Has a friend or family member asked you for a loan? This can be a difficult situation. On one hand, you likely want to help them out. On the other hand, you don’t want to be out the money or put a strain on the relationship. The trick is to know how to loan money the right way.

Before you agree to loan any money to a friend or family member, think about how reliable they are. Can you depend on them to repay the money? Secondly, you might want to ask them what they need the money for and why they can’t take out a personal loan. The answers to these questions might provide some clues as to whether you should lend them money or not.

For instance, if they need the money because they’re past due on bills, this could be a sign that they may not have the funds to repay the loan. If they can’t secure a loan due to bad credit, they may not be very reliable. However, if they simply have limited credit due to their age or other factors, it might not be an indicator.

If you decide lending money to your friend or family member is the right option for you, keep reading for tips to make the process as seamless as possible.

How to Loan Money: Lending Money vs. Cosigning a Loan

If you can choose between lending money and cosigning a loan, lending money is probably the best option. When you lend money, you can do so on your terms. You determine the amount of money, payment terms, and interest rates. By cosigning a loan, you’re stuck with the terms and conditions of that loan.

However, that’s not the major problem with cosigning a loan. The biggest issue is that if your friend or family member decides to stop paying on the loan, you’re responsible for paying the balance due. Additionally, your credit could be significantly impacted, especially if your loved one fails to make on-time payments and doesn’t tell you.

Get matched with a personal

loan that’s right for you today.

Learn

more

Alternative Lending Option

Before you hand over any money, you might want to encourage your loved one to apply for a personal loan with bad credit. Help them determine what their credit score is so they can decide if applying for this type of loan is a viable solution.

Credit.com’s Free Credit Report Card can be a good source for this information. This report card provides a free credit score, along with notes on what you can do to improve your scores. For example, you can raise a credit score by paying down high credit card balances, disputing credit report errors, and using a starter line of credit, like a secured credit card or credit-builder loan, to establish a solid payment history.

Keep in mind that loans for those with bad credit often come with higher-than-average interest rates. However, making on-time payments can help them start building their credit.

What’s the Smart Way to Loan Money?

If you’re willing to lend money to a loved one, there are a few things you should keep in mind, including getting everything in writing and setting a firm payment schedule. These steps can protect you if you go to court.

Here are three tips to keep in mind when considering how to loan money.

1. Get It in Writing

While you may be dealing with friends or family members, loaning them money is still a business deal. Make sure to get all the terms of the loan in writing. This will prevent any confusion and provide you with the necessary evidence if you need to go to court to collect the money.

If your loved one is borrowing a small amount, you can probably write the details of the loan agreement on a piece of paper that all involved parties sign. Be sure to include the total amount due and any added fees, such as late payment fees or interest.

For larger sums of money, you may want to have your attorney draw up a formal contract for all parties to sign.

2. Set Fair Interest Rates

You might be a little hesitant to charge interest on the loan. However, this may be the only way to protect yourself from paying gift tax. Being able to prove you’re charging interest can help you show the IRS that it’s a loan and not a gift. This factor is especially important when lending larger amounts of money.

When deciding how much interest to charge, you want to be fair to both yourself and your friend or family member. Be sure to set an interest rate that’s higher than the amount you could have earned having the money sit in your bank account. On the other hand, you may not want to charge as much as standard lenders.

The best option is to talk to your friend or family member to negotiate a deal.

3. Create a Clear Payment Schedule

Don’t make the mistake of telling your loved one to pay you back whenever they can. This leaves the payment terms up in the air. Plus, your friend or family member may never feel financially able to repay their debt.

Instead, create a clear payment schedule that states exactly how much is due and at what intervals. For example, you can create a schedule that requires them to pay $100 on the first of each month until the debt is paid in full. You should also detail what forms of payment you can accept, including cash, money order, check, or PayPal.

It’s a good idea to start a journal that tracks the exact date and amount of each payment. It’s important to always list additional fees, such as late payment fees, separately. You should also provide your friend or family member with a receipt for each payment made.

Lending money to your friends or family members can be a viable option if you have the funds to spare and trust the person borrowing the money. But don’t go into this type of agreement without getting everything in writing. Instead, follow the above tips on how to loan money.

If you decide not to lend money to your loved one, encourage them to take steps to improve their credit, such as signing up for Credit.com’s ExtraCredit® credit monitoring subscription to see 28 of their credit scores and what factors are affecting it most. This way, they’ll be able to work on the areas affecting their credit to better be able to secure the funds they need in the future.

A security is any financial instrument with a fungible value (meaning a value that’s essentially equal) that investors can trade. Common securities include stocks, bonds, and index and mutual funds, as well as options and other derivatives that derive their value from other assets. Most securities trade on financial exchanges, and all play a role in aiming to build wealth for individuals, companies, and other investors.

What are securities in finance and how do they work? Here’s a glimpse inside the world of securities in trading.

What is a Security?

A security is a tradable investment vehicle that traders can buy and sell on financial exchanges or other platforms. In general, investors earn money by buying securities at a low price and selling them at a higher one.

Securities in finance have some monetary value; buyers and sellers determine their value when trading them. Securities vary in nature – stocks, for example, represent ownership in a company, while bonds are essentially loan vehicles where borrowers pay lenders interest for their loan money.

Here are some common security categories.

Equity Securities

This type of securities in finance includes stocks and stock funds. Typically traded on exchanges, the price of equity securities rise or fall depending on the economy, the performance of the underlying company that offers the stock (or companies in the fund), and the sector that company or fund operates. Individual stocks may also pay dividends to investors who own them. 💡 Quick Tip: Investment fees are assessed in different ways, including trading costs, account management fees, and possibly broker commissions. When you set up an investment account, be sure to get the exact breakdown of your “all-in costs” so you know what you’re paying.

Debt Securities

This group includes bonds and other fixed-income vehicles where lenders borrow money from investors and pay an interest rate (i.e., the price for borrowing) on the investment principal. Bond issuers may include states, local and municipal governments, companies, and banks and other financial institutions. Typically, debt securities pay investors a specific interest rate paid usually twice per year until a maturity date, when the bond expires.

Some common debt securities include:

• Treasury bills. Issued by the U.S. government, T-Bills are considered among the safest securities.

• Corporate bonds. These are bonds issued by companies to raise money without going to the equity markets.

• Bond funds. These allow investors to get exposure to the bond market without buying individual bonds.

Derivatives

This group of securities includes higher-risk investments like options trading and futures which offer investors a higher rate of return but at a higher level of risk.

Derivatives are based on underlying assets, and it’s the performance of those assets that drive derivative security investment returns. For example, an investor can buy a call option based on 100 shares of ABC stock, at a specific price and at a specific time before the option contract expires. If ABC stock declines during that contract period, the call option buyer has the right to buy the stock at a reduced rate, thus locking in gains when the stock price rises again.

Derivatives allow investors to place higher-risk bets on stocks, bonds, and commodities like oil or gold, and currencies. Typically, institutional investors, such as pension funds or hedge funds, are more active in the derivative market than individual investors.

Hybrid Securities

A hybrid security combines two or more distinct investment securities into one security. For example, a convertible bond is a debt security, due to its fixed income component, but also has characteristics of a stock, since it’s convertible.

Hybrid securities sometimes act like debt securities, as when they provide investors with a floating or fixed rate of return, as bonds normally do. Hybrid securities, however, may also pay dividends like stocks and offer unique tax advantages of both stocks and bonds. 💡 Quick Tip: How to manage potential risk factors in a self-directed investment account? Doing your research and employing strategies like dollar-cost averaging and diversification may help mitigate financial risk when trading stocks.

How Security Trading Works

Securities often trade in open financial exchanges where investors can buy or sell securities with the goal of making a financial profit.

Stocks, for example, are listed on global stock exchanges and investors can purchase them during market trading hours. Exchanges are highly regulated and expected to comply with strict fair-trading mandates. For example, U.S.-based stock exchanges like the New York Stock Exchange or Nasdaq must adhere to the rules and regulations laid out by Congress and enforced by the U.S. Securities and Exchange Commission (SEC).

Each country has their own rules and regulations for fair and compliant securities trading, including oversight of stocks, bonds, derivatives, and other investment vehicles. Debt instruments, like bonds, usually trade on secondary markets while stocks and derivatives are traded on stock exchanges.

There are many ways for investors to engage in security trading. A few of the most common ones include:

Brokerage Accounts

Once an investor opens a brokerage account with a credentialed investment firm, they can start trading securities.

All a stock or bond investor has to do is fill out the required forms and deposit money to fund their investments. Investors looking to invest in higher-risk derivatives like options, futures, or currencies may have to fill out additional documentation proving their credentials as educated, experienced investors. They may also have to make larger cash deposits, as trading in derivatives is more complex and has more potential for risk.

Some investors with brokerage accounts can engage in margin trading, meaning that they trade securities using money borrowed from the broker.

Retirement Accounts

By opening a retirement account, through work or a bank or brokerage account, investors can invest in a range of securities, including stocks, mutual and index funds, bonds and bond funds, and annuities.

The type of securities you have access to will depend on the type of retirement account that you have. Workplace plans such as 401(k)s typically have fewer investment choices (but higher limits for tax-advantaged contributions) than Individual Retirement Accounts.

The Takeaway

There are many different types of securities that investors may purchase as part of their portfolio. Choosing which securities to invest in will depend on several factors, including your financial goals, current financial picture, and risk tolerance.

A great way to start building a portfolio of securities is by opening a brokerage account on the SoFi Invest® investment platform. Securities on the platform include stocks and exchange-traded funds.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

What are the four types of securities?

The four types of securities are: equity securities (such as stocks), debt securities (such as bonds), derivatives (such as higher-risk investments like options trading), and hybrid securities (such as convertible bonds).

What is a securities investment?

A securities investment is an investment in a security such as stocks, bonds, or derivatives. A security is a tradable type of investment that traders can buy and sell.

What’s the difference between securities and shares?

Stocks, also known as equity shares, are a type of security. The term “securities” refers to a range of different investments, one of which is stocks, or shares.

Photo credit: iStock/paulaphoto

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi Invest® SoFi Invest refers to the two investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser (“SoFi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC.

2) Active Investing and brokerage services are provided by SoFi Securities LLC, Member FINRA(www.finra.org)/SIPC(www.sipc.org). Clearing and custody of all securities are provided by APEX Clearing Corporation.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of SoFi Digital Assets, LLC, please visit SoFi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Bank, N.A.

A guaranteed mortgage loan gives lenders the ability to qualify borrowers with looser eligibility requirements, allowing for lower credit scores, higher debt loads and more.

Many mortgages with less than 20 percent down are made possible by a guarantee.

The funds for guaranteed mortgages come from private-sector lenders, but the loan is backed by a guarantor, typically a government agency, that will pay out money to the lender if the borrower defaults.

Guaranteed loans are a critical part of the mortgage marketplace, offering borrowers more flexible qualifying terms. These loans are backed by a third party, most often the U.S. government, who agrees to cover a portion of the loan if the borrower defaults.

What is a guaranteed mortgage?

Guaranteed loans require a lower down payment percentage or no down payment at all, and can have lower credit score requirements.

A guaranteed loan is any loan that’s backed by a party other than the lender. That third party assumes some of the responsibility for the loan to the benefit of the lender. If the borrower stops repaying the loan, or defaults, the guarantor pays the lender some or all of the outstanding debt.

How guaranteed mortgages work

With a guaranteed mortgage, the third party guarantees, or agrees to be responsible for, some or all of the loan if the borrower defaults. The guarantor might extend the guarantee to all or a portion of the loan. The guarantee protects the lender, not the borrower.

Ultimately, the guarantee allows the lender to more confidently qualify a borrower who isn’t making a substantial down payment or otherwise might present more risk, such as having a lower credit score.

8%

The typical down payment for first-time homebuyers in 2022

Source:

National Association of Realtors

Guaranteed loans are most often backed by the U.S. government, namely the Federal Housing Administration (FHA) and the Department of Veterans Affairs (VA), which back FHA loans and VA loans, respectively. The Department of Agriculture also guarantees USDA loans in eligible areas.

One point of distinction: The VA loan program is generally considered a “guarantee,” while the FHA loan program is viewed more as “insurance.” From the borrower and lender’s perspective, however, they each provide third-party backing that helps borrowers qualify for a loan.

Despite the lower down payment, a guaranteed mortgage loan must meet underwriting standards established by the lender and the third party. Lenders often have additional requirements beyond what the guarantor mandates, a practice known as “overlaying.” For instance, the FHA requires a minimum credit score of 580 to allow a borrower to put just 3.5 percent down, but some lenders set the minimum higher, at 620.

Guaranteed vs. non-guaranteed loans

The main difference between guaranteed and non-guaranteed loans comes down to qualifying for the loan. Specifically, a guaranteed mortgage loan means:

Looser eligibility requirements: Because the third party promises to step in if you can’t or don’t repay what you borrow, the lender has a security net. As a result, lenders generally extend looser qualification requirements for a guaranteed mortgage loan — from credit score to income — than with a non-guaranteed loan.

Lower down payment: A guarantee for a home loan often incentivizes lenders to accept a larger loan-to-value (LTV) ratio, allowing for a smaller down payment — or potentially none at all, if you’re eligible for a VA loan.

More favorable rates and terms: Exploring a guaranteed mortgage might help you land a lower interest rate or terms that are otherwise more favorable.

Restrictions on use cases: Depending on the guarantor, you might be limited in how you can use the loan. You can only get a USDA loan, for example, if you purchase a home in a qualifying rural area.

Additional costs: While the guarantee provides protection for the lender, the guarantor might require you to pay into the pot. For example, with an FHA loan, you’ll need to pay for mortgage insurance.

Types of guaranteed home loans

FHA loans

The FHA loan program is popular for several reasons:

Borrowers can purchase with as little as 3.5 percent down, provided they have a credit score of 580 or better. For borrowers with a credit score between 500 and 579, the program requires 10 percent upfront.

Borrowers can qualify with a 43 percent debt-to-income ratio (DTI); however, a large portion actually qualify with a higher DTI ratio, sometimes over 50 percent. This is due to “compensating factors,” such as cash reserves or a higher credit score, that augment a borrower’s creditworthiness.

FHA interest rates are sometimes lower than those of conventional loans, which aren’t guaranteed or insured by the government.

However, if you choose this kind of mortgage guarantee, be ready to pay two insurance premiums: one premium paid upfront that’s equal to 1.75 percent of the loan principal and an annual premium ranging from 0.15 percent to 0.75 percent of the balance, paid monthly. In some cases (depending on the size of your down payment), the mortgage insurance goes away after 11 years. Otherwise, the annual premium can’t be removed unless you refinance to a different type of loan or pay off your FHA loan completely.

VA loans

VA loans are available to eligible active-duty servicemembers, veterans and surviving spouses to help finance or refinance a home with zero down — a benefit that can be used more than once. The VA guarantee for a home loan promises a certain amount to a lender should a VA loan borrower default.

VA loans give borrowers and lenders a lot of leeway. For example, VA guidelines don’t include minimum credit score standards or loan limits. Instead, lenders set their own credit score requirements and loan money to the extent the borrower is financially qualified.

VA loans also have a residual income standard that helps lenders determine how much a borrower needs, after expenses, to qualify for a loan.

When purchasing or refinancing, VA loan borrowers have to pay an upfront funding fee, although the fee can be waived under certain circumstances.

USDA loans

USDA loans are also available to lower- and moderate-income borrowers with no money down, but only in defined rural areas. (The term “rural” can be surprisingly broad, so check your area to find out if it qualifies.)

A USDA loan has both an upfront and annual fee, which are a percentage of the loan principal, in order to sustain the guarantee from the USDA. These fees are charged to the lender but usually passed on as a cost to the borrower.

Is a guaranteed loan right for you?

With guaranteed loans, more borrowers can qualify for mortgages. With that guarantee, a lender might extend looser LTV and DTI ratios, along with lower credit score and income thresholds. The guarantee might also translate to more favorable loan terms, like a lower interest rate — but also means paying additional costs, such as mortgage insurance or fees.

A loan officer can help you determine which option is right for you and what you’re likely to be preapproved for based on your credit and financial situation.

Life is expensive and paying for rent can take up a significant chunk of your paycheck. In an ideal world, 30 percent of your income should go towards rent and housing costs. But life happens and you may come up short on rent due to loss of income or other unexpected expenses, leaving you wondering if you should take out a loan to pay rent. Coming up short on your rent payment is an extremely stressful situation and you’ll be looking for ways to make your rental payment and avoid eviction.

If you find yourself in this situation, what do you do? There are several options to weigh and taking out a loan to pay rent is one of them. Let’s walk through the pros and cons of rent loans and discuss several options you can consider if you’re behind on rent payments.

Is it possible to take out a loan to pay for rent?

If you get behind on rent payments, you’re not alone. In fact, more than 7 million renter-occupied households are behind on just last month’s rent alone. So, what are your options and is it possible to take out a loan to pay for rent? The short answer is yes, you can.

Using a loan to pay rent is an option. You can obtain a personal loan to pay rent and for some people, it’s a good idea. However, before you take out rent loans, you need to consider if it’s the right choice for you.

Pros of using a personal loan for rent

If you’re strapped for cash and need to pay for rent, there are some plus sides to taking out a personal loan for rent.

Pro #1: Provides a window of time for re-assessing your finances

By taking out a personal loan to cover your rent, you buy yourself some time to get your budget back on track. With a personal loan, you can pay for rent (either what you owe from missed payments or for future rent payments). Once you pay your rent, you’ll find yourself less stressed and you’ll think more clearly so you can get your budget back in a place where you can pay your loan back and have enough money for future rent payments.

Pro #2: Gives you flexibility

Personal loans allow you to use the loan money for anything you need. So, taking out a personal loan gives you the flexibility to use the money for rent or any other expense you need to cover. This flexibility is enticing for renters who need some financial help as the loan doesn’t specify what you can and cannot use the money for.

Pro #3: You can shop loan ranges and rates

Before taking out a personal loan, you’ll be able to shop around for loan ranges and rates. Make sure to compare your findings before you make a decision. You can take out a loan for as little as $1,000 or as much as $60,000 if needed. You can also compare interest rates.

It is important to try and find a loan with a low interest rate so you don’t accrue more debt than is absolutely necessary.

Pro #4: Can build a credit score

This is both a pro and con of personal loans, depending on how diligent you are with repayment. If you make your loan repayments in full and on time every single time, you’ll pay the loan off within the limits and build your credit score. If your credit score took a hit or is low, this is one way to rebuild your credit history.

However, it’s essential that you meet the terms of the loan for this to benefit you.

Cons of using a personal loan for rent

As with everything, when there are pros there are cons. Before taking out a loan to pay rent, consider the negative impacts of rent loans.

Con #1: You’ll pay interest

With any type of loan, you’ll pay interest on the amount you borrow. So, if you take out a personal loan toward rent, not only will you pay the rent money, you’ll also be paying money toward the interest.

If you have no other options, then taking out a loan for rent allows you to make your payment, stay in your apartment and come up with a new financial plan. Keep in mind that you’ll pay more with this option because of interest.

Con #2: Adds to debt

When you take out a personal loan to pay rent, you’re adding to the overall amount of debt you have. This may compound your stress and overall debt, causing more problems down the road. Also, when you rent, you aren’t putting money toward eventually owning an asset as with a mortgage toward a house. So, you’re compiling debt without working toward an eventual purchase.

Con #3: Could harm your credit score

If you fail to make your monthly loan payment, you could seriously damage your credit score putting you at risk for further financial hardship.

How to find a personal loan to pay back your rent?

If you’ve come to the conclusion that a personal loan is right for you, then you’ll need to know where to look and find one. Most financial institutions will offer loans and you can shop around for the loan that is right for you. Here are some places you can go to find a personal loan to pay back your rent:

Bank

Credit union

Online banks

Loan comparison websites

Because different places offer different rates on your loan, it’s smart to get several recommendations before taking out a loan.

Other options to pay back your rent

Unsure that a personal loan is right for you? We also have provided several other options to consider when you need money to pay back your rent. Before taking out a loan, you could consider:

1. Talking to your landlord

When you first realize that you may not have the money to pay your rent or if you’ve missed the due date, you’ll want to talk to your landlord immediately. Getting in front of the issue and addressing it openly is always a wise move.

Ask your landlord if he/she is willing to defer rent, offer a payment plan or waive late fees. You never know unless you ask!

2. Borrowing from a friend or family member

Do you have a trusted friend or family member that could loan you money for rent payback? If so, this is a less expensive option compared to getting a personal loan. Sometimes, close family or friends will loan you the money, interest-free, which is always a better option.

3. Call 211

You can the 211 community phone line to get referrals for services, like financial resources. If you’re in a bind, try calling this number and get in touch with local resources that can help with rent relief.

4. Consider a roommate

Imagine your rent payment being cut in half. Would that free up some of your budget? The answer is most likely yes. If you have space, you may consider getting a roommate who can share the cost of rental expenses and save you money, too.

5. Get a side gig

Nowadays, there are several side hustles that you can do from home, after work or at your convenience that pays well and would help your income. If you can get a side hustle that’ll cover the additional money you need for rent, this is a great option because it puts you in control of your money and you don’t need a loan to cover the extra expense of rent paybacks.

6. Reallocate your budget

Sometimes, we spend money on things like coffee, eating out or shopping and don’t realize how much of our budget it’s taking up.

Before you take out a personal loan, take a hard look at your expenses and budget to see where you can trim the fat. If there are areas to cut back on and reallocate expenses to rent payback, do this before taking out a personal loan.

Know your financial options

Now that you understand the pros and cons of loans to pay rent, you can make an informed decision if this is right for you. As always, you may want to consult a financial advisor before making a big decision like this to get professional guidance on what is best for you and your situation.

The information contained in this article is for educational purposes only and does not, and is not intended to, constitute legal or financial advice. Readers are encouraged to seek professional legal or financial advice as they may deem it necessary.

Sage Singleton is a freelance writer with a passion for literature and words. She enjoys writing articles that will inspire, educate and influence readers. She loves that words have the power to create change and make a positive impact in the world. Some of her work has been featured on LendingTree, Venture Beat, Architectural Digest, Porch.com and Homes.com. In her free time, she loves traveling, reading and learning French.

Inside: Are you looking for ways to make money quickly and easily? This guide has you covered with tips on how to double your money in 24 hours.

Doubling your money is an aspiration many investors feasibly target, and it’s critical to your future financial stability.

This enticing objective involves transforming a small amount of money and doubling it for tomorrow. You need cash fast, so that is why you are reading this post.

You will quickly learn there are easy ways to double money in 24 hours and others that over time you can be skilled at and easily double your cash.

Given that 58% of borrowers struggle to meet basic monthly expenses and 70% of borrowers are using loan money for rent and other basic expenses. 1

You want to learn how to double your money before you actually need to, so by inevitably secure financial confidence for upcoming expenses.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

How can I double my money quickly?

Doubling your money in less than 24 hours isn’t straightforward, but it is possible if you’re willing to take high risks.

These are popular methods to double your money:

Engagement in day trading. It’s risky but one of the fastest ways to double your investment.

Try your hand at gambling. Remember, the house typically has the upper hand. This is not recommended as you are more likely to lose more money than you prefer.

Consider investing in digital real estate. This is similar to real-life property flipping.

Most importantly, avoid get-rich-quick schemes; they’re mostly scams. So, do your homework before diving in!

20 Easy Ways to Double Money in 24 Hours

As inflation rises and people are struggling with their budgets, the question of how to double money in just 24 hours often comes up.

While it may sound like a lofty goal, there exist strategies that can significantly boost your financial growth in a surprisingly short time.

However, keep in mind these are not risk-free endeavors, and they each require a good understanding and judicious implementation to yield profitable results.

1. Invest in Stocks

If you’re hunting for opportunities to double your money fast – investing in stocks could be your ticket, especially with the current volatility.

Although there’s a risk factor involved, it’s a time-tested strategy for impressive returns. Learn how fast you can make money in stocks.

Honestly, one of the best ways to improve your net worth is learning how to invest in the stock market. Yet, many people shy away from the idea.

By not investing in stocks, you are slowing your pace to financial freedom. So, why not learn how to invest in stocks for beginners?

The choice entirely depends on your risk appetite, investment horizon, and personal preferences. Start by evaluating your risk tolerance. Personally, I can tell you this is one of the ways I double money in 24 hours consistently.

Motley Fool

The Motley Fool is dedicated to helping the world invest — better.

They help millions of people attain financial freedom through their site, podcasts, and premium investing services.

Learn More

2. Options Trading

Options trading can double your cash in a mere 24 hours, thanks to its inherent rapid return benefits. However, with the potential for high returns, it also poses significant risks.

Options trading is an advanced strategy for buying stocks with an option contract. Thus, you get the right but not a duty to buy (call options) or sell (put options) a stock at a specific price.

It presents the possibility of doubling, tripling, or quadrupling your money.

This is an avenue to pursue if you want the potential for huge profits, but you must take this investing course to learn the proper way to trade options.

However, you run the high risk of losing the entire investment! So, this is risky for novice investors and you need a brokerage for this type of trading.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

3. Flip Items for Arbitrage

Retail arbitrage, essentially the practice of buying and reselling goods, is a beneficial way of doubling one’s money in a short time. This can be particularly effective by taking advantage of clearance sales in mainstream stores like Walmart and Kohl’s, and then reselling the products on online marketplaces.

Notable items often flipped include apparel, books, electronics, and toys. You can check a full list of popular items to flip.

According to the Flea Market Flippers, you can use a variety of platforms to sell your flipped items.

4. Rent Out Your Property

Renting out unused property or space can be a lucrative form of passive income. This may include a spare room, or underutilized sections like a garage, with various platforms facilitating such financial transactions like Neighbor or VRBO.

Another example is it is financially beneficial to rent out items, like a lawn mower which costs $500 but brings in $15-20 for each rental. Thus, paying for itself in a short amount of time.

Despite the potential risks associated with property investments, including unpredictability in the real estate market and tenant issues, leveraging a good understanding of the local market can make it quite possible to double your investment over time.

5. Become A Side Hustles Expert

Becoming a side hustle expert requires a clear understanding of your goals and the willingness to trade your time for money. You can identify profitable opportunities which can range from ridesharing to teaching English as a second language (ESL) online.

Honestly, this is best to set up BEFORE you are desperate for cash.

Patience is key as nurturing a side hustle often takes time before it becomes an efficient income-generating endeavor.

To help you out, here are specific side hustles based on your stage of life:

6. Rent Out Your Skills

Renting out your skills is a smart quick-fix to double your money within 24 hours. It’s all about capitalizing on what you can do best and offering it to those who need it.

Start by identifying a skill or knowledge you’re proficient in. Are you a wizard in web design? A maven of SEO?

Select the right platform. Websites like Fiverr, Freelancer.com, and TaskRabbit are excellent for freelancers.

Promote your services. Reach out to your networks or use social media to boost your visibility.

This is a great way to earn $300 fast if you know what you are doing.

TaskRabbit

Find local jobs that fit your skills and schedule.

With TaskRabbit, you have the freedom and support to be your own boss.

Plus set your own rates!

Get Started

7. Deliver with DoorDah or GrubHub

Double your income in a day by delivering with platforms like DoorDash or GrubHub. As a courier, you get paid for each delivery – so the more you do, the higher your earnings.

With a smartphone and transportation, you can start making extra cash immediately. Some top delivery options:

Working with DoorDash

Serving with GrubHub

Remember, it’s all about completing as many deliveries as possible. Every order increases your day’s earnings, potentially doubling them if you put in enough hours.

8. Invest in Cryptocurrencies

Invest in cryptocurrencies like Bitcoin, Ethereum, and Bitcoin Cash holds the potential to double your money in 24 hours due to their volatile nature.

To start:

Keep tabs on crypto trends through monitoring websites or apps.

Buy popular or promising cryptocurrency during their low-cost phase.

The trick to doubling your funds is selling at peak prices.

Remember, trends can change rapidly, so only invest what you can afford to lose. For newbies, it’s beneficial to seek advice from a financial advisor knowledgeable in the crypto market.

9. Take Surveys

Looking to double your money in a day? Consider taking paid surveys. However, you will have to take quite a few surveys to make a significant amount of cash.

To boost your earnings:

Seek high paying surveys – Survey Junkie could bring in up to $3 per survey.

Use free time efficiently – complete quick tasks on Swagbucks.

Refer friends – earn 10% of their earnings on Swagbucks.

Remember, more effort equals higher rewards!

Swagbucks

Swagbucks is a fun rewards program that gives you free gift cards and cash for the everyday things you already do online.

Earn points when you shop at your favorite retailers, watch entertaining videos, search the web, answer surveys, and more!

Start for FREE

Get $10 Sign Up Bonus

10. Lend Money on Peer-to-peer platforms

Lending money on Peer-to-Peer (P2P) platforms can be a profitable strategy, offering a unique method for individuals to loan and borrow money without traditional financial institution interference.

Users can sign up as lenders on recognized P2P platforms like LendingClub, Prosper, and Upstart, and yield high-interest returns based on their borrower’s creditworthiness.

However, this process also poses risks such as potential defaults, making it important for the lenders to do their research and diversify their loans across multiple recipients.

11. Do Odd Jobs

Engaging in odd jobs is a practical approach to earning additional income. Whether it’s mowing neighbors’ lawns or offering handyman services, these simple tasks can often pay upward to $30 per hour.

Digital platforms, like TaskRabbit, even allow you to list your talents locally, extending your reach for potential earnings.

All in all, odd jobs provide an accessible door to financial gain without requiring a significant starting capital.

12. Selling High Demand Printables

Selling printables online is a viable way to generate income. It’s important to create a follower base or an email list to successfully promote and sell your products.

With strategic pricing and high-quality content, you could potentially double your initial investment in a short span of time.

Here are the digital products that sell on Etsy that are in high demand.

By creating high-demand printables, you can buy low, sell high, and double your money all within 24 hours!

13. Max Out you 401(k) Match

Maxing out your 401(k) match can double your money in no time. While this may not happen in 24 hours, it can happen the next time you get paid and greatly increase your retirement savings.

When you contribute to your 401(k) plan, your employer might match it by 50% or 100%. You will have to check your Human Resources department to see what your company offers.

Contribute the maximum amount your employer is willing to match. This is free money for you. For instance, if you’re making $100,000 and your employer’s match is up to 3.5% of your salary, put in at least $3,500.

Are you one of the 5 people making this costly mistake? 2

14. Sell Courses and Subscriptions

Selling courses and memberships online is a highly profitable low-risk venture that requires just a small initial investment of your time and money. Once the course is developed, it can continue to generate passive income every month.

Tools such as Podia or Teachable allow you to easily sell and manage your courses, while also offering additional benefits such as digital downloads, subscription plans, and an opportunity to begin selling directly to your followers.

15. Work for Employers

In case you haven’t heard, time is money. And you can trade your time for money at any point.

Working for employers often ensures a steady income which can be supplemented by various benefits.

One of the greatest advantages is the employer match on a 401(k) account, which allows employees to double their contributions effortlessly. This means that if an employee contributes 5 percent of their salary to the retirement account, the employer adds another 5 percent.

Expert Tip: Continually upgrade your skill set to increase your value to employers. More demanding or specialized tasks often command higher pay, propelling you towards your double-money goal quicker.

16. Sell Your Goods

Selling goods online provides a dynamic platform for entrepreneurs, allowing them to reach a wider audience. This involves identifying high-demand products, purchasing from a reliable supplier, and selling them on popular e-commerce platforms like Amazon, eBay, and Etsy.

Get involved in flea market flipping. Hunt for undervalued items at yard sales or flea markets and resell online. Facebook Marketplace could be a goldmine.

Unload used or vintage items. These platforms can help you earn huge profits, especially from expensive items. Don’t let seller fees deter you; big profits are still achievable.

Books are an easy sell. Buy used ones from local or online stores and sell them in different areas or on different platforms. Diversifying the categories you offer can potentially boost your profits.

Pricing is set considering the purchase cost, overheads, and the competitive market.

17. Invest in Collectibles

Investing in collectibles presents a thrilling opportunity to generate significant profit in a short span. The key is identifying profitable niches, such as vintage comic books, rare coins, or baseball cards.

The rarity and condition of an item directly influence the price it can command.

The strategy involves buying low, often from garage sales or online platforms like eBay or Etsy, and selling high. However, one must perform diligent research and be aware of market trends, as failure to do so can lead to risks.

18. Get Rid of Your Most Valuable Items

Selling your own possessions is an effective way to declutter your home while also generating a potential cash flow.

This is one way to accumulate over $1,000 in cash earnings.

This may not be what you want to do, but your possessions are worth money and it may be necessary.

19. Save Money and Increase It

You’ve heard it said: a penny saved is a penny earned. This principle isn’t just about saving but also growing your money as an effective way to double your income.

Here’s how:

First, begin with saving. The more you can put away, the better. Remember, your coffee can strategy may not earn interest, so consider a deposit into a savings account.

Next, let’s talk about compound interest. Suppose you invest $1000 at a 5% interest rate. After a year, your money grows to $1050. The next year, you earn interest on this increased amount. Over time, the effect snowballs, significantly augmenting your investment.

Lastly, protection against inflation is key. Always aim for an interest rate higher than the rate of inflation. This means, in real terms, your money is consistently growing.

Done right, these steps can effectively increase your savings rapidly.

Raisin

Simply select one of the high-yield savings products offered by their network of federally insured banks and credit unions to begin your savings journey.

You can open a free Raisin account in just a few minutes!

Compare Rates

20. Game or Bet on A Sport

While it’s often overlooked, betting on sports or games could be a fast track to doubling your money in less than a day. This risky Vegas plan may be worth the potentially rewarding pursuit.

Beware – while some have been successful, this method is heavily debated due to the significant risk factors. As such you may be better off becoming a referee for youth sports, which is a popular side hustle for men.

Remember, it’s all fun and games until the cash is lost – don’t stake what you can’t afford to lose.

FAQ

Doubling $1,000 quickly calls for some calculated risks and smart choices.

One way is investing in stocks, potentially high-return yet high-risk assets. Another route could be starting a side hustle, like an online course or freelance work, where initial investment is low but returns could be impressive.

This is a hard ask given many people this month. However, doubling $3000 fast can be achieved through smart investments and income diversification.

Using online platforms and flipping high-demand items may yield quick profits. Additionally, utilizing skills for a freelance portfolio or selling an online course can quickly boost initial capital.

Doubling your $5000 swiftly may seem like a daunting task, but with strategic planning, connection establishment, and careful investments, it’s more achievable than you might think.

Here’s how you can try it:

Start by investing in stocks. Rapid-growth stocks or volatile currency pairs can double your money. Invest wisely based on market analyses.

Try real estate flipping. Buy undervalued properties, renovate, then sell.

Entrepreneurship is another avenue. Turn your skills or ideas into a profitable business.

Peer-to-peer lending platforms yield high return rates with the right borrower.

Playing the lottery or gambling could work, but highly risky.

Remember, to double up money quickly, ensure you are knowledgeable in your chosen method and anticipate potential downsides. Do comprehensive research first.

Is Doubling Money in 24 Hours Possible?

Yes, you, dear reader, can indeed double your money in 24 hours! It won’t be a cakewalk though, requiring specific skills, solid strategies, and of course a pinch – maybe a handful – of luck.

You could tap into high-growth potential fields like day trading, selling high-demand goods online, or capitalizing on your skills as a content creator. Remember, this quick win has its fair share of risks too.

Now, make sure to do proper due diligence and check the integrity of whatever way you choose to make more or dive into the gig economy.

Now, learn how to double 10k quickly.

Source

Federal Reserve Bank of St. Louis. “Fast Cash and Payday Loans.” https://research.stlouisfed.org/publications/page1-econ/2019/04/10/fast-cash-and-payday-loans#:~:text=However%2C%207%20of%2010%20borrowers,difficulty%20meeting%20basic%20monthly%20expenses. Accessed November 7, 2023.

Motley Fool. “1 in 5 Americans Are Making a Terrible 401(k) Mistake.” https://www.fool.com/investing/2018/02/09/1-in-5-americans-are-making-a-terrible-401k-mistak.aspx. Accessed November 7, 2023.

Know someone else that needs this, too? Then, please share!!

Did the post resonate with you?

More importantly, did I answer the questions you have about this topic? Let me know in the comments if I can help in some other way!

Your comments are not just welcomed; they’re an integral part of our community. Let’s continue the conversation and explore how these ideas align with your journey towards Money Bliss.

Generally, the credit bureaus consider anything over 670 a good credit score.

Considering applying for a new line of credit like a mortgage or credit card, but not sure how your credit score stacks up? If your score is 670 or higher, you’re doing fairly well. The best credit score and the highest credit score possible is 850 for both FICO® and VantageScore® models. FICO considers a score between 800 and 850 to be “exceptional,” while VantageScore considers a score above 780 to be “excellent.” It’s possible to get an 850 credit score, but it’s tough to achieve.

In This Piece

What Is a Good Credit Score?

A good credit score will depend on the scoring model, but either 670 or above would be considered good. Credit scores calculated using the FICO or VantageScore 3.0 scoring models range from 300 to 850. Those scores are broken down into five categories, though the breakdowns differ slightly. Since they have somewhat different range calculations, what’s considered good for VantageScore may be considered fair for FICO, and what’s considered very good for FICO may only be good by the VantageScore model.

FICO and VantageScore aren’t the only credit scoring models. However, they are the most commonly used models and the ones used by the three major credit bureaus: Experian®, Equifax® and TransUnion®. Some lenders even have their own scoring models. But most lenders and credit card companies use FICO scores or VantageScores.

What Is a Good FICO Score?

For FICO, a good credit score is 670 or higher. A score over 739 would be considered very good, while a score above 800 is considered exceptional—the highest designation possible aside from a perfect 850.

What Is a Good VantageScore?

In the VantageScore 3.0 model, a good score is 661 or higher. Since this model doesn’t have a designation between good and excellent, the range of good scores is much wider than it is for FICO. Excellent scores start at 781 rather than 800 in this model, with 850 also being considered a perfect score.

Understanding Credit Score Ranges

The credit score ranges vary depending on whether you’re looking at a FICO score or a VantageScore. They line up fairly similarly, but their score designations have different labels — FICO lacks a “very poor” designation, while VantageScore lacks a “very good” range. Here’s how they break down.

FICO Score Range

Poor: 300-579

Fair: 580-669

Good: 670-739

Very Good: 740-799

Exceptional: 800-850

VantageScore Range

Very Poor: 300-499

Poor: 500-600

Fair: 601-660

Good: 661-780

Exceptional: 781-850

Credit Score Range Chart

To give you a clear idea of how FICO and VantageScore’s credit score ranges compare, here’s a comparison credit score range chart.

What Are Credit Scores?

The three-digit figures called credit scores are what scoring institutions use to rate your credit profile based on your credit report. Since these bureaus have their own records, your score might differ from one scoring institution to the next.

Your score suggests to potential creditors how likely you could be to repay a loan, pay off a credit card, make late payments, and default on payments. Basically, it helps them determine whether you’re an acceptable risk and if they should approve your application for a loan or credit card. A low score doesn’t always mean lenders will decline your application. Instead, it might mean they’ll consider approving you with higher interest rates or less favorable loan terms.

How to Get a Good Credit Score

VantageScore and FICO scores are calculated using similar information. Each model may use slightly different terms for these, but here’s what they’re looking for.

Payment History

FICO weight: 35 percent

VantageScore weight: 40 percent

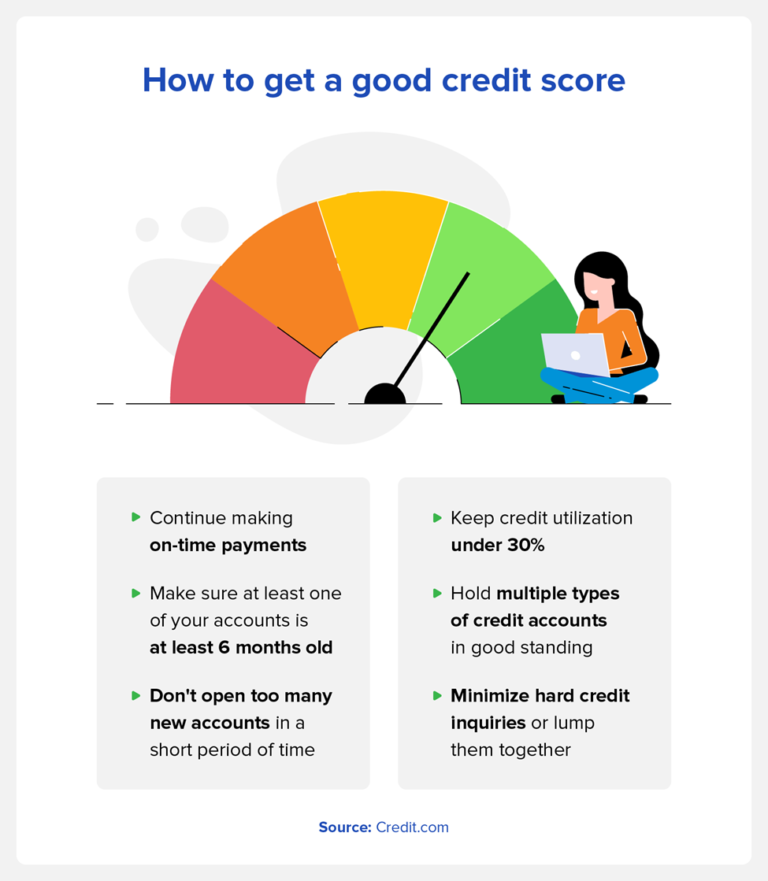

Late and missed payments can have a major impact on your credit score. Both FICO and VantageScore take your history of payments into account when calculating your score and look at your number of late payments, the number of accounts you’ve missed payments on, and the overall number of missed payments. Maintaining a consistent, on-time payment history goes a long way in establishing good credit.

Amounts Owed/Credit Utilization

FICO weight: 30 percent

VantageScore weight: 20 percent

Credit utilization is calculated as a ratio. It divides the amount of credit you’ve used by your total credit limit. If your credit limit is $5,000, for example, and you use $2,000 in credit, your utilization rate is 40 percent. It’s recommended to keep this rate to 30 percent or less and preferably below 10 percent. To help improve your credit score, try to reduce your utilization ratio if you often find yourself going above 30 percent.

Length of Credit History/Credit Age

FICO weight: 15 percent

VantageScore weight: 21 percent

Your credit history refers to the amount of time your credit accounts have been open, averaged across all of your accounts. That means that if your credit history has factored in your oldest account for the last 15 years but you suddenly close that account, your average credit age will drop accordingly, which could also lead to a drop in your credit score.

For that reason, it’s a good idea to maintain your oldest credit accounts. As a rule of thumb, try to make sure you have one account that’s six months old or older open at all times.

Credit Mix

FICO weight: 10 percent

VantageScore weight: N/A

Your credit mix refers to the number of revolving and installment accounts you have open. Here’s how those accounts differ:

Installment accounts: These are essentially defined long-term loans like home mortgages or vehicle financing on which you make payments in specified amounts over a predetermined period.

Revolving accounts: These types of accounts set a specific amount of credit you can use as needed, such as a credit card. You only pay back the amount of credit you borrow against this limit.

Potential lenders will want to know you can manage both of these account types, so it helps to have a history of successfully managing each. While FICO has a category explicitly for this, VantageScore does not—though it still may factor into other elements of your VantageScore. As such, it can be helpful to have multiple types of accounts in good standing regardless of the scoring model.

New Credit/Recent Credit

FICO weight: 10 percent

VantageScore weight: 5 percent

Opening multiple new credit accounts in a short period of time can have a negative impact on your credit score. Since lenders may see it as a red flag for a borrower to have several recent accounts open, it may be helpful to let your current accounts continue aging while paying them off consistently if you want to maintain or improve your score.

Balances and Available Credit

FICO weight: NA

VantageScore weight: 14 percent

Though only VantageScore has categories specifically for balances (11 percent) and available credit (3 percent), they still play a role in your FICO credit score. The amount of money you owe to lenders and your available credit factor into credit history and utilization rate, so keeping your balances low in comparison to your available credit can be a good idea when trying to achieve a good credit score.

A Note on Credit Inquiries

A hard credit inquiry gets pulled when a lender requests your credit report to assess your creditworthiness. This type of inquiry can drop your score by as much as 5 to 10 points and may stay on your credit report for up to two years, but it will impact your score for only 12 months. To get and maintain good credit, it’s best to avoid these as much as possible.

If you need to apply for multiple credit accounts in a short time or want to shop around for loan rates, it can help to keep those applications within a 14-45-day window so they get grouped into one inquiry. FICO and VantageScore differ on this, with FICO using 45 days and VantageScore using only a 14-day span.

Keep in mind this is only for hard inquiries, as soft inquiries shouldn’t affect your score.

How Lenders Use Credit Scores

Credit scores can offer a gauge of creditworthiness for lenders to determine things like whether or not to approve you for a credit line, how much credit to approve you for, and what your interest rate should be. But while your credit score has a big role to play in this, it’s considered alongside your credit report. Lenders may also consider your income, debt, and your ratio of debt to income.

How Can I Get My Credit Scores?

You can request a full credit report from all three credit bureaus from AnnualCreditReports.com, however, your score is not included with your report.

Most online options for viewing your credit score—free or paid—are limited to one or two scores. ExtraCredit from Credit.com takes it twenty-six steps further by offering you 28 of your FICO scores from all three major credit bureaus. When you sign up for an ExtraCredit account, you can also earn money when you get approved for select offers, monitor your accounts with $1 million identity theft insurance, and get exclusive discounts froma leader in credit repair services. All for one low monthly price.

If you’re not ready for ExtraCredit, Credit.com also offers a free Credit Report Card. This comes especially in handy as it offers you your Experian VantageScore 3.0 credit score for free.

FAQs about Good Credit Scores

Want to know more? Here are a few common questions about what good credit scores are and how they’re used.

Do Lenders Prefer a Good VantageScore Score over a Good FICO Score?

Lenders don’t necessarily prefer one score over the other. It’s likely, though, that a given lender uses only one credit-scoring institution. FICO reports that 90% of the top U.S. lenders use FICO scores when deciding whether to loan money to an applicant. On the other hand, VantageScore states that between March 2021 and February 2023, approximately 14.5 billion VantageScore credit scores were used.

Both models are consistent enough that knowing where you stand in one gives you a reliable indication of your credit in general.

What Is a Good Credit Score to Buy a House?

A FICO score of 580 is the minimum credit score required to qualify for maximum financing. , according to the U.S. Department of Housing and Urban Development. Below 580, borrowers will have to make a minimum downpayment of 10 percent. That doesn’t necessarily mean that you’re guaranteed to qualify for a loan with maximum financing with a score of 580 or above, but it’s what you’ll need if you want the flexibility of a lower down payment.

What Is the Highest Credit Score?

850 is the highest credit score possible for both the FICO and VantageScore models.

What Is Credit?

Credit is access to capital provided by a lender with an expectation that it will be repaid within an agreed time frame. This could be a set installment account—such as a mortgage or car loan that gets paid off gradually—or a revolving account like a credit card with a maximum balance that can be borrowed at a given time.

What if I Don’t Have a Good Credit Score?

Now that you know what’s a good credit score, it’s crucial to act on yours. If your credit is fair or poor, find out why. Then you can address the factors and work to improve your score.

Do you need more credit history? Check out our ExtraCredit Build It feature! Use ExtraCredit to report rent and utility bills you’re already paying and add them to your credit profile as tradelines. This allows the credit bureaus to see additional payment information from you, which can help you build your credit profile.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.