Wachovia said today that it will discontinue wholesale loan origination beginning this Friday, leaving very few players in the broker-originated space.

It’s unclear how many jobs will be lost as a result of the shift in operations, but that will likely be disclosed when the company announces second quarter results tomorrow.

It is assumed that loans already locked and in progress will continue to be processed until a certain funding cut-off date.

Tim Wilson, Head of Loan Origination for Wachovia Mortgage, explained that the bank and mortgage lender was repositioning itself to work with clients who have existing relationships and live in areas where the bank’s franchises are located.

The Charlotte-based bank’s third-party origination unit Vertice is apparently not affected by the changes, and will continue to offer broker-originated loans.

Wachovia has been hard-hit by the ongoing mortgage crisis, especially after acquiring option arm specialist Golden West for a staggering $25 billion in 2006.

The company has since stopped originating option arms with the negative amortization feature, and has waived prepayment penalties tied to the so-called toxic loans.

In early June, Wachovia said it would contact all portfolio loan applicants whose loans were submitted by mortgage broker clients in what it referred to as “enhanced customer service”.

The bank is expected to report a second quarter loss in the range of $2.6 billion to $2.8 billion, according to Reuters estimates.

That includes a $4.2 billion increase in loan-loss reserves, with $3.3 billion going towards those nasty pick-a-pays.

Shares of Wachovia slipped 71 cents, or 5.37%, to $12.52 in after hours trading.

For months, I’ve been banging on about the lack of a refinance program for private-label mortgages, those not backed by Fannie Mae and Freddie Mac.

Sure, HARP is great for underwater homeowners whose loans are owned by the pair, but what about those who aren’t so fortunate?

I’ve brought up proposals such as HARP 3 on several occasions, along with Oregon Senator Jeff Merkley’s refinance program that targets those who hold mortgages that aren’t government-backed.

The Obama administration has also been open to an expanded HARP for these types of borrowers, but without Congressional approval, any stirrings of such relief continue to fall on deaf ears.

But apparently these borrowers are actually receiving some assistance outside of HARP.

45% of Borrowers Have Received a Loan Modification

A new commentary released today by Fitch Ratings revealed that about 45% of all underwater borrowers with private-label mortgages have received a loan modification.

The company noted that loan modifications, distressed loan liquidations, and home price gains have reduced the number of underwater loans in private-label residential mortgage-backed securities (RMBS) by a sizable 25%.

There are still roughly 1.5 million underwater loans in these at-risk securities, though that number has fallen from 2.04 million.

Perhaps the biggest driver has been home price increases, with double-digit growth seen in some of the hardest-hit areas, including Arizona, California, and Nevada.

Assuming home prices continue to tick higher, which they’re expected to, the number of waterlogged loans will continue to drop at a steady clip.

While this is all good and well, the carnage is far from over. Fitch said about one-third of all outstanding borrowers in private-label RMBS pools (no pun intended) remain underwater.

It’s unclear how deeply underwater they are, but underwater nonetheless.

Additionally, the company projects some regions of the United States, notably the Northeast, to experience further home price declines before bottoming.

Why This Is Good and Bad

At first glance, it appears to be good news. Underwater borrowers with all types of loans are generally getting the help they need to continue making mortgage payments and hold on to their homes.

This benefits everyone involved because it makes for a stronger housing market. But the numbers can be deceiving.

Sure, 45% of these non-Fannie/Freddie underwater borrowers received loan mods, but what type of loan mod?

Did they get a $100 off their loan each month? Did they get a .125% interest rate reduction? Was principal forgiveness involved?

We don’t know what level of assistance they received, and if history tells us anything, a lot of these private loan mods weren’t all that attractive, at least not compared to HARP.

Through HARP, borrowers have been able to refinance their mortgages to interest rates a few percentage points lower than their previous rate.

That’s serious assistance, enough to stick around and see this crisis out. The private mods are another question.

This improvement also doesn’t bode well for an expanded HARP for non-Fannie/Freddie borrowers. The more improvement we see and hear about, the less likely Congress will be to act.

So the prospects of a new assistance program are dwindling each day.

The Multnomah Pilot Program

There is a small glimmer of hope though. Last month, the Treasury Department approved a new pilot program to assist underwater borrowers without Fannie and Freddie loans.

The so-called “Rebuilding American Homeownership Assistance” (RAHA) Pilot was launched in Multnomah County, which includes the city of Portland.

It’s limited to borrowers with “significant negative equity” who intend to stay in the prpoerty for 5+ years. They must not own any other residential property and be current on the mortgage.

Welcome to the land of majestic Mount Rushmore, endless prairies and the dazzling Badlands.

When it comes to finding your forever home or maybe just a fresh start, South Dakota offers a ton of appealing options. From bustling urban hubs to cozy lakeside towns, this guide to the best places to live in South Dakota is your golden ticket to discovering the towns that boast excellent schools and stable job markets in undeniably beautiful surroundings.

Population: 196,528

Average age: 34.2

Median household income: $66,761

Average commute time: 18.5 minutes

One-bedroom average rent: $995

Sioux Falls is often considered one of the best places to live in South Dakota, and it’s easy to see why. This bustling city is a haven for outdoor enthusiasts, artists and aspiring professionals alike. The Big Sioux River winds its way through town, offering scenic beauty and outdoor activities like kayaking and fishing, right at your doorstep. But if you’re more of an indoor person, don’t worry; the city is home to the Washington Pavilion, a unique space with an art gallery, science museum and even a performing arts theater.

When it comes to everyday life, Sioux Falls is as practical as it is picturesque. The city boasts a robust job market, with opportunities in healthcare, financial services and retail, among other industries. Schools are top-notch, offering a quality education for the younger generation, while the healthcare facilities are some of the most advanced in the area. Ease of living is another big draw — traffic jams are a rarity, and most amenities are just a short drive away.

Population: 76,184

Average age: 37.2

Median household income: $58,072

Average commute time: 15.7 minutes

One-bedroom average rent: $1,205

If you’re thinking about the best places to live in South Dakota, Rapid City should be on your radar. Imagine a city where you can have breakfast Downtown, hike in the Black Hills National Forest by lunchtime, and be back in time for a locally brewed beer from Lost Cabin Beer Company and a buffalo burger for dinner. This isn’t a fantasy; it’s just an average Saturday in Rapid City.

Rapid City is surrounded by pristine nature and serves as the ideal home base for those looking to explore natural wonders like Mount Rushmore and the Crazy Horse Memorial. With an eclectic mix of art galleries, cozy coffee shops and historic architecture, Downtown Rapid City is more than just a pit stop, it’s a destination in its own right.

The Rapid City economy is strong, buoyed by tourism and a fast-growing tech industry, so you’ll find a variety of career options. Schools are solid, and there are ample parks and recreational facilities for kids and adults alike. The city also hosts a series of community events throughout the year, from summer concerts to winter ice-skating festivals.

What you won’t find? The hassles of big city living. Traffic is manageable, the cost of living is reasonable, and people generally say “hello” when you pass them on the street. Rapid City captures the essence of South Dakota — friendly, scenic and endlessly fascinating.

Population: 23,577

Average age: 24.5

Median household income: $53,845

Average commute time: 13.3 minutes

One-bedroom average rent: $940

Brookings emerges as a compelling choice as one of the best places to live in South Dakota, especially for those who appreciate a blend of intellect and community spirit. Home to South Dakota State University, the town has an atmosphere brimming with youthful energy and academic curiosity.

The McCrory Gardens offer a breath of fresh air and botanical beauty, while the Children’s Museum of South Dakota provides a magical world of learning for the youngest residents. College sports are a big deal here, and even if you’re not a student, you’ll find yourself swept up in the fervor of a Jackrabbits football game before you know it.

Excellent schools make Brookings ideal for families, and there’s a burgeoning job market in industries like agriculture, healthcare and education. Shopping and dining options are plentiful, offering everything from homegrown produce at the local farmers’ market to sushi and international cuisine. The town even has an active arts scene with frequent community theater performances, art walks and concerts. Safe streets and a strong sense of community make Brookings a place where neighbors know each other and people look out for one another.

Population: 12,358

Average age: 36.1

Median household income: $52,258

Average commute time: 17.6 minutes

One-bedroom average rent: $775

Known for its breathtaking landscapes, Spearfish is encircled by the Black Hills, Spearfish Canyon and a wealth of outdoor opportunities. Whether you’re into mountain biking, hiking or fishing, you’re practically destined to become an outdoor enthusiast here. But Spearfish isn’t just about the great outdoors; it’s also a hub for education and culture. The town is home to Black Hills State University, which adds a layer of youthful energy and intellectual depth to the community, along with venues like the Matthews Opera House & Arts Center, showcasing everything from plays to musical acts.

On the practical side of everyday life, Spearfish delivers and then some. The local economy is strong and diverse, benefiting from a mix of education, tourism and small businesses. Its public schools are top-rated, making it a safe bet for families, and the community itself is close-knit, often gathering for seasonal events and festivals. Plus, unlike some small towns where you have to drive miles for basic amenities, Spearfish has a solid range of shopping and dining options.

What truly sets Spearfish apart is its genuine sense of community combined with the backdrop of natural wonder. It’s a place where you can catch a university lecture one evening and find yourself fly fishing in crystalline waters the next morning.

Population: 28,324

Average age: 35.8

Median household income: $58,439

Average commute time: 10.9 minutes

One-bedroom average rent: $845

Known as “Hub City,” Aberdeen serves as a regional hub for healthcare, commerce and culture. The city boasts several landmarks like the Aberdeen Community Theatre and the Dacotah Prairie Museum, both of which offer regular events that enrich the social scene. If you’re in the mood for something more outdoorsy, Wylie Park and Richmond Lake are perfect spots for fishing, camping and unwinding under the South Dakota sun.

Aberdeen shines in terms of everyday convenience and quality of life. The job market is steady, with opportunities in healthcare, education and manufacturing. Educational facilities, from elementary schools to Northern State University, offer top-notch learning environments. Even better, Aberdeen has a low cost of living, making it easier to stretch a dollar whether you’re buying a house or enjoying a night out at one of the town’s tasty restaurants.

Population: 14,000

Average age: 38.7

Median household income: $69,868

Average commute time: 12.5 minutes

One-bedroom average rent: $755

As the state capital, Pierre is a hub of political activity, and you can feel the historical gravitas just by walking near the South Dakota State Capitol building with its iconic copper dome. But the city offers more than just legislative action; it’s also a sportsman’s paradise. Sitting on the banks of the Missouri River, Pierre is an angler’s dream come true with an abundance of walleye, and it’s no slouch when it comes to hunting either, offering some of the best pheasant hunting in the United States.

By and large, life in Pierre is straightforward and hassle-free. The local job market is solid, primarily driven by government jobs, healthcare and education. There’s a lot to do here for singles and families, whether it’s hiking along the scenic LaFramboise Island Nature Area or taking part in the many community events that pepper the town’s calendar. Pierre offers a unique blend of outdoor activities and political buzz, making it a distinctive spot for those looking to experience the best of South Dakota.

Population: 11,802

Average age: 23.3

Median household income: $47,920

Average commute time: 14.6 minutes

One-bedroom average rent: $995

Home to the University of South Dakota, Vermillion is a small but lively town where brains meet beauty on the banks of the Missouri River. You’ll find a mix of students, professors and residents enjoying everything from Coyotes football games to riverside picnics. The National Music Museum — featuring an awe-inspiring collection of musical instruments from various epochs and cultures — is another local treasure that elevates the town’s appeal.

The educational ecosystem in Vermillion is top-notch, with excellent public schools complemented by the intellectual resources of the university. Employment opportunities are ample, thanks to the university and a variety of small businesses. You won’t be stuck in traffic for hours; instead, you can spend that time enjoying local parks or taking in a college basketball game. What’s more, the cost of living here is quite reasonable, making it easier to enjoy what the town has to offer without breaking the bank.

Population: 15,453

Average age: 41.3

Median household income: $59,190

Average commute time: 11.6 minutes

One-bedroom average rent: $632

In a state rich with scenic beauty and friendly communities, Yankton stands out as one of the best places to live in South Dakota. Located along the Missouri River and famously the former Dakota Territory capital, Yankton melds historical significance with an array of modern attractions. Outdoorsy types will be quick to appreciate the town’s proximity to Lewis and Clark Recreation Area, where water sports, camping and hiking opportunities abound.

Everyday life in Yankton checks off all the boxes for a well-rounded experience. The local economy is buoyed by a mixture of manufacturing, healthcare and retail jobs. Education is a strong suit as well, with a range of public and private schools that consistently earn high marks. Local businesses — from cozy coffee shops to essential grocery stores — meet daily needs while the friendly residents make you feel part of a genuine community. Events like the annual Riverboat Days festival encapsulate Yankton’s communal spirit and offer an entertaining diversion for residents young and old.

Population: 22,722

Average age: 37.6

Median household income: $56,520

Average commute time: 13.5 minutes

One-bedroom average rent: $630

Known for its stunning lakes, particularly Lake Kampeska and Lake Pelican, Watertown is a haven for anyone who loves water sports, fishing or just gazing at beautiful sunsets over the water. And don’t forget the town’s signature attraction, the Bramble Park Zoo, which boasts an impressive collection of wildlife and offers educational programs designed for residents of all ages. Watertown is also home to the Redlin Art Center, showcasing the works of Terry Redlin, a renowned American wildlife painter, making it a hidden gem for art aficionados.

Watertown offers a high standard of living while maintaining that cherished small-town charm. The job market is steady with a focus on manufacturing, healthcare and retail industries. In terms of attractions, Watertown has plenty to offer, from shopping malls to restaurants that go well beyond the standard small-town fare. You’ll also find a rich social fabric here, marked by community events like outdoor concerts and seasonal festivals that provide plenty of opportunities for mingling with neighbors.

Population: 6,071

Average age: 37.0

Median household income: $58,564

Average commute time: 11.8 minutes

One-bedroom average rent: $640

Home to Dakota State University, Madison is a hub for technology and innovation, a place where you can bump into cybersecurity experts as easily as lifelong anglers. Speaking of lakes, Lake Herman and Lake Madison offer ample opportunities for fishing, boating and picnics, making them popular spots for family outings or tranquil solitude.

Madison delivers on the practicalities of daily life, too. With a stable job market centered around education, healthcare and local business, making a living here isn’t a high-stakes gamble. Plus, community events like the annual Prairie Village Jamboree add a layer of entertainment and social engagement that keeps life interesting.

Settle down in South Dakota

Whether you’re an outdoor enthusiast, a tech whiz or someone who just wants to enjoy the simple pleasures of a tight-knit community, South Dakota has something for everyone. From the buzz of the state capital in Pierre to the academic atmosphere of Vermillion, or the natural allure of Watertown, the Mount Rushmore State is an undiscovered gem for those looking to improve their quality of life.

Making a list of the best places to live in South Dakota isn’t just about numbers and statistics — it’s about understanding the lifestyle, culture and opportunities that make each place unique. So pack your bags and set your GPS, because your dream apartment might just be in a South Dakota zip code.

The Possible Card — issued by Coastal Community Bank, in partnership with Possible Finance — began slowly rolling out to the public in April 2023. As of this writing, the card is available in most states, with the exception of Hawaii, Nevada and Maryland.

While still in its early stages, the Possible Card won’t help propel your credit journey forward because it currently doesn’t report payments to major credit bureaus like TransUnion, Equifax and Experian. Even once it begins reporting payments, it still won’t be your most cost-effective option. Possible Finance touts “peace of mind” that you won’t be charged interest, but there’s a big caveat: Instead of an annual percentage rate, the card has a monthly fee.

Monthly fees on credit cards are a hot trend now, especially among young financial technology companies (fintechs). But depending on the balance you’re carrying, that fee can be more expensive than interest charges you’d find on a traditional credit card.

The Possible Card does offer predictability in terms of your monthly payment, and it also allows you to bypass a credit check and security deposit. But unlike a security deposit, which is refundable, those monthly fees won’t be. Plenty of other credit cards can jump-start your credit-building goals at a lower cost.

Here’s what you need to know about the Possible Card.

🤓Nerdy Tip

While any credit card’s rewards, benefits and fee structure can be adjusted at any time, new cards from startup financial technology companies are particularly prone to significant changes as they find their place in the market. Keep that in mind as you research your credit card options.

1. The monthly fee adds up

The monthly fee to hold the Possible Card is either:

$8 per month ($96 annually) for a $400 credit limit, or

$16 per month ($192 annually) for an $800 credit limit.

That makes the Possible Card more expensive than similar newcomers in its class. For example:

The Tomo Credit Card (currently waitlisted as of September 2023) charges $2.99 per month. There’s no credit check, upfront deposit or APR.

The Pesto Mastercard costs $3.33 a month, and while a deposit is required, it can be an asset instead of cash.

In fact, for no monthly or annual fee at all, you could consider cards like the Chime Credit Builder Visa® Credit Card, which lets you set your own security deposit, or the Grow Credit Mastercard, which has a free membership tier. Neither card carries an APR, neither conducts a credit check, and all of these aforementioned cards report your payments to credit bureaus.

Or, you could fare even better with a traditional secured credit card. Yes, you’ll have to come up with a one-time security deposit upfront, but for many of the best secured credit cards, you need a minimum of just $200, or nearly what you’d pay — every year and nonrefundable — for the Possible Card’s higher-limit version. Plus, many traditional secured cards come with upgrade paths to better products. The Possible Card does not, nor do many newer fintech-backed cards, for that matter.

The Discover it® Secured Credit Card is a good example of the kind of features to look for in a starter card. It requires a minimum security deposit of $200, but it has a $0 annual fee and earns rewards. It reports payments to all three major credit bureaus, and Discover begins automatic reviews starting at seven months to see whether you qualify to upgrade to an unsecured card and get your deposit back.

🤓Nerdy Tip

If you’re approved for the Possible Card, you can immediately start using the virtual card if you enroll in autopay. Otherwise, you’ll have to wait for the physical card to arrive in the mail.

2. There’s no credit check

The Possible Card doesn’t require a credit check and instead relies on a cash-flow-based underwriting algorithm to determine whether you qualify. But that underwriting process requires you to link an eligible account through a third party called Plaid.

This practice of skipping a credit check in exchange for linking a bank account has become a fairly common practice for certain credit cards, especially newcomers backed by fintechs. But there are better credit cards that don’t require a credit check.

The previously mentioned Chime Credit Builder Visa® Credit Card, for instance, requires opening a Chime Spending Account, but it doesn’t charge any fees or interest. It’s a secured credit card with a flexible deposit. The amount of money that you move from the spending account to the Credit Builder secured account is the amount you have available to spend.

3. No APR or late fees apply, but don’t be fooled

Some credit cards that charge monthly fees instead of interest market the idea of being “predictable,” for budgeting purposes. Possible Finance claims on its website that the monthly fee is cheaper than the charges on a traditional credit card, but that’s misleading. For most credit cards, interest charges don’t apply at all if you pay off the balance in full every month.

With the Possible Card, you’ll owe the monthly fee whether you carry a balance or not.

Depending on the size of your balance, that monthly fee could cost more than the interest charged on a traditional credit card, especially in cases where the card’s credit limit is relatively low. You can use the sliding scales below to illustrate this:

For context, the average APR for credit cards assessed interest in May 2023 was 22.16%, according to Federal Reserve data. If you have less-than-ideal credit, that percentage may be higher.

Trying to get approved for a card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

4. You can carry a balance over a short term

Unlike some credit cards in its class, the Possible Card allows you to revolve a balance, up to a limit. The card’s Pay Over Time option lets you pay off the balance over four installments if you schedule automatic payments and enroll in the app. There’s no additional charge to use this option as long as the account has a balance of at least $50 and no pending payments.

The downside of the Pay Over Time feature is that the card will be locked and cannot be used for new purchases or automatic recurring expenses until the installment loan is paid off. But the benefit is that this guardrail can prevent you from taking on more debt than you can handle.

If you’re using your Possible Card to make automatic recurring payments for streaming services or other expenses, make sure to change your payment method when you opt in to the Pay Over Time feature.

5. It doesn’t report payments to credit bureaus

The Possible Card is still in its infancy and does not report payments to the credit bureaus as of this writing. The company shared in an email that it has plans to start reporting payments to one bureau in the fourth quarter of 2023.

When your goal is to build credit with a credit card, reporting payments to the three major credit bureaus is a must-have feature. Ideally, you want your credit history to be recorded by all of them so that future lenders can access that information easily.

See more from Chime

Chime says the following:

The Chime Credit Builder Visa® Card is issued by Stride Bank, N.A., Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa credit cards are accepted.

To apply for Credit Builder, you must have received a single qualifying direct deposit of $200 or more to your Checking Account. The qualifying direct deposit must be from your employer, payroll provider, gig economy payer, or benefits payer by Automated Clearing House (ACH) deposit OR Original Credit Transaction (OCT). Bank ACH transfers, Pay Anyone transfers, verification or trial deposits from financial institutions, peer to peer transfers from services such as PayPal, Cash App, or Venmo, mobile check deposits, cash loads or deposits, one-time direct deposits, such as tax refunds and other similar transactions, and any deposit to which Chime deems to not be a qualifying direct deposit are not qualifying direct deposits.

On-time payment history may have a positive impact on your credit score. Late payment may negatively impact your credit score. Chime will report your activities to Transunion®, Experian®, and Equifax®. Impact on your credit may vary, as Credit scores are independently determined by credit bureaus based on a number of factors including the financial decisions you make with other financial services organizations.

Money added to Credit Builder will be held in a secured account as collateral for your Credit Builder Visa card, which means you can spend up to this amount on your card. This is money you can use to pay off your charges at the end of every month.

By the end of 2022, 27 million Americans had an outstanding personal loan balance with the average amount owed being $11,116. The interest rates of these loans are also the highest they’ve been since 2011 at 11.23 percent.

Sources: TransUnion and the St. Louis Federal Reserve

As of the second quarter in 2022, Americans owed over $192 billion in personal loans, according to TransUnion®. This was a 31% increase from 2021 and is thought to be due to the financial hardships Americans experienced during the COVID pandemic that overwhelmed the nation in 2020.

If you’re one of the many Americans who took out a personal loan in early 2022, the good news is that interest rates were very low, according to the St. Louis Federal Reserve. Since then, rates have reached new highs, so many Americans are struggling to pay back these loans.

Understanding the current trends in personal loans can help you see where you stand financially. We’ve gathered 10 personal loan statistics that include the most common reasons people take out personal loans, delinquency rates and which states have the highest personal loan debt to help you make better financial decisions if you’re accumulating too much debt.

In This Piece

Must-know Personal Loan Statistic Findings

Millions of Americans are taking out personal loans, and the following are some of the most interesting facts on the topic.

Get matched with a personal

loan that’s right for you today.

Learn

more

27 million Americans have personal loan debt (TransUnion)

At the end of 2022, the average new loan amount was $8,018 (TransUnion)

The average amount owed in personal loan debt was $11,116 at the end of 2022 (TransUnion)

In November of 2022, personal loan interest rates were the highest they’ve been since May of 2011 (St. Louis Federal Reserve Bank)

New Jersey has the highest average new personal loan account balance at $13,494 (TransUnion)

Average Personal Loan Debt in America

According to TransUnion, Americans owed roughly $9,896 on average as of the first quarter in 2022, the highest it’s been in recent years. Americans took out loans at an average of $6,656 per loan, which was over $1,000 more than in the previous quarter of 2022.

The amount owed per borrower dropped significantly between Q2 and Q3 in 2022, but by the end of the fourth quarter, the average amount owed increased by over 100 percent with the new loan amount dropping to $8,018.

The increase in personal loan debt may have been due to the inflation the country experienced in 2022. TransUnion also reports that there were more loans approved to “super prime borrowers,” or those with credit scores over 720, stating, “On a percentage basis, personal loan originations for subprime and near-prime borrowers increased in the single digits [year over year] whereas super prime borrowers experienced a 33% rise in the third quarter.”

How Many Americans Have Personal Loans?

The amount of Americans taking out personal loans increased 12 percent from 23.9 million in the first quarter of 2022 to 27 million by the fourth quarter.

Prior to the beginning of the COVID-19 pandemic, the total amount of personal loan borrowers was 23.3 million at the end of 2019 and dropped to 21.2 million by the end of 2020. The number of borrowers then grew back to 22.8 million in the following fourth quarter of 2021 and continued to grow as the pandemic regressed.

Quarter

Q4 2022 Average new account balance

Q4 2019

23.3 million

Q4 2020

21.2 million

Q4 2021

22.8 million

Q4 2022

27 million

The Most Common Reasons to Take Out a Personal Loan

LendingTree conducted a survey of their users in 2022 and found that the most common reason consumers took out personal loans was to pay down other debts. Over 58 percent of borrowers used these loans to pay down debt, and the other main reasons included credit card refinancing, home improvements and other major purchases.

Rank

Reason

Percentage of respondents

1

Debt consolidation

41%

2

Other

17.3%

3

Credit card refinance

17.3%

4

Home improvements

6.2%

5

Major purchase

4.1%

6

Medical expenses

3.0%

7

Moving/relocation

2.9%

8

Everyday bills

2.9%

9

Car financing

1.7%

10

Car repair

1.1%

11

Business

0.9%

12

Vacation

0.5%

13

Homebuying

0.4%

14

Wedding expenses

0.4%

Average Personal Loan Interest Rates

During the second quarter of 2022, the Federal Reserve Bank of St. Louis reported that interest rates reached an all-time low of 8.73 percent. By the end of the year, these rates were the highest they’ve been since 2011 at over 11.2 percent.

Personal Loan Debt Compared to Other Debts

Based on TransUnion data, personal loans account for less than four percent of the total number of accounts when compared to other types of loans, such as credit cards, home and auto loans.

Account type

Number of accounts

Percentage of accounts

Credit card

518.4 million

76.3%

Auto loan

81.2 million

11.9%

Mortgage loan

52.6 million

7.83%

Personal loan

27 million

3.97%

It’s also important to note that not all credit card accounts carry a balance.

Personal Loan Delinquency Rates

Delinquent accounts are accounts 60 days or more past due and can hurt your credit score. The Q4 TransUnion report shows that the delinquency rate dropped year over year between 2019 and 2020, but was up 53 percent as of 2022, with an overall delinquency rate of 4.14 percent.

Quarter

Delinquency rate

Q4 2019

3.48%

Q4 2020

2.7%

Q4 2021

3%

Q4 2022

4.14%

TransUnion’s 2022 Credit Snapshot shows that in the last month of the report, those with the lowest credit scores have the highest delinquency rate of 23.9 percent, while super prime borrowers are only at 12 percent.

Credit score range

Percentage of delinquent borrowers

Subprime (300 to 600)

23.9%

Near prime (601 to 660)

23.7%

Prime (661 to 720)

23.3%

Prime plus (721 to 780)

17%

Super prime (781 to 850)

12%

Personal Loan Statistics by State

TransUnion’s 2022 Credit Snapshot reports that New Jersey has the highest average new account balance at over $13,000, and Oklahoma has the lowest at $3,170. Although Oklahoma has the lowest new account balance, they have the highest delinquency rate at 7.73 percent.

State

Q4 2022 Average new account balance

Q4 2022 Delinquency rate

AK

$10,296

2.9%

AL

$4,362

6.59%

AR

$7,089

5.18%

AZ

$9,343

3.78%

CA

$10,454

3.47%

CO

$12,322

2.03%

CT

$11,712

2.57%

D.C.

$9,016

6.55%

DE

$9,146

4.04%

FL

$8,379

3.94%

GA

$8,621

5.18%

HI

$12,224

2.28%

IA

$7,443

2.94%

ID

$9,072

4.38%

IL

$9,236

3.46%

IN

$7,439

2.97%

KS

$8,349

3.05%

KY

$6,875

3.36%

LA

$6,797

5.07%

MA

$12,518

2.24%

MD

$10,956

2.77%

ME

$6,651

1.67%

MI

$7,052

3.21%

MN

$10,692

3.73%

MO

$6,522

6.69%

MS

$5,179

4.96%

MT

$9,326

2.53%

NC

$10,035

3.03%

ND

$8,051

1.89%

NE

$7,755

3.65%

NH

$11,719

2.31%

NJ

$13,494

3.49%

NM

$5,418

6.31%

NV

$8,839

3.74%

NY

$11,843

2.77%

OH

$7,595

3.75%

OK

$3,170

7.73%

OR

$10,523

2.93%

PA

$10,418

3.06%

RI

$8,744

2.14%

SC

$5,924

4.89%

SD

$9,945

2.06%

TN

$5,355

5.38%

TX

$4,952

6.33%

UT

$7,966

4.23%

VA

$9,875

3.37%

VT

$6,180

0.82%

WA

$9,570

2.94%

WI

$6,489

3.95%

WV

$10,864

1.96%

WY

$7,698

2.66%

Personal Loan Statistics by Type of Lender

More and more Americans are turning to financial technology companies, also known as FinTech, for their personal loans. These are online banking services that are done via a company’s website or mobile app, and 32.9 percent of all personal loans are done through these types of companies.

Lender type

Distribution of total balances

FinTech

32.9%

Banks

20.5%

Credit unions

19.7%

Other finance companies

26.9%

Can Personal Loan Debt Affect Your Credit Score?

If you’re one of the 27 million Americans with a personal loan, you don’t have to let your debt harm your credit score. As you’ve learned from these personal loan statistics, many Americans have turned to personal loans to pay off other debts, but many people are delinquent with their payments, which can hurt their scores.

Credit.com provides a variety of credit tools and tips to help you work to repair and improve your credit. You can learn more about our services, like ExtraCredit, or click here to get your free credit report card.

You’ve probably used Venmo a lot this past year, but is Venmo safe? And if so, what are the advantages of Venmo over other online payment providers? Read answers to these questions and more in our helpful guide below.

In This Piece

What Is Venmo?

Venmo is a type of peer-to-peer—or person-to-person—payment app. Its parent company is money-moving giant PayPal, which had over 377 million registered users in the last quarter of 2020. Think of Venmo like “PayPal lite”—you can receive cash and send money to people, but you can’t send invoices or do anything complex.

PayPal launched Venmo for one reason—to compete in the P2P payment marketplace. Not everyone needs PayPal’s full suite of services, but they appreciate a convenient way to split the bill. You can pay for part of a dinner or your share of the shopping with Venmo, and some online retailers also accept Venmo as a form of payment.

Venmo began offering a cash back rewards debit card—the Venmo Debit Card—in 2018. In late 2020, it launched the Venmo Credit Card. Like the Venmo Debit Card, the Venmo Credit card offers cash back—up to 3% on your “top spend” category.

How Does Venmo Work?

Venmo works a little like PayPal. To use the services you simply:

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Download and install the app on your phone

Link the app to your bank account, debit card, or credit card

Begin sending payments to friends, family members, and select online retailers

Venmo has an initial $299.99 weekly sending and receiving limit. To lift that limit, you need to provide identification documents. Once your ID is confirmed, you’ll have a $4,999.99 weekly limit.

If you want a Venmo Debit Card, you’ll need to apply online. To get a Venmo Credit Card, you need to be over 18 and a U.S. resident—and you also need to have had your Venmo account for at least 30 days.

Is Venmo Safe? What Are the Risks of Using Venmo?

Venmo is generally very safe—the company uses bank-level encryption to keep your data safe. You can add a PIN number and enable multi-factor authentication (MFA) to make your account even more secure. A strong password combined with a PIN and MFA greatly reduces the chance of hacking.

Venmo’s default profile and payment settings are public. Thankfully, you can change your privacy settings to keep your payment settings under wraps. Venmo’s three privacy levels are:

Anyone can find you and see your transactions.

Only you and the person you send payment to will see a transaction.

Friends only. Your Venmo friends can see you and can also see your transactions.

You can set your privacy settings to default to any of these three levels, or you can set levels on a transaction-by-transaction basis. You can also hide your past transactions.

Is Venmo Free?

Depending on how you use Venmo, it can be 100% free. Believe it or not, if you’re strictly using Venmo to transfer payments from one party to another and you’re not using a credit card, you may be able to use it for free.

However, there are some instances where Venmo does charge a fee. For example, if you’re using Venmo as part of your business, you’ll likely need to pay merchant fees. Here’s a look at the various fees Venmo charges account holders.

Instant Transfer Fees

You can transfer money from your Venmo account to your bank account at any time. This process can take 1-2 days to complete. If you need the money faster, you can opt for the instant transfer option, but it will cost you. Venmo charges an instant transfer fee of 1.75%, with a minimum fee of $0.25 and a maximum fee of $25.

Processing Fees

If you choose to make a Venmo payment using your bank account or debit card, you’ll incur no additional fee. If, on the other hand, you use a credit card to make this payment, you must pay processing fees. Venmo’s processing fees are 3%.

Check Deposit Fees

Venmo allows account holders to deposit checks directly into their Venmo account. However, it charges a fee for this service. The check deposit fee is 1% or a $5 minimum when depositing government-issued or payroll checks and 5% or a $5 minimum when depositing all other checks.

Merchant Fees

If you’re using Venmo to accept payments for a business you operate, you must pay merchant fees. Venmo charges business owners a 1.9% merchant fee plus an additional $0.10 per transaction.

What Is Venmo Debit Card and How Does It Work?

If you use your Venmo account quite often or have your payroll or government check deposited into your Venmo account, you might want to consider applying for a debit card with Venmo. This card is similar to any other debit card from a financial institution. It lets you spend the money in your Venmo account anywhere that accepts debit cards.

You can track your deposits and payments directly on the Venmo app, and you can also check the balance in your account. Since this is a debit card, it doesn’t have the same strict credit requirements you might run into when attempting to obtain a credit card. Obtaining this type of debit card can avoid the need to transfer funds from your Venmo account to your bank account.

There can be some fees associated with having a Venmo debit card. For instance, you incur a $2.50 fee when you withdraw funds from your Venmo account via an out-of-network ATM. There’s no fee for using an in-network MoneyPass ATM. A $3 fee applies for an over-the-counter cash withdrawal at a bank. Additionally, you can only withdraw up to $400 per day from your Venmo account.

Venmo and Taxes

If you’re only using Venmo to transfer funds to friends and family members, taxes won’t be an issue. If, on the other hand, you’re using Venmo to collect payments for your business, you may be responsible for paying taxes. If you earn over a certain amount during the year, you need to include any Venmo payments you received for your business on your taxes. Before starting any business, it’s important to understand what your tax responsibilities are.

Venmo Scams to Watch Out for

If you’re wondering “Is Venmo safe to use?” the answer is yes, it’s relatively safe to use. Venmo uses encryption security to protect your personal information from hackers. Its robust security features are in place to keep your money safe.

Even these robust security features can’t stop all scammers. But there are steps you can take to avoid this type of bank account fraud. It’s important to recognize these scams before scammers take advantage of you. Below is a look at the most common Venmo scams.

Fake Products for Sale

One of the most common Venmo scams involves online sales. The scammer pretends to be selling something online. However, once you make a payment, you never receive the product.

Once a Venmo payment is processed, you can’t reverse it and there’s no way to get your money back. This is why it’s so important to only submit payments to people and businesses you know and trust.

Pretending to Be from Venmo

Another common scam involves scammers pretending to be Venmo. If you receive an email or text message claiming to be from Venmo, don’t automatically assume it is. Some scammers send these messages to try to steal your personal information, such as your account number and password. Once they have this information, they can hack into your account and make payments without your permission.

Using Your Phone

There have been reports of strangers asking a person to borrow their phone. Instead, they actually open the Venmo account on your phone to send money to an account associated with them. Unfortunately, trying to do a good deed by letting someone borrow your phone could cost you hundreds or thousands of dollars.

Why Does Venmo Require Identify Verification?

If you open an account with Venmo, you’ll have to prove your identity. This isn’t just a Venmo requirement. According to the Consumer Identification Program under the U.S. Patriot Act, all financial institutions must verify the identities of all their customers.

This program helps prevent terrorists from sending and receiving money and helps to stop money laundering. It can also help reduce the risk of fraud on Venmo. However, even identity verification can’t prevent all forms of fraud. It’s important to always remain vigilant and report any suspicious activity to Venmo.

Staying Safe with Venmo

There are several things you can do to protect yourself when using Venmo.

Monitoring Your Account

Be sure to periodically check your Venmo account for unauthorized transactions. If you notice any, report it to Venmo immediately.

Set Up Venmo Notifications

Receiving notifications as soon as there’s suspicious activity on your Venmo account may help prevent a scammer from accessing your account. Always be sure to have your notifications on for Venmo.

Secure Your Account

There are multiple ways to secure your Venmo account if you lose your phone or allow someone to use it. First, turn on the PIN feature. This step requires you to enter a specific PIN number before you can even open your Venmo account. You should also set up the two-function authentication feature to make it even more difficult for someone to hack into your account.

Choose Private Setting

You may not realize it, but Venmo automatically makes all accounts public. While other users can’t see the specific details of your account, they can see how often you use Venmo. To keep your account safe, it’s recommended to switch your account to private so only your friends and family members can see your information.

Don’t Keep a High Balance

It’s recommended to avoid keeping a high balance in your Venmo account. This way, if your account is hacked, you’re not at risk of losing too much money. Instead, take steps to transfer your Venmo balance to your bank account as soon as possible.

Don’t Share Phone

Even if you’re using the passcode and two-factor authentication features, it’s recommended not to let a stranger use your phone. Only those you know and trust should have access to your phone.

Only Enter Venmo Through the App or Website

Don’t activate your Venmo account through a link you receive in an email or text message. This could be a phishing email designed to steal your Venmo account information, such as your account number and password. Instead, only access your Venmo account through the Venmo app or website.

Venmo Alternatives

Venmo isn’t alone in the payment marketplace. Like most other payment options, it has a long list of rivals. Let’s line up three formidable adversaries for comparison.

Tip: PayPal is another popular payment app. Check out our safety review for more information.

App Name

Venmo

Zelle

Cash App

Parent company

PayPal

Early Warning Services

Square

Need a bank account?

No

Yes—but you can still use and download the app if your bank doesn’t offer Zelle

No

Who can you pay?

Friends, family members and other people you trust

Friends, family members and other people you trust

Anyone, including contractors, utility companies and charities

Debit card available?

Yes

No

Yes

Can you hold a balance?

Yes

No—but Zelle is connected to your bank account by default

Yes

How much does it cost?

Free if you use a bank account, a debit card or your Venmo balance. If you use a credit card, Venmo charges a 3% fee. Instant outgoing bank transfers cost 1%, while standard bank transfers are free.

No fees to send or receive money. Your connected bank may charge fees, however.

Free if you use a bank account, a debit card or your Cash App balance. If you use a credit card, Cash App charges a 3% fee. Instant outgoing bank transfers cost 1.5%, while standard bank transfers are free.

Any limits?

You’ll have a $299.99 weekly peer-to-peer limit immediately after signup. If you confirm your identity, your weekly limit will go up to $4,999.99.

Limits depend on the financial institution. If your bank doesn’t offer Zelle, your weekly transaction limit will be $500.

You can send or receive up to $1,000 during a period of 30 days.

Venmo Versus Credit Cards

What if you don’t want to pay via an app, and you don’t like carrying cash around either? In that case, your best bet might be a credit card. You’ll need to ask your waiter or your cashier to split the bill, but most merchants are happy to oblige.

Look for credit cards with the following perks:

A low APR. Choose a low-interest credit card to save money on interest payments.

Cash back rewards. Why go for a standard credit card when you can get a little money back each time you shop?

Balance transfer offers. Transferring your balance from another credit card? In that case, look for a 0% balance transfer offer.

Credit builder cards. If you don’t qualify for an unsecured credit card, go for a secured card or a credit builder card to boost your credit score.

So is Venmo Safe?

Let’s recap. Venmo is a P2P payment app, and its parent company is PayPal. You can send money to friends, family members and other trusted individuals via Venmo. Some online stores accept the payment method, too. Venmo offers a debit card and—if you qualify—a credit card. You can fund your account with your bank account, a credit card or a debit card.

If you prefer not to pay by app and you don’t feel safe carrying cash, you might want to go with a credit card. Looking for the right credit card for you? Check out ExtraCredit® today. You’ll see select personalized credit offers when you visit your Reward It portal.

A hard credit inquiry is when a credit card issuer or another lender reviews a credit report as part of your credit application. Their request to review your credit will be shown as a hard inquiry on your credit report and will affect your credit score.

Let’s say you’re looking to apply for a new credit card. Whether you want to expand your available credit, create a credit mix, or simply apply for a credit card online with your desired rewards, you’ll often encounter a hard inquiry.

A hard credit inquiry—or a hard credit check—is a natural part of the credit card application process. It happens when the lender or bank associated with your credit card company checks your credit report to see if you are eligible for acceptance.

What Are Hard Inquiries?

Hard inquiries—or hard credit checks—occur whenever a lender or bank accesses your credit account. The credit bureaus log the activity, recording the date and the name of the company or entity that accesses it.

Hard inquiries refer to when a lender accesses your credit report to evaluate your merit as a borrower. In other words, hard inquiries happen when lenders look at the information in your report to decide whether to approve or deny your credit card application.

How Do Hard Inquiries Impact Your Credit?

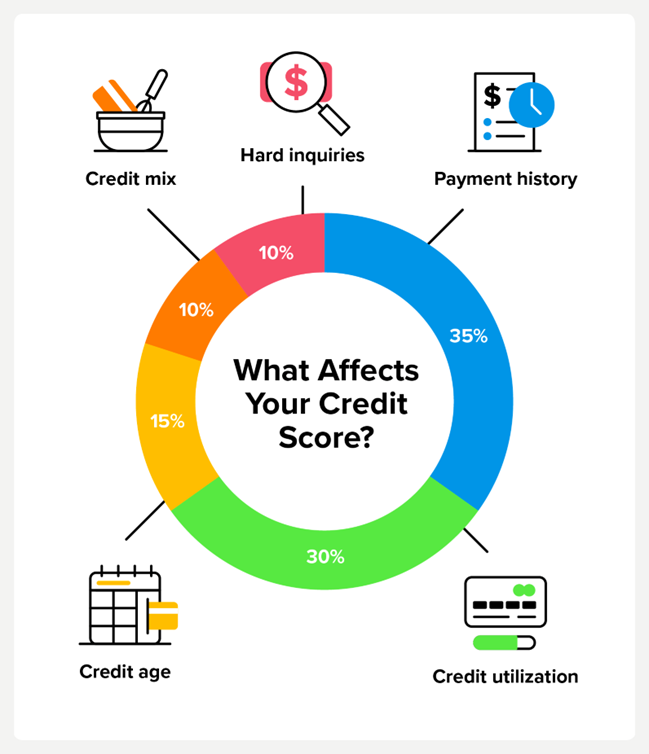

Hard inquiries aren’t the most impactful thing that affects your credit score, but they are one of the five major factors that make up your credit score. That’s because having many hard inquiries on your account looks like you’re chasing credit. Lenders don’t want to see that behavior from potential borrowers as it reduces their credibility.

Here are the five factors that impact your credit score:

Payment history accounts for around 35% of your credit score. This factor is whether you pay your bills on time and as agreed upon.

Credit utilization accounts for around 30%. This reports how much of your available revolving credit limit you’re actively using.

Credit age accounts for around 15% of your score. This is how long you’ve had credit and the age of your oldest accounts.

Credit mix makes up around 10% of your credit score. Creditors want to see that you can manage different types of accounts, such as revolving and installment accounts.

Hard inquiries affect around 10% of your score. This is the number of recent hard inquiries on your report.

Hard Inquiries vs. Soft Inquiries

Not all inquiries that show up on your credit report impact your score. Only those that evaluate your financial creditworthiness do—these are hard credit checks.

Soft inquiries, which are purely informational, have little to do with credit and don’t have the same impact. They’re also not usually visible to lenders or banks—only you.

Hard inquiries

Soft Inquiries

Affect your credit score

Don’t affect your credit score

Count against your credit score for 1 year

Appear only to you on your credit report

Occur during the approval process

Occur during pre-approval processes

Happen when you’re actively searching for credit

Happen during noncredit screenings and background checks

Require your authorization

Do not require authorization

Examples of Hard Inquiries

Hard inquiries happen when you apply for a line of credit that will impact your financial health. Hard credit checks will affect your credit score and stay on your credit report for a year or two, so having too many of them in a short period may hurt you in the long run.

Credit card companies, car dealerships, banks, lenders, and others may perform a hard credit check only after your written approval—you will always know when a hard credit check will happen.

Examples of things that will require hard inquiries include:

Examples of Soft Inquiries

Soft inquiries typically happen for nonfinancial inquiries and don’t affect your credit score. Typically, only you can see the soft credit checks on your report. Soft credit checks also don’t need your permission to happen. Though employers will request permission for background checks, creditors can run a soft credit pull to prequalify you for marketing purposes. Note that you do have the opportunity to opt out of those soft checks, though.

Soft inquiries happen when:

Employers run background checks

Credit card companies do a pre-approval process

Utility companies screen you

You check your credit report

Disputing Hard Credit Inquiries

You should always review the hard inquiries on your credit report to ensure that you authorized them. If you see something on your credit report that you didn’t authorize or approve, you can dispute your hard inquiry by following these steps:

Reach out to your current lenders and confirm that they didn’t create a hard credit inquiry for your credit.

Research the creditor that authorized the hard inquiry. Sometimes, they will remove the inquiry from your report.

Open a formal dispute with the credit bureaus. You will normally do this by filing a dispute on an online platform.

You will generally need to wait around 30 days (give or take) before receiving a reply about your hard inquiry dispute. When the credit bureaus reach a conclusion, they will remove the hard inquiry from your credit report.

Frequently Asked Questions

How Long Do Hard Inquiries Last?

According to Experian®, hard inquiries remain on your credit report for 25 months. However, they only tend to impact your credit score in the first 12 months.

How much a hard inquiry affects your credit depends on various factors, including what your credit score was to begin with. Experian notes that a hard inquiry can bring your score down 5-10 points on average. The drop might be even less if you have excellent credit and no other issues.

How Many Hard Credit Inquiries Is Too Many?

There’s no set number of inquiries that are too many. If you suddenly have a lot of inquiries, it can look bad to potential creditors. And if you’re losing up to 10 points for each one, you could drop from excellent or good credit to fair or poor credit with just five or more inquiries.

Spacing out the inquiries and ensuring that your credit report doesn’t take a hit can help minimize these issues. It also gives your score time to recover before another inquiry.

Are Hard Inquiries Bad?

Not necessarily. They’re simply an aspect of how credit reporting works—it’s actually good that this information gets recorded. Knowing who accessed your personal credit information and why can help keep you informed on your credit application history.

That said, hard inquiries aren’t neutral. They can impact your credit, so you want to keep them to a minimal number when possible.

What Triggers a Hard Inquiry?

Any time you apply for credit-related accounts with a lender, you will trigger a hard inquiry that will appear on your credit report. It’s important to remember that you will always authorize hard credit checks, so be mindful of how you space them out and what loans you need at what times.

Minimize Your Hard Inquiries

So, how do you reduce the impact of hard inquiries on your credit score? Nowadays, it can be challenging to go through life without ever applying for credit. But you can follow the steps below to reduce how hard inquiries impact your score:

Don’t spread out loan shopping: Credit scoring models know that you’ll want to shop around for the best rates. Because of that, multiple applications for credit during short periods can appear as a single inquiry on your credit report.

Don’t apply without confidence: Understand your credit score and what type of credit you are likely to qualify for, and only apply when you need the credit. Otherwise, you’ll rack up hard inquiries for no reason.

Manage other aspects of your score responsibly: Make payments on time, keep your credit utilization low, and manage multiple types of accounts well. These all have more impact on your credit score than hard inquiries.

Keep tabs on your credit report: The last step in minimizing hard inquiries is tracking your report and score. Check your credit regularly to see where you stand and whether potential mistakes could bring down your score.

You can check your Vantage 3.0 score with Credit.com’s free Credit Report Card or get many versions of your FICO® Score with ExtraCredit®. Neither of these options constitutes a hard inquiry, so using them won’t hurt your credit.

While the good news about housing keeps flooding in, one piece of negative data jumped out at me today.

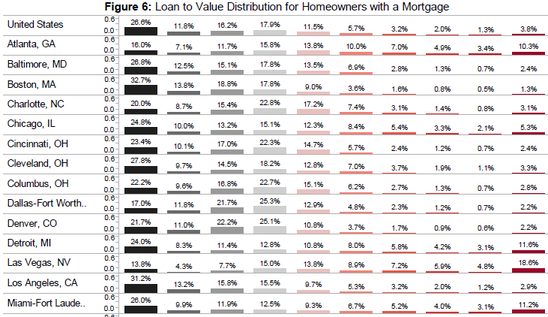

The latest Zillow Negative Equity Report released today revealed that nearly one out of every five (18.6%) Las Vegas homeowners with a mortgage owed double what their home was worth as of the end of the fourth quarter.

In other words, if their home’s present value is $100,000, their mortgage balance is somewhere around $200,000.

For most people, this would signal being past the point of no return. After all, most of us have enough trouble paying off a mortgage when we’re above water, so the thought of owing double is daunting, even with a kick-butt mortgage rate.

Of course, if you stick around long enough, home price appreciation should do some of the heavy lifting, but it’s still a big ask for struggling homeowners.

While I cherry-picked a bad piece of data, it should be noted that 26.7% of Vegas homeowners were in this position one year earlier, so it’s not nearly as bad as it was.

And only 8.9% of underwater homeowners are delinquent on their mortgage payments, down from 9.9% a year earlier.

So yes, things are getting better…at the same time, the 200%+ loan-to-value (LTV) ratio bracket was the most prominent in Sin City.

In other words, if you went door to door and asked Vegas homeowners with mortgages what their LTV was, most would say 200%+.

The second largest distribution for Vegas homeowners was the 80-100% LTV tier (15% of borrowers), followed by the 100-120% LTV tier and under 40% tier, both at 13.8%.

3.8% of American Mortgagors Owe More Than Double Home’s Worth

If we expand the data to the whole of the United States, 3.8% of Americans with mortgages owed more than double what their homes were worth at the end of 2012.

That’s pretty scary, though the majority of U.S. homeowners with mortgages (26.6%) have LTV ratios south of 40%.

And 72.5% have a LTV somewhere below 100%, meaning they’re not the proud owners of an underwater mortgage.

If you look at the graphic below, you’ll notice that the LTV distribution is improving in every category, thanks to continued home price appreciation.

The low-LTV brackets are rising, and the high-LTV brackets are declining. All good news…

Overall, Zillow noted that the negative equity rate dropped to 27.5% in the fourth quarter from 28.2% a quarter earlier, and is now well below the 31.1% rate seen at the end of 2011.

As a result, nearly two million homeowners were able to get below the 100% LTV mark in 2012, though 13.8 million remain underwater.

Still, roughly one-third of all homeowners own their homes free and clear because they don’t have a mortgage.

Where’s the Inventory?

Zillow also has a nice little chart detailing how many homeowners will be “freed from negative equity” in 2013.

Using this data, we can guess which metros will see an increase in housing inventory, as that many more borrowers will finally be able to list their homes and move on to greener pastures.

The company expects 72,696 homeowners in Los Angeles to get above water in 2013, making it the leading metro in terms of total numbers.

Nearby Riverside is expected to “free” 62,407 homeowners, which represents a 21.2% decrease in the negative equity rate there, the second largest percentage decrease behind Sacramento (-21.3%).

In hard-hit Vegas, only 8,435 homeowners are expected to get above water this year, which represents just a 4.3% decline in negative equity.

And in Chicago, negative equity is actually forecast to get worse, with 7,019 more homeowners going under in 2013.

But overall, 999,601 homeowners should be “freed” in 2013, thanks in part to Zillow’s 3.3% home appreciation estimate.

This all reminds me of a post I wrote back in 2010, which claimed some real estate markets wouldn’t see a return to peak home prices until 2039.

In other words, while there is plenty of good news, it’s going to take a while to undo this mess.

Just weeks after New York-based digital lender Better Home & Finance Holding went public, Better issued pink slips to employees in early September in a new round of layoffs, Insider reported.

Better laid off about a quarter of its U.S. mortgage sales and origination team, according to the news outlet, citing two former employees who were affected by the latest downsizing.

The layoff news comes on the heels of Better going public via special purpose acquisition company (SPAC) Aurora Acquisition Corp. in August.

About 75 employees are left on the mortgage origination team in the U.S. as well as some employees in India, according to Insider.

While Better didn’t respond toHousingWire‘s inquiry about the number of affected employees, spokeswoman Jessica Schaefer told Insider the firm has more than 100 people left on the team.

Better plans to fill some vacant positions from the layoffs.

“As a publicly listed company, we’re focused on making prudent and disciplined decisions that account for market dynamics so that we can continue to serve both customers and shareholders for the long-term,” Better’s spokesperson said in an e-mailed statement to HousingWire.

“We are hiring more seasoned professionals who can sell in this tough mortgage environment and then making them 10X more productive through our continued investment [in] technologies such as Tinman and One Day Mortgage, which have created efficiencies that streamline and automate nearly every major function of homeownership,” the spokesperson said.

As of June, Better had 950 team members, a 91% decrease over an 18-month period from 10,400 in Q4 2021, according to its previous filing with the Securities and Exchange Commission (SEC).

While Better was an efficient refi shop during the pandemic years when rates hit record lows, the lender and other independent mortgage banks (IMBs) were hit hard by the Federal Reserve‘s monetary policy.

The digital lender reported a net loss of $45.5 million in Q2, an improvement from a net loss of $89.9 million the previous quarter.

In Q2, Better’s origination volume was $900 million across 2,421 loans, compared to production of $800 million across 2,347 loans funded in Q1.

When Better debuted on Nasdaq in late August, the SPAC deal unlocked $565 million of fresh capital for the unprofitable company.

The digital lender has pivoted its strategy from being a one-stop-shop to becoming a “mortgage-as-a-service” company or a white-label provider of mortgage tech.

“For things like homeowner’s insurance, title insurance, and Realtors, we’ve now just become a marketplace. We match the consumer with a partner capable of delivering the best product to them. So, we ended Better Real Estate for the sake of efficiency and savings for the consumer. We partner with best-in-class agents, insurance companies and title companies,” Better CEO Vishal Garg said in an interview with HousingWire in August.

Better will invest in tech-driven products like One Day Mortgage, a program that will allow customers to apply for a mortgage, get preapproved, lock their rate and receive a mortgage commitment letter within 24 hours.

“We are committed to further developing this technology during an interest rate environment where customers need it the most,” Better’s spokesperson noted.

Better was ranked as the 59th largest lender in Q1 2023, plummeting from the 19th in 2021, according to Inside Mortgage Finance.

Fed’s inflation fight tightens the U.S. housing supply and makes home buying even more difficult

Conventional wisdom dictates that U.S. inflation will continue to decline as the Federal Reserve keeps interest rates high. This action, which makes loans more expensive for businesses and consumers, should lead to less spending, less consumption and higher unemployment.

Or at least that’s Econ 101. Yet both consumers and investors have acclimated to the current market environment. Moreover the key driver of inflation — housing — cannot be adequately contained through the Federal Reserve’s usual tactics.

In fact, the Fed’s policies have created a Catch-22 in the housing market by creating “golden handcuffs.” Instead of easing consumer demand, the Fed’s actions unintentionally restricted U.S. housing supply, resulting in a stalemate between home buyers and sellers. Homeowners who locked into historically low mortgage rates before and during the pandemic are now reluctant to sell, which in turn is increasing the likelihood of persistent higher inflation.

The case for this condition to persist , which the market is mostly failing to consider, continues to grow stronger as the odds of a recession fade. This should be an alarm bell and a potential opportunity for investors to redeploy at least part of their capital into hard assets to serve as a hedge against inflation risk.

The recession that never was

Many economists have predicted that a recession would hit the U.S. Their reasoning was sound: aggressive monetary action by the Federal Reserve, investor dissatisfaction with inflation, loss of consumer confidence and reductions in home asking prices — all points that were hard to argue against.

Yet most of the key ingredients needed for a recession have not materialized. Investors have acclimated to inflation, consumer confidence is growing and the housing market has, by and large, entered a period of stalemate where prices remain high due to lack of supply.

In fact, the only relevant argument in the recession camp that remains is the Fed continuing its aggressive posture against inflation — now considered the fastest monetary policy tightening cycle in more than 40 years. Such action continues to lead many to speculate that recession is imminent, and the only questions left to answer are “when,” and “how deep it will be?”

Housing prices obey the laws of supply and demand

Housing is perhaps the most consequential category that makes up the Consumer Price Index (CPI), which markets track every month as a core measure of inflation.

The undersupply of housing in the U.S. is grounded in years of underbuilding and is not the result of a single federal policy, war, or external event. If anything, the power to create more housing supply rests with state and local governments, which often require working through a patchwork quilt of differing zoning and land-use regulations.

The high estimate of the country’s current housing shortage is pegged at about 7.3 million units, while the most conservative estimate shows it to be about 1.7 million. While the true shortage is most likely somewhere inbetween, the bottom line is that the United States faces a textbook housing shortage that cannot be solved overnight. Worse, the Fed’s current policies are making the prospect of home ownership even more difficult.

Nobody wants to move and reset their loans at much higher rates.

Central bank measures designed to clamp down on inflation by making borrowing more expensive (which theoretically should drive down the costs of homes), are having the opposite effect. This is because homeowners, who locked in historically low mortgage rates before and during the pandemic, are now reluctant to sell their home.

Simply put, nobody wants to move and reset their loans at much higher rates. Would-be sellers are therefore sitting on the sidelines, which has unintentionally created an even greater shortage in supply. Meanwhile, potential buyers, who cannot afford higher mortgage rates, are incentivized to rent instead.

To end this stalemate, the Fed would need to start cutting interest rates, which it has stated is unlikely this year. But if inflation is being driven by the cost of housing, as demonstrated in the Consumer Price Index, more attempts to tame inflation via rate hikes suggests homeowners will only become more entrenched as supply dwindles further As the labor market continues to prove surprisingly resilient, homeowners, and by extension everyday consumers, don’t seem to mind waiting it out.

Read: Nouriel Roubini says a return to 2% inflation is ‘mission impossible’

Also: Most long-term investors can ignore the Federal Reserve’s latest move

The case for hard assets

Seasoned investors know that during times of rising interest rates, restrictive credit and prolonged inflation, more investments flow into “hard” asset classes such as real estate. This hedging strategy is used almost like an insurance policy by investors to preserve capital from the depreciating effects of inflation. And according to research, it works. For example, a Stanford University study found that residential real estate is historically an investment haven during inflationary periods. Even during the inflation of the 1970s, home prices increased relative to the size of the economy. This is because housing is typically tied to consumer prices and rises with inflation.

With housing assets so closely tied to inflation, as well as to the laws of supply and demand, investments in this hard asset class deserve due consideration. Strong economic growth, coupled with the one-two punch of resilient consumer spending and near record-low unemployment, is good news. It also means the Fed won’t be lowering rates soon. Housing will remain a key driver of inflation, and future rate-hikes will further entrench homeowners and push more would-be buyers into renting.

To achieve a return to 2% inflation, U.S. policymakers would be wise to work with state and local governments to incentivize development, which would drive down the greatest expense for most Americans. But even with decisive action, fixing the fundamental housing shortage that is responsible for sustaining stubbornly persistent inflation will be a longer process than most investors realize.

David Piscatelli focuses on research, economic analysis and strategy at Avenue One, a property technology service platform and marketplace for institutional owners, buyers and sellers of residential homes. Views of the writer do not necessarily reflect the views of Avenue One.

More: Meet the brave Americans buying and selling their homes, despite stubbornly high interest rates

Plus: 9 ways home buyers can stretch their dollars even though mortgage rates are high

-David Piscatelli

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.