Nestled in the heart of Utah Valley, Provo has increasingly been a topic of discussion for those looking to relocate.

Known for its close proximity to natural wonders like Provo Canyon and Utah Lake, it’s a location that offers both city life and natural retreat. However, with such growing attention, the question arises: Is Provo, Utah, a good place to live?

Geographic overview

Provo, located in Utah County, sits about 45 miles south of Salt Lake City. As part of the larger Provo-Orem metro area, it’s surrounded by breathtaking views, notably the majestic Wasatch Front mountains. The city enjoys a beautiful position by the Provo River, leading many to the popular Provo River Parkway Trail for outdoor activities.

Educational excellence: BYU and beyond

Central to Provo’s identity is Brigham Young University (BYU). As one of the top institutions in the country, BYU has significantly influenced Provo’s status as a college town. The presence of BYU means Provo is bursting with educational opportunities, from lectures at the BYU Museum and Bean Life Science Museum to events at the BYU campus itself.

Quality of life in Provo

Economic, cultural and safety factors drive movers to Provo in droves.

Economic stability

Provo’s unemployment rate is below the national average. The presence of institutions like BYU and the Provo City Center Temple ensures steady employment in the education and service sectors. Additionally, with a tech boom happening in the broader Salt Lake Valley, many are finding new job opportunities within a commutable distance from Provo.

Cultural richness

Provo is home to a rich blend of cultures. While there is a significant presence of members of The Church of Jesus Christ of Latter-day Saints, Provo is diverse in thought and lifestyle. The city houses several art galleries, theaters, and the iconic Provo City Center Temple, a testament to its rich history and cultural significance.

Safety

One of the notable features of living in Provo is its low crime rates. Both violent crimes and property crimes are below the national average, making Provo a safe environment for young families and college students alike.

Cost of living: breaking down the numbers

Is Provo Utah expensive to live in? Compared to other cities along the Wasatch Front, Provo’s cost of living is slightly below average. However, with the city’s growth, housing costs have been on the rise.

Housing market insights

The median home price in Provo has seen an upward trend over the past few years, though it remains competitive compared to Salt Lake City. Average rent for apartments is also reasonable, particularly given the high student population from BYU and Provo College. However, the demand for affordable homes has been steadily increasing.

Everyday expenses

When comparing Provo’s cost for groceries, transportation, and healthcare to the national average, residents find it reasonable and often below average. However, as with any city, certain luxuries or non-essentials can drive up living costs.

The heart of Provo: its people

With a population density of around 2,500 people per square mile, Provo is lively without feeling overcrowded. The median age skews younger, thanks in part to the influx of college students. Provo residents are generally known for their hospitality, community spirit and active lifestyles, taking advantage of nearby attractions like Provo Beach and Rock Canyon.

Before you pack: Moving to Provo insights

What do I need to know before moving to Provo Utah? Here are some considerations:

Outdoor Activities: With Provo River, Provo Canyon, and myriad trails, there’s always something to do outdoors. Whether you’re into hiking, fishing, or just picnicking, Provo has you covered.

Community Feel: Provo, often dubbed “Happy Valley”, has a tight-knit community. Neighbors often become lifelong friends, and community events are frequent.

Religious Considerations: As mentioned, Provo has a substantial Mormon population. While this brings a unique cultural flavor, it’s essential to be respectful and understanding of religious practices and holidays.

Public Transportation: The bus system in Provo is reliable, but having a car might be convenient for broader exploration and commuting.

Final verdict

Living in Provo offers a harmonious blend of city life and nature, academia and culture, community and individuality. With its reasonable cost of living, low crime rates and opportunities for both personal and professional growth, Provo stands out as one of the best cities in North Central Utah. Whether you’re a student at Brigham Young University, a young family looking to settle or anyone in between, Provo provides a backdrop for memories, experiences and growth.

In the balance of life’s considerations, the essence of Provo UT seems to be this: it’s more than just a city — it’s a community, an experience, and, for many, it’s home.

So, to the question, “Is Provo Utah a good place to live?” the answer resounds as a confident “Yes!” Search our Provo apartments for rent.

Advertiser Disclosure: Credit.com has partnered with CardRatings for our coverage of credit card products. Credit.com and CardRatings may receive a commission from card issuers.

Editorial Disclosure:Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.

Snapshot: No annual fee and fantastic cash back opportunities as high as 10% on select purchases. Great rewards card option if you frequently spend on dining, travel or groceries.

Basic Features

Ongoing APR: reg_apr,reg_apr_type depending on creditworthiness

Annual fee: annual_fees

Credit needed: Scores in the credit_score_needed range

Additional Details

10% cash back on Uber and Uber Eats purchases

8% cash back on purchases through Capital One Entertainment

5% cash back on select travel reservations booked with Capital One Travel

3% cash back at approved grocery stores

1% cash back on everything else

Full Review of Capital One SavorOne Cash Rewards Card

What You’ll like About It

The Drawbacks

Is It Worth It?

FAQ

Full Review of Capital One SavorOne Cash Rewards Card

In general, this is a great card if you have experience with cash back rewards cards and you like to hunt down a good deal. Maximizing your rewards will require some attention to detail – for example, booking travel reservations through Capital One Travel to earn that 5% cash back or knowing what grocery stores qualify for the rewards points.

But, this card does offer 1% cash back on “everything else,” so even if you’re not paying attention, you’re still earning something. Heads up, this card does have a relatively high APR of reg_apr,reg_apr_type. You’ll need to pay off your card consistently to avoid that interest rate and profit off those rewards.

Like what you’re reading? Learn more about applying for the Capital One SavorOne Cash Rewards Card

What You’ll Like About It

Easy Cash Back for Food Purchases

If you’re the kind of person who loves eating out (or ordering in), this is the card for you. The Capital One SavorOne Cash Rewards card offers a variety of different rewards categories for entertainment, travel and general purchases, but your best opportunity for earning cash back rewards is with food purchases. This card offers 10% cash back on Uber Eats purchases for those splurge nights when you don’t want to leave the house.

Even if you’re not eating out, this card allows you to earn 3% cash back on grocery store purchases. (Excluding some stores like Walmart and Target. creditworthiness, income and existing debt.

How Soon Can I Increase My Credit Limit After Being Approved for a Capital One SavorOne Cash Rewards Card?

Typically, most credit card issuers require at least 6 months of on-time payments before considering you for a credit limit increase. You can improve your chances of getting an increase by paying your bills on time and managing your credit well.

How Good is a Capital One SavorOne Cash Rewards Card for Building Credit?

Like most credit cards, Capital One will report on-time payments to the credit bureaus, which could help you build up good credit over time. However, if you have a low credit score and are looking to build your credit back up with on-time credit card payments, this may not be the best option. If you’re concerned about whether or not your credit is strong enough to be approved for this card, it may be better to start out with a secured credit card that will help you upgrade to another “unsecured” credit card.

Learn more about how to sign up for a Capital One SavorOne Cash Rewards Card

Advertiser Disclosure: Credit.com has partnered with CardRatings for our coverage of credit card products. Credit.com and CardRatings may receive a commission from card issuers.

Why Your Checking Account Should Contain as Little Money as Possible

By: Natasha Etzel |

Updated

Oct. 4, 2023 – First published on Oct. 4, 2023

A bank account is an excellent place to keep your money so it’s organized and readily available when needed. Many people keep their cash in a checking account. But, while you want to stash enough money in your checking account to cover your bills and everyday expenses, you want to avoid keeping all of your cash there. I’ll explain why here, and suggest a better place to stash your extra savings.Don’t miss out on interestThe average checking account doesn’t accrue interest. That means you won’t get rewarded for keeping money in your bank account. Instead of keeping all your cash in your checking account, you should only keep enough to cover your monthly expenses. You may want to keep a bit more than just enough to cover your bills. That way, you’ll be covered if you have an unexpected charge or a more costly bill than anticipated. How much extra should you have? It depends. For some people, a couple hundred extra dollars may be ideal. But for others, it may be a good idea to include a few hundred or up to an extra $1,000 in their checking accounts for extra wiggle room.But don’t keep every last dollar you have in your checking account. If you do, you’ll miss out on interest. Instead, move your extra savings into a bank account that accrues interest. With an interest-earning bank account, you’ll get rewarded as your cash sits in the bank. You could earn money with a savings accountMany people keep extra cash in a savings account. Review the bank’s annual percentage yield (APY) when considering a new savings account. This rate is the amount of money or interest you’ll earn over a year. The higher the APY, the more money you can make. You can take advantage of an attractive interest rate by opening a high-yield savings account. At the time of writing, the bank accounts on our best high-yield savings accounts list offer APYs ranging from 4.30% to 5.26%. If you have a significant amount of extra cash and keep it in an account like this, you can earn money without doing extra work. $5,000 in savings accumulates this much interest To determine how much interest you can earn by moving your extra cash to a savings account, multiply your initial deposit by the APY your bank account offers. This will show you how much interest you can earn by keeping your money in the bank for a year. Let’s imagine you have $5,000 extra sitting in your checking account right now. If you instead move that money to a high-yield savings account with an APY of 5% and you keep it in the bank for an entire year (and your APY doesn’t change; note that banks can raise or lower APYs at any time), you’ll earn $250. That’s much better than making $0 by keeping your savings in a checking account that doesn’t accrue interest. Now you can see why it pays to avoid keeping all your money in a checking account. You can earn extra money from interest by keeping your spare cash in a savings account that offers interest. For additional tips like this, check out our free personal finance resources.

3 Reasons I Don’t Like Aldi as Much as I Used To

By: Maurie Backman |

Updated

Sept. 13, 2023 – First published on Sept. 13, 2023

At some point in 2022, I discovered Aldi and began shopping there weekly. I found that I was able to save money on my grocery bill by purchasing certain produce items there. And since I happen to have an Aldi adjacent to my local Costco, it wasn’t particularly out of my way.But over the past few months, I’ve become less enamored with Aldi. Here’s why.1. The selection is just too limitedAldi — at least near me — is a minimally stocked grocery store. The shelves aren’t loaded the way they are at my nearby ShopRite and Stop & Shop.To be fair, this was the case when I first started shopping there. But because there’s just not a lot of selection, I’m generally limited to only buying a few items when I pop into Aldi.Not so long ago, I was running into Aldi for some fruit, which I usually buy there, and I needed to grab shredded cheddar cheese. Normally, I get that at Costco, but I didn’t want to run next door to Costco and wait in a line for cheese alone. Unfortunately, though, Aldi didn’t have the cheese I needed, so I had to make an extra stop anyway.2. The inventory is too inconsistentNot only is there a limited selection of food items I can buy at Aldi, but sometimes, I can’t even find the five or six things I’m looking for. Aldi was once my go-to source for avocados, since it’s an expensive purchase and Aldi tends to sell them for less than Costco (at least in my area). But the last few times I stopped at Aldi, avocados weren’t in stock.And that’s happened to me with other things, too. Over the past several months, I’ve struggled to find everything from cucumbers to strawberries at Aldi as well.3. What the store saves me on groceries, I lose via lost working hoursShopping at Aldi still has the potential to save me a little money on groceries. At a time when supermarket prices are up 3.6% on an annual basis, that helps.The problem, however, is that even though Aldi is right near Costco in my neighborhood, thereby allowing me to combine those trips, it still takes time to visit an extra supermarket. I have to find parking, wait in a checkout line, and spend time searching the shelves.While it’s nice to save $2 here and $3 there, the reality is that a stop at Aldi might cost me 20 or more minutes of work — especially when I don’t manage to find the things I need. And losing out on that work time often means forgoing more than $2 or $3 of income. So from a time perspective, it’s just not worth it.Shopping at Aldi could make sense for a lot of people. If you’re someone with flexibility in your schedule and grocery list, and you’re not so picky about the brands you bring home, then it could pay to spend the time visiting Aldi, even if you don’t always manage to find all the things you need. But I’ve reached the point where shopping at Aldi makes less and less sense for me, so I’ll most likely stop going there unless it’s a one-off basis.

7 Little-Known Gift Cards You Should Always Buy at Costco

By: Steven Porrello |

Updated

Sept. 29, 2023 – First published on Sept. 29, 2023

Costco gift cards are one of the warehouse’s best deals. Costco often will add 10% to 30% of value when you buy its gift cards in a bundle. It would be one thing if the gift cards were for places you’d never shop, like Bed, Bath, and Beyond (R.I.P.). But Costco gift cards are surprisingly varied and include many restaurants and retailers you’re probably already spending money with.So if you, like me, pinch pennies for your finances, here are seven gift cards you should always buy at Costco.1. Jiffy LubeCostco will add 25% of value when you buy a set of two $50 Jiffy Lube eGift cards for $74.99. While Jiffy Lube doesn’t offer the cheapest oil change on the market (Walmart will likely take the gold for that), its technicians do go through rigorous training via the Jiffy Lube University to ensure no accidental damage is done to your vehicle. If quality trumps price for your vehicle, this deal will save you $25 off your next oil change (limit of five per membership).2. Alaska AirlinesPacific Northwesterners will appreciate this deal — Costco will give you a $500 eCertificate to Alaska Airlines for $449.99. That comes to 10% off your next Alaska Airlines flight (limit of four per membership).3. Southwest AirlinesIf that was the first time you’d heard of Alaska Airlines, here’s a gift card package with a more familiar airline: Southwest. Costco will add 10% of value when you buy $500 of Southwest Airlines gift cards for only $449.99.4. Cinemark TheatresIn a great deal for moviegoers, you can buy a $50 Cinemark Theatres eGift card for only $39.99 at Costco. That’s an extra 20% of value that you can use for movie tickets, food, drinks, or merchandise (limit of 10 per membership).5. Miller PaintPainting your house ain’t cheap. Interior paint jobs will cost about $2 to $6 per square foot, according to the home improvement site HomeAdvisor, while exterior paint jobs can cost about $1.50 to $4 per square foot. To ease those costs, Costco will sell you $100 of Miller Paint gift cards for $69.99 — a whopping 30% of extra value.6. SpafinderIf you thought the cost of painting your house was bad, imagine how your back will feel after hours of painting walls. To ease that pain, Costco has an irresistible gift card deal: two $50 eGift cards for $79.99 to be used at thousands of spas and salons across the country. You can also use them at participating yoga and fitness studios (limit of 10 per membership).7. Synergy RestaurantsOne of the more interesting gift card packages I’ve come across, this extremely lucrative deal — two $50 eGift cards for a sticker price of $69.99 — will help you foot the bill at hundreds of local restaurants in numerous cities across Arizona, California, Colorado, Nevada, New Mexico, and Texas. This is perhaps one of the best deals I’ve seen and can be perfect for locals in those states and travelers who are visiting them.Most members don’t realize how many gift cards Costco actually sells. In fact, these seven packages only scratch the surface. Next time you’re at your local Costco warehouse, be on the lookout for gift card packages, which are often found at the ends of aisles. You might find a deal you can’t get anywhere else.

5 Amazing Costco Buys for Less Than $10

Costco is a favorite among bargain hunters. But because it’s a place where you typically buy in bulk, it’s often not great when you only want to spend a few bucks. Believe it or not, though, there are some deals at Costco for $10 or less. Here are five amazing Costco finds that will set you back no more than $10.1. Rotisserie chickenNot surprisingly, the $4.99 rotisserie chicken tops this list. Costco debuted its famed bird for $4.99 way back in 1994. It briefly raised the price by $1 during the Great Recession in 2008, then knocked it back down to $4.99 one year later. Had Costco raised its prices to keep up with inflation since 1994, that chicken would cost $10.48 today.Costco’s rotisserie chicken will always be a fan favorite for those looking for an effortless dinner. Just be aware: Costco keeps the prices low because its rotisserie chicken is what’s called a loss leader. The warehouse giant is willing to lose money selling them because it knows it can get customers into stores, where they’ll probably buy more than just a chicken.2. Hot dog and soda comboCostco has raised the prices of many of its food court items in recent years, but the price of one perennial favorite shows no signs of budging: the hot dog and soda combo, which has cost $1.50 since it debuted in 1985. Adjusted for inflation, the hot dog and soda combo should cost $4.28. Last year, during a quarterly earnings call, Costco chief financial officer Richard Galanti said the warehouse giant could keep the $1.50 price point “forever.”3. Kirkland Signature Creamy Almond ButterYou can use almond butter as a salad dressing ingredient, slather it on toast, put it in baked goods, or just eat it straight from the jar. If you’re the type who likes to devour almond butter by the spoonful, you don’t want to pass up a 27-ounce jar of Kirkland Signature Creamy Almond Butter, available for just $7.99. That works out to less than $0.30 per ounce. By comparison, a 16-ounce jar of Trader Joe’s Creamy Almond Butter Salted costs $6.99.4. Olde Thompson Kosher Sea Salt, 5 lbsSea salt has plenty of uses that go beyond cooking. You can use it for cleaning, as an exfoliant for your skin, and sprinkle it around your garden to keep unwanted bugs away. For just $5.99, you can score a 5-pound jar of Olde Thompson Kosher Sea Salt and keep it handy for all your household and kitchen needs.5. Bisquick Pancake & Baking Mix, 96 OuncesBisquick is another one of those things that’s handy to keep in your pantry. You can use it to whip up a quick batch of pancakes or waffles for breakfast or keep it on hand for a variety of baked good recipes. A 96-ounce box of Bisquick is available at Costco for $8.89. It’s normally priced at $10.99, but there’s a $2.10 manufacturer’s discount that’s good through Oct. 8, 2023.What are the best deals at Costco?Since Costco tends to sell large quantities, you’ll typically find that a lot of the best deals cost well above $10. Regardless of the exact price, it usually makes sense to buy products at Costco that have a long shelf life. For example, even if you find great deals on fresh produce and milk, you probably don’t want to load up on these items unless you’re feeding a large crowd, as they’ll go bad quickly.Also, make sure you look beyond the grocery department for savings. For example, getting your prescriptions from Costco Pharmacy or using Costco to fill up your gas tank could also save you money.If you want to maximize the benefits of your membership, try shopping with a Visa credit card that offers rewards. (Costco only accepts Visa credit cards.) That way you can earn travel rewards or cash back when you load up on groceries and other necessities.

5 Ways to Turn $100 Into Passive Income

By: Chris Neiger |

Updated

Oct. 1, 2023 – First published on Oct. 1, 2023

Creating passive income is one of the best ways to build wealth and protect your personal finances from an emergency, like losing a job or having your salary cut. According to U.S. Census Bureau data, about 20% of Americans have some level of passive income, with the average amount earned from passive income being $4,200 annually.Passive income strategies aren’t get-rich-quick schemes, and many initially require a significant time investment. The good news is that many can be started with $100 or less. Here are a few inexpensive ways you can start generating passive income.1. Buy stocksSome people think that owning stocks is only for rich people. It’s not. In fact, 61% of Americans own stocks, according to Gallup. And while you won’t get rich investing $100, you do have the potential to easily make money.You can open an online brokerage account for free and typically buy stocks for either little or no fees these days. The hard part is figuring out what company you think will do well over the long term so that you get the largest return.Let’s look at one popular company that many people own stock in: Apple. Let’s say you invested $100 annually over the past 10 years to buy Apple’s stock and reinvested any dividends you received to buy more shares. Thanks to Apple’s phenomenal growth over the past decade, your stock would be worth $4,848 — a 385% return on your investment.Of course, picking stocks can be difficult. If you want to potentially earn passive income in the market without picking specific stocks, you may want to buy shares of an exchange-traded fund (ETF). These funds follow market indices and can be purchased for as little as $1, thanks to online platforms that allow you to purchase fractional shares.2. Rent out an extra roomThis one is super easy and might cost you $0 if you already have the extra space. The latest Census Bureau data shows that 27.6% of Americans live alone. This means that many Americans may have a spare room in their home that could be transformed into a passive income stream.While it’s not for everyone, renting out a room in your home could be one of the easiest ways to generate passive income because you’re already in the space — either renting or as a homeowner — so all you need to do is find a roommate and collect their rent payments.This could be a very lucrative way to boost your income, considering that rent prices have skyrocketed over the past few years.3. Rent out your carWith 13% of full-time Americans working from home right now and 28% on hybrid schedules, many cars are sitting unused throughout the work week. With some planning and effort, your vehicle could quickly begin generating income through car-sharing websites like Turo.You can list your vehicle on the site for free and pay Turo a fee when you’ve rented out the vehicle. Turo says the average annual income for one car on its site is $10,516. Of course, some work is required to keep the vehicle clean and coordinate pick-up and drop-off. Still, renting out your vehicle could be a low-cost way to earn semi-passive income.4. Create an online courseMany people have accumulated many skills through jobs and even hobbies. You likely know how to get certain things done that someone else would find very useful — and pay for.There are many online platforms — including Udemy, Skillshare, and Thinkific — where you can create your own professional course and then sell it to an established online audience.You’ll need to do a fair amount of work upfront creating your course — including planning the sessions, recording videos, and making other content — but once you have it up and running, you can earn passive income from your hard work.Some course-creating platforms charge a monthly fee, while others may take a percentage of each sale you make. But while this option isn’t free, it’s certainly inexpensive.5. Start a dropshipping businessThere are many different businesses that fall under the dropshipping category, including selling T-shirts online or print-on-demand content like notebooks and journals.The startup cost for dropshipping businesses is low because you don’t buy any inventory and don’t have to rent an office or retail space. Instead, you’ll spend money setting up a website and potentially selling ads to market your products. You can even become a seller on Amazon and sell products without investing in your own online shop.You’ll have to invest significant time on the front end to build your business. Still, once you’ve found a niche and have established the relevant products, dropshipping allows you to spend minimal time keeping up the business while still making online sales.Keep these things in mindWhile all of these ideas will cost you little money and have the potential to generate passive income, you’ll still need to invest time and mental energy in setting them up. For example, you may need to do a lot of research before setting up a dropshipping business or launching an online course.Like anything worthwhile, be patient and take small steps to get started. You likely won’t be an overnight success, but making any progress toward generating passive income will move you further toward your personal financial goals.

Mastercard has announced new partnerships with Instacart and Peacock. Benefits are as follows:

Instacart: Eligible World Mastercard and World Elite Mastercard cardholders who are new to the Instacart+ membership program will receive a two-month free trial and $10 off their second eligible Instacart purchase each month. Cardholders will also be eligible for perks like no delivery fees on orders over a certain size, reduced service fees, and credit back on eligible Pickup orders. With Instacart’s broad selection of local retailers, customers can shop for everything on their list from groceries and household items, pet supplies, electronics, beauty, home improvement, sporting goods and much more.

Peacock: Eligible World Mastercard and World Elite Mastercard cardholders new to Peacock Premium will receive a $3 statement credit on the Peacock Premium monthly streaming subscription. Eligible World Elite Mastercard cardholders will receive a $5 statement credit on the Peacock Premium+ monthly streaming subscription. Additionally, Mastercard cardholders will have access to Priceless Experiences such as NBCUniversal’s iconic shows and studios across the country, BravoCon and much more.

Peacock frequently has deals for 12 months for $19.99. Instacart offer is useful for anybody that orders more than twice a month.

A financial instrument is simply a contract between entities that represents the exchange of money for a certain asset. Financial instruments include most types of investments: cash, stocks, bonds, mutual funds, exchange-traded funds (ETFs), certificates of deposit (CDs), loans, derivatives, and more.

Financial instruments facilitate the movement of capital through the markets and the broader economic system. While this may take different forms, the flow of capital remains a central feature.

What Is a Financial Instrument?

Generally Accepted Accounting Principles (GAAP) defines a financial instrument as cash; evidence of an ownership interest in a company or other entity; or a contract. A financial instrument confers either a right or an obligation to the holder of the instrument, and is an asset that can be created, modified, traded, or settled.

Investors can trade financial instruments on a public exchange. The New York Stock Exchange (NYSE) is an example of a spot market in which investors can trade equity instruments for immediate delivery. 💡 Quick Tip: The best stock trading app? That’s a personal preference, of course. Generally speaking, though, a great app is one with an intuitive interface and powerful features to help make trades quickly and easily.

Financial Instrument vs Security

A security is a type of financial instrument with a fluctuating monetary value that carries a certain amount of risk for the individual or entity that holds it. Investors can trade securities through a public exchange or over-the-counter market.

The federal government regulates securities and the securities industry under a series of laws, including the Securities Act of 1933, the Securities Exchange Act of 1934, and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.

All securities are financial instruments but not all financial instruments are securities.

Like financial instruments, securities fall into different groups or categories. The four types of securities include:

• Equities. Equities represent an ownership interest in a company. Stocks and mutual funds are examples of equity securities.

• Debt. Debt refers to money lent by investors to corporate or government entities. Corporate and municipal bonds are two examples of debt securities.

• Derivatives. Derivatives are financial contracts whose value is tied to an underlying asset. Futures and stock options are derivative instruments.

• Hybrid. Hybrid securities combine aspects of debt and equity. Convertible bonds are a type of hybrid instrument.

Recommended: Bonds vs. Stocks: Understanding the Difference

Types of Financial Instruments

Financial instruments are not all alike. There are different types of financial instruments in different asset classes. Certain financial instruments are more complex in nature than others, meaning they may require more knowledge or expertise to handle or trade.

1. Cash Instruments

Cash instruments are financial instruments whose value fluctuates based on changing market conditions. Cash instruments can be securities traded on an exchange, such as stocks, or other types of financial contracts.

For example, a certificate of deposit account (CD) is a type of cash instrument. Loans also fall under the cash instrument heading as they represent an agreement or contract between two parties where money is exchanged.

2. Derivative Instruments

Derivative instruments or derivatives draw their value from an underlying asset, and fluctuate based on the changing value of the underlying security or benchmark.

As mentioned, options are a type of derivative instrument, as are futures contracts, forwards, and swaps.

3. Foreign Exchange Instruments

Foreign exchange instruments are financial instruments associated with international markets. For example, in forex trading investors trade currencies from different currencies through global exchanges.

Asset Classes of Financial Instruments

Financial instruments can also be broken down by asset class.

4. Debt-Based Financial Instruments

Companies use debt-based financial instruments as a means of raising capital. For example, say a municipal government wants to launch a road improvement project but lacks the funding to do so. They may issue one or more municipal bonds to raise the money they need.

Investors buy these bonds, contributing the capital needed for the road project. The municipal government then pays the investors back their principal at a later date, along with interest.

5. Equity-Based Financial Instruments

Equity-based financial instruments convey some form of ownership of an entity. If you buy 100 shares of stock in XYZ company, for example, you’re purchasing an equity-based instrument.

Equity-based instruments can help companies raise capital, but the company does not have to pay anything back to investors. Instead, investors may receive dividends from the stock shares they own, or realize profits if they’re able to sell those shares for a capital gain.

Are Commodities Financial Instruments?

Commodities such as oil or gas, precious metals, agricultural products and other raw materials are not considered financial instruments. A commodity itself, such as pork or copper, doesn’t direct the flow of capital.

That said, there are certain instruments whereby commodities are traded, including stocks, exchange-traded funds, and futures contracts.

A futures contract represents an agreement to buy or sell a certain commodity at a specific price at a future date. So, for example, an orange grower might sell a futures contract agreeing to sell a certain amount of their crop for a set price. An orange juice company could then buy a contract to purchase oranges at X price.

For the everyday investor, futures trading in commodities typically doesn’t mean you plan to take delivery of two tons of coffee beans or 4,000 bushels of corn. Instead, you buy a futures contract with the intention of selling it before it expires. 💡 Quick Tip: It’s smart to invest in a range of assets so that you’re not overly reliant on any one company or market to do well. For example, by investing in different sectors you can add diversification to your portfolio, which may help mitigate some risk factors over time.

Uses of Financial Instruments

Investors and businesses may use financial instrument for the following purposes:

1. As a Means of Payment

You already use financial instruments in your everyday life. When you write a check to pay a bill or use cash to buy groceries, you’re exchanging a financial instrument for goods and services.

Likewise, business entities may charge purchases to a business credit card. They’re borrowing money from the credit card company and paying it back at a later date, often with interest.

2. Risk Transfer

Investors use financial instruments to transfer risk when trading options and other derivative instruments, such as interest rate swaps. With options, for example, an investor has the option to buy or sell an underlying asset at a specified price on or before a predetermined date. A contract exists between the individual who writes the option and the individual who buys it. This type of financial instrument allows an investor to speculate about which way prices for a particular security may move in the future.

3. To Store Value

Businesses often use financial instruments in this way. For example, say you default on a credit card balance. Your credit card company can write off the amount as a bad debt and sell it to a debt collector. Meanwhile, businesses with outstanding invoices they’re awaiting payment on can use factoring or accounts receivables financing to borrow against their value.

4. To Raise Capital

Companies may issue stocks or bonds in order to get access to capital that they can invest in their business. In this case, the financial instruments could be a means of raising capital for one party and a store of value for the other.

Importance of Financial Instruments

Financial instruments are central to not only the stock market, but also the financial and economic system as a whole. They provide structures and legal obligations that facilitate the regulated exchange of capital via investing, lending and borrowing, speculation and growth.

In short, financial instruments keep the financial markets moving, and they also help businesses to keep their doors open and allow consumers to manage their finances, plan for the future, and invest with the hope of future gains.

For example, you may also have a savings account that you use to hold your emergency fund, an Individual Retirement Account (IRA) that you use to save for retirement and a taxable brokerage account for trading stocks. Your checking account is one of the basic tools you might use to pay bills or make purchases.

You might be paying down a mortgage or student loans while occasionally using credit cards to spend. All of these financial instruments allow you to direct the flow of money from one place to another.

The Takeaway

Financial instruments are integral to every aspect of the financial world, and they also play a significant part in business transactions and day-to-day financial management. If you trade stocks, invest in an IRA, or write checks to your landlord, then you’re contributing to the movement of capital with various financial instruments. Understanding the different types of financial instruments is the first step in becoming a steward of your own money.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

Invest with as little as $5 with a SoFi Active Investing account.

Photo credit: iStock/Love portrait and love the world

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by email customer service at [email protected]. Please read the prospectus carefully prior to investing. Shares of ETFs must be bought and sold at market price, which can vary significantly from the Fund’s net asset value (NAV). Investment returns are subject to market volatility and shares may be worth more or less their original value when redeemed. The diversification of an ETF will not protect against loss. An ETF may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

It’s never too early to start learning smart strategies for managing one’s money. Most teens don’t get a formal education in topics like budgeting, investing, and choosing the right financial institution for their money, which is a missed opportunity.

That’s why it can be especially important for young people to take steps to build their own financial insights and skills. That can mean understanding the right amount to save and spend when earning a salary; what the challenges of managing credit can be; and how to invest money wisely.

This guide covers these aspects of financial literacy and more. Consider it a smart starting point as you build your money knowledge and know-how. Whether you’re thinking about buying your first car, affording college, or starting your own business someday, you’ll learn some of the key steps to bring your financial life into focus.

Why Is Financial Literacy Important for Teens?

Sad but true: Most people are launched into adulthood without being educated on personal finance. What’s more, in many households, money isn’t a topic that’s freely discussed, so kids don’t grow up hearing about how much their parents earn, spend, or save.

These are factors that can make it a challenge to gain financial knowledge and money management skills. However, learning about how to budget, save, invest, and spend wisely when young can set you up on the path to achieve your short- and long-term goals. That’s why you’ll learn some financial tips for teenagers right here.

The sooner you understand your way around money, the earlier you can get on the path to, say, travel around Europe for a summer, manage student loan debt, or even start saving for your dream house.

💡 Quick Tip: Typically, checking accounts don’t earn interest. However, some accounts do, and online banks are more likely than brick-and-mortar banks to offer you the best rates.

5 Key Financial Tips for Teens

Making the most of your money as you start on the path to your independent life doesn’t need to be complicated. Here are five important financial literacy concepts for teens.

1. Opening a Bank Account

Financial planning for teens often starts with having a bank account. Not only will a bank account make it easier to cash those birthday checks from Grandma, it also provides a place to monitor money and start saving.

Most bank accounts billed as “teen accounts” are really just joint bank accounts, because teenagers under 18 typically need a parent or guardian to also be an account holder. This makes it possible to open a bank account for a minor.

Although it’s sometimes easier for teens to open an account at the same place their parents bank, it may be worth researching which banks in the area have the best benefits for teenagers specifically. Some points to know:

• The age for opening up an account varies from bank to bank, so make sure to check specifications on the bank’s website beforehand.

• Valid identification like a student ID, driver’s license, passport, birth certificate, and/or social security card is also required for account owners when opening a teen checking account.

• In some cases, a parent or guardian must be present to open the account, but some banks do offer the opportunity to open an account online. This will often require uploading the same documents to prove your identity.

• Some banks also offer parental controls, setting withdrawal and debit card limits, or even text alerts about account activity. Before opening an account, it may be worth considering what is most important and beneficial — definitely talk it over with a parent or legal guardian.

• Learning about any fees or minimum balances from the bank is also important step in personal finance for teens. Make sure to ask the right questions in person or check out the bank’s fee structure on their website. Ideally, you might want an account with no fees and the ability to earn a bit of interest (many checking accounts pay no interest). You are typically more likely to find such offers at online vs. traditional banks.

• Having a bank account means access to making deposits and withdrawals, plus online banking tools that can help with money management.

A word about debit cards: A teen checking account typically offers access to a debit card, which allows account holders to take out cash from ATMs and use the card for purchases in stores or online.

And since a debit card takes money directly out of the checking account for payments, it may help to download the bank’s mobile app, if available. This can help with checking account balances and, at some banks, setting up alerts if the account falls below a certain balance.

A bank account is a great first step in learning money management, whether it’s using a debit card, checking balances, transferring money, or setting up a direct deposit for paychecks. Especially with a new job, a weekly or bi-weekly paycheck comes with learning more financial responsibility. With a personal bank account, teens can pick up crucial financial skills before turning 18.

And, at many banks, once someone does turn 18, the account can turn into a standard checking account, which they can either choose to keep or leave for a new banking institution. (Important note: There may be new fees, so it’s important to keep an eye on what those might be.)

Recommended: What Is a Student Checking Account?

2. Budgeting For Teens

Another financial tip for teenagers involves learning how to balance income and expenses. Making a simple budget can help keep things on track. Whether it’s keeping tabs on a monthly allowance or income from a part-time job, knowing how much money is spent versus how much money gets made is a key part of money management. Plus, a budget can show how much money is available to save every month.

Many banks with mobile or online banking offer simple budgeting tools, such as categorizing money into simple buckets like “spendable” or “set aside.” One pretty practical budget suggestion is the 50/30/20 method. This helps to simplify spending categories: rather than trying to decipher every transaction and having hundreds of small budgets for individual items, the 50/30/20 method just divides monthly income into thirds.

• 50% of income would be put toward necessities, such as bills and other regular spending that’s hard to do without. For teens, this might mean car-related expenses, like insurance and gas, or a monthly cellphone bill. If 50% seems like a lot — especially if parents are still paying for big expenses like groceries and housing — consider putting an extra 10% into savings or other financial goals for now.

• 30% would be allocated for day-to-day spending, like going out to eat with friends, entertainment, shopping, and other fun activities.

• The remaining 20% would be allocated for financial goals, usually savings or debt payoff. Maybe this can be the start of a college fund, or saving up for a big purchase in the future?

3. Smart Savings

In tandem with having a budget, learning how to save money is an important part of financial planning. Opening both a checking and savings account may make it simpler to put money away.

Since a debit card is only tied to a checking account, that’s like an added buffer from the money in a savings account. Plus, learning to regularly transfer money into a savings account can help create healthy money habits.

When you have a regular paycheck, one of the simplest ways to save more is to set up direct deposit to divide the funds between a checking and savings account. If 20% automatically goes directly into savings, it requires little extra thought each pay period.

Automating your savings in this way takes away the need to manually transfer money. This can help eliminate any mental gymnastics surrounding the desire to spend money in your checking account immediately — it’s like it was never there in the first place.

Plus, in an emergency, a connected savings account can help prevent overdraft fees. If college is in the plans, saving now could mean taking out fewer loans in the future.

In fact, this thinking can be applied to any money goal, whether it’s a new phone, car, or a big post-graduation trip. Saving now can make it easier to achieve later.

💡 Quick Tip: Most savings accounts only earn a fraction of a percentage in interest. Not at SoFi. Our high-yield savings account can help you make meaningful progress towards your financial goals.

4. Being Cautious With Credit

Financial tips for teens are full of dire warnings about the perils of credit cards. But learning early on how credit cards work and how to manage credit is also part of mastering money management. Building credit now may open more doors in the long run.

For example, establishing a positive credit history can help make it more likely to successfully secure a loan for a car or rent an apartment down the road.

One way for teens to start is to get added as an authorized user on a parent’s credit card. The authorized user gets the benefits of the credit card and building credit history without the responsibility of being the primary cardholder and making payments.

However, since late payments may impact both credit scores, teens can also set up an arrangement to pay off any debt incurred using the card each month.

In fact, it’s getting harder for people under the age of 21 to get a credit card, because federal law under the Credit CARD Act of 2009 requires credit card issuers to verify that the applicant has the following before a credit card is issued:

• A cosigner’s signature. The cosigner can be a parent, guardian, etc. as long as they are able to pay the applicant’s debt from the card.

• Official financial information proving that the applicant can repay the debt on their own.

The submitted application must be written. And if a person under 21 is approved for a card, they can’t get a credit limit increase without written approval from the cosigner.

Eventually opening an individual credit card without a cosigner, of course, means a lot more financial responsibility. Paying a credit card in full each month, as opposed to carrying a balance, is an important financial habit to get the hang of, as paying in full each billing cycle means the cardholder won’t pay interest on a balance and it can help build credit score.

Until then, an authorized user receives a separate credit card in his or her name, but there may be no need to even use the card. Just having it issued can help build credit if the main cardholder is keeping up with their payments. As credit builds, it’s smart to monitor credit reports and scores for errors or fraud. It might be a good idea to start monitoring credit through a free site like FreeCreditReport.com .

5. Setting Up a Side Hustle

If a part-time job or summer gig isn’t an option just yet, whether due to age, school work, or other restrictions, there are other options for earning extra cash. One of the benefits of a side hustle is being able to bring in income. And any income, however small, could help build good personal finance habits like budgeting and saving.

For ideas, look to needs in the community, such as assisting older adults with technology, babysitting, tutoring, or lawn care. Helping on a moving day, walking dogs, or washing cars are also great ways to step up from a beginner’s lemonade stand.

You might also consider your hobbies: Do you paint landscapes in your free time? Make jewelry? You could possibly sell your work to bring in some cash.

For those nearing college and looking for a part-time or entry-level job, it may be worth considering a company that offers tuition support or reimbursement for their employees.

Building smart financial planning skills now may make it even easier down the road when starting a full-time job — with budgeting and saving.

Can You Invest as a Teenager?

Many teenagers are curious about investing and how they might build wealth that way. Here are a few things to know if you’re wondering how to invest as a teenager:

• If you are under age 18, you cannot be the sole owner of a standard brokerage account.

• With adult supervision, you may open what is known as a custodial account. This means that the adult oversees the account while you are under 18. When you turn 18, you can likely take over control of the account with the adult’s approval.

By collaborating with an adult in this way on investments, you can learn the basics and begin to experiment. The conventional wisdom is that, the younger you are, the more risk you can afford to take with investing, since you have time to recoup any losses and ride out the ups and downs of the market.

Just do keep in mind that investment does have inherent risk, as your portfolio isn’t insured the same way money in the bank is.

Once You Are Old Enough to Invest, Where Do You Start?

If you are old enough, here’s how to invest as a teenager. Keep these tips in mind:

• Do your research. There is plenty of information about investing available online, via apps and classes, in books, on podcasts, and beyond. Find reputable resources and educate yourself on how to invest money as a teen. This can include both principles of investing as well as different kinds of investments to consider.

• Set goals. When you begin investing, it’s wise to figure out your goals, and you may indeed have more than one. Perhaps you want to invest in the short-term to help generate money to pay back student loans. And maybe you also want to begin saving to start a business when you are 35. Those different goals and timeframes can influence how you invest.

• Opening a brokerage account. Once you are old enough, you will have a choice about the sort of account you open and how it is managed. Whether you want to work with a financial professional or try robo advising, spend time understanding the pros and cons of your options.

When you make a decision, you’ll be ready to invest money as a teenager, but it doesn’t have to be set in stone. You can shift gears and try other methods as well.

Making Smart Money Moves With SoFi as a Teen

While SoFi doesn’t offer bank accounts for minors, take a look at what we offer for when you are of legal age to open an account. Or, if you are age 15 or older, see if you might be added as an authorized user to an adult’s account.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

What should high school students know about financial literacy?

It is important for high school students to learn about opening bank accounts, budgeting, saving, managing credit wisely, and bringing in income.

How can a 16-year-old invest money?

A 16-year-old typically cannot open their own brokerage account. However, they can open a custodial account with a trusted adult.

How would you invest $1,000 as a teenager?

A teenager typically cannot invest money on their own; they would have to open a custodial account with a trusted adult. Then, they would have to identify a goal for the funds (to generate income ASAP? To grow slowly for use later in life?) and select the right kind of investments.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.50% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.50% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 8/9/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Interest rates can have a real impact on inflation. Learn how it works and what changing interest rates could mean for you.

October 3, 2023

When inflation is on the rise, everything from groceries to gas can get more expensive. And while a little inflation is normal, the Federal Reserve Board (also known as “the Fed”) tries to prevent steep increases in prices. Inflationary spikes can occur due to several factors, including supply chain issues, a booming labor market, and a low interest rate environment.

The Fed monitors inflation by tracking the average costs of goods and services. One of the most relied-upon measures of inflation is the Consumer Price Index (CPI), which looks at common expenses like food, energy, transportation, shelter, and health care.

When inflation is high, as it was in 2021 and 2022—with the headline number peaking in June 2022 at 9.1%, per a Bankrate article citing the Bureau of Labor Statistics (BLS)—consumers’ dollars don’t go as far because goods and services are more expensive. This not-so-fun reality tends to put a damper on economic growth, and people with a lower income are disproportionately burdened because they cannot afford higher prices. But it’s not a great situation for anyone.

So, how does raising interest rates affect inflation? Let’s start with why inflation can happen in the first place.

Why is inflation so high?

The pandemic sparked a chain of events—including supply chain disruptions, disruptions in production, and pandemic stimulus packages, per Bankrate—that helped lead to the inflationary spike between 2021 and 2022.

First, the global supply chain, which encompasses all stages of manufacturing, assembly, and logistics that make it possible for goods to be delivered around the globe in a timely fashion, was severely impacted by illness, business closures, and travel restrictions, per Bankrate. Simultaneously, demand for goods increased as people—many working from home—began ordering more things online to be shipped directly to their front doors.

It’s economics 101: When demand goes up and supply goes down, prices rise. And that causes inflation.

Then, as the pandemic started to ease, another event that would lead to price shocks occurred: Russia’s invasion of Ukraine. Russia is a major supplier of the world’s oil. As more countries placed war-related sanctions on Russia, oil prices rose—a lot. According to Bankrate, the price of a barrel of oil nearly doubled from February 2022 (when the war began) to July 2022.

Meanwhile, the upward trajectory of a robust job market and a roaring stock market in the U.S. meant that many consumers could afford to pay higher prices at the stores and the pumps. This combination of forces can propel prices even higher and keep economists and policymakers at the Fed up at night.

Luckily, the Fed has a tool to combat runaway inflation: interest rates.

What happens to inflation when interest rates rise?

The Federal Reserve’s job is to keep inflation manageable so that consumers are encouraged to spend and save. Interest rates—which represent the cost of borrowing money—are reflected in the annual percentage yields (APYs) of savings accounts and mortgage rates. (Learn more about how the Federal Reserve can affect mortgage rates.)

How does raising interest rates affect inflation?

When interest rates go up, borrowing money gets more expensive. How does this increase in interest rates affect you? Mortgages, car loans, and business loans aren’t as attractive. As a result, fewer consumers are willing to take out loans to buy or invest in things. Higher interest rates tamp down demand, which usually leads to a dip in prices as well.

Consumers are affected in other ways, too. Because interest rates on savings accounts, certificates of deposit (CDs), and money market accounts tend to increase, people move more of their money into these savings products to reap the benefits. Here’s how raised interest rates can affect those different accounts:

Savings Accounts

Banks’ interest rates typically track what the Federal Reserve is doing. So if you’re wondering when savings account interest rates will go up, it’s usually after a Fed rate hike. Money in a high-yield savings account during periods of higher interest rates will yield more returns as your funds compound over time.

CDs

CDs offer a guaranteed interest rate for the entire term of the CD, no matter what is happening in the stock market or if interest rates are rising (or falling). That said, these savings vehicles are especially beneficial when CD rates are high because you can lock in that rate over a set period—typically between three months and 10 years.

Choose your term, lock in your rate, and watch your CD grow

Discover Bank, Member FDIC

Money Market Accounts

Money market accounts also benefit from higher interest rates. They can feature an APY that’s competitive with savings accounts, but they can also include a debit card like a checking account for easy access to your money. To get the most out of a money market account, choose one with a high APY that doesn’t include fees.

When will inflation go down?

Inflation doesn’t last forever. In fact, after a series of interest rate hikes by the Fed, inflation had simmered down to 3% by June 2023, its lowest since March 2021, according to the BLS.

Economic experts predict, however, that inflation could continue through 2024, according to Bankrate. And the Federal Reserve may raise interest rates at least once or twice more, according to a Bankrate poll.

Keep saving through the ups and downs of inflation

Though no one knows for sure when inflation will go up or down, here’s one piece of advice that’s always wise during uncertain economic times: Stay the course. That means continuing to save for retirement and spend money wisely to make your financial goals a reality.

Looking for a safe place to keep your savings that also offers a high interest rate so your money can grow over time? Look no further than a high-yield online savings account.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

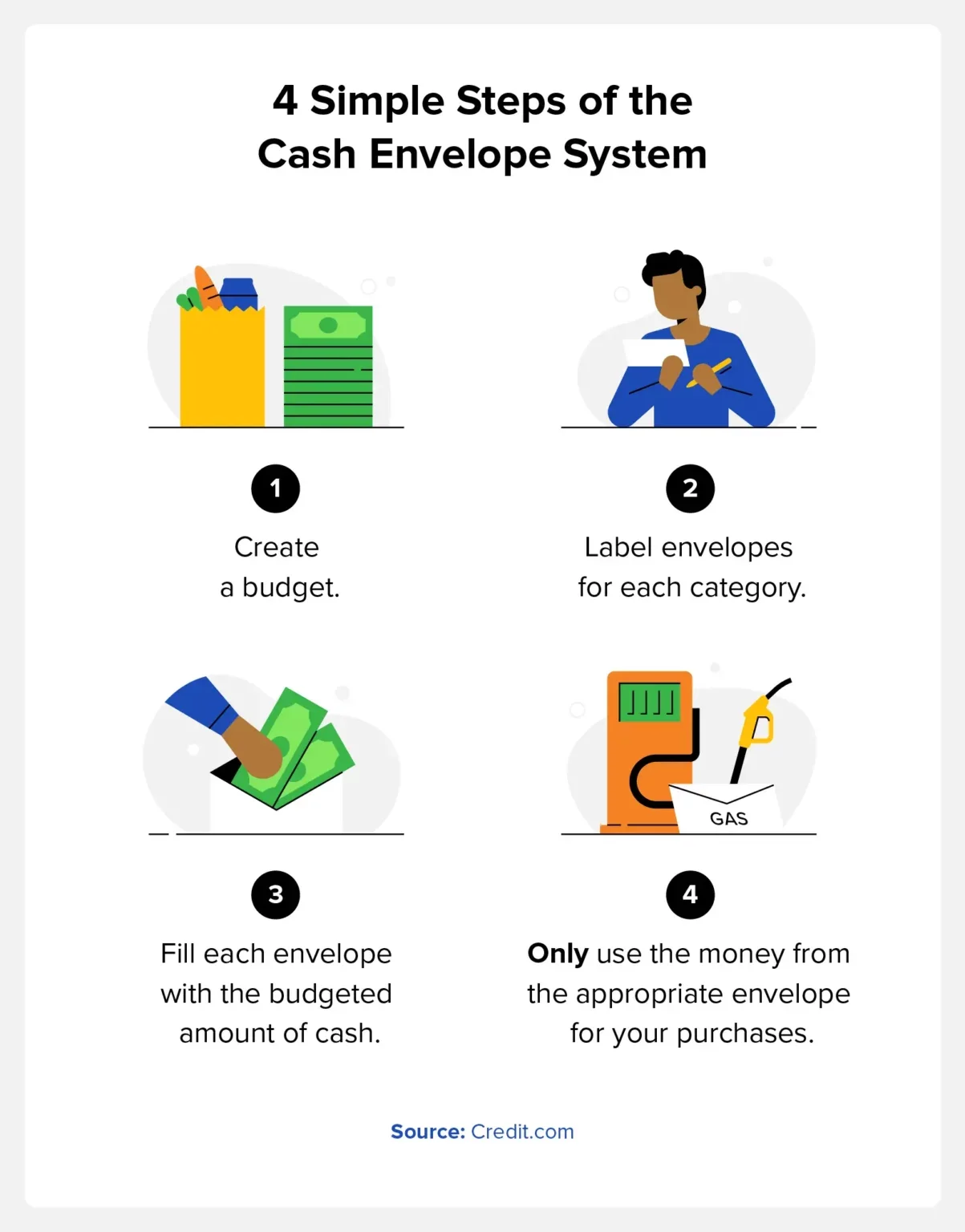

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

A place for everything, and everything in its place.

Have you ever visited a friend and opened their pantry doors to find an extremely organized space? If so, you can attest that it’s almost breathtaking. They’ve aligned bottles of oils, and beautiful jars contain nuts and dried fruit. Clear, labeled containers hold pasta and grains. They may have even gone so far as to color-coordinate each shelf.

Of course, we can’t all be Marie Kondo in the pantry. That is to say, don’t feel bad if your pantry has become the place to store, well, everything, from food to mail and kitchen appliances. You are definitely not alone.

So, how do you get started sorting it out and regaining control of this important organizational space? Let’s take it step-by-step with these 10 pantry organization ideas. You can create a pantry that captivates you and your family and friends.

Fair warning: Once you’ve organized your pantry with these organization ideas, the rest of your kitchen is sure to follow.

1. Clean out and declutter

Albert Einstein said, “Out of clutter, find simplicity. From discord, find harmony. In the middle of difficulty lies opportunity.” So, consider this an opportunity to bring harmony to your home with unique pantry organization ideas. As most humans, you’ve probably thought about organizing your pantry a hundred times. You may have even started with a shelf only to find yourself waylaid by one of life’s many other demands.