Florida topped the nation in mortgage fraud for the second year running, according to a report released today by the Mortgage Asset Research Institute (MARI).

Nevada and Michigan followed in a close second and third, respectively, according to the study.

The group found that the most common type of mortgage fraud in 2007 involved fudged employment history and claimed income, the same issue prevalent a year earlier.

However, undisclosed/incorrect debts, liens, and judgments increased 50 percent from 2006 to 2007.

The second most common type of fraud involved verifications of deposit, followed by fraud tied to tax/financial statements, home appraisal fraud, and fraud involved in escrow/closing.

Fraud was also prevalent in verifications of employment and in credit reporting, revealing that no area was exempt from misrepresentation.

MARI noted that rising property values forced unqualified borrowers and prospectors to “stretch the truth” on loan applications to gain approval with the help of industry professionals who assumed endless higher values would clear up any future problems.

But as property values continue to slide, the amount of fraud that took place is becoming all too evident.

“As we began to notice last year, the stagnant and/or declining real estate markets in Florida, Nevada, and California have resulted in easier identification of mortgage fraud,” the report said.

“Borrowers unable to re-sell their property, end up becoming delinquent on their loans, unmasking the misrepresentation(s) and therefore higher rates of MIDEX reporting.”

Here are the top 10 states by level of mortgage fraud for 2007:

1. Florida 2. Nevada 3. Michigan 4. California 5. Utah 6. Georgia 7. Virginia 8. Illinois 9. New York 10. Minnesota

Virginia made its first appearance in the top ten in this year’s report, and Colorado showed the most improvement, falling to 17th from ninth a year earlier.

“Fraud is persistent. In constricting markets, fraud becomes a tool of desperation that dishonorable companies and individuals use to maintain lifestyles, livelihoods and bottom lines,” the report concluded.

Prominent YouTube content creator Jimmy Donaldson — best known as MrBeast — took on the world of luxury real estate, and hundreds of millions of viewers tuned in to watch him tour upscale properties with some of his most famous friends (Justin Timberlake, Mark Cuban, and Miranda Cosgrove).

The YouTuber, who holds the title of the most-subscribed individual on the platform (and also has the second-most-subscribed channel overall), is famous for his viral videos centered around expensive stunts, challenges, and donations.

And he’s set quite a few records since launching his channel in 2013.

In 2017, he released his “counting to 100,000” video — which became his breakthrough viral video — and he has become increasingly popular ever since, with most of his videos gaining hundreds of millions of views.

By 2021, MrBeast was making headlines for breaking the record for the fastest non-music video to reach 100 million views, thanks to his Squid Game-themed video. That video now has over 500 million views.

He’s also known for his charitable endeavors, and for the fact that the more popular he gets, the more money he gives away.

While many have claimed that his monetary giveaways could be the primary reason why he accrues millions upon millions of video views, one of his most recent viral hits debunks this theory.

[embedded content]

On October 14, MrBeast released a new video titled $1 vs $100,000,000 House!, where the YouTuber — alongside his crew and several famous pals — tour homes of different price points, from a $1 shack to a $100 million mansion in Los Angeles (that’s actually worth $139 million).

The video garnered more than 100 million views in its first 10 days and shattered the previous record for the most views within 24 hours — a record that MrBeast himself had set with his “7 Days Stranded at Sea” video — proving to naysayers that giving money away is not the reason behind Donaldson’s success.

Now, since the content crossed the threshold into our turf — the world of luxury real estate — we wanted to provide some background info on the properties featured in MrBeast’s video — including specs, updated prices, photos and more.

And we also got some behind-the-scenes tidbits that the listing agents shared with us, including how long ago the property tours took place, and what type of response they saw after the video launched.

All the luxury homes featured in MrBeast’s “$1 vs $100,000,000 House!” video

While there’s not much to say about the $1 shack that kicked off the video (that one might even be best summarized as “what you see is what you get”), there’s lots to learn about the other striking homes that made the cut. We’ll also skip the $1 million house, as that price point doesn’t necessarily fall into luxury territory in many of the real estate markets we cover.

We talked to some of the agents in charge of the listings featured in the viral video, and they shared their excitement about being part of the project.

“It was a cool experience to be affiliated with Mr. Beast,” says Rachael Williams with Revel Real Estate, who holds the listing for the $15 million property featured in the video. “Apparently this video broke the world record for most views in 24 hours. So essentially being a part of history is pretty awesome! 😎“

Wondering whether it was MrBeast’s team that sourced the houses? We were thinking the same, and it turns out that “Mr. Beast’s team reached out to us to be featured,” Ben Bacal, Founder and real estate agent at Revel Real Estate tells us. “We were told our property might, or might not make the final cut, but it did! And we’re so happy that they included it. “

The agents also told us that filming — at least for some of the properties — took place back in August, despite the final cut being released in October.

Naturally, that also means that some of the prices have changed in the meantime.

The $45 million house was most recently listed for $29.888 million, while the art-filled Malibu home dropped its asking from $69 million to $59 million. And the $100 million house is actually far more expensive in real life. So let’s take them one at a time.

The $100 million house, LA FIN

The focal point of the video, the striking $100 million house MrBeast tours alongside celebrity guest Justin Timberlake is actually a $139 million mega-mansion in Bel Air, California.

Newly built in 2021, the spec mansion is dubbed LA FIN, and is touted as “the pinnacle of homes designed for entertaining at a scale comparable to the best hotels in the world.” And for good reason.

Featuring an impressive total of 12 bedrooms, 17 bathrooms, and a guest penthouse, the luxury abode has an entire array of amenities that you’d be hard-pressed to find anywhere else, including a 6,000-square-foot nightclub, a unique 6-car elevator that displays the car collection above the nightclub, and an ice-cold vodka-tasting room furnished with fur coats.

Other notable features include a cigar lounge, a cutting-edge gym equipped with Peloton equipment and a rock-climbing wall

The primary bedroom suite of the luxury Bel Air mansion is nestled in its private wing.

Cloaked in Italian oak, the bedroom’s centerpiece is a striking fireplace crafted from Portuguese marble, and has an adjoining bathroom reminiscent of a world-class spa with Calacatta gold marble, a sweeping 100-square-foot shower, and a bathtub sculpted from a singular marble block.

With so many unique features, we could talk about this property all day. But since pictures are worth a thousand words, why not take a closer look inside the ultra-luxurious Bel Air mansion instead (Swipe for more pics):

Price & property history: The $139 million mansion was first listed in February 2022, with Jon Grauman and Adam Rosenfeld (The Agency). And while it has retained its asking price, representation for the property has since changed, with Shawn Elliot or NestSeekers International.

The art-filled $69 million house

Joined by iCarly actress Miranda Cosgrove, MrBeast tours the second most expensive home, a Malibu architectural gem that bears the signature of lauded architect Ed Niles.

The art-filled glass-and-steel house — which we’ve covered in depth here following its recent price adjustment, that brought it from $69 million down to $59.5 million — is propped up on a hill just 75 feet away from water and pairs its excellent oceanfront location with a distinct architecture that makes it one of Malibu’s most impressive real estate offerings.

The avant-garde abode is defined by sharp geometric angles, varied shapes, and out-of-the-box materials like glass, steel, and concrete, all thoughtfully executed and flowing beautifully together.

Photo credit: Simon Berlyn courtesy of Compass

Featuring 4 bedrooms and 6 bathrooms with a detached one-bed, one-bath guesthouse on 8,206 square feet, the glass-and-steel house incorporates many Feng Shui principles.

Price & property history: Originally listed in March 2023 with an ambitious $68.8 million price tag, the Ed Niles-designed home recently had its price re-adjusted to $59.5 million.

Madison Hildebrand and Jennifer Chrisman at Compass and Wendy Wong and Katherine Quach of Treelane Realty Group are spearheading the home sale.

The $45 million Brentwood house

Our favorite property on this list — though we might be a bit biased, as we’ve written extensively about this mansion before — is a newly built spec mansion in Los Angeles’ family-friendly Brentwood neighborhood.

Toured alongside billionaire Mark Cuban (who lives in an equally impressive luxury mansion), the spectacular property known as Allure is a 14,000-square-foot mansion that’s been carved into the mountainside — an arduous process that included the removal of approximately 680 truckloads of dirt to create over an acre of flat land.

Photo credit: Nils Timm / Nils Timm Visuals

First listed for $45 million (price later dropped to $29.888 million) ‘Allure’ is inspired by “The Greats” across various domains — including elite athletes, top Hollywood stars, influential C-suite executives, and international business tycoons.

And its long (and creative) list of amenities reflects that.

The 7-bedroom, 8-bath home has a movie theater with a Rolls Royce starlight ceiling, two striking living moss walls, a dedicated regulation-sized pickleball court, an NBA-sized half-court sporting a Michael Jordan design, a putting green, and a sanctuary spa with a fitness center and sauna.

Photo credit: Nils Timm / Nils Timm Visuals

The upscale Brentwood mansion was developed by Ramtin “Ray” Nosrati of Huntington Estates Properties, the mastermind behind some of LA’s most affluent homes.

Price & property history: The 14,000-square-foot house was first listed for $45 million. With a revised price of $29.888 million, Allure is listed with Sally Forster Jones and Nicole Plaxen of Sally Forster Jones Group at Compass, Santiago Arana at The Agency, Shauna Walters at Beverly Hills Estates, and Josh and Matt Altman of The Altman Brothers at Douglas Elliman.

Take a closer look inside: This $29.888 million Brentwood mansion is the Michael Jordan of homes

The $30 million mansion with an indoor water park

While most of the houses in MrBeast’s videos are located in California, the $30 million mansion takes us on a trip to Leverett, Massachusetts, to visit a highly unique property likened to “a candy store for adults.”

Known as the Juggler Meadow Estate, the $30 million Massachusetts property is the former home of late Yankee Candle founder Michael Kittredge II and is a local celebrity in its own right (which comes as little surprise after watching the video tour).

With an impressive 120,000 square feet of interior space — split between 8 structures — the compound features a 25,000-square-foot main residence, a 55,000-square-foot spa, an indoor water park, three tennis courts, a three-lane bowling alley, two grotto-like wine cellars, and a 10-seat movie theater, among many other amenities.

Price & property history: The former Yankee Candle founder’s house was listed in the second half of 2022 for $23 million. Popular listing websites like Zillow and Realtor.com still show the same $23 million asking price, while the official listing on the brokerage’s website (the house is repped by Johnny Hatem Jr with The Sarkis Team at Douglas Elliman) says the price is only available upon request.

The $15 million house

While the other luxury houses MrBeast visited strayed a bit from the price point shown in the video, the next property on our list is a true-to-story $15 million home in the Hollywood Hills — with a killer location and spectacular design.

Perched atop the famous Bird Streets (widely known as some of LA’s most desirable streets, (attracting celebrities like Leo DiCaprio, Tobey Maguire, or Jodie Foster), the 7,217-square-foot contemporary, Ameen Ayoub-designed residence was completed in 2021.

Photo credit: Hunter Kerhart courtesy of Revel Real Estate

Packed with world-class amenities — including a chef’s kitchen with Miele appliances, an aquarium bar that looks into the infinite pool, a custom-built honeycomb quartz wine cellar, a decoupled home theatre, a subterranean garage, and a state-of-the-art fitness center with a sauna and steam shower — the 3-bed, 5-bath home is pure luxury.

Photo credit: Hunter Kerhart courtesy of Revel Real Estate

It also has a jaw-dropping primary suite with a fireplace and private terrace, dual bathrooms, and a designer closet.

Price & property history: Listed for $14,900,000 with by Ben Bacal and Rachel Williams of Revel Real Estate, the $15 million was listed in mid-2023, and hasn’t had any price adjustments since.

After being featured in MrBeast’s $1 vs $100,000,000 House! video, the property’s agents share that the Hollywood Hills mansion already received an offer — for a one-year lease. And more will likely follow, as the viral video keeps accruing millions of views.

Which property did you love the most?

*Featured image credit: Fidias, CC BY 3.0, via Wikimedia Commons, Nils Timm / Nils Timm Visuals & Simon Berlyn courtesy of Compass

More stories

Hype House: the TikTok Mansion Owned by Some of the Internet’s Biggest Stars

A Closer Look at Machine Gun Kelly’s house in Los Angeles, Bought from Youtuber Logan Paul

Tour Andrew Rea’s (Binging with Babish) House in Brooklyn

MBA advocated for action in three key areas: the reauthorization of the NFIP, assured access to property insurance, and reforms to the FHA-Insured multifamily program. Reauthorization of the NFIP As new NFIP policies cannot be issued during a lapse in authorization, MBA stressed the necessity of a longer-term authorization to provide stability and certainty for … [Read more…]

Jamie Woodwell, head of commercial real estate research at MBA, shed some light on current market trends: “The logjam in the commercial real estate markets that began last summer has remained firmly in place. Questions about supply and demand dynamics for some properties, the rise and volatility in interest rates, the low number of transactions, … [Read more…]

US mortgage rates rose for the third week in a row but stayed just under the 7% threshold.

The 30-year fixed-rate mortgage averaged 6.96% in the week ending August 10, up from 6.90% the week before, according to data from Freddie Mac released Thursday. A year ago, the 30-year fixed-rate was 5.22%.

Elevated mortgage rates in the wake of the Federal Reserve’s historic rate-hiking campaign have taken home affordability to its lowest level in several decades. Buying a home is more expensive because of the added cost of financing the mortgage, and homeowners who previously locked in lower rates are reluctant to sell. The combination of low inventory and high costs has squeezed would-be homebuyers.

Rates have been above 6.5% since the end of May, and this week’s average rate matches the highest level since November.

“There is no doubt continued high rates will prolong affordability challenges longer than expected,” said Sam Khater, Freddie Mac’s chief economist. “However, upward pressure on rates is the product of a resilient economy with low unemployment and strong wage growth, which historically has kept purchase demand solid.”

The average mortgage rate is based on mortgage applications that Freddie Mac receives from thousands of lenders across the country. The survey includes only borrowers who put 20% down and have excellent credit.

All eyes on employment and inflation data

The rate stayed elevated this week after the Federal Reserve highlighted its reliance on jobs and inflation data in its July monetary policy meeting and in recent comments.

Markets had been waiting for July’s inflation report, released Thursday morning. That report showed inflation rose in July to 3.2% annually, compared to a 3% annual increase in June. That was the first time inflation picked up in a year. The data also showed that shelter costs contributed 90% of the total increase in inflation last month.

“July’s Consumer Price Index holds significant importance for the Fed’s upcoming decisions,” said Jiayi Xu, an economist at Realtor.com.

That faster pace of price increases could support the Fed’s concern that the battle is not over, Xu said. The Fed also will consider the forthcoming August employment and inflation data prior to the next policy meeting, in September.

In addition, the most recent jobs report offered some mixed signals about the labor market, Xu said, including a smaller number of net new jobs added and a dipping unemployment rate.

“While July’s jobs report itself is very unlikely to have a direct impact on the Fed’s upcoming decision, the decline to a 3.5% unemployment rate may imply that more significant slowing is needed to align with the Fed’s projected year-end rate of 4.1%,” she said.

Affordability challenges remain

Borrowing costs will remain elevated until financial markets see an “all clear” signal from the Federal Reserve, accompanied by a stop in interest rate hikes, said George Ratiu, chief economist at Keeping Current Matters, a real estate market insights and content company.

While the Fed does not set the interest rates that borrowers pay on mortgages directly, its actions influence them. Mortgage rates tend to track the yield on 10-year US Treasuries, which move based on a combination of anticipation about the Fed’s actions, what the Fed actually does and investors’ reactions. When Treasury yields go up, so do mortgage rates; when they go down, mortgage rates tend to follow.

Currently mortgage rates are running higher than they should be in relation to the 10-Year Treasury, given historical trends, he said. The spread between the 30-year fixed rate mortgage and the 10-year Treasury hovers around 300 basis points, Ratiu pointed out, a level seen only a handful of times in the past 50 years and mostly during periods of high inflation and economic turbulence.

“In the absence of the elevated risk premium and hewing closer to a historical average of 172 basis points, today’s 30-year fixed mortgage rate would be around 5.7%,” Ratiu said.

Homebuyers remain sensitive to elevated interest rates, with applications for mortgage rates dropping last week, according to the Mortgage Bankers Association.

“Due to these higher rates, there was a significant pullback in mortgage application activity,” said Bob Broeksmit, MBA president and CEO. “Both prospective buyers and sellers are feeling the squeeze of higher rates as well as low housing inventory, which has prompted a pronounced slowdown in activity this summer.”

While real estate markets are benefiting from more people gaining jobs and better paychecks this year, sales of existing homes have been lagging, said Ratiu.

“The challenge comes mainly from too many buyers chasing not enough available properties,” he said.

Looking to history as a guide, Ratiu said mortgage rates tend to start cooling once inflation abates, with a six-to-eight-month lag.

Shopping for a mortgage has never been easier, thanks to the array of online options. Brick and mortar lenders may still be a viable option, but you may find that an online lender has even more to offer.

Furthermore, exploring online mortgage lenders allows you to compare mortgage rates. You can also receive customized mortgage loan offers in your inbox in minutes. Even better, you’ll have direct access to a loan officer in case you have questions.

Who are the top online mortgage lenders for 2023?

If you’re in the market for a new home and ready to start your search for online lenders, here are some reputable options to choose from.

Best Online Mortgage Lenders of 2023

loanDepot

loanDepot is an online lender, but don’t think that means they are lacking in customer service. They provide over 150 loan stores across the country for customers that prefer in-person service.

The lender is a suitable option for anyone who wants to take out a mortgage with the assistance of a loan officer.

loanDepot offers various mortgage products, including fixed and adjustable-rate mortgages. You can also apply for jumbo loans, VA loans, and FHA loans. You’ll need a minimum credit score of 620 to qualify for a mortgage.

loanDepot ranks high in customer satisfaction and most buyers seem to have a good experience working with them. However, they do charge higher fees than other mortgage lenders.

Quicken Loans

This online lender takes the hassle out of securing a mortgage by letting you complete the entire process online.

You’ll need to provide a few key details about your finances using this form to get started. A Home Loan Expert will review your application and contact you to discuss loan options.

And no need to worry about getting overwhelmed. Quicken Loans offers online tools to help you understand loan options and the home buying process. Plus, the customer service is excellent; a live representative is always standing by.

You can also upload all your documents and monitor the status of your application directly from the portal. This means you never have to pick up the phone if you don’t want to.

And when you’re ready to close, you have the option to schedule the closing when it’s convenient for you.

Better.com

If you’re looking for an online mortgage lender, you should check out Better.com. The company uses technology to simplify the lending process for its customers. Better.com promises a fast and transparent mortgage experience.

The lender is willing to work with all different kinds of buyers, including individuals who are self-employed or have unique job situations.

At least a third of its mortgages are taken out by first-time homebuyers, and over 70% of all buyers pay a down payment that is less than 20%.

Better.com mortgages don’t come with any hidden fees; there are no application or origination fees. To get started, you can visit the company’s website and get pre-approved in just a few minutes.

Rocket Mortgage by Quicken Loans

Rocket Mortgage is a division of Quicken Loans. Their key competitive advantage is the asset importer tool, which takes the guesswork out of determining whether you’re approved.

Instead of uploading documents, importing them from the information provider guarantees the accuracy of the numbers and allows you to receive loan offers using real-time interest rates in a matter of minutes.

And once you’ve selected a loan that works for you or created a custom option, you’ll be able to close in record time. Plus, Rocket Mortgage customer service experts are standing by to assist with questions you may have every step of the way.

NBKC Bank

NBKC Bank is not as widely known as many of the other lenders on this list. But that doesn’t mean you should rule them out as a potential mortgage lender.

There are several features that make the Kansas City-based lender a great option. The bank promises fast home closings and provides exceptional customer service.

NBKC Bank focuses mostly on online mortgages and offers its customers competitive interest rates. It does have several brick-and-mortar locations but focuses mostly on processing online mortgages.

You’ll need a minimum credit score of 620 to qualify for a mortgage, so this is a suitable option for borrowers with fair credit. NBKC Bank offers various mortgage products, as well as personal accounts. This makes them a great option for anyone looking for a full-service lender.

Guaranteed Rate

You can apply for a mortgage in a matter of minutes from the homepage of this digital mortgage provider’s site.

All you have to do is answer a few questions about your desired home, credit, and finances to receive a comprehensive listing of loan types and interest rates you may qualify for.

Guaranteed Rate has plenty of no-down-payment loan options like VA loans and USDA loans. They also offer a knowledge center to help you understand mortgages and how the process works.

Once you decide on a mortgage product that best suits your needs, you’ll work directly with a loan expert to upload and sign documents and finalize the loan. If you prefer to meet with a loan expert, there are 170 Guaranteed Rate branches across the United States.

Truist

Truist is known for its brick-and-mortar presence, but they also have an impressive online mortgage platform. Available in English and Spanish, Truist mortgage offers an array of mortgage solutions to choose from.

You can initiate the application process online or directly from your mobile device through the SMARTGUIDE tool.

You can also call 877-907-1020 to speak with a loan officer or chat online from the website. Or if you wish to meet with a loan officer, use the locator tool to find a Truist branch near you.

You can also take advantage of their Doctor Loan program if you’re a medical professional and meet select income criteria.

SoFi Mortgage

SoFi mortgage is another online lender that stands out from the masses. Although they don’t offer government-backed home loans, SoFi mortgage has programs that require a down payment as low as 10 percent, and they do not assess mortgage insurance.

Customers also enjoy a seamless prequalification and application process, along with no origination fees. Even better, it may be possible to close on your loan in under 30 days.

Penny Mac

If you’re searching for flexibility, Penny Mac may be the ideal lender for you. They offer several options to consumers of varying financial backgrounds. To date, they’ve served over 1 million customers and funded over $5 billion in loans in 2017, alone.

You can request a no-obligation free quote online, chat with an expert, or call (888)870-6229 to get started.

Reali

Crediful’s rating

Reali caters to consumers looking to purchase or refinance their homes. Through their Interactive Loan Dashboard, you can apply, upload any documents needed, and track your loan’s progress at the tap of a fingertip.

You’ll also have access to a Home Loan Advisor 24/7 to address any concerns you may have. And because of their streamlined process and low fees, you can expect to close in record time without spending a fortune.

Unfortunately, Reali does not offer government-backed products, like FHA loans, USDA loans, and VA loans.

This can be a turnoff to first-time, credit-challenged, or cash-strapped buyers.

Another major drawback is that they only operate in Arizona, California, Colorado, Florida, Georgia, Illinois, Michigan, Oregon, Pennsylvania, Texas, Virginia, and Washington.

The good news is they plan to expand their offerings to more states soon.

Pros and Cons of Online Mortgage Lenders

The rise of the internet has revolutionized many industries, and the mortgage industry is no exception. Online mortgage lenders have steadily been gaining a more substantial market share due to their distinct advantages. However, as with anything, they come with their own set of disadvantages. Here, we break down the pros and cons of opting for an online mortgage lender.

Pros of Online Mortgage Lenders

1. Lower Costs: Operating primarily online, these lenders often have fewer overhead costs compared to traditional brick and mortar lenders. This can translate into competitive mortgage rates and lower lender fees, making online mortgage lenders potentially cheaper.

2. Convenience: The ability to initiate and complete the entire application process online is a significant advantage. You don’t have to schedule meetings with a loan officer or travel to a bank branch. Instead, you can apply anytime, anywhere, which fits well with busy schedules and modern, on-the-go lifestyles.

3. Range of Loan Products: Online mortgage lenders often offer a broad range of loan products, including FHA and VA loans, USDA loans for rural properties, conventional loans, and jumbo mortgages. These lenders often cater to a diverse demographic, meaning whether you’re a first-time homebuyer seeking down payment assistance, a veteran, or someone with less-than-perfect credit, you can often find an online mortgage product that suits your needs.

Cons of Online Mortgage Lenders

1. Technological Hurdles: Not everyone is tech-savvy. If you’re not comfortable navigating online platforms or don’t have reliable internet access, you may find the online mortgage process daunting. The learning curve associated with digital platforms can be a deterrent for some people.

2. Lack of Personal Interaction: Some people prefer a high-touch, personalized service when dealing with significant transactions like buying a home. With online lenders, face-to-face interaction is usually minimal or non-existent, which can be a downside for those who prefer a more traditional approach to their financial transactions.

3. Negotiability of Fees: While online mortgage lenders are often cheaper, certain costs like origination fees and closing costs may not be as negotiable as they could be with a traditional lender. Also, mortgage insurance may still be required for government-backed loans, like FHA or VA loans, and the requirements for jumbo loans may be stricter.

4. Trustworthiness: The online space can be a breeding ground for scams and unscrupulous practices. Not all online mortgage lenders are trustworthy, making it crucial to do your homework. It’s important to research each online lender thoroughly, checking their reputation, reading customer reviews, and ensuring they are registered with appropriate financial oversight institutions.

Despite these potential downsides, many homebuyers find that the convenience, competitive rates, and the ability to shop around from multiple lenders offered by online mortgage lenders outweigh the cons. But the best online mortgage lender for you ultimately depends on your personal finance needs, comfort level with technology, and unique home loan situation.

Factors to Consider when Choosing an Online Mortgage Lender

Finding the right online mortgage lender for your home-buying journey involves more than just hunting for the lowest interest rate. You need to consider a variety of factors, from loan types to the speed of loan processing. Here’s a breakdown of what to look for:

Interest Rates

As a prospective borrower, interest rates are often one of your first considerations. The interest rate can significantly influence your monthly mortgage payment and the total cost of your loan. Due to their lower overhead costs, online mortgage lenders often advertise competitive rates. However, it’s essential to compare rates across different lenders to ensure you’re getting the best deal.

Fees and Hidden Charges

While interest rates play a crucial role in determining your loan cost, it’s equally important to consider fees and potential hidden charges. This could include origination fees, appraisal fees, closing costs, and other service charges. Some lenders may also charge additional fees for rate locks or early repayments. Always ask for a comprehensive cost breakdown and be wary of lenders who are not transparent about their charges.

Loan Types

Each online mortgage lender may offer a variety of loan types, such as FHA loans, VA loans, conventional loans, and more. Depending on your personal circumstances and needs, you might need specific loan products like USDA loans for rural properties, FHA or VA loans for a low down payment, or jumbo loans for larger properties. Ensure that the lender you choose caters to the type of loan that suits your situation best.

Customer Service and Support

Excellent customer service is crucial when dealing with online lenders as your primary communication methods will be via phone, email, or online chats. Lenders who offer high-quality customer service can significantly streamline the mortgage process, making it less stressful for you. Consider checking customer reviews and ratings for insights into a lender’s customer support.

Speed of Loan Processing

The time it takes for online mortgage lenders to process your loan application and close your loan can vary. If you’re working within a specific timeframe, you may prefer a lender known for quick processing. This is particularly crucial in competitive real estate markets, where being able to close swiftly could make all the difference.

Pre-approval Process

A seamless pre-approval process can signify an efficient online mortgage lender. Pre-approval offers you a rough estimate of how much you can borrow and helps you stand out in competitive property markets. Seek lenders that provide easy pre-approvals, preferably with only a soft credit check to avoid impacting your credit score.

User-friendly Technology

With most of your interaction with online lenders taking place digitally, user-friendly technology becomes paramount. Consider factors such as the simplicity of the application process, online document upload functionality, digital signature capabilities, and the ease of online loan tracking. A lender with a robust, intuitive platform can significantly simplify your online mortgage process.

Tips for Applying for a Mortgage Online

Embarking on the journey of applying for a mortgage online can feel overwhelming, especially if it’s your first time. But don’t worry – we’ve got some helpful tips to guide you through the process.

How to Prepare

Before you start your online mortgage application, it’s important to get your financial house in order. Here’s how:

Check your credit score: Your credit score is one of the main factors that lenders consider when evaluating your loan application. Make sure to check your credit reports for any errors and dispute them if needed. If your score is low, you might want to consider improving it before applying for a mortgage.

Verify your income: You will need to provide proof of income, so gather your recent pay stubs, W-2s, or tax returns. If you’re self-employed, you may need to provide additional documentation, like bank statements or profit and loss statements.

Get your documents in order: Apart from income verification, you’ll need other documentation, like identification, proof of assets, and information about your debts. Having these documents ready can speed up the application process.

Navigating the Application Process

Once you’re ready to apply, keep the following in mind:

Understand the terms: Make sure you understand the terms of the mortgage, like the interest rate, whether it’s fixed or adjustable, the length of the loan, and any fees involved.

Use online tools: Many online lenders offer useful tools like mortgage calculators. These can help you understand what your monthly payments might be based on different interest rates and down payment amounts.

Stay organized: Keep track of where you are in the application process. Most online platforms will save your progress, but it’s good to have your own record too.

Questions to Ask Your Lender

Securing a mortgage can often feel like a daunting process, particularly when applying online. To navigate this path with more confidence, it’s crucial to arm yourself with the right questions when engaging with potential lenders. The responses to these questions will not only give you a clearer idea about the mortgage terms but also about the lender’s transparency and commitment to customer service.

What types of loans do you offer?

The world of mortgages encompasses a variety of loan types designed to cater to different borrower needs. This includes conventional loans, government-backed loans such as FHA, VA, and USDA loans, and jumbo loans for larger mortgages.

Understanding the unique benefits and requirements of each type is important. For example, FHA loans may be suitable for those with lower credit scores, while VA loans are primarily designed for veterans. Your potential lender should be able to provide a comprehensive explanation of each option and help guide you towards the loan type that best fits your unique situation.

What are the interest rates and APR?

While the interest rate of a loan often takes center stage, the Annual Percentage Rate (APR) should not be overlooked. The APR provides a more comprehensive measure of cost as it includes the interest rate, lender fees, and other loan charges, offering a more complete picture of the long-term cost of the loan.

What fees are involved?

Beyond the interest rate, mortgages often involve several other fees that can impact the overall cost of the loan. These include origination fees, appraisal fees, home inspection fees, and potentially prepayment penalties. Some lenders may even charge for rate locks, which secure your interest rate for a specified period. It’s critical to ask for a detailed breakdown of all fees involved to ensure that there are no hidden costs that might surprise you down the line.

What Is the estimated timeline for approval and closing?

Mortgage approval and closing timelines can vary greatly among different lenders. Knowing the expected timeline can be crucial, especially if you’re working with a specific move-in date. In a competitive real estate market, a quick approval and closing process could make all the difference when multiple offers are being considered.

What are your minimum credit score and down payment requirements?

Understanding a lender’s minimum credit score and down payment requirements can help you gauge your chances of approval. These requirements can vary greatly depending on the loan type and the individual lender’s policies.

Do you consider alternative credit data?

For those with a limited credit history, some lenders may consider alternative credit data such as utility bill payments or rent payment history. Asking about these possibilities could potentially help you qualify for a loan even with less conventional credit information.

What is your process for loan servicing?

Understanding whether the lender will service your loan or if they intend to sell it to another company is important. If they plan to sell it, knowing who your point of contact would be for any issues or inquiries is crucial.

Bottom Line

Choosing an online mortgage lender is a significant decision that can impact your financial situation for years to come. Therefore, it’s critical to take the time to carefully evaluate each lender. From comparing interest rates to analyzing the type of customer service they offer, there are many factors to consider in this selection process.

We’ve touched upon some of the best online mortgage lenders available today. These lenders were chosen based on their competitive rates, comprehensive loan options, excellent customer service, and user-friendly platforms. However, remember that the “best” lender will vary depending on individual circumstances, and the top choices for others might not be the best for you.

While online mortgage lenders offer convenience and often competitive rates, they also come with their unique set of challenges. It’s vital to remember that transparency, trustworthiness, and a clear understanding of the terms and conditions are paramount in any financial decision, including choosing a mortgage lender.

We encourage you to conduct your own research and take advantage of online tools and resources that many of these lenders offer. Shopping around and comparing multiple lenders will help you find the best mortgage fit for your specific needs.

Remember, a mortgage is a long-term commitment. The time and effort spent in making a careful, well-researched decision now will pay dividends over the life of your loan. Happy home hunting!

When the housing market was searing hot, buyers faced intense competition — bidding wars, cash investors, and buy/sell decisions made on rapid deadlines. Now that real estate has cooled, there are fewer homes for sale, two-decade-high interest rates, and stubbornly elevated house values.

It’s rarely easy to buy a home. And if you can find a house you love, the question becomes: Is now a good time to buy?

The 2023 housing market

Looking for the perfect time to buy? Fewer than one in five consumers surveyed by Fannie Mae in July 2023 thought that it was a good time to buy a home. Yet, timing the housing market is more complicated than timing the stock market. Which is impossible. There are few “just right” Goldilocks real estate markets.

But you’re not buying the market. You’re buying a house in a city, neighborhood, and block where you want to live. Hopefully, for quite a while.

Mortgage rates

We all know this story. Interest rates have risen — and mortgage rates are no exception. The Federal Reserve has been raising short-term interest rates for well over a year in an effort to shrink inflation — the rise in consumer prices. Not only do the Fed’s rate increases immediately lift short-term mortgage rates such as variable-rate loans, but they also tend to influence long-term mortgage rates upwards as well eventually.

And though we don’t live in a 2%-3% world these days, mortgage rates are near their 52-year historical average.

Since April 1971, the 30-year mortgage rate has averaged 7.74%, based on data collected by Freddie Mac.

Of course, that’s little comfort to homebuyers today who remember when rates were under 3% for much of 2021. Conversely, the highest rate on record was a whopping 18.63% in October 1981.

According to Zillow research, the trend of mortgage rates — whether interest rates are generally rising or falling — may influence whether existing homeowners would consider selling their existing house to move into another. With so many existing homeowners paying a much lower mortgage rate, the study found it would take rates to fall somewhere to between 4% and 5% before they would sell the home they’re in and buy another.

This rate gridlock is contributing to the lack of existing homes for sale.

Take action: Consider the interest rate strategies below until (and if) mortgage rates fall significantly lower for an opportunity to refinance.

Home values

There is a little good news, though. Higher mortgage rates have softened the real estate market, and the increase in home prices is moderating.

The rise in existing home values is slowing. Home values are lower year-over-year in almost half (23) of the 50 largest metro areas, according to a Zillow analysis.

Take action: Look for homes with price reductions where you want to live. Then negotiate even harder.

But listings for existing homes are far fewer. For more than 12 months, new listings have been down year-over-year. The number of new listings of homes for sale is down more than 20% from pre-pandemic levels, according to Realtor.com.

Take action: Consider expanding your search to more affordable areas close to your favorite neighborhood if it’s too pricey.

New home inventory is rising. Construction of new homes is showing promise of growth, according to the U.S. Census Bureau. However, builders are still wary of oversupplying the market, concerned that consumer demand could sag as potential buyers shy away from rising mortgage rates.

Take action: If you want to buy a house now, consider new construction. You may be able to choose some finishes or make an even better deal on a spec home that’s been on the market for a while.

When is a good time to buy a house?

Buying a home is more than considering macroeconomic factors. It’s an important life decision based on your personal and financial situation.

Where do you want to be in 5 years?

When you rent, the decision to move is broken down into six months, or a year or two at a time, as your lease renews. But every dollar-related detail makes a home purchase a medium- to long-term investment. Buying a house includes various costs: the down payment, closing costs, and financing fees, moving expenses, property taxes, and perhaps selling your existing place.

Homeownership requires a years-long timeline. How you make a living, your friends, family, and even community amenities all come into play.

Your income

A primary consideration: your job. Will it require a location change anytime soon, or can you live where you please? Is your income steady and all but assured?

Your credit score

One of the significant factors that will qualify you for a home loan is your credit score. It’s important to know it before applying for a mortgage.

For the most common loan, a conventional mortgage not backed by a government agency, you generally need a FICO score of 620 or better.

FHA loans can allow a credit score as low as 580 with 3.5% down. VA loans issued to qualified military service members and veterans don’t officially have a minimum credit score, though some lenders will require a FICO score of 620.

As a benchmark to where you stand, the median credit score on a new mortgage in the second quarter of 2023 was 769, according to the New York Federal Reserve.

Of course, minimum scores are the entry-level to qualifying; the higher your score, the better the loan terms you’ll be offered. Most importantly, that can mean you’ll pay a lower annual percentage rate over the life of the loan. You may also have more room to negotiate on fees.

Your current debt load

A primary financial metric lenders will use to determine your creditworthiness is your debt-to-income ratio.

Fannie Mae, a government-sponsored entity that provides liquidity to the home loan market, looks for a maximum total DTI ratio of 36% of “the borrower’s stable monthly income.” Exceptions can allow for total DTIs up to 50%, but it’s usually best to avoid working on the edges of qualification if you can.

You can calculate your DTI by dividing your total recurring monthly debt by your gross (before taxes and other deductions) monthly income.

Include debt such as monthly mortgage payments (or rent), real estate taxes, and homeowner’s insurance. Also, add any car payments, student loans, and the monthly minimum due on credit cards. Remember any personal loan payments and child support or alimony.

Do not include debt such as monthly utilities — like electricity, water, garbage, or gas bills — or car insurance, television streaming subscriptions, or cell phone bills. You can also exclude health insurance costs and miscellaneous expenses such as groceries or entertainment.

Your savings

Having a cash cushion in the form of emergency savings shows lenders that you are prepared for the unexpected. Of course, that savings account should also include …

Your down payment

A large chunk of your savings account should be dedicated to the down payment. A minimum of 3% down is required in order to qualify for a conventional loan targeted to first-time homebuyers — or ideally, 20% to avoid private mortgage insurance. Yes, zero-down options exist if you are eligible for a VA- or USDA-backed loan.

According to Realtor.com, the average down payment in the first quarter of 2023 was 13%.

4 rate-relief strategies to consider

Buying a house when interest rates are high can require some financial finesse to enhance affordability.

1. Buying discount points

Prepaying interest in order to lower your ongoing mortgage rate is called buying discount points. One point is equal to 1% of the loan amount. However, lenders sometimes add a point or two to a mortgage proposal to make their loan offer appear more enticing. But you’re actually paying for the discount with an upfront fee.

When shopping for a loan, compare loan offers with zero points. Then, you can decide whether to buy points to lower your interest rate. It is important to note that buying one point (paying 1% of the loan amount upfront) will generally reduce your interest rate by only one-quarter of a percentage point.

2. An interest rate buydown

Borrowers can lower their mortgage interest rate for the first few years at the beginning of the loan term with a buydown. Home builders, sellers, and some lenders sometimes offer an interest rate buydown to boost sales.

While you get a short-term break on the interest rate, your payments and total interest may actually be higher. It’s a strategy that requires running the numbers on the long-term benefits.

If you’re paying for the buydown, compare a mortgage both with and without a buydown. By the way, lenders will qualify you based on the permanent interest rate, not the temporary buydown rate.

3.An adjustable-rate mortgage

A mortgage product that increases in popularity whenever rates begin to rise is back: the adjustable-rate mortgage.

ARMs have a fixed interest rate for an introductory period, often five to 10 years, and then the rate changes regularly, usually once or twice a year. Tips when shopping for an ARM:

Look for an introductory rate that is lower than a fixed-rate mortgage.

Choose a term you feel comfortable with, perhaps in line with how long you plan to stay in the home.

Make sure you budget for possible increases in your monthly payment if the interest rate moves higher after the end of the introductory rate period.

4. A shorter-term mortgage

Are you more comfortable with an interest rate that never changes, even if your monthly payment is slightly higher than you’d like? Consider a shorter-term loan. Mortgages with 20- or 15-year fixed terms, as opposed to the traditional 30-year term, typically come with lower interest rates. The lower rate and shorter term combination means you’ll gain equity in your home faster, too.

Your next move

Buy smart and shop a lot. Relentlessly shop mortgage rates and lenders for the best loan offers and justified fees. Get a written preapproval from your lender, then shop for a house you can love and can afford. Your home buying competition is.

According to Zillow, when it comes to first-time buyers versus repeat buyers, first-timers are more likely to reach out to at least three lenders and three real estate agents.

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

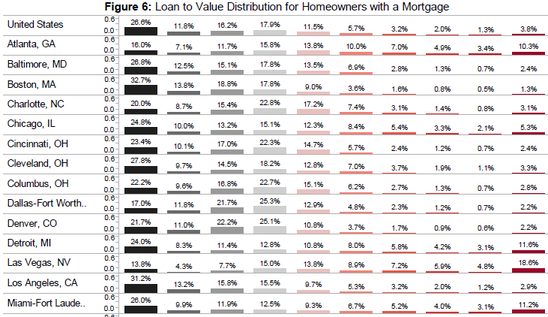

While the good news about housing keeps flooding in, one piece of negative data jumped out at me today.

The latest Zillow Negative Equity Report released today revealed that nearly one out of every five (18.6%) Las Vegas homeowners with a mortgage owed double what their home was worth as of the end of the fourth quarter.

In other words, if their home’s present value is $100,000, their mortgage balance is somewhere around $200,000.

For most people, this would signal being past the point of no return. After all, most of us have enough trouble paying off a mortgage when we’re above water, so the thought of owing double is daunting, even with a kick-butt mortgage rate.

Of course, if you stick around long enough, home price appreciation should do some of the heavy lifting, but it’s still a big ask for struggling homeowners.

While I cherry-picked a bad piece of data, it should be noted that 26.7% of Vegas homeowners were in this position one year earlier, so it’s not nearly as bad as it was.

And only 8.9% of underwater homeowners are delinquent on their mortgage payments, down from 9.9% a year earlier.

So yes, things are getting better…at the same time, the 200%+ loan-to-value (LTV) ratio bracket was the most prominent in Sin City.

In other words, if you went door to door and asked Vegas homeowners with mortgages what their LTV was, most would say 200%+.

The second largest distribution for Vegas homeowners was the 80-100% LTV tier (15% of borrowers), followed by the 100-120% LTV tier and under 40% tier, both at 13.8%.

3.8% of American Mortgagors Owe More Than Double Home’s Worth

If we expand the data to the whole of the United States, 3.8% of Americans with mortgages owed more than double what their homes were worth at the end of 2012.

That’s pretty scary, though the majority of U.S. homeowners with mortgages (26.6%) have LTV ratios south of 40%.

And 72.5% have a LTV somewhere below 100%, meaning they’re not the proud owners of an underwater mortgage.

If you look at the graphic below, you’ll notice that the LTV distribution is improving in every category, thanks to continued home price appreciation.

The low-LTV brackets are rising, and the high-LTV brackets are declining. All good news…