When most people think about what it’ll be like to buy their first home, they think about their ideal floor plan or how they want to decorate their home. But before you can even get to that point, you need to make it through the underwriting process.

During the underwriting process, your mortgage lender evaluates whether you’re a good candidate for a mortgage. Going through underwriting may sound intimidating, but knowing what to expect can make the entire process run more smoothly.

What is mortgage underwriting?

Mortgage underwriting is simply a method used by your lender to assess your eligibility for a mortgage loan. This evaluation is performed by reviewing your credit, conducting a comprehensive analysis of your finances, and appraising the property.

After this, the lender will determine if you’re a suitable candidate for the loan. The majority of this process occurs discreetly, but your participation is vital.

As the borrower, it’s your responsibility to furnish your lender with all the financial information they require. By being transparent and forthcoming with information, you facilitate the lender’s decision-making process and increase the chances of approval for your mortgage application.

What does a mortgage underwriter do?

A mortgage underwriter’s role is to evaluate risk and assess if you’re a suitable candidate for a mortgage loan. They analyze your financial information to determine the likelihood of you defaulting on your mortgage payments.

The underwriter focuses on four key areas in their assessment: credit, assets, income, and the home appraisal. Let’s take a look at what they consider in each area:

Credit: Your credit score is a major factor in the underwriting process. A high credit score indicates a strong track record of repaying debt and could increase your chances of getting approved for a mortgage. To qualify for a mortgage, you must have a minimum credit score of 620, but to secure the best interest rates, you should aim for a score of 740 or higher.

Income: Your lender will want to see evidence of a stable source of income to ensure that you can make your monthly mortgage payments. You can verify your income by providing W-2s, bank statements, tax returns, and if self-employed, business tax returns and profit and loss statements.

Assets: To mitigate the risk of default, your lender will consider all your assets, which can act as collateral. Relevant assets include savings, retirement accounts, stocks, and investment properties. A substantial number of assets also shows the lender that you have the means to cover your down payment and closing costs.

Appraisal: Before finalizing the mortgage, the lender will perform an appraisal of the property to ensure that you’re not overpaying. An appraisal protects both you and the lender by providing a fair assessment of the home’s value.

5 Steps of the Mortgage Underwriting Process

The underwriting process can feel pretty overwhelming when you’re in the beginning stages. Here is an overview of the five steps you’ll need to take to purchase your home.

1. Get preapproved for a mortgage

The first step in the home buying journey is securing preapproval for a mortgage. This crucial step should be taken before starting the search for a house. The preapproval process involves an evaluation of your financial information and a credit check by your lender.

Documents like bank statements, tax returns, and employment verification must be submitted to the lender. Upon preapproval, your lender will issue a letter indicating the amount you have been approved to borrow.

Getting preapproved is important as it gives a clear picture of your budget for the home purchase. Additionally, having a preapproval letter enhances the credibility of your offer and makes you a stronger candidate in the eyes of listing agents and sellers.

2. Get your home appraised

With preapproval for your mortgage in hand, it’s time to start your search for your dream home. Once you’ve found it, a home appraisal is the next step.

A professional appraiser will assess the value of the property based on its location, neighborhood, and features, ensuring that you don’t end up borrowing more than the home’s actual worth.

3. Perform a title search

Before purchasing a home, it’s essential to check for any existing claims, unpaid taxes, or liens. After the appraisal of the property, the title company will conduct a thorough search to ensure its clear legal standing.

Upon confirming that the property is free from any legal disputes, the title company will secure a title insurance policy. This insurance provides protection for the lender and verifies the home’s eligibility for purchase.

4. Find out whether you’ve been approved for a mortgage

Once your mortgage loan application has gone through underwriting, you’ll find out if you’ve been approved for a mortgage. Hopefully, your application is approved, and you’ll be all set to close on your home.

However, you could receive one of the following three decisions:

Approved with conditions: Your mortgage application may be approved on the condition that you provide additional information. For instance, you may need to provide more financial documents or further proof of employment.

Denied: The lender may reject your loan application. If this happens, you want to understand why so you can figure out your next steps. For instance, you might have been turned down because your debt-to-income ratio is too high. Or your credit score may have been too low. Knowing this information gives you tangible steps you can take to improve your finances and reapply in the future.

Suspended: Your loan application may get suspended if something is missing from your file. If this happens, the lender will let you know what information they need to continue the underwriting process.

5. Close on your home

Once your lender has cleared any loan contingencies and locked in your interest rate, you’re free to close on your home. Once you’ve closed on the mortgage and received the keys to your new home, the loan process is finished.

How long does the underwriting process take?

There really is no standard time frame to complete the underwriting process; it can take from a few days to a few weeks. The length of time depends on the type of home loan you’re applying for and any issues that arise along the way.

A lot of this will be outside your control, but there are steps you can take to make the experience easier. The best thing you can do is to respond quickly to any requests from your lender.

For instance, if they contact you and request additional bank statements, then try to provide that information as quickly as possible. The underwriting process cannot proceed without this documentation.

What can I do to ensure a smooth underwriting process?

To prepare for the mortgage underwriting process, it’s essential to compile all the required documents and verify the accuracy of your credit report. Additionally, ensure your income and work history are recent and correct and follow these guidelines:

Manage your debt level: Avoid incurring new debt or making significant financial changes that may impact your debt-to-income ratio during the loan processing period.

Stay connected with your lender: Respond promptly to any questions or requests for additional information during the underwriting process. Utilize online resources to stay organized and easily communicate with your mortgage loan officer.

Be transparent about your finances: Provide accurate and complete information about your income, credit history, and assets. If there are any discrepancies, include explanations for them to help the underwriter make a faster decision.

By keeping these tips in mind, you can make the mortgage underwriting process easier and increase your chances of becoming a homeowner.

Bottom Line

During the mortgage underwriting process, your lender assesses your financial information and decides whether you meet the criteria for a loan. For first-time homebuyers, this stage can be overwhelming, but there are steps you can take to simplify the process.

Take the time to carefully compare and choose your lender, opting for one that is willing to support you and provide you with the best terms possible. Additionally, collaborating with a well-informed real estate agent can make the journey smoother.

Don’t be discouraged if your credit score is lower than you’d like. There are many mortgage programs available that are designed to assist borrowers with bad credit. With these options, buying your first home can still be a possibility.

That didn’t take long. Just a few months after housing experts predicted a soft recovery, their pessimism has quickly turned into optimism.

Per the latest Zillow® Home Price Expectations Survey, which comes from 113 economists, market strategists, and housing experts, home prices are expected to rise 2.3% in 2012.

That’s up from a previous forecast of -0.4% in the June survey. Yes, just three months ago, depreciation was the word on the street, even though the bottom was largely agreed upon.

The most optimistic respondents in the latest survey predict home prices rising 4.4% this year, while the most pessimistic see an average increase of just 0.3%.

The group also upped their home price appreciation predictions for 2013 through 2016, meaning we should see steady growth for years to come.

Zillow Chief Economist Dr. Stan Humphries noted that the group hasn’t been this bullish since mid-2010, when the homebuyer tax credit boosted demand artificially.

Humphries even referred to it as “further evidence” of an “organic recovery,” though you have to wonder if he’s forgetting about the mortgage rate manipulation taking place at the Fed.

Sure, the correlation between home prices and mortgage rates is a tricky one, but you have to assume demand has risen as a result of the unprecedented low rates on offer.

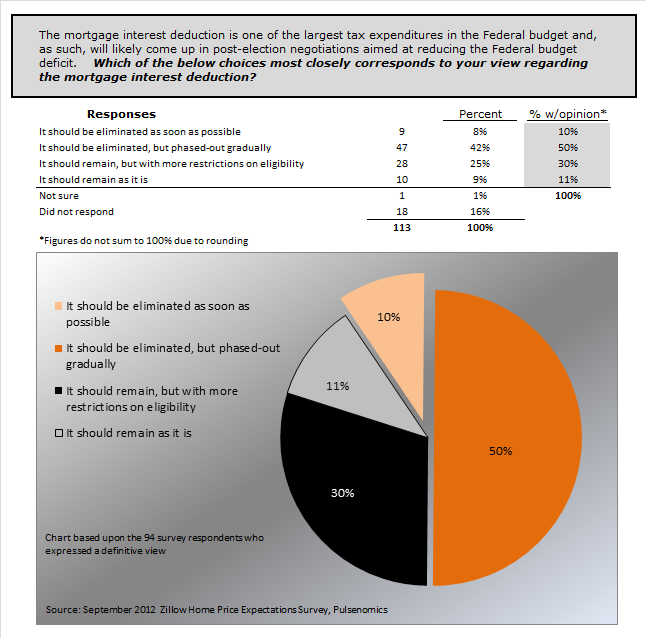

Most Want Changes to Mortgage Interest Deduction

Zillow also asked what should be done about the now under-fire mortgage interest deduction.

About half of respondents believe it should be eliminated, but phased out over time, while 10% feel it should be eliminated as soon as possible.

Another 30% believe it should remain, but with more restrictions, and 11% think it should remain intact as is.

While changes may be advisable, you have to wonder if messing with anything right now that could diminish homeownership would be the right move.

The problem is it supposedly costs the federal government about $90 billion a year, and certainly helps homeowners disproportionately.

Eminent Domain and Politics

The issue of eminent domain and political leanings were also included in this edition, with an overwhelming 91% against the former.

As for politics, 34% said they were voting for Obama, and 45% were on Romney’s side. Another 20% were undecided, and leaning in either direction.

Regardless of which candidate they favored, 47% felt Obama would promote “more significant” housing policy changes, compared to just 21% in the Romney camp.

[See: Romney’s Housing Plan for more on that.]

However, 25% felt Obama’s initiatives would impair the housing market, while just 17% felt his policies would bolster the market.

An even greater percentage (27%) felt his policies would have no meaningful effect whatsoever.

And they’re probably right. For the most part, many of the weapons in the arsenal have already been fired, including Hope Now, HAMP, HARP, HARP 2, and many other programs.

The only biggie missing is a program for private-label mortgages, which likely wouldn’t happen without bipartisan support.

Additionally, now that optimism has returned to the housing market, you have to wonder if any wildcards that haven’t been played will be.

Obama may have had an ace up his sleeve, but if confidence has already returned to the market, there may be no need to exercise such an option.

We know mortgage rates are going to stay low, longer, thanks to the Fed’s new QE3 initiative, and with home prices on the up, more underwater borrowers will be able to unshackle themselves from their negative equity problems.

So it may be reasonable not to expect any more support from the government on the housing front.

Read more: Why your mortgage may get more expensive.

Mortgage rates that spiked last year have continued to rattle Colorado Springs’ housing market in 2023.

In September, for example, year-over-year home sales fell for the 16th consecutive month, a recent Pikes Peak Association of Realtors market trends report shows.

Homeowners who were able to sell their properties within days — and even hours — two to three years ago waited more than five weeks, on average, last month for a buyer to come along, according to the report.

A Pikes Peak Regional Building Department report shows that while single-family building permits — which signal the construction of new homes — rose modestly in September compared with the same time last year, last month’s total nevertheless was the lowest for any September since 2011 and continued a mostly weak trend of building permit numbers for the year.

“The market was dramatically affected by the rapid, historical increase in mortgage rates,” said Gordon Dean, a real estate agent with Re/Max Advantage in Colorado Springs and the incoming board chairman of the Pikes Peak Association of Realtors.

From mid-2019 through 2021, 30-year, fixed-rate mortgages — the most common loan for homebuyers —plunged to an average of 3% and below nationally, according to mortgage buyer Freddie Mac.

Those historically low rates fueled homebuying nationwide and, combined with a shortage of new and existing properties available for purchase, sent home prices to record highs in markets such as Colorado Springs. Home sellers often fielded multiple offers for their properties and frequently received bids that topped their asking prices by thousands and tens of thousands of dollars.

When 2022 began, 30-year, fixed-rate loans averaged 3.22% nationally, Freddie Mac figures show.

After the Federal Reserve began to hike interest rates last year to curtail soaring inflation, however, mortgage rates began a steady ascent. By year’s end, after briefly topping 7%, long-term mortgage rates stood at 6.42%.

Long-term rates stayed below 7% for much of this year, but began to climb again in late summer. By mid-August, 30-year, fixed-rate mortgages had jumped again; on Thursday, they rose to a national average of 7.57%, which was the highest since 2000.

“Several factors, including shifts in inflation, the job market and uncertainty around the Federal Reserve’s next move, are contributing to the highest mortgage rates in a generation,” Sam Khater, Freddie Mac’s chief economist, said in a news release this month. “Unsurprisingly, this is pulling back homebuyer demand.”

And because many homebuyers felt priced out of the market because of higher rates or they no longer could qualify for a mortgage, the pace of buying, selling and construction slowed in Colorado Springs and the Pikes Peak region, along with other areas nationwide.

“I think it’s a good market because the demand is high,” said Grace Covington co-owner and co-CEO of Covington Homes, a Springs builder.

“We have a lot of people who are ready, willing and want to buy, (but) just not able because of interest rates.”

With the third quarter in the books, here’s a snapshot look at where conditions stand for Colorado Springs’ single-family housing market:

• Home sales have fallen and can’t get up — or so it seems.

Space Command decision expected to positively impact Colorado Springs real estate market

In September, Colorado Springs-area home sales totaled 1,008, a 22.1% decline from the same month last year, the Realtors Association’s market trends report and Gazette historical data show. Likewise, last month’s total was the fewest number of home sales for any September since 2013.

“That’s not much, literally,” real estate agent Harry Salzman of Salzman Real Estate Services and ERA Shields Real Estate said of September’s sales.

Other numbers in the association’s market trends report and Gazette historical data that underscore the slowdown in sales: Year-over-year home sales have dropped each month since June 2022; sales for the first three quarters of this year totaled 9,402, a 24% drop from the same period a year ago; and year-to-date sales for 2023 are at their lowest point since the same period in 2014.

Also, homes spent an average of 38 days on the market before selling in September, up from 25 days a year ago.

• Pickings still are relatively slim when it comes to finding a home to purchase.

The supply of homes listed for sale at the end of September totaled 2,484. On the one hand, that total rose 2.6% over August and was the highest for any month since October of last year.

Yet, from a historical standpoint, inventory is low. In pre-Great Recession years, September listings routinely topped 4,000, which provided homebuyers with many more choices, Gazette historical data show.

Residents in Colorado Springs’ outlying areas watch as growth creeps closer

Some owners who bought their properties or refinanced when mortgage rates were in the 3% neighborhood and are considering selling are holding on to their properties for now, which has contributed to the tight inventory, real estate experts say.

Sure, those homeowners might want to move up or downsize, but they’re not willing to abandon their rock-bottom mortgage rate and take on a new loan that’s in the 6% to 7% range, the experts say.

At the same time, some homebuyers who purchased in 2021 or 2022 haven’t seen their values appreciate enough to a point where they can sell their property and get the price they need to pay off their mortgage and real estate costs, said Patrick Muldoon, broker/owner and president of Colorado Springs real estate company Muldoon Associates.

As a result, those homeowners aren’t selling, he said. Instead, they’re calling the property management side of his business, Muldoon said, and looking to rent their homes. That keeps those properties from being added to the overall inventory of houses for sale.

“I can’t sell my house or I tried to sell my house or I’m upside down on my house and my next option is, I’m a forced landlord,’” Muldoon said he’s hearing from some homeowners.

• Despite slow sales, home prices rose in September.

The median price of homes that sold last month rose to $475,000, a 3.3% year-over-year increase, the Realtors Association report shows. It was the first year-over-year increase in median prices since November 2022.

But if sales fell in September, why did prices increase? Blame tight inventory, Salzman said.

“It’s got to be supply and demand. Not a doubt,” he said. “We don’t have very many selections for people to take a look at, no matter what the price range is. Particularly, even if you’re, say, under $500,000 in a purchase price? There’s not much inventory to select.”

As a result, some sellers can list their homes at prices that are a little more aggressive than a few months ago, Salzman said.

“You’re going to get a better price today because if you’ve got a buyer today at these interest rates, they’re a motivated buyer,” he said. “And when you’re a motivated buyer, sometimes you might have to pay a little more, like we did a couple years ago, because there’s no inventory.”

Sign up for free: News Alerts

Stay in the know on the stories that affect you the most.

Success! Thank you for subscribing to our newsletter.

5 growth hotspots around Colorado Springs: A closer look

Muldoon suggested that the latest figures showing an increase in median prices in September might be misleading. Some of the homes that sold last month are on the high end of the price range, which pushed up the overall median price, he said.

A real estate agent friend told him “we’re only grading the winners,” Muldoon said. “We’re looking at the stats and we’re only grabbing the houses that have sold, and those houses that have sold are the upper end of the bell curve.”

And some sellers still are getting top dollar for their properties, even as the market has cooled.

Attractive properties that are in good condition and priced correctly to reflect the current market and comparable homes in their neighborhood still can receive multiple offers — just not nearly as many as a few years ago, said Dean, of Re/Max Advantage.

“When you can provide someone in a desirable school district and great condition and, hypothetically, a stucco rancher with three bedrooms on the main (floor), that is a golden goose egg in the marketplace and I would be shocked if, priced correctly … it’s probably going to draw multiple offers,” Dean said.

In fact, he said he and his wife, Amy, who’s also a real estate agent, marketed a home that fit that description — and fielded a cash offer that came in about $15,000 over the seller’s asking price.

• The new home side of the housing market also has felt the effects of high mortgage rates.

In September, building permits issued for the construction of single-family, detached homes totaled 136, a slight, 1.5% increase over the same month a year earlier, according to the Pikes Peak Regional Building Department. That figure doesn’t include townhomes, condominiums or duplexes.

As Colorado Springs grows, 20-somethings are the fastest growing cohort

Even with last month’s increase, and an inflated number of permits that builders pulled in June in advance of a building code change taking effect, single-family permits for the first nine months of 2023 totaled 1,791 — a nearly 35% nosedive from 2,738 during the same period in 2022.

“The interest rate environment is certainly the main culprit for that,” said Tom Hennessy, president and CEO of Challenger Homes, one of Colorado Springs’ largest builders. “When you have interest rates pushing 8%, you’re just making affordability that much more difficult for that many more people.”

The difficulty in affording today’s higher mortgage rates stands in contrast to a generally positive outlook for the Springs, Hennessy said.

“What’s really kind of interesting is, there’s still people looking (for homes) and Colorado Springs’ economy is still generally pretty good,” he said. “Unemployment is still low. We still have a lot of jobs moving in. We have a lot of military in and out of the area. People want to buy. It’s just of matter of can they buy?”

Not only have buyers been stymied by high mortgage rates, but their costs for consumer goods, utilities and other expenses have soared because of inflation, said Covington, who’s co-CEO and co-owner of her homebuilding company with her husband, Ron.

Businesses saddled with high interest rates for loans have passed on their increased costs to consumers, which also affects their personal finances and their ability to buy homes, Grace Covington said.

“We really just need to get inflation under control and rates down again,” she said.

For now, Challenger, Covington and other builders continue to woo buyers with mortgage rate buydowns — incentive programs in which they effectively reduce, or buy down, a mortgage rate for the first few years of a loan to help buyers afford monthly payments and get them into a new home.

A year ago, builders also might have offered incentives such as discounts on premium lots or reduced prices on home upgrades to interest a buyer, Hennessy said.

Now, however, mortgage buydowns are the main focus for builders, he said.

“Today, it pretty much all deals with house payment and buying down the mortgage rate,” Hennessy said.

“The name of the game today is house payment. How can I get into a house with a payment that I can afford?”

• What’s ahead for Colorado Springs’ housing market?

That’s a question that every real estate agent and builder wants to know.

Who Are We? What the population numbers for El Paso County and Colorado Springs show

Salzman advices homebuyers who can afford a home to take the plunge now, even if prices remain high. The value of their investment always will appreciate over time, he said, and today’s 7% mortgage can be refinanced lower when rates fall.

Even if rates are high today, Salzman suggests that buyers talk with their mortgage lender to ask about getting a break on their loan origination fee in exchange for agreeing to refinance with the same lender in two to three years.

“Because their business is way down, anything is negotiable,” Salzman said of mortgage lenders.

A drop in mortgage rates, not surprisingly, would help boost sales and the overall market, Dean said. But how far would rates have to fall?

Six percent and below, he said, would help encourage borderline buyers to jump back into the market and persuade owners with a low mortgage rate to feel comfortable leaving it behind and accepting a higher rate to get the home they want.

“If we do see a reasonable drop, and I say reasonable, 6 flat on interest rates, we’re going to have a very robust market again,” Dean said.

Colorado Springs’ ‘beating heart?’ Check the pulse of downtown, mayor and area backers say

“For me personally, at the end of the day … it’s that interest rate that’s going to be the main driver for anybody,” he added. “Affordability. That’s affordability, in my opinion.”

Muldoon, however, echoed his previous bearish comments on the outlook for the housing market.

A recession in 2024, waves of layoffs, more bank failures, continued high interest rates and other national economic forces could have a ripple effect on local businesses and employers in Colorado Springs, Muldoon said. As a result, the local housing slowdown could continue and even worsen — with falling prices being one of the biggest impacts, he said.

“If Colorado Springs started showing signs of economic issues,” Muldoon said, “then you would see sellers start with some pretty swift reductions on prices.”

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

The proposed merger between Bank of America and mortgage lender Countrywide took another big step forward after the Federal Reserve gave the takeover bid its blessings.

During a public comment period, nearly 150 people testified at hearings and another 770 submitted comments via oral testimony and/or written statements.

Those in support of the deal praised Bank of America for its commitment to local communities and its favorable, affordable mortgage programs.

Those opposed were concerned with Bank of America’s large share of national deposits, its monopoly of the loan origination and servicing sector, and the safety and soundness of such an acquisition.

Most who commented also urged BofA to develop a loss-mitigation plan to deal with the scores of borrowers facing foreclosure, and criticized the way the pair served minorities.

Despite the criticism, the Fed concluded that the mortgage servicing industry would remain “unconcentrated,” and that the merger wouldn’t have a substantial adverse affect on the competitive nature of the banking sector.

Although the transaction would make Bank of America the largest servicer and originator of mortgages in the United States, the Fed believes enough competition remains because of other large players like Wells Fargo and Chase.

Additionally, the Fed noted that Bank of America has a good track record when it comes to taking over large institutions, and its well-balanced mix of loan programs and community involvement prove its commitment to promoting positive homeownership.

While the Fed decision is clearly good news, the takeover is still subject to a shareholder vote, set to take place on June 25, with Countrywide executives unanimously recommending a “yes” vote.

If the deal is consummated as expected, Bank of America would remain the largest depository organization in the nation, with roughly $1.9 trillion in assets and deposits of about $773.4 billion, or 10.91 percent of total insured deposits in the U.S.

Due to the financial challenges created by the COVID-19 pandemic, federal student loan payments were automatically paused from March 2020 to September 2023. During that time, interest didn’t accrue and collections activities were also paused. But now that payments are due again, many borrowers are looking for ways to make their loans more manageable, especially those who are facing ongoing financial hardships.

One option is student loan deferment, which allows you to temporarily pause your student loan payments. As with most financial decisions, there are pros and cons to deferring your student loans. Here’s more information about student loan deferment and what it could mean for your financial future.

What Is Student Loan Deferment?

Deferment is a program that allows you to temporarily stop making payments on your federal student loans or to temporarily reduce your monthly payments for a specified time period.

This is similar to another option known as forbearance. However, unlike forbearance, you may not be charged interest while your loan is in deferment. According to the Department of Education, if you hold one of the following types of loans, you will not be responsible for paying interest on your loan while it is in deferment:

• Direct Subsidized Loan

• Subsidized Federal Stafford Loan

• Federal Perkins Loan

• The subsidized portion of a Direct Consolidation Loan

• The subsidized portion of a Federal Family Education Loan (FFEL) Consolidation Loan

If you have one of the following types of loans, you will be responsible for paying the accrued interest on your loan while it is in deferment:

• Direct Unsubsidized Loan

• Unsubsidized Federal Stafford Loan

• Direct PLUS Loan

• FFEL PLUS Loan

• The unsubsidized portion of a Direct Consolidation Loan

• The unsubsidized portion of a FFEL Consolidation Loan

If you are responsible for paying interest on your student loans while they are in grad school deferment, you have two options: 1) you can make interest-only payments on the loans while they are in deferment; 2) if you choose not to make these interest-only payments, the accrued interest will capitalize (be added to the loan principal) when the deferment period is over. 💡 Quick Tip: Ready to refinance your student loan? With SoFi’s no-fee loans, you could save thousands.

How Do You Qualify for Student Loan Deferment?

In order to qualify for student loan deferment, you must meet one of the following requirements:

• You’re enrolled at least part-time at a qualifying university

• You’re unemployed or unable to find employment (for up to three years)

• You’re experiencing an economic hardship

• You’re currently volunteering in the Peace Corps

• You’re on active-duty military service (or are in the 13 months following that service)

• You’re in an approved graduate fellowship program

• You’re in an approved rehabilitation program (for disabled students)

Requesting a Deferment

If you’re interested in deferring student loans to go back to school, you’ll need to apply for an in-school deferment. Most likely, you will request the deferment directly through your loan servicer—there is usually a form for you to fill out. When you request a deferment, you’ll also need to provide some sort of documentation to prove that you qualify for a deferment.

If you are enrolled in an eligible college or career school at least half-time, may be placed in deferment automatically . If it is, your loan servicer will notify you that deferment has been granted. If you enroll at least half-time and do not automatically receive a deferment, you will need to contact the school in which you are enrolled. The school will then send the appropriate paperwork to your loan servicer, so that your loan can be placed in deferment.

Pros and Cons of Student Loan Deferment

The biggest benefit of student loan deferment is the ability to temporarily postpone student loan repayment. As of the first quarter of 2023, 2.8 million loans were in deferment.

If you are deferring for extreme financial hardship, deferment allows you to free up money to pay off bills that require immediate attention like rent or electricity.

For students who have qualified for deferment through community service, like a stint in the Peace Corps, deferment gives them the opportunity to serve their community without any added stress from student loan payments.

While temporarily pausing loan repayment may seem like a blessing, it can come at a cost, especially if your student loans are not subsidized by the government. When in deferment, interest continues to accrue on your loan. And at the end of your deferment period, that interest will be capitalized on the loan. (This means that the accrued interest will be added to the principal balance of the loan. So ultimately, you’ll be paying interest on top of interest.)

This can mean you end up paying even more money over the life of the loan. To see how much deferring your student loans could cost, you can use an online calculator to get an estimate of how much interest will accrue while the loan is in deferment.

The Pros and Cons to Student Loan Refinancing

If you have private loans that aren’t eligible for federal student loan deferment, refinancing your student loans is another option to consider. You may also want to think about refinancing when you’re done with your graduate degree to pay off your loans at a potentially lower interest rate.

When you refinance, your existing student loans are paid off with a new loan from a private lender. If you are refinancing private loans before going back to graduate school, you may be after a lower monthly payment, which you could potentially qualify for when refinancing your loans and extending the loan term. (You may pay more interest over the life of the loan if you refinance with an extended term.)

Alternatively, if you’re looking to refinance after graduate school, you could potentially qualify for a lower interest rate, which could reduce the amount of money you spend over the life of the loan. The lender will use your credit score and earning potential to determine what interest rate you’ll qualify for. And thanks to your new graduate degree, you could have significantly increased your earnings.

Another big benefit of student loan refinancing? You’re able to combine all of your student loan payments – for both federal and private loans – into one easy-to-manage payment.

If you hold only federal student loans, however, you could look into a Direct Consolidation Loan , which allows you to consolidate federal loans into one loan with a single monthly payment. The new interest rate will be the weighted average of your current interest rates (rounded to the nearest one-eighth of 1%), so unlike refinancing, when you consolidate your student loans, you won’t necessarily qualify for a lower interest rate.

If you are taking advantage of your federal loans’ flexible repayment plans or student loan forgiveness programs (or if you are planning to do so), refinancing might not be the best option for you. A major con of student loan refinancing is that you’ll lose access to federal loan benefits when refinancing with a private lender—including deferment and income-driven repayment plans.

Refinancing Your Loans with SoFi

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

Student Loan Refinancing If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Buying a house is a dream for many Americans, but it can feel very out of reach for some people. To qualify for a mortgage, you’ll need an adequate credit score and down payment, which many people just don’t have.

That is where the Neighborhood Assistance Corporation of America (NACA) comes in. The NACA has helped hundreds of thousands of people find affordable housing with no money down and no minimum credit score. NACA also provides financial assistance for approved homeowners that encounter financial difficulties.

If you’ve been struggling to figure out how you’ll afford to purchase a home, then the NACA program could help. This article will explain how the NACA mortgage process works and how the organization could help you find your next home.

What is the NACA mortgage program?

The Neighborhood Assistance Corporation of America (NACA), a non-profit organization established in 1988, is dedicated to providing affordable housing options to Americans. Its mission is to combat discriminatory and unjust lending practices. With 45 branches across the United States, NACA assists borrowers with low credit scores in securing affordable mortgages.

NACA offers various solutions such as property improvement and foreclosure avoidance to help achieve this goal. Additionally, the organization helps homeowners reorganize their existing mortgages, preventing them from losing their homes to foreclosure. Nevertheless, NACA’s signature mortgage program remains the most sought-after offering among its services.

How does the NACA program work?

The NACA is known for its purchase program, which it calls the Best in America Mortgage Program. This program is designed to make homeownership more affordable for everyone.

If you applied for a mortgage through a bank or credit union, you would undergo an extensive credit check. But the NACA makes it possible to buy a home with:

No down payment requirement

No closing costs

No requirement for perfect credit

No limits on your income

No fees – The lender pays the appraisal costs, attorney fees, title insurance, transfer tax, settlement agent fees, and buyer closing costs.

All of this is available at a below-market interest rate. Currently, the NACA is offering a 30-year fixed-rate mortgage of 2.125% APR and a 15-year fixed-rate mortgage of 1.75% APR. You’d be hard-pressed to find a better deal anywhere else.

Bank of America stands as NACA’s largest and most significant partner, providing a major portion of the funding for the loans.

NACA Requirements and Qualifications

Before you assume the NACA mortgage program is too good to be true, there are certain requirements you’re going to have to meet to qualify. Unlike traditional lending practices, NACA evaluates creditworthiness based on character, rather than solely relying on credit scores.

For instance, NACA members won’t be penalized for financial hardship caused by an injury or illness. But you must demonstrate that you can afford to pay your monthly housing expenses.

These expenses include your mortgage payments, property taxes, homeowners insurance, and HOA dues. And your income can’t fluctuate from month to month.

While there are no income restrictions in the NACA purchase program, earning higher than the median income could limit your home buying options to specific regions. It’s also worth noting that owning another property while closing on a NACA mortgage is strictly prohibited.

Furthermore, as a NACA mortgage recipient, you are expected to engage in a minimum of five membership activities annually. These activities include volunteering at NACA offices, participating in protests, or offering support to other members during the home buying process.

Eligible States

Unfortunately, the NACA mortgage program still isn’t available everywhere, though the organization is working hard to expand across the U.S. It’s currently available in the following states:

Alabama

Arkansas

Arizona

California

Colorado

Connecticut

District of Columbia

Florida

Georgia

Hawaii

Illinois

Louisiana

Massachusetts

Maryland

Michigan

Minnesota

Missouri

Mississippi

North Carolina

New Jersey

Nevada

New York

Ohio

Pennsylvania

South Carolina

Tennessee

Texas

Virginia

Wisconsin

NACA Program Pros and Cons

Here are some of the biggest advantages and disadvantages of taking out a mortgage through the NACA.

Pros

Buying a home with no down payment or standard closing costs

Snag a below-market interest rate on a 15-year or 30-year mortgage

No credit requirements or income limits to apply

Receive extensive borrower education and training

Cons

Time-consuming application process

Program isn’t available in all 50 states

There are limits to how much you can borrow

You’ll have to pay for property taxes and homeowners insurance

NACA Loan Limits

The NACA home buying program has loan limits that cap your mortgage amount. The purchase price of a home cannot exceed the conforming loan limit, which is $647,200 for a single-unit property in most states. The conforming loan limit for a single-unit home in Alaska and Hawaii is $970,800.

Who qualifies for the NACA program?

The NACA mortgage program is very generous, but there are several steps you’ll need to take before you can close on your home. Here are the seven steps you’ll take to complete the NACA loan qualification process.

1. Attend a free homebuyer workshop

If you’re considering applying for a NACA mortgage, you’ll first have to attend a homebuyer workshop. During this free workshop, you’ll learn more about homeownership and how to qualify for the NACA mortgage program. Then, you can register on the company’s website to reserve your spot.

2. Meet with your housing counselor

Once you’ve completed the homebuyer workshop, the NACA will assign you a housing counselor to guide you through this process. Your housing counselor will help you determine an affordable monthly mortgage payment and help you come up with a reasonable monthly budget. You’ll continue to meet with your counselor until you’ve qualified for the NACA housing program.

3. Attend a NACA purchase workshop

Once you’ve qualified for the mortgage program, you must attend a purchased workshop at the NACA office. During this workshop, you’ll review the home purchase process and work with a real estate agent to help you find the right home.

4. Receive a property qualification letter

Once you’ve chosen the home you plan to buy, you’ll have to get in touch with your housing counselor again. They will help you secure your qualification letter.

This letter states that you are qualified to purchase the home you’re interested in. Your NACA counselor and real estate agent can also help you draft an offer on the home.

5. Get your home inspected

Before you can purchase a home, it must pass a NACA home inspection and pest inspection. If the inspection reveals any problems with the home, you must resolve those issues before you can close on the home.

6. Meet with your mortgage consultant

Throughout this entire mortgage process, you should be saving money, maintaining your income level, and paying your bills on time. At this point, you’re going to meet with your mortgage consultant to prove that you’ve met the required guidelines and are ready to move forward with the mortgage application.

7. Close on your mortgage

Now it’s time to close on your home! There are no closing costs for a NACA mortgage. Additionally, NACA members do not pay private mortgage insurance (PMI).

Instead, your NACA membership provides you with a post-purchase assistance program through NACA’s Membership Assistance Program (MAP). But this is the final step that allows you to close on your new home and finalize the process.

Alternatives to the NACA program

The NACA program may not be suitable for everyone, or you may not qualify. If this is the case, consider other mortgage programs that may be available to you.

FHA Loans

For low-to-moderate income borrowers who may not meet the stringent requirements of conventional loans, the Federal Housing Administration offers the FHA loan program. With lower down payment needs and more lenient credit score standards, these loans provide a viable option for those looking to finance their first home.

USDA Loans

The U.S. Department of Agriculture extends its support to those seeking to purchase a home in rural or suburban areas through its USDA loan program. These loans offer attractive terms such as low or no down payment options and competitive interest rates, with the aim of fostering home ownership in less densely populated regions.

VA Loans

As a way to show appreciation for the sacrifices made by military service members, veterans, and their surviving spouses, the Department of Veterans Affairs provides VA loans.

These loans, exclusive to eligible individuals, boast features such as no down payment requirement, no private mortgage insurance, and interest rates that are often more favorable than those of traditional loans.

First-Time Homebuyer Programs

For those entering the housing market for the first time, many states and local governments offer programs tailored to their needs. First-time homebuyer programs often provide financial assistance in the form of lower interest rates and down payment assistance, as well as other incentives, making homeownership a reality for those who may not have the funds for a down payment otherwise.

Down Payment Assistance

To help alleviate the burden of the upfront costs of buying a home, down payment assistance (DPA) programs are available from government agencies, non-profit organizations, and private lenders.

These programs provide homebuyers with the necessary funds to cover their down payment, allowing them to get one step closer to affordable homeownership.

National Homebuyers Fund

As a non-profit organization, the National Homebuyers Fund offers down payment assistance to low-and moderate-income homebuyers in the form of grants that do not need to be repaid. Their mission is to provide a helping hand to those who may not have the resources to make a down payment on their own.

Chenoa Fund

The CBC Mortgage Agency’s Chenoa Fund is a down payment assistance program that provides low-and moderate-income homebuyers with up to 3.5% of the home’s purchase price. This support is provided through either forgivable or repayable second mortgage loan options.

Bottom Line

If you’re concerned that you don’t have the down payment or credit requirements necessary to apply for a traditional mortgage, a NACA mortgage may be a suitable option. Borrowers that qualify could receive low-interest mortgages with no down payment, closing costs, or fees. The application process is tedious, but the benefits can help you achieve the dream of homeownership.

Frequently Asked Questions

Is there a minimum credit score requirement for the NACA program?

No, NACA does not consider credit scores for mortgage approval. Instead, they look at your payment history and ability to make future mortgage payments.

Is there an income limit to qualify for the NACA program?

There is no strict income limit to qualify for the NACA program. The program is designed primarily to assist low- to moderate-income individuals and families, but it does not set an upper limit on income. The focus is more on your ability to afford the mortgage payments, and whether you meet other program criteria.

How long does the NACA mortgage process take?

The time frame can vary depending on individual circumstances, but generally, it takes several months from attending the initial workshop to closing on a home. The more promptly you can provide the required documentation and fulfill program requirements, the quicker the process will likely be.

How does the NACA mortgage differ from a traditional mortgage?

NACA mortgages typically offer more favorable terms compared to traditional mortgages. They come with no down payment, no closing costs, and no requirement for private mortgage insurance (PMI). The interest rates are often below market rate as well.

Can I use a NACA mortgage to refinance my existing loan?

No, NACA mortgages are designed for the purchase of a primary residence only. They cannot be used for refinancing existing loans or for investment properties.

What a difference four years make. Back in 2007, the only subject the presidential hopefuls talked about was mortgages.

In fact, it got to a point where it became nauseating, all the talk about mortgages and loan modifications and foreclosures and housing woes.

At the time, the candidates’ lack of knowledge surrounding those subjects was also painfully clear; they stumbled when trying to explain what exactly was going on, but pledged to do whatever it took to help turn things around.

Leading up to this year’s round of debates, I had paper and pen out, ready to jot down all the interesting mortgage references, and then pick them apart.

But as the night went on, I pushed my pad of paper to the side of me, capped my pen, and realized there weren’t going to be any mentions of housing woes or foreclosures or any of it.

Apparently such talk is “so four years ago.”

What Exactly Was Said?

Well, funnily enough, the first mention of “mortgage” didn’t even come from one of the candidates, but rather from an audience member, who asked about the future of the mortgage interest deduction, along with other deductions.

The question was for Romney, who responded by saying deductions would be reduced, perhaps to a fixed number such as $25,000, and then you could decide which deductions to take using that money.

So you could use it all on the mortgage deduction, or spread it among charitable and child tax deductions as well.

Of course, Romney also pledged to lower the tax rate, so even though deductions were on the chopping block, theoretically you’d save money.

And that was that. Not another word about mortgage or housing or foreclosures or anything else. Obama didn’t even take the opportunity to tout the record low mortgage rates or the recent drop in foreclosures.

Why It’s Good

So, what to make of all this? Well, an optimist would say that because it wasn’t discussed, the worst must be behind us.

Perhaps the mortgage crisis is in our rearview mirror now, and we can focus on other, more important issues, such as nagging unemployment.

After all, home prices are on the up and up, and millions of existing homeowners are getting their heads back above water as a result.

Demand for housing is also strong, perhaps because of the lack of inventory, and homebuilders are the most optimistic they’ve been in six years. Maybe they’ll build more homes to satisfy our hunger.

Additionally, the bevy of loan modification and large-scale refinance programs available seem to be working, as evidenced by the latest HARP figures released yesterday.

Even Bank of America’s chief financial officer believes we have turned the corner on housing, “clearly.”

Why It’s Bad

At the same time, the lack of any housing talk could be interpreted as bad news as well, depending upon your situation.

Not in the sense that the candidates are avoiding the subject because it’s a scary topic, but rather that it might mean no more help is on the way, or in the barrel.

If Obama and Romney aren’t talking about housing woes anymore, what would the motivation be to introduce new initiatives to help existing homeowners?

Have all the cards been played? What happened to that last-minute mega refinance program aimed at helping every single struggling homeowner save money on their monthly mortgage payment, even those without government-backed mortgages?

Maybe the candidates assessed the situation and decided no further action was necessary, or worthy enough to push for in order to get a few million votes.

Or perhaps they just realized it would be impossible to introduce any new measures to combat the problems, as bipartisan support would be needed.

Long story short, you got your help and you’re on your own now. That is, unless there is an eleventh hour gift yet to be unveiled.

For the record, the word “mortgage” was only uttered eight times in the first debate, and nothing noteworthy was said that time either.

Inside: Looking for a job that pays at least $25 per hour? This list has the best jobs that fit that description. Each job offers unique benefits and opportunities, so take a look and see if any of them match your interests and skills.

Making $25 an hour is not a pipe dream; it’s a viable reality for thousands of people worldwide.

Earning such an income not only instills a sense of financial well-being but also provides a robust platform to plan for the future.

Today, we dive into elucidating the different opportunities potential jobs offer, aligning your skills and experience with an hourly rate that feels just right for your wallet.

Hence, securing such a job is not a function of luck but more a strategic alignment of skills, passion, and industry demands. But if you’re not entirely sure about where to begin or how to hone your skills for these high-paying jobs, don’t worry.

Imagine earning smooth entry-level jobs 25 an hour, all from the comfort of your workspace. Sounds enticing, right?

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Jobs That Pay $25 an Hour

This section will highlight various professions across distinct fields that provide such a desirable pay rate.

Looking for jobs that pay $25 per hour? We’ve got you covered.

Whether you’re transitioning careers or just starting, this list could help you discover a role that fits your skills and experience.

1. Paralegal

A paralegal role is an excellent job choice due to the vast knowledge gained in the field of law and legal procedures.

Being a paralegal involves a variety of interesting tasks, such as helping lawyers prepare for hearings, trials, and corporate meetings.

This position is not solely monetarily advantageous, it also presents opportunities for growth and professional development in the legal sector.

Earning Potential: It offers rewarding prospects with an average pay of $25 per hour, with the potential to earn up to $40 an hour depending on experience and expertise.

2. Landscaper

Why toil in a stuffy office when the great outdoors can be your workspace? Relish the satisfaction of planting, pruning, and mowing yourself into a healthier, happier lifestyle.

Ideal for nature enthusiasts and people persons out there, landscaping combines green-thumbed work with personnel management. A knack for the outdoors and previous work experience will be your stepping stones, while a certificate in grounds maintenance can make your application stand out.

Start by volunteering in your local community gardens or offering your services to neighbors. Through this, not only will your skills blossom, but your resume will flourish, too.

Earning Potential: You can expand your lucrative landscaping journey by owning your own company and training others to be laborers.

3. Truck Driver

Why is it a top-tier job, you ask? Consider this: truck drivers are the beating heart of global commerce, pivotal figures in ensuring warehouses stay stocked and goods reach their desired destinations. Plus, you’re free of the traditional office environment.

This job is perfect for those who prefer to work alone as well as those who prefer delivery routes that often stretch into the night.

You must be over the age of 21 years old and able to pass a CDL exam. Many truck drivers to a training course to get a jumpstart in the industry.

Earning Potential: Many truck drivers start their own company and will employ a couple of rigs to make passive income.

4. Social Media Marketing

Do you have a knack for creating engaging captions or a Sherlockian eye for data? Then Social Media Marketing could be your calling.

This position, hot in demand and rewarding, calls for creativity and analytical prowess.

Why is it a top job? Well, it’s not for the adrenaline rush of its fast pace. It’s the fact that you get to put your tech-savviness to great use. Social media marketers nurture and grow brands through smart strategies and engaging content.

Earning Potential: Many people start working for someone else as a Social Media Coordinator and then go on to open up their own business.

5. Event Planners

As an event planner, you are the unseen forces behind flawless galas, memorable weddings, and standout corporate functions. If you thrive on creativity, organization, and people skills, you will ensure that each event is meticulously executed.

This role allows you to blend creativity with pragmatic decision-making: from the captivating process of selecting venues, and coordinating with caterers

It’s a dream job for you if you love putting smiles on people’s faces and making their day unforgettable.

Earning Potential: An enticing reason is its attractive pay rate: on average, $24-28 per hour, peaking up to $40, with the potential of a quick pay raise. Plus those lucrative tips!

6. Mechanical Technician

If you’re seeking a rewarding, high-paying role that gets you hands-on with varied machinery, then a Mechanical Technician career.

This role is particularly apt for those with a fascination for machinery and a problem-solving mindset. To climb the ladder to success, one needs to keenly understand how to operate and maintain industrial machines, prevent damage, and optimize performance.

So gear up to diagnose, adjust, repair, and don’t forget – your hands, mind, and machines are a team.

Earning Potential: With an average pay of $26 per hour, you can start repairing machines and set up your own company.

Virtual Savvy

If you’ve ever wanted to make a full-time income while working from home, you’re in the right place!