As anyone savvy in personal finance knows, it’s never too early or too late to start thinking about retirement. An individual retirement account, or IRA, is a retirement account that allows you to save money for your golden years in a tax-advantaged way.

There are several types of IRAs—Traditional, Roth, SEP, and SIMPLE—with varying rules and benefits. With the right account, you can grow your savings, manage your tax burden, and prepare for a comfortable retirement.

6 Best IRA Accounts

Check out our top 6 picks for 2023‘s best IRA accounts. Let’s examine each one so you can decide quickly and easily which is best for you.

Charles Schwab

Charles Schwab offers one of the best IRA accounts available thanks to its superior customer service. The company offers 24/7 customer support as well as extensive resources about retirement planning.

Charles Schwab recently eliminated its commissions on stocks, EFT, and options trades. Standard trades are $4.95. So, you can begin investing commission-free, and there’s no account minimum to get started.

The company also offers a robo-advisor called Schwab Intelligent Portfolios. The company will invest your money in up to 20 different asset classes at no annual charge.

This feature alone makes Charles Schwab one of the best options for new investors and anyone who is looking for a low-cost investing option.

Merrill Edge

Merrill Edge is one of the best brokerages for hands-on investors. The company is owned by Bank of America, so it’s a great option for anyone who is already a customer of the bank.

And this means Merrill Edge customers also have the option to receive in-person customer service. If you live near any of the bank’s locations, you can receive in-person assistance at the bank.

Merrill Edge offers unlimited $0 online stock and ETF trades with no trade or balance minimums. The company also offers mutual funds for $19.95 per purchase, though some mutual funds are available for free.

And the online broker doesn’t have a minimum deposit requirement to open an account. So, it’s an excellent option for new investors and anyone who is looking for in-person customer support.

Betterment

Betterment works to automate and simplify the investment process and offers traditional, SEP, rollover, and Roth IRAs. This robo-advisor makes managing your IRA extremely hands-off while helping you save money on excessive fees.

What’s the pricing structure like?

You have two levels of service to choose from. The first is the Digital level, which comes with a 0.25% annual fee and no minimum balance. So if your first year’s balance is $5,000 your fee would be $12.50.

Because Betterment is a robo-advisor, it offers automatic rebalancing so that you’re always hitting your target allocations, even with a shifting market.

Their portfolios are globally diversified, and you can adjust your risk tolerance based on your preferences. Plus, Betterment implements automatic tax-loss harvesting to boost your after-tax returns.

Need to talk to a certified financial planner?

No problem, you can chat online with a licensed expert with no limit on the number of questions you ask. If you want even more advice and support, you can upgrade to the Premium level. The annual fee jumps to 0.40%, and you’ll need at least $100,000 to start your retirement account.

But you get holistic advice on all of your financial questions, not just those related to your Betterment investments. So in addition to chatting about retirement, you can also talk to your advisor about joint financial goals with your spouse.

You can also discuss college savings plans for your children, and new and existing investments.

If you’re interested in a “set it and forget it” mentality for your IRA, Betterment certainly provides that option.

Ally Invest

Ally Invest is a great option if you’re just starting to build out your IRA rather than rolling over existing funds. It’s also directed to individuals who want to manage their own investments.

There’s no account minimum to get started, and you can choose from multiple types, including Roth, traditional, rollover, SIMPLE, and SEP IRAs.

Account fees are fairly limited as well. You don’t have to pay anything to set up the account, and there’s no minimum account opening, so it’s easy for anyone to start saving. Ally also doesn’t charge an annual fee or an inactivity fee.

There’s a $50 fee if you decide to terminate your IRA account with Ally Invest. If you transfer your funds, you’ll have to pay an additional $50 as a transfer fee — plus the first $50 termination fee. There’s also a $50 conversion fee if you want to change from a traditional IRA to a Roth IRA or the other way around.

If you’re an active trader even with your IRA, then you’ll appreciate Ally’s low trading fees.

Stocks and exchange-traded funds (ETFs) are $4.95 per trade, but you can get that lowered to $3.95 if you trade at least 30 times each quarter or have a balance of $100,000 or more. Options fees start at $4.95 each plus $0.65 per contract, and that price also lowers with heavy quarterly trading activity.

If you don’t want the burden of actively trading your IRA portfolio, then look elsewhere for an IRA account. But if you like handling your investments regularly, then Ally Invest could be a strong contender for your IRA account.

Wealthfront

Wealthfront is a robo-advisor that’s growing quickly. Your first $10,000 is managed for free. Thereafter, you’re charged an annual management fee of 0.25%, regardless of how much you have in your account.

You do have to open an IRA with at least $500. The more friends you refer to Wealthfront, the more you access free services, like getting an additional $5,000 managed for free. You can choose from a few different IRA types, including traditional, Roth, SEP, and rollovers.

Where does Wealthfront shine?

The answer is in retirement analytics. Wealthfront has a retirement planning tool called Path. It lets you integrate your various retirement accounts across financial institutions so you can see an accurate and comprehensive picture of your overall retirement plan.

Wealthfront economists use projects for things like inflation and Social Security to help plan for a realistic future.

Considering a major life event or financial change?

Wealthfront’s Path program lets you see potential impacts of these types of scenarios, so you’re not surprised at how your retirement savings are affected. Plus, like other online robo-advisors, all Wealthfront investments provide tax-loss harvesting and portfolio rebalancing.

You don’t have to worry about tracking individual stocks and funds. Instead, you get to invest passively while Wealthfront’s analytics keeps track of your portfolio. With IRA options and other tools at your disposal, Wealthfront is a solid choice for hands-off retirement investing.

E*TRADE

E*TRADE offers a ton of financial products, and their IRA offerings are straightforward with low fees.

There’s a great balance of getting access to in-depth research and resources, while also having the option to let E*TRADE take on your account management.

You can choose from a traditional IRA, Roth IRA, rollover IRA, or one-stop rollover IRA. That last one lets you transfer existing IRA funds in a diversified ETF that is managed by professionals.

This adaptive portfolio takes advantage of the automation processes. It requires a $5,000 minimum deposit to get started and comes with an annual advisory fee of 0.30%.

If you’re an avid ETF trader, you can trade for free on more than 100 funds; otherwise, it’s $6.95. Like Ally, that number drops if you make 30 or more quarterly trades, costing just $4.95 per trade at that point.

Stock trades also cost $6.95 each, with the same discount available as ETFs. Fees vary on mutual funds, but E*TRADE offers more than 4,400 no-transaction-fee mutual funds.

If you’re happy working with certain restrictions on the funds you choose, you can get away with a lot of fee-free trading via E*TRADE. Plus, you don’t have to worry about a minimum opening balance for most IRA accounts.

The company has been around for decades and consistently gets strong ratings from external sources, so they have a strong reputation in the industry, which can be comforting for beginning investors.

Understanding Different Types of IRAs

Now that we’ve explored the best IRA accounts of 2023, it’s crucial to understand the differences between the various types of IRAs. Each one comes with distinct advantages and rules tailored to unique financial circumstances and retirement goals.

Whether you’re just starting your retirement journey or you’re well on your way, familiarizing yourself with these options can help you make informed decisions about your future. Here, we delve into Traditional IRAs, Roth IRAs, SEP IRAs, and SIMPLE IRAs.

Traditional IRAs

Traditional IRAs provide a way to save for retirement with tax-deductible contributions. The contributions you make to a traditional IRA may lower your taxable income, meaning you’ll pay less income tax in the year you make the contribution.

You’ll pay taxes on your withdrawals in retirement. This type of IRA might be beneficial if you anticipate being in a lower tax bracket during retirement than you are now.

Roth IRAs

With Roth IRAs, you make contributions with after-tax dollars. This means you pay income taxes on contributions upfront, but qualified withdrawals in retirement are tax-free. Roth IRAs are attractive if you expect to be in the same or higher tax bracket in retirement.

Additionally, Roth IRAs don’t have required minimum distributions (RMDs) during the owner’s lifetime, a feature that can provide significant tax advantages.

SEP IRAs

SEP (Simplified Employee Pension) IRAs are for self-employed individuals and small-business owners. They work like a traditional IRA, allowing you to contribute pre-tax money, which grows tax-deferred until you withdraw it in retirement.

SIMPLE IRAs

SIMPLE (Savings Incentive Match Plan for Employees) IRAs are also for small businesses and self-employed individuals. They offer higher contribution limits than traditional and Roth IRAs but come with mandatory employer contributions.

Criteria for Selecting the Best IRA Accounts

As you embark on IRA investing, there are a few key factors you should consider when selecting the best IRA accounts.

Fees: Look for IRA providers with low or no annual account fees, low expense ratios on mutual funds or exchange-traded funds (ETFs), and no transaction fees. Even small fees can add up over time, eroding your investment returns.

Investment options: The best IRA accounts offer a broad array of investment options, including mutual funds, index funds, ETFs, bonds, and individual stocks. More options mean more opportunities to create a diversified portfolio.

Minimum balance requirement: Some providers require a minimum deposit to open an account, while others don’t have account minimums. This can be a barrier for new investors who want to start small.

Customer support: Excellent customer support can be invaluable, particularly if you’re new to investing. Look for providers that offer easy-to-use platforms, comprehensive educational resources, and responsive support.

Additional services: Some IRA providers also offer services like automated investing, financial planning, and wealth management, which can help you craft and stick to a retirement savings strategy.

Taxation: Understanding how different IRAs are taxed can help you optimize your retirement savings. For instance, traditional IRAs provide a tax deduction on contributions, but you’ll pay taxes upon withdrawal. Roth IRAs, on the other hand, don’t offer a tax deduction on contributions, but the growth and withdrawals are tax-free.

How to Open an IRA Account

Opening an IRA account is a fairly straightforward process, similar to opening a regular savings or brokerage account.

Choose an IRA provider: Decide whether you prefer an online bank, an investment firm, a robo advisor, or a traditional bank for your IRA. Each of these financial institutions offers unique benefits, so choose the one that fits your needs best.

Decide the type of IRA: Choose between a Roth IRA and a Traditional IRA based on your current income, future income predictions, and tax considerations. If you’re self-employed or a small business owner, you might consider a SEP or SIMPLE IRA.

Open an account: Visit your chosen provider’s website and select ‘open an account.’ You’ll need to provide some personal information, including your Social Security number, date of birth, mailing address, and employment information.

Fund your account: Decide how much you want to contribute to your account. Be mindful of the annual IRA contribution limits set by the IRS. You can fund your account through a transfer from a bank account or rollover from another retirement account.

Select your investments: Choose how your money is invested. Depending on the provider, you might be able to choose individual stocks and bonds, or you might select from a list of mutual funds or ETF trades. Some providers also offer target-date funds, which automatically adjust your asset allocation based on your age and retirement timeline.

Set up automatic contributions: If possible, set up automatic contributions to your account. Regular, consistent contributions can help your retirement savings grow over time.

Remember, it’s essential to regularly review your IRA to ensure it aligns with your retirement goals. Over time, you may need to adjust your contributions or rebalance your investment portfolio.

Common Mistakes to Avoid When Investing in an IRA

Procrastinating on opening an account: The sooner you open an IRA and start contributing, the more time your money has to grow. With the power of compounding, even small contributions can grow significantly over time.

Not contributing enough: Try to contribute the maximum amount to your IRA each year to take full advantage of the tax benefits and growth potential. If you can’t afford the max, aim to increase your contributions over time.

Investing in high-fee funds: Fees can eat into your retirement savings. Be sure to understand the expense ratios, management fees, and any transaction fees associated with your investments.

Not considering your tax situation: The tax benefits of Traditional and Roth IRAs are different, so consider your current and future tax situation when choosing an account. If you anticipate being in a higher tax bracket when you retire, a Roth IRA may be a better choice since withdrawals are tax-free.

Ignoring the income limits: Roth IRAs have income limits that can affect your ability to contribute. If you earn too much, you may be unable to contribute directly to a Roth IRA, though you might still be able to contribute to a Traditional IRA or execute a backdoor Roth IRA conversion.

Failing to update your beneficiary designations: Life changes, and so should your beneficiary designations. Make sure to review them regularly, especially after major life events like marriage, divorce, or the birth of a child.

Bottom Line

When it comes down to picking your IRA account, two of the most important factors are cost and your preferred management style. The two generally go hand in hand.

Do you want a DIY IRA that lets you do your own trading? You’ll need to compare online brokers and robo-advisors that offer free trades or lower-cost trade fees based on your trading activity.

Prefer a hands-off style? Think about how much money you’re likely to invest in the near term. Then, pick an IRA account that lets you go on autopilot while charging a flat annual fee.

For these types of IRA accounts, you’ll definitely want to dig deeper into how the financial advisors’ portfolios are chosen and whether their investment styles agree with your own.

Having any type of IRA can help you prepare for retirement. You can always transfer or roll over your funds into another IRA. However, choosing the best account in the first place can help prevent unnecessary fees.

And once you’re ready to retire, you’ll have a healthy nest egg helping you to finance your daily expenses.

Frequently Asked Questions

What is the maximum contribution limit for IRAs in 2023?

The maximum contribution limit for IRAs in 2023 stands at $6,500 for individuals who are under 50 years of age, and it’s $7,500 for those who are 50 or older. This represents a $500 increase from the 2022 limits for all age groups. It’s important to remember that these contribution limits apply collectively to your contributions to both traditional and Roth IRAs.

Can I have both a traditional IRA and a Roth IRA?

Yes, you can have both a traditional IRA and a Roth IRA. However, the total amount you can contribute to both accounts combined cannot exceed the annual contribution limit.

What is a backdoor Roth IRA?

A backdoor Roth IRA is a strategy for people whose income exceeds the Roth IRA income limits to still contribute to a Roth IRA. It involves contributing to a traditional IRA and then converting that contribution to a Roth IRA. There may be tax implications with this strategy, so it’s recommended to consult a certified financial planner or tax advisor.

Is the money I contribute to an IRA protected from loss?

No, the money you contribute to an IRA is not protected from loss. The value of your IRA is subject to market fluctuations and the performance of the investments within the account. It’s important to diversify your investments and align them with your risk tolerance and retirement goals.

Can I withdraw money from my IRA before retirement age?

Yes, you can withdraw money from your IRA before reaching retirement age. However, early withdrawals are subject to income tax and potentially a 10% early withdrawal penalty. There are some exceptions to the penalty, such as using the funds for qualified education expenses or a first-time home purchase. Be sure to understand the rules and potential tax implications before making an early withdrawal.

Are there any penalties for not taking distributions from my IRA?

Yes, there are penalties for not taking required minimum distributions (RMDs) from your traditional IRA. The penalty is 50% of the amount you should have withdrawn but didn’t. Roth IRAs, on the other hand, do not require minimum distributions during the owner’s lifetime.

When you purchased your first home, it likely checked off all the boxes. But over time, perhaps your lifestyle has changed and your family has grown, and now you’ve started asking yourself, “Should I buy a bigger house?” Whether you’re looking for larger bedrooms, expanded family space or more storage solutions, buying a bigger home — or even just moving to a different layout or location — might be a change you’re ready to make.

Scott Bridges, Senior Managing Director of Consumer Direct Lending at Pennymac, says that upsizing happens frequently. He explains that a “healthy percentage of buyers are looking to buy up for space, neighborhood, school district and work proximity reasons. It’s a great pursuit and one of the more exciting chapters in one’s homeownership journey.”

Here’s how to figure out if you’ve outgrown your current home and how to determine how big a house you actually need.

The Signs You’ve Outgrown Your Home

While starting a new chapter in a bigger home may sound appealing, moving is a big decision that can come with a hefty price tag. How do you know if you’ve really outgrown your house? Bridges says the following are some of the most important items to consider.

Physical Aspects

One of the first things you’ll want to assess is the number of bedrooms and bathrooms you have versus the number you need. Bridges notes, “If your family is growing, if you have kids or parents moving in, you will need additional space for the new members of the household.”

Evolving household dynamics can also change your idea of an optimal home layout. If you currently have a one-story home, do you want to move to a two-story residence or vice versa? Do you want your children’s bedrooms on the same floor as yours? Do you need a separate entrance and living area for mom and dad or grandma and grandpa?

You’ll also want to think about your outdoor space. Bridges recommends asking yourself how much space you’ll need. For example, will you want to entertain, maybe have a pool, how much yard would you like to manage? All things to consider when looking to buy a bigger house.

Future Plans

Even if you’re comfortable in your home right now, do you foresee life events on the horizon that may lead to things getting cramped? Think carefully about your future plans and determine if they align with your current living environment. Consider the following:

Will you be having more children or expanding your family?

How long will your kids be living in the house before they leave for college or work?

Will you need a larger garage or driveway as your children get their driver’s licenses?

Do you envision an elderly parent moving in with you at some point?

Your answers to these questions will help you decide if moving to a bigger home is right for you.

Daily Life

Your home’s physical size may be the primary factor when deciding if you’ve outgrown it, but there are other lifestyle factors to consider as well. For example, do you have a short or a long commute from your current home? Bridges points out, “Most people don’t want to add significant time to their commute, even if it is for a larger home.” Others, however, may feel a longer commute is an adequate trade-off for increased space.

Or maybe you aren’t commuting as much because you work or attend school from home. Could a dedicated work area in a larger home reduce distractions?

Consider, too, the benefits and drawbacks of your present location. Even if you love your neighborhood, perhaps you want to move to a quiet, traffic-minimal cul-de-sac. Or maybe you’d like to be within walking distance of stores, restaurants or public transportation.

Quality of life is key. If your current home is causing you stress and not providing you the comfort you need, it may be time to upsize. Bridges urges, “Carefully think about how much better your day could potentially be with more space, a bigger kitchen, larger yard and more rooms.”

Considerations for Staying Put

There are many reasons why you may want or need to move to a bigger house. But that increase in square footage will likely increase your expenses and responsibilities. Here are a few reasons why staying put may be a better option for some homeowners.

Difficulty Finding a Home in Your Ideal Location

Depending on your desired location, a larger home in your price range may be difficult to find. If you want to remain in the same neighborhood or school district, you’ll have to decide whether moving away from your preferred area for a bigger space is worth the sacrifice.

Higher Costs Beyond the Mortgage

Even if you can comfortably afford your down payment and monthly mortgage payment, there are other expenses you’ll need to consider when moving to a bigger house. “If you live in an area with colder winters, understand your heating costs will go up,” Bridges says. “In a warmer climate, think Arizona and Texas in the summer, AC costs can run very high electric bills in bigger homes.”

Increased Responsibilities

A larger home requires more interior and exterior upkeep. There’s more to clean, furnish, repair, landscape and maintain, which takes time, money and energy.

Not a Guaranteed Investment

If you’re purchasing a home based on an anticipated greater return on investment, keep in mind that real estate values can be unpredictable. There’s no guarantee that your larger home will increase in value when you’re ready to sell.

Commute

Housing costs are often less the further you move away from city centers, giving you more bang for your real estate buck. But if it takes you longer to get to your job, the added time, hassles and transportation expenses may not be worth it. Bridges notes, “If you’re extending your commute to live in a bigger house in the suburbs, the drive may be just too hard.”

Financial Tips for Buying a Larger Home on a Budget

Moving involves a considerable amount of expense, stress and time. Many people try to avoid it by buying a home that will meet their needs for many years to come. However, it’s also important not to buy a house bigger than what you really need. Maintenance requirements, increased utility bills and expensive mortgage payments can be significant burdens. When purchasing a home, how can you be prepared for a growing family without overstretching your budget? Here are a few tips.

Anticipate Costs

Try your best to forecast the additional costs of a bigger home. “When you buy a larger home, you can easily anticipate your mortgage, taxes and insurance costs increasing, but many people don’t anticipate the additional costs of a larger home,” Bridges explains. “Your utilities will be more expensive, lawn and landscaping and amenities like pools will increase your monthly expenses as well. Lastly, repair costs can be much more expensive on bigger homes. Think of a roof replacement on a 2,000 square foot house versus a 4,000 square foot house.”

Consider Your Income and Employment Stability

While more space may support your plans, Bridges stresses that stability of income and employment must be part of the discussion when considering moving to a larger home. Your household income will need to cover the higher costs of owning a bigger house — now and in the days ahead.

Rent Out Your Original House for Income

It may make sense to sell your current home and use the proceeds for the down payment. But if you don’t have to do that, consider keeping it as a rental. Some homeowners move to a bigger home while renting out their old home, creating what can be a lucrative income stream in the future. Bridges advises, “Depending on how much you owe on your house, sometimes it makes sense to keep the original house and rent it out, as it can represent a good income source in the long run. Over time, real estate tends to appreciate and rents tend to rise, so holding the property as a rental can add to your overall wealth as the years go by.”

What to Look Out for When You’re Ready to Buy a Bigger House

Moving to a larger home is a significant change and takes careful thought. If you’re ready to upsize, think about how your prospective new home could adapt as your needs evolve. Bridges says that during the buying stage, homeowners with growing families often look for the following:

Bedrooms on the same floor

A bigger kitchen, a nursery or a media room

Backyard space for kids and pets

A better school district, which generally speaking, impacts home value stability

Want to start your new home search now? See how much your current home is worth, and then go beyond home affordability calculators to determine how much house you can actually afford.

Are You Ready to Move to a Larger Home?

So, should you move to a bigger home? “Every buyer has to make their own decision, as their circumstances vary,” Bridges says. Moving may be challenging, and selling is a process, but he adds, “At the end of the day, buying a bigger home might be one of the more memorable and enjoyable things you can do in your life, so don’t wait too long, if you can!”

Choosing a home that is the right size for your life today and tomorrow involves balancing both your family needs and your budget. If you’re ready to take the next step toward a larger home and are looking for expert guidance in the mortgage loan process, get a custom instant rate quote from Pennymac today.

The Fannie Mae Flex Modification Program (FMP) is a mortgage assistance solution designed to relieve borrowers facing financial hardship.

Are you looking to improve your mortgage management but don’t know where to start? Handling mortgage payments is challenging, especially if you’re facing economic difficulties and don’t know where or how to get financial assistance. The Fannie Mae and Freddie Mac Flex Modification Program may be the solution you’re looking for.

Learn what you need to know about the Flex Modification Program: how it works, who qualifies for it, and how you can apply. This comprehensive guide will help you understand the many benefits of FMP for a more stable financial future.

In This Piece:

What Is the Flex Modification Program?

The Fannie Mae Flex Modification program is a mortgage assistance solution designed to relieve borrowers facing financial hardship. This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure.

Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners.

Get matched with a personal

loan that’s right for you today.

Learn

more

How Do Fannie Mae and Freddie Mac Work?

The mortgage market has a few essential entities, including the government-sponsored enterprises called Fannie Mae and Freddie Mac. Their approach allows lenders to free up funds to provide more mortgage loans to borrowers.

But how does it work? Fannie Mae and Freddie Mac helped make mortgages more accessible by buying them from lenders. This allows lenders to have more money available to provide new mortgages to borrowers or invest in other financial opportunities. For example, if a lender originates a mortgage, they can sell it to Fannie Mae or Freddie Mac, who then include it in their portfolio or package it into mortgage-backed securities.

How Flex Modification Works

The Flex Modification Program offers loan modifications to eligible borrowers experiencing financial hardship. Here’s a breakdown of how the program operates:

Eligibility Requirements:

You must have a mortgage loan owned or guaranteed by Fannie Mae or Freddie Mac.

The mortgage loan must be at least 60 days delinquent or at risk of imminent default.

You must demonstrate a hardship that affects your ability to make timely mortgage payments.

Modification Terms:

The program aims to reduce your monthly mortgage payment to 20% or more below your pre-modification.

The modification may involve adjusting the interest rate, extending the loan term, or forbearing a principal portion.

The goal is to make the mortgage payment more affordable while ensuring it’s sustainable for you.

Application Process:

Apply to the Flex Modification Program through a loan servicer.

The loan servicer will assess your eligibility and collect the necessary documentation.

Once approved, the loan servicer will work with you to finalize the modification terms.

Why Should You Consider the Flex Modification Program?

Before considering the Flex Modification Program, it’s essential to understand its potential pros and cons.

Pros:

Lower monthly payments: The program aims to reduce your mortgage payment to a more affordable level, making it easier to manage your finances on time.

Protection from foreclosure: By modifying your loan, the program can help you avoid the devastating consequences of foreclosure.

Improved financial stability: By participating in the Flex Modification Program, you can regain control of your financial situation. Providing you with a sense of stability and peace of mind, allowing you to focus on rebuilding your financial health.

Simplified application process: Applying for the program is relatively straightforward, and you can work directly with your loan servicer to navigate the process.

Potential principal reduction: The FMP may offer this, which means that a portion of the outstanding loan balance could be forgiven or deferred, reducing the overall amount owed. This can be particularly beneficial if you owe more on the mortgage than your current property value.

Preservation of homeownership: One of the primary goals of the FMP is to help borrowers preserve their homeownership. The program offers a viable alternative to foreclosure by providing a framework for loan modifications.

Cons:

Extended loan term: Modifying your loan may result in a more extended repayment period, meaning you’ll make mortgage payments for longer.

Impact on credit score: While participating in the program doesn’t directly affect your credit score, the delinquency prior to modification might be reported on your credit report.

Limited availability: The program is specifically for Fannie Mae or Freddie Mac borrowers with owned or guaranteed loans. You won’t qualify for this program if either entity doesn’t back your loan. However, other programs may exist. Contact your lender if you’re struggling to make your mortgage payments.

Remember, these pros and cons will vary based on your circumstances. It’s essential to consult with your loan servicer and thoroughly review the modification terms to understand the potential benefits you may receive from participating in the program.

Who Qualifies for the Flex Modification Program?

The Flex Modification Program is designed for borrowers struggling with mortgage payments due to financial hardship.

To qualify for the program, you must meet the following criteria:

Loan ownership: The mortgage loan must be owned or guaranteed by Fannie Mae or Freddie Mac.

Delinquency or imminent default: Borrowers must be at least 60 days delinquent on their mortgage payments or at risk of imminent default.

Demonstrated hardship: Borrowers need to demonstrate a hardship that affects their ability to make timely mortgage payments. Hardships may include job loss, income reduction, medical expenses, divorce, or other significant life events.

Additionally, you must comprehend what a “hardship” entails to be considered for a loan modification. Each situation is evaluated individually, but common examples of hardships include loss of income, disability, serious illness, divorce, or the death of a co-borrower.

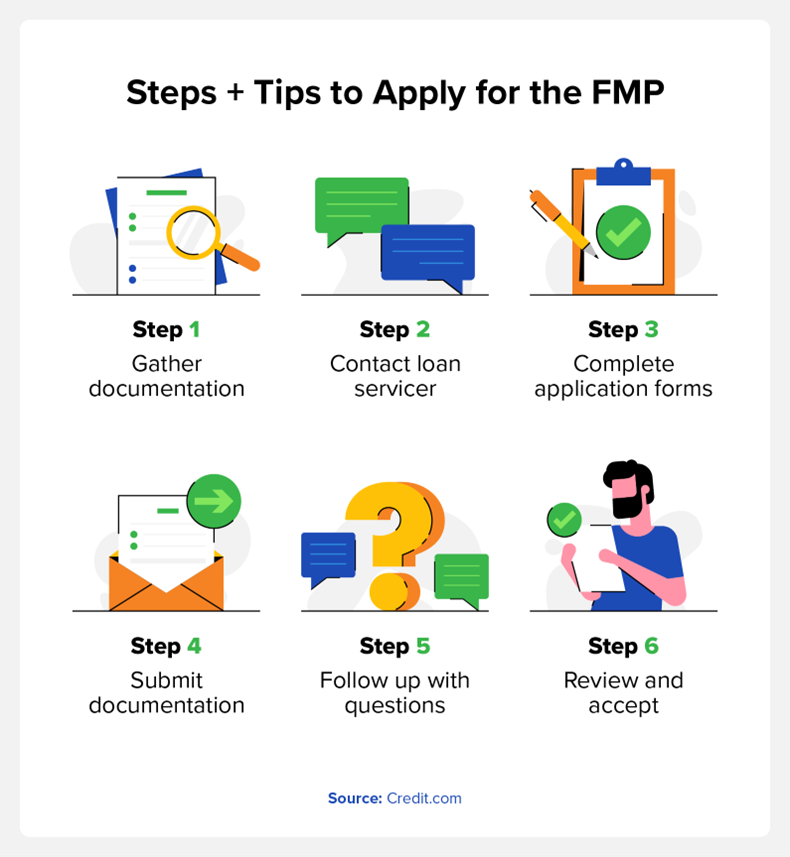

How to Apply for the FMP

If you believe you meet the eligibility requirements for the Flex Modification Program, you can follow these steps and tips to apply:

Gather documentation: Prepare the necessary documents, such as proof of income, bank statements, tax returns, and any other documentation required by your loan servicer.

Contact your loan servicer: Inform your loan servicer about your interest in the Flex Modification Program.

Complete application forms: Your loan servicer will provide the necessary forms and guidance to complete the application process.

Submit documentation: Submit all the required documentation and the completed application forms to your loan servicer.

Follow up and provide additional information: Be proactive in promptly following up with your loan servicer and providing any additional information they request.

Review and accept the modification terms: Once your loan servicer evaluates your application, they will provide you with the proposed modification terms. Review them carefully and, if acceptable, sign and return the necessary paperwork to proceed with the modification.

Remember, each loan servicer may have a specific application process, so it’s crucial to communicate directly with them to ensure you have all the necessary information and are following the correct steps. Having to redo the application process due to easily-avoided mistakes is the last thing you need.

Other Mortgage Payment Help Options

What if I don’t qualify? What can I do? Other mortgage payment assistance options are available if the FMP is not the right fit.

Fannie Mae and Freddie Mac offer additional programs catering to different circumstances. Some of these options include:

Home Affordable Modification Program (HAMP): This aims to help homebuyers struggling with financial hardship and mortgage payments.

Repayment plan: Allows you to catch up on missed mortgage payments by adding a portion of the past-due amount to your regular expenditures over an agreed-upon period.

Forbearance: Temporarily suspends or reduces your mortgage payments with this program. It can be for a specific period, providing short-term relief during financial difficulties, so you can reassess the situation.

But before you move forward with one of these, it’s essential to analyze your alternatives and consult with your loan servicer to determine the best course of action based on your specific circumstances.

FAQs

Let’s address some frequently asked questions about the Flex Modification Program:

Does the Flex Modification Program Affect Your Credit Score?

Participating in the Flex Modification Program doesn’t directly impact your credit score. However, the delinquency prior to modification might be reported on your credit report

What if Fannie Mae or Freddie Mac Doesn’t Own My Loan?

If your loan isn’t owned or guaranteed by Fannie Mae or Freddie Mac, you won’t be eligible for the Flex Modification Program. However, you should contact your loan servicer to inquire about other available mortgage assistance options or loan modification programs specific to your loan type.

How Long Does the Flex Modification Program Last?

The duration of the Flex Modification Program varies depending on the specific terms of the modification. Typically, the program aims to provide long-term mortgage relief by modifying the loan terms to make payments more affordable and sustainable for the borrower.

The revised terms may involve extending the loan term or adjusting the interest rate. It’s important to discuss the duration of the modification with your loan servicer, as it will depend on your circumstances and the terms agreed upon.

Can I Qualify for the Flex Modification Program if I’ve Previously Received a Loan Modification?

If you have previously received a loan modification, you may still be eligible for the Flex Modification Program. However, the specific requirements and eligibility criteria may change depending on your previous modification and the current guidelines set by Fannie Mae and Freddie Mac.

It’s crucial to communicate with your loan servicer and provide them with all the necessary information regarding your previous modification. They will assess your eligibility based on your unique circumstances and guide you through the application process.

Remember, these answers are general guidelines, and you must consult with your loan servicer to get accurate and personalized information based on your situation.

What Are the Next Steps?

The Fannie Mae Flex Modification Program provides borrowers with a potential lifeline during financial hardship. It aims to make mortgage payments more manageable and sustainable by offering loan modifications. If you’re facing challenges with your mortgage payments, exploring the Flex Modification Program and other mortgage payment help options can help you find the assistance you need.

To take control of your mortgage management and improve your financial well-being. Consult with your loan servicer for accurate and personalized information based on your situation, and research different mortgage rates to make informed financial decisions.

No one can predict the future of real estate, but you can prepare. Find out what to prepare for and pick up the tools you’ll need at the immersive Virtual Inman Connect on Nov. 1-2, 2023. And don’t miss Inman Connect New York on Jan. 23-25, 2024, where AI, capital and more will be center stage. Bet big on the roaring future, and join us at Connect.

The U.S. looks to be headed for a “mild recession” in the first half of next year, but continued strength in the economy could keep mortgage rates from coming down as much as previously expected, economists at mortgage giant Fannie Mae said in a forecast released Monday.

While the Federal Reserve isn’t expected to raise rates when policymakers wrap up a two-day meeting Wednesday, persistent inflation could still prompt the Fed to hike rates later this year, or implement a “higher for longer” rate strategy.

The good news is that even though mortgage rates have settled in above 7 percent, the risk that rates will do even more damage to home sales is limited, as the share of cash purchases remains high and sales are now driven more by life events than discretionary move-up buys, Fannie Mae forecasters said.

Nevertheless, Fannie Mae economists forecast that home sales will drop by 14.7 percent this year, and stay at about the same level next year.

“We expect that total housing market activity will remain at a low level into 2024 as the Federal Reserve continues to hold the line on interest rates against inflation,” Fannie Mae Chief Economist Doug Duncan said, in a statement.

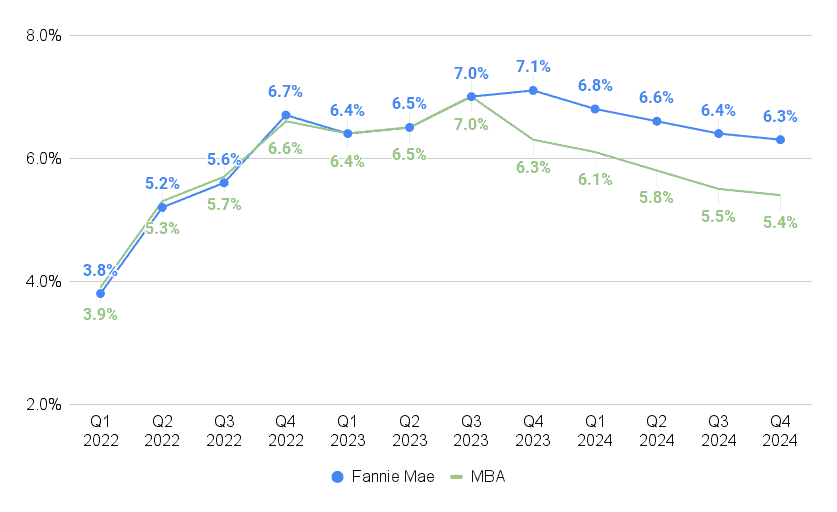

Last month, economists at Fannie Mae were expecting rates for 30-year fixed-rate conforming mortgages would peak at 6.8 percent during the third quarter of this year before retreating to an average of 6 percent during the final three months of 2024. Forecasters at the Mortgage Bankers Association (MBA) were even more optimistic, predicting mortgage rates would drop to an average of 5 percent by Q4 2024.

Mortgage rates projected to ease next year

Source: Fannie Mae, Mortgage Bankers Association forecasts.

That was before strong economic data sent rates on the popular 30-year fixed-rate conforming loans soaring to a 2023 high of 7.30 percent, according to rate lock data tracked by the Optimal Blue Mortgage Market Indices, which show rates have only pulled back slightly since then.

With the economy cooling more slowly than expected, Fannie Mae analysts now see mortgage rates peaking at 7.1 percent during the final three months of 2023, before easing to 6.3 percent by Q4 2024. In releasing their latest forecast Monday, MBA economists predicted mortgage rates will start coming down this year, but remain well above 5 percent next year.

Home sales projected to drop 17.4% this year

Source: Fannie Mae Housing Forecast, September 2023.

Fannie Mae is forecasting 4.8 million total home sales in 2023, which would be a 17.4 percent drop from last year and the slowest annual pace since 2011. Next year isn’t expected to be much different, with sales expected to bounce back by less than 1 percent.

“While the additional downside risk from rate movements to date is minimal, the prospects of a recovery in existing sales in the near future is unlikely given strong mortgage rate ‘lock-in’ effects and stressed affordability,” Fannie Mae economists said in commentary accompanying their September forecast.

New home sales are expected to grow by more than 6 percent this year, as builders race to complete homes in markets where the lock-in effect — reluctance on the part of homeowners to give up the low rate on their existing mortgage — has made listings scarce.

“New home sales were surprisingly strong in the first half of the year, due partly to homebuilder rate buydowns, which become more expensive when mortgage rates rise,” Duncan noted. But he said Fannie Mae forecasters expect new home sales to pull back slightly next year, “due to the higher mortgage rate environment and recent decline in homebuilder confidence.”

The National Association of Home Builders/Wells Fargo Housing Market Index, a gauge of builder confidence, dipped six points in August and another five points in September, to 45. It was the first time the index has been below 50 in five months, which indicates more builders view conditions as poor than good.

The recent rebound in mortgage rates “is making homebuilders nervous,” Pantheon Macroeconomics Chief Economist Ian Shepherdson said in a note to clients Monday.

“To be clear, the impact of mortgage rates returning to 7-1/4 percent from their recent 6-1/2 percent lows will be nothing like as bad as the initial surge from 3 percent to 7-1/4 percent in the year to September 2022,” Shepherdson said. “But it ought to be enough to quash the nonsensical media/Fed narrative that the housing market is starting to recover. It isn’t.”

Large pipeline of multifamily housing coming online

Source: Fannie Mae Housing Forecast, September 2023.

Fannie Mae economists expect single-family housing starts to plateau at 910,000 next year, and for multifamily construction to slow by 22 percent, to 389,000 units.

“With sluggish rent growth on a national level, more normalized vacancy rates, and tighter construction and development loan lending standards, we expect multifamily construction starts to continue to slow,” Fannie Mae forecasters said. “These dynamics may also play into softening demand for single-family housing: There is a large pipeline of multifamily housing coming online, and the rent-to-buy calculus for prospective homebuyers may tilt a little more in favor of renting for longer.”

Mortgage lending expected to grow by 20% next year

Source: Fannie Mae Housing Forecast, September 2023.

With home prices holding firm and mortgage rates expected to ease next year, Fannie Mae forecasters expect mortgage originations will grow by 20 percent next year. The slight uptick in home sales projected for next year would boost purchase loan originations by 9.4 percent, to $1.433 trillion, while lower mortgage rates are expected to boost refinancing by 76 percent, to $442 billion.

Mild recession seen as ‘likeliest outcome’ of Fed tightening

Fannie Mae economists have been predicting that the U.S. was headed for a recession since April 2022, after the Fed began raising interest rates and the impact of stimulus measures introduced during the pandemic faded.

While mixed economic data continues to “muddle the near-term outlook,” Fannie Mae economists say they continue to expect a “mild recession” in the first half of 2024, based on the belief that consumers will need to rein in spending in order to live within their means.

“Fundamentally, personal consumption remains at what we believe to be an unsustainable level relative to incomes, and the full effects of monetary policy tightening are still working through the economy,” Fannie Mae forecasters said.

In their weekly brief on the U.S. economy, Shepherdson and his Pantheon Macroeconomics colleague Kieran Clancy noted three potential wildcards on the economic horizon: A strike launched last week by the United Auto Workers targeting the big three automakers, next month’s resumption of federal student loan payments, and a “likely” government shutdown.

“An all-out strike lasting a month could be expected to depress quarterly GDP [gross domestic product] growth by about 1.7 percentage points, before taking account of the hit to the supply chain,” the Pantheon Macroeconomics team said. “The problem for the Fed is that it would be impossible to know in real time how much of any slowing in economic growth could confidently be pinned the strike, and how much could be due to other factors, notably the hit to consumption from the restart of student loan payments. The latter already is making itself felt in falling restaurant diner and airline passenger numbers.”

Fannie Mae economists agree that a sustained strike could “drive a negative payroll report in October, as well as dampen the GDP measure,” but that a short-lived strike “would likely be followed by a rebound in auto manufacturing output thereafter.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Additionally, the mortgage application measure and the pending home sales index are increasingly diverging, reflecting the higher cash share of sales, the ESR group noted.

While the additional downside risk from rate movements to date is minimal, the prospects of a recovery in existing sales in the near future is unlikely given strong mortgage rate “lock-in” effects and stressed affordability.

Going forward, the ESR Group expects new home sales to pull back slightly due to the higher mortgage rate environment and recent decline in homebuilder confidence.

Homebuilder confidence fell six points from July to a reading of 50 in August. It’s the first decline in 2023 reflecting the difficulties of 7% mortgage rates and reduced housing affordability.

The recent rise in mortgage rates will also now test the resiliency of the new home sales market, which showed remarkable strength over the first half of the year.

The lack of existing homes for sale has helped support demand for new homes, including an increasing share of first-time buyers.

To what extent homebuilders will continue to offer generous mortgage rate buydowns to drive sales is a big question that needs to be answered, according to the ESR group.

“When mortgage rates originally jumped to 7% in late 2022, a pullback in homebuilder activity ensued as buying activity slowed. It is uncertain whether this same rate threshold will result in a similar effect this time around or whether buyers and homebuilders have increased their willingness to purchase and subsidize at current rates,” Fannie Mae noted.

Fannie Mae expects Q4 new home sales to average around 691,000 units on an annualized basis, down slightly from the most recent pace of 714,000 in July.

Purchase mortgage origination volume is expected to be $1.3 trillion in 2023 and $1.4 trillion in the following year. Refi volume is forecast to be at around $10 billion in 2023 and $14 billion in 2024.

Fannie Mae’s projection of a mild economic downturn in Q1 2024 remains unchanged.

While the GSE’s initial April 2022 forecast of a mild recession was in the second half of 2023, housing production held up and household savings supported consumer spending longer than Fannie Mae had expected.

“Our current prediction for a mild downturn in the first half of 2024 is predicated on the belief that consumers will begin pausing their spending, in part due to the exhaustion of those funds and having to realign to a more sustainable relationship between spending and incomes,” said Doug Duncan, SVP and chief economist at Fannie Mae.

Flowers have the remarkable ability to elevate the decor of any home. Whether you live in an apartment in Irvine, CA or a home in Lexington, KY, adding a touch of elegance and freshness to your living spaces will make a positive impact. Whether you’re a seasoned floral enthusiast or just starting, these expert tips will help you enhance your home’s floral decor.

1. Embrace neutral tones for timeless elegance

“When in doubt, use neutral tones. Colors like white and green compliment any space regardless of decor choice, while also adding a touch of modern elegance,” shares Stephanie from Mercer Island Florist.

Neutral tones act as a canvas, allowing your flowers to take center stage. White lilies, green foliage, and soft creams create a serene atmosphere that complements any interior style.

2. Focus on flower variety, space, and placement

Flowers can freshen up any space, but their impact depends on the flower variety, space, and placement. Justine Aylward, Program and Category Manager at Floral at New Seasons Market, advises, “For higher spaces like mantles or bookcases, go dramatic with tall and draping flowers and branches to make a statement. Try tall flowers, such as lilies or sunflowers that drape a bit with an accent flower like hanging amaranthus.”

3. Match containers to your home’s style

According to Lawrence The Florist Team, “Choose containers that mimic your home’s style, whether it’s new or vintage, to inspire your arrangement’s design. Bring the beauty of the Pacific Northwest into your home by choosing local seasonal foliage and flowers with your favorite colors and textures whenever possible.”

Selecting containers that resonate with your decor style can fluidly bring your space together.

4. Maintain freshness for longer lasting blooms

“Flowers do best away from direct light and kept as cool as possible. Even putting them in a cool dark room when you are not home enjoying them can extend their life. I also recommend a re-cut of the stems at an angle and changing the water often,” states Ann Vandehey, owner of Annabell’s Garden & Floral Design.

A recut of the stems at an angle and regular water changes keep your blooms vibrant for longer.

Owner of Goldenrod Floral Design Carlee Donnelly, advises, “When choosing or designing flowers for your own home, always, always strip any bottom leaves or foliage from the stems. Leaving foliage in water will cause your flowers to die faster.”

“The key to longer-lasting blooms is fresh, clean water,” says the Ribbon and Twine Floral Team. “Remove all leaves and dirt from the stems before placing them in the vase and refill with new water every few days.”

Clean water and removing foliage is essential for keeping your floral arrangements vibrant.

5. Embrace seasonal blooms

Cory Beckman, Owner of Milwaukie Floral and Garden, emphasizes the importance of freshness, “Fresh is best. Local flower shops refresh selections all week long, but in my professional experience shopping midweek guarantees a good selection of fresh blooms.”

“To add cheer to a room or spruce up your decor, keep it simple and fresh by asking your florist for the flowers that are currently in their peak season,” says Laura Gifford Kerr, Owner of Gifford’s Flowers.

Seasonal blooms not only reflect nature’s beauty but also align with the changing seasons, keeping your decor fresh. Choosing flowers that are in season ensures their quality and affordability.

“Pick flowers that are in season, even going with a bunch of the same flower. Keep it simple,” suggests Owner of Emerald Petals, Hilary Holmes. Single-variety blooms gathered in your favorite vase create a timeless and elegant look that suits any decor style.

6. Choose containers wisely

“Use an opaque container that will disguise any discoloration in the water,” advises The Flower Lab Team. “Ask your florist for a design that reflects the home’s style, such as modern garden style, or architectural for the most appropriate style.”

Containers play a crucial role in enhancing your floral arrangements’ visual appeal and blending with your home’s decor.

7. Create a living arrangements for longevity

Val Wayne of Acorn Floral recommends creating living arrangements. “Start with a decorative planter, choose a few orchid plants from your local grocery store or garden center and a few small 2 inch potted plants and assemble them pot and all inside your decorative planter. Then use crumpled butcher paper to wedge all the plants in place and cover with sheet moss. These living arrangements can run up to hundreds of dollars retail, but you can DIY one for under $100.”

Living arrangements are ideal for home decor because they can last for months and instantly elevate a space. It’ll be worth the cost when you consider the shelf life.

8. Combine flowers with herbs for aromatherapy

According to Lisa Aliment of Bear Creek Florist, “Growing herbs like sage, mint, or rosemary isn’t just for cooking anymore. Add those clippings to simple flower bouquets to add more aromatherapy to the room.”

The combination of flowers and herbs can engage multiple senses, enhancing the ambiance of your space.

9. Set the mood with color and design

“When selecting flowers for your home, think about the feeling you are trying to create,” advises Jennifer Silberg, Owner of Juniper Blooms. “Colorful, vibrant flowers bring a lively energy to the room, while a soothing neutral palette provides a more calm and peaceful environment.”

Consider how the flower arrangements can guide the viewer’s gaze around the room, whether through tall, eye-catching designs or low, intimate ones.

10. Brighten every room with small bunches

The One Little Bunch Team suggests, “Smaller bunches placed throughout the house will brighten up each room. A little bunch in the bathroom adds freshness and a pop of interest, or add a little bunch to your side or entry hall table for a welcoming surprise.”

Small floral accents can elevate the ambiance of every corner of your home.

11. Improve your mood with bouquets

“Flowers are not only beautiful but studies have shown that people report reduced stress levels when receiving bouquets or having flowers in their home after just 3 days,” says Melissa Mercado-Denke, founder of Campanula Design Studio. “Keep it simple – just a few bud vases in areas you spend the most time such as your kitchen or bedroom will have a positive impact on your mood.”

12. Create nostalgic vibes with flower choices

Juliet LaVassar, designer at LaVassar Florists, recommends selecting flowers that evoke memories: “Smell and memories are closely related, according to a 2020 Harvard study. Having flowers around that remind you of loved ones or life events brings joy into your home.”

Personal touches in your floral decor selections add a sentimental dimension to your home.

Incorporating these tips into your home decor journey will not only enhance your living space but also infuse it with the timeless beauty and natural charm of flowers. Whether you opt for dramatic arrangements or simple single-variety bouquets, the right flowers can transform any room into a sanctuary of color, fragrance, and elegance. So, let your creativity bloom and watch your home come to life with the magic of flowers.

Many companies featured on Money advertise with us. Opinions are our own, but compensation and in-depth research may determine where and how companies appear. Learn more about how we make money.

For months, experts have been sounding the alarm about how Americans who took out mortgages when rates were low are reluctant to sell and borrow now that they’ve skyrocketed.

New research, however, has found there is a magic number that makes homeowners more motivated to move.

A June survey of 1,815 homeowners from real estate listing site Zillow found that homeowners with mortgage rates 5% or higher were significantly more likely than those with lower rates to say they plan to sell. As home listings tick down amid today’s elevated rates, the findings suggest that supply could increase again in the coming years.

What the data says

Homeowners with mortgage rates 5% and up were twice as likely to say they plan to sell their homes in the next three years than those with rates under 5%. Among homeowners who said they have plans to sell, almost half paying mortgage rates above 5% said they already have their house listed for sale. (Only 20% of homeowners paying rates below 5% said the same.)

For perspective, about 80% of mortgage borrowers said their current rate is below 5%, and 90% have a rate under 6%. Nearly a third said their rate was less than 3%.

Of homeowners with higher mortgage rates who said they were thinking about selling, 65% said rates were an influencing factor. About 35% of lower-rate homeowners said the same.

Keep in mind, though, that factors other than mortgage rates can play a role in a homeowner’s choice. The survey found that fewer than half (42%) of all homeowners thinking about selling said that mortgage rate fluctuations were a reason they decided to move.

What it means

Mortgage rates are hovering around 7% at the moment, and most homeowners would have to take out new mortgages at a higher rate if they were to move. According to Zillow, the ordinary monthly mortgage payment is now twice what it was in 2020, when rates were at historic lows.

Homeowners who took out mortgages when rates were lower could pay hundreds more a month if they take out a new mortgage right now. It’s no surprise that, as a result, homeowners are reluctant to move and locked into their current rates.

Mortgage rate locks push home prices up and listings down, creating a challenging market for buyers. Zillow’s June housing market report found that there were 28% fewer new for-sale listings compared to the same time last year.

Home values have climbed in all the 50 largest metropolitan areas, bringing the typical U.S. home price to more than $350,000. Another recent report from real estate listing site Redfin found that homebuyers have lost $60,000 in purchasing power in the last year. Mortgage rates are so high that “many homeowners will move only for major life events, like a new baby or retirement,” Orphe Divounguy, a senior economist at Zillow Home Loans, said in a news release.

Despite the difficult circumstances, Zillow says its analysis offers hope that more homes could hit the market in the next few years as homeowners accept higher rates as the new norm. About 23% of homeowners surveyed said they were thinking about selling in the next three years or already have their home listed. Among homeowners with a mortgage rate above 5%, 38% said they would consider selling their home in the next three years.

Ads by Money. We may be compensated if you click this ad.Ad

Getting creative

Additional research from Zillow Home Loans also found that buyers are finding creative ways to cope with high mortgage rates.

A separate survey released in April found that 45% of all buyers are purchasing mortgage points — which allow buyers to pay a fee to buy down the interest rate on a loan — to lower their interest rate. They’re also opting for smaller, cheaper homes and keeping an open mind when it comes to their wish lists.

More from Money:

Foreclosures Are on the Rise in These 10 U.S. Cities

Housing Market Forecast: Will Home Prices Drop in 2023?

Property Values Might Fall Soon — Here’s What Homeowners Can Do to Prepare

A money market account is an interest-earning savings account, with some features of a checking account.

Saving money is the best way to prepare for unexpected life events and take control of your finances. But where is the best place to save your money?

If you’ve been researching different savings accounts, you may have wondered, “What is a money market account?” at some point. As of March 2023, interest rates for money market accounts are up to 4.45%,which is higher than normal.

Keep reading for a money market account definition, its benefits, and how it stacks up to other kinds of accounts.

In This Piece:

What Is a Money Market Account?

A money market account (MMA) is a type of savings account that earns interest at a bank or credit union. They are sometimes called money market deposit accounts (MMDAs).

MMA interest rates are usually higher than regular savings accounts and have some features of a checking account, like debit card and check-writing privileges, though there are more restrictions.

How Does a Money Market Account Work?

Money market accounts pay more competitive interest rates than a traditional savings account, with more access to your money than a high-yield savings account. They may also require a larger minimum deposit and balance than a traditional savings account.

As a hybrid between a savings and checking account, money market accounts have some unique features.

Interest: The interest rate offered by MMAs is typically higher than regular savings accounts. It is a variable rate, meaning it changes as the market changes.

Access to your money: Some MMAs come with a debit card and/or checks that you can use to make limited purchases.

Minimum balance: Money market accounts may have a required minimum balance, ranging from $0-$25,000. Each bank has different requirements, and they may scale for getting certain APYs.

Although money market accounts have some features of a checking account, they aren’t meant to be used as a replacement for a traditional checking account.

This is because money market accounts often limit you to six transactions per month. This includes withdrawals or payments by check, debit card, draft, or electronic transfer.

However, you can usually make an unlimited number of transactions in person or by ATM, mail, messenger, or telephone check.

Benefits of Money Market Accounts

Money market accounts are great for short-term savings goals, like an emergency fund. You’ll earn a higher interest rate than standard savings accounts while still being able to easily access your money if needed.

However, this type of account comes with its own set of restrictions. If you’re considering opening a money market account, consider these pros and cons.

Pros of Money Market Accounts:

Higher interest rates than traditional savings accounts

Safe place to keep money with insurance up to $250,000 per account owner

More access to your money than other savings accounts with debit card and check features

Cons of Money Market Accounts:

Lower interest rates than other accounts like high-yield savings accounts or CDs

Requires a higher minimum deposit and balance than traditional savings accounts

Monthly limit on number of transactions

Remember that every financial situation is different, and while a money market account may work well for one person, it may not be a good fit for another.

Money Market Account vs. Other Accounts

Money market account features overlap with different types of savings and checking accounts. The differences between these accounts may be important depending on your financial goals.

If you’re not sure if a money market account is best for you, see how they compare to other accounts.

Standard Savings Accounts

Interest type: Variable

Higher interest rates: No

Insured: Yes

Debit card/checks available: No

Minimum deposit/balance: Yes

The biggest difference between money market accounts and traditional savings accounts is access to a debit card and checks with an MMA.

Money market accounts also generally offer a higher interest rate than savings accounts. In February 2023, the average interest rate for an MMA was 0.48% and 0.35% for a traditional savings account, according to the Federal Deposit Insurance Corporation (FDIC). However, some banks like Discover and Ally are offering up to 3.4% on their MMAs.

The difference is not always that substantial, as MMA interest rates vary with the market. If you find that the interest rate for an MMA isn’t that much higher than your standard savings account, it may not be worth the higher minimum deposit and balance requirements.

High-yield Savings Accounts

Interest type: Variable

Higher interest rates: Yes

Insured: Yes

Debit card/checks available: No

Minimum deposit/balance: Yes

Money market accounts and high-yield savings accounts are very similar. Both offer higher interest rates than standard savings accounts and are insured. In March 2023, MMA and high-yield savings account interest rates were comparable.

One main difference is the addition of debit cards and checkbooks with an MMA, allowing you more access to your money than a high-yield savings account.

If you’re torn between the two options, make sure to compare interest rates, minimum deposit and balance requirements, potential fees, and transaction limits.

Checking Accounts

Interest type: Variable (or none)

Higher interest rates: No

Insured: Yes

Debit card/checks available: Yes (unlimited)

Minimum deposit/balance: Yes

While money market accounts have some features of checking accounts, they aren’t meant to replace a checking account. You still need a checking account for daily expenses, since MMAs are usually capped at six transactions per month.

Additionally, most checking accounts don’t earn interest, and if they do it’s a very low rate. These accounts work best when used together—one can’t replace the other.

Certificates of Deposit (CD)

Interest type: Fixed

Higher interest rates: Yes

Insured: Yes

Debit card/checks available: No

Minimum deposit/balance: Yes

A certificate of deposit (CD) and a money market account are both insured savings accounts that earn higher interest rates than standard savings accounts.

In fact, CDs can earn even higher interest rates than MMAs. They also have fixed interest rates, meaning your money will earn the same amount of interest during its life cycle.

In February 2023, the FDIC reported an average interest rate of 1.36% for a 12-month CD, with banks like Marcus by Goldman Sachs and Discover offering up to 4.5%.

However, the money you put into a CD gets locked up for a set period of time, usually months or even years. If you withdraw money early, you have to pay a penalty. This makes it the least flexible savings account option.

If you have extra money you’d like to safely invest, a CD is a great option. But if you prefer more accessibility to your money, a money market account is the better choice.

Money Market Funds

Interest type: Variable

Higher interest rates: Yes

Insured: No

Debit card/checks available: No

Minimum deposit/balance: Yes

It’s easy to get money market accounts and money market funds confused, or even think they’re the same thing. In reality, these accounts are very different.

Money market funds are offered by investment funds, not government securities like MMAs. This means while money market funds may have a higher interest rate, they’re not insured by the FDIC or the National Credit Union Administration (NCUA), so you could potentially lose money.

You will also have less access to your money with money market funds and may have to pay monthly maintenance or management fees.

Investing in a money market fund may be a good idea for someone who already has a large amount of savings built up in other accounts and is ready to diversify their assets.

Money Market Account FAQ

Still have questions about money market accounts? Check out the answers to these frequently asked questions regarding MMAs.

What Is the Interest Rate for a Money Market Account?

Money market account interest rates in February 2023 were 0.48% on average, but some banks are currently offering up to 3.4%. The interest rate on MMAs is variable, which means it can change depending on the market.

Are Money Market Accounts Safe?

Yes, money market accounts are a safe place to save your money. They are insured through your bank or credit union by either the FDIC or the NCUA.

Your money is insured up to $250,000 per depositor per account ownership category by both the FDIC and NCUA.

What Is the Typical Minimum Balance for a Money Market Account?

The minimum balance required for a money market account depends on the bank or credit union. Minimum balance requirements could be anywhere from $0 to $25,000 depending on the bank or current promotion.

Generally, you can expect MMAs to require a higher minimum balance than standard savings accounts, but you may be able to find an account with no balance requirements.

Some banks have one requirement for avoiding fees and another for securing a specific interest rate. Compare rates from different banks to find the best deal.

Is a Money Market Account a Savings Account?

Yes, a money market account is a type of savings account with certain privileges of a checking account, like a debit card and checkbook.

Money market accounts are a great way to safely earn interest while working toward a short-term savings goal. If you’re not sure that a money market account is a perfect fit for your savings goals, compare high-interest savings accounts.

It didn’t always feel like it, but 2016 was a pretty good year for the housing market. From Brexit to Trump, there were several surprises, but ultimately, we’re heading into 2017 with a solid footing underneath us.

No one knows exactly what will happen in the new year, and with a new administration taking office in January, it’s not easy to make detailed predictions. However, there are several data points that we can use to point us in the right direction.

So what’s in store for the housing in market in 2017? Here are 5 things to watch out for.

1. Mortgage rates will move higher

The 2016 housing market was fueled by extremely low mortgage rates. We saw rates bottom out last year at near record levels (around 3.5%) after the Brexit vote. Post-election, they’ve skyrocketed over seventy basis points (one basis point = 0.1%), mostly due to expectations that the Donald Trump administration will boost the economy with its infrastructure spending plan. While the quickness with which rates rise might soften somewhat, it’s widely expected for mortgage rates to continue on their ascent next year.

The Federal Reserve’s Federal Open Market Committee (FOMC) just recently raised the benchmark interest rate by a quarter-point for the second time in a decade.

The FOMC will meet at least eight times in 2017, and fed officials have stated that they believe it will be appropriate to raise the federal funds rate around three times throughout the year. It’s true that the FOMC does not directly control the direction of mortgage rates, but it can play a large role in influencing which way rates are headed.

So how high will mortgage rates rise?

It’s not unfathomable to suggest that mortgage rates could be somewhere between 4.75%-5.0% in the fourth quarter of 2017. Long-term interest rate speculation should always be taken with a grain of salt though. Many, many things could happen between now and then.

Click here to get today’s latest mortgage rates.

2. Millennials will buy more homes

In 2016, Millenials (ages currently 18-34) surpassed Baby Boomers as the largest living generation in the United States. While rising mortgage rates might price some of them out of the market, they are still poised to be one of biggest demographics of home buyers (some estimates are saying they will account for up to 33% of home buyers).

Marriage and children are no doubt on the way for many of them, and those are two key life events that often precede the motivation to purchase a home.

One other interesting trend for millennials in 2017 is the decision to settle in the Midwest. Apparently, the affordability and the proximity to big universities is enough of a draw in to keep millennials from heading to the coast.

3. Home price growth will soften

In 2016, home prices rose around an estimated 5%, putting them back to where they were before the housing bubble burst in 2008. While that may be great news for home owners, it’s not something every prospective home buyer is crazy about.

Nevertheless, home prices are expected to continue to rise over the course of the new year, albeit by a slightly lower margin. Zillow’s Chief Economist Svenja Goodell is predicting home prices will increase by 3.6% next year. That’s right about where other economists are predicting, give or take a few basis points.

Of course, in a nation as large and varied as the United States, not every housing market is created equal. Some markets will continue to march forward with strong growth while others will slow down and falter. For instance, cities in the western United States are predicted to outperform their eastern counterparts (just as they did in 2016) next year. As you can see below, five of the top ten cities in the graphic below are located out west.

Taken as a whole, though, home price growth will moderate somewhat compared to 2016.

4. New home construction gets more expensive

The construction industry struggled to find workers in 2016, and that trend is expected to continue. According to the National Association of Homebuilders, there are an estimated 200,000 vacant positions in the construction industry right now.

It’s not just confined to one position either. Employers are finding it extremely difficult to find both entry level and experienced workers alike. With less laborers competing for jobs, companies are forced to raise wages in order to attract talent.

Those extra costs will inevitably get passed on to customers, resulting in an increased cost for new construction. Not only that, this shortage of labor means that fewer houses are being produced.

Wild Cards

Fed overplaying their hand

Not everyone is so optimistic about the housing market and the economy in general. A recent report from the Financial Times shows that many economists are extremely doubtful that the Federal Reserve will wind up proceeding with multiple rate hikes in 2017. Instead, they believe that the Fed will raise rates once at their June meeting.

It’s definitely reasonable to be fairly skeptical of fed rate hike predictions, seeing how some fed officials were touting up to four rate hikes this year and in the end they barely pulled one off.

Doubts about Trump stimulus

While the stock markets surged after Donald Trump came out and stated that he has plans for substantial fiscal stimulus, some experts believe the path ahead won’t be so smooth. Euro Pacific Capital CEO Peter Schiff has come out recently as one of the few economists to question the efficacy of Trump’s plan. Here it is in his own words:

“The Federal Reserve is going to have to step up to the plate big league if Donald Trump is going to want to move forward with the tax cuts and spending increases that he has promised the electorate. That’s where the markets have it wrong. They somehow think that fiscal stimulus is a substitute for monetary stimulus. It’s not. If we’re going to have larger deficits, it’s impossible to finance them unless the Federal Reserve does it. That means they’re going to have to be launching another round of quantitative easing that is much larger than the ones we’ve had in the past. Rather than being dollar positive, this is a negative for the dollar … If currency traders actually understood what was happening, higher inflation is very bad for the dollar because the Fed cannot fight it.”

Bottom Line