentals, RV rentals can provide additional income by renting out your recreational vehicle when you’re not using it. Your RV could easily become one of your income-generating assets.

You may be able to earn $100 to $300 a day, or even more, by renting out your RV on RVShare.

If you have an RV that is just sitting there and not being used, then you may be able to earn an income with it by renting it out to others who are interested in RVing. Cash flow-generating assets like RVs are a win-win for both you and the renter who wants to experience life in a recreational vehicle.

You can learn more at How To Make Extra Money By Renting Out Your RV.

17. Vending machines

With a vending machine business, you can generate income by selling a variety of products, from food to fishing supplies, beauty products to baby items, and more.

You may be able to earn $1,000+ a month by running a vending machine business. That’s enough reason to take a closer look at income-producing assets like this.

You can learn more at How To Start A Vending Machine Business – How I Make $7,000 Monthly.

Questions about income generating assets

Here are common questions that you may have about income-generating assets:

How do I start passive income from nothing?

Starting passive income from nothing requires creativity and resourcefulness. You can begin by identifying skills you possess or interests that can be turned into income-generating opportunities.

What are the assets that generate income?

The assets I talked about above include:

Dividend-paying stocks and stock market investing

High-yield savings accounts and CDs

Real estate

Bonds

Mutual funds

Index funds and exchange-traded funds

Annuities

Websites and online businesses

Royalties and intellectual property

Stock photos

Crowdfunding and peer-to-peer lending

Renting out your storage space

Car rentals

RV rentals

Vending machines

How do I start buying income generating assets?

There are traditional investments or more creative options. Do as much research as you can before deciding which option fits you best.

What are good assets to buy?

After deciding if you want to purchase traditional investments or more creative options, choose an asset that you can afford and best fits your lifestyle.

What are the best assets to buy for beginners?

For beginners seeking income-generating assets, you may want to look into:

Dividend-paying stocks for your investment portfolio

Crowdfunded real estate investing: Platforms like Fundrise allow smaller investments with lower risk exposure.

ETFs and index funds: They provide diversification and passive income through dividends.

What is income generating real estate?

Income-generating real estate refers to properties that produce regular rental income, such as apartments, commercial properties, or short-term vacation rentals.

How do I start passive income in real estate?

There are a few ways that you can earn passive income from real estate, including:

Buying a property, such as an apartment building or duplex, and renting it out to tenants

Using real estate crowdfunding platforms

Investing in REITs

How to make passive income with real estate without owning property?

You don’t need to actually own property in order to make money with real estate. Instead, you can earn passive income from real estate by investing in REITs and using real estate crowdfunding platforms.

This is an option for those who want to be diversified with their income-generating assets but don’t want to spend all of their money or time on a single piece of real estate.

How to make $1,000 a day in passive income?

Making $1,000 a day in passive income with assets that produce income will not be easy. If it were easy, then everyone would be doing it, after all.

Making $1,000 a day in passive income may require a large amount of money up front, diversifying into different assets mentioned above, and lots of patience from you because it will take time to make that kind of money.

You may want to start off by focusing on building multiple income streams and reinvesting your profits as you earn them.

What to think about before investing in income producing assets?

There are many different things to think about when it comes to income-generating assets. You want to find the best assets to invest your money in that will also be the best fit for you.

Remember, as I said at the beginning of this article, not everything will be applicable to everyone. Everyone is different! You may prefer to create a stock photo portfolio and hate real estate, whereas someone else may really enjoy being a real estate investor — or it may even be the other way around.

Here are some of my tips if you are interested in income-generating assets:

Do your research and talk to experts —I recommend researching as much as you can on the asset you are interested in. And, if you still have questions, don’t be afraid to talk to an expert.

Diversify — One of the important parts of building a successful income-generating portfolio is finding ways to be diversified.

Think about the risks —When making money, there’s usually some sort of risk. I recommend evaluating the risks and seeing what you are comfortable with.

What are the best books on income generating assets?

Some highly recommended books on income-generating assets include:

The Simple Path to Wealth by JL Collins

The Millionaire Real Estate Investor by Gary Keller

The Little Book of Common Sense Investing by John C. Bogle

Income Generating Assets — Summary

I hope you enjoyed this article on the best income-generating assets. As you learned, there are many different types of assets that you can invest in so that you can earn an income.

The best income-producing assets, if they’re right for you, can truly change your life.

With these assets, you can build wealth through a reliable passive income, giving you peace of mind and freedom to live life on your own terms.

Are you looking to build income-generating assets? What are your favorite ways?

Whether you’re moving out of your parent’s house or leaving the dorm life behind, becoming a first-time apartment renter is a big and exciting step. However, if you don’t know the ins and outs of the rental process, the task can seem overwhelming. Luckily, we at Redfin put together a list of 8 key tips to help first-time renters find their perfect first apartment and make the transition as smooth as possible. Whether you’re renting an apartment in Los Angeles, CA, or in Brooklyn, NY, these tips will be invaluable in your journey to securing the ideal rental space.

1. Your budget needs to cover more than just rent

If you’re a first-time apartment renter, knowing how to budget for your first apartment is crucial. Your monthly rent will, of course, be the most considerable expense you need to account for, but there are other one-time and ongoing fees that you should be able to pay. Let’s take a look at these costs more closely.

Initial, one-time costs

Before moving into your new apartment, you should save enough money to pay for the following upfront costs:

Recurring costs

Once you’ve moved into your first apartment, there are several ongoing expenses you’ll need to cover every month:

Rent

Utilities, such as electricity, garbage, water, sewage, etc.

Internet and phone

Parking

Laundry

As a first-time apartment renter, this might be the first time you’re responsible for these types of expenses. The last thing you want to do is misjudge what you can afford because you forgot to factor in these essential components of your cost of living.

2. Make a list of needs, then prioritize them

Start with your dream apartment – what is your ultimate living situation? While you may not end up with everything on your list, it’s essential to understand what you value in your home. Some common needs for first-time apartment renters are:

Functional kitchen

Balcony, patio, or other private outdoor space

Closet and storage space

Proximity to work, nightlife, dog parks, or other amenities

Natural light and direction of exposure

Air conditioning

Building amenities, such as a gym, rooftop, or business center

Once you have your list, prioritize the items from most to least important. This will help you narrow down your choices and choose between similar properties.

3. Ask a lot of questions during apartment tours

There are some things you just need to know when you’re shopping for apartments. You may direct these questions to your prospective landlord, or you might have to do some research on your own. Here is a list of must-ask questions, but you may choose to add others depending on your needs.

How much is the rent?

Are utilities included? If not, how much do they usually cost?

How much is the security deposit?

How do I pay rent and utilities?

Is there a parking fee?

Is the apartment pet-friendly, and if so, what are the associated fees?

Are any deposits or fees refunded at the end of the lease?

Do I need proof of renters insurance?

What’s the application process, and is there a fee?

How long is the lease term?

How often does rent increase and by how much?

What alterations can I make to my apartment?

How is apartment maintenance dealt with?

Is there a property manager?

Am I responsible for any maintenance?

What amenities are available nearby?

Are there any particular policies I should know about?

These questions are just the beginning. You likely have special needs or preferences that should inspire additional questions. Keep a list of these questions with you when touring, along with a way of recording the answers.

4. Know the rental application requirements

Each apartment will have a different rental process. Generally, your process will include some or all of the following:

Fill out an apartment application

Show proof of income

Complete a credit check

Complete a background check

Provide rental history with the landlord’s contact information or a personal reference

Add a co-signer if you have a low credit score or no credit history

Include an optional cover letter

To show proof of income, you’ll likely need to provide your most recent pay stubs. You can also use an offer letter or letter from your employer if you’re moving for work. Many landlords or property management companies want to see that you have a reliable monthly income appropriate for the rent payment. While it depends on the apartment, there is often an income requirement that the renter needs to make 2 to 3 times the monthly rent amount.

5. Clarify the parking situation

Some rentals come with a designated parking area or parking spot(s). If you plan to live with a roommate and you both have cars, are there enough parking spaces to easily accommodate both of you? When there are not enough parking spaces or tandem parking, roommates will often switch off week to week or find another acceptable compromise. If the apartment complex does have parking spaces, be sure to ask if this comes at an additional cost. Parking fees are becoming increasingly common at rental properties.

On the other hand, many apartments don’t come with parking, especially in bigger cities like New York City or San Francisco. In this case, pay close attention to the street parking. The street parking signs will tell you which days or times of day parking is limited or prohibited (usually for street-sweeping or snow plowing). But you should also note how many parking spaces are free on your street— is there plenty of room or are cars packed bumper to bumper? Streets with cars parked close together usually mean that parking is difficult to find.

6. Know the best time of year to rent an apartment

You can’t always control when you need to move, but if you do have flexibility, choosing the right time of year to rent an apartment could have a large impact. If your main concern is price, you’ll want to look for an apartment during the winter months. Typically, most people move in the summer months (college students moving away from home, etc.), so demand and prices are typically highest during this time and lowest in the winter. Keep in mind that while rent prices may be lower, there might not be a large selection of apartment complexes with availability.

On the other hand, if your ideal apartment is your top priority, then moving during the summer may be a better option. Most renters sign 12-month leases in the summer. Therefore, most leases usually also end around that time. This means the highest number of new apartments are coming on the market, so you’ll have plenty of options to choose from. The main downside here is that rent prices will typically be higher, and you’ll need to act fast before the best apartments are off the market.

7. Thoroughly read and understand the lease agreement

As a first-time apartment renter, reviewing your lease agreement is one of the most important steps to getting your apartment. Though the lease may contain complex language, it will outline the most important agreements you’re making by signing it. Here are a few things you should make a note of:

The length of your lease

The pet policy and any special terms (like additional fees)

Deposit requirements and how your deposit is returned

Sub-letting rules

Utility responsibilities

Maintenance procedures

Liens or claims to your property if you don’t pay rent

When in doubt, having your lease reviewed by a landlord-tenant attorney is a great idea. The attorney will be able to catch any illegal provisions, explain how provisions work, point out unfavorable provisions and their consequences, and suggest changes that provide you with a more favorable lease.

8. Get renters insurance

In many cases, carrying renters insurance may be required by your landlord, especially if you’re a first-time apartment renter. Even if it isn’t, it’s still a good idea to have it – regardless of if you’re a long-time tenant or a first-time apartment renter. A renters insurance policy protects you in three significant ways:

Personal property protection: If someone steals, damages, or destroys your personal belongings, you will receive a payout (minus the deductible).

Personal liability: If someone gets hurt in your home, renters insurance will pay for medical bills and lost wages, depending on the terms of your policy. You may also be covered if you end up in a lawsuit.

Loss of use: If your apartment becomes uninhabitable, loss of use coverage pays for your expenses, up to coverage limits, while you live outside your home.

Always be sure to review your policy carefully. It’s a good idea to create an inventory of your personal belongings so that you both have a record of what you own and ensure your coverage limits are high enough to protect you in the event of a total loss. If you are unsure about any part of your insurance policy, speak with your agent.

A final note on renting your first apartment

Searching and finding a perfect apartment rental requires some diligence, patience, and preparation. By following these tips, you can avoid possible pitfalls and make your apartment hunting process as seamless as possible, especially if you’re a first-time apartment renter.

As technology continues to advance across the board, it should come as no surprise that it is playing a powerful role in shaping the property management industry and its future progression. The rental market is getting more and more competitive – for both property managers and tenants – and many property owners are using amenities as a way to stand out from the crowd. According to the National Apartment Association, the top amenity today’s renters are demanding revolves around connectivity: renters prefer anything that can make their lives easier through technology.

Tenants want to stay connected to the digital world from the comfort of their homes, whether on a mobile device or desktop, for work or entertainment. One study shows that Americans spend over 10 hours each day interacting with digital devices, and nearly 40% of young adults (ages 18-29) access the internet almost constantly. In the past, property managers may have offered internet services as an additional perk to entice renters in competitive markets, but now connectivity may be seen as a necessity to keep up. By including internet services as an amenity for tenants at your rental property, you can increase your property’s desirability and decrease vacancy time.

Including Internet Services: The Good

Offering free internet as an amenity isn’t an industry standard, so going this route can set you apart from your competitors. Rental property owners can provide high-speed internet in the common areas of their multifamily properties, or include personal access in each unit – either way, you can easily market reliable and fast broadband internet as a way to attract tenants. In addition to attracting tenants, offering a service that other properties don’t include can also keep tenants around longer as they will have to consider taking on an additional expense if they move.

If you’re already offering cable TV services at your property, internet should be an easy and relatively inexpensive add-on. You may even be able to negotiate a deal with your internet service provider if you’re planning on offering internet services to a large quantity of units within one property. Some property managers choose to include internet costs as part of a tenant’s rent at a discounted rate, while others charge a set fee on top of the monthly rent. Think about it this way: if your multifamily property has even 10 units, and each unit pays approximately $100 each month for internet services, your building is paying $12,000 a year for Internet. If you absorb this cost yourself and can secure it at a discounted rate, charging your tenants directly for internet services can actually turn out to be a profitable business.

Including Internet Services: The Questionable

Providing your tenants with internet services can come with some risk. One concern is that tenants may look to their landlord for IT support. The last thing you need as a property manager is tenants reaching out about connectivity or technology concerns. To combat this issue, clearly provide your tenants with information on whom they should contact with any questions or concerns.

Security can be another issue that property managers face when it comes to offering internet services to their tenants. Tenants want their personal networks to be secure and protect their personal information, while property managers want to ensure their network is only used for legal activity. To protect yourself, you should include specific language in your lease about the terms of use, prohibiting any illegal activity. This is also something you should address when choosing an internet service provider.

At the end of the day, deciding to provide internet services for your tenants at your rental properties will depend heavily on the supply and demand in your rental market. If your vacancy rate is low and you don’t experience much competition when it comes to finding tenants, you may not need this additional service to attract and retain tenants. If you live in a market where supply and demand are both relatively high, you might consider providing internet to set yourself apart. Most tenants want access to the internet in their homes, and including internet services in the monthly rent is usually one of the features tenants appreciate the most.

Homeowners can now see potential short-term rental income estimates on Realtor.com thanks to an integration with Airbnb.

Short-term rental earnings estimates for hosting one room or the entire house will be available to homeowners via Realtor.com’s My Home dashboard, according to an announcement on Thursday.

The estimated earnings for a seven-day rental are based on Airbnb data from similar listings in the ZIP code.

A recent survey from Realtor.com and CensusWide found that 39% of homeowners have or would consider renting out part of their primary home, with 23% having rented out their home previously or are planning on doing so in the future and 16% reporting that they are considering renting out part or some of their home in the future.

Financial reasons are the primary motivator for homeowners to rent out their home, as 34% who have rented or plan to rent out their home are doing so in order to save money for a home purchase with a higher mortgage rate, while 29% are doing it prepare for potential upswings in a variable mortgage and 21% are doing it to help pay their current mortgage.

According to Realtor.com, the integration will also enable homeowners to see if it is a good idea to rent out their current home as an alternative to selling it. Of the homeowners surveyed, 60% reported they would consider renting out their current home rather than selling, if they look to buy or rent elsewhere, with 21% citing extra income from a renter and 19% citing the ability to maintain the home equity they have built as primary motivators.

“Short-term rentals are a great way to help with some of the costs of homeownership – renting out their house for a couple days or weeks out of the year when it’s not in use could generate extra income that can be put toward the mortgage, maintenance, or even help cover the cost of a vacation,” Mausam Bhatt, the chief product officer of Realtor.com, said in a statement. “By arming homeowners with information about how much they could potentially make by renting a room or their whole home on Airbnb, Realtor.com is helping them better understand their options and in turn make more informed decisions about their home.”

Realtor.com’s integration with Airbnb comes as many metro areas are looking to crackdown on short term rentals. Earlier this month, thousands of New York City Airbnb listings vanished from the market as the city introduces some of the strictest regulations in the U.S. for short-term rentals. City councils in Dallas, Philadelphia and New Orleans have passed their own restrictions on short-term rentals.

Running an Airbnb in L.A. has never been more profitable.

As the city tries to crack down on illegal listings, and advocacy groups complain about the company’s effect on L.A.’s housing crisis, hosts are charging higher rates than ever while raking in bigger and bigger payouts.

But don’t expect them to talk about it.

Data show that a vast number of homes are operating without an active registration, which is required by the city to operate a short-term rental. Several such hosts spoke to The Times anonymously for fear of being fined by the city or, worse, getting their listing shut down by Airbnb.

“This is my primary source of income,” said one host who operates three different listings. “I’m finally making a decent living off of this. One listing alone wouldn’t cut it.”

Advertisement

Since 2020, revenues for hosts have steadily risen far beyond pre-pandemic levels. The average revenue climbed to $17,654 in 2022, up more than $4,000 year-over-year, and the numbers are at a similar pace for 2023, according to data from short-term rental analytics company AllTheRooms.

In total, L.A. hosts earned a combined $375 million last year, a spokesperson for Airbnb said.

A few factors contribute to the rise. For one, daily rates for Airbnb rentals have spiked over the last four years, swelling from $152 in 2019 to $244 in 2023. It’s a trend that’s happening across the short-term rental industry, as hotel and VRBO rates have steadily risen since the COVID-19 pandemic as well.

Basic supply and demand is another factor. Save for a drop during the first few months of the pandemic, Airbnb occupancy rates have largely stayed consistent, with the average rental occupied more than 40% of the time. But the amount of listings has dropped dramatically.

In August 2019, there were 16,973 Airbnb listings in L.A. Currently, there are 7,360.

Supply is down for now, but advocates worry that if revenues continue to rise, more homeowners will convert properties into Airbnbs.

Advertisement

Much of the drop was due to the pandemic, but the supply hasn’t risen since 2020 partly due to the city’s enforcement of its Home-Sharing Ordinance, a law that went into effect in 2019 that limits Angelenos to hosting only short-term rentals in their primary residence — homes where they can prove they live at least six months per year.

L.A. and Airbnb have worked in tandem over the years to enforce the law, launching a system in 2020 that streamlines the process of identifying and taking down illegal short-term rental listings.

It has been effective; the number of listings for short-term rental units across all home-sharing sites has dropped more than 70% over the last four years, going from roughly 36,600 in November 2019 to just under 10,000 in June 2023, according to the city planning department.

But plenty remain.

The Times previously reported that thousands of listings violate the law, and last year, a report claimed that 22% of L.A. listings host guests for more than 180 days a year.

“I can’t afford to rent out my place for only six months a year. I’d lose half my revenue,” said one host who rents a two-bedroom apartment in Hollywood on Airbnb.

Two other Airbnb hosts hung up the phone mid-interview when asked about whether their listing was their primary residence, or whether their registration number was valid.

“It’s a don’t ask, don’t tell system. I can’t afford to have my business threatened over a registration number,” one said.

The average daily rate for an Airbnb in L.A. has risen to $244 in 2023.

(K.C. Alfred San Diego Union-Tribune)

As of August, there are 4,293 active home-sharing registrations, according to the city’s planning department. But on Airbnb alone, there are currently 7,360 listings up for rent.

“L.A. has a big enough rent problem on its own, and then you have a rogue industry that swoops into the city and starts taking rental properties off the market,” said Peter Dreier, a professor at Occidental College.

Dreier worked with the team that drafted Measure ULA, a new tax that funnels money toward affordable housing initiatives, and said that the short-term rental industry is contributing to both the housing crisis and homelessness crisis.

“When you take units off the market and rent them to tourists, one consequence is that it leads to more people fighting over fewer units. And that leads to higher rents,” he said.

The planning department is preparing a report with other departments analyzing enforcement of the Home-Sharing Ordinance. It will provide recommendations to the City Council on how to improve the program.

In the meantime, more listings bring more tax dollars. L.A. charges a 14% transient occupancy tax, often called a “bed tax,” paid by guests in a hotel or a short-term rental such as an Airbnb.

In the 2021-22 fiscal year, the city collected $33.88 million in transient occupancy taxes, according to the planning department.

It’s a hefty amount, but a report from McGill University urban planning professor David Wachsmuth suggests that the city could be raking in even more by fining illegal short-term rental listings.

The study claimed that 45% of all short-term rental listings are illegal in one way or another, and that the city could have levied between $56.8 million and $302.2 million in fines in 2022.

“I’ve never paid a fine, but my guests pay the tax. As long as the city’s getting money from somewhere, they’ll be fine,” said the Hollywood Airbnb host.

Randy Renick, an attorney with Hadsell Stormer Renick & Dai LLP, serves as executive director of Better Neighbors LA, a coalition that includes hotel employees, renters’ rights groups and housing advocates. He co-founded the group in 2019 as a public education campaign to emphasize the impact that short-term rentals have on communities.

He said rental hosts bend the rules in a few ways. One strategy is the bait-and-switch, where a host will advertise that a property is somewhere near the border of Los Angeles, such as West Hollywood, and thus not subject to L.A.’s stringent rules. But when renters show up, the property is actually in L.A.

Others give false registration numbers — some more cleverly than others.

“1234567 was popular for a while,” Renick said.

Some simply use expired registration numbers, and others used an active registration number but for several properties.

The organization’s website keeps a hotline for Angelenos to call and report illegal listings in their neighborhood, and Renick said they receive multiple calls per week.

From there, they urge the city to take action for matters both small and large. Sometimes it’s a call asking to enforce a fine on a certain property, and sometimes it’s a campaign on how short-term rentals can drive up long-term rent in an area by taking homes off the market and renting them to tourists.

“We try to show the impact of short-term renting and how it’s contributing to the housing and homelessness crisis,” Renick said. “Robust enforcement will result in returning thousands of units back to long-term rental.”

He pointed to Santa Monica and New York City as two cities that L.A. could model itself after. Santa Monica has a robust enforcement system, including multiple full-time staff focused on interviewing owners and issuing fines to illegal listings.

The coastal city allows only short-term rentals (less than 30 days) if the host lives on the property throughout the visitor’s stay. New York City adopted a similar rule last year, and the enforcement begins on Tuesday.

Though it has a long way to go, Renick said L.A. has raised the bar on proof required to show that a listing is the host’s primary residence.

Frank Tai, the owner of a luxury beachfront rental in Playa del Rey, has seen that process firsthand. He has only one listing and makes sure to renew his license every year, but the process has gotten more laborious over the years as both the city and Airbnb look to catch illegal listings.