The Miami housing market has been a topic of interest for both buyers and sellers in recent years. With its lively vibe, beautiful beaches and booming economy, Miami has become a desirable location for people of all walks of life looking to invest in real estate.

In this article, we will delve into the current state of the Miami home prices, exploring key trends, average home prices and market competitiveness. Whether you’re a prospective buyer, seller or simply curious about the Miami real estate scene, this is the place to be to gain valuable insights you need to enter the market with confidence.

Miami housing market at a glance

Miami’s housing market has experienced significant growth in recent years, with rising home prices and increased demand. In December 2023, the median sale price for homes in Miami reached $570,000, reflecting an 11.8% increase compared to the previous year. This price surge indicates a strong market and a favorable environment for sellers.

Average days on the market

One important factor to consider in the Miami housing market is the average number of days homes stay on the market. Homes in Miami sell after an average of 69 days, which is a slight decrease from the previous year’s average of 71 days. This suggests that the market is relatively quick-paced, with buyers actively searching for properties and pulling the trigger when they see something they like.

Competitiveness of the Miami housing market

To assess the competitiveness of the Miami housing market, we can look at multiple offers and sale-to-list price ratios. In Miami, multiple offers are relatively rare, indicating a less competitive market compared to other cities. On average, homes in Miami sell for about 4% below the list price.

Miami’s pricing compared to the national average

Miami’s median sale price of $570,000 is 41% higher than the national average. This significant difference highlights the desirability of the Miami real estate market and the premium prices buyers may expect to pay. Additionally, the overall cost of living in Miami is 19% higher than the national average, further emphasizing the city’s appeal to those in higher tax brackets.

Number of homes sold

The number of homes sold in Miami provides valuable insights into the overall market activity. In December 2023, there were 495 homes sold, representing an increase from the previous year’s 472 homes sold. This uptick indicates a strong housing market with a healthy level of buyer demand.

Miami rental market overview

Apart from the housing market, Miami’s rental market is also a crucial aspect to consider for anyone seeking temporary or long-term accommodations. 2024 has already proven a positive year for renters as prices have slowly dipped in several key markets, and landlords are willing to offer valuable renter incentives. Let’s explore the average prices and trends in Miami’s available rentals to provide a comprehensive analysis.

Average rent prices in Miami

The average rent prices in Miami vary depending on the type of apartment. For studio apartments, the median price started at $2,644 in January and gradually decreased to $2,210 by December. On the other hand, the median price for one-bedroom apartments remained relatively stable throughout the year, ranging from $2,579 to $2,726. For two-bedroom apartments, the median sale price fluctuated between $3,872 and $3,600.

Month

Studio

1 Bed

2 Beds

Jan 2023

$2,644

$2,579

$3,872

Feb 2023

$2,579

$3,009

$3,972

Mar 2023

$2,633

$2,986

$3,908

Apr 2023

$2,615

$2,938

$3,790

May 2023

$2,615

$2,952

$3,811

Jun 2023

$2,435

$2,927

$3,702

Jul 2023

$2,423

$2,921

$3,728

Aug 2023

$2,355

$2,770

$3,675

Sep 2023

$2,249

$2,719

$3,504

Oct 2023

$2,274

$2,700

$3,401

Nov 2023

$2,270

$2,684

$3,565

Dec 2023

$2,209

$2,658

$3,552

Jan 2024

$2,210

$2,726

$3,600

Rental market trends

Understanding Miami’s rental market trends can help landlords and tenants make informed decisions. Let’s take a closer look at the changes in average rent prices over the past year.

Average rent price fluctuations

In the past year, the average rent in Miami experienced slight fluctuations. Studio apartments saw a 16% decrease in rent, starting at $2,644 in January and ending at $2,210 in December. Similarly, one-bedroom apartments experienced a 9% decrease, with rent ranging from $2,579 to $2,726. For two-bedroom apartments, the rent decreased by 7%, fluctuating between $3,972 and $3,600.

Apartment type

Avg. rent

Annual change

Studio

$2,210

-16%

1 Bed

$2,726

-9%

2 Beds

$3,600

-7%

Affordable neighborhoods in Miami

For those looking for more affordable housing options in Miami, certain neighborhoods offer lower rent prices. Let’s explore some of the most affordable neighborhoods in Miami and the average rent prices for one-bedroom apartments.

Neighborhood

Average rent for 1-bedroom apartment

Allapattah

$1,700

Little Haiti

$1,700

Model City

$1,700

Little River

$1,700

Shore Crest

$1,700

Neighborhood rent trends

Different neighborhoods in Miami may have varying rent trends, making it key to consider location-specific factors when searching for rental properties. Here is a breakdown of rent trends for studio apartments in various neighborhoods in Miami.

Neighborhood

Studio Avg Rent

Annual Change

Lower Brickell

$3,810

-7%

Miami Financial District

$3,500

+32%

Brickell

$3,159

+17%

Miami Urban Acres

$2,940

-27%

Riverside

$2,828

+21%

Riverview

$2,813

+20%

West Brickell

$2,660

-2%

Brickell Village

$2,619

+9%

Downtown

$2,584

-4%

Riverfront

$2,550

N/A

Comparison with other cities

If you’re considering Miami as a potential relocation destination, it’s helpful to understand how it compares to other cities in terms of rental prices. Here is a comparison of studio apartment average rent prices in Miami and several other cities.

City

Studio Avg Rent

Annual Change

Coral Gables

$2,723

-15%

Miramar

$2,370

+76%

Sunny Isles Beach

$2,350

-2%

Doral

$2,142

-2%

Boca Raton

$1,972

-16%

Plantation

$1,930

+21%

Fort Lauderdale

$1,920

-14%

Coconut Grove

$1,800

+3%

Hialeah

$1,800

+4%

Miami Beach

$1,766

-12%

Make Miami your home

The Miami housing market is a fertile environment for buyers, sellers and renters alike. With rising home prices, a relatively quick sales process and increased demand, Miami proves to be an attractive real estate destination.

The rental market provides a range of options, from affordable neighborhoods to upscale areas. By understanding the current trends and market conditions, anyone can make an informed decision when navigating the Miami housing and rental market. So, whether you’re looking to buy, sell or rent, Miami is a great place to call home.

There’s no one-size-fits-all mortgage. When deciding between a conventional loan vs FHA loan, you’ll have to compare costs and benefits based on your personal finances.

Compare home loan options. Start here

A conventional loan is often better if you have good or excellent credit because your mortgage rate and PMI costs will go down. But an FHA loan can be perfect if your credit score is in the high-500s or low-600s. For lower-credit borrowers, FHA is often the cheaper option.

These are only general guidelines, though. And the choice between a conventional loan vs FHA loan might be different for you. So be sure to look closely at both loan types and choose the best one for your financial situation.

In this article (Skip to…)

Conventional loan vs FHA comparison

There are plenty of low-down-payment options for today’s home buyers. But many will choose either a conventional loan with 3% down or an FHA loan with 3.5% down.

Compare home loan options. Start here

So, which type of home loan program is better? That depends on your financial situation.

Here’s an overview of what you need to know about qualifying for a conventional loan vs FHA loan.

Conventional 97 Loan

FHA Loan

Minimum Down Payment

3%

3.5%

Minimum Credit Score

620

580

Maximum Debt-to-Income Ratio

43%

50%

Loan Limit for 2024 (in most areas)

$

$

Income Limit

No income limit

No income limit

Mortgage Insurance

Annual fee

Annual and upfront fee

Down payment requirements

Both conventional and FHA mortgage programs have minimum down payment amount requirements which borrowers must meet in order to be eligible for a home loan and reach their goal of homeownership.

Compare home loan options. Start here

FHA: 3.5% down with a 580 credit score, or 10% down a score between 500-579

Conventional 97: 3% down

Like other conventional loans, conventional 97 applicants will pay private mortgage insurance (PMI) with less than 20% down. And all FHA borrowers are required to pay mortgage insurance regardless of down payment.

Credit scores

In deciding between an FHA loan and the Conventional 97 loan, your individual credit score matters. This is because your credit score determines the type of mortgage loan you’re eligible for. Credit history affects your monthly mortgage payments, too.

Compare home loan options. Start here

Minimum credit score requirements for FHA and conventional loans are:

FHA: 580 credit score with 3.5% down, or 500-579 credit score with 10% down

Conventional: 620 credit score

If your credit score is between 500 and 620, the FHA loan is best suited for you because it’s your only available option.

But if your credit score is above 620, it’s worth looking into a conventional loan with 3% down. Especially because, as your credit score goes up, your mortgage rate and PMI costs go down.

Debt-to-income ratio

Another factor you need to consider when choosing between a conventional and FHA loan is your debt-to-income ratio or DTI ratio. This is the amount of debt you owe on a monthly basis, compared to your monthly gross income.

Compare home loan options. Start here

Conventional loans usually allow a maximum DTI of 43% — meaning your debts take up no more than 43% of your gross monthly income

FHA loans allow for a higher DTI of up to 50% in some cases

However, even with FHA loans, you’ll have to shop around if your debt-to-income ratio is above 45%. Because the FHA allows mortgage lenders to set their own in-house loan requirements, some may set stricter DTI requirements that are below 50%.

Debt-to-income ratios tend to make a bigger difference in high-cost areas, like big cities, where home values are high.

If you’re buying somewhere like Los Angeles, New York, or Seattle, your monthly debt (including mortgage costs) will take up much more of your income simply because real estate is so much more expensive.

Mortgage insurance

FHA and conventional loans both charge mortgage insurance. But the cost varies depending on which type of loan program you have, and how long you keep the mortgage.

Compare home loan options. Start here

FHA mortgage insurance (MIP): The costs for MIP is the same for most borrowers: 0.55% of the loan amount per year, with a one-time upfront fee of 1.75%

Conventional loans private mortgage insurance (PMI): The costs for PMI vary depending on your credit score and loan-to-value ratio. You’ll only pay PMI when you put less than 20% down, and you’ll only continue to pay monthly premiums until you reach 20% home equity

Conventional Loans

FHA Loans

Mortgage Insurance Type

Private Mortgage Insurance (PMI)

Mortgage Insurance Premium (MIP)

Upfront Mortgage Insurance Fee

n/a

1.75% of loan amount

Annual Mortgage Insurance Rate

Up to 2.25% of loan amount

0.55% of loan amount

Duration

Until the loan reaches 80% LTV

11 years (down payment of 10% or more) OR life of the loan (down payment of 3.5% to 10%)

The cheaper mortgage insurance option for you depends on your financial situation.

Conventional 97 mortgage insurance goes away at 80% loan-to-value. You’ll also hear loan officers refer to this as 20% home equity (both terms essentially refer to the same thing).

This means that, over time, your Conventional 97 can become a better value — especially for borrowers with high credit scores.

Also, consider upfront charges.

In addition to MIP, the FHA charges an upfront mortgage insurance premium known as UFMIP. UFMIP costs 1.75% of your loan size, is added to your loan balance, and is non-recoverable except via the FHA Streamline Refinance

The Conventional 97 charges no equivalent upfront fee for mortgage insurance. It only charges monthly mortgage insurance premiums

Conventional loan vs FHA loan limits

Both the FHA and conventional loans have limits on the amount of money you can borrow.

Compare home loan options. Start here

In 2024, the FHA loan limits for a single-family home is $ in most of the U.S.

The conventional loan limit for a single-family home is $.

Any loan amount that exceeds these limits are considered non-conforming loans or jumbo loans.

Conventional loan vs FHA mortgage rates

Mortgage rates typically look lower for FHA loans than conventional loans on paper. For instance, today’s average FHA rates are as low as % (% APR)*, while conventional mortgage rates are as low as % (% APR)*.

Compare conventional and FHA mortgage rates. Start here

However, those rates can’t be taken at face value. First, because mortgage rates vary depending on your personal finances, your rate will likely be different from the average rate.

Second, PMI and credit score can also affect your interest rate and mortgage payment. For conventional loans, a lower credit score means a higher interest rate. So if your score is in the low- to mid-600s, an FHA loan might be cheaper.

Conventional loans also base mortgage insurance rates on your credit score, which contributes to a higher monthly payment as well.

*Current rates according to The Mortgage Reports’ lender network. Rates are for sample purposes only; your own rate will be different.

Conventional loan vs FHA mortgage payments

For home buyers with good credit scores, a conventional loan may be more attractive. That’s because conventional loan costs are more dependent on your credit score and down payment than FHA loan costs. And as a result, your monthly payments and PMI are lower when your credit score is higher. This is a key difference from how FHA loans work.

Compare conventional and FHA mortgage rates. Start here

With an FHA loan, your mortgage rate and MIP cost the same no matter what your FICO score.

That means in the short term, FHA loans may be more advantageous.

But over the long-term, borrowers with above-average credit scores will typically find Conventional 97 loans more economical relative to FHA ones.

Remember, mortgage insurance for conventional loans can be canceled at 20% loan-to-value ratio. But FHA mortgage insurance lasts the entire life of the loan. The only way to bypass this requirement is if you put down at least 10% down. This way you may be able to drop FHA mortgage insurance after 11 years (assuming 20% loan-to-value).

So if you’ll be staying in the home long enough to reach 20% equity — and especially if you have a good credit score — a conventional loan could be your cheaper option in the long run.

FHA vs Conventional infographic

Alternative low-down-payment loan programs

The conventional 97 loan and FHA loan aren’t the sole options for low-down-payment mortgages. Explore a variety of other mortgage loans with low or no upfront expenses to make homeownership more accessible:

Compare your home loan options. Start here

Fannie Mae HomeReady: This home loan offers below market interest rates, reduced private mortgage insurance costs, and it allows the income of everyone living in the household to qualify. However, there are income limits, loan maximums, and you’ll need a FICO score of 620 or more and a DTI of 50% or less

Freddie Mac Home Possible: Similar to HomeReady, it has income and loan limits, and it requires a minimum credit score of 660, 3% down payment, and DTI below 43%. However, Freddie Mac Home Possible offers flexible loan approval requirements that help low-income families become homeowners

VA loan: This mortgage loan requires no down payment and offers flexible credit score minimums and below-market rates. VA loans have no maximum loan amounts. Plus, bankruptcy and foreclosure are not immediate disqualifications. Yet, this program is only available to eligible service members and veterans

USDA loan: This rural housing government-backed loan requires no down payment and has no maximum home purchase price. Although there are drawbacks. This government-agency loan does have property standards that require the home to be located in a rural area. There are also income limits for the buyer, and it does carry mortgage insurance for the entire loan term

Most of these mortgage loan products can only be used to purchase a primary residence — a home in which you live in for the majority of the year.

Vacation homes and investment properties are generally not allowed.

For many first-time homebuyers, though, the choice among low-down payment loans will be between the FHA loan and the Conventional 97. This is because VA loans are available to military borrowers only. USDA loans are restricted to suburban and rural areas, with maximum loan and income limits, and HomeReady has similar income restrictions.

Conventional loan vs FHA loan FAQ

Which is a better loan, FHA or conventional?

Between FHA and conventional, the better loan for you depends on your financial circumstances. FHA might be better than conventional if you have a credit score below 680, or higher levels of debt (up to 50 percent DTI). Conventional loans become more attractive the higher your credit score is because you can get a lower interest rate and monthly payment.

Can you switch from FHA to conventional?

You can switch from an FHA to a conventional loan by refinancing your mortgage. This means you get a new conventional loan to pay off your existing FHA loan. This might make sense to do if you have at least 20 percent equity in your home and a 620 or higher credit score. Then, you may be able to save by switching from an FHA to a conventional loan with no PMI.

What are the benefits of a conventional home loan?

If you get a conventional loan with 20 percent down or more, you won’t have to pay for mortgage insurance. That’s a big benefit over FHA loans, which require mortgage insurance regardless of your down payment size. The conventional 97 loan also lets you put just 3 percent down, while FHA requires 3.5 percent at minimum. And conventional loans offer lower mortgage rates the higher your credit score is. That’s good news if you have a good credit score of 720 or higher.

Is an FHA loan bad?

FHA loans are great for borrowers who need a home loan with a lower bar of entry. The big benefits are that they allow lower down payments (just 3.5 percent) and a lower credit score (580) than many other mortgage loans.

What are the disadvantages of FHA loans?

You have to pay for FHA mortgage insurance regardless of your down payment size. And you can’t get rid of it unless you refinance. So if you have a great credit score and/or you’re putting 20 percent or more down, an FHA loan likely isn’t the right choice for you. In that case, look into a conventional loan instead.

What credit score do I need for a conventional loan?

Conventional loans require a credit score of at least 620. But some mortgage lenders might set their own requirements, starting at 640, 660, or even higher. Plus, your conventional mortgage rate will be better the higher your credit score is. So especially if your credit is on the lower end, be sure to show around with different lenders for the best deal.

What credit score do I need for an FHA loan?

FHA loans require a credit score of 580 or higher in most cases. You might be able to get an FHA loan with a credit score of 500-580 if you make a 10 percent or bigger down payment. But you’ll have to search for the right lender because few mortgage companies allow scores in that range for FHA loans.

What’s the interest rate on a conventional loan?

Conventional loan interest rates are typically a little higher than FHA mortgage rates. That’s because FHA loans are backed by the Federal Housing Administration, which makes them less “risky” for lenders and allows for lower rates. However, if you have a great credit score (above 680, in most cases) you might qualify for a lower conventional rate. But, you also have to consider the annual mortgage insurance rate with each loan. Depending on your credit score and down payment, conventional mortgage insurance rates could be higher or lower than FHA insurance rates. This will affect which loan is cheaper overall.

Who qualifies for a conventional loan?

You might qualify for a conventional loan if you have a credit score of at least 620; a debt-to-income ratio of 43 percent or lower; a 3 percent down payment; and a steady, two-year employment history proven by tax returns and bank statements. To qualify for the low-down-payment conventional 97 loan, you must buy a single-family property (no 2-,3-, or 4-units allowed).

Which loan type has a higher credit score requirement?

Generally, conventional loans have a higher credit score requirement than FHA loans. Conventional loans may require a credit score of 620 or higher, while FHA loans may allow for a credit score as low as 500 to 580, depending on the lender.

What is mortgage insurance, and how does it differ for conventional loans and FHA loans?

Mortgage insurance is a type of insurance that protects lenders in case the borrower defaults on the loan. With a conventional loan, private mortgage insurance (PMI) is generally required if the down payment is less than 20%. With an FHA loan, mortgage insurance premiums (MIP) are required for the life of the loan.

Which loan type has more flexible underwriting requirements?

FHA loans generally have more flexible underwriting requirements compared to conventional loans. They may allow for higher debt-to-income ratios, lower credit scores, and non-traditional credit histories. Conventional loans may have stricter underwriting requirements.

Can you refinance from an FHA loan to a conventional loan?

Yes, you can refinance from an FHA loan to a conventional loan. Refinancing may help you get a lower interest rate, lower monthly payments, or eliminate mortgage insurance. However, it’s important to evaluate the potential costs, benefits, and qualification requirements before proceeding with the refinance.

Conventional loan vs FHA: The bottom line

For today’s low down payment home buyers, there are scenarios in which the FHA loan is what’s best for financing; and there are scenarios in which the Conventional 97 is the clear winner. Mortgage rates for both home loans should be reviewed and evaluated.

Ready to make a home purchase? Talk with a loan officer about your mortgage options. You should compare personalized quotes for both FHA and conventional loans to see which one is cheaper for your situation and suits your needs best.

Time to make a move? Let us find the right mortgage for you

While the dream of homeownership might seem elusive on a tight budget, the availability of low income home loans offers a beacon of hope.

These specialized loans come in handy, particularly when the obstacles of saving for a down payment loom large—a common hurdle if you’re already strapped with rent payments.

So if you’re wondering how to bridge the financial gap between renting and owning, read on to explore the various low income home loan programs that could unlock the door to your future home.

Verify your home buying eligibility. Start here

In this article (Skip to…)

Can I buy a house with low income?

Yes, you can buy a house with a low income by qualifying for housing assistance programs and special mortgage loans. That’s because there is no minimum income requirement to buy a house.

However, your ability to do so will depend on a variety of factors specific to your financial situation. A mortgage lender will examine your credit score, debt-to-income ratio, and down payment to determine if you qualify.

Check your mortgage eligibility. Start here

What are low income home loans?

The path to homeownership can be fraught with challenges, particularly for those with limited financial resources. Enter low income home loans—a specialized type of mortgage designed to level the playing field for buyers facing financial barriers.

Low-income mortgage programs focus on addressing the common challenges that low-income earners encounter, such as managing debt, maintaining less-than-stellar credit scores, and struggling to save for a significant down payment.

Verify your home buying eligibility. Start here

Minimal down payment requirements: One of the most daunting aspects of buying a home is accumulating a large down payment. Low income home loans often require smaller down payments, making it easier for buyers to make the initial leap.

Lenient credit criteria: Having a perfect credit score is not always feasible, especially when living on a limited income. These loans often have more flexible credit requirements, allowing for a broader range of credit histories.

Reduced costs at closing: High closing costs can be another hurdle. Low income home loan programs may offer reduced or even waived closing costs in certain circumstances.

Competitive mortgage interest rates: High interest rates can quickly make a mortgage unaffordable. Low income home loans often feature competitive interest rates, reducing long-term costs.

Lower mortgage insurance premiums: Some programs offer reduced premiums for mortgage insurance, further lowering monthly payments.

Interestingly enough, some of these programs often have income caps, essentially barring applicants who have incomes that are considered too high. This ensures that the programs benefit those who need them most.

Requirements for low income home loans

Your ability to qualify for a loan is not solely based on your income. Lenders will assess your debt-to-income (DTI) ratio, a key metric that represents your monthly debts as a percentage of your monthly income. Generally, a DTI under 35% is viewed as favorable, making you a more appealing candidate for a mortgage.

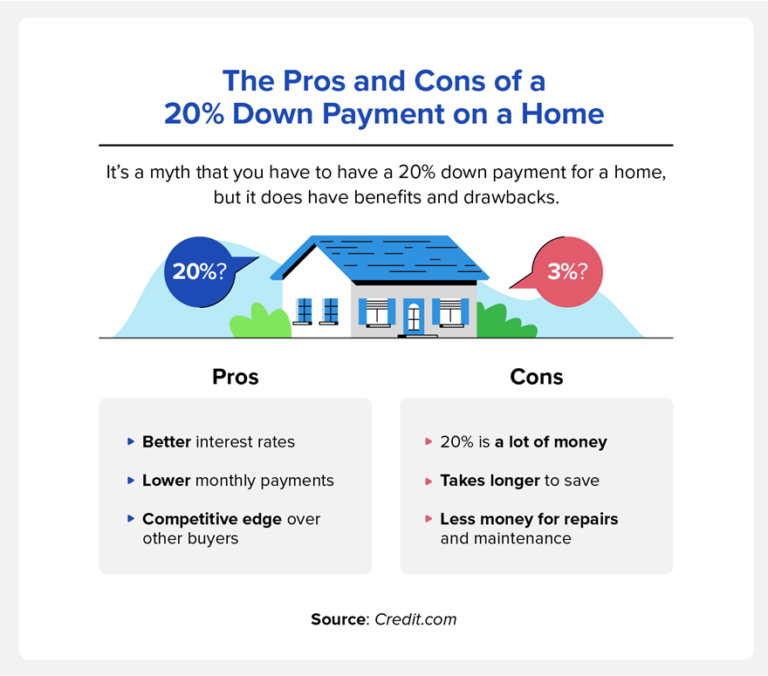

If saving a down payment is your chief concern, don’t worry; there are plenty of options that require minimal, or sometimes zero, down payments. Despite common misconceptions, a 20% down payment is not a universal requirement.

Additional Assistance

Beyond the loan itself, there are various homebuyer assistance programs that can help with the down payment and closing costs. Some of these are structured as grants that don’t require repayment, making it easier to achieve the dream of owning a home.

Navigating the complexities of mortgages and home buying can be intimidating, but low income home loans and assistance programs offer a lifeline to those who dream of owning their own home. These financial products and services are tailored to alleviate the most common obstacles, offering a viable path to homeownership for those who may have thought it was out of reach.

Low income home loans

Low income home buyers have plenty of loan options and special assistance programs to help with a home purchase. Here’s what you can expect.

Check your mortgage eligibility. Start here

Loan Type

Credit Score

Down Payment

Unique Requirements

HomeReady

Generally 620

As low as 3%

Income limits based on area, homebuyer education course required

Home Possible

Generally 660

As low as 3%

Must be primary residence, income limits may apply, can include 1-4 unit properties

Must be a qualifying service member, veteran, or eligible spouse; primary residence only

USDA Loans

Usually 640

No down payment required

Must be in a qualifying rural area, income limits apply, primary residence only

HomeReady and Home Possible mortgages

Fannie Mae’s HomeReady program and Freddie Mac’s Home Possible loan are geared toward lower-income home buyers. You need only 3% down to qualify, and there is no minimum “required contribution” from the borrower. That means the money can come from a gift, grant, or loan from an acceptable source.

Even better, the home seller can pay closing costs worth up to 3% of the purchase price. Instead of negotiating a lower sales price, try asking the seller to cover your closing costs.

Private mortgage insurance (PMI) may also be discounted for these low income home loans. You’re likely to get a lower PMI rate than borrowers with standard conventional mortgages, which could save you a lot of money from month to month.

“This is the biggest benefit,” says Jon Meyer, The Mortgage Reports loan expert and licensed mortgage loan originator. “The PMI is offered at a lower rate than with a standard conventional loan.”

Finally, Home Possible and HomeReady might make special allowances for applicants with low incomes. For instance, HomeReady lets you add income from a renter on your mortgage application, as long as they’ve lived with you for at least a year prior. This can help boost your qualifying income and make it easier to get financing.

You might qualify for HomeReady or Home Possible if your household income is below local income limits and you have a credit score between 620 and 660.

FHA loans

FHA loans offer flexible approval requirements for repeat and first-time home buyers alike. This program, which the Federal Housing Administration backs, relaxes borrowers’ standards to get a mortgage. This can open up the home-buying process to more renters.

You might be able to get an FHA home loan with a debt-to-income ratio (DTI) up to 45% or a credit score as low as 580 while paying only 3.5% down

Select FHA lenders even allow credit scores as low as 500, provided the buyer can make a 10% down payment

Thanks to these perks and others, the FHA loan is one of the most popular low-down-payment mortgages on the market.

Check your FHA loan eligibility. Start here

VA loans

Veterans Affairs-backed VA loans provide military homebuyers with a number of advantages.

No down payment requirement. You can finance 100% of the purchase price. You can also refinance 100% of your home’s value using a VA loan

No mortgage insurance. But you will pay a one-time VA Funding Fee. You can wrap it into the loan amount.

No minimum credit score. Although lenders are allowed to add their own minimums. Those that do often require a FICO score of at least 580 to 620.

Sellers can pay up to 4% of the purchase price in closing costs. So if you find a motivated seller, you could potentially get into a home with nothing out of pocket

If you’re a veteran, active-duty service member, or surviving spouse, the VA mortgage program should be your first stop.

Check your VA loan eligibility. Start here

USDA loans

If you’re not buying in a large city, you may qualify for a USDA home loan. Officially called the Single-Family Housing Guaranteed Loan Program, the USDA loan was created to help moderate- and low-income borrowers buy homes in rural areas.

With a USDA loan, you can buy a home with no money down. The only catch is that you must buy in a USDA-approved rural area (though these are more widespread than you might think). You can find out if the property you’re buying is located in a USDA-eligible rural area and whether you meet local income limits using the USDA’s eligibility maps.

Your monthly payments might be cheaper, too. That’s because interest and mortgage insurance rates are typically lower for USDA loans than for FHA or conforming loans.

There are two types of USDA loans.

The Guaranteed Program is for buyers with incomes up to 115% of their Area Median Income (AMI)

The Direct Program is for those with incomes between 50% and 80% of the AMI

Standard USDA-guaranteed loans are available from many mainstream lenders. But the Direct program requires borrowers to work directly with the U.S. Department of Agriculture.

You typically need a credit score of 640 or higher to qualify.

Check your USDA loan eligibility. Start here

Low income home loan programs

Aside from mortgages that are designed to help people with low incomes buy a home, there are also a number of other programs that offer help to make homeownership more accessible.

Verify your home buying eligibility. Start here

Program

Description

Who Is Eligible

Hud Homes

Discounted homes sold by the Department of Housing and Urban Development.

Low- to moderate-income families, with preference for those who will make it their primary residence. May include single-family homes.

Housing Choice Voucher Program

Vouchers to subsidize the cost of housing in the private market.

Low-income families; must meet income and other criteria set by state and local housing programs.

Good Neighbor Next Door

Significant discounts on homes for teachers, firefighters, police officers, and EMTs.

Must commit to living in the property as a primary residence for at least 36 months. Includes single-family homes.

HFA Loans

Loans offered by state Housing Finance Agencies with reduced interest rates and down payment assistance.

First-time or repeat buyers with low to moderate incomes must meet income requirements. Often, it must be a primary residence.

Down Payment Assistance

Grants or loans to cover the down payment and sometimes closing costs.

Typically for low- to moderate-income families, though criteria can vary by program. Often for single-family homes.

State or Local Assistance

Various grants, loans, or tax credits are offered at the state or local level.

Eligibility varies but usually targets low- to moderate-income families. May include single-family homes.

Mortgage Credit Certificates

Tax credit to reduce federal income tax liability.

First-time homebuyers who meet income requirements; must be primary residence.

Manufactured and Mobile Homes

Loans or grants specifically for manufactured or mobile homes.

Low- to moderate-income families; must meet criteria set by specific housing programs. Usually must be primary residence.

Hud Homes

When the FHA forecloses on homes, those properties are often put up for sale as HUD Homes. And, you can generally purchase one at a steep discount. To qualify for a HUD Home, it will need to be your primary residence for at least 12 months. Additionally, you must not have purchased another HUD in the past 24 months.

Keep in mind that HUD Homes are sold as-is. Many are fixer-uppers. Moreover, HUD Homes are purchased through a bidding process. You’ll need a real estate agent or mortgage broker licensed with HUD to bid on an FHA property.

You can find HUD Homes on the official HUD website, hudhomestore.com. There, you’ll see all HUD real estate owned (REO) single-family properties in your area.

Good Neighbor Next Door

The Good Neighbor Next Door program offers unique benefits for nurses, first responders, and teachers. If you’re eligible, you can buy HUD foreclosure homes at a 50% discount. Use an FHA mortgage, and you only need $100 for a down payment.

You can find the homes on the U.S. Department of Housing and Urban Development website. You’ll also need a HUD-licensed real estate agent to put your offer in for you.

If your offer is accepted and you qualify for financing, you get the home. The 50% discount makes homeownership a lot more affordable. However, be aware that this discount is actually a second mortgage. But it has no interest and requires no payments. Live in the home for three years, and the second mortgage is forgiven entirely.

HFA home loans

Not to be confused with FHA loans, HFA loans are offered in partnership with state and local Housing Finance Authorities.

Many HFA loans are conventional mortgages backed by Fannie Mae and Freddie Mac. They may require as little as 3% down, and many HFA programs can be used with down payment assistance to reduce the upfront cost of home buying.

Borrowers who qualify for an HFA loan might also be in line for discounted mortgage rates and mortgage insurance premiums. To qualify, you’ll typically need a credit score of at least 620. But eligibility requirements vary by program.

Find and contact your state’s public housing finance agency or authority to learn more and see if you qualify. Also, be aware that this type of loan program will require additional approval steps that may make loan closing take longer.

Down payment assistance programs (DPAs)

Down payment assistance is exactly what it sounds like. It provides help with down payments on home purchases and often closing costs. Government agencies, nonprofits, and other sources commonly offer down payment and closing cost assistance. They are usually in the form of a grant or loan (though the loans may be forgiven if you stay in the house for five to ten years).

Most DPA programs target low-income home buyers and have guidelines that make qualifying easier. Some, however, provide assistance to people who buy in “underserved” or “redevelopment” areas, regardless of income. Many DPA programs offer assistance worth tens of thousands of dollars.

Talk to a lender about your options. Start here

Mortgage Credit Certificates (MCCs)

Mortgage credit certificates (MCCs) can stretch your home-buying power. If you meet income requirements, you could get a tax credit equal to some percentage of your mortgage interest. Lenders are allowed to add this credit to your qualifying income when underwriting your mortgage. This allows you to qualify for a higher mortgage amount than you otherwise could.

There are numerous states, counties, and cities that issue mortgage credit certificates, and their regulations and amounts vary greatly. Check with your local housing finance authority to find out whether MCCs are available where you live.

Housing Choice Voucher Program

The Housing Choice Voucher homeownership program (HCV) provides both rental and home buying assistance to eligible low-income households. Also known as Section 8, this program allows low-income home buyers to use housing vouchers to purchase their own homes.

Because local public housing agencies run these voucher programs, eligibility varies depending on location. Still, you’ll likely need to meet the following requirements:

Program-specific income and employment conditions

Being a first-time home buyer

Completing a pre-assistance homeownership and counseling program

Keep in mind that not all states offer voucher programs, and some programs have waiting lists. Also, these programs could limit how much you can sell the home for later on. To find out if your area offers a participating program, use the HUD locator web tool.

Manufactured and mobile homes

A manufactured home usually costs less than a traditional, site-built home. When placed on approved foundations and taxed as real estate, manufactured homes can be financed with mainstream mortgage programs.

Many programs require slightly higher down payments or more restrictive terms for manufactured homes. HomeReady, for example, increases the minimum down payment from 3% to 5% if you finance a manufactured home. Other programs require the home to be brand new.

Additionally, there are often requirements regarding the year the home was built and the property’s foundation. These guidelines will vary between lenders. Mobile homes that are not classified as real estate can be purchased with personal loans like the FHA’s Title 2 program. These are not mortgages because the homes are not considered real estate.

Check your mortgage options. Start here

Tips for buying a house with low income

Whether you’re buying a new home or your first home, these tips can help you achieve your homeownership goals.

Verify your home buying eligibility. Start here

Improve your credit history

Improving your FICO score is the best way to increase your chances of loan approval and qualify for lower mortgage rates.

The credit score needed to purchase a home varies depending on the type of loan you apply for. Conventional loans typically require a score of at least 620, while FHA loans often require at least 580.

Start by pulling free credit reports from annualcreditreport.com to determine your current score. Next, consider a few of the common methods for increasing credit scores. The amount of work that you’ll need to do will depend on your personal financial situation.

As an example, if your credit score is low because you’re using too much of your available credit, you may benefit from a debt consolidation loan to tame your high-interest account balances and improve your credit utilization.

On the other hand, if your credit history reveals missed payments, you’ll need to show at least 12 months of regular, on-time payments to improve your score.

Save for a down payment

The average first-time home buyer puts just 13% down on a new home. Yet, many loan programs require as little as 3% down or no down payment at all.

Remember that you still have to pay closing costs, which are typically around 2% to 5% of your mortgage loan amount. If you put less than 20% down, you’ll almost certainly have to pay for mortgage insurance.

In addition, you may need cash reserves in your savings account. This assures lenders that you can make your monthly mortgage payments should you suffer a financial setback. However, don’t let the down payment scare you away from homeownership. Many buyers qualify without even knowing it.

Pay down debts

Paying down debts will lower your debt-to-income ratio and improve your odds of mortgage approval. This is especially true for those with high-interest credit card debt.

You’ll likely qualify for lower rates when you have:

A low debt-to-income ratio (DTI)

High credit score

3% to 5% down payment

Stable income for the past two consecutive years

Use a first-time home buyer program

First-time buyer programs offer flexible guidelines for qualified buyers. Plus, these special programs exist in every state to help low-income households achieve homeownership.

Unlike traditional conventional loans, the government backs many first-time buyer mortgages. This allows mortgage lenders to offer loans with better rates and lower credit score requirements than they normally would be able to.

Verify your low income home loan eligibility. Start here

Model your budget

Owning a home requires more than qualifying for a loan and making monthly mortgage payments. Homeowners are responsible for a variety of ongoing costs, including:

Homeowners insurance

Property taxes

Mortgage insurance (in many cases)

Utility bills

Ongoing home maintenance

Home improvements

Appliance repair and replacement

Home buyers who have experience paying these ongoing costs of homeownership will be better prepared for the big day when they get the keys to their dream home.

Plus, sticking to this model budget in the months and years before purchasing a home and then saving the money you would spend on housing costs, such as insurance premiums and utilities, is a great way to build cash reserves and save for a down payment.

Use a co-signer

If you’re on the edge of qualifying for your own loan, using a co-signer may be an option.

Essentially, when you buy a house with a co-signer, you and your co-signer are both responsible for making the monthly payments. You’ll both also build and share in the home’s equity. Purchasing a home with a co-signer is quite common among unmarried couples, friends, and family members.

FAQ: Low income home loans

Verify your home buying eligibility. Start here

How do you buy a house with low income?

To buy a house with a low income, you have to know which mortgage program will accept your application. A few popular options include: FHA loans (allowing low income and as little as 3.5 percent down with a 580 credit score); USDA loans (for low-income buyers in rural and suburban areas); VA loans (a zero-down option for veterans and service members); and HomeReady or Home Possible (conforming loans for low-income buyers with just 3 percent down).

I make $25K a year; can I buy a house?

Mortgage experts recommend spending no more than 28 percent of your gross monthly income on a housing payment. So if you make $25K per year, you can likely afford around $580 per month for a house payment. Assuming a fixed interest rate of 6 percent and a 3 percent down payment, that might buy you a house worth about $100,000. But that’s only a rough estimate. Talk with a mortgage lender to get the exact numbers for your situation.

How do I qualify for a low-income mortgage?

Whether or not you qualify for a low income home loan depends on the program. For example, you might qualify for an FHA mortgage with just 3.5 percent down and a 580 credit score. Or, if your house is in a qualified area and you’re below local income caps, you might be able to get a zero-down USDA mortgage. Veterans can qualify for a low-income mortgage using a VA loan. Or, you can apply for the mortgage with a co-borrower and qualify based on combined incomes.

What programs are available for first-time home buyers?

Low income home loans can help first-time home buyers overcome hurdles like low credit or income, smaller down payments, or high levels of debt. A few good programs for first-time home buyers include Freddie Mac’s Home Possible mortgage, Fannie Mae’s HomeReady mortgage, the Conventional 97 mortgage, and government-backed loans like FHA, USDA, and VA. First-time home buyers can also apply for down payment assistance grants through their state or local housing department.

Can the government help me buy a house?

There are a number of ways the government can help you buy a house. Perhaps the most direct way to get help is by applying for down payment assistance. This is a grant or low-interest loan to help you make a down payment. You can also buy a house using a government-backed mortgage, like the FHA or USDA. With these programs, the government essentially insures the loan, so you can buy with a lower income, credit score, or down payment than you could otherwise.

How do I buy a house without proof of income?

You can no longer buy a house without proof of income. You have to prove you can pay the loan back somehow. But there are modern alternatives to stated-income loans. For instance, you can show “proof of income” through bank statements, assets, or retirement accounts instead of W2 tax forms (the traditional method). Many people who want to buy a house without proof of income these days find a bank statement loan to be a good option.

How do you rent to own?

A lease option or rent-to-own home isn’t exactly what it sounds like. You don’t simply rent until the house is paid off. Instead, you usually pay a higher rent for a set period of time. That excess rent then goes toward a down payment when you buy the house at a later date. Rent-to-own might help you buy a house if you don’t have a lot of cash on hand right now or if you need to improve your credit score before applying for a mortgage. However, rent-to-own requires seller cooperation and comes with unique risks.

Can I rent-to-own with no down payment?

Rent-to-own does not mean you can buy a house with no down payment. When you rent-to-own, you’re paying extra rent each month that will go toward your down payment later on. And usually, rent-to-own contracts include an option fee that’s a lot like a down payment. The option fee is smaller. Think 1 percent of the purchase price instead of 3 to 20 percent. And that fee eventually goes toward your purchase. But it’s still a few thousand dollars you must pay upfront to secure the right to buy the home later on.

Can I get a grant to buy a house?

Qualified buyers can get a grant to buy a house. These are called down payment assistance grants. They won’t pay for the whole house, but they can help cover your down payment to make a mortgage more affordable. You’re most likely to qualify for a grant to buy a house if you have a low to moderate income and live in a target area.

What type of low income home loan is the easiest to qualify for?

FHA loans are generally the easiest low income home loan to qualify for. The federal government insures these loans, which means lenders can relax their qualifying rules. It’s possible for a home buyer with a credit score of 500 to get approved for an FHA loan, but most FHA lenders look for scores of 580 or better. And a FICO score of 580 lets you make the FHA’s minimum down payment of 3.5 percent.

How can I get a home loan with low monthly payments?

To get the lowest possible monthly payment, choose a 30-year loan term, find a cheaper home, put more money down, and make sure you have excellent credit before applying for your mortgage. If you can afford a 20 percent down payment, you can avoid PMI premiums, which lower your monthly payments even more. Veterans can get VA loans that require no PMI, regardless of their down payment size.

What’s the lowest amount you can put on a house?

Some home buyers can put no money down with a VA or USDA loan. Conventional loans will require at least 3 percent down, and FHA loans will require at least 3.5 percent down. Down payment assistance grants and loans could help you cover some or all of this down payment.

How much house can I afford if I make $30K a year?

If you make $30,000 a year, you could probably spend about $110,000 on a house, assuming you get a 30-year fixed-rate mortgage at 6 percent. This is a rough estimate. Your unique financial situation may be different. Getting a pre-approval from a lender is the only way to find your actual price range.

What are today’s mortgage rates for low income home loans?

Many low-income mortgage programs have lower interest rates than “standard” mortgage loans. So you might get a great deal.

However, interest rates vary depending on the borrower, the loan program, and the lender.

To find out where you stand, you’ll need to compare loan offers from several lenders and then choose your best deal.

Time to make a move? Let us find the right mortgage for you

Average mortgage rates fell moderately yesterday. That was a bit of a surprise (though a welcome one) because yesterday’s inflation report would normally have pushed them higher. Read on for why markets might have reacted unexpectedly.

Earlier this morning, markets were signaling that mortgage rates today might fall. But these early mini-trends often switch direction or speed as the hours pass — as we saw yesterday.

Current mortgage and refinance rates

Find your lowest rate. Start here

Program

Mortgage Rate

APR*

Change

Conventional 30-year fixed

7.015%

7.03%

-0.07

Conventional 15-year fixed

6.28%

6.31%

-0.1

Conventional 20-year fixed

6.91%

6.93%

-0.065

Conventional 10-year fixed

6.09%

6.125%

-0.14

30-year fixed FHA

5.875%

6.545%

-0.3

30-year fixed VA

5.99%

6.14%

-0.085

5/1 ARM Conventional

6.31%

7.56%

-0.005

Rates are provided by our partner network, and may not reflect the market. Your rate might be different. Click here for a personalized rate quote. See our rate assumptions See our rate assumptions here.

Should you lock your mortgage rate today?

Yesterday’s fall in mortgage rates showed markets continuing to have faith in a “soft landing,” which will occur if we continue to see falling inflation together with a resilient economy. Indeed, it suggests that faith can’t be shaken even by occasional unfriendly data.

I think a soft landing remains the most likely scenario for 2024.

So, my personal rate lock recommendations are:

LOCK if closing in 7 days

FLOAT if closing in 15 days

FLOAT if closing in 30 days

FLOAT if closing in 45 days

FLOATif closing in 60days

However, with so much uncertainty at the moment, your instincts could easily turn out to be as good as mine — or better. So let your gut and your own tolerance for risk help guide you.

>Related: 7 Tips to get the best refinance rate

Market data affecting today’s mortgage rates

Here’s a snapshot of the state of play this morning at about 9:50 a.m. (ET). The data are mostly compared with roughly the same time the business day before, so much of the movement will often have happened in the previous session. The numbers are:

The yield on 10-year Treasury notes tumbled to 3.93% from 4.04%. (Good for mortgage rates.) More than any other market, mortgage rates typically tend to follow these particular Treasury bond yields

Major stock indexes were rising this morning. (Bad for mortgage rates.) When investors buy shares, they’re often selling bonds, which pushes those prices down and increases yields and mortgage rates. The opposite may happen when indexes are lower. But this is an imperfect relationship

Oil prices increased to $74.42 from $72.80 a barrel. (Bad for mortgage rates*.) Energy prices play a prominent role in creating inflation and also point to future economic activity

Goldprices climbed to $2,065 from $2,036 an ounce. (Good for mortgage rates*.) It is generally better for rates when gold prices rise and worse when they fall. Gold tends to rise when investors worry about the economy.

CNN Business Fear & Greed index — inched lower to 73 from 75. (Good for mortgage rates.) “Greedy” investors push bond prices down (and interest rates up) as they leave the bond market and move into stocks, while “fearful” investors do the opposite. So lower readings are often better than higher ones

*A movement of less than $20 on gold prices or 40 cents on oil ones is a change of 1% or less. So we only count meaningful differences as good or bad for mortgage rates.

Caveats about markets and rates

Before the pandemic, post-pandemic upheavals, and war in Ukraine, you could look at the above figures and make a pretty good guess about what would happen to mortgage rates that day. But that’s no longer the case. We still make daily calls. And are usually right. But our record for accuracy won’t achieve its former high levels until things settle down.

So, use markets only as a rough guide. Because they have to be exceptionally strong or weak to rely on them. But, with that caveat, mortgage rates today look likely to decrease. However, be aware that “intraday swings” (when rates change speed or direction during the day) are a common feature right now.

Find your lowest rate. Start here

What’s driving mortgage rates today?

Yesterday

I suspect that Wall Street has bought the narrative of a soft landing (see above) and, for now, is prepared to stick to it through thick and thin. That’s my only real explanation for why mortgage rates fell yesterday despite an unfriendly inflation report.

True, some saw the report as less unfriendly than others. The New York Times (paywall), for example, reported it under the headline, “Price Increases Tick Higher, but Show Moderation.”

But the consumer price index (CPI) was undeniably worse than expected. And that would normally exert some upward pressure on mortgage rates. Still, let’s not give this gift horse too close a dental inspection.

Today

Producer price indexes (PPIs) are typically less important than CPIs. But they still sometimes affect mortgage rates.

Today’s PPI showed factory-gate and wholesale prices rising more slowly than expected. And that would normally be good for mortgage rates. However, as we saw yesterday, markets don’t always follow such “rules.”

Next week

Rather like this week, next week starts slowly but contains an important economic report. Things are especially quiet on Monday because bond markets are closed for Martin Luther King Day. And closed bond markets mean mortgage rates shouldn’t move. (So, we shall not be publishing this daily report on Monday.)

Tuesday’s similarly dull with no economic reports scheduled for release.

However, Wednesday is potentially next week’s big day for mortgage rates, led by the retail sales report for December. But, after that, things tail off again.

Don’t forget you can always learn more about what’s driving mortgage rates in the most recent weekend edition of this daily report. These provide a more detailed analysis of what’s happening. They are published each Saturday morning soon after 10 a.m. (ET) and include a preview of the following week.

Recent trends

According to Freddie Mac’s archives, the weekly all-time lowest rate for 30-year, fixed-rate mortgages was set on Jan. 7, 2021, when it stood at 2.65%. The weekly all-time high was 18.63% on Sep. 10, 1981.

Freddie’s Jan. 11 report put that same weekly average at 6.66%, up from the previous week’s 6.62%. But note that Freddie’s data are almost always out of date by the time it announces its weekly figures.

Expert forecasts for mortgage rates

Looking further ahead, Fannie Mae and the Mortgage Bankers Association (MBA) each has a team of economists dedicated to monitoring and forecasting what will happen to the economy, the housing sector and mortgage rates.

And here are their rate forecasts for the last quarter (Q4/23) and the following three quarters (Q1/24, Q2/24 and Q3/24).

The numbers in the table below are for 30-year, fixed-rate mortgages. Fannie’s were updated on Dec. 19 and the MBA’s on Dec. 13.

Forecaster

Q4/23

Q1/24

Q2/24

Q3/24

Fannie Mae

7.4%

7.0%

6.8%

6.6%

MBA

7.4%

7.0%

6.6%

6.3%

Of course, given so many unknowables, both these forecasts might be even more speculative than usual. And their past record for accuracy hasn’t been wildly impressive.

Important notes on today’s mortgage rates

Here are some things you need to know:

Typically, mortgage rates go up when the economy’s doing well and down when it’s in trouble. But there are exceptions. Read ‘How mortgage rates are determined and why you should care’

Only “top-tier” borrowers (with stellar credit scores, big down payments, and very healthy finances) get the ultralow mortgage rates you’ll see advertised

Lenders vary. Yours may or may not follow the crowd when it comes to daily rate movements — though they all usually follow the broader trend over time

When daily rate changes are small, some lenders will adjust closing costs and leave their rate cards the same

Refinance rates are typically close to those for purchases.

A lot is going on at the moment. And nobody can claim to know with certainty what will happen to mortgage rates in the coming hours, days, weeks or months.

Find your lowest mortgage rate today

You should comparison shop widely, no matter what sort of mortgage you want. Federal regulator the Consumer Financial Protection Bureau found in May 2023:

“Mortgage borrowers are paying around $100 a month more depending on which lender they choose, for the same type of loan and the same consumer characteristics (such as credit score and down payment).”

In other words, over the lifetime of a 30-year loan, homebuyers who don’t bother to get quotes from multiple lenders risk losing an average of $36,000. What could you do with that sort of money?

Verify your new rate

Mortgage rate methodology

The Mortgage Reports receives rates based on selected criteria from multiple lending partners each day. We arrive at an average rate and APR for each loan type to display in our chart. Because we average an array of rates, it gives you a better idea of what you might find in the marketplace. Furthermore, we average rates for the same loan types. For example, FHA fixed with FHA fixed. The end result is a good snapshot of daily rates and how they change over time.

How your mortgage interest rate is determined

Mortgage and refinance rates vary a lot depending on each borrower’s unique situation.

Factors that determine your mortgage interest rate include:

Overall strength of the economy — A strong economy usually means higher rates, while a weaker one can push current mortgage rates down to promote borrowing

Lender capacity — When a lender is very busy, it will increase rates to deter new business and give its loan officers some breathing room

Property type (condo, single-family, town house, etc.) — A primary residence, meaning a home you plan to live in full time, will have a lower interest rate. Investment properties, second homes, and vacation homes have higher mortgage rates

Loan-to-value ratio (determined by your down payment) — Your loan-to-value ratio (LTV) compares your loan amount to the value of the home. A lower LTV, meaning a bigger down payment, gets you a lower mortgage rate

Debt-To-Income ratio — This number compares your total monthly debts to your pretax income. The more debt you currently have, the less room you’ll have in your budget for a mortgage payment

Loan term — Loans with a shorter term (like a 15-year mortgage) typically have lower rates than a 30-year loan term

Borrower’s credit score — Typically the higher your credit score is, the lower your mortgage rate, and vice versa

Mortgage discount points — Borrowers have the option to buy discount points or ‘mortgage points’ at closing. These let you pay money upfront to lower your interest rate

Remember, every mortgage lender weighs these factors a little differently.

To find the best rate for your situation, you’ll want to get personalized estimates from a few different lenders.

Verify your new rate. Start here

Are refinance rates the same as mortgage rates?

Rates for a home purchase and mortgage refinance are often similar.

However, some lenders will charge more for a refinance under certain circumstances.

Typically when rates fall, homeowners rush to refinance. They see an opportunity to lock in a lower rate and payment for the rest of their loan.

This creates a tidal wave of new work for mortgage lenders.

Unfortunately, some lenders don’t have the capacity or crew to process a large number of refinance loan applications.

In this case, a lender might raise its rates to deter new business and give loan officers time to process loans currently in the pipeline.

Also, cashing out equity can result in a higher rate when refinancing.

Cash-out refinances pose a greater risk for mortgage lenders, so they’re often priced higher than new home purchases and rate-term refinances.

Check your refinance rates today. Start here

How to get the lowest mortgage or refinance rate

Since rates can vary, always shop around when buying a house or refinancing a mortgage.

Comparison shopping can potentially save thousands, even tens of thousands of dollars over the life of your loan.

Here are a few tips to keep in mind:

1. Get multiple quotes

Many borrowers make the mistake of accepting the first mortgage or refinance offer they receive.

Some simply go with the bank they use for checking and savings since that can seem easiest.

However, your bank might not offer the best mortgage deal for you. And if you’re refinancing, your financial situation may have changed enough that your current lender is no longer your best bet.

So get multiple quotes from at least three different lenders to find the right one for you.

2. Compare Loan Estimates

When shopping for a mortgage or refinance, lenders will provide a Loan Estimate that breaks down important costs associated with the loan.

You’ll want to read these Loan Estimates carefully and compare costs and fees line-by-line, including:

Interest rate

Annual percentage rate (APR)

Monthly mortgage payment

Loan origination fees

Rate lock fees

Closing costs

Remember, the lowest interest rate isn’t always the best deal.

Annual percentage rate (APR) can help you compare the ‘real’ cost of two loans. It estimates your total yearly cost including interest and fees.

Also, pay close attention to your closing costs.

Some lenders may bring their rates down by charging more upfront via discount points. These can add thousands to your out-of-pocket costs.

3. Negotiate your mortgage rate

You can also negotiate your mortgage rate to get a better deal.

Let’s say you get loan estimates from two lenders. Lender A offers the better rate, but you prefer your loan terms from Lender B. Talk to Lender B and see if they can beat the former’s pricing.

You might be surprised to find that a lender is willing to give you a lower interest rate in order to keep your business.

And if they’re not, keep shopping — there’s a good chance someone will.

Fixed-rate mortgage vs. adjustable-rate mortgage: Which is right for you?

Mortgage borrowers can choose between a fixed-rate mortgage and an adjustable-rate mortgage (ARM).

Fixed-rate mortgages (FRMs) have interest rates that never change unless you decide to refinance. This results in predictable monthly payments and stability over the life of your loan.

Adjustable-rate loans have a low interest rate that’s fixed for a set number of years (typically five or seven). After the initial fixed-rate period, the interest rate adjusts every year based on market conditions.

With each rate adjustment, a borrower’s mortgage rate can either increase, decrease, or stay the same. These loans are unpredictable since monthly payments can change each year.

Adjustable-rate mortgages are fitting for borrowers who expect to move before their first rate adjustment, or who can afford a higher future payment.

In most other cases, a fixed-rate mortgage is typically the safer and better choice.

Remember, if rates drop sharply, you are free to refinance and lock in a lower rate and payment later on.

How your credit score affects your mortgage rate

You don’t need a high credit score to qualify for a home purchase or refinance, but your credit score will affect your rate.

This is because credit history determines risk level.

Historically speaking, borrowers with higher credit scores are less likely to default on their mortgages, so they qualify for lower rates.

For the best rate, aim for a credit score of 720 or higher.

Mortgage programs that don’t require a high score include:

Conventional home loans — minimum 620 credit score

FHA loans — minimum 500 credit score (with a 10% down payment) or 580 (with a 3.5% down payment)

VA loans — no minimum credit score, but 620 is common

USDA loans — minimum 640 credit score

Ideally, you want to check your credit report and score at least 6 months before applying for a mortgage. This gives you time to sort out any errors and make sure your score is as high as possible.

If you’re ready to apply now, it’s still worth checking so you have a good idea of what loan programs you might qualify for and how your score will affect your rate.

You can get your credit report from AnnualCreditReport.com and your score from MyFico.com.

How big of a down payment do I need?

Nowadays, mortgage programs don’t require the conventional 20 percent down.

In fact, first-time home buyers put only 6 percent down on average.

Down payment minimums vary depending on the loan program. For example:

Conventional home loans require a down payment between 3% and 5%

FHA loans require 3.5% down

VA and USDA loans allow zero down payment

Jumbo loans typically require at least 5% to 10% down

Keep in mind, a higher down payment reduces your risk as a borrower and helps you negotiate a better mortgage rate.

If you are able to make a 20 percent down payment, you can avoid paying for mortgage insurance.

This is an added cost paid by the borrower, which protects their lender in case of default or foreclosure.

But a big down payment is not required.

For many people, it makes sense to make a smaller down payment in order to buy a house sooner and start building home equity.

Verify your new rate. Start here

Choosing the right type of home loan

No two mortgage loans are alike, so it’s important to know your options and choose the right type of mortgage.

The five main types of mortgages include:

Fixed-rate mortgage (FRM)

Your interest rate remains the same over the life of the loan. This is a good option for borrowers who expect to live in their homes long-term.

The most popular loan option is the 30-year mortgage, but 15- and 20-year terms are also commonly available.

Adjustable-rate mortgage (ARM)

Adjustable-rate loans have a fixed interest rate for the first few years. Then, your mortgage rate resets every year.

Your rate and payment can rise or fall annually depending on how the broader interest rate trends.

ARMs are ideal for borrowers who expect to move prior to their first rate adjustment (usually in 5 or 7 years).

For those who plan to stay in their home long-term, a fixed-rate mortgage is typically recommended.

Jumbo mortgage

A jumbo loan is a mortgage that exceeds the conforming loan limit set by Fannie Mae and Freddie Mac.

In 2023, the conforming loan limit is $726,200 in most areas.

Jumbo loans are perfect for borrowers who need a larger loan to purchase a high-priced property, especially in big cities with high real estate values.

FHA mortgage

A government loan backed by the Federal Housing Administration for low- to moderate-income borrowers. FHA loans feature low credit score and down payment requirements.

VA mortgage

A government loan backed by the Department of Veterans Affairs. To be eligible, you must be active-duty military, a veteran, a Reservist or National Guard service member, or an eligible spouse.

VA loans allow no down payment and have exceptionally low mortgage rates.

USDA mortgage

USDA loans are a government program backed by the U.S. Department of Agriculture. They offer a no-down-payment solution for borrowers who purchase real estate in an eligible rural area. To qualify, your income must be at or below the local median.

Bank statement loan

Borrowers can qualify for a mortgage without tax returns, using their personal or business bank account. This is an option for self-employed or seasonally-employed borrowers.

Portfolio/Non-QM loan

These are mortgages that lenders don’t sell on the secondary mortgage market. This gives lenders the flexibility to set their own guidelines.

Non-QM loans may have lower credit score requirements, or offer low-down-payment options without mortgage insurance.

Choosing the right mortgage lender

The lender or loan program that’s right for one person might not be right for another.

Explore your options and then pick a loan based on your credit score, down payment, and financial goals, as well as local home prices.

Whether you’re getting a mortgage for a home purchase or a refinance, always shop around and compare rates and terms.

Typically, it only takes a few hours to get quotes from multiple lenders — and it could save you thousands in the long run.

Time to make a move? Let us find the right mortgage for you

Current mortgage rates methodology

We receive current mortgage rates each day from a network of mortgage lenders that offer home purchase and refinance loans. Mortgage rates shown here are based on sample borrower profiles that vary by loan type. See our full loan assumptions here.

For a third day, average mortgage rates barely moved yesterday. But that’s good because it means last week’s big falls remain effectively uneroded.

First thing, it was again looking as if mortgage rates today might fall, perhaps modestly or moderately. However, that could change as the hours pass.

Current mortgage and refinance rates

Find your lowest rate. Start here

Program

Mortgage Rate

APR*

Change

Conventional 30-year fixed

7.125%

7.14%

-0.075

Conventional 15-year fixed

6.385%

6.415%

-0.1

Conventional 20-year fixed

6.975%

7%

-0.045

Conventional 10-year fixed

6.12%

6.145%

-0.065

30-year fixed FHA

5.98%

6.88%

-0.095

30-year fixed VA

6.165%

6.315%

-0.13

5/1 ARM Conventional

6.425%

7.675%

-0.035

Rates are provided by our partner network, and may not reflect the market. Your rate might be different. Click here for a personalized rate quote. See our rate assumptions See our rate assumptions here.

Should you lock your mortgage rate today?

Every day that passes makes a corrective bounce (when mortgage rates rise as markets think they’ve got carried away) less likely. And it reinforces my hope that those rates are in a downward trend that could last well into next year.

So, my personal rate lock recommendations are:

LOCK if closing in 7 days

FLOAT if closing in 15 days

FLOAT if closing in 30 days

FLOAT if closing in 45 days

FLOATif closing in 60days

However, with so much uncertainty at the moment, your instincts could easily turn out to be as good as mine — or better. So let your gut and your own tolerance for risk help guide you.

>Related: 7 Tips to get the best refinance rate

Market data affecting today’s mortgage rates

Here’s a snapshot of the state of play this morning at about 9:50 a.m. (ET). The data are mostly compared with roughly the same time the business day before, so much of the movement will often have happened in the previous session. The numbers are:

The yield on 10-year Treasury notes edged lower to 3.90% from 3.92%. (Good for mortgage rates.) More than any other market, mortgage rates typically tend to follow these particular Treasury bond yields

Major stock indexes were mostly falling this morning. (Good for mortgage rates.) When investors buy shares, they’re often selling bonds, which pushes those prices down and increases yields and mortgage rates. The opposite may happen when indexes are lower. But this is an imperfect relationship

Oil prices climbed to $75.14 from $73.12 a barrel. (Bad for mortgage rates*.) Energy prices play a prominent role in creating inflation and also point to future economic activity

Goldprices held steady at $2,049 an ounce. (Neutral for mortgage rates*.) It is generally better for rates when gold prices rise and worse when they fall. Gold tends to rise when investors worry about the economy.

CNN Business Fear & Greed index — ticked down to 77 from 78. (Good for mortgage rates.) “Greedy” investors push bond prices down (and interest rates up) as they leave the bond market and move into stocks, while “fearful” investors do the opposite. So lower readings are often better than higher ones

*A movement of less than $20 on gold prices or 40 cents on oil ones is a change of 1% or less. So we only count meaningful differences as good or bad for mortgage rates.

Caveats about markets and rates

Before the pandemic, post-pandemic upheavals, and war in Ukraine, you could look at the above figures and make a pretty good guess about what would happen to mortgage rates that day. But that’s no longer the case. We still make daily calls. And are usually right. But our record for accuracy won’t achieve its former high levels until things settle down.

So, use markets only as a rough guide. Because they have to be exceptionally strong or weak to rely on them. But, with that caveat, mortgage rates today look likely to decrease. However, be aware that “intraday swings” (when rates change speed or direction during the day) are a common feature right now.

Find your lowest rate. Start here

What’s driving mortgage rates today?

The Federal Reserve

This morning’s Wall Street Journal (paywall) observed: “After their policy meeting last week, Fed officials released projections of at least three rate cuts [in general interest rates] next year. They have since been flummoxed that investors expect even faster and deeper cuts. The result: Confusion over when and how quickly the Fed might cut as the central bank tries to bring inflation down without a painful recession.”

This could turn into a real issue that could push mortgage rates higher, probably in the new year. Wall Street has a long and inglorious record of hearing what it wants the Fed to say rather than what the Fed actually says. And we’ve seen quite recently examples of sharp rises in mortgage rates when markets’ wishful thinking collides with reality.