Apache is functioning normally

FHFA revises current single-family mortgages backed by Fannie Mae, Freddie Mac (iStock)

FHFA revises current single-family mortgages backed by Fannie Mae, Freddie Mac (iStock)

The Federal Housing Finance Agency (FHFA) will revise the treatment of active single-family mortgages backed by government-sponsored enterprises Fannie Mae and Freddie Mac for which borrowers elected a COVID-19 forbearance under the Enterprises’ representations and warranties framework, according to its newest media release.

“Under the updated rep and warrant policies, loans for which borrowers elected a COVID-19 forbearance will be treated similarly to loans for which borrowers obtained forbearance due to a natural disaster,” the FHFA said. “As a result, loans with a COVID-19 forbearance will remain eligible for certain rep and warrant relief based on the borrower’s payment history over the first 36 months following origination.”

FHFA Director Sandra L. Thompson argued that homeowners, who needed more time to keep up with housing costs during the pandemic, benefited from a mortgage forbearance plan that would reduce or suspend mortgage payments.

“Forbearance was an invaluable tool for borrowers experiencing financial hardship due to the COVID-19 pandemic,” Thompson said. “Servicers went to great lengths to implement forbearance quickly amid a national emergency, and the loans they service should not be subject to greater repurchase risk simply because a borrower was impacted by the pandemic.”

The Enterprises’ existing rep and warrant policies with respect to natural disasters allow the time the borrower is in forbearance to be included when demonstrating a satisfactory payment history in the first 36 months following origination, the FHFA noted. These policies will now expand to loans for which borrowers elected a COVID-19 forbearance.

Thompson stressed the importance of helping current and prospective homeowners manage present housing conditions at the Mortgage Bankers Association Annual Convention last week. “In a housing market like this one, it is all the more important that both our policies and the industry’s efforts align to support existing and aspiring homeowners,” Thompson said. “That is why I believe a model based on partnership and mutual feedback is necessary for us to achieve our shared goal of promoting affordable and sustainable housing opportunities.”

If you’re considering becoming a homeowner, it could help to shop around to find the best mortgage rate. Visit Credible to compare options from different lenders and choose the one with the best rate for you.

MORTGAGE RATES KEEP CLIMBING, BUT BUYERS CAN FIND THE BEST DEALS BY DOING THESE TWO THINGS: FREDDIE MAC

Mortgage rates are continuing their ascent. The average 30-year fixed-rate mortgage rose to 7.63% for the week ending Oct. 19, according to the Freddie Mac’s latest Primary Mortgage Market Survey. This time in 2022, the 30-year fixed-rate was below 7%.

Buyers may do well for themselves by browsing for the best home loans and making a considerable down payment. Freddie Mac’s Chief Economist Sam Khater said “in this environment, it’s important that borrowers shop around with multiple lenders for the best mortgage rate.”

Freddie Mac announced last week the launch of DPA One®, a new tool that strives to help mortgage lenders quickly find and match borrowers to down payment assistance programs nationwide.

“DPA One delivers a one-stop shop at no cost that brings lenders and their borrowers greater detail and visibility into these programs, while seamlessly connecting the right assistance program with the lender, housing counselors and borrowers who need this assistance the most,” Sonu Mittal, Freddie Mac’s senior vice president of and head of single-family acquisitions, explained.

“With research showing down payment is the single largest barrier to first-time homebuyers attaining homeownership, borrowers should also ask their lender about down payment assistance,” Khater said.

If you’re looking to buy a home, you could still find the best mortgage rates by shopping around. Visit Credible to compare your options without affecting your credit score.

MANY AMERICANS PREPARING FOR A RECESSION DESPITE SIGNS THAT SAY OTHERWISE: SURVEY

By end of 2023, there is likely to have been around 4.1 million existing home sales in the U.S., which would mark the weakest year of home sales since the Great Recession of 2008, according to a Redfin report.

Redfin’s Economic Research Lead Chen Zhao said current conditions have led to buyer and seller hesitancy across the board.

“Buyers have been in a bind all year,” Zhao said. “High mortgage rates and still-high prices are making it harder than ever to afford a home, shutting many young people out of homeownership and causing homeowners to reevaluate whether 2023 is the right time to move. Mortgage rates are staying high longer than anticipated, keeping away everyone except those who need to move and pushing our sales projection for the year down to a 15-year low.

“The last time home sales were this low was during the Great Recession,” Zhao continued.

Redfin agents suggest that buyers invest in newly built properties which are performing more strongly than existing-home sales. Newly constructed homes saw sales increase 1.5% year-over-year in September as prices dropped about 4%, according to Redfin’s data.

Based on the findings from a National Association of Realtors (NAR) report, the total amount of home sales decreased by 2% from August to September and have dropped 15.4% since September 2022.

Looking to reduce your home buying costs? It may benefit you to compare your options to find the best mortgage rate. Visit Credible to speak with a home loan expert and get your questions answered.

AFFORDABILITY KEEPING YOU FROM OWNING A HOME? HERE’S HOW YOU CAN GET READY

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at [email protected] and your question might be answered by Credible in our Money Expert column.

Source: foxbusiness.com

Due to the financial challenges created by the COVID-19 pandemic, federal student loan payments were automatically paused from March 2020 to September 2023. During that time, interest didn’t accrue and collections activities were also paused. But now that payments are due again, many borrowers are looking for ways to make their loans more manageable, especially those who are facing ongoing financial hardships.

One option is student loan deferment, which allows you to temporarily pause your student loan payments. As with most financial decisions, there are pros and cons to deferring your student loans. Here’s more information about student loan deferment and what it could mean for your financial future.

Deferment is a program that allows you to temporarily stop making payments on your federal student loans or to temporarily reduce your monthly payments for a specified time period.

This is similar to another option known as forbearance. However, unlike forbearance, you may not be charged interest while your loan is in deferment. According to the Department of Education, if you hold one of the following types of loans, you will not be responsible for paying interest on your loan while it is in deferment:

• Direct Subsidized Loan

• Subsidized Federal Stafford Loan

• Federal Perkins Loan

• The subsidized portion of a Direct Consolidation Loan

• The subsidized portion of a Federal Family Education Loan (FFEL) Consolidation Loan

If you have one of the following types of loans, you will be responsible for paying the accrued interest on your loan while it is in deferment:

• Direct Unsubsidized Loan

• Unsubsidized Federal Stafford Loan

• Direct PLUS Loan

• FFEL PLUS Loan

• The unsubsidized portion of a Direct Consolidation Loan

• The unsubsidized portion of a FFEL Consolidation Loan

If you are responsible for paying interest on your student loans while they are in grad school deferment, you have two options: 1) you can make interest-only payments on the loans while they are in deferment; 2) if you choose not to make these interest-only payments, the accrued interest will capitalize (be added to the loan principal) when the deferment period is over.

💡 Quick Tip: Ready to refinance your student loan? With SoFi’s no-fee loans, you could save thousands.

In order to qualify for student loan deferment, you must meet one of the following requirements:

• You’re enrolled at least part-time at a qualifying university

• You’re unemployed or unable to find employment (for up to three years)

• You’re experiencing an economic hardship

• You’re currently volunteering in the Peace Corps

• You’re on active-duty military service (or are in the 13 months following that service)

• You’re in an approved graduate fellowship program

• You’re in an approved rehabilitation program (for disabled students)

If you’re interested in deferring student loans to go back to school, you’ll need to apply for an in-school deferment. Most likely, you will request the deferment directly through your loan servicer—there is usually a form for you to fill out. When you request a deferment, you’ll also need to provide some sort of documentation to prove that you qualify for a deferment.

If you are enrolled in an eligible college or career school at least half-time, may be placed in deferment automatically . If it is, your loan servicer will notify you that deferment has been granted. If you enroll at least half-time and do not automatically receive a deferment, you will need to contact the school in which you are enrolled. The school will then send the appropriate paperwork to your loan servicer, so that your loan can be placed in deferment.

The biggest benefit of student loan deferment is the ability to temporarily postpone student loan repayment. As of the first quarter of 2023, 2.8 million loans were in deferment.

If you are deferring for extreme financial hardship, deferment allows you to free up money to pay off bills that require immediate attention like rent or electricity.

For students who have qualified for deferment through community service, like a stint in the Peace Corps, deferment gives them the opportunity to serve their community without any added stress from student loan payments.

While temporarily pausing loan repayment may seem like a blessing, it can come at a cost, especially if your student loans are not subsidized by the government. When in deferment, interest continues to accrue on your loan. And at the end of your deferment period, that interest will be capitalized on the loan. (This means that the accrued interest will be added to the principal balance of the loan. So ultimately, you’ll be paying interest on top of interest.)

This can mean you end up paying even more money over the life of the loan. To see how much deferring your student loans could cost, you can use an online calculator to get an estimate of how much interest will accrue while the loan is in deferment.

If you have private loans that aren’t eligible for federal student loan deferment, refinancing your student loans is another option to consider. You may also want to think about refinancing when you’re done with your graduate degree to pay off your loans at a potentially lower interest rate.

When you refinance, your existing student loans are paid off with a new loan from a private lender. If you are refinancing private loans before going back to graduate school, you may be after a lower monthly payment, which you could potentially qualify for when refinancing your loans and extending the loan term. (You may pay more interest over the life of the loan if you refinance with an extended term.)

Alternatively, if you’re looking to refinance after graduate school, you could potentially qualify for a lower interest rate, which could reduce the amount of money you spend over the life of the loan. The lender will use your credit score and earning potential to determine what interest rate you’ll qualify for. And thanks to your new graduate degree, you could have significantly increased your earnings.

Another big benefit of student loan refinancing? You’re able to combine all of your student loan payments – for both federal and private loans – into one easy-to-manage payment.

If you hold only federal student loans, however, you could look into a Direct Consolidation Loan , which allows you to consolidate federal loans into one loan with a single monthly payment. The new interest rate will be the weighted average of your current interest rates (rounded to the nearest one-eighth of 1%), so unlike refinancing, when you consolidate your student loans, you won’t necessarily qualify for a lower interest rate.

If you are taking advantage of your federal loans’ flexible repayment plans or student loan forgiveness programs (or if you are planning to do so), refinancing might not be the best option for you. A major con of student loan refinancing is that you’ll lose access to federal loan benefits when refinancing with a private lender—including deferment and income-driven repayment plans.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

Student Loan Refinancing

If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOSL0923056

Source: sofi.com

Buying a house is a dream for many Americans, but it can feel very out of reach for some people. To qualify for a mortgage, you’ll need an adequate credit score and down payment, which many people just don’t have.

That is where the Neighborhood Assistance Corporation of America (NACA) comes in. The NACA has helped hundreds of thousands of people find affordable housing with no money down and no minimum credit score. NACA also provides financial assistance for approved homeowners that encounter financial difficulties.

If you’ve been struggling to figure out how you’ll afford to purchase a home, then the NACA program could help. This article will explain how the NACA mortgage process works and how the organization could help you find your next home.

The Neighborhood Assistance Corporation of America (NACA), a non-profit organization established in 1988, is dedicated to providing affordable housing options to Americans. Its mission is to combat discriminatory and unjust lending practices. With 45 branches across the United States, NACA assists borrowers with low credit scores in securing affordable mortgages.

NACA offers various solutions such as property improvement and foreclosure avoidance to help achieve this goal. Additionally, the organization helps homeowners reorganize their existing mortgages, preventing them from losing their homes to foreclosure. Nevertheless, NACA’s signature mortgage program remains the most sought-after offering among its services.

The NACA is known for its purchase program, which it calls the Best in America Mortgage Program. This program is designed to make homeownership more affordable for everyone.

If you applied for a mortgage through a bank or credit union, you would undergo an extensive credit check. But the NACA makes it possible to buy a home with:

All of this is available at a below-market interest rate. Currently, the NACA is offering a 30-year fixed-rate mortgage of 2.125% APR and a 15-year fixed-rate mortgage of 1.75% APR. You’d be hard-pressed to find a better deal anywhere else.

Bank of America stands as NACA’s largest and most significant partner, providing a major portion of the funding for the loans.

Before you assume the NACA mortgage program is too good to be true, there are certain requirements you’re going to have to meet to qualify. Unlike traditional lending practices, NACA evaluates creditworthiness based on character, rather than solely relying on credit scores.

For instance, NACA members won’t be penalized for financial hardship caused by an injury or illness. But you must demonstrate that you can afford to pay your monthly housing expenses.

These expenses include your mortgage payments, property taxes, homeowners insurance, and HOA dues. And your income can’t fluctuate from month to month.

While there are no income restrictions in the NACA purchase program, earning higher than the median income could limit your home buying options to specific regions. It’s also worth noting that owning another property while closing on a NACA mortgage is strictly prohibited.

Furthermore, as a NACA mortgage recipient, you are expected to engage in a minimum of five membership activities annually. These activities include volunteering at NACA offices, participating in protests, or offering support to other members during the home buying process.

Unfortunately, the NACA mortgage program still isn’t available everywhere, though the organization is working hard to expand across the U.S. It’s currently available in the following states:

Here are some of the biggest advantages and disadvantages of taking out a mortgage through the NACA.

The NACA home buying program has loan limits that cap your mortgage amount. The purchase price of a home cannot exceed the conforming loan limit, which is $647,200 for a single-unit property in most states. The conforming loan limit for a single-unit home in Alaska and Hawaii is $970,800.

The NACA mortgage program is very generous, but there are several steps you’ll need to take before you can close on your home. Here are the seven steps you’ll take to complete the NACA loan qualification process.

If you’re considering applying for a NACA mortgage, you’ll first have to attend a homebuyer workshop. During this free workshop, you’ll learn more about homeownership and how to qualify for the NACA mortgage program. Then, you can register on the company’s website to reserve your spot.

Once you’ve completed the homebuyer workshop, the NACA will assign you a housing counselor to guide you through this process. Your housing counselor will help you determine an affordable monthly mortgage payment and help you come up with a reasonable monthly budget. You’ll continue to meet with your counselor until you’ve qualified for the NACA housing program.

Once you’ve qualified for the mortgage program, you must attend a purchased workshop at the NACA office. During this workshop, you’ll review the home purchase process and work with a real estate agent to help you find the right home.

Once you’ve chosen the home you plan to buy, you’ll have to get in touch with your housing counselor again. They will help you secure your qualification letter.

This letter states that you are qualified to purchase the home you’re interested in. Your NACA counselor and real estate agent can also help you draft an offer on the home.

Before you can purchase a home, it must pass a NACA home inspection and pest inspection. If the inspection reveals any problems with the home, you must resolve those issues before you can close on the home.

Throughout this entire mortgage process, you should be saving money, maintaining your income level, and paying your bills on time. At this point, you’re going to meet with your mortgage consultant to prove that you’ve met the required guidelines and are ready to move forward with the mortgage application.

Now it’s time to close on your home! There are no closing costs for a NACA mortgage. Additionally, NACA members do not pay private mortgage insurance (PMI).

Instead, your NACA membership provides you with a post-purchase assistance program through NACA’s Membership Assistance Program (MAP). But this is the final step that allows you to close on your new home and finalize the process.

The NACA program may not be suitable for everyone, or you may not qualify. If this is the case, consider other mortgage programs that may be available to you.

For low-to-moderate income borrowers who may not meet the stringent requirements of conventional loans, the Federal Housing Administration offers the FHA loan program. With lower down payment needs and more lenient credit score standards, these loans provide a viable option for those looking to finance their first home.

The U.S. Department of Agriculture extends its support to those seeking to purchase a home in rural or suburban areas through its USDA loan program. These loans offer attractive terms such as low or no down payment options and competitive interest rates, with the aim of fostering home ownership in less densely populated regions.

As a way to show appreciation for the sacrifices made by military service members, veterans, and their surviving spouses, the Department of Veterans Affairs provides VA loans.

These loans, exclusive to eligible individuals, boast features such as no down payment requirement, no private mortgage insurance, and interest rates that are often more favorable than those of traditional loans.

For those entering the housing market for the first time, many states and local governments offer programs tailored to their needs. First-time homebuyer programs often provide financial assistance in the form of lower interest rates and down payment assistance, as well as other incentives, making homeownership a reality for those who may not have the funds for a down payment otherwise.

To help alleviate the burden of the upfront costs of buying a home, down payment assistance (DPA) programs are available from government agencies, non-profit organizations, and private lenders.

These programs provide homebuyers with the necessary funds to cover their down payment, allowing them to get one step closer to affordable homeownership.

As a non-profit organization, the National Homebuyers Fund offers down payment assistance to low-and moderate-income homebuyers in the form of grants that do not need to be repaid. Their mission is to provide a helping hand to those who may not have the resources to make a down payment on their own.

The CBC Mortgage Agency’s Chenoa Fund is a down payment assistance program that provides low-and moderate-income homebuyers with up to 3.5% of the home’s purchase price. This support is provided through either forgivable or repayable second mortgage loan options.

If you’re concerned that you don’t have the down payment or credit requirements necessary to apply for a traditional mortgage, a NACA mortgage may be a suitable option. Borrowers that qualify could receive low-interest mortgages with no down payment, closing costs, or fees. The application process is tedious, but the benefits can help you achieve the dream of homeownership.

No, NACA does not consider credit scores for mortgage approval. Instead, they look at your payment history and ability to make future mortgage payments.

There is no strict income limit to qualify for the NACA program. The program is designed primarily to assist low- to moderate-income individuals and families, but it does not set an upper limit on income. The focus is more on your ability to afford the mortgage payments, and whether you meet other program criteria.

The time frame can vary depending on individual circumstances, but generally, it takes several months from attending the initial workshop to closing on a home. The more promptly you can provide the required documentation and fulfill program requirements, the quicker the process will likely be.

NACA mortgages typically offer more favorable terms compared to traditional mortgages. They come with no down payment, no closing costs, and no requirement for private mortgage insurance (PMI). The interest rates are often below market rate as well.

No, NACA mortgages are designed for the purchase of a primary residence only. They cannot be used for refinancing existing loans or for investment properties.

Source: crediful.com

The mere thought of filing for bankruptcy is enough to make anyone nervous. But in some cases, it really can be the best option for your financial situation. Even though it stays as a negative item on your credit report for up to ten years, bankruptcy often relieves the burden of overwhelming amounts of debt.

There are actually three different types of bankruptcy, and each one is designed to help people with specific needs. Read on to find out which type of bankruptcy you might be eligible for. We’ll also help you determine whether it really is the best option available.

In general, bankruptcy is the process of eliminating some or all of your debt, or in some cases, repaying it under different terms from your original agreements with your creditors.

It’s a very serious endeavor but can help alleviate your debt if you calculate that it’s unlikely to you’ll be able to repay everything throughout the coming years.

The two most common for individuals are Chapter 7 and Chapter 13. Chapter 11 is primarily used for businesses but can apply to individuals in some instances. Let’s take a look at some bankruptcy basics and the other details that set them apart from each other.

Chapter 7 bankruptcy is designed for individuals meeting certain income guidelines who can’t afford to repay their creditors. You must pass a means test to qualify. Then, instead of making payments, a bankruptcy trustee can sell your personal property to help settle your debts, including both secured and unsecured loans.

There are certain exemptions you can apply for to keep some things from being taken away. It all depends on which debts are delinquent. If your mortgage is headed towards foreclosure, you might only be able to delay the process through a Chapter 7 delinquency.

If you’re only delinquent on unsecured debt, like credit card debt or personal loans, then you can file for an exemption on major items like your home and car. That way they won’t be repossessed and auctioned off.

Eligible exemptions vary by state. Usually, there is a value assigned to your assets that are eligible for exemption. You may keep them as long as they are within that maximum value. For example, if your state has a $3,000 auto exemption and your car is only valued at $2,000 then you get to keep it.

Most places also allow you to subtract any outstanding loan amount to put towards the exemption. So, in the situation above, if your car is valued at $6,000, but you have $3,000 left on your car loan, then you’re still within the exemption limit.

Chapter 7 bankruptcy is the fastest option to go through, lasting just between three and six months. It’s also usually the cheapest option in terms of legal fees. However, keep in mind that you’ll likely have to pay your attorney’s fees upfront if you choose this option.

A chapter 13 bankruptcy is the standard option when you make too much money to qualify for a Chapter 7 bankruptcy. The benefit is that you get to keep your property but instead repay your creditors over a three- to five-year period. Your repayment plan depends on several variables.

All administrative fees, priority debts (like back taxes, alimony, and child support), and secured debts must be paid back in full over the repayment period. These must be paid back if you want to keep the property, such as your house or car.

The amount you’ll have to repay on your unsecured debts can vary drastically. It depends on the amount of disposable income you have, the value of any nonexempt property, and the length of your repayment plan.

How long your plan lasts is actually determined by the amount of money you earn and is based on income standards for your state. For example, if you make more than the median monthly income, you must repay your debts for a full five years.

If you make less than that amount, you may be able to reduce your repayment period to as little as three years. You can enter your financial information into a Chapter 13 bankruptcy calculator for an estimate of what your monthly payments might look like in this situation.

To qualify for Chapter 13, your debts must be under predetermined maximums. For unsecured debt, your total may not surpass $1,149,525 and your secured debt may not surpass $383,175. However, unlike Chapter 7 bankruptcy, you may include overdue mortgage payments to avoid foreclosure.

Chapter 11 bankruptcy is usually associated with companies. However, it can also be an option for individuals, especially if their debt levels exceed the Chapter 13 limits. A lot of the characteristics of Chapter 11 and Chapter 13 are the same, such as saving secured property from being repossessed.

Having to pay back priority debts in full and having a higher income bracket than a Chapter 7 bankruptcy are also common characteristics. However, unlike Chapter 13, you must make repayment for the entire five years with a Chapter 11. There is no option to pay for just three years, no matter where you live or how much you make.

Another reason to pick Chapter 11 is if you are a small business owner or own real estate properties. Rather than losing your business or your income properties, you get to restructure your debt and catch up on payments while still operating your business, whether it’s as a CEO or as a landlord.

One downside to be aware of with a Chapter 11 bankruptcy is that it’s usually the most expensive option. However, you can pay your legal fees over time so you don’t have to worry about spiraling back into debt.

It should come as no surprise that going through bankruptcy causes your credit score to plummet. Depending on what else is on your report, your score could drop anywhere between 160 and 220 points.

Those effects linger. A Chapter 13 bankruptcy stays on your credit report for seven years. And a Chapter 7 bankruptcy remains there for as many as ten years. Their effects on your credit score do, however, begin to diminish as time goes by.

You’ll probably have trouble getting access to credit immediately following your bankruptcy. Eventually, you’ll start getting approved for loans and credit cards, but your interest rates are likely to be extremely high.

A new mortgage will probably be out of reach for at least five to seven years from the time you file for bankruptcy. Additionally, any employer performing a credit check can see all of these items on your credit report.

Government agencies can’t legally discriminate against you because of your bankruptcy, but there is no specific rule for privately-owned companies. It could be particularly damaging if the job you’re applying for deals with money or any type of financials. No matter where you work, though, you can’t be fired from a current employer because of a bankruptcy.

There’s no correct answer to this question. It’s ultimately something you’ll need to decide on your own. However, there are a few things you can do to make sure you’re making the best decision possible. Start by finding a licensed credit counselor to help analyze your individual situation. They’ll help you review the guidelines for each type of bankruptcy and determine if you’re even eligible.

At first glance, filing for bankruptcy may seem like a great way to settle your debts and move on with your life. Unfortunately, the process isn’t as simple as filling out a form. The effects of bankruptcy will stick with you for years.

As you begin the evaluation process of whether bankruptcy is right for you, there are several considerations to consider. This overview will get you thinking about your situation. It will also point you in the right direction for more in-depth resources when you need them.

You should also look at your expected future and compare your potential earnings to your amounts of debt. If you don’t see how you’ll ever pay off that debt, then bankruptcy may be a wise option. Also, understand the types of debt you owe. Tax payments, student loan debt, and liens on your mortgage or car will not be discharged even when you file for bankruptcy.

Once you figure out which specific options are available to you, it’s time to contact a bankruptcy attorney. You’re certainly able to represent yourself, but the process is complicated. It’s usually best to have a professional work on the case on your behalf. Just be sure to interview a few different lawyers to get multiple opinions and prices to compare.

Even when your bankruptcy is underway, it’s smart to spend some time evaluating how you got there. Was it due to a one-time financial hardship, like a long bout of unemployment? If that’s the case, then you know that you have a brighter future ahead of you with the promise of work and steady income to pay your bills.

However, if you’re on the path to bankruptcy because of reckless spending, you really need to look inward and address your overspending habits. Otherwise, it becomes too easy to put yourself in the same situation a few years down the road. Use your bankruptcy as a second chance to start fresh with a clean financial slate.

If you’re considering bankruptcy, then you’re most likely feeling overburdened with debt and other financial obligations. You probably have a tough time paying your bills each month and may even worry about how you’ll ever pay off some of your outstanding balances.

If you’ve already exhausted your other options, like working overtime and cutting back on your non-necessities, it might be time to seriously think about potentially declaring bankruptcy. Some signs that you might be ready include:

If one or more of these situations apply to you, then you should probably continue your research into bankruptcy. If not, try finding other ways to improve your financial situation. For example, you could rework your budget if there are easy places to cut back on.

You can also try negotiating with your lenders, particularly if you’re experiencing just a short-term setback. Most lenders are willing to work with you. They would much rather set up a new payment plan than have the debt discharged or settled through bankruptcy.

If you want to file for bankruptcy it takes careful planning. Due to the long-term legal and financial consequences of bankruptcy, there are many rules that must be followed before you’re eligible.

For example, it’s necessary to show the bankruptcy court that you have obtained credit counseling and considered debt relief options like debt settlement or debt consolidation. Bankruptcy is controlled exclusively by the federal judicial system, which strongly recommends hiring an attorney before attempting to file.

If you need help finding a bankruptcy lawyer, contact the American Bar Association. They offer free legal advice, and you may qualify for free legal services if you are unable to afford an attorney.

Before you file for bankruptcy, there are several important questions you should ask yourself. There are also several key steps that you need to take. First, it’s necessary to ask yourself if you really need to file for bankruptcy.

If you don’t, you probably won’t be approved anyway. You also need to calculate income, expenses, and assets, find a trustworthy attorney, and select a credit counseling program.

It’s helpful to be methodical and to use a checklist. Failure to take the right steps and find the right credit counseling could result in more wasted money and a bankruptcy dismissal where they throw out the case.

Even if bankruptcy is the best choice for you, there may be some situations where it’s smart to delay the process so you can maximize your benefits. First, if you had a high income within the last six months that no longer applies to your situation, then you might want to wait.

That’s because the bankruptcy court weighs your last six months of income to determine your eligibility for Chapter 7 bankruptcy. If you had a nice monthly salary a few months ago but have been laid off since then, that means test isn’t going to reflect your current situation accurately.

Another reason to delay bankruptcy is if you are anticipating an upcoming major debt. New debt isn’t allowed to be discharged once you file for bankruptcy.

So, for example, if you’re about to have a major medical surgery, you might consider waiting until it’s over to include the medical bills as part of your bankruptcy plan. Talk to a professional to see the eligibility requirements. Luxury items charged right before a bankruptcy filing, for example, likely won’t be included as part of your debt discharge.

Before getting started, it’s important to note the changes that went into effect in 2005 under the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA). While the changes don’t affect some people applying for bankruptcy, they may affect others.

Federal bankruptcy laws require mandatory credit counseling to make sure you fully understand the consequences of declaring bankruptcy. It also created stricter eligibility requirements for Chapter 7 bankruptcies. For Chapter 13 bankruptcy filings, the law requires tax returns and proof of income.

An informed decision begins with understanding bankruptcy laws, the bankruptcy process, and what has changed. It’s essential to better understand these changes before you make any final decisions.

Understanding how bankruptcy works means understanding the process and laws related to Chapters 7 and 13 of the Bankruptcy Code. Depending on the details of your situation, you might be eligible to file under Chapter 7 or Chapter 13. Which route you choose has a lot to do with your income and what assets you want to keep.

Your debts can either be resolved quickly or over a several-year period. It’s helpful to read up on in-depth frequently asked questions related to each route.

To have all your unsecured debts eliminated under Chapter 7 bankruptcy, you must qualify under the Chapter 7 means test. Using your personal information, or a basic estimate, an online calculator can help determine this for you. When filing bankruptcy, you must also fill out an appropriate form in which you enter your income, expense information, and data from the Census Bureau and IRS.

If you don’t meet the income level requirements to file for Chapter 7 bankruptcy, you can still file for Chapter 13. A Chapter 13 will settle many of your debts after you successfully complete a three to five-year repayment program.

Your debts qualify for bankruptcy relief when you can prove you are unable to pay them, but a great deal depends on your situation and which chapter you are filing bankruptcy under. Debts can be either unsecured or secured. Secured debts include mortgages, cars, and debts related to a property you’re still paying for.

Unsecured debts include credit card debt, bills, collections, judgments, and unsecured loans. It’s important to know which debts qualify for bankruptcy. But, it’s even more important to know whether your situation makes you eligible for this major step. To determine this, a full financial assessment is necessary. You can start by reading more about debts that qualify.

If you have defaulted on a student loan, there are several options open to you. Bankruptcy is one of them, but if your goal is to have a student loan discharged under Chapter 7, this can be very difficult.

Nevertheless, taking certain steps as soon as possible can help prevent wage garnishment. Knowing your options can help you make the best choice before matters become more difficult. Under Chapter 13, your defaulted loan can be consolidated with your other bills. This will give you a better payment plan or a temporary reprieve from making payments.

If you have a federal student loan, check out your repayment options, especially if you are facing financial hardship. Otherwise, read more to figure out how to pull yourself out of student loan default.

Depending on how you file for bankruptcy, there are certain assets you can keep. Different states have different exemptions, and in certain states, you can choose between state and federal bankruptcy exemptions.

If you need to have debts discharged, are out of work, and cannot afford a repayment plan, some assets might be lost. In most cases, however, people who declare bankruptcy can keep their homes and cars and much of what they own while they repay their debts under a modified plan. It all depends on your unique circumstances and how you file.

A bankruptcy can affect your credit for 7 to 10 years and should be considered a last resort option when all other options have failed. Many times, people file bankruptcy when it is completely unnecessary. A credit professional can help you fix your credit and deal with your creditors so you can avoid filing for bankruptcy.

Before filing bankruptcy, talk to a credit specialist:

Visit the website and fill out the form for a free credit consultation with a professional credit repair company.

Source: crediful.com

Editor’s Note: For the latest developments regarding federal student loan debt repayment, check out our student debt guide.

What happens if I miss a student loan payment? That’s the question on many borrowers’ minds as federal student loan payments resume after more than three years of emergency forbearance.

Missing payments on student loans can have a variety of negative consequences, including damage to your credit score and wage garnishment. However, the Biden administration is offering a temporary “on-ramp” to ease the transition back into repayment. Until the end of September 2024, borrowers will not have to worry about their student loans falling into default or damage to their credit score if they miss payments.

Interest will continue to accrue during this time, though, and any missed student loan payments will be due eventually. Rather than ignoring your student loan bills, take some time to review your options for making them more affordable. The Department of Education offers various plans to help struggling borrowers get back on track.

Missing federal student loan payments typically leads to delinquency and default, but from October 2023 through September 2024, borrowers who miss a payment will avoid these consequences. Here’s a closer look at what this student loan on-ramp entails, followed by what typically happens when you miss payments.

Federal student loan borrowers have been exempt from student loan payments and interest since March of 2020. With the end of this emergency forbearance, the Biden administration is offering a one-year on-ramp for borrowers to adjust to the new reality. Until Sep. 30, 2024, borrowers won’t face the usual consequences if they miss payments.

For example, your loans won’t fall into delinquency or default, and missed payments won’t be reported to the credit bureaus. Your loans won’t go into collections, and you won’t have to worry about garnishment of your wages, tax refund, or Social Security benefits.

What’s more, the interest that accrues during this year won’t be capitalized, or added onto, your principal balance when the on-ramp expires. This on-ramp gives borrowers time to start making payments again after the lengthy pause.

However, interest will still accrue during this time, and you’ll still have to pay back your loan eventually. Instead of skipping payments over the next year, you may be better off applying for an income-driven repayment plan for more affordable monthly bills.

Normally, your student loan is considered delinquent the day after you miss a payment. Even if you start making the next payments, your account will remain delinquent until you make up for the missed payment or receive deferment or forbearance.

Once 90 days pass, your loan servicer will let the major credit reporting agencies know that your loan is delinquent. Your credit score will take a hit, making it more difficult to qualify for good terms on loans or credit cards or to rent an apartment.

If you continue not paying, your loan will go into default. For federal loans, the government will wait 270 days. Defaulting on your student loan has serious consequences. The entire amount you owe on your loan, including interest, becomes due immediately.

You won’t be able to take out any other student loans, and you’ll no longer qualify for deferment or forbearance or be able to choose your own mortgage, car loan, or other forms of credit. The government may take your tax refund or federal benefits to pay off your loan. You may also have your wages garnished, meaning your employer will take part of your paycheck and send it to the government to be applied toward the loan.

It’s rare, but the government can also sue you at any time — there’s no statute of limitations. You may also be responsible for collection fees, attorney’s fees, and other costs. In other words, you do not want to default on your student loans. (If you do, options exist for getting out of default, such as the Fresh Start program.)

💡 Quick Tip: Get flexible terms and competitive rates when you refinance your student loan with SoFi.

Private lenders usually give you much less leeway than the federal government. Exactly what happens if you miss a payment depends on the company’s policies and your loan terms. A private lender can tack on late fees and transfer your loan to a debt collection agency.

Also, private lenders can sue you if you stop paying your student loans. If they win, a court can sign a judgment allowing them to garnish your wages. States set the statute of limitations for lawsuits about payment of private loans; the time period usually ranges from three years to a decade. But the lender can continue trying to collect the debt for as long as they want. Plus, certain actions can reset the statute of limitations, such as making a payment or even acknowledging that the debt belongs to you.

If you stop paying your student loans, they will not go away. However, it may be possible to discharge student loans in bankruptcy or qualify for student loan forgiveness or discharge.

For example, federal student loans can be discharged if you suffer from a total permanent disability or your school closes while you’re attending or soon after you leave. You can also pursue student loan forgiveness programs, such as Public Service Loan Forgiveness or Teacher Loan Forgiveness.

Student loan cancellation from an income-driven repayment plan may also be an option. Income-driven plans will discharge your remaining student loan balance at the end of your term. While the term is 20 or 25 years for some plans, the new SAVE plan will offer forgiveness after 10 years if your original principal balance was $12,000 or less. On all the income-driven plans, it’s possible that your monthly payment could be $0, depending on your discretionary income.

For instance, borrowers who earn less than $32,800 as individuals or $67,500 as a family of four in most states could have $0 monthly payments on the SAVE plan. If this describes you, you could essentially stop paying your student loans and see them go away after anywhere from 10 to 25 years on the plan, depending on how much you borrowed and whether you took out the loans for undergraduate or graduate school.

However, you’ll have to apply for income-driven repayment and recertify your income annually to stay on the plan and keep making progress toward loan cancellation. If you give the Department of Education permission to access your tax information, it can recertify your plan automatically each year.

If you are having a tough time with your finances or are putting off making a late student loan payment, don’t just ignore your loans; instead, approach your lender or loan servicer to discuss your options.

For federal loans, an income-driven repayment plan could help. Income-driven plans, which include SAVE, PAYE, Income-Based Repayment, and Income-Contingent Repayment, adjust your monthly payments based on a percentage of your discretionary income. Most also extend your loan terms and offer loan forgiveness if you still owe a balance at the end. The new SAVE plan particularly has the most generous terms for borrowers.

You might also be able to qualify for a deferment or student loan forbearance, allowing you to temporarily stop or reduce payments. If you’re in deferment, depending on the type of loan you have, you may not be responsible for paying the interest that accrues during the deferment period. Among other reasons, you can apply for deferment if you’re in school, in the military, unemployed, or not working full-time.

You can apply for forbearance if your student loan payments represent 20% or more of your gross monthly income, if you’ve lost your job or seen your pay reduced, if you can’t pay because of medical bills, or if you’re facing another financial hardship, among other things. Private lenders are not required to offer relief if you’re facing hardship, but some, including SoFi, do.

It is possible that if your student loan is in default it may be sent to a collections agency. Federal student loans in default are managed by the Department of Education’s Default Resolution Group. The Default Resolution Group oversees collections for all federal student loans that are in default, so they are not sent to a private collections agency.

The Department of Education is temporarily offering a Fresh Start program for student loans in default. By calling your loan servicer or logging into myeddebt.ed.gov, you can get your loans back into active repayment, enroll in a new repayment plan, and have the record of default removed from your credit report. You’ll also regain access to federal financial aid.

Private student loans may be sent to a collection agency as soon as the loan enters default, which is generally after 90 days of non-payment.

Deferment, forbearance, and relief offered by private lenders are temporary solutions. If your financial hardship looks like a long-term issue, you’ll need a permanent fix.

With federal loans, you may be eligible for an income-driven repayment plan. The government currently offers four plans that aim to make payments affordable by tying them to your monthly income.

On most plans, the payments range between 10% and 20% of your discretionary income, and if you make them on time, the balance is eligible to be forgiven in 20 or 25 years.. As mentioned, though, the new SAVE plan may offer loan forgiveness after just 10 years, depending on your original loan balance. Plus, starting in July 2024 it will cut monthly payments on undergraduate loans in half. For most borrowers, the SAVE plan will likely offer the most affordable monthly payments. However, parent loans are not eligible for SAVE. If you’re a parent borrower, your only option for an income-driven plan is Income-Contingent Repayment.

Private student loans are also not eligible for income-driven repayment, and most private lenders don’t offer this option. If you’re struggling to afford your private student loan bills, though, it’s worth explaining your situation to the lender and seeing if they can work with you on a feasible repayment plan. It’s in their interest to continue collecting even partial payments from you, rather than seeing payments stop altogether and having to go through the trouble of lawsuits or referrals to collection agencies.

Another potential long-term solution to unaffordable payments is student loan refinancing. With a private lender like SoFi, you can refinance federal student loans, private loans, or both. Refinancing involves obtaining a new loan to pay off all of your old ones and committing to the new terms and interest rate.

Refinancing your student loans can make sense if you qualify for a lower interest rate, which, depending on the term you choose, may be able to cut down the money you spend in interest over the life of your loan. Or, if you choose a longer term than you originally had when refinancing, you could lower your monthly payments, which can make the loan more affordable for you now. You may pay more interest over the life of the loan if you refinance with an extended term.

When you refinance with SoFi, you won’t pay any origination fees to refinance, and if your financial situation improves down the line and you want to pay off your loan faster, you won’t face prepayment penalties. It takes just two minutes online to figure out whether you qualify and the potential rates you can obtain.

Missing student loan payments can have serious consequences, including entering default and damaging your credit score. Fortunately, borrowers have some leeway through September 2024 as they adjust to making payments on their federal loans again. However, private student loans offer no such benefit.

Refinancing could be an option to consider for borrowers looking to secure a lower interest rate. Consider SoFi — where there are zero fees for refinancing student loans and qualifying borrowers can secure a competitive interest rate.

Hoping to get a handle on your student debt? Look into whether refinancing your student loans with SoFi could help you lower your payments or save money in the long term.

If you are late on a student loan payment, the loan may be considered delinquent. The loan will remain delinquent until a payment is made, or other arrangements — such as deferment or forbearance — are made. Through Sep. 30, 2024, missing payments on your federal loan payments won’t cause them to go into delinquency or default thanks to the student loan on-ramp.

A late payment may have a negative impact on your credit score. With the exception of the student loan on-ramp through the fall of 2024, federal loans are normally reported to the credit bureau if they remain delinquent for 90 days. Private student lenders may report a late payment to credit bureaus after 30 days.

If you fail to make payments on your federal student loan for 270 days, the student loan will enter default (again, with the exception of the temporary student loan on-ramp). Consequences of default can be serious, such as the total balance of the loan becoming due immediately.

Private student loans may be considered in default after 90 days.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Student Loan Refinancing

If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

SoFi Private Student Loans

Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

SOSL0923018

Source: sofi.com

In a survey about how money matters in relationships, we asked both men and women if they’d ever broken up with someone over money. Around a quarter of respondents said they had, while around a fifth said someone had broken up with them over financial matters.

Clearly, financial factors can create friction in relationships—and that’s true whether or not someone breaks up over these issues. According to a poll conducted by the Association of International Certified Professional Accountants, almost 70% of Americans who were married or living with a partner said they’d fought about money with their significant other within the past 12 months.

With money a stressor in relationships, it’s not surprising that financial infidelity sometimes occurs. Find out more about financial infidelity and the role finances play in relationships below.

People often shy away from the importance of finances in a marriage or other relationship because they don’t want to seem materialistic or as if they’re putting money and things before their significant other. In reality, though, finances are critically important because they can provide stability—or take it away, as the case may be. Being honest with each other about finances and working together transparently for future financial goals builds trust and helps the entire marriage or relationship succeed.

Some things that might be important to financial fidelity in a relationship include:

Financial infidelity occurs when you lie about money matters to each other in a relationship where there’s an expectation that you won’t. Usually this is possible when a couple shares finances, but it’s also possible even if you keep your finances separate and are dishonest about things.

A few examples of financial infidelity include:

If you’re worried that financial infidelity is at play in your relationship, consider the following common signs:

Whether you should break up with someone or ask for a divorce based on financial infidelity is a personal choice, and one that probably should take into account many other factors. According to our survey, men are slightly more likely to initiate a breakup over financial issues, with almost 30% saying they had, compared to close to 23% of females.

Age also seems to play a role. Almost 30% of those aged 25 to 34 say they’ve broken up with someone over finances, and just over 30% of those aged 35 to 49 said the same. For people aged 50 to 64 and 18 to 24, the number drops to less than 15%, and for those over age 65, only around 6% said they had broken up with someone for these reasons.

Couples know they have to work on issues like communication and intimacy. But they often don’t realize they should put the same effort into working on finances together. Start today by being open and honest about money. Consider signing up for your free credit scores together at Credit.com, so you can see where you both stand.

This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,019 responses per question and is not statistically representative of the general population. This survey was conducted in September 2022.

Source: credit.com

Buying a used car can lower the cost of your purchase, letting you move into car ownership with a much smaller loan. This might also be beneficial if you don’t have the credit or income to qualify for a loan amount that would cover a new car price. You might get an even better deal if you buy a used car through a private seller. However, it’s important to ensure you’re protected from scams and engaging in a safe transaction.

This piece covers how to buy a used car from a private seller. That includes how to get a loan for a used car from a private seller.

When you’re buying a car from a private seller, there are some additional concerns you may not have when buying a vehicle from a dealership. Private sellers don’t have consumer reviews and brand reputation you can consider. So, you have to do some legwork to ensure you’re getting a good deal and aren’t getting scammed. Follow the steps below to buy a car from a private seller.

Start by understanding what you can afford. If you want to know how to finance a private car sale, start by getting an auto loan first. You can apply for auto loans online or with a local bank. Once you get pre-approved, you know how much used car you can afford.

Not sure if you can get approved for a car loan? Get your credit score first to see your odds of being approved and work toward improving your scores before moving forward with your purchase.

Privacy Policy

Use your loan pre-approval or cash on hand to set a budget for your car purchase. Avoid going outside that budget so you don’t have a financial hardship once you buy the used car.

Get matched with a personal

loan that’s right for you today.

Learn

more

Start researching cars that fit your needs. Read about cars you’re interested in online, and look into different considerations for older models. This helps you know what type of common issues to look for when you start checking out cars from private sellers.

Next, review the cars available from private sellers in your area. You can research options on Facebook marketplace, Auto Trader, eBay and any local classified publications, such as your city’s newspaper.

Once you spot a potential new-to-you ride, start by making contact with the seller. Take some time to feel them out and ensure they’re legitimate. Avoid meeting anyone by yourself or in a location you’re not comfortable with. If the seller is willing to come to a public location with the vehicle, that’s best. If not, take someone with you when you go to their home.

Ask to test-drive the vehicle. If you can have a mechanic or someone you trust who knows a lot about cars look over the vehicle, do so. You can also look up the CARFAX report on the vehicle using its VIN. This database and others like it provide some information about the vehicle’s history, including potential accidents, service records and how many owners the vehicle might have had.

Once you’re confident you’ve found the vehicle for you, start negotiations.

Once you and the private seller agree on a price for the vehicle, move forward with the transaction. Make sure you get any agreement in writing to protect yourself in the future. You may also want to pay by check so you have a paper trail demonstrating that money changed hands for the car.

Verify ownership documents when you complete the sale. If the individual has the title on hand, they should sign it over to you at that time. If the seller owes money on the car, there’s a lien on the title. You’ll need a bill of sale indicating you paid for the vehicle. The owner will then take your money to their bank to pay off the car so they can get a title to transfer to you.

Even if you go through a private seller and not a dealership, buying a car requires lots of paperwork. You’ll need to:

Always have a plan when you’re making large purchases. Create a budget and stick to it to avoid overcommitting yourself financially. Do the research to protect yourself from scammers. If a deal seems too good to be true, it may be.

If you need a loan to buy a used car from a private seller, start by comparing auto loan rates. Then, you can prepare yourself with everything you need to help finance your new car.

Article updated. Originally published July 15h, 2015.

Source: credit.com

The Fannie Mae Flex Modification Program (FMP) is a mortgage assistance solution designed to relieve borrowers facing financial hardship.

Are you looking to improve your mortgage management but don’t know where to start? Handling mortgage payments is challenging, especially if you’re facing economic difficulties and don’t know where or how to get financial assistance. The Fannie Mae and Freddie Mac Flex Modification Program may be the solution you’re looking for.

Learn what you need to know about the Flex Modification Program: how it works, who qualifies for it, and how you can apply. This comprehensive guide will help you understand the many benefits of FMP for a more stable financial future.

In This Piece:

The Fannie Mae Flex Modification program is a mortgage assistance solution designed to relieve borrowers facing financial hardship. This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure.

Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners.

Get matched with a personal

loan that’s right for you today.

Learn

more

The mortgage market has a few essential entities, including the government-sponsored enterprises called Fannie Mae and Freddie Mac. Their approach allows lenders to free up funds to provide more mortgage loans to borrowers.

But how does it work? Fannie Mae and Freddie Mac helped make mortgages more accessible by buying them from lenders. This allows lenders to have more money available to provide new mortgages to borrowers or invest in other financial opportunities. For example, if a lender originates a mortgage, they can sell it to Fannie Mae or Freddie Mac, who then include it in their portfolio or package it into mortgage-backed securities.

The Flex Modification Program offers loan modifications to eligible borrowers experiencing financial hardship. Here’s a breakdown of how the program operates:

Before considering the Flex Modification Program, it’s essential to understand its potential pros and cons.

Pros:

Cons:

Remember, these pros and cons will vary based on your circumstances. It’s essential to consult with your loan servicer and thoroughly review the modification terms to understand the potential benefits you may receive from participating in the program.

The Flex Modification Program is designed for borrowers struggling with mortgage payments due to financial hardship.

To qualify for the program, you must meet the following criteria:

Additionally, you must comprehend what a “hardship” entails to be considered for a loan modification. Each situation is evaluated individually, but common examples of hardships include loss of income, disability, serious illness, divorce, or the death of a co-borrower.

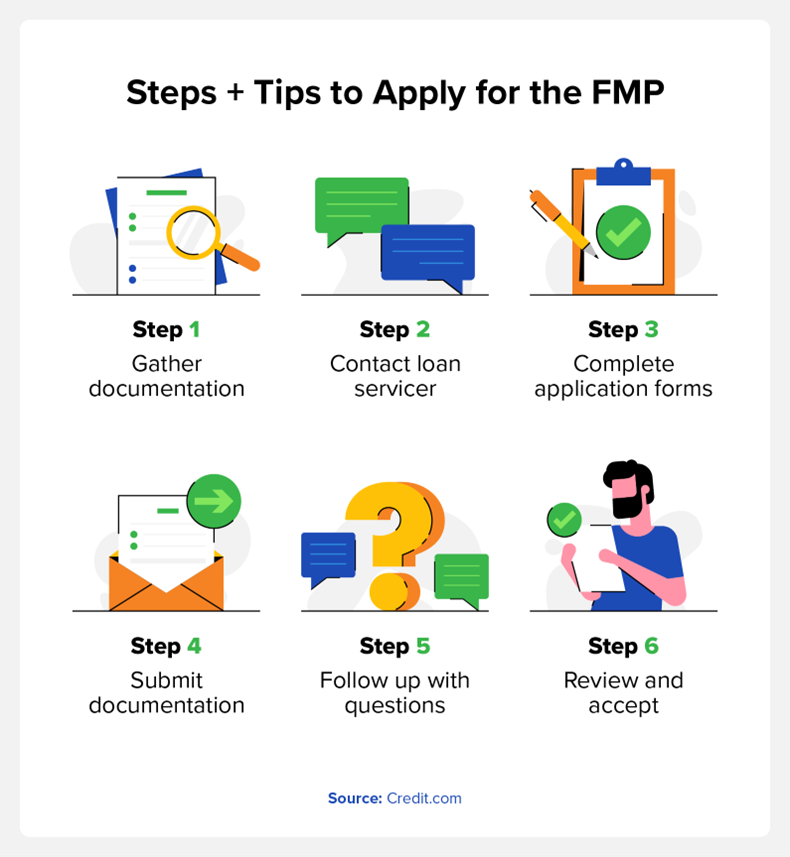

If you believe you meet the eligibility requirements for the Flex Modification Program, you can follow these steps and tips to apply:

Remember, each loan servicer may have a specific application process, so it’s crucial to communicate directly with them to ensure you have all the necessary information and are following the correct steps. Having to redo the application process due to easily-avoided mistakes is the last thing you need.

What if I don’t qualify? What can I do? Other mortgage payment assistance options are available if the FMP is not the right fit.

Fannie Mae and Freddie Mac offer additional programs catering to different circumstances. Some of these options include:

But before you move forward with one of these, it’s essential to analyze your alternatives and consult with your loan servicer to determine the best course of action based on your specific circumstances.

Let’s address some frequently asked questions about the Flex Modification Program:

Participating in the Flex Modification Program doesn’t directly impact your credit score. However, the delinquency prior to modification might be reported on your credit report

If your loan isn’t owned or guaranteed by Fannie Mae or Freddie Mac, you won’t be eligible for the Flex Modification Program. However, you should contact your loan servicer to inquire about other available mortgage assistance options or loan modification programs specific to your loan type.

The duration of the Flex Modification Program varies depending on the specific terms of the modification. Typically, the program aims to provide long-term mortgage relief by modifying the loan terms to make payments more affordable and sustainable for the borrower.

The revised terms may involve extending the loan term or adjusting the interest rate. It’s important to discuss the duration of the modification with your loan servicer, as it will depend on your circumstances and the terms agreed upon.

If you have previously received a loan modification, you may still be eligible for the Flex Modification Program. However, the specific requirements and eligibility criteria may change depending on your previous modification and the current guidelines set by Fannie Mae and Freddie Mac.

It’s crucial to communicate with your loan servicer and provide them with all the necessary information regarding your previous modification. They will assess your eligibility based on your unique circumstances and guide you through the application process.

Remember, these answers are general guidelines, and you must consult with your loan servicer to get accurate and personalized information based on your situation.

The Fannie Mae Flex Modification Program provides borrowers with a potential lifeline during financial hardship. It aims to make mortgage payments more manageable and sustainable by offering loan modifications. If you’re facing challenges with your mortgage payments, exploring the Flex Modification Program and other mortgage payment help options can help you find the assistance you need.

To take control of your mortgage management and improve your financial well-being. Consult with your loan servicer for accurate and personalized information based on your situation, and research different mortgage rates to make informed financial decisions.

Source: credit.com

While some states offset the high cost of college with substantial financial aid programs, Rhode Island’s offerings are much more limited. In fact, it has one of the lowest rates of state grant aid per full-time undergraduate student; Rhode Island provides about $170 in funding per student, the seventh-lowest amount in the country, according to a 2022 College Board report.

To put that in perspective, consider that South Carolina — the state with the highest level of state grant aid — provided about $2,590 per student.

Though limited, there are still some state aid programs. Whether you have your heart set on attending Brown University, The University of Rhode Island or the Rhode Island School of Design, here are the available financial aid programs specific to Rhode Island.

There are 13 public and private non-profit colleges and universities in Rhode Island.

Higher education in Rhode Island tends to be much more expensive than it is in other states. Even public universities and community colleges, which are typically lower-cost options, are costly.

Based on the average rates of tuition, fees and room and board for the 2020-2021 academic year, here’s how much you can expect to pay, according to data from the National Center for Education Statistics:

Public four-year school (in-state): $26,946 per year, about 26% more than the national average of $21,337.

Private four-year school: $61,692 per year, about 33% higher than the national average of $46,313.

Community college (in-state): $4,806 per year, about 37% higher than the national average of $3,501. (Community college costs don’t include room and board.)

Several factors are behind the high college costs. In addition to Rhode Island’s high cost of living and limited financial aid, it’s also home to several well-known private universities with hefty price tags that drive up average tuition rates. For example, a student’s estimated total cost for the 2023-2024 academic year at the Rhode Island School of Design is $81,810 — nearly double the national average for private schools.

Although public schools are more expensive in Rhode Island than in other states, attending a public university is still cheaper than private school — but only if you qualify for in-state tuition.

You qualify for in-state tuition if you meet one of the following criteria:

You attended an approved Rhode Island high school for at least three years.

You graduated from an approved Rhode Island high school.

You lived in the state for at least 12 months prior to enrollment.

Unlike some states, Rhode Island extends residency to undocumented students, including those with Deferred Action for Childhood Arrivals (DACA) status. As a result, undocumented and DACA students are eligible for in-state tuition and state aid in Rhode Island if they meet the other residency requirements.

Students may also have trouble finding funding opportunities in Rhode Island because its aid programs aren’t listed in one central location. Programs are usually provided through partnerships with other organizations, so they’re often listed on non-government websites that can be difficult to find if you don’t already know about them.

Although Rhode Island’s options are more limited than those of other states, you may be able to use one or more of the following programs to finance your education:

529 plans.

In-state tuition.

Scholarships.

Tuition waivers.

Student loans.

Other aid programs.

Student loan repayment assistance.

Rhode Island doesn’t have a prepaid tuition plan, but families can use a CollegeBound Saver 529 account to save and invest for a child’s future education. The money can grow tax-deferred in a CollegeBound Saver account, and the withdrawals are tax-free as long as they’re used for qualifying education expenses. Beneficiaries may use the funds at any U.S.-accredited college; they aren’t limited to Rhode Island schools.

Rhode Island has a higher-than-usual maximum contribution limit; families can contribute to an account until its total market value reaches $520,000 per beneficiary.

The CollegeBound Saver 529 has two other benefits:

State income tax deduction: Rhode Island taxpayers who contribute to this account may qualify for a state income tax deduction. They can deduct up to $500 in contributions individually, or $1,000 if they are married and file a joint return.

Starter Bonus: If you have a newborn or recently adopted a child, Rhode Island will contribute $100 if you open a new CollegeBound Saver account and deposit at least $100.

The average total cost of attendance for in-state students at Rhode Island public schools is less than half the average cost of attending a private school.

However, students who want to attend college outside of Rhode Island may qualify for the New England Board of Higher Education’s Tuition Break program. Students who are residents of member states — Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island and Vermont — can enroll in an eligible program at a public community college or university in another participating state at a reduced rate.

According to NEBHE , the average full-time student saves $8,600 per year with Tuition Break. Exact savings depend on the program and state. You can view the eligible programs and schools on the NEBHE website.

Rhode Island offers just two state scholarship programs, both of which are awarded based on academic merit and financial need. The programs are typically very limited in scope and are only available to students at particular schools.

The two Rhode Island scholarship programs are:

Through the Rhode Island Promise Scholarship Program, the state will cover up to the full cost of tuition and fees for qualifying students who attend the Community College of Rhode Island (CCRI) full-time for two years..

To qualify, students must be Rhode Island residents and enroll full-time at CCRI for the semester beginning immediately after their high school graduation.

The Rhode Island College Hope Scholarship is a state-funded award offered to eligible students at Rhode Island College (RIC). It is a last-dollar award, meaning it covers the student’s remaining tuition and fees after other grants and scholarships are applied.

To qualify, students must be Rhode Island residents and in their junior or senior years at RIC with a GPA of at least 2.5. Applicants must be on track to graduate or earn an approved certificate in a total of four years.

Adult students who have earned at least 60 credits within a four-year period at RIC are also eligible for the scholarship over a duration of two years or less.