Dallas is a fast-growing and highly desirable city to live in. It’s ranked city No. 24 on U.S. News & World Report’s “Best Places to Live” list for a good reason. In Dallas, you can find big-city vibes as well as toned-down suburban-style living depending on where you settle down — making it suitable for any lifestyle.

The cost of living in Dallas is 7.7 percent higher than the national average, but it still costs less to live here than in cities like Los Angeles, Boston and Chicago. Within Dallas, the average rent is declining year-over-year, and if you have ever considered moving to Dallas, now is the time!

Before moving to Dallas, you should consider some basic expenses like housing, food and utilities. These are all common things to think about before making your move. The below sections will help you determine if living in Dallas makes sense for you.

Housing costs in Dallas

Experts predict the Dallas-Fort Worth metroplex to rank as the sixth-hottest housing market in the nation in 2021.

With that being said, you should know that the cost of living in Dallas for housing is 15.9 percent above the national average and properties do not sit on the market long. Don’t let that deter you from rolling your sleeves up and going after what you want. Just keep in mind that the market is pretty competitive.

Some of the most expensive neighborhoods to live in Dallas are Knox/Henderson, East Dallas, Main Street District and Vickery Place. To reside in one of these neighborhoods, you will find yourself paying $2,000 to $2,500 on average monthly rent for a one-bedroom apartment. Don’t worry though — you get your money’s worth. These neighborhoods are known for their walkability factor, unique restaurant options and upscale services.

On the other hand, you can live in neighborhoods like Highland Hills, Southeast Dallas or Riverway Estates and rent a one-bedroom for under $800. It depends on which amenities are important to you and the lifestyle you want to live within the city.

If you’re house hunting, you’ll also find a vast range of options. According to Redfin, the Dallas home market is up 17.1 percent since last year, and the median sale price is $410,000 — well above the national average of $353,000.

Food costs in Dallas

Food costs in Dallas are right around the national average, making it very reasonable to fill your belly and not break the bank. You can balance dining out at fancy rooftop restaurants with cost-effective home-cooked meals since groceries here remain fairly priced.

If you’re shopping for supermarket staples, you’ll see ground beef costs $4.42, a half-gallon of milk costs $1.97 and eggs are $1.15 for a dozen. There are also farmer’s markets on the weekends, specialty grocery stores for unique items or low-cost grocery stores for everyday essentials.

The foodie scene here is incredible, too. The benefit of living in Dallas means the meal options are endless — you can find something to fit any budget. You can score a food truck meal for under $5. Not into that? Scour the city for the best burger and pay $18 a pop.

Living in Dallas means getting used to having casual eateries, mid-priced options or five-star restaurants with highly accredited chefs right at your fingertips.

Utility costs in Dallas

What you pay for utilities will rely on usage, but you can expect them to run 8 percent above the national average. In case you haven’t heard, Texas summers are sizzling hot.

A monthly energy bill is close to $200, higher than in New York, Atlanta and even Los Angeles. Trying to stay cool in Dallas is no joke so just prepare to crank up that A/C.

The monthly cost of a phone bill is around $185, the internet is $45 and water bills are usually under $100. The cost of water is high in Texas due to the dry climate.

Transportation costs in Dallas

It’s very reasonably priced to get around Dallas, whether you own a car, take advantage of public transportation or use ride-booking services in the city. Dallas has a transit score of 45, a walk score of 57 and a bike score of 56.

There are newly built highways and toll roads that make getting from one side of Dallas to the other a breeze. If you own a Toll Tag, you get a special toll rate of 19 cents per mile — worth the initial $40 payment.

Dallas also has the DART (Dallas Area Rapid Transit) system, so if you don’t want to get behind the wheel, you buy a daily pass for $6 or a monthly pass for $96.

Transportation costs in Dallas are 6.8 percent under the national average. A gallon of regular unleaded gas costs $1.92 and is cheaper than in other large, popular Texas cities like Houston and Austin.

Healthcare costs in Dallas

Healthcare requirements vary so much from person to person, so it’s tough to come up with an average for overall healthcare. Just know that whether you are seeking a general family doctor, an emergency comes up or you need special medical attention, Dallas has elite healthcare providers, services, hospitals and facilities.

Medical City Dallas is an example of a leading health care provider. It’s one of the largest in the region and includes 16 hospitals employing over 17,000 employees.

Healthcare costs in Dallas remain steep — 13.8 percent higher than the national average. A doctor visit will run you $121, a trip to the dentist costs $134 and seeing the optometrist is $98.

Goods and services costs in Dallas

Aside from the essential bills, the goods and services category encompasses anything that is not consumable.

Dallas ranks 7.1 percent higher than the national average in this category. Examples include office pens, a new hairbrush, a movie ticket and services like dog grooming, landscaping and home repairs.

Dallas is a very pet and dog-friendly city but just know that a trip to the vet will set you back $64

A trip to a beauty salon averages $45, a movie ticket runs $11 and a yoga costs about $21 per class.

Taxes in Dallas

Fun little fact: There’s no state or local personal income tax in Texas. That means that there are no taxes at a state level for Social Security benefits, pensions, 401(k)s or any other type of retirement income. This helps save a bit of money and offsets the high property taxes, but you don’t have to worry about that if you’re renting.

Texas’ statewide sales tax is a modest 6.25 percent, but total sales taxes, including county and city taxes, sit at 8.25 percent. So, f you spend $100 in Dallas, you can expect to pay $8.25 in sales tax or less.

Dallas residents also benefit from three Texas tax-free weekends where the state and local taxes get waived for specific items.

How much do you need to earn in Dallas?

Experts suggest you not spend more than 30 percent of your annual income on housing.

If you take the average rent price for a one-bedroom in Dallas, which is $1,390, and multiply that by 12, you get what you need for housing for the year — $16,680.

So, to cover for housing that is 30 percent of your annual income, you need to earn at least $55,600 annually in Dallas. For more specific needs you can use our rent calculator.

Living in Dallas

While there are many things to consider before moving to Dallas, this vibrant city has a lot to offer. From budget-friendly living to lavish lifestyles and everything in between, Dallas is a great place to plant your roots and call home.

Cost of living information comes from The Council for Community and Economic Research.

Rent prices are based on a rolling weighted average from Apartment Guide and Rent.’s multifamily rental property inventory of one-bedroom apartments in April 2021. Our team uses a weighted average formula that more accurately represents price availability for each individual unit type and reduces the influence of seasonality on rent prices in specific markets.

The rent information included in this article is used for illustrative purposes only. The data contained herein do not constitute financial advice or a pricing guarantee for any apartment.

Your home’s roof can take a beating, whether roasting in the sun during the summer, getting coated with ice in winter, and withstanding wind and rain year-round. In other words, it’s one of your house’s key MVPs. But eventually, roofs wear out and need to be replaced or fixed. You may notice a small (or big) leak. It could be 15, 20, or even 50 years, but at some point, your roof will likely need to be repaired or replaced. While costs can range widely, the average roof replacement currently costs $11,500.

In this guide, you’ll learn about roof replacement costs, as well as what your options are for paying for roofing expenses.

How Much Does a New Roof Cost?

The average roof lasts 25 to 50 years, though repairs (both minor and major) can pop up more often. Sometimes, damage to one part of a roof can nudge a homeowner to go ahead and replace the whole thing.

You likely got a general idea of the condition of your home’s roof during the home inspection, when you were buying your property. If now is the time to get the job done, though, you’ll want to understand the costs involved.

When looking at new roof installation costs, there are a number of factors that will impact the overall price:

• Size of the roof being replaced

• Material to be used on the roof

• Style of the roof (those with multiple eaves, lots of detailing, or steeper pitches could take longer and cost more)

• What part of the country you live in (cost of living can vary considerably)

• What time of year you are having work done (doing so off-season could potentially save you extra money; roofers tend to be most in demand in late summer and early fall).

• The size and style of the roof may contribute to the overall cost. The height and pitch of your roof are also important factors because there are additional safety and labor costs to consider.

The average cost to replace a roof is approximately $11,500 on average, but the price could range from $6,700 to $80,000.

When creating an estimate, roofers sometimes define costs per roofing square. One roofing square is equal to a 10-by-10-foot (100 square feet) area. So a 1,700-square-foot roof would be 17 squares. Currently, squares can range in price from $450 to $750, depending on materials and other costs. 💡 Quick Tip: A low-interest personal loan can consolidate your debts, lower your monthly payments, and help you get out of debt sooner.

Getting a New Roof

Some pointers on getting a new roof:

• If you are replacing your roof as a part of general home maintenance, you may have a little more time to prepare for the costs associated with the repairs. It allows you to be more methodical about pricing the project out and selecting a roofer. And having a bit of a runway will allow you to start saving and develop a workable budget for the project.

• Get an estimate from several reputable contractors. When doing so, be sure to pay close attention to the quality of the materials specified in the estimate. It’s even better if you can get a recommendation from someone you know. Regardless, definitely check reviews and references carefully.

• Remember that, while a new roof can be a major expense, it can improve the value of your home for future sale, stave off ongoing repairs from leaks, and, of course, protect the residents.

Paying for Roof Repairs

If your roof is damaged, then you are faced with a different challenge than figuring the roof replacement cost.

• In the case of a natural disaster caused by an earthquake or hurricanes, you may even be eligible for help from the Federal Emergency Management Agency“>Federal Emergency Management Agency (FEMA). Whatever the cause, it could be helpful to take photographs sooner rather than later to document the damage.

• Your homeowners’ policy or home warranty may include coverage that could possibly help defray some of the costs, depending on the cause of the damage and the age of the roof.

• If it’s determined that the damage is from normal wear and tear, then it will likely be considered regular maintenance and may not be covered. Many roofing jobs fall into that common home repair category.

• Also, if your roof is older than 10 years, you may only be eligible for part of the cost determined to be a depreciated value of the roof. Whatever the circumstance, it could be worthwhile to call your insurance company and find out if you’re covered and to what extent.

• And, before you start work, it bears repeating that it’s wise to get multiple estimates to help you make an informed decision and ensure that you’re getting the most value for your investment. You may want to consult with a few licensed roofing contractors and compare bids.

Recommended: How to Pay for Emergency Home Repairs

Ways to Help Pay for Home Repairs

Whether you are replacing your entire roof or just replacing a damaged portion, you may want to consider financing all or part of the work. One option worth considering: a personal loan.

• A personal loan can be a good option for some homeowners. With a personal loan, you’ll usually get a lower interest rate than credit cards. Also, with an unsecured personal loan, there typically is no additional lien against your property. Often, these loans can be processed quickly and with minimal fees.

• Another financing option homeowners turn to for home improvements is a home equity loan or a home equity line of credit (HELOC). The application for a HELOC is akin to that of a mortgage. How much you’re able to borrow depends on several factors, including the value of your home. You may also have to arrange and pay for a home appraisal.

As you consider your costs associated with a roofing or other home project, you may want to use a home improvement cost calculator to help you budget appropriately.

The Takeaway

Replacing your home’s roof is typically a big-budget home repair project; it often costs in the five-figure range. However, it’s an important investment in your home’s value and integrity. You can look into financing options such as HELOCs and personal loans to help you pay for the work.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

As Florida’s insurance crisis makes hurricane hardening more important than ever, consumer advocates have pressed to reign in a popular — but controversial — loan program that allows homeowners to pay for new roofs or impact windows through their property tax bills.

Some counties and tax collectors across the state have pushed for clearer disclosures for a program that has generated hundreds of complaints from people who say they were misled on costs or didn’t understand that the loan amounts to a long-term tax lien on their home.

Now, one agency that bankrolls construction projects for the Property Assessed Clean Energy program, known commonly as PACE, is pushing back — arguing that individual counties have no legal right to force it to follow additional rules or even decide where it can operate.

The fight has led to a high-stakes lawsuit that includes nearly half the counties in the state, several of which have blasted the continued operations of a single quasi-governmental agency in Northeast Florida as “an immediate danger to the health, safety or welfare” of residents. Tax collectors from Alachua County to Palm Beach have complained in emails and court records that the Florida PACE Funding Agency’s statewide expansion is “running roughshod” over local government rights. For now, Broward and Miami-Dade are staying out of it, but the outcome has big implications for two counties that lead the state in PACE contracts.

The case in Tallahassee shapes up as a major legal test for the few but hard-won consumer protections already in place across the state, including new ones in Miami-Dade County, and, perhaps, the future of Florida’s PACE program.

And it could also impact nearly 13,000 property owners across Florida who’ve recently signed agreements with Florida PACE Funding Agency for more than $500 million in home improvement projects — with no guarantee that the tax-lien arrangement they agreed to will stick. Potentially, they could be hit with big bills from contractors or lenders instead.

The Florida PACE Funding Agency, meanwhile, has launched its own public relations offensive, taken multiple tax collectors to court and vowed to take the case to Florida’s Supreme Court if the judge doesn’t rule its way.

Mike Moran, executive director of Florida PACE, strongly defends his agency’s actions as well as the industry itself. He argues his quasi-governmental agency has its own authority to levy property taxes. He paints the agency’s statewide expansion as a plus for the state and consumers, an opportunity for people who might not otherwise qualify for conventional loans to make crucial home repairs at a cheaper price (usually 9 to 11% interest) than a credit card.

“I can’t finance because you don’t like your kitchen counter top. It has to be a public purpose, home hardening and energy efficiency,” he said. “If you take this option away, they’re just going to put it on a 29% credit card.”

Follow trends affecting the local economy

Subscribe to our free Business by the Bay newsletter

We’ll break down the latest business and consumer news and insights you need to know every Wednesday.

Loading…

You’re all signed up!

Want more of our free, weekly newsletters in your inbox? Let’s get started.

Explore all your options

Going rogue

Up until last year, the PACE program worked like this: groups like the Florida PACE Agency, which serve as middlemen between homeowners and loan companies like FortiFi and Home Run Financing, needed a county’s permission to work within its boundaries.

Unlike a traditional bank loan, which is based on credit and financial records, PACE agreements are based on home equity. In exchange for the cash to complete a construction project, PACE providers put a lien on the property and collect annual payments through the property tax bill, which is gathered by a county property tax collector.

The bump to the tax bill can be steep, in some cases a 200% to 300% rise, and unlike a loan from a bank, failing to pay a tax bill can lead to foreclosure.

As the program grew in popularity across Florida in the last decade, tax collectors started hearing complaints from residents who didn’t understand why their tax bills had risen so steeply, or believed they had been signed up for the program under false pretenses by contractors.

In response, several counties passed new consumer protections like limiting loans to the lifespan of the product, requiring recorded phone calls and more thorough disclosure forms. Others did nothing, leaving a patchwork of protections across the state.

Then, starting in January, the Florida PACE Funding Agency abruptly announced that it no longer had to follow any of those rules, thanks to a Leon County judge’s ruling.

A ruling changes landscape

It was supposed to be a routine hearing, the same kind PACE agencies across Florida regularly attend to ensure they’re checking the right financial boxes. But instead of just asking the judge if his bond documents were in order, Moran asked the judge to rule on whether Florida PACE needed permission from a local government to operate within its borders.

In his ruling, the judge said no, they didn’t need permission.

Moran said that gives Florida PACE Funding Agency the right to operate in any county in Florida, including those that have explicitly banned the program.

“We do all of those consumer protections. There’s not a single one that someone asked us to do that we aren’t doing,” he told the Miami Herald. In court records, however, Alachua County said Moran “vehemently” fought a new consumer protection it tried to enact in 2022, and Leon County said Moran negotiated with the county to tweak some of its proposed protections the same year.

Tax collectors stop collecting

Tax collectors across the state have fought Moran’s moves. They sent cease and desist letters, passed county commission resolutions and called in county attorneys and legislators. At least 30 tax collectors have joined a lawsuit against Florida PACE over the issue.

“What a judge did in Tallahassee should never have happened in a bond-type hearing,” said Mike Fasano, Pasco County’s tax collector and a longtime vocal critic of PACE. “That’s not what the Legislature had any intent of happening. There was always supposed to be this interlocal agreement.”

As the fight spread to new counties, Florida PACE continued to sign up thousands of homeowners in counties across the state without their permission, including Alachua, Hillsborough and Palm Beach.

In response, some tax collectors said they weren’t going to collect the PACE assessments tacked on to their residents’ tax bills.

“I believe the responsibility tax collectors have is we’re only going to collect what is proper and authorized on the tax rolls. As it stands right now, these assessments are not proper or authorized, so they’re not getting collected,” Rob Stoneburner, Collier County’s tax collector, told the Herald.

That left Florida PACE scrambling to recoup its investments and quell questions from its investors. In an October news release, Moran said bondholders and private investors withdrew funding from Florida.

“The consequences of this withdrawal are far-reaching, impacting tens of millions of dollars that were to be used to pay contractors who have recently completed or are currently working on renovation projects. Furthermore, many ongoing projects face uncertainty, potentially leaving homeowners in a precarious financial situation,” he wrote.

At that, Moran sued.

He took multiple tax collectors to court to force them to collect the assessments he insists are legally valid, based on the Leon County ruling. So far, judges have agreed with his argument in some counties, including Hernando and Sarasota, where he is chairperson of the county commission and is running for tax collector, and disagreed in others, including Alachua, Bradford and Hillsborough.

“We don’t do ‘mother may I’ to another governmental authority to tell them to put it on the tax bill, we are the governmental authority,” Moran said. “There are a billion dollars of bondholders on the street in Florida that need to be paid back, and property tax collectors need to put this on the tax bill. That is not a complicated discussion.”

What the courts say

Experts say this drama will end in two ways. Either a judge rules that Moran is right or wrong, or the Florida Legislature tweaks the rules of PACE to resolve the dispute.

Stoneburner, the tax collector from Collier, said tax collectors across the state need “a clear answer” on whether or not Florida PACE needs permission from a county to operate there.

“Either they’re right or they’re not right. If they’re right, OK, in my mind it’s going to be the Wild West because then all the other PACE providers will do the same type of thing, they’re going to operate however they want,” he said.

But Moran said that even if the Legislature moves to fix the issue in the upcoming session — or get rid of PACE entirely — he still wants the courts to weigh in.

“If that curtain went down and PACE is gone, you still have that billion dollars of bondholders that need to get paid back,” he said.

That decision could come as soon as February, when the same Leon County judge whose ruling set off the crisis has agreed to revisit the discussion, after a legal push from at least 30 tax collectors across the state.

Moving is part of most people’s lives. Maybe you’re heading to grad school a couple of towns away. Or perhaps you have a job offer hundreds of miles away that you’re excited to accept.

Whatever the reason, the logistics of getting your stuff from the old place to the new one will need wrangling. Here, you’ll learn more about your options for moving, how much it may cost (from a couple of hundred dollars to thousands), and how to afford the expense.

DIY Moving Costs

Yes, you could move yourself. This could be a smart move for a small, local move, and it can help keep costs within your budget.

Exactly how much this might cost will be based on several factors:

• Cost of transportation (can you borrow a friend’s van or do you need to rent one)?

• Cost of the packing materials you use (recycled boxes and old newspapers vs. the pros’ higher-end and job-specific supplies

• How much stuff you’re moving (and if you need to figure out insurance for any pricey items)

• How far you’re going

• Whether you need to store some things temporarily.

As you might guess, packing up the contents of a dorm room and moving it half a mile away to the apartment you’re renting with friends will cost one amount. Supplies might cost, say, $65.

Loading up the contents of the sweet bungalow you’ve been living in for a couple of years and depositing your worldly possessions at a new place 1,000 miles away will be a much more involved and expensive undertaking. Packing materials alone could be a few or several hundred dollars, and renting a moving truck could be anywhere from $20 to $100 per day, depending on your local cost of living. Also, you will likely have to pay to stay somewhere overnight and also spend at least a couple of hundred dollars on gas, dollies, and insurance. 💡 Quick Tip: Some personal loan lenders can release your funds as quickly as the same day your loan is approved.

Full Service Moving Costs

If you decide a full-service move best meets your needs, you’re probably going to want to gather some estimates, so you can nail down the details and be ready when it’s time to go. Some pointers as you do so:

• Also, do check ratings and references carefully. There are plenty of instances of fraud and scams in this realm, and it’s wise to protect yourself.

• Booking your truck four to eight weeks in advance is typically a good rule of thumb — maybe even further out if you’re moving in the busy summer months.

• Professional moving companies can give you an estimate based largely on how many rooms of furniture you have. Most have websites, so you can often get a quick estimate online. A typical local (or fairly local, not long-haul) move for a three-bedroom home is about $2,100.

The average moving costs if you relocate cross-country can easily be twice that, or $4,300 for a distance of about 1,225 miles. Keep in mind, specifics will vary. Oversized or extremely heavy items might cost you extra — as could lots of stairs, or things that need to be taken apart and put back together.

Recommended: Average Personal Loan Rates

Extra Moving Costs to Think About

Then there are the extras that go along with getting out of one place and into another.

• Transportation: If you’re taking your car across the country, you’ll probably want to get a tune-up before you go. And then there’s gas, hotel stays, and eating on the road. Having a car transported instead of driving it yourself could cost anywhere from $700 to $2,000.

If you’re in a hurry and decide to fly, that’s another expense. And if you’re taking a pet, you may have to add a little bit more to your overall bill, depending on the mode of transportation you choose for your furry friend.

• Getting into your new home: Don’t forget about deposits you might have to make at your new location. That could be anything from first and last month’s rent and a pet deposit at a new apartment, to utility deposits at a new house.

• Home repairs and cleaning: Be ready to pay for some home repairs on both ends of your move. You may have to make some quick fixes to get out of your rental without losing the deposit or maybe even major repairs if you’re selling a home. When you get to your new location, you could find some unexpected problems. Or you may just want to hire someone to come in and clean so you can cross that off your ever-growing moving to-do list.

• Starting out fresh: You’ll probably need to buy some things at your new home (like curtains, curtain rods, hangers, bedding, etc.) that are easily overlooked. Then there’s that fridge to fill. All those little costs can add up.

• Cash for tips: You will likely need to withdraw money from an ATM to thank people for their help when you move. Tips for the movers. Tips for the handyman or housekeeper who helps you get things in shape. Tips at your hotel. Tips for waitstaff at the restaurants you’ll be eating at until you get your new place up and running—or at the very least, tips for the pizza delivery guy.

Recommended: Typical Personal Loan Requirements Needed for Approval

Financing Your Move

If you have enough room on multiple credit cards, you could go that route, but should you? Interest rates can be considerable.

Or would a personal loan make more sense for you to cover all those costs, big and small?

Remember, even if you’ll be reimbursed by your employer or plan to take some moving deductions when you file your tax return, it’s very likely you’ll be paying at least some moving costs up front. And the longer those expenses sit on a credit card, the more interest racks up.

The Takeaway

Even if you have a small amount of stuff and aren’t moving very far, moving takes time, energy, organization, and money. With the average professional move costing a couple of thousand dollars, you may want to plan carefully for this expense. It’s likely not a good reason to dip into your emergency fund, so you may want to save in advance or consider a personal loan. If you qualify for a personal loan, your interest rate may be lower than a credit card, which can free up some cash and reduce your money stress.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Inside: Learn how many months it usually takes for your budget to start working effectively. Plus explore successful budgeting strategies.

Learning to budget can often be a challenging process, but its benefits are irreplaceable. Initially, it might feel overwhelming, as it involves accounting for every small expenditure, adhering to a fixed financial plan, and exercising self-control.

The frustration often emerges from unexpected expenses or changes in income, like getting a raise or having to make a new car loan payment.

However, this ongoing process ultimately fosters financial discipline, enables goal-setting, offers a clear financial picture, and encourages proactive handling of money matters, making the frustration worthwhile.

According to experts, it could take up to three months to adapt to a new budget.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

The Essential Role of Budgeting

Financial budgeting plays a critical role in managing resources efficiently, informing financial goals, prioritizing initiatives, optimizing financing opportunities, and offering flexibility in various situations.

These reasons make it a highly regarded tool in business and personal finance.

Defining Financial Budgeting

Financial budgeting is a systematic approach to managing your finances by mapping out your income and expenditures over a designated period.

This process provides a framework to guide your financial decisions, which aids in achieving your monetary objectives.

It’s essentially an overview of your financial position, goals, and cash flows.

How many months does it usually take for your budget to start working as a budget should?

As per our expert opinion, it typically takes around three months for a budget to start functioning effectively.

When starting a new budget, it’s normal not to see results immediately.

This time frame allows for adjusting to new spending habits, dealing with unexpected costs, and instilling a sense of discipline and control over your finances. Remember, budgeting requires patience and commitment.

Practicing Efficient Budgeting Techniques

Now, the key to being successful is having a few budgeting tricks up your sleeve.

I can guarantee you that budgeting is actually freeing. This is how you do it!

The Process of Getting One Month Ahead

Getting one month ahead in your financial budgeting means living off last month’s income.

In this practice, you pay November’s bills with October’s income, for example, essentially preventing you from spending money you haven’t earned yet.

To set up this process, create a monthly budget, determine your income and expenditures, establish your spending goals, and ensure your income exceeds your spending. More than likely, you will have to save money to get one month ahead of bills completely. YNAB can help you with this.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

Familiarizing with Zero-Based Budgeting

Zero-based budgeting is a method where every penny of your income is allocated to different categories, from necessary and discretionary spending to savings and debt payments.

You start each month with a fresh budget, balancing out your expenses and income to zero. This approach demands meticulous attention to detail and is best suited for individuals with a fixed income and predictable expenses.

Executing the Envelope Method

The envelope method involves assigning an envelope (physical or digital) to each spending category, such as grocery or utilities, and putting cash into each envelope for planned expenditure. Once the cash in an envelope finishes, it means you’ve exhausted your budget for that category.

This method, as per expert suggestion, instills discipline and curbs overspending, making it an ideal choice for cash-driven individuals. Connecting this method with digital tracking systems is possible with the cashless envelope system to cater to those using debit or credit cards.

12 Effective Strategies to Make Budgets Work

These strategies not only allow the allocation of resources efficiently, but also help set realistic financial goals, prioritize projects based on their potential cash flow, and explore optimal chances to reach financial independence.

Moreover, having a budgeting plan in place also ensures flexibility to adjust to unanticipated financial challenges, contributing to long-term wealth creation.

1. Determine Goals and Objectives

Start your budgeting process by clearly defining your financial goals and objectives. Are you aiming to buy a new home, fund your education, or build an emergency fund?

Whatever aspiration you have, short- or long-term, incorporating them into your budget amplifies your drive and focus on achieving them.

This goal-driven strategy aligns your budgeting with your needs and wishes, creating a financial roadmap toward your envisioned milestones. Consider these smart financial goals to get you started.

2. Better Planning, Fewer Surprises

Planning your budget effectively requires a thorough consideration of all personal budget categories.

Also, incorporate both short and long-term financial goals into your budget by prioritizing them, such as purchasing a home, taking a vacation, or furthering your education. Regularly reviewing and adjusting your budget accordingly, based on changes in income or unexpected expenses, can also ensure you stay on track.

Utilizing a variety of budgeting tools, like spreadsheets, apps, or budgeting software, can simplify this process and help keep you accountable.

Quicken

Personal finance and money management software allows you to manage spending, create monthly budgets, track investments, retirement and more.

I have used this platform for over 20 years now.

Pros:

Birds-eye view of your complete financial picture.

Conveniently download your spending activities, and automatically categorize them (Quicken connects to over 14,000 financial institutions).

Track investments with it’s features like portfolio analytics, retirement goals, and market comparison.

Cons:

Little complex to use at first, the learning curve is moderate.

Yearly subscription-based model to use the platform.

Save 40% on New Memberships

Our Review

3. Reduced Financial Stress through Budgeting

A successfully implemented budget significantly reduces financial stress by providing an accurate picture of your financial health.

With a well-defined budget, worries about overspending, living from paycheck to paycheck, or falling into debt diminish. Monitoring and updating your budget will allow you to feel more confident and secure about your financial standing, paving the way to monetary stability.

4. Deciding When to Review Your Budget More Frequently

An effective budget is not a set-and-forget one; it requires regular check-ins and updates. A bill calendar is very helpful.

A recommended starting point is a monthly review. However, when first starting out, you will need to review your budget monthly until you find it working for you.

Other situations may need more frequent check-ins according to changes in income, financial goals, or unexpected expenses.

5. Spot Potential Room for Improvement

Budgeting provides a realistic view of your spending patterns, allowing you to identify areas of improvement.

Upon reviewing your budget, you might notice unnecessary expenditures or categories where expenses consistently exceed budgeted amounts. Such insights help you re-evaluate your spending habits and update your budget accordingly.

This phase coupled with a no spend challenge involves being brutally honest with yourself, taking into account your needs, wants, and financial realities.

6. Analyze Your Expenses and Income

Critical examination of your income and expenses is crucial for successful budgeting. Begin by calculating your total income, then list and categorize your monthly expenses into fixed and variable.

Pinpointing the difference between the totals can highlight whether you’re living within your means.

If your income surpasses your spending, consider investing the surplus.

Conversely, if your expenses outnumber your earnings, think about ways to increase income or decrease spending.

7. Set Limits for Your Budget Items

Setting reasonable spending limits for your budget categories ensures financial discipline. Check each category of spending—groceries, entertainment, or personal care, for instance—and contemplate areas you can cut back.

Ask around to see how much others are spending in certain categories in your neighborhood.

Remember, your budget should be flexible and realistic to your lifestyle, ensuring you don’t feel deprived. Embed small “wants” into your budget to keep the whole process enjoyable and sustainable.

simplifi

Manage your money less in 5 minutes each week.

Reach your money goals with confidence!

“The easiest, most comprehensive way to both see where your money is going and plan for future expenses.”

Start FREE Trial

8. Create a System for Tracking Your Expenses

Creating an efficient system for tracking expenses is vital to maintaining control over your finances. This could be a simple spreadsheet, a manual ledger, or budgeting apps on your smartphone.

Tally every cent spent, dividing your expenses into their respective categories—rent, food, clothing, utilities, etc.

This way, you get a detailed insight into your financial habits and can identify potential areas for savings. The method isn’t as important as its thoroughness in ensuring no expense gets overlooked.

9. Track Your Spending with a Spreadsheet

Spreadsheets are an optimal resource for tracking spending. You can utilize an online template, like Tally, or make one yourself from scratch.

As you spend, record each transaction under the fitting category. This real-time monitoring can help spot overspending, analyze spending habits, and adjust budgets as needed.

So, if you’re a whiz with Excel or Google Sheets, tracking expenses this way might be your best bet.

Tiller Money

Your financial life in a spreadsheet, automatically updated each day.

Tiller is the fastest, easiest way to manage your money with the unlimited flexibility of a spreadsheet.

Update your finances in one place, so you can take control of spending, optimize cash flow, and confidently plan your financial future.

Pros:

Tiller automatically updates Google Sheets and Microsoft Excel with your latest spending, balances, and transactions each day.

No more tedious data entry, CSV files, or logging into multiple accounts.

You can customize everything and finally track your money, your way.

Try Tiller Free

10. Budget for Emergencies

Budgeting for the unexpected is an essential aspect of sound financial planning. Financial emergencies don’t knock before they occur; therefore, creating a buffer in your budget helps you face them without plunging into debt.

As an expert, we suggest an emergency fund of one month of income or at least $1000. Then, start a rainy day fund with three to six months of expenses.

Having these funds built into your budget ensures you’re financially covered for challenging situations such as job loss, medical emergencies, or sudden home repairs.

11. Talk to Your Family About Your Budget

Talking to your family about your budget ensures everyone understands and works towards your financial goals. This discussion becomes especially crucial if you’re budgeting for a household.

I always provide my family with an overview of the budget, explaining how it works and how we can achieve our goals. Being open about your financial plan can foster greater accountability, and cooperation to achieve shared financial objectives more seamlessly.

12. Look for Ways to Make Money

Increasing your income can be an effective strategy to make your budget work better, rather than solely focusing on cutting expenses.

By finding ways to earn more money, for example by taking a part-time job, freelancing, selling unused items, or investing, you add flexibility to your budget and reduce the pressure on spending.

Moreover, the additional income could be directed towards savings, debt repayment, or funding your personal goals as identified in your budget plan.

Financial Budgeting FAQs

Starting a budget begins by assessing your total income, followed by identifying and categorizing your expenses.

Once done, subtract your expenses from your income to understand your financial standing.

Next, set your financial goals—short term and long term.

Then, allocate your earnings across different categories, maintaining a balance between savings, expenditures, and other aspirations.

Review and adjust this plan periodically to ensure it aligns with your financial landscape.

Budgeting should ideally start as soon as a person starts earning money. It’s never too early to begin planning where your money should go, and late starters can still benefit significantly.

Budgeting is a lifelong practice that guides you to live within your means, handle emergencies smoothly, and achieve your financial goals efficiently. It’s an indispensable tool for ensuring monetary success and stability.

Successful Budgeting as an Essential Life Skill

Successful budgeting is undeniably an essential life skill. It not only helps you live within your means but also provides a clear direction towards your financial goals.

Mastering this skill early on can lead to effective financial decision-making, lesser financial stress, and a more secure way of life.

There will be fluctuations in your budgeting, so you can start to forecast your budget. It also reinforces the value of discipline and planning, offering improved self-management and positive monetary habits.

Ultimately, progressing from just surviving to thriving financially is the goal, and disciplined budgeting is a tool to get you there.

This is just one step towards becoming financially independent.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

As interest rates increased rapidly throughout 2022, the number of refinance mortgage originations declined. The composition of these refinances also changed. Cash-out refinances – where a homeowner borrows an amount substantially greater than what they owe on their existing mortgage – became more common than non-cash-out (also known as “rate-and-term”) refinances. An equity “cashed out” from the home – which, in turn, increases the mortgage balance – is often used by the borrower to pay down other debts, fund home repairs, and pay for educational expenses, among other big-ticket purchases. A cash-out refinance takes the place of the original mortgage, but alternative products that tap home equity, such as home equity loans and home equity lines of credit, leave the original first-lien mortgage intact. Such needs for cash may be necessary and unavoidable, hence the persistence of some (albeit reduced) amount of cash-out refinances even in the face of rising interest rates.

Despite the recent decrease in volume, cash-out refinance originations are a segment of the mortgage market worth monitoring, especially since they were considered one of the mechanisms that exacerbated the 2008 financial crisis.1 In the case of both cash-out and non-cash-out refinances, the borrower’s home is used as collateral for the loan. Failing to make payments or meet other loan conditions can result in the borrower losing their home through foreclosure. The added risk for borrowers originating a cash-out refinance, especially in today’s interest-rate environment, is that their mortgage payments and mortgage loan terms are both likely to increase.

Who are the homeowners taking out cash-out refinances, and are their loans comparable to non-cash-out refinance loans? Are cash-out refinance borrowers more likely to become delinquent? In this post, we look at the loan and borrower characteristics of homeowners who originated a cash-out refinance compared to a non-cash-out refinance. We study refinances originated between 2013 and 2023. This allows us to study delinquencies—one manifestation of risk—throughout the post-crisis period, and how they vary among the population. This period includes periods of falling and rising interest rates, as we have observed recently. With this information, we can better gauge the risk to consumers and the housing market of the recent trends in refinances. We find that:

Cash-out refinances were a larger share of all refinances during periods of rising interest rates.

Borrowers of cash-out refinances had lower credit scores, lower incomes, and smaller loan amounts compared to non-cash-out refinance borrowers.

Loan-to-value and debt-to-income ratios were similar for cash-out and non-cash-out refinances.

Cash-out refinances had larger shares of older, female, Black, and Hispanic borrowers, compared to non-cash-out refinances.

Serious delinquencies were rare for borrowers with higher credit scores, regardless of whether the refinance was cash-out or not.

For borrowers with lower credit scores, both cash-out and non-cash-out refinance borrowers have similar two-year delinquency rates, except for a relative increase in delinquencies among cash-out refinance borrowers in 2017—a year marked by rising interest rates.

We conclude with a comparison of the market for cash-out refinances before the financial crisis to the post-crisis time period, as well as potential concerns with cash-out refinances to monitor going forward.

Loan and borrower characteristics of refinances

We used refinance data in the National Mortgage Database to compare the loan characteristics and two-year delinquency status of cash-out refinances and non-cash-out refinances. The National Mortgage Database is a representative 1-in-20 sample of all closed-end first-lien mortgages in the United States. We identify refinances as cash-out refinance mortgages when the total value of sampled refinance loans and their associated junior liens were more than five percent larger than the total value of the preceding loans and associated junior liens.

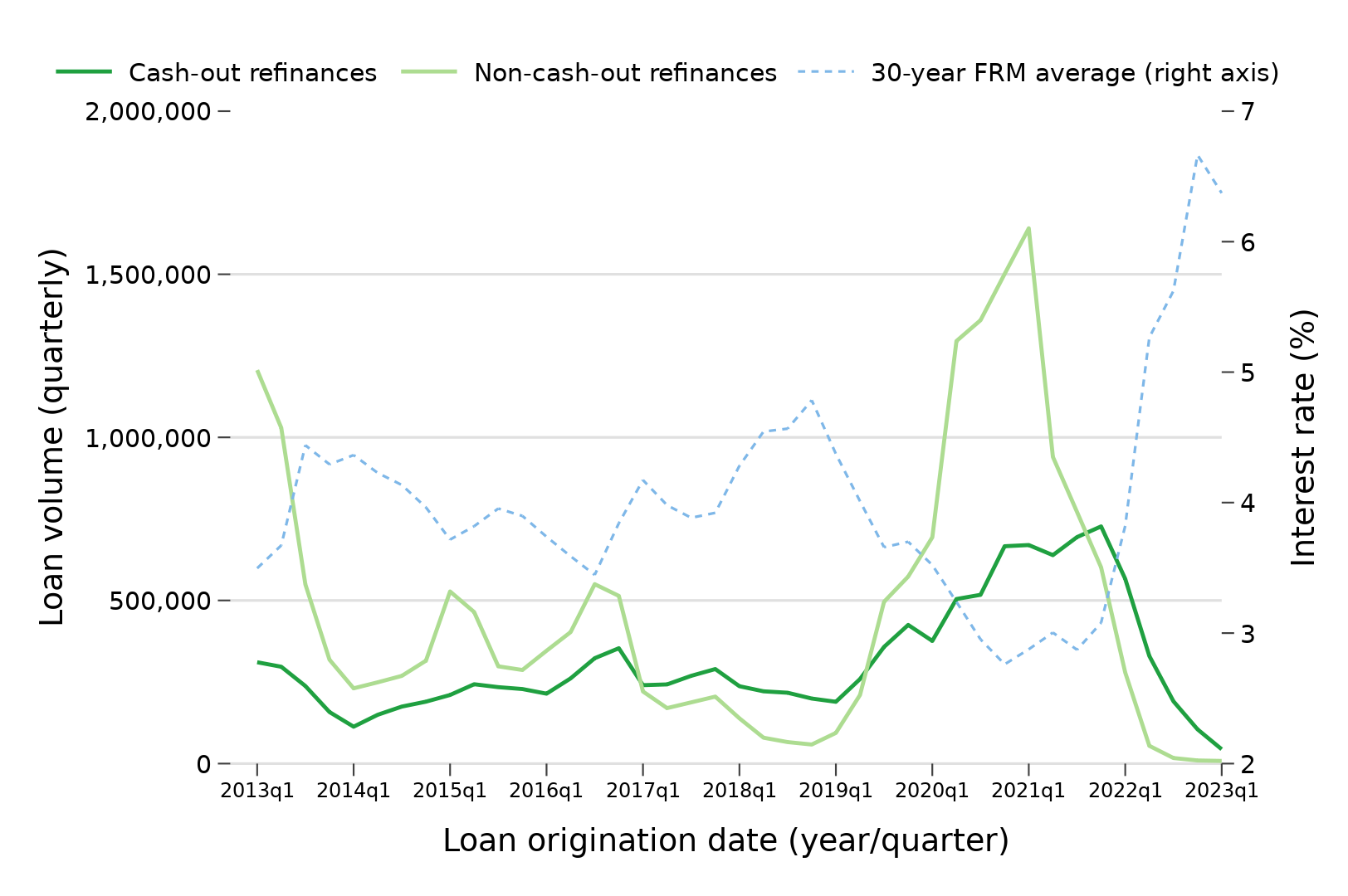

Figure 1 shows the quarterly volume of refinances, cash-out and non-cash-out, from the first quarter of 2013 through the first quarter of 2023 (the latest quarter for which we have data). We added the average interest rate on 30-year fixed-rate mortgages from Freddie Mac’s Primary Mortgage Market Survey on the right axis.

As Figure 1 indicates, non-cash-out refinances are typically more common when interest rates are decreasing and borrowers seek better rates compared to their original mortgages. Cash-out refinances make up a larger proportion of all refinances during periods when interest rates are increasing, such as 2017 to 2019 and 2022 to 2023. For example, from 2013 to 2019, cash-out refinances averaged about 240,000 originations per quarter, followed by an increase to almost 730,000 in the fourth quarter of 2021. Cash-out refinance volumes then fell throughout 2022, down to 44,000 originations in the first quarter of 2023.

Figure 1: Quarterly volume of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 2 plots median credit scores by refinance type. The median credit scores of cash-out refinance borrowers were lower than non-cash-out refinance borrowers throughout the 2013-2023 period.

Figure 2: Median credit score at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Figure 3 plots median combined loan-to-value ratios (100 percent less borrower equity in the house) by refinance type. The median combined loan-to-value ratios for cash-out refinances are generally similar to or lower than non-cash-out refinances originated in the same period, except during high interest-rate periods from 2017 to 2019 and 2022 to 2023, when median combined loan-to-value ratios for cash-out refinances are relatively higher than non-cash-out refinances.

Figure 3: Median combined loan-to-value ratio at origination of cash-out versus non-cash-out refinances, 2013-2023

Source: National Mortgage Database

Table 1 describes other loan and borrower characteristics of cash-out and non-cash-out refinances originated between 2013 and 2023. We see that the median loan amount and borrower incomes for cash-out refinances were smaller than for non-cash-out refinances; the primary borrowers for cash-out refinances were older; and cash-out refinances were more likely to only have female borrowers and borrowers aged 62 and older. Cash-out refinance borrowers were also more likely to be Hispanic or Black and less likely to be Asian, compared to non-cash-out refinance borrowers.

Table 1: Loan and borrower characteristics by cash-out versus non-cash-out refinances

Loan/borrower characteristics

Cash-out refinances

Non-cash-out refinances

Loan amount (median)

$198,000

$241,700

Cash-out amount (median)

$37,131

N/A

Interest rate (median)

3.62%

3.38%

Combined loan-to-value ratio (median)

70

72

Debt-to-income ratio (median)

36

34

Borrower income (median)

$84,000

$102,000

Credit score (median)

741

765

Age of primary borrower (median)

51

47

Share of refinances with only female borrowers (%)

22.8

18.8

Share of refinances with only age 62 and older borrowers (%)

21.1

15.0

Share of refinances with any Hispanic borrower (%)

10.5

9.6

Share of refinances with any Black borrower (%)

9.1

7.5

Share of refinances with any Asian borrower (%)

4.7

9.8

Share of refinances with any American Indian borrower (%)

0.7

0.5

Share of refinances with any Native Hawaiian/Pacific Islander borrower (%)

0.7

0.8

Share of refinances with any borrower listing two or more races (%)

1.9

1.7

Observations (N)

641,657

957,748

Note: Sample includes refinance mortgages that were opened between the first quarter of 2013 and the first quarter of 2023. A cash-out refinance is identified when the total value of the sampled refinance loan and their associated junior liens was more than five percent larger than its preceding loan and associated junior liens. “Only female (or only age 62 and older) borrowers” means that for loans with only one borrower, that borrower is female (or age 62 and older), and for loans with multiple co-borrowers, that all co-borrowers are female (or age 62 and older). Source: National Mortgage Database.

Delinquencies of refinanced mortgages: the importance of borrowers’ credit scores

In terms of delinquencies at the two-year mark after their refinance loan origination, Figure 4 shows two-year delinquency rates of refinances, by year originated, from 2013 to 2020. We use a broad measure of delinquency: 60 or more days past due, including other adverse conditions such as bankruptcy and foreclosure. We also split the sample by credit score: refinances with a borrower credit score at or below the median credit score of 756 at origination (left panel) compared to refinances with a borrower credit score above the median (right panel).

Figure 4: Rates of serious delinquency (60+ days or worse) two years after origination for cash-out versus non-cash-out refinance borrowers

Source: National Mortgage Database.

We first see that serious delinquencies two years after origination are rare among both types of refinances involving borrowers with higher credit scores: no higher than 0.1 percent for originations between 2013 and 2020. By contrast, serious delinquencies are more likely among refinances involving borrowers with lower credit scores but are still uncommon in absolute terms: ranging between 0.7 and 0.8 percent for all refinances originated between 2013 and 2016, followed by an increase in 2017 to 1 percent for cash-out refinances and 0.9 percent for non-cash out refinances.2 Two-year delinquency rates then fall among all refinances with lower credit scores originated after 2018, likely due to mortgage forbearance programs in the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Worth noting is the increase in two-year delinquency rates for cash-out refinances originated in 2017. We know that these borrowers refinanced at a time when interest rates were rising (see Figure 1), and that credit scores were lower overall for cash-out borrowers in 2017 compared to previous years (see Figure 2). These findings from 2017 suggest that we may see increased delinquencies among cash-out refinance mortgages originated in 2022, another period with an increase in interest rates and a decrease in cash-out borrowers’ credit scores.

Discussion and potential concerns with cash-out refinances

In summary, during periods of rising interest rates, refinance volume declines and their composition shifts toward cash-out refinances, since homeowners may need cash from their home even when interest rates increase. From the first quarter of 2013 to the first quarter of 2023, cash-out refinances tended to have smaller loan amounts, lower borrower incomes, and lower borrower credit scores compared to non-cash-out refinances, but other loan characteristics, such as loan-to-value and debt-to-income ratios, were similar. We then showed that two-year delinquency rates were similar between both types of refinances, with only a noticeable increase for lower credit-score borrowers taking out cash-out refinances in 2017.

Prior research has focused on cash-out refinances as one of the mechanisms that exacerbated the 2008 financial crisis. However, mortgage originations from 2013 to 2023 are fundamentally different from mortgage underwriting before the financial crisis. Many risky features are now absent from the market – for example, interest-only mortgages, negative amortization mortgages, and mortgages with loan-to-value ratios over 100 percent – and lenders are now required to document borrowers’ ability to repay their loans. As we have shown above, most cash-out refinances now have loan-to-value ratios below 80 percent, requiring a 20 percent or more drop in house prices to be underwater. Most cash-out amounts are also below $50,000 during this period, and the volume of cash-out refinances has been declining each quarter since the start of 2022. Although cash-out refinances gained popularity from 2019 to 2021 due to record-low interest rates , the amount of equity extracted was lower than during the pre-2008 boom, despite home prices having increased substantially. These characteristics of cash-out refinances over the past decade suggest that cash-out refinances are now a smaller source of systemic risk than before the 2008 financial crisis.

Beyond the potential systemic risk of equity extraction contributing to a new financial crisis, cash-out refinances present at least two other concerns for borrowers. First, research from the JPMorgan Chase Institute showed that a typical cash-out refinance in their data had a longer loan term and larger monthly payment compared to the paid-off mortgage. This suggests that cash-out borrowers are more likely to still be paying off their mortgage and less likely to own their home free and clear in retirement, potentially exposing these borrowers to more future financial shocks while the mortgage is outstanding. Second, a cash-out refinance with a higher interest rate than the prior paid-off mortgage could effectively lead to much higher borrowing costs, relative to the original mortgage or to other sources of credit, like home equity loans or home equity lines of credit, that do not raise the interest rate on the existing first-lien loan balance.3 Prior research has shown that higher interest rates can cause delinquency and default.4 This relationship highlights the importance for borrowers of finding and obtaining lower interest-rate loans, and aligns with efforts to help borrowers refinance when interest rates fall as a way to avoid delinquencies.

As the interest-rate environment continues to evolve, the CFPB’s Office of Research will continue analyzing mortgage refinances and other home equity loan products to understand consumers’ borrowing decisions and loan performance.

Many people want to buy a home but think it isn’t possible because they don’t have money to put toward a down payment. Traditionally, lenders require a 20% down payment toward your mortgage.

But a 20% down payment adds up to a lot of money. For example, if you plan to purchase a $150,000 home, you’d need to come up with a $30,000 down payment. Many people cannot afford this, but fortunately, the 20% rule is a lot less common than you might think.

Is a buying a house with no money down possible?

The National Association of Realtors (NAR) reports that 39% of non-owners believe they need a 20% down payment or more and 22% believe they need a 10% to 14% down payment.

But neither of these are true. Many mortgage lenders will let you buy a home by putting down as little as 3%. And some lenders will let you skip the down payment altogether.

NAR also found that 61% of first-time homebuyers made a down payment between zero and 6%. So, it’s safe to say that a 20% down payment isn’t the standard anymore. But unfortunately, many consumers choose not to pursue homeownership because they believe this down payment myth.

Weighing the Pros and Cons of No Down Payment Mortgages

Is there any reason to aim for 20% down when most home buyers buy with a down payment less than 20%? If you can afford it, yes, the 20% rule is still a wise choice.

The more money you put toward your mortgage, the less debt you’ll have to repay and the less your monthly payment will be. Plus, there are several drawbacks to putting down less than 20%:

Less favorable rates: If you pay less than 20%, lenders will probably see you as a risky investment. And they will take this into consideration when calculating your mortgage rates. In general, you can expect to pay a higher interest rate if you put down a smaller down payment.

Higher closing costs: Closing costs are based on the size of your mortgage. So, the smaller your down payment is, the higher your closing costs will be. However, you may be able to get around this if you live in a state where it’s typical for the seller to pay the closing costs.

Private mortgage insurance (PMI): Private mortgage insurance is a type of mortgage insurance designed for borrowers who make a down payment lower than 20%. It protects your mortgage lender in case you end up defaulting on your loan.

PMI can cost as much as 1% of your total monthly mortgage payment. So for a $150,000 mortgage, you’ll end up paying $150 per month.

However, this may not be that bad, especially if you have a less expensive mortgage. And once you reach 20% home equity, you can cancel your PMI and get rid of these extra payments.

Check Out Our Top Picks for 2023:

Best Mortgage Lenders

How to Buy a House With No Money Down

Fortunately, there are several lending programs that do not require a down payment. Here are five payment assistance programs that will help you buy a home with little to no down payment.

1. VA Loans

VA loans are a valuable option for eligible military veterans, active-duty service members, and certain surviving spouses. These government-backed loans offer several benefits, making homeownership more accessible and affordable through the use of a VA loan.

100% Financing and No Down Payment

One of the most significant advantages of VA loans is the 100% financing, meaning you won’t need to make a down payment when utilizing a VA loan. This can save borrowers a substantial amount of money upfront, making it easier to enter the housing market.

No Private Mortgage Insurance (PMI) Requirement

Unlike conventional loans that require PMI for down payments less than 20%, VA loans do not require PMI. This can save borrowers hundreds or even thousands of dollars per year in mortgage insurance premiums when using a VA loan.

VA Funding Fee

While VA loans offer numerous benefits, there is a one-time funding fee charged to help offset the costs of the program. The funding fee is 2.15% of the total loan amount for first-time users of VA loans and 3.3% for subsequent uses.

This fee can be financed into the VA loan, reducing the out-of-pocket expenses for the borrower. In some cases, borrowers may be exempt from the funding fee, such as those with service-connected disabilities.

Certificate of Eligibility

To apply for a VA loan, borrowers need to obtain a Certificate of Eligibility (COE) from the Department of Veterans Affairs. The COE verifies the borrower’s eligibility for the VA loan program based on their military service or, in some cases, the service of their spouse. The COE can be requested online through the Department of Veterans Affairs website, by mail, or through an approved lender.

Additional Benefits

VA loans also offer competitive interest rates, more lenient credit requirements, and flexible underwriting guidelines compared to conventional loans. Additionally, there are no prepayment penalties, allowing borrowers to pay off their VA loans early without incurring additional fees.

2. Navy Federal Credit Union

Navy Federal Credit Union’s loan program is similar to what the VA offers. It offers a zero down mortgage and no mortgage insurance. And Navy Federal’s funding fee is only 1.75%.

Navy Federal offers a 30-year loan and a 30-year jumbo loan. 30-year loans have a loan limit of $424,100 while jumbo loans are available up to $1 million. However, you will have to be a Navy Federal member to qualify.

3. USDA Loans

If you’re looking to move to a rural area, you might qualify for a USDA loan. The United States Department of Agriculture Housing Program was designed to aid rural development and is aimed at low-income families. USDA loans offer 100% financing with low interest rates.

Here are the eligibility requirements you must meet to qualify for a USDA loan:

When buying a home it must be within the USDA’s boundaries: Although this loan targets rural areas, some suburban areas may still qualify. You can look at this map on the U.S. Department of Agriculture’s website to see if your location falls within the USDA’s geographical boundaries.

Your household income can’t exceed a certain threshold: This applies to everyone living in the household, even if they won’t be listed on the mortgage. For instance, if you have a parent living with you who collects Social Security, this counts toward the gross income of all members of a household. The maximum household income varies by state and county so you can find out if you qualify here.

See also: Best Home Loans for Low-Income Borrowers

4. Lease-Option

A lease-option (also known as rent-to-own) allows you to rent a home with the option to buy it at a predetermined price after a certain period. A portion of your monthly rent may be applied toward the purchase price or down payment. This can be a solid option if you need more time to save for a down payment or improve your credit.

5. Seller Financing

In some cases, the seller may be willing to finance the property for you, allowing you to purchase the home without a traditional mortgage. This arrangement typically requires a contract outlining the terms of the loan, including the interest rate, payment schedule, and any potential penalties.

Seller financing can be a viable option if you have a strong relationship with the seller or if the seller is having difficulty selling the property.

6. Crowdfunding

Crowdfunding is a method where you raise money from multiple individuals, typically through online platforms. You can set up a campaign to raise funds for your down payment or even the entire purchase price. This method may work best if you have a strong network of friends, family, and supporters who are willing to contribute to your home-buying goal.

7. Shared Equity Agreements

Shared equity agreements involve partnering with an investor who provides a portion or all of the down payment in exchange for a percentage of ownership in the property. When the property is sold or refinanced, the investor receives a return on their investment based on the agreed-upon share of equity. This can be an attractive option if you can’t afford a down payment but are willing to share future appreciation in the home’s value.

8. Housing Assistance Programs

There are numerous local, state, and federal housing assistance programs that offer grants, low-interest loans, or other forms of financial support to help eligible individuals purchase a home with no money down. These programs often have specific requirements, such as income limits, property location, or first-time homebuyer status. Be sure to research and apply for any programs for which you might be eligible.

Low Down Payment Loans

If you’re unable to buy a house with no money down but can afford a small down payment, consider these low down payment options that can help make homeownership more accessible.

1. 97% LTV mortgages

97% LTV mortgages is a loan program that is offered to first-time homebuyers by Fannie Mae and Freddie Mac. They require a 3% minimum down payment and private mortgage insurance.

Here are the guidelines for the program:

You’ll need a credit score of at least 680

One of the borrowers must be a first-time homeowner

Manufactured housing isn’t permitted

Gifts, grants, and other funds may be used toward the down payment

2. Federal Housing Administration (FHA) Loans

The Federal Housing Administration (FHA) was established in 1934 to reduce the requirements to qualify for a mortgage. This government-backed mortgage program offers flexible requirements, making it an attractive option for first-time homebuyers.

Here are the guidelines you’ll need to meet to qualify for an FHA loan:

Credit Score Requirements

The minimum credit score required to qualify for an FHA loan is 500. The specific down payment requirements depend on your credit score:

If your credit score is between 500 and 579, you’ll need to make a 10% down payment.

If your credit score is 580 or higher, you’ll have to make a 3.5% down payment.

Seller Contributions

FHA loans allow sellers to contribute up to 6% of the closing costs. This can help reduce the upfront costs for the buyer and make it easier to afford the purchase.

Mortgage Insurance Requirements

Mortgage insurance is required for an FHA loan, protecting the lender in case the borrower defaults on the loan. However, once you build 20% equity in the home, you can refinance to a conventional loan to eliminate the mortgage insurance requirement.

Debt-to-Income Ratios

FHA loans accept high debt-to-income (DTI) ratios, allowing borrowers with significant existing debt to still qualify for a mortgage. The FHA typically requires a maximum DTI of 43%, but exceptions can be made for borrowers with compensating factors, such as substantial savings or a history of making large payments on time.

3. HomeReady Mortgage

The HomeReady mortgage is a Fannie Mae program designed for low-to-moderate-income borrowers. It requires a down payment as low as 3% and offers flexible underwriting guidelines, making it an attractive option for first-time homebuyers or those with limited credit history.

4. Home Possible Mortgage

Similar to the HomeReady mortgage, the Home Possible mortgage is a Freddie Mac program that allows for a down payment as low as 3%. It is designed to help low-to-moderate-income borrowers achieve homeownership and offers flexible underwriting guidelines.

5. State and Local Homebuyer Assistance Programs

Many state and local governments offer homebuyer and down payment assistance programs that provide grants or low-interest loans to help cover down payment and closing costs. These programs typically have income and property location requirements, so be sure to research and apply for any programs for which you might be eligible in your area.

Each of these low down payment mortgage options has its own set of eligibility requirements and potential benefits. Be sure to research and compare these options to determine which one best aligns with your financial situation and home-buying goals.

Preparing for Homeownership

Before jumping into the home buying process, it’s essential to prepare yourself financially and mentally. This section covers tips for improving credit scores, creating a budget, and managing debt to make the home buying process smoother.

Credit Score Improvement Tips

Improving your credit score involves checking your credit report for errors and disputing any inaccuracies. Ensure that you pay your bills on time and reduce outstanding debt as much as possible. Keep credit card balances low, avoid opening new credit accounts, and consider requesting a credit limit increase without increasing your spending.

Creating a Budget

Creating a budget requires tracking your income and expenses to understand your spending habits better. Categorize your expenses and set realistic limits for each category. Allocate funds for saving and investing, including a down payment and emergency fund, and regularly review and adjust your budget as needed.

Managing Debt

Managing your debt effectively involves prioritizing high-interest debt and paying more than the minimum payment. Consider debt consolidation or refinancing options to secure a lower interest rate. Avoid taking on new debt before applying for a mortgage and create a debt repayment plan that you can stick to.

Understanding the Total Cost of Homeownership

Understanding the total cost of homeownership means factoring in property taxes, insurance, maintenance, and utility costs. Estimate homeowners association (HOA) fees if applicable and consider the costs of furnishing and updating the home. Prepare for potential increases in expenses over time, such as property tax hikes.

How to Choose the Right Mortgage Option

With various mortgage options available, it’s crucial to select the one that suits your financial needs and long-term goals. This section discusses factors to consider when choosing a mortgage, such as loan term, interest rates, and mortgage insurance.

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-rate mortgages have a consistent interest rate for the loan’s duration, providing stability and predictable monthly payments. In contrast, adjustable-rate mortgages (ARMs) have an initial fixed-rate period followed by periodic rate adjustments, which may result in lower initial payments but potential rate increases over time.

Mortgage Term: 15-Year vs. 30-Year

The mortgage term plays a crucial role in determining the overall cost of your mortgage. 15-year mortgages typically have lower interest rates and allow for faster equity buildup, but require higher monthly payments. 30-year mortgages offer lower monthly payments, but result in more interest paid over the loan’s lifetime.

Mortgage Insurance Considerations

PMI may be required for conventional loans with less than a 20% down payment. Loans backed by the federal government, such as FHA, VA, or USDA loans, may have different insurance requirements or fees.

Assessing Your Long-Term Goals

When choosing a mortgage option, consider how long you plan to live in the home and whether your financial situation or housing needs may change. Evaluate the potential for home value appreciation and the impact on your future financial goals.

Planning Your Next Steps

Assess Your Financial Situation

The amount of money you choose to put toward a down payment is a personal choice. If you feel ready for homeownership but know that a 20% down payment isn’t feasible for you, there are many options available to help you.