Equity Prime Mortgage (EPM), which shifted to the TPO business after exiting its retail channel in the fall, has embarked on a new chapter. EPM wants to help grow the industry’s wholesale channel through its newly launched broker recruiting website.

BLVR – a marketing and promotional campaign launched by EPM on Monday – aims to reach as many retail loan officers to provide information about the wholesale channel.

When retail loan originators visit the website, LOs are asked to fill out their names, contact information and comments or questions about wholesale lending.

A third-party call center agent of BLVR will reach out to the loan officer for a follow-up and potentially connect the LO with another broker to explore business options in the wholesale channel.

“They can continue the conversation [with another broker] to the point where they make the decision to stay in retail or move over to the light side of the force,” Phil Mancuso, president and chief investment officer of EPM, said in an interview with HousingWire.

“As folks come into the funnel, we just push it through a call center and out to the brokers (…) There are no strings attached. If EPM happens to get one of those loans down the line, great, even better. We believe that we will earn business if the pie is bigger.” Mancuso explained.

The goal is to bring more than 4,000 loan officers to the wholesale channel over the next 12 months, EPM said.

The BLVR website gives retail loan officers a glimpse of the opportunities in wholesale origination, Mancuso added.

With mortgage rates having sharply risen since 2022, loan officers who have already made the jump to wholesale say they have an advantage in being able to shop around for lower rates.

Not having to bake in overhead costs found in the retail channel is a key advantage, wholesale lenders say.

About 16.8% of first-lien mortgage originations last quarter came from the broker channel, correspondent lending took up 26.8% and retail consisted of 56.5% of total volume, according to data from Inside Mortgage Finance (IMF).

That’s a jump in the broker (13.9%) and correspondent (24.1%) channels while a drop in retail origination(62%) in Q2 2022.

“The broker portion of the industry is less than it was pre-financial crisis. Yet, brokers have never been more competitive. The offering had never been more compelling. We’re pretty adamant, as others are about the future of this segment of our business (wholesale lending),” Mancuso said.

Timing the market, as it relates to trading and investing, requires a whole lot of luck. In effect, it means waiting for ideal market conditions, and then making a move to try and capitalize on the best market outcome. But nobody can predict the future, and it’s a high-risk strategy.

When seeing stock market charts and business news headlines, it can be tempting to imagine striking it rich by timing investments perfectly. In reality, figuring out when to buy or sell stocks is extremely difficult. Both professional and at-home investors make serious mistakes when trying to time their market entrance or exit.

Why Timing the Stock Market Doesn’t Work

Waiting to start investing could cost an individual thousands of dollars over their lifetime. It’s also important to know that by leaving money in a checking or savings account, a person is not protecting their money from inflation risk. That’s because the value of that cash in a checking or savings account erodes if the prices of goods and services increase.

Meanwhile, stock market timing is incredibly complex. Stock prices can be influenced by global macroeconomic events, political events in a country, developments in specific industries or companies, as well as the sentiment of investors as a collective.

Even professional investors struggle to “beat the market,” which often means simplifying trying to outperform a benchmark stock index. In fact, most investors can’t beat the market, and are likely better off sticking to index investing.

Fear and Greed in Investing

When investing, it’s also important not to let two key emotions – fear and greed – drive decisions. That means if the stock market is plummeting, investors may be fearful, but they can’t let those feelings push them toward a decision to sell. That could cause them to “lock in” losses. There’s even a Fear and Greed Index that investors sometimes use to make contrarian decisions.

Take for instance what happened during the 2008 financial crisis. After Lehman Brothers Holdings Inc. filed for bankruptcy in September 2008, the stock market entered a tumultuous stretch. The S&P 500 finally bottomed on March 9, 2009. However, the index eventually regained all its losses in the course of roughly the next four years. Investors who had hung on likely may have recovered their losses.

Meanwhile, greed can cause investors to make poor decisions as well. For instance, during the dotcom bubble, investors bought into many newly public Internet companies without always doing the research. Some of these stocks weren’t even turning a profit, making their businesses vulnerable to going belly up. Ultimately, many at-home investors suffered losses when the dot-com bubble burst.

Of course there are no guarantees when it comes to investing. There’s always risk and volatility involved. However, one of the most tried and true methods for building wealth has been a buy-and-hold strategy when it comes to stock investing.

💡 Quick Tip: When people talk about investment risk, they mean the risk of losing money. Some investments are higher risk, some are lower. Be sure to bear this in mind when investing online.

Why It May Be a Good Idea to Invest Immediately

One of the most important predictors of your returns is the length of time you’ve invested in the stock market. While it’s difficult to predict what the market will do in the near future, an investor can get a better sense over the long term.

When an investor lets their money grow, it has the chance to weather short-term ups and downs and grow over time. On average, the S&P 500, often used as a market benchmark, has grown 7% a year after adjusting for inflation. That doesn’t mean a person can predict what will happen this year, or even in the next 10 years, but looking at long term trends can give them a better sense of market dynamics.

An individual might put off investing because they want to pay off all debts first or achieve other goals, like buying a house. In some cases, that might be true, like paying off high-interest credit cards or saving for a short-term goal, such as a three to six-month emergency fund.

But once a person has an emergency fund and is out of credit card debt, they should consider investing, even if they have a mortgage or student loan debt. Even if they’re only investing for retirement, it’s a good idea to start as soon as possible.

💡 Quick Tip: How to manage potential risk factors in a self-directed investment account? Doing your research and employing strategies like dollar-cost averaging and diversification may help mitigate financial risk when trading stocks.

Consider Investing as Early as Possible

The younger you are when you invest, the better the chances are that you’ll reach your financial goals. For example, imagine Person A invests $200 a month in a retirement account starting at age 25.

Person B invests the same amount starting at age 35. They both continue to add $200 a month to their account. When they both retire at age 65, Person A will have almost twice as much as Person B: $306,689, compared to $167,550, assuming a 6% rate of return, 2% inflation rate, and 15% tax rate.

That’s true even though Person A only contributed 33% more to her account. This is how compound interest grows investments, or the power of how earnings from one’s investments can continue to build wealth.

Percentage of Retail Investors in Stock Market

As mentioned, after the 2008 financial crisis, many people were reluctant to invest in the stock market. But in recent years, that’s changed. Retail investor participation in the U.S. stock market increased considerably in 2020 and 2021, for a variety of reasons.

As of 2023, retail inventors comprise about a quarter of all total trading volume in the stock market. That may change in the future, too, as younger investors – with quicker, easier access to investing tools, in many cases – look at getting into the markets.

The Takeaway

Timing the market is difficult, if not impossible, and involves trying to “time” trading or investing moves to coincide with an increase or decrease in the stock market. Nobody can tell what the future holds, so it’s generally hard to accurately pick the right investments at the right time. That’s not to say that some investors don’t get it right from time to time, but as an overall strategy, it’s likely not advisable.

If an individual is skittish about investing, their anxiety makes sense in light of the dramatic market ups and downs many have witnessed in the past two decades. But trying to time the market doesn’t work. Instead, investing in a diversified portfolio can be a good step toward building individual wealth.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

By waiting for mortgage rates to fall, buyers could risk losing out on their dream home.

Getty Images

As long as inflation is still persistent — and above the Federal Reserve’s 2% goal — interest rates will remain elevated. In fact, after months of cooling inflation actually ticked back up in July. And the benchmark interest rate now sits at a 22-year high.

Mortgage interest rates have also suffered in recent months. After hovering around record lows in 2020 and 2021, rates have risen exponentially and now currently sit around 7.5%. Rates on mortgages are the highest they’ve been in decades, leaving homebuyers with a series of poor options.

That said, even with rates as high as they currently are, there are some compelling reasons why buyers should act now and stop holding out for a better rate environment.

Start by exploring your mortgage rate eligibility here now.

4 reasons why you shouldn’t wait for mortgage rates to drop

Here are four reasons why buyers shouldn’t wait for mortgage rates to fall.

Rates could go higher

Sure, rates are high now, but what happens if they rise even further? Don’t dismiss the possibility of additional rate hikes. Federal Reserve chair Jerome Powell has already implied that additional rate increases could be coming in 2023. If that doesn’t happen this month, then don’t be surprised if it comes around the holidays.

That could be devastating news for those buyers who were planning on timing the market to improve their rate offer. While a 7.5% interest rate isn’t anyone’s idea of a great deal, it could prove to be a desirable one when compared to the prevailing rate in November, December or even January 2024. Just ask those who locked in a “high” 6% rate earlier this year.

Check rates and terms here now to learn more.

You may lose your dream home

Your dream home may only come on the market at one time, and it may not be during the most favorable rate environment. So don’t make perfect the enemy of the good and skip out on the chance to buy the home.

“Date the rate and marry the home,” most experts advise. In other words: The interest rate you secure now is temporary and can (and likely will) be adjusted in the future. But the dream home available now could be gone forever. Adjust your purchase plans accordingly.

You could refinance in the future

Mortgage rates and mortgage refinance rates are both elevated now. But they won’t be forever, at which point you could refinance to a lower rate and, potentially, even better terms.

So don’t feel like you’ll be saddled with a higher rate forever. While experts don’t agree on when rates will come down (and by how much), they all do agree that they will come down at some point — giving you an opportunity to take advantage and pay less.

The rate may not be as bad as it looks

Don’t get discouraged by the rate you find online. There are multiple ways you can secure something lower. This includes (but is not limited to) taking out an adjustable-rate mortgage (which comes with a lower introductory rate before changing over time) or purchasing mortgage points from the lender (to secure a permanently lower rate).

Neither option is ideal and both should be approached cautiously. But both options can save buyers money with a lower rate now. And that extra money could be very helpful to have in today’s economy.

Learn more about your mortgage options here now.

The bottom line

While mortgage rates are high today, buyers should be judicious about their approach. Waiting for them to drop back to pandemic-era lows may not be the wisest move. Instead, buyers should understand that rates could go even higher. And, if they wait for them to stabilize, they may lost the chance to buy their dream home. Plus, they could always refinance to a lower rate in the future — or get a lower one now by applying for an adjustable-rate mortgage or buying mortgage points from their lender.

The U.S. Department of Housing and Urban Development (HUD) on Thursday joined seven other federal agencies to clarify in writing that Title VI of the Civil Rights Act of 1964 prohibits forms of discrimination, including antisemitism, Islamophobia and other related forms.

To accomplish that goal, HUD published a housing-specific fact sheet about Title VI protections.

“In addition to shared ancestry and ethnic characteristics, religion is also a protected class under the Fair Housing Act, which HUD will continue to vigorously enforce,” the department said in a statement.

The administration unveiled its National Strategy to Counter Antisemitism in May, and HUD has remained a committed partner in its implementation across the federal government.

Reiterating Title VI protections and reminding people of their broader implications is key to accomplishing the administration’s equal housing goals, according to HUD Secretary Marcia Fudge.

“Antisemitism, Islamophobia, and any other form of hate have no place anywhere, including in the home,” Fudge said in a statement. “No one should be discriminated against because of their ancestry or ethnic characteristics or their faith or beliefs.”

She added: “[This] announcement will further the Biden-Harris Administration’s commitment to combating discrimination in all its forms and guide our partners on the ground to enforce this country’s legal protections for Americans against acts of hatred.”

Discrimination based on “shared ancestry or ethnic characteristics” is illegal under Title VI of the Civil Rights Act, and ensuring that fact is understood is key to the White House’s housing policies, according to Demetria McCain, HUD’s principal deputy assistant secretary for fair housing and equal opportunity.

“This announcement is in line with HUD’s continued commitment to combat housing discrimination in all forms,” McCain said. “It informs those who call America home of their right to be treated equally regardless of their shared ancestry or ethnic characteristics–putting us one step closer to building a housing system that prioritizes fairness and equality.”

In alignment with the Biden administration’s national strategy was a coordinated announcement from the other involved agencies, including the U.S. Departments of Agriculture, Health and Human Services, Homeland Security, Justice, Interior, Labor, Treasury and Transportation, according to White House announcement.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

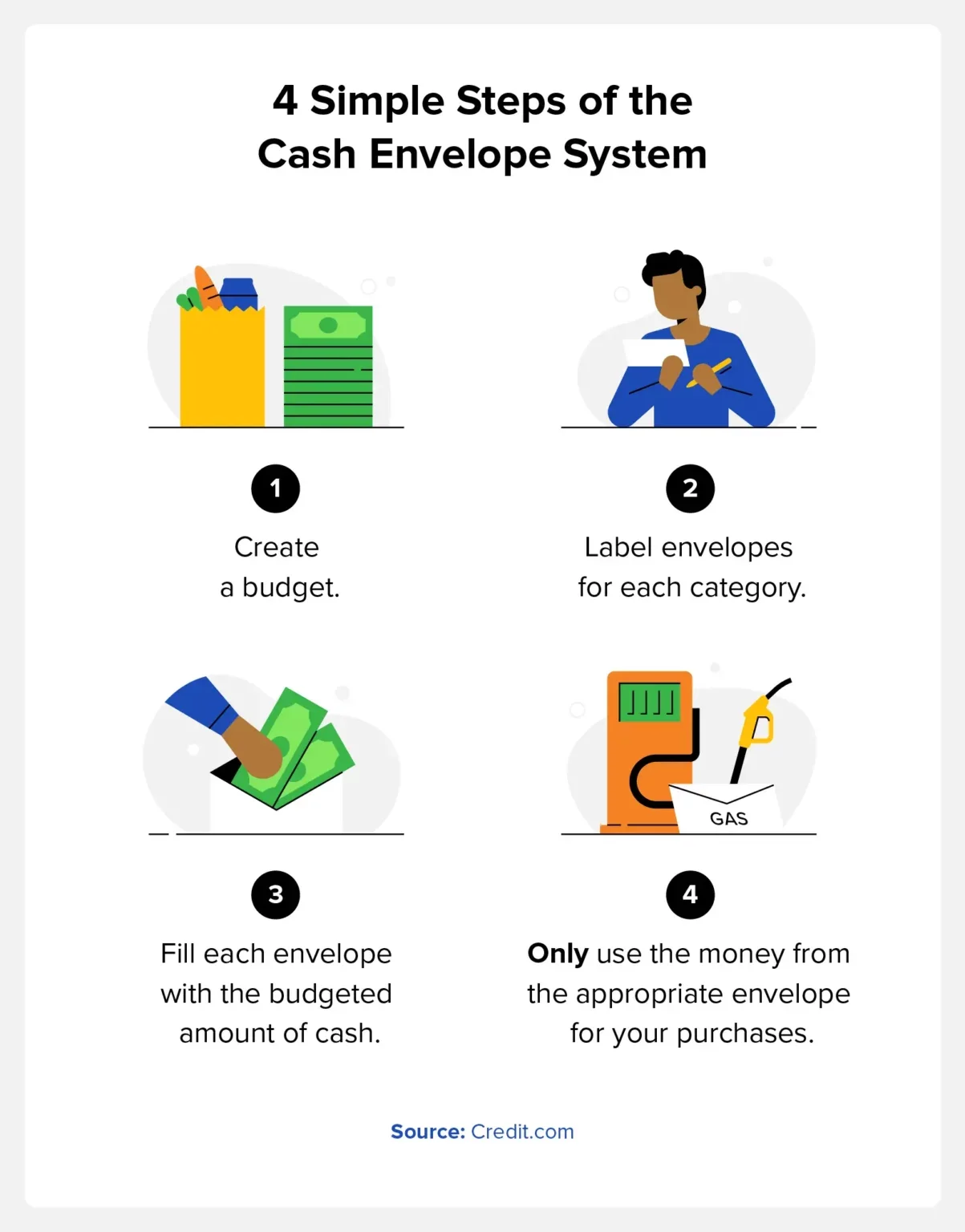

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

This article is part of a series put together by the Total Mortgage marketing team that provides loan officers and other sales professionals with a crash course in marketing and self-promotion. To read other articles in this series, click here.

This article is designed to teach loan officers and other sales professionals how to properly maintain and boost their social media presence. It will hit all the key points such as connecting, managing multiple profiles, engaging with influencers, and what to post.

Want to jump ahead?

LinkedIn

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Facebook

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Twitter

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencer

How and What to Post

Google +

Connecting & following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

LinkedIn

How to Gain/Find Connections

When you first started setting up your LinkedIn account, you were prompted to import your contacts from your email address book. If you clicked yes, you probably already have a few dozen connections. However, once your profile is completed, you will need to search for those connections you didn’t have on your contact list, like loan officers you met at a conference or realtors you haven’t had a chance to work with yet. There are many different ways to go about finding and linking with connections on LinkedIn.

The first way is arguably the easiest way: using the Search box. It can be found on the top of any tab of the LinkedIn interface. There are also many “Advanced Search” options available if you click the “Advanced” text link right next to the search button.

You could also find connections from clicking onto your Profile, scrolling down to your experience and hovering over your business place icon and then clicking onto the icon or your company title, highlighted by the red arrow.

After clicking on your company’s icon, scroll down until you see the “How You’re Connected” on the right side of the screen. Click “See all.”

Now you have the opportunity to see coworkers and contacts who you’re not connected to.

Managing Multiple Profiles

LinkedIn is generally a place where you focus on one personal profile. However, if you run your own business, you will want to create a company page for it. If you need help creating a company page, check out my Social Media Basics post. If you only manage one page, then this section may not be that useful.

If you are on your profile page and you want to switch to your company page, you simply click on the small icon on the top right hand corner of your screen (where the arrow is shown) then on “Company Page.”

This will lead you to this screen.

You’ll now be able manage, change, analyze, and update your company page. If you want to switch back to your profile page, just click on the home tab or profile tab.

Engaging with Influencers

Connecting with influencers—that is, the people who are active, established, and popular in your industry—is a great way to widen your reach. Of course, engaging with influencers on LinkedIn is not something you should do blindly. It takes strategy and time to do correctly.

Do Not:

Do not connect with an influencer without ever interacting with them

Do not like, comment, or share everything they post

Do not post more than 3 times per day

Do:

Do connect if you had previous relations

Do connect if you are connected on other networks

Do connect if you have exchanged emails or contact info

How and What to Post on LinkedIn

Posting on LinkedIn is very straight forward. LinkedIn allows you to share updates, publish a post, upload a photo, share in groups, and post job opportunities. You can access these options in the home tab, except for sharing in groups and posting job opportunities.

Sharing in a Group

Sharing in a group could be a great way to get your content to a broader audience. Joining groups on LinkedIn is very easy. First, click on the “Interests” tab and then click on “Groups” If you are already a member of a group it will appear under the “My Groups” section. If you aren’t a member of any groups, just click on the “Discover” tab and LinkedIn will provide recommendations for groups to join. You have the option to select “not interested,” “ask to join,” or you can ignore and continue to scroll.

Once you ask to join a group, your request must get approved by an admin, which can take a day or two depending on how busy they are. After you’re accepted, you can view what the others in the group are posting. To get started, click on “Start a conversation with your group.” The box will expand and you get the options listed below. At this screen, type in your title and a brief description with a link to the real content. Follow the same process for posting a job opportunity in a group.

If you run a LinkedIn business page, then you have the option of posting a job ad through the “Business Services” tab. Once you hover over “Business Services,” click on “Post a Job” to get to this screen.

After you fill out the appropriate information and click “Start job post,” LinkedIn will walk you through a series of prompts, where you will fill out information like job function, company industry, and job description. Once that’s done, review everything and click submit.

What to Post:

Career status updates

News and events

Articles shared by your connections

Your own articles

What not to Post:

Quotes

Updates trying to sell services/items

Material you deem not appropriate for the workplace

Facebook:

How to Gain Followers:

With more than 1.65 billion monthly active users, Facebook has the potential to connect you to people across the globe. If you’re using Facebook for business purposes, you need to understand how to properly navigate it to connect with others.

There are multiple strategies to take. For example, you can create a personal account, a business page, or both. If you’re in an industry where you need to keep things professional (like, for instance, the mortgage and financial industry), then I recommend creating a business page so you can separate your professional life from your personal life. You have to mindful of whom you invite to like your page, but we’ll touch on that topic a little later.

If you’re completely new to Facebook, prepare to spend some time connecting with people you know. You can manually add friends by clicking in the search box at the top of the screen and typing the name of the person you are trying to find. Eventually Facebook will tailor a carousel of “People You May Know,” which will allow you to click “Add Friend.” Thankfully, Facebook has implemented a few tricks to make it easier to add friends in bulk.

Go to the Friends Request page then to the “Add Personal Contacts,” enter your email and click find friends.

After you enter your email it will take you through to a similar screen. Click “Agree,” then follow the on-screen instructions.

On the Go

You can also import contacts from your mobile device.

Tap

Hit “Find Friends” in the Apps section

Tap “Contacts,” then follow the on-screen instructions

Connecting to Others Via Your Business Page

Click on the triangle in the top right corner of your home page.

Click on the drop down menu and select your business page.

Click on the […] on your cover photo and then click on “Invite Friends.”

Search all friends: click the invite box next to your friends’ names to invite them to like your page—or type their names in the search box.

Managing Multiple Profiles

Facebook does a fantastic job of making it easy to manage as many pages as you want. Their interface organizes your pages so you can easily switch through and manage every single of one of them. Every time you create a new page, Facebook allows you to add that page into your “Favorites” section. I highly recommend doing this, because it keeps all of your pages in easy reach, which you can see in the image below.

You can also switch between pages by clicking the drop-down triangle on the upper right corner of your home page. In that menu, you’ll find a list of three of your pages. Shown below:

If you manage more than 3 pages—like we do here at Total Mortgage—you can just click on “See More…” and it will give you a list of all the Facebook pages that you manage. To switch back to your personal page, you simply just need to hit the “Home” button and it will take you back to your feed.

Properly Engaging with Influencers

Recently, Facebook has changed how you interact with other people or businesses when you’re on your business page. Once, you were able to be on your business profile, click on “Home” and interact with people and businesses that follow your business page. However, that is essentially nonexistent today. Now you really need to be creative if you want to engage with influencers in your community.

To Like a Different Page as Your Business Profile

Go to the page you want to like and click on the […]

Click “Like As Your Page.” Then this screen will pop up and you choose the business account that you want your like to come from. Click “Save.”

Tagging other influencers in your Facebook posts is simple if you know the name of their business page. A lot of influencers have both personal and professional profiles, however, so make sure you know which one you’d like to connect with.

Unfortunately, you can’t tag a personal account from your business profile. If you want to tag a professional account from your business page, you craft your post, then add the appropriate tag at the end. You always want to convey that you got the content from a source and you are using it credibly.

In the picture below, you see that I have crafted a draft of my message and tagged the source I got it from with the tag “via @[name].” Instead of via you could use from, by, thanks to, etc. When possible, try to use a link shortener such as Buffer or Hootsuite to keep things looking tidy.

Once you get the proper etiquette down for interacting with influencers, now it’s time to engage with them. Like I mentioned above, you can like other pages as your page. You are able to do the same for posts. You do that by going to the page you want to like something on and scrolling to the post that you want to interact with. Before you like the post or comment, make sure you switch from your profile to your business profile. You do this by:

1. Clicking on the downwards arrow next to your small Facebook default icon

2. Click on the account you want to like and comment as.

You are now liking and commenting as your business account. This is the best way you can engage with your influencers. There are 3 important things you must always remember to do and don’t do before you start engaging with influencers.

Do Not:

Do not like/comment on everything that they post

Do not ask for a favor like sharing a post right away

Do not reach out to them right away

Do:

Gradually interact with them by liking their page and commenting on a few posts/pictures 1-3 times a week

Share some of their posts 1-2 times a week

Always remember to thank them for sharing information that you find important

Here’s where you use your gut. Once you think you’ve earned yourself a spot on the influencer’s radar, the next step is to reach out personally. This can be done in an open forum through commenting, or it can be done through private message. The eventual goal is to take the conversation “offline” through either phone or email so you can begin building an even more personal relationship.

How and What to Post on Facebook

Posting and sharing on Facebook is very easy. If you have a personal Facebook, you already know the drill. If this is your first time on Facebook or you don’t know how to post to your business page, then keep reading.

Posting on Your Personal Page

Bring your mouse to the top tab and click on your name

Click on the box where it says:

3. Click on the kind of post you want to craft: status, photo/video, or life event. Finish typing it with the appropriate tags (if needed) and click post.

Posting on your Business Page

Make your way over to your business page

Click on the box where it says “status, photo/video, or life event” and create the post you want to send out

When you are finished, click “Publish”

What to Post on Facebook

There are two types of content that you should post on Facebook. The difference depends on what account you plan to post with. For both profiles, you should post content that really resonates with your audience and makes people see you as a credible source (i.e. if you’re a loan officer, try content based around changes in the industry or tips on how to make the mortgage process easier).

Content like this positions you as an authority and encourages your audience to consider using your services if they are shopping for a home or refinancing. Every once in a while, it’s okay to throw in a shameless plug, whether you’re asking for referrals or encouraging people to use your services. Your personal page can have all the other updates—photos of your family, your dog, things you’re passionate about, etc. It is ok to post some business topics on your personal page, but make sure to do so sparingly. Your personal page is meant for personal things.

Twitter:

How to Gain Followers

Twitter is a great place to gain followers based on things that you find interesting. You can use the search box to find other professionals and people in your industry by looking for relevant hashtags, like #realestate.

Top Tips for Gaining Followers

Try finding your connections from other places like Facebook and LinkedIn on Twitter

Follow users who follow your followers

Follow the accounts recommended by Twitter

Join a Twitter chat

Managing Multiple Profiles

Unfortunately, Twitter doesn’t have an interface within itself to switch profiles easily—unless you are on your mobile device or want to use multiple web browsers. However, there are certain tricks, tips and hacks you can use to make managing multiple profiles easier.

Toggling Profiles in the Twitter App for iOS

From the “Me“ tab, tap the people icon

Tap “More options.”

From here you can “Create new account” or “Add an existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the people icon.

Toggling Profiles in the Twitter App for Android:

Tap the overflow icon

Tap “Accounts.”

From here you can “Create new account” or “Add existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the overflow icon, then tapping “Accounts.”

If you’re uninterested in downloading the Twitter app for your mobile device, there are other options. If you manage more than one profile you can easily manage multiple accounts if you use a tool like Tweetdeck, Buffer, or Hootsuite. All of these applications have free versions, so you don’t have to worry about spending money.

These apps make it easy to manage countless amounts of accounts. My personal favorite of the three is Buffer, because the interface is very easy to use and it provides multiple tabs to check out how your account is doing in terms of analytics. It also has a built-in link shortener that automatically shrinks your links when you are adding them to a post. Shown below is a screenshot of my Buffer interface.

Engaging with Influencers

Engaging with influencers on Twitter is a great way to kick-start your influencer marketing strategy. This is where Twitter search comes in handy; you can use it to find the people who tweet regularly in your industry regularly. If you want to stay organized, I recommend creating a spreadsheet that has a list of your influencers, their names, follower count, and what stage of your relationship you’re in. Once you’ve found a handful of them, it’s time to start engaging.

Do not:

Tweet, retweet, or like everything that they tweet

Try to directly reach out to them—it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally tweet, retweet, or like their posts to get on their radar

Appreciate their content by tweeting it out to your audience (and making sure your attribute the author)

Once you established a relationship, make it easy for them to tweet about your service by crafting an email with a few sample tweets that they could send out about your services. Make sure you convey the message that you are willing to reciprocate the favor

How and What to Post:

Posting on Twitter is very simple. If you are on the web browser version of Twitter the tweet box is one of the first things that you see. You can find it by looking for the “What’s happening?” text.

To compose a tweet you just click on this box and type the content you want to share.

Posting a Tweet on a Mobile Device

Tap the compose Tweet icon accessible from your Home timeline, the Notifications tab, or your profile (usually located on the upper right hand of your screen.)

Start typing where it says “What’s happening?”

If you’d like to Tweet an image, tap the camera icon

Tap “Tweet” to post.

What to Post

Just like any other platform, choosing what to post comes down to a few key factors.

Who your audience is

What kind of message are you trying to portray

What kind of content will resonate with that audience

Make sure you don’t forget to utilize the power of hashtags on Twitter. To see how a hashtag is performing simply search the hashtag in the search box before you post the tweet or check it out on Tagboard.

You want to have the appropriate amount of hashtags to text ratio. Most marketers recommend using no more than 3 hashtags per tweet. However, if your tweet only contains 3 words, don’t hashtag them all. Finding the perfect mix of creativity and content is surely a challenge but once you find your niche you will be good to go.

Google Plus

Google+ is one of the most underrated social media platforms, but it could be a great asset to your strategy if used properly.

How to Gain Followers

Make Your Profile Look Good

I know, it sounds obvious, but a lot of people just use the default graphics that Google supplies. Make sure your profile looks good and is customized so you reach people in your niche.

Follow other Google Plus People

Just like other social platforms, you’ll need to work for your followers. You do this by following as many people as possible. There are multiple ways of doing this. If you are looking for people to connect with , search for something relevant to your industry like, for example, “Real Estate.” A list like below will pop up and you will be able to decide who what you want to follow, whether it be collections, communities, people & pages, or if you just want to view posts.

You can also follow people manually:

Click the People Icon on the left side of the screen

You should see a “Find People” option. Click on that

Go through the list of people and see who you want to add

You can add them to just your follower base or you can add them to relevant circles, such as “Realtors”

Join Communities

If you’re looking for the fast track way of getting your name in front of dozens, even hundreds of people at once, then you’re looking for communities. When you join a community, you are part of a much larger group of people who are interested in a certain topic. This is how you engage the right kind of followers.

Utilize Hashtags

With Google Plus know you can search content by words, phrases, and hashtags. Even though hashtags are more popular on Twitter, they work the same way on Google+.

Let’s say you hashtag a word or phrase in your post, i.e. #RealEstate. Thanks to that hashtag, your post enters a stream with hundreds of other posts with that same hashtag. Meaning, anyone watching that stream or looking for specific information centered on that topic will easily find your post.

Add a Google+ Badge to Your Website

If you have your own website, it’s a sin in 2016 to not have visible social widgets. These are clickable icons that take you right to your social media pages. They take the hassle out of finding your social pages, making it easier to gain followers.

Managing Multiple Profiles

Managing multiple profiles on Google+ is very simple if you add all your accounts to one email address. Once you associate all your different profiles to that one email address it becomes very easy to switch back and forth between the different profiles from the Google+ interface. Don’t forget—you can always use a social media management tool like Buffer to switch profiles simultaneously.

Switching Profiles:

Click the icon on the upper right hand corner (Note: Your icon will be different from ours)

Once you click on that icon it will release a drop down menu of all the other profiles you have connected to your account

Now you are free to switch through whichever profile you deem necessary

Properly Engaging with Influencers

Engaging with influencers is a lot like engaging with influencers on any other platform—you need a strategy and you need to find the right influencers.

Do not:

Plus one (+1) everything they share

Try to directly reach out to them–it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally +1, comment, and share their posts

Appreciate their content by sharing it in your communities

Share some of their posts 1-2 times a week

Thank them for sharing information that you find important

How and What to Post

Posting on Google+ seems a lot more complicated than it really is. Just keep in mind that you can post publicly, in a community, or in a group. To post you simply go to the page, community or group you want to post to.

Click on the pencil icon on the bottom right hand corner

Which will bring you to this screen

Here you type in the text of the message you want to draft in the ‘What’s new with you?’ section. If you are adding a link, click on the. If you want to add a picture (recommended) click on the camera icon. You can also add your location by clicking on the location pin.

What to Post

Just like any other network, you need to find your niche before posting blindly. Finding content that really resonates with your audience is half the battle. Like I said previously, try testing a few types of content to see what works best.

Don’t be afraid to use content with a lot of pictures like infographics. The more pictures the better. A very good post is a combination of clever content, great pictures and captive CTA’s (call to actions.) Once you find this balance roll with it and optimize your Google+ account to its full potential.

Thinking About Your Next Steps?

All of these social media platforms are great for connecting and getting your content out there. Each platform is a little different from the next, so don’t try to implement the same strategy throughout all of them. Finding your groove might take some time, but keep working towards it and tweaking your strategy to see what gives you the best results. Once you hit that sweet spot, roll with it.

You can learn more about what the Total Mortgage marketing team does for our loan officers by checking out other articles in this series, or by visiting our career portal.

Carter Wessman

Carter Wessman is originally from the charming town of Norfolk, Massachusetts. When he isn’t busy writing about mortgage related topics, you can find him playing table tennis, or jamming on his bass guitar.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!

Though FICO® and VantageScore® ranges start at 300, most new credit users don’t start this low. In fact, if you’ve never taken out credit or applied for a loan, you might not have a credit score at all.

When applying for credit cards and loans, you begin to build credit, but you may be wondering—what does your credit score start at? Most people’s initial credit scores are between 500 and 700 points, depending on the steps taken when establishing credit. However, you won’t have a credit score to report if you’ve never opened a credit account.

Read on to learn more about your starting credit score and how to build your credit over time.

What Credit Score Does an 18-year-old Start with?

Contrary to popular belief, you don’t automatically receive a credit score the day you turn 18 years old. However, you need to be at least 18 years of age to apply for credit and start building your score. Remember that if you haven’t used credit yet, you likely won’t have a score at all.

Once you start using credit, you will get a score roughly three to six months after opening your first credit account. Your credit score will be calculated based on a variety of factors outlined in the next section.

How Are Credit Scores Calculated?

So, how are credit scores determined if everyone doesn’t receive the same default credit score? According to FICO, they use the following five factors to calculate your credit score:

Payment history: The most important factor to determine your credit score is your history of paying credit accounts on time.

Accounts owed: While owing money on credit accounts isn’t necessarily bad, using a majority of your available credit can lead to lenders viewing you as higher-risk.

Length of credit history: Generally, the longer your credit history, the better it is for your score since lenders have a more accurate assessment of your risk.

Credit mix: The different types of credit you have, such as credit cards, installment loans, and finance company accounts, are your credit mix.

New credit: Opening too many credit cards in a short period of time can hurt your score since doing so signals to lenders that you’re a greater risk.

How to build credit

If you’re new to credit, you may be wondering how to start building your credit in the first place. Receiving a loan without a credit score might be difficult, so FICO suggests the following ways to start building credit:

Become an authorized user on a family member’s credit card. You can be added to a card owner’s account, which allows you to make purchases with their credit card. Keep in mind that this method doesn’t have a large effect on your score but can be a good stepping stone to building credit.

Apply for a secured credit card. As a person with no credit, your risk to lenders is considered very high. A secured credit card requires you to pay a refundable security deposit to mitigate risk.

Report rent and other service providers. Credit and loans aren’t the only factors that affect credit. While landlords and utility companies typically don’t report to the credit bureaus, you can request that they do so to start building your credit.

How long does it take to build a 700 credit score?

According to FICO, a credit score of 700 or above is considered good. And since the national average credit score is 716 as of April 2022, it certainly is achievable, although it will take time. If you’re starting with no credit, you can expect building a 700 credit score to take at least six months of practicing positive credit habits.

Keep in mind that there are steps you can take to increase your initial credit score and reach your credit score goal of 700 or higher credit.

How to improve your initial credit score

So, how can you help make sure that you start out with a good credit score? Follow the tips below to improve your credit score.

Review your credit report. Once you open a credit account, be sure to view your credit report and look for any inaccuracies.

Be on time with your payments. Since payment history is the most important factor that influences your credit score, be sure to pay your bill on time and avoid missing payments.

Limit applying for multiple lines of credit in a short period of time. Applying for credit results in a hard inquiry, which may slightly lower your credit score. Too many of these hard inquiries in a short period of time can cause your credit score to drop.

Keep your credit utilization ratio under 30 percent. Credit utilization refers to the amount of credit you’re using divided by the amount that is available to you. For example, if your monthly credit limit is $1,500, aim to use under $450 each month.

Be patient. Again, the length of credit history is an important factor that contributes to your credit score. The more time that passes since you opened your account, the better for your score.

FAQs

Below, we’ve answered some common questions regarding your first-time credit score.

Does your credit score start at 0?

Your credit score doesn’t start at zero. In fact, the lowest credit score possible is 300. However, you likely won’t start at this score unless you’ve made actions that have damaged your credit score.

Does everyone start with the same credit score?

Everybody doesn’t start with the same credit score. As mentioned above, your individual credit score is based on a number of factors.

Is no credit worse than bad credit?

No credit means you lack a credit history, whereas bad credit means you’ve made credit-damaging mistakes, such as multiple late payments. While both scenarios can cause limitations, building credit from scratch is generally easier than rebuilding a bad credit score. As a result, it’s worse to have bad credit than no credit.

What’s a good credit score for young adults?

A good credit score is 670 and up. According to Experian®, the average credit score for young adults ages 18-25 is 679, so any score above that is considered above average for the age group.

How to check your credit score for free

Once you begin building credit, it’s crucial to follow responsible financial practices that will help you raise your credit score over time. And don’t forget to regularly monitor your credit to make sure you’re on the right track.

ExtraCredit by Credit.com gives you tools to manage your credit at an affordable monthly price so you have information you need to help you achieve your financial goals. Get started today.

Figuring out how to double your money with investments often hinges on striking the right balance between risk and reward. Your personal risk tolerance and goals can influence how you invest and the returns your portfolio generates.

However, doubling your money is a reasonable goal, especially if you’re willing to wait for your money to grow. And that’s a big variable to keep in mind: Time. If you’re interested in doubling your money and growing wealth for the long-term, there are several investing strategies to consider.

Investing Strategies to Double Your Money

1. Get to Know the Rule of 72

The rule of 72 can be a helpful guideline for answering this question: How long to double your money?