With mortgage rates higher than they have been in over two decades, homebuyers may be looking for alternative ways to finance their home.

An interest-only mortgage can free up some front-end cash, allowing a buyer to cheaply purchase otherwise expensive property, but it carries long-term risks that borrowers should seriously consider.

Here, CNBC Select shares everything you need to know about interest-only mortgages, including how they work and their benefits and risks.

What we’ll cover

What is an interest-only mortgage?

In a traditional loan, borrowers gradually repay the principal (the money borrowed) and the interest (the amount it costs to borrow that money).

This is slightly different in an interest-only mortgage. After a borrower takes out an interest-only loan, they are allotted an introductory grace period, during which they do not have to make payments on the principal of the loan. Instead, they only make interest payments throughout that set period.

Borrowers must then repay the loan in full, whether by lump sum or gradual monthly payments when that set period is over.

Interest-only mortgages are primarily designed for borrowers who stand to make a profit from their loan-funded purchase. For example, if you flip houses, you might take out an interest-only loan to purchase a fixer-upper, since you plan to sell the house at a higher price later. By doing so, you postpone your principal payments until you have sold the renovated house, freeing up front-end cash to make said renovations.

Several of CNBC Select’s top-ranked mortgage lenders offer interest-only mortgages, including Chase Bank and PNC Bank.

CNBC Select found PNC Bank to be the best lender for flexible loan options. PNC Bank offers interest-only mortgages to eligible borrowers with a minimum credit score of 620 and a minimum down payment of 3%. Further, the national lender offers a plethora of tailored mortgage options as well as online and in-person application processes.

PNC Bank

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Conventional loans, FHA loans, VA loans, USDA loans, jumbo loans, HELOCs, Community Loan and Medical Professional Loan

Terms

10 – 30 years

Credit needed

Minimum down payment

0% if moving forward with a USDA loan

Terms apply.

Meanwhile, Chase Bank stood out for its flexible down payment options. Similar to most lenders, Chase Bank offers interest-only mortgages to eligible borrowers with a minimum credit score of 620 and a minimum down payment of 3%. Further, the company offers a wide range of mortgage terms and a number of educational resources to support their borrowers through the home-buying process.

Chase Bank

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Conventional loans, FHA loans, VA loans, DreaMaker℠ loans and Jumbo loans

Terms

10 – 30 years

Credit needed

Minimum down payment

3% if moving forward with a DreaMaker℠ loan

Terms apply.

How to calculate an interest-only mortgage payment

To calculate the payment you’ll make on an interest-only loan, multiply the loan balance by the annual interest rate, then divide by 12.

For example, say you borrow $100,000 at a 5% interest rate. Your calculation would look like this: (100,000 x .05)/12 = 416.67. This means that your interest-only payment would be $416.78 per month.

Payments will then increase to those of a typical, amortized loan, covering both principal and interest. Because your new monthly payment amount is based on the remaining principal, the payments should marginally change as you pay off the mortgage.

Benefits of an interest-only mortgage

The most obvious benefit of an interest-only mortgage is that monthly payments are initially considerably lower than of typical loans. These loans allow the borrower to make larger purchases that they would otherwise only be able to afford a few years down. Thus, interest-only loans might be a wise investment if you are expecting a significant income boost in the coming months and years.

Interest-only mortgages typically turn into an adjustable-rate mortgage (ARM) once principal payments begin, and borrowers can potentially benefit from a lower rate than the fixed-rate average.

But in the same vein, that adjustable-rate mortgage might be significantly higher than a fixed-rate traditional mortgage taken out initially, and this is one among many risks associated with interest-only mortgages.

Risks of an interest-only mortgage

Though a borrower’s monthly payments are initially temporarily lower than those of a traditional loan, there are several considerable risks.

First, if you take out an interest-only mortgage, you will not gain any equity in your home (beyond the equity of your down payment) until you begin principal payments.

Home equity is astoundingly important for your financial future. Equity is the money owed to you should you sell or refinance your home in the future. So, if you take out an interest-only mortgage with a five-year grace period, and you move out in five years, you will likely make no money from the sale of your home (unless the market has boomed exponentially since closing). Your interest-only payments will have realistically acted similarly to rent payments.

Alternatively, if the housing market goes down during your interest-only period and you try to sell your house without paying off any of your principal, you may actually owe the bank money at the time of sale.

Homeowners sometimes take out a home equity line of credit to access cash value tied up in their home’s mortgage. If you purchase your home with an interest-only mortgage, there will be less equity, or less cash, to access if you must take out a second mortgage.

Second, your monthly payments will be relatively high once you begin paying back the principal. This will cause a considerable shift in your monthly budget. Unless you are incredibly financially disciplined, you might not be able to afford these payments. Some interest-only mortgages even require that you pay off the loan in a lump sum when the introductory grace period ends.

Read the terms of an interest-only loan closely and make a sound plan for the duration of the loan. Otherwise, you might end up stuck in financial mud.

Compare offers to find the best loan

FAQs

What is an adjustable-rate mortgage?

One way that buyers can get the keys to a new home without locking in a fixed rate for 30 years is by taking out an adjustable-rate mortgage (ARM), during which interest rates fluctuate with the market through the duration of your loan. Because rates are so high right now, this can save you money in home loan interest down the road when interest rates cool.

What credit score do I need to qualify for an interest-only mortgage?

Interest-only mortgages typically require a credit score of 670 or above.

What is a home equity line of credit?

A home equity line of credit, or HELOC, is essentially a second mortgage that liquidates (usually up to 85% of your home’s equity), or the amount that you have paid toward your principal home loan. A HELOC is more commonly known as a second mortgage. Taking out a HELOC will usually cost you between 2% and 5% of the loan amount.

Bottom line

An interest-only mortgage is smart for the forward-thinking borrower who has a sound plan to make future payments. Otherwise, it makes more sense to pursue a traditional mortgage, avoiding the temptation to bite off more than your wallet can chew.

Subscribe to the CNBC Select Newsletter!

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here.

Why trust CNBC Select?

At CNBC Select, our mission is to provide our readers with high-quality service journalism and comprehensive consumer advice so they can make informed decisions with their money. Every personal finance guide is based on rigorous reporting by our team of expert writers and editors with extensive knowledge of personal finance products. While CNBC Select earns a commission from affiliate partners on many offers and links, we create all our content without input from our commercial team or any outside third parties, and we pride ourselves on our journalistic standards and ethics.

Catch up on CNBC Select’s in-depth coverage of credit cards, banking and money, and follow us on TikTok, Facebook, Instagram and Twitter to stay up to date.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

Arizona’s largest airport, Phoenix Sky Harbor International Airport, is located about four miles from downtown Phoenix. A focus city for both American Airlines and Southwest Airlines, Phoenix Airport is the 10th busiest airport in the United States by aircraft movements.

If you have a trip to or from Phoenix Sky Harbor Airport in the near future, this guide, which includes information on how to get to the airport by public transport, terminal details and what lounges are available, is for you.

Phoenix Sky Harbor Airport quick facts

Airport code: PHX.

Address: 3400 E. Sky Harbor Blvd.

Number of runways: Three.

Number of terminals: Two — Terminal 3 and Terminal 4.

Transport between terminals: PHX Sky Train.

Daily flights served: 1,200.

Daily passenger count: 125,000.

Phoenix Airport map

For PHX Sky Harbor terminals and an interactive map, visit this page.

Airlines with service to Phoenix airport

Nearly two dozen airlines, both U.S.-based and international, operate flights to and from Phoenix Sky Harbor International Airport. Depending on the carrier you’re flying, you’ll be departing from one of the terminals below.

Terminal 3 airlines

Advanced Air.

Air Canada.

Alaska Airlines.

Allegiant Air.

Breeze Airways.

Contour Airlines.

Delta Air Lines.

Denver Air Connection.

Frontier Airlines.

Hawaiian Airlines.

JetBlue Airways.

Southern Airways Express.

Spirit Airlines.

Sun Country Airlines.

United Airlines.

Terminal 4 airlines

American Airlines.

British Airways.

Condor Airlines.

Southwest Airlines.

TSA PreCheck lines at Phoenix airport

Both terminals have TSA PreCheck lines, so if you’re a member of the Trusted Traveler Programs, you can use the following checkpoints to breeze through security:

Terminal 3

North checkpoint.

Terminal 4

Checkpoint A.

Checkpoint B.

Checkpoint C.

Checkpoint D.

Getting to and from Phoenix airport

Bus

Two bus lines serve Phoenix Airport: Route 13 and Route 44. Route 13 stops near the airport’s operations building, west of Terminal 3, and at 24th Street PHX Sky Train Station. Route 44 stops at the 44th Street PHX Sky Train Station.

Train

Take the free Sky Train to the 44th Street PHX Sky Train Station and head to the Valley Metro Rail platform. You can use the light rail to reach Phoenix, Tempe and Mesa.

Ride-hailing apps

Both Lyft and Uber operate in the Phoenix metro area, meaning you can request a ride to and from the airport.

Rental car companies at Phoenix airport

If you need to rent or drop off a vehicle, you can take the PHX Sky Train between the rental car center and the terminals.

The following car rental companies have offices at the car rental center at Phoenix Airport:

Phoenix airport car rental options

Enterprise.

NÜ Car Rentals.

Phoenix airport lounges

Terminal 3

Location: Near Gate F8.

Hours: 4:45 a.m. to 12 a.m.

Location: At the intersection of E and F gates, mezzanine level, next to Passage by Hudson.

Hours: 4:30 a.m. to 10 p.m.

Location: Near Gate E3.

Hours: 5 a.m. to 11:30 p.m.

Terminal 4

Location: Above Gates A7 and A9.

Hours: 6 a.m. to 11:30 p.m.

Location: Between Gates A19 and A21.

Hours: 4 a.m. to 8 p.m.

Admirals Club, Concourse B

Location: Above Gates B5 and B7.

Hours: 6 a.m. to 8 p.m.

Escape Lounge – The Centurion® Studio Partner

Location: Across from Gate B22.

Hours: 5 a.m. to 10 p.m.

Location: Across from Gate B22, on the upper level.

Hours: 6 a.m. to 9 p.m.

USO Lounge

Location: Level 2, East End, near B and C elevators (pre-security).

Hours: 7 a.m. to 3 p.m. Monday through Thursday and 7 a.m. to 7 p.m. Friday through Sunday.

Restaurants at Phoenix airport

If you don’t have lounge access, you can grab a bite at many restaurants available at Phoenix Sky Harbor International Airport. The eateries include national chains as well as some local establishments.

Terminal 3 restaurants

Ajo Al’s Mexican Cafe.

Giant Coffee.

Humble Torta & Taco.

Panera Bread.

Peet’s Coffee.

PHX Beer Co.

SanTan Brewing Company.

Shake Shack.

Starbucks.

The Roadie.

The Tavern.

Terminal 4 restaurants

Barrio Cafe.

Blanco Tacos & Tequila.

Cartel Roasting Co.

Chelsea’s Kitchen.

Cheuvront Restaurant & Wine Bar.

Cowboy Ciao.

Deluxburger Express.

Dilly’s Deli.

Dunkin’.

Fazoli’s.

Focaccia Fiorentina.

Four Peaks Brewing Company.

Humble Pie.

La Grande Orange.

La Madeleine.

Los Taquitos.

Matt’s Big Breakfast.

McDonald’s.

O.H.S.O. Brewery.

Olive & Ivy.

Panda Express.

Peet’s Coffee.

Pei Wei Asian Kitchen.

Sir Veza’s Taco Garage.

Starbucks.

Sweet Republic.

Tammie Coe To Go.

Wendy’s.

Wildflower Bread Company.

Zinburger.

Zinc Brasserie.

Shops at Phoenix Airport

A slew of retail shops is available for passengers looking for last-minute items in between flights. Among the traditional travel swag, you’ll also find some merchandise showcasing the spirit of the American Southwest.

Terminal 3 shops

Best Of The Valley Market.

Discover Arizona.

Indigenous Mosaic.

InMotion Entertainment.

Ironwood by Hudson.

Johnston & Murphy.

Passage by Hudson.

Phoenix Public Market.

Stellar News + Market.

Tech On The Go.

Travel Outfitters.

Terminal 4 shops

Arizona Highways.

AZCentral.com.

Brooks Brothers.

Bunky Boutique.

Cactus Candy.

CASA Airport.

CNBC 12 News.

Connections.

Earth Spirit.

Hudson News.

Indigenous.

InMotion Entertainment.

Johnston & Murphy.

Lucky Break.

Phoenix Duty Free

Roosevelt Row.

Sonora Southwest Living.

Sunglass Hut.

TripAdvisor.

Uno de 50.

Uptown Phoenix.

Frequently asked questions

Does Phoenix Airport have Clear lanes?

Yes, Terminal 3 and Terminal 4 both have Clear lanes for Clear Plus members and enrollment options for passengers interested in joining the program. North checkpoint as well as Checkpoints A, B, C and D all have Clear lanes.

What terminal is Southwest at PHX?

Southwest Airlines is located in Terminal 4 at Phoenix Sky Harbor Airport.

Where is the Delta terminal at Sky Harbor Airport?

Delta flights depart from Terminal 3 at Phoenix Sky Harbor Airport.

What terminal is United at Phoenix Airport?

The Sky Harbor United terminal is Terminal 3.

What airlines are based at Phoenix Airport?

American Airlines and Southwest Airlines have operational hubs at Phoenix Airport.

How do I reserve parking at PHX Sky Harbor?

It’s possible to reserve a long-term parking spot at Phoenix Airport. To make a reservation, select the date and time of your entry and exit from the lot, select the preferred parking facility, fill out your information and provide payment details.

You can make a parking reservation as early as six months and as late as two hours before departure. The maximum number of days available for parking pre-booking is 60.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

Our experts answer readers’ home-buying questions and write unbiased product reviews (here’s how we assess mortgages). In some cases, we receive a commission from our partners; however, our opinions are our own.

Buying a home is an exciting time that can fill you with a sense of accomplishment.

But you don’t want to get swept up in the excitement and jeopardize everything you worked for.

Take practical steps that can save you time, money, and effort down the road.

Loading

Something is loading.

mortgage down payment, closing costs, and moving expenses. Money will definitely be tight — and might be that way for a while — because your savings are depleted, and monthly expenses may also be higher, thanks to the new costs that come with homeownership, such as water, higher electric bills, and extra homeowner’s insurance.

Of course, I was ready to personalize my new home and upgrade temporary apartment furniture to something nicer, but my dad advised that I shouldn’t go on a massive spending spree to improve everything all at once. Just as important as getting my first home was staying in it, and as much as I wanted to immediately renovate the kitchen — I had already reached out to a contractor — it wasn’t worth jeopardizing my financial stability.

Give yourself time to adjust to homeownership’s expenses and rebuild your savings account — the kitchen will still be waiting for you when you can do more.

2. Don’t put off necessary maintenance

One of the new expenses that accompany homeownership is making repairs — there’s no landlord to call if your roof is leaking or your toilet is clogged. When I moved into my home, the windows needed replacing to the point that downstairs was ice-cold during the winter and the electric bill was over $500 a month. But since that wouldn’t be as aesthetically pleasing as renovating the kitchen or getting a glossy new bathroom, I wasn’t in a rush to do it. My dad let me know that I was costing myself money.

By not taking care of a necessary window replacement, I was paying a higher electric bill and inconveniencing myself every time I went downstairs wrapped in a blanket.

While you should exercise restraint in purchasing the nonessentials, you shouldn’t neglect any problem that could worsen over time. Delays can turn relatively small problems into much larger and costlier ones, and in a home, everything works together for better or for worse. Have a water leak? Now you have a higher water bill — and maybe water damage. Need new energy-efficient windows? You will pay a higher electric bill until you get them replaced.

3. Invest now so you only pay once

I will admit that I was in love with the bones of my home: the high ceilings, the staircase, the fireplace, the yard, and the location. But there were several serious elements of the house that needed replacing, and that was going to be expensive. The water heater, the furnace, the washer, and the dryer all needed replacing, not to mention smaller items such as ceiling fans and window treatments.

So of course, when getting estimates, in the beginning, I would gravitate toward the cheapest option. My dad said, “There is no reason to buy the cheapest version and be right back here in two years. Invest now so you only have to pay once.” After that I always asked for three options and landed on the middle number.

You may not need the most expensive option with the name brand and all the extra bells and whistles, but the cheapest option is typically cheap for a reason and could cost you more money down the road.

Jennifer Streaks

Senior Personal Finance Reporter and Spokesperson

Jennifer is a Senior Personal Finance Reporter and Spokesperson for the Personal Finance vertical at Business Insider. She started her career covering personal finance at Black Enterprise Magazine, went on to CNBC where she covered personal finance, women and money and tech and then Forbes, where she reported on personal finance, business, tech and money matters related to the economy, investing, credit and entrepreneurship. Jennifer is also the author of Thrive!…Affordably: Your Month to Month Guide to living your Best Life without breaking the bank. The book offers advice, tips and financial management lessons geared towards helping the reader highlight strengths, identify missteps and take control of their finances. In addition, she has extensive experience as an on-air financial commentator and has been a featured expert discussing credit and savings, investing and retirement, mortgages and all things money and personal finance. She has an ability to discuss and simplify complex financial issues and make them easier to understand.

No one can predict the future of real estate, but you can prepare. Find out what to prepare for and pick up the tools you’ll need at Virtual Inman Connect on Nov. 1-2, 2023. And don’t miss Inman Connect New York on Jan. 23-25, 2024, where AI, capital and more will be center stage. Bet big on the future and join us at Connect.

Economists are scratching their heads and housing industry leaders are venting their frustrations as mortgage rates continue a relentless climb to new heights not seen in more than two decades, chasing yields on government debt that are being pushed higher by factors beyond Federal Reserve tightening.

The Optimal Blue Mortgage Market Indices, which track daily rate lock data, show rates on 30-year fixed-rate conforming loans hitting a new 2023 high of 7.59 percent Tuesday — an all-time high in Optimal Blue records dating to 2017.

At 7.95 percent, rates on jumbo mortgages that exceed Fannie Mae and Freddie Mac’s loan limits looked poised to push through the 8 percent benchmark, as paper losses mount at banks that fund most jumbo lending and Treasury yields rise.

National Association of Realtors Chief Economist Lawrence Yun vented his frustration with Fed policymakers, who have telegraphed their intention to implement at least one more rate hike this year.

“The Fed is overdoing the rate hike,” Yun said in a LinkedIn post Wednesday. “The economy is measurably slowing. Even the lagging indicator job gains are coming in light.”

Yun said he’s worried that rising interest rates could actually fuel inflation as would-be homebuyers throw in the towel, fueling more demand for rentals, and making housing more scarce as builders balk at paying higher rates on construction loans.

A weekly survey of lenders by the Mortgage Bankers Association (MBA) showed that applications for purchase loans were down a seasonally adjusted 6 percent last week when compared to the week before, and 22 percent from a year ago.

Joel Kan

“The purchase market slowed to the lowest level of activity since 1995, as the rapid rise in rates pushed an increasing number of potential homebuyers out of the market,” MBA Deputy Chief Economist Joel Kan said in a statement.

With rates on 30-year fixed-rate conventional loans rising for the fourth consecutive week to the highest rate since 2000, Kan said some borrowers searching for ways to lower their monthly payments are turning to adjustable-rate mortgage (ARM) loans.

Although ARM loans accounted for 8 percent of mortgage applications last week, they had an even bigger share when mortgage rates made a similar surge last fall. During the second week of October 2022, ARM loans accounted for 13 percent of applications, the highest share since March 2008.

Appearing on CNBC’s “Squawk Box,” Yun noted that rates on ARM loans aren’t much lower than those for more traditional 30-year fixed-rate conventional loans (according to the MBA survey, rates on ARM loans averaged 6.49 percent last week). “My advice right now is go into the 30-year fixed, because even with that, one can always refinance once the interest rate goes down,” Yun said. “The mortgage rates are topping out now — hopefully there is some downward drift in the upcoming months.”

MBA CEO Bob Broeksmit expressed similar sentiments on CNBC Wednesday, urging the Fed to “be clear that they’re done with rate increases” and to also “make clear that they’re not going to sell mortgage-backed securities off their balance sheets.”

Jumbo mortgage rates spike

Homebuyers seeking jumbo mortgages exceeding Fannie and Freddie’s conforming loan limits — $726,200 for one-unit properties in most areas of the country — have been hit particularly hard by recent rate increases.

At this time last year, rates on jumbo mortgages were about half a percentage point less than for conforming loans. Now the situation has reversed, with the “spread” between jumbo mortgages and conforming loans widening to nearly 40 basis points on Wednesday, according to Optimal Blue rate lock data.

Conforming loans are largely financed by investors who buy mortgage-backed securities guaranteed by Fannie and Freddie. But jumbo mortgages are mostly provided by banks that hold the loans on their books. Stresses on regional banks sparked by the failures of Silicon Valley Bank, Signature Bank and First Republic Bank have made jumbo loans more expensive and harder to come by this year.

This week, Rocket Mortgage began offering some relief by pricing mortgages of up to $750,000 as conforming, in anticipation that Fannie and Freddie’s 2024 loan limits will go up by at least 3 percent on Jan. 1 to reflect home price appreciation over the last year.

Mike Fawaz

“The market has changed a lot, and jumbo pricing isn’t as favorable as it used to be,” Mike Fawaz, executive vice president of Rocket’s wholesale channel, Rocket Pro TPO, told Inman.

Banks that have large holdings of Treasurys are seeing the value of those assets decline as interest rates rise, helping push unrealized losses on bank balance sheets up by 8.3 percent during the second quarter, to $558.4 billion, according to the Federal Deposit Insurance Corp.

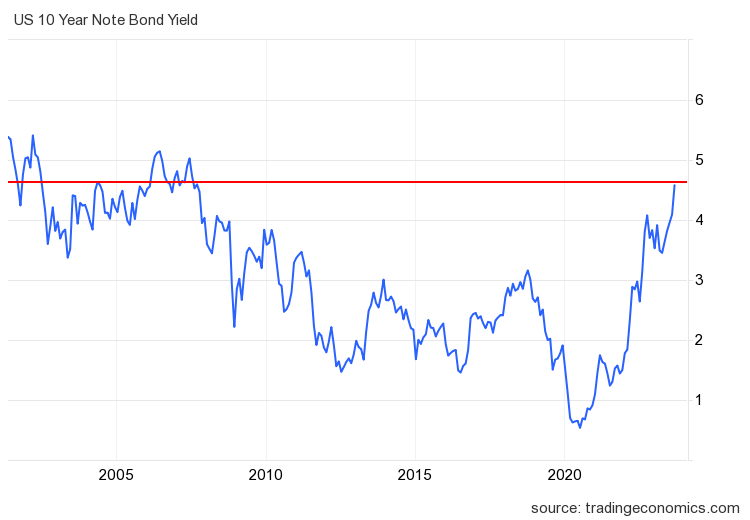

10-year Treasury yields at highest since 2007

Yields on 10-year Treasury notes, a barometer for mortgage rates, surged to a new 2023 high of 4.80 percent Tuesday, a level not seen since August 2007 on the eve of the subprime mortgage crisis.

While the Fed has tight control over short-term interest rates, rates on long-term assets like Treasurys and mortgage-backed securities (MBS) that fund most home loans are dependent on investor demand. When investors are eager to put their money in bonds and MBS, that pushes rates down. But when investors lose their appetite for those assets, that drives rates up.

The recent surge in long-term Treasury yields has defied many forecasters’ expectations, and economists are searching for reasons.

Last year’s rise in long-term rates was driven “by market expectations of higher short-term rates as the Fed tightened policy and by investors’ demands for extra compensation to hold longer-dated assets because of fears of higher inflation,” The Wall Street Journal’s Nick Timiraos reported Wednesday.

With inflation seemingly cooling and the Fed signaling that it’s done, or will soon be done, raising short-term rates, economists suspect flagging demand for Treasurys by foreign investors, U.S. banks and investment managers could be factors in the sustained rise in long-term rates, Timiraos reported.

Even if long-term rates have peaked, there’s increasing uncertainty over whether they’ll come down next year, as many economists and investors had been anticipating.

“What we’re seeing is a reappraisal of how the bond market prices uncertainty itself,” PGIM Fixed Income economist Daleep Singh told Timiraos. “The compensation required to underwrite potentially the new structural regime with more volatile growth and inflation and fewer predictable sources of demand to absorb record amounts of government debt issuance has clearly risen.”

Another factor crimping demand is that the Fed, which bought trillions of Treasurys bonds and MBS during the pandemic to bring borrowing costs to historic lows, is now letting those investments roll off its books.

Fed has trimmed $1 trillion from balance sheet

Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis

The Fed’s Treasury and MBS holdings peaked at $8.5 trillion last year, but a shift to “quantitative tightening” has allowed the central bank to trim its assets by more than $1 trillion by allowing $60 billion in maturing Treasurys and $35 billion in MBS to roll off its books each month.

Broeksmit said that the spread between 10-year Treasury yields and 30-year fixed-rate mortgages is about 125 basis points higher than its historic norm and that the Fed is partly responsible.

“I still think some of the increase in the spread between the Treasury and the mortgages is a fear that the Fed would actually sell [MBS] in the open market,” Broeksmit said on CNBC. “So if they were to make clear that that’s not on the horizon, I think that that would help and the bank demand will, I think, come back. We’ve seen some increase in supply with some of the failed banks MBS being on the market, but I think that’s mostly been resolved.”

Where rates are headed next

Futures markets tracked by the CME FedWatch Tool put the probability of one or more additional Fed rate hikes this year at 37 percent, but see a one-in-five chance (19.6 percent) that the Fed will bring rates back down below current levels by March before the spring homebuying season kicks off.

The upcoming Nonfarm Payrolls report to be released Friday by the U.S. Bureau of Labor Statistics is likely to play a factor in determining where rates are headed next, as Fed policymakers see tightness in the labor market as a key driver of inflation.

Tuesday’s release of the Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey (JOLTS) report seemed to panic bond market investors, sending yields on 10-year Treasurys up 12 basis points.

The JOLTS data, which showed job openings increased by 690,000 at the end of August, to 9.6 million, “was startling, but the data are very noisy and are subject to large revisions,” Pantheon Macroeconomics analysts said in their U.S. Economic Monitor report Wednesday.

“We don’t take JOLTS seriously, but the surge in yields and plunge in stock prices after the release of the data yesterday says a great deal about the pervasive nervousness of investors,” Pantheon economists Ian Shepherdson and Kieran Clancy wrote.

Bond market investors “appear to be taking seriously the Fed’s collective assertion that rates will stay higher for longer, despite the abundant evidence that the Fed’s interest rate forecasts are rarely correct,” they said.

‘Dot plot’ reflects Fed’s ‘higher for longer’ rate strategy

Fed policymakers voted unanimously on Sept. 20 to keep the central bank’s target for the short-term federal funds rate at 5.25 to 5.5 percent.

But looking at the Federal Open Market Committee’s latest “dot plot” — projections of where policymakers think the short-term federal funds rate will be in the future — most see the need for one more rate hike this year. By the end of next year, however, some think it will be as low as 4.375 percent or as high as 6.125 percent (hawkish Federal Reserve Governor Michelle Bowman could be the outlier on the high end).

That is an “enormous” spread of 1.75 percentage points, Shepherdson and Clancy wrote, “but markets for now are interested only in the upside risks.”

Betting that Treasury yields have peaked “seems extraordinarily risky,” the Pantheon economists concluded. “But unless you think the U.S. economy can grow at a real 2 1⁄2 percent pace forever, untroubled by the Fed, 10-year yields can’t be sustained at the current level. The market won’t flip, though, until the data shift, and Fed officials acknowledge the change.”

In the meantime, Pantheon economists say, “yields could overshoot further.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

One of my concerns with higher rates has been whether new listings data would take another leg lower, which wouldn’t be a good thing for the housing market. Not only has that not happened, but we have had an orderly seasonal decline this year — outside some wild swings around Labor Day and schools starting.

This proves that we are trying to form a historical bottom in this data line, something I discussed earlier in the year on CNBC. As we can see in the chart below, it is very steady, considering how crazy rates have been lately.

One of the things I have gotten wrong in 2023 is my premise that if mortgage rates rose, the inventory growth would pick up for a few weeks, at least between 11,000-17,000. However, even with 8% mortgage rates last week, I am still batting a zero in 2023 as inventory growth last week was just 7,900.

Last year, the seasonal peak for inventory was Oct. 28. Last week, according to Altos Research:

Weekly inventory change (Oct. 13-Oct. 20): Inventory rose from 546,450 to 554,350

Same week last year (Oct. 14-Oct. 21): Inventory rose from 567,452 to 571,944

The inventory bottom for 2022 was 240,194

The inventory peak for 2023 so far is 554,350

For context, active listings for this week in 2015 were 1,171,430

Traditionally, one-third of all homes have price cuts all year long. When rates rise and demand gets weaker, the price cut percentage can grow. The price cut percentage in 2023 is still 4% below what we had in 2022, even with higher home prices and mortgage rates. Price cut percentages in recent years:

2023 38.5%

2022 42.5%

2021 28%

Mortgage rates and the 10-year yield

The bond market and mortgage rates have had such a wild ride recently, and it reminds me of the action during the first week of COVID-19 when we saw massive volume in buying treasuries. In the same vein, the bond market is now very oversold. However, more importantly, real yields are very restrictive for the economy now. In the last week, the 10-year yield went from 4.62% to 4.99%, ending at 4.92%.

I recently discussed on the HousingWire Daily podcast whether these rates are recessionary because the history of real yields being this restrictive has always led to a recession. Earlier in the year on CNBC I said that the Fed wouldn’t be satisfied until the labor market breaks. Even though the Fed has talked about no more rate hikes, now that the 10-year yield and mortgage rates are higher, they believe the monetary policy is restrictive enough to accomplish the goal they always wanted from the start: attack the labor supply.

Mortgage rates went from 7.66% to 8.03% last week to end at 7.97%. If the Fed wants to create a job-loss recession, attacking the housing market a second time looks like their target. They remain frustrated that the labor market is not breaking.

Purchase application data

Purchase application data was down 6% last week versus the previous week, making the year-to-date count 18 positive prints, 21 negative prints and one flat week. If we start from Nov. 9, 2022, it’s been 25 positive prints versus 21 negative prints and one flat week.

Of course, higher rates have made affordability worse; whenever rates move up or down by just one 1%, millions of potential homebuyers are qualified or not qualified to buy a home.

The week ahead: Home sales data and jobless claims

Next week, we have new home sales and pending home sales — which are at significant risk of a big miss. Jobless claims, of course, come out every Thursday and that has been the key data line for me at this expansion stage. Also, there are many variables worldwide, and who knows what the Fed will say. We will be tracking all the live data to keep you updated.

A contractor works on a new home under construction in Tucson, Arizona, on Tuesday, Feb. 22, 2022.

Rebecca Noble | Bloomberg | Getty Images

Builder confidence in the market for single-family homes dropped to the lowest level since January, as builders contend with a market dominated by high mortgage rates and costs for financing.

The monthly National Association of Home Builders/Wells Fargo Housing Market Index dropped 4 points to 40 in October, and September’s read was revised down 1 point. Anything below 50 is considered negative. This marks the third straight monthly decline in builder confidence.

Builders point squarely to mortgage rates, which are now at a 23-year high. The average rate on the popular 30-year fixed mortgage has remained over 7% for two months. Affordability has fallen to near record lows.

“Builders have reported lower levels of buyer traffic, as some buyers, particularly younger ones, are priced out of the market because of higher interest rates,” said Alicia Huey, NAHB’s chairman and a homebuilder and developer from Birmingham, Alabama. “Higher rates are also increasing the cost and availability of builder development and construction loans, which harms supply and contributes to lower housing affordability.”

Of the index’s three components, current sales conditions fell 4 points to 46, sales expectations in the next six months dropped 5 points to 44, and buyer traffic dropped 4 points to 26.

In order to get buyers in the door, builders are using more incentives again. This includes buying down mortgage interest rates. About 62% of builders reported offering sales incentives of all forms in October, up from 59% in September and tied with the previous high for this cycle set in December 2022.

In addition, 32% of builders said they cut home prices. That is unchanged from the previous month but still the highest rate since December (35%). The average price discount is steady at 6%.

“The housing affordability crisis can only be solved by adding additional attainable, affordable supply,” said Robert Dietz, NAHB’s chief economist. “Boosting housing production would help reduce the shelter inflation component that was responsible for more than half of the overall Consumer Price Index increase in September and aid the Fed’s mission to bring inflation back down to 2%. However, uncertainty regarding monetary policy is contributing to affordability challenges in the market.”

Regionally, on a three-month moving average, builder sentiment in the Northeast fell 4 points to 50 and in the Midwest dropped 3 points to 39. In the South it fell 5 points to 49, and in the West it fell 6 points to 41.

Online banking has made managing money easier than ever. However, it has also led most people to rely solely on digital assets.

Precious metals are a popular investment choice for people wishing to buy a tangible asset that retains its value over time. In particular, gold and silver generally maintain their value even when the stock market faces major financial fluctuations.

They also do well in times of inflation and political uncertainties. When traditional stocks fluctuate due to these external factors, precious metals only become more valuable.

Investors who prefer a hands-off approach have the option of purchasing gold and silver stocks. These stocks are traded daily just like any other stock. However, many people prefer to keep a physical store of their precious metal.

While relatively illiquid, buying physical gold and silver is typically viewed as a long-term investment. It’s certainly a practical option if you’re concerned about inflation or the future of fiat currency.

Best Places to Buy Gold and Silver Online

eBay and Craigslist are both great places to start. But unless you’re confident that you’re dealing with a reputable seller, you might want to look into other sites that specialize in precious metals.

To help you find the best place to buy gold and silver, we’ve compiled a list of the best online gold dealers.

Money Metals Exchange

Money Metals Exchange, or MoneyMetals.com, has received several accolades, including the “Best Overall Gold Dealer” by Investopedia.

They’ve also done over $2 billion in transactions.

Money Metals Exchange has an A+ rating from the BBB. They offer 24/7 online support, indicating a strong commitment to customer service.

Products include gold, silver, rhodium, palladium, and platinum. You can also invest in a self-directed precious metals IRA.

You can often find great deals and promotions on Money Metals Exchange, so it’s a site you may want to bookmark.

Silver Gold Bull

Silver Gold Bull offers a suite of services for their customers. In addition to buying and selling through the company’s website, you can also store your hard assets in their secure facilities.

Another helpful feature is an automated spot alert. You can get up-to-the-minute data on where prices are throughout the day and buy when they hit your target price.

Plus, the Silver Gold Bull sales team is full of seasoned veterans, so you can get answers to your questions from people who truly know their stuff.

The company sells a wide range of gold, silver, platinum, palladium, copper, and collectibles online and over the phone.

Gainesville Coins

With an A+ rating from the Better Business Bureau, Gainesville Coins has been keeping customers happy for more than ten years.

In fact, the company has also received a five-star rating from the National Inflation Association—the only bullion dealer to receive such a distinction.

You’ll find a wide selection of gold, silver, platinum, and other metals like copper, palladium, and rhodium on the Gainesville Coins website.

The company also sells pre-1933 gold and has an extensive clearance section with time-sensitive deals. In addition, you can calculate shipping based on your zip code and items placed in your cart. Only Florida residents pay sales tax on their purchases.

Gainesville is one of the best places to buy gold online.

Golden State Mint

Golden State Mint is a trusted source for premium precious metal products, providing buyers direct access to top-notch items straight from the manufacturer.

With 40+ years of experience, the company inspects each piece with precision before shipment, ensuring its authenticity and quality.

Customers can rest assured that all products are brand-new, never previously owned or circulated.

Investing in precious metals for retirement? Golden State Mint offers expert support in establishing an IRA account, stocked with an array of products that fully comply with IRS standards.

Whether you’re a seasoned pro or just starting out, Golden State Mint is committed to helping you achieve your investment objectives through purchasing physical gold and silver.

Provident Metals

What started as a precious metals trade show business has launched into one of today’s largest online bullion dealers.

Provident Metals holds several professional memberships. These include the American Numismatic Association, the Professional Coin Grading Service, and the Numismatic Guaranty Corporation.

Provident’s collections include gold, silver, copper, platinum, and palladium, with an extensive selection of each one. In addition to coins, rounds, and bullion bars, Provident Metals also sells U.S. and foreign coins, wholesale products, and IRA bullion products.

You’ll appreciate the company’s attentive service and timely delivery. And if you order $99 or more, shipping is free; otherwise, it costs just $5.95 to ship.

APMEX (American Precious Metals Exchange)

APMEX is one of the largest online dealers in the world, which allows it to pass along savings to its customers. This is due to the sheer volume of business it does each day. Not only can you buy silver, gold, and other metals, you can also sell or trade from your current holdings.

The selection is huge, covering the major precious metals, historic gold coins, “elite” coins, old banknotes, and foreign coins. It also has an extensive collectibles section with rare coins and currency from around the world.

Scottsdale Mint

Scottsdale Mint (formerly Scottsdale Silver) focuses on silver and gold while also offering each in different collectible series. They sell both types of metal in coins, bullion bars, and rounds, with a particular premium set on artistic minting.

For example, some recent popular collectible sets include a Vikings series and a Godfather set featuring images from the iconic movie franchise.

To qualify for free shipping with insurance, you must make a minimum purchase of $500. This may seem steep compared to some other companies providing free shipping at $99. However, much of the allure of Scottsdale Mint comes from the company’s creative minting process.

JM Bullion

Shipping is free on all JM Bullion orders over $199. They sell physical gold, silver, platinum, and other bullion that arrive directly at your door. They inspect every inventory item to ensure only quality products are sold. Payment options include Visa, MasterCard, PayPal, PayPal Credit, bank wires, paper checks, and Bitcoin.

JM Bullion is fully accredited at both state and federal levels. They also have reliable customer service that you can reach via phone or 24-hour Live Chat. Sign up for email, and they will mail you exclusive sales and promotions.

Kitco

Kitco has many precious metal types, including gold, silver, palladium, platinum, and rhodium.

The website also provides a slew of data and news to help you with your portfolio decisions. You can even download apps for gold news, market alerts, and scrap value calculations for your smartphone.

GoldSilver.com

As its name implies, GoldSilver solely sells gold bars, coins, and jewelry and silver bars and coins. They also sell products such as safes and storage containers. You can also create an account to sell back your gold bullion, gold coins, and silver bars through the website.

There’s a flat rate shipping fee of $25 for any order under $500. Otherwise, shipping, handling, and insurance are free. In addition to traditional payment options, GoldSilver also accepts PayPal.

Silver.com

Don’t be fooled by the name. While Silver.com could be the best place to buy silver online, they also sell various gold, platinum, and copper products. In addition to government mints, you can also find gold coins, gold bullion, silver coins, silver bars, and more from private domestic and foreign mints.

The order threshold for free shipping is high at $3,000, but their tiered flat rate shipping fees are reasonable. Smaller orders up to $299 cost just $4.95 for shipping and insurance. The highest tier of orders from $1,000 to $2,999 cost just $9.95.

SD Bullion

Silver, gold, platinum, and copper comprise SD Bullion’s core product line, with coins, bars, and rounds from around the world.

They also sell lead bullion in the form of ammo as well as vaults, survival food, and herbal medicine. In addition, SD Bullion offers weekly specials and currently has a promotion for all orders shipped at just $7.77.

Texas Precious Metals

Texas Precious Metals offers several unique features, including the ability to sign up for limit orders. For example, you can automatically place a standing order if gold or silver reaches your desired value.

All orders ship for free using UPS Next Day Air, and all orders ship within three business days of payment. The website offers a curated selection of gold coins, gold bars, silver coins, silver bars, and pre-1933 gold.

Golden Eagle Coins

Golden Eagle Coins is a place for gold and silver investors and collectors alike. Take one look at their website, and you’ll see why — their inventory is enormous.

Prices are updated in real time as their quotes come directly from the commodities exchange. This is a great site to use if you are researching when to buy.

Shipping is free on orders $99 and over. Also, be sure to check out their bi-monthly blog for new items and savings.

Gold Dealer

Quoted on CNN, CNBC, and PBS, Gold Dealer offers a complimentary newsletter written by industry masterminds Ken Edwards and Richard Schwary.

They have a physical office moments away from LAX. However, if you don’t want to travel to Los Angeles, you can visit website instead. It has everything you’d expect from a reputable gold dealer.

Gold Dealer offers free, insured shipping on every order. Their low prices are the result of reducing operating expenses over time.

Monarch Precious Metals

Monarch Precious Metals is a newer company established in 2008 to help with the immense public demand for gold bullion. They only use quality metals, so anything you buy from them will be .999+ fine.

They triple-check the weight of every bar they ship. If it is ever underweight, they re-melt it. If it’s ever overweight, it’s a win-win for you because they always let it pass and ship it as is.

Everything is custom hand-poured and marked in the old way, giving their metals a unique, old-fashioned look. They accept all methods of payment except PayPal, and every order is properly insured.

CMI: Gold & Silver

An A+ Accredited Business, CMI is located in Phoenix, Arizona. However, CMI will buy and sell precious metals online to investors all over the United States.

Its president, Bill Haynes, considers it his responsibility to educate the public about the dangers and benefits of buying gold and silver products.

He regularly updates his blog on global factors that influence the prices of metals. It’s a helpful resource for determining when to buy.

With solid prices, IRAs, and a plethora of educational material to read, CMI should be a website you routinely check if you are a serious investor.

BGASC: Buy Gold and Silver Coins

With thousands of positive customer reviews, it’s not hard to realize why BGASC is an A+ BBB accredited business. They offer free shipping on orders $99 and up. Every order is insured while in transit. Additionally, they always ship your order the next business day.

BGASC is one of the largest coin and bullion dealers in the US. They sell nearly every type of US coin ever made. They also have a large selection of mints from other countries, such as China, Mexico, and Canada.

The Basics of Precious Metals

Before buying gold or silver, it’s important to understand the different forms they come in. Each type has its pros and cons. Some people focus on one kind they prefer, while others create a diverse mix of different kinds. Before you buy precious metals, figure out which strategy is best for you.

Silver

Let’s start by talking about silver. Typically, you can buy silver either in the form of bullion or junk silver. Silver bullion refers to silver as a bar, coin, ingot, or round.

Silver Coins

The most popular silver coins you’ll come across are as follows:

American Silver Eagle

Canadian Silver Maple Leaf

British Silver Britannia

Mexican Silver Libertad

Austrian Silver Philharmonic

South African Silver Krugerrand

Australian Silver Kangaroo

Chinese Silver Panda

Junk Silver

Junk silver, on the other hand, is any type of old U.S. currency containing real silver. Any U.S. half-quarters, quarters, or dimes minted before 1965 are considered junk silver. However, in reality, they aren’t very junky at all.

You can sometimes find junk silver below the spot price. This can often allow you to start with a profit on your investment.

Silver Rounds

Silver rounds are privately minted silver pieces shaped like coins but produced by private mints. They are not government minted or legal tender, so they are not referred to as coins. The most popular silver round is the American Silver Buffalo. However, Scottsdale Mint also produces some beautiful rounds called “Omnia.”

Gold

Gold also comes in bars and coins, each one giving you a different type of entry point into precious metal investing. Buying gold coins is the easiest way for gold investors to start because you can begin by just purchasing a few at a low price point.

Gold Coins

The most popular gold coins to buy are as follows:

American Gold Eagle

Canadian Gold Maple Leaf

British Gold Britannia

British Gold Queen’s Beast

Mexican Gold Libertad

Austrian Gold Philharmonic

South African Gold Krugerrand

Australian Gold Kangaroo

Chinese Gold Panda

Gold Rounds

Similar to silver rounds, the most popular is the American Gold Buffalo.

Perhaps you’re stocking up as a hedge against inflation or to use as currency in a potential crisis. If so, you’ll find that coins of any type (gold or silver) will be easier to barter with than bars.

If you decide to buy bars, you can get them in different sizes to suit your space or budget. For example, you can purchase 1 to 10-ounce gold bars or up to 100-ounce silver bars. You can even find bars at just a fraction of an ounce if you want to start small.

One of the most significant advantages of this tactic is that you get the lowest premium when you buy larger bars. So while they might not be as easy to sell when you’re ready, you’ll get a better value if you can make that large of an investment upfront.

Copper

While silver and gold are the most popular, there are other precious metals to consider as well. For example, copper also comes in bars, rounds, and coins and is very affordable for novice investors.

Some experts believe it’s a wise investment opportunity because of its rising demand and shrinking supply.

Platinum and Palladium

Platinum is perhaps the most precious of all metals. It’s 15x rarer than gold, and its value exceeds that of gold. Platinum is usually sold as coins minted in the U.S., Canada, or Australia.

Palladium is similar to platinum in its properties and is actually 30x rarer than gold. Because these metals are so rare, not many people invest in them. However, a growing number of investors are adding them to their portfolios. It’s something you may want to consider as well.

Gold and Silver: Frequently Asked Questions

Where is the best place to buy gold?

The two best places to buy gold are online retailers and local coin shops.

Online retailers, such as the ones we’ve listed above, offer a wide selection of gold coins, bars, and rounds at competitive prices. These retailers often offer free shipping and insurance, making it easy and convenient to buy gold from the comfort of your own home.

Local coin shops are another great option if you want to prefer gold in person. These shops often have a knowledgeable staff who can help you find the right gold products for your needs and budget. You may also be able to negotiate on price of the gold.

Where is the best place to buy silver?

The best place to buy silver is typically also the best place to buy gold: online dealers and local shops. These options provide a wide range of products to choose from and allow you to compare prices and quality before making a purchase.

Online dealers offer the convenience of shopping from home, while local shops provide the advantage of in-person interaction with knowledgeable staff who can answer your questions and guide you towards the right products for your investment goals.

Whether you want to buy silver coins or silver bars, these options typically offer competitive prices, flexible shipping policies, and convenient payment options.

We recommend checking out at least a few of the best online gold dealers we mentioned above, regardless of what your needs are. Compare prices, selection, and shipping policies on numerous sites.

What is the cheapest way to buy gold and silver?

The most cost-effective method of acquiring gold and silver is by buying bars. They tend to have smaller markups compared to spot prices compared to coins, due to their lower production costs.

Buying in bulk is also a smart way to lower the cost per ounce as many online dealers offer discounts for larger purchases.

Is it safe to buy gold and silver online?

Buying precious metals online is as safe as any other transaction you make online. It’s also just as safe to buy online is as it is to buy from a physical retailer. The key is to buy gold and silver from a reputable gold dealer.

Is it better to buy gold coins or bars?

There is no right or wrong answer to this question. It depends on your situation, your needs, your budget, and what you prefer. As mentioned, it’s typically cheaper to buy gold bars. However, you will most likely get a better value from gold coins when it comes time to sell your gold.

Gold and silver coins and small bars offer more flexibility when it comes time to sell. Owning smaller units of gold and silver allows you to sell only a portion of your precious metals instead of your whole portfolio.

How much gold and silver should I own?

Experts recommend holding 5-25% of your net worth in precious metals. However, it depends on your goals, your situation, and risk tolerance. Precious metals can be a great addition to your portfolio as long as you know why you’re adding it.

Can I store gold at home?

Storing gold in your home offers a sense of security and privacy for your valuable assets. As a form of wealth preservation, it provides complete control without the need for outside storage. However, it’s crucial to be mindful of potential security threats and to ensure your assets are adequately insured.

To mitigate these risks, it’s advisable to implement a secure storage system. Ultimately, home storage is a viable solution for individuals who value personal ownership and control of their gold holdings.

Ryan Ratliff, center, real estate sales associate with Re/Max Advance Realty, shows Ryan Paredes, left, and Ariadna Paredes a home for sale in Cutler Bay, Florida, on April 20, 2023.

Joe Raedle | Getty Images

The average rate on the popular 30-year fixed mortgage rose to 7.72% on Tuesday, according to Mortgage News Daily.

Mortgage rates follow loosely the yield on the 10-year Treasury, which has been climbing this week following strong economic data. Rates have not been this high since the end of 2000.

At the beginning of this year, the 30-year fixed rate dropped to about 6%, causing a brief burst of activity in the spring housing market. But it began rising steadily again over the summer, causing sales to drop, despite strong demand. The current trend appears to be even higher, with the possibility of rates crossing over 8%.

The Federal Reserve did not raise interest rates two weeks ago but indicated the possibility of another hike this year and fewer cuts than expected next year. Investors were waiting to see the results of economic data in the first week of October.

“It is now the first week of October, and data has been stronger,” wrote Matthew Graham, chief operating officer at Mortgage News Daily. “This morning’s JOLTS (job openings and labor turnover survey) is the biggest, baddest confirmation so far this week, and it’s pushing yields to fresh long-term highs. Pretty simple stuff, actually, even if unpleasant and unfortunate for fans of low rates.”

Higher rates have crushed affordability, hitting both the new and existing home sales markets. While builders had been benefiting from the tight supply of existing homes for sale, higher mortgage rates are a major concern now. Builder sentiment slipped into negative territory in September for the first time in five months.

To put rates in perspective, for a borrower purchasing a $400,000 home with a 20% down payment on a 30-year fixed loan, the monthly payment today is about $930 more than it was when rates were at 3% during the height of the Covid-19 pandemic.

This statement from the Fed is classic Fed at work.

The Fed has not helped its own cause here, as Austan Goolsbee, president and CEO of the Federal Reserve Bank of Chicago, said in a speech last week: “I’m still trying to process why long-end interest rates are increasing.”

My answer: “Stop talking about raising rate at this stage with a hawkish outlook!”

The Fed has expressed that real yields, meaning where inflation is currently and where rates are, are restrictive to the economy, so sounding hawkish on monetary policy at this stage can lead the bond market to go higher more than the Fed would like. Land the plane, folks, land the plane!

As you can see in the chart below, it was another wild week in the bond market. Mortgage rates went from 7.39% to a high of 7.65% and ended the week at 7.44%. Before last week the high for mortgage rates this year was 7.49%.

The bond market has been volatile, but after the 10-year yield broke the 4.34% level, I am watching for the 4.63% level. A close above that and follow-through bond market selling could lead to higher mortgage rates. Hopefully, the last two weeks caught the Fed’s attention. If they cared about a soft landing, which I have been skeptical about from the start, as I talked about here on CNBC, the Fed would be more mindful of what they say and do.

Weekly housing inventory data

One of the things I got wrong this year is that I believed if mortgage rates stayed higher for longer, active inventory would grow between 11,000 and 17,000 for at least some of the weeks; that hasn’t happened recently with higher rates — close but no cigar. T

Last week, the growth of active listings slowed to 6,808. Seasonality is kicking in now, but we should be able to continue growing housing inventory like we did last year, as higher rates slow sales down, keeping homes on the market longer.

Last year, the seasonal peak was Oct. 28. Last week, according to Altos Research:

Weekly inventory change (Sept.22-29): Inventory rose from 527,938 to 534,746

Same week last year (Sept. 23-30): Inventory rose from 556,865 to 561,229

The inventory bottom for 2022 was 240,194

The inventory peak for 2023 so far is 534,746

For context, active listings for this week in 2015 were 1,187,2000

After some volatile weeks with the new listings data, things look similar to earlier in the year when we had an orderly seasonal decline in new listings data, which has been trending at the lowest levels ever for over 13 months. Even with rates spiking, the new listing data hasn’t created another new leg lower. This is important, as I expect flat to slightly positive data soon due to a shallow bar.

Historically, one-third of all homes have price cuts every year. Last week’s price cuts were lower than last year at the same time by 4%. This is happening even with rates over 7% and part of the reason is that housing inventory has been negative year over year since mid-June. As mortgage rates move higher, the percentage of price cuts can grow but it’s trailing last year’s percentage as home sales aren’t crashing like they did last year.

Price cuts for last week over the years:

2021: 29%

2022: 42%

2023: 38%

Purchase application data

Purchase application data was 2% lower last week versus the previous week, making the year-to-date count 17 positive prints, 19 negative prints, and one flat week. If we start from Nov. 9, 2022, it’s been 24 positive prints versus 19 negative prints and one flat week. The week-to-week data has gotten softer since mortgage rates have been trending above 7%. However, it’s not crashing like last year because we are working from a lower bar.

The week ahead: It’s jobs week! (If the government is open)

If we don’t have a government shutdown, the week ahead will be jobs week again! The Fed was happy about labor data last month as job openings have been falling, and the job growth data is cooling down. However, jobless claims are still going strong, so they have more work to do in attacking the labor supply. In addition to jobless claims, this week we will also have job openings, the ADP jobs report, and the BLS Jobs Friday report, which could move the bond market this week.

Also, I will watch this week to see if more Fed members comment about rising long-term rates. The Fed would like to keep rates higher for longer, but if the bond market gets a whiff of any terrible recession data, it will take yields down. So far, jobless claims data hasn’t given them any reason to do so.

But here’s the big takeaway: That money is yours, and those savings stay with you whenever you quit a job.

If you have less than $1,000 in your 401(k)

If your 401(k) has less than $1,000 when you quit a job, the IRS allows the plan administrator to automatically withdraw your money and send you a check, minus 20% in taxes, per the IRS.

You can also initiate a rollover: a direct transfer of your money from a 401(k) account to another tax-advantaged retirement account. (More on rollover deadlines and tax implications later.) The easiest way to roll over your money is to contact your 401(k) administrator and have them handle it.

Communicate your preferences quickly, though — if your 401(k) account has a low balance, most companies won’t delay closing the account and cutting you a check, according to CNBC.

If you have between $1,000 and $5,000 in your 401(k)

If your 401(k) has between $1,000 and $5,000 when you quit, your employer may move your money into an individual retirement account, or IRA, according to the IRS.

If you don’t have an IRA, some employers will automatically open an account for you and deposit your funds into the account. If you do have an IRA, you initiate the rollover by contacting your 401(k) administrator.

You can also withdraw your money, but you’ll pay 20% in federal income tax, as well as a 10% early withdrawal penalty (unless you’re at least 59 ½ years old), according to the IRS.

🤓Nerdy Tip

An IRA is a tax-advantaged retirement account that an individual typically sets up, unlike a 401(k) account, which an employer sets up.

If you have at least $5,000 in your 401(k)

If your 401(k) account has at least $5,000 when you quit a job, your employer isn’t allowed to move your money without your consent. What happens next is up to you. There are a few things you can do with your money, according to the investment advisor Vanguard:

Roll over your money into a new retirement account

Leave your money in your old 401(k)

Cash out your 401(k) — and potentially pay a 10% federal penalty tax

Let’s dig into those options.

Rolling your money into a new 401(k) or IRA

What is a rollover?

Reminder: A 401(k) rollover is the process of moving money from your 401(k) account into another retirement account.

So, say you’re leaving your job for a different position, and your new employer offers a 401(k) plan. You can roll over your old 401(k)’s funds into a new 401(k) account, if your new employer allows this, according to the IRS.

Or you can roll over your old 401(k) to an IRA. This type of account typically offers more investment options than a 401(k), says Christopher Manske, a certified financial planner and the president and founder of Manske Wealth Management in Houston.

“In your individual retirement account, you’re going to have a lot more flexibility to tailor the investments to the wide world of what’s available out there,” Manske says.

Whether you roll over your retirement savings into an IRA or new 401(k), moving your money to a single fund can make it easier to manage your money and keep track of your retirement savings.

That’s as opposed to simply keeping your old 401(k) open, which becomes one more account to manage. (We’ll dive into that option in a bit.)

How to roll over funds — and avoid tax missteps

If a rollover sounds like a solid option, contact the administrators of both your old 401(k) and the other retirement account — either your new 401(k) or an IRA. Tell them you’d like to roll over your funds.

They’ll collect information from you and initiate a direct rollover, which means one institution directly transfers funds to another institution, according to Fidelity.

This is as opposed to an indirect rollover, meaning your 401(k) plan administrator sends you a check, and you personally deposit the 401(k) funds into another retirement account. In that case, your plan administrator would likely withhold 20% of your 401(k) funds for taxes.

With this indirect rollover, you then have 60 days to deposit the complete 401(k) account balance — including the amount kept for taxes — into the new account. So to deposit the full amount, you would need to come up with the 20% portion yourself. Then you’d get a refund for that amount come tax time.

If you miss the 60-day deadline, you’d likely get penalized for early withdrawal and have to pay income taxes on the distribution, according to Capitalize, a 401(k) rollover resource.

One last important note: Whether you choose a direct or indirect rollover, if you move money from your old 401(k) account to a Roth IRA — a specific kind of IRA — you’ll have to pay income tax on that transfer, according to the IRS. (This doesn’t apply if you’re rolling over your funds from a Roth 401(k), though.)

Leaving your money in your old 401(k)

Another option? Do nothing.

Your 401(k) account isn’t going to disappear once you quit a job; that money will always be there. But once you leave the job that set up the 401(k) account, you can’t make any more deposits, per Vanguard.

While leaving your 401(k) on autopilot is the simplest option, it may not be in your best interest. Assuming you’ll continue investing in another account or have a new 401(k) at your next employer, it will be harder to track your finances in more places.

And some 401(k) plan providers may charge you fees if you’re no longer an active employee, according to Charles Schwab, the financial services firm.

“I can’t think of any pros of leaving it there,” Manske says. “You’re not really connected formally to that company anymore, so why would you keep your money there? They don’t have a reason to keep you happy.”

Cash out your 401(k) — which is rarely recommended

Yes, you can withdraw the cash from your 401(k) whenever you want. But there are significant downsides to this option.

Pulling out money from your 401(k) before retirement can trigger hefty taxes, says Joe Buhrmann, certified financial planner and senior financial planning consultant at Fidelity’s eMoney Advisor.

Any withdrawals from a 401(k) before you reach the age of 59 ½ are considered early withdrawals and are slapped with a 10% penalty tax, per the IRS. That’s in addition to federal income taxes and, depending on where you live, state income taxes.

“Hypothetically, on a $50,000 401(k), you might lose as much as $20,000 to taxes and penalties and be left with $30,000,” Buhrmann says.

If you urgently need cash, that might be a reason to withdraw some money from your 401(k). But doing so should be regarded as a last resort, Manske says.

There are other ways to get money quickly that don’t come with taxes and penalties, such as community loans, gig work, and more.

Buhrmann encourages individuals to not just consider the immediate losses that come with withdrawing your 401(k), but also the long-term earnings they’re missing out on.

“They’re not just having to pay some taxes and pay some penalties,” Manske says.