Soaring interest rates and a higher-for-longer policy will take its toll on the economy, according to Fannie Mae’s Economic and Strategic Research (ESR) group.

“The cause of the recent run-up in long-term rates is multifactorial and likely includes some expectation of more resilient economic growth coupled with a higher-for-longer monetary policy stance from the Federal Reserve,” the ESR group said in its latest economic commentary.

After the 10-year treasury yield began July at around 3.8%, rates were about one full percentage point higher three months later. On October 18, the 10-year treasury yield peaked at 4.91%.

In part because of the recent run-up in long-term rates, Fannie Mae does not expect additional Fed rate hikes, Doug Duncan, Fannie Mae’s senior vice president and chief economist, said.

Several Fed officials have indicated that a rate pause is necessary while stressing rates will remain higher for longer. The Mortgage Bankers Association(MBA) had also expected the central bank would pause on rate hikes as real rates – which are inflation-adjusted– are 2%. Philly Fed P

Fannie Mae noted that the economy likely faces fewer structural headwinds than previously thought after significant updates to the national accounts showed real consumption and incomes are in better balance than had been reported previously.

Personal consumption expenditure (PCE) inflation remained elevated in August at 3.5% year over year and September’s consumer price index (CPI) rose 3.7% year over year, holding steady with August’s annual gain and above economists’ expectations.

“Personal consumption has not only remained resilient, but recent official data revisions indicate that the consumer has been in a better position than previously thought, increasingly the likelihood of an economic ‘soft landing,’” Duncan said.

The ESR group revised its 2023 real GDP prediction to 2.5% on a Q4/Q4 basis but continues to expect a modest recession in the first half of 2024.

Home prices proved more resilient than expected, in turn leading Fannie Mae to revise its 2023 home price expectation from 3.9% to 6.7% on a Q4/Q4 basis.

Fannie Mae forecast that home price growth will decelerate in 2024 as affordability remains constrained.

Further declines in home sales from an already low level due to the run-up in mortgage rates will likely be muted relative to the slowdown in 2022, the ESR group projected.

But the annualized pace of existing home sales are expected to fall below 4 million units in the fourth quarter, according to Fannie Mae.

New home sales continue to hold up better than existing home sales due to ongoing inventory constraints, though the ESR group’s forecast calls for a modest deceleration in both new single-family sales and starts in coming quarters.

Fannie Mae forecasts 2023 mortgage originations to remain roughly unchanged from last month at $1.3 trillion.

In 2024, Fannie Mae expects purchase volumes to rise 10% to $1.4 trillion, a $7 billion increase from September’s forecast as stronger home price expectation outweighs minor downward revisions to the sales forecast.

“We expect the higher mortgage rate environment to continue to dampen housing activity and further complicate housing affordability into 2024,” Duncan said.

If you thought 8% mortgage rates were bad, what about 9% mortgage rates?

What was once unthinkable is now not so hard to believe, with 30-year fixed mortgage rates climbing ever higher.

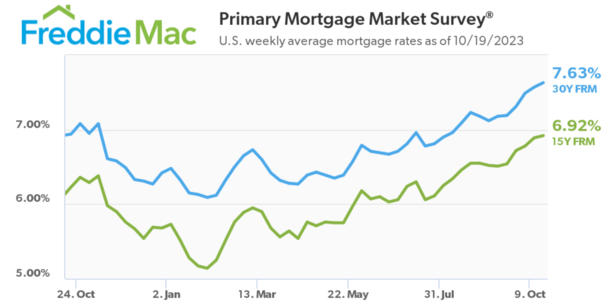

At last glance, the 30-year was priced at 7.63%, per Freddie Mac’s lagging weekly survey.

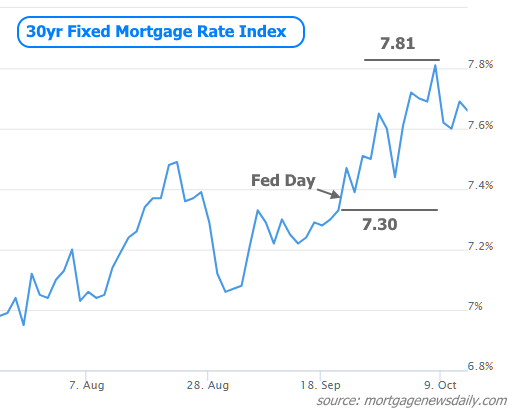

But other estimates have been higher, including MND’s daily index that put the 30-year at a ripe 8.03%.

And today I even saw someone calling for 12% mortgage rates by Q2 2024. Yikes!

Are 9% Mortgage Rates Next?

I’ve already written about 7% mortgage rates and 8% mortgage rates for that matter, at the time wondering if and when they’d arrive.

Now here I am writing about 9% mortgage rates, which is worrisome given those past fears coming to fruition.

However, that doesn’t necessarily mean we keep going higher from here, nor do we climb another 1% higher.

If you look at mortgage rates over the past year, they’ve gone up, but not by an enormous amount.

Take Freddie Mac’s weekly survey data, which pegged the 30-year fixed at 6.48% to begin 2023.

Today, they said the 30-year fixed averaged 7.63%, which represents an increase of 1.15%.

Yes, it’s higher. And yes, it’s further eroding home buyer affordability and hurting housing demand. But an increase of just over 1% over more than 10 months isn’t massive movement.

Consider the year 2022, when the 30-year kicked off January at 3.22% and ended with a bang at 6.42% in December.

Mortgage rates literally almost doubled during 2022 (short two basis points), while they’ve only risen 17% so far in 2023.

So the rate of ascent has slowed tremendously, if there is but one silver lining here (the other actually being that more high-rate loans being originated will present opportunity later).

Anyway, because mortgage rates are now a lot higher, the percentage gains pale in comparison. And there’s the question of rates nearing their peak.

I’m not convinced we go to 9%, at least by Freddie Mac’s measure, or even MND’s.

Sure, some loan scenarios with layered risk (low FICO score, high LTV, investment property, etc.) may already be at 9%. Or close.

But for the average home loan scenario, I don’t know if we go that high. If anything, 8% rates could signal a turning point.

The 21st Century High for Mortgage Rates Is 8.64% Per Freddie Mac

While we’re on the subject, I’d like the point out that the 21st century high for the 30-year fixed is 8.64%, per Freddie Mac data.

And it took place during the week of May 19th, 2000. So we are not far off from hitting a new high for this century, assuming rates continue their upward trajectory.

But until then, I’d be wary of anyone saying rates haven’t been this high since the 1990s, or something to that effect.

Also, recall that rates only increased 1.15% so far in 2023. They’d still need to rise another one percent by Freddie’s measure to get there.

Maybe that happens, maybe it doesn’t. Either way, there’s still a ways to go to reach that point.

Do We Need Higher Rates, or Just More Time to Let Them Sink In?

Everyone seems to be obsessed with higher and higher interest rates. As if pushing them ever higher will fix inflation.

But do they actually need to keep climbing into the stratosphere, or are we simply being impatient?

Perhaps they just need time to do their thing, which is basically what Fed chair Jerome Powell echoed today.

It coincides with the higher for longer mantra, that interest rates will need to stay at elevated levels longer than expected.

That could be enough to slow demand, consumer spending, home price appreciation, new hiring, etc.

They don’t necessarily need to keep going up from here. And that’s perhaps why the Fed is taking a wait and see approach with their own policy rate.

Of course, the Fed doesn’t control mortgage rates, but their own fed funds rate can act as a signal for the direction of the economy, and long-term rates such as 30-year fixed mortgage rates.

The fact that they’ve essentially stopped hiking should be a somewhat bullish sign that rates are sufficiently restrictive.

Powell also noted that the bond market might be turning its attention to the federal deficit and increased government spending, for which a couple wars might be to blame.

So there might be less importance to look at what the Fed is up to as there was earlier in the year.

The 10-Year Bond Yield Is About to Hit 5%

Meanwhile, the 10-year bond yield, which has been a fairly reliable indicator of 30-year mortgage rates, nearly hit 5% today.

At last glance, it was literally 4.99%, with apparent resistance at slightly higher levels. Some believe it could be a tipping point where bond buyers see opportunity.

If that’s true and yields calm down, chances are mortgage rates can too. At the same time, the mortgage rate spread between the 10-year yield is double its normal.

Usually around 170 basis points, it has widened to over 300 bps, meaning 5% yield plus that spread puts the 30-year fixed at roughly 8%.

During normal times, the math puts the 30-year fixed at about 6.75%. That alone would go a long way in fixing mortgage rates.

But until mortgage-backed securities (MBS) investors get more certainty, those spreads will remain wide.

Especially when you consider the prepayment risk if rates go down a lot and everyone refinances their 7-8% mortgages.

The takeaway for me at this juncture is that mortgage rates probably will continue rising from here, but maybe only gradually and by much smaller amounts.

That’s the good news. The bad news is they might have to linger at these high levels for longer than anticipated.

Ultimately, I really don’t want to write an article about 10% mortgage rates anytime soon.

Inside: Do you want to know the legit ways on how to make 200 dollars fast? This guide will show you how to start working on fast money ideas. With tips on side hustles, online trading, and more, you’ll be able to build up a healthy bank account in no time.

Do you want to know the different ways to make 200 dollars in your leisure time? I bet you do! We all would like extra money in our pockets.

In an era of digitization, earning an extra $200 in your spare time has become more accessible.

Various online platforms offer numerous possibilities to gain this amount swiftly without any major investments or specialized skills. Utilizing these platforms can not only help you reach your financial goal but also provide you with an enjoyable experience.

Let’s delve into the uncomplicated and quick ways to make 200 dollars fast.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Ways to Make Money 200 Dollars Fast

Discover the best ways to earn 200 dollars quickly by enlisting and acquiring the necessary skills.

You don’t even need to start a business or learn new skills virtually if you need the following legit ways to make $200 fast.

Just to note, you will find many of these ideas to be similar to how to make 300 dollars fast.

1. Sell Things You No Longer Need

Want to declutter and make some quick cash, to the tune of 200 dollars?

Start selling your no-longer-needed items and hit your goal. This method perfectly fits for minimalists looking to clear out space, or parents whose kids frequently outgrow their clothes and toys.

For instance, selling gently used toys or clothes could net you $200 in no time. Who knew making money could be as easy as cleaning up?

Even better turn this into a money-making business by flipping items for a living.

2. Sell gift cards

Struggling to add cash to your wallet? Turn those neglected gift cards lounging in your drawers into quick money.

Convert idle (Gift Cards) money to tangible cash by listing and selling on sites like CardCash at a discounted rate.

Another option is to trade your gift cards (you won’t use them) into something you want (like Apple or Amazon). So, weigh your options wisely.

In fact, you can read my CardCash review on my personal experience trading in gift cards.

3. Take on freelance jobs

Let’s start harnessing our skills and take on freelancing jobs online. Freelancing offers a flexible and income-generating platform, perfect for anyone looking to make a quick buck.

It is an effective income hustle, proven by data-driven facts. Best yet, it’s not exclusive to professionals alone. As a beginner, freelance gigs can offer an excellent starting point.

To get started, build a solid profile on a freelance platform that best suits your skills. Offer your virtual skills by getting jobs done in freelancing and experience good compensation for your comfort zone through this job.

4. Get Paid to Travel by Housesitting

Immerse yourself in a world of four-legged friends, greenery, and cozy, well-furnished homes while your wallet gets a welcomed cash addition.

Housesitting is not just about watching homes; it includes pet sitting and dog walking. All you need to do is join such platforms at no cost, set your rates and hours, and voila, you’re earning money while sleeping.

Essentially make money in your leisure time while enjoying the companionship of adorable pets. Who knew earning extra money could indeed entail wagging tails and furry hugs by signing up with Trusted Housesitters?

5. Rent Out Your Spare Space

Do you have spare space gathering dust? Turn it into a $200 goldmine!

Rent your unused closet, driveway, or extra room and have a quick injection of cash. Websites like Neighbor and VRBO are ideal platforms where you can list and rent out these spaces.

Start by exploring the listings in your area, identify the market range, and list your space accordingly. The extra income is just a few clicks away.

Best suited for property owners with underutilized spaces, this idea can serve as a consistent source of income and isn’t just a one-time fix.

6. Participate in Focus Groups

Get ready to voice your opinion and earn 200 dollars instantly!

Focus groups can be your golden ticket to making a quick $200. From my personal experience, they are organized discussions run by companies eager to pay for consumer insights.

Follow these steps and you could be cashing in:

Start by signing up and participating in a focus group that typically involves finding a suitable event in your area.

Involve yourself with popular websites like Bestmark.

Once you start searching for focus groups, you are likely to be targeted with sponsored ads on Facebook that match up to your opportunities.

By participating in discussions, I have earned a range from $50 to over $200.

7. Babysitting is Great Money

Looking for a quick way to pad your wallet? Babysitting is the golden ticket.

This gig is ideal for teenagers, college students, or anyone with some free evenings or weekends who enjoys hanging out with kids and can tolerate the occasional tantrum.

Start marketing your talent by creating a profile on care portals like Sittercity. Having a certificate in CPR can increase your profile and give assurance to the parent looking for a babysitter.

Remember to start with your personal network. Friends, family, and neighbors are a great way to kickstart your babysitting journey. With a bit of effort, you could be earning in less than 24 hours.

8. Make Videos

Are you passionate about making your own video or editing someone’s video to earn an incredible 200-dollar quickly? Jumpstart your day by hitting each click on your computer and adding sound effects on various kinds of videos on any social media.

You can also monetize your own videos by becoming a YouTube vlogger content creator and signing up for the YouTube Partner Program.

With an incredible shift to a remote life, you can now instantly earn from making your own videos through ad sponsorship, brand affiliation, and paid subscription on any application.

9. Get a Side Hustle

Engage yourself in a side gig, a savvy way to rake in cash promptly. Side hustles harmonize best with go-getters seeking financial flexibility or pursuing dreams outside the 9-to-5 grind.

Kickstart your hustle journey with free webinars or training. These platforms provide insights into key strategies and the nitty-gritty of the field.

Get cracking now to transform your monetizing dreams into reality!

Very popular are these side hustles for men. Or especially these side hustles for college students!

10. Online trading with Stocks and Options

Trading stocks and options emerge as a financial adrenaline rush, providing a swift track to earning money. You can convert spare moments into potential cash gains with just a few clicks.

Expert tips include starting with research, practicing with a simulation trading account, and diversifying your portfolio to mitigate risks.

The journey to online trading success begins with educating yourself. You must participate in a free investing webinar to undergo training to grasp trading basics, understand market trends, and form your strategy.

Check out how I learned to trade stocks and options with this Trade and Travel review.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

11. Take Up a Part-Time Job

Eager to fill your pockets a bit more, huh? Part-time jobs are your key to fast cash without compromising your ‘me-time’.

A part-time job supplements your primary income, leaving your piggy bank a bit heavier. Where you get to choose the timing that fits around your primary commitments.

Honestly, some of the best part-time jobs are actually low-stress jobs after retirement. You don’t need to wait for extra money. So, go get that financial freedom and earn more than just the minimum.

12. Yard Sale

Hosting a yard sale is a nonchalant trick to amass cash swiftly. It’s your winning lottery ticket staring at you from your cluttered garage floor.

Kick-off by hosting it on Friday or Saturday, when shopping spirits fly high! If your neighborhood or city has a date set for a community garage sale or jackpot, you’ll be swimming in extra traffic.

Don’t hesitate to unleash your inner salesperson, but remember, no rule binds you to wait for an event to rake in cash.

Remember, yard sales are your fast lane to quick money, and with these tips, you’re ready to speed!

13. Make Money with Your Collectibles

Turn your old favorite collection of Pokemon cards or Beanie Babies into a treasure chest waiting to be unlocked.

This money-making method is perfect for those who have carefully amassed certain collectibles over time. Sign up for eBay now and enlist your collectibles, antiques, and merch items to earn from it.

Want to kickstart your financial journey with collectibles? Find the most popular items to flip as well as insights on what to look for.

14. Collect and sell items from the trash

It’s time to transform your everyday trash into a hefty stash of cash! Collecting recyclable trash can be turned into a worthwhile moneymaker.

Start by saving cans, bottles, or scrap metal that you’d usually throw away. Then, locate a local recycling center that’s willing to pay for these items – the prices may surprise you!

This method is great for anyone willing to invest a little time and energy, particularly those who are environmentally conscious and eager to declutter. Perfect job for those who are frugal green.

Think about it, that old toaster might just be your next treasure trove! You may even find some highly valuable items in the trash to flip!

15. Sell Used Clothing

Selling used clothing is a clever and straightforward way to turn spare time into real cash.

Remember, a vibrant description for your clothes will attract buyers, so play up any unique or high-quality aspects of your garments.

Fashion enthusiasts want to earn a quick buck on the side. Begin by taking a charming picture of your clothes and posting it to Facebook Marketplace and ThredUp.

16. Do Social Media Marketing

Welcome to the era of making money by simply being social media savvy. Transform your digital skills into quick cash through Social Media Marketing.

Explore the digital world that awaits with all of the social media platforms. You can create engaging content while responding to the readers.

Take your skills to the next level, consider enriching your knowledge via a free webinar or online training.

This is an easy job that pays more than $25 an hour.

17. Sell Printables on Etsy

Do you love making creative paintings and printable designs? Imagine, your beautifully designed chore chart or a fascinating word puzzle bringing joy to scores of customers.

You can dive into this free training to jumpstart your side hustle. This method is a sure-shot hit for you.

Find out which digital products to sell on Etsy.

18. Invest in Cryptocurrencies

Do you have extra money in savings in your account and don’t know where to invest it?

Since 2008, cryptocurrency has taken the world by storm. Known for its decentralizing nature and secured by cryptography, it’s no regular dough.

Turn the tides in your favor and download an investment app to make your $200 grow faster. Consider taking a free webinar or training for a crash course.

You see, investing in cryptocurrencies is not a heavy-duty task. With the right smarts and patience, you can ride the next crypto wave!

19. Get Paid to Click

Among the numerous ways to earn an extra $200, getting paid to click is a simple and fun method.

Websites provide users with the opportunity to earn money through ‘pay to click’ surveys or rewarding viewers for ad consumption. Additionally, apps such as Survey Junkie and Swagbucks allow you to earn money by taking surveys, participating in focus groups, or simply navigating the web.

Each user generally earns from a few cents to a dollar per click. With patience and consistent effort, you can gradually accumulate your earnings to reach your $200 target.

Here are the top legit survey platforms:

20. Check Out Cashback Apps

Earn a cashback every time you shop at your favorite retail store or online.

Start off by signing up for apps like Dosh, Fetch, Rakuten, and Ibotta which offer bonuses just for signing up.

Lastly, apps like Acorns or CoinOut provide cash back on everyday shopping, even rounding up your purchases to add a bit more to your savings.

21. Do Odd Jobs as a TaskRabbit

Wanna earn cash quickly? Sign up and do freelance labor with TaskRabbit.

This user-friendly job marketplace connects people in need of task assistance with capable individuals willing to complete the tasks for a fee. It offers a diverse array of tasks, from assembling furniture and helping with moves to painting, yard work, and minor home repairs.

Just by performing various tasks, such as events staffing, running errands, or crafting. With the average TaskRabbit making double the minimum wage, this might be the gig for you.

TaskRabbit

Find local jobs that fit your skills and schedule.

With TaskRabbit, you have the freedom and support to be your own boss.

Plus set your own rates!

Get Started

22. Earn Money with Your Knowledge

Using your personal set of skills is a major advantage in freelancing platforms such as Fiverr, Upwork, and Freelancer.com.

Be it graphic design, content creation, SEO mastery, or even web development, you can monetize these proficiencies directly from your home. Data shows a significant growth in the gig economy over the past decade, suggesting a flourishing potential for remote work and online income generation.

Remember, your vast knowledge pool is your strength here. So, focus on what you’re best at, and let the money flow in.

Indeed, by effectively marketing your skills, pulling in a sum over $200 within a few hours is achievable. Remember to value your work appropriately and not devalue your aptitude just to land a job.

23. Tutoring

Online tutoring provides plenty of diverse opportunities in various subjects beyond just English. You can choose to specialize in specific topics and decide to tutor students of different age groups – from young children to college students.

Platforms like VIPKID and Magic Ears allow qualified tutors to offer virtual classes, specifically in the English curriculum for kids aged 4-12 years.

Tutors are usually compensated with payments ranging from $7 – $9 per class or up to $25 or more per hour. Also, you can increase your rate once you gain experience and build a reputation as a tutor. With in-person tutoring, you can expect to earn $20 an hour or more.

24. Petsitting

Looking for a quick way to make $200 fast? If you’re an animal lover, offering pet-sitting services isn’t just enjoyable, but also quite profitable.

Simply sign up with platforms like Rover, you can possibly get paid two days after service completion and you can always set your own rates. Just by walking the dog from house sitting.

Fun fact: Dog sitters often earn up to $50 a day. This is flexible and enjoyable work that could definitely help you reach your $200 target quicker than you’d imagine!

Rover

Get paid to play with pets!

Rover makes it easy and promotes you to the nation’s largest network of pet owners.

Earn money doing something you love.

Become a Sitter

25. Collect Scrap Metals and Junk

One man’s trash is indeed another man’s treasure.

Thinking of ways to earn quick cash? Consider collecting scrap metals and junk. This simple but profitable task can be done by anyone, with no particular set of skills necessary. All you need are keen eyes, a truck, and, admittedly, a little bit of strength to do the following:

Identify Metals: Start by identifying the most valuable metals – brass, copper, and aluminum.

Collect: Gather your metals, either from your home or by browsing local dumps. Remember, one man’s trash can be another man’s treasure.

Sell: Locate a local scrapyard and sell your haul at a fair price.

Keep in mind that patience is key; you might start with just $100 a day, but with experience, this can increase to a lucrative $500 a day!

26. Cash Out Your Coins

Are you sitting on a pile of coins? Maybe it’s time to cash them out. Here’s how:

Gather all your change together. Check under the sofa cushions, in car cup holders, and even in the bottom of your bag.

Take your coins to a coin-counting machine. These can be found at many grocery and department stores as well as your local bank.

Deposit these coins in a savings bank.

Expert Tip: Many banks provide free coin-counting services to their customers. Save on the counting machine charges by using these instead.

27. Run A Dropshipping Business

Dropshipping is a retail fulfillment method where you sell products without ever handling the inventory. This side hustle could potentially make you a quick $200 if executed strategically. Ready to dive in?

To level up, consider enrolling in free webinars on sites like Skillshare or free dropshipping training programs like Oberlo 101. This method is most suitable for those game to learn the ins and outs of online retail business and are ready to deal with customer interactions.

Remember, selling high-demand items will turn a quicker profit!

28. Do Micro Tasks

Looking to make cash fast? Turn your spare time into cash by capitalizing on microtask websites and get paid for completing simple jobs!

This method is particularly effective for those with meticulous attention to detail and those who can afford to spend some time on basic tasks such as data entry, data verification, information sorting, and transcription.

Microtasking might not be a golden goose, but it sure can help you accrue $200 surprisingly fast. The beauty of this hustle is in its simplicity, making easy money with minimal to no investment.

29. Find Sign-Up Bonuses

Did you know that many banks and credit companies offer sign-up bonuses as a strategy for attracting new clients?

For instance, some banking promotions in the United States can offer bonuses of up to $300 in total value when you sign up for a new account or credit card. Also, there are several credit cards that provide bonuses ranging from $500 to $800 or more, simply for registering and spending a defined amount within a specific timeframe.

Some cards, such as Chase Sapphire Preferred, offer lucrative rewards like a $1,000 bonus after a spend of $4,000 in the first 3 months.

It’s definitely rewarding to explore these possibilities to supplement your income, but it’s crucial to maintain a good credit score and commit to paying off your balance monthly to avoid any interest charges.

30. Cash Advances

Cash advances offer a rapid solution, but it’s essential to use them wisely.

Basically, a Cash advance is an advance on your next paycheck, and yes, it’s a viable way to get your hands on some quick cash. Also, some budget apps like Chime offer this service automatically.

Keep in mind, though, it’s an advance and not additional income. So, plan your expenses wisely and make it count!

FAQ

If you’re on a quest to make $200 as fast as possible, we’ve got your back. From selling items you own to completing quick gigs online, there is a plethora of opportunities out there for everyone.

For example, suppose you’re handy at a skill – be it haircuts, car repairs, pet sitting, or painting. You can start by offering your services to people in your neighborhood.

Or, if you’re the digital savvy type, consider selling items you no longer need on online platforms such as Facebook Marketplace or Craigslist. You’d be surprised at how quickly you can make money from items collecting dust in your home.

Ultimately, make sure you choose a fast money-making plan that aligns with your skills, interests, and resources. Go forth and rake in that cash.

If you need to make $200 today, you have a range of options at your disposal.

You can try different online strategies, including participating in online surveys, offering your skills on freelance platforms, or even reselling items online. While many people will sell the idea of a blog to make money, that is not a way to make money today.

Remember, the key is to zone in on tasks that require minimal effort but offer swift returns; these could include grandma sitting, dog walking, or even participating in online offers and promotions.

To kick-start your financial venture, locate valuable items in your home that you no longer need. Your dusty old guitar or that once-loved designer handbag could do the trick. Sell these items on widely used platforms such as Craigslist or Facebook Marketplace for instant cash.

Also, in the digital age, skills are an asset. Offering your skills on platforms like Fiverrcan turn your talents into quick cash. Don’t underestimate the power of quick gigs!

Tapping into the world of free sign-up bonuses can also fill your wallet quickly. Or even participating in a paid focus group!

If you need to make $200 quickly, there are several tried and tested methods. You could start by driving for Uber or Lyft for the evening during a concert.

My preferred method is trading options in the stock market. While this one is a skill, I developed over time. It has proved to be a tried and true method for me to make $200 in a few hours.

Time to Get 200 Dollars Instantly

By reading this article, you have learned and discovered the most effective ways to earn $200 quickly.

In order to have quick success, here are tips to help you out:

Sign up for a complimentary training or webinar that focuses on effective and proven methods of earning money swiftly.

Learning from other’s experiences can certainly save you some trial and error.

Ensure these training modules offer you practical skills and insights rather than just theory. Real-world applications of these strategies are what will help you rake in some quick cash.

Remember, your motivation and dedication are as important as the information and tools you acquire.

If you are looking to make a little bit more, check out how to make 500 dollars fast. Or even how to make 2000 fast!

Know someone else that needs this, too? Then, please share!!

Our rate index has rapidly grown in popularity and exposure in recent years because it is timely and because it accounts for upfront costs in a way that other single-number indices cannot. Because we began this effort in 2009, we can only technically say our index is the highest in 14 years, but there’s no question that today’s mortgage rates are the highest in 23 years.

That’s actually rather unremarkable given the prevailing trend in rates. “8%” may be an interesting milestone for headlines, but it isn’t much higher than yesterday’s 7.92%–also the highest rate in 23 years.

The first break above the 23 year ceiling took place in late 2022 and it wasn’t challenged again until August of 2023. Since then, however, we haven’t made it more than a few weeks without hitting a new long-term high. The time since the Fed’s September 20th announcement has been particularly bad with SEVEN new 23 year highs in less than a month.

While unfortunate, this is also rather unremarkable. This is a rising rate environment. Bonds/rates are increasingly capitulating to the notion of “higher for longer.” It makes for a typical market pattern where the swings between highs and lows are smaller but more frequent. In that sense, today was just another day on the same old path.

But where is that path leading? Are rates headed to 10%? It’s too soon to say or know. Certainly, we would never want to rule out the possibility of any interest rate that is only 2% away from current rates. On the other hand, if the Fed is correct in their assessment that no further rate hikes are needed to facilitate monetary policy, it would take increasingly surprising data/events to push rates higher at the prevailing pace.

This isn’t to say rates can’t or won’t go higher. Rather, the goal is to say that if the economy begins to soften as the Fed expects and if inflation remains roughly in line with the last few months, upward rate momentum should be dying down, all other things being equal. One big unknown is the stance of fiscal policy/spending where markets have increasingly expressed concern over Treasury issuance implications.

Treasury issuance matters because Treasuries set the tone for just about every other interest rate in the US. If issuance is higher than expected, the government has to pay higher rates to attract sufficient demand. Mortgage-backed securities tend to move in the same direction as Treasuries, so if 5, 7, 10yr yields are higher, mortgage rates will typically be higher as well. Every time the government announces a big spending initiative (or legislation that implies lower revenues), the bond market runs the risk of protesting by breaking another rate ceiling.

US mortgage rates rose for the third week in a row but stayed just under the 7% threshold.

The 30-year fixed-rate mortgage averaged 6.96% in the week ending August 10, up from 6.90% the week before, according to data from Freddie Mac released Thursday. A year ago, the 30-year fixed-rate was 5.22%.

Elevated mortgage rates in the wake of the Federal Reserve’s historic rate-hiking campaign have taken home affordability to its lowest level in several decades. Buying a home is more expensive because of the added cost of financing the mortgage, and homeowners who previously locked in lower rates are reluctant to sell. The combination of low inventory and high costs has squeezed would-be homebuyers.

Rates have been above 6.5% since the end of May, and this week’s average rate matches the highest level since November.

“There is no doubt continued high rates will prolong affordability challenges longer than expected,” said Sam Khater, Freddie Mac’s chief economist. “However, upward pressure on rates is the product of a resilient economy with low unemployment and strong wage growth, which historically has kept purchase demand solid.”

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. The survey includes only borrowers who put 20% down and have excellent credit.

All eyes on employment and inflation data

The rate stayed elevated this week after the Federal Reserve highlighted its reliance on jobs and inflation data in its July monetary policy meeting and in recent comments.

Markets had been waiting for July’s inflation report, released Thursday morning. That report showed inflation rose in July to 3.2% annually, compared to a 3% annual increase in June. That was the first time inflation picked up in a year. The data also showed that shelter costs contributed 90% of the total increase in inflation last month.

“July’s Consumer Price Index holds significant importance for the Fed’s upcoming decisions,” said Jiayi Xu, an economist at Realtor.com.

That faster pace of price increases could support the Fed’s concern that the battle is not over, Xu said. The Fed also will consider the forthcoming August employment and inflation data prior to the next policy meeting, in September.

In addition, the most recent jobs report offered some mixed signals about the labor market, Xu said, including a smaller number of net new jobs added and a dipping unemployment rate.

“While July’s jobs report itself is very unlikely to have a direct impact on the Fed’s upcoming decision, the decline to a 3.5% unemployment rate may imply that more significant slowing is needed to align with the Fed’s projected year-end rate of 4.1%,” she said.

Affordability challenges remain

Borrowing costs will remain elevated until financial markets see an “all clear” signal from the Federal Reserve, accompanied by a stop in interest rate hikes, said George Ratiu, chief economist at Keeping Current Matters, a real estate market insights and content company.

While the Fed does not set the interest rates that borrowers pay on mortgages directly, its actions influence them. Mortgage rates tend to track the yield on 10-year US Treasuries, which move based on a combination of anticipation about the Fed’s actions, what the Fed actually does and investors’ reactions. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

Currently mortgage rates are running higher than they should be in relation to the 10-Year Treasury, given historical trends, he said. The spread between the 30-year fixed rate mortgage and the 10-year Treasury hovers around 300 basis points, Ratiu pointed out, a level seen only a handful of times in the past 50 years and mostly during periods of high inflation and economic turbulence.

“In the absence of the elevated risk premium and hewing closer to a historical average of 172 basis points, today’s 30-year fixed mortgage rate would be around 5.7%,” Ratiu said.

Homebuyers remain sensitive to elevated interest rates, with applications for mortgage rates dropping last week, according to the Mortgage Bankers Association.

“Due to these higher rates, there was a significant pullback in mortgage application activity,” said Bob Broeksmit, MBA president and CEO. “Both prospective buyers and sellers are feeling the squeeze of higher rates as well as low housing inventory, which has prompted a pronounced slowdown in activity this summer.”

While real estate markets are benefiting from more people gaining jobs and better paychecks this year, sales of existing homes have been lagging, said Ratiu.

“The challenge comes mainly from too many buyers chasing not enough available properties,” he said.

Looking to history as a guide, Ratiu said mortgage rates tend to start cooling once inflation abates, with a six-to-eight-month lag.

Buying a home is one of the most expensive purchases you’re bound to make in your life. That’s why it’s so important to get the right mortgage before you sign on the dotted line.

A few differences in mortgage rates or other terms can equate to tens of thousands of dollars either spent or saved. But with so many options available on the market, it’s hard to know where to start.

There are traditional lenders and online mortgage lenders, local ones and large multinational ones. Plus, many lenders specialize in different types of loans.

To get started, browse some of the best mortgage lenders and find a few that match your needs.

Best Mortgage Lenders & Online Loan Marketplaces of 2023

You have several great options available, from online lenders to brick and mortar branches, from excellent credit to bad credit lenders. Check out the complete list of lenders to find the best choice for your next home loan.

loanDepot

Offering home loans in all 50 states, loanDepot works with a wide range of borrowers. The minimum credit score for most loans is 620. However, some government-insured programs may allow your credit score to be as low as 580.

You also have access to various mortgage options. They provide fixed and adjustable-rate mortgages, jumbo mortgages, FHA loans, VA loans, and home equity loans.

If you want to talk over these choices, you’ll appreciate the online lender’s no steering policy. That means your loan officer doesn’t receive any incentive to point you in any one specific direction, so you can trust the advice you get.

Do keep an eye on your origination fees. Depending on your application, those could cost you anywhere between 1% and 5% of your home’s purchase price.

The first step of applying for a mortgage is talking to a loan officer. However, the application process occurs online. That means you can do the bulk of the work at your convenience.

Read our full review of loanDepot

LendingTree

LendingTree is the best if you want to compare multiple offers as they partner with the largest network of lenders who compete for your business.

You can get up to five different loan offers within minutes of submitting your application. If you’ve already found the place you want to call home, start here.

Another great feature is that you can submit a request online for conventional, FHA, or VA loans. LendingTree’s website also provides many in-depth resources for first-time buyers, regardless of where you are in the process.

They provide tips for qualifying for a mortgage, mistakes to avoid when purchasing a house, and a bank of frequently asked questions. For home loan guidance and receiving multiple offers at once, LendingTree is the place to go.

Read our full review of LendingTree

Rocket Mortgage

Rocket Mortgage is a great pick if you prefer applying for a mortgage online and has excellent customer service when needed.

Rocket Mortgage provides FHA loans, USDA loans, and Freddie Mac and Fannie Mae loan products that come with down payments as low as 3%.

A branch of Quicken Loans, Rocket Mortgage’s online application process is highly streamlined with an approval time of just a few minutes. You can also avoid the hassle of paperwork by using a secured platform to share your financial information.

Once you have your proposed interest rate, you can test out different house prices and down payment amounts to create a customized monthly payment. Once you get a contract on your new home, closing is easy and takes place at a location of your choice.

Read our full review of Rocket Mortgage

New American Funding

New American Funding offers conventional, FHA, and VA loans. You can also explore options for a mortgage that includes a home renovation loan.

Less common available loans include jumbo loans, reverse mortgages, and interest-only mortgages.

New American Funding also has first-time homebuyer loan programs available and works with down payment assistance programs in 14 states, including California, Illinois, Florida, and Texas.

Once you have an idea of what you’re looking for, go step-by-step through their questionnaire to get more details on potential loan terms you could qualify for.

Read our full review of New American Funding

Alliant Credit Union

Alliant Credit Union offers both fixed and adjustable-rate mortgages, and you can qualify with a down payment as low as 3% of the home price.

On a $200,000 house, that equates to just $6,000 needed in cash for your down payment.

You can qualify anywhere in the country and enjoy a low origination fee of just $995. If having cash on hand is an issue for you when purchasing a home, check out Alliant to see how they stack up to other mortgage lenders.

Alliant also offers home equity lines of credit.

Read our full review of Alliant Credit Union

Guaranteed Rate

Guaranteed Rate originated about $24 billion in mortgages for 2018, which is no surprise. The website allows you to get an idea of your qualifying interest rates easily.

All you need to do is input just a few details about your estimated credit score and the type of home you’d like to buy.

You can then browse several loan options to see your interest rates and APR options. It’s easy to compare mortgage options to get an idea of which kind of mortgage is best for you.

You can also browse their Knowledge Center for tons of in-depth resources on the home buying process.

Read our full review of Guaranteed Rate

First Internet Bank

Solely based online, First Internet Bank is an online mortgage lender that allows you to complete the entire mortgage application from your own home.

However, you can still call to talk to them on the phone whenever you’d like. First Internet Bank also offers a wide range of loans, including conventional, jumbo, FHA, VA, USDA, and home equity loans.

You can get a personalized mortgage rate in less than a minute. You can even sign up for email alerts to track mortgage rates as you shop for houses.

Getting prequalified takes just moments, and you can then submit the appropriate loan documents to get pre-approved. This extra step gives you a leg up on the competition once you’re ready to make an offer on a home.

Read our full review of First Internet Bank

Carrington Mortgage Services

If you have a question about a loan, you can chat with a Carrington representative from 7 a.m. until 6 p.m. PST. They’ve even been featured on Lifetime’s Designing Spaces.

So, it should go without saying that Carrington is available, and they want your business. Peruse their website, and you’ll see how user-friendly it is within moments.

They have a list of mortgage tools that will help you understand what you can afford. They also have a step-by-step guide outlining the loan application process.

Additionally, you’ll find a list of common mortgage terms that banks use, an explanation of loan types, and a mortgage application checklist.

Carrington is a top-notch mortgage company with an intuitive, user-friendly interface and great rates to boot.

Read our full review of Carrington Mortgage Services

Truist

Truist has a significant online presence for mortgages in addition to its physical branches throughout the country.

You can create an online account to apply for a mortgage loan or enter your zip code to find a location near you. Truist offers a suite of mortgages on top of the typical government-backed loans, including high-cost home financing.

Alternatively, if you meet certain income eligibility requirements, you may qualify for a HomeReady/Home Possible loan, which can help make homeownership more affordable.

Truist also offers a unique program for doctors to help licensed medical interns, residents, and fellows qualify for a mortgage.

Read our full review of Truist

U.S. Bank

Prequalify online within minutes, and from there, you can start making intelligent decisions about your future home. U.S. Bank offers conventional, fixed-rate loans, VA loans, ARMs, and FHA loans.

Want to design and build your dream home? They even have new construction loans and investment property loans.

They also have a “loan officer near you” app that lets you speak with someone who’s knowledgeable about your area and what it is specifically you’re looking to purchase.

You can also call their national number directly and someone will speak to you right then and there. U.S. Bank even has a FAQ section that answers questions you didn’t even know you had.

Read our full review of U.S. Bank

Other Top Mortgage Lenders to Consider

Didn’t find one on the list that you liked? Read our reviews of some other good lenders:

How to Find the Best Mortgage Lender

To find the best mortgage lender, it’s wise to compare mortgage rates and terms from multiple lenders. This will help you find a lender that offers the best deal. The lending standards may be similar across lenders, but the way they implement them may vary.

You might be surprised at how much variation you see in your different offers. Plus, mortgage loans can be structured in various ways to accommodate your financial situation or personal preferences.

If you don’t have a lot of spare cash on hand, you may be able to pay a higher interest rate to avoid higher closing costs. If you want to lower your monthly payments, your lender may let you pay for points to qualify for a lower rate.

It’s also helpful to understand where mortgage rates are right now and where they’re headed. A good real estate agent may be able to help you with this as they usually know the market quite well.

Know your credit score and the type of rate you should qualify for so you can negotiate the best deal possible. Some credit card issuers give you your FICO score for free.

How to Compare Mortgage Lenders

Here are some questions you may want to ask when searching for the best mortgage lenders:

How is their customer service?

What can they tell you about their closing costs and other associated lender fees?

How much do you need for a down payment?

How quickly can you close once you find a home?

These are all questions you should pose to at least two or three separate mortgage lenders.

Compare answers and determine which lender can offer you the best financial deal and meet any other expectations you have surrounding the loan process.

What should you look for in a mortgage lender?

Finding the best mortgage lender for your needs can take a while, so give yourself time. If you’re interested in a particular type of loan, such as a VA loan or an FHA loan, make sure the lender actually offers it.

Mortgage Interest Rates

Pick at least two or three mortgage lenders with good customer satisfaction ratings to compare pre-qualification offers. Then, take a look at the interest rates they offer you, whether the rate is fixed or adjustable, and what your monthly mortgage payments will be.

Taxes and Mortgage Insurance

Make sure they include an estimate for taxes and mortgage insurance, not just your principal and interest because that can make your payment increase by at least a couple hundred dollars.

Property Taxes

If you live in a more expensive area like a major city, expect to pay even more for property taxes. Of course, you can always refinance to get a lower rate down the road, but it’s expensive because of closing costs.

Fees and Closing Costs

Next, compare the closing fees of each mortgage lender. Some of the expenses won’t change from lender to lender. A title search, for example, will cost about the same amount regardless of what lender you go through. Origination fees, on the other hand, can vary greatly.

Expect to pay 3% to 5% of the loan amount for total closing expenses. Which end of the spectrum you end up on can make a huge difference in how much cash you’ll need.

A good lender will help you explore your options based on how much cash you have and how long you plan to be in the home.

Mortgage Points

If you have extra money and intend to make your new place your “forever home,” it may be worth paying extra points at closing in exchange for a lower mortgage rate. Ask each lender for different scenarios to see which best fits your individual needs.

How can you get pre-qualified for a mortgage?

There are two ways to start the mortgage process: a pre-qualification and a pre-approval.

Getting prequalified is an informational step to get an idea of what rates to expect and how much you can borrow based on your income and debt levels. You don’t have to supply any documentation at this time.

The quotes you receive are not set in stone and are subject to change with your official application. But it’s good to find out what types of loans you should consider, how much cash you’ll likely need, and what price range of home you should look at.

You’ll need more to actually make an offer on a home because most sellers don’t view a pre-qualification as official enough to indicate likely financing.

What is a pre-approval letter?

A pre-approval letter takes the pre-qualification process one step further. You essentially submit your entire application and all the accompanying documentation.

This includes things like your tax returns from the last two years, bank statements, explanations of any negative remarks on your credit history, and employment verification.

The mortgage lender also performs a hard credit pull to determine your mortgage interest rate. It takes a bit of time, but once you’ve been pre-approved, the lender provides a letter stating how much of a loan you qualify for and how much down payment you can provide.

When you submit an offer on a house, this addition makes it much stronger because the seller knows that you’re likely to get approved for the mortgage. Once your offer is accepted, you can lock in an interest rate with your mortgage lender for a certain number of days.

What type of mortgage should I get?

Some quick introspection is necessary to answer this question. Start by examining your financial position, household needs, and long-term goals. How secure is your income? Where do you want to live in the next few years? How much money can you raise for the down payment?

Answering these questions helps you pick the most appropriate mortgage type for you. Typically, the choice boils down to a conventional or government-backed mortgage. Conventional home loans have stricter requirements, such as a high credit score and sizable down payments. Government-backed loans allow lower credit scores and little to no down payment to qualify.

There are eight different types of mortgages spread across the two categories. Dig in as we explore each of them below.

8 Types of Mortgage Loans

Conventional Mortgage Loans

Conventional mortgages are home loans that the government doesn’t insure and fall into two categories: conforming and non-conforming.

A conforming loan means the loan falls within limits set by the Federal Housing Finance Agency. Non-conforming loans, such as jumbo loans, exceed the FHFA limit, which varies between counties.

Conventional Loan Requirements

Conventional loans have stringent credit score and debt-to-income ratio requirements. Mortgage lenders approve borrowers with a credit score of at least 620 and a 20% down payment. Buyers who can put at least 3% down may also be eligible but must pay primary mortgage insurance.

Pros

Cheaper than unconventional loans

Can qualify by putting 3% down

Cons

PMI on deposits less than 20%

Strict credit score and DTI ratio requirements

Best for: Buyers with large down payments, high income, stellar credit scores, and excellent credit history.

Fixed-Rate Mortgage

A fixed-rate mortgage is a home loan that carries a fixed interest rate over its lifespan. Once the interest rate is locked in, it’s not affected by changes in market rates.

Fixed-rate mortgages are the most popular home loans, thanks to their predictability. Knowing your mortgage payment every month helps borrowers more easily plan their finances. As a result, you can be sure that there are no surprises month-to-month.

Fixed-Rate Mortgage Loan Requirements

Lenders use your credit score, debt-to-income ratio, credit history, income, and down payment to determine eligibility and set mortgage rates. Credit scores are a primary determinant, and most mortgage lenders approve borrowers with scores above 620.

Credit scores above 740, low DTI ratio, stellar credit history, and a significant down payment command the most competitive mortgage rates. Conversely, low credit scores lead to higher interest rates, and a down payment of less than 20% triggers the need to pay private mortgage insurance (PMI).

Fixed-rate mortgage terms range from 10 to 30 years, but 30 and 15-years loans are most popular. The length of your mortgage also determines the interest rates and monthly payments.

Pros

Predictable monthly payments

Nonfluctuating interest rates

Easy qualifications

Large tax deductions

Cons

Higher mortgage rates

High-interest amount

Slow equity growth

Adjustable-Rate Mortgage

As the name suggests, adjustable-rate mortgages carry an adjustable interest rate set by the prevailing market rate. An ARM starts with a fixed interest rate for a few years then changes to a variable rate for the remaining loan term.

An ARM can be locked for one, three, five, seven, or ten years, but 5/1 ARM loans are most common. With a 5/1 ARM, the interest rate is locked for the first five years and then adjusted annually for the remainder of the term.

Typically, the interest rate on an ARM adjusts upwards because the initial interest rate is often lower than the prevailing market rate.

Pros

Predictable and low initial monthly payments

You can save a considerable amount of money at first

Cons

Increased mortgage rates

Monthly payments can be expensive

Best for: Borrowers who are likely to secure a pay hike in the future but want to lock in lower rates when their income is lower.

FHA Mortgage

An FHA loan is a mortgage guaranteed by the federal government and insured by the Federal Housing Administration (FHA). You can only secure an FHA loan from an FHA-approved lender. The agency insures home loans are issued by accredited lenders such as credit unions, banks, and mortgage companies, protecting mortgage lenders if a borrower defaults on payment.

FHA Loan Requirements

These loans help modest-income households buy a home. You need a 3.5% down payment, a credit score of 580 or higher, and a DTI less than 50 to qualify for an FHA loan. You can be eligible with a 500 credit score if you raise a 10% down payment.

Since the government insures FHA loans, FHA lenders can extend favorable terms to people who wouldn’t otherwise qualify for a mortgage. FHA loans carry a mortgage insurance premium (MIP) for at least 11 years, and FHA mortgages with less than 10% down must carry FHA insurance over the life of the loan.

You can use an FHA to buy or refinance a condo, single-family home, 2 to 4-unit multi-family home, and select manufactured homes. In addition, some FHA loans can finance new construction and home renovation.

The limits on FHA loans vary by county, and as of 2021, you can borrow between $420,860 and $970,800. Your county’s living costs determine the limit on FHA loans.

Pros

Requires a 3.5% deposit

High loan limits

Accommodates low credit scores

Cons

Mandatory mortgage insurance

Only finances primary residence

Best for: Low and moderate-income households and borrowers without a large down payment.

VA Mortgage

VA loans are guaranteed by the U.S. Department of Veteran Affairs but issued by private lenders such as mortgage companies, banks, and credit unions. VA loans help veterans, current service members, and eligible spouses buy a home without a down payment.

The government guarantee allows VA accredited lenders to extend favorable terms to borrowers without a deposit. Although VA loans carry attractive terms, they have stringent qualification requirements. Only qualified active-duty service members, veterans, and surviving spouses can apply for VA loans.

VA Loan Requirements

While a VA loan offers 100% financing when buying a home, VA lenders will consider credit score, DTI, and income level when issuing a loan. There are no minimum credit score requirements, but you typically need a credit score of at least 620 to qualify.

In addition, veteran and surviving spouses can only use a VA loan to finance their primary residence. But active-duty service members can use the loan to buy a second home if they plan to move into it within 60 days of closing.

Your county of residence determines the VA loan limit. As of 2021, the county limit on VA loans ranges from $548,250 to $822,375, depending on the cost of living. However, you can get a VA loan that exceeds the county limit if you make a down payment.

Pros

No down payment

Competitive mortgage rates

Lower closing costs

No private mortgage insurance

Cons

Can’t finance an investment property or vacation home

Carries a VA loan funding fee

Strict property requirement

Best for: Eligible veterans, active-duty service members, and surviving spouses.

USDA Mortgage

USDA loans are zero-down payment government-backed mortgages guaranteed by the U.S. Department to help rural homebuyers. The loans help people with modest incomes who can’t buy homes using traditional mortgages.

USDA home loans are offered under the USDA loan program or USDA Rural Development Guaranteed Housing Loan Program. The program aims to bolster the economy and improve the quality of life for people in rural America. It waives the down payment, offers competitive mortgage interest rates, and is highly accessible.

You can apply to any of the three USDA loan programs, including:

Loan guarantees: The USDA guarantees a mortgage issued by a local lender. That allows you to access a loan with attractive terms without a deposit.

Direct loans: These are subsidized home loans for low and very low-income borrowers with interest rates as low as 1%.

Home improvement loans and grants: These are loans or outright grants to help homeowners upgrade or repair their homes. Some loan packages pair the loan with grants of up to $27,000.

USDA Loan Requirements

Qualifying for a USDA-backed home loan depends on the income and size of your household. The income limits vary by location and depend on your county of residence. Only U.S. citizens or permanent residents can use these loans to finance an owner-occupied primary residence.

You can qualify for a USDA mortgage with a credit score of 640 or higher, a DTI of less than 41%, and if the monthly repayment won’t exceed 29% of your monthly income. The USDA may consider a higher DTI for applicants with credit scores above 680. Applicants with scores lower than 640 may still qualify but are subject to more stringent borrowing conditions.

You also need to demonstrate a dependable income over two years, have a good credit history, and have no account in collection within the last year.

The USDA loan limit is a moving target that varies between counties, based on the cost of living. The loan can be as high as $500,000 in high-cost counties like Hawaii and California and $100,000 in rural America.

You can only access a direct loan from the USDA if your home is less than 2,000 square feet and has a market value below your county loan limit. The USDA program excludes metropolitans but covers some suburbs.

Pros

100% financing

Ultra low fixed interest rates

Includes financial grants

No private mortgage insurance

Cons

Geographical restrictions

Finances single owner-occupied residences

Best for: Borrowers with limited financial resources or those wishing to live in rural areas.

Jumbo Mortgage

Jumbo loans finance homes that exceed the FHFA limits of a conventional mortgage. Jumbo loans are considered non-conforming mortgages and are considered high-risk loans.

Since they exceed the FHFA limits, Freddie Mac and Fannie Mae do not guarantee jumbo loans. That means the mortgage lender may incur losses if the borrower defaults. Jumbo loans can carry an adjustable or fixed interest rate and have strict requirements.

Jumbo Loan Requirements

You need a credit score of 700 to 720, a DTI of less than 45%, and plentiful cash reserves in the bank to qualify for a jumbo loan. Lenders require extensive documentation to show excellent financial standing. You’ll need W-2s, complete tax returns, and 1099s as well as your investment accounts and bank statements.

The minimum down payment on jumbo loans is often higher than traditional loans because they lack a government guarantee. Most mortgage lenders require a 10% to 30% deposit. Jumbo mortgage rates depend on your finances and your lender.

Some lenders charge higher rates on jumbo loans than conforming ones, while others offer lower rates. The closing costs and lender fees on a jumbo loan are often higher because of extra qualifying steps and the high loan amount.

You can use a jumbo loan to buy a home, refinance an existing mortgage for cash-out purposes, or purchase an investment property and land. However, since FHFA doesn’t govern jumbo loans, the loan limit could run into the millions.

Pros

Higher loan limits

Can finance investment property

Competitive interest rates

Flexible uses

High loan amounts

Cons

Requires high credit scores

You need high income

Requires plenty of cash reserves

Best for: People buying expensive property and homeowners looking to refinance a large loan.

Interest-Only Mortgages

Interest-only mortgages are relatively short-term loans, usually structured as ARMs for 5 to 10 years. During the loan, borrowers pay interest on the loan without repaying the principal. Since you’re not paying back any borrowed money, you’re not building equity in the home. Your equity in the house remains the value of the down payment and any appreciation in the home’s market value.

At the end of the loan term, your loan amount remains the same unless you’ve made separate payments to offset the principal. Once the initial term lapses, you can pay off the loan, switch to making amortized payments, refinance, or sign up for another interest-only term.

Interest-Only Mortgage Loan Requirements

An interest-only loan requires a good credit score, 700 or higher, a large deposit, and a low debt ratio. There are no standard requirements, so they vary widely between mortgage lenders. But you’ll need to demonstrate an ability to pay and own ample assets to qualify.

Pros

Low initial monthly payment

Low initial mortgage rates

Variable loan terms

Cons

You don’t build equity

Your equity declines if property value drops

Best for: People with high disposable income, large cash reserves, rising incomes, or borrowers who receive large annual bonuses.

Best Mortgage Lenders FAQs

Which lenders have the best mortgage rates?

Mortgage rates can vary significantly from lender to lender, and can also fluctuate over time. It’s difficult to say which lender has the “best” mortgage rates at any given time. It can depend on a variety of factors, such as your credit score, the type of loan you’re looking for, and the location of the property you’re buying.

That being said, some lenders may offer more competitive rates than others. One way to find the best mortgage rates is to shop around and compare offers from different lenders. You can do this by visiting the websites of different banks and mortgage companies, or by working with a mortgage broker.

Another important factor to consider when shopping for a mortgage is the fees associated with the loan. Some lenders may have lower rates but charge higher fees, while others may have higher rates but charge lower fees. Make sure to compare the total cost of the loan, including the mortgage rate and fees, when shopping for a mortgage.

How do I get the best mortgage rate?

To get the best mortgage rate, you should:

Have a good credit score. The higher your credit score, the more likely you are to qualify for a low mortgage rate.

Shop around for rates from multiple lenders. Compare rates from banks, credit unions, and online lenders to find the best rate.

Make a large down payment. Putting more money down on the home can lower your mortgage rate.

Consider different loan types. Adjustable-rate mortgages and shorter-term mortgages typically have lower rates than fixed-rate mortgages.

Consider paying “points” or additional fees to lower your rate.

Get Pre-approved for a mortgage before you shop for a house.

Be prepared to provide extensive documentation to the lender to show you can afford the loan and can make the payments.

It’s worth noting that interest rates are not the only thing to consider when shopping around for a mortgage. You should also compare other terms, fees, and loan programs that lenders offers. It’s always a good idea to consult a mortgage expert or a financial advisor for guidance on this matter.

How much house can I afford?

A widely accepted method for determining how much you can afford to spend on a home is the 28/36 rule. This rule states that you should not spend more than 28% of your gross, or pre-tax, monthly income on housing expenses.

Additionally, the rule states that you should not spend more than 36% of your income on all debt payments, including your mortgage, credit cards, and other loans, such as auto and student loans.

For example, if your gross monthly income is $5,000, you should not spend more than $1,400 (28% of $5,000) on housing expenses, including your mortgage payment, property taxes, and insurance. And you should not spend more than $1,800 (36% of $5,000) on all debt payments, including your mortgage, credit cards, and other loans, such as auto and student loans.

So, if you have $500 in existing debt payments, your monthly mortgage payment should not exceed $900.

From the towering peaks of its mountain ranges to the hushed elegance of its river valleys, Idaho’s geographical diversity is a testament to the timeless artistry of nature.

Stepping into the vast expanse of Idaho, you’ll be struck by a landscape that oscillates between serene beauty and dramatic grandeur. Whether it’s the lively urban appeal of Boise, the historic charm of Lewiston or the tranquil allure of Meridian, each location in Idaho paints a different hue on the state’s canvas, collectively creating a picture of life that is as varied as it is captivating.

Listed below are seven of the best places to live in Idaho for everyone from young professionals with families to active retirees and everyone in between. Find your favorite spot, schedule an apartment tour and settle down in your new happy place.

Population: 240,713

Median household income: $98,300

Average commute time: 18.4 minutes

Walk score: 38

Studio average rent: $1,437

One-bedroom average rent: $1,450

Two-bedroom average rent: $1,768

At first blush, Boise might appear to just be the state’s capital city, another spot on the map where the urban grid has staked its claim. But spend a little time here, wander its streets, listen to its stories and you quickly realize this diverse community is anything but ordinary.

Start in downtown Boise, a place that seems to exist in two eras simultaneously. It’s as though time got wonderfully tangled here, old red-brick buildings rubbing shoulders with sleek, modern edifices, each with their own story to tell. This isn’t simply a downtown—it’s an ongoing conversation between past and present.

And oh, the great outdoors! In Boise, nature is not an abstract concept but a close friend. The Ridge to Rivers trail system stitches the city to the vast expanses of Idaho’s wilderness like a beautifully embroidered seam. On these trails and nearby national parks, city slickers become explorers, trading sidewalks for dirt paths, the hum of traffic for the rustle of leaves.

Then there’s Boise State University, a hub of youth and innovation, its energy spilling over into the college town. You can almost feel the hum of thoughts and ideas, as though the city itself is learning, growing and evolving right along with its scholars.

The beauty of Boise isn’t just in its landscapes or its architecture, but in its spirit. This is a city comfortable in its own skin, unpretentious and genuine. It has its quirks and oddities, but rather than smoothing them out, Boise not only embraces them but celebrates them. This city doesn’t try to be anything other than what it is, and what it is, quite simply, is a great place to call home.

Three great apartment complexes in Boise:

Population: 58,242

Median household income: $60,984

Walk score: 35

Studio average rent: $925

One-bedroom average rent: $1,720

Two-bedroom average rent: $1,995

Coeur d’Alene is defined by its proximity to nature’s grandeur, an undeniably charming downtown and a welcoming community that welcomes folks from all walks of life. Nestled in the northern panhandle of Idaho, with its glittering lake and towering pine forests, it’s a slice of heaven, lifted straight from a storybook and gently settled in Gem City.

The star of the show here is undoubtedly the majestic Lake Coeur d’Alene, spanning 25 miles in length, framed by pine-clad mountains and blessed with a gorgeous swimming beach. Its turquoise waters reflect the ever-changing sky and offer not just spectacular views but a year-round playground for boating, fishing and swimming in summer; ice skating and bald eagle watching in winter. Watch the sunset over the water paint the sky a fiery red, life in Coeur d’Alene really is nothing short of a religious experience.

You can’t talk about Coeur d’Alene without mentioning its charming downtown, steeped in a kind of authentic Americana, where it’s easy to meander through a jumble of local boutiques, art galleries and historic buildings.

But a place is not defined merely by its geography or its buildings. It’s the people who breathe life into the locale. The community in Coeur d’Alene is warm and inclusive, making newcomers feel at home in no time. The small city also hosts myriad events, from art walks to the famed Ironman competition, fostering a sense of belonging that’s often lost in larger cities.

Three great apartment complexes in Coeur d’Alene:

Population: 69,450

Median household income: $57,412

Walk score: 42

Studio average rent: $617

One-bedroom average rent: $1,040

Two-bedroom average rent: $1,675

Idaho Falls embodies the quintessence of small-town America, tucked into an embrace of picturesque landscapes. The city emanates tranquility and serenity. It’s an evolving canvas adorned by the mighty Snake River’s waters, the resilient spirit of its people and the vibrant strokes of its culture.

The city’s heart beats in sync with the Snake River, which etches a serpentine course through its center. The river offers more than a namesake; it contributes to the city’s persona. The city’s waterfalls, cascading from snake river canyon right through the city’s heart, present more than scenic beauty; they are the city’s pulse, their incessant flow echoing the community’s resolve.

Surrounded by the sublime vistas of Idaho, the city serves as a gateway to an extraordinary natural playground, making it an easy choice for one of the best places to live in Idaho. The jagged peaks and spurting geysers at Yellowstone National Park, the untamed wilderness of Grand Teton and the surreal landscapes of Craters of the Moon lie just a short journey away.

However, Idaho Falls isn’t just an Eden for nature lovers, it’s also a burgeoning arts hub. The city’s downtown harmonizes the old with the new, historic buildings standing shoulder-to-shoulder with contemporary structures. From the lush expanse of the Idaho Falls Greenbelt to the myriad artifacts at the Museum of Idaho, the city center is always abuzz with creativity and life.

At its core, Idaho Falls is a tightly-knit community. The residents, imbued with a sense of hardiness and a pioneering spirit, are the city’s greatest strength. The town radiates a unique sense of camaraderie and friendliness. With high-quality public and private schools, lower cost of living and a family-friendly environment, the city provides a splendid backdrop for nurturing a family.

Three great apartment complexes in Idaho Falls:

Population: 34,896

Median household income: $60,581

Walk score: 49

Studio average rent: N/A

One-bedroom average rent: N/A

Two-bedroom average rent: N/A

Lewiston is an unassuming gem nestled in the state’s north central region. It is as if the tranquil rhythm of the Snake and Clearwater rivers has seeped into the very spirit of the former resort town. Lewiston, it seems, has a way of whispering sweetly to those who have the patience to listen. The lush landscape, with its wide-open skies and placid river banks, embodies a distinct and vibrant serenity that is difficult to find elsewhere. This landscape is not just a background but an active participant in the daily life of Lewiston’s residents.

But Lewiston’s charm isn’t confined to its natural beauty. It is found in the way the town retains a distinctive blend of the past and present. Historic downtown Lewiston, with its weathered brick buildings and quaint streets, tells a tale of a storied past. Yet, a blossoming culture imbues the city with fresh energy, where local crafts, eclectic eateries and thriving farmers’ markets create a harmonious blend of the old and the new.

Educational institutions such as Lewis-Clark State College contribute to Lewiston’s vibrancy, offering youthful energy and intellectual stimulation, while the city’s active outdoor recreation culture, ranging from fishing to hiking to boating and more, keeps the community grounded, healthy and engaged.