Well now that the Super Bowl is over, it’s time to look forward toward spring and the rest of 2013.

The holidays have passed and now many individuals are determining what their financial goals are for the year.

Is this the year to finally sell a home, buy a home, or just continue to sit tight?

While all those questions may have different answers, depending upon your current position, it’s clear that it’s a seller’s market right now.

It’s not a traditional seller’s market, largely because most homeowners don’t have much home equity, but the current environment does favor sellers because inventory is just so tight.

There’s also voracious demand at the moment, thanks to the perception that the worst is now behind us, and that if you buy in now, you’ll get a cheap home with an even cheaper mortgage.

Unfortunately, this herd mentality often precedes a bubble, that is, an unwarranted surge in price before a sudden and dramatic correction.

Housing Bubble Part Deux?

So, are we in for more trouble, now that seemingly every pundit, analyst, government official, interested party, and American is in on the supposed recovery?

The few who believe we are in for another bubble basically think the Fed created artificial demand for housing by pushing mortgage rates to new record lows, via quantitative easing like QE3.

It’s hard to argue with that fact – mortgage rates did indeed fall to unprecedented levels, and with that seemed to come a newfound demand for housing.

But even though demand is up, home sales are still lower than they have been historically.

All the recent “killer numbers” are only good, or improved, relative to the preceding dismal years.

And one could argue that home prices are on the mend because they’re cheap, not because rates are low. After all, plenty of recent sales have gone to cash buyers who could care less about rates.

If you look at the historical relationship of home prices and mortgage rates, it’s not what you’d think.

There’s not much of a correlation, and higher mortgage rates could actually come with higher home prices as a result of an improving economy.

It’s not as if the moment rates rise home prices will plummet, though the current situation is a little unprecedented.

Additionally, home prices are only up from the “bottom,” and nowhere close to fully recovered, assuming they eventually match the prices seen during the previous bubble, which history tells us they will.

In other words, inventory shortages and low prices are the real driver of demand at the moment, not necessarily low rates.

The low rates are more a boon to those looking to refinance their now expensive mortgages, not reason alone to purchase a home.

Housing bears also believe unemployment will continue to hinder a real recovery, and that there just aren’t any real buyers, only speculators.

The reasoning here is that there aren’t any first-time homebuyers because the economy is in the dumps, and there aren’t any move-up buyers because existing owners don’t have equity.

I think this is a convenient way of summing things up, but doesn’t represent reality. There are plenty of individuals who “missed” the first bubble, and have been patiently waiting to get in this time around.

There are also millions of existing owners with plenty of equity that want to buy again, especially at much lower prices.

What About Mortgage Quality?

To further argue against another housing bubble, the quality of mortgages this time ‘round is night and day.

Can you really compare a 30-year fixed at 3.5% to an option arm with a 1% teaser rate, which after five years, will reset to a fully-indexed and variable rate of 6% or higher.

Or a more straightforward interest-only ARM that becomes fully amortizing (and fully indexed) after 10 years, pushing a homeowner to the brink of default?

Oh, and those types of loans were also taken out at the height of the market, making mortgage payments that much more unsustainable.

Today, borrowers are taking out mortgages they can truly afford, with more skin in the game and no surprise resets in the future. Surely that will make for a more bubble-resistant housing market going forward.

But don’t be surprised if there are some hiccups along the way, because there will always be ups and downs.

Average mortgage rates jumped for all loan terms compared to a week ago, according to data compiled by Bankrate. Rates for 30-year fixed, 15-year fixed, 5/1 ARMs and jumbo loans moved higher.

Mortgage rates have been increasing for some time, with the popular 30-year fixed rate loan breaking through 7 percent this summer. After a stretch of record lows, rates climbed in 2022 thanks to inflation and the Federal Reserve’s response. The Fed last hiked its key interest rate in July, the latest in a tightening cycle that began last year.

The central bank decided to hold firm on another hike at its September meeting, indicating it expects rates to remain elevated in the near term and that it’s not done battling inflation just yet. “Until inflation goes down to the Fed’s target of 2 to 2.5 percent, do not expect rates to move lower,” says Derek Egeberg, a branch manager for Academy Mortgage in Yuma, Arizona.

The increase in mortgage rates comes alongside appreciating home prices, both of which have prevented more homebuyers from entering the market. More than half of home purchase mortgages originated in July had a monthly payment over $2,000, according to Black Knight. Twenty-three percent of originations in July had a payment over $3,000.

Rates as of September 28, 2023.

The rates listed here are averages based on the assumptions here. Actual rates available on-site may vary. This story has been reviewed by Suzanne De Vita. All rate data accurate as of Thursday, September 28th, 2023 at 7:30 a.m.

30-year mortgage rate trends higher, +0.24%

Today’s average 30-year fixed-mortgage rate is 7.83 percent, up 24 basis points since the same time last week. A month ago, the average rate on a 30-year fixed mortgage was lower, at 7.53 percent.

At the current average rate, you’ll pay a combined $721.95 per month in principal and interest for every $100,000 you borrow. That’s $16.56 higher compared with last week.

Standard lending practices defer to the 30-year, fixed-rate mortgage as the go-to for most borrowers buying a home because it allows the borrower to spread payments out over 30 years, keeping their monthly payment lower.

15-year fixed mortgage rate goes up, +0.08%

The average rate for a 15-year fixed mortgage is 6.90 percent, up 8 basis points over the last seven days.

Monthly payments on a 15-year fixed mortgage at that rate will cost around $893 per $100,000 borrowed. That may squeeze your monthly budget than a 30-year mortgage would, but it comes with some big advantages: You’ll save thousands of dollars over the life of the loan in total interest paid and build equity much more rapidly.

5/1 adjustable rate mortgage moves up, +0.12%

The average rate on a 5/1 ARM is 6.63 percent, climbing 12 basis points since the same time last week.

Adjustable-rate mortgages, or ARMs, are home loans that come with a floating interest rate. In other words, the interest rate will change at regular intervals, unlike fixed-rate mortgages. These loan types are best for people who expect to sell or refinance before the first or second adjustment. Rates could be materially higher when the loan first adjusts, and thereafter.

While borrowers shunned ARMs during the pandemic days of super-low rates, this type of loan has made a comeback as mortgage rates have risen.

Monthly payments on a 5/1 ARM at 6.63 percent would cost about $641 for each $100,000 borrowed over the initial five years, but could climb hundreds of dollars higher afterward, depending on the loan’s terms.

Jumbo mortgage interest rate moves higher, +0.24%

The average rate for a jumbo mortgage is 7.86 percent, up 24 basis points from a week ago. A month ago, the average rate was below that, at 7.55 percent.

At today’s average rate, you’ll pay a combined $724.03 per month in principal and interest for every $100,000 you borrow. That’s $16.58 higher compared with last week.

Interested in refinancing? See rates for home refinance

Current 30 year mortgage refinance rate trends upward, +0.20%

The average 30-year fixed-refinance rate is 7.98 percent, up 20 basis points since the same time last week. A month ago, the average rate on a 30-year fixed refinance was lower, at 7.66 percent.

At the current average rate, you’ll pay $732.37 per month in principal and interest for every $100,000 you borrow. That’s an increase of $13.88 over what you would have paid last week.

Where are mortgage rates going?

Economists can’t say for certain where mortgage rates are going from here, according to Bankrate’s latest forecast. Some have speculated the 30-year rate could increase to 8 percent, while others expect rates to cool down by the end of 2023.

30-year fixed mortgage rates mostly follow the 10-year Treasury yield, which shifts continuously as economic conditions dictate, while the cost of variable-rate home loans mirror the Fed’s moves.

“Economic data that is not too hot and not too cold would be helpful to mortgage rates and could get rates back down below 7 percent,” says Greg McBride, chief financial analyst for Bankrate, adding, “but that has to be true for inflation, job growth, wages and consumer spending.”

What current rates mean for you and your mortgage

While mortgage rates move up and down on a daily basis,, there is some consensus that we won’t see rates return to 3 percent for some time. If you’re shopping for a mortgage now, it might be wise to lock your rate when you find an affordable loan. If your house-hunt is taking longer than expected, revisit your budget so you’ll know exactly how much house you can afford at prevailing market rates.

Keep in mind: You could save thousands over the life of your mortgage by getting at least three loan offers, according to Freddie Mac research. You don’t have to stick with your bank or credit union, either. There are many types of mortgage lenders, including online-only and local, smaller shops.

“All too often, some [homebuyers] take the path of least resistance when seeking a mortgage, in part because the process of buying a home can be stressful, complicated and time-consuming,” says Mark Hamrick, senior economic analyst for Bankrate. “But when we’re talking about the potential of saving a lot of money, seeking the best deal on a mortgage has an excellent return on investment. Why leave that money on the table when all it takes is a bit more effort to shop around for the best rate, or lowest cost, on a mortgage?”

More on current mortgage rates

Methodology

Bankrate displays two sets of rate averages that are produced from two surveys we conduct: one daily (“overnight averages”) and the other weekly (“Bankrate Monitor averages”).

The rates on this page represent our overnight averages. For these averages, APRs and rates are based on no existing relationship or automatic payments.

Learn more about Bankrate’s rate averages, editorial guidelines and how we make money.

There’s been plenty to be happy about in housing lately. Home prices seem to have bottomed, and there is talk about double-digit appreciation over the next five years.

Mortgage delinquencies continue to march lower and distressed inventories keep shrinking.

Additionally, purchase mortgage applications increased to the highest level since May of 2010, per the Mortgage Bankers Association.

However, as I noted in a recent post, all this “good news” has made it less attractive to buy a house at the moment, despite the low rates and reduced home prices.

Why? Well, for one, sellers are upping their asking price, and many of the homes that festered on the market for months are appearing again. The scary part is that this time they’ll probably sell, and at a premium!

Top Mortgage Lender Not Enthused

I’m not the only one that feels this way. The top mortgage lender in the United States, Wells Fargo, seems to think the recent run up in home prices isn’t sustainable.

In fact, economists at the San Francisco-based bank and lender noted in a special commentary that the housing market is experiencing a “bubble within a bust.”

What they mean is that there is a “temporary spike in home prices,” which will pop once conditions deteriorate.

In other words, it’s not going to be a straight line onward and upward – there will be plenty of ups and downs as the market attempts to find its “new normal.”

And there are already signs of a slowdown, with unemployment festering, economic activity cooling, and the spring home selling season off to what they call a “mediocre start.”

Additionally, homebuilder confidence took a turn for the worse recently thanks to higher construction costs, along with a shortage of developed lots and skilled workers.

On top of that, the economists believe investors will stop converting single-family homes to rentals once interest rates increase, as the returns offered for such ventures will diminish.

There’s also fear that higher mortgage rates will slow home price appreciation. Though higher rates could also push more would-be buyers to pull the trigger…

Housing Recovery Still on Track

While the headline and opening paragraph of the economists’ commentary seemed bleak, the underlying message is positive.

They still believe housing is on track to make a recovery, just at a more modest and reasonable pace. Darn.

We can’t simply erase the housing crisis in five years – it takes time to right the many wrongs that occurred, especially when we’re using artificially low mortgage rates as the solve-all.

Yes, you can snag a low mortgage payment thanks to those low rates, but don’t expect your home to double in value anytime soon.

Put simply, we got a little ahead of ourselves, as we often do with just about everything.

This is the bubble mentality in a nutshell – everyone believes at the same exact time that something is destined for greatness.

And then the crash comes…

Be Reasonable About Your Home Purchase

What this all means is that you should be prudent in your decision to purchase a home, as always.

First and foremost, a home is a shelter, not an investment. Regardless of that fact, there are still good times to buy, and bad times to buy.

If you have flexibility, it may be wise to wait it out a little longer. At the moment, the inventory is poor at best, and the competition is fierce.

As noted earlier in the post, lots of dodgy homes are making their way back to market, and the worry here is that overzealous home buyers will overlook the reasons the properties didn’t sell the first time around.

Don’t be one of those people who makes the decision to purchase a home for the sole reason that it’s the greatest time in history to buy.

That mentality often leads to disappointment once the enthusiasm wanes. Yes, housing is on the road to recovery, but don’t buy all the hype.

Past Ginnie Mae president Ted Tozer has argued that the FHA should lower or completely eliminate its current 3.5% down payment requirement.

He discussed the controversial take during a Community Home Lenders of America Roundtable in Washington, D.C. earlier this week, per Inside Mortgage Finance.

This isn’t the first time he’s floated the idea of turning the FHA home loan program into a zero-down-payment program.

In the past while arguing this same position, he noted that the Bush administration even proposed such a change all the way back in 2004.

The question is does this invite more risk at a time when home prices and mortgage rates are already out of reach for most?

Most FHA Loan Borrowers Need a Minimum 3.5% Down Payment

At the moment, FHA loan borrowers need to scrounge up 3.5% of the purchase price when buying a home, assuming they have a 580 FICO score.

Those with scores between 500 and 579 need at least a 10% down payment.

While this is seemingly a pretty low bar, it still acts as a roadblock for many prospective home buyers, especially low-income borrowers with little savings.

According to a semi-recent Federal Reserve study, the average American household had about $42,000 in savings.

But if you break it down by age, those under 35 only had $11,250 and those 35 to 44 only about $28,000.

A home purchase, even with a small down payment, could easily wipe out these accrued savings. And remember that these numbers are an average.

Many households have much less, which is why they’re probably still renting if their desire is to own.

Tozer has argued that after accounting for rent, taxes, food, utilities, and other necessities, prospective first-time home buyers have little left to save for a down payment.

The FHA Minimum Down Payment Was Increased in 2009

If you recall, the FHA Modernization Act of 2008 resulted in the FHA minimum down payment rising from 3% to 3.5%.

It also banned seller-funded down payment assistance, which correlated with much higher default rates on FHA loans.

Ironically, these types of loans resulted in a near-$5 billion loss for the FHA and put the entire program at risk.

Around that time, some lawmakers argued for even higher down payment requirements, such as a minimum of 5% down. That didn’t happen.

Back then, the big argument was about having skin in the game, as those with little invested had no problem walking away from an underwater mortgage.

That’s why the timing of this idea is a bit of a head-scratcher, with home prices at/near all-time highs and mortgage rates more than double their early 2022 levels.

While it isn’t quite 2006 all over again, there has been a lot of speculation in the housing market and prices are certainly not cheap.

The saving grace is that most homeowners hold boring old 30-year fixed-rate mortgages at ultra-low rates this time around.

And zero down loans are generally few and far between, other than homebuyer assistance offered by some state housing finance agencies (HFAs).

What’s the Argument for a 0% FHA Loan Today?

At the moment, you need a minimum 3.5% down payment to obtain an FHA loan, slightly more than the minimum 3% required on conventional loans.

Interestingly, you used to need 5% down to get a conventional loan before they introduced 97% LTV offerings in 2014.

This 3.5% is also significantly higher than what’s required for other government-backed home loans.

Tozer pointed out that both VA loans and USDA loans don’t require a down payment (100% financing OK!).

The thing is those loans are reserved for members of the military or those buying in rural areas, respectively. Conversely, FHA loans are much more widely available.

Regardless, he argues that underwriting should focus on a borrower’s credit history as opposed to the down payment.

But if we recall from the prior mortgage crisis, credit scores got a big share of the blame for the sharp rise in defaults.

So relying on credit score alone might not be the best policy either. While defaults certainly rise as credit scores fall, a holistic approach is best when formulating underwriting standards.

This means looking at layered risk, such as credit score, down payment, DTI ratio, employment history, and more.

The Skin in the Game Is the Cost to Relocate

As for skin in the game at zero down payment, Tozer said the skin is the cost to move.

In other words, once low- and moderate-income homeowners move in, it would cost them way too much to relocate.

And this is apparently what would keep them there. While that might be true, would they continue making payments?

Tozer’s proposal is unlikely to materialize as it would require Congress to act at a time when housing supply is already dismal and affordability historically low.

However, there is other proposed legislation that would offer 100% financing to first responders who need a mortgage, via the HELPER Act of 2023.

In the meantime, other options already exist to get an FHA loan with zero down.

As noted, many state HFAs have programs that offer deferred-payment junior loans that cover the down payment and even the closing costs.

There are also private lenders that offer FHA with zero down, such as the Movement Boost from Movement Mortgage, which relies on a repayable second mortgage.

So options already exist without the need for an across-the-board elimination of the FHA’s down payment requirement.

At last glance, 30-year fixed mortgage rates were sitting above 7%. Despite this, there are virtually no homes for sale.

One would assume that after such a massive interest rate spike, demand would flounder and supply would flood the market.

Yet here we are, looking at a housing market that has barely any for-sale inventory available.

And when you remove the new home inventory (from home builders) from the equation, it’s even worse.

Let’s explore what’s going on and what it might take to see listings return to the market.

Why There Are No Homes for Sale Right Now?

The housing market is highly unusual at the moment, and has been for quite some time.

In fact, since the pandemic it’s never really been normal. The housing market came to a halt in early 2020 as the world stopped, but then took off like a rocket.

If you recall, the 30-year fixed spent the entire second half of 2020 in the sub-3% range, fueling voracious demand from buyers.

And as Zillow pointed out, the age demographics had already lined up nicely for a surge of demand anyway.

Around that time, some 45 million Americans were expected to hit the typical first-time home buyer age of 34.

When you combined the demographics, the record low mortgage rates, a pandemic (which allowed for increased mobility), and already limited inventory, it didn’t take much to create a frenzy.

At the same time, you had existing homeowners buying up second homes on the cheap, due to those low rates and generous underwriting guidelines.

And let’s not forget investors, who were taking advantage of the very accommodative interest rate environment and the insatiable demand from buyers.

The rise of Airbnb and short-term rentals (STRs) coincided with this low-rate environment, potentially taking additional inventory off the market.

This quickly depleted supply, which was already trending down thanks to a lack of new home building after the prior mortgage crisis.

Home builders got burned in the early 2000s as foreclosures and short sales spiked and prices plummeted. And their excess supply sat on the market.

As a result, they developed cold feet and didn’t build enough in subsequent years to keep up with the growing housing needs of Americans.

Collectively, all of these events led to the massive housing supply shortage.

Low Mortgage Rates Got Buyers in the Door, But Will They Ever Leave?

Low supply aside, another unique issue affecting housing supply is a concept known as mortgage rate lock-in.

In short, there’s an argument that today’s homeowners have such low mortgage rates that they won’t sell. Or can’t sell.

Either they don’t want to give up their low mortgage rate simply because it’s so cheap. Or they are unable to afford a home purchase at today’s rates and prices.

Simply put, most can’t trade in a 3% rate for a 7% rate and purchase a home that’s probably more expensive than theirs was a few years earlier.

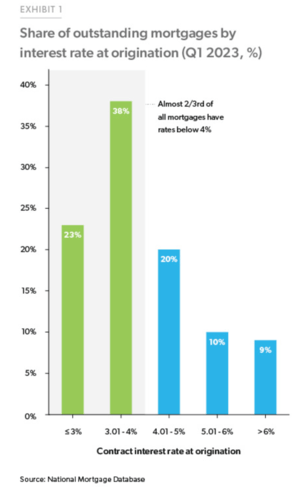

And this isn’t some tiny subset of the population. Per Freddie Mac, nearly two-thirds of all mortgages have an interest rate below 4%.

And nearly a quarter have a mortgage rate below 3%. How on earth will these folks sell and buy a replacement home if prices haven’t come down, but have in fact risen?

The answer is most will not budge, and will continue to enjoy their low, fixed-rate mortgage for many years to come.

This further explains why inventory is so tight and not really improving, despite the Fed’s attack on housing demand via 11 rate hikes.

[Why are home prices not dropping?]

Housing Supply Is at an All-Time Low

Redfin reported that the total number of homes for sale hit a record low in August.

Active listings were down 1.1% month-over-month on a seasonally adjusted basis, and a whopping 20.8% year-over-year.

That’s the biggest annual decrease since June 2021. However, new listings have ticked higher the past two months on a seasonally adjusted basis.

In August, new listings increased 0.8% from a month earlier after increasing the month before that.

But due to nearly a year’s worth of monthly declines prior to that, new listings were still off a big 14.4% year-over-year.

This meant months of supply stood at just two months, well below the 4-5 months usually considered healthy.

Redfin Economics Research Lead Chen Zhao noted that “new listings have likely bottomed out,” arguing that those who are locked in by low rates have already decided not to sell.

That leaves those who must sell their property, due to stuff like divorce or a change in work-from-home policy.

Interestingly, even some WFH homeowners are moving back closer to work, but keeping their homes because they can rent them out.

Because homeowners got in so cheap, it’s not out of the question to keep the old house and go rent or buy another property.

All of this has created a huge dearth of existing home supply, but there is one winner out there.

Home Builders Are Gaining a Ton of Market Share

While existing homes, also known as previously-owned or used homes, are hard to come by, newly-built homes are somewhat plentiful.

In fact, newly built single-family homes for sale were up 4.5% year-over-year in June, per Redfin, while existing homes for sale were down 18%.

And roughly one-third of homes for sale were new builds, up markedly from prior years and well above the norm that might be closer to 10%.

Astonishingly, new homes accounted for more than half (52%) of single-family homes for sale in El Paso, Texas.

Similar market share could be seen in Omaha (46%), Raleigh (42.1%), Oklahoma City (39%), and Boise (38%).

Meanwhile, the National Association of Realtors (NAR) predicts that new home sales will increase 12.3% this year, and 13.9% in 2024.

As for why home builders are seeing a big increase in market share, it’s mostly due to a lack of competition from existing home sellers.

In short, they’re the only game in town, and they don’t need to worry about finding a replacement property if they sell (like existing homeowners)

Additionally, they’re able to tack on huge incentives such as rate buydowns, including temporary and permanent ones, along with lender credits.

This allows them to sell at higher prices but make the monthly payment more palatable for the buyer.

Perhaps more importantly, it allows buyers to still qualify for a mortgage at today’s sky-high prices.

When Will More Homes Hit the Market?

For now, this new reality is expected to be the status quo. After all, those with so-called golden handcuffs have 30-year fixed-rate mortgages.

That means they can continue to take advantage of their dirt-cheap mortgage for the next few decades.

This includes second home owners and investors, who got in cheap when prices were much lower and mortgage rates were also on sale.

Meanwhile, the home builders don’t seem to be going nuts with supply, and even if they ramped up production, it wouldn’t satisfy the market.

Remember, existing home sales typically account for around 85-90% of sales, so builders won’t come close to satisfying demand.

The only real way we get a big influx of supply is via distress, sadly. That could be the result of a bad recession with mass unemployment.

And it could be triggered by the 11 Fed rate hikes already in the books, coupled with a lack of new stimulus and the resumption of things like student loan payments.

Compounding that is sticky inflation, which has made everything more expensive and is quickly depleting the savings accounts of Americans.

But even then, you could argue that a mass loan modification program would be unveiled to at least keep owner-occupied households in their properties.

Considering how cheap their housing payments are, assuming they’ve got a low fixed-rate mortgage, it’d be hard to find them a cheaper alternative, even if renting.

In the early 2000s this wasn’t the case because the typical homeowner held a toxic mortgage, such as an option ARM or an interest-only loan. And many weren’t even properly qualified to begin with.

Read more: Today’s Housing Market Risk Factors: Is Real Estate in Trouble?

U.S. home loan applications are the lowest in decades as evidence mounts that rising mortgage rates and home prices are shutting out many aspiring homeowners

ByALEX VEIGA AP business writer

September 7, 2023, 5:50 PM

FILE – A “SOLD” sign decorates the lawn of a new house in Pearl, Miss., Sept. 23, 2021. U.S. home loan applications are at the lowest level in decades, the latest evidence that rising mortgage rates and home prices are shutting out many aspiring homeowners. (AP Photo/Rogelio V. Solis, File)

The Associated Press

LOS ANGELES — U.S. home loan applications are the lowest in decades as evidence mount that rising mortgage rates and home prices are shutting out many aspiring homeowners.

An index that tracks mortgage application volume shows applications for loans to buy a home fell last week to the lowest level in 28 years, according to the Mortgage Bankers Association.

The MBA’s home loan application index shows that home purchase loans fell 2.1% last week from the prior week to a seasonally adjusted reading of 141.9. That’s down about 28% from a year earlier and represents the lowest level for the index since April 1995.

“Both purchase and refinance applications fell, with the purchase index hitting a 28-year low, as prospective buyers remain on the sidelines due to low housing inventory and elevated mortgage rates,” said Joel Kan, the MBA’s deputy chief economist.

Mortgage rates have been climbing in recent weeks, echoing a steady rise in the 10-year Treasury yield, which lenders use as a guide to pricing loans.

The average rate on the benchmark 30-year home loan was 6.48% at the start of this year, falling as low as 6.12% in February, according to mortgage buyer Freddie Mac. Since then, its been hovering around 7%, in-line with the average seen near the turn of the century.

High rates can add hundreds of dollars a month in costs for borrowers, limiting how much they can afford in a market already unaffordable for many Americans. They also discourage homeowners who locked in low rates two years ago from selling, a trend that’s helped keep the inventory of previously occupied U.S. homes on the market at near-record lows.

The lack of housing supply has weighed on sales of previously occupied U.S. homes, which are down 22.3% through the first seven months of the year versus the same stretch in 2022.

The average rate on a 30-year mortgage remains more than double what it was two years ago, when it was just 2.87%. As more homeowners locked in bottom-barrel rates in recent years, demand for home loan refinancing has plunged.

The MBA’s refinance loan index fell to a seasonally adjusted rate of 388.1 last week, down 4.7% from the previous week and 30.3% below a year ago.

Fixed rate mortgages have dipped below 5 per cent for the first time since early July, offering some hope to struggling homeowners.

Yorkshire Building Society has launched a 4.99 per cent fixed-rate deal which is available to both home buyers and those remortgaging.

It’s available at 75 per cent loan-to-value, meaning eligible customers can apply as long as they either have at least a 25 per cent deposit or 25 per cent equity within their home.

Best rate: Yorkshire Building Society has launched a 4.99 per cent fixed rate deal aimed at both homebuyers and those remortgaging

Someone with a £200,000 mortgage could expect to pay £1,168 a month if repaying over a 25-year term, compared to the market average of £1,249 a month.

The five-year deal comes with a £1,495 fee, however, and a mortgage with a higher rate but a lower fee may be a better deal for some customers.

You can compare rates and fees and work out the true cost of a mortgage using our calculator.

After Yorkshire BS, the next best deal is Virgin Money which has a five-year fix at 5.07 per cent and is available to home buyers purchasing with at least a 35 per cent deposit (65 per cent loan-to-value).

HSBC has a five-year fix at 5.09 per cent for home buyers with at least a 40 per cent deposit (loan-to-value of 60 per cent).

Nationwide also has a 10-year fix available at 5.04 per cent which is available to home buyers with a deposit of 15 per cent or more (85 per cent loan-to-value).

The average five-year fixed mortgage rate is now 5.67 per cent, according to Rightmove.

Rachel Springall, finance expert at Moneyfacts said: ‘It’s great to see such competitive deals launched by Yorkshire Building Society.

‘Borrowers looking for a new low-rate mortgage will find the sub-5 per cent five-year fixed deal is the lowest rate available in its sector.

‘The incentive packages available across all the new deals today may also be popular with borrowers looking to save on the upfront cost of their mortgage.’

Why are mortgage rates going down?

Yorkshire BS’ decision to cut rates, which includes shaving off up to 0.46 percentage points from its 95 per cent loan-to-value deals, is partly due to competition between lenders.

HSBC has also slashed mortgage rates by 0.15 percentage points on average today, alongside rate cuts across its buy-to-let range of up to 0.3 percentage points.

Last week there were also cuts from Coventry BS, Nationwide BS, Accord, Generation Home, Barclays, and Clydesdale Bank.

Past the peak? Fixed mortgage rates appear to be falling back somewhat after a barrage of rate hikes in recent months

Rate cuts have also been encouraged by future market expectations over where interest rates are heading.

Market expectations are reflected in swap rates. These are agreements in which two counter parties, for example banks, agree to exchange a stream of future fixed interest payments for a stream of future variable payments, based on a set amount.

Mortgage lenders enter into these agreements to shield themselves against the interest rate risk involved with lending fixed rate mortgages.

Put more simply, swap rates show what financial institutions think the future holds concerning interest rates.

Five-year swaps are currently at around 4.56 per cent, which is down from 4.74 per cent at the start of this month.

Only as recently as July, five year swaps were above 5 per cent. Similarly, the two-year swap rate is now 5.21 per cent. In July early this was around 6 per cent.

Ben Merritt, director of mortgages at Yorkshire Building Society, said: ‘This week, favourable market swap rates presented just such a window to reduce our mortgage costs, and offer the greatest incentive to those people who typically struggle the most, those with the lowest deposits to put down, including first-time buyers.’

Nicholas Mendes, mortgage technical manager at broker, John Charcol says he wouldn’t rule out a five-year fix at 4.5% by the end of the year

Will mortgages be hiked again if base rate rises?

The Bank of England is widely expected to increase the base rate from 5.25 per cent to 5.5 per cent on Thursday, though some economists are betting on it remaining the same.

The decision will come the day after we learn August’s inflation reading, which many are expecting may go up as a result of higher fuel prices. This may have some bearing on what the Bank of England decides to do with base rate.

If base rate does go up, this will likely increase costs for those on variable rate mortgage deals.

However, it is unlikely to have the same impact on fixed rate products, according to Nicholas Mendes, mortgage technical manager at broker John Charcol. In fact, he expects fixed rate deals to continue falling.

‘The MPC meeting is expected to either hold or rise by 0.25 per cent which will no doubt be the last [rate rise],’ says Mendes.

‘Even in the event there is a rate rise this has already been caked into fixed rate pricing.

‘As a result I expect to see fixed rate pricing on two and five year fixes continue to reduce.

‘While no one can accurately be confident, I wouldn’t rule out a five year fixed at 4.5 per cent by the end of the year based on current pricing trajectory.’

How are mortgage rates affecting the housing market?

While it is good news that mortgage rates are falling, we remain a long way from the low rates enjoyed in previous years.

This time last year, it was possible to secure a fixed rate at 3 per cent and the year before that borrowers were able to secure deals at less than 1 per cent.

The change in mortgage rates has unsurprisingly had an impact on the housing market. Transactions are down by almost 20 per cent, while house prices are also falling.

Last week it was reported that mortgage arrears had hit their highest level for nearly seven years.

The value of outstanding home loans with arrears climbed by 13 per cent to £16.9billion in the second quarter of this year, according to Bank of England figures.

It was the highest level since the third quarter of 2016, and 29 per cent higher than the same period a year ago.

Although there may be less activity across the housing market, Mendes says he isn’t expecting to see a sudden surge in forced sales.

‘Fixed rate mortgages around 5 per cent may dampen purchase demand as prospective home movers postpone their plans, but I still expect to see first-time buyers to continue purchasing,’ he says.

‘With rents continuing to increase, fixed rates at 5 per cent or less could encourage more first time buyers and those in rented accommodation to purchase as a cost-effective alternative.

‘A significant increase in arrears was down to landlords which is understandable in this climate over the past year.

Downwards: Over the past few weeks, mortgages rates have continued to trickle downwards due to competition between lenders and market expectations about interest rates in the future

‘For residential homeowners there are more options to avoid falling into arrears – unless they decide to bury their head in the sand.

‘There is more support from lenders and the Mortgage Charter which allows a grace period of six months which would allow mortgage holders to sell a property before things start to escalate downwards.’

Mark Harris, chief executive of mortgage broker SPF Private Clients, says that falling mortgage rates will result in buyers being able to afford bigger mortgages which should lead to an increase in transactions.

Harris adds: ‘Falling interest may encourage more borrowers to take the plunge and take on a mortgage. However, it is not just about falling mortgage rates but affordability and the underwriting of the loan.

‘Lenders are still required to stress test the borrowing at a minimum of 1 per cent above the reversion rate, with some lenders utilising different lower rates for long/longer term fixes.

‘When these stress rates also start to fall, borrowers will be able to take on bigger mortgages, which may lead to an uptick in transactions and mortgage lending.’

Zillow debuted its 1% down payment program on Thursday, agreeing to contribute an additional 2% at closing in an effort to “reduce the time eligible homebuyers need to save [money],” the real estate marketplace said in a statement.

“Most markets are in the midst of an affordability crisis, and saving for a down payment remains one of the biggest barriers for many potential homebuyers,” Zillow said — the same day mortgage rates in America hit their highest level since 2001.

Mortgage buyer Freddie Mac said Thursday that the average rate on the benchmark 30-year home loan climbed to 7.23% from 7.09% last week — significantly higher than just one year ago, when the rate averaged 5.55%, and more than double what it was two years ago.

The average rate on 15-year fixed-rate mortgages, popular with those refinancing their homes, rose to 6.55% from 6.46% last week. A year ago, it averaged 4.85%, Freddie Mac said.

It’s the fifth consecutive weekly increase for the average rate, which is now at its highest level since early June 2001, when it averaged 7.24%.

Zillow announced that it’s offering mortgages with a 1% down payment to US homebuyers who are being squeezed by mortgage rates that are more than double what they were just two years ago and their highest level since 2001.AFP via Getty Images

Zillow’s 1% program could also be a way to win back business after two years of declining sales. The company’s now-shuttered home-flipping business, Zillow Offers, lost a staggering $881 million in 2021.

For the entire fiscal year, the company posted a net loss of $528 million and laid off about 2,000 staffers, roughly 25% of its workforce. In 2022, Zillow reported $101 million in net losses and $1.95 billion in annual revenue — an over 8% dip from the previous year.

already unaffordable to many Americans. They also discourage homeowners who locked in low rates two years ago from selling.

The terms of Zillow’s down payment program are currently vague, though the real estate marketplace advised aspiring buyers to prepare for getting a mortgage by not closing any accounts and holding off on financing large new purchases.AFP via Getty Images

According to the National Association of Realtors, first-time homebuyers, on average, put down 6% of the purchase price at the time of closing, while repeat buyers typically put down 13%.

It’s a common misconception that buyers need to purchase 20% equity in their home at the time of sale, the association said, which has discouraged many aspiring homeowners from shopping around or applying for a mortgage.

The issues in the housing market are compounded by a lack of inventory as buyers who locked in lower borrowing costs from as recent as two years ago are now reluctant to sell and jump into a higher rate on a new property.

It’s a key reason new home listings were down nearly 21% nationally in July from a year earlier, according to Realtor.com.

Meanwhile, mortgage rates have been rising along with the 10-year Treasury yield, used by lenders to price rates on mortgages and other loans.

The yield has been climbing as bond traders react to more reports showing the US economy remains remarkably resilient, which could keep upward pressure on inflation, giving the Federal Reserve reason to keep interest rates higher for longer.

High inflation drove the Fed to raise its benchmark interest rate 11 times since March 2022, with the latest hike lifting the federal funds rate to a range between 5.25% and 5.5%.

The hike sent the benchmark rate to its highest point since 2001 — and Powell signaled that another increase is possible before the year’s out as officials continue to wrestle with stubbornly high inflation.

There are plenty of so-called experts and gurus out there with all types of advice on what you should do with your money, but perhaps the most celebrated is Warren Buffett, known affectionately as the “Oracle of Omaha.”

On Saturday, the 82-year old financial wizard held his annual shareholder meeting for Berkshire Hathaway in Nebraska’s largest city, which many refer to as “Woodstock for Capitalists.”

He talked about everything from politics to the economy to his personal life on Star Wars Day (May the fourth…), and every single word was taken as gospel by his loyal legion of followers.

Fox News also caught up with Buffett, who took the time to discuss the state of the economy with Liz Claman.

The most interesting tidbits (to me) were about housing and mortgages, something you may want to pay attention to if you’re thinking about buying a home or refinancing.

Buffett Says Get a Mortgage Today

One major takeaway from the interview was the line, “if you ever want to get a mortgage, today is the day to get a mortgage.”

If you’re wondering why he is so bullish on mortgages, it’s pretty simple. Mortgage rates are at or near all-time record lows, so you can borrow money on the cheap.

This low-rate environment explains why housing is so affordable at the moment, even though home price-to-income ratios are above historic norms.

Like anyone else with half a brain, he knows interest rates (including mortgage rates) will eventually rise, and so locking in a low fixed rate today is paramount.

He also said those who are borrowing money to finance a home should do so for a “long period of time,” meaning go with the 30-year fixed mortgage instead of the 15-year fixed.

Heck, one could even make an argument for a 40-year fixed mortgage if they’re comfortable investing elsewhere.

Why? Well, as I’ve discussed in other posts, most recently my mortgages vs. inflation post, the value of money erodes over time. And a fixed mortgage balance will be easier to pay off in the future with inflation-adjusted dollars.

For the record, Buffett expects inflation in the future thanks to the quantitative easing that has been keeping rates low for years now.

In other words, why pay off your mortgage as quickly as possible when rates have never been lower and money is expected to be worth less?

Why not take advantage of a low fixed mortgage rate for as long as you possibly can, seeing that we may never see them this low again.

Sure, this advice comes from a big-time investor who can easily beat the rate of return on a mortgage, but even amateurs can probably pull it off with rates so low.

[Pay off mortgage or invest?]

Good Time to Invest in Single-Family Homes

Speaking of investing, Buffett also noted that today is a good time to invest in a single-family home, though he did say, “It’s not quite as attractive as it was a year ago.”

Yes, home prices have increased from levels seen a year ago, but they’re expected to keep flying higher thanks to limited inventory, low rates, and other market factors.

However, Buffett believes that those who buy today should expect to stay put for a long period of time to do well in housing. Of course, Buffett isn’t a day trader, so his trades are never seen as short-term.

He’s not going to tell you to buy a home to flip a year from now, even if you could make a huge profit doing so.

Finally, Buffett spoke out about the mortgage interest deduction, which he doesn’t think is going anywhere.

Despite ongoing pressure from certain groups to eliminate the favorable tax break, he thinks it’s unlikely to be dropped, and if it is, it will be part of a larger piece of legislation.

So that’s that. Even Warren Buffett thinks it makes sense for you to buy a house and finance it with a mortgage, as if you needed another reason.

Looking to build wealth with the best income-generating assets? As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life. This is because you can invest in assets that will generate you income, earning you more passive income. Today’s article will introduce you to…

Looking to build wealth with the best income-generating assets?

As you set out on the path to financial freedom, understanding the different types of income-generating assets can truly change your life.

This is because you can invest in assets that will generate you income, earning you more passive income.

Today’s article will introduce you to a range of assets that reliably bring in cash, giving you peace of mind and the freedom to live life on your own terms.

From traditional investments like stocks and bonds to more creative options like peer-to-peer lending or real estate, income-generating assets give you the power to diversify your portfolio and build wealth over time.

Related content:

What are income generating assets?

Before we begin, I want to talk about the basics on income-generating assets, in case you are new to the subject or if you want a background first.

Income-generating assets are investments that, as the name suggests, generate income for you. These are assets that provide you with a steady cash flow, allowing you to earn passive income and build your wealth over time.

Examples include rental real estate and dividend-paying stocks (we will go over 17 different types of income-generating assets below in more detail).

There are several benefits of the best income-generating assets such as:

Passive income: You earn money without actively working, and this can provide financial freedom and the ability to focus on other things in life. You can earn money in your sleep, while on vacation, making dinner, and more.

Diversification: You can diversify your investments so that all of your income is not coming from just one source.

Wealth building: Earning income and generating a steady cash flow can help you build your wealth over time.

Note: Please keep in mind that there is no one-size-fits-all approach when investing in any of these income-producing assets. Everyone is different and while one asset may work great for someone, it may not be the right asset for you. I recommend doing as much research as you can if you are interested in one of the asset investments I talk about below.

Types Of Income Generating Assets

There are many types of income-generating assets. Some may be more traditional such as dividend-paying stocks, and others may be more alternative income-generating assets, such as selling stock photos, and even renting out your driveway.

Today, I will talk about 17 different types of income-generating assets, but this is not a full list of the best income-producing assets. There are many, many more!

The different types of income-generating assets that I will talk about today include:

1. Dividend-paying stocks

One of the best assets to invest in are dividend-paying stocks.

Dividends are simply a payment in cash or stock that public companies distribute to their shareholders.

The amount of a dividend is determined by a company’s board of directors, and they are given as a way to reward those who have stock in their company. Both private and public companies pay dividends, but not all companies pay dividends.

How do dividends work? If you own shares of a dividend-paying stock, then a dividend is paid per share of that stock. So, if you have 10 shares in Company ABC, and they pay $5 in cash dividends each year, then you will get $50 in dividends that year. While dividends can be paid on a monthly, quarterly, or yearly basis, they are most commonly paid out quarterly — so, four times a year. In this example, the $5 in cash dividends the company pays each year will most likely be distributed as $1.25 per quarter for each share of stock.

The most common type of dividends are cash dividends. Shareholders may choose to get this deposited right into their brokerage account. Stock dividends are another common type of dividend. In this case, shareholders get extra shares of stock instead of cash.

Both cash dividends and stock dividends are great income-generating assets that will earn more money for you.

As a shareholder, you can earn income when companies distribute profits to their shareholders. Look for stocks with a history of consistent dividend payouts and a high dividend yield. Keep in mind that dividend stocks are still subject to market fluctuations, and just because a company has paid a dividend in the past does not mean that they always will in the future.

Related content:

2. High-yield savings accounts and CDs

High-yield savings accounts and CDs are a great way to grow your savings, but most people have their money in accounts with low rates. Unfortunately, that means many of you are losing out on some easy money.

Savings accounts at brick-and-mortar banks are known for having really low interest rates. That’s because they have a much higher overhead — paying for the building, paying the tellers to help you in person at the bank, etc.

High-yield savings accounts offer an easy option for earning interest on your cash. Online banks often offer higher interest rates than traditional banks. As of the writing of this blog post, you can easily find high-yield savings accounts that can earn you above 4.00%.

Certificates of Deposit (CDs), another form of income-generating assets, are FDIC insured and provide a guaranteed interest rate over a specific term. Remember that access to your money is limited during the term of the CD. You will agree upon the term before putting your money in the CD. The terms typically vary in length from around 3 months to 5 years.

Money market accounts are also offered by banks and often with a higher yield than other types of savings accounts.

3. Real estate

Real estate is one of the most common income-generating assets that people think of.

Investing in rental properties is a popular way to generate steady cash flow. You can earn rental income from tenants, and properties typically appreciate in value over time.

Location and property management are important factors that can impact your return on investment.

By investing in real estate, you may be investing in residential properties, commercial real estate, short-term rentals, REITs, and more.

Recommended reading: How This Woman In Her 30s Owns 7 Rental Homes

4. Real estate investment trusts (REITs)

An REIT is a company that owns and manages income-producing real estate. They then sell shares to investors like stock.

By investing in REITs, you can make money in the real estate market without actually owning real estate.

So, if you don’t want to be a landlord, then this may be something for you to look into. This makes it much more passive than actually owning real estate and having to manage it.

You can even diversify your income stream with REITs by investing in different property types, such as residential homes, commercial office space, industrial, and retail store properties.

5. Bonds

Bonds are fixed-income investments that are issued by governments and companies. If you own a bond, you receive interest payments from borrowers on a regular basis.

An easy way to explain this is: When you buy a bond, you are giving someone a loan and they are agreeing to pay you back with interest.

Bonds with higher credit ratings are generally a safer investment but may offer lower interest rates.

6. Mutual funds

Mutual funds gather funds from investors to invest in stocks, bonds, or other securities. Basically, the funds are pooled together and there’s a fund manager who chooses the best investments.

Income-generating assets like this have multiple types of mutual funds available for multiple types of investors. Some of these fund types include bond funds, stock funds, balanced funds, and index funds.

Mutual funds typically have higher fees because they have fund managers who are actively trying to beat the market.

With a mutual fund, you get diversification because the fund manager mixes the assets in it.

7. Index funds and exchange-traded funds (ETFs)

ETFs and index funds are popular options for those who are looking to diversify their portfolio of income-generating assets.

This is because index funds and ETFs track a specific market index and invest in a wide range of stocks or other assets, instead of picking and choosing stocks in an attempt to beat the market. This is what makes them different from mutual funds.

They often have lower fees and higher diversification compared to actively managed funds.

8. Annuities

Annuities are long-term investments offered by insurance companies that give you a guaranteed income stream to build wealth. In exchange for a lump-sum payment or periodic contributions (such as monthly or annually), you’ll receive steady payments in the future.

The way it works is you pay premiums into the annuity for a set amount of time. Later, you stop paying premiums, and the annuity starts sending regular payments to you. Some are even set up to pay you back with a lump sum.

Annuities can be fixed or variable. A fixed annuity offers a guaranteed payment amount — which means a predictable income for you. As for a variable annuity, the payment amount does vary, depending on how the market is doing.

9. Websites and blogs

Starting a website can generate income through the money-making assets of advertising, affiliate marketing, or the sale of products and services.

Since I started Making Sense of Cents, I have earned over $5,000,000 from my blog through affiliate marketing, sponsored partnerships, display advertising, and online courses. These income-generating assets make sense for building wealth.

Blogging allows me to travel as much as I want, have a flexible schedule — and I earn a great income doing it.

Now, it’s not entirely passive, but I do earn semi-passive income from my blog.

You can learn how to start a blog in my How To Start a Blog FREE Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog

Day 2: How to decide what to write about (your blog niche!)

Day 3: How to create your blog (in this lesson, you will learn how to start a blog on WordPress)

Day 4: The different ways to make money with your blog

Day 5: My advice for making passive income with your blog

Day 6: How to get pageviews

Day 7: Other blogging tips to help you see success

Recommended reading: The 25 Most-Asked Blogging Questions To Get You Started Today

10. Royalties and intellectual property

Intellectual property, such as patents, copyrights, and trademarks, can generate income through licensing fees or royalties. This particular option is good for creative professionals, such as authors, musicians, and inventors, who are looking for income-generating assets.

Royalties are a way to earn income from your creative work or intellectual property. By granting others permission to use or distribute your intellectual property, you can receive ongoing payments known as royalties.

Whether you’re a musician, author, inventor, or artist, royalties offer a passive income stream as your creations continue to generate revenue over time.

Royalties can be paid out periodically or as a lump sum on these passive income assets, depending on your agreement with the licensee.

11. Stock photos

If you have a talent for photography, you can monetize your skills by selling stock photos on platforms such as Shutterstock or Adobe Stock. The more high-quality images you upload, the more potential passive income you can generate.

With stock photography, you simply upload photos that you have taken to a platform such as DepositPhotos, turning your pictures into income-generating assets. Then, you will receive a commission whenever someone buys one of your stock photos.

Stock photos are used for all sorts of reasons by websites, companies, blogs, and more. Businesses need stock photos because they are not usually in the business of taking photos of everything that they need. Instead, they can use stock photos to make their content, website, or business more visually appealing.

Some examples of stock photography include pictures of:

Travel, vacations, landmarks, outdoor adventures

Family members, such as parents, children, family gatherings

Food and drink

Cars, boats, RVs

Businesses, pictures of people in meetings, in an office.

Sports, professional events

Animals, such as household pets or wildlife

The photo possibilities are almost endless for this type of income-generating asset.

Recommended reading: 18 Ways You Can Get Paid To Take Pictures

12. Crowdfunding and peer-to-peer lending

Crowdfunding platforms enable you to invest in real estate deals with a smaller amount of money than buying real estate up front, giving you a passive income through rental income or even a property increasing in value.

Peer-to-peer lending platforms allow you to lend money directly to borrowers. Typically you can earn higher returns than traditional savings accounts, though there’s always the risk of a borrower not paying you back.

Both of these types of assets — crowdfunding and peer-to-peer lending — use technology to connect investors with those looking for funding.

13. Renting out storage space

If you own unused land or unused space in your home, renting it out for storage can be a simple way to generate passive income.

You can offer storage solutions for vehicles or boats. If you have a smaller space, then offer it to store personal belongings. You can rent out your driveway, closet, basement, attic, and more. You can even rent out a shelf.

A website where you can list your storage space is Neighbor. You can earn $100 to $400+ each month on this platform. This depends on the demand in your area and the type of income-generating assets you are renting out. And, you can choose who, what, and when — who to rent to, what things are stored, and when it will happen.

You can learn more at Neighbor Review: Make Money Renting Your Storage Space.

14. Short-term rentals

Short-term rentals can be a lucrative income-generating asset if you own properties in popular tourist destinations or business hubs.

Websites like Airbnb provide a platform to rent out your property to travelers for short periods, potentially generating higher returns than traditional long-term leases.

Furnished Finder is another website for short-term rentals. This is a way to connect with travel nurses in need of short-term housing.

Keep in mind that rental income can be affected by local regulations, potential vacancies, or seasonal fluctuations.

15. Car rentals

Car rental platforms like Turo allow you to rent out your car when you’re not using it. Assets that generate cash flow include your own wheels, and that means no significant initial investment besides the cost of the car you already own.

Be mindful of risks such as wear and tear, insurance, and potential damage caused by renters.

It’s an affordable alternative to traditional rental car companies for customers, and it’s a good way to make money if you’re already working from home and don’t need your car, or are a two-car household.

Turo is one of a few different places to rent out your car, turning your vehicle into one of your income-generating assets. Your car is covered by Turo with up to a $1 million insurance policy. You can also pick the dates for when your car is available and set your rates.

Turo says you can earn an average of $706 per month by listing your car on their site.

16. RV rentals

Similarly to car rentals, RV rentals can provide additional income by renting out your recreational vehicle when you’re not using it. Your RV could easily become one of your income-generating assets.

You may be able to earn $100 to $300 a day, or even more, by renting out your RV on RVShare.

If you have an RV that is just sitting there and not being used, then you may be able to earn an income with it by renting it out to others who are interested in RVing. Cash flow-generating assets like RVs are a win-win for both you and the renter who wants to experience life in a recreational vehicle.

You can learn more at How To Make Extra Money By Renting Out Your RV.

17. Vending machines

With a vending machine business, you can generate income by selling a variety of products, from food to fishing supplies, beauty products to baby items, and more.

You may be able to earn $1,000+ a month by running a vending machine business. That’s enough reason to take a closer look at income-producing assets like this.

You can learn more at How To Start A Vending Machine Business – How I Make $7,000 Monthly.

Questions about income generating assets

Here are common questions that you may have about income-generating assets:

How do I start passive income from nothing?

Starting passive income from nothing requires creativity and resourcefulness. You can begin by identifying skills you possess or interests that can be turned into income-generating opportunities.

What are the assets that generate income?

The assets I talked about above include:

Dividend-paying stocks and stock market investing

High-yield savings accounts and CDs

Real estate

Bonds

Mutual funds

Index funds and exchange-traded funds

Annuities

Websites and online businesses

Royalties and intellectual property

Stock photos

Crowdfunding and peer-to-peer lending

Renting out your storage space

Car rentals

RV rentals

Vending machines

How do I start buying income generating assets?

There are traditional investments or more creative options. Do as much research as you can before deciding which option fits you best.

What are good assets to buy?

After deciding if you want to purchase traditional investments or more creative options, choose an asset that you can afford and best fits your lifestyle.

What are the best assets to buy for beginners?

For beginners seeking income-generating assets, you may want to look into:

Dividend-paying stocks for your investment portfolio

Crowdfunded real estate investing: Platforms like Fundrise allow smaller investments with lower risk exposure.

ETFs and index funds: They provide diversification and passive income through dividends.

What is income generating real estate?

Income-generating real estate refers to properties that produce regular rental income, such as apartments, commercial properties, or short-term vacation rentals.

How do I start passive income in real estate?

There are a few ways that you can earn passive income from real estate, including:

Buying a property, such as an apartment building or duplex, and renting it out to tenants

Using real estate crowdfunding platforms

Investing in REITs

How to make passive income with real estate without owning property?

You don’t need to actually own property in order to make money with real estate. Instead, you can earn passive income from real estate by investing in REITs and using real estate crowdfunding platforms.

This is an option for those who want to be diversified with their income-generating assets but don’t want to spend all of their money or time on a single piece of real estate.

How to make $1,000 a day in passive income?

Making $1,000 a day in passive income with assets that produce income will not be easy. If it were easy, then everyone would be doing it, after all.

Making $1,000 a day in passive income may require a large amount of money up front, diversifying into different assets mentioned above, and lots of patience from you because it will take time to make that kind of money.

You may want to start off by focusing on building multiple income streams and reinvesting your profits as you earn them.

What to think about before investing in income producing assets?

There are many different things to think about when it comes to income-generating assets. You want to find the best assets to invest your money in that will also be the best fit for you.

Remember, as I said at the beginning of this article, not everything will be applicable to everyone. Everyone is different! You may prefer to create a stock photo portfolio and hate real estate, whereas someone else may really enjoy being a real estate investor — or it may even be the other way around.

Here are some of my tips if you are interested in income-generating assets:

Do your research and talk to experts —I recommend researching as much as you can on the asset you are interested in. And, if you still have questions, don’t be afraid to talk to an expert.

Diversify — One of the important parts of building a successful income-generating portfolio is finding ways to be diversified.

Think about the risks —When making money, there’s usually some sort of risk. I recommend evaluating the risks and seeing what you are comfortable with.

What are the best books on income generating assets?

Some highly recommended books on income-generating assets include:

The Simple Path to Wealth by JL Collins

The Millionaire Real Estate Investor by Gary Keller

The Little Book of Common Sense Investing by John C. Bogle

Income Generating Assets — Summary

I hope you enjoyed this article on the best income-generating assets. As you learned, there are many different types of assets that you can invest in so that you can earn an income.

The best income-producing assets, if they’re right for you, can truly change your life.

With these assets, you can build wealth through a reliable passive income, giving you peace of mind and freedom to live life on your own terms.

Are you looking to build income-generating assets? What are your favorite ways?