Mortgage rates could drop in 2024 but the decrease may be small.

Getty Images

In less than two years, mortgage rates have more than doubled. At the end of 2021, the average 30-year fixed-rate mortgage had a 3.11% interest rate, according to Freddie Mac. Now, at the beginning of November 2023, the average has climbed to 7.94%.

The picture isn’t necessarily any brighter for other mortgage types either. For an adjustable rate mortgage (ARM), the average 5/1 ARM (meaning the interest rate is fixed for five years and then changes once per year after) has an annual percentage rate (APR) of 8.16%, while a 10/1 ARM comes in at 8.23%, according to Bankrate.

But will the picture look different in 2024? It depends who you ask. Some experts take a stronger view on rates falling in 2024, while others are less certain that will happen. In general, though, most seem to think that mortgage rate drops are more likely to occur toward the second half of 2024, though the change might be relatively small.

Not sure what mortgage interest rate you can qualify for? Find out here now.

Will mortgage rates go down in 2024?

Fannie Mae, for example, projects 30-year fixed-rate mortgages will start 2024 at an average of 7.1% and fall to 6.7% by Q4 2024.

“In 2024, do not anticipate mortgage rates to drop significantly. The current market environment leans towards stability rather than volatility and fear,” says Nathaniel Pitchon-Getzels, a buyer’s agent and listing agent at Compass.

“Before we see rates come down, it’s possible we’ll experience another rate increase. If they do decrease, it’s likely to be a gradual shift, possibly occurring at the end of the second quarter or the beginning of the third quarter,” he adds.

Rhonda Fisher, a real estate broker at Trust Equity Group and eminent domain expert with Consumer Notice, takes a similar view.

While she says she hopes mortgage rates come down in 2024, “the economic forecast suggests otherwise. With a strong employment market and inflation not decreasing as quickly as hoped, it doesn’t appear the Federal Reserve will be able to bring down rates anytime soon. The current rates are slated to continue until next year.”

Depending on economic variables like inflation, however, it’s possible that overall interest rates, including mortgage interest rates, will trend downward next year.

“If inflation and the economy weaken then we should expect to see interest rates lower toward the end of 2024,” says Fisher.

One way to get an idea of when mortgage rates are turning the corner and heading lower is to see when mortgage lenders stop making discount points mandatory. In the current environment, lenders often require homebuyers to pay money upfront in exchange for lower mortgage rates, in order for lenders to then be able to sell those loans to investors, explains Dan Green, CEO of Homebuyer.com.

“If you want to look smart and predict when mortgage rates will fall, keep an eye on discount points. Discount points will be a leading indicator for next year’s rates. When lenders start charging fewer points to buyers, that’s your signal that rates are about to drop,” he says.

He also thinks rates for different common loan types will generally move cohesively.

“Mortgage rates are generally close for the four major loan types – conventional, FHA, USDA, and VA. Over the last five years, VA and USDA loans averaged 0.25 percentage points below conventional loans, which averaged 0.15 percentage points lower than FHA loans. Buyers shouldn’t expect much change there,” says Green.

Learn more about your mortgage rate options here now.

Navigating the real estate market in 2024

If rates aren’t expected to drop significantly in 2024, what does that mean for buyers and current homeowners?

“Exactly what I always say to folks: what are your goals, what are you hoping to accomplish?” says Fisher. “For example, if a homeowner needs to make home improvements or renovations that are costly, a cash-out refinance might prove financially better than a personal loan.”

Some homebuyers also might be better off buying now than waiting to see if mortgage rates in 2024 drop.

“In the upcoming year, buyers need to be strategic and act promptly if they want to purchase a house. Waiting may lead to substantial losses in equity because property values continue to rise,” says Pitchon-Getzels.

Some sellers are also offering concessions, such as rate buy-downs in this environment, adds Fisher.

Still, it’s important to be mindful of what you can truly afford. Even if you think interest rates will drop and you can refinance later, that can be a risky strategy.

“When you buy a home, you have to expect that you’ll make its payments for the next 30 years because, even if mortgage rates drop, there’s no guarantee you’ll be eligible to refinance,” says Green. “What if you take a pay cut? What if you fall ill? What if life throws you a curveball?”

Instead, he says, “the best strategy for a homebuyer is to pick a mortgage and a payment that’s comfortable and stick with it. If the market improves and refinancing is possible, that’s terrific and lucky. But if refinancing is never an option, that’s okay, too, because the payment you’re making is within your zone of comfort.”

If you are in the market for a mortgage, be sure to shop around with different mortgage providers to see where you can get the best rate. Even a small difference in interest rates can add up to thousands of dollars in interest over the life of your loan, depending on the specifics, so it’s important to find the best fit for your circumstances.

The so-called “Foreclosure Prevention Act of 2008” introduced by senators Christopher Dodd and Richard Shelby has been fast-tracked by the Senate and could be voted on as early as next week.

The legislation contains a series of provisions to combat the rising foreclosure epidemic in the United States, including FHA reform so borrowers have better access to affordable housing.

“Senator Shelby and I have worked diligently over the past 24 hours to develop legislation that will help provide solutions to the housing crisis which is forcing millions of homeowners into foreclosure, freezing up the liquidity in our markets, and causing a tightening of credit,” said Dodd in a statement on his website.

Included in the bill is FHA modernization that would increase the FHA loan limit permanently from 95 percent to 110 percent of the area median home price, capped at 132 percent of the GSE limit (conforming loan limit), which is currently $550,000.

Additionally, a down payment of 3.5 percent would be required for any FHA loan and counseling requirements would be enhanced to help promote stable homeownership.

A whopping $4 billion would be provided to communities hardest hit by foreclosures and $100 million would be allocated to housing counseling agencies throughout the nation to better connect borrowers with loan servicers.

The bill also includes a standard property tax deduction, enhanced mortgage disclosures, and the controversial extension of net operating loss carry-back (tax break) to homebuilders and other businesses affected by the ongoing mortgage crisis.

Lastly, a tax credit of $7,000 would be offered to those who buy homes already in foreclosure, a measure the senators believe will help buoy flagging property values.

Private mortgage insurance company Triad Guaranty said today via an SEC filing that it may stop writing new business because of rising mortgage defaults and costly claims.

The Winston-Salem, North Carolina-based company noted that the mortgage industry boomed during the last five years, but in 2007 property values began to decline and mortgage defaults shot upward, especially in markets that experienced high rates of appreciation.

“The ability to refinance with relative ease coupled with strong home price appreciation contributed to a lower default rate and facilitated loss mitigation efforts, particularly in fast growth states such as California and Florida,” the company said in the filing.

“Over the past six to nine months, however, these distressed markets have experienced substantial growth in default rates and also have significantly higher average loan amounts. As a result, our average reserve and claim size on defaulted loans is significantly greater in these distressed markets than with respect to our overall portfolio.”

The company added that its risk-to-capital ratio has “risen dramatically” over the last 12 months, driven by a significant increase in risk-in-force coupled with operating losses during the second half of 2007.

“Based on our internal projections, we must significantly augment our capital resources in the second quarter of 2008 in order to preserve our ability to continue to write new insurance.”

“The proposals that have been considered involve structures under which Triad would implement a “run-off” plan and a newly formed mortgage insurer would acquire certain of Triad’s employees, infrastructure, sales force and insurance underwriting operations. In addition, we would cease writing new business.”

A month ago, Triad reported a $75 million fourth-quarter loss and a net loss of $77.5 million for 2007, compared to net income of $65.6 million in 2006.

The company blamed ongoing deterioration in the housing and mortgage markets, particularly in states like California and Florida, where default counts rose a combined 85 percent.

Shares of Triad Guaranty were down $1.32, or 25.14%, to $3.93 in afternoon trading on Wall Street, more than 90 percent below their 52-week high.

A very large majority of home appraisers are being pressured to inflate property values, according to a survey conducted by Valufinders, a national provider of valuation services.

The company said 91 percent of those surveyed said they’ve been asked to pump up the value of the homes they appraise, while 81 percent worried they’d lose repeat business if they failed to bring in the desired result.

Some of the appraisers polled even expressed concern about losing a job if they didn’t provide a value to the client upfront, before the appraisal was ordered.

Nearly two-thirds (65 percent) said they were affected by the pressure to overvalue a property, indicating that integrity was undermined as a result of the constant competition.

“We’ve all been pressured to inflate values and loan officers are often ‘fishing for value’ with their ‘comp check’ requests,” said one appraiser who was surveyed.

At the same time, another appraiser expressed that he takes an “impartial approach,” and has no trouble telling borrowers the value of their home, good or bad.

Asked if their workload would be less burdensome if the mortgage industry adopted a facilitated appraisal process, just over half (52 percent) of respondents said yes.

In early March, the OFHEO unveiled the Home Valuation Code of Conduct, which would eliminate broker-ordered appraisals, prohibit appraiser coercion, and reduce the use of in-house appraisals come 2009.

Summerville, a picturesque town nestled in the heart of South Carolina, encapsulates a unique blend of southern charm, historic significance and modern convenience.

The overarching question — is Summerville, SC, a good place to live? — becomes easier to answer as one delves into the fabric of this quaint yet burgeoning locale. The aim of this article is to provide a well-rounded view of living in Summerville, the cost of living, employment opportunities and the social and cultural fabric that awaits newcomers and longtime residents alike.

Location, location, location

Summerville’s geographical positioning allows its residents to experience a plethora of sceneries and activities. Charleston Harbor is a mere 24 miles away, offering access to an expansive maritime vista, while a short drive to Folly Beach or Sullivan’s Island opens up a gateway to sun, sand and surf.

Demographic diversity in Summerville

The racial makeup of Summerville, SC, presents a mosaic of cultures, predominantly comprising white, Black, Latine and Asian communities, thus fostering a rich cultural blend. The inclusion of different ethnicities is a part of Summerville’s charm, allowing for a vibrant, multicultural community.

Historic significance

History aficionados would be drawn to Summerville’s rich history, with the town playing host to numerous historically significant sites. The Drayton Hall, Magnolia Plantation and the Aiken Rhett House Museum offer glimpses into the antebellum era and Civil War history.

Weather and natural disasters

While Summerville, SC, does experience hurricanes, the town has a solid infrastructure in place to manage and mitigate the effects of such natural disasters. Its inland location serves as a natural barrier, providing a level of protection against the harshest weather conditions.

Education and employment in Summerville, SC

Charleston Southern University, located a short drive away, is one of many educational institutions offering quality education to Summerville residents. The town also boasts a growing job market with varied employment opportunities, ensuring a stable economic outlook.

Recreational activities

The abundance of walking trails like the Oakbrook Nature Trail, and waterways such as Ashley River, provide ample recreational opportunities. The nearby Jessen Public Boat Landing is a favorite among boating enthusiasts.

Cost of living in Summerville

The cost of living in Summerville, SC, is generally lower than the national average, which is a significant draw for many. Housing, represented by a mix of historic homes, new construction, and Summerville homes in serene neighborhoods, is relatively affordable with the median home price being attractive to both young families and retirees.

Summerville’s real estate market

The real estate market in Summerville, SC is thriving, thanks to a boom in population growth and the subsequent demand for housing. Real estate agents are seeing an upward trend in property values, yet the cost of owning or renting a home remains affordable compared to many other regions in the South.

Culinary scene in Summerville, SC

The culinary palette in Summerville is as diverse as its populace. From smoked chicken to pork belly, ribeye steaks to fried green tomatoes, the food scene is a blend of traditional southern and modern cuisines. Restaurants and food trucks alike offer a wide range of food options, catering to different tastes.

Social aspects

Southern hospitality is alive and well in Summerville. The small town feel, coupled with the friendliness of Summerville residents, creates a welcoming environment. Community events like the Flowertown Festival are a testament to the town’s social cohesion, bringing together people from all walks of life.

Summerville’s growth trend

Summerville’s growth trend is a positive indicator of its viability as a place to live. The influx of more people, bolstered by opening doors of opportunity, is transforming the town while retaining its historic charm.

Conclusion

The blend of affordable living, a robust real estate market, promising job opportunities and a welcoming community makes Summerville, SC a great place to live. Its proximity to beaches, historic downtown Charleston and numerous tourist attractions, like the Folly Beach County Park, add to the allure.

Individuals and families considering moving to Summerville will find a balanced mix of historical essence, modern amenities, and a promising future. If you’re ready to make your move, take a look at our Summerville, SC, apartments for rent.

Cassidy spoke to MPA during the annual FUSE conference staged in Las Vegas by the Association of Independent Mortgage Experts (AIME). The gathering took place Oct. 4-7. It’s not brokers who are leaving amid challenging times Cassidy pointed to a positive aspect inherent to the current challenges of the housing market – what with inflation, … [Read more…]

Whether you’re selling your home to begin a new adventure or refinancing your existing home, getting an appraisal with the value you want is an important hurdle to clear. You may feel that the appraisal process is out of your control, but there are many easy and inexpensive ways to get both yourself and your home ready.

We put together a checklist of our top tips below. But first, let’s quickly cover the basics of home appraisals.

What Is a Home Appraisal and Why Is It Important?

A home appraisal is an unbiased report on the value of your home performed by a trained and state-licensed individual. Appraisals are an essential part of the home financing process, ensuring the homebuyer, seller and mortgage lender each have an impartial, consistent and accurate assessment of the value of the property under consideration.

The lender is responsible for ensuring that your home provides adequate collateral for the mortgage. For most loans, the lender obtains a signed and completed appraisal report that accurately reflects the market value, condition and marketability of the property.

It’s the appraiser’s job to provide a factual, unbiased and detailed description of the property and the neighborhood. They must take into account all factors that influence a home’s value when developing the market value opinion in the appraisal report.

Home Appraisal Cost

While home appraisal costs can vary by state and property size, the fee can range between $300 and $1,200. Most fall somewhere around $600-$1,000, with costs based primarily on the geographical area of the home.

How Long Does a Home Appraisal Take?

From start to finish, the home appraisal process usually takes approximately 7-10 days to complete.

The required in-person visit by a home appraiser can take over an hour, depending on the size of your home. However, several other steps are involved in making an unbiased and professional assessment of your home’s value. Your appraiser will research trends, local county records and recently closed comparable homes in your area, known in the industry as “comps.”

Once your appraiser compiles and analyzes all the information and data, they will present a final report of your home’s value.

What Do Home Appraisers Look For?

A home appraiser uses several sources of information to determine a property’s value. As part of the assessment, the appraiser will visit the property in person and review recently completed sales of comparable homes. Common factors examined during home appraisals include:

Property size. In real estate appraisals, size significantly affects the final number. In general, the higher the square footage of a home, the higher its value. An appraiser will also look at the kitchen, number of bedrooms, bathrooms and closets.

Exterior condition. When assigning a value to your property, the appraiser will consider not only the exterior appearance of your home but also its condition. They will check the following:

The condition of the roof, foundation, siding, gutters, chimney and walls, looking for signs of leaks, mold and other safety hazards

Lot size, including front and backyard square footage

Pool, outdoor kitchen, deck, porch and other amenities

Interior condition. Again, this refers not only to the appearance of the interior but also to the working condition of standard household assets such as:

Plumbing

Electrical and HVAC systems

Doors and windows

Light fixtures

Any kitchen appliances to be included in the sale

Attic, basement and foundation. A finished basement or attic may impact a home’s value, but these areas must meet specific requirements to be considered part of the Gross Living Area (GLA). An appraiser will also evaluate your home’s foundation and its condition.

Home improvements and renovations. Tell your appraiser about any work or upgrades you have done to spruce up your home. This can include anything from the central air system you installed 10 years ago to the kitchen flooring and countertops you just renovated (along with the new oven and fridge to match, of course).

What Hurts a Home Appraisal?

If an appraisal is in your future, it’s essential to understand the factors that could negatively impact it, such as the following:

Low-value comps and decreasing neighborhood property values

Poorly maintained interior or exterior

Age of the home

Location, such as a flood zone or busy road

Signs of mold, insect infestation, leaks or other safety concerns

Issues with the home’s systems, such as plumbing, electric or HVAC

Lack of parking

Hazardous construction materials like lead paint or asbestos tile

Outdated or faulty plumbing, electrical and heating systems

Some issues are in your control and some may not be. Whether you choose to address the correctable concerns or not, being aware of crucial appraisal criteria can help you avoid the potential unwelcome surprise of a lower-than-expected home value.

Top 7 Tips Home Appraisal Checklist

How does one best prepare for a home appraisal? We put together a checklist of common (and not-so-common) tips to help you get a high valuation from your appraiser.

1. Do Your Own Appraisal

Imagine that you are the appraiser. Walk around your home’s interior and exterior and really scrutinize it as if you were going to complete the appraisal report yourself. Take note of any obvious damage or deferred maintenance that needs your attention. Leaks, broken systems and damaged surfaces should all go on your list of things to repair.

Thoroughly inspect safety equipment like smoke alarms, carbon monoxide alarms and home security systems. Are they all functioning, or do parts or entire systems need to be replaced? Make a plan to repair these issues and clean up any cosmetic issues that may have occurred as a result.

2. Investigate Comps

Check out recent home sales in your neighborhood. What has the price range been for homes with features and updates similar to yours? The values of these comparable homes should be similar to what your home will appraise for. This information can help you know where to focus your time, efforts and funds.

If you know a neighbor (or real estate agent) who recently sold a home in your area, contact them to find out if there were any appraisal issues or insights that they can share.

If you’re working with a real estate agent, you can request that they collect some comps for you and your appraiser to review. Particularly if your home has unique or uncommon features, your agent may need to get creative while staying within the guidelines for selecting comps.

A quick way to get a rough idea of how much your home is worth is to use a home value estimator calculator. Add some basic information to gauge your home’s current value and view recent home sales in your area.

3. Get Superficial

Clean your house from top to bottom and remove extra clutter. Once you’ve scrubbed and straightened up everything possible, consider making some easy, low-cost cosmetic updates that can have a big impact, like the following:

Paint or touch up existing paint

Hang updated window treatments

Replace worn faucets, doorknobs and cabinet hardware

If you’ve been planning to update your decor after you move, consider bringing in a few of the newer pieces to make the old house look fresh and modern. Downsizing or packing for a long-distance move? Ask your real estate agent if they have staging furnishings you can borrow or recommendations for a service you can use.

4. Make Your Outdoor Areas Truly Great

Now that your home’s interior looks fantastic, it’s time to pay attention to the exterior. Make sure that your landscaping is looking its best by doing the following:

Mow your lawn, trim your trees and bushes

Remove weeds and dead vegetation

Add color with inexpensive, seasonal flowers in the spring, summer or fall, and ensure that snow removal is neat and tidy in the winter

You’ll also want to:

Remove outdoor clutter, like yard tools and stray toys, from everywhere on the property

Consider staging any outdoor living spaces with new furniture or accessories

Power wash your home’s exterior, as well as your driveway and any deck or patio surfaces

Ensure your pool is well-maintained and in safe operating condition

Most of this can be accomplished in a weekend, and the increased curb appeal will be worth it.

Check out expert tips for outdoor home renovations — you may find just the right improvement to increase your value!

5. Be Sure To Share Your Upgrades

Tell your home appraiser about the improvements you’ve made to your home. Inform them of upgrades like the following that will positively impact your appraisal value:

New features that you have added, like a security system

Updated HVAC units

Exterior improvements like siding, gutters or a new roof

High-value room remodels like kitchens and bathrooms

An easy way to make sure that your appraiser remembers all of these improvements is to create and share a short, one-page list detailing each. You should have this list ready in advance and include any applicable permit information.

6. Know Your Neighborhood

Make your appraiser aware of any recent improvements in your overall neighborhood. It’s worth mentioning things like:

New or highly rated schools

Parks

Transportation enhancements

Shopping

Other beneficial amenities

These kinds of changes can add significant value to your home, and if your appraiser is not a local resident, they may not be aware of them. Appraisers are often familiar with the general area, but you probably know your specific neighborhood better than they do.

7. Stay Focused

While you are working your way through the tasks and updates listed above, it’s important to remember not to go overboard and take on too many projects. Invest your time, money and effort only on issues that clearly need attention. If you’re getting an appraisal for a home you’re selling, you most likely already have a buyer who liked your home enough in its current state to make an offer on it. Making unnecessary major changes could end up being a waste of your time and resources.

Your home’s selling price is affected by much more than just the appraisal! Find out how the time of year can increase your sale price.

Although it’s not possible to change your bungalow into a country estate overnight, taking the time to tackle a few strategic projects before your appraisal can help put you in a better position to get the outcome you want. If you’re ready to move or refinance the home you love living in, get a custom mortgage rate quote from Pennymac today. Our Loan Experts can answer your questions and help guide you through the mortgage loan process.

Share

Categories

buying a home selling a home appraisal fundamentals

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

It’s common for home buyers to purchase a property in a certain school district.

This ensures their children can attend a specific school if they’ve got their eye on one in particular.

Heck, even those without kids might favor a certain home because it resides in a highly-sought after district.

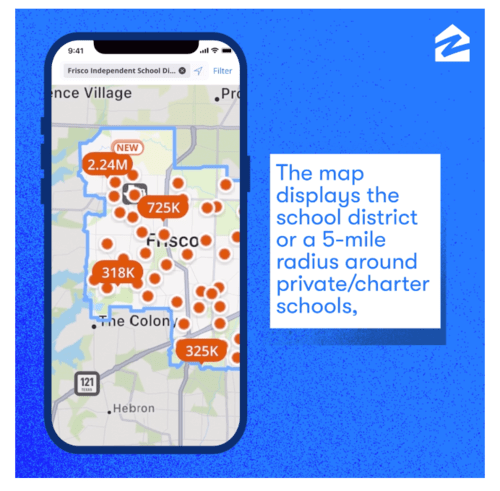

Now Zillow has made it easier for prospective home buyers to find properties in attendance zones or school districts simply by using the search bar.

When using the company’s mobile app, you’ve got the option to search by school, just as you would city or neighborhood.

Search by School on Zillow to Find a Home in Your Desired District

The latest update to the Zillow app allows home shoppers to search by school attendance zone or school district.

Simply open the app and navigate to the search bar. Instead of typing in a certain city or neighborhood, type the name of a school you like.

From there, Zillow will automatically display the attendance zone boundaries on the associated map in the app.

You’ll be able to see properties that are available for sale (or rent) within the attendance zone selected.

And if you search for open enrollment, or for a charter or private school without an assigned boundary, Zillow will display homes within a 5-mile radius surrounding the school.

The new search-by-school feature also allows home shoppers to receive instant or daily alerts when new for-sale or for-rent homes within their preferred school district or attendance zone come online.

That way you’ll be the first to know if a property meeting your school district needs pops up.

Since homes in desirable school districts are often quite popular, this can provide a competitive edge over other prospective buyers.

Those who are logged-in users will also see auto-complete suggestions for relevant schools and school districts based on their search history.

As always with any sort of property details, be sure to double-check that the home is indeed in the school district.

While it’s helpful to have this information generated automatically, it’s always smart to verify that the details are accurate.

This functionality is currently available on Zillow’s iOS mobile app and will launch on Android by the end of 2024 (it will be on the web sometime next year).

School Districts Are Very Important to Home Buyers

While there are a number of reasons why home buyers choose their properties, school district is a biggie, especially for those in their 30s.

And the prime first-time home buyer age is around 34, so most home buyers are going to be very focused on the associated school district.

As noted, even those without kids (or no interest in having kids) should be concerned with school districts as they can impact valuations pretty significantly.

You’ll often find that property values (and list prices) are notably higher in highly-sought after school districts.

This means a home seller can unload their property for a premium, or rent it out for more to a family who wants to reside in the district.

But it is also typically means you’ll pay more for it, and/or face more competition when attempting to buy the property.

Per Zillow’s Consumer Housing Trends Report, 75% of home buyers in their 30s emphasize the importance of school district selection.

Additionally, 67% of buyers in their 40s and 61% of first-time buyers consider school district a highly important factor in their home search.

This trend also seems to be growing, with the percentage of buyers who considered school districts highly important rising to 52% in 2023 after holding steady at 43% from 2018 to 2021.

Homes Tend to Appreciate More in Good School Districts

Back in 2016, I wrote that you should buy a home in a good school district even if you don’t have kids because they tend to appreciate more than those in not-good districts.

A study by ATTOM Data Solutions analyzed average test scores from about 19,000 elementary schools nationwide that covered nearly 46 million single-family homes and condos.

They discovered that in zip codes with at least one good school, the average estimated home value was 77% higher than in zip codes without any good schools.

Despite being more expensive, these good school district properties increased an average of $74,716 since the time of purchase, compared to just $23,311 for the not-good districts.

In other words, the purchase price might be higher to start, because it’s located in a good school district, but over time it should outperform properties located in the not-good school districts.

This might explain why there are even single-family home investors who are actively targeting properties in “elite school districts” these days.

While I don’t necessarily endorse that approach, since it makes getting into good school districts even more competitive for young families, it makes business sense.

All that being said, school districts aren’t everything. It can also pay off to buy a home near a Starbucks, a Target, or a Whole Foods or Trader Joe’s.

But ultimately, you should love the home you make an offer on, and want it for a variety of reasons that go beyond it’s potential monetary value.

Read more: When should you start looking for a house?