The high cost of housing is driving Southern California’s biggest challenges. Income is not keeping pace with housing costs. It hasn’t for at least two generations, and the problem of unaffordable shelter shows few signs of letting up.

There’s a metric called “housing burden” that lays the situation bare. Over the last 50 years, it tracks the growing, gaping mismatch between income and shelter costs in Los Angeles County.

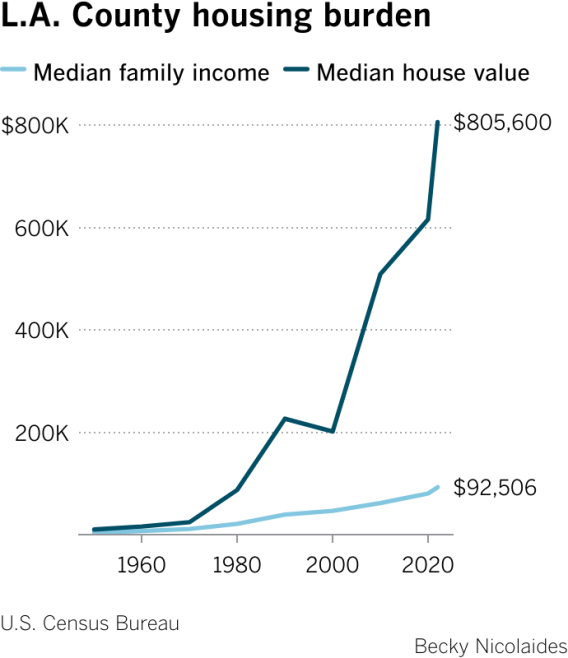

In 1979, UCLA land experts Leo Grebler and Frank Mittelbach wrote: “As a general, time-honored rule of thumb” house prices in a community “should not exceed 2 to 2½ times the annual income” of its residents.

Within a decade, home prices began to drastically violate this rule. If it were applied today, it would mean a four-person household with the median Los Angeles County income of $98,200 could afford to buy a house that cost $245,500. However, the median home price in the county last month, according to Redfin, was $980,000.

Advertisement

How did things get so unbalanced?

In the 1950s and 1960s, buying a single-family home in Los Angeles was an attainable prospect. The GI Bill and the Federal Housing Authority helped with loans and mortgage dollars (albeit primarily for white families). And home building was on a tear, thanks to the region’s pro-development political climate.

By the 1970s, however, a cascade of factors — local to global — changed the equation.

Housing prices first shot ahead of income in the mid-1970s. Analysts attributed the spike to the first cohort of baby boomers reaching home-buying age, which expanded the pool of buyers and created a seller’s market. The 1973 oil crisis and ensuing inflation pushed buyers to pay up for fear prices would rise even higher. Unrelenting demand thus not only kept pace with prices, it increased them.

Social-demographic factors also factored in. Per capita income doubled from 1966 to 1977, due in part to more women in the workplace. When federal policies struck down gender discrimination in loan and credit decisions, two-income families could qualify for larger mortgage loans, elevating the demand for higher-priced homes.

Advertisement

Then land and building costs climbed, pushing prices even higher. And in 1978, Proposition 13 became law.

The ballot measure slashed property taxes and with them, funding for municipal services. Cities and towns scrambled to recoup the lost revenue. New real estate developments were “money-losers,” as urban planner and former Ventura Mayor William Fulton observed, because property taxes fell so low. Instead, municipalities turned to retail development to generate lucrative sales tax revenue. Prop. 13 thus became a powerful disincentive to build housing.

The rising slow-growth movement put another damper on housing supply. It was pushed by homeowners who resisted adding multifamily housing in single-family neighborhoods or new development in nearby open space.

One study by the California Legislative Analyst’s Office found that by the early 2000s, more than two-thirds of cities and counties in coastal California metro areas had slow-growth policies in place, and that when a community added such a policy, it resulted in a 3% to 5% increase in home prices. Moreover, the historical momentum of R-1 (single family) zoning stymied the construction of multifamily units.

The upshot of all these pressures? From 1980 to 2010 in Los Angeles, the population grew by 31.3% while housing units grew by only 20.6%.

L.A.’s spiraling housing costs paralleled trends in large, global metro regions by the turn of the 21st century, suggesting that forces beyond L.A. were also at work. In the 1990s and early 2000s, the housing bubble was driven by finance structures linked to global markets, inflows of global capital and unregulated banking practices that set off unrestrained and predatory lending and buying frenzies. Even after the 2007-09 banking crisis and Great Recession, home prices in L.A. soon regained traction.

Taking a longer view, economist Robert Shiller traced rising housing costs in the late 1980s and early 2000s across metro areas globally, including L.A. He pinned a good deal of the blame on “irrational exuberance” that motivated uncontrolled buying. The psychological draw of metro areas such as Paris, London, Sydney and L.A. reinforced the belief that land prices would continue to go up and up. Media fed these perceptions. And housing bubbles blew up.

Looking at the housing burden graph, the price surge since 2020 is truly eye-popping. Urban analyst Richard Florida attributes it to pandemic-driven demands for more housing space especially among millennials, a massive shortage of housing overall and, perhaps most disturbingly, the growing competition from large institutional investors who’ve been snapping up homes and apartments in recent years. In 2021, they bought 29% of all single-family homes in California and, with their ability to outbid other buyers, they drive up prices.

Over the last 50 years, L.A.’s housing burden has evolved from challenging to simply unsustainable. The consequences are all around us, in skyrocketing rents, a ubiquitous homelessness crisis, housing overcrowding, rising commuting times to drive-till-you-qualify exurbs, population flows out of California and intensified wealth inequality.

Solutions must come from both the housing and the income side.

Increasing the housing supply is crucial. It must be accompanied by policies that protect individual buyers from corporate competitors, ensure the ongoing production of affordable housing, and guard against gentrification.

Even more importantly, wages and salaries must climb considerably to make housing affordable again. The major employers in our region — from the movie studios to hotels to hospitals and logistics firms — must take a long, hard look at the housing burden graph and see in it their own role in widening the gap. The Writers Guild and actors’ strikes, the Unite Here Local 11 hospitality industry strike and the strike vote last week by Kaiser Permanente healthcare workers speak directly to L.A.’s housing burden.

The struggle to match income to cost of shelter is an inescapable fact of L.A. life that demands swift, conscientious redress.

Becky Nicolaides is a research affiliate at the Huntington-USC Institute on California and the West, and author of “The New Suburbia: How Diversity Remade Suburban Life in Los Angeles After 1945,” forthcoming from Oxford University Press. The data set collected for the book, a granular look at demographics from 1950 to 2010, will be published online by the USC libraries next year.

With the holiday shopping season just starting and prices of many consumer goods continuing to rise, saving money can seem impossible. But those financial pressures also make doing so even more important.

“Saving is your margin,” says Eric Maldonado, a certified financial planner and owner of Aquila Wealth Advisors. “When things happen — your car breaks down or there’s a layoff, or smaller stuff like gifts for the holidays — you have something to fall back on.” Maldonado notes that saving can also allow you to have money for fun things.

The personal savings rate for Americans has been dropping in the last few months, and as of July was 3.5%, according to the U.S. Bureau of Economic Analysis.

Maldonado recommends aiming for a savings rate closer to 20% of your take-home income. “You can live off of 80% and put 20% toward deferred gratification,” he suggests.

That guidance matches the popular 50/30/20 budget, which suggests putting 50% of your take-home income toward needs, 30% toward wants, and 20% toward savings and any debt payments. “If you’re just starting out, then it can be too daunting, but you can work toward it,” Maldonado adds.

If you’re looking for ways to power up your savings, consider these strategies:

Pause before buying

“One of the biggest mistakes people make is buying things you don’t need,” says Vivian Tu, author of the forthcoming book “Rich AF: The Winning Money Mindset That Will Change Your Life” and a TikTok influencer who posts as @YourRichBFF. To counter that tendency, she recommends “taking a beat” before making any purchase. “Really ask yourself, ‘Why do I want that thing? What makes it special?’” she suggests.

Tu says asking herself that question helped her scale back on material purchases so she had more money for experiences, like vacations and brunches with friends.

Spread out the impact of big expenses

For big expenses that are on the horizon, Cary Carbonaro, a CFP and senior vice president at financial advisory firm ACM Wealth, recommends setting aside a small amount of money each month so the final cost doesn’t overwhelm your budget.

“If you know you’re going to spend $1,200 at Christmas, then put aside $100 a month for the whole year,” Carbonaro suggests. “Everybody overspends in December unless you budgeted for it.”

Try curbside pickup

When Ryan Greiser, a CFP and founder of the financial firm Opulus, and his wife noticed their credit card bill going up with inflation, they brainstormed ways to cut back. One of their most successful ideas was relying on online grocery ordering with curbside pickup.

“We noticed that if we did curbside pickup, our bill was $50 to $100 less than if we went into the store because we only bought the things on our list. It reduced impulse buys and allowed us to easily compare prices and coupons that popped up on the screen,” Greiser says. Given their weekly shopping needs for a family with three young children, that shift allowed them to save $200 to $400 a month.

Rotate subscriptions

Greiser and his family also started saving $10 to $30 a month by rotating their streaming subscriptions based on what shows they were currently watching. “We keep one or two active subscriptions and cancel the rest or pause it when a show wraps up so we can rotate to the next one,” he says, adding that he sets a reminder on his calendar so he doesn’t forget to cancel.

Similarly, he pauses his fitness subscriptions when the weather is good enough to exercise outside. “They are month to month, so easy to pause and restart,” he says.

Ask for discounts

Speaking up for yourself is another saving strategy. “You have power as a consumer,” Tu says.

That means you can ask your bank to waive late fees or overcharge fees, or ask for a discount on shoes that have a scuff on them. “Be polite, be kind, but you can be entitled and understand that your business has value,” she adds. The answer might be “no,” but there’s no reason not to ask, and it might just save you some money.

Shop around for insurance

Find discounts on the bills you don’t look at very often, too. Instead of letting your home and auto insurance auto-renew each month, consider taking time to shop around through an online comparison tool. When Greiser did that, he ended up saving a total of $1,000 on his bundled auto and home insurance plan.

Sign up for cash-back apps

Popular cash-back apps like Rakuten, Ibotta and RetailMeNot allow you to earn cash back for online shopping after you set up an account. “I highly recommend using cash-back apps,” Tu says. “I know it seems like kind of a pain to sign up, but you can save hundreds of dollars a year because it lets you get cash back on purchases you were already making.”

Sometimes making the extra effort pays off, right into your savings account.

This article was written by NerdWallet and was originally published by The Associated Press.

Are you looking for the best side jobs for teachers? Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher. Side hustles for…

Are you looking for the best side jobs for teachers?

Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher.

Side hustles for teachers are great because they can help you make extra income, pay off debt, save for a vacation, and more.

Teachers have many useful skills, which make them a great fit for many different side hustles alongside their main teaching job.

Quick Summary on Side Jobs For Teachers:

Online tutoring and selling lesson plans are popular side jobs for teachers that use their existing skills

Selling crafts, selling printables, or teaching online courses can be a nice creative outlet

Short-term and seasonal side gigs like coaching sports or teaching summer school may be better for your schedule than year-round gigs

Best Side Jobs For Teachers

There are 36 side jobs for teachers listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Below are 36 side hustles for teachers.

1. Sell educational printables

Selling educational printables can be a great way for teachers to make extra income and it is great for anyone who wants to learn how to make passive income as a teacher.

An educational printable is a teaching resource, either digital or physical, that educators create to help with learning.

Other teachers buy these for their classes and so do parents.

Educational printables are things like math problems, vocabulary cards, and science experiments. They work for different grades and learning goals, making it an easy way to add to regular teaching or homeschooling. You can share these resources online or print them for in-person classes, making them a helpful tool for improving education.You can learn more at How I Make $400,000 Per Year Selling Educational Printables.

Do you want to make money selling printables online? This free training will give you great ideas on what you can sell, how to get started, the costs, and how to make sales.

2. Tutor online or in person

Tutoring services or helping kids get ready for standardized tests either online or in person can be a great side hustle for teachers.

This option can be a natural fit, as you can use your teaching skills to tutor students.

To start, check out different online tutoring websites like Tutor.com or you can also do in-person tutoring sessions. For in-person tutoring sessions, you can contact local tutoring companies or promote your services on social media or in local Facebook parent groups for your area.

3. Sell your lesson plans

As a teacher, you already make lesson plans for your classes. You can actually sell your lesson plans, earn extra money, and help other teachers.

The most popular platform for this kind of side job is Teachers Pay Teachers (TPT). Here, you can upload your lesson plans, activities, assessments, and other educational resources. Each time someone purchases one of your items, you’ll earn some income.

Lesson plans need to be well-organized, easy to understand, and tailored to specific grade levels and subjects (such as fifth grade math). You should include clear objectives and step-by-step instructions to make your lesson plans more appealing to potential buyers.

4. Coach a school sport or other after-school program

Coaching a school sport is something that you can do within your own school district as many schools are in need of help with their sports teams.

Some sports and after-school programs that can be a teacher’s side hustle include soccer, basketball, volleyball, and track-and-field, as well as clubs such as yearbook, chess, choir, and more.

5. Start a dog bakery

Starting a dog bakery can be a fun side job for teachers who love both dogs and baking.

You can make an extra $500 to $1,000, or even more, each month by making treats for dogs. You can make dog treats like cupcakes, cookies, cakes, and more.

You can learn more at How I Make $4,000 Per Month Baking Dog Treats (With Zero Baking Experience!).

6. Sell crafts on Etsy

Selling crafts on Etsy can be a great way to make extra money by being creative.

Etsy is a website where people from all over can buy and sell handmade and digital products.

Some ideas for products you can create and sell on Etsy that are teaching-related include:

Classroom decor items

Educational games and activities

Customized planner pages and stickers

Flashcards and study materials

Of course, you can create things that aren’t related to teaching at all, such as knitwear, jewelry, and more.

7. Sell on Teachers Pay Teachers

Teachers Pay Teachers (TPT) is a site specifically for educators to buy and sell educational materials, and this is a popular teacher side hustle. If you’ve developed lesson plans, worksheets, or other teaching tools for your classroom, you can share and earn from them on TPT.

I know I talked about selling education printables and lesson plans above, but I want to talk more about Teachers Pay Teachers in its own section because it is such a popular teacher side hustle.

You can sell:

Lesson plans and unit studies

Worksheets and printable activities

PowerPoint presentations and interactive notebooks

Posters, charts, and visual aids

For example, I looked on Teachers Pay Teachers and searched for third grade lesson plans. There, I found over 49,000 results such as math lesson plans about rounding, substitute teacher plans for third graders, reading comprehension lesson plans, and more. Here’s an example of one that you can look at.

The average teacher on Teachers Pay Teachers can make around $300 to $500 extra, but there are some teachers that make hundreds of thousands of dollars extra each year.

8. Babysit

As a teacher, you may find that babysitting is an easy side job to pick up, and, depending on where you live, you may be able to earn around $15 to $25 an hour. Parents love hiring teachers as babysitters because they have so much experience with children.

While babysitting, you’ll find that your existing skills from teaching make a difference in providing the best care possible.

9. Teach English as a second language online

Teaching English as a second language (ESL) online is a popular side job for teachers. As an online ESL teacher, you can help students learn English and work from home.

Most jobs require you to be a fluent English speaker with a bachelor’s degree.

10. Teach summer school

One of the obvious ways for teachers to make extra money in the summer is to teach summer school.

It’s a great way to make use of your teaching skills while earning extra income. Plus, summer school takes place during summer break, so it should fit well with your schedule of already being off from school.

11. Summer camp counselor

Another great option during the summer months is to become a summer camp counselor.

As a counselor, you’ll supervise children in activities such as sports, arts, and crafts. Camps are always looking for instructors with teaching experience, making this a good side job for educators.

12. Grade papers

Grading papers as a side job may appeal to you if you’re looking for a more flexible, at-home option.

Companies such as Measurement Inc. hire teachers to grade student work, such as essays and test answers.

They are hiring evaluators to score in the subjects of English, mathematics, science, and more and pay starts at $15 per hour.

13. Work at a restaurant

If you’re looking for something completely different from teaching, you could take a part-time job at a restaurant.

Working in restaurants can be a good fit for teachers because they often offer flexible hours that can align with your teaching schedule. You can choose jobs like being a server, host, and more.

14. Proofread

As a teacher, you are probably already a great proofreader and are able to spot mistakes easily. With these skills, proofreading can be a great side job. By proofreading, you can help authors, website owners, students, and more improve their writing while earning some extra income.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

15. Blog

Blogging can be a fun way for you, as a teacher, to make extra money from home. Many blogs are run by teachers, and I completely get why – you can blog in your spare time and you don’t have to stick to any formal schedule.

To start your own blog, first, choose a topic that you’re interested in writing about, maybe something related to your teaching field or a hobby you enjoy.

You can make money from your blog in ways such as:

Affiliate marketing – Share links to products or services related to the topic you are writing about, and earn a commission for sales generated from your referral links.

Advertising – Include display ads or sponsored posts on your blog.

Courses and ebooks – You can create courses or ebooks related to your area of expertise, and sell them through your blog.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog, and it all started as a side job.

Learn more at How To Start A Blog FREE Course.

Similar to blogging, a teacher could also start a YouTube channel, a TikTok, and more.

16. Freelance write

If you are looking for side jobs for teachers from home, then becoming a freelance writer can be a great choice.

Freelance writers write content for blogs, websites, magazines, newspapers, advertising companies, and so much more.

You can find different writing jobs on platforms like Upwork and Fiverr, or even find clients on your own, such as by reaching out to websites that you are interested in writing for.

Recommended reading: 14 Places To Find Freelance Writing Jobs – (Start With No Experience!)

17. Transcribe

An online transcriptionist’s job is to listen to video or audio files and then type out everything that they are hearing. There are many different types of transcriptionists, such as legal, general, and medical transcriptionists.

This job requires strong typing and listening skills, and you can work from home on your own schedule.

Transcriptionists earn around $15 to $30 per hour on average.

I recommend watching FREE Workshop: Is a Career in Transcription Right for You? You’ll learn how to get started as a transcriptionist, how you can find transcription work, and more.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

18. Flip used items for resale

Flea market flippers find underpriced items at flea markets, yard sales, and thrift stores, then resell them for a profit. This job requires a good eye for finding valuable items that you believe can be sold for a higher price.

As a teacher, you could find and sell items in the evening, on the weekends, over holiday breaks, and in the summer. You get to make your own schedule, and it can be however many or few hours as you want.

Some items that you can resell include:

Vintage furniture

Collectibles, such as toys, coins, stamps, books, and more

Sporting equipment

Clothing

Electronics

I recommend signing up for a helpful webinar on this topic, How To Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business.

19. Bookkeep

Bookkeepers are people who keep track of all the money-related things for businesses. Bookkeepers do tasks like:

Tracking income

Organizing expenses

Making financial reports

This is typically a flexible job that you can do from home on your own time.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

20. Sell Canva templates

Creating and selling Canva templates online allows you to work from home in your free time.

A Canva template is like a pre-designed layout that you can use for creating things like social media graphics, Pinterest pins, ebooks, or presentations. It is a helpful starting point if you’re not very skilled at designing from scratch. Business owners, marketing professionals, nonprofit organizations, educators, event planners, restaurants, and more buy templates all the time.

Canva templates come with blank spaces where buyers can add their own words or pictures, adjust colors and fonts, and more. They’re useful for people who want their graphics to look high quality without spending a lot of time in the process (or perhaps they don’t know how to do it so templates help them a lot!).

Making and selling Canva templates can be a great way to earn extra money as you only need to create them once, and then you can sell them as many times as you’d like.

Recommended reading: How I Make $2,000+ Monthly Selling Canva Templates

21. Rover (walk and watch pets)

Rover is a website that links pet owners with pet sitters and dog walkers. You can do this job on the weekends throughout the year, or simply only open up your schedule during the summer months. It is up to you.

Getting started is easy on Rover – you set up a profile that talks about your experience with pets and the services you can provide, like dog walking, pet sitting, and house sitting.

Then, you will receive requests from customers and talk about pricing. Rover takes care of processing payments, and you’ll receive payments directly into your account.

You can sign up for Rover here.

22. Care.com

Another platform for finding pet and house sitting side jobs is Care.com. Care.com is not limited to pet care and includes other caregiving services, such as childcare and senior care.

You can browse available jobs in your area and apply to those that match your skills and interests. Care.com also allows clients to contact you directly for your services after you’ve created a profile. Once a job is completed, you’ll receive payment through the site.

23. Be a virtual assistant

A virtual assistant provides administrative, technical, or creative support to clients from home.

Some of the tasks you might do as a virtual assistant include managing schedules, responding to emails, making travel arrangements, handling social media accounts, and even writing articles or creating presentations.

If you want to become a virtual assistant, I recommend taking the free workshop called 5 Steps To Become a Virtual Assistant.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

24. Be a food photographer

Food photography can be a fun and creative way to earn extra income during your free time. Food photographers do just that – take pictures of food.

Whether you’re working directly for restaurants, magazines, or on a freelance basis, this job allows you to use your skills and interests to create beautiful images.

You can learn more at How To Become a Food Blog Photographer And Earn Over $50,000 Each Year.

25. House sit

As a teacher, you might be looking for ways to make some extra money during breaks or weekends. One option to consider is house sitting, and this is when you watch someone’s home (such as watering their plants and collecting mail) and sometimes take care of pets while their owners are away. People also hire house sitters so that their homes aren’t sitting empty because a visible presence can deter potential thefts.

To get started in house sitting, you can join house-sitting websites to find opportunities in your area, or ask friends and family for referrals (you might want to start by house sitting for people you know and then ask for references that you can use to broaden your job search).

26. Rent out an unused room in your home

If you have a room in your home that you are not using, then you may be able to rent it to someone on either a short-term (such as by becoming an Airbnb host) or long-term basis (getting a full-time roommate).

I have rented out rooms many times in the past, and it was a great way to make some extra income for space that I wasn’t using.

You can learn more at What You Need To Know About Renting A Room In Your House.

27. Rent your garage space

If you have empty storage space, such as a garage, driveway, closet, basement, or attic, you may be able to rent it out and make extra money. This can be a lucrative side hustle where you don’t have to use up much of your spare time.

You can use Neighbor to list your extra space for rent and make up to $15,000 per year by doing so. With Neighbor, you can rent out your garage, driveway, basement, or even a closet.

You can sign up at Neighbor for free here and list your space.

You can also learn more about Neighbor at Neighbor Review: Make Money Renting Your Storage Space.

28. Rent out a photo booth

Renting a photo booth can be a fun side job for teachers.

To get started, you will need to buy a photo booth as well as things like backdrops and props for people to hold in the picture (such as hats, signs, fun things to hold, etc.).

On average, photo booth rentals can range from $500 to $1,000 per event, and in some cases, even more for specialized events or packages with additional features.

I have personally rented a photo booth for an event in the past, and it was a lot of fun!

29. Online surveys and focus groups

Taking online surveys and answering questions for focus groups is very part-time and can be a way to side hustle for teachers.

You share your thoughts plus answer questions and can earn cash or free gift cards.

The survey companies I recommend signing up for are:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

PrizeRebel

User Interviews – These are the highest paying surveys with the average being around $60.

Recommended reading: 18 Best Paid Survey Sites To Make $100+ Per Month

30. Voice over act

A voice-over actor is the person whose voice you hear but don’t see in YouTube videos, radio ads, educational videos, and more.

Different companies need a wide variety of voices, and that’s where you come in.

Recommended reading: How To Become A Voice Over Actor And Work From Anywhere

31. Mystery shop

I was a secret shopper in the past, and there were often mystery shops that gave me $100 to put toward a free dinner. I always looked forward to these, as I was living paycheck to paycheck, and I used these restaurant mystery shops to reward myself every now and then.

There were other mystery shops that paid me actual money, and some paid me in free items, such as makeup, movie theater tickets, and car oil changes.

Companies hire mystery shoppers to get an understanding of their customer’s experience. Companies want to know a real product opinion, how the customer felt they were treated at their business, how phone calls were handled, and more.

Basically, mystery shopping is a way to anonymously test the entire shopping experience.

You can learn more at How To Become A Mystery Shopper.

32. Fitness trainer

Fitness trainers help people reach their health goals through customized exercise plans and nutrition advice. This is typically a job where you can choose your schedule, so you can choose to work hours outside of your teaching job, such as in the evenings and on the weekends.

I actually know a few teachers who are fitness trainers on the side, so it must be a good fit!

Another positive is that you can even choose between in-person and online coaching. Online coaching can mean that you can work remotely, making it a more flexible side job for teachers looking to earn extra income.

33. Find random gigs on Craigslist

As a teacher looking for side jobs, you can look for random gigs on Craigslist to earn some extra income. To begin your search, simply go to the Craigslist website and select your city from the home page.

Here are some jobs I found through a quick search:

Cleaning a house

Help assembling furniture

Taking down a shed in a backyard

Garage cleanup

Mover

Handyman

Movie extra

Sign holder

You can even post your own services on Craigslist if you have a skill you’d like to share with others, such as giving music lessons or tutoring.

34. Deliver groceries with Instacart

Grocery delivery services are popular because there are more and more people who want someone to do their grocery shopping for them.

Services like Instacart need personal grocery shoppers, and the average shopper makes $15 to $20 an hour to deliver groceries. Drivers are paid per order, and you get to keep 100% of your tips. You also get to choose your schedule, so a teacher could choose to work in the evenings or on weekends. Or, you could choose to only deliver groceries during the summer.

You can click here to sign up to be an Instacart Shopper.

You can also learn more at Instacart Shopper Review: How much do Instacart Shoppers earn?

There are many other gig ideas that you can try out too, such as Uber Eats and DoorDash.

35. Real estate agent

Some teachers are real estate agents on the side of their full-time job as a teacher. This is because you can list and sell homes on your weekends, during breaks, at night, and over the summer.

Selling homes can be more difficult, though, as your clients may want your full attention during the day occasionally and you would be busy teaching, so this is something to think about.

36. Driver’s ed teacher

A common side hustle for teachers is teaching driving lessons to teenagers and adults. As a teacher, you may be able to check if the high school near you is in need of a teacher for this subject. Or, you can reach out to a local driving school to see if they are hiring.

Driving instructors make around $20 an hour more or less, depending on where you live.

Frequently Asked Questions

Below are answers to common questions about side hustles for teachers.

How can I make money on the side while teaching?

Some good side jobs for teachers include tutoring, freelancing, transcribing, blogging, selling lesson plans, and more.

What can teachers do to make extra money?

Teachers can do a lot of things to make extra money, such as jobs like tutoring, freelance writing, blogging, or creating educational printables.

What is a second career for teachers?

Second careers for teachers can include jobs such as educational consultants, curriculum developers, or even working in corporate training and development.

Do most teachers have 2 jobs?

Many teachers have two jobs. This is for many reasons, such as the typically low pay of a teacher as well as teachers wanting to make money while they are off in the summer.

How to make extra money on Teachers Pay Teachers?

Teachers can make extra money on Teachers Pay Teachers by selling lesson plans and printables.

How can teachers make money in the summer?

Teachers can make money when they’re off in the summer by teaching summer school, helping students with test prep, babysitting, selling lesson plans, working at a restaurant, working as a real estate agent, and more.

What to do after quitting teaching? How do you pivot out of teaching?

Quitting teaching and moving on to something else will take a few steps, and you can begin by thinking about your skills and interests. Then, start exploring different job options and connect with people in the field you’re interested in, attend industry events, and consider getting any certifications that you may need.

How can teachers earn extra income through online tutoring?

Sites like Tutor.com look for teachers to tutor students remotely, and you can even offer your services through social media.

How can a teacher make six figures by utilizing their skills?

While it’s not always easy for teachers to earn a six-figure salary, it is possible if you find ways to make extra income or by starting a business of your own.

What opportunities do music educators have for side income?

Side income ideas for music educators can include jobs like giving private music lessons or working as a weekend or evening instructor at a music school. Music educators can also sell lesson plans (I found some examples on Teachers Pay Teachers here).

What are some good side jobs for teachers?

I hope you enjoyed this article on the best side jobs for teachers.

Whether you are looking for side jobs for teachers from home, side jobs for teachers in the summer, or if you want to learn how to make passive income as a teacher, there are many ways to make extra money as a teacher.

Some of the best side hustles for teachers include:

Sell educational printables

Tutor online or in person

Sell your lesson plans

Coach a school sport

Start a dog treat bakery

Sell crafts on Etsy

Sell on Teachers Pay Teachers

Babysit

Teach English as a second language online

Teach summer school

Summer camp counselor

Grade papers

Work at a restaurant

Proofread

Blog

Freelance write

Transcribe

Flip used items for resale

Bookkeep

Sell Canva templates

Rover (walk and watch pets)

Virtual assistant

Food photographer

House sit

Rent out an unused room in your home

Rent your garage space

Rent a photo booth

Online surveys and focus groups

Voice over act

Mystery shop

Fitness trainer

Find random gigs on Craigslist

Deliver groceries

Real estate agent

Driver’s ed instructor

What do you think are the best ways for teachers to make extra money?

But here’s the big takeaway: That money is yours, and those savings stay with you whenever you quit a job.

If you have less than $1,000 in your 401(k)

If your 401(k) has less than $1,000 when you quit a job, the IRS allows the plan administrator to automatically withdraw your money and send you a check, minus 20% in taxes, per the IRS.

You can also initiate a rollover: a direct transfer of your money from a 401(k) account to another tax-advantaged retirement account. (More on rollover deadlines and tax implications later.) The easiest way to roll over your money is to contact your 401(k) administrator and have them handle it.

Communicate your preferences quickly, though — if your 401(k) account has a low balance, most companies won’t delay closing the account and cutting you a check, according to CNBC.

If you have between $1,000 and $5,000 in your 401(k)

If your 401(k) has between $1,000 and $5,000 when you quit, your employer may move your money into an individual retirement account, or IRA, according to the IRS.

If you don’t have an IRA, some employers will automatically open an account for you and deposit your funds into the account. If you do have an IRA, you initiate the rollover by contacting your 401(k) administrator.

You can also withdraw your money, but you’ll pay 20% in federal income tax, as well as a 10% early withdrawal penalty (unless you’re at least 59 ½ years old), according to the IRS.

🤓Nerdy Tip

An IRA is a tax-advantaged retirement account that an individual typically sets up, unlike a 401(k) account, which an employer sets up.

If you have at least $5,000 in your 401(k)

If your 401(k) account has at least $5,000 when you quit a job, your employer isn’t allowed to move your money without your consent. What happens next is up to you. There are a few things you can do with your money, according to the investment advisor Vanguard:

Roll over your money into a new retirement account

Leave your money in your old 401(k)

Cash out your 401(k) — and potentially pay a 10% federal penalty tax

Let’s dig into those options.

Rolling your money into a new 401(k) or IRA

What is a rollover?

Reminder: A 401(k) rollover is the process of moving money from your 401(k) account into another retirement account.

So, say you’re leaving your job for a different position, and your new employer offers a 401(k) plan. You can roll over your old 401(k)’s funds into a new 401(k) account, if your new employer allows this, according to the IRS.

Or you can roll over your old 401(k) to an IRA. This type of account typically offers more investment options than a 401(k), says Christopher Manske, a certified financial planner and the president and founder of Manske Wealth Management in Houston.

“In your individual retirement account, you’re going to have a lot more flexibility to tailor the investments to the wide world of what’s available out there,” Manske says.

Whether you roll over your retirement savings into an IRA or new 401(k), moving your money to a single fund can make it easier to manage your money and keep track of your retirement savings.

That’s as opposed to simply keeping your old 401(k) open, which becomes one more account to manage. (We’ll dive into that option in a bit.)

How to roll over funds — and avoid tax missteps

If a rollover sounds like a solid option, contact the administrators of both your old 401(k) and the other retirement account — either your new 401(k) or an IRA. Tell them you’d like to roll over your funds.

They’ll collect information from you and initiate a direct rollover, which means one institution directly transfers funds to another institution, according to Fidelity.

This is as opposed to an indirect rollover, meaning your 401(k) plan administrator sends you a check, and you personally deposit the 401(k) funds into another retirement account. In that case, your plan administrator would likely withhold 20% of your 401(k) funds for taxes.

With this indirect rollover, you then have 60 days to deposit the complete 401(k) account balance — including the amount kept for taxes — into the new account. So to deposit the full amount, you would need to come up with the 20% portion yourself. Then you’d get a refund for that amount come tax time.

If you miss the 60-day deadline, you’d likely get penalized for early withdrawal and have to pay income taxes on the distribution, according to Capitalize, a 401(k) rollover resource.

One last important note: Whether you choose a direct or indirect rollover, if you move money from your old 401(k) account to a Roth IRA — a specific kind of IRA — you’ll have to pay income tax on that transfer, according to the IRS. (This doesn’t apply if you’re rolling over your funds from a Roth 401(k), though.)

Leaving your money in your old 401(k)

Another option? Do nothing.

Your 401(k) account isn’t going to disappear once you quit a job; that money will always be there. But once you leave the job that set up the 401(k) account, you can’t make any more deposits, per Vanguard.

While leaving your 401(k) on autopilot is the simplest option, it may not be in your best interest. Assuming you’ll continue investing in another account or have a new 401(k) at your next employer, it will be harder to track your finances in more places.

And some 401(k) plan providers may charge you fees if you’re no longer an active employee, according to Charles Schwab, the financial services firm.

“I can’t think of any pros of leaving it there,” Manske says. “You’re not really connected formally to that company anymore, so why would you keep your money there? They don’t have a reason to keep you happy.”

Cash out your 401(k) — which is rarely recommended

Yes, you can withdraw the cash from your 401(k) whenever you want. But there are significant downsides to this option.

Pulling out money from your 401(k) before retirement can trigger hefty taxes, says Joe Buhrmann, certified financial planner and senior financial planning consultant at Fidelity’s eMoney Advisor.

Any withdrawals from a 401(k) before you reach the age of 59 ½ are considered early withdrawals and are slapped with a 10% penalty tax, per the IRS. That’s in addition to federal income taxes and, depending on where you live, state income taxes.

“Hypothetically, on a $50,000 401(k), you might lose as much as $20,000 to taxes and penalties and be left with $30,000,” Buhrmann says.

If you urgently need cash, that might be a reason to withdraw some money from your 401(k). But doing so should be regarded as a last resort, Manske says.

There are other ways to get money quickly that don’t come with taxes and penalties, such as community loans, gig work, and more.

Buhrmann encourages individuals to not just consider the immediate losses that come with withdrawing your 401(k), but also the long-term earnings they’re missing out on.

“They’re not just having to pay some taxes and pay some penalties,” Manske says.

One interesting aspect of the home loan process is the sheer number of individuals you’ll work with along the way.

You don’t just speak to a salesperson and call it a day. Lots of people are involved in what is a very complex transaction.

Aside from salespeople, there are loan underwriters, processors, appraisers, escrow officers, real estate attorneys, and more.

Let’s discuss the roles these people hold to help you better understand what it takes to get a mortgage.

Remember, you’re asking to borrow a large sum of money, so it’s going to take time and energy (and lots of people) to get to the finish line.

The Sales Rep/Loan Officer/Mortgage Broker

The first step in the home loan process typically involves a sales person, which can be a banker at your local branch or credit union, a loan officer, or a mortgage broker.

If we’re talking about a purchase, this may come before/during your home search or after you’ve found your property with the assistance of a real estate agent.

If it’s a mortgage refinance, you’d simply jump right to this step to rework the details of your existing home loan if you wanted a rate and term refinance or a cash out refi.

You might be referred to an individual/company, or you might do your own discovery to find a suitable partner. Either way, always look beyond the referral you were given.

Your real estate agent might know a great lender, but you your own research as well.

It’s important to gather multiple quotes from different companies to ensure you get the best deal.

Now, this individual will be your main point of contact during the loan process, and perhaps most importantly, will provide you with pricing.

Bankers and loan officers work at the retail level, while mortgage brokers offer wholesale rates from their lender partners.

You can read more about the differences (banks vs. brokers) but either way they’ll likely be the person you speak with most.

Aside from providing pricing, these individuals can help get you pre-qualified or pre-approved for a mortgage, discuss different loan scenarios, and guide you on loan choice.

If you have mortgage questions, they should be able to provide answers and give you guidance.

They may make certain recommendations, such as down payment amount, loan type, or provide an opinion about paying discount points or when to lock your rate.

This individual will be with you from start to finish, but doesn’t work alone. They’ve got an entire team to help you close your loan in a timely fashion.

FYI, you may also come across a “mortgage planner,” which is an individual who may assist a busy senior loan officer.

They can communicate loan status, provide follow-up, collect conditions, and perform other tasks if the LO is unavailable or simply needs a hand.

The Loan Processor

Once you’ve spoken to a sales representative (or LO/broker) and have decided to move forward, you’ll be in put in touch with a loan processor.

The main goal of the processor is to put together a clean loan file that can be submitted to the underwriting department.

This means collecting key documents, ensuring there are no red flags, double-checking everything, and making any necessary corrections.

The processor may also reach out after the loan is approved to collect additional documents to satisfy any outstanding conditions.

They will also provide updates to the loan officer or broker, who will then keep you in the loop about where you’re at in the process.

The processor essentially acts as a liaison between the underwriter and sales rep/LO/broker.

This ensures things move along smoothly and any hiccups can be resolved quickly without delay.

The Loan Underwriter

The loan underwriter probably holds the most important role in the home loan process.

They decide if the mortgage is approved, declined, or potentially suspended pending further explanation.

It’s for this reason that the loan processor only sends the loan package to the underwriter once everything has been thoroughly checked.

You only get one chance to make a first impression, so it’s imperative to get it right. Otherwise you could face delays or simply get flat out denied.

Aside from approving the loan, the underwriter will also provide a list of conditions needed to close the loan.

Most mortgage approvals are conditional, meaning you might need to furnish additional information or documentation to obtain your final approval.

Once these documents are provided, whether it’s another bank statement or letter of explanation, the underwriter will clear the outstanding conditions and move the loan to the funding department.

The Home Appraiser

While your loan is being reviewed by the underwriter, an appraisal will be ordered to determine the value of the underlying property.

Remember, aside from determining your ability to repay the loan, the bank also needs to ensure the collateral for the loan is valued properly.

This individual will visit the property to assess its condition, take photographs, and determine recent sales comparisons.

They will formulate a valuation based on the property details, such as number of bedrooms and bathrooms, square footage, amenities, location, lot size, condition, and so on.

The value they come up with, known as the appraised value, is used as the basis for the loan-to-value ratio.

Generally, the goal is for the appraiser to support the purchase price of the property or the value declared for a refinance.

If the value is lower, the details of the loan may need to be reworked, such as a higher down payment.

For certain types of loans, such as FHA loans and VA loans, the home appraiser will also ensure that certain Minimum Property Requirements (MPRs) are met.

This ensures the property is safe for the occupants, that there are adequate living conditions, and no major hazards, such as lead paint or termites.

The Home Inspector

If we’re discussing a home purchase, you’ll want to get an inspection done. And you’ll want to do it ASAP while any contingencies are still in place.

While a home inspection typically isn’t required, they’re generally a good idea.

Aside from finding out what’s potentially wrong with the property, you can ask for credits from the seller if the inspector finds any significant issues.

As the name suggests, a home inspector will come out to the property and assess the condition of the structure itself, the foundation, the interior, the roof, the electrical, HVAC, and more.

Some may also inspect the pool and spa, if one exists, though you could be charged extra.

They’ll make notes as they survey the property and issue a formal report afterwards. This can be used to negotiate with the seller if anything material comes up.

The Notary Public

Once it’s time to sign your loan documents, you’ll need to make an appointment with a notary public.

This individual serves “as an impartial witness” when signing important documents, such as those related to a home purchase or mortgage loan.

Your settlement agent should organize a time to meet with this individual to conduct your signing.

The notary may come to your home or meet you somewhere else to review and sign documents.

The main job of the notary is to verify the identity of the signer and ensure they are willing to sign the documents “without duress or intimidation.”

This requires you to furnish identification, such as a driver’s license, during the signing appointment.

The Escrow Officer

Another very important individual in the transaction is the escrow officer, a third-party who facilitates the loan closing and collects/disburses funds to the appropriate parties.

Some of their key roles include preparing final statements for the buyer, such as cash required to close, and determining costs such as property taxes, insurance, prepaid interest, and loan payoffs.

The escrow officer will send you a settlement statement that lists all the fees and closing costs associated with your loan, along with any lender credits and loan payoffs and funds required.

They will also liaise with a title company and forward necessary documents for loan recording.

Importantly, they’ll provide wiring instructions to all parties, including the buyer, so you know where to send funds (cash to close).

If you have questions about things like prepaid items, mortgage impounds, and loan payoffs, they can be particularly helpful.

The Title Agent

To ensure the property is free of any liens, encumbrances, or defects, a title insurance policy is usually required in order to take out a mortgage.

A title agent is the individual who conducts a title search, orders a preliminary title report, and eventually issues title insurance on the subject property. This makes them a licensed insurance agent

They are also in charge of recording the deed and loan documents with the county once the loan has funded.

You might hear the words title and escrow used interchangeably, but title has to do with property ownership/lien history, while escrow is about the calculation, collection, and disbursement of funds.

However, they may perform other settlement tasks beyond just title depending on the state where they’re located.

The Loan Closer/Funder

If you’ve made it this far, it means the loan is almost funded. But there’s still work to be done.

The loan closer/funder has to review the file to ensure everything is accurate and complete, and if not, address and fix any errors or outstanding issues.

They must ensure all prior to funding (PTF) conditions are satisfied and work with the settlement agent to prepare funding figures and timing of disbursement.

This includes the review of signed closing documents and items like hazard insurance and the preliminary title report.

And if everything looks good, request the wire instructions from escrow after a thorough review.

The Real Estate Attorney

Note that in certain states, a real estate attorney could be required to prepare certain documents and/or to conduct the loan closing.

This individual may order and certify a title report, review loan documents, and advise you if necessary.

Beyond that, they can ensure the interests of all parties are protected, and handle any legal issues or disputes that may come up.

One last thing. You may find that there is some overlap with a title company and escrow company, as the former can also provide escrow and notary services as well.

So depending on where you live, you could have one company or individual handle several tasks.

As you can see, there are quite a few people involved in the funding of a home loan, which explains why they take a month or longer to close.

Once you know more about each person’s role, it should be easier to navigate the home loan process and make better sense of it all.

And perhaps adjust your expectations that there isn’t a same-day mortgage and likely won’t be for the foreseeable future.

If you’re in the market for purchasing a new home or taking on a business loan or personal loan, you’re likely finding it difficult to score the almost-2% APR we saw in 2020. That’s becausethe Federal Reserve has been hiking interest rates since March 2022 in an effort to cool inflation.

“The Fed has two objectives: To keep inflation low, their current obsession, and to keep unemployment low, which is of current lesser concern,” says Amy Hubble, a certified financial planner who has a Ph.D. in consumer economics. “In practice, this means they lower rates to incentivize growth and hiring, and raise rates to combat inflation when the economy gets overextended. This leads to a policy teeter-totter meant to balance out economic activity in the US.”

So the question remains: When will we finally see interest rates start to come down? CNBC Select asked three experts to give their take on what lies ahead for interest rates. Here’s what they had to say.

What we’ll cover

When will interest rates come back down?

Nobody outside of the Federal Open Market Committee (FOMC), the 12 men and women tasked with setting target interest rates, can predict with any certainty what will happen with rates and when. But that hasn’t stoppedeconomists like Preston Caldwell, a senior U.S. economist for Morningstar Research Services LLC, from making their own educated guesses.

“I think rates will start cutting in early 2024,” Caldwell says. “I think inflation will be nearing the Federal Reserve’s 2% target at that phase and the economy will show signs of slowing, but it’s hard to predict.”

Other professionals in the space echo a similar vision. Hubble points to a recent FOMC report that includes committee members’ projections on gross domestic product (GDP) growth, inflation and the unemployment rate — all factors the Fed will weigh when deciding how aggressively to cut rates.

“All FOMC members believe that rates will be stable or higher through 2023 before slowly coming down in 2024–2025 to settle at a comfortable 2.5% for the longer-term,” she says.

Elliot Eisenberg, the Chief Economist at Graphs and Laughs agrees. “There was a belief that once the second half of 2023 came around, rates would’ve been lower than they were at the end of 2022,” he says. “But it hasn’t come down. These things take a long time to work their way through the economy, so sometime in 2024 sounds about right.”

However, he also warns that it’s hard to believe that we’ll see any interest rate cooling in 2023.

Subscribe to the CNBC Select Newsletter!

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here.

What should you do when interest rates go down?

Lower interest rates make borrowing money cheaper. That means all other factors (like your credit score) being equal, you’ll generally pay less in interest on anynewstudent loans, personal loans, business loans and mortgages than you would during today’s high-rate environment. Existing loans with a variable rate may also start charging less interest as the Fed lowers interest rates.

That’s why waiting until interest rates come down beforeborrowing money for alarge purchase — like a home — can be easier on your bank account. The current average mortgage interest rate on a 30-year loan is 7.98% even for borrowers witha credit score between 700 and 719. That’s a tough pill for a first-time homebuyer to swallow month after month as they pay their mortgage.

However, if holding off on getting a mortgage isn’t doable for you, make sure you improve your credit score before applying so you can qualify for an interest rate that’s as low as possible. Also consider choosing a mortgage lender that helps you save money throughout the process. Ally Bank, for instance, doesn’t charge any lender fees. And if you qualify for a Navy Federal Credit Union mortgage, you can get a home loan with no private mortgage insurance (PMI) requirements even if you make a down payment of less than 20%.

Ally Home

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Conventional loans, HomeReady loan and Jumbo loans

Terms

15 – 30 years

Credit needed

Minimum down payment

3% if moving forward with a HomeReady loan

Terms apply.

Navy Federal Credit Union

Annual Percentage Rate (APR)

Apply online for personalized rates

Types of loans

Conventional loans, VA loans, Military Choice loans, Homebuyers Choice loans, adjustable-rate mortgage

Terms

10 – 30 years

Credit needed

Not disclosed but lender is flexible

Minimum down payment

0%; 5% for conventional loan option

You can also refinance your mortgage down the line during a lower interest rate environment so you can score a better rate on your loan. PNC Bank is one of the most accessible lenders because it has locations in all 50 states and customers can apply both online and in-person.

PNC Bank Mortgage Refinance

Annual Percentage Rate (APR)

Apply online for personalized rates; fixed-rate and adjustable-rate mortgages included

Types of loans

Fixed-rate, adjustable-rate, FHA loans, VA loans and jumbo loans

Fixed-rate Terms

10 – 30 years

Adjustable-rate Terms

Available in periods of 7 and 10 years for a fixed rate, followed by an adjustment period when the interest rate may increase or decrease on an annual or semi-annual basis

Credit needed

Not disclosed

Pros

Refinance available for primary and secondary homes, and investment properties

Offers a wide variety of loans to suit an array of customer needs

Offers refinancing for VA and FHA loans

Available in all 50 states

Online and in-person service available

Cons

Doesn’t offer home renovation loans

Lower interest rates can also have an impact on the APY you earn on your high-yield savings account. While buying a house or taking out a personal loan becomes more affordable during lower interest rate environments, you typically can’t earn as high an interest rate from the money in your deposit accounts.

That’s becausebanks use the Fed rate as a benchmark for yields on savings accounts. So when the Fed rate falls, the interest rate on your high-yield savings account will likely also decrease. Right now, some high-yield savings accounts, like the UFB High Yield Savings Account, are offering more than 5% APY on account balances.

UFB High Yield Savings

UFB High Yield Savings is offered by Axos Bank, a Member FDIC.

Annual Percentage Yield (APY)

Earn up to 5.25% APY

Minimum balance

Monthly fee

Maximum transactions

No max number of transactions; max transfer amounts may apply

Excessive transactions fee

Overdraft fee

Overdraft fees may be charged, according to the terms, but a specific amount is not specified; overdraft protection service available

Offer checking account?

Offer ATM card?

Terms apply.

Even though we’re unlikely to see sky-high APYs stick around after the Fed lowers interest rates, it’s still worth keeping your money in a high-yield savings account even in a lower-rate environment. You’ll still grow your money faster in a high-yield account than with most traditional savings accounts, and it provides a safe, FDIC-insured place to keep your emergency fund.

Bottom line

According to experts, we aren’t likely to see significantly lower interest rates this year, but 2024–2025 is likely to see more progress on that front. Lower rates can make life easier for individuals who have been waiting to buy a house or take on other types of loans, even if savers won’t enjoy the high APYs that thrive in a world of high rates.

Meet our experts

At CNBC Select, we work with experts who have specialized knowledge and authority based on relevant training and/or experience. For this story, we interviewed:

Preston Caldwell, a senior U.S. economist for Morningstar Research Services LLC.

Elliot Eisenberg, a chief economist and Graphs and Laughs.

Amy Hubble, a CFP with a Ph.D. in consumer economics.

Why trust CNBC Select?

At CNBC Select, our mission is to provide our readers with high-quality service journalism and comprehensive consumer advice so they can make informed decisions with their money. Every article is based on rigorous reporting by our team of expert writers and editors with extensive knowledge of personal finance. While CNBC Select earns a commission from affiliate partners on many offers and links, we create all our content without input from our commercial team or any outside third parties, and we pride ourselves on our journalistic standards and ethics. See our methodology for more information on how we choose the best mortgage lenders and high-yield savings accounts.

Catch up on CNBC Select’s in-depth coverage of credit cards, banking and money, and follow us on TikTok, Facebook, Instagram and Twitter to stay up to date.

Editorial Note: Opinions, analyses, reviews or recommendations expressed in this article are those of the Select editorial staff’s alone, and have not been reviewed, approved or otherwise endorsed by any third party.

There is a significant difference between being an adult and behaving like one. Legally, teens become adults when they turn 18. It’s pretty common for teenagers to ponder the moment of their transition into adulthood and the distinguishing factors between being an adult and a child. Here’s a list of life skills we think every adult needs to know in order to really act like an adult.

1. Financial Management

Photo Credit: Shutterstock

Acquiring the ability to handle your financial matters is an essential life skill that every individual should grasp before reaching 18 years of age. Financial management encompa-es skills such as devising and adhering to a budget, saving funds, comprehending credit, and preparing for future expenditures. Acquiring strong financial management abilities in your youth can establish a foundation for long-term financial stability in the future. Learning how to prioritize critical expenses (like rent), avoid overspending, and save for emergencies and future goals is important. It’s never too early to start learning; kids as young as 7 or 8 can begin practicing with their allowance.

One Redditor said, “Developing skills of positive financial management is a process many overlook.”

Another also added, “So much this. Or even just understanding how to budget and a basic understanding of household bills.”

2. Good Hygiene

Photo Credit: Shutterstock.

Proper hygiene is crucial for averting illnesses and diseases and enhancing personal appearance and contentment. Cultivate healthy routines like consistently washing your hands, caring for your oral hygiene, taking showers, and donning fresh clothing. Practicing good hygiene in public places and when you’re sick is also essential. By learning good hygiene at a young age, you can develop habits that benefit your own health and make it easier to keep a strong group of friends—giving you a healthier community overall.

3. Cooking

Photo Credit: Shutterstock.

Cooking is important not only for saving money but also because it can teach you time management, budgeting, nutrition, and many other things. Cooking at home gives you greater control over the ingredients they use, which is especially helpful if you have allergies. Overall, learning how to cook is a valuable skill that provides numerous benefits, including increased self-sufficiency. It is never too early to start learning and developing cooking skills at a young age can set individuals up for a lifetime of healthy and enjoyable eating habits.

One user said, “Oh, and cooking some basic meals is a lifesaver. I don’t know why schools don’t have home economics cla-es. It’s such a shame.”

4. Simple First Aid

Photo Credit: Shutterstock.

Acquiring a basic understanding of first aid holds significance, as it enables you to navigate emergencies without succumbing to the fight-or-flight instinct and instead provide practical a-istance. Basic first aid skills can help prevent injuries from worsening and sometimes even save lives. It’s good to know how to treat minor cuts, burns, and bruises and respond to choking, allergic reactions, and other medical emergencies. Knowing how to perform CPR and use an automated external defibrillator (AED) usually requires certification, but it can be life-saving in some situations.

Understanding how to see the big picture in an emergency is important, such as a-essing the situation, calling paramedics, and staying calm and focused.

5. Critical Thinking

Photo Credit: Shutterstock.

Critical thinking is how we carefully analyze information, evaluate evidence, and make logical decisions. The foundation of critical thinking is really just asking good questions, trying to find out all the relevant information before you make a decision, and developing your problem-solving abilities. The world is full of information, misinformation, and confusing situations (like finding an honest mechanic or negotiating with a landlord). The ability to think critically and ask good questions will take you a long way.

One Redditor said, “Don’t take things at face value; really consider what is being told to you, why, and by who. There are good people in the world of course, but there are many who do NOT have your best interest at heart and will attempt to take advantage of your ignorance. Go slow, listen, learn, and Think.”

6. Time Management

Photo Credit: Shutterstock.

Time management is an essential life skill; it can benefit anyone at any age, but it’s particularly important to learn it as you move away from home and encounter the world on your own. Managing your time is important for everything from the obvious (working, school, making plans with friends), to cooking a meal or cleaning your house. As you become an adult, practice managing your time and creating a schedule or using a calendar or planner. Time management can help you be more productive, achieve your goals, and reduce stress.

7. Emotional Intelligence

Photo Credit: Shutterstock.

Take some time as you become an adult to learn or brush up on emotional intelligence. You don’t have to read thoughts, but staying attentive to the emotions, reactions, and expressions of the people around you can teach you so much and help a lot with all kinds of relationships. Everything from working to dating relationships relies a lot on working with other people’s moods and emotions, even if they’re unfair. Developing these skills will help navigate social relationships and communicate clearly and effectively.

One Redditor added, “Emotional intelligence. I didn’t start developing this at all until I was in my late 20s. I feel like men especially struggle with this.”

8. Self Control

Photo Credit: Shutterstock.

Delayed gratification is one of the hardest skills to learn: almost everybody is tempted by the instant payoff. Learning self-control is essential to make better decisions, regulate emotions, and achieve goals. Self-control skills include delayed gratification, but also impulse control, self-motivation, and stress management. The ability to manage your stress, keep yourself motivated, and keep control over your impulses will take you a long way in life.

One Redditor stated, “Self-control, you are now an adult, and whatever protections you had for your actions as a minor are largely gone, and the consequences are now higher.”

9. Communication Skills

Photo Credit: Shutterstock.

Learning to communicate well can provide significant benefits, such as improved relationships, better academic performance, increased employability, improved mental health, and enhanced problem-solving abilities. Some ways to develop communication skills include practicing speaking, reading, and writing, joining clubs or organizations, active listening, and seeking feedback. Whatever way you find to practice, do it with mindfulness and intention, not just to get it done.

10. Developing Your Own Opinions

Photo Credit: Shutterstock.

Developing your opinions is an important skill to develop before age 18 because it helps you become a critical thinker and an independent individual. It is essential to form your own opinions based on evidence, logic, and reasoning rather than simply adopting the beliefs of others.

11. Learn a New Skill

Photo Credit: Shutterstock.

As you age and become more independent, don’t stop studying and learning new things. New skills are not only just interesting (and make you a more interesting person), but they can increase your overall joy, inspire you in your school or career, and keep your mind sharp. Some really valuable skills to consider brushing up on include a foreign language, coding or computer programming, public speaking, writing, critical thinking, and problem-solving.

As a user added, “There are a lot of skills one should possess before turning 18; they include social skills, communication networking, tech skills, video editing, graphics designing, and coding…”

While you might not try to learn those exact skills for your personal career path, keep studying and learning whatever direction you decide to take.

Source: Reddit.

10 Crazy Good Movies Where Women Are the Bad Guys

Image Credit: Lionsgate

Are you looking for a movie night with a twist? Look no further than these Reddit-voted top ten films where women take on the destructive bad guy role.

10 Crazy Good Movies Where Women Are the Bad Guys

10 of the Worst TV Series Ever According to the Internet

There’s Seinfeld, The Sopranos, Game of Thrones, The Office, and other legendary shows. But have you considered that for each show that garners universal critical acclaim, there is an inverse show lurking on the other end of the IMDb rating scale?

10 of the Worst TV Series Ever According to the Internet

Photo Credit: Shutterstock

Have you ever known someone and thought you liked them—until you learned about their hobbies? Then you get to know them and then you’re like, “Wow, red flag.” Well, you’re not alone.

These 10 Activities Are an Immediate Red Flag

Photo Credit: Shutterstock.

Some celebrities definitely seem to enjoy the limelight and keep working to stay in the public eye. While others quickly move out of the spotlight. Many of these actors and actresses stepped out of the spotlight to live a more private life without constant media pressures.

10 Celebrities That Made the Big Times Then Disappeared Off The Face of the Earth

Image Credit: Troma Entertainment

We’ve all been there – sitting through a movie that we can’t help but cringe at, but somehow it still manages to hold a special place in our hearts.

These 10 Terrible Movies Are Still People’s Favorites

This article is part of a series put together by the Total Mortgage marketing team that provides loan officers and other sales professionals with a crash course in marketing and self-promotion. To read other articles in this series, click here.

Launching a website with strong content is important to initial success. However, to maintain a high amount of traffic you’ll need to regularly update your site with fresh content. Whatever your medium (e.g. blogs, videos), without new content your site will inevitably get pushed into the back corner of the web. That’s because the algorithm that search engines use to determine what results show up first gives more weight to sites that are fresh and dynamic, as opposed to stale and static.

The following guide will teach you how to go about finding the best topics and optimal post times to help keep your website at the forefront of the web.

Killer content starts with a killer topic. You can write a mind-bending blog on adjustable mortgage rates in Amarillo, Texas, but if no one cares about that, it’s not going to perform well. You’ve got to tap into the minds of homebuyers and figure out what information would be most valuable to them. Remember, the best topics are based on questions that lots of people have, but that haven’t been answered before—or haven’t been answered well before. Here are a few tips to keep the ideas flowing.

Check out sites like Quora and Reddit

These two sites get lots of traffic and lots of curious users. Questions are posted periodically and typically have a high amount of engagement. It’s an easy way to check in and see what prospective homebuyers are thinking. You can search for whatever mortgage/home-buying topic you want at Quora, and Reddit has a subreddit dedicated to mortgages.

Google Autocomplete

Google likes to try and figure out what you’re going to type. As a user, it can be both helpful and annoying. As a marketer, it provides a glimpse into the inner-workings of potential clients. If a phrase is popping up in autocorrect, that means a lot of people want to know about it. That provides a great opportunity for you to answer a question or provide information for a large audience. You can type anything into google, but starting your phrase with who/what/when/where/why/how often yields the best results.

Google Keyword Tool

Google AdWords has a keyword planner tool that can be useful when trying to choose a topic. You can get search volume data and trends, new keywords using a phrase, website, or category, and enter keyword lists to get new keywords. Search volume data is helpful when you’re unsure if there is enough interest in a given topic to warrant a post about it.

Think about your interactions with borrowers or referral partners