Buying a home in the U.S. often involves weighing the trade-offs between a 15-year and 30-year mortgage. With the interest rate staying constant, the first option has higher monthly payments, but the loan is repaid sooner than it is with the second option that offers lower monthly payments.

But home loan borrowers in the U.K., Canada, Australia and most European countries have a wider array of choices: They can break up their loan tenure into smaller chunks of two, three, or five years, and get lower interest rates as their loan size reduces and credit rating improves over time.

A new research paper by Wharton finance professor Lu Liu, titled “The Demand for Long-Term Mortgage Contracts and the Role of Collateral,” focuses on the U.K. housing market to explain the choices in mortgage fixed-rate lengths by mortgage borrowers. She pointed out that the length over which mortgage rates stay fixed is an important dimension of how households choose their mortgage contracts, but that has “not been studied explicitly thus far.” Her paper aims to fill that gap.

Liu explained that the U.K. market is “an ideal laboratory” for the study for three reasons: It offers borrowers an array of mortgage length choices; it is a large mortgage market with relatively risky mortgage loans similar to the U.S.; and it offers the opportunity to study market pricing of credit risk in mortgages. In the U.S. market, the pricing of credit risk is distorted as the government-backed Fannie Mae and Freddie Mac provide protection against defaults. “The U.S. is a big outlier in mortgage structure. It has essentially removed credit risk in the markets for long-term contracts.”

How Beneficial Are Long-term Mortgages?

At first sight, long-term mortgage contracts may seem preferable because they have a fixed interest rate, and thus allow borrowers to protect themselves from future rate spikes, the paper noted. “Locking in rates for longer protects households from the risk of repricing, in particular having to refinance and reprice when aggregate interest rates have risen,” Liu said. “In order to insure against such risks, risk-averse households should prefer a longer-term mortgage contract to the alternative of rolling over two short-term mortgage contracts, provided that they have the same expected cost.”

But in studying the U.K. housing market, Liu found that there is an opposing force that may lead some households to choose less protection against interest rate risk. This has to do with how the decline of credit risk over time affects the credit spreads borrowers pay. She explained how that occurs: As a loan gets repaid over time, the loan-to-value (LTV) ratio decreases as households repay the loan balance and house prices appreciate, the paper noted. This reduces the credit spread that households pay on their mortgage over time. When high-LTV borrowers decide to lock in their current rate, the credit spread will account for a large portion of that rate.

“[30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in.” – Lu Liu

As the LTV ratio declines and collateral coverage improves over time, they raise the opportunity cost of longer-term contracts, in particular for high-LTV borrowers, Liu noted. “Locking in current mortgage rates [protects] households against future repricing, but it also locks in the current credit spread, leading households to miss out on credit spread declines over time.”

High-LTV borrowers, or those who opt for low down payments and bigger loans, have to initially pay large credit spreads that can be as high as 220 basis points higher than what a borrower with prime-grade credit would pay. But refinancing with shorter-term contracts allows them to reduce those credit spreads over time. “They’re not locking in to a rate over 30 years; they’re probably locking in at shorter terms of two, three, or five years, and they do it maybe six or seven times,” Liu said. Riskier borrowers with higher LTV ratios hence face a trade-off, as locking in rates while the LTV is high is relatively costly, so they end up choosing shorter-term contracts, meaning they choose less interest-rate protection than less risky borrowers.

“In markets where the credit risk is priced using market prices – without government intervention as in the U.S. — the credit risk is expensive as lenders charge relatively higher rates for that,” Liu said. “If I’m a risky borrower, I face this very difficult trade-off: I want to insure myself like everyone else. But it also means that I’m locking in relatively high rates, with a big credit spread.” That of course does not always make sense for borrowers, she pointed out. “This may help explain why very long-term mortgage contracts with high-LTV mortgage lending are rare across countries.”

Liu said her data, which covered the period from 2013 to 2017, showed that the propensity is lower among riskier borrowers to opt for a 5-year fixed-rate mortgage compared to a 2-year fixed-rate mortgage. The higher the loan-to-value ratio, the lesser was their incentive to choose longer mortgage tenures, her research found. “Borrowers at 95% LTV are less than half as likely to take out a 5-year fixed-rate contract, compared to borrowers at 70% LTV,” the paper stated. The findings help explain the “reduced and heterogeneous demand for long-term mortgage contracts.”

How to Make U.S. Mortgages More Efficient

Liu said the findings in her paper are relevant for mortgage market design. “High-LTV borrowers face a difficult trade-off between their demand to lock in overall interest rate levels, and an expected decline in credit spreads over time,” she said. “Households could benefit substantially from being able to lock in base interest rates, while repricing their credit spreads.”

The findings are important also from both a monetary policy and financial stability perspective, Liu continued. “High-LTV borrowers are more exposed to interest rate risk, which can also cause vulnerabilities in a rising rate environment, since these borrowers may be most affected by mortgage cost increases.”

“There is political resistance to institutional change and borrower resistance to novel mortgage products.” – Lu Liu

The findings of Liu’s research are also timely, given the recent spike in the inflation rate. She noted that the U.S. Federal Reserve has increased interest rates more aggressively than its counterparts in the U.K., Canada, and Australia. All those countries have varying degrees of short-term fixed or variable-rate mortgages. Unlike in those countries, U.S. mortgage borrowers are “relatively shielded from interest rate rises, as the vast majority of households have locked in previous low rates for 30 years,” she noted.

Unintended Consequences of Long-term Mortgage Contracts

But the design of mortgage contracts in the U.S. creates disruptions beyond the housing markets to the broader financial system. “The 30-year fixed-rate mortgages in the U.S. have led to duration mismatch and financial stability risks in the banking sector, as rate rises have reduced the market values of these loans and mortgage-backed securities,” Liu said. She cited the recent collapse of Silicon Valley Bank as a case in point, which was triggered by the fall in the valuation of its bond holdings in a rising interest rate environment. In the U.K., in contrast, banks typically hedge the 2-to 5-year fixed-rate legs of mortgages using swaps, with the remaining part of the contract having a variable rate and thus not causing duration mismatch for the banks.

Long-term contracts have other consequences, too. “The [30-year mortgages] have had knock-on effects on mobility and housing markets due to mortgage lock-in,” Liu continued. Mortgage lock-in occurs in a rising interest rate environment, where homeowners find it a losing proposition to refinance mortgages they had taken out when interest rates were at historical lows. As a result, “people aren’t moving, and the housing market is frozen,” she said.

Liu said policy makers ought to rethink the 30-year fixed-rate mortgage, noting that Harvard economics professor John Y. Campbell had proposed that in a presentation at the Georgia Tech-Atlanta Fed Household Finance Conference in March 2023.

That said, the nature of mortgage systems in different countries is “highly persistent over time,” so any recommendation to radically change them might be far-fetched, Liu noted. “There is political resistance to institutional change and borrower resistance to novel mortgage products,” she added. If the U.S. were to move in the direction of more of a Canadian system that has mortgage rates fixed for five years, she noted, “any implementation of shorter-term fixed-rate contracts would need to take into account the credit risk dimension, which could result in risky households insuring less against interest rate risk.” Such a move has the potential to make monetary policy more effective and the banking system more stable, but further research is needed, she added.

Many experts predict mortgage rates will come down somewhat in 2024, though not all agree on what that will exactly look like.

Getty Images/iStockphoto

In 2020, interest rates plummeted as the Federal Reserve tried to prevent the economy from crashing due to the pandemic. These low rates helped fuel a real estate frenzy, with many homebuyers locking in 30-year fixed-rate mortgages at sub-3% rates. Now, however, as the Fed has tried getting a handle on inflation, interest rates have soared, including for mortgages.

As of October 11, 2023, the average 30-year fixed-rate mortgage in the US is 7.83%. Many prospective homebuyers are hoping for some relief, but it’s unclear when exactly that will happen. Current homeowners also face high rates. The average 30-year-fixed mortgage refinance rate is 8.02% as of October 11, 2023, according to Bankrate.

Still, many experts think mortgage interest rates will start to trend downward in 2024, although perhaps not at a very fast rate. Below, we’ll break down everything experts think will happen to mortgage rates next year. Start by exploring your mortgage rate options here today to see what you could qualify for.

Mortgage interest rate forecast for 2024

Here’s where experts think mortgage rates will start in 2024, how they think they’ll change and other economic factors to monitor.

Where do experts think mortgage rates will start in 2024?

With the new year just a few months away, and the Fed signaling that rates aren’t likely to come down in the near future, many experts predict that mortgage rates will start the year roughly where they left off.

A hot job market and inflation not coming down as quickly as expected is making it difficult for the Federal Reserve to bring down rates, explains Jeremy Schachter, mortgage loan officer at Fairway Independent Mortgage Corporation.

And while the Fed doesn’t set mortgage rates, there’s a correlation.

“Mortgages and inflation go hand in hand,” says Schachter. “I personally think mortgage rates will begin roughly where we ended in the low 7s.”

Similarly, Robert Frick, corporate economist at Navy Federal Credit Union, predicts 30-year fixed-rate mortgages will start the year in the 7.25%-7.50% range.

Some, however, think rates will continue to climb.

“It has become increasingly evident that rates will be ‘higher for longer’ as economic resiliency persists, and the Fed remains committed to bringing inflation in line with its long-term target of 2%,” says Kelly Miskunas, senior director of capital markets at Better. “Until the market can comfortably assume the hiking cycle is over, we may see mortgage rates continue to drift higher through the early part of 2024.”

If rates do rise higher in the months to come, it may make sense for some buyers to lock in a rate now. See what rates you could qualify for here.

How will mortgage rates change throughout 2024?

While rates might be roughly in line with current levels at the start of next year, give or take a little, some experts predict a stronger drop throughout 2024.

“I personally see mortgage rates coming down into the mid-6s by the second quarter and ending up in the lower 6s or high 5s by the end of the year,” says Schachter.

Frick takes a similar view.

“The economy and inflation should weaken next year, causing the Fed to lower rates,” he says. “This will influence rates overall and should result in mortgage rates at, or just below, 6%.” By the end of 2024, he predicts a range of 5.50%-6.00%.

However, some experts think it will take longer for rates to come down.

“The Fed seems like it will remain unwavering in its fight against inflation,” says Miskunas. “Right now, this is reflected in the futures market with the expectation that the Fed funds rate will not deviate much from where it is right now until mid/late 2024.”

So, until the Fed starts to reverse course on interest rates, mortgage rates might not move much.

“We anticipate that once the Fed has achieved its goals and begins to loosen monetary policy, mortgage rates will decline. This could occur in the latter half of 2024,” says Miskunas.

Economic factors to keep an eye on

Predictions can change as data and circumstances change. So, consider watching out for economic shifts to get an updated idea of where mortgage rates might be heading.

In addition to what the Fed is doing, for example, Frick points to economic indicators such as the spread between the 10-year Treasury and 30-year fixed-rate mortgages.

These two interest rates generally move in the same direction, but how close they are to one another can vary. If the spread starts to close, then that could mean mortgage rates will more closely follow the Fed’s changes.

“The lack of certainty and heightened volatility of 2023 has caused mortgage spreads to widen to historically high levels, but once market participants believe that the Fed’s hiking cycles are over, mortgage rates will improve significantly,” says Miskunas.

Relatedly, data such as monthly jobs reports and the Consumer Price Index (CPI) could also inform where mortgages are heading in 2024. For rates to come down, “we would need to see stronger unemployment numbers and key inflation indicators lower than what was previously shown,” says Schachter. When exactly that will happen is hard to say, but in general, experts predict that mortgage rates will trend downward at some point in 2024 as the economy cools.

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

The mere thought of filing for bankruptcy is enough to make anyone nervous. But in some cases, it really can be the best option for your financial situation. Even though it stays as a negative item on your credit report for up to ten years, bankruptcy often relieves the burden of overwhelming amounts of debt.

There are actually three different types of bankruptcy, and each one is designed to help people with specific needs. Read on to find out which type of bankruptcy you might be eligible for. We’ll also help you determine whether it really is the best option available.

What are the different types of bankruptcy?

In general, bankruptcy is the process of eliminating some or all of your debt, or in some cases, repaying it under different terms from your original agreements with your creditors.

It’s a very serious endeavor but can help alleviate your debt if you calculate that it’s unlikely to you’ll be able to repay everything throughout the coming years.

The two most common for individuals are Chapter 7 and Chapter 13. Chapter 11 is primarily used for businesses but can apply to individuals in some instances. Let’s take a look at some bankruptcy basics and the other details that set them apart from each other.

Chapter 7 Bankruptcy

Chapter 7 bankruptcy is designed for individuals meeting certain income guidelines who can’t afford to repay their creditors. You must pass a means test to qualify. Then, instead of making payments, a bankruptcy trustee can sell your personal property to help settle your debts, including both secured and unsecured loans.

There are certain exemptions you can apply for to keep some things from being taken away. It all depends on which debts are delinquent. If your mortgage is headed towards foreclosure, you might only be able to delay the process through a Chapter 7 delinquency.

If you’re only delinquent on unsecured debt, like credit card debt or personal loans, then you can file for an exemption on major items like your home and car. That way they won’t be repossessed and auctioned off.

Eligible exemptions vary by state. Usually, there is a value assigned to your assets that are eligible for exemption. You may keep them as long as they are within that maximum value. For example, if your state has a $3,000 auto exemption and your car is only valued at $2,000 then you get to keep it.

Most places also allow you to subtract any outstanding loan amount to put towards the exemption. So, in the situation above, if your car is valued at $6,000, but you have $3,000 left on your car loan, then you’re still within the exemption limit.

Chapter 7 bankruptcy is the fastest option to go through, lasting just between three and six months. It’s also usually the cheapest option in terms of legal fees. However, keep in mind that you’ll likely have to pay your attorney’s fees upfront if you choose this option.

Chapter 13 Bankruptcy

A chapter 13 bankruptcy is the standard option when you make too much money to qualify for a Chapter 7 bankruptcy. The benefit is that you get to keep your property but instead repay your creditors over a three- to five-year period. Your repayment plan depends on several variables.

All administrative fees, priority debts (like back taxes, alimony, and child support), and secured debts must be paid back in full over the repayment period. These must be paid back if you want to keep the property, such as your house or car.

The amount you’ll have to repay on your unsecured debts can vary drastically. It depends on the amount of disposable income you have, the value of any nonexempt property, and the length of your repayment plan.

How long your plan lasts is actually determined by the amount of money you earn and is based on income standards for your state. For example, if you make more than the median monthly income, you must repay your debts for a full five years.

If you make less than that amount, you may be able to reduce your repayment period to as little as three years. You can enter your financial information into a Chapter 13 bankruptcy calculator for an estimate of what your monthly payments might look like in this situation.

To qualify for Chapter 13, your debts must be under predetermined maximums. For unsecured debt, your total may not surpass $1,149,525 and your secured debt may not surpass $383,175. However, unlike Chapter 7 bankruptcy, you may include overdue mortgage payments to avoid foreclosure.

Chapter 11 Bankruptcy

Chapter 11 bankruptcy is usually associated with companies. However, it can also be an option for individuals, especially if their debt levels exceed the Chapter 13 limits. A lot of the characteristics of Chapter 11 and Chapter 13 are the same, such as saving secured property from being repossessed.

Having to pay back priority debts in full and having a higher income bracket than a Chapter 7 bankruptcy are also common characteristics. However, unlike Chapter 13, you must make repayment for the entire five years with a Chapter 11. There is no option to pay for just three years, no matter where you live or how much you make.

Another reason to pick Chapter 11 is if you are a small business owner or own real estate properties. Rather than losing your business or your income properties, you get to restructure your debt and catch up on payments while still operating your business, whether it’s as a CEO or as a landlord.

One downside to be aware of with a Chapter 11 bankruptcy is that it’s usually the most expensive option. However, you can pay your legal fees over time so you don’t have to worry about spiraling back into debt.

What are the long term effects of bankruptcy?

It should come as no surprise that going through bankruptcy causes your credit score to plummet. Depending on what else is on your report, your score could drop anywhere between 160 and 220 points.

Those effects linger. A Chapter 13 bankruptcy stays on your credit report for seven years. And a Chapter 7 bankruptcy remains there for as many as ten years. Their effects on your credit score do, however, begin to diminish as time goes by.

You’ll probably have trouble getting access to credit immediately following your bankruptcy. Eventually, you’ll start getting approved for loans and credit cards, but your interest rates are likely to be extremely high.

A new mortgage will probably be out of reach for at least five to seven years from the time you file for bankruptcy. Additionally, any employer performing a credit check can see all of these items on your credit report.

Government agencies can’t legally discriminate against you because of your bankruptcy, but there is no specific rule for privately-owned companies. It could be particularly damaging if the job you’re applying for deals with money or any type of financials. No matter where you work, though, you can’t be fired from a current employer because of a bankruptcy.

Should I file bankruptcy?

There’s no correct answer to this question. It’s ultimately something you’ll need to decide on your own. However, there are a few things you can do to make sure you’re making the best decision possible. Start by finding a licensed credit counselor to help analyze your individual situation. They’ll help you review the guidelines for each type of bankruptcy and determine if you’re even eligible.

At first glance, filing for bankruptcy may seem like a great way to settle your debts and move on with your life. Unfortunately, the process isn’t as simple as filling out a form. The effects of bankruptcy will stick with you for years.

As you begin the evaluation process of whether bankruptcy is right for you, there are several considerations to consider. This overview will get you thinking about your situation. It will also point you in the right direction for more in-depth resources when you need them.

Is your current status temporary or permanent?

You should also look at your expected future and compare your potential earnings to your amounts of debt. If you don’t see how you’ll ever pay off that debt, then bankruptcy may be a wise option. Also, understand the types of debt you owe. Tax payments, student loan debt, and liens on your mortgage or car will not be discharged even when you file for bankruptcy.

Once you figure out which specific options are available to you, it’s time to contact a bankruptcy attorney. You’re certainly able to represent yourself, but the process is complicated. It’s usually best to have a professional work on the case on your behalf. Just be sure to interview a few different lawyers to get multiple opinions and prices to compare.

Evaluate Your Situation

Even when your bankruptcy is underway, it’s smart to spend some time evaluating how you got there. Was it due to a one-time financial hardship, like a long bout of unemployment? If that’s the case, then you know that you have a brighter future ahead of you with the promise of work and steady income to pay your bills.

However, if you’re on the path to bankruptcy because of reckless spending, you really need to look inward and address your overspending habits. Otherwise, it becomes too easy to put yourself in the same situation a few years down the road. Use your bankruptcy as a second chance to start fresh with a clean financial slate.

Why Consider Bankruptcy?

If you’re considering bankruptcy, then you’re most likely feeling overburdened with debt and other financial obligations. You probably have a tough time paying your bills each month and may even worry about how you’ll ever pay off some of your outstanding balances.

If you’ve already exhausted your other options, like working overtime and cutting back on your non-necessities, it might be time to seriously think about potentially declaring bankruptcy. Some signs that you might be ready include:

Increased interest rates because of late payments or bad credit

Using credit cards for daily purchases without paying off the balance each month

Already downsized things like house, car, and other assets

Working multiple shifts or jobs

Paying off debt with retirement funds

Wages are being garnished

If one or more of these situations apply to you, then you should probably continue your research into bankruptcy. If not, try finding other ways to improve your financial situation. For example, you could rework your budget if there are easy places to cut back on.

You can also try negotiating with your lenders, particularly if you’re experiencing just a short-term setback. Most lenders are willing to work with you. They would much rather set up a new payment plan than have the debt discharged or settled through bankruptcy.

Bankruptcy Alternatives

If you want to file for bankruptcy it takes careful planning. Due to the long-term legal and financial consequences of bankruptcy, there are many rules that must be followed before you’re eligible.

For example, it’s necessary to show the bankruptcy court that you have obtained credit counseling and considered debt relief options like debt settlement or debt consolidation. Bankruptcy is controlled exclusively by the federal judicial system, which strongly recommends hiring an attorney before attempting to file.

If you need help finding a bankruptcy lawyer, contact the American Bar Association. They offer free legal advice, and you may qualify for free legal services if you are unable to afford an attorney.

Creating a Checklist to Avoid Dismissal

Before you file for bankruptcy, there are several important questions you should ask yourself. There are also several key steps that you need to take. First, it’s necessary to ask yourself if you really need to file for bankruptcy.

If you don’t, you probably won’t be approved anyway. You also need to calculate income, expenses, and assets, find a trustworthy attorney, and select a credit counseling program.

It’s helpful to be methodical and to use a checklist. Failure to take the right steps and find the right credit counseling could result in more wasted money and a bankruptcy dismissal where they throw out the case.

Reasons to Delay Bankruptcy

Even if bankruptcy is the best choice for you, there may be some situations where it’s smart to delay the process so you can maximize your benefits. First, if you had a high income within the last six months that no longer applies to your situation, then you might want to wait.

That’s because the bankruptcy court weighs your last six months of income to determine your eligibility for Chapter 7 bankruptcy. If you had a nice monthly salary a few months ago but have been laid off since then, that means test isn’t going to reflect your current situation accurately.

Another reason to delay bankruptcy is if you are anticipating an upcoming major debt. New debt isn’t allowed to be discharged once you file for bankruptcy.

So, for example, if you’re about to have a major medical surgery, you might consider waiting until it’s over to include the medical bills as part of your bankruptcy plan. Talk to a professional to see the eligibility requirements. Luxury items charged right before a bankruptcy filing, for example, likely won’t be included as part of your debt discharge.

Changes in Bankruptcy Law

Before getting started, it’s important to note the changes that went into effect in 2005 under the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA). While the changes don’t affect some people applying for bankruptcy, they may affect others.

Federal bankruptcy laws require mandatory credit counseling to make sure you fully understand the consequences of declaring bankruptcy. It also created stricter eligibility requirements for Chapter 7 bankruptcies. For Chapter 13 bankruptcy filings, the law requires tax returns and proof of income.

An informed decision begins with understanding bankruptcy laws, the bankruptcy process, and what has changed. It’s essential to better understand these changes before you make any final decisions.

Filing Under Chapter 7 or Chapter 13

Understanding how bankruptcy works means understanding the process and laws related to Chapters 7 and 13 of the Bankruptcy Code. Depending on the details of your situation, you might be eligible to file under Chapter 7 or Chapter 13. Which route you choose has a lot to do with your income and what assets you want to keep.

Your debts can either be resolved quickly or over a several-year period. It’s helpful to read up on in-depth frequently asked questions related to each route.

Calculating Chapter 7 Means

To have all your unsecured debts eliminated under Chapter 7 bankruptcy, you must qualify under the Chapter 7 means test. Using your personal information, or a basic estimate, an online calculator can help determine this for you. When filing bankruptcy, you must also fill out an appropriate form in which you enter your income, expense information, and data from the Census Bureau and IRS.

If you don’t meet the income level requirements to file for Chapter 7 bankruptcy, you can still file for Chapter 13. A Chapter 13 will settle many of your debts after you successfully complete a three to five-year repayment program.

Qualifying and Qualifying Debts

Your debts qualify for bankruptcy relief when you can prove you are unable to pay them, but a great deal depends on your situation and which chapter you are filing bankruptcy under. Debts can be either unsecured or secured. Secured debts include mortgages, cars, and debts related to a property you’re still paying for.

Unsecured debts include credit card debt, bills, collections, judgments, and unsecured loans. It’s important to know which debts qualify for bankruptcy. But, it’s even more important to know whether your situation makes you eligible for this major step. To determine this, a full financial assessment is necessary. You can start by reading more about debts that qualify.

Defaulting on a Student Loan

If you have defaulted on a student loan, there are several options open to you. Bankruptcy is one of them, but if your goal is to have a student loan discharged under Chapter 7, this can be very difficult.

Nevertheless, taking certain steps as soon as possible can help prevent wage garnishment. Knowing your options can help you make the best choice before matters become more difficult. Under Chapter 13, your defaulted loan can be consolidated with your other bills. This will give you a better payment plan or a temporary reprieve from making payments.

If you have a federal student loan, check out your repayment options, especially if you are facing financial hardship. Otherwise, read more to figure out how to pull yourself out of student loan default.

What Assets You Can Keep During Bankruptcy

Depending on how you file for bankruptcy, there are certain assets you can keep. Different states have different exemptions, and in certain states, you can choose between state and federal bankruptcy exemptions.

If you need to have debts discharged, are out of work, and cannot afford a repayment plan, some assets might be lost. In most cases, however, people who declare bankruptcy can keep their homes and cars and much of what they own while they repay their debts under a modified plan. It all depends on your unique circumstances and how you file.

Get a FREE Credit Evaluation Before You File Bankruptcy

A bankruptcy can affect your credit for 7 to 10 years and should be considered a last resort option when all other options have failed. Many times, people file bankruptcy when it is completely unnecessary. A credit professional can help you fix your credit and deal with your creditors so you can avoid filing for bankruptcy.

Before filing bankruptcy, talk to a credit specialist:

Visit the website and fill out the form for a free credit consultation with a professional credit repair company.

As the sun-soaked capital of Arizona, Phoenix isn’t just a bustling metropolis in its own right. It’s also surrounded by a ton of stellar suburbs, each offering its own unique flavor and charm.

From luxury enclaves to tech hubs to serene family-friendly neighborhoods, the Phoenix suburbs described below provide great options for every lifestyle. This article dives into the crème de la crème of the Phoenix suburb scene, providing insights into what makes each spot stand out in the heart of the Southwest.

Population: 242,753

Average age: 47.7

Median household income: $97,409

Average commute time: 22.9 minutes

Walk score: 32

One-bedroom average rent: $2,024

Two-bedroom average rent: $2,984

In the picturesque landscape of Phoenix suburbs, Scottsdale stands out as an oasis of luxury, art and outdoor activities. With world-class golf courses that would make any link lover’s heart race, upscale shopping districts that can satiate even the most discerning shopper and restaurants that range from gourmet to eclectic, Scottsdale is the epitome of suburban elegance.

Three great apartment complexes in Scottsdale

But it’s not all about the glitz and glam. This Phoenix suburb supports an array of outdoor activities, from the scenic trails of McDowell Sonoran Preserve to horseback riding under the vast Arizona sky. Dive into Scottsdale and discover what makes this Phoenix suburb a crown jewel of the Southwest.

Population: 279,458

Average age: 36.7

Median household income: $91,299

Average commute time: 24.9 minutes

Walk score: 35

One-bedroom average rent: $1,785

Two-bedroom average rent: $2,000

Among the constellation of Phoenix suburbs, Chandler shines brightly with its unique blend of tech-driven progress and laid-back Southwestern charm. As the hub of the Silicon Desert, Chandler boasts a growing technology industry, attracting innovators and professionals eager to make their mark.

Three great apartment complexes in Chandler

What sets Chandler apart in the lineup of Phoenix suburbs is its commitment to balancing urban sophistication with hometown warmth. From high-end shopping centers to local farmers markets and from cutting-edge theaters to the annual Ostrich Festival, this Phoenix suburb ensures residents never have a dull moment.

Population: 273,136

Average age: 34.5

Median household income: $105,733

Average commute time: 27.1 minutes

Walk score: 29

One-bedroom average rent: $1,747

Two-bedroom average rent: $1,991

Once known as the “Hay Shipping Capital of the World,” Gilbert has grown exponentially, trading hay bales for innovative businesses and growing communities. Gilbert is a shining example of how a city can expand without losing its historic charm.

Three great apartment complexes in Gilbert

Dive deeper into what Gilbert offers among Phoenix suburbs, and the picture only gets rosier. It’s a haven for families, thanks to its top-rated schools and pristine parks. And for those craving some sun-soaked adventure, there are outdoor concerts, farmers markets and green spaces where residents can relax. In the vast sea of Phoenix suburbs, Gilbert floats to the top and provides an unbeatable mix of the past, present and future.

Population: 509,475

Average age: 36.2

Median household income: $65,725

Average commute time: 25.4 minutes

Walk score: 38

One-bedroom average rent: $1,360

Two-bedroom average rent: $1,637

As the third-largest city in Arizona, Mesa doesn’t merely ride the coattails of its size. It’s an epicenter for aerospace ventures, higher education institutions and tech enterprises, making it a hotspot for those with an eye on the future. Yet, with the backdrop of the majestic Superstition Mountains and access to the shimmering Salt River, Mesa ensures that residents are never too far from Arizona’s captivating wilderness.

Three great apartment complexes in Mesa

But wait, there’s more that sets Mesa apart from other Phoenix suburbs. The city prioritizes fun and adventure, evident in its sprawling golf courses, thrilling water parks and extensive trail systems. Add to that a healthy selection of restaurants, cozy cafes and ritzy retreats, ensuring that every culinary whim is always catered to.

Population: 12,682

Average age: 54.9

Median household income: $203,659

Average commute time: 24.5 minutes

Walk score: 14

One-bedroom average rent: $2,050

Two-bedroom average rent: $2,100

The name itself evokes images of a dreamy haven, and Paradise Valley doesn’t disappoint. Famed for its upscale estates and celebrity residents, Paradise Valley offers a level of opulence seldom seen elsewhere. Breathtaking mountain views, especially from the vantage point of Mummy Mountain or Camelback Mountain, serve as daily reminders of the stunning natural beauty Arizona has to offer.

Three great apartment complexes near Paradise Valley

But Paradise Valley is not just about grandeur in the Phoenix suburbs landscape. It strikes a harmonious balance between luxury and leisure. Championship courses call to all golfers, while swanky resorts offer an oasis of relaxation and rejuvenation. Dining here is an experience unto itself, with a ton of gourmet restaurants tantalizing the taste buds.

Population: 249,630

Average age: 33.8

Median household income: $60,499

Average commute time: 28.0 minutes

Walk score: 40

One-bedroom average rent: $1,299

Two-bedroom average rent: $1,650

Recognized as Arizona’s Antique Capital, Glendale offers a delightful stroll down memory lane with its historic downtown, where boutiques and eateries provide a nostalgic setting for casual shopping and good conversation. Yet, this Phoenix suburb isn’t just about looking back; it’s also home to the State Farm Stadium, where adrenaline-pumping Cardinals games and massive concerts ignite the spirits of thousands.

Three great apartment complexes in Glendale

Switching gears, Glendale wears another feather in its cap in the Phoenix suburbs scene as a premier destination for events and festivals. From chocolate fests that satiate the sweet tooth to hot air balloon shows painting the sky, there’s always something happening in this dynamic corner of the desert.

Population: 194,917

Average age: 40.3

Median household income: $81,017

Average commute time: 29.4 minutes

Walk score: 30

One-bedroom average rent: $1,555

Two-bedroom average rent: $1,776

Peoria is an adventurer’s paradise with the sprawling Lake Pleasant Regional Park in its backyard, offering the perfect setting for water-based activities all set against the backdrop of the sun-kissed Arizona landscape. On land, Peoria’s P83 District is where the action’s at, boasting a ton of dining options, bars and events that keep the energy up year-round.

Three great apartment complexes in Peoria

But Peoria doesn’t stop at fun and games in the world of Phoenix suburbs. It’s also a beacon for those seeking a serene suburban life, characterized by beautifully master-planned communities and top-tier educational institutions. Couple this with a forward-thinking local government and an engaged community, and it’s clear why Peoria consistently ranks high on the desirability scale.

Population: 149,191

Average age: 41.9

Median household income: $76,623

Average commute time: 30.7 minutes

Walk score: 21

One-bedroom average rent: $1,525

Two-bedroom average rent: $1,825

Expectations run high with a name like Surprise, and this Phoenix suburb delivers in spades. From the city’s Spring Training baseball games to its well-maintained parks, there’s an avenue for everyone to feel the rush or simply unwind.

Three great apartment complexes in Surprise

But there’s another layer to Surprise that distinguishes it in the Phoenix suburbs roster. It’s a growing hub for education and healthcare, boasting some of the region’s top schools and hospitals. Add to that a commitment to sustainable growth, a friendly community spirit and a diverse range of housing options, and the allure of Surprise becomes undeniable.

Population: 24,987

Average age: 59.7

Median household income: $87,080

Average commute time: 28.7 minutes

Walk score: 19

One-bedroom average rent: $3,000

Two-bedroom average rent: $2,100

Fountain Hills is a visual masterpiece, where the Sonoran Desert’s natural beauty gets a touch of architectural elegance, providing residents with panoramic views that will steal your breath away. From the rolling desert hills to the shimmering blue of Fountain Lake, it’s a treat for the senses at every turn.

Three great apartment complexes near Fountain Hills

But Fountain Hills isn’t just about aesthetic appeal. It’s also a community that prides itself on community events. The town hosts renowned art fairs, craft shows and local markets that draw both residents and visitors alike. With spacious parks, scenic hiking trails and a commitment to community engagement, Fountain Hills provides an idyllic blend of leisure and lifestyle.

Population: 90,564

Average age: 31.6

Median household income: $69,241

Average commute time: 28.4 minutes

Walk score: 26

One-bedroom average rent: $1,421

Two-bedroom average rent: $1,678

Avondale is home to the Phoenix Raceway, where the roar of engines and the thrill of nail-biting races draw legions of NASCAR fans every year. But Avondale isn’t just for the adrenaline junkies; it’s home to many parks, trails and open spaces that serve as perfect spots for family picnics, weekend strolls or quiet afternoons with a good book in hand.

Three great apartment complexes in Avondale

Yet, there’s another side to Avondale that solidifies its spot on the Phoenix suburbs’ leaderboard. Its flourishing local economy presents plenty of employment opportunities, making it an attractive place for professionals and entrepreneurs. Add in a dash of delightful restaurants, shopping areas and a community that’s warm and welcoming, and it’s evident why Avondale has become one of the go-to Phoenix suburbs for those seeking a balanced life.

Find the best Phoenix suburb for you

Navigating the Phoenix suburbs can be a journey of discovery, as each presents its distinct character and amenities. Whether it’s the allure of lakeside views, the thrill of a raceway or the serene embrace of the desert landscape, there’s a Phoenix suburb tailored for every dream and desire.

As the city continues to grow and evolve, its surrounding suburbs are sure to remain as diverse and dynamic as ever, offering residents a slice of paradise in the desert. Today’s the day to make your move to the perfect apartment for rent in one of Phoenix’s top suburbs.

We know what you’re thinking: Is it too soon to start thinking about winter holiday decor? The short answer: Absolutely not, especially since it’s the last day of Amazon’s massive Prime Big Deal Days sale event. That means this is your last chance to save big on home decor.

Luckily, we took the time to look through every single deal and bring you a careful edit of the top holiday home decor essentials markdowns you can’t miss. Get ready to save on mantel statement pieces, outdoor decor, and beyond. Check out our top 13 picks below.

Our Top Amazon Prime Day Deal Picks on Holiday Decor

Sanjicha Lighted Birch Tree Two-Pack

Amazon

These battery-powered, little birch trees will give your living space a warm glow and help foster a festive atmosphere instantly. Keep them together on either side of your mantel, or use one as a centerpiece and the other for your entryway.

Ivenf Christmas Outdoor Porch Sign Set

Amazon

If you’re looking for traditional outdoor decorations beyond string lights, consider this two-piece porch sign set. The larger lettering on the traditional tartan print will add a playful touch to your patio or front porch.

National Tree Company Pre-Lit Artificial Christmas Garland

Amazon

This pre-styled artificial garland will do the heavy lifting for you regarding greenery and lighting. The 9-foot garland is clustered with pine cones and berries and pre-strung with lights, so all you have to do is find a place for it and plug it in.

Kwaiffeo Meteor Shower Lights

Amazon

Give your outdoor space a charmingly whimsical flair with the Kwaifeo Meteor Shower Lights. The cascade of white LEDs gives a breathtaking visual of bright icicles or falling lights for a low-maintenance outdoor decoration that brings the holiday spirit to life.

Aetegit Christmas Pillow Covers

Amazon

An easy way to awaken the Christmas spirit inside your home is by refreshing interiors. Swiftly update your space with this four-piece set of throw pillow covers that showcase different cheery messages and phrases.

Neilden Three-Piece Gnome Decor

Amazon

Bring the adorable gnomes out to play when you need to give your space an extra joyful vibe. Each of these gnomes is about 20 inches tall and are easy to move around, so you can have them by the presents under the tree one day and by the window sill the next.

Oriental Cherry Floating Candles

Amazon

You may recall the floating candles from the magical world of Harry Potter, but now they’re fit to bring into your living or dining room for a truly magical experience. A wand controller powers them too, making it more convenient to turn them on and off.

Puhong Outdoor Star String Lights

Amazon

Hang this tree-shaped light display right outside your home to add some Christmas cheer outdoors. The string lights can work as a perfect backdrop for the rest of your outdoor holiday decor or stand alone as an eye-catching focal piece.

Runleo Snowflake String Lights

Amazon

Is it really Christmas time without snowflakes—even artificial ones? Invite the winter delight of the outdoors inside with this enchanting set of string lights. Use them to line a doorway or to wrap around your Christmas tree.

Funpeny Lighted Gift Boxes

Amazon

Stick these gorgeous lighted gift boxes under your tree for an elevated ambiance. They’ll make a beautiful statement, especially after you fill your tree with gift-wrapped presents. This set comes with three different sizes to ensure you can create a diverse display of gifts.

OuMuaMua Hanging Snowflakes

Amazon

Finish off your winter wonderland with these hanging paper snowflakes. At $9 per 12-piece set, we wouldn’t blame you for wanting to buy a bundle to bring the magic of a snowy Christmas day inside your home, no matter the weather outside.

ProductWorks 24-Inch Charlie Brown Christmas Tree

Amazon

For a very nostalgic evening of celebration, center your decor on the iconic Charlie Brown Christmas Tree. The nostalgic display includes the classic red ornament with Linus’ blue blanket wrapped around the base.

Snowkingdom Gold Table Runner Set

Amazon

Amp up your tablescape this year with the set of gold-flecked table runners. Made of a soft fiber mesh decked out in gold foil, the 9-foot runners can be used alone or layered over another decorative tablecloth for a more dramatic effect.

Home builder confidence took a hit in September as average mortgage rates for a 30-year fixed-rate loan stayed above 7%.

Builder confidence in the market for newly built single-family homes in September fell five points to 45, according to the National Association of Home Builders / Wells Fargo Housing Market Index released Monday. This follows a six-point drop in August.

The monthly index looks at current sales, buyer traffic and the outlook for sales of new-construction homes over the next six months. September’s reading is the first time in five months that overall builder sentiment levels dropped below the break-even measure of 50.

“The two-month decline in builder sentiment coincides with when mortgage rates jumped above 7% and significantly eroded buyer purchasing power,” said Alicia Huey of the NAHB.

Home builder sentiment had been rising earlier this year, riding the wave of demand caused by lack of inventory in the existing home market. But confidence dropped for the first time this year in August, as rates climbed.

In addition, builders continue to grapple with a shortage of construction workers and buildable lots, which is further adding to housing affordability challenges, said Huey.

All three dimensions of the new housing market evaluated saw declines in September: The index gauging current sales conditions fell six points to 51. The component charting sales expectations in the next six months also declined six points to 49. And the gauge measuring traffic of prospective buyers dropped five points to 30.

“High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower,” said Robert Dietz, NAHB Chief Economist. “Putting into place policies that will allow builders to increase the housing supply is the best remedy to ease the nation’s housing affordability crisis and curb shelter inflation. Shelter inflation posted a 7.3% year-over-year gain in August, compared to an overall 3.7% consumer inflation reading.”

New homes have become an attractive alternative for buyers frustrated by extraordinarily low inventory of existing homes as homeowners hunker down with their ultra-low mortgage rates of 2%, 3%, 4% rather than selling and becoming a buyer at a 7% rate.

As mortgage rates stayed above 7% over the last month, more builders cut prices to boost sales, according to NAHB.

In September, 32% of builders reported dropping home prices, compared to 25% in August. That’s the largest share of builders cutting prices since last December. The average price discount is 6%.

Meanwhile, 59% of builders provided sales incentives of all forms in September, more than any month since April.

This available inventory and price flexibility has gotten the attention of first-time homebuyers.

According to the NAHB, 42% of new single family home buyers were first time buyers so far this year. That’s significantly higher than the 27% of first time buyers purchasing new construction homes during the same time period in 2018, when the market was more typical.

If you’ve been keeping track lately, you might be wondering why mortgage rates plunged this week.

Last week was a totally different story, with a hotter-than-expected jobs report almost enough to push the 30-year fixed across the daunting 8% threshold.

But then the unexpected happened over the weekend, as is often the case with geopolitical events.

In times of uncertainty, bonds are typically a safe haven, and when demand for them rises, their associated yields (or interest rates) fall.

This, coupled with some more dovish talk from Fed speakers, might explain the recent pullback in rates.

How Much Have Mortgage Rates Plunged?

First off, the word “plunge” might be a strong one given how much mortgage rates have climbed over the past 18 months.

While mortgage rates have indeed fallen all week, they remain well above recent lows. And even much higher than levels seen this summer.

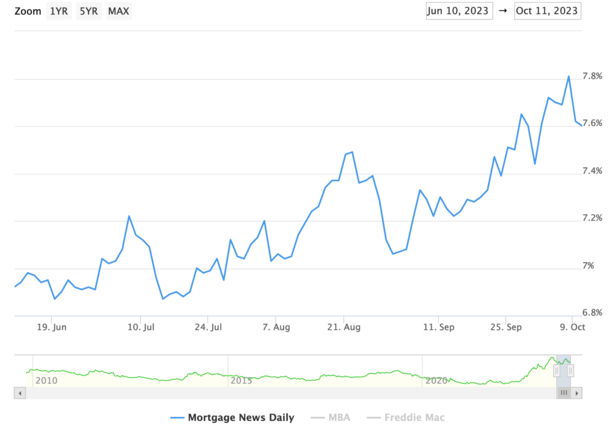

If we want to use MND’s widely cited daily rate survey as the measure, the 30-year fixed now stands at 7.60%.

That’s down from 7.81% on Friday October 6th. So basically mortgage rates have improved by about 20 basis points, or perhaps .25% depending on the lender.

It also reduced the year-over-year change in rates from 0.77% to 0.46%, providing a glimmer of hope that the worst could be behind us.

And better yet, perhaps mortgage rates have peaked. While that remains to be seen, it’s been hard to get any meaningful relief lately.

Typically, any pullback or improvement in rates has been met with further increases. And the wins are generally short-lived.

Will that be the case again this time or is there finally light at the end of the tunnel?

Mortgage Rates Helped by New Geopolitical Risks

As for why mortgage rates improved this week, one would be quick to point to the events that took place in Israel (and continue to unfold).

Generally, mortgage rates tend to go down if there is the threat of war or similar tension in the air.

The reason is uncertainty, which is a friend to bonds because of their relative certainty.

In short, investors will flee riskier markets like equities and pile into bonds, which is known as the flight to safety.

If more investors are buying bonds, the price goes up and the yield drops. Since Friday, the 10-year bond yield has fallen from 4.84 to about 4.61 today.

Of course, this could prove to be a short-term reaction to what has been a clear move higher for bond yields lately.

So it’s entirely possible that the 10-year yield marches on back to those recent levels (and beyond) depending on what transpires.

And the conflict in the Middle East could actually exacerbate inflation if oil prices (and gas prices) rise.

No More Fed Rate Hikes Could Take Pressure Off Mortgage Rates