Nestled among the rolling hills of Los Angeles, the legendary neighborhood of Bel Air has long been synonymous with opulence and seen as the pinnacle of West Coast luxury living.

And for good reason.

Located directly across from the iconic Sunset Boulevard, the world-famous enclave — whose very name is associated with lavish estates, Hollywood glamour, and understated affluence — continues to captivate both the privileged few and those who aspire to call it home.

Bel Air’s reputation as an exclusive haven for the world’s elite is well-earned, and its prestigious zip codes are graced with stunning architectural marvels, each a testament to the grandeur and sophistication that defines the area.

With bigger lots and more expensive residences than the equally famous Beverly Hills (which sits merely a few miles away), Bel Air effortlessly combines the allure of old-world charm with the comforts of contemporary living.

The reasons behind Bel Air’s enduring appeal are as diverse as the people who are drawn to its lush landscapes and private estates.

Breathtaking canyon views, impeccably manicured gardens, and a sense of seclusion rarely found in the midst of a bustling metropolis are just some of the factors that make this neighborhood an aspirational address for many.

The allure of Bel Air isn’t solely about its extravagant homes; it’s about the lifestyle it offers — a unique blend of tranquility and proximity to the cultural heartbeat of Los Angeles.

Bel Air mansions for sale

Today, we’ll explore a curated list of the most extravagant mansions currently on the market in Bel Air, each a testament to the neighborhood’s unmatched desirability and exclusivity.

These residences are more than just houses; they represent a way of life that is the envy of the world. Join me as we embark on a journey through the opulent world of Bel Air real estate, where luxury knows no bounds.

#1 755 Sarbonne Road, Bel Air – $39,900,000

Photo credit: Anthony Barcelo courtesy of Westside Estate Agency

Villa Sarbonne, one of the most impressive Bel Air houses currently up for grabs, sits mere minutes away from the neighborhood’s famous The One mansion — developer Nile Niami’s record-breaking project, which was once listed for $500 million.

With an impressive 15,000 square feet of ultra-luxurious living space, Villa Sarbonne has 6 bedrooms, 10 baths, and a long list of amenities.

To name just a few, 755 Sarbonne Road features a private wine cellar, home theater, library, a gourmet home kitchen, and a separate chef’s kitchen, as well as a wellness center with a travertine-clad steam room.

Photo credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate Agency

Stand-out features include a sculptural staircase and a 5,000+ sq. ft. terrace with panoramic city-to-ocean views.

Photo credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate Agency

The property is listed with Kurt Rappaport at Westside Estate Agency, who shares the listing with The Agency founder Mauricio Umansky and Farrah Brittany, also with The Agency.

#2 10702 Levico Way, Bel Air, California – $30,950,000

Photo credit: Anthony Barcelo courtesy of Westside Estate Agency

This quintessential Bel Air mansion sits in the ultra-exclusive, guard-gated community of Levico Estates, on a massive 4.3-acre lot.

Photo credit: Anthony Barcelo courtesy of Westside Estate Agency

Featuring over 12,000 square feet with every conceivable amenity, the luxury property has 6 bedrooms, 9 baths, a stunning 2-story entry, a large living room, a library/office, a gourmet kitchen with family room, a gorgeous primary suite with dual baths and closets, a gym, and a wine cellar.

Photo credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate Agency

And while the opulent interiors definitely caught our eye, the amenity list continues as we step outside, where the generous 4+ acre lot has everything from an outdoor loggia to a pool house, championship tennis court, large lawns, and gardens — all opening up to 360-degree city and canyon views.

Related: The ‘Fresh Prince of Bel-Air’ House Isn’t Even in Bel-Air

Photo credit: Anthony Barcelo courtesy of Westside Estate AgencyPhoto credit: Anthony Barcelo courtesy of Westside Estate Agency

The trophy property at 10702 Levico Way is listed with Kurt Rappaport of Westside Estate Agency.

#3 1740 Bel Air Rd – $19,900,000

Photo credit: Trevor Tondro courtesy of the Fridman Group / Compass

As the listing puts it, this “masterpiece of artful design nestled in the secluded hills of Bel Air… immediately transports you to a level of world-class beauty, serenity, and tranquility from the moment you enter the privately gated driveway.”

Built in 2014, the massive 11,246-square-foot home sits on a generous one-acre lot located just a short drive from world-class luxury shopping, fine dining, and entertainment venues.

With 7 bedrooms, 10 baths, a beautifully appointed open-concept living space, and floor-to-ceiling windows that showcase killer views, the property at 1740 Bel Air Rd is rightfully touted as a private sanctuary.

Photo credit: Trevor Tondro courtesy of the Fridman Group / CompassPhoto credit: Trevor Tondro courtesy of the Fridman Group / CompassPhoto credit: Trevor Tondro courtesy of the Fridman Group / CompassPhoto credit: Trevor Tondro courtesy of the Fridman Group / Compass

The inviting living room fireplace, the spacious chef’s kitchen with an oversized island, slab natural stone countertops, and custom natural wood cabinetry all against a canyon backdrop, the spa-like primary suite, the indulgent home theater with bar, and studio, are all spaces where every detail has been carefully curated to evoke a sense of calm livability.

Outside, the property is equally impressive, with lush landscaping and mature trees that provide privacy and seclusion.

Photo credit: Trevor Tondro courtesy of the Fridman Group / CompassPhoto credit: Trevor Tondro courtesy of the Fridman Group / Compass

The luxury property is listed with Tomer Fridman of The Fridman Group at Compass.

#4 10901 Chalon Road – $16,495,000

Photo credit: Nils Timm courtesy of The Agency

In prime Bel Air, nestled behind mature Pepper trees and lush California landscaping, sits a 9,000-square-foot contemporary marvel with bespoke interiors by KNA Design and tranquil outdoor entertaining spaces.

The gated 6 bed/8 bath private residence boasts upscale finishes throughout (including oak wood, glass, natural honed stone and organic textures) and embodies California’s indoor-outdoor living to perfection.

Photo credit: Nils Timm courtesy of The Agency

With an elegant formal living room with a floor-to-ceiling marble fireplace and built-in-bar, vaulted ceilings, sky-high windows, and sliding doors that open into the expansive backyard, the Bel Air mansion also features a formal dining room with a walk-in wine closet and a showstopping kitchen with a large marble-clad center island and cozy breakfast nook.

Photo credit: Nils Timm courtesy of The AgencyPhoto credit: Nils Timm courtesy of The AgencyPhoto credit: Nils Timm courtesy of The Agency

The 10901 Chalon Road property also has a double-height ceiling living room upstairs, which connects four of the bedrooms, and a spacious primary suite that overlooks views of Bel Air from a private balcony connecting to the wellness area below.

Photo credit: Nils Timm courtesy of The AgencyPhoto credit: Nils Timm courtesy of The Agency

The property is listed with David Parnes and James Harris (Bond Street Partners) and Monique Navarro with The Agency.

#5 14319 W Mulholland Drive – $8,350,000

Photo credit: Mike Kelley courtesy of Compass

A newly built contemporary home perched in the Bel Air mountaintop at the end of a winding, privately gated driveway, is looking for a buyer. And we doubt it will have any issues finding one, as the 4,500-square-foot home is quite the stunner.

Photo credit: Mike Kelley courtesy of Compass

With three bedrooms, four baths, a grand double wooden staircase separated by a glass walkway, upper-level tranquil gardens with lounge areas, and a rooftop garden area, the 2023-built home is far from your ordinary home.

The lower level hosts a generously sized living space where we find the great room, a wet bar for entertaining, and an impeccably designed chef’s kitchen — that boasts a sleek, contemporary dark color palette and custom stacked cabinetry.

Photo credit: Mike Kelley courtesy of CompassPhoto credit: Mike Kelley courtesy of CompassPhoto credit: Mike Kelley courtesy of CompassPhoto credit: Mike Kelley courtesy of CompassPhoto credit: Mike Kelley courtesy of Compass

Outside, we find a true backyard oasis with several seating areas, an infinity edge pool, an al fresco dining area, and a custom built-in bar.

Photo credit: Mike Kelley courtesy of CompassPhoto credit: Mike Kelley courtesy of Compass

And while it’s hard to believe that this is the most affordable property out of all the beautiful Bel Air mansions we went over today, it’s the only one that sports a price tag under $10 million. Listed for $8,350,000, 14319 W Mulholland Drive is repped by Tomer Fridman with the Fridman Group at Compass.

All the above Bel Air mansions for sale are representative of the caliber of homes in the sought-after Los Angeles neighborhood. And we’ll be keeping an eye out for new listings popping up on the market, as well as notable sales in the area, to provide you with a comprehensive resource on the most extraordinary Bel Air houses making moves on the Los Angeles real estate scene.

If you’re a real estate professional with equally impressive listings in the Bel Air area, you can reach out to us at [email protected] and submit them for consideration.

More stories

The Weeknd’s house in Bel Air: An extravagant $70 million mansion

A striking $150M modern mansion could set a new record for Bel Air

Wonderfully Witchy: The Full Story of the Spadena House in Beverly Hills

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Disclosure regarding our editorial content standards.

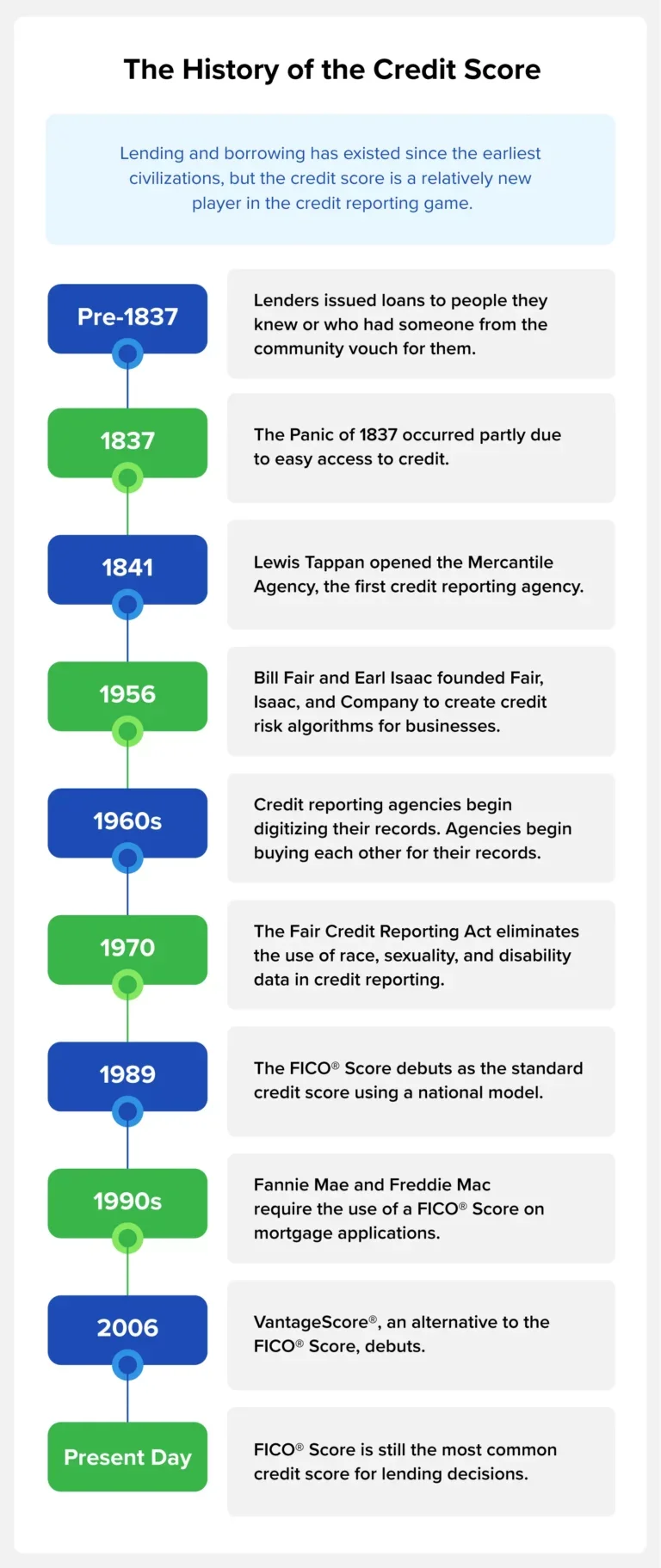

The credit score was invented in 1989 to make credit reports more actionable for lenders.

Credit scores affect many parts our lives: whether we qualify for a loan, what interest rate we pay, even where we can rent or whether we get our dream job. But that three-digit number is a relatively new invention—the credit score was invented in 1989, less than 50 years ago.

Understanding the origins of the credit score can help you better comprehend why lenders use it and how to improve your financial situation.

When Credit Scores Were Invented

People have borrowed and lent money for centuries. In the early days, storekeepers and lenders only extended credit to people they knew, or they would ask people they respected in town for their views on a person’s credit risk. This informal credit reporting system was highly localized and incredibly subjective.

But as credit became more critical to daily life and people began to move around more, the need for a more widespread credit reporting method arose.

The 1800s: The Rise of Credit Reporting Agencies

After the Panic of 1837 (partly caused by easy access to credit), Lewis Tappan recognized that businesses might benefit from a better understanding of who to issue credit to. In 1841, he formed Tappan’s Mercantile Agency, the first credit reporting agency in America, to meet this need.

His company hired “correspondents,” reliable men (often attorneys and ministers) who would investigate people’s standing in their communities and report it to the central office. They would then add the information to a central ledger in New York City. Many businesses subscribed to the Mercantile Agency to view these reports before issuing credit.

Tappan was a strict abolitionist, so he only worked with businesses in free states, so other credit reporting agencies began to spring up to work with businesses in the South. Hundreds of these credit reporting agencies existed all over the country by the end of the Civil War, but the system had a few problems:

Each agency had different information based on who they hired as correspondents.

Information was highly subjective and included information about a person’s race, gender, and overall moral character, which allowed bias to play a role in lending decisions.

Lenders didn’t know how to interpret the information in the credit reports because they were so subjective, and lenders often didn’t know the person applying for credit.

As more people began to access credit to purchase items like cars and homes in the late 1880s and early 1900s, these credit reporting agencies continued to thrive.

1950s and 1960s: Digitizing Credit Reports

This system was still in place in the 1950s when the ability to digitize records meant that some standardization could occur. Larger agencies started buying their smaller counterparts for additional data they could add to their reports, and national credit bureaus began to form.

In 1956, Bill Fair and Earl Isaac created Fair, Isaac, and Company to make credit reports more actionable for lenders. They used the data in a credit report to perform a statistical analysis that would inform a lender of a person’s credit risk. What resulted was a more analytical approach to interpreting credit reports, but each business or lender had its own algorithm based on the factors they prioritized.

As records continued to be digitized, many people became concerned about the surveillance being done to gather credit information and discriminatory practices in credit reporting. People also realized that credit mistakes would be available forever and could potentially hurt people’s ability to borrow for their entire lifetimes. The Fair Credit Reporting Act of 1970 put several protections into place, including:

Removing data related to race, sexuality, and disability from credit reports

Requiring credit reporting agencies to delete information after seven to 10 years, depending on the type of data

1989: The FICO Credit Score

While more effective for lenders than the previous system, scores varied widely based on a company’s priorities.

The credit reporting bureaus wanted something more standardized, so they partnered with Fair, Isaac, and Company (now known as FICO®) to create the FICO Score, a national scoring model for everyone. The FICO Score debuted in 1989 and quickly became popular with lenders, who no longer needed to hire companies to create their own algorithms. Consumers, who could now know their credit score before applying for a loan, also appreciated the FICO Score.

In the 1990s, the FICO Score cemented itself as part of the lending landscape when Fannie Mae and Freddie Mac began requiring the score as part of mortgage applications.

VantageScore and Other Credit Scores

In 2006, the three major credit reporting bureaus—Equifax®, Experian®, and TransUnion®—launched the VantageScore®, an alternative to the FICO score. There have been four iterations of the VantageScore since 2006, and the latest version incorporates trended credit data, which includes monthly data points over 24 months. It also utilizes machine learning and does not factor medical debt into its algorithms.

Each major credit reporting bureau also has its own proprietary scoring models that lenders may also consider:

Equifax Credit Score

Experian PLUS Score

TransUnion CreditVision New Account score

Despite these options, most top lenders use the FICO Score.

Why Credit Scores Were Invented

Before the credit score, lenders determined a person’s credit risk based on credit reports, which include:

Personal information

Account information

Hard inquiries into your credit

Public financial records such as liens or bankruptcies

Often, lenders weren’t sure how to interpret your credit report, which led to bias in lending decisions and general confusion for consumers regarding whether they would be approved for a loan when they applied.

The credit score was invented to standardize the lending process to make it faster and more equitable. It prevented lenders from using racial, gender, and class bias when determining someone’s credit risk.

Problems With Modern Credit Scoring

While credit scores eliminated the problems of previous credit reporting systems, they aren’t perfect. Here are a few issues with modern credit scoring:

Inappropriate use of credit scores. When the credit score was originally invented, its sole purpose was to determine credit risk for loans. Now, lenders, landlords, and employers often use it to determine a person’s level of responsibility, which can influence car insurance rates and hiring decisions.

Upholding social hierarchies: People with low credit scores, or the roughly 10% of Americans with no credit history, are often denied access to loans or credit cards. When they receive a loan, they often have to make a larger down payment and pay more in interest.

Racial disparities: While the Fair Credit Reporting Act of 1970 removed the use of race as an explicit factor in one’s credit, institutional racism may still impact the remaining factors. For example, redlining continues to prohibit many Black Americans from purchasing a home, preventing them from building wealth through homeownership. As a result, their credit length and payment history, two factors that impact your credit score, may be shorter. This may explain why multiple studies have shown that racial minorities have lower credit scores than white people.

Inaccurate information: A recent study found that 34% of people have at least one error on their credit report. These errors can lower your credit score, resulting in you paying more in interest. While you can dispute errors on your credit report, it may take time to see an increase in your credit score.

These problems could result in you paying more in interest for a loan or being denied the loan altogether.

The Future of Credit Scores

Credit scores have changed since they were invented and will continue to do so as consumer spending and technology change. Here are a few trends that may impact how credit bureaus determine your credit score in the near future:

Buy Now, Pay Later (BNPL): Also called point-of-sale (POS) installment loans, BNPL plans allow you to divide purchases into lower monthly payments, often without interest. Currently, these short-term loans aren’t reported to a credit bureau unless you don’t make your payments, but that may change as technology advances to allow real-time data and these become more popular with consumers.

AI and Machine Learning: Experts are currently debating the use of AI and machine learning to automate and improve credit scoring. Some parties claim it will result in more accurate credit risk assessments and allow credit reporting to occur in real time, making it more accurate. Others are concerned about the potential invasion of privacy and the ethical use of data since AI is only as good as the data it is fed.

Inclusion of alternative data: Nearly 37 million Americans are credit underserved, meaning they have little to no credit history. As a result, they are unable to get access to credit. To help the credit invisible gain credit, credit reporting companies have begun considering alternative data, called consumer-permissioned data, including bank account information and monthly payments like rent, utilities, and streaming subscriptions. Currently, consumers can choose to share this information with lenders and then retract access once they’ve built credit, but this information could begin factoring into everyone’s credit score since AI can make this data easier to use.

Track Your Credit Score With Credit.com

Your credit score is one of the most important numbers in your life. Understanding the history of the credit score and its challenges can help you in your journey to improve your credit. As technology continues to advance, stay informed on the latest updates to credit scoring and take proactive steps to manage your credit with Credit.com.

In San Francisco’s quaint, upscale community of Russian Hill, home to the famously crooked Lombard Street, a 4-bedroom home is now up for grabs.

And it comes with some of the best views money can buy.

Beautifully updated, the 4-bedroom, 2-bathroom single-family home features the timeless architecture typical for the area, and a rooftop terrace with a wet bar and phenomenal views of the San Francisco area facing south, west, and north — including views of Lombard Street which is a crossroad for this home.

Lombard Street, San Francisco. Photo credit: Aerial Canvas courtesy of Coldwell Banker Realty

Located at 2300 Leavenworth St, on the northeast corner of Leavenworth and Lombard, the 1913-built property is part of the historic Castle Court gated community — which has ties to the Fay family (Fay Brothers Soap Factory founder David Fay owned a house here too, later rebuilt by his descendants and now known as the Fay-Berrigan House and Park).

Listed for $3,495,000, the ideally located San Francisco home is listed with The Swann Group, affiliated with Coldwell Banker Realty.

Inside, the entry level offers a spacious flex space for a media room, office, or guest space, with a full bath and gym. The main living floor is up one level and features an open kitchen, dining, living, and office with South, West, and Northern views.

Photo credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker Realty

The top floor has three bedrooms, a full bath, and direct access to the rooftop terrace.

A true showstopper that makes the most of the home’s great San Francisco location, the rooftop terrace offers picture-perfect views of Alcatraz, Coit Tower, the Bay Bridge, the skyline of the financial district, and the world-renowned flowering crooked street.

Photo credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker Realty

Its sought-after location in Russian Hill places it mere moments away from the excellent amenities of Hyde Street, North Beach, the Polk Street corridor, and Fay Park.

More San Francisco homes

The real ‘Full House’ house in San Francisco and where to find it

Mrs. Doubtfire’s house is hiding in plain sight in San Francisco

San Francisco’s Most Famous Houses: How Much are the ‘Painted Ladies’ Worth?

Buying a house is a dream for many Americans, but it can feel very out of reach for some people. To qualify for a mortgage, you’ll need an adequate credit score and down payment, which many people just don’t have.

That is where the Neighborhood Assistance Corporation of America (NACA) comes in. The NACA has helped hundreds of thousands of people find affordable housing with no money down and no minimum credit score. NACA also provides financial assistance for approved homeowners that encounter financial difficulties.

If you’ve been struggling to figure out how you’ll afford to purchase a home, then the NACA program could help. This article will explain how the NACA mortgage process works and how the organization could help you find your next home.

What is the NACA mortgage program?

The Neighborhood Assistance Corporation of America (NACA), a non-profit organization established in 1988, is dedicated to providing affordable housing options to Americans. Its mission is to combat discriminatory and unjust lending practices. With 45 branches across the United States, NACA assists borrowers with low credit scores in securing affordable mortgages.

NACA offers various solutions such as property improvement and foreclosure avoidance to help achieve this goal. Additionally, the organization helps homeowners reorganize their existing mortgages, preventing them from losing their homes to foreclosure. Nevertheless, NACA’s signature mortgage program remains the most sought-after offering among its services.

How does the NACA program work?

The NACA is known for its purchase program, which it calls the Best in America Mortgage Program. This program is designed to make homeownership more affordable for everyone.

If you applied for a mortgage through a bank or credit union, you would undergo an extensive credit check. But the NACA makes it possible to buy a home with:

No down payment requirement

No closing costs

No requirement for perfect credit

No limits on your income

No fees – The lender pays the appraisal costs, attorney fees, title insurance, transfer tax, settlement agent fees, and buyer closing costs.

All of this is available at a below-market interest rate. Currently, the NACA is offering a 30-year fixed-rate mortgage of 2.125% APR and a 15-year fixed-rate mortgage of 1.75% APR. You’d be hard-pressed to find a better deal anywhere else.

Bank of America stands as NACA’s largest and most significant partner, providing a major portion of the funding for the loans.

NACA Requirements and Qualifications

Before you assume the NACA mortgage program is too good to be true, there are certain requirements you’re going to have to meet to qualify. Unlike traditional lending practices, NACA evaluates creditworthiness based on character, rather than solely relying on credit scores.

For instance, NACA members won’t be penalized for financial hardship caused by an injury or illness. But you must demonstrate that you can afford to pay your monthly housing expenses.

These expenses include your mortgage payments, property taxes, homeowners insurance, and HOA dues. And your income can’t fluctuate from month to month.

While there are no income restrictions in the NACA purchase program, earning higher than the median income could limit your home buying options to specific regions. It’s also worth noting that owning another property while closing on a NACA mortgage is strictly prohibited.

Furthermore, as a NACA mortgage recipient, you are expected to engage in a minimum of five membership activities annually. These activities include volunteering at NACA offices, participating in protests, or offering support to other members during the home buying process.

Eligible States

Unfortunately, the NACA mortgage program still isn’t available everywhere, though the organization is working hard to expand across the U.S. It’s currently available in the following states:

Alabama

Arkansas

Arizona

California

Colorado

Connecticut

District of Columbia

Florida

Georgia

Hawaii

Illinois

Louisiana

Massachusetts

Maryland

Michigan

Minnesota

Missouri

Mississippi

North Carolina

New Jersey

Nevada

New York

Ohio

Pennsylvania

South Carolina

Tennessee

Texas

Virginia

Wisconsin

NACA Program Pros and Cons

Here are some of the biggest advantages and disadvantages of taking out a mortgage through the NACA.

Pros

Buying a home with no down payment or standard closing costs

Snag a below-market interest rate on a 15-year or 30-year mortgage

No credit requirements or income limits to apply

Receive extensive borrower education and training

Cons

Time-consuming application process

Program isn’t available in all 50 states

There are limits to how much you can borrow

You’ll have to pay for property taxes and homeowners insurance

NACA Loan Limits

The NACA home buying program has loan limits that cap your mortgage amount. The purchase price of a home cannot exceed the conforming loan limit, which is $647,200 for a single-unit property in most states. The conforming loan limit for a single-unit home in Alaska and Hawaii is $970,800.

Who qualifies for the NACA program?

The NACA mortgage program is very generous, but there are several steps you’ll need to take before you can close on your home. Here are the seven steps you’ll take to complete the NACA loan qualification process.

1. Attend a free homebuyer workshop

If you’re considering applying for a NACA mortgage, you’ll first have to attend a homebuyer workshop. During this free workshop, you’ll learn more about homeownership and how to qualify for the NACA mortgage program. Then, you can register on the company’s website to reserve your spot.

2. Meet with your housing counselor

Once you’ve completed the homebuyer workshop, the NACA will assign you a housing counselor to guide you through this process. Your housing counselor will help you determine an affordable monthly mortgage payment and help you come up with a reasonable monthly budget. You’ll continue to meet with your counselor until you’ve qualified for the NACA housing program.

3. Attend a NACA purchase workshop

Once you’ve qualified for the mortgage program, you must attend a purchased workshop at the NACA office. During this workshop, you’ll review the home purchase process and work with a real estate agent to help you find the right home.

4. Receive a property qualification letter

Once you’ve chosen the home you plan to buy, you’ll have to get in touch with your housing counselor again. They will help you secure your qualification letter.

This letter states that you are qualified to purchase the home you’re interested in. Your NACA counselor and real estate agent can also help you draft an offer on the home.

5. Get your home inspected

Before you can purchase a home, it must pass a NACA home inspection and pest inspection. If the inspection reveals any problems with the home, you must resolve those issues before you can close on the home.

6. Meet with your mortgage consultant

Throughout this entire mortgage process, you should be saving money, maintaining your income level, and paying your bills on time. At this point, you’re going to meet with your mortgage consultant to prove that you’ve met the required guidelines and are ready to move forward with the mortgage application.

7. Close on your mortgage

Now it’s time to close on your home! There are no closing costs for a NACA mortgage. Additionally, NACA members do not pay private mortgage insurance (PMI).

Instead, your NACA membership provides you with a post-purchase assistance program through NACA’s Membership Assistance Program (MAP). But this is the final step that allows you to close on your new home and finalize the process.

Alternatives to the NACA program

The NACA program may not be suitable for everyone, or you may not qualify. If this is the case, consider other mortgage programs that may be available to you.

FHA Loans

For low-to-moderate income borrowers who may not meet the stringent requirements of conventional loans, the Federal Housing Administration offers the FHA loan program. With lower down payment needs and more lenient credit score standards, these loans provide a viable option for those looking to finance their first home.

USDA Loans

The U.S. Department of Agriculture extends its support to those seeking to purchase a home in rural or suburban areas through its USDA loan program. These loans offer attractive terms such as low or no down payment options and competitive interest rates, with the aim of fostering home ownership in less densely populated regions.

VA Loans

As a way to show appreciation for the sacrifices made by military service members, veterans, and their surviving spouses, the Department of Veterans Affairs provides VA loans.

These loans, exclusive to eligible individuals, boast features such as no down payment requirement, no private mortgage insurance, and interest rates that are often more favorable than those of traditional loans.

First-Time Homebuyer Programs

For those entering the housing market for the first time, many states and local governments offer programs tailored to their needs. First-time homebuyer programs often provide financial assistance in the form of lower interest rates and down payment assistance, as well as other incentives, making homeownership a reality for those who may not have the funds for a down payment otherwise.

Down Payment Assistance

To help alleviate the burden of the upfront costs of buying a home, down payment assistance (DPA) programs are available from government agencies, non-profit organizations, and private lenders.

These programs provide homebuyers with the necessary funds to cover their down payment, allowing them to get one step closer to affordable homeownership.

National Homebuyers Fund

As a non-profit organization, the National Homebuyers Fund offers down payment assistance to low-and moderate-income homebuyers in the form of grants that do not need to be repaid. Their mission is to provide a helping hand to those who may not have the resources to make a down payment on their own.

Chenoa Fund

The CBC Mortgage Agency’s Chenoa Fund is a down payment assistance program that provides low-and moderate-income homebuyers with up to 3.5% of the home’s purchase price. This support is provided through either forgivable or repayable second mortgage loan options.

Bottom Line

If you’re concerned that you don’t have the down payment or credit requirements necessary to apply for a traditional mortgage, a NACA mortgage may be a suitable option. Borrowers that qualify could receive low-interest mortgages with no down payment, closing costs, or fees. The application process is tedious, but the benefits can help you achieve the dream of homeownership.

Frequently Asked Questions

Is there a minimum credit score requirement for the NACA program?

No, NACA does not consider credit scores for mortgage approval. Instead, they look at your payment history and ability to make future mortgage payments.

Is there an income limit to qualify for the NACA program?

There is no strict income limit to qualify for the NACA program. The program is designed primarily to assist low- to moderate-income individuals and families, but it does not set an upper limit on income. The focus is more on your ability to afford the mortgage payments, and whether you meet other program criteria.

How long does the NACA mortgage process take?

The time frame can vary depending on individual circumstances, but generally, it takes several months from attending the initial workshop to closing on a home. The more promptly you can provide the required documentation and fulfill program requirements, the quicker the process will likely be.

How does the NACA mortgage differ from a traditional mortgage?

NACA mortgages typically offer more favorable terms compared to traditional mortgages. They come with no down payment, no closing costs, and no requirement for private mortgage insurance (PMI). The interest rates are often below market rate as well.

Can I use a NACA mortgage to refinance my existing loan?

No, NACA mortgages are designed for the purchase of a primary residence only. They cannot be used for refinancing existing loans or for investment properties.

Inside: Looking for a job that pays at least $25 per hour? This list has the best jobs that fit that description. Each job offers unique benefits and opportunities, so take a look and see if any of them match your interests and skills.

Making $25 an hour is not a pipe dream; it’s a viable reality for thousands of people worldwide.

Earning such an income not only instills a sense of financial well-being but also provides a robust platform to plan for the future.

Today, we dive into elucidating the different opportunities potential jobs offer, aligning your skills and experience with an hourly rate that feels just right for your wallet.

Hence, securing such a job is not a function of luck but more a strategic alignment of skills, passion, and industry demands. But if you’re not entirely sure about where to begin or how to hone your skills for these high-paying jobs, don’t worry.

Imagine earning smooth entry-level jobs 25 an hour, all from the comfort of your workspace. Sounds enticing, right?

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Jobs That Pay $25 an Hour

This section will highlight various professions across distinct fields that provide such a desirable pay rate.

Looking for jobs that pay $25 per hour? We’ve got you covered.

Whether you’re transitioning careers or just starting, this list could help you discover a role that fits your skills and experience.

1. Paralegal

A paralegal role is an excellent job choice due to the vast knowledge gained in the field of law and legal procedures.

Being a paralegal involves a variety of interesting tasks, such as helping lawyers prepare for hearings, trials, and corporate meetings.

This position is not solely monetarily advantageous, it also presents opportunities for growth and professional development in the legal sector.

Earning Potential: It offers rewarding prospects with an average pay of $25 per hour, with the potential to earn up to $40 an hour depending on experience and expertise.

2. Landscaper

Why toil in a stuffy office when the great outdoors can be your workspace? Relish the satisfaction of planting, pruning, and mowing yourself into a healthier, happier lifestyle.

Ideal for nature enthusiasts and people persons out there, landscaping combines green-thumbed work with personnel management. A knack for the outdoors and previous work experience will be your stepping stones, while a certificate in grounds maintenance can make your application stand out.

Start by volunteering in your local community gardens or offering your services to neighbors. Through this, not only will your skills blossom, but your resume will flourish, too.

Earning Potential: You can expand your lucrative landscaping journey by owning your own company and training others to be laborers.

3. Truck Driver

Why is it a top-tier job, you ask? Consider this: truck drivers are the beating heart of global commerce, pivotal figures in ensuring warehouses stay stocked and goods reach their desired destinations. Plus, you’re free of the traditional office environment.

This job is perfect for those who prefer to work alone as well as those who prefer delivery routes that often stretch into the night.

You must be over the age of 21 years old and able to pass a CDL exam. Many truck drivers to a training course to get a jumpstart in the industry.

Earning Potential: Many truck drivers start their own company and will employ a couple of rigs to make passive income.

4. Social Media Marketing

Do you have a knack for creating engaging captions or a Sherlockian eye for data? Then Social Media Marketing could be your calling.

This position, hot in demand and rewarding, calls for creativity and analytical prowess.

Why is it a top job? Well, it’s not for the adrenaline rush of its fast pace. It’s the fact that you get to put your tech-savviness to great use. Social media marketers nurture and grow brands through smart strategies and engaging content.

Earning Potential: Many people start working for someone else as a Social Media Coordinator and then go on to open up their own business.

5. Event Planners

As an event planner, you are the unseen forces behind flawless galas, memorable weddings, and standout corporate functions. If you thrive on creativity, organization, and people skills, you will ensure that each event is meticulously executed.

This role allows you to blend creativity with pragmatic decision-making: from the captivating process of selecting venues, and coordinating with caterers

It’s a dream job for you if you love putting smiles on people’s faces and making their day unforgettable.

Earning Potential: An enticing reason is its attractive pay rate: on average, $24-28 per hour, peaking up to $40, with the potential of a quick pay raise. Plus those lucrative tips!

6. Mechanical Technician

If you’re seeking a rewarding, high-paying role that gets you hands-on with varied machinery, then a Mechanical Technician career.

This role is particularly apt for those with a fascination for machinery and a problem-solving mindset. To climb the ladder to success, one needs to keenly understand how to operate and maintain industrial machines, prevent damage, and optimize performance.

So gear up to diagnose, adjust, repair, and don’t forget – your hands, mind, and machines are a team.

Earning Potential: With an average pay of $26 per hour, you can start repairing machines and set up your own company.

Virtual Savvy

If you’ve ever wanted to make a full-time income while working from home, you’re in the right place!

This intensive training combines thousands of hours of research, years of experience in growing a virtual assistant business, and the power of a coach who has helped thousands of students launch and grow their own businesses from scratch.

Swipe our exact methods to start earning a living from anywhere as a VA – no experience needed!

Learn More

Download Free Checklist

7. Maintenance Technician

This job is best suited for those who enjoy diagnosing technical puzzles and are adept at hands-on solutions.

By developing a strong mechanical aptitude, attention to detail, and top-notch problem-solving skills. Remember, your primary duty is ensuring machinery and equipment operate smoothly – the backbone of any industry.

Start by checking out some free online webinars or training programs related to industrial maintenance.

This is a low-stress job that pays well without a degree.

Earning Potential: As an entry-level worker, you can start by having a vocational certification or general education diploma (GED).

8. HVAC Technician

This role is perfect for those who love hands-on work and can’t get enough of problem-solving – who wouldn’t enjoy the thrill of being an office’s last defense against an impending heatwave?

The key to thriving in this breezy career path is training – dive into an HVAC training program at a vocational school or consider an associate degree in RACH (refrigeration, air conditioning, and heating).

Earning Potential: Being an HVAC technician pays around $25.75 an hour, which will keep your bank balance healthily ‘ventilated’. By having experience, your hourly wage can increase more.

9. IT Support Specialist

If terms like configuring, maintaining, and troubleshooting tech equipment are your weekend chat topics, you’re the perfect match for this.

Thanks to Google’s free certification program, you can start this job by having online training in your spare time.

Start your journey by heading over to Google’s free IT certification program today. Master the IT realm, earn well, and enjoy your work- the trifecta is right there!

Earning Potential: An IT Support Specialist has an average above $25 an hour wage and could rise to $51 an hour for having experience.

10. Day Trader

By poised as a top job due to its flexibility and potential for high earnings, day trading allows you to take full control of your income by making well-informed decisions about the financial market.

It’s perfect for those with an acute mind for numbers, an unflappable nerve, and those who enjoy working from the comfort of their study.

All it takes to get started is some knowledge about the stock market – something you can easily acquire by attending a free webinar or training, which is accessible online!

Of course, remember the golden rule – never invest money you can’t bear to lose. Now, conquer the finance world, one trade at a time!

Earning Potential: By having the eagerness to be a learner and acquire more knowledge about this job, you can earn way higher than you thought. But, there will always be a risk when trading stocks.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

11. Bartender

This job is perfect for friendly individuals! As you’re the life of the party.

Your life will be as vibrant as a well-mixed cocktail—chock-full of lively conversations and new friendships.

Bartending has a steep learning curve, but the payoff is big as it is a job that pays weekly and even daily. Know your spirits, perfect your pour, and master the mix—each skill is a toast to your increasing bank balance.

So, roll up your sleeves, flash that charismatic smile, and prepare to shake things up in the bustling world of bartending.

Earning Potential: With an entry-level job—at a local pub or a fine dining restaurant, you’ll get paid handsomely, at least $25 an hour.

12. Mechanic

The job is a perfect blend for those with a knack for solving complex issues and have the stamina to be on their feet for prolonged periods.

If you’re not averse to the roar of engines and the smell of oil, you might be the grease monkey we’re looking for.

This job is perfect for dipping your toes in oily water. So, go ahead, rev up your career with a mechanic job!

Earning Potential: Personally, my independent auto mechanic makes way more than $25 an hour, but he has years of expertise and opened his own shop.

13. Transcription

Transcription suits anyone craving flexibility or looking to dip their toes into fields like legal, medical, and entertainment.

To shine, you’ll need to master speed, accuracy, and the art of capturing every ‘um’ and ‘ah.’ Noise-canceling headphones and a quiet workspace are your best friends.

Kickstart your move to transcription with free training like a mini-course to see if you like it. Gain insights into making money and build your portfolio.

This high-demand job needs skills you convert audio into text.

Earning Potential: By working remotely as a transcription, you can earn an impressive $25 an hour or more.

Transcript Proofreading

Get the step-by-step guide Caitlin Pyle used to build a thriving at-home business making a full-time income!

A booming legal industry means that transcript proofreaders are in higher demand than ever…

Enroll Now

14. Accountant

Start your second act as an accountant today. The balance sheets await your expertise.

By aiding your clients in reviewing their financial information, preparing tax and finance documents, and updating their changes in tax laws or governmental regulations. Certified Public Accountants (CPAs) can earn exceptionally well.

The longer you’re in the industry, the more you can be able to demand potential compensation for your service. Just by conducting audits, successful financial and bookkeeping strategies. CPAs perform a pivotal role that justifies their earnings.

Earning Potential: Right now, there is a severe shortage of accountants graduating from college. So, your earning potential will substantially increase with each year of experience, and possibly earn up to $50 an hour.

15. Proofreader

Proofreader is an ideal job for detail-oriented individuals with a passion for perfect punctuation, splendid spelling, and grandiose grammar.

Did you get a degree in English or similar? Perfect! But remember, while it helps, it isn’t a must-have.

It’s an excellent stepping stone for a stay-at-home parent or anyone seeking to make some extra cash it is one of the best jobs for moms. So hop on the proofreading wagon and ride your way to a more profitable future!

Earning Potential: Just by sitting and reading on your couch, you can now hop on and start earning $25 an hour depending on experience.

16. Recreational Therapist

Bring great immense job satisfaction by improving the lives of those grappling with illness and disability.

To get started, all you need is a bachelor’s degree in recreational therapy and then obtain a Certified Therapeutic Recreation Specialist credential.

So, why wait to become an everyday hero with a salary that smiles back at your bank account?

Earning Potential: You can earn more than $25 an hour by being a Certified Therapeutic Recreational Therapist.

17. Dental Assistant

Do you have strong communication skills, and the ability to partake in a hands-on career?

Just sterilizing equipment or lending a diligent hand during treatments will be part of your daily grind. Ensure every instrument screams ‘clean’ before the dentist reaches for it.

To become a dental assistant, you typically need to earn a certification or diploma through a dental assisting program, which often takes about a year to complete.

On-the-job training may also be required, during which you’d learn about dental procedures, patient care, and office duties under the supervision of a dentist.

You may have found the tooth fairy’s best job yet! Dive in!

Earning Potential: With a wage average of $19 an hour and earning up to $25 just being a Dentist Assistant.

18. Certified Nursing Assistant

Have a career dream to dive into the healthcare industry? Familiarize yourself with basic health practices, hygiene, and safety procedures.

Start your journey as a Certified Nursing Assistant by attending to patients, assisting nurses, and providing emotional support to everyone. You will have to start a training program, but thankfully there are many to choose from.

Earning Potential: This career pays more than $25 an hour and might increase through experience and skills.

19. Housecleaners

According to Zippia, 48.9% of the housecleaner’s qualification is to have a high school diploma, but experience could help. You must have a strong understanding of cleaning procedures and practices.

Also, you can consider taking a course to learn about safety guidelines and recommendations.

Other important attributes include attention to detail, physical stamina, and excellent time management skills.

Earning Potential: Whether you’re a single mom or a high school graduate, you can potentially earn up to $25 an hour.

20. Nanny

Fascinated by child psychology or studying pedagogy? Or just love kids? Then, this job is tailored for you; it offers both consistent income and practical field experience.

Getting started can seem daunting, but it doesn’t have to be. Step into the kiddie world, it might just be the best move you make. Where you are not required to pass any school diploma.

You can find plenty of nanny gigs on Sittercity.

Earning Potential: If being a nanny is just a child game then I want in and earn up to an incredible $1000 to $1100 a week.

21. Delivery Drivers

Welcome to the job of a delivery driver, a blend of independence and earning potential on wheels. When you are good at your job, you don’t have customers wondering how late does Amazon deliver.

This career is a perfect fit for introverts who prefer their own company, the job offers flexibility with the ability to set your hours.

But, keep in mind that larger roles, such as FedEx, may require truck driving experience, the ability to lift heavy boxes, and the completion of a few additional checks.

Earning Potential: Most delivery drivers for FedEx and UPS are union workers. Thus, they have the union to fight for pay increases. Plus you can increase your salary by moving up in the ranks.

22. Licensed Plumbers

Get ready to hop into commercial, residential, and industrial projects, working flexibly based on your schedule.

If you love problem-solving and can handle the occasional wade through the muck, then this amazing career is for you! Don’t worry about your expertise level; It’s the perfect time for you to dip your toes into the world of plumbing.

Earning Potential: Don your gloves, grab your tool kit, and join the ranks of expert plumbers making upwards of $25 an hour.

23. Athletic Trainers

Are you into sports and fancy being in the thick of the action?

You are considering becoming an Athletic Trainer – a well-paid role that combines both your passions brilliantly. Then, get to work closely with athletes, which means you’re right at the heart of the sports action.

You’ll need to be certified and licensed in healthcare to offer your professional services. The ball’s in your court!

Earning Potential: Earning about $25 per hour, it’s among the few amazing careers that can up your game financially and health-wise. Also, it may take you to the Super Bowl as the team’s athletic trainer!

24. Customer Service Managers

So, you’re a people person with a knack for solving problems? Consider a job as a Customer Service Manager.

This job is best for ambitious, empathetic individuals who love making a difference in customer experience, enhancing team performance, and ensuring business profitability.

Want to up your game? Brush up on customer relationship tools like Hubspot or project management tools like Asana. Then, prepare to rule the customer service realm as an expert Customer Service Manager.

This can be a great non-phone work-from-home job as many customer service requests are handled through chat and email.

Earning Potential: One of the amazing careers that pay a satisfying $25 per hour, it’s a chance to flex those crucial customer service muscles while managing a team.

25. Freight Broker

With an average pay topping most traditional roles, this often-overlooked profession is a gem amidst the rubble.

Here’s why: Despite its lucrative nature, competition in freight brokerage is surprisingly low.

Jumpstart your journey with a free webinar or training – there are many available online. This will equip you with vital information about the ins and outs of the role and the industry.

Earning Potential: You will be surprised to learn what a freight broker’s salary can be.

Freight 360

Designed as a 101-level course on freight brokerage, you’ll learn the basics of freight brokering in this online course.

This course is designed for freight brokers in any setting, regardless of their employment status.

This course is designed to help you source more leads and move more freight. Or even start your brokerage!

Start Now

FAQs

Have you ever dreamt of earning $25 an hour with flexible hours at your convenience?

The list above are some of the jobs that can earn $25 an hour. However, try to evaluate yourself if the requirements perfectly suit you. By having skills and experience on the said job you can ace up and boost your chances of getting one of the high-paying jobs above.

Unlock and upgrade your skills now by attending any training that aligns with your dream job. Be able to receive a rewarding amount of earnings in your pocket!

These amazing careers above can fetch you at least $25 per hour. Start earning big and turn your dream into your paycheck.

Improving your skills through attending training, updating certificates, and seeking additional knowledge in your field. Plus, It increases your chances of landing a job that pays $30 an hour.

Actively applying for new jobs, particularly those that value your enhanced skills, can open the door to higher-paying opportunities potentially enabling you to reach that $30 an hour wage.

So master the craft, build your credibility, and let your work do the talking.

The ball is in your court now. Step up and start crafting your destiny, one skill (and dollar) at a time. So, start attending any training that is aligned with the career you’re looking for.

Find out what should I do for a living. Sign up for a free webinar or training. Sites like Udemy and Coursera offer a plethora of free courses to help you fine-tune your skills or discover new ones.

Which Applications will you Submit for jobs paying 25 an hour?

The possibilities in today’s remote job market are exhilarating. Amid the myriad of options, some rake in at least a solid 25-dollar-an-hour job.

Begin by brushing up on your skills or discovering new ones through free webinars or training sessions that align with your chosen profession to increase your qualifications. Make sure your resume is polished and start applying to suitable jobs in your field. The next step is nailing that job interview.

Thus, finding and applying for such lucrative positions is not just an aspiration for a better standard of living, but a practical step towards improved financial stability.

Remember to job-seek smartly and relentlessly. The end game is finding that perfect remote job – working on your terms, from your comfy corner of the world, and padding your bank account one $25 hour at a time. It’s time to get cracking!

Know someone else that needs this, too? Then, please share!!

Online banking has made managing money easier than ever. However, it has also led most people to rely solely on digital assets.

Precious metals are a popular investment choice for people wishing to buy a tangible asset that retains its value over time. In particular, gold and silver generally maintain their value even when the stock market faces major financial fluctuations.

They also do well in times of inflation and political uncertainties. When traditional stocks fluctuate due to these external factors, precious metals only become more valuable.

Investors who prefer a hands-off approach have the option of purchasing gold and silver stocks. These stocks are traded daily just like any other stock. However, many people prefer to keep a physical store of their precious metal.

While relatively illiquid, buying physical gold and silver is typically viewed as a long-term investment. It’s certainly a practical option if you’re concerned about inflation or the future of fiat currency.

Best Places to Buy Gold and Silver Online

eBay and Craigslist are both great places to start. But unless you’re confident that you’re dealing with a reputable seller, you might want to look into other sites that specialize in precious metals.

To help you find the best place to buy gold and silver, we’ve compiled a list of the best online gold dealers.

Money Metals Exchange

Money Metals Exchange, or MoneyMetals.com, has received several accolades, including the “Best Overall Gold Dealer” by Investopedia.

They’ve also done over $2 billion in transactions.

Money Metals Exchange has an A+ rating from the BBB. They offer 24/7 online support, indicating a strong commitment to customer service.

Products include gold, silver, rhodium, palladium, and platinum. You can also invest in a self-directed precious metals IRA.

You can often find great deals and promotions on Money Metals Exchange, so it’s a site you may want to bookmark.

Silver Gold Bull

Silver Gold Bull offers a suite of services for their customers. In addition to buying and selling through the company’s website, you can also store your hard assets in their secure facilities.

Another helpful feature is an automated spot alert. You can get up-to-the-minute data on where prices are throughout the day and buy when they hit your target price.

Plus, the Silver Gold Bull sales team is full of seasoned veterans, so you can get answers to your questions from people who truly know their stuff.

The company sells a wide range of gold, silver, platinum, palladium, copper, and collectibles online and over the phone.

Gainesville Coins

With an A+ rating from the Better Business Bureau, Gainesville Coins has been keeping customers happy for more than ten years.

In fact, the company has also received a five-star rating from the National Inflation Association—the only bullion dealer to receive such a distinction.

You’ll find a wide selection of gold, silver, platinum, and other metals like copper, palladium, and rhodium on the Gainesville Coins website.

The company also sells pre-1933 gold and has an extensive clearance section with time-sensitive deals. In addition, you can calculate shipping based on your zip code and items placed in your cart. Only Florida residents pay sales tax on their purchases.

Gainesville is one of the best places to buy gold online.

Golden State Mint

Golden State Mint is a trusted source for premium precious metal products, providing buyers direct access to top-notch items straight from the manufacturer.

With 40+ years of experience, the company inspects each piece with precision before shipment, ensuring its authenticity and quality.

Customers can rest assured that all products are brand-new, never previously owned or circulated.

Investing in precious metals for retirement? Golden State Mint offers expert support in establishing an IRA account, stocked with an array of products that fully comply with IRS standards.

Whether you’re a seasoned pro or just starting out, Golden State Mint is committed to helping you achieve your investment objectives through purchasing physical gold and silver.

Provident Metals

What started as a precious metals trade show business has launched into one of today’s largest online bullion dealers.

Provident Metals holds several professional memberships. These include the American Numismatic Association, the Professional Coin Grading Service, and the Numismatic Guaranty Corporation.

Provident’s collections include gold, silver, copper, platinum, and palladium, with an extensive selection of each one. In addition to coins, rounds, and bullion bars, Provident Metals also sells U.S. and foreign coins, wholesale products, and IRA bullion products.

You’ll appreciate the company’s attentive service and timely delivery. And if you order $99 or more, shipping is free; otherwise, it costs just $5.95 to ship.

APMEX (American Precious Metals Exchange)

APMEX is one of the largest online dealers in the world, which allows it to pass along savings to its customers. This is due to the sheer volume of business it does each day. Not only can you buy silver, gold, and other metals, you can also sell or trade from your current holdings.

The selection is huge, covering the major precious metals, historic gold coins, “elite” coins, old banknotes, and foreign coins. It also has an extensive collectibles section with rare coins and currency from around the world.

Scottsdale Mint

Scottsdale Mint (formerly Scottsdale Silver) focuses on silver and gold while also offering each in different collectible series. They sell both types of metal in coins, bullion bars, and rounds, with a particular premium set on artistic minting.

For example, some recent popular collectible sets include a Vikings series and a Godfather set featuring images from the iconic movie franchise.

To qualify for free shipping with insurance, you must make a minimum purchase of $500. This may seem steep compared to some other companies providing free shipping at $99. However, much of the allure of Scottsdale Mint comes from the company’s creative minting process.

JM Bullion

Shipping is free on all JM Bullion orders over $199. They sell physical gold, silver, platinum, and other bullion that arrive directly at your door. They inspect every inventory item to ensure only quality products are sold. Payment options include Visa, MasterCard, PayPal, PayPal Credit, bank wires, paper checks, and Bitcoin.

JM Bullion is fully accredited at both state and federal levels. They also have reliable customer service that you can reach via phone or 24-hour Live Chat. Sign up for email, and they will mail you exclusive sales and promotions.

Kitco

Kitco has many precious metal types, including gold, silver, palladium, platinum, and rhodium.

The website also provides a slew of data and news to help you with your portfolio decisions. You can even download apps for gold news, market alerts, and scrap value calculations for your smartphone.

GoldSilver.com

As its name implies, GoldSilver solely sells gold bars, coins, and jewelry and silver bars and coins. They also sell products such as safes and storage containers. You can also create an account to sell back your gold bullion, gold coins, and silver bars through the website.

There’s a flat rate shipping fee of $25 for any order under $500. Otherwise, shipping, handling, and insurance are free. In addition to traditional payment options, GoldSilver also accepts PayPal.

Silver.com

Don’t be fooled by the name. While Silver.com could be the best place to buy silver online, they also sell various gold, platinum, and copper products. In addition to government mints, you can also find gold coins, gold bullion, silver coins, silver bars, and more from private domestic and foreign mints.

The order threshold for free shipping is high at $3,000, but their tiered flat rate shipping fees are reasonable. Smaller orders up to $299 cost just $4.95 for shipping and insurance. The highest tier of orders from $1,000 to $2,999 cost just $9.95.

SD Bullion

Silver, gold, platinum, and copper comprise SD Bullion’s core product line, with coins, bars, and rounds from around the world.

They also sell lead bullion in the form of ammo as well as vaults, survival food, and herbal medicine. In addition, SD Bullion offers weekly specials and currently has a promotion for all orders shipped at just $7.77.

Texas Precious Metals

Texas Precious Metals offers several unique features, including the ability to sign up for limit orders. For example, you can automatically place a standing order if gold or silver reaches your desired value.

All orders ship for free using UPS Next Day Air, and all orders ship within three business days of payment. The website offers a curated selection of gold coins, gold bars, silver coins, silver bars, and pre-1933 gold.

Golden Eagle Coins

Golden Eagle Coins is a place for gold and silver investors and collectors alike. Take one look at their website, and you’ll see why — their inventory is enormous.

Prices are updated in real time as their quotes come directly from the commodities exchange. This is a great site to use if you are researching when to buy.

Shipping is free on orders $99 and over. Also, be sure to check out their bi-monthly blog for new items and savings.

Gold Dealer

Quoted on CNN, CNBC, and PBS, Gold Dealer offers a complimentary newsletter written by industry masterminds Ken Edwards and Richard Schwary.

They have a physical office moments away from LAX. However, if you don’t want to travel to Los Angeles, you can visit website instead. It has everything you’d expect from a reputable gold dealer.

Gold Dealer offers free, insured shipping on every order. Their low prices are the result of reducing operating expenses over time.

Monarch Precious Metals

Monarch Precious Metals is a newer company established in 2008 to help with the immense public demand for gold bullion. They only use quality metals, so anything you buy from them will be .999+ fine.

They triple-check the weight of every bar they ship. If it is ever underweight, they re-melt it. If it’s ever overweight, it’s a win-win for you because they always let it pass and ship it as is.

Everything is custom hand-poured and marked in the old way, giving their metals a unique, old-fashioned look. They accept all methods of payment except PayPal, and every order is properly insured.

CMI: Gold & Silver

An A+ Accredited Business, CMI is located in Phoenix, Arizona. However, CMI will buy and sell precious metals online to investors all over the United States.

Its president, Bill Haynes, considers it his responsibility to educate the public about the dangers and benefits of buying gold and silver products.

He regularly updates his blog on global factors that influence the prices of metals. It’s a helpful resource for determining when to buy.

With solid prices, IRAs, and a plethora of educational material to read, CMI should be a website you routinely check if you are a serious investor.

BGASC: Buy Gold and Silver Coins

With thousands of positive customer reviews, it’s not hard to realize why BGASC is an A+ BBB accredited business. They offer free shipping on orders $99 and up. Every order is insured while in transit. Additionally, they always ship your order the next business day.

BGASC is one of the largest coin and bullion dealers in the US. They sell nearly every type of US coin ever made. They also have a large selection of mints from other countries, such as China, Mexico, and Canada.

The Basics of Precious Metals

Before buying gold or silver, it’s important to understand the different forms they come in. Each type has its pros and cons. Some people focus on one kind they prefer, while others create a diverse mix of different kinds. Before you buy precious metals, figure out which strategy is best for you.

Silver

Let’s start by talking about silver. Typically, you can buy silver either in the form of bullion or junk silver. Silver bullion refers to silver as a bar, coin, ingot, or round.

Silver Coins

The most popular silver coins you’ll come across are as follows:

American Silver Eagle

Canadian Silver Maple Leaf

British Silver Britannia

Mexican Silver Libertad

Austrian Silver Philharmonic

South African Silver Krugerrand

Australian Silver Kangaroo

Chinese Silver Panda

Junk Silver

Junk silver, on the other hand, is any type of old U.S. currency containing real silver. Any U.S. half-quarters, quarters, or dimes minted before 1965 are considered junk silver. However, in reality, they aren’t very junky at all.

You can sometimes find junk silver below the spot price. This can often allow you to start with a profit on your investment.

Silver Rounds

Silver rounds are privately minted silver pieces shaped like coins but produced by private mints. They are not government minted or legal tender, so they are not referred to as coins. The most popular silver round is the American Silver Buffalo. However, Scottsdale Mint also produces some beautiful rounds called “Omnia.”

Gold

Gold also comes in bars and coins, each one giving you a different type of entry point into precious metal investing. Buying gold coins is the easiest way for gold investors to start because you can begin by just purchasing a few at a low price point.

Gold Coins

The most popular gold coins to buy are as follows:

American Gold Eagle

Canadian Gold Maple Leaf

British Gold Britannia

British Gold Queen’s Beast

Mexican Gold Libertad

Austrian Gold Philharmonic

South African Gold Krugerrand

Australian Gold Kangaroo

Chinese Gold Panda

Gold Rounds

Similar to silver rounds, the most popular is the American Gold Buffalo.

Perhaps you’re stocking up as a hedge against inflation or to use as currency in a potential crisis. If so, you’ll find that coins of any type (gold or silver) will be easier to barter with than bars.

If you decide to buy bars, you can get them in different sizes to suit your space or budget. For example, you can purchase 1 to 10-ounce gold bars or up to 100-ounce silver bars. You can even find bars at just a fraction of an ounce if you want to start small.

One of the most significant advantages of this tactic is that you get the lowest premium when you buy larger bars. So while they might not be as easy to sell when you’re ready, you’ll get a better value if you can make that large of an investment upfront.

Copper

While silver and gold are the most popular, there are other precious metals to consider as well. For example, copper also comes in bars, rounds, and coins and is very affordable for novice investors.

Some experts believe it’s a wise investment opportunity because of its rising demand and shrinking supply.

Platinum and Palladium

Platinum is perhaps the most precious of all metals. It’s 15x rarer than gold, and its value exceeds that of gold. Platinum is usually sold as coins minted in the U.S., Canada, or Australia.

Palladium is similar to platinum in its properties and is actually 30x rarer than gold. Because these metals are so rare, not many people invest in them. However, a growing number of investors are adding them to their portfolios. It’s something you may want to consider as well.

Gold and Silver: Frequently Asked Questions

Where is the best place to buy gold?

The two best places to buy gold are online retailers and local coin shops.

Online retailers, such as the ones we’ve listed above, offer a wide selection of gold coins, bars, and rounds at competitive prices. These retailers often offer free shipping and insurance, making it easy and convenient to buy gold from the comfort of your own home.

Local coin shops are another great option if you want to prefer gold in person. These shops often have a knowledgeable staff who can help you find the right gold products for your needs and budget. You may also be able to negotiate on price of the gold.

Where is the best place to buy silver?

The best place to buy silver is typically also the best place to buy gold: online dealers and local shops. These options provide a wide range of products to choose from and allow you to compare prices and quality before making a purchase.

Online dealers offer the convenience of shopping from home, while local shops provide the advantage of in-person interaction with knowledgeable staff who can answer your questions and guide you towards the right products for your investment goals.

Whether you want to buy silver coins or silver bars, these options typically offer competitive prices, flexible shipping policies, and convenient payment options.

We recommend checking out at least a few of the best online gold dealers we mentioned above, regardless of what your needs are. Compare prices, selection, and shipping policies on numerous sites.

What is the cheapest way to buy gold and silver?

The most cost-effective method of acquiring gold and silver is by buying bars. They tend to have smaller markups compared to spot prices compared to coins, due to their lower production costs.

Buying in bulk is also a smart way to lower the cost per ounce as many online dealers offer discounts for larger purchases.

Is it safe to buy gold and silver online?

Buying precious metals online is as safe as any other transaction you make online. It’s also just as safe to buy online is as it is to buy from a physical retailer. The key is to buy gold and silver from a reputable gold dealer.

Is it better to buy gold coins or bars?

There is no right or wrong answer to this question. It depends on your situation, your needs, your budget, and what you prefer. As mentioned, it’s typically cheaper to buy gold bars. However, you will most likely get a better value from gold coins when it comes time to sell your gold.

Gold and silver coins and small bars offer more flexibility when it comes time to sell. Owning smaller units of gold and silver allows you to sell only a portion of your precious metals instead of your whole portfolio.

How much gold and silver should I own?

Experts recommend holding 5-25% of your net worth in precious metals. However, it depends on your goals, your situation, and risk tolerance. Precious metals can be a great addition to your portfolio as long as you know why you’re adding it.

Can I store gold at home?

Storing gold in your home offers a sense of security and privacy for your valuable assets. As a form of wealth preservation, it provides complete control without the need for outside storage. However, it’s crucial to be mindful of potential security threats and to ensure your assets are adequately insured.

To mitigate these risks, it’s advisable to implement a secure storage system. Ultimately, home storage is a viable solution for individuals who value personal ownership and control of their gold holdings.

As borrowers gear up for federal student loan bills resuming this fall, they face a revamped landscape that includes a new repayment plan, servicer switches and long call wait times. Another imminent concern: scammers who want to take advantage of the moment.

“Whenever there’s confusion in the marketplace, that’s when the criminal fraudsters get active,” says Clayton LiaBraaten, senior executive advisor at Truecaller, an app that blocks spam calls.