The VA home loan: Unbeatable benefits for veterans

For many who qualify, VA home loans are some of the best mortgages available.

Verify your VA loan eligibility. Start here

Backed by the U.S. Department of Veterans Affairs, VA loans are designed to help active-duty military personnel, veterans and certain other groups become homeowners at an affordable cost.

The VA loan asks for no down payment, requires no mortgage insurance, and has lenient rules about qualifying, among many other advantages.

Here’s everything you need to know about qualifying for and using a VA loan.

In this article (Skip to…)

Top 10 VA loan benefits

1. No down payment on a VA loan

Most home loan programs require you to make at least a small down payment to buy a home. The VA home loan is an exception.

Verify your VA loan eligibility. Start here

Rather than paying 5%, 10%, 20% or more of the home’s purchase price upfront in cash, with a VA loan you can finance up to 100% of the purchase price.

The VA loan is a true no-money-down home mortgage opportunity.

2. No mortgage insurance for VA loans

Typically, lenders require you to pay for mortgage insurance if you make a down payment that’s less than 20%.

This insurance — which is known as private mortgage insurance (PMI) for a conventional loan and a mortgage insurance premium (MIP) for an FHA loan — would protect the lender if you defaulted on your loan.

VA loans require neither a down payment nor mortgage insurance. That makes a VA-backed mortgage very affordable upfront and over time.

3. VA loans have a government guarantee

There’s a reason why the VA loan comes with such favorable terms.

The federal government guarantees these loans — meaning a portion of the loan amount will be repaid to the lender even if you’re unable to make monthly payments for whatever reason.

This guarantee encourages and enables private lenders to offer VA loans with exceptionally attractive terms.

4. You can shop for the best VA loan rates

VA loans are neither originated nor funded by the VA. They are not direct loans from the government. Furthermore, mortgage rates for VA loans are not set by the VA itself.

Instead, VA loans are offered by U.S. banks, savings-and-loans institutions, credit unions, and mortgage lenders — each of which sets its own VA loan rates and fees.

This means you can shop around and compare loan offers and still choose the VA loan that works best for your budget.

5. VA loans don’t allow a prepayment penalty

A VA loan won’t restrict your right to sell the property partway through your loan term.

There’s no prepayment penalty or early-exit fee no matter within what time frame you decide to sell your home.

Furthermore, there are no restrictions regarding a refinance of your VA loan.

You can refinance your existing VA loan into another VA loan via the agency’s Interest Rate Reduction Refinance Loan (IRRRL) program, or switch into a non-VA loan at any time.

6. VA mortgages come in many varieties

A VA loan can have a fixed rate or an adjustable rate. In addition, you can use a VA loan to buy a house, condo, new-built home, manufactured home, duplex, or other types of properties.

Or, it can be used for refinancing your existing mortgage, making repairs or improvements to your home, or making your home more energy-efficient.

The choice is yours. A VA-approved lender can help you decide.

Verify your VA loan eligibility. Start here

7. It’s easier to qualify for VA loans

Like all mortgage types, VA loans require specific documentation, an acceptable credit history, and sufficient income to make your monthly payments.

But, compared to other loan programs, VA loan guidelines tend to be more flexible. This is made possible because of the VA loan guarantee.

The Department of Veterans Affairs genuinely wants to make the loan process easier for military members, veterans, and qualifying military spouses to buy or refinance a home.

8. VA loan closing costs are lower

The VA limits the closing costs lenders can charge to VA loan applicants. This is another way that a VA loan can be more affordable than other types of loans.

Money saved on closing costs can be used for furniture, moving costs, home improvements, or anything else.

9. The VA offers funding fee flexibility

VA loans require a “funding fee,” an upfront cost based on your loan amount, your type of eligible service, your down payment size, and other factors.

Funding fees don’t need to be paid in cash, though. The VA allows the fee to be financed with the loan, so nothing is due at closing.

And, not all VA borrowers will pay it. VA funding fees are normally waived for veterans who receive VA disability compensation and for unmarried surviving spouses of veterans who died in service or as a result of a service-connected disability.

10. VA loans are assumable

Most VA loans are “assumable,” which means you can transfer your VA loan to a future home buyer if that person is also VA-eligible.

Assumable loans can be a huge benefit when you sell your home — especially in a rising mortgage rate environment.

If your home loan has today’s low rate and market rates rise in the future, the assumption features of your VA become even more valuable.

VA loan rates

The VA loan is viewed as one of the lowest-risk mortgage types available on the market.

Verify your VA loan eligibility. Start here

This safety allows banks to lend to veteran borrowers at lower interest rates.

Today’s VA loan rates*

Loan Type

Current Mortgage Rate

VA 30-year FRM

% (% APR)

Conventional 30-year FRM

% (% APR)

VA 15-year FRM

% (% APR)

Conventional 15-year FRM

% (% APR)

*Current rates provided daily by partners of the Mortgage Reports. See our loan assumptions here.

VA rates are more than 25 basis points (0.25%) lower than conventional rates on average, according to data collected by mortgage software company Ellie Mae.

Most loan programs require higher down payment and credit scores than the VA home loan. In the open market, a VA loan should carry a higher rate due to more lenient lending guidelines and higher perceived risk.

Yet the result of the Veterans Affairs efforts to keep veterans in their homes means lower risk for banks and lower borrowing costs for eligible veterans.

VA mortgage calculator

Eligibility

Am I eligible for a VA home loan?

Contrary to popular belief, VA loans are available not only to veterans, but also to other classes of military members.

Find and lock a low VA loan rate today. Start here

The list of eligible VA borrowers includes:

Active-duty service members

Members of the National Guard

Reservists

Surviving spouses of veterans

Cadets at the U.S. Military, Air Force or Coast Guard Academy

Midshipmen at the U.S. Naval Academy

Officers at the National Oceanic & Atmospheric Administration.

A minimum term of service is typically required.

Minimum service required for a VA mortgage

VA home loans are available to active-duty service members, veterans (unless dishonorably discharged), and in some cases, surviving family members.

To be eligible, you need to meet one of these service requirements:

You’ve served 181 days of active duty during peacetime

You’ve served 90 days of active duty during wartime

You’ve served six years in the Reserves or National Guard

Your spouse was killed in the line of duty and you have not remarried

Your eligibility for the VA home loan program never expires.

Veterans who earned their VA entitlement long ago are still using their benefit to buy homes.

The VA loan Certificate of Eligibility (COE)

What is a COE?

In order to show a mortgage company you are VA-eligible, you’ll need a Certificate of Eligibility (COE). Your lender can acquire one for you online, usually in a matter of seconds.

Verify your VA home loan eligibility. Start here

How to get your COE (Certificate of Eligibility)

Getting a Certificate of Eligibility (COE) is very easy in most cases. Simply have your lender order the COE through the VA’s automated system. Any VA-approved lender can do this.

Alternatively, you can order your certificate yourself through the VA benefits portal.

If the online system is unable to issue your COE, you’ll need to provide your DD-214 form to your lender or the VA.

Does a COE mean you are guaranteed a VA loan?

No, having a Certificate of Eligibility (COE) doesn’t guarantee a VA loan approval.

Your COE shows the lender you’re eligible for a VA loan, but no one is guaranteed VA loan approval.

You must still qualify for the loan based on VA mortgage guidelines. The guarantee part of the VA loan refers to the VA’s promise to the lender of repayment if the borrower defaults.

Qualifying for a VA mortgage

VA loan eligibility vs. qualification

Being eligible for VA home loan benefits based on your military status or affiliation doesn’t necessarily mean you’ll qualify for a VA loan.

You still have to qualify for a VA mortgage based on your credit, debt, and income.

Verify your VA loan eligibility. Start here

Minimum credit score for a VA loan

The VA has established no minimum credit score for a VA mortgage.

However, many VA mortgage lenders require minimum FICO scores of 620 or higher — so apply with many lenders if your credit score might be an issue.

Even VA lenders that allow lower credit scores don’t accept subprime credit.

VA underwriting guidelines state that applicants must have paid their obligations on time for at least the most recent 12 months to be considered satisfactory credit risks.

In addition, the VA usually requires a two-year waiting period following a Chapter 7 bankruptcy or foreclosure before it will insure a loan.

Borrowers in Chapter 13 must have made at least 12 on-time payments and secure the approval of the bankruptcy court.

Verify your VA loan home buying eligibility. Start here

VA loan debt-to-income ratios

The relationship of your debts and your income is called your debt-to-income ratio, or DTI.

VA underwriters divide your monthly debts (car payments, credit cards, and other accounts, plus your proposed housing expense) by your gross (before-tax) income to come up with your debt-to-income ratio.

For instance:

If your gross income is $4,000 per month

And your total monthly debt is $1,500 (including the new mortgage, property taxes and homeowners insurance, plus other debt payments)

Then your DTI is 37.5% (1500/4000=0.375)

A DTI over 41% means the lender has to apply additional formulas to see if you qualify under residual income guidelines.

VA residual income rules

VA underwriters perform additional calculations that can affect your mortgage approval.

Factoring in your estimated monthly utilities, your estimated taxes on income, and the area of the country in which you live, the VA arrives at a figure which represents your “true” costs of living.

It then subtracts that figure from your income to find your residual income (e.g. your money “left over” each month).

Think of the residual income calculation as a real-world simulation of your living expenses.

It is the VA’s best effort to ensure that military families have a stress-free homeownership experience.

Here is an example of how residual income works, assuming a family of four which is purchasing a 2,000 square-foot home on a $5,000 monthly income.

Future house payment, plus other debt payments: $2,500

Monthly estimated income taxes: $1,000

Monthly estimated utilities at $0.14 per square foot: $280

This leaves a residual income calculation of $1,220.

Now, compare that residual income to for a family of four:

Northeast Region: $1,025

Midwest Region: $1,003

South Region: $1,003

West Region: $1,117

The borrower in our example exceeds VA’s residual income standards in all parts of the country.

Therefore, despite the borrower’s debt-to-income ratio of 50%, the borrower could get approved for a VA loan.

Verify your VA loan eligibility. Start here

Qualifying for a VA loan with part-time income

You can qualify for this type of financing even if you have a part-time job or multiple jobs.

You must show a 2-year history of making consistent part-time income, and stability in the number of hours worked. The lender will make sure any income received appears stable. See our complete guide to getting a mortgage when you’re self-employed or work part-time.

VA funding fees and loan limits

About the VA funding fee

The VA charges an upfront fee to defray the costs of the program and make it sustainable for the future.

Veterans pay a lump sum that varies depending on the loan purpose and down payment amount.

The fee is normally wrapped into the loan. It does not add to the cash needed to close the loan.

Find out if you qualify for a VA loan. Start here

VA home purchase funding fees

Type of Military Service

Down Payment

Fee for First-Time Use

Fee for Subsequent Use

Active Duty, Reserves, and National Guard

None

2.3%

3.6%

5% or more

1.65%

1.65%

10% or more

1.4%

1.4%

VA cash-out refinance funding fees

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

2.3%

3.6%

VA streamline refinances (IRRRL) & assumptions

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

0.5%

0.5%

Manufactured home loans not permanently affixed

Type of Military Service

Fee for First-Time Use

Fee for Subsequent Uses

Active Duty, Reserves, and National Guard

1.0%

1.0%

VA loan limits in 2024

VA loan limits have been repealed, thanks to the Blue Water Navy Vietnam Veterans Act of 2019.

There is no maximum amount for which a home buyer can receive a VA loan, at least as far as the VA is concerned.

However, private lenders may set their own limits. So check with your lender if you are looking for a VA loan above local conforming loan limits.

Verify your VA loan eligibility. Start here

Eligible property types

Houses you can buy with a VA loan

VA mortgages are flexible about what types of property you can and can’t purchase. A VA loan can be used to buy a:

Detached house

Condo

New-built home

Manufactured home

Duplex, triplex or four-unit property

Find out if you qualify for a VA loan. Start here

You can also use a VA mortgage to refinance an existing loan for any of those types of properties.

VA loans and second homes

Federal regulations limit loans guaranteed by the Department of Veterans Affairs to “primary residences” only.

However, “primary residence” is defined as the home in which you live “most of the year.”

Therefore, if you own an out-of-state residence in which you live for more than six months of the year, this other home, whether it’s your vacation home or retirement property, becomes your official “primary residence.”

For this reason, VA loans are popular among aging military borrowers.

Buying a multi-unit home with a VA loan

VA loans allow you to buy a duplex, triplex, or four-plex with 100% financing. You must live in one of the units.

Buying a home with more than one unit can be challenging.

Mortgage lenders consider these properties riskier to finance than traditional, single-family residences, so you’ll need to be a stronger borrower.

VA underwriters must make sure you will have enough emergency savings, or cash reserves, after closing on your house. That’s to ensure you’ll have money to pay your mortgage even if a tenant fails to pay rent or moves out.

The minimum cash reserves needed after closing is six months of mortgage payments (covering principal, interest, taxes, and insurance – PITI).

Your lender will also want to know about previous landlord experience you’ve had, or any experience with property maintenance or renting.

If you don’t have any, you may be able to sidestep that issue by hiring a property management company. But that’s up to the individual lender.

Your lender will look at the income (or potential income) of the rental units, using either existing rental agreements or an appraiser’s opinion of what the units should fetch.

They’ll usually take 75% of that amount to offset your mortgage payment when calculating your monthly expenses.

VA loans and rental properties

You cannot use a VA loan to buy a rental property. You can, however, use a VA loan to refinance an existing rental home you once occupied as a primary home.

For home purchases, in order to obtain a VA loan, you must certify that you intend to occupy the home as your principal residence.

If the property is a duplex, triplex, or four-unit apartment building, you must occupy one of the units yourself. Then you can rent out the other units.

The exception to this rule is the VA’s Interest Rate Reduction Refinance Loan (IRRRL).

This loan, also known as the VA Streamline Refinance, can be used for refinancing an existing VA loan on a home where you currently live or where you used to live, but no longer do.

Check your VA IRRRL eligibility. Start here

Buying a condo with a VA loan

The VA maintains a list of approved condo projects within which you may purchase a unit with a VA loan.

At VA’s website, you can search for the thousands of approved condominium complexes across the U.S.

If you are VA-eligible and in the market for a condo, make sure the unit you’re interested in is approved.

As a buyer, you are probably not able to get the complex VA-approved. That’s up to the management company or homeowner’s association.

If a condo you like is not approved, you must use other financing like an FHA or conventional loan or find another property.

Note that the condo must meet FHA or conventional guidelines if you want to use those types of financing.

Veteran mortgage relief with the VA loan

The U.S. Department of Veterans Affairs, or VA, provides home retention assistance. The VA intervenes when a veteran is having trouble making home loan payments.

The VA works with loan servicers to offer loan options to the veteran, other than foreclosure.

Find out if you qualify for a VA loan. Start here

In fiscal year 2019, the VA made over 400,000 contact actions to reach borrowers and loan servicers. The intent was to work out a mutually agreeable repayment option for both parties.

More than 100,000 veteran homeowners avoided foreclosure in 2019 alone thanks to this effort.

The initiative has saved the taxpayer an estimated $2.6 billion. More importantly, vast numbers of veterans and military families got another chance at homeownership.

When NOT to use a VA loan

If you have good credit and 20% down

A primary advantage to VA home loans is the lack of mortgage insurance.

However, the VA guarantee does not come free of charge. Borrowers pay an upfront funding fee, which they usually choose to add to their loan amount.

The fee ranges from 1.4% to 3.6%, depending on the down payment percentage and whether the home buyer has previously used his or her VA mortgage eligibility. The most common fee is 2.3%.

Find out if you qualify for a VA loan. Start here

On a $200,000 purchase, a 2.3% fee equals $4,600.

However, buyers who choose a conventional mortgage and put 20% down get to avoid mortgage insurance and the upfront fee. For these military home buyers, the VA funding fee might be an unnecessary expense.

The exception: Mortgage applicants whose credit rating or income meets VA guidelines but not those of conventional mortgages may still opt for VA.

If you’re on the “CAIVRS” list

To qualify for a VA loan, you must prove you have made good on previous government-backed debts and that you have paid taxes.

The Credit Alert Verification Reporting System, or “CAIVRS,” is a database of consumers who have defaulted on government obligations. These individuals are not eligible for the VA home loan program.

If you have a non-veteran co-borrower

Veterans often apply to buy a home with a non-veteran who is not their spouse.

This is okay. However, it might not be their best choice.

As the veteran, your income must cover your half of the loan payment. The non-veteran’s income cannot be used to compensate for the veteran’s insufficient income.

Plus, when a non-veteran owns half the loan, the VA guarantees only half that amount. The lender will require a 12.5% down payment for the non-guaranteed portion.

The Conventional 97 mortgage, on the other hand, allows down payments as low as 3%.

Another low-down-payment mortgage option is the FHA home loan, for which 3.5% down is acceptable.

The USDA home loan also requires zero down payment and offers similar rates to VA loans. However, the property must be within USDA-eligible areas.

If you plan to borrow with a non-veteran, one of these loan types might be your better choice.

Explore your mortgage options. Start here

If you apply with a credit-challenged spouse

In states with community property laws, VA lenders must consider the credit rating and financial obligations of your spouse. This rule applies even if he or she will not be on the home’s title or even on the mortgage.

Such states are as follows.

Arizona

California

Idaho

Louisiana

Nevada

New Mexico

Texas

Washington

Wisconsin

A spouse with less-than-perfect credit or who owes alimony, child support, or other maintenance can make your VA approval more challenging.

Apply for a conventional loan if you qualify for the mortgage by yourself. The spouse’s financial history and status need not be considered if he or she is not on the loan application.

Verify your VA loan home buying eligibility. Start here

If you want to buy a vacation home or investment property

The purpose of VA financing is to help veterans and active-duty service members buy and live in their own home. This loan is not meant to build real estate portfolios.

These loans are for primary residences only, so if you want a ski cabin or rental, you’ll have to get a conventional loan.

If you want to purchase a high-end home

Starting January 2020, there are no limits to the size of mortgage a lender can approve.

However, lenders may establish their own limits for VA loans, so check with your lender before applying for a large VA loan.

Spouses and the VA mortgage program

What spouses are eligible for a VA loan?

What if the service member passes away before he or she uses the benefit? Eligibility passes to an unremarried spouse, in many cases.

Find and lock a low VA loan rate today. Start here

For the surviving spouse to be eligible, the deceased service member must have:

Died in the line of duty

Passed away as a result of a service-connected disability

Been missing in action, or a prisoner of war, for at least 90 days

Been a totally disabled veteran for at least 10 years prior to death, and died from any cause

Also eligible are remarried spouses who married after the age of 57, on or after December 16, 2003.

In these cases, the surviving spouse can use VA loan eligibility to buy a home with zero down payment, just as the veteran would have.

VA loan benefits for surviving spouses

Surviving spouses have an additional VA loan benefit, however. They are exempt from the VA funding fee. As a result, their loan balance and monthly payment will be lower.

Surviving spouses are also eligible for a VA streamline refinance when they meet the following guidelines.

The surviving spouse was married to the veteran at the time of death

The surviving spouse was on the original VA loan

VA streamline refinancing is typically not available when the deceased veteran was the only applicant on the original VA loan, even if he or she got married after buying the home.

In this case, the surviving spouse would need to qualify for a non-VA refinance, or a VA cash-out loan.

A cash-out mortgage through VA requires the military spouse to meet home purchase eligibility requirements.

If this is the case, the surviving spouse can tap into the home’s equity to raise cash for any purpose, or even pay off an FHA or conventional loan to eliminate mortgage insurance.

Qualifying if you receive (or pay) child support or alimony

Buying a home after a divorce is no easy task.

If, prior to your divorce, you lived in a two-income household, you now have less spending power and a reduced monthly income for purposes of your VA home loan application.

With less income, it can be harder to meet both the VA Home Loan Guaranty’s debt-to-income (DTI) guidelines and the VA residual income requirement for your area.

Receiving alimony or child support can counteract a loss of income.

Mortgage lenders will not require you to provide information about your divorce agreement’s alimony or child support terms, but if you’re willing to disclose, it can count toward qualifying for a home loan.

Different VA-approved lenders will treat alimony and child support income differently.

Typically, you will be asked to provide a copy of your divorce settlement or other court paperwork to support the alimony and child support payments.

Lenders will then want to see that the payments are stable, reliable, and likely to continue for another 36 months, at least.

You may also be asked to show proof that alimony and child support payments have been made in the past reliably, so that the lender may use the income as part of your VA loan application.

If you are the payor of alimony and child support payments, your debt-to-income ratio can be harmed.

Not only might you be losing the second income of your dual-income households, but you’re making additional payments that count against your outflows.

VA mortgage lenders make careful calculations with respect to such payments.

You can still get approved for a VA loan while making such payments — it’s just more difficult to show sufficient monthly income.

VA loan assumption

What is VA loan assumption?

One benefit for home buyers is that VA loans are assumable. When you assume a mortgage loan, you take over the current homeowner’s monthly payment.

Verify your VA loan home buying eligibility. Start here

That could be a big advantage if mortgage rates have risen since the original owner purchased the home. The buyer would be able to acquire a low-rate, affordable loan — and it could make it easier for the seller to find a willing buyer in a tough market.

VA loan assumption savings

Buying a home via an assumable mortgage loan is even more appealing when interest rates are on the rise.

For example:

Say a seller-financed $200,000 for their home in 2013 at an interest rate of 3.25% on a 30-year fixed loan

Using this scenario, their principal and interest payment would be $898 per month

Let’s assume current 30-year fixed rates averaged 4.10%

If you financed $200,000 at 4.10% for a 30-year loan term, your monthly principal and interest payment would be $966 per month

Additionally, because the seller has already paid four years into the loan term, they’ve already paid nearly $25,000 in interest on the loan.

By assuming the loan, you would save $34,560 over the 30-year loan due to the difference in interest rates. You would also save roughly $25,000 thanks to the interest already paid by the sellers.

That comes out to a total savings of almost $60,000!

How to assume (take on) a VA loan

There are currently two ways to assume a VA loan.

The new buyer is a qualified veteran who “substitutes” his or her VA eligibility for the eligibility of the seller

The new home buyer qualifies through VA standards for the mortgage payment. This is the safest method for the seller as it allows the loan to be assumed knowing that the new buyer is responsible for the loan, and the seller is no longer responsible for the loan

The lender and/or the VA needs to approve a loan assumption.

Loans serviced by a lender with automatic authority may process assumptions without sending them to a VA Regional Loan Center.

For lenders without automatic authority, the loan must be sent to the appropriate VA Regional Loan Center for approval. This loan process will typically take several weeks.

When VA loans are assumed, it’s the servicer’s responsibility to make sure the homeowner who assumes the property meets both VA and lender requirements.

VA loan assumption requirements

For a VA mortgage assumption to take place, the following conditions must be met:

The existing loan must be current. If not, any past due amounts must be paid at or before closing

The buyer must qualify based on VA credit and income standards

The buyer must assume all mortgage obligations, including repayment to the VA if the loan goes into default

The original owner or new owner must pay a funding fee of 0.5% of the existing principal loan balance

A processing fee must be paid in advance, including a reasonable estimate for the cost of the credit report

Find out if you qualify for a VA loan. Start here

Finding assumable VA loans

There are several ways for home buyers to find an assumable VA loan.

Believe it or not, print media is still alive and well. Some home sellers advertise their assumable home for sale in the newspaper, or in a local real estate publication.

There are a number of online resources for finding assumable mortgage loans.

Websites like TakeList.com and Zumption.com give homeowners a way to showcase their properties to home buyers looking to assume a loan.

With the help of the Multiple Listing Service (MLS), real estate agents remain a great resource for home buyers.

This applies to home buyers specifically searching for assumable VA loans as well.

How do I apply for a VA loan?

You can easily and quickly have a lender pull your certificate of eligibility (COE) to make sure you’re able to get a VA loan.

Most mortgage lenders offer VA home loans. So you’re free to shop and compare rates with just about any company that catches your eye.

Getting a VA loan for your new home is similar in many ways to securing any other purchase loan. Once you find an ideal home in your price range, you make a purchase offer, and then undergo VA appraisal and underwriting.

VA appraisal ensures that the home meets its minimum property requirements (MPRs) and is structurally sound and safe for occupancy.

What’s more, VA-specific mortgage lenders are actually some of the highest-rated (and lowest-priced) on the market. Here are a few we’d recommend checking out.

Time to make a move? Let us find the right mortgage for you

Why should lenders and vendors care about servicing? (STRATMOR’s current blog is titled, “It’s 2024: Do You Know Where Your Servicing Is?”) Not only do servicing values fluctuate, which impacts the prices that borrowers see, but servicing is a huge touchpoint with consumers and therefore garners the attention of regulators like the CFPB, headlines, and the courts. The latest example is a California couple suing Specialized Loan Servicing, LLC for negligence that led to a “lost home and destroyed life.” Of course, anyone can sue anyone at any time, but the multi-count lawsuit against Specialized Loan Servicing, LLC alleges breach of contract, theft, and several other counts, accusing SLS of negligence as the mortgage servicer added a quarter of a million dollars to the couple’s mortgage, leading to their “financial and personal ruin.” (Today’s Commentary podcast can be found here and this week’s is sponsored by Lender Toolkit and its AI-powered AI Underwriter and Prism borrower income automation tools. By providing lightning-fast underwriting decisions, your market reputation with borrowers and Realtors will soar, which means more repeat and referral business. Hear an interview with Jeremy Potter and Marvin Chang on broader and more flexible tools for homeowners to navigate our fast-paced and modern economy.)

Lender and Broker Software, Products, and Services

What’s better than a free consultation from a mortgage tech expert? Getting the advice of six. That’s what’s in store if you join “Strategies to Master the Market Now with the Right Mortgage Technology,” next Wednesday, Feb. 21 at 2 pm ET. This free webinar, co-sponsored by Floify and Truv, Christy Soukhamneut, chief lending officer at UFCU; Raven Johnson, VP business systems at Legacy Mutual Mortgage; Craig Ungaro, COO AnnieMac Home Mortgage; features Jodi Hall, founder & CEO of DandaRoad, LLC; Richard Grieser, vice president of marketing at Truv; and Sofia Rossato, president & GM of Floify. Click here to register.

Shake it up + flashback to the 80s with Sagent at MBA Servicing! Be part of the most EPIC MBA Servicing party and shake it up with Sagent on Wed. 2/21 at 7PM ET at Jo Jo’s Shake Bar. Join the team and top industry players for some boozy milkshakes + throwback jams, where you’ll be dancing ‘All Night Long’… Don’t forget to pack your best 80s attire (think Member’s Only jackets, parachute pants) because this party is one you don’t want to miss. Click the link here reserve your spot and we’ll see you there!

“Tired of messy or late closings? LOs know that even if they provide the most amazing customer service, it won’t mean anything if there are delays in getting their borrower’s mortgage approved and closed. The biggest lenders are offering same-day approvals, and so can you. Lender Toolkit’s AI-powered AI Underwriter™ and Prism™ income automation help streamline underwriting so that you can get loans approved faster than ever. By providing almost-instantaneous underwriting decisions, your market reputation with borrowers and Realtors will soar, which means more repeat and referral business. Notes Mark Workens, CEO Mortgage 1: “My company’s ability to be profitable in any market condition is largely due to Lender Toolkit’s Maas™ Platform, including AI Underwriter and Prism.” So why get left behind? Schedule a demo here, or meet us in person for a live demo at EXP24 next month by booking here. We can’t wait to show you what’s possible with our high-tech solutions.”

New: Maxwell’s Q4 2023 Mortgage Lending Report Shows Signs of Market Recovery. Wondering what to expect from 2024’s market? Maxwell’s brand new Q4 2023 Lending Report shows powerful signs of market recovery. In a major reversal, loan volume in Q4 grew year-over-year for the first time since 2021. Plus, the report reveals areas where lenders are finding opportunity, such as through outside-the-box offerings like HELOCs. To gain exclusive data, charts, and advice on how to get ahead of the market reset, click here to download Maxwell’s Q4 2023 Mortgage Lending Report.

Get a Sweetheart Deal with Loan Stream’s February Specials on FHA/VA and Non-QM Price Improvements! Get 37.5 BPS Price Improvement on all FHA and VA, Low Balance, and High Balance >=680 FICO, excludes DPA and 25 BPS Price Improvement on FHA Streamlines/IRRRLS. Plus, a Non-QM Price improvement of 50 BPS on all Non-QM, not including Closed End Seconds and Select Programs. Valid for loans locked 2/1/2024 through 2/29/2024. Terms/Conditions apply see our site and talk with your Account Executive. Don’t miss this month’s webinar on Closed End Seconds and how to Prepare for the CalHFA Dream for All. Register now!

Lenders and borrowers deserve technology that improves the mortgage process, saves time and money, and is intuitive. As both a startup and a company with decades of technology experience, Dark Matter Technologies (DMT) has a unique vantage point for identifying how to improve value for customers, and how to work with an ecosystem of like-minded partners to bring many of those ideas to fruition. In its latest podcast episode, The Spotlight, we meet Chief Product Officer Stephanie Durflinger, the 15-year industry veteran now guiding DMT’s product development team. Stephanie formerly held key positions at both ICE Mortgage Technology and Ellie Mae and brings her unique perspective and discerning eye to guiding the future of Empower and other DMT products. The podcast is hosted by DMT Vice President of Marketing Wes Horbatuck. Listen to the interview now.

Picture this… it’s Saturday afternoon and your borrower finds out they were out-bid and have a small window to decide if they want to offer more on their dream home. You’re at your kid’s soccer game and they’re in panic mode… how much does the payment increase? How much more cash will I need? When can I get an updated pre-approval letter? Fortunately, it’s 2024 and lenders using QuickQual never have to worry about this. Borrowers AND Realtors AND Loan Officers can run accurate payment and closing cost scenarios from their phones and they can generate updated pre-approval letters within guardrails set by the loan officer. Crisis averted with QuickQual.

Technology and operations leaders who care about making sure their technology and operations are competitive for today’s market, as well as learning what’s possible when you push the limits, you don’t want to miss this live event! On February 15, at 1PM CT come join Jonathan Spinetto, COO and Co-Founder of NFTYDoor, Janelle Lindseth, Senior Product Manager of Docutech, and Richard Grieser, Vice President of Marketing of TRUV, as they unpack how Jonathan and his team launched the business with zero loan volume, and in just 2 years, NFTYDoor debuted its digital home equity loan platform, was acquired by Homebridge, and is now on track to reach 3,000 loans per month in 2024, making them a major player in the market. Their technology is built from the ground up and processes everything from credit, KYC, valuations, disclosures, closing (RON), and payments, and all in full regulatory compliance. This is a success story as Jonathan and his team pushed the limits and accepted the risk, but those lessons learned can be immediately applied by you. Come and see the future of lending technology.

Capital Markets

The link between interest rates, mortgage rates, and borrower behavior is always changing. Although the Federal Reserve is apparently “on hold” until its May meeting, it is still important to see and understand what will cause interest rates to move higher and lower over time. Mortgage rates have stayed close to where they started the year, despite swings in Treasury yields because of slowing inflation offset by stronger than expected readings on the job and the housing markets.

The U.S. Federal Reserve is keenly aware of inflation. No news was good news when it came to inflation revision data to close last week, with the Consumer Price Index revised downward slightly in December and the fourth quarter left unchanged at 3.3 percent. A year ago, revisions to the November and December 2022 reports showed higher core inflation than what was initially reported, sending bond yields higher as investors prepared for a “higher for longer” interest rate environment. Dallas Fed President Logan said that disinflation progress has been “tremendous,” but the central bank is in no rush to start lowering interest rates.

The CPI revisions likely give the Federal Reserve further breathing room while allaying any concerns traders might have had about progress on inflation. The revisions were also in sharp contrast to last year’s, in which CPI was revised significantly higher. It’s not at the “magic” 2 percent level, but there is progress. Easing inflation data, a resilient economy and a solid earnings season so far have sparked this year’s stock market rally, which has seen the three major averages tallying their fifth straight weekly gains, and this adds to consumer confidence.

The narrative of late has been a resilient U.S. economy, with low unemployment, inflation largely under control, and the Fed’s fabled soft landing very much in sight. Focus now shifts to January’s CPI tomorrow and if price pressures continue to recede, it may pave the way for the Fed to begin cutting interest rates sooner rather than later.

We also learned last week that January’s ISM Services Index rose to 53.4 from 50.5 in December. The expansion in the services sector of the economy exceeded economists’ expectations as consumers return to pre-pandemic spending behaviors. The prices paid subindex jumped from 56.7 to 64.0, a sign that inflationary pressures remain. This was the largest monthly percentage gain since August 2012.

Consumer spending remains strong and despite higher interest rates, expanded to a record $5.1 trillion in December, although the pace of consumer credit expansion declined from 7.6 percent in 2022 to 2.4 percent in 2023. Rising incomes due to a strong labor market are expected to support the pace of consumer spending as a meaningful slowdown in the job market has yet to materialize. Jobless claims fell to 218,000 during the week ending February 3 and continuing claims declined to 1.87 million, suggesting that those who do find themselves in the job market do not remain there for long.

This week sees the return of “first tier” data including updates on CPI, retail sales, industrial production / capacity utilization, PPI, and Michigan sentiment. Other data includes regional Fed surveys, import prices, factory orders, NAHB HMI, and housing starts. Fed speakers are currently limited to a few Fed presidents, while Treasury supply will consist of just bills. Regarding MBS, Class B and C 48-hours are tomorrow and Thursday, respectively.

Today’s lone data point is the January budget statement, due out this afternoon, with the CBO forecasting a deficit of $21 billion, compared with $38.8 billion in the prior fiscal year. Markets will also receive remarks from Minneapolis Fed President Kashkari. We begin Monday with Agency MBS prices a few 32nds (ticks) better than Friday afternoon, the 10-year yielding 4.16 after closing last week at 4.19 percent, and the 2-year is at 4.46.

Jobs

“Hey, mortgage sales professionals DO NOT join radius financial group for our amazing culture, president club trips, best workplace accolades, 100 percent 401K match or because of our shared success program which grants phantom stock to ALL employees. Join radius to grow your business, mortgage team and wealth. Over the past 23 years, radius has become the best at what we do by caring intensely about the career growth of our team members and investing in technology that simplifies and automates our process. We are a world-class customer obsessed team focused on our loan officers’ growth and success. So, if you want real opportunities to grow, the ability to make a positive impact starting on day one and the freedom to chart the career you’ve always wanted, at radius, you can! For confidential inquires please contact Carla Herrera and visit us at radius financial group inc., Mortgage Lending Careers.

The Money Store has announced that Coleen Bogle has joined the mortgage lender as its Chief Marketing Officer. Bogle has more than 15 years of experience leading marketing departments in the home financing industry, and in her new role, she will focus on enhancing the brand, expanding marketing services, and attracting top-tier mortgage origination talent to the organization.

Private mortgage insurance companies are hiring: MGIC, National MI, Arch MI, Radian, Essent, and Enact (in no particular order). And while’s we’re at it, Fannie Mae and Freddie Mac. And my cat Myrtle’s friend the CFPB has career opportunities.

Don’t forget that anyone can post a resume, for free, at www.lendernews.com for potential employers to view for a nominal charge of $75 for several months.

Download our mobile app to get alerts for Rob Chrisman’s Commentary.

Share via Social Media:

All social media shares will include the image and link to this page.

PPE, Audit and Risk, AI/ML Adoption, Closed-End 2nd Products; Lenders and Court Cases; CRA News

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

PPE, Audit and Risk, AI/ML Adoption, Closed-End 2nd Products; Lenders and Court Cases; CRA News

By: Rob Chrisman

Mon, Jan 29 2024, 10:57 AM

“Sometimes it takes me all day to get nothing done.” But things are always changing. When I was a kid I “got a drink of water.” Now kids “hydrate.” Really? A few years ago, a good originator could do 10-20 loans per month. Now, it is rumored that 80 percent of volume is being done by 40 percent of originators, and lenders have instituted minimum production numbers: “If you’re not funding 2 loans per month, we’re going to let you find success elsewhere.” Diving into 2023’s production via NMLS looking at 234,000 records, Ingenious found that only 24 percent of originators did 24 units or more! 30 percent did 18 or more units, 40 percent did 12 or more units, and 60 percent did 5 or more units. Has the “norm” changed? Certainly a portion of marketing has shifted to people under the age of 40s, and Mortgages with Millennials with Kristin Messerli and Robbie Chrisman talking about Overlooked Strategies to Win with Millennials tomorrow at 1PM ET. Today’s podcast can be found here and this week’s is sponsored by Calque. With The Trade-In Mortgage powered by Calque, lenders help their clients negotiate a lower purchase price, reduce their interest payments, and eliminate PMI. Hear an interview with Truv’s Richard Grieser on the latest verification solutions and how lenders can combat fraud.

Lender and Broker Software, Products, and Services

Introducing The 2024 Lender Playbook: 4 Tips to Drive Profitability in a Recovering Market. How will the coming election, housing inventory, and Fed action impact the mortgage market (and your lending success) this year? There’s a lot going on in 2024, and market recovery won’t be straightforward. The good news? You can still build a strong, forward-thinking plan for resilience and profitability. Tenured industry experts from Maxwell’s senior team helped create this guide to teach you how to reduce costs, win borrower business, and capture intermittent loan volume as it reemerges in the market. To get a leg up on the competition and build agility into your business, click here to download The 2024 Lender Playbook: 4 Tips to Drive Profitability in a Recovering Market.

Unleash Opportunities with LoanStream’s new Closed End Seconds webinar on Tuesday, February 20th, for borrowers who want to tap into their equity without refinancing or help them save money by avoiding costly mortgage insurance. Plus, it’ll include an update on the upcoming CalHFA Dream For All Loan Program. Reserve you or your Team’s spot now for this informative webinar.

The human circulatory system is more than 60,000 miles long! Running a system that complex would take all your waking energy if it wasn’t automated by your brain’s blood-flow command center. As the command center of your mortgage operation, your LOS similarly coordinates hundreds of loan tasks at once so you can focus on building relationships and running your business. And soon, your LOS could become even more powerful, adaptive, and proactive thanks to AI and machine learning. But is your organization ready? A new blog from Dark Matter Technologies offers tips for building an AI/ML adoption strategy so you can plan today for a more productive tomorrow.

“In a year where companies are trying to differentiate themselves, MQMR has that solved. While we know culture eats strategy for lunch, leaders didn’t think this could be done in a virtual environment. Happy to report that MQMR has built a thriving culture with teammates in 14 states and 3 continents, a world-class employee NPS in the high 70s, and 50%+ of its clients are multi-product clients, many of whom have been doing business since 2011. For lenders seeking an audit, risk, and compliance partner, there’s only one to choose from, so choose the one that not only delivers results but someone who has a fun culture to work with! MQMR takes care of its teammates because MQMR knows those teammates take care of you. Check out our fun year-end video with an inside look at the beating heart of our culture and in case you missed Saturday’s Spotlight, MQMR was the featured company!”

Polly, leading provider of innovative mortgage capital markets technology and operator of the industry’s first cloud-native, commercially scalable product and pricing engine (PPE), just announced the appointment of industry powerhouse Troy Coggiola as COO. Coggiola’s appointment follows a record year for Polly, both in industry adoption and product innovation. As COO, Coggiola will lead Polly’s product, implementation, support, and design teams, ensuring seamless cross-organization collaboration as the company continues to scale. Coggiola is the latest in a string of notable leadership hires; Parvesh Sahi, former SVP of Business and Client Development for ICE Mortgage Technology, joined the company as CRO in 2023. Former Fannie Mae executive and industry veteran Andrew Bon Salle, as well as former Ellie Mae CEO and mortgage industry visionary Jonathan Corr sit on the company’s board of directors. Read the press release.

Legal News and Regulations

This has absolutely nothing to do with mortgages, but what happens in the court system can be puzzling. What is the value of a human life? 33-year old Bryn Spejcher, convicted of killing her boyfriend Chad O’Melia by stabbing him 108 times during a “cannabis-induced psychosis,” received two years’ probation and ordered to perform 100 hours of community service according to the Ventura County Star. That’s it. (Ventura County Superior Court Judge David Worley, appointed by Republican Governor Arnold Schwarzenegger.)

Connecticut Banking Commissioner Jorge L. Perez issued a temporary order to cease and desist against LoanSnap, Inc., and notifying LoanSnap that its state mortgage lender license will be revoked and a civil money penalty will also be issued against it. The charges against the California-based mortgage lender include alleged violations of the Truth in Lending Act and the Fair Credit Reporting Act, but the focus was on unlicensed origination activities. According to the allegations, department examiners discovered that from at least August 29, 2022, to December 2, 2022, LoanSnap employed individuals who were not licensed as mortgage loan originators in Connecticut yet acted as mortgage loan originators by taking residential mortgage loan applications, soliciting Connecticut borrowers for residential mortgage loans, and offering or negotiating terms of residential mortgage loans. These unlicensed mortgage loan originators worked in out-of-state call centers and their titles were described as “sales development representatives” or “call center representatives.”

The U.S. District Court for the Southern District of Florida denied Freedom Mortgage’s motion to stay a case filed by the CFPB after Freedom argued that judicial economy (the preservation of the court’s time and resources) favored the stay because the defendant’s pending motion to dismiss is premised on the same constitutional issue addressing the CFPB’s funding structure now before the Supreme Court. Orrick reports that, “In opposition, the CFPB argued that the Supreme Court may take months to issue a ruling, the public interest in enforcement of consumer protection laws, and the failure to show how an adverse ruling in the Supreme Court case would definitively result in dismissal of this case… The District Court sided with the CFPB, stating that as of now, the CFPB ‘is a valid agency that is entitled to enforce the consumer financial laws.’ With the stay denied, the court will now consider the defendant’s motion to dismiss.”

Mortgage banks don’t accept deposits, so can’t reinvest them in the local community. But that hasn’t stopped some states from pushing CRA requirements onto some institutions. The Illinois Department of Financial and Professional Regulation issued a proposed rule pursuant to the Illinois Community Reinvestment Act (ILCRA). The ILCRA is modeled off the Community Reinvestment Act but expands its scope of covered financial institutions to include credit unions and licensed entities. Orrick reports that, “The proposed rule establishes a framework and criteria by which the Department will evaluate a covered mortgage licensee’s record of helping to meet the mortgage credit needs of Illinois, including low- and moderate-income neighborhoods and individuals, through different tests and performance standards depending on the number of loans made by a covered mortgage licensee. Tests and considerations for evaluating licensees’ record include a lending test, service test, performance record, data collection and reporting, and content and recordkeeping of information received from the public.

“To mitigate the impact on small businesses, a licensee that has made less than 200 home mortgage loans in Illinois in the last calendar year will not be subject to the service test. Furthermore, licensees that made less than 100 home mortgage loans in Illinois in the previous calendar year will have less frequent examinations than those with more than 100. Based on the licensee’s performance under the lending and service tests, the proposed rule specifies that a licensee’s rating of ‘outstanding,’ ‘satisfactory,’ ‘needs to improve,’ or ‘substantial noncompliance’ will affect how frequently they are evaluated. Compliance with the proposed rule is required six months from its effective date, and comments are due by February 26.”

Capital Markets

Last week closed with economic growth in the fourth quarter beating forecasts as gross domestic product increased 2.5 percent for the year. Importantly, the PCE Price Index, the inflation number that matters most to the Fed, rose 0.2 percent month-over-month, as did the core rate which excludes food and energy. Trends in annual inflation numbers continue to move lower and now sit at an almost three-year low, even with strong holiday spending. That report capped a year that began with economic “experts” warning the public of a guaranteed American recession, but inflation retreated at a much faster rate than the Fed anticipated, all while a robust job market kept driving consumer spending. The most recent data has led to more optimism that the economy can power through the Fed’s efforts to corral inflation.

This week is packed with market moving potential including the latest Federal Open Market Committee decision followed by Chair Powell’s press conference on Wednesday afternoon with the Quarterly Refunding announcement Wednesday morning. The December jobs report will be released on Friday where early estimates are for an increase of 178k in headline payrolls (versus 216k in December). Besides payrolls, the U.S. calendar includes updates on home prices, ADP employment, productivity / unit labor costs, manufacturing PMIs with factory orders and Michigan sentiment. Sweden’s Riksbank and the BoE will release their latest decisions on Wednesday and Thursday morning.

Today’s calendar sees just one data point, the non-market moving Dallas Fed Texas manufacturing for January, due out during the day. There are some short-duration Treasury auctions, and the Quarterly Refunding estimate will be announced. We begin the week with Agency MBS prices better by .125-.250, the 10-year yielding 4.10 after closing Friday at 4.16 percent, and the 2-year is at 4.33.

Employment and Transitions

“We are looking for “The Best Account Executive Ever.” If this should be your title, contact me, [email protected]. Outstanding Account Executives understand the value of their relationships and so do we. Yes, product expertise is essential but first-rate relationship management puts you head and shoulders above your competition. Explore your options with Freedom Mortgage Wholesale. We are Historically, Currently and 4EVER Wholesale. Let’s connect today. Everyone wants rates to structure winning loans for their borrowers. Have you seen what Freedom is offering? Freedom Mortgage Wholesale is making brokers and borrowers happy. Check out our FHA and VA rates for best execution…for free on LenderPrice. Reach out to Freedom for more information at 855.915.4800. Freedom Mortgage Wholesale is Historically, Currently and 4EVER Wholesale.

A&D Mortgage announced the hiring of Tommy Williams, Betsy Marvin, and Lori Welton as Account Executives. “These three industry veterans bring a wealth of experience and expertise to A&D Mortgage, especially in the Conventional mortgage business” and join recent hires Andrew Taylor and Bobby Frank. Andrew Taylor is now A&D’s Senior Vice President of Wholesale Lending Sales and Bobby Frank is Senior Vice President of Wholesale Lending Strategy. Congratulations all around!

FHA Program Analyst (Computerized Home Underwriting Management System (CHUMS) Coordinator) in Santa Ana, CA. Job duties include coordinating activities related to the CHUMS

Lender Access System (CLAS). Update software to the CKAS system to permit enhancements. Monitor and assign program code identifiers for CHUMS users. Analyze CHUMS data and develop new methods of correlating and disseminating. FHA Job Announcement 24-HUD-589-P.

FHA Senior Single Family Housing Specialist (Quality Assurance Division) Job duties include acting as HUD expert and advisor required for compliance on the lender origination and servicing practices. Prepare correspondence, technical back-up documentation, status reports, schedules, and other information. Identify actions necessary for the correction of the lender’s deficiencies. FHA Job Announcement 24-HUD-587-P.

Download our mobile app to get alerts for Rob Chrisman’s Commentary.

Share via Social Media:

All social media shares will include the image and link to this page.

It’s time to check out “Toll Brothers Mortgage,” which is a subsidiary of home builder Toll Brothers.

Toll Brothers is one of the largest home builders in the United States, priding itself on being a luxury home builder.

Instead of relying on third-party lenders to provide financing to their customers, they have a built-in financing division.

This allows them to oversee the process firsthand and navigate the complexities of new construction financing.

They say they’ve got a proven track record of smooth closings, and if they can offer you a mortgage rate the other guys can’t, they could be worth looking into.

Toll Brothers Mortgage Fast Facts

Direct-to-consumer retail mortgage lender

Provides new construction lending and home purchase loans

Parent company is nation’s 5th largest home builder

Founded in 1967, headquartered in Fort Washington, PA

Licensed to do business in 24 states nationwide and D.C.

Funded nearly $2 billion in home loans last year

Most active in California, Pennsylvania, and Texas

Offers mortgage rate specials to Toll Brothers customers

Also operates a full-service title and insurance company

As noted, Toll Brothers is a major home builder, the fifth largest at last glance, behind only D.R. Horton, Lennar, Pulte, and NVR.

They are a publicly-traded company (NYSE:TOL) and are currently valued at around $9 billion.

The company was founded in 1967 and refers to itself as the nation’s leading builder of luxury homes.

This includes both new construction homes and quick move-in homes. The company’s dedicated mortgage division is known as Toll Brothers Mortgage Company, or TBI Mortgage for short.

They exist solely to serve Toll Brothers customers who need to finance their new home purchases, and have about 77 loan officers on staff, per the NMLS.

In 2022, the company funded a healthy $2 billion in home loans, with 20% of volume coming from the states of California and Texas, and another 9% from Pennsylvania.

The company also did a lot of business in Arizona, Colorado, Florida, Idaho, Nevada, and Virginia.

They are licensed to lend in Arizona, California, Colorado, Connecticut, Delaware, Florida, Georgia, Idaho, Illinois, Maryland, Massachusetts, Michigan, Nevada, New Jersey, New York, North Carolina, Oregon, Pennsylvania, South Carolina, Tennessee, Texas, Utah, Virginia, and Washington.

Those purchasing a Toll Brothers home can also take advantage of in-house title, escrow, and insurance services via Toll Brothers Insurance Agency.

How to Get Started

To begin, you can visit a new home sales office or simply check out their website.

If you go online, they have a contact form and a loan officer directory that lists individual employees by state.

They can provide loan pricing and answer mortgage questions you might have about the loan process.

If you’re ready to proceed, they’ll ask you to complete a mortgage pre-qualification questionnaire and create a secure Toll Brothers account.

Within 14 days of signing a home purchase agreement, you’ll be asked to submit the loan application and upload required documents.

Their digital loan application is powered by ICE (formerly Ellie Mae). It allows borrowers to start the process from any device and complete most tasks electronically.

This includes linking accounts like pay stubs, tax returns, bank statements, along with eSigning necessary disclosures.

If approved, they’ll provide you with a loan commitment, as well as conditions needed to fund your loan.

Importantly, the loan approvals are valid through the completion of your home. And are integrated with Toll Brothers to sync with the builder process.

Since building a new construction home can take up to 12 months, their loan process may have longer timelines than a typical existing home purchase.

But they also offer quick move-in properties, in which case the process will likely only be 30 to 45 days.

Loan Programs Offered

Home purchase loans

Conventional loans backed by Fannie Mae and Freddie Mac

FHA loans

VA loans

Fixed-rate mortgages: terms ranging from 10 to 30 years

Adjustable-rate mortgages: initial fixed terms of 3, 5, 7, 10, or 15 years

Available on primary residences, second homes, and investment properties

While Toll Brothers Mortgage only offers home purchase loans (no mortgage refinances), they have a decent loan menu.

This includes all the usual offerings such as conforming loans backed by Fannie/Freddie, jumbo loans, FHA loans, and VA loans.

The only loan programs they appear to be missing are USDA loans and second mortgages, though these aren’t widely used by home buyers these days.

They’ve got a good selection of both fixed-rate mortgages and adjustable-rate mortgages, including a 10-year fixed and 15-year fixed.

With regard to the adjustable-rate loans, they’ve got the 5/6 ARM, 7/6 ARM, and even an ARM with an initial fixed term of 15 years.

And you can get an ARM if taking out an FHA loan or VA loan, which is less common.

So there’s no shortage of loan programs, and they finance primary residences, second homes and investment properties.

Toll Brothers Mortgage Rates and Fees

Like other mortgage lenders, they do not have a page dedicated to mortgage rates, nor are they publicized elsewhere.

Instead, they simply say they offer “competitive rates,” which obviously doesn’t give us a lot to go on.

However, they offer personalized financing packages and there’s a good chance they’ve got some special financing offers unique to home builders.

If you browse the Toll Brothers main website, you might see specials for certain communities.

I came across an exclusive offer of 5.99% on a 30-year fixed while rates are closer to 7.5% at the moment.

Lately, the captive mortgage lenders of home builders have been hard to beat, thanks to their big temporary and permanent mortgage rate buydowns.

Many are offering rates well below market if you buy certain homes by a specific date.

But always take the time to compare their rates and fees to outside lenders as well. You’ll never know what else is out there if you don’t put in the time to look.

LockSolid Rate Protection program

Since the home building process can take time, Toll Brothers Mortgage offers a special mortgage rate program called “LockSolid Rate Protection.”

Since It allows home buyers to lock in a mortgage rate for up to 345 days, with no cost until loan closing.

The up-front lock deposit is advanced by Toll Brothers, giving buyers peace of mind in an uncertain mortgage rate environment.

Additionally, a float down option is available on many programs. So if rates happen to fall below the rate you locked in within 30 – 45 days of closing, they can re-lock your loan at a better price.

The program is available on both fixed- and adjustable-rate mortgages offered by the company.

Just keep in mind that it doesn’t always make sense to lock in a rate well ahead of time. If you have an extended time horizon, floating your mortgage rate can provide more opportunities.

It’s also generally cheaper to lock in a rate with a shorter lock period.

Toll Brothers Mortgage Reviews

There aren’t a ton of reviews for Toll Brothers Mortgage specifically, though I did come across some.

Over at Zillow, they have a pretty poor 1.36/5-star rating from about a dozen reviews. Not a big sample size, but not glowing reviews either.

Similarly, they have a 1.8/5 from another dozen mortgage reviews on Google for their Fort Washington, PA headquarters.

They have a 5-star rating on Redfin, but it’s only from three reviews. Meanwhile, their parent company has a 1.12/5 rating on the Better Business Bureau (BBB) website from 85 reviews.

However, the company maintains an ‘A+’ rating based on customer complaint history, so they appear to handle issues that come up appropriately.

Take the time to read the customer reviews and complaints to see what the common issues are, and how you might be able to avoid them.

At the end of the day, using the builder’s lender can make sense if they offer a below-market mortgage rate.

There’s also the perception that they’re in better sync with the builder as the companies operate under the same parent.

But based on the complaints, this isn’t always the case. So be sure to shop around and get quotes from other mortgage companies and some independent mortgage brokers too.

Even if you do decide to use Toll Brothers Mortgage, you can use those other quotes to negotiate a better deal.

Toll Brothers Mortgage Pros and Cons

The Good Stuff

Can apply for a home loan online

Offer a digital, mostly paperless application powered by ICE

Loan approvals good through completion of your home

May offer special financing incentives to Toll Brothers customers

Lots of loan programs to choose from including ARMs

LockSolid Rate Protection program

A+ BBB rating

Mortgage glossary and mortgage calculator online

The Maybe Not

Only licensed in a handful of states where they build homes

Well, mortgage rates are still rock bottom. In fact, the 15-year fixed-rate mortgage actually hit a new all-time low this week, falling to 3.11%, per Freddie Mac.

So who’s actually benefiting? Well, a new loan origination report from Ellie Mae breaks it all down for us to see what’s working and what isn’t.

The data looks at loan applications from February, and it’s rather robust, with about 20% of all mortgage apps in the United States flowing through Ellie Mae’s Encompass360 mortgage management software.

Average Fico Score 750

I always highlight credit score as being one of the most important aspects of qualifying for a mortgage.

Without a solid credit score, it doesn’t really matter if you have $1 million in liquid assets and a job that pays you $200,000 a year.

[What credit score is needed for a mortgage?]

Banks and mortgage lenders still want to know that you will meet your obligations on time every month. Heck, even if they do grant you a mortgage, a low credit score will mean a higher-than-market mortgage rate. And who wants that?

That said, the average Fico score for all funded loans in February was 750, which is up from 740 six months ago.

Meanwhile, the average Fico score for denied loans was 699, which is still pretty high in the grand scheme of things.

In other words, lenders expectations keep on rising, so if you want the low mortgage rates, you need to clean up your act.

Average LTV 76%

Meanwhile, the average loan-to-value ratio on closed loans was 76%, which means most homeowners had nearly 25% equity in their homes.

It was also down from the 79% average seen back in August.

Sure, there are programs for borrowers who are underwater on their mortgage, such as HARP phase II, but most loans are still going to those with adequate home equity.

And remember, the lower your LTV, the better your chances or securing a low mortgage rate, and approval for that matter.

For conventional loan purchases, the average buyer put down 22% and had a 764 Fico score. Wow. Talk about no-nonsense lending.

DTI Ratios of 23/34

Ellie Mae also noted that the average front-end debt-to-income ratio for loans that funded was 23%, meaning less than a quarter of gross monthly income went toward the monthly housing payment.

And the mortgage plus all other monthly liabilities only accounted for 34% of gross income for approved borrowers.

For comparison sake, those who got denied had ratios of 28/44, which meant homeowners were spending nearly a third of income on their housing payment.

Bring It All Together

Overall, 48% of all loan applications eventually closed, and there was a higher percentage of purchase closings (60%) than refinances (42%)

[7 reasons why you can’t refinance your mortgage.]

Still, the refinance share of applications (67%) dominated purchases (33%), but clearly not all the refis are working out.

Layered risk comes to mind, that is, the combination of a lower-than-average credit score, coupled with higher-than-average DTI and LTV ratios.

This is essentially what mortgage underwriters look for, so it’s imperative that you don’t present too much default-risk when applying for a mortgage.

The average loan that did eventually fund took 44 days, from application to closing.

In summary, step up your game folks. Lenders want quality these days…

You know that awesome refinance you’ve got all planned? The one that’s going to save you hundreds on your mortgage payment every month.

Well, I hope you’re an extremely patient person, because the average time it takes to close a refinance is nearly 60 days, according to the latest monthly loan origination report from Ellie Mae.

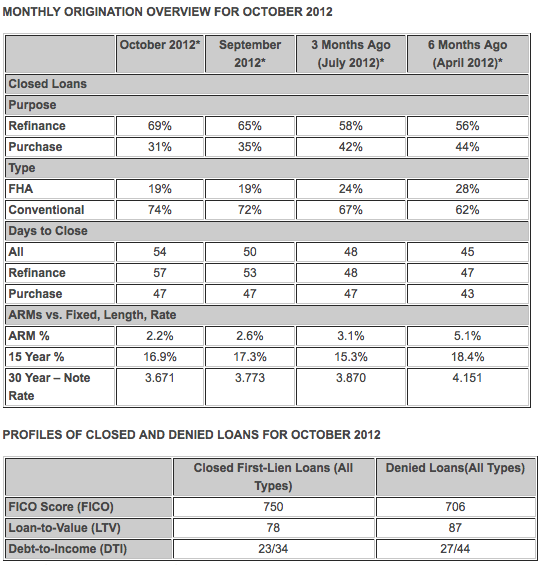

The company, which provides mortgage management software, noted that the “days to close” for a refinance rose to a staggering 57 days in October, up from 53 days in September.

That compares to 48 days three months ago (July 2012) and 47 days six months ago (April 2012).

All the more reason to ponder the question of whether to lock or float your mortgage rate.

The refinance share also increased to 69% of total origination volume, up from 65% in September.

Low Rates Fueling Demand

It all makes perfect sense. Mortgage rates are at their lowest point in history, and there just aren’t enough loan officers, loan processors, and underwriters around to handle it all.

Sure, banks and mortgage lenders have hired more employees in recent months, but employment levels in the industry are still much lower today than they were during the boom.

And you better believe companies aren’t about to go on a hiring spree, only to let those same people go after the refinance frenzy slows down.

After all, refinance activity is expected to fall to $785 billion in 2013, down from an estimated $1.2 trillion this year, per the latest Mortgage Bankers Association forecast released last month.

In short, as rates rise, refinancing will come to a crawl, especially since everyone and their mother is jumping on the refinance train now, when rates are at their lowest.

Kind of explains why Bank of America reportedly had a waiting list to refinance earlier this year.

For the record, the average 30-year note rate for those who took out a loan last month was 3.671%, down from 3.773% in September and 4.274% a year earlier.

That doesn’t bode well for refinancing going forward unless rates surprise us once again.

More Refis Funding

While the time it takes to refinance is clearly on the rise, more loans are actually making it to the finish line.

Ellie Mae noted that the closing rate for refinances increased to 51.3% in October, up from 45.3% in September.

It’s the first time the pull-through rate for refinances has topped 50% since the company began tracking the metric in August 2011.

And it was as low as 37.9% as recently as July, so that’s certainly good news. Perhaps HARP 2.0 is helping the cause, with fewer restrictions in place to kill deals.

Higher property values may also be helping, with fewer low appraisals being a burden.

All the refinance activity is also making it harder to close more time-sensitive purchase-money loans, though the day to close hasn’t changed a whole lot in months.

It stood at 47 days in October, unchanged over the past three months, but up from 43 days in April.

The close rate for purchases has also steadily improved, increasing from 55.2% in April to 61.2% last month.

So at least all the hard work originators and banks are putting in is actually paying dividends (and healthy commissions).

The average FICO score for a successful loan last month was 750, unchanged from September, while denied loans had an average FICO score of 706, up from 704 a month earlier.

In other words, those with really good credit are still missing out on refinancing or buying a home for one reason or another.

Yes, credit is very important, but it’s not everything.

Today is the 15th anniversary of the collapse of Lehman Brothers. The great financial crisis (GFC) revealed a defective supply chain, metrics unable to assess local risk and markets incapable of answering Ben Bernanke’s defining question – “what’s this stuff worth?”

The requirements of a Digital Housing Platform were well understood long before the crisis. The components needed to move housing past a costly, error prone, disconnected system include:

Authentication: Identity is the key control point in any digital interaction. The capability to “identity proof” the participants in a complex, multi-party transaction is fundamental to establishing trust, reducing fraud and removing friction between “relying parties.” The capability to authenticate, issue and revoke digital credentials is central to controlling access, verifying rights and accepting content from supply chain partners.

Authorization: A digital loan file of record accessed by a broad range of trusted identities from lenders to guarantors to investors requires a permission structure. What functions are individuals and organizations allowed to perform including viewing, editing, printing, exporting and approving? The capability to enforce these rights can eliminate errors and rework. The result should be collapsing costs and cycle times, improving quality, reducing repurchase risk and certifying that a loan, and its related assets are “Fit 4 Sale.”

Non-Repudiation: E-sign became federal law in 2000 but digital signatures are only a subset of the integrity component. Investors require assurance that a file, note or instrument reflects the verifiable intentions of the committed parties. Sensitive content must be protected in motion over networks and at rest within repositories. Technologies like encryption help deliver certainty that content has not been tampered with.

Validation: Mortgage is a manufacturing process with end products dependent on accurate information. Data is imported from multiple sources including credit agencies, public records aggregators, appraisers, inspectors, title and insurance firms and Realtors. How do we know that the data is correct, can the source be verified, does it meet quality standards and can compliance with pricing guidelines be guaranteed?

Federation: Integrating the fragmented, localized and diverse housing ecosystem is the major challenge for any network delivering content from trusted sources. Standard agreements define shared responsibilities and what happens when mistakes happen. These policy considerations, enforced by technology and legal conventions, are required for interoperability among supply chains and between competing “Super Apps.”

Registration: A golden record of who owns the asset is a prerequisite for any commercial trading system. Improving the ability of MERS to verify and transfer ownership required capital, time and technology. Extending the registration component to county recording offices was another platform foundation.

Transactions: Platforms are “plug and play” once federated policies are widely implemented. Matching and clearing trades in open exchanges for multiple asset classes is a core ICE capability. The Ellie Mae component provided a critical mass of connections to begin the process of reinventing the property transaction.

Compensation: Payments reveal the end points of the ad-hoc networks that characterize real estate. A servicing system that touches the consumer every month can be extended to all the participants in the original transaction. As every consumer facing commercial platform will attest — payments are the prize.

Information: Listings are on platform and new metrics will assess the risk, value and volatility of submarkets.