Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

One of the best ways to grow your wealth is to take advantage of a high-yield savings account and make money from the interest. Depending on your age, the average savings in America can vary, but those who start younger can build more wealth because they have more time.

Use our free simple savings account calculator to see how your money can make money over time from interest payments.

Simple Savings Calculator

Total Savings

$

Breakdown of Savings

Starting Deposit

Total Contributions

Earned Interest

Simple Savings Account Calculator Help

The simple savings account calculator helps you easily calculate the annual percentage yield (APY) and accurately show how your investment can grow. Below, we go over each aspect of the calculator and how it works.

Starting deposit: When you open a savings account, this is your initial deposit. This first deposit plays a big role in how much your wealth will grow over time.

Monthly contribution amount: It’s beneficial to continue depositing into your savings account monthly. Adjust this amount in the savings account calculator to see how much your money can grow and benefit from compound interest.

Number of years: Giving your money time to grow is the ideal strategy due to compound interest.

Annual interest rate: Interest rates can vary depending on the bank and type of account. You can use certificates of deposit (CDs), a high-yield savings account, or money market accounts. Be sure to shop around to find the best interest rates before you decide.

How Much Should You Save Each Month?

How much you save each month is unique to your financial situation. However much you choose to deposit into your savings account, the important thing is to be consistent. One way to do this is by setting up automatic transfers from your checking to your savings each month after a payday.

You’ll also want to ensure you’re budgeting properly so you don’t fall behind on other expenses like bills or debt payments. A monthly budget template can help you create a strategy and see what amount works for you.

How Do You Calculate APY?

To calculate the simple interest amount in a savings account, multiply the account balance by the annual percentage rate. For example, if you save $10,000 in a year and have a high-yield savings account with a 4% interest rate, the calculation is:

$10,000 x 0.04 = $400

How Savings Can Improve Your Financial Well-Being

Having a savings account is not only helpful for building your wealth, but it also provides you with some security in an emergency. By finding a savings account with a high interest rate, you will make money by simply storing your savings in the account.

Improving your credit score can also help your financial well-being. A good credit score lets you benefit from lower interest fees and access to additional loans and lines of credit. If you want to know where you stand with your credit, sign up for your free credit report card. You can also utilize Credit.com’s ExtraCredit® service to get credit monitoring alerts, additional credit reporting, and more.

Helpful Links to Start Saving

Check out some of our other articles for more tips and strategies for saving and growing your wealth.

The average American net worth varies due to many factors, with some people making far more than others. If you’re behind the national average, it may seem difficult to catch up, but whether you have bad credit or a lot of debt, you can still begin building your net worth by learning how to generate passive income.

Passive income is a great way to generate more income, pay down your debt, and start saving and investing for your future. Here you’ll learn what passive income is, as well as different ways to make passive income online and offline. With 25 passive income ideas, there is something for everyone.

25 Passive Income Ideas:

Write an E-Book

Start a YouTube Channel

Try Affiliate Marketing

Create a Blog

Sell Stock Photos and Videos

Create an Online Course

Make Sponsored Content

Invest in Dividend Stocks

Invest in REITs

Invest in Index Funds and ETFs

Try Peer-to-Peer Lending

Stake Cryptocurrency

Utilize High-Yield Savings Accounts

Buy Government Bonds

Invest in Art

Buy Property to Rent

Rent Out a Room in Your Home

Buy Domain Names

License Your Music

Design Custom Products

Rent Out Your Vehicle

Use Your Vehicle as Ad Space

Create an App

Flip Unique Items

Rent Out Your Parking Space

What Is Passive Income?

Passive income is a type of income that comes from sources other than your regular employment, and involves a more hands-off approach. Passive income isn’t a “get rich quick” scheme, though some companies make big claims about generating passive income without any work. Passive income does take work to set up, but the goal is that you can make money without managing it on a day-to-day basis.

You’ll generally do most of the work by setting up your source of passive income. While it may require some upkeep every now and then, like updating a product or maintaining a rental property, you’ll earn the majority of your income while pursuing other endeavors.

Like other sources of additional income, passive income is taxable, but when done correctly, you can make enough passive income to surpass your tax bill.

1. Write an E-Book

Whether you’re a writer or not, an e-book can be a fantastic way to generate passive income. We no longer live in a world where publishers are the gatekeepers of books, so you can self-publish a book that can generate passive income. Various websites let you self-publish books, like Amazon’s Kindle Direct Publishing, Apple Books, and Barnes & Noble. Some of these sites also offer print-on-demand services for customers who want physical copies.

You can write a nonfiction book if you’re knowledgeable about a certain subject, or you can write fiction if you have an interesting story idea. Although this can generate passive income, self-publishing can require a bit of an investment. You’ll need to pay for an editor and book cover designer, and you may also want to pay for advertisements. But if you can do the cover art and marketing on your own, you may be able to save some money.

2. Start a YouTube Channel

There are many ways to make money using social media, but YouTube is one of the best ways to make passive income. YouTube pays content creators to run ads on their videos. In order to qualify for the YouTube Partner Program, you’ll need at least 500 subscribers, three new videos within the last 90 days, and 3,000 watch hours within the last year. Previously, you needed 1,000 subscribers and 4,000 watch hours, but the policy was updated in June 2023 with lower requirements.

Like other sources of passive income, making money from YouTube will require an up-front investment of time and money. You need a stable internet connection, camera, microphone, computer, and editing software. You also need to make consistent videos to qualify for the partner program. You can eventually generate passive income by making evergreen videos, because people will watch old videos that bring in revenue—and the more videos you have on your channel, the more money you can make.

3. Try Affiliate Marketing

Affiliate marketing is when you share a link to a product or service, and the company gives you a percentage of any sales made through that link. You can share these links on your social media pages, blog, newsletter, or anywhere else that allows you to post a link. Affiliate marketing is one of the best online passive income opportunities, and you can combine it with any other online method we mention in this article.

One of the most popular affiliate link programs is Amazon Associates. Let’s say you have a YouTube channel where you review electronics, and you make a video reviewing a new TV or laptop. If you link to that product on Amazon with your affiliate link, you’ll receive a percentage of the sale each time someone uses your link.

This isn’t only limited to Amazon, either. Many companies offer affiliate links, so it can be advantageous to reach out to companies for products and services you use regularly to see if they have an affiliate program.

4. Create a Blog

There are a variety of ways to make money from writing a blog. Like YouTube, old blog posts can generate passive income even if people read the post months or years after you wrote it. If you create your own website to host your blog, you can integrate Google Ads and use affiliate links to make money online.

Platforms like Substack combine blogs and newsletters, so every time you write a new post, subscribers receive an email. You can have paid subscriptions on Substack, so users pay a monthly fee to read your posts, and you can have free posts that go out to non-paying subscribers as well.

5. Sell Stock Photos and Videos

If you’re a photographer or videographer, you can earn money for your photos and videos. There are many different websites that buy stock photos and videos, like Shutterstock, iStock, and Getty Images. One thing to consider is that the website gets exclusive rights to your images or videos, but on some sites you can make between 15% and 45% in royalties.

6. Create an Online Course

Many people have expertise in a certain area, and utilizing your knowledge and skills to create an online course is a great way to make passive income online. For example, you can create a course for how to knit, how to take amazing photos, or how to program an app. Websites like Kajabi and Teachable allow you to host and sell your courses.

You may need to invest some time and possibly money in marketing your course to ensure you find the right audience. Some course-hosting platforms like Skillshare also categorize courses by topic for better discoverability.

If you start gaining a following on social media platforms or through a blog, you may get the opportunity to do sponsored content. Companies want to ensure they target the right audience, so if you have followers who may buy their product or service, they’re more likely to sponsor a piece of content. This typically means you discuss their product in a video or write about it in a caption.

In order to generate passive income from a sponsored opportunity, the company will give you an affiliate link. This allows you to make money up front for the sponsored content as well as passive income from anyone who uses your link to buy the product or service.

This route for passive income may take some time because companies typically want people to have a decent following before sponsoring content.

8. Invest in Dividend Stocks

Stocks can be a great way to make money while also investing in your future. When you buy a stock, you buy a small portion of a company. If the stock price rises and you sell it at a higher price, you make a profit, but the stock can also drop in price and lose you money. Some, but not all, stocks offer dividends, which pay investors a dividend per share if the company has a profitable quarter.

When the stock pays out dividends, you can receive the payment directly from your brokerage or reinvest the dividends by buying more of the stock. Like other investments, this can compound and turn into a lot of money over time if the company continues to profit. As you invest in dividend stocks, keep in mind the companies can raise or lower the dividend percentage at any time.

Use MarketBeat’s dividend calculator to look up specific stocks and estimate dividend returns.

9. Invest in REITs

Real estate investment trusts (REITs) are another investment opportunity. Rather than investing directly in a property, you can invest in a REIT, which is a company that owns and manages real estate.

Similar to other investments, there is risk that comes along with investing in REITs. For example, there’s a possibility your REIT investments will lose money if there’s a drop in the housing market.

10. Invest in Index Funds and ETFs

Index funds and exchange-traded funds (ETFs) are some of the safest investments because they offer diversification. Rather than investing in one company, index funds and ETFs allow you to invest in multiple companies simultaneously.

Legendary investor and founder of Vanguard John Bogle was a major advocate for index fund investing. More specifically, he advised people to invest in the S&P 500, an index of the 500 largest companies in the United States. ETFs are slightly different because there are higher fees, but they allow you to invest in a group of stocks for a specific industry. For example, ARKK is an ETF that holds shares for companies that work on innovative technology.

There is still a risk when investing in index funds and ETFs, but they are often lower risk than other forms of stock investing.

11. Try Peer-to-Peer Lending

Another way to make passive income is to become your own type of “bank” by doing peer-to-peer lending, sometimes called P2P lending. Banks make money on loans by charging interest to customers, and P2P lending allows you to do the same thing. Websites like Prosper and Funding Circle allow everyday people to lend and borrow money with various interest rates.

12. Stake Cryptocurrency

Cryptocurrency investing is a highly volatile form of investing, making it especially high risk. Some cryptocurrency platforms allow you to “stake” your crypto, which is when you allow the platform to hold your crypto and lend it to other people. Similar to P2P lending, you make money off the interest.

Cryptocurrency lending and trading is also high risk because there is little to no regulation. Crypto platforms like Voyager have been known to offer extremely high returns and then go bankrupt, preventing them from paying back their users. In extreme cases, there are stories of fraudulent activity from crypto platforms. But if you have a high risk tolerance, this form of investing can be incredibly lucrative.

13. Utilize High-Yield Savings Accounts

A safer way to make passive income is to open up a high-yield savings account, which allows you to make money simply by holding it in your account. Banks use customer funds to lend out money, but unlike crypto staking, bank funds are backed by the U.S. government via the FDIC. This means that if, for some reason the bank doesn’t have the money when you want your funds, the government would provide the bank with the money to pay you up to $250,000.

Many banks and financial institutions offer high-yield savings accounts, with some offering an annual percentage yield (APY) of over 4%. So if you opened an account with a 4.5% APY and deposited $1,000, you would have $1,045 after a year.

People maximize their passive income by not touching this money because it compounds each year. So using that same example, in the second year, you would then earn 4.5% of the $1,045 rather than the original $1,000. And if you add to the savings account each month, you can make quite a bit of money over time.

14. Buy Government Bonds

Perhaps the safest way to earn passive income from investing is to buy government bonds. A government bond is basically a loan to the federal government that pays you back the original amount with interest over a certain period. The reason government bonds are so safe is because the government backs them. When buying a stock, it’s possible to lose your money if the company goes out of business. Bonds are safer because as long as the government exists, you’ll make your money back.

Although government bonds are very low risk, they also offer low returns. Depending on various factors, government bonds may offer a 3–5% return over two to 30 years. To put that into perspective, S&P 500 index fund investing offers an average return rate of over 7.5%[1] .

15. Invest in Art

Similar to stocks, you can also invest in artwork. One way to do this is to buy works of art that you believe will increase in value later. If you’re knowledgeable about art and can find pieces selling for below their value that you can sell later for a profit, you can make a bit of money. Websites like Masterworks allow you to buy shares of artwork with other investors so you take on less risk.

16. Buy Property to Rent

Many people generate passive income by purchasing properties to rent. If you can afford the initial investment of buying a single-family home or condo, you can then rent them out to tenants for a profit. For example, if you buy a house and your mortgage is only $1,000, you can make a profit by charging any amount over your mortgage cost.

In order to take advantage of the passive income aspect of renting, you may benefit from hiring an individual or company to manage the property. Property managers collect the monthly rent and take care of maintenance issues for a fee. Should you decide to invest in rental properties, it’s helpful to factor in the cost of potential home repairs before, during, and after tenants live there.

17. Rent Out a Room in Your Home

If you don’t have the money for a down payment or don’t want to take on the risk of purchasing a rental home, you can always make some extra income by renting out a room. If you have a spare room in your home, you can rent it out for a monthly fee. This is a great option for families whose children recently moved out.

You can use websites like Airbnb and VRBO to connect you with renters. Although many people use Airbnb for short-term rentals during vacations, you can also offer long-term rentals through the website. These sites also let you vet renters before they move in, so you have control over who rents the room.

18. Buy Domain Names

Buying domain names is a sort of investing, so it does come with some risk. People and businesses buy domain names to host their websites, so you can purchase a variety of inexpensive domain names in hopes of people buying them from you later for more. You can typically buy domain names for less than $10 through websites like GoDaddy, but if they don’t sell, you’ll need to pay the annual cost to keep the name.

While this may be a risky investment, people have made a lot of money flipping domain names. It was a big money-maker during the “dot com boom” in the 1990s, Help.com sold for $3 million and NFTs.com sold for $15 million in 2023. Many domains don’t sell for millions, but you may still be able to make a decent profit off domain names in high demand.

19. License Your Music

If you’re a musician, you can license your music in a similar way to selling stock photos and videos. Some websites like Music Vine pay musicians 30% for nonexclusive deals or more for an exclusive license. There are also websites like Epidemic Sound that market to YouTubers and filmmakers by offering a subscription service for royalty-free music.

20. Design Custom Products

For those who are artistically inclined, you can make money creating designs and selling them on websites that sell custom products. Websites like Redbubble, Teespring, and Society6 offer print-on-demand services for your artwork. These websites sell a wide range of products like T-shirts, coffee mugs, phone cases, and more. You get a percentage of the sale every time a customer goes to the website and chooses your design for any of these products

If you have old artwork you created in the past or simply feel like creating in your spare time, you can generate passive income as long as your art is hosted on these types of websites.

21. Rent Out Your Vehicle

Services like Uber and Lyft are popular side hustles, but you can make passive income by renting out your vehicle instead. When people are traveling or have their car in the repair shop, they often need a vehicle to get around. Rather than going to a rental car company, they can rent a vehicle through other websites like Turo or Getaround.

22. Use Your Vehicle as Ad Space

In addition to renting out your vehicle, you can make passive income by using your vehicle as ad space.

Websites like Wrapify connect businesses and drivers, and depending on how much of your car you’re willing to cover with ads, Wrapify will pay you between $181 and $452 per month. There are also sites like FreeCarMedia.com that pay you for wrapping your vehicle or simply advertising on your rear window.

23. Create an App

If you’re a programmer who can create an app, this may be the best way for you to make passive income. Whether it’s a fun game or an app that provides value and convenience, use your creativity and skills to generate income. Apple and Google allow developers to submit their apps, giving you a percentage of the sale each time someone buys the app.

24. Flip Unique Items

One of the oldest ways to generate passive income is to buy unique items, hold them, and sell them at a later date for a profit. If you’re knowledgeable about a certain type of item or are willing to learn, you can make a decent amount of money by buying and holding items.

This is ideal for people who like shopping at thrift stores or going to garage sales. You may find antique toys, memorabilia, sports trading cards, comic books, or other items for a low price that are either worth a lot of money now or will be in the future.

To sell the items or see how much items are selling for, you can use websites like eBay, OfferUp, Craigslist, or Facebook Marketplace.

25. Rent Out Your Parking Space

Some people are willing to pay for a good parking spot. If you have a space you’re not using or don’t mind giving up, you can make money renting it out—especially if you live in an urban area. Websites like SpotHero allow you to list your space.

What’s the Best Source of Passive Income?

The best source of passive income is unique to each individual. There are many options on this list, and some allow you to capitalize on different skill sets. For example, if you have expertise in certain subjects, the best sources of passive income may be online courses and e-books. If you have knowledge about stocks or are willing to learn, investing may be the best option.

When deciding which passive income sources are right for you, it may be beneficial to weigh out the pros, cons, and risks of each one. Remember that many of these options require an initial investment of money and time to get started. Consider your own risk tolerance and financial situation before going all in on any of these methods.

Do You Need Money to Make Passive Income?

While you’ll need money to get started with many passive income ideas, this isn’t the case for every method. For example, if you own a vehicle or have an extra room in your home, you can start renting them out. If you have a computer and internet connection, you have even more options.

Many people who make passive income succeed because they are willing to learn and can invest time into researching these topics. There’s a wealth of information online where you can learn how to excel at specific passive income opportunities like writing an e-book, succeeding as a YouTuber, or using affiliate links.

The Benefits of Multiple Streams of Income

Depending on your specific situation, you may want more than one source of passive income. Whether you’re already in a healthy financial situation or are trying to build your personal wealth and credit score, more income streams means more financial freedom.

The primary benefit of passive income is that you can make money with minimal effort. This means once you get one source of passive income rolling, you can begin adding others so you have multiple income streams that don’t require too much time or attention.

How Passive Income Can Help Improve Your Credit Score

A poor credit score can lead to many challenges—like making it difficult to get approved for new lines of credit, loans, and rental applications—and cost you a lot of money in interest in the long run. Passive income can help you fix your credit by allowing you to pay off your debts. Lenders also look at your total income, so making additional income can help with approvals for new lines of credit, which can also help improve your score. It’s important to know the current state of your credit health. You can get a free credit report card on Credit.com which breaks down your credit score factors and assigns a letter grade for each area, or sign up for our ExtraCredit® subscription for additional credit tools.

Not only are SUVs spacious, but many are also family vehicles, so they come with high-end safety features. These features make some SUVs cheaper to insure than other popular vehicles on the market. The Subaru Outback takes the top spot on this list, and it’s also rated one of the safest midsize vehicles by the Insurance Institute for Highway Safety.

SUV

Average Annual Premium

Subaru Outback

$1,603

Honda CR-V

$1,635

Honda Pilot

$1,726

Ford Escape

$1,734

Honda Odyssey

$1,735

What Factors Make a Vehicle Expensive to Insure?

The primary factor that makes a vehicle more expensive to insure than another is the risk. Insurance companies calculate the risk for different vehicles based on how many claims people file for those vehicles, plus the cost of the repairs. While this data can’t predict the likelihood of someone getting into an accident, the data gives insurers a rough idea.

Insurance providers look at how much a vehicle costs to repair and the likelihood of the vehicle being in an accident. For example, insurance rates are higher for sports cars because people who buy sports cars are more likely to speed and drive recklessly, based on the data.

Some of the most common factors that make vehicles more expensive to insure include:

Vehicle age: An older vehicle may not have the newest safety features, but premiums may be lower on some older vehicles if the average repairs cost less.

Vehicle value: When cars are more expensive, they’re often more expensive to insure as well.

Cost of parts: Some vehicles have more expensive and specialty parts, which cost more to replace if the vehicle is in an accident. Various trim features in a vehicle can also raise the price of premiums.

Safety rating: Many insurance policies also cover physical injuries to you or another driver, which is why safety ratings play a major role in determining the cost of insurance.

Size: Although a larger vehicle may be safer, it can also cause more damage if it’s involved in an accident.

Most Expensive Cars to Insure

If you’re thinking about purchasing a new or used vehicle, it’s helpful to know which types of vehicles typically have the highest rates. They include:

Sports cars

High-end luxury vehicles

Electric vehicles

Cars that attract thieves

These vehicles are more expensive than others primarily due to the overall cost of repairs. For example, while electric vehicles may save you money on fuel, the cost of the battery can range from $4,000 to $20,000. There are also certain vehicles that thieves commonly target. A recent article from MoneyGeek[1] listed the following as the top 10 most stolen vehicles in America:

Chevrolet trucks

Ford trucks

Honda Civic

Honda Accord

Toyota Camry

GMC trucks

Nissan Altima

Honda CR-V

Jeep Cherokee and Grand Cherokee

Toyota Corolla

5 Tips to Get Cheaper Car Insurance

Whether you want cheap insurance for your new vehicle or to lower the rate for your current vehicle, these five tips may help.

Be a good driver. This sounds obvious, but it’s a must. When you’re a good driver, you save money on insurance. This means avoiding car accidents, DUIs, and other major violations.

Consider the insurance cost when buying a new vehicle. A vehicle’s make and model alone can make car insurance more expensive. Remember this when you’re buying a new vehicle, because not only will you have monthly car payments when financing a car, but you’ll also have insurance premiums.

Shop around. Like many other expenses and purchases, it’s a good idea to get multiple quotes before settling on an insurance company.

Look for discounts. Some insurance providers offer discounts, so be sure to ask. You may also receive discounts for bundling your auto and home insurance through one provider.

Improve your credit score. Your credit score may impact your car insurance rate, so make sure you watch for derogatory marks on your credit report that can lower your score.

FAQ

Here, we go over some of the most common questions people have about car insurance rates.

What Type of Car is the Least Expensive to Insure?

Subaru holds the top two spots for the cheapest cars to insure: the Subaru Outback and the Subaru Crosstrek.

Why Are Some Cars Cheaper to Insure?

Some cars are cheaper to insure because they’re cheaper to repair, have better safety features, and are a low-risk for insurance providers based on their data.

Is Insurance Cheaper for Older Cars?

Insurance for older cars is not necessarily cheaper than newer cars. If an older vehicle is more expensive to repair or has poor safety features, it may have higher rates. on the other hand, older vehicles that meet current safety standards and are inexpensive to repair may have lower rates than some newer vehicles.

What’s the Most Expensive Car to Insure?

Out of the top 25 most popular vehicles in the United States, the Tesla Model Y is the most expensive car to insure, and the Tesla Model 3 is the second most expensive.

How Your Credit Score Affects Your Car Insurance Rate

Many people don’t realize that not only does your credit score affect the cost of your vehicle, but it can also affect your insurance rates. If you have derogatory marks on your credit report from late payments, missed payments, or collections, you may face higher insurance premiums.

Before you shop for auto insurance, it’s helpful to know your credit score. You can receive a free credit report card at Credit.com, and our ExtraCredit® subscription offers even more credit management tools.

Methodology

Data was sourced from Quadrant Information Services and provided to NerdWallet[1] and Bankrate[2] . Both studies analyze data from ZIP codes throughout all 50 states and Washington, D.C., and are weighted based on geographic region and population.

NerdWallet’s research used data from Kelley Blue Book for the top 25 best-selling models, along with rates from different ZIP codes in the United States. NerdWallet based its data on both male and female drivers 35 years old with good credit and clean driving records using the following coverage limits:

$100,000 bodily injury liability coverage per person

$300,000 bodily injury liability coverage per crash

$100,000 property damage liability coverage per crash

$100,000 uninsured motorist bodily injury coverage per person

$300,000 uninsured motorist bodily injury coverage per crash

Collision coverage with $1,000 deductible

Comprehensive coverage with $1,000 deductible

The Bankrate study analyzed rates for a 40-year-old female and male who have clean driving records and good credit. Rates are for full coverage and are based on the following limits for a 2021 Toyota Camry that drives five days per week and roughly 12,000 miles per year:

$100,000 bodily injury liability per person

$300,000 bodily injury liability per accident

$50,000 property damage liability per accident

$100,000 uninsured motorist bodily injury per person

$300,000 uninsured motorist bodily injury per accident

Here are some alternatives to no-credit-check loans that are ideal for individuals with little to no credit history.

Search for Lenders Who Take Alternative Credit Backgrounds Into Account

While credit history is typically used to assess a borrower’s risk, some banks will accept alternative data to determine your eligibility such as salary, rent, or utility payment history and bank statements. Remember that most lenders will only accept alternative data for smaller loans like credit cards, personal loans, and auto loans as opposed to larger loans like mortgages.

To find a lender that accepts alternative credit backgrounds, contact financial institutions in your area or apply for loans online. Make sure to have important documents such as bank statements, W-2s, tax returns, and rent payments readily available.

You can also opt to have alternative data reflected in your credit history. For example, you can sign up for a service that reports your rent and utility payments to the three credit bureaus. This is an excellent way to start building your credit.

Credit tip: You may have better luck if you consult with a lender face-to-face rather than over the phone.

Request a Payday Alternative Loan (PAL) Through Your Credit Union

Some credit unions offer payday alternative loans that are typically lower-cost substitutes to pricey payday loans. PALs are small loans granted in amounts ranging from $200 to $1,000, and they have a maximum APR of 28%. To qualify, you must have been a member of a credit union for at least one month.

Credit tip: You can research credit unions to join by visiting MyCreditUnion.gov.

Apply for a Secured Loan

Secured loans involve putting down a valuable asset as collateral. Assets typically used as collateral include cars, houses, or savings accounts. While these types of loans are beneficial because they have less strict credit history requirements, they are risky in the sense that you could potentially lose the asset you put down as collateral if you’re unable to pay the loan back.

Credit tip: Assess whether you can avoid losing the asset before putting it down as collateral.

Borrow Money From Your Retirement Account

If you have a 401(k) plan, you can take out a loan against your account. Most plans allow you to borrow up to 50% of your savings up to $50,000. Since you are essentially borrowing money from yourself, you won’t need to show credit history to take out a 401(k) loan.

While taking this route could cost you in investment earnings, it is generally a better option than other no-credit-check loans that charge high interest rates. Just make sure to repay the loan within five years to avoid paying taxes and penalties.

Credit tip: Avoid taking out a 401(k) loan if you plan on leaving the company, as you may have to pay it off right away.

Find a Trustworthy Cosigner

If you lack credit history, including a trustworthy family member or friend as a cosigner might help you secure a loan. For a cosigner to improve your chances of being approved, they need to have a good credit score and preferably a long credit history.

However, getting someone to agree to cosign may prove to be difficult, because if you miss payments or default, the cosigner’s own credit will be hurt. Note that this could strain your relationship with the cosigner if you get behind on payments.

Credit tip: If someone in your life agrees to cosign, consider scheduling a reminder to make payments on time.

Turn to a Family Member

If you’re in a position where you need money to cover an expense, consider asking a family member or close friend for a loan. While it might be tough to bring it up, this route can help you avoid getting stuck in a situation with a predatory lender.

Credit tip: When borrowing money from family, consider drafting up a contract to ensure everyone is on the same page about the loan amount, repayment timelines, and any interest that may be charged.

How to Get a Loan With No Credit FAQ

Below, we’ve answered some common questions regarding getting a loan with no credit.

Can I Get a Loan With No Credit?

Yes, it’s possible to get a loan with no credit, although it will be more difficult to get approved, and you may incur a higher interest rate.

What Loans Can I Get With No Credit?

Types of loans you can get with no credit include no-credit-check loans, secured loans, online loans, credit union loans, and family loans.

How Much Can I Borrow With No Credit?

The exact amount you can borrow with no credit will depend on the type of credit account you’re approved for. Remember that the higher your credit score, the more money you’ll be able to borrow.

What Is a Good Credit Score to Get a Loan?

While the exact credit score to get a loan varies, borrowers need a FICO® score of at least 670 to fall within the good credit score range.

How to Build Credit

Establishing credit from the ground up can seem daunting. Here are some ways to start building credit so you can get approved for loans more easily in the future:

Become an authorized user: Ask a trusted person in your life to add you as an authorized user to their credit card account so that you can establish credit history.

Apply for a secured credit card: A secured credit card is a type of beginner-friendly card that requires you to put down a refundable deposit. Since these cards pose less risk to the lender, they’re easier to get approved for when first establishing credit.

Report rent or utilities: While most companies don’t report to the credit bureaus, you can sign up for a rent and utility reporting service that reports these payments to build credit faster.

Apply for a credit-builder loan: A credit-builder loan is an installment loan specifically geared to individuals looking to build credit history. When you take out a credit builder loan, the borrowed funds are placed in a secure savings account or certificate of deposit (CD) and held as collateral until you repay the loan.

Ready to start building your credit? ExtraCredit® is a tool that provides complete credit coverage, including rent and utility reporting and other credit profile-building offers. Try it for free today.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Information in this piece is accurate as of August 2023.

The best credit cards provide you with cash back rewards, points you can redeem for purchases at your favorite stores, travel miles and much more. Each credit card is fine-tuned with specific perks and benefits, and you’ll find plenty here that will fulfill your needs.

We’ve reviewed 25 credit cards from our partners that not only provide great rewards, but we’ve found the best credit cards for people with no credit, bad credit and fair credit. We’ve also provided a complete guide to help you better understand how credit cards work, as well as some tips to assist you in choosing the right one.

Table of Contents:

Best Overall Cards From Our Partners

The best credit cards bring in new customers by providing various perks, bonuses and benefits. The following credit cards have some of the best sign-up offers that come in the form of cash back rewards and travel miles.

Best for: Repairing credit

Secured Chime Credit Builder Visa® Credit Card

Apply Now

on Chime’s secure website

Annual fee

Recommended credit score

You can qualify for the Secured Chime Credit Builder Visa® Credit Card with a $200 direct deposit

or more, and all you need is a checking account. As you use this secured credit card, you can

build your credit score—and there’s no minimum security deposit.

see more details

Pros

Helps build credit

No security deposit required

No interest

Cons

Needs Chime checking account

Best for: Low APR

Upgrade Cash Rewards Visa®

Apply

Now

on Upgrade’s secure website

Annual fee

Recommended credit score

The Upgrade Cash Rewards Visa® card has a flat rate rewards program for all purchases, which go on

your card when you make your monthly payments. The card also comes with peace of mind from its free

fraud liability program.

see more details

Pros

No annual fee

Fraud liability

Flat rate rewards

Cons

No debt card for welcome bonus

Balance Transfer

Balance transfer credit cards allow you to transfer debt from one account to another, and the best ones come with little to no fees.

Best for: Bonus categories and balance transfers

UNITY® Visa Secured Credit Card – The Comeback Card™

Apply

Now

on OneUnited Bank’s secure website

Annual fee

Recommended credit score

The UNITY® Visa Secured Credit Card – The Comeback Card™ is not only a balance transfer card, but

it’s a secured credit card as well, so there’s no minimum credit score required. This card has a

9.95% balance transfer rate for six months and a low fixed-interest rate of 17.99%.

see more details

Pros

No minimum credit score required

Low fixed interest rate

Fast approval

Cons

Annual fee

$250 deposit to open account

No Interest

Low interest is great, but having 0% interest is even better. These cards have their advantages and disadvantages, such as the advantage of not needing a good credit score, but their usage may be limited.

Best for: No interest

Merit Platinum Card

Apply

Now

on Merit Platinum’s secure website

Annual fee

Recommended credit score

The Merit Platinum Card does have an annual fee broken into monthly payments of $14.77, but their 0%

APR makes up for this. They also allow for a seven-day risk-free trial. With this card, you’ll gain

access to a $750 line of credit for Horizon Outlet and have other member benefits like roadside

protection and credit report monitoring.

see more details

Pros

0% APR

$750 line of credit

Works with bad or no credit

Cons

Annual fee

Can only use at Horizon Outlet

Doesn’t report to credit bureaus

Best for: No interest

Net First Platinum

Apply

Now

on NetFirst Platinum’s secure website

Annual fee

Recommended credit score

The Net First Platinum is a credit card that you can get approved for without any credit as well as

if you have bad credit. It provides you with a $750 line of credit for Horizon Outlet, and you also

receive member benefits like legal assistance, roadside protection and identity theft insurance.

see more details

Pros

0% APR

$750 line of credit

Works with bad or no credit

Cons

Annual fee

Can only use at Horizon Outlet

Doesn’t report to credit bureaus

Best for: No APR

Freedom Gold Card

Apply

Now

on Freedom Gold’s secure website

Annual fee

Recommended credit score

The Freedom Gold Card gives cardholders a $750 line of credit for Horizon outlet, which sells a wide

range of products as well as clothing. There’s no credit check or employment check required to get

approved, either. It also comes with additional member benefits like roadside protection.

see more details

Pros

No activation fee

$750 credit limit

No credit check

Cons

Annual fee

Can only use at Horizon Outlet

Lowest Interest

One of the primary factors people look for in a credit card is a low annual percentage rate (APR). This is the interest you pay on purchases after the introductory rate.

Best for: Bonus categories and balance transfers

UNITY® Visa Secured Credit Card – The Comeback Card™

Apply

Now

on OneUnited Bank’s secure website

Annual fee

Recommended credit score

The UNITY® Visa Secured Credit Card – The Comeback Card™ is not only a balance transfer card, but

it’s a secured credit card as well, so there’s no minimum credit score required. This card has a

9.95% balance transfer rate for six months and a low fixed-interest rate of 17.99%.

The Applied Bank® Secured Visa® Gold Preferred® Credit Card provides you with a credit limit of up to

$5,000 and has no minimum requirement for your credit score. You can open an account with a deposit

as low as $200.

see more details

Pros

Low fixed APR

High max credit limit

Cons

Annual fee

Cash Back

Cash back credit cards put money back in your pocket based on your spending. This can be either a flat rate or for specific categories like dining, entertainment or retail shopping.

Best for: Auto, home and health spending

Upgrade Triple Cash Rewards Visa®

Apply

Now

on Upgrade’s secure website

Annual fee

Recommended credit score

The Upgrade Triple Cash Rewards Visa® credit card provides 3% cash back for auto, home and health

categories. This is a quality choice if you’re doing home upgrades, repairing your car or purchasing

medications and using a gym membership

see more details

Pros

Up to 3% cash back

Umlimited rewards

Fraud liability coverage

Cons

Niche reward categories

Need debit card for welcome bonus

Best for: High percentage rewards

Petal® 2 Card

Apply Now

on Petal’s secure website

Annual fee

Recommended credit score

The Petal 2 card has no fees and is the perfect card for individuals with credit scores from poor to

excellent. You’ll receive 1% to 1.5% cash back on all purchases and up to 10% cash back when

shopping at certain stores.

see more details

Pros

No fees

High cash back rewards

No minimum credit score

Cons

No introductory offer

High APR

Travel

For those who travel, travel cards with top-tier rewards may be the right choice for you. You can get free airline miles along with other perks like points for rental cards and hotel stays.

Best for: Travel

Mastercard® Black Card™

Apply

Now

on Luxury Card’s secure website

Annual fee

Recommended credit score

The Mastercard® Black Card™ is a travel card that has 2% airfare redemptions with no blackout dates

or seat restrictions. You’ll also receive enrollment in Priority Pass™ Select, with access to 1,300+

airport lounges worldwide with no guest limit.

see more details

Pros

Low ongoing

Lounge access

Luxury travel benefits

Cons

High annual fee

Best for: Low APR and travel

Mastercard® Titanium Card™

Apply Now

on Luxury Card’s secure website

Annual fee

Recommended credit score

The Mastercard® Titanium Card™ is a travel card with a low ongoing APR of 19.24%. You’ll receive 24/7

Luxury Card Concierge® as one of the benefits along with 2% for airfare demptions with no blackout

dates or seat restrictions.

see more details

Pros

Luxury Card Travel® benefits

Airfare rewards

Cell phone protection

Cons

Annual fee

Best for: Low APR and travel

Mastercard® Gold Card™

Apply

Now

on Luxury Card’s secure website

Annual fee

Recommended credit score

The Mastercard® Gold Card™ has 2% airfare redemptions with no blackout dates or seat restrictions and

2% cash back. You also receive lounge access at over 1,300 airports worldwide and additional

benefits at hotels like room upgrades and free wifi.

see more details

Pros

Luxury Card Travel® benefits

Airfare rewards

Lounge access

Cons

High annual fee

Bad Credit

In order to build credit, you need a history of good credit—these are our top picks for credit cards if you’re working on improving your mid- to low-range credit score by adding more positive payments to your credit report.

Best for: Groceries and gas

Aspire® Cash Back Reward Card

Apply

Now

on Aspire’s secure website

Annual fee

Recommended credit score

The Aspire® Cash Back Reward Card gives cardholders a credit line of up to $1,000, and you’ll also

receive 1% cash back on all of your purchases. When shopping for groceries or getting gas, you can

earn up to 3% cash back as well.

see more details

Pros

Up to 3% cash back

1% flat-rate on other purchases

Up to $1,000 credit limit

Cons

Annual fee

High APR

Fair Credit

If your credit score falls within the 630 to 689 range, while not an excellent credit score, there are still plenty of cards you can apply for.

Best for: Building credit

Avant Credit Card

Apply

Now

on Avant’s secure website

Annual fee

Recommended credit score

The Avant Credit Card allows people with a credit score of 580 to 669 begin building their credit

score. It can be difficult to get a credit card with a fair credit score, so this card can be quite

helpful—they alsoregularly review your payment history for potential credit line increases.

see more details

Pros

Fast and easy application

Soft inquiry for credit check

Cons

Annual fee

High APR

Best for: Low APR

Upgrade Cash Rewards Visa®

Apply

Now

on Upgrade’s secure website

Annual fee

Recommended credit score

The Upgrade Cash Rewards Visa® card has a flat rate rewards program for all purchases, which go on

your card when you make your monthly payments. The card also comes with peace of mind from its free

fraud liability program.

see more details

Pros

No annual fee

Fraud liability

Flat rate rewards

Cons

No debt card for welcome bonus

Secured Credit Cards

Secured credit cards are a great option for those with no credit or bad credit. They work by providing you a credit line that uses your own money. You simply make a deposit, which becomes your credit limit, and you raise your score as you use your card and make your monthly payments.

Best for: Repairing credit

Secured Chime Credit Builder Visa® Credit Card

Apply

Now

on Chime’s secure website

Annual fee

Recommended credit score

You can qualify for the Secured Chime Credit Builder Visa® Credit Card with a $200 direct deposit

or more, and all you need is a checking account. As you use this secured credit card, you can

build your credit score—and there’s no minimum security deposit.

see more details

Pros

Helps build credit

No security deposit required

No interest

Cons

Needs Chime checking account

Best for: Repairing credit

PREMIER Bankcard® Secured Credit Card

Apply

Now

on PREMIER Bankcard®’s secure website

Annual fee

Recommended credit score

The PREMIER Bankcard® Secured Credit Card doesn’t require a checking account, and you can have a

credit limit of however much you deposit, up to $5,000. Regardless of your credit score, you can use

this card to begin building or repairing your credit.

The Applied Bank® Secured Visa® Gold Preferred® Credit Card provides you with a credit limit of up to

$5,000 and has no minimum requirement for your credit score. You can open an account with a deposit

as low as $200.

see more details

Pros

Low fixed APR

High max credit limit

Cons

Annual fee

Best for: Secured credit

The First Latitude Platinum Mastercard® Secured Credit Card

Apply Now

on First Latitude’s secure website

Annual fee

Recommended credit score

The First Latitude Platinum Mastercard® Secured Credit Card offers lines of secured credit between

$100 and $2,000. During your first year, they have an introductory offer for a $25 annual fee, which

changes to just $35 per year after that.

see more details

Pros

Low first-year annual fee

No credit score requirement

Low minimum deposit

Cons

Annual fee

*FICO scores and credit scores are used to represent the creditworthiness of a person and may be one indicator to the credit type you are eligible for. However, credit score alone does not guarantee or imply approval for any credit offer.

The Top Cards

The best credit cards depend on what you need. Whether you’re looking for a card that has low interest, one with the most rewards or one that gives you points for traveling, we broke down the top cards into nine categories.

Using similar criteria to our overall methodology, we’ve chosen the top card from each category.

How We Chose the Best Credit Cards

To rank the best credit cards, we reviewed over 25 credit cards from our partners. The primary criteria we looked at takes into consideration aspects cardholders look at during their decision-making process and includes:

Intro APR (10 points)

Regular APR (20 points)

Fees (15 points)

Works with low credit scores (15 points)

Cash back rewards (20 points)

Bonus offers (15 points)

Additional perks (5 points)

The best credit cards depend on your specific wants, needs and circumstances based on your specific credit score. Below, we discuss more about how to choose the right credit card for your situation.

There’s a lot of information about each specific card, so we listed the top cards with each of their primary benefits below to give you an overview at a glance.

Best Overall Cards From Our Partners

Secured Chime Credit Builder Visa® Credit Card: This is a card that is for individuals with bad credit or no credit, and it also has 0% interest on purchases. There’s no minimum security deposit as well.

Upgrade Cash Rewards Visa®: For every purchases, you make with this card, you’ll receive 1.5% cash back, and it also comes with a $200 signup bonus.

Best Balance Transfer Credit Cards

UNITY® Visa Secured Credit Card – The Comeback Card™: 9.95% on balance transfers for the first six months and then 17.99% fixed APR after.

Best Credit Cards for No Interest

Secured Chime Credit Builder Visa® Credit Card: This secured credit card helps those looking to repair or build credit and comes with 0% interest. There’s also no minimum security deposit.

Merit Platinum Card, Net First Platinum and Freedom Gold Card: Each of these cards comes with the same benefit of 0% interest as well as member benefits for their $177.24 annual fee. Although the card is limited to shopping at Horizon Outlet, 0% interest is hard to beat.

Best Credit Cards for Low Interest

UNITY® Visa Secured Credit Card – The Comeback Card™: 9.95% on balance transfers for the first six months and then 17.99% fixed APR after.

Applied Bank® Secured Visa® Gold Preferred® Credit Card: This card gives cardholders a credit limit of up to $5,000, and there’s no minimum credit score required. It also has a low 9.99% fixed interest rate and is great for anyone looking to build their credit score.

Best Cash Back Credit Cards

Upgrade Triple Cash Rewards Visa®: Ongoing APR as low as 14.99% on all purchases along with 3% cash back on home, auto and health purchases.

Petal® 2 Card: The Petal® 2has one of the highest cash back percentages at 10% when you shop at select merchants, and you’ll receive 1.5% cash back on all other purchases.

Best Travel Credit Cards

Mastercard® Titanium Card™: 0% APR for the first 15 billing cycles and 2% rewards on airfare redemptions with no blackout dates or seat restrictions.

Mastercard® Gold Card™: 0% APR for the first 15 billing cycles and 2% rewards on airfare redemptions with no blackout dates or seat restrictions.

Mastercard® Black Card™: 0% APR for the first 15 billing cycles and 2% rewards on airfare redemptions with no blackout dates or seat restrictions.

Best Credit Cards for Bad Credit

Secured Chime Credit Builder Visa® Credit Card: Secured credit card you can open with a $200 deposit or more along with a checking account.

Aspire® Cash Back Reward Card: A secured credit card option that also gives you 1% cash back on all of your purchases. You can also earn up to 3% cash back on groceries and gas.

Best Credit Cards for Fair Credit

Avant Credit Card: Can qualify with a credit score between 580 and 669.

Upgrade Cash Rewards Visa®: Ongoing APR as low as 14.99% and 1.5% flat-rate cash back on purchases.

Best Secured Credit Cards

Secured Chime Credit Builder Visa® Credit Card: Secured credit card you can open with a $200 deposit or more along with a checking account.

PREMIER Bankcard® Secured Credit Card: Secured credit card with a spending limit of up to $5,000.

Applied Bank® Secured Visa® Gold Preferred® Credit Card: Requires a $200 deposit and can go up to $5,000.

The First Latitude Platinum Mastercard® Secured Credit Card: Secured credit card with a limit of between $100 and $2,000.

A Beginner’s Guide to the Best Credit Cards

Whether you’re new to credit and credit cards or are experienced and just looking for the best options, this brief guide will provide you with additional information before choosing your new card.

How Do Credit Cards Work?

Credit cards are like taking out small loans, allowing you to buy something now and pay for it later on. You’ll need to pay back the money you borrowed on your credit card, and this comes with interest.

Some cards offer 0% interest for a certain amount of time, which means you’ll only pay back the same amount charged on the credit card.

Here’s what a basic credit card transaction looks like:

The purchase: Make a purchase with your credit card.

The authorization: The card reader used to run your card contacts your credit card company to ensure the funds are available based on your max limit.

The merchant payment: Your credit card company pays the merchant for the product or service you purchased.

The credit card payment: Each month, you’ll have a statement that shows how much you owed based on all of the purchases you made.

Learn more: How do credit cards work?

How Do Credit Card Rewards Work?

Credit cards with the best rewards will give you a high percentage of cash back or points that you can use at places you make purchases. The following are the two main types of rewards:

Cash back: Cash back rewards pay down your balance. For example, if you’re getting five percent cash back on $5,000 worth of purchases, those purchases would technically cost $250 less.

Points and miles: Rather than cash back, some cards offer points or miles. You can use points to redeem gift cards and other merchandise. With travel cards, your earned miles give you discounted or free travel, depending on how much you have saved.

The rate of the rewards come in two different forms as well:

Flat rate: Cards that offer flat rate rewards give you the same percentage on all purchases. While this is more consistent, they’re lower than tiered rewards.

Tiered rewards: The most common rewards cards offer tiered rewards, which means you receive different rates based on where you use your card. For example, you may receive five percent cash back on groceries, travel and fuel but one percent for everything else.

Which type of reward structure you choose should be based on how you spend. If a card has tiered rewards with a high percentage cash back on purchases you make regularly, that type of card may be a better option. And if you travel a lot, you may benefit more from a travel card rather than a cash back rewards card.

Learn more: 5 ways to maximize credit card rewards without overspending

How Do You Track Credit Card Rewards?

The majority of credit cards have a separate account that stores your rewards, which you can access through your credit card’s website or mobile app. Depending on the card and card issuer, you may see your rewards instantly after purchases, or they may not appear until the following billing cycle.

Here’s how the reward process looks:

You make a purchase

Your rewards are calculated based on a flat rate or tiered rewards

Your rewards are credited to your account

You redeem your rewards through the card issuer’s website or mobile app

Learn more: Ways to redeem your credit card reward points

How Does APR Work?

APR stands for annual percentage rate, which is the interest you’ll pay on your purchases. Simply put, this is what the card issuer charges you for borrowing money through your line of credit. Depending on the credit card, the APR may be fixed or changed based on the current economic conditions.

Below, we’ve listed some more helpful information about interest:

Your interest rate is generally based on your credit score, and you’ll get approved for lower rates when you have a better credit score.

While interest is shown as an annual rate, you’re charged, daily. For example, a 20 percent APR divided by 365 days in the year means you pay roughly .055 percent per day.

Your monthly statement shows how much interest you’re being charged.

Interest is not compounded, so you’ll pay your full interest cost each month.

Learn more: Help! I really don’t understand my credit card APR

How Does the Credit Card Application Process Work?

In the early days, credit card applications were done on paper, but now, you mainly do them online. When you apply for a credit card, the card issuer is evaluating your level of risk and trustworthiness based on your credit score. A good credit score indicates that you’ll pay back the money you borrow from your line of credit.

Here’s what the application process looks like:

Step 1: Fill out the application. You’ll need some personal information like your name, address and Social Security number. The card issuer may request other items.

Step 2: The card issuer runs your credit, which will check your score as well as your actual credit report. The credit score is just a number, but the report gives additional details such as how many cards you recently applied for or any additional details they may need.

Step 3: You’ll receive an approval or denial. These days, many online applications approve or deny you within just a few minutes.

If you’re approved for the credit card, you’ll typically receive the card by mail within 10 business days. Once you receive it, you can activate it and begin spending.

Learn more: How to apply for a credit card online

How Many Credit Cards Should You Have?

How many credit cards you have is really dependent on your situation and your preferences. There’s no optimal number of credit cards. Rather than the number of credit cards you have, you should take into consideration your credit utilization as well as how often you’re applying for new cards.

For example, if you have 10 credit cards but have a 20 percent credit utilization ratio, you’re doing great. But if you have three cards with a 70 percent utilization ratio, that can hurt your score. If you were to have that high of a utilization ratio with 10 cards as well, that would hurt your score. If you apply for new cards too often, this can also harm your score.

Learn more: How many credit cards is too many?

Types of Credit Cards Explained

When choosing a credit card, it’s helpful to know the various types. Different cards are beneficial for different lifestyles, purchasing decisions and personal preferences. Below, we’ve listed some of the most common types along with a brief summary of what they do.

Rewards cards: These cards pay you back via cash that you can use to pay down your credit card debt or points that you can redeem at stores or in the form of airline miles. You earn rewards by using your card.

Balance transfer cards: All credit cards have interest that you need to pay, but some have lower rates than others. Balance transfer cards allow you to move debt and give you a year or more to pay it back with no interest. This often comes with a fee, but the fee is usually less than the interest.

Low and no interest cards: These cards are some of the most popular because interest payments make purchases cost more than the original price. For those who plan on carrying their balance over to the following month, these are the ideal cards.

College student cards: Young people are just starting out with credit building, so these cards get marketed towards college students and can help with the process. They’re easier to get approved for, but you’ll still need to meet qualifications beyond being a student to receive an approval.

Small business cards: Business owners and entrepreneurs often need to make purchases with credit, and these cards offer perks that are specifically geared towards business categories.

Cards for building credit: Whether you have no credit or bad credit, these cards can help you repair or build your credit score when you use them responsibly and make payments on time. They’re easier to receive an approval for, but they sometimes come with high interest rates or deposits.

How Credit Card Companies Work

In order to understand how credit card companies work, it’s helpful to know that they’re more than just companies. Each card company works within a network, and, sometimes, they’re partnered with another brand.

Credit card issuers: A credit card company is the card issuer. This can be a bank or financial institution that maintains your account. For example, Wells Fargo, Chase and Capital One are all card issuers.

The network: On every credit card, you’ll see names like Visa, Mastercard, American Express or Discover. These are basically the go-between companies that manage the transaction.

Co-brand partners: In some cases, cards have branded partners. An example would be an airline, hotel or store credit card.

Let’s look at an example using one of the top cards from our Travel category, the Citi Premier® Card. Citi Bank is the card issuer, using the Mastercard network and doesn’t have a co-brand partner. Then, there are cards like the Hilton Honors American Express Card, where American Express is the card issuer and the network, and Hilton Hotels is the co-brand partner.

Top Credit Card Companies

There are quite a few credit card companies out there, but which one is the best? J.D. Power does a regular study to see which one is the best.

Here are the rankings of the top 10 companies from the 2022 J.D Power U.S. Credit Card Satisfaction Study based on a 1,000-point scale:

American Express (848 points)

Discover (841 points)

Bank of America (818 points)

Segment Average (814 points)

Chase (813 points)

Capital One (812)

Citi (808)

Barclays (797)

Wells Fargo (797)

U.S. Bank (791)

Remember, what’s considered “the best” is subjective, so you may want to do additional research to see which company is right for you. Some may have benefits that suit your needs and spending habits, or you may find it better to get a card through your current bank.

How to Choose the Card That’s Right for You

There’s a lot to consider when choosing the right credit card, so we’ve listed some of the primary features of various cards to help you make the best for you. It’s also helpful to remember that by improving your credit score, you’ll have more options for which credit card companies will approve your application.

Annual Fees

Many cards come with no annual fee, but the ones that do often offer some additional perks and benefits. You’ll need to see if the fee makes sense based on what you’ll use the card for.

A great example is when it comes to travel credit cards. These may come with a fee, but you might save more than enough due to the rewards you gain in comparison to the annual fee.

Other Fees

Different cards come with different fees, and they’re not always advertised front and center when you’re applying for a credit card. You’ll often need to go looking on the application page for additional information to find out which fees you’ll pay as you use your card.

Some of the most common fees include:

Balance transfer fee: A fee for transferring debt from one card to another, which is often a percentage of the amount transferred.

Foreign transaction fee: When you’re out of the country, many cards charge up to 3% for using your card while traveling abroad.

Cash advance fee: Some credit cards allow you to use them like an ATM card for a cash advance, but these come with high interest rates as well as a fee.

Late fees: Credit cards usually have a grace period for making your payments, but these may also come with a late fee.

Learn more: How much does one late payment affect credit scores?

Introductory Rates

Credit card companies make money by charging interest, but many have promotional offers where you’ll receive low interest on purchases for a certain amount of time. Some are as low as 0% interest.

Regular Rates

Regular rates, also called “ongoing rates,” are the interest rates you pay once the introductory period is over. You can find this rate in the terms and conditions on the application, so you can use it to compare it to other cards.

Rewards

We’ve gone over the various types of rewards, such as flat-rate, tiered and points. This is where comparing cards gets specific to your lifestyle. If you travel a lot, a card with travel rewards may be right for you, but if you don’t, you may want to look at cards that give you cash back at places where you shop. You may also get a sign-up bonus with some credit cards that come as cash back rewards or points.

Perks

In addition to rewards, there are sometimes additional perks like cell phone insurance, identity theft security, rental car coverage and more.

How to Get a Credit Card in Six Steps

Now that you have all the knowledge you need to choose the right card, we’re going to put it all together in six simple steps:

Step 1: Check your credit score to know what types of cards you can apply for.

Step 2: Research various cards that sound like they might be the right ones for you

Step 3: Narrow down your options so you don’t apply for too many cards. Remember, each application may trigger a hard inquiry on your credit report, which can temporarily drop your credit score.

Step 4: Apply for the card through the card issuer’s website.

Step 5: Wait for a decision.

Step 6: If you’re approved, you should receive your card within 10 business days, and then you can start using the card for purchases once the card is activated.

FAQ

The following are some additional questions people have about finding the best credit cards.

What’s the Best Credit Card?

There’s no single best credit card. The card that’s the “best” will vary from person to person based on their needs, credit score and lifestyle.

What’s the Best Credit Card Company?

According to J.D. Power’s 2022 survey, American Express is the best credit card company. This is based on criteria like customer satisfaction based on a specific sample size, so some people may prefer a different card issuer.

When is it Time to Get a New Credit Card?

Here are a few reasons you may want to get a new credit card:

To increase your credit limit

To increase your credit utilization ratio

To accommodate a lifestyle change like traveling more often

Improve Your Odds of Getting the Best Card

To get the best credit cards and have endless options, improving your credit score should be your top priority. The best credit cards with the most rewards and best perks typically look for applicants with a score of 690 or higher—falling within the “good” to “excellent” range.

Credit.com has a wide range of services like our ExtraCredit program, which can help you learn more about credit and may lead to better credit health. If you’re unsure of your credit score, get your credit score for free here.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

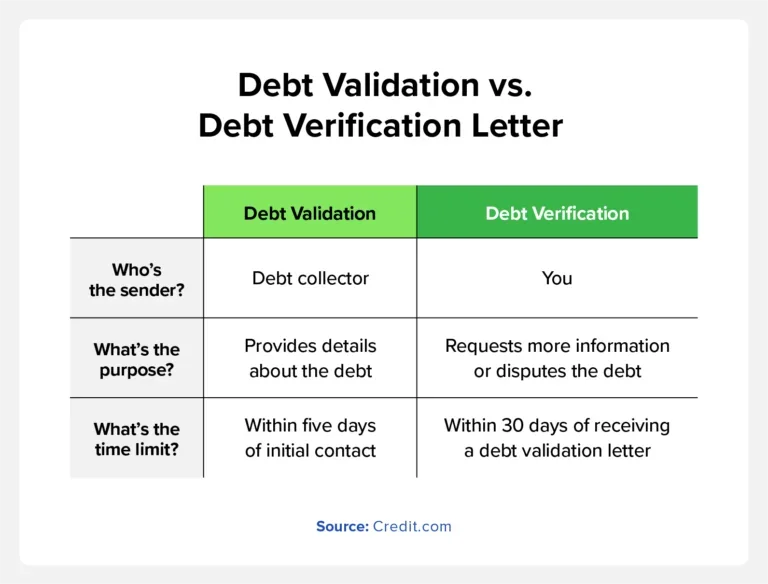

Debt collectors send debt validation letters show what debts you owe, the amount, and to whome you owe it to.

While a debt collector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Before paying the debt collector, verify that the debt is actually yours. The debt collection industry is subject to mishaps and mistakes, with some individuals being asked to pay debts they don’t owe.

That’s why you should receive a debt validation letter from the debt collector proving the debt is yours. If you still don’t recognize the debt, you can send a debt verification letter requesting more information or disputing the debt.

In this article, we’ll discuss the importance of debt validation letters and what information they should include. We’ll also provide a debt verification letter sample and a free template to help you get started.

Key takeaways:

Debt collectors are legally required to send you a debt validation letter within five days of initially contacting you.

A debt validation letter should include information about the debt, such as the amount you owe and the original creditor’s name.

If you’re unsure if the debt is accurate, send a debt verification letter to dispute the debt or ask for additional details.

Table of Contents:

What Is a Debt Validation Letter?

What Should a Debt Validation Letter Include?

When to Send a Debt Verification Request

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

Debt Verification Letter Template + Sample

How Long Does a Creditor Have to Respond to a Debt Verification Request?

What to Do If a Debt Collector Doesn’t Respond to a Debt Verification Request

What Is a Debt Validation Letter?

A debt validation letter is written correspondence that debt collectors are legally obligated to send you that provides information about the debt they’re collecting. The letter should include details about the debt, the original lender, and the debt collector’s authority to collect the money.

The creditor should send a debt validation within five days of their initial contact with you. If you don’t receive a debt validation letter, the debt collector could be an illegitimate person attempting to scam you. Therefore, you should avoid providing sensitive information to the debt collector until you’ve verified they’re legitimate.

What Should a Debt Validation Letter Include?

According to the Consumer Financial Protection Bureau (CFPB), the debt validation letter should include:

The amount of debt you owe

The name of the original lender requesting payment

The account details associated with the debt

An option to dispute the debt within a 30-day time period

An opportunity to request more details about the original lender

A statement acknowledging that the collector will provide verification if you dispute the debt

When to Send a Debt Verification Letter

If after receiving the debt validation letter and you’re still unsure of whether the debt is accurate, you can send a debt verification request to the debt collector. A debt verification request is a letter that you, as the consumer, can send to the debt collector to ask for information about the debt they’re collecting.

Typically, you have 30 days to send your debt verification request after receiving the debt validation letter. If you don’t send the letter within this time frame, the debt collector will assume the debt is valid and legally continue their efforts to collect.

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

It’s important to understand the difference between a debt verification letter and a debt validation letter:

A debt verification letter is a correspondence that you, the consumer, send to the debt collector requesting more information about the debt.

A debt validation letter is a document the debt collector sends to you, providing details about the debt.

Debt Verification Letter Template + Sample

When writing a debt verification letter, it’s important to be clear and concise. State that you’re disputing the debt and list what information you’re requesting from the debt collector.

Below is a debt verification letter sample and a template to help you get started. Remember to use your own information where there is bolded text.

[Name]

[Address]

[Today’s date]

[Name of the debt collector]

[Address of the debt collector]

Re: [Debt account number, if it was provided to you]

Dear [Name of the debt collector]:

I’m replying to your communication regarding a debt you’re attempting to collect. You reached out to me via [phone/mail] on [date] and provided the following account details:

[Account number, if provided]

[Name of the original creditor, if provided]

I am informing you that I dispute the debt you’re claiming I owe.

If you have reason to believe that I’m still responsible for this debt, kindly provide the following details to ensure I have all the necessary information:

The creditor’s name and address who is currently requesting payment

The original creditor’s name and address (if different from above)

The amount owed

The account number

Documentation that proves there is a legitimate reason you think I owe the debt, i.e., a copy of the original contract

The most recent billing statement the original creditor sent to me

An itemized list of any additional interest or fees

An itemized list of any payments since the most recent billing statement

If you’re providing this data to a credit bureau, please report that I’m disputing this debt.

Sincerely,

[Your name]

How Long Does a Creditor Have to Respond to a Debt Verification Request?