If you’re getting ready to buy your first home, there are probably thousands of questions running through your mind. Questions about location, real estate services, expenses, and more — it’s a huge financial commitment and you probably want to make sure you have the best chance at getting exactly what you want. While it can be a difficult process to navigate, there is help for first-time homebuyers, from resources and advice to first-time homebuyer programs to help you finance a home.

If you’re worried you won’t ever be able to purchase a home, take a deep breath and a good look at your finances. You can start by reviewing your current financial situation and beginning to save for a down payment. (There are investment accounts and savings options that can help you reach your goal of buying a home, too.) Here are 12 helpful tips for first-time homebuyers.

1. Know Your Credit Score

Your credit score is typically very influential in determining what kind of interest rate you can get on a home mortgage loan. You can get one free credit report from each of the three major credit bureaus (Equifax®, Experian®, and TransUnion®) every 12 months, and may also be able to view free reports more frequently online. You can review your credit report to spotlight any errors that may affect what lenders are willing to offer you.

If you find any errors, you can report them and have them removed. This process can sometimes take a while, even if the mistakes are obvious, so consider starting a credit report review early on in your home-buying process.

2. Calculate What You Can Afford

Do you know how to figure out how much house you can afford? While the size of your mortgage is generally determined by an evaluation of your personal finances and debt, there are a few rules of thumb that may be relevant.

One general guideline is that your housing costs, including your mortgage payment, should, ideally, be no more than 28% of your gross monthly income.

If you are paying off student loans, credit card debt, or have a car payment, you may want to adjust your budget accordingly. Some people try to keep their debt to 36% of their gross monthly income, so that they can still prioritize financial goals like saving for retirement. (This is just another rule of thumb and everyone’s financial goals are different.)

And having less debt may make you more appealing to mortgage lenders. Understanding how much money you feel comfortable spending on a house can, in turn, impact the properties you consider. As you build your budget, you can also check out SoFi’s mortgage calculator.

3. Look into First-Time Homebuyers’ Programs

While you are evaluating your options and creating your budget, it could be worth looking into some first-time homebuyers’ programs. Some programs offer down payment and closing cost assistance, or loans with reduced interest rates.

There are a variety of options available for first-time homebuyers looking for assistance. For example, the Federal Housing Administration offers a mortgage insured by the FHA. These loans often come with competitive interest rates and allow for smaller down payments.

The USDA also helps first-time homebuyers with a program focused in rural areas. And the VA loan program provides assistance to active duty military members, veterans, and surviving spouses. There are even more first-time homebuyer programs and loans available from various states as well.

4. Understand the Expenses

There are plenty of other expenses that come with purchasing a home beyond your down payment and closing costs. For example, when you’re renting property, you don’t have to worry about property tax or general maintenance. When you own property, you do.

In addition to property tax, you’ll likely also need insurance to protect your new home. And you’ll be responsible for maintaining the property, of course, which can include painting, replacing windows, updating the roof, replacing appliances, and more regular maintenance and upkeep.

You may also need to factor in additional purchases like a lawn mower or professional landscaping if the property you are looking at has a yard. Will you need to buy a snowblower to clear the driveway during long winters? These are all factors that can come into consideration when figuring out the cost of your new home.

Check out our Home Affordability Calculator to estimate how much house you can afford.

💡 Quick Tip: Jumbo mortgage loans are the answer for borrowers who need to borrow more than the conforming loan limit values set by the Federal Housing Finance Agency ($726,200 in most places, or $1,089,300 in many high-cost areas). If you have your eye on a pricier property, a jumbo loan could be a good solution.

5. Remember that Location Matters

Location is, obviously, important to many buyers. In some cases, you may have to decide if being in the neighborhood you want is more important than having extra square footage or other, similar trade-offs.

If you have kids or are planning to, you will likely be considering the school district each potential property falls in. Even if you aren’t planning to have kids, it could be worth considering the school district since it can have an impact on the value of your property and could make it easier to sell the house down the line.

6. Plan for the Future

Zoning laws and development plans are another factor to consider when house-hunting. If there is undeveloped land nearby, it can’t hurt to do some digging and see if there are any plans for development.

It may also be worth looking into the property value of other homes in the area. Have they been declining in recent years? If so, this could impact the future value of a home you’re considering.

7. Use Your Imagination

When shopping around for houses, you can take the opportunity to look at a property’s potential, as well as its current value. It’s easy to be distracted by the current owner’s décor, paint, carpet, or other factors that are easy to change. You can easily repaint or update the appliances, but you won’t be able to adjust the location, floorplan, or add rooms to the home as easily. 💡 Quick Tip: Backed by the Federal Housing Administration (FHA), FHA loans provide those with a fair credit score the opportunity to buy a home. They’re a great option for first-time homebuyers.

8. Reserve Cash for Home Improvements

When you’re getting ready to put a down payment on a house, it may be tempting to clean out your savings account. And while that’s completely understandable, keeping your emergency fund close at hand may be a good idea when becoming a homeowner.

After closing costs have been sorted out and you’ve moved into your new home, you might find that unexpected repairs pop up. Having a reserve stash of cash can be helpful if the roof in your new home starts leaking, or you need to replace an appliance.

9. Get a Real Estate Agent

With all of the housing apps and free resources available on the internet, it may seem like a real estate agent is unnecessary. But in reality, navigating the housing market can be tricky and hiring an agent up front can save you time and help make your home-buying experience easier.

While you could spend your time going to open houses and scouring real estate listings, an agent can tailor the home search so that you spend less time looking at houses that don’t meet your criteria. They also can have access to new listings that aren’t yet on the market and may be willing to “preview” homes for you. A real estate agent can also help you navigate the intricacies of contract negotiations and paperwork. If you’re wondering how the real estate agent gets paid take heart: They are typically paid from the seller’s proceeds.

10. Know What to Expect from a Home Inspection

Having a home inspection completed is a critical step in buying a home. Inspection procedures vary from state to state, so it can be important to understand what is included in the home inspection in your state, since this is a great chance to truly examine the property and uncover any issues—before they become your issues.

Inspectors should have access to every part of the house including the roof and crawl spaces, and you should be able to attend the inspection yourself.

Don’t be afraid to ask the inspector questions; the more information you have, the better prepared you can be to decide if this is the right house for you.

11. Negotiate the Offer

You’ll have an opportunity to negotiate when you’re making an offer on a house. A lot of factors can influence an offer and negotiating terms in your favor could result in serious savings, especially if you are in a buyer’s market.

If you are working with a real estate agent, they can help give you a good idea of what is considered a reasonable purchase bid by providing comparable sales. A “comparable” is a home similar to the one you are considering (and in the same condition and location) that has sold in the last three months. An agent can help give you an estimated price range and manage your expectations.

12. Find the Right Mortgage

Before committing to a mortgage, it’s smart to shop around and see what various lenders are willing to offer you. A few things to consider include the interest rates, loan terms, application process (Is it lengthy? Online only?), and any hidden fees included in applying for or repaying the mortgage. Familiarize yourself with the different types of mortgage loans available during this shopping process.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% – 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It’s online, with access to one-on-one help.

SoFi Mortgages: simple, smart, and so affordable.

Photo credit: iStock/PeopleImages

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

The world of real estate is vast and varied, with numerous options catering to renters’ diverse needs. Among the many choices available, private-owner house rentals have carved out a distinct niche, appealing to those seeking a more individualized experience.

These rentals, run by individual homeowners rather than large corporations, possess their own unique set of merits and challenges. We’ll provide an in-depth exploration of the benefits, drawbacks and nuances surrounding houses for rent by a private owner, contrasting them with more traditional rental avenues.

Defining private-owner house rentals

Private-owner house rentals refer to properties that are rented out by individual homeowners rather than by property management companies or real estate corporations. These private-landlord rentals can range from vacation homes to apartments to single-family residences and more.

Pros of privately owned house rentals

If you’re looking for a place to rent, private-owner house rentals emerge as a unique option, often favored for their personalized approach and distinct charm. Unlike properties managed by larger firms, these rentals offer potential benefits that arise from direct interaction with individual homeowners and the idiosyncratic character of their properties. Let’s delve into some of the prominent advantages of choosing private owner house rentals over those run by large companies.

Personal touch: Private homeowners might offer a more personal touch compared to larger property management firms. This could mean more flexibility in terms of lease agreements, move-in/move-out dates or any other limitations and stipulations.

Direct communication: Renters often communicate directly with the property owner, often leading to quicker response times for maintenance requests or other concerns.

Unique properties: These rentals might have distinctive and unique properties that aren’t typically found in larger apartment complexes or managed communities. Think crown molding, brick walls, hardwood floors and more.

Potential for lower costs: Without the overhead of a property management company, private owners might offer better rental prices.

Flexible terms: Some private owners might be open to short-term leases, month-to-month arrangements or other non-traditional rental agreements.

Cons of privately owned rental properties

Now that we’ve covered some of the most appealing aspects of private-owner rentals, let’s dive into some of the downsides and pitfalls that can potentially affect your experience with a private-owner house rental.

Inconsistency: The experience can vary widely from one private owner to another. While some might be highly professional and organized, others may be less so.

Limited amenities: Private rentals might not offer the same amenities that larger complexes or communities do, such as swimming pools, fitness centers or security services.

Maintenance delays: Some private owners might not have the resources or connections to address maintenance issues as promptly as larger management firms.

Lack of formal process: There may be a lack of formal processes in areas like application screening, security deposits and lease agreements, which could lead to potential legal disputes.

Potential for bias: Without the procedures and policies of a larger company, there might be more room for unconscious bias or discrimination in the rental process.

Private-owner house rentals present a compelling blend of advantages and challenges. While their personal touch can provide renters with a tailored experience, the potential inconsistencies and lack of standardized processes can pose challenges.

As with any rental decision, potential tenants should carefully consider the pros and cons before making any decisions, ensuring that their choice aligns with their preferences, needs and expectations for a harmonious living arrangement.

Other considerations when looking at houses for rent

Like most of life’s major decisions, there’s more to consider about private-owner house rentals than just the pros and cons.

Research is key: Due diligence is essential when considering a private owner house rental. Potential renters should research the property, check references and understand the lease terms thoroughly.

Legal protections: Both renters and landlords should be aware of local rental laws and regulations to ensure that they’re both protected. This might include understanding rights related to security deposits, eviction processes and property maintenance.

Contracts: even if renting from a private owner, having a written lease or rental agreement is crucial. This document should clearly outline the terms of the rental, including rent amount, duration of the lease, maintenance responsibilities and any other relevant details.

While there are many advantages to this type of arrangement, potential challenges can arise. As always, thorough research and understanding of the rental agreement are essential for a successful rental experience.

Nuances in legalities between a house and an apartment

Understanding the differences between renting a house and an apartment from a private owner goes beyond just the physical structure; there are also legal nuances to consider. Both situations will involve lease agreements and rights for tenants and landlords, but there are some distinctions to be aware of:

Zoning and land use

Houses might be situated in areas with zoning restrictions that dictate how the property can be used. For instance, certain residential zones might prohibit running a business from home or may have specific parking regulations. On the other hand, apartments are generally in zones designated for multifamily dwellings, which can come with their own set of rules and regulations.

Maintenance and repairs

For houses, the responsibility for external areas like lawns, gardens and driveways often falls on the tenant unless otherwise stipulated in the lease. With apartments, the responsibility for maintaining common areas typically rests with the property management or homeowners association.

Security deposits

Both houses and apartments usually require security deposits to cover wear and tear. However, with houses, there might be additional deposits or fees for landscaping or potential damage to larger outdoor areas.

Utility responsibilities

In apartments, certain utilities like water, trash collection or electricity might be covered by the landlord or the property management, especially if they are shared resources. In contrast, tenants renting a house usually bear the responsibility for all utilities, including water, electricity and garbage.

Liability

Homeowners might have broader liability concerns. For example, suppose a person gets injured on the property, like slipping on an icy driveway. In that case, the responsibility might fall onto the homeowner or the tenant, depending on the terms of the lease. In apartment complexes, the liability for common areas is usually on the property management or owner.

Subleasing and assignments

Lease agreements for houses might be more flexible compared to apartments, which may have stricter guidelines enforced by property management. This isn’t a strict rule, but a general trend given that a private landlord might negotiate these terms.

Pets and modifications

Apartments often have strict rules regarding pets, alterations or additions to the unit. Houses might have more flexibility, but that’s not a given. Still, a house renter might have more latitude to request permissions for larger modifications or to keep larger pets, possibly dodging some breed restrictions in the process.

Is a private-owner house rental right for you?

While the basic principles of landlord-tenant law apply to both houses and apartments, the specific responsibilities, rights and restrictions can differ based on the nature of the property. Renters and landlords need to be clear on these nuances to ensure a smooth rental experience and avoid potential disputes. Navigating the intricacies of real estate rentals requires a nuanced understanding of each available option. Private-owner house rentals offer an alternative to the conventional rental route, underlined by a personalized touch and distinctive property features.

However, as with all choices, potential renters must balance these benefits against possible drawbacks. By staying informed and conducting thorough research, renters can make educated decisions and find a home that aligns seamlessly with their needs.

A native of the northern suburbs of Chicago, Carson made his way to the South to attend Wofford College where he received his BA in English. After working as a copywriter for a couple of boutique marketing agencies in South Carolina, he made the move to Atlanta and quickly joined the Rent. team as a content marketing coordinator. When he’s off the clock, you can find Carson reading in a park, hunting down a great cup of coffee or hanging out with his dogs.

Imagine waking up to the gentle sound of waves, feeling the ocean breeze on your skin, and having breathtaking views right from your own home. If you’re dreaming of owning a piece of paradise in Florida, waterfront properties offer an enticing opportunity to turn that dream into a reality. In this comprehensive guide, we’ll dive into the world of Florida waterfront properties, covering everything you need to know about finding, buying, and enjoying your dream waterfront home.

Enjoying our content? Subscribe to our free weekly newsletter to get real estate market insights, news, and reports straight to your inbox.

1. The Draw of Florida Waterfront Properties

Florida’s coastline boasts some of the most sought-after real estate in the country. From stunning beachfront homes to serene lakefront retreats and scenic riverfront properties, the options are diverse and captivating. Living on the waterfront provides not only a luxurious lifestyle but also a chance to connect with nature and enjoy an array of recreational activities.

2. Types of Waterfront Properties

Florida offers an array of waterfront options, each with its own unique charm:

Beachfront Properties: These properties offer direct access to the sandy shores and spectacular ocean views.

Lakefront Homes: Enjoy serene lake views, fishing, boating, and water-based activities.

Riverfront Residences: Perfect for boating enthusiasts, these homes provide access to navigable rivers and picturesque landscapes.

3. Choosing Your Ideal Location

The key to finding your dream waterfront home lies in selecting the right location. Consider factors like proximity to amenities, quality of schools, safety, and lifestyle preferences. Popular Florida waterfront regions include Miami, Fort Lauderdale, Tampa Bay, and the Gulf Coast. On Zoocasa, you can also filter homes by their school zones to see which school region a property falls under.

4. Navigating the Real Estate Market

The Florida waterfront real estate market can be competitive, so here are some recommended actions to be well prepared:

Work with a Local Realtor: Partner with a real estate agent who specializes in waterfront properties to gain insights into local market trends.

Set a Realistic Budget: Determine your budget and consider additional costs like insurance, property taxes, and maintenance.

Research Zoning Regulations: Understand local regulations regarding construction, shoreline protection, and property usage.

5. Property Inspection and Due Diligence

Before finalizing any purchase, ensure that you:

Inspect the Property: Waterfront homes are exposed to unique weather conditions. Ensure the property is in good condition and not prone to flooding or erosion.

Review Flood Zone Maps: Determine if the property is in a flood zone, which can impact insurance rates.

Understand Ownership Rights: Some waterfront properties come with coastal rights, granting you access to the water.

6. Property Financing and Insurance

Securing financing for waterfront properties might require a specialized approach due to their higher value. Additionally, consider property insurance that covers potential risks associated with waterfront living, such as hurricanes or water damage.

7. Living the Waterfront Lifestyle

Owning a waterfront property offers a unique lifestyle:

Recreation: Enjoy activities like boating, fishing, kayaking, and paddleboarding right from your doorstep.

Entertainment: Host gatherings with stunning waterfront backdrops, whether it’s a beach bonfire or a lakeside barbecue.

Relaxation: Experience tranquillity as you watch sunsets over the water or take leisurely walks along the shore.

Are you looking for a waterfront property? Call us today to connect with an experienced real estate agent in your area!

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

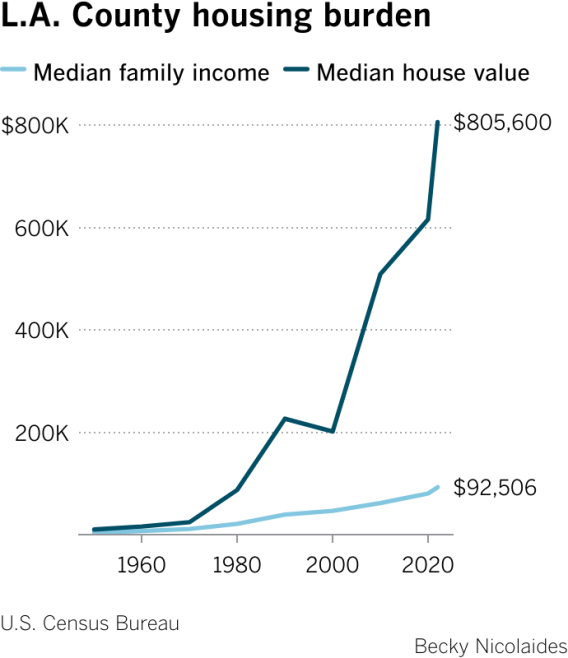

The high cost of housing is driving Southern California’s biggest challenges. Income is not keeping pace with housing costs. It hasn’t for at least two generations, and the problem of unaffordable shelter shows few signs of letting up.

There’s a metric called “housing burden” that lays the situation bare. Over the last 50 years, it tracks the growing, gaping mismatch between income and shelter costs in Los Angeles County.

In 1979, UCLA land experts Leo Grebler and Frank Mittelbach wrote: “As a general, time-honored rule of thumb” house prices in a community “should not exceed 2 to 2½ times the annual income” of its residents.

Within a decade, home prices began to drastically violate this rule. If it were applied today, it would mean a four-person household with the median Los Angeles County income of $98,200 could afford to buy a house that cost $245,500. However, the median home price in the county last month, according to Redfin, was $980,000.

Advertisement

How did things get so unbalanced?

In the 1950s and 1960s, buying a single-family home in Los Angeles was an attainable prospect. The GI Bill and the Federal Housing Authority helped with loans and mortgage dollars (albeit primarily for white families). And home building was on a tear, thanks to the region’s pro-development political climate.

By the 1970s, however, a cascade of factors — local to global — changed the equation.

Housing prices first shot ahead of income in the mid-1970s. Analysts attributed the spike to the first cohort of baby boomers reaching home-buying age, which expanded the pool of buyers and created a seller’s market. The 1973 oil crisis and ensuing inflation pushed buyers to pay up for fear prices would rise even higher. Unrelenting demand thus not only kept pace with prices, it increased them.

Social-demographic factors also factored in. Per capita income doubled from 1966 to 1977, due in part to more women in the workplace. When federal policies struck down gender discrimination in loan and credit decisions, two-income families could qualify for larger mortgage loans, elevating the demand for higher-priced homes.

Advertisement

Then land and building costs climbed, pushing prices even higher. And in 1978, Proposition 13 became law.

The ballot measure slashed property taxes and with them, funding for municipal services. Cities and towns scrambled to recoup the lost revenue. New real estate developments were “money-losers,” as urban planner and former Ventura Mayor William Fulton observed, because property taxes fell so low. Instead, municipalities turned to retail development to generate lucrative sales tax revenue. Prop. 13 thus became a powerful disincentive to build housing.

The rising slow-growth movement put another damper on housing supply. It was pushed by homeowners who resisted adding multifamily housing in single-family neighborhoods or new development in nearby open space.

One study by the California Legislative Analyst’s Office found that by the early 2000s, more than two-thirds of cities and counties in coastal California metro areas had slow-growth policies in place, and that when a community added such a policy, it resulted in a 3% to 5% increase in home prices. Moreover, the historical momentum of R-1 (single family) zoning stymied the construction of multifamily units.

The upshot of all these pressures? From 1980 to 2010 in Los Angeles, the population grew by 31.3% while housing units grew by only 20.6%.

L.A.’s spiraling housing costs paralleled trends in large, global metro regions by the turn of the 21st century, suggesting that forces beyond L.A. were also at work. In the 1990s and early 2000s, the housing bubble was driven by finance structures linked to global markets, inflows of global capital and unregulated banking practices that set off unrestrained and predatory lending and buying frenzies. Even after the 2007-09 banking crisis and Great Recession, home prices in L.A. soon regained traction.

Taking a longer view, economist Robert Shiller traced rising housing costs in the late 1980s and early 2000s across metro areas globally, including L.A. He pinned a good deal of the blame on “irrational exuberance” that motivated uncontrolled buying. The psychological draw of metro areas such as Paris, London, Sydney and L.A. reinforced the belief that land prices would continue to go up and up. Media fed these perceptions. And housing bubbles blew up.

Looking at the housing burden graph, the price surge since 2020 is truly eye-popping. Urban analyst Richard Florida attributes it to pandemic-driven demands for more housing space especially among millennials, a massive shortage of housing overall and, perhaps most disturbingly, the growing competition from large institutional investors who’ve been snapping up homes and apartments in recent years. In 2021, they bought 29% of all single-family homes in California and, with their ability to outbid other buyers, they drive up prices.

Over the last 50 years, L.A.’s housing burden has evolved from challenging to simply unsustainable. The consequences are all around us, in skyrocketing rents, a ubiquitous homelessness crisis, housing overcrowding, rising commuting times to drive-till-you-qualify exurbs, population flows out of California and intensified wealth inequality.

Solutions must come from both the housing and the income side.

Increasing the housing supply is crucial. It must be accompanied by policies that protect individual buyers from corporate competitors, ensure the ongoing production of affordable housing, and guard against gentrification.

Even more importantly, wages and salaries must climb considerably to make housing affordable again. The major employers in our region — from the movie studios to hotels to hospitals and logistics firms — must take a long, hard look at the housing burden graph and see in it their own role in widening the gap. The Writers Guild and actors’ strikes, the Unite Here Local 11 hospitality industry strike and the strike vote last week by Kaiser Permanente healthcare workers speak directly to L.A.’s housing burden.

The struggle to match income to cost of shelter is an inescapable fact of L.A. life that demands swift, conscientious redress.

Becky Nicolaides is a research affiliate at the Huntington-USC Institute on California and the West, and author of “The New Suburbia: How Diversity Remade Suburban Life in Los Angeles After 1945,” forthcoming from Oxford University Press. The data set collected for the book, a granular look at demographics from 1950 to 2010, will be published online by the USC libraries next year.

Fed’s inflation fight tightens the U.S. housing supply and makes home buying even more difficult

Conventional wisdom dictates that U.S. inflation will continue to decline as the Federal Reserve keeps interest rates high. This action, which makes loans more expensive for businesses and consumers, should lead to less spending, less consumption and higher unemployment.

Or at least that’s Econ 101. Yet both consumers and investors have acclimated to the current market environment. Moreover the key driver of inflation — housing — cannot be adequately contained through the Federal Reserve’s usual tactics.

In fact, the Fed’s policies have created a Catch-22 in the housing market by creating “golden handcuffs.” Instead of easing consumer demand, the Fed’s actions unintentionally restricted U.S. housing supply, resulting in a stalemate between home buyers and sellers. Homeowners who locked into historically low mortgage rates before and during the pandemic are now reluctant to sell, which in turn is increasing the likelihood of persistent higher inflation.

The case for this condition to persist , which the market is mostly failing to consider, continues to grow stronger as the odds of a recession fade. This should be an alarm bell and a potential opportunity for investors to redeploy at least part of their capital into hard assets to serve as a hedge against inflation risk.

The recession that never was

Many economists have predicted that a recession would hit the U.S. Their reasoning was sound: aggressive monetary action by the Federal Reserve, investor dissatisfaction with inflation, loss of consumer confidence and reductions in home asking prices — all points that were hard to argue against.

Yet most of the key ingredients needed for a recession have not materialized. Investors have acclimated to inflation, consumer confidence is growing and the housing market has, by and large, entered a period of stalemate where prices remain high due to lack of supply.

In fact, the only relevant argument in the recession camp that remains is the Fed continuing its aggressive posture against inflation — now considered the fastest monetary policy tightening cycle in more than 40 years. Such action continues to lead many to speculate that recession is imminent, and the only questions left to answer are “when,” and “how deep it will be?”

Housing prices obey the laws of supply and demand

Housing is perhaps the most consequential category that makes up the Consumer Price Index (CPI), which markets track every month as a core measure of inflation.

The undersupply of housing in the U.S. is grounded in years of underbuilding and is not the result of a single federal policy, war, or external event. If anything, the power to create more housing supply rests with state and local governments, which often require working through a patchwork quilt of differing zoning and land-use regulations.

The high estimate of the country’s current housing shortage is pegged at about 7.3 million units, while the most conservative estimate shows it to be about 1.7 million. While the true shortage is most likely somewhere inbetween, the bottom line is that the United States faces a textbook housing shortage that cannot be solved overnight. Worse, the Fed’s current policies are making the prospect of home ownership even more difficult.

Nobody wants to move and reset their loans at much higher rates.

Central bank measures designed to clamp down on inflation by making borrowing more expensive (which theoretically should drive down the costs of homes), are having the opposite effect. This is because homeowners, who locked in historically low mortgage rates before and during the pandemic, are now reluctant to sell their home.

Simply put, nobody wants to move and reset their loans at much higher rates. Would-be sellers are therefore sitting on the sidelines, which has unintentionally created an even greater shortage in supply. Meanwhile, potential buyers, who cannot afford higher mortgage rates, are incentivized to rent instead.

To end this stalemate, the Fed would need to start cutting interest rates, which it has stated is unlikely this year. But if inflation is being driven by the cost of housing, as demonstrated in the Consumer Price Index, more attempts to tame inflation via rate hikes suggests homeowners will only become more entrenched as supply dwindles further As the labor market continues to prove surprisingly resilient, homeowners, and by extension everyday consumers, don’t seem to mind waiting it out.

Read: Nouriel Roubini says a return to 2% inflation is ‘mission impossible’

Also: Most long-term investors can ignore the Federal Reserve’s latest move

The case for hard assets

Seasoned investors know that during times of rising interest rates, restrictive credit and prolonged inflation, more investments flow into “hard” asset classes such as real estate. This hedging strategy is used almost like an insurance policy by investors to preserve capital from the depreciating effects of inflation. And according to research, it works. For example, a Stanford University study found that residential real estate is historically an investment haven during inflationary periods. Even during the inflation of the 1970s, home prices increased relative to the size of the economy. This is because housing is typically tied to consumer prices and rises with inflation.

With housing assets so closely tied to inflation, as well as to the laws of supply and demand, investments in this hard asset class deserve due consideration. Strong economic growth, coupled with the one-two punch of resilient consumer spending and near record-low unemployment, is good news. It also means the Fed won’t be lowering rates soon. Housing will remain a key driver of inflation, and future rate-hikes will further entrench homeowners and push more would-be buyers into renting.

To achieve a return to 2% inflation, U.S. policymakers would be wise to work with state and local governments to incentivize development, which would drive down the greatest expense for most Americans. But even with decisive action, fixing the fundamental housing shortage that is responsible for sustaining stubbornly persistent inflation will be a longer process than most investors realize.

David Piscatelli focuses on research, economic analysis and strategy at Avenue One, a property technology service platform and marketplace for institutional owners, buyers and sellers of residential homes. Views of the writer do not necessarily reflect the views of Avenue One.

More: Meet the brave Americans buying and selling their homes, despite stubbornly high interest rates

Plus: 9 ways home buyers can stretch their dollars even though mortgage rates are high

-David Piscatelli

This content was created by MarketWatch, which is operated by Dow Jones & Co. MarketWatch is published independently from Dow Jones Newswires and The Wall Street Journal.

The U.S. housing market is short by at least 6.5 million homes. After more than a decade of under-building relative to population growth, there are simply not enough affordable entry-level and first-time move-up options available for buyers. Renters are finding themselves priced out of areas within a reasonable commuting distance to work.

The scarcity of housing has driven home prices and rents prices to an all-time high and pushed affordability to a multi-decade low. Over the next decade, there will be more than two million adults added annually to the U.S. population, due to a combination of aging and immigration. This shift will drive a voracious need for more housing, especially among entry-level and first-time move-up homes at lower price points given structural affordability challenges.

Reasons for the housing shortage plentiful

Housing has been materially unbuilt for the past 15 years. Most production builders have focused on ever larger and more expensive new homes, and relatively few new homes have been built that cater to lower-income households and entry-level buyers, especially in high-cost coastal markets.

Most recently, rising interest rates have intensified the fight for housing. From February 2011 to April 2022, mortgage rates never rose above 5%, making the cost to borrow money and buy a home very cheap. However, since 2022, there has been a rapid rise in rates that has created a “lock-in effect” and stalled many families who would have otherwise considered moving. Homeowners who “locked-in” a mortgage rate of 3-4% during the pandemic are unwilling to buy a home at a 7%+ on a new mortgage, which means even fewer homes are going on the market as existing homeowners choose to stay put.

For those hoping to buy a home for the first time, the rise in rates means that monthly payments are effectively double what they would have been a year ago, a reality that has priced many people out of buying. Couple that with rising costs of home insurance and the general price inflation, and there is a massive housing affordability problem facing the majority of the country.

A need for alternatives

This persistent housing shortage has generated a pressing need for alternatives that can bridge the gap between demand and supply, while accounting for a limited availability of land in top areas.

Enter the Accessory Dwelling Unit, commonly known as an ADU, or more informally called an in-law suite, granny flat or backyard home. ADUs are small, self-sufficient structures that usually have one to three bedrooms, a private entrance, and all the amenities that a resident would require including kitchens and bathrooms. ADUs are one of the most effective ways to add density and rental properties in a higher cost market. These generally detached structures can be built in less than a year and cost far less to build than primary homes. Depending on where you live, there are also various state-run programs such as the CalHFA ADU Grant in California that can bring down building costs tremendously.

For homeowners, ADUs offer an opportunity to provide affordable housing on the rental market or house relatives that would otherwise be unable to afford the neighborhood. These structures can generate rental income to offset rising mortgage payments, and create more long-term rental supply, ultimately lowering the average rental cost for tenants. For local governments, ADUs can increase the number of tenants in areas where high-rise dwellings are not a desirable option. ADUs also offer a compelling option for multi-generational living, which can be a tremendous help with families that want to reduce burdens of childcare and senior care.

Changing policies good for ADUs

Fortunately, we are seeing many government authorities focusing on changing housing policies and zoning codes to make ADUs a more actionable solution. It’s a rare example of government housing policies driving the private market to solve a critical problem. For example, California’s changes in laws and regulations have made ADUs much easier to build. The momentum from these regulations has resulted in a large increase in ADU construction activity: permits for ADUs in California have increased nearly 22x from around 1,100 in 2015 to nearly 24,000 in 2022 and roughly 68,000 ADUs were built across California between 2017-2021. As a result, there are a large number of new housing units that have been added to high-cost locations where people hope to live and work.

Nationwide, many local and state governments are starting to follow the California example. Washington, Oregon, Florida, and Colorado, to name a few states, are starting to make ADUs a more prevalent part of solving the housing affordability issue. Ultimately, ADUs alone won’t solve decades of housing issues. But they can close the gap between the number of people looking for affordable housing and the number of homes available for rent or purchase.

Sean Roberts is CEO of Villa, an ADU builder in California.

This column does not necessarily reflect the opinion of RealTrends’ editorial department and its owners.

To contact the author of this story: Sean Roberts at [email protected]

To contact the editor responsible for this story: Tracey Velt at [email protected]

If you’ve found yourself wondering, ‘What exactly is a twin home, and could it be right for me?’ you’re in the right place. Among the various housing options available, one term that frequently piques interest is the ‘twin home.’ But what does it mean exactly? Is it a duplex, a townhome, or something entirely different?

In this Redfin article, we’ll explain everything you need to know about twin homes. We’ll cover the unique features of this home type, discuss the advantages and drawbacks, and help you determine if it’s the right housing choice for you. So whether you’re looking at homes for sale in Columbus or considering renting in Houston, keep reading to learn all about twin homes.

What is a twin home?

A twin home is also known as a semi-detached home. It’s a residential property with two separate living units, each having its own entrance and private space, housed within one building. The units are usually mirror images of each other in terms of layout and design. Unlike a traditional single-family home, where the dwelling stands alone, twin homes share a common wall along one side.

Twin home vs. duplex: What is the difference?

While twin homes and duplexes may seem similar at first glance due to their shared wall structure, they possess distinct differences that set them apart. A duplex generally refers to a building divided into two separate units, often stacked one on top of the other or side by side. These units can have different layouts, sizes, and designs, whereas twin homes typically mirror each other in layout and design, offering a sense of symmetry and balance. In a twin home, the design intention is to create a harmonious look, as if two identical homes were joined together.

“It’s critical to know if you’re buying a duplex or a twin home because of the difference in how the land is divided,” says Mark Shattuck of Dream Home Studio. “Duplexes are two attached homes with separate ownership, yet the land that both residences sit on is co-owned and co-maintained by both duplex owners. This makes duplexes multi-family properties. However, twin homes are classified as two attached single-family homes (and only two, as opposed to townhomes) because twin homes have separate land ownership, both split along a common property line and shared wall. Nothing looks visually different between duplexes and twin homes, but the land ownership, rights, and classification are very different.”

Pros and cons of living in a twin home

Pros:

Affordability: Twin homes often offer a more affordable housing option compared to single-family homes, making them appealing to first-time homebuyers or those looking for cost-effective alternatives.

Community feel: Living in close proximity to another household can foster a sense of community and provide an added layer of security with neighbors looking out for one another.

Efficient use of land: Twin homes are an efficient use of urban and suburban land, which can lead to shorter driveways, smaller yards, and more sustainable development practices.

Maintenance: With a shared wall, there might be less exterior maintenance compared to standalone homes, and homeowners’ association fees may cover some maintenance tasks.

Potential for Rental Income: One unit of a twin home can be rented out, providing homeowners with an opportunity for passive income if they choose to live in the other unit.

Cons:

Noise: Shared walls can sometimes lead to noise transfer between units, which might impact residents’ comfort and privacy.

Limited customization: While twin homes offer uniformity, this can limit the extent of customization options that homeowners might have compared to single-family homes.

Space constraints: Twin homes could have less outdoor space compared to single-family homes, limiting gardening and landscaping opportunities. Some twin homes may also have limited parking spaces or shared driveways, which can become a logistical challenge, especially if there are multiple vehicles involved.

Are twin homes considered single-family homes?

Twin homes often occupy a gray area between single-family homes and multi-family dwellings. Twin homes have private entrances and separate living spaces, much like single-family homes. However, their distinguishing features are the shared wall and the two units housed within one building. Local regulations and zoning ordinances can vary, and the classification of twin homes might vary depending on how they are legally defined within a specific jurisdiction.

A final note on twin homes

Twin homes offer a unique middle ground between single-family and multi-family homes, providing homeowners with the benefits of both privacy and community living. As the housing market continues to diversify, twin homes stand as a viable option for those seeking affordability, a sense of community, and a distinctive living arrangement.

With mortgage rates near 20-year highs and relatively few homes listed for sale, the Atlanta-areahousing market in August reached something of a precarious — and possibly temporary — plateau with prices rising, but slowly.

The median price of a home sold last month was $404,000, according to data released this week by the Georgia Multiple Listing Service.

That was just 1% higher than in July and only 2.3% above the median price of a home sold a year earlier, compared to double-digit increases for previous years, said John Ryan, chief marketing officer of the Georgia MLS.

The dampener on price hikes has been mortgage rates, pushed higher by the Federal Reserve’s campaign to tame inflation by raising borrowing costs.

When that changes, the market will see a flood of buying, predicted broker Kristen Jones, owner of Re/Max Around Atlanta. “Eventually, the Fed will stop, and mortgage rates will come down. At that point, we expect the floodgates to open.”

But right now, those gates are high and they’re holding.

The average rate for a 30-year mortgage was 7.18% at the end of August, the highest it has been since March 2002, according to the Federal Home Loan Mortgage Corp., which insures loans in secondary markets.

Many who do buy now are betting that can’t continue, Jones said. “Buyers crossing their fingers that they can refinance in the next few years.”

Higher rates not only make monthly payments dramatically higher for new buyers, they freeze many potential sellers who don’t want to trade their current low rates for a high rate if they move, Jones said. “Sellers are not motivated to list. About 61% of all outstanding mortgages have an interest rate below 4%.”

With so many potential sellers standing pat, inventory — that is, the number of homes listed for sale — was 12.1% lower in August than it was a year earlier, according to the Georgia MLS.

Fewer than 11,000 homes in the region were listed for sale, which represents barely two months of sales. In a healthy, balanced market, the inventory level should represent at least six months of sales.

Part of the problem is an overall housing shortage in metro Atlanta.

After years of exuberant overbuilding, construction came to a virtual halt during the 2007-09 recession and has never regained its previous pace despite the region’s population growth. Since 2012, the shortage — and the flow of millennials into the market — has kept home prices rising, which increasingly made affordability an issue.

Then came the pandemic, which roiled expectations about commuting and home offices, and spurred federal efforts to protect household finances by driving interest rates down to historic lows and pumping money into the economy.

The rebound from the pandemic has meant rapid job growth, along with higher pay for many.

But at least until recently, Atlanta home price gains far outpaced income growth. That made down-payments for homes a challenge, shoving many potential buyers out of the market.

Demand for housing has spurred construction, most of it well outside the city of Atlanta. Even so, high land prices and various zoning restrictions have made construction for first-time buyers rare.

In Alpharetta, Blue River Lifestyle Communities this week announced a 24-unit development that includes both townhomes and single-family houses. The homes will be listed at $1.3 million or more.

Nearly 80% of baby boomers own a home, but only about half of the nation’s millennials do, according to national brokerage Redfin. About 1 of every 5 millennials say they don’t think they’ll ever be able to afford one, according to a Redfin poll.

But at least renters have also seen a moderation in the market. Metro Atlanta’s median rent is $2,127 a month, according to Rent.com, which tracks rentals nationally. That is virtually unchanged from a year ago, the group said.

And rate hikes are also biting homeowners who stay put.

The Fed’s campaign ripples through to virtually all borrowing, from car loans to credit cards. So even homeowners with low-rate mortgages will pay more than before if they want to tap their mortgage for a loan, said Andy Walden, vice president of research at Black Knight, a real estate analysis firm recently purchased by Atlanta-based Intercontinental Exchange.

Nationally, mortgage holders withdrew $39 billion in equity from their homes in the second quarter of this year, which is only about half as much as before interest rates started to climb, he said. “Rising rates are having a clear impact on how — and how much — equity mortgage holders are willing to withdraw from their homes.”

Metro Atlanta housing market, August

Median sales price: $404,000

Number of sales: 5,299

Number of homes listed for sale: 10,927

Price compared to year earlier: up 2.3%

Sales compared to year earlier: down 15.8%

Price compared to January 2020: up 50%

Average rate, 30-year, fixed-rate mortgage

Aug. 31, 2023: 7.18%

Aug. 31, 2022: 5.66%

Aug. 31, 2021: 2.87%

Aug. 31, 2020: 2.91%

High since 1999: 8.64% (May 2000)

Last time above 7%: March 29, 2002

Source: Georgia Multiple Listing Service, S&P Case Shiller Index, Federal Home Loan Mortgage Corp.

Though most individuals are familiar home insurance, not all home owners are knowledgeable about title insurance. However, this form of insurance can be very helpful in times of need. To determine how it could be of assistance to you, check out our breakdown of title insurance, its benefits, and some common issues that individuals can face in regards to a title.

What is Title Insurance?

In a nutshell, title insurance covers events that may have happened before the date a title was issued to a new party, and it does not cover events that happen after issuance. In other words, it protects the new owner from any missteps of the previous owner.

Before a new title insurance policy is issued, an insurer will do a title search. This search tends to reveal a number of possible issues:

incorrect names on the title

improper vesting