Looking for jobs where you work alone? If you’re an introvert or simply want minimal human interaction, here are 40 ideas.

Looking for the best jobs where you work alone? If you’re an introvert or simply want minimal human interaction, here are 40 ideas.

With there being so many different types of jobs out there nowadays, more and more people are looking for jobs where they can be by themselves, away from the busy office or customers. They find comfort in jobs where they can do tasks on their own, letting them really concentrate and do well in what they do best.

For me, I have worked mostly alone for over a decade now, and I wouldn’t change it for the world. I enjoy the flexibility of working on my own and having less stress.

Jobs that let you work this way are usually appealing to introverted individuals, those who like a calmer setting, or people who just work better with more independence.

Knowing which jobs let you work alone is really important for those who want to find the right mix of being on their own and getting things done well.

Top Jobs Where You Work Alone

There are 40 jobs where you can work alone listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Benefits of Jobs Where You Work Alone

More and more people are looking for jobs where they can work alone, and I get it! I have been working mostly alone for over a decade and I really love it.

After all, a person spends so much of their time working, so you might as well like what you’re doing. If you’re an introvert, or if you like working by yourself, there are jobs where you can do just that.

Some of the positives of working alone include:

Less stress if you’re an introvert – If you’re an introvert, then you may feel stress when working with other people, such as coworkers and customers.

Getting more stuff done in less time – Working alone may mean that you can complete your tasks faster because there are fewer distractions.

Having a more flexible schedule – Some jobs where you work on your own sometimes let you choose when you want to work, as long as you get the work done.

If you’re looking for jobs where you work alone, think about what you’re good at and what you enjoy (and also think about what you don’t like!).

40 Jobs Where You Work Alone

Below are 40 jobs where you can work on your own. The jobs below range from earning a part-time to a full-time income too.

1. Proofreader

Proofreaders check and edit written content for errors and inconsistencies, and this job requires strong attention to detail and excellent grammar skills.

If you’re good at paying close attention to details, then proofreading could be an ideal work-alone job for you.

Authors, website owners, and students often hire proofreaders to improve their work. There’s a high demand for proofreaders, and you can find jobs through many different platforms.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend joining this free 76-minute workshop focused on proofreading. In this workshop, you’ll learn how to begin your own freelance proofreading business.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

2. Virtual Assistant

One of my first side jobs was as a virtual assistant and it was a fun and flexible way to earn income. While you do have a boss when you are a VA, a lot of the tasks that you do will require you to take charge and complete them by yourself in your own home.

A virtual assistant is someone who helps people with office tasks from a distance. This could be from your home or while you’re traveling. It might include things like replying to emails, setting up appointments, and managing social media accounts.

This job can pay you more than $50,000 each year.

If you want to find part-time or full-time virtual assistant jobs, I recommend joining the free workshop called “5 Steps To Become a Virtual Assistant“.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

3. Bookkeeper

Bookkeepers are people who keep track of all the money-related things for businesses such as writing down sales, keeping a record of expenses, and making financial reports.

This is a job where you can work alone and a typical salary is $40,000+ each year. Plus, you’ll mainly be dealing with numbers and not people.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

4. Blogger

Blogging is a great way to make money while working on your own. It’s one of the reasons I really enjoy it, haha! I get to work by myself, for myself, and I can pick the projects I want to work on.

As a blogger, you write content for others to read online. You get to choose what you want to write about as well as how you want to make money blogging because there are so many different options (like affiliate marketing or displaying ads).

You can begin a successful blog about a specific topic like finance, travel, lifestyle, family, and many others.

Blogging is my main source of income, and it has completely transformed my life. I have the freedom to travel whenever I want, set my schedule, and be my boss.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog. I earned this money by working with companies through sponsored partnerships, affiliate marketing, display ads, and selling online courses.

Learn more at How To Start A Blog FREE Course.

5. Delivery Driver

Delivery drivers pick up and drop off packages. And, they get to work by themself most of the time as they are in the vehicle alone.

A delivery driver may drive a car, truck, or even a bike, depending on the company they work for. They don’t usually have a boss watching them all day nor have to deal with very many customers for long periods.

6. Book Reviewer

Book reviewers read books and share their thoughts in book reviews.

There are websites where you can get paid for sharing your thoughts about books and you may earn money through PayPal or a bank transfer, and sometimes you get to keep the book you reviewed.

They don’t just want positive reviews either, they want to know what you really think! You see, authors and publishers like to send out free copies of their books so that they can get honest opinions. Just like us, they know it’s helpful to read reviews before deciding if a book is worth the time.

Some sites that pay for book reviews include Online Book Club, Kirkus Media, and BookBrowse.

Recommended reading: 7 Best Ways To Get Paid To Read Books

7. Deliver RVs or Cars

You can earn money by traveling across the country and delivering vehicles for people and dealerships. Sometimes you’ll be towing the vehicle, and other times you’ll be driving it.

If you want a job with minimal human interaction, this can be a good one to look into as you are mostly by yourself. You simply pick up the vehicle, drive by yourself, and then drop it off.

For this job, you need to have a clean driving record. Those who do this type of work can earn around $300 to $400 (or much more!) for each vehicle they deliver. It depends on the distance they are traveling and what is being transported.

8. Digital or Graphic Designer

A graphic designer is someone who creates designs for others, such as people and businesses.

As a digital designer, you may be making things like images, printables, planners, t-shirt designs, calendars, business card designs, social media graphics, stickers, logos, and more.

Recommended reading: How To Make Money As A Digital Designer

9. Pet Sitter and Dog Walker

Pet sitters and dog walkers take care of pets while pet owners are away, such as on vacation or in the hospital. Some of the tasks include feeding, taking dogs for walks, and playing with them.

You might have pets come to your home or you can go to their owner’s place (this is something that is agreed upon beforehand). Dog walkers earn around $20 for every hour walking a dog. Looking after someone’s pet overnight can earn a person around $25-$100+ or even more each day.

I have personally paid a person to watch my dogs overnight in their home $100 a day. She was so wonderful too and my dogs loved her.

Now, with this job, you’re not working entirely alone, because you will be with pets. But, they can be great friends and companions!

Rover is a company you can sign up with and list your dog walking and pet sitting services.

10. House Cleaner

House cleaners make sure homes and businesses are nice and clean. They might work alone or with a small group. They can earn between $25 to $50 an hour for cleaning for others.

You can work for a cleaning company, but you’ll likely make more money if you have your own business.

Starting this kind of business isn’t expensive because you likely already have the cleaning supplies you need. You can advertise your services on Facebook, tell your friends and family, or make an account on Care.com.

11. Transcriptionist

An online transcriptionist’s main task is to listen to video or audio files and then type out everything that is being said, a process known as transcribing. The aim is to accurately write down what is heard, without any mistakes in spelling, grammar, or punctuation.

There are many different types of transcriptionists as well – legal, general, and medical transcriptionists.

This job requires strong typing and listening skills, and you can work from home all by yourself.

Online transcriptionists earn around $15 to $30 per hour on average, with new transcribers on the lower end of that.

A helpful free resource to take is FREE Workshop: Is a Career in Transcription Right for You? You’ll learn how to get started as a transcriptionist, how you can find transcription work, and more.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

12. House Flipper

House flippers buy, renovate, and sell properties for a profit. This job involves managing renovation projects, and you can work alone or with a small crew.

House flipping is when someone buys a property at a lower price, fixes it up (like painting, redoing the kitchen, and improving the outside appearance), and then sells it for more money to make a profit. This is done to make a quick return on the investment.

Recommended reading: 10 Best Books on Flipping Houses To Make Money

13. Grocery Shopper

Grocery shoppers buy groceries for people like you and me, offering a helpful service for those who don’t have the time or can’t shop on their own. You’ll work on your own and talk to clients through an app on your phone.

One service you can easily sign up with to become a grocery shopper is Instacart. This is a popular site for people who want to make extra money by shopping for and delivering groceries.

Instacart shoppers make money from a mix of base pay, tips from customers, and sometimes bonuses or rewards (like for finishing orders during busy times).

You can sign up here to get started as a grocery shopper with Instacart.

Recommended reading: Instacart Shopper Review: How much do Instacart Shoppers earn?

14. Affiliate Marketer

Affiliate marketers share products or services with their followers for a commission. You do this by placing a referral link on your website, blog, or social media (like Instagram). When people use that link to buy something, you then get a commission.

For example, if you share a link to a book on Amazon and someone buys it through your link, you make some money. Companies like Amazon want people like you to help them sell things, so they’re happy to work with you as it helps them.

If you get someone to sign up through your special link, the company gives you a commission for telling others about their product. It’s like a little thank-you for your help!

This is one of my favorite jobs where you work alone from home, and what I do full-time!

Click here to get Affiliate Marketing Tips – Free eBook.

15. Flea Market Flipper

Flea market flippers find underpriced items at flea markets, yard sales, and thrift stores, then resell them for a profit. This job requires a good eye for valuable items and the ability to research market value.

Finding items to resell may be one of the best jobs to work alone on this list because we all have things in our house we could probably sell. Plus, there are always things that you can buy for a low price and possibly resell for a profit.

If you are looking for work-alone jobs, this is a great one to look further into.

I recommend signing up for this great webinar, Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business In As Little As 14 Days, that will help you learn how to make money by flipping items as well.

16. Sell Printables on Etsy

Creating and selling digital printables on Etsy is a great way to work independently and earn money.

Making printables can also be a pretty hands-off job since you only have to create one digital file for each product, and you can sell it as many times as you like. It’s quite affordable to start because you only need a laptop or computer and an internet connection.

Printables are digital items that customers can download and print at home. They can include things like bridal shower games, grocery shopping checklists, budget planners, invitations, printable quotes for wall art, and patterns.

I recommend signing up for Free Workshop: How To Earn Money Selling Printables. This free training will give you great ideas on what you can sell, how to get started, the costs, and how to make sales.

17. Mechanic

Mechanics diagnose and repair vehicles, working independently or in small shops. Strong problem-solving skills and knowledge of automotive systems are important.

Being a mechanic is a job where you often work on your own. While they might work in a garage with other mechanics, they often have their own tasks to do. They need to be really careful and pay close attention to make sure everything gets fixed just right.

18. Dog Treat Baker

Do you really like dogs? If you do, here’s a way to work mainly alone and make an extra $500 to $1,000 or even more each month.

You don’t need to know how to bake beforehand, because you can learn this skill. You can make special treats like cupcakes, cookies, cakes, and more, all for dogs.

You can sign up for this free training workshop that shows how to start a dog treat bakery.

You can learn more at How I Make $4,000 Per Month Baking Dog Treats (With Zero Baking Experience!).

19. Amazon Seller

Selling items on Amazon is a job where you work alone (mostly) and don’t have to deal with customers face-to-face.

Even if you’re new to selling on Amazon, you can make money by selling household goods, books, electronics, and more.

If you’re interested in learning about starting an Amazon business, you can join this free training that will teach you how to sell products on Amazon and make around $100 to $500+ each day.

20. Stock Photo Photographer

Stock photo photographers work on their own, and this job can be done without talking to anyone for the most part. Almost all of the tasks can be done with just a camera and then uploading photos on a site.

Stock image sites are some of the most popular ways for photographers to sell their pictures. These are sites where customers can buy pictures for websites, TV shows, books, social media accounts, and more. There are stock photos that I have purchased within this blog post that you can take a look at to see an example.

One great thing about stock photo sites is that they can be a great form of passive income. You can take pictures, upload them, and earn money from an older photo for months or even years in the future. There is no need to talk to anyone as everything is online and mostly automated.

Some stock photo websites include Shutterstock, iStock, DepositPhotos, and Dreamstime.

Recommended reading: 18 Ways You Can Get Paid To Take Pictures

21. Social Media Manager

Social media managers post on social media accounts for businesses and their goal is to bring in new customers and help a business grow.

Social media managers may post a picture or a video of a product or the company, join in a viral trend to get more views (such as on TikTok), answer common questions from customers, and more.

This includes social media platforms such as TikTok, Pinterest, Instagram, Twitter, and Facebook.

Salary can vary, and this job can be done part-time or full-time.

22. Landscaper

A landscaper improves and maintains outdoor areas, such as by taking care of the lawn, planting flowers, or even renovating a whole outdoor area (such as to make it more enjoyable to sit outside and have company).

If you’re interested in jobs where you work alone outside, this is one to consider as you will be outdoors and working on your own a lot. Customers may talk to you occasionally, but you are mostly by yourself.

Landscapers work at houses, apartment complexes, businesses, or somewhere else.

23. Data Entry Clerk

Data entry clerks enter, update, and check information in databases or spreadsheets. They type information such as numbers and names into computers to keep things organized and recorded.

This job can sometimes be done remotely and alone, with minimal supervision or interaction with customers.

Data entry jobs typically pay around $15-$20 an hour.

24. Editor

Editors review and improve written content for clients and they usually work on their own as most of their time is spent editing content.

Their job is to read articles, blog posts, advertising, books, and more to make them better. They fix any mistakes in grammar or spelling and help the words flow smoothly.

Editors typically earn anywhere from $40-$60+ an hour.

25. Freelance Writer

Freelance writers write content for clients, such as blog posts, advertising, and more. Freelance writing jobs where you work by yourself are common as you’ll be given a topic to write about from the client, and when you are done you may be given some feedback (such as paragraphs to improve or add to). But, that is usually as much human interaction as you’ll get if you want.

You can find different writing jobs on platforms like Upwork and Fiverr, or even find clients on your own.

I was a freelance writer for many years before switching to working full-time writing here on Making Sense of Cents. It is a great career path where you can work from home mostly by yourself.

Recommended reading: 14 Places To Find Freelance Writing Jobs – (Start With No Experience!)

26. Translator

Translators convert written content from one language to another, requiring fluency in at least two languages. Freelance and remote opportunities are available.

If you know another language, you might be able to find a work-from-home job where you can earn money by reading books and translating them. Another option is to get paid for proofreading or editing translated books to ensure they read smoothly and accurately.

There are lots of places you can find translation jobs, such as UpWork, Babelcube, Today Translations, Ulatus, Fiverr, and more.

27. Computer Programmer

Computer programmers write and maintain computer software, often working alone on projects.

They use coding to tell computers what to do and create all sorts of things like apps, games, and websites.

28. Canva Template Designer

Creating and selling Canva templates online allows you to work alone.

A Canva template is like a ready-made design that you can use for things like making posters, Pinterest pins, ebooks, or presentations. It’s like having a helpful starting point if you’re not super good at designing things from scratch. Canva templates come with empty spaces where you can put in your own words and pictures and you can also change colors and fonts to make them just how you like. They’re really helpful for people who want their things to look nice without spending a lot of time on it.

Making and selling Canva templates can be a great way to earn extra money as you only need to create them once, and then you can sell them as many times as you like.

Recommended reading: How I Make $2,000+ Monthly Selling Canva Templates

29. Voice Over Actor

A voice-over actor is the person whose voice you hear but don’t see in YouTube videos, radio ads, educational videos, and more.

Voice-over actors many times work right from their own homes!

Voice actors don’t need experience for this job (eventually, it does help, yes). Instead, they need to have a voice that the company is looking for.

Recommended reading: How To Become A Voice Over Actor And Work From Anywhere

30. Truck Driver

Truck drivers are people who move things from one place to another. To do this job, truck drivers need a commercial driver’s license (CDL). This job often involves working by yourself for long hours.

The salary for a truck driver can depend on things like what kind of items they’re moving and the miles they have to drive. Usually, they can make between $45,000 and $75,000 or even more in a year.

31. UPS Driver

UPS drivers deliver packages to people’s homes and businesses. They do this mostly on their own, in their trucks by themselves.

UPS drivers make a good income and they earn about $30-$45 per hour or even more, depending on how many years they have worked at UPS and where they work.

32. Security Guard

Security guards protect property and/or people, and they usually work alone.

A security guard’s salary depends on things like where they work, how long they’ve been doing the job, and what exactly they have to do. Usually, they can make between $25,000 and $35,000 in a year.

33. Self-Storage Facility Owner

Self-storage facilities are where people store their belongings, like boxes of their mementos, vehicles, RVs, and more.

Owning a self-storage business can be a way to make money and run a business with low expenses, plus they typically only have a couple of employees.

Many of the times when I’ve been to a self-storage lot, it’s been just the owner or an employee of theirs working. There are almost no customers either.

Recommended reading: How To Invest In Self-Storage For Beginners

34. Laundromat Owner

Similar to a self-storage business, a laundromat typically does not have very many employees.

Running a laundromat can be a way to make money, with low costs, as most things are automated (the washer and dryer machines do all of the washing).

Recommended reading: Are Laundromats Profitable? How Much Do Laundromats Make?

35. Get Paid To Text

When getting paid to text, you will many times be talking to someone else, but it is all done through text messages.

Some jobs may include:

Text Therapy or Coach

Answering questions, such as if you are a mechanic, doctor, lawyer, veterinarian, home expert, appraiser, computer expert

Customer support

Recommended reading: 28 Ways To Get Paid To Text And Make Money

36. Survey Taker

Taking online surveys and answering questions for focus groups is not a full-time job, but it can be a way to make some extra money.

You share your thoughts and answer straightforward questions, and in return, you can receive cash or rewards such as Amazon gift cards.

The survey companies I recommend signing up for and the best-paying survey sites include:

American Consumer Opinion

Survey Junkie

Swagbucks

InboxDollars

Branded Surveys

Pinecone Research

Prize Rebel

User Interviews – These are the highest paying surveys with the average being around $60.

Recommended reading: 18 Best Paid Survey Sites To Make $100+ Per Month

37. Twitch Streamer

Twitch is a site where you can make money playing video games, talking online in a live stream, and more. A streamer may be able to make money from their own home and all alone. Yes, they do need to be live recording their life, but they are their own boss.

There are many ways to make money on Twitch such as with paid subscriptions, display ads, selling merchandise (like t-shirts and mugs), and more.

Some of the most successful Twitch streamers make hundreds of thousands or even millions of dollars each year, but, it’s important to know that most don’t earn much at all.

Recommended reading: How Much Do Twitch Streamers Make?

38. Litter Cleanup Worker

If you own a business, it’s important to keep your place clean and tidy. Nobody likes to see trash lying around, right?

That’s why some business owners are happy to pay for someone to clean up before their business opens for the day. A clean area makes the place look nice and welcoming for customers.

This business can be started all alone and earnings on average are about $30 to $50 for every hour you work. It’s pretty simple too. You’ll just need a broom, a dustpan, and some tools to help you pick up litter easily. It’s almost like taking a stroll while you work! Plus, you can choose when you want to do it, so it can fit nicely into your schedule.

Recommended reading: How I Started A $650,000 Per Year Litter Cleanup Business

39. Google Rater

A Search Engine Evaluator, also known as a Google Rater, is a person who looks at websites and blogs and gives them a score based on how good and helpful they are for Google.

You don’t need to be a tech expert or have a fancy background for this job. Google actually wants regular people, just like you, to rate websites. Plus, you can do this in your own language. Google works in lots of different countries, so you can help out right from where you are.

Recommended reading: How To Become a Search Engine Evaluator

40. Actuary

An actuary is a financial expert who helps businesses figure out and manage their money-related risks, such as for insurance, pensions, and investments.

They use mathematics and statistics to forecast what might happen and help companies make smarter financial decisions.

Actuaries can earn a good salary, and as they get more experience and pass more exams, they can make even more money. Depending on where they work and how experienced they are, actuaries earn average salaries of anywhere between $70,000 to well over $100,000 each year.

Frequently Asked Questions About Jobs Where You Work Alone

Here are answers to common questions about finding jobs where you work alone.

What are jobs with no interaction?What jobs allow me to work by myself?

Yes, there are jobs where you don’t need to talk to people a lot. For example, being a night shift security guard, a transcriptionist, or a stock photo photographer.

How can I work alone from home?

There are jobs where you can work alone at home such as being a blogger, a transcriptionist, or a computer programmer.

What are jobs where you work alone with no degree?

Many jobs don’t require bachelor’s or master’s degrees (a high school diploma will work for many on the list above) and offer the opportunity to work independently. Mowing lawns, painting houses, repairing cars, or walking dogs often don’t require formal education and focus more on skills and experience.

Which part-time jobs are best suited for solitary workers?

Many of the jobs in this blog post can be done part-time, such as any of the freelance jobs, house cleaning, dog walking, and taking surveys. That is one of the joys of many of the jobs above – you can choose your schedule.

What trade jobs can one perform independently?

Trade jobs that you can perform independently include carpentry, welding, or plumbing. These professions usually require specific skills or certifications but may offer opportunities to work alone.

Are there any tech jobs ideal for people who prefer to work alone?

Yes, there are tech jobs that can work well for people who want to work on their own such as web developers, software engineers, or data analysts. These roles usually involve solving problems and working independently, though there might be some instances where collaboration is needed from time to time.

What jobs can be done in isolation with no experience required?

Jobs such as house cleaning, taking surveys, and flea market flipping can be good places to start for entry-level jobs.

How can I find work-alone job opportunities near me?

To find work-alone job opportunities near you, try perusing local job boards, classified ads, or online sites like Indeed or LinkedIn. You can also network with people in your community or join online forums related to your interests to find jobs.

Jobs Where You Work Alone – Summary

I hope you enjoyed this article on jobs where you work alone.

These jobs are like a safe space for people who like being by themselves. It’s a place where you can really concentrate and do your own thing with low social interaction. Jobs where you work alone often appeal to introverts and individuals who require fewer distractions.

Jobs like writing, coding, and freelancing let you work on your own. Not everyone may like working alone, but for those who do, it can be a lot less stressful and overwhelming.

I have been working mostly on my own for years now, and I really love it!

For example, bank regulators in July released a plan to increase capital requirements for residential mortgages, the Basel III Endgame rules. Redwood executives are positioning the company to acquire mortgage loans in the market, mainly jumbos, with the expectation that banks will have a reduced appetite.

Abate doesn’t think “banks are going to necessarily exit the mortgage market,” but they will “be heavily disincentivized from growing mortgage portfolios.” Ultimately, “the real shift is going to be all those jumbos that were going to banks will come back out, hopefully to non-banks like us.”

Another opportunity is in the home equity space. Redwood launched in September its in-house home equity investment (HEI) origination platform called Aspire. Through Aspire, Redwood plans to directly originate HEIs by leveraging the company’s nationwide correspondent network of loan officers and establishing direct-to-consumer origination channels, the company said.

“The interesting thing about HEIs is instead of a homeowner taking out equity in the form of cash and paying a mortgage on it, there is no monthly payment within HEI,” Abate said. “The way the investor gets paid is that you share in the upside of the home.”

Abate explained the impacts of the Basel III Endgame rules on the market, the rationale behind the home equity investment product, and more about Redwood strategies in an interview with HousingWire from a company’s office in New York last week.

This interview has been condensed and edited for clarity.

Flávia Nunes: How has Redwood strategically positioned itself in the residential mortgage space amid all of these potential regulatory changes?

Christopher Abate: Redwood is almost a 30-year-old company. The company was originally built to serve banks and others with the thought that there was no private sector [to invest in mortgage assets], only Fannie Mae and Freddie Mac. We would partner with banks to buy their loans and securitize them so the banks could recycle their capital. We don’t originate residential mortgages. We don’t service them. We’re very similar to the GSEs. We modeled the business to serve that role in the private sector. The mortgage market has changed over the decades. We’ve seen a few cycles. We’ve got the Great Financial Crisis, the Covid-19 pandemic, and now we’ve had a lot of interest rate volatility. Along the way, there have been many regulatory changes that have impacted the market; the CFPB has been created, and there’s the Dodd-Frank Act. Then there are the Basel rules, the regulatory capital rules for banks. And that’s what’s really in play today.

We’ve positioned the company, from a strategic perspective, with the thought that banks will be heavily disincentivized from growing mortgage portfolios as an earning asset class. The banks are not going to necessarily exit the mortgage market because the mortgage asset is the biggest that a client takes out, and you want to be there for all the cross-selling in all the other consumer products. Banks will always serve their best clients. But viewing the mortgage portfolio as an investment class, that’s where the posture will shift because the capital required to hold against it [residential mortgages] is going to go up. And just based on the rapidly rising rate of deposits, just given where interest rates are at, the net interest income that they earn is getting squeezed. Banks move slowly. This will be an evolutionary shift, not an overnight shift.

Nunes:As you noted, bank regulators released a plan to increase capital requirements for mortgages through the Basel III Endgame rules. Can we expect changes to what was proposed?

Abate: Yes, it will change. In particular, some of the sliding scale capital charges are based on things like LTV [loan-to-value]; there’s a fair likelihood that that changes because of the way it disproportionately impacts first-time homebuyers and underserved communities. But the rule is not going away. Bank regulators are paid to keep things safe. And the idea that regulators are going to allow banks to continue to do what a First Republic or Silicon Valley Bank did, I don’t see that in the cards.

We saw significant changes after the Great Financial Crisis, which was more of a credit crisis. We saw banks getting out of risky credit mortgages like option ARMs and some subprime lending happening back then. There will be changes. Banks will not wait for the rule to be finalized to start implementing it. There will be some evolution to the rule itself. But the thrust of the rule is that it’s going to be more expensive for banks to hold mortgages.

Nunes:If banks won’t wait for the Basel III Endgame to be finalized, how are they anticipating the rules?

Abate: A year ago, banks were very happy to hold mortgages, deposit rates were sticky, and the cost of deposits was still very low. Now, all of them are looking for a capital partner, at least an option to have liquidity. The tone has changed dramatically amongst bank executives. Some banks move more slowly than others.

I like to remind people that independent mortgage banks live and die by liquidity. They care about the basis point. Banks don’t operate that close to the ground. Things take longer to develop, but the relationships are also typically stickier. Once you forge a strong partnership with a bank partner, the likelihood of them shopping for that liquidity is much less than an independent mortgage bank that is trying to optimize every dollar.

Nunes: In your recent 2Q 2023 earnings report, you mentioned acquiring three bulk pools of loans from depositories, primarily with seasoned underlying loans at attractive discounts. How is the secondary market now for these trades in terms of volumes and prices?

Abate: I certainly expect RMBS volumes to go up significantly over time. It’s not something that happens overnight. We’ve been active. We just completed a deal in August. I would expect us to continue using securitization.

Right now, we’re in this hybrid phase where loans that are getting securitized are partially seasoned loans, and some of the loans have gone down in value–the lower coupon mortgages. The banks have been slowly selling some of those, and Wall Street dealers have quite a bit in inventory. We’re still seeing a lot of that aged collateral coming out through securitization. Issuers like Redwood have been combining current coupon mortgages. We saw this last year in the private sector securitization market, where we had all of this aged inventory. It was hard to get investors to focus on the collateral because there was so much sitting in inventory that they could price it wherever they wanted to. The pricing now is probably the best it’s been in a year, maybe two years. So, the market is finally starting to cross back into more current coupon on-the-run production, which is what we’re focused on.

We’ve completed well over 100 residential securitizations, close to 140 If we factor CoreVest. There’s been years we’ve done 12-15 securitizations. There’s been years where we’ve done none or one. So, we very much want to get volume going again to the extent we could be in the market with certainly a deal a quarter, but if not two or three, that would feel the base to me.

Nunes:In terms of products, what the current landscape brings in terms of opportunities?

Abate: Right now, the biggest opportunity, ironically, is in the regular prime jumbo market because that was the product banks were most focused on. And they weren’t wrong to focus on it from a credit standpoint because when the banks got through the Great Financial Crisis, all the big regulatory shifts were to get them out of taking risky mortgages on the balance sheet. Then, they started taking less risky mortgages, which are jumbos. The real shift is going to be all those jumbos that were going to banks will come back out, hopefully to non-banks like us.

Nunes:Redwood also launched a home equity platform. What is the strategy here?

Abate: When you look at prime rates in the high single digits and add a credit spread to that, even for the most well-qualified borrowers, you are looking at a 10% to 12% interest rate on a second mortgage. For a well-qualified borrower, 750 FICO or above, and a low-LTV first mortgage, you might be comfortable paying 10% to 12%. But that’s the best-case scenario. For everybody else, unlocking that equity is even more expensive. We’re seeing that for the traditional second mortgage products, there’s way more investor demand than consumer demand.

We’ve rolled out the traditional products and a newer product called home equity investment [HEI] options. The interesting thing about HEIs is instead of a homeowner taking out equity in the form of cash and paying a mortgage on it, there is no monthly payment within HEI. The way the investor gets paid is that you share in the upside of the home, so the home price appreciation. There are a lot of use cases for HEI over traditional products. If you think about somebody with a lot of student debt or lower FICO, they’re going to qualify for a very expensive second mortgage. So, this is a good option. It doesn’t add to their monthly payment obligation. You can do what you want with the cash, just like with a home equity line of credit, but not having the payment. It’s a bridge until the second mortgage is cheaper.

Nunes:To invest in this product, investors must believe home prices will keep rising, right?

Abate: There are a couple of things investors care about. You haveto believe in a HPA [home price appreciation] story. But one way we mitigate that is we strike the price of the home at a discount to its current appraised value. So that, even if the home is sold next week, the investor will make money. If you believe that interest rates are nearing the top, as far as the Fed’s rate hike cycle, HPA should start to realign. If rates are going down, HPAs are going up. Investors are starting to get comfortable with this huge move in rates, hopefully, this fall is gonna pause.

Then, ultimately, the investors want to understand if we give you $100,000 with this HEI, when do they get their money back? Because it’s a 30-year product. And that’s where we’ve designed the product, which is unique to Redwood, that creates strong incentives for the homeowner to refi.

Nunes: How did you get the property at a discount?

Abate: The product is for people in their homes that are not moving out. There isn’t an actual transaction on the property. It’s somebody that wants to stay in their home. And if it’s a $1 million home, and we offer you $150,000 HEI, we might strike that HEI at $900,000. Let’s say it’s a $1 million home, and for purposes of coming up with the investor return, we’re going to call it a home at $850,000. Even if they sold the home at a $50,000 loss, the investor would still generate a return, and that’s what gets investor capital into the asset class. But what the homeowner gets is all of the proceeds, the cash and no monthly payments

The investors are institutional investors, well-known institutions, firms, pension funds, and life companies; they’re all just to varying degrees focused on HEI now. And the big reason is that nobody’s been able to tap this massive home equity opportunity. We are going to give it a try.

Nunes: Residential mortgages are just one facet of the business. What are your plans for commercial real estate, which has had a challenging year?

Abate:What we do here in New York is our business-purpose lending platform. We realized a number of years ago that investors are becoming a much bigger participant in the real estate markets. Serving them and providing bridge loans to investors who want to flip homes or provide turned-out financing for investors who want to rent homes, that’s an entire other residential business that we run under the flag of CoreVest. In residential, we’ve more or less stuck to our knitting of non-agency. We’ve had opportunities to enter the agency space in the past and participated in certain instances, but mostly, what we do is non-agency.

Nunes: You mentioned banks, but what are the business opportunities with IMBs?

Abate: We’ve had a great long-term relationship with the IMBs. The IMBs have a big opportunity to pick up some [market] share. Since the Great Financial Crisis, most of our business has been with the IMBs. We have a network of between 150 to 200 [partners], predominantly non-banks that we will buy mortgages from. We expect that to rebalance in the next few years. But the IMBs are also a big opportunity to take clients from the banks.

Nunes: And what are the plans for servicing mortgage rights?

Abate: Servicing will continue to move out of the banks. That’s another big opportunity that we’ll focus on. We don’t plan to operate as a servicer, but we might own servicing rights. What we’ve done typically is when we own servicing rights, we will subservice. We want to hire somebody with a call center. And we’ll pay them a monthly fee. But when you balance out the revenue potential with the servicing asset, with the cost of service, there are still good opportunities. There’s a lot of competition for servicing. For some mortgage REITs, that’s their primary asset class, just not for us.

Nunes:Can you shed some light on your partnership with Oaktree and Riverbend?

Abate: Both of those are related to the business-purpose lender space. Oaktree is a great example of us expanding our capital partnerships into the private credit sector. Redwood is a publicly traded company, and historically, when we needed to raise money, we would do a common stock offering or a public market deal. When rates started going up, things got pretty ugly for the mortgage REIT space and the public markets. We and all other mortgage REITs started trading at discounts. Raising money in that environment hasn’t been overly attractive. So, building partnerships with private credit firms like Oaktree to focus on specific asset classes is a big part of what we want to do. One aspect that’s attractive to us is we can earn asset management fees.

The Oaktree model is something that we want to replicate on the residential side as the jumbo opportunity picks up. We’ve been in discussions with other private credit investors and institutional investors who see the same opportunity as in jumbo and non-QM.

Nunes: With a reported cash and cash equivalents of $357 million as of June 2023, can we anticipate any M&A activities, especially considering the challenges faced by many lenders in the industry?

Abate: M&A activity has picked up in the space and based on our track record, we are a logical call. Part of our strategy is: to be active in M&A, you have to be active. It’s not efficient to call on at eight, seven different firms. You start with the ones that have shown interest in actually transacting. We have seen some opportunities, and nothing I can share in this interview, but it’s safe to say we’ve been active in M&As and we’ll continue to focus on that as part of our growth strategy.

We haven’t been open to it [acquiring a lender]. For many years, we’ve wanted to keep the business sort of regulator-light. The best way to do that is not to directly face consumers with products. We’re comfortable originating to investors, that’s what CoreWest does. But investors are sophisticated business-run ventures and not homeowners who may or may not be sophisticated in the financial markets. We have tended to not originate, but I think where we’re at as a company is from a strategic standpoint, we’d be much more open to it through M&A.

Nunes: What do you expect for the macro landscape in the coming year?

Abate: There’s such a vast shortage of supply of homes in many parts of the country, which is supporting home prices. The Fed consciously inflated home prices, particularly during the COVID years. These high asset values prevented normal credit losses you might see through a cycle. The combination of QE-fueled asset prices with an economy that hasn’t dropped off too much has created a strong housing market.

But credit in residential housing should perform immensely better than many facets of the commercial real estate market. There’s so much vacancy in these central business districts. These buildings are valued based on cash flows– not like a residential home, which is an appraisal. If it’s 50% full, it’s worth half as much. From a credit standpoint, certain facets of the commercial real estate sector will have a rough road ahead.

I’m probably supposed to say this, but I feel better about my sector. The technical supporting housing will continue to be strong. The big challenge with residential today is just transaction activity. If you own a home with a 3% mortgage, you don’t want to sell it. If your home suits your needs, the prospect of doubling your monthly payment to move is very unappealing. The real challenge in residential has been a lot of capacity to make loans, but there’s not much demand. If rates do stabilize, that will change quickly. When the market thought in January that rates were stabilizing, we saw a pickup in loan activity, and then they started going up again; we’ll see what happens this fall.

Nunes:Do you see a crisis on the commercial side of the market? If so, how could it impact the residential side?

Abate: It’s hard to say. The only real obvious driver for a crisis is what could be a permanent impairment of occupancy in these commercial office buildings. The way that can affect our markets is there’s a trickle-down effect. If the buildings aren’t full, the restaurants aren’t full, the delis aren’t full, the subways are not full, and the hotels aren’t full because people aren’t traveling to see people in the office. That could have an effect on the economy in general, which would impact housing indirectly. As far as the economy goes, the airports seem more full than ever, and hotels seem to be doing fine. Overall, [the problem] is probably mostly office. But if it keeps getting worse, it certainly could have downstream effects.

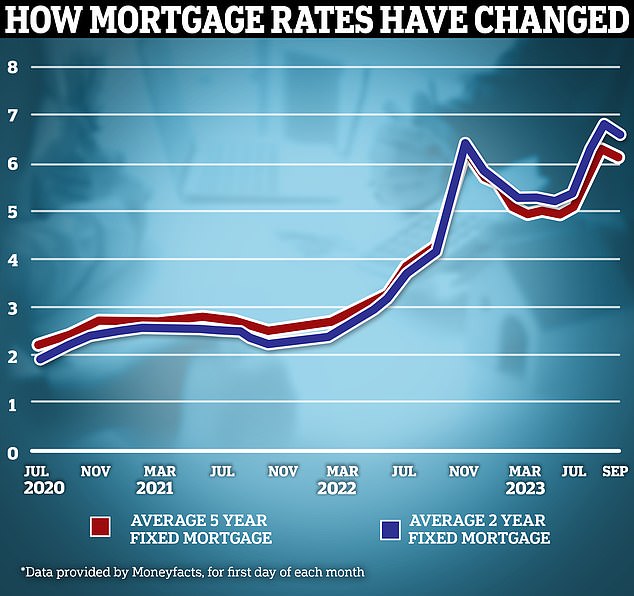

Fixed rate mortgages have dipped below 5 per cent for the first time since early July, offering some hope to struggling homeowners.

Yorkshire Building Society has launched a 4.99 per cent fixed-rate deal which is available to both home buyers and those remortgaging.

It’s available at 75 per cent loan-to-value, meaning eligible customers can apply as long as they either have at least a 25 per cent deposit or 25 per cent equity within their home.

Best rate: Yorkshire Building Society has launched a 4.99 per cent fixed rate deal aimed at both homebuyers and those remortgaging

Someone with a £200,000 mortgage could expect to pay £1,168 a month if repaying over a 25-year term, compared to the market average of £1,249 a month.

The five-year deal comes with a £1,495 fee, however, and a mortgage with a higher rate but a lower fee may be a better deal for some customers.

You can compare rates and fees and work out the true cost of a mortgage using our calculator.

After Yorkshire BS, the next best deal is Virgin Money which has a five-year fix at 5.07 per cent and is available to home buyers purchasing with at least a 35 per cent deposit (65 per cent loan-to-value).

HSBC has a five-year fix at 5.09 per cent for home buyers with at least a 40 per cent deposit (loan-to-value of 60 per cent).

Nationwide also has a 10-year fix available at 5.04 per cent which is available to home buyers with a deposit of 15 per cent or more (85 per cent loan-to-value).

The average five-year fixed mortgage rate is now 5.67 per cent, according to Rightmove.

Rachel Springall, finance expert at Moneyfacts said: ‘It’s great to see such competitive deals launched by Yorkshire Building Society.

‘Borrowers looking for a new low-rate mortgage will find the sub-5 per cent five-year fixed deal is the lowest rate available in its sector.

‘The incentive packages available across all the new deals today may also be popular with borrowers looking to save on the upfront cost of their mortgage.’

Why are mortgage rates going down?

Yorkshire BS’ decision to cut rates, which includes shaving off up to 0.46 percentage points from its 95 per cent loan-to-value deals, is partly due to competition between lenders.

HSBC has also slashed mortgage rates by 0.15 percentage points on average today, alongside rate cuts across its buy-to-let range of up to 0.3 percentage points.

Last week there were also cuts from Coventry BS, Nationwide BS, Accord, Generation Home, Barclays, and Clydesdale Bank.

Past the peak? Fixed mortgage rates appear to be falling back somewhat after a barrage of rate hikes in recent months

Rate cuts have also been encouraged by future market expectations over where interest rates are heading.

Market expectations are reflected in swap rates. These are agreements in which two counter parties, for example banks, agree to exchange a stream of future fixed interest payments for a stream of future variable payments, based on a set amount.

Mortgage lenders enter into these agreements to shield themselves against the interest rate risk involved with lending fixed rate mortgages.

Put more simply, swap rates show what financial institutions think the future holds concerning interest rates.

Five-year swaps are currently at around 4.56 per cent, which is down from 4.74 per cent at the start of this month.

Only as recently as July, five year swaps were above 5 per cent. Similarly, the two-year swap rate is now 5.21 per cent. In July early this was around 6 per cent.

Ben Merritt, director of mortgages at Yorkshire Building Society, said: ‘This week, favourable market swap rates presented just such a window to reduce our mortgage costs, and offer the greatest incentive to those people who typically struggle the most, those with the lowest deposits to put down, including first-time buyers.’

Nicholas Mendes, mortgage technical manager at broker, John Charcol says he wouldn’t rule out a five-year fix at 4.5% by the end of the year

Will mortgages be hiked again if base rate rises?

The Bank of England is widely expected to increase the base rate from 5.25 per cent to 5.5 per cent on Thursday, though some economists are betting on it remaining the same.

The decision will come the day after we learn August’s inflation reading, which many are expecting may go up as a result of higher fuel prices. This may have some bearing on what the Bank of England decides to do with base rate.

If base rate does go up, this will likely increase costs for those on variable rate mortgage deals.

However, it is unlikely to have the same impact on fixed rate products, according to Nicholas Mendes, mortgage technical manager at broker John Charcol. In fact, he expects fixed rate deals to continue falling.

‘The MPC meeting is expected to either hold or rise by 0.25 per cent which will no doubt be the last [rate rise],’ says Mendes.

‘Even in the event there is a rate rise this has already been caked into fixed rate pricing.

‘As a result I expect to see fixed rate pricing on two and five year fixes continue to reduce.

‘While no one can accurately be confident, I wouldn’t rule out a five year fixed at 4.5 per cent by the end of the year based on current pricing trajectory.’

How are mortgage rates affecting the housing market?

While it is good news that mortgage rates are falling, we remain a long way from the low rates enjoyed in previous years.

This time last year, it was possible to secure a fixed rate at 3 per cent and the year before that borrowers were able to secure deals at less than 1 per cent.

The change in mortgage rates has unsurprisingly had an impact on the housing market. Transactions are down by almost 20 per cent, while house prices are also falling.

Last week it was reported that mortgage arrears had hit their highest level for nearly seven years.

The value of outstanding home loans with arrears climbed by 13 per cent to £16.9billion in the second quarter of this year, according to Bank of England figures.

It was the highest level since the third quarter of 2016, and 29 per cent higher than the same period a year ago.

Although there may be less activity across the housing market, Mendes says he isn’t expecting to see a sudden surge in forced sales.

‘Fixed rate mortgages around 5 per cent may dampen purchase demand as prospective home movers postpone their plans, but I still expect to see first-time buyers to continue purchasing,’ he says.

‘With rents continuing to increase, fixed rates at 5 per cent or less could encourage more first time buyers and those in rented accommodation to purchase as a cost-effective alternative.

‘A significant increase in arrears was down to landlords which is understandable in this climate over the past year.

Downwards: Over the past few weeks, mortgages rates have continued to trickle downwards due to competition between lenders and market expectations about interest rates in the future

‘For residential homeowners there are more options to avoid falling into arrears – unless they decide to bury their head in the sand.

‘There is more support from lenders and the Mortgage Charter which allows a grace period of six months which would allow mortgage holders to sell a property before things start to escalate downwards.’

Mark Harris, chief executive of mortgage broker SPF Private Clients, says that falling mortgage rates will result in buyers being able to afford bigger mortgages which should lead to an increase in transactions.

Harris adds: ‘Falling interest may encourage more borrowers to take the plunge and take on a mortgage. However, it is not just about falling mortgage rates but affordability and the underwriting of the loan.

‘Lenders are still required to stress test the borrowing at a minimum of 1 per cent above the reversion rate, with some lenders utilising different lower rates for long/longer term fixes.

‘When these stress rates also start to fall, borrowers will be able to take on bigger mortgages, which may lead to an uptick in transactions and mortgage lending.’

HELOC, Manufactured, Technology, Marketing, and Digital Tools; Central Banks and Inflation

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

HELOC, Manufactured, Technology, Marketing, and Digital Tools; Central Banks and Inflation

By: Rob Chrisman

7 Hours, 56 Min ago

If you want something sobering, almost mesmerizing, here’s a short drone video of the flood damage in Libya (at the 15 second mark you can see how it tore through the city). Fortunately not so sobering are some stats out of the United States. The U.S. homeownership rate in 2022 was even higher than before the COVID-19 pandemic at 65.8 percent compared to 64.6 percent in 2019. That rebound was driven largely by those aged 44 and younger. And who says Millennials aren’t buying homes? Homeownership continued to climb from the foreclosure crisis (2004) and Great Recession (2008), when rates dipped as low as 63.4 percent in 2016. Homeownership rates recovered approximately half of the 5.6 percent decrease from 2004 to 2016. In Hawai’i the homeownership rate is 59 percent, I bring up the Aloha State because American Savings Bank, First Hawaiian Bank, and Central Pacific Bank joined Hawaiʻi Community Lending, a Hawaiʻi-based nonprofit community development financial institution, in pledging to provide mortgage forbearances to Maui families impacted by the recent wildfires. (Today’s podcast can be found here and this week’s is sponsored by the Trade-In Mortgage powered by Calque. Homeowners can buy before they sell, make non-contingent offers, and tap their home equity to fund the down payment on their next home. Lenders can help their clients negotiate a lower purchase price, reduce their interest payments, and eliminate PMI. Today’s podcast features Greg Korn and Ben Petit in an interview from the New England Mortgage Bankers Conference.)

Lender and Broker Software, Products, and Services

In an era defined by technological advancements, Dark Matter Technologies LLC emerges as a transformative force in the mortgage origination landscape, marking its evolution from Black Knight Origination Technologies. Under the Perseus Operating Group of Constellation Software Inc., Dark Matter Technologies remains steadfast in its commitment to pioneering innovation. CEO Rich Gagliano aptly sums up the company’s vision: “Dark Matter Technologies is on a mission to revolutionize the mortgage origination business by supporting, growing, and aggressively innovating new and existing products.” With over 1,300 dedicated mortgage technology experts and a portfolio that includes Empower, AIVA, Exchange, and more, Dark Matter Technologies is poised to lead the industry into a new era of unparalleled transformation. Learn more about Dark Matter Technologies and their mission, here.

There is approximately $9T in agency or government MSR outstanding. Billions of dollars are being transacted daily and this volume requires disciplined loan accounting processes to record loans accurately, produce investor reporting, and power business decisions. SBO from SitusAMC is a comprehensive loan accounting and master servicing platform that reconciles daily and monthly servicer cash collections down to the penny, aiding in the discovery of potentially misplaced funds and enhancing the financial integrity of the entire process. Servicers using SBO produce accurate and timely details providing confidence that their investor reporting obligations are being met. Schedule a demo of SBO with SitusAMC’s client-focused experts.

“Did you hear Capacity’s big announcement at TMC Fall? We’ve acquired Denim Social! Together, we’re building a support automation platform that helps you automate support, connect more authentically with your borrowers, and close more loans, faster. Read the press release to learn more! We also gave away a personalized AI Assessment worth $10,000 to help mortgage lenders identify opportunities for improving their business with AI. Plus, our new GSE Search feature pulls accurate, up to date GSE regulations within seconds using generative AI. Want to join the AI in mortgage revolution? Meet the Capacity team today.”

A new era in loan origination has arrived. Mortgage Machine Services, an industry leader in digital origination technology to residential mortgage lenders, announced the launch of its namesake platform Mortgage Machine™, an out-of-the-box, all-in-one LOS designed to accelerate lenders’ operational velocity and support an end-to-end digital origination process. Developed by digital mortgage pioneer and industry veteran Jeff Bode, Mortgage Machine utilizes intelligent automation, configurable business workflows and a cloud-based infrastructure to optimize the entire loan lifecycle and create a seamless lending experience. Key platform features include AI-powered task automation, a scalable cloud-based infrastructure, flexible APIs, pre-configured workflows for retail and TPO channels, integrated document management and POS functionality. Mortgage Machine also offers all-in-one eClosing capabilities, including an eClose room, eNotes, eVault and RON, and utilizes MISMO SMART Doc® data and security standards. Visit here to get started on your digital transformation journey.

Blend Labs continues to be the mortgage industry’s leading technology platform. Core to the platform is Blend’s unique integration with Desktop Underwriter® (DU®) and LPA. These integrations help streamline your approval process for borrowers, with all the conditions lined up for your fulfillment team. Add in intelligent and automated follow-ups and you’ll get to the closing table faster and more efficiently. Putting this information at the loan officer’s fingertips creates a streamlined process and eliminates manual work which equals lower costs, higher pull-through, and increased revenue. See more ways that Blend is committing to innovation and continues to lead the way.

Looking for timely advice on how to capture more loan volume and improve your bottom line in a down market? Now is the time to explore ways to tap into new markets. Expanding your mortgage footprint through new products and channels or by reaching new geographies insulates your business against economic and interest rate volatility by diversifying your sources of volume and revenue. By setting the groundwork to connect with new borrower markets now, you’ll open new revenue possibilities for when the market inevitably recovers, positioning your business to hit the ground running and beat out the competition. Download this informative eBook from mortgage solutions provider Maxwell for actionable advice, including how to create your expansion plan and choose the offerings best suited to the markets you want to pursue. Click here to download Growing Your Mortgage Footprint: How to Launch New Loan Products, Channels & Geographic Expansions.

Broker and Correspondent Products

Build your book with AFR Wholesale® (AFR)! Now, get the chance to listen from and ask questions directly to AFR and Freddie Mac to turn those prospects to active pipeline at the next Why Wait webinar series covering Manufactured Home Financing on Wednesday, September 20th at 1 PM EST. Register here today! Have you and your borrowers looked into Manufactured Housing as an option? With unbeatable affordability, customization options that are very tailored, quick installation and trusted quality, manufactured homes are worth exploring. Especially with a top lending partner in AFR who has been an industry leader for over 25 years. This is a live webinar, and a recording will not be provided so make sure to join and get great insight and have the opportunity to ask questions and listen to scenarios! Visit AFR Wholesale, email [email protected], or dial 1-800-375-6071. AFR Wholesale® – Don’t wait. Register today!

“With Cash-Outs on the decline during this high interest rate environment, it is important to present your borrowers with different cash-out options. That is why Vista Point is announcing a brand new HELOC product coming soon, in addition to our existing Closed-End Second. Our HELOC product is being designed as a complement to our Closed-End Second to provide a full suite of Equity Solutions. Our HELOC will provide a specific solution for borrowers that want the optionality of an interest-only payment, or the ability to draw up and buy down their line during the 5-year draw period with no Appraisals up to $250k. Just like on our Closed-End Second offering, with HELOC loan amounts up to $550K and combined lien amounts up to $2.5M, your borrowers can get the cash they need without sacrificing their advantageous 1st mortgage rate. HELOC will be available for full doc and bank statements on OO and 2nd homes. For more information, reach out to us, or meet us at the Philly MBA to discuss.”

Capital Markets

We learned last week that prices in August rose by the largest monthly percentage in 15 months. However, that month-over-month inflation was widely expected due to a surge in gasoline prices. Underlying oil prices are also pointing towards further increases in September. Meanwhile, core prices were up 0.3 percent and core goods prices declined by 0.1 percent. Over the last three months core prices have increased at an annualized pace of 2.4 percent, the lowest three-month pace since March 2021. Retail sales rose faster than analysts’ expectations in August, also due to higher gas prices. Many analysts expect consumer spending to slow as excess savings built up over the pandemic have materially declined and credit is increasingly costly and difficult to obtain. Additionally, the resumption of student loan payments is expected to cut into discretionary spending. It will take more than expectations of slower spending before the Federal Reserve feels inflation is firmly under control.

What could move mortgage rates this week? The U.S. Federal Reserve, Bank of England, Bank of Japan, and the central banks of Norway, Sweden, and Switzerland are all announcing rate decisions after a spate of recent inflation data shows that price increases are alive and well. The Fed’s Federal Open Market Committee (FOMC), the action arm of “the Fed,” is not expected to raise rates. It’s unlikely that the commentary around the commitment to keep fighting inflation and higher rates for longer will change either, but it could tilt a little more to the hawkish side after a stronger-than-anticipated inflation report for August.

The week could also see some extra drama on the political front as the countdown continues toward a potential government shutdown on October 1 in addition to the battle between the United Auto Workers (UAW) union and Detroit automakers. The auto worker strike could complicate Fed Chair Powell’s bid for a soft landing. Union leaders are asking for a 36 percent wage increase over four years, to match the similar recent pay increase for top executives. The union also wants pay to rise automatically with inflation in the future, as it did before the financial crisis.

This week brings the aforementioned FOMC meeting that begins tomorrow and concludes on Wednesday with the Statement, updated SEP (where fed funds projections will be closely scrutinized), and Chair Powell’s press conference. The treasury will also be in the headlines with more coupon auctions scheduled: $13 billion reopened 20-year bonds tomorrow and $15 billion reopened 10-year TIPS on Thursday. The only scheduled, probably non-market moving, news out today is the NAHB Housing Market Index for September. We begin the week with Agency MBS prices roughly unchanged from Friday, the 10-year yielding 4.34 after closing last week at 4.33 percent, and the 2-year is at 5.00 percent.

Employment

Are you more energized, more encouraged, and more motivated to succeed today than yesterday? Zig Ziglar famously stated, “People often say that motivation doesn’t last. Well, neither does bathing; that’s why we recommend it daily.” “As an industry leader, Thrive knows that motivation, discipline, and belief in your ability to succeed is critical,” stated Randell Gillespie, National Sales Leader for Thrive Mortgage. “There is no better time than now to find ways to continually motivate your team, which is why we put so much focus on daily opportunities like these at Thrive. Through our weekly High-Performance Coaching Calls, our very own nationally-recognized Marketing Master, James Duncan, leads these motivating and educational experiences for results. The biggest names in the mortgage industry and thought-leadership have been part of our Thrive Nation broadcasts. We want everyone to be better today than yesterday. Start a conversation with us and find out how.

“The fall season is here, and now more than ever is the time to build rapport with your referral partners and clients to maintain a steady stream of business. At Guaranteed Rate Affinity, not only do we have the greatest number of products, but we have the tech platform for our loan officers to do business from anywhere. With PowerVP, you can do anything from creating loan applications to sending pre-approval letters all from your mobile phone. Anything you could do from your desk, you can now do on the go with PowerVP. Gone are the days of being chained to your desk and missing out on important moments. Primarily, it gives you a work-life balance you never thought possible. Luckily, we’re hiring the best of the best loan officers to leverage our tech platform to grow their business. Ready to learn more? Contact Tim McGraw to get started.”

Download our mobile app to get alerts for Rob Chrisman’s Commentary.

Share via Social Media:

All social media shares will include the image and link to this page.

Dark Matter Technologies, formerly Black Knight Origination Technologies, is focused on mainly two things: the smooth transition to new owners, and lowering the cost to originate loans for lenders.

Executives from Dark Matter Technologies, under the Constellation Software umbrella, said that a down market is the best time to make investments in technology and prepare for the next cycle.

With lenders focused on bringing origination costs down in a tough origination environment, the firm saw up to a 300% year-over-year growth in new user numbers for the past couple of years.

“We actually do well in any kind of market,” Rich Gagliano, CEO of Dark Matter Technologies and former president of Black Knight, said in an interview with HousingWire on Friday.

“Now we’re in a down cycle, they need to do it with fewer people and they need to be more efficient to get the cost down. So it’s really the same story, just different markets,” Gagliano said.

Dark Matter Technologies, which completed the acquisition of Black Knight’s Empower and Optimal Blue last week, will be working towards a smooth transition over to Constellation Software with its 1,300-plus employees for the remainder of the year.

The company doesn’t plan to raise pricing for Empower and is focused on services and products that will drive down the cost of origination and employee borrower retention, executives said.

Gagliano, Sean Dugan, CRO of Dark Matter Technologies and Tom George, co-president of Romulus, part of the Perseus Group of Constellation Software, participated in the interview.

Read on to learn more about Dark Matter Technologies’ plan for mortgage.

This interview has been condensed and lightly edited for clarity.

Connie Kim: Constellation’s Perseus Group has a pretty big real estate portfolio. What were the reasons for buying Black Knight’s Empower and Optimal Blue? What opportunities did the firm see?

Tom George: The way Constellation operates is that we focus on acquiring vertical market software companies and portfolios of vertical market software companies with the intent to stay in these industries forever.

We started almost 20 years ago and Perseus in the homebuilding industry, we built a significant player in homebuilding software, that led us to an adjacency residential real estate where we bought over 20 companies. More recently, we started acquiring businesses in the mortgage tech space.

We plan to be in the mortgage tech space forever. And we plan to continue to acquire there.

Kim: What other mortgage tech companies has Constellation Software acquired?

George: We’ve acquired three other businesses in the mortgage space. We bought Mortgage BuilderSoftware from Altisource Portfolio Solutions in 2019. There have been two additional acquisitions – ReverseVision, which is a leader in the reverse mortgage LOS space, and then a document storage product called Back Support.

Kim: Are you expecting any layoffs during the transition? Will the same management from Black Knight’s Empower and Optimal Blue be in place?

Rich Gagliano: We’re not expecting any changes. [About] 1300 [employees] are going to move over with us and it’s business as usual.

Kim: It’s a tough mortgage origination market right now. How does the company expect to manage profit amid industry consolidation, bankruptcies and attrition?

Gagliano: We’ve seen a strong pipeline. Even though the markets are down, what we encourage and talk to clients about is when you’re slow, that’s the best time to make technology changes. Now is the time for that change, and get yourself ready for the next cycle.

We actually do well in any kind of market. But honestly, when the market is crazy, lenders are looking for efficiencies because they can’t find and hire enough staff. Now we’re in a down cycle, they need to do it with fewer people and they need to be more efficient to get the cost down. So it’s really the same story, just different markets.

Kim: I definitely hear a lot of mortgage tech companies saying ‘this is the time to invest, especially when the market is down.’ You mentioned a strong pipeline, are we talking about new clients?

Sean Dugan: We’ve had 200% to 300% growth year-over-year for the last couple of years. And we don’t see that backing up. Those are not financial metrics, that was just on the number of clients acquired. When we took the Empower LOS platform to the down- to mid-market clients and really focused on that, we saw the number of acquisitions per year grow in a really significant fashion.

Kim: Empower has an estimated market share of around 10-15% after ICE’s Encompass which takes up about 40 to 45% of market share. How does Dark Matter plan to compete against Encompass?

Gagliano: We believe strongly in technology. We’re generally in most of the deals when we know about them. We believe that the automation, and the technology and the solution that we bring, and the ecosystem that we have, is best in the industry and really helps these lenders drive cost out of the system.

We compete with multiple product providers out there, including Encompass. But we like where we are positioned and I think our clients like the innovations that we’ve brought over the past over years.

Kim: When I talk to lenders, they say when using a company’s LOS, using the same company’s add-on products makes it more cost-efficient and seamless. What are some of the add-on products the company has already developed or is seeking to develop to win over lenders?

Gagliano: Just over the past couple of years, we’ve added Ava, which is our artificial intelligence capability. Ava has added a couple of additional products over the past two years. We’ve added an underwriting efficiency product, we’ve added a post-close product that’s going into production – so fairly new products.

We’re going to continue to use the products that we have in our bundle today and sell those so no changes there. But we are incrementally adding new technology, new innovations, that are going to help drive that cost down.

Dugan: We’ve also delivered digital portals for each one of our business channels within Empower, which would include retail, wholesale, correspondent, home equity and assumptions. We also have business intelligence as a component, and then a vendor aggregation platform, which was by the name of Exchange. Those are some of the components that make up the Dark Matter-owned bundle of services within Empower.

Kim:I know Ava has some kind of AI aspect to it. Right now, a lot of mortgage tech companies are focusing on AI. How they’re going to utilize AI to be that middleman between the customer and the loan originator. I’m curious how Dark Matter is going to integrate AI and machine learning (ML) to the LOS and other products.

Dugan: Regardless of what the technology solution is, clients are looking for flexibility, configurability – things that they can configure to meet their particular requirements. They’re looking for a really significant return on their investment, and they’re looking to drive the cost of origination as well as employee and borrower retention.

Kim: One of the concerns about the ICE-Black Knight merger was the fear that ICE would raise prices on the LOS products.Will there be any pricing changes for Dark Matter Technologies?

Gagliano: We don’t have anything planned at this point. Our Constellation partners haven’t asked us to come in and raise prices. That’s not part of their strategy, their strategy is to acquire quality companies and run the businesses.

Kim: Who does Dark Matter Technologies consider as competitors right now?

Dugan: It’s any origination technology provider. There are a number of providers that are delivering services specific to underwriting capabilities, so we would compete with them. So I think it’s a host of providers and vendors across the ecosystem of this particular vertical that we compete with on a day-by-day basis.

Kim: What are your prospects for the remainder of the year for mortgage origination? What are some of the larger goals for Dark Matter Technologies?

Gagliano: Through the end of the year, we’re going to be transitioning to Constellation moving off Black Knight Technologies. We’ve added some corporate-level capabilities already. So we feel good about where we are and stay focused on that through the end of the year.

More than seven in 10 landlords (71%) say they are unlikely to buy a property which has an EPC rating of less than C, according to the latest BVA BDRC landlord research for quarter two 2023.