US mortgage rates ticked downfor the second week in a row but remain above 7%.

It’s the fourth consecutive week rates have been above 7% as inflation pressure lingers.

The 30-year fixed-rate mortgage averaged 7.12% in the week ending September 7, down from 7.18% the week before, according to data from Freddie Mac released Thursday. A year ago, the 30-year fixed-rate was 5.89%, the last time the weekly average has been under 6%.

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. The survey includes only borrowers who put 20% down and have excellent credit. The data was collected during a holiday-shortened week.

Mortgage rates have spiked during the Federal Reserve’s historic inflation-curbing campaign, sending home affordability to its lowest level in nearly four decades. Buying a home is more expensive because of the added cost of financing the mortgage and rising home prices.

“The economy remains buoyant, which is encouraging for consumers,” said Sam Khater, Freddie Mac’s chief economist.

But it isn’t good news for inflation, which needs to drop further for mortgage rates to come down.

Even though inflation has started to ease, strong economic data has continued to keep mortgage rates elevated this week, Khater said. That is straining potential homebuyers, who have seen their purchasing power dwindle.

The combination of low inventory and high costs has squeezed would-be homebuyers and sent home sales lower than last year.

Inflation is still too high

Rates are not expected to move much in the near term, said Danielle Hale, chief economist for Realtor.com. They didn’t move much during the shortened Labor Day week, and the strong economy, which has been keeping rates over 7%, has been cooling but at a moderate pace.

“In addition to fewer job openings and slower hiring this summer, recent readings on inflation have shown progress,” Hale said a statement.

Still, inflation remains well above the Federal Reserve’s 2% target. The Personal Consumption Expenditures index for July, released last week, showed that prices increased 3.3% annually.

The Fed has been raising interest rates in an effort to cool the economy and bring inflation closer to its target. But as the economy shows signs of resilience, the bond market is concerned that more hikes may be required to tame inflation. The central bank has three remaining policy meetings this year, including later this month.

While the Fed does not set the interest rates that borrowers pay on mortgages directly, its actions influence them. Mortgage rates tend to track the yield on 10-year US Treasuries, which move based on a combination of anticipation about the Fed’s actions, what the Fed actually does and investors’ reactions. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

Although home prices have crept up recently due to historically low inventory, rent prices have trended lower, which Hale says should help move inflation back toward its target in the months ahead.

The economy is nearing an inflection point, she says. But until it shows signs of cooling without protracted job losses or a recession – what’s known as a soft landing – mortgage rate volatility may continue.

Housing market ‘appears to be stuck’

With high mortgage rates, stubbornly high home prices and low inventory, fewer people are buying a home.

Applications for a mortgage to buy a home dropped to a 27-year low this week, according to the Mortgage Bankers Association.

“The housing market appears to be stuck heading into autumn, with sales activity likely to stay stagnant until housing inventory increases and mortgage rates decline to more affordable levels,” said Bob Broeksmit, MBA president and CEO in a statement.

However, August saw an uptick in newly-listed homes, according to data from Realtor.com, “suggesting the possibility that we’ve reached a point where some current homeowners are ready for a change despite the market’s challenges,” Hale said.

Still, the number of homes on the market is historically low, and August’s new listings lag behind prior years for the same period.

“This has kept housing markets surprisingly competitive,” Hale said.

In May 2021, the median price for a home was $350,300. That reflected a 23% increase year-over-year, demonstrating that the housing marketing was bustling after the impact of the COVID-19 pandemic. But it’s not just a rise out of the pandemic that has created a competitive housing market in 2021 and beyond. The record high in May 2021 followed 111 months of year-over-year gains, starting in March 2012.

In 2021 and 2022, the housing marketing has been awash in demand. But there aren’t enough homes to go around, leading to bidding wars and other challenges for buyers. Looking at this landscape, you may wonder, can you buy a house with bad credit?

The Challenges of Buying a Home with Bad Credit

Mortgage lenders look at a lot of factors to determine if you qualify for a home loan. Of course, your annual income and debts are crucial, but your credit score is also a significant factor. Applicants with great credit scores—750 or higher—tend to have an easier time getting approved for a mortgage and getting the most competitive interest rates available. Applicants with credit scores below 650 may have a more difficult time getting approved for a mortgage or securing low interest rates.

For a mortgage lender, all applicants present some sort of calculated risk. Lenders perceive those with higher credit scores as being at lower risk of foreclosure or defaulting on their home loans. As a result, people with high scores can get a lower interest rate and more favorable terms on a loan. Unfortunately, those with bad credit scores are automatically perceived to be a higher risk and—if they can get a loan—may end up paying higher interest rates and having to agree to less appealing terms that come with a bad credit mortgage.

COVID-19’s Impact on Buying a Home

The pandemic had some impact on the mortgage-buying process. That’s true for individual buyers as well as the entire process.

Get matched with a personal

loan that’s right for you today.

Learn

more

Homebuyers may have faced financial struggles during the pandemic, for example. Job or income loss could have led to difficulties paying bills or the need to take out loans to cover living expenses short-term. Those situations can impact credit and your ability to get a home loan.

At the same time, the Federal Reserve dropped interest rates in 2020 to help support the struggling pandemic economy. One result was that buying a house became very attractive, in part due to the lower overall cost of the loans.

Bad Credit in a Competitive Market

But now rates are increasing again—and may continue to rise throughout the year. Increasing rates may decrease competition between buyers, but they can make it more difficult for someone with less-than-great credit to buy a home for a number of reasons, including:

You may not be able to outbid others. Lenders may be willing to take a risk on someone with poor credit, but that risk is usually fairly limited. That means you may not be able to get approved over a certain amount, limiting how much you can pay for any home.

Your loan options may limit you. Buying a house with bad credit often means leveraging a government-backed loan, such as FHA or USDA loans. These loans must follow certain requirements about loan-to-value ratios, inspections and other steps to buying a home. In today’s housing market, having to stick to strict requirements can put you at a disadvantage.

Sellers may not choose your offer. Even if your offer is competitive, if you’re bidding with an FHA loan or other such financing, sellers may opt for a cash offer or one backed by a traditional commercial loan. Right or wrong, there’s some perception that cash or traditional loan offers are more likely to go through.

How to Buy a House with Bad Credit

It’s not all a lost cause, though. There are options for buying a home with poor or bad credit, such as Federal Housing Administration (FHA) loans. That’s true even in a competitive market.

FHA Loans

FHA loans have some of the most lenient qualification requirements. And they’re available to any homebuyer, not just first-time buyers.

To be eligible for an FHA loan, you need a credit score of at least 500. You’ll also have to meet other requirements, including appropriate debt-to-income ratios and not having certain types of open collection accounts in your credit history. Overall, you need to demonstrate to the lender that you’re reasonably able to pay the mortgage associated with the loan.

If you have a credit score between 500 and 579, the loan-to-value ratio is limited to a maximum of 90% on any FHA loan you might be approved for. That means you’ll need to come up with at least 10% of the purchase price as a down payment. For example, if you buy a home for $200,000, you’ll need at least $20,000 for the down payment.

If you have a credit score of 580 or above, you could be eligible for maximum financing. That means you may be able to get a loan with as little as 3.5% down.

VA Loans

Veterans Administration loans are available to military veterans and qualified spouses. The VA doesn’t set a specific credit score requirement for its programs, though it does state that borrowers will need to meet creditworthiness requirements. At the very least, the lender must determine that you have the means to pay the mortgage.

Some benefits of VA loans include:

They don’t necessarily require a down payment

No requirement for PMI, even if you don’t put down 20%

Competitive interest rates you might not be able to access elsewhere

USDA Loans

The United States Department of Agriculture offers mortgages to home buyers in eligible rural areas whose incomes fall in the low-to-average income range for their areas. The USDA doesn’t publish a minimum credit score requirement. It simply states that borrowers must have the willingness and ability to repay the loan, as demonstrated in part by their credit history. USDA lenders must look at three years of credit history.

Other Options

There are ways to increase your chances of getting approved for a mortgage with bad credit, even if you don’t want to go with one of the above government-backed options. Consider saving up for a larger down payment. A larger down payment reduces the amount you need to borrow and increases your likelihood of getting approved for a mortgage.

You may also be able to avoid the need for Private Mortgage Insurance with a higher down payment. Bypassing the need for PMI can easily save you $1,000 per year or more. It also frees up more money so you can pay down other debts, which can improve your credit.

Know Your Credit Score

If you’re thinking about trying to buy a home in the near future, the first step you should take is finding out where your credit stands. Begin by looking at your current credit reports and carefully reviewing them. Specifically, be on the lookout for any mistakes or errors on your report.

If you notice something incorrect on your report, you can file a dispute—most credit bureaus let you file a dispute online. You should also take the time to calculate how much of a mortgage you can reasonably afford before applying for one.

If you’re not sure what your credit score is, you can see your credit score for free on Credit.com. You also get a free credit report card that shows you ways to improve your credit score in each of the five areas that factor into how your score is calculated.

For even more information about where your credit stands, consider signing up for ExtraCredit®. You’ll get access to 28 of your FICO® scores, including the type of scores used by lenders to evaluate you as a mortgage borrower.

Once you know where you stand with your credit score and have done what you can to improve it, you can start shopping for mortgage rates and loans.

A bear market is defined as a broad market decline of 20% or more from recent highs, which lasts for at least two months. Although bear markets make for dramatic headlines, the truth is that bull markets tend to last much longer — the average bear market typically ends within a year.

While most investors know the difference between a bull and a bear market, it’s important to know some of the characteristics of bear markets in order to understand how different market conditions may impact your portfolio and your investment choices.

What Is a Bear Market?

Investors and market watchers generally define a bear market as a drop of 20% or more from market highs. So when investors refer to a bear market, it usually means that multiple broad market indexes, such as the Standard & Poors 500 Index (S&P 500), Dow Jones Industrial Average (DJIA), and others, fell by 20% or more over at least two months.

To be sure, 20% is a somewhat arbitrary barometer, but it’s a common enough standard throughout the financial world.

The term bear market can also be used to describe a specific security. For example, when a particular stock drops 20% in a short time, it can be said that the stock has entered a bear market.

Bear markets are usually associated with economic recessions, although this isn’t always the case. As economic activity slows, people lose jobs, consumer spending falls, and business earnings decline. As a result, many companies may see their share prices tumble or stagnate as investors pull back.

Why Is It Called a Bear Market?

There are a variety of explanations for why “bear” and “bull” have come to describe specific market conditions. Some say a market slump is like a bear going into hibernation, versus a bull market that keeps charging upward.

The origins of the term bear market may also have come from the so-called bearskin market in the 18th century or earlier. There was a proverb that said it is unwise to sell a bear’s skin before one has caught the bear. Over time the term bearskin, and then bear, became used to describe the selling of assets.

Characteristics of a Bear Market

There are two different types of bear markets:

• Regular bear market or cyclical bear market: The market declines and takes a few months to a year to recover.

• Secular bear market: This type of bear market lasts longer and is driven more by long-term market trends than short-term consumer sentiment. A cyclical bear market can happen within a secular bear market.

History of Bear Markets

The most recent U.S. bear market began in June 2022, largely sparked by rising interest rates and inflation. The bear market officially ended on June 8, 2023, lasting about 248 trading days, according to Dow Jones Market Data, and resulting in a market drop of about 25.4%.

Including the most recent bear market, the S&P 500 Index posted 12 declines of more than 20% since World War II. The table below shows the S&P 500’s returns from the highest point to the lowest point in a downturn. Bear markets average a decline of 34%, and generally last a little more than a year: about 400 days.

Recommended: What Is a Financial Crisis?

Bear markets have occurred as close together as two years and as far apart as nearly 12 years. A secular bear market refers to a longer period of lower-than-average returns; this could last 10 years or more. A secular bear market may include minor rallies, but these don’t take hold.

A cyclical bear market is more likely to last a few weeks to a few months and is more a function of market volatility.

Peak (Start)

Trough (End)

Return

Length (in days)

May 29, 1946

May 17, 1947

-28.78%

353

June 15, 1948

June 13, 1949

-20.57%

363

August 2, 1956

October 22, 1957

-21.63%

446

December 12, 1961

June 26, 1962

-27.97%

196

February 9, 1966

October 7, 1966

-22.18%

240

November 29, 1968

May 26, 1970

-36.06%

543

January 11, 1973

October 3, 1974

-48.20%

630

November 28, 1980

August 12, 1982

-27.11%

622

August 25, 1987

December 4, 1987

-33.51%

101

March 27, 2000

Sept. 21, 2001

-36.77%

545

Jan. 4, 2002

Oct. 9, 2002

-33.75%

278

October 9, 2007

Nov. 10, 2008

-51.93%

408

Jan. 6, 2009

March 9, 2009

-27.62%

62

February 19, 2020

March 23, 2020

-34%

33

June 2022

June 8, 2023

-25%

248

Average

-34%

401

Source: Seeking Alpha/Dow Jones Market Data as of June 8, 2023.

What Causes a Bear Market?

Usually bear markets are caused by a loss of consumer, investor, and business confidence. Various factors can contribute to the loss of consumer confidence, such as changes to interest rates, global events, falling housing prices, or changes in the economy.

When the market reaches a high, people may feel that certain assets are overvalued. In that instance, people are less likely to buy those assets and more likely to start selling them, which can make prices fall.

When other investors see that prices are falling, they may anticipate that the market has reached a peak and will start declining, so they may also sell off their assets to try and profit on them before the decline. In some cases panic can set in, leading to a mass sell-off and a stock market crash (but this is rare).

Is a Recession the Same as a Bear Market?

No. Bear market conditions can lead to recessions if the market slump lasts long enough. But this isn’t always the case. According to the National Bureau of Economic Research as reported in The New York Times, the U.S. has been in a recession only 14% of the time since World War II.

What Is a Bear Market Rally

Things can get tricky if there is a bear market rally. This happens when the market goes back up for a number of days or weeks, but the rise is only temporary. Investors may think that the market decline has ended and start buying, but it may in fact continue to decline after the rally. Sometimes the market does recover and go back into a bull market, but this is hard to predict.

If the bear market continues on long enough then it becomes a recession, which can go on for months or years. That said, it’s not always the case that a bear market means there will be a recession.

Once asset prices have decreased as much as they possibly can, consumer confidence begins to rise again, and people start buying. This reverses the bear market trend into a bull market, and the market starts to recover and grow again.

Example of a Bear Market

The most recent bear market occurred in June of 2022, when the S&P 500 closed 21.8% lower than its high on Jan. 3, 2022.

While the Nasdaq and the Dow showed a similar pattern in early 2022, the decline of those markets didn’t cross the 20% mark that signals official bear market territory.

Bear Market vs Bull Market

A bull market is essentially the opposite of a bear market. As consumer confidence increases, money goes into the markets and they go up.

A bull market is defined as a 20% rise from the low that the market hit in a bear market. However, the parameters of a bull market are not as clearly defined as they are for a bear market. Once the bottom of the bear market has been reached, people generally feel that a bull market has started.

Investing Tips During a Bear Market

There are a few different bear market investing strategies one can use to both prepare for a bear market and navigate through one.

1. Reduce Risky Investments

When preparing for a bear market, it’s a good idea to reduce riskier holdings such as growth stocks and speculative assets. One can move money into cash, gold, bonds, or other ‘safe’ investments to reduce the risk of losses if the market goes down.

These safe investments tend to perform better than stocks during a bear market. Types of stocks that tend to weather bear markets well include consumer staples and healthcare companies.

2. Diversify

Another investing strategy is diversification. Rather than having all of one’s money in stocks, distribute your investments across asset classes, e.g. precious metals, bonds, crypto, real estate, or other types of investments.

This way, if one type of asset goes down a lot, the others might not go down as much. Similarly, one asset may increase a lot in value, but it’s hard to predict which one, so diversifying increases the chances that one will be exposed to the upward trend, and you’ll see a gain.

3. Save Capital and Reduce Losses

During a bear market, a common strategy is to shift from growing capital into saving it and reducing losses. It may be tempting to try and pick where the market has hit the bottom and start buying growth assets again, but this is very hard to do. It’s safer to invest small amounts of money over time using a dollar-cost averaging strategy so that one’s investments all average out, rather than trying to predict market highs and lows.

4. Find Opportunities for Future Growth

However, in a broad sense if the market is at a high and assets are clearly overvalued, this may not be the best time to buy. And vice versa if assets are clearly undervalued it may be a good time to buy and grow one’s portfolio. A bear market can be a good time to identify assets that might grow in the next bull market and start investing in them.

5. Short Selling

A very risky strategy that some investors take is short selling in anticipation of a bear market. This involves borrowing shares and selling them, then hoping to buy them back at a lower price. It’s risky because there is no guarantee that the price of the shares will fall, and since the shares are borrowed, typically using a margin account, they may end up owing the broker money if their trade doesn’t work out as they hope.

Overall, it’s best to create a long-term investing strategy rather than focusing on short-term trends and making reactive decisions to market changes. It can be scary to watch one’s portfolio go down, especially if it happens fast, but selling off assets because the market is crashing generally doesn’t turn out well for investors.

The Takeaway

Bear markets can be scary times for investors, but even a prolonged drop of 20% or more isn’t likely to last more than a few months, according to historical data. In some cases, bear markets present opportunities to buy stocks at a discount (meaning, when prices are low), in the hope they might rise.

Also there are strategies you can use to reduce losses and prepare for the next bull market, including different types of asset allocation. The point is that whether the markets are considered bearish or bullish, any time can be a good time to invest.

If you’re looking to build a portfolio, no matter what the market, it’s easy when you set up an Active Invest account with SoFi Invest. The secure investing app lets you research, track, buy and sell stocks, ETFs, crypto, and other assets right from your phone or computer. You can easily move between different types of assets and you can set automated recurring investments if you want to put in a certain dollar amount each week or month. All you need is a few dollars to get started.

Start building a portfolio today.

FAQ

How long do bear markets last?

Bear markets may last a few months to a year or more, but most bear markets end within a year’s time. If they go on longer than that they typically become recessions. And while a bear market can end in a few months, it can take longer for the market to regain lost ground.

When was the last bear market?

The most recent bear market started in June of 2022, when the S&P 500 fell from record highs in January for more than two months.

Photo credit: iStock/Morsa Images

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

As an Amazon Associate I earn from qualifying purchases.

The procedure of looking for the ideal opulent apartment can frequently be intimidating. To locate the greatest luxury flats that suit your needs and tastes among the various possibilities accessible, you should have a plan in place. In this post, we’ll look at six tips that can make your rental property search more efficient, from picking a great location to using helpful online tools.

Utilize Online Resources: Expand Your Search

The days of only depending on newspaper classifieds or personal referrals are long gone. There are several online tools available nowadays that can help with your search for the ideal property. Specialized real estate websites can provide thorough listings with in-depth details on available residences. With the help of these sites, you can narrow down your search results depending on your preferences, such as price range, the number of bedrooms, available facilities, and location. Consider using online groups and social media sites as well, where people frequently post details on available flats. You can cast a broader net and improve your chances of discovering the best premium condo that satisfies your needs by using these resources.

Think Beyond the Listing: Network and Connect

The most incredible high-end homes occasionally could not even be on the list yet. You can find hidden treasures that haven’t hit the market by networking and establishing connections with local real estate brokers, property managers, and even current tenants. To broaden your network, go to open houses, check out neighborhood events, and talk to locals. Making contacts and remaining engaged in your apartment search may help you find unique chances that others have missed. Keep in mind that referrals from friends and family can frequently help you locate the best possible rentals that aren’t necessarily listed anyplace else.

The Power of Location: Finding an Excellent Home

When looking for the most amazing luxury apartment rentals, the location is one of the most important aspects to take into account. Your quality of life can be improved by a fantastic location, which offers comfort, accessibility, and a desirable area. Start by thinking about your daily requirements and lifestyle choices to identify the right place. Do you prefer a busy city environment or a quiet suburban setting? Make a list of the facilities and sights that are significant to you, such as closeness to your place of employment, retail establishments, dining options, parks, and cultural organizations. You may refine your search and uncover premium flats that are well-situated to suit your lifestyle by paying attention to these characteristics.

Schedule Multiple Viewings: Look Beyond the Surface

Making many viewing appointments is essential while looking for the ideal posh property. Don’t limit yourself to internet photo browsing or rely only on virtual tours. You can evaluate the apartment’s condition, design, and atmosphere by seeing it in person. Pay attention to specifics like the standard of the finishes, the amount of storage space, the amount of natural light, and the efficiency of the appliances. Make a note of any maintenance or repair concerns that require attention. You can make an informed decision and make sure you’re choosing the best upscale condo that meets your criteria by carefully inspecting the property during the viewing.

Be Prepared: Gather Your Documentation

Being ready can offer you an advantage while trying to land a high-end home. Many landlords and property managers demand that applicants present proof of their capacity to pay their rent and be reliable renters. Collect necessary papers such as credit reports, bank statements, references from past landlords, and proof of income to speed up the application process. You can prove your eligibility and improve your chances of getting the nicest flat before someone else does by having these documents on hand. All other factors, such as decor and personalization, can easily be taken care of later, as long as you come prepared.

Consider Long-Term Costs: Look Beyond the Rent

It’s crucial to take into account both the monthly rent and the property’s long-term costs while considering premium condos. Consider other charges like utility bills, parking fines, homeowner association dues, and any other pertinent expenses. Examine the amenities provided by the apartment building to see if they suit your needs. For instance, having an on-site gym can help you save money on external gym memberships if you enjoy exercise activities. You can choose the flat that delivers the best return on your investment by carefully weighing the long-term costs and advantages. Remember, you must take these factors into account in addition to the initial rent in order to make a wise financial decision.

Choosing an excellent luxury condo demands great thought and preparation. You can easily manage the apartment-hunting procedure by concentrating on the above-mentioned suggestions. Remember, you’ll be well-equipped to select the ideal home that meets your interests and improves your living experience if you have these six techniques in your toolbox.

Equal Housing Opportunity

Rental providers will not refuse to rent a rental unit to a person because the person will provide the rental payment, in whole or in part, through a voucher for rental housing assistance provided by the District or federal government.

Amazon and the Amazon logo are trademarks of Amazon.com, Inc, or its affiliates.

The Q2 national growth rate was the highest since the third quarter of 2019 thanks to declining property prices and mortgage rates and increased net operating income (NOI) in most markets. “The index experienced a sharp annual decline in each of the prior four quarters, but a pullback in property prices and moderating mortgage rates … [Read more…]

Are you looking for the best side jobs for teachers? Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher. Side hustles for…

Are you looking for the best side jobs for teachers?

Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher.

Side hustles for teachers are great because they can help you make extra income, pay off debt, save for a vacation, and more.

Teachers have many useful skills, which make them a great fit for many different side hustles alongside their main teaching job.

Quick Summary on Side Jobs For Teachers:

Online tutoring and selling lesson plans are popular side jobs for teachers that use their existing skills

Selling crafts, selling printables, or teaching online courses can be a nice creative outlet

Short-term and seasonal side gigs like coaching sports or teaching summer school may be better for your schedule than year-round gigs

Best Side Jobs For Teachers

There are 36 side jobs for teachers listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Below are 36 side hustles for teachers.

1. Sell educational printables

Selling educational printables can be a great way for teachers to make extra income and it is great for anyone who wants to learn how to make passive income as a teacher.

An educational printable is a teaching resource, either digital or physical, that educators create to help with learning.

Other teachers buy these for their classes and so do parents.

Educational printables are things like math problems, vocabulary cards, and science experiments. They work for different grades and learning goals, making it an easy way to add to regular teaching or homeschooling. You can share these resources online or print them for in-person classes, making them a helpful tool for improving education.You can learn more at How I Make $400,000 Per Year Selling Educational Printables.

Do you want to make money selling printables online? This free training will give you great ideas on what you can sell, how to get started, the costs, and how to make sales.

2. Tutor online or in person

Tutoring services or helping kids get ready for standardized tests either online or in person can be a great side hustle for teachers.

This option can be a natural fit, as you can use your teaching skills to tutor students.

To start, check out different online tutoring websites like Tutor.com or you can also do in-person tutoring sessions. For in-person tutoring sessions, you can contact local tutoring companies or promote your services on social media or in local Facebook parent groups for your area.

3. Sell your lesson plans

As a teacher, you already make lesson plans for your classes. You can actually sell your lesson plans, earn extra money, and help other teachers.

The most popular platform for this kind of side job is Teachers Pay Teachers (TPT). Here, you can upload your lesson plans, activities, assessments, and other educational resources. Each time someone purchases one of your items, you’ll earn some income.

Lesson plans need to be well-organized, easy to understand, and tailored to specific grade levels and subjects (such as fifth grade math). You should include clear objectives and step-by-step instructions to make your lesson plans more appealing to potential buyers.

4. Coach a school sport or other after-school program

Coaching a school sport is something that you can do within your own school district as many schools are in need of help with their sports teams.

Some sports and after-school programs that can be a teacher’s side hustle include soccer, basketball, volleyball, and track-and-field, as well as clubs such as yearbook, chess, choir, and more.

5. Start a dog bakery

Starting a dog bakery can be a fun side job for teachers who love both dogs and baking.

You can make an extra $500 to $1,000, or even more, each month by making treats for dogs. You can make dog treats like cupcakes, cookies, cakes, and more.

You can learn more at How I Make $4,000 Per Month Baking Dog Treats (With Zero Baking Experience!).

6. Sell crafts on Etsy

Selling crafts on Etsy can be a great way to make extra money by being creative.

Etsy is a website where people from all over can buy and sell handmade and digital products.

Some ideas for products you can create and sell on Etsy that are teaching-related include:

Classroom decor items

Educational games and activities

Customized planner pages and stickers

Flashcards and study materials

Of course, you can create things that aren’t related to teaching at all, such as knitwear, jewelry, and more.

7. Sell on Teachers Pay Teachers

Teachers Pay Teachers (TPT) is a site specifically for educators to buy and sell educational materials, and this is a popular teacher side hustle. If you’ve developed lesson plans, worksheets, or other teaching tools for your classroom, you can share and earn from them on TPT.

I know I talked about selling education printables and lesson plans above, but I want to talk more about Teachers Pay Teachers in its own section because it is such a popular teacher side hustle.

You can sell:

Lesson plans and unit studies

Worksheets and printable activities

PowerPoint presentations and interactive notebooks

Posters, charts, and visual aids

For example, I looked on Teachers Pay Teachers and searched for third grade lesson plans. There, I found over 49,000 results such as math lesson plans about rounding, substitute teacher plans for third graders, reading comprehension lesson plans, and more. Here’s an example of one that you can look at.

The average teacher on Teachers Pay Teachers can make around $300 to $500 extra, but there are some teachers that make hundreds of thousands of dollars extra each year.

8. Babysit

As a teacher, you may find that babysitting is an easy side job to pick up, and, depending on where you live, you may be able to earn around $15 to $25 an hour. Parents love hiring teachers as babysitters because they have so much experience with children.

While babysitting, you’ll find that your existing skills from teaching make a difference in providing the best care possible.

9. Teach English as a second language online

Teaching English as a second language (ESL) online is a popular side job for teachers. As an online ESL teacher, you can help students learn English and work from home.

Most jobs require you to be a fluent English speaker with a bachelor’s degree.

10. Teach summer school

One of the obvious ways for teachers to make extra money in the summer is to teach summer school.

It’s a great way to make use of your teaching skills while earning extra income. Plus, summer school takes place during summer break, so it should fit well with your schedule of already being off from school.

11. Summer camp counselor

Another great option during the summer months is to become a summer camp counselor.

As a counselor, you’ll supervise children in activities such as sports, arts, and crafts. Camps are always looking for instructors with teaching experience, making this a good side job for educators.

12. Grade papers

Grading papers as a side job may appeal to you if you’re looking for a more flexible, at-home option.

Companies such as Measurement Inc. hire teachers to grade student work, such as essays and test answers.

They are hiring evaluators to score in the subjects of English, mathematics, science, and more and pay starts at $15 per hour.

13. Work at a restaurant

If you’re looking for something completely different from teaching, you could take a part-time job at a restaurant.

Working in restaurants can be a good fit for teachers because they often offer flexible hours that can align with your teaching schedule. You can choose jobs like being a server, host, and more.

14. Proofread

As a teacher, you are probably already a great proofreader and are able to spot mistakes easily. With these skills, proofreading can be a great side job. By proofreading, you can help authors, website owners, students, and more improve their writing while earning some extra income.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

15. Blog

Blogging can be a fun way for you, as a teacher, to make extra money from home. Many blogs are run by teachers, and I completely get why – you can blog in your spare time and you don’t have to stick to any formal schedule.

To start your own blog, first, choose a topic that you’re interested in writing about, maybe something related to your teaching field or a hobby you enjoy.

You can make money from your blog in ways such as:

Affiliate marketing – Share links to products or services related to the topic you are writing about, and earn a commission for sales generated from your referral links.

Advertising – Include display ads or sponsored posts on your blog.

Courses and ebooks – You can create courses or ebooks related to your area of expertise, and sell them through your blog.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog, and it all started as a side job.

Learn more at How To Start A Blog FREE Course.

Similar to blogging, a teacher could also start a YouTube channel, a TikTok, and more.

16. Freelance write

If you are looking for side jobs for teachers from home, then becoming a freelance writer can be a great choice.

Freelance writers write content for blogs, websites, magazines, newspapers, advertising companies, and so much more.

You can find different writing jobs on platforms like Upwork and Fiverr, or even find clients on your own, such as by reaching out to websites that you are interested in writing for.

Recommended reading: 14 Places To Find Freelance Writing Jobs – (Start With No Experience!)

17. Transcribe

An online transcriptionist’s job is to listen to video or audio files and then type out everything that they are hearing. There are many different types of transcriptionists, such as legal, general, and medical transcriptionists.

This job requires strong typing and listening skills, and you can work from home on your own schedule.

Transcriptionists earn around $15 to $30 per hour on average.

I recommend watching FREE Workshop: Is a Career in Transcription Right for You? You’ll learn how to get started as a transcriptionist, how you can find transcription work, and more.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

18. Flip used items for resale

Flea market flippers find underpriced items at flea markets, yard sales, and thrift stores, then resell them for a profit. This job requires a good eye for finding valuable items that you believe can be sold for a higher price.

As a teacher, you could find and sell items in the evening, on the weekends, over holiday breaks, and in the summer. You get to make your own schedule, and it can be however many or few hours as you want.

Some items that you can resell include:

Vintage furniture

Collectibles, such as toys, coins, stamps, books, and more

Sporting equipment

Clothing

Electronics

I recommend signing up for a helpful webinar on this topic, How To Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business.

19. Bookkeep

Bookkeepers are people who keep track of all the money-related things for businesses. Bookkeepers do tasks like:

Tracking income

Organizing expenses

Making financial reports

This is typically a flexible job that you can do from home on your own time.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

20. Sell Canva templates

Creating and selling Canva templates online allows you to work from home in your free time.

A Canva template is like a pre-designed layout that you can use for creating things like social media graphics, Pinterest pins, ebooks, or presentations. It is a helpful starting point if you’re not very skilled at designing from scratch. Business owners, marketing professionals, nonprofit organizations, educators, event planners, restaurants, and more buy templates all the time.

Canva templates come with blank spaces where buyers can add their own words or pictures, adjust colors and fonts, and more. They’re useful for people who want their graphics to look high quality without spending a lot of time in the process (or perhaps they don’t know how to do it so templates help them a lot!).

Making and selling Canva templates can be a great way to earn extra money as you only need to create them once, and then you can sell them as many times as you’d like.

Recommended reading: How I Make $2,000+ Monthly Selling Canva Templates

21. Rover (walk and watch pets)

Rover is a website that links pet owners with pet sitters and dog walkers. You can do this job on the weekends throughout the year, or simply only open up your schedule during the summer months. It is up to you.

Getting started is easy on Rover – you set up a profile that talks about your experience with pets and the services you can provide, like dog walking, pet sitting, and house sitting.

Then, you will receive requests from customers and talk about pricing. Rover takes care of processing payments, and you’ll receive payments directly into your account.

You can sign up for Rover here.

22. Care.com

Another platform for finding pet and house sitting side jobs is Care.com. Care.com is not limited to pet care and includes other caregiving services, such as childcare and senior care.

You can browse available jobs in your area and apply to those that match your skills and interests. Care.com also allows clients to contact you directly for your services after you’ve created a profile. Once a job is completed, you’ll receive payment through the site.

23. Be a virtual assistant

A virtual assistant provides administrative, technical, or creative support to clients from home.

Some of the tasks you might do as a virtual assistant include managing schedules, responding to emails, making travel arrangements, handling social media accounts, and even writing articles or creating presentations.

If you want to become a virtual assistant, I recommend taking the free workshop called 5 Steps To Become a Virtual Assistant.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

24. Be a food photographer

Food photography can be a fun and creative way to earn extra income during your free time. Food photographers do just that – take pictures of food.

Whether you’re working directly for restaurants, magazines, or on a freelance basis, this job allows you to use your skills and interests to create beautiful images.

You can learn more at How To Become a Food Blog Photographer And Earn Over $50,000 Each Year.

25. House sit

As a teacher, you might be looking for ways to make some extra money during breaks or weekends. One option to consider is house sitting, and this is when you watch someone’s home (such as watering their plants and collecting mail) and sometimes take care of pets while their owners are away. People also hire house sitters so that their homes aren’t sitting empty because a visible presence can deter potential thefts.

To get started in house sitting, you can join house-sitting websites to find opportunities in your area, or ask friends and family for referrals (you might want to start by house sitting for people you know and then ask for references that you can use to broaden your job search).

26. Rent out an unused room in your home

If you have a room in your home that you are not using, then you may be able to rent it to someone on either a short-term (such as by becoming an Airbnb host) or long-term basis (getting a full-time roommate).

I have rented out rooms many times in the past, and it was a great way to make some extra income for space that I wasn’t using.

You can learn more at What You Need To Know About Renting A Room In Your House.

27. Rent your garage space

If you have empty storage space, such as a garage, driveway, closet, basement, or attic, you may be able to rent it out and make extra money. This can be a lucrative side hustle where you don’t have to use up much of your spare time.

You can use Neighbor to list your extra space for rent and make up to $15,000 per year by doing so. With Neighbor, you can rent out your garage, driveway, basement, or even a closet.

You can sign up at Neighbor for free here and list your space.

You can also learn more about Neighbor at Neighbor Review: Make Money Renting Your Storage Space.

28. Rent out a photo booth

Renting a photo booth can be a fun side job for teachers.

To get started, you will need to buy a photo booth as well as things like backdrops and props for people to hold in the picture (such as hats, signs, fun things to hold, etc.).

On average, photo booth rentals can range from $500 to $1,000 per event, and in some cases, even more for specialized events or packages with additional features.

I have personally rented a photo booth for an event in the past, and it was a lot of fun!

29. Online surveys and focus groups

Taking online surveys and answering questions for focus groups is very part-time and can be a way to side hustle for teachers.

You share your thoughts plus answer questions and can earn cash or free gift cards.

The survey companies I recommend signing up for are:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

PrizeRebel

User Interviews – These are the highest paying surveys with the average being around $60.

Recommended reading: 18 Best Paid Survey Sites To Make $100+ Per Month

30. Voice over act

A voice-over actor is the person whose voice you hear but don’t see in YouTube videos, radio ads, educational videos, and more.

Different companies need a wide variety of voices, and that’s where you come in.

Recommended reading: How To Become A Voice Over Actor And Work From Anywhere

31. Mystery shop

I was a secret shopper in the past, and there were often mystery shops that gave me $100 to put toward a free dinner. I always looked forward to these, as I was living paycheck to paycheck, and I used these restaurant mystery shops to reward myself every now and then.

There were other mystery shops that paid me actual money, and some paid me in free items, such as makeup, movie theater tickets, and car oil changes.

Companies hire mystery shoppers to get an understanding of their customer’s experience. Companies want to know a real product opinion, how the customer felt they were treated at their business, how phone calls were handled, and more.

Basically, mystery shopping is a way to anonymously test the entire shopping experience.

You can learn more at How To Become A Mystery Shopper.

32. Fitness trainer

Fitness trainers help people reach their health goals through customized exercise plans and nutrition advice. This is typically a job where you can choose your schedule, so you can choose to work hours outside of your teaching job, such as in the evenings and on the weekends.

I actually know a few teachers who are fitness trainers on the side, so it must be a good fit!

Another positive is that you can even choose between in-person and online coaching. Online coaching can mean that you can work remotely, making it a more flexible side job for teachers looking to earn extra income.

33. Find random gigs on Craigslist

As a teacher looking for side jobs, you can look for random gigs on Craigslist to earn some extra income. To begin your search, simply go to the Craigslist website and select your city from the home page.

Here are some jobs I found through a quick search:

Cleaning a house

Help assembling furniture

Taking down a shed in a backyard

Garage cleanup

Mover

Handyman

Movie extra

Sign holder

You can even post your own services on Craigslist if you have a skill you’d like to share with others, such as giving music lessons or tutoring.

34. Deliver groceries with Instacart

Grocery delivery services are popular because there are more and more people who want someone to do their grocery shopping for them.

Services like Instacart need personal grocery shoppers, and the average shopper makes $15 to $20 an hour to deliver groceries. Drivers are paid per order, and you get to keep 100% of your tips. You also get to choose your schedule, so a teacher could choose to work in the evenings or on weekends. Or, you could choose to only deliver groceries during the summer.

You can click here to sign up to be an Instacart Shopper.

You can also learn more at Instacart Shopper Review: How much do Instacart Shoppers earn?

There are many other gig ideas that you can try out too, such as Uber Eats and DoorDash.

35. Real estate agent

Some teachers are real estate agents on the side of their full-time job as a teacher. This is because you can list and sell homes on your weekends, during breaks, at night, and over the summer.

Selling homes can be more difficult, though, as your clients may want your full attention during the day occasionally and you would be busy teaching, so this is something to think about.

36. Driver’s ed teacher

A common side hustle for teachers is teaching driving lessons to teenagers and adults. As a teacher, you may be able to check if the high school near you is in need of a teacher for this subject. Or, you can reach out to a local driving school to see if they are hiring.

Driving instructors make around $20 an hour more or less, depending on where you live.

Frequently Asked Questions

Below are answers to common questions about side hustles for teachers.

How can I make money on the side while teaching?

Some good side jobs for teachers include tutoring, freelancing, transcribing, blogging, selling lesson plans, and more.

What can teachers do to make extra money?

Teachers can do a lot of things to make extra money, such as jobs like tutoring, freelance writing, blogging, or creating educational printables.

What is a second career for teachers?

Second careers for teachers can include jobs such as educational consultants, curriculum developers, or even working in corporate training and development.

Do most teachers have 2 jobs?

Many teachers have two jobs. This is for many reasons, such as the typically low pay of a teacher as well as teachers wanting to make money while they are off in the summer.

How to make extra money on Teachers Pay Teachers?

Teachers can make extra money on Teachers Pay Teachers by selling lesson plans and printables.

How can teachers make money in the summer?

Teachers can make money when they’re off in the summer by teaching summer school, helping students with test prep, babysitting, selling lesson plans, working at a restaurant, working as a real estate agent, and more.

What to do after quitting teaching? How do you pivot out of teaching?

Quitting teaching and moving on to something else will take a few steps, and you can begin by thinking about your skills and interests. Then, start exploring different job options and connect with people in the field you’re interested in, attend industry events, and consider getting any certifications that you may need.

How can teachers earn extra income through online tutoring?

Sites like Tutor.com look for teachers to tutor students remotely, and you can even offer your services through social media.

How can a teacher make six figures by utilizing their skills?

While it’s not always easy for teachers to earn a six-figure salary, it is possible if you find ways to make extra income or by starting a business of your own.

What opportunities do music educators have for side income?

Side income ideas for music educators can include jobs like giving private music lessons or working as a weekend or evening instructor at a music school. Music educators can also sell lesson plans (I found some examples on Teachers Pay Teachers here).

What are some good side jobs for teachers?

I hope you enjoyed this article on the best side jobs for teachers.

Whether you are looking for side jobs for teachers from home, side jobs for teachers in the summer, or if you want to learn how to make passive income as a teacher, there are many ways to make extra money as a teacher.

Some of the best side hustles for teachers include:

Sell educational printables

Tutor online or in person

Sell your lesson plans

Coach a school sport

Start a dog treat bakery

Sell crafts on Etsy

Sell on Teachers Pay Teachers

Babysit

Teach English as a second language online

Teach summer school

Summer camp counselor

Grade papers

Work at a restaurant

Proofread

Blog

Freelance write

Transcribe

Flip used items for resale

Bookkeep

Sell Canva templates

Rover (walk and watch pets)

Virtual assistant

Food photographer

House sit

Rent out an unused room in your home

Rent your garage space

Rent a photo booth

Online surveys and focus groups

Voice over act

Mystery shop

Fitness trainer

Find random gigs on Craigslist

Deliver groceries

Real estate agent

Driver’s ed instructor

What do you think are the best ways for teachers to make extra money?

There have long been stirrings of a potential Fannie Mae and Freddie Mac merger, or the outright dissolution of the under-fire companies ever since they fell under conservatorship back in 2008.

And now it looks as if the wheels are finally in motion.

Yesterday, during prepared remarks at an economic conference in Washington, FHFA director Edward DeMarco revealed plans for a “new business entity,” essentially a securitization platform that could eventually serve as the framework for the secondary mortgage market.

The initial operation and funding for the business will be provided by Fannie and Freddie, though the venture will be led by individuals outside the two companies, in a physically separate location.

In short, the company is being formed to replace the outdated infrastructure that exists at the two companies today, which some feel led to the mortgage crisis.

Fannie and Freddie provide liquidity in the mortgage market to ensure banks and lenders have money to make new loans, but in recent years they’ve grown far too large.

They’re also inherently flawed, seeing that they were public-private companies (before the takeover) that attempted to meet government housing goals while also competing with private market participants, so much so that they took part in high risk lending during the housing run-up.

The Need for Private Capital

At present, Fannie, Freddie, and the FHA/VA support more than 90% of new mortgages originated, meaning private capital is largely absent from the mortgage market. It has been since crisis first took hold, with no one willing to take on the risk without an explicit government guarantee.

Unfortunately, this means the American taxpayer is essentially guaranteeing the housing market, which is no bueno.

In 1980, Fannie and Freddie owned or guaranteed just seven percent of the residential mortgage market, and saw that number spike to about 47% in 2003, per the Heritage Foundation.

By 2010, Fannie and Freddie owned or guaranteed roughly half of all outstanding residential mortgages in the United States, and financed nearly two-thirds of new mortgages.

Going forward, the aim is to reduce the presence of Fannie and Freddie (and the FHA) and get back to a more private mortgage market with much less government involvement.

Aside from the new securitization platform, DeMarco noted that the pair is expected to reduce its massive footprint in the mortgage market by selling off loans held in its retained portfolios.

They will also be directed to take part in “credit risk sharing transactions” involving things like expanded mortgage insurance and credit-linked securities from the private market.

Along with that, DeMarco said he expects the FHFA to continue increasing guarantee fees in 2013, after raising them twice in 2012.

This will mean higher mortgage rates for consumers, as g-fees are typically just passed along to the borrower.

But the aim in increasing the fees is to lure in more private capital by making Fannie and Freddie-backed loans less competitive.

For the record, the FHA has employed similar tactics, with both the upfront mortgage insurance premium and annual mortgage insurance premium increased to account for more risk.

An Alternative to Fannie and Freddie

The Bipartisan Policy Center has already come up with an alternative to Fannie and Freddie; a wholly owned government corporation known as the “Public Guarantor.”

Unlike Fannie and Freddie, it wouldn’t buy and sell mortgages, or issue mortgage-backed securities. Instead, it would leave all that to the private sector.

However, it would guarantee investors the timely payment of principal and interest on the underlying securities.

In the event of default, the Public Guarantor would be in a fourth-loss position, behind the borrower and their home equity, private credit enhancers, and issuers and servicers.

The “PG” would also be responsible for qualifying participating institutions, establishing guarantee fees, and setting standards, including conforming loan limits.

What It Means to Homeowners

Without getting overly technical, the dissolution of Fannie and Freddie shouldn’t have an enormous impact on borrowers and the housing market at large.

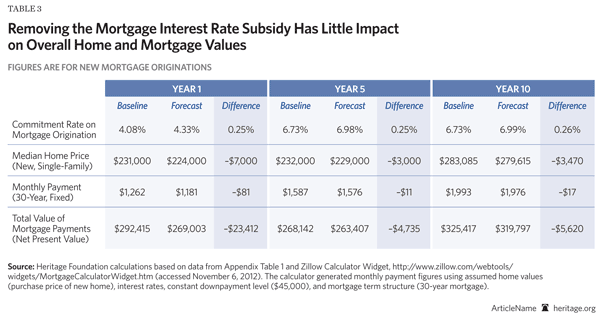

The Heritage Foundation (which seems to despise Fannie and Freddie) ran a simulation over 10 years and found that sales of new homes would fall an average of 0.81% and sales of existing homes would slip 1.58%.

As a result, the homeownership rate in the United States would fall just 0.11% over the decade.

Meanwhile, without Fannie and Freddie guaranteeing mortgages, those who wind up holding the mortgages would demand a higher interest rate to offset the increased risk.

They predict rates on a 30-year mortgage to be anywhere from 25 to 40 basis points higher.

In other words, instead of a 4.08% mortgage rate, you’d be looking at a rate of 4.33% or higher. However, rate movement could be a lot more volatile, with large swings and less predictable rate tracking.

But because home prices would be slightly lower as well, monthly mortgage payments would actually drop.

Clearly there are implications at all levels, but changes are necessary.

The past few days have seen rates surge to new multi-decade highs with the average lender quoting 7.6+ for top tier conventional 30yr fixed scenarios. Not too much has changed today apart from the direction of the movement and the fact that modest gains weren’t brutally dashed as the day progressed.

In fact, most lenders updated rates for the better at some point today as the underlying bond market improved. The caveat is that the outright levels aren’t much lower than yesterday’s multi-decade highs.

Nonetheless… longest journeys, single steps, and all that…

Any time rates skyrocket–whether for a period of hours, days, or months–market watchers are on the lookout for a bounce. Bounces come in all shapes and sizes. In all cases, it only ever makes sense to take them one day at a time until a clear trend has been established. Furthermore, that trend has to have backing from a clear shift in the economic data and Fed policy stance.

The current bounce is best measured in “hours” so far. We’re a long way from being able to say it represents some sort of ceiling for rates, but we can always hope this tiny sapling grows into a mighty tree as long as we remember that hope is no basis for a strategy.

Today was “nice.” If tomorrow is nice, that would also be “nice.” But it’s a good time to remain skeptical and defensive until the niceness becomes overwhelming.

Other indices showed significantly higher mortgage rates this week.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s 30-year fixed rate for conventional loans at 7.43% on Wednesday, compared to 7.22% the previous week. At Mortgage News Daily on Wednesday, the 30-year fixed rate for conventional loans was 7.65%, up from 7.33% the previous week.

“With the explosion of the bond market, the strength of the U.S. dollar, the positive jobless claim data combined with the Fed’s hawkish tone, 10-year yields just shot up and mortgage rates followed,” HousingWire’s Logan Mohtashami said.

On Thursday, the 10-year yield reached 4.61%, the highest level since 2007.

Home sales transactions will decline this fall

In August, sales of existing homes and new homes were down, as were pending home sales, which suggests conditions will remain slow for the next quarter. Additionally, new home prices also declined, signaling that August may be the beginning of the end of this resilient housing market, according to Bright MLS Chief Economist Lisa Sturtevant.

“For many would-be homebuyers, a mortgage rate above 7% simply means that the numbers do not work for them,” Sturtevant said in a statement. “The 7% threshold, above which mortgage rates have been now for seven weeks, according to Freddie Mac, is a psychological, as well as a financial, barrier for consumers. Consumer confidence has started to stumble as individuals and households are becoming more anxious about the economy.”

Consumers are growing more cautious amid rising economic uncertainty, Sturtevant added.

Meanwhile, sellers are also refraining from listing their homes, adding pressure to an already depleted housing inventory. The absence of uptick in homes listed also means that there might not be any major price drops in the foreseeable future.

“Rates over 7% and low for-sale inventory continue to create affordability challenges for prospective buyers, Mortgage Bankers Association President and CEO Bob Broeksmit said in a statement. “Until rates start to come back down, we anticipate housing market activity will remain slow.”

UK ‘mortgage meltdown’ looms amid ‘terrifying’ growth in arrears

Jump in borrowers unable to make payments with landlords particularly hit and ‘worse to come’

Analysis: will the Bank listen to business and halt rate rises?

Mortgage balances with arrears jumped by 13% in the second quarter of the year to the highest level since 2016, according to Bank of England figures that underscore the stress in the UK mortgage market.

Rising interest rates and unemployment over recent months have put pressure on household disposable incomes, forcing some families to cut or suspend their monthly mortgage payments.

Buy-to-let mortgage payers have also come under pressure in parts of the country where tenants are struggling with the cost of living crisis.

The Bank of England said the total value of mortgage balances which had some arrears rose to £16.9bn, up by 29% on the previous year and the highest since the third quarter of 2016.

Mortgage arrears are based on figures showing the number of borrowers failing to make payments equivalent to at least 1.5% of the outstanding mortgage balance or where the property is in possession.

Mortgage lending was also hit in the second quarter with gross advances falling by £6.3bn to £52.4bn. Year on year, mortgage lending slumped by almost a third, to the lowest level since the worst of the Covid-19 collapse in lending in the second quarter of 2020.

Lewis Shaw, founder of Mansfield-based Shaw Financial Services, told the news agency Newspage a “mortgage meltdown” is approaching, unless the Bank of England changes its approach.

Shaw said: “The speed at which mortgage arrears are increasing is terrifying and should give cause to pause at the next Bank of England interest rate meeting. This is dire data, and we know that it’s about to get an awful lot worse with 1.6m mortgage holders due to renew over the next 12 months at significantly higher rates than anyone has been used to for well over a decade.”

Simon Gammon, managing partner at the finance arm of estate agents Knight Frank, said the proportion of mortgage payers falling behind with payments remained low at just 1%, despite the “sizeable jump in arrears”.

He said: “That’s because the vast majority of outstanding mortgages were issued under the post-global financial crisis regime, which was much more stringent when it comes to affordability.”

However, while homeowners were more likely to make cuts to other spending before falling behind with mortgage payments, buy-to-let landlords may take a different view, he said.

“We are more likely to see arrears in the buy-to-let sector, where landlords face a unique set of challenges. If a landlord finds their mortgage is no longer affordable, or the rent no longer covers their outgoings, they only have two choices – sell or default. If they opt to sell, they may have to wait up to a year for the tenancy to end, unless they are willing to sell with a tenancy in place, which is more difficult.

“Landlords are also more likely to opt to default than those struggling with a mortgage secured against their main residence, so this is an area to watch,” he added.

Incoming Bank of England deputy governor Sarah Breeden said she agreed with her future colleagues on the monetary policy committee (MPC), which sets UK interest rates, that inflation may fall at a slower pace next year than expected, forcing the central bank to keep the cost of borrowing higher for longer than expected.

Breeden, who will replace Jon Cunliffe as the Bank’s deputy governor for financial stability after the MPC’s meeting next week, said there was also a risk that growth and unemployment will worsen.

skip past newsletter promotion

after newsletter promotion

“I will, after November, be very careful in balancing those two factors: the risk of inflation becoming embedded through more persistent, second-round effects, as well as the impact of tightening coming through,” she told parliament’s Treasury Committee in a hearing convened to approve to her appointment.

“The challenge right now is that wages are high and rising and there is a real risk that second-round effects means that this inflation becomes embedded,” she said, adding that in keeping a lid on inflation, “it is not our intention to cause a recession”.

The MPC is expected to raise interest rates by a quarter point to 5.5% on 21 September, raising the average mortgage payments by £3,000 a year for a household that refinances a 2-year fixed product.

Breeden said she expected inflation to be “around the [Bank of England’s] 2% target in two years’ time”.