These streets will make you feel brand new. Big lights will inspire you.

The Big Apple is one of the most iconic places on Earth. New York City residents even go as far as to associate the concrete jungle with who they are as a person. With world-class museums, accessible public transportation, delicious restaurants, influential theatres and many famous landmarks, the city is truly a tourist’s paradise.

But while visiting is fun, moving to New York City may feel overwhelming. Between apartment hunting, navigating steep annual rent and the various boroughs of the city, the city feels like no other city.

In this guide, we’ll break down what you need to know before you pack your bags and set off to become a New Yorker.

Moving to New York: the complete Big Apple overview

New York City is the most populous city in the United States. Thinking of the city might conjure up images of the Empire State Building, the Statue of Liberty and the bright lights of Broadway.

However, there’s much more to the city than the tourist hotspots. New York City is divided into five boroughs: Manhattan, Brooklyn, Queens, the Bronx and Staten Island. Each has a distinctive personality, with different cultural influences and attractions.

While each area is different, here are some key figures to give you a glimpse of the city overall.

Population: 8,500,000

Population density (people per square mile): 29,302.6

Median income: $70,663

Average studio rent: $4,264

Average one-bedroom rent: $5,367

Average two-bedroom rent: $7,914

Cost of living index: 100

Popular neighborhoods in New York

Between all five boroughs, New York City has hundreds of neighborhoods to explore. But don’t let this intimidate you. They’re all connected by New York’s world-famous transit system, so you can peruse them at your leisure. Here are a few of our favorite neighborhoods to get you started.

Astoria: Astoria is located in Queens, just across the river from Manhattan’s Upper East Side. This charming neighborhood is made up of low-rise buildings and small businesses, giving it a more suburban feel than you might expect in the big city.

Riverdale: Who said you couldn’t get beautiful green spaces in New York City? Riverdale, located above Manhattan in the Bronx, is known for its natural landscapes. With Van Cortlandt Park, Wave Hill and stunning Hudson River views, this quiet residential neighborhood is ideal for New Yorkers who still want to enjoy the great outdoors.

West Village: The West Village, located in downtown Manhattan, perfectly encapsulates the New York you know from your favorite movies and TV shows. This charming spot is tucked inside the larger Greenwich Village. It features tree-lined streets, historic brownstones and plenty of well-preserved historical landmarks from the neighborhood’s bohemian past.

Upper East Side: The Upper East Side offers excellent residential options and world-famous cultural sites. Located between Central Park and the East River, the neighborhood offers plenty of places to get outside and explore. The Upper East Side is also home to Museum Mile, where more than a dozen art and history museums await.

Williamsburg: Williamsburg is a great example of New York’s diversity. The Brooklyn neighborhood has long been a place where cultures blend, with plenty of eclectic dining, art and entertainment options. It’s also known for its family-friendly atmosphere with parks and tree-lined streets.

The pros of moving to New York

New York, the city that never sleeps, holds a unique place in the hearts of its residents. There’s no place in the world quite like New York City and few cities that even come close to comparable. Here are just a few of the reasons that people love living in this city.

A true cultural melting pot

More languages are spoken in NYC than in any other American metro. With its long, rich immigration history, the city hosts a colorful blend of traditions, cuisines and lifestyles. Especially through the distinct boroughs of New York City, which each have its own unique personality and cultural identity.

From the vibrant energy of Manhattan to the artistic ambiance of Brooklyn, the historical charm of Queens, the green serenity of the Bronx and the island spirit of Staten Island, no matter where you go in New York, you’ll always have the opportunity to learn about a different culture.

No car required

New Yorkers love to complain about their subway system. However, even they secretly know they have it better than most people in the other cities. New York City’s subway serves more than 400 stations, making it a breeze to get where you need to be.

The subway map shows the subway also connects to numerous bus lines, ferry stops and commuter trains, giving riders even more options. From the Upper West Side to Staten Island, the subway is the easiest way to get around your new city.

There’s always something to do

Getting bored in NYC just might be impossible. The city boasts hundreds of restaurants, bars, museums, theaters and places to shop. New York City also has excellent parks, scenic riverfront trails and even beaches. Whether your ideal Saturday is spent at the Metropolitan Museum or taking a subway ride to walk the Brooklyn Bridge, you will never run out of places to explore.

The cons of moving to New York City

Of course, no city is perfect. Here are a few downsides that you should consider before you move to New York.

The high cost of living

New York City is one of the most expensive cities in America. Here, you can expect everything from your monthly rent to your groceries to cost a bit more. Space is also at a premium, so even expensive rentals tend to be smaller than what newcomers might be used to. Even your security deposit will be a tad pricier than you are probably used to.

It’s hard to avoid the crowds

NYC is the most densely populated city in America. As such, it can be hard to avoid the crowds when you’re out and about. Neighborhoods in midtown and downtown Manhattan can get particularly packed, so plan accordingly. Consider neighborhoods like Staten Island and Brooklyn when opting for a less densely populated area in New York, with all the same perks and amenities.

The realities of big-city living

Living in any big city can take some getting used to and New York is no exception. The city can be noisy, dirty and downright overwhelming. If you’re coming from a smaller city or town, New York may feel like a different planet. It’s best to visit the Big Apple during your apartment hunt to really get a feel for the space and pace of the city.

How to get started on your move to New York

New York is a city that’s in constant motion. But for the people who live here, no place feels more like home. If you’re ready to make New York your home, we’re here to guide you every step of the way. Find your perfect New York City apartment here, and get ready for your journey to the city that never sleeps.

Methodology

Rent prices are based on a rolling weighted average from Apartment Guide and Rent.’s multifamily rental property inventory of one-bedroom apartments. Data was pulled in October 2023 and goes back for one year. We use a weighted average formula that more accurately represents price availability for each individual unit type and reduces the influence of seasonality on rent prices in specific markets.

Population and income numbers are from the U.S. Census Bureau. Cost of living data comes from the Council for Community and Economic Research.

The rent information included in this article is used for illustrative purposes only. The data contained herein do not constitute financial advice or a pricing guarantee for any apartment.

Wesley is a Charlotte-based writer with a degree in Mass Communication from the University of South Carolina. Her background includes 6 years in non-profit communication and 4 years in editorial writing. She’s passionate about traveling, volunteering, cooking and drinking her morning iced coffee. When she’s not writing, you can find her relaxing with family or exploring Charlotte with her friends.

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Snapshot: This OpenSky Secured Visa credit card offers a way for those with poor or no credit to build credit. It has a fairly low annual fee ($35 ) and is simple to qualify for, making it an affordable way to enter into the credit card market for younger adults.

OpenSky® Secured Visa® Credit Card

No credit check to apply and find out instantly if you are approved

OpenSky gives everyone an opportunity to improve their credit with an 85% average approval rate for the past 5 years

Get considered for a credit line increase after 6 months, with no additional deposit required

You could be eligible for the OpenSky Gold Unsecured Card after as few as 6 months

Reports to all 3 major credit bureaus monthly, unlike a prepaid or debit card. Easy application, apply in less than 5 minutes right from your mobile device

View your FICO® Score through your OpenSky account, an easy way to stay on top of your credit

Nearly half of OpenSky cardholders who make on-time payments improve their FICO score 30+ points in the first 3 months

Your refundable* deposit, as low as $200, becomes your OpenSky Visa credit limit

Offer flexible payment due dates which allow you to choose any available due date that fits your payment schedule

*View the cardholder agreement

Table of Contents:

Full Review of OpenSky Secured Visa Credit Card Review

What You’ll Like About This Card

The Drawbacks

Pros and Cons Summary

Is the OpenSky Secured Visa Credit Card Worth It?

OpenSky Secured Visa Credit Card FAQ

Full Review of OpenSky Secured Visa Credit Card

If you’re worried about poor or bad credit preventing you from qualifying for a credit card, the OpenSky Secured Visa Credit Card is a great place to start. Like most secured credit cards, it requires a refundable[1] security deposit ($200 minimum security deposit required, maximum is $3,000) that determines your credit limit.

Meanwhile, your OpenSky Secured Visa Credit Card will appear as a credit card account on your credit reports, helping you build positive credit with each on-time payment.

All in all, the OpenSky Secured Visa Credit Card has some interesting benefits that we believe make it worth the annual fee. Let’s get into it.

What You’ll Like About This Card

No Credit Check

OpenSky Secured Visa Credit Card doesn’t require a credit check to apply (great if you’re concerned about a low or non-existent credit score). If you’re ready to get started building your credit with OpenSky, provided you are approved, you can get started right away.

Credit Line Increase After 6 Months

No additional deposit required, provided that you have 6 months of on-time payments and have demonstrated responsible behavior, OpenSky may consider you for a credit line increase. This means that you would have access to funds beyond your deposit, like a typical credit card.

Flexible Payment Due Dates

OpenSky also offers flexible payment dates, so you can choose when your monthly payment is due to best fit your budget. For example, if you have a lot of bills due on the first of the month (rent, utilities, etc.) you may want to schedule your bill payment date a few weeks out to give yourself more time.

The Drawbacks

Annual Fee

Like we said above, the OpenSky Secured Visa Credit Card does have an annual fee of $35 . While this isn’t unusual for secured credit cards, there are other secured credit cards that don’t require a fee. OpenSky even offers the OpenSky Plus Secured Visa Credit Card that requires no annual fee with a minimum security deposit of .

Not Many Rewards

Some secured credit cards offer consumers some reward options, similar to typical credit cards. OpenSky Secured Visa Credit Card doesn’t offer any at this time.

Pros and Cons Summary

Pros

Cons

No credit check required

Must secure your credit limit with a deposit

OpenSky reports to all three credit bureaus, helping you build a positive credit history with responsible use

$35 annual fee

Potential to get approved for an OpenSky unsecured credit card within 6 months of on time monthly payments

Is the OpenSky Secured Visa Credit Card Worth It?

The deposit you make to secure your credit line is refundable when you close your OpenSky credit card, assuming you’ve paid off your balance. This, along with the fact that the secured credit card is easy to get approved for, can make it a good option for those who are trying to build or rebuild credit.

If you can find a secured credit card or other credit-building option that doesn’t have an annual fee, you may want to try that option first. That being said, the annual fee for the OpenSky credit card is competitive, and it’s easy-approval process and refundable deposit range more than make up for the fee.

OpenSky Secured Visa Credit Card FAQ

What are the credit limits for OpenSky Secured Visa Credit Card?

The credit limit for your OpenSky Secured Credit Card depends on how much you deposit when you open the account. At a minimum, you must have $200 to deposit, making the lowest possible credit limit $200. The maximum credit limit OpenSky tends to approve is $3,000, though this does require that amount in the initial deposit.

How soon can I increase my credit limit after being approved for an OpenSky Secured Visa credit card?

After 6 months of responsible account management and timely payments, OpenSky may offer you the chance to apply for an unsecured OpenSky credit card. These typically have a higher credit limit.

How good is an OpenSky Secured Visa Credit Card good for building credit?

OpenSky Secured Visa Credit Card is ideal for building credit! This is because OpenSky reports to all three credit bureaus. If you keep your credit utilization low and pay your bills on time, you can build a positive credit history on all your credit reports with this card. OpenSky recommends you keep your credit utilization under 30% and make timely payments to see the greatest impact.

[1] OpenSky® Secured Visa® credit cards require a refundable security deposit. Your credit limit is based on the amount of your security deposit. Minimum $200 and up to $3,000 (Subject to approval)

2 Based on 2Q 2023 OpenSky® Secured Visa® Credit Card average approval rate is 88.7%. Individual results may vary

Searching for a new apartment often takes a lot of time and research; in fact, it can be disheartening if you have a hard time finding an apartment you love. And that’s why winter is the best time to rent an apartment. You might be surprised at how easy it is to discover your next apartment, one that you can’t wait to turn into a home.

1. There often is lower demand in the winter

It’s no secret people love to move in the summer. The weather usually is great, the kids are out of school for families looking to relocate and there often is less demand on our time for other activities. In fact, 40 percent of all moves occur in the summer, with just 5% taking place in November and December. As a result, apartment shoppers can find some great apartments for rent, particularly new apartments that may be completed during the season.

2. You could find more options for apartment size, style

In tandem with lower demand, renters may find there is a wider variety of apartment sizes and styles available during the winter than in other seasons. Because demand is lower, it might be easier to find that two-bedroom apartment you wanted instead of having to settle for a one-bedroom unit. This also applies to those new apartments that are completed during the winter. That means you could land a great apartment with new appliances, updated finishes and special spaces such as a sunroom or screened porch.

3. There could be more availability with movers

Because people don’t move as often during the winter, you may be able to book your movers on your timetable instead of having to wait for one to become available. This is important so you can schedule the movers around your commitments and work schedule and don’t have to use valuable personal or vacation days for moving instead. Also, during this slower season, movers may not be as rushed, so might be less likely to damage your items.

4. You could have more time off to move

No one wants to spend their personal or vacation days moving instead of on a much-needed vacation. When moving in the winter, particularly around the holidays, you likely could have extra days off that won’t interfere with your PTO or vacation days. Although no one wants to spend their holidays moving, it could prove beneficial if you don’t have to take off extra time at work.

5. You could snag an apartment when a fall graduate vacates

Looking for an apartment near a college campus could be especially challenging because many, if not most, apartments are already booked from September through May. However, if you are moving to a college town during the winter, particularly in December or January, you could score an apartment when a fall graduate prepares to move out. After all, no landlord wants an apartment to sit empty until the new students arrive in August or September.

6. You could save money

While you may not be looking for a less expensive apartment, you could still score one during the winter. No landlord wants a vacant apartment, so it’s not uncommon for them to run rent specials during the winter when demand is low. This could range from waiving the security deposit to offering a free month of rent to reducing rent for the entire term of the rental agreement.

7. It’s a good time to negotiate preferred rental terms

Because landlords want to rent empty apartments during the winter, the tenant is in a good position to negotiate the rental agreement terms. This could include asking for a shorter- or longer-term lease, waiving fees such as those for pets or upgrading the appliances in the unit. If there’s something you want, now is the time to ask. The worst that could happen is the landlord says no.

Yes, winter is the best time to rent an apartment

As you can see, renting an apartment during the winter could provide many benefits, so don’t hesitate to start looking for a new apartment when the weather turns cold. You could end up scoring a hot deal on your next home.

Alicia Underlee Nelson is a freelance writer and photographer. Her work has appeared in Thomson Reuters, Food Network, USA Today, Delta Sky Magazine, AAA Living, Midwest Living, Beer Advocate, trivago Magazine, Matador Network, craftbeer.com and numerous other publications. She’s the author of North Dakota Beer: A Heady History, co-host of the Travel Tomorrow podcast and leads travel and creativity workshops across the Midwest.

Screening tenants is the only true way to know that the people moving into your rental are the best fit. Make a list of questions to ask tenants so you can streamline the process and ensure that you’re treating all applicants fairly.

Tenant screening questions can reveal a lot, such as the applicant’s track record as a renter, their ability to pay rent on time and whether they’ll adhere to the lease agreement. Discuss each of the questions to ask renters before conducting a background check or checking references to save you time and money.

Top questions to ask tenants

Tenant screening questions to ask renters should revolve around a potential renter’s income, their rental history and how they’ll maintain the property’s condition. So, what should (and shouldn’t) you ask? Here are 10 questions to ask tenants during the screening process:

How long have you lived in your current residence?

This question gives you a sense of the applicant’s stability as a renter and you should ask it early. If the applicant has skipped out on a lease or moves every year, that’s something to think about. Ideally, you want a tenant who will live in your rental for as long as possible. Having to fill a vacancy after the lease ends, usually just a year later, will be a headache and cost you rental income as the property sits empty.

Why are you moving?

Finding out why someone is moving out of their current home also offers a glimpse into their rental history. It could reveal past evictions or issues of where they broke a lease. But, most renters have a legit reason for moving. The cost of rent inspired 27 percent of renters to move in the past year, while 24 percent needed more space and 18 percent simply wanted a change, according to a survey by Entrata.

Have you ever been evicted or violated a lease?

You don’t want to rent to someone with a history of evictions or breaking leases. Asking about past evictions or lease agreement breaches gives renters the chance to come clean about past infractions. They might have experienced a rough patch and struggled to pay rent but are now more stable, or maybe they had to move out of a home unexpectedly due to an unforeseen event. Tenants might not answer this question truthfully, so that’s why it’s a good idea to talk to previous landlords.

What’s your monthly income?

This is an important question to ask tenants because you need to ensure they can afford the rent and pay on time. Generally, renters shouldn’t spend more than 30 percent of their income on rent. If you charge $900 a month for rent, the tenant should earn at least $3,000 a month. Property managers and owners can ask for pay stubs and contacts for their employer and conduct a credit history. But, make sure you know what you’re allowed to ask in regards to income in your area — some state rental laws let you ask about total monthly income but not how the tenant earns income.

Can I contact your employer and past landlords?

With rental history and income such important topics when screening tenants, it’s a good idea to ask for references. Contacting past landlords and the renter’s current employer will provide you with the information you need. Ask employers to verify that the tenant works there, how long they’ve worked there and how much they earn. Ask previous landlords if the tenant was reliable, if they paid on time and if they’d rent to them again.

How many people will live in the home?

You have the right to know everyone who is living in your rental. So, it’s a good idea to ask how many people will live there and who will be on the lease. This question is especially crucial if your state sets occupancy limits for a rental property or requires a home to have a certain number of bedrooms per person. Just don’t ask for too many details about family status, such as how the relation of tenants or how many children they have, which could violate fair housing rules.

Do you smoke?

Smoking is a source of property damage. As a property owner or manager, you have the right to set a no-smoking policy or designate certain smoking areas. When you ask applicants if they smoke, remind them of this policy and be sure to also include it in the lease agreement.

Do you have any pets?

Whether to allow pets in your rental is up to you. But keep in mind that most households have pets, so not allowing them automatically reduces your tenant pool. If you do allow pets, you can and should set parameters. A pet policy stipulates the type and size of pets allowed and if you’ll charge pet deposits or monthly pet rent. Asking tenants this question lets you determine if their pets adhere to your policy and give you a chance to remind renters of what’s allowed. Fair Housing laws don’t allow you to prohibit service or emotional support animals.

Do you agree to a background and credit check?

A few other questions to ask tenants involve their criminal and credit history. First, ask them if they consent to a background and credit check (and get written permission). If someone won’t agree to a check, you don’t have to rent to them. Ask, too, if there’s anything you should know before running the reports. Credit reports will show past bankruptcies and other issues, so this gives tenants a chance to explain what happened and how they’re working to improve past mistakes.

You can’t deny applicants for committing a crime or having been arrested. But you can deny someone if they’ve been convicted of a crime that potentially puts you, your property, others in the tenant’s household or the neighborhood at risk. Burglary, arson, illegal manufacturing of drugs or violent crimes are things you should note.

When do you want to move in?

Another critical question to ask tenants is when they would like to move into the home. Knowing their moving timeframe helps ensure you and the renter are on the same page. If you’re looking to fill a vacancy immediately and they’re not planning to move for a few months, it’s not a good match. Once you establish that the timing aligns, be sure to let them know about the security deposit and other fees that you charge and ask if they’ll be able to pay everything when they sign the lease.

What you should not ask tenants

When crafting your list of questions, be mindful of the Fair Housing Act, which prohibits discrimination in housing based on sex, race, color, national origin, disability, religion, disability and familial status. Some states extend Fair Housing laws to other protected classes, including sexual orientation or marital status. So, there are several topics you should not bring up with renters, including:

Where they were born

Their race or nationality

Their sexual orientation

Which languages do they speak

How many children they have — or, the ages and gender of their children and where the kids go to school

Whether they’re interested in nearby religious congregations

Do they have a service dog or a disability

If they’ve ever been arrested

If they receive public assistance

The best tenant screening questions to ask tenants

Screening tenants and learning more about their rental history and monthly income will help you choose someone who’s likely to pay rent on time and take care of your home. Listing your property on Rent. lets you accept applicants and screen tenants online. Creating a standard list of questions to ask everyone will ensure that you’re being as fair as possible.

Erica Sweeney covers real estate, business, health, wellness and many other topics. Her work has appeared in The New York Times, The Guardian, Good Housekeeping, HuffPost, Parade, Money, Business Insider, Realtor.com and lots more.

Though FICO® and VantageScore® ranges start at 300, most new credit users don’t start this low. In fact, if you’ve never taken out credit or applied for a loan, you might not have a credit score at all.

When applying for credit cards and loans, you begin to build credit, but you may be wondering—what does your credit score start at? Most people’s initial credit scores are between 500 and 700 points, depending on the steps taken when establishing credit. However, you won’t have a credit score to report if you’ve never opened a credit account.

Read on to learn more about your starting credit score and how to build your credit over time.

What Credit Score Does an 18-year-old Start with?

Contrary to popular belief, you don’t automatically receive a credit score the day you turn 18 years old. However, you need to be at least 18 years of age to apply for credit and start building your score. Remember that if you haven’t used credit yet, you likely won’t have a score at all.

Once you start using credit, you will get a score roughly three to six months after opening your first credit account. Your credit score will be calculated based on a variety of factors outlined in the next section.

How Are Credit Scores Calculated?

So, how are credit scores determined if everyone doesn’t receive the same default credit score? According to FICO, they use the following five factors to calculate your credit score:

Payment history: The most important factor to determine your credit score is your history of paying credit accounts on time.

Accounts owed: While owing money on credit accounts isn’t necessarily bad, using a majority of your available credit can lead to lenders viewing you as higher-risk.

Length of credit history: Generally, the longer your credit history, the better it is for your score since lenders have a more accurate assessment of your risk.

Credit mix: The different types of credit you have, such as credit cards, installment loans, and finance company accounts, are your credit mix.

New credit: Opening too many credit cards in a short period of time can hurt your score since doing so signals to lenders that you’re a greater risk.

How to build credit

If you’re new to credit, you may be wondering how to start building your credit in the first place. Receiving a loan without a credit score might be difficult, so FICO suggests the following ways to start building credit:

Become an authorized user on a family member’s credit card. You can be added to a card owner’s account, which allows you to make purchases with their credit card. Keep in mind that this method doesn’t have a large effect on your score but can be a good stepping stone to building credit.

Apply for a secured credit card. As a person with no credit, your risk to lenders is considered very high. A secured credit card requires you to pay a refundable security deposit to mitigate risk.

Report rent and other service providers. Credit and loans aren’t the only factors that affect credit. While landlords and utility companies typically don’t report to the credit bureaus, you can request that they do so to start building your credit.

How long does it take to build a 700 credit score?

According to FICO, a credit score of 700 or above is considered good. And since the national average credit score is 716 as of April 2022, it certainly is achievable, although it will take time. If you’re starting with no credit, you can expect building a 700 credit score to take at least six months of practicing positive credit habits.

Keep in mind that there are steps you can take to increase your initial credit score and reach your credit score goal of 700 or higher credit.

How to improve your initial credit score

So, how can you help make sure that you start out with a good credit score? Follow the tips below to improve your credit score.

Review your credit report. Once you open a credit account, be sure to view your credit report and look for any inaccuracies.

Be on time with your payments. Since payment history is the most important factor that influences your credit score, be sure to pay your bill on time and avoid missing payments.

Limit applying for multiple lines of credit in a short period of time. Applying for credit results in a hard inquiry, which may slightly lower your credit score. Too many of these hard inquiries in a short period of time can cause your credit score to drop.

Keep your credit utilization ratio under 30 percent. Credit utilization refers to the amount of credit you’re using divided by the amount that is available to you. For example, if your monthly credit limit is $1,500, aim to use under $450 each month.

Be patient. Again, the length of credit history is an important factor that contributes to your credit score. The more time that passes since you opened your account, the better for your score.

FAQs

Below, we’ve answered some common questions regarding your first-time credit score.

Does your credit score start at 0?

Your credit score doesn’t start at zero. In fact, the lowest credit score possible is 300. However, you likely won’t start at this score unless you’ve made actions that have damaged your credit score.

Does everyone start with the same credit score?

Everybody doesn’t start with the same credit score. As mentioned above, your individual credit score is based on a number of factors.

Is no credit worse than bad credit?

No credit means you lack a credit history, whereas bad credit means you’ve made credit-damaging mistakes, such as multiple late payments. While both scenarios can cause limitations, building credit from scratch is generally easier than rebuilding a bad credit score. As a result, it’s worse to have bad credit than no credit.

What’s a good credit score for young adults?

A good credit score is 670 and up. According to Experian®, the average credit score for young adults ages 18-25 is 679, so any score above that is considered above average for the age group.

How to check your credit score for free

Once you begin building credit, it’s crucial to follow responsible financial practices that will help you raise your credit score over time. And don’t forget to regularly monitor your credit to make sure you’re on the right track.

ExtraCredit by Credit.com gives you tools to manage your credit at an affordable monthly price so you have information you need to help you achieve your financial goals. Get started today.

Is your poor credit history preventing you from obtaining your financial goals, such as getting a credit card, buying a car, or purchasing a home? If so, there are steps you can take right now to improve your credit score in as little as three months.

This article provides actionable steps you can take today to start on the path to rebuilding your credit.

In This Piece

How Quickly Can You Improve Your Credit?

The exact amount of time it can take to repair your credit score depends on several factors, such as your current credit score, the amount of debt you owe, your ability to repay your debt, and your overall credit history.

Despite this, you can start making improvements in as little as three months. Below is a look at five things you can do to improve your credit score, along with tips to keep in mind.

1. Pay Off the Debt You Can

Start by paying off as much debt as possible. There are several strategies you can use to pay down your debt, including the debt avalanche method, the snowball method, and a debt consolidation loan. No matter which method you use, the faster you can pay down some of your debt, the sooner your credit can start to improve.

Keep in mind that it could take your creditors up to 30 days to report payments to the credit bureaus and another 30 days for the credit bureaus to post these payments to your account.

2. Minimize Your Credit Utilization

Your credit utilization ratio accounts for up to 30% of your overall credit score. This ratio compares the amount of credit you have available with the amount of credit you’ve used. It’s recommended to keep this ratio below 30%. If you’re having trouble hitting this number, here are some things you can do.

Ask for a Higher Credit Limit

If your credit utilization ratio is above 30%, you can ask your credit card company to increase your credit card limit. This strategy will increase the amount of credit you have available, which can help lower your credit utilization ratio.

Use as Little Credit as Possible

Instead of using your credit card to make multiple or large purchases, consider using another method to pay. The less you have charged to your credit card, the better your credit utilization ratio will be.

Taking these steps to decrease your credit utilization rate could start to improve your credit in as little as 60 days.

3. Keep an Eye on Your Credit Report

According to a recent study, 34% of Americans found at least one mistake on their credit report. Just one credit card error could damage your credit score. This is why it’s so important to keep an eye on your credit report.

You can request a free credit report from all three major credit reporting agencies, Experian, Equifax, and TransUnion, at annualcreditreport.com. Obtaining your credit report is just the first step; you also want to perform the following tasks.

Check Your Report for Errors

Carefully review your credit report to make sure all the information listed is correct, including your personal information and account details. Make a list of any incorrect information and any accounts or personal information that’s missing.

Dispute Inaccurate Information

The best way to remove incorrect information on your credit report is to file a dispute with the credit reporting agency. Write a dispute letter that clearly explains what inaccurate information is listed on your credit report and why it’s incorrect. Submit this letter, along with any supporting documents, to the credit bureaus listing the error.

Typically, the credit reporting agencies have up to 30 days to investigate your dispute and another 5 days to let you know their decision.

Ask if Lenders Will Remove Paid-Off Items From Your Report

Many lenders report past-due accounts to credit reporting agencies to entice customers to pay their debts. Once you pay your debt off, the lender may be willing to remove this debt from your credit report. Contact your lender directly to make this request.

It could take days, weeks, or months to receive a clear answer from your lender. If they do agree to remove this debt, it could take up to 60 days to reflect on your credit report.

How to Add Your Utility Bills to Your Credit Report

Typically, utility companies don’t report on-time payments to the credit bureaus. You can, however, work with a reporting service company, such as Credit.com’s ExtraCredit service, to make sure these payments along with your rent payments are listed on your credit report. This step can help prove you have a strong payment history.

Once you sign up for a credit reporting service, you can expect to see these payments on your credit report within 60 days.

4. Consider Applying for a New Line of Credit

Having a mix of different types of credit accounts, such as revolving credit accounts and fixed-payment accounts, makes up to 10% of your credit score. If you want to boost your credit score, it’s important to have a nice mix of different accounts. Below is a look at some types of credit accounts you may qualify for even if you don’t have good credit.

Are Credit Builder Loans Right for You?

As the name suggests, credit builder loans are designed to help you build credit. This type of loan is different from traditional loans, as you don’t have access to the money until you make all your payments. Obtaining a credit builder loan can be a great way to save money while building your credit because these lenders often report loan payments to the credit bureaus.

Types of Credit to Consider

If you can’t obtain a traditional credit card, there are other options, such as:

Secured credit card. With a secured credit card, you’ll be required to put down a cash security deposit prior to obtaining your card. Otherwise, these credit cards work just like traditional cards and can help you build your credit.

Authorized user. If you can’t obtain your own credit card, you can ask a friend or family member to add you as an authorized user to their account. If the credit card company reports your authorized user status, it can help build your credit.

Tips for Applying for New Credit

While maintaining a mix of credit accounts can help you build your credit, you want to make sure you don’t open too many new accounts too quickly. This action could damage your credit score due to excessive credit inquiries. Instead, take it slow and gradually open a mix of accounts.

Opening just two different types of credit accounts, such as a car loan and a credit card, can impact your credit as soon as they’re reported on your credit report.

5. Keep on Top of Your Finances

Keeping on top of your finances is a very important building block in your credit foundation. Start by building a budget and sticking to it. This step can make sure you don’t overspend, help you start to save money, and learn to be more conscious of how you’re spending your money on credit.

What to Do if You Don’t Have Credit

If you currently have little to no credit, you may be wondering how you can build credit in just a few months. Taking some of the steps above, such as working with a reporting service company, obtaining a secured credit card, or becoming an authorized user, can help you build credit as soon as they are reported.

Knowing how to raise a credit score in three months is just the first step. Now, it’s time to take action.

The Possible Card — issued by Coastal Community Bank, in partnership with Possible Finance — began slowly rolling out to the public in April 2023. As of this writing, the card is available in most states, with the exception of Hawaii, Nevada and Maryland.

While still in its early stages, the Possible Card won’t help propel your credit journey forward because it currently doesn’t report payments to major credit bureaus like TransUnion, Equifax and Experian. Even once it begins reporting payments, it still won’t be your most cost-effective option. Possible Finance touts “peace of mind” that you won’t be charged interest, but there’s a big caveat: Instead of an annual percentage rate, the card has a monthly fee.

Monthly fees on credit cards are a hot trend now, especially among young financial technology companies (fintechs). But depending on the balance you’re carrying, that fee can be more expensive than interest charges you’d find on a traditional credit card.

The Possible Card does offer predictability in terms of your monthly payment, and it also allows you to bypass a credit check and security deposit. But unlike a security deposit, which is refundable, those monthly fees won’t be. Plenty of other credit cards can jump-start your credit-building goals at a lower cost.

Here’s what you need to know about the Possible Card.

🤓Nerdy Tip

While any credit card’s rewards, benefits and fee structure can be adjusted at any time, new cards from startup financial technology companies are particularly prone to significant changes as they find their place in the market. Keep that in mind as you research your credit card options.

1. The monthly fee adds up

The monthly fee to hold the Possible Card is either:

$8 per month ($96 annually) for a $400 credit limit, or

$16 per month ($192 annually) for an $800 credit limit.

That makes the Possible Card more expensive than similar newcomers in its class. For example:

The Tomo Credit Card (currently waitlisted as of September 2023) charges $2.99 per month. There’s no credit check, upfront deposit or APR.

The Pesto Mastercard costs $3.33 a month, and while a deposit is required, it can be an asset instead of cash.

In fact, for no monthly or annual fee at all, you could consider cards like the Chime Credit Builder Visa® Credit Card, which lets you set your own security deposit, or the Grow Credit Mastercard, which has a free membership tier. Neither card carries an APR, neither conducts a credit check, and all of these aforementioned cards report your payments to credit bureaus.

Or, you could fare even better with a traditional secured credit card. Yes, you’ll have to come up with a one-time security deposit upfront, but for many of the best secured credit cards, you need a minimum of just $200, or nearly what you’d pay — every year and nonrefundable — for the Possible Card’s higher-limit version. Plus, many traditional secured cards come with upgrade paths to better products. The Possible Card does not, nor do many newer fintech-backed cards, for that matter.

The Discover it® Secured Credit Card is a good example of the kind of features to look for in a starter card. It requires a minimum security deposit of $200, but it has a $0 annual fee and earns rewards. It reports payments to all three major credit bureaus, and Discover begins automatic reviews starting at seven months to see whether you qualify to upgrade to an unsecured card and get your deposit back.

🤓Nerdy Tip

If you’re approved for the Possible Card, you can immediately start using the virtual card if you enroll in autopay. Otherwise, you’ll have to wait for the physical card to arrive in the mail.

2. There’s no credit check

The Possible Card doesn’t require a credit check and instead relies on a cash-flow-based underwriting algorithm to determine whether you qualify. But that underwriting process requires you to link an eligible account through a third party called Plaid.

This practice of skipping a credit check in exchange for linking a bank account has become a fairly common practice for certain credit cards, especially newcomers backed by fintechs. But there are better credit cards that don’t require a credit check.

The previously mentioned Chime Credit Builder Visa® Credit Card, for instance, requires opening a Chime Spending Account, but it doesn’t charge any fees or interest. It’s a secured credit card with a flexible deposit. The amount of money that you move from the spending account to the Credit Builder secured account is the amount you have available to spend.

3. No APR or late fees apply, but don’t be fooled

Some credit cards that charge monthly fees instead of interest market the idea of being “predictable,” for budgeting purposes. Possible Finance claims on its website that the monthly fee is cheaper than the charges on a traditional credit card, but that’s misleading. For most credit cards, interest charges don’t apply at all if you pay off the balance in full every month.

With the Possible Card, you’ll owe the monthly fee whether you carry a balance or not.

Depending on the size of your balance, that monthly fee could cost more than the interest charged on a traditional credit card, especially in cases where the card’s credit limit is relatively low. You can use the sliding scales below to illustrate this:

For context, the average APR for credit cards assessed interest in May 2023 was 22.16%, according to Federal Reserve data. If you have less-than-ideal credit, that percentage may be higher.

Trying to get approved for a card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

4. You can carry a balance over a short term

Unlike some credit cards in its class, the Possible Card allows you to revolve a balance, up to a limit. The card’s Pay Over Time option lets you pay off the balance over four installments if you schedule automatic payments and enroll in the app. There’s no additional charge to use this option as long as the account has a balance of at least $50 and no pending payments.

The downside of the Pay Over Time feature is that the card will be locked and cannot be used for new purchases or automatic recurring expenses until the installment loan is paid off. But the benefit is that this guardrail can prevent you from taking on more debt than you can handle.

If you’re using your Possible Card to make automatic recurring payments for streaming services or other expenses, make sure to change your payment method when you opt in to the Pay Over Time feature.

5. It doesn’t report payments to credit bureaus

The Possible Card is still in its infancy and does not report payments to the credit bureaus as of this writing. The company shared in an email that it has plans to start reporting payments to one bureau in the fourth quarter of 2023.

When your goal is to build credit with a credit card, reporting payments to the three major credit bureaus is a must-have feature. Ideally, you want your credit history to be recorded by all of them so that future lenders can access that information easily.

See more from Chime

Chime says the following:

The Chime Credit Builder Visa® Card is issued by Stride Bank, N.A., Member FDIC, pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa credit cards are accepted.

To apply for Credit Builder, you must have received a single qualifying direct deposit of $200 or more to your Checking Account. The qualifying direct deposit must be from your employer, payroll provider, gig economy payer, or benefits payer by Automated Clearing House (ACH) deposit OR Original Credit Transaction (OCT). Bank ACH transfers, Pay Anyone transfers, verification or trial deposits from financial institutions, peer to peer transfers from services such as PayPal, Cash App, or Venmo, mobile check deposits, cash loads or deposits, one-time direct deposits, such as tax refunds and other similar transactions, and any deposit to which Chime deems to not be a qualifying direct deposit are not qualifying direct deposits.

On-time payment history may have a positive impact on your credit score. Late payment may negatively impact your credit score. Chime will report your activities to Transunion®, Experian®, and Equifax®. Impact on your credit may vary, as Credit scores are independently determined by credit bureaus based on a number of factors including the financial decisions you make with other financial services organizations.

Money added to Credit Builder will be held in a secured account as collateral for your Credit Builder Visa card, which means you can spend up to this amount on your card. This is money you can use to pay off your charges at the end of every month.

This correlation between the average cost of living and credit card limit continues when we look at the 10 states with the lowest average credit card limit. In the chart below, the states marked with an asterisk are also on the list of states with the lowest cost of living.

State

Average Credit Card Limit

Average Credit Score

Mississippi*

$21,676

667

Arkansas

$24,570

683

West Virginia*

$24,684

687

Alabama*

$25,621

680

Louisiana

$25,781

677

Kentucky

$25,962

692

Oklahoma*

$26,041

682

Indiana*

$26,676

699

Idaho

$26,871

711

Iowa*

$27,052

720

Source: Experian, Wisevoter

How Are Credit Card Limits Determined?

Credit card companies use several factors to determine your limit, which they review periodically over time. Some factors count more than others, varying by the credit card issuer.

Your Credit Score

A higher credit score indicates you are more likely to pay your debts, which tells credit card issuers you are lower-risk. As a result, people with higher credit scores often have higher credit card limits.

According to FICO®, a variety of factors determine credit scores, including:

Payment history: Your payment history determines 35% of your credit score, which shows how likely you are to pay your debts on time.

Credit utilization rate: Your credit utilization rate is the ratio of the debt you owe to the total amount of credit available to you. You can factor your credit utilization rate by dividing your current balance by your total credit limit and multiplying the result by 100. A healthy credit utilization rate is considered anything below 30% —any higher and potential lenders may consider you overextended.

Length of credit history: The longer your credit history, the better picture a lender has of your risk level. A short history isn’t necessarily bad unless it contains a poor payment history and high utilization rate.

Recent hard inquiries: A hard inquiry is a record of a lender checking your credit. Too many hard inquiries in a short period can lower your credit score temporarily, so experts recommend six months between hard inquiries.

Credit card companies also use your credit score to determine your interest rate, so keeping an eye on your score with free credit reports is important.

Monthly Income

Credit card issuers want to know if you have monthly income to ensure you can pay your debts. The higher your monthly income, the more likely you are to get approved for a higher credit limit.

Monthly Expenses

Credit card companies look at your total monthly expenses, especially compared to your monthly income. Generally, they’ll look at your monthly housing costs (mortgage or rent), although they may also ask for information about other regular expenses such as utilities. Your monthly expenses are then compared to your monthly income to determine your credit card limit.

High monthly expenses won’t hurt your credit card limit as long as your monthly income is high enough to cover them.

Debt-to-Income Ratio

Credit card issuers also examine your debt-to-income ratio when determining your credit card limit. Experts consider anything under 36% to be a good debt-to-income ratio for a credit card.

To calculate your DTI ratio, divide your total recurring monthly debt (mortgage, auto loan, student loans, existing credit card debt, etc.) by your gross monthly income (how much you make before taxes) and multiply the answer by 100.

Your History with the Issuer

If you already have a positive credit history with the company issuing the credit card, they may be more likely to give you a higher credit limit. However, if they feel you have too many cards or a rocky credit history with them, they may issue a lower credit limit.

The Issuer’s Credit Approval Policies

Every credit card company wants to avoid risk and crafts a specific set of policies to determine how much credit to extend to a cardholder. Its policies may consider elements not listed here or weigh factors differently than another company, which is why credit card limits are not standard across companies.

Current Economic Outlook

When the economy is healthy, credit card companies may be more open to taking risks and offer higher credit card limits. However, when the economy is uncertain, such as during the pandemic, issuers are less likely to take risks, offering lower credit card limits for new cardholders.

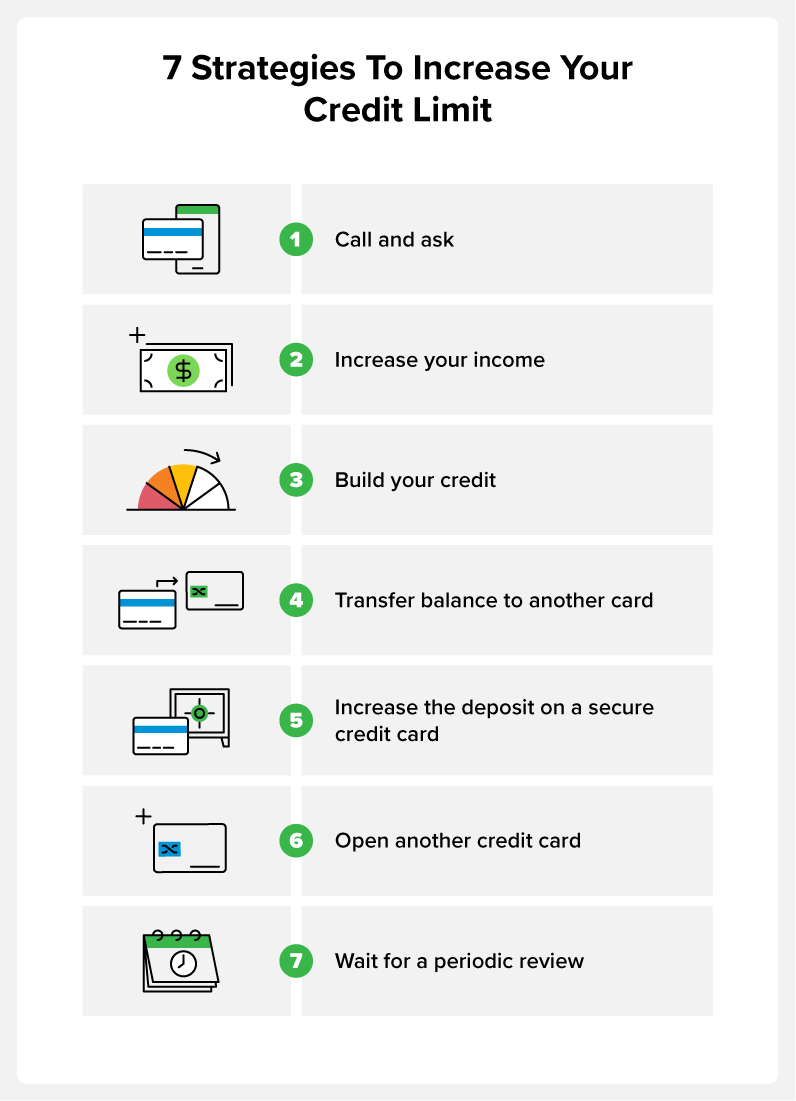

How to Get a Higher Credit Limit

A low credit card limit isn’t necessarily bad, but it can make getting approval for additional loans or credit challenging if your credit utilization rate is too high. It can also put large purchases, such as an appliance or unexpected car repair, out of reach.

To get a higher credit card limit:

Call your credit card issuer and ask for an increase. Call the customer service number on the back of your card and ask the representative for a higher credit card limit. Only consider this if you are trying to lower your credit utilization rate to raise your credit score. They look for six months of on-time payments and will ask for updates on your annual income, employment status, and monthly expenses before deciding.

Increase your income. Since monthly income is a factor in your credit limit, increasing your monthly income can boost your credit card limit. Ask for a raise at work, get a second job, or start a side hustle. When your credit card issuer sees you have more income, they may offer you a higher credit limit. You can update this information with them anytime by contacting them directly, or you can wait until they discover it in a periodic review of your status.

Build your credit. Pay your bills on time and pay down debt to increase your credit score. Over time, your credit score should increase, which can lead your credit card issuer to raise your credit limit.

Transfer the balance from one card to another. Some credit cards allow you to transfer debt from one account to another in a credit transfer. If you have multiple credit cards and one allows credit transfers, transfer the debt from one card to another. This won’t increase your credit card limit overall, but it can increase the amount of credit available on a specific card.

Increase your deposit on a secure credit card. If your card is a secured credit card, your credit card limit directly correlates to your security deposit. Add more to your security deposit, and you’ll have a higher credit card limit.

Open another credit card. This won’t increase the credit card limit on your current card, but it will expand how much credit is available to you. Avoid temporarily dinging your credit score by waiting six months between credit card applications.

Wait. Most credit card companies annually review your account, and as long as you pay your bills on time, they can likely naturally increase your credit card limit.

You can also always pay off purchases immediately rather than waiting until the end of your payment period to gain access to more credit without increasing your credit limit.

Credit scores strongly indicate what your potential credit card limit will be, so learn more about yours today. Before applying for a new credit card, get a sense of where you stand with a credit report card. Then use the tools and features in ExtraCredit to see where you need to work toward your credit goals to qualify for a higher credit card limit.

FAQ

Here are some answers to common questions regarding credit card limits.

What Happens if I Go Over My Credit Limit?

If you try to make a purchase over your credit limit, most credit card companies will deny the transaction. Some may allow the purchase but charge a fee, although most companies have abandoned this practice.

If I Request an Increase to My Credit Limit, Will That Impact My Credit Score?

When you request an increase to your credit card limit, your credit score may drop if your credit card issuer places a hard inquiry on your credit score. This can temporarily lower your credit score, and not all credit card companies do so.

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

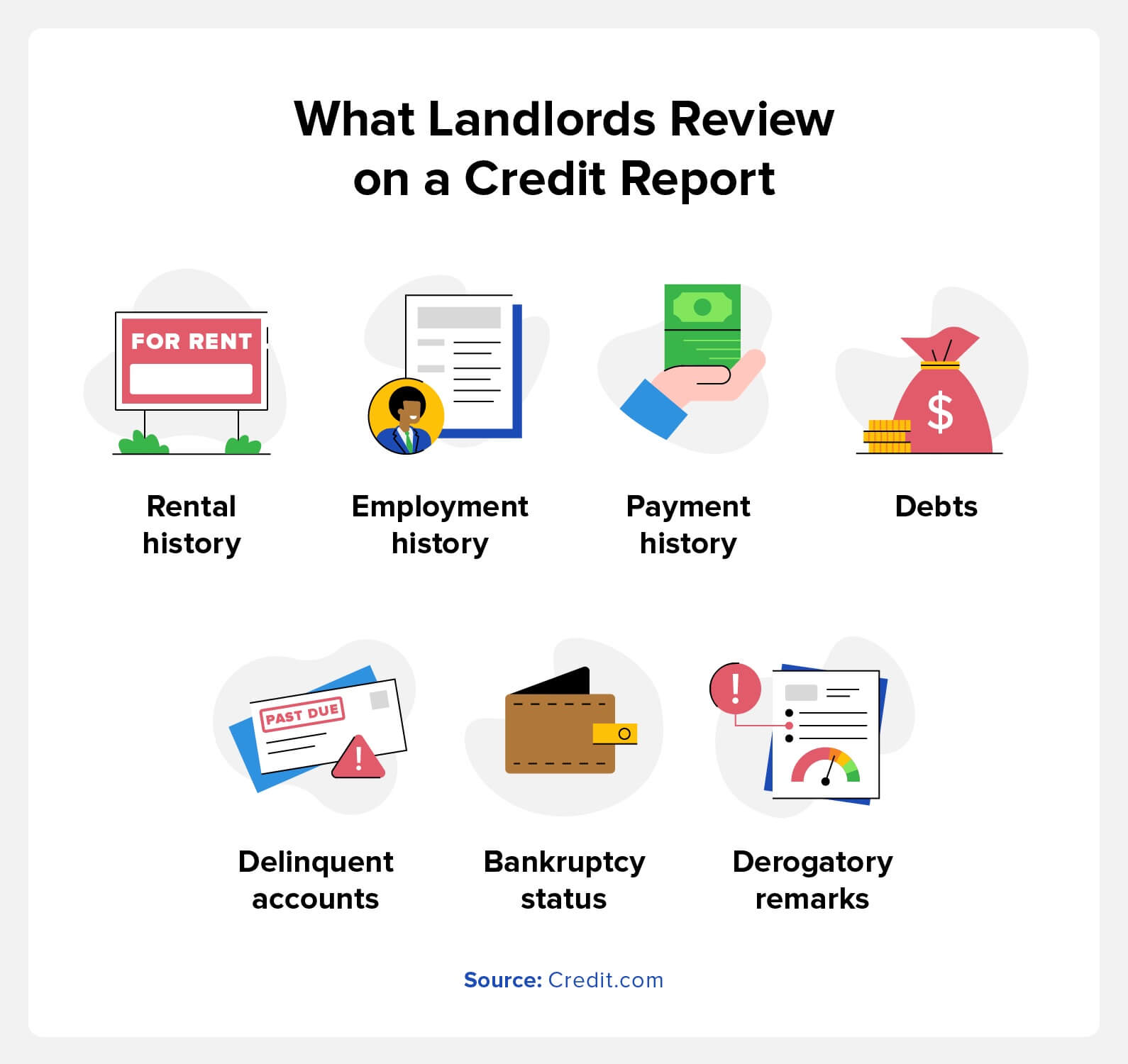

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.