Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

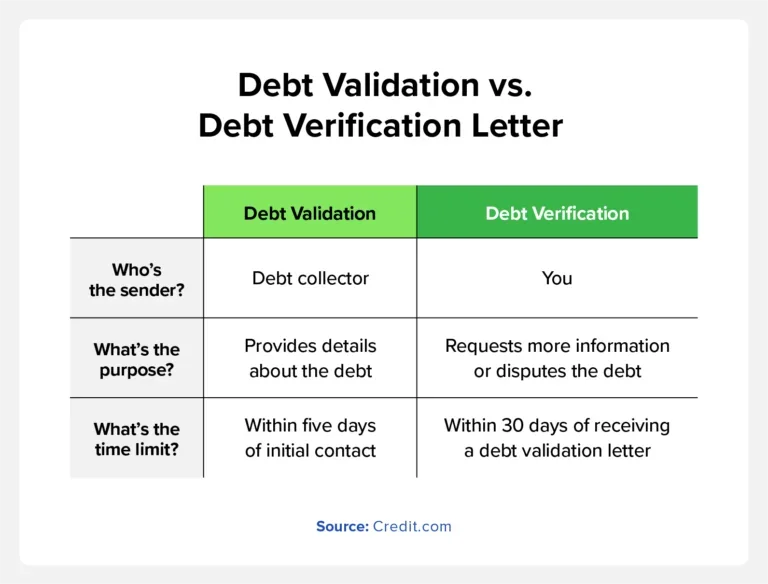

Debt collectors send debt validation letters show what debts you owe, the amount, and to whome you owe it to.

While a debt collector contacting you can be stressful, it’s important to pause and remember your rights as a debtor. Before paying the debt collector, verify that the debt is actually yours. The debt collection industry is subject to mishaps and mistakes, with some individuals being asked to pay debts they don’t owe.

That’s why you should receive a debt validation letter from the debt collector proving the debt is yours. If you still don’t recognize the debt, you can send a debt verification letter requesting more information or disputing the debt.

In this article, we’ll discuss the importance of debt validation letters and what information they should include. We’ll also provide a debt verification letter sample and a free template to help you get started.

Key takeaways:

Debt collectors are legally required to send you a debt validation letter within five days of initially contacting you.

A debt validation letter should include information about the debt, such as the amount you owe and the original creditor’s name.

If you’re unsure if the debt is accurate, send a debt verification letter to dispute the debt or ask for additional details.

Table of Contents:

What Is a Debt Validation Letter?

What Should a Debt Validation Letter Include?

When to Send a Debt Verification Request

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

Debt Verification Letter Template + Sample

How Long Does a Creditor Have to Respond to a Debt Verification Request?

What to Do If a Debt Collector Doesn’t Respond to a Debt Verification Request

What Is a Debt Validation Letter?

A debt validation letter is written correspondence that debt collectors are legally obligated to send you that provides information about the debt they’re collecting. The letter should include details about the debt, the original lender, and the debt collector’s authority to collect the money.

The creditor should send a debt validation within five days of their initial contact with you. If you don’t receive a debt validation letter, the debt collector could be an illegitimate person attempting to scam you. Therefore, you should avoid providing sensitive information to the debt collector until you’ve verified they’re legitimate.

What Should a Debt Validation Letter Include?

According to the Consumer Financial Protection Bureau (CFPB), the debt validation letter should include:

The amount of debt you owe

The name of the original lender requesting payment

The account details associated with the debt

An option to dispute the debt within a 30-day time period

An opportunity to request more details about the original lender

A statement acknowledging that the collector will provide verification if you dispute the debt

When to Send a Debt Verification Letter

If after receiving the debt validation letter and you’re still unsure of whether the debt is accurate, you can send a debt verification request to the debt collector. A debt verification request is a letter that you, as the consumer, can send to the debt collector to ask for information about the debt they’re collecting.

Typically, you have 30 days to send your debt verification request after receiving the debt validation letter. If you don’t send the letter within this time frame, the debt collector will assume the debt is valid and legally continue their efforts to collect.

Debt Verification Letter vs. Debt Validation Letter: What’s the Difference?

It’s important to understand the difference between a debt verification letter and a debt validation letter:

A debt verification letter is a correspondence that you, the consumer, send to the debt collector requesting more information about the debt.

A debt validation letter is a document the debt collector sends to you, providing details about the debt.

Debt Verification Letter Template + Sample

When writing a debt verification letter, it’s important to be clear and concise. State that you’re disputing the debt and list what information you’re requesting from the debt collector.

Below is a debt verification letter sample and a template to help you get started. Remember to use your own information where there is bolded text.

[Name]

[Address]

[Today’s date]

[Name of the debt collector]

[Address of the debt collector]

Re: [Debt account number, if it was provided to you]

Dear [Name of the debt collector]:

I’m replying to your communication regarding a debt you’re attempting to collect. You reached out to me via [phone/mail] on [date] and provided the following account details:

[Account number, if provided]

[Name of the original creditor, if provided]

I am informing you that I dispute the debt you’re claiming I owe.

If you have reason to believe that I’m still responsible for this debt, kindly provide the following details to ensure I have all the necessary information:

The creditor’s name and address who is currently requesting payment

The original creditor’s name and address (if different from above)

The amount owed

The account number

Documentation that proves there is a legitimate reason you think I owe the debt, i.e., a copy of the original contract

The most recent billing statement the original creditor sent to me

An itemized list of any additional interest or fees

An itemized list of any payments since the most recent billing statement

If you’re providing this data to a credit bureau, please report that I’m disputing this debt.

Sincerely,

[Your name]

How Long Does a Creditor Have to Respond to a Debt Verification Request?

There isn’t a specific time frame in which creditors must reply to a debt verification request. However, if you send the debt verification letter within 30 days of receiving the validation letter, they must cease all collection efforts until they respond to your letter and provide verification.

What to Do If a Debt Collector Doesn’t Respond to a Debt Verification Request

If the debt collector doesn’t respond to your debt verification request, it could be due to one of the following reasons:

The debt collector requires additional time to gather the information you’ve asked for.

The debt collector cannot verify the debt.

The debt is beyond the statute of limitations, so the debt collection agency cannot file a lawsuit.

You were dealing with a debt collection scammer.

If you sent the debt verification letter within the 30-day time frame, the debt collector cannot attempt to collect until they provide the information you requested. If the debt collector continues with attempts to contact you, you can submit a complaint with the CFPB, your state’s attorney general’s office, or the Federal Trade Commission.

Debt validation and verification letters can help you exercise your rights and avoid potential debt collection scams. If the debt collector fails to verify your debt, be aware that it may be wrongfully hurting your credit. Check your credit report for inaccurate information and report errors to the credit bureaus to potentially remove the accounts from your credit report.

It’s important to monitor your credit so you can get alerted if inaccurate information is hurting your credit. Try ExtraCredit® for free today for help managing your credit.

Today we’ll check out “Lennar Mortgage,” which is the financing division of parent company Lennar Corp.

If you weren’t aware, Lennar is one of the nation’s largest home builders, and is also nearly 70-years old.

Like many large builders, they have an in-house mortgage company that facilitates their new home sales.

Instead of outsourcing home loan lending to a third-party company, they’re able to provide the customer with a streamlined process from end to end.

Read on to learn more about their history and what types of loan offerings they have available, including special incentives you won’t find elsewhere.

Lennar Mortgage Fast Facts

The home loan division of parent company Lennar Corp.

Lennar is the nation’s second largest home builder, founded in 1954

Formerly known as Eagle Home Mortgage before a name change in 2020

Headquartered in Miami, FL, founded in 1981

Currently have building operations in 26 states nationally

Primarily utilized by home buyers who purchase a Lennar property

Funded over $14 billion in home loans in 2022

Known for offering big mortgage rate buydowns

As noted, Lennar Mortgage is the financing unit of its parent company, Lennar Corp.

While the parent company is nearly 70 years old, Lennar Mortgage is a lot younger.

In fact, they were acquired by Lennar back in 1999, at the time known as “Eagle Home Mortgage.” That company had been around since 1981.

As of December 5th, 2020, they were renamed Lennar Mortgage to make it clearer to customers that the company was part of the Lennar family.

At the moment, they have building operations in 26 states, meaning Lennar Mortgage is essentially available to customers in roughly half the country.

They primarily operate in the states of California, Florida, and Texas, along with the Mountain West and Mid-Atlantic states.

Last year, the company funded over $14 billion in home loans, with about 75% being conventional loans, 15% FHA loans, and 12% VA loans, per HMDA data.

While their website indicates that they offer refinance loans, they primarily serve their own home buyer customers with purchase loans.

Aside from operating a mortgage unit, Lennar also has Lennar Title and Lennar Insurance Agency, which allows them to streamline the home buying process.

They have physical branches throughout the country (where new home communities exist) and roughly 1,200 lending associates.

How to Apply with Lennar Mortgage

To get started, you can visit their website and get pre-qualified for a mortgage, or simply coordinate with your home buying rep after visiting a new home community.

They’ve got local loan officers throughout the country and physical branches in the states where they build homes.

Their new home communities may also have sales offices with lending representatives present.

Like other mortgage lenders, Lennar Mortgage offers a digital home loan experience that is mostly paperless.

It appears to be backed by ICE Mortgage Technology, one of the leading fintech companies in the mortgage space.

Customers can apply from any device and auto-save their loan application to pick up where they left off.

And automatically connect bank statements, tax returns, and income documentation within minutes, with bank-level encryption to provide peace of mind.

On-demand digital mortgage support is also available for those who need help along the way, though most tasks can be completed without the need for human interaction if that’s a preference.

All in all, it appears they offer a good combination of human support, if needed, along with the latest technology for convenience.

Loan Options Available at Lennar Mortgage

Home purchase loans (and mortgage refinances)

Conforming and jumbo loans

FHA/VA/USDA loan options

Fixed-rate and adjustable-rate loans available

They lend on single-family homes and townhomes

As noted, most Lennar Mortgage customers will use the company for a home purchase mortgage.

While they do offer refinance loans, their primary objective is getting their parent company’s home buyers a mortgage.

The good news is they offer all the major home loan types a home buyer would need, whether it’s a conforming loan or a jumbo loan.

Or a fixed-rate mortgage or adjustable-rate mortgage, including the popular 7/1 ARM.

They also offer the complete suite of government-back loans, including FHA, VA, and USDA loans.

Down payments can be as low as zero on the government loan options, or just 3% for the conventional loan options.

They offer financing on primary residences, second homes, and investment properties.

Lennar Mortgage Rates

Once huge advantage to using Lennar Mortgage is their mortgage rate buydowns, which are pretty hard to beat.

Since mortgage rates surged higher, from around 3% in early 2022 to nearly 8%, companies like Lennar Mortgage have been offering large rate buydowns to their own customers.

So those who use the company to purchase a Lennar home can take advantage of big interest rate reductions they likely won’t find elsewhere.

For example, you might see an advertised mortgage rate special of 4.99%, despite the 30-year fixed currently averaging 7.50% or higher.

Or a big dollar amount in incentives, which can be used like a lender credit to cover closing costs or apply toward a rate buydown.

This is their big advantage as a home builder’s captive financing unit. They’re able to offer special deals that can boost affordability, even if market rates are high.

In terms of advertising their rates, you won’t find a page dedicated to mortgage rates on their website.

And these rate specials will vary from community to community nationwide, depending on supply and demand of newly-built homes.

Is Lennar Mortgage Legit?

Yes, they are the official financing division of Lennar, one of the largest home builders in the United States.

In fact, Lennar Corp. was reportedly the second largest home builder in the nation as of 2023, trailing only D.R. Horton.

The company is also publicly traded on the New York Stock Exchange (NYSE: LEN) and is valued at over $34 billion at last glance.

They are a Fortune 500 company as well and date back to the 1950s, which is older than most mortgage companies in existence today.

Lennar Mortgage also has a 4.89/5 star rating on Zillow from over 2,100 customer reviews and holds an ‘A+’ Better Business Bureau (BBB) rating.

Keep in mind that you don’t need to use Lennar Mortgage just because you’re purchasing a Lennar home.

It’s perfectly acceptable to use a third-party lender, though it may be difficult for them to match the pricing incentives offered.

At the end of the day, Lennar Mortgage will likely have a huge leg up compared to other lenders thanks to their ability to structure pricing and rates in-house to boost affordability.

And because they offer a wide range of loan options and a digital mortgage experience, it’ll likely be a challenge for outside lenders to compete.

That being said, always take the time to gather other mortgage quotes and be sure to negotiate with the company.

Simply letting them know you are looking into other financing alternatives could result in more leverage and/or a better deal.

But when it comes time to refinance your loan, they likely won’t be nearly as competitive on pricing. At that stage, you’d probably be better off finding a new mortgage company to work with.

Lennar Mortgage Pros and Cons

The Good

Can apply for a home loan online or at a physical branch

Offer a paperless digital mortgage experience

Integrated title and homeowners insurance companies

Lots of loan options including fixed rates and ARMs

Offer big incentive to home buyers including rate buydown and lender credits

Free credit guidance to those who need to boost their FICO scores

Access to mortgage calculators and learning center online

Excellent reviews from past customers

The Maybe Not

Do not advertise their daily mortgage rates online

Buying a home is an exciting—and typically very expensive—venture. Understanding the mortgage process, your financial status, and what you really want and need in a home are all important to ensuring a desirable outcome when you begin your home search. But what you might not realize is that when you do find the home that ticks most of the boxes, you don’t necessarily have to pay what the seller is asking. Learn more about negotiating house prices below.

Tips for Negotiating House Price

Can You Offer Less Than Asking Price on a House?

It may feel odd to haggle over house price, but you can offer less than what the seller is asking for a home. That’s why it’s called making an offer. The seller doesn’t have to accept the offer, though, and you might find yourself entering into negotiations if you do want the home. During this process, it’s important to balance your desire for the home with a practical approach to how much you should, can, or even want to spend on it.

Tips for Negotiating House Prices

Knowing how to negotiate house price is important because it helps you get a better deal. But you aren’t the only one that might be making an offer, so you also want to follow some best practices so your dream home doesn’t get scooped up by someone else while you’re hedging your bets with the seller.

1. Partner with a real estate agent who can help.

You might start by entering the homebuying process with a bit of help. A qualified real estate agent can serve as your partner as you look for homes and make offers. Here are some of the services a real estate agent can do for you:

Help you drill down to what you really want in a home

Offer greater understanding of the local real estate market

Find homes that meet your criteria that you might not know were for sale or be able to find otherwise

Arrange showings

Act as your go-between and advisor during negotiations with sellers

It’s important to note that not all real estate agents have negotiation experience or even offer this service in an aggressive manner. As a buyer hiring an agent, make sure you look for one with experience writing real estate contracts and negotiating on behalf of clients.

2. Understand how motivated the seller is.

Try to gauge how motivated a seller is to determine where you can start your negotiation. For example, a seller that must sell one home before buying another may be motivated to sell at anything but a loss. But one that doesn’t have to sell the home or is listing a property just to see if it might sell isn’t that motivated and may be able to reject any offer under asking price.

Get matched with a personal

loan that’s right for you today.

Learn

more

A good real estate agent can also help you understand seller motivation. Here’s some information that can help you gauge it:

How long the house has been on the market. In general, the longer a home is on the market, the likelier a seller is to accept a lower offer.

How many offers have been made. If the seller hasn’t had any offers over a period of time, they may be more willing to consider yours. If they’ve declined many offers, it could be a sign they aren’t super motivated.

Whether the seller is on a deadline. If the seller has to move or needs to sell the home in a short time period for any other reason, it may put you in a good position as a buyer.

The home has been foreclosed on, which means the lender may be motivated to sell it to recoup whatever it can.

3. Be realistic with your offer.

Whatever state the markets and the seller are in, make sure you’re realistic when you make an offer. First, that means being realistic about what you can pay every month and whether you can get approved for a mortgage for the offer amount.

Getting pre-approved for a mortgage before you start negotiating can be a good idea. This process lets you know around what amount you’re likely to be approved for, how much down payment you might need, and whether you can get an interest rate that works for you. It also demonstrates to sellers that you’re a serious buyer and that you are likely to be able to obtain funding if your offer is accepted. That can make a difference in negotiations.

On the flip side, you should also be realistic about what the seller is likely to accept as an offer. Lowball offers can be seen as insulting and don’t set you on a good foundation for future negotiations.

What is considered a lowball offer? That varies, and your real estate agent can help you determine an appropriate offer in each case.

4. Show enthusiasm but don’t be too tied to the property.

The art of negotiation involves keeping a straight face, right? Actually, in the homebuying process, it might benefit you to demonstrate that you do really like the home in question. After all, the seller may have called this property home for a number of years and be personally attached to it. Selling it to someone else who will genuinely love and care for it could be important.

If it comes down to two similar offers from separate buyers and you’re the one who was delighted with the home and the seller saw you connect with the property, the odds might balance out in your favor. Just don’t overdo it and ensure that you’re making logical choices about financial matters no matter how much you love a house.

5. Put a deadline on the offer.

Finally, put a deadline on your offer. That helps reduce the chances that competing offers might come in and pushes the seller to make a decision or counteroffer so you can move on with the negotiation or your hunt for a different home.

What Else Can You Negotiate with Home Sellers?

If the seller’s firm on the price, you might be able to negotiate other things. Here are some tactics to consider:

Ask the seller to pay some or all of the closing costs.

Use the home inspection to point out items of concern and ask the seller to make repairs to the home in exchange for you paying the full asking price.

Agree to make certain repairs yourself, but ask the seller to agree to a cash payout at closing. This means they come to closing with a check for you to cover the costs of the repairs.

Get creative and ask the seller to leave certain appliances, such as a washer and dryer or refrigerator in the home.

Shop Mortgages Online

If you’re ready to buy your next home, you can start the mortgage process online. Follow these steps to get started.

Check your credit. You can sign up for ExtraCredit to see 28 FICO® Scores, including those commonly used by mortgage lenders.

Make sure your credit score is accurate by challenging inaccurate negative items, if necessary.

Continue to make strong financial decisions to help boost your score so you stand a better chance at getting approved for a mortgage.

Shop mortgage rates at Credit.com, get pre-approved or apply for a mortgage with one of our partner lenders.

There are numerous ways to invest for college students, including using brokerage accounts, or even retirement accounts like individual retirement accounts (IRAs) or 401(k)s. But there are many other things that college students should take into account before or while investing, too.

For college students, it’s never too early to start investing your money. In fact, the earlier you start, the faster you may be able to meet long-term goals such as a graduate degree, buying a house, or even retirement.

Why You Should Start Investing Early

There are a number of reasons to start investing early. Chief among them is potential return. The average annual return offered by the S&P 500 — a market-capitalization-weighted index of the 500 largest companies in the U.S. – is around 10%.

That’s considerably more than you’re likely to generate from putting your money in a savings account – even a high-yield savings account. That means that while money in a savings account is accruing interest, it’s actually losing value at the same time. Investing may help you outpace inflation and give you an extra boost towards your long term goals. 💡 Quick Tip: Look for an online brokerage with low trading commissions as well as no account minimum. Higher fees can cut into investment returns over time.

3 Ways to Invest While in College

There are numerous ways for college students to invest their money, including the use of tax-advantaged retirement accounts, and traditional brokerage accounts.

IRA

Traditional and Roth IRAs are a type of retirement account that almost anyone can open up and start contributing to. There are rules regarding how much you can contribute every year, and when you can take withdrawals (depending on the type of IRA you open), but they can be relatively easy ways to kick-start a college students’ investment portfolio.

Brokerage Account

A brokerage account allows you to make investments through a brokerage firm by depositing funds with them. Your bank may already have brokerage options, or you may consider other outside firms.

A brokerage account allows students to buy and sell stocks, bonds, mutual funds, and other assets through a brokerage firm. Be aware that selling assets can trigger short-term or long-term capital gains taxes. Short-term taxes are charged at your regular income tax rate, and long-term rates are either 0%, 15%, or 20% depending on your tax bracket.

401(k)

A 401(k) is a type of retirement account offered through an employer, though there are some versions, such as Solo 401(k)s, you can open yourself. Like IRAs, there are annual contribution limits, and traditional and Roth 401(k)s to choose from.

The money you put in the account is tax deductible and it grows tax-free while it’s invested. That said, generally, you can’t withdraw money from the account until you reach age 59 ½, or you’ll be subject to a 10% early withdrawal penalty.

Steps to Start Investing as a College Student

For college students getting started investing, there are several steps that they can take to find their footing. It starts by giving some thought to your overall financial goals, determining what you can afford to invest, and then building your portfolio.

Set Clear Financial Goals

It’s important, before you make your first investment as a college student, to give some serious thought and consideration to your financial goals. Do you want to hit a total net worth or dollar amount by a certain age, for instance? Or, do you want to save up enough to buy a home or start a family?

These are the types of financial goals you should think about. Having clear financial goals in mind before you start investing can help guide your decision-making in regard to what types of investments you make.

Determine How Much Money You Can Set Aside

With your goals in mind, you’ll want to think about how much money you realistically can set aside to invest. Odds are, you won’t be able to invest your entire paycheck – there’s rent to pay and groceries to buy, after all. But if you can free up some additional money in your budget for investing, that should help you get your portfolio started. Again, think about how much you can realistically use for investment purposes.

Choose the Right Investment Account

Knowing how much you have to invest and some end-goals in mind, you’ll need to decide what type of investment account will best help you reach those goals. As discussed, this might be a retirement account like an IRA or 401(k), or a brokerage account, which will allow you to buy and sell stocks, or even day trade, if you’d like – though most financial professionals may caution against it.

Understand Types of Investments

You’ll also want to review and deepen your understanding of the various types of investments out there. That can include a variety of asset types such as stocks, bonds, cash, real estate, commodities, precious metals, and more. Not all types will be best for each and every investor – again, it depends on your goals.

Fund Your Investments

The rubber is finally starting to meet the road! You’ll finally want to actually fund your chosen account (be it a brokerage account, etc.) and make your initial investments. This marks the start of your investment portfolio.

Tips for Investing as a College Student

Investing as a college student may seem relatively easy – particularly to get started – but it never hurts to accept some guidance. Here are a few tips for investing as a college student.

Stay Diversified

A good rule of thumb for investors of all stripes is to try and stay diversified by investing in many types of assets and asset classes. The basic idea of portfolio diversification is that the fewer investments you expose yourself to, the more risk you take on should they perform poorly.

Imagine you invest in only one stock and that company folds — if that happens, you’ve lost your entire investment. However, if you invested in 100 different stocks, one company failing would affect you far less. Diversification, however, does not eliminate all risks, including the risk of loss.

One way to stay diversified is by investing in mutual funds or exchange traded funds, which bundle groups of stocks together, essentially doing the work of diversification for you.

Avoid Emotional Investing

The market experiences natural ups and downs. As these fluctuations occur, it’s important to try to avoid letting your emotions impact your investing.

When the market makes a big dip, you may feel the urge to sell investments. However, by doing so you’re actually locking in your losses. Examine what is motivating you to sell, as it’s usually a good idea to let reason prevail so you don’t miss out on any future upturn that may take place. 💡 Quick Tip: Did you know that opening a brokerage account typically doesn’t come with any setup costs? Often, the only requirement to open a brokerage account — aside from providing personal details — is making an initial deposit.

Timing the Market vs Time in the Market

When the market is doing well, you may find yourself tempted to get in on the action and end up buying investments that are too expensive. This type of buying and selling is known as timing the market. You may want to avoid checking the market multiple times a day to help keep your emotions in check and avoid the temptation to time the market.

It might help to think of investing as a long-term proposition. The longer you allow your investments to stay in the market, the more opportunity they have to ride out downturns — and the more opportunity you have to take advantage of an upswing.

Balancing Investing With Academic Responsibilities

As a college student, you should keep your studies in mind, first and foremost. Your academic responsibilities, in most cases, should probably take precedence over your investing activity – though you should keep an eye on your portfolio and learn as much as you can about the markets, too. Everyone is different, but the main point is to not ignore your studies in lieu of watching the market fluctuate.

Investing with SoFi Invest®

Investing as a college student isn’t necessarily difficult, and there are many ways to get started. But given that college students are often working with a limited budget, there may be constraints. Even so, it’s important for relatively young investors to take advantage of the time they have on their side, as the market tends to rise over the years.

College students can look at various retirement accounts, or even a simple brokerage account to get started investing. Investing involves risk, however, which is something students should keep in mind, too. It never hurts to consult with a financial professional, either.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

Inside: Looking for a job that pays at least $25 per hour? This list has the best jobs that fit that description. Each job offers unique benefits and opportunities, so take a look and see if any of them match your interests and skills.

Making $25 an hour is not a pipe dream; it’s a viable reality for thousands of people worldwide.

Earning such an income not only instills a sense of financial well-being but also provides a robust platform to plan for the future.

Today, we dive into elucidating the different opportunities potential jobs offer, aligning your skills and experience with an hourly rate that feels just right for your wallet.

Hence, securing such a job is not a function of luck but more a strategic alignment of skills, passion, and industry demands. But if you’re not entirely sure about where to begin or how to hone your skills for these high-paying jobs, don’t worry.

Imagine earning smooth entry-level jobs 25 an hour, all from the comfort of your workspace. Sounds enticing, right?

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Jobs That Pay $25 an Hour

This section will highlight various professions across distinct fields that provide such a desirable pay rate.

Looking for jobs that pay $25 per hour? We’ve got you covered.

Whether you’re transitioning careers or just starting, this list could help you discover a role that fits your skills and experience.

1. Paralegal

A paralegal role is an excellent job choice due to the vast knowledge gained in the field of law and legal procedures.

Being a paralegal involves a variety of interesting tasks, such as helping lawyers prepare for hearings, trials, and corporate meetings.

This position is not solely monetarily advantageous, it also presents opportunities for growth and professional development in the legal sector.

Earning Potential: It offers rewarding prospects with an average pay of $25 per hour, with the potential to earn up to $40 an hour depending on experience and expertise.

2. Landscaper

Why toil in a stuffy office when the great outdoors can be your workspace? Relish the satisfaction of planting, pruning, and mowing yourself into a healthier, happier lifestyle.

Ideal for nature enthusiasts and people persons out there, landscaping combines green-thumbed work with personnel management. A knack for the outdoors and previous work experience will be your stepping stones, while a certificate in grounds maintenance can make your application stand out.

Start by volunteering in your local community gardens or offering your services to neighbors. Through this, not only will your skills blossom, but your resume will flourish, too.

Earning Potential: You can expand your lucrative landscaping journey by owning your own company and training others to be laborers.

3. Truck Driver

Why is it a top-tier job, you ask? Consider this: truck drivers are the beating heart of global commerce, pivotal figures in ensuring warehouses stay stocked and goods reach their desired destinations. Plus, you’re free of the traditional office environment.

This job is perfect for those who prefer to work alone as well as those who prefer delivery routes that often stretch into the night.

You must be over the age of 21 years old and able to pass a CDL exam. Many truck drivers to a training course to get a jumpstart in the industry.

Earning Potential: Many truck drivers start their own company and will employ a couple of rigs to make passive income.

4. Social Media Marketing

Do you have a knack for creating engaging captions or a Sherlockian eye for data? Then Social Media Marketing could be your calling.

This position, hot in demand and rewarding, calls for creativity and analytical prowess.

Why is it a top job? Well, it’s not for the adrenaline rush of its fast pace. It’s the fact that you get to put your tech-savviness to great use. Social media marketers nurture and grow brands through smart strategies and engaging content.

Earning Potential: Many people start working for someone else as a Social Media Coordinator and then go on to open up their own business.

5. Event Planners

As an event planner, you are the unseen forces behind flawless galas, memorable weddings, and standout corporate functions. If you thrive on creativity, organization, and people skills, you will ensure that each event is meticulously executed.

This role allows you to blend creativity with pragmatic decision-making: from the captivating process of selecting venues, and coordinating with caterers

It’s a dream job for you if you love putting smiles on people’s faces and making their day unforgettable.

Earning Potential: An enticing reason is its attractive pay rate: on average, $24-28 per hour, peaking up to $40, with the potential of a quick pay raise. Plus those lucrative tips!

6. Mechanical Technician

If you’re seeking a rewarding, high-paying role that gets you hands-on with varied machinery, then a Mechanical Technician career.

This role is particularly apt for those with a fascination for machinery and a problem-solving mindset. To climb the ladder to success, one needs to keenly understand how to operate and maintain industrial machines, prevent damage, and optimize performance.

So gear up to diagnose, adjust, repair, and don’t forget – your hands, mind, and machines are a team.

Earning Potential: With an average pay of $26 per hour, you can start repairing machines and set up your own company.

Virtual Savvy

If you’ve ever wanted to make a full-time income while working from home, you’re in the right place!

This intensive training combines thousands of hours of research, years of experience in growing a virtual assistant business, and the power of a coach who has helped thousands of students launch and grow their own businesses from scratch.

Swipe our exact methods to start earning a living from anywhere as a VA – no experience needed!

Learn More

Download Free Checklist

7. Maintenance Technician

This job is best suited for those who enjoy diagnosing technical puzzles and are adept at hands-on solutions.

By developing a strong mechanical aptitude, attention to detail, and top-notch problem-solving skills. Remember, your primary duty is ensuring machinery and equipment operate smoothly – the backbone of any industry.

Start by checking out some free online webinars or training programs related to industrial maintenance.

This is a low-stress job that pays well without a degree.

Earning Potential: As an entry-level worker, you can start by having a vocational certification or general education diploma (GED).

8. HVAC Technician

This role is perfect for those who love hands-on work and can’t get enough of problem-solving – who wouldn’t enjoy the thrill of being an office’s last defense against an impending heatwave?

The key to thriving in this breezy career path is training – dive into an HVAC training program at a vocational school or consider an associate degree in RACH (refrigeration, air conditioning, and heating).

Earning Potential: Being an HVAC technician pays around $25.75 an hour, which will keep your bank balance healthily ‘ventilated’. By having experience, your hourly wage can increase more.

9. IT Support Specialist

If terms like configuring, maintaining, and troubleshooting tech equipment are your weekend chat topics, you’re the perfect match for this.

Thanks to Google’s free certification program, you can start this job by having online training in your spare time.

Start your journey by heading over to Google’s free IT certification program today. Master the IT realm, earn well, and enjoy your work- the trifecta is right there!

Earning Potential: An IT Support Specialist has an average above $25 an hour wage and could rise to $51 an hour for having experience.

10. Day Trader

By poised as a top job due to its flexibility and potential for high earnings, day trading allows you to take full control of your income by making well-informed decisions about the financial market.

It’s perfect for those with an acute mind for numbers, an unflappable nerve, and those who enjoy working from the comfort of their study.

All it takes to get started is some knowledge about the stock market – something you can easily acquire by attending a free webinar or training, which is accessible online!

Of course, remember the golden rule – never invest money you can’t bear to lose. Now, conquer the finance world, one trade at a time!

Earning Potential: By having the eagerness to be a learner and acquire more knowledge about this job, you can earn way higher than you thought. But, there will always be a risk when trading stocks.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

11. Bartender

This job is perfect for friendly individuals! As you’re the life of the party.

Your life will be as vibrant as a well-mixed cocktail—chock-full of lively conversations and new friendships.

Bartending has a steep learning curve, but the payoff is big as it is a job that pays weekly and even daily. Know your spirits, perfect your pour, and master the mix—each skill is a toast to your increasing bank balance.

So, roll up your sleeves, flash that charismatic smile, and prepare to shake things up in the bustling world of bartending.

Earning Potential: With an entry-level job—at a local pub or a fine dining restaurant, you’ll get paid handsomely, at least $25 an hour.

12. Mechanic

The job is a perfect blend for those with a knack for solving complex issues and have the stamina to be on their feet for prolonged periods.

If you’re not averse to the roar of engines and the smell of oil, you might be the grease monkey we’re looking for.

This job is perfect for dipping your toes in oily water. So, go ahead, rev up your career with a mechanic job!

Earning Potential: Personally, my independent auto mechanic makes way more than $25 an hour, but he has years of expertise and opened his own shop.

13. Transcription

Transcription suits anyone craving flexibility or looking to dip their toes into fields like legal, medical, and entertainment.

To shine, you’ll need to master speed, accuracy, and the art of capturing every ‘um’ and ‘ah.’ Noise-canceling headphones and a quiet workspace are your best friends.

Kickstart your move to transcription with free training like a mini-course to see if you like it. Gain insights into making money and build your portfolio.

This high-demand job needs skills you convert audio into text.

Earning Potential: By working remotely as a transcription, you can earn an impressive $25 an hour or more.

Transcript Proofreading

Get the step-by-step guide Caitlin Pyle used to build a thriving at-home business making a full-time income!

A booming legal industry means that transcript proofreaders are in higher demand than ever…

Enroll Now

14. Accountant

Start your second act as an accountant today. The balance sheets await your expertise.

By aiding your clients in reviewing their financial information, preparing tax and finance documents, and updating their changes in tax laws or governmental regulations. Certified Public Accountants (CPAs) can earn exceptionally well.

The longer you’re in the industry, the more you can be able to demand potential compensation for your service. Just by conducting audits, successful financial and bookkeeping strategies. CPAs perform a pivotal role that justifies their earnings.

Earning Potential: Right now, there is a severe shortage of accountants graduating from college. So, your earning potential will substantially increase with each year of experience, and possibly earn up to $50 an hour.

15. Proofreader

Proofreader is an ideal job for detail-oriented individuals with a passion for perfect punctuation, splendid spelling, and grandiose grammar.

Did you get a degree in English or similar? Perfect! But remember, while it helps, it isn’t a must-have.

It’s an excellent stepping stone for a stay-at-home parent or anyone seeking to make some extra cash it is one of the best jobs for moms. So hop on the proofreading wagon and ride your way to a more profitable future!

Earning Potential: Just by sitting and reading on your couch, you can now hop on and start earning $25 an hour depending on experience.

16. Recreational Therapist

Bring great immense job satisfaction by improving the lives of those grappling with illness and disability.

To get started, all you need is a bachelor’s degree in recreational therapy and then obtain a Certified Therapeutic Recreation Specialist credential.

So, why wait to become an everyday hero with a salary that smiles back at your bank account?

Earning Potential: You can earn more than $25 an hour by being a Certified Therapeutic Recreational Therapist.

17. Dental Assistant

Do you have strong communication skills, and the ability to partake in a hands-on career?

Just sterilizing equipment or lending a diligent hand during treatments will be part of your daily grind. Ensure every instrument screams ‘clean’ before the dentist reaches for it.

To become a dental assistant, you typically need to earn a certification or diploma through a dental assisting program, which often takes about a year to complete.

On-the-job training may also be required, during which you’d learn about dental procedures, patient care, and office duties under the supervision of a dentist.

You may have found the tooth fairy’s best job yet! Dive in!

Earning Potential: With a wage average of $19 an hour and earning up to $25 just being a Dentist Assistant.

18. Certified Nursing Assistant

Have a career dream to dive into the healthcare industry? Familiarize yourself with basic health practices, hygiene, and safety procedures.

Start your journey as a Certified Nursing Assistant by attending to patients, assisting nurses, and providing emotional support to everyone. You will have to start a training program, but thankfully there are many to choose from.

Earning Potential: This career pays more than $25 an hour and might increase through experience and skills.

19. Housecleaners

According to Zippia, 48.9% of the housecleaner’s qualification is to have a high school diploma, but experience could help. You must have a strong understanding of cleaning procedures and practices.

Also, you can consider taking a course to learn about safety guidelines and recommendations.

Other important attributes include attention to detail, physical stamina, and excellent time management skills.

Earning Potential: Whether you’re a single mom or a high school graduate, you can potentially earn up to $25 an hour.

20. Nanny

Fascinated by child psychology or studying pedagogy? Or just love kids? Then, this job is tailored for you; it offers both consistent income and practical field experience.

Getting started can seem daunting, but it doesn’t have to be. Step into the kiddie world, it might just be the best move you make. Where you are not required to pass any school diploma.

You can find plenty of nanny gigs on Sittercity.

Earning Potential: If being a nanny is just a child game then I want in and earn up to an incredible $1000 to $1100 a week.

21. Delivery Drivers

Welcome to the job of a delivery driver, a blend of independence and earning potential on wheels. When you are good at your job, you don’t have customers wondering how late does Amazon deliver.

This career is a perfect fit for introverts who prefer their own company, the job offers flexibility with the ability to set your hours.

But, keep in mind that larger roles, such as FedEx, may require truck driving experience, the ability to lift heavy boxes, and the completion of a few additional checks.

Earning Potential: Most delivery drivers for FedEx and UPS are union workers. Thus, they have the union to fight for pay increases. Plus you can increase your salary by moving up in the ranks.

22. Licensed Plumbers

Get ready to hop into commercial, residential, and industrial projects, working flexibly based on your schedule.

If you love problem-solving and can handle the occasional wade through the muck, then this amazing career is for you! Don’t worry about your expertise level; It’s the perfect time for you to dip your toes into the world of plumbing.

Earning Potential: Don your gloves, grab your tool kit, and join the ranks of expert plumbers making upwards of $25 an hour.

23. Athletic Trainers

Are you into sports and fancy being in the thick of the action?

You are considering becoming an Athletic Trainer – a well-paid role that combines both your passions brilliantly. Then, get to work closely with athletes, which means you’re right at the heart of the sports action.

You’ll need to be certified and licensed in healthcare to offer your professional services. The ball’s in your court!

Earning Potential: Earning about $25 per hour, it’s among the few amazing careers that can up your game financially and health-wise. Also, it may take you to the Super Bowl as the team’s athletic trainer!

24. Customer Service Managers

So, you’re a people person with a knack for solving problems? Consider a job as a Customer Service Manager.

This job is best for ambitious, empathetic individuals who love making a difference in customer experience, enhancing team performance, and ensuring business profitability.

Want to up your game? Brush up on customer relationship tools like Hubspot or project management tools like Asana. Then, prepare to rule the customer service realm as an expert Customer Service Manager.

This can be a great non-phone work-from-home job as many customer service requests are handled through chat and email.

Earning Potential: One of the amazing careers that pay a satisfying $25 per hour, it’s a chance to flex those crucial customer service muscles while managing a team.

25. Freight Broker

With an average pay topping most traditional roles, this often-overlooked profession is a gem amidst the rubble.

Here’s why: Despite its lucrative nature, competition in freight brokerage is surprisingly low.

Jumpstart your journey with a free webinar or training – there are many available online. This will equip you with vital information about the ins and outs of the role and the industry.

Earning Potential: You will be surprised to learn what a freight broker’s salary can be.

Freight 360

Designed as a 101-level course on freight brokerage, you’ll learn the basics of freight brokering in this online course.

This course is designed for freight brokers in any setting, regardless of their employment status.

This course is designed to help you source more leads and move more freight. Or even start your brokerage!

Start Now

FAQs

Have you ever dreamt of earning $25 an hour with flexible hours at your convenience?

The list above are some of the jobs that can earn $25 an hour. However, try to evaluate yourself if the requirements perfectly suit you. By having skills and experience on the said job you can ace up and boost your chances of getting one of the high-paying jobs above.

Unlock and upgrade your skills now by attending any training that aligns with your dream job. Be able to receive a rewarding amount of earnings in your pocket!

These amazing careers above can fetch you at least $25 per hour. Start earning big and turn your dream into your paycheck.

Improving your skills through attending training, updating certificates, and seeking additional knowledge in your field. Plus, It increases your chances of landing a job that pays $30 an hour.

Actively applying for new jobs, particularly those that value your enhanced skills, can open the door to higher-paying opportunities potentially enabling you to reach that $30 an hour wage.

So master the craft, build your credibility, and let your work do the talking.

The ball is in your court now. Step up and start crafting your destiny, one skill (and dollar) at a time. So, start attending any training that is aligned with the career you’re looking for.

Find out what should I do for a living. Sign up for a free webinar or training. Sites like Udemy and Coursera offer a plethora of free courses to help you fine-tune your skills or discover new ones.

Which Applications will you Submit for jobs paying 25 an hour?

The possibilities in today’s remote job market are exhilarating. Amid the myriad of options, some rake in at least a solid 25-dollar-an-hour job.

Begin by brushing up on your skills or discovering new ones through free webinars or training sessions that align with your chosen profession to increase your qualifications. Make sure your resume is polished and start applying to suitable jobs in your field. The next step is nailing that job interview.

Thus, finding and applying for such lucrative positions is not just an aspiration for a better standard of living, but a practical step towards improved financial stability.

Remember to job-seek smartly and relentlessly. The end game is finding that perfect remote job – working on your terms, from your comfy corner of the world, and padding your bank account one $25 hour at a time. It’s time to get cracking!

Know someone else that needs this, too? Then, please share!!

Refinancing your mortgage can be a smart financial move if you do it the right way. You can tap into your home equity, get a lower interest rate, or even shorten or lengthen the terms of your loan. All of these are great outcomes for you and your wallet.

But here’s something that’s not so great: Picking the wrong mortgage refinance lender.

This one major mistake can potentially cost you tons of money in closing costs, hidden fees, and high interest rates.

You can avoid that by learning just a bit about what to expect throughout the refinance process and how to find the right lender. We’ll walk you through everything you need to know and give you some suggestions for the big decision.

9 Best Mortgage Refinance Lenders of 2023

We’ve compiled a list of the best mortgage refinance companies with the most competitive mortgage rates. Read through our short reviews to understand what kind of mortgage products they offer and how their process works. It’s an excellent resource for narrowing down your list of refinance lenders to consider.

1. loanDepot

loanDepot is a lender that values and earns customer loyalty. This is evident by their refinancing lifetime guarantee. Once you refinance with them the first time, they will waive their lender fees and reimburse your appraisal fee.

It’s also an excellent choice for people who like a person-to-person connection. You can call them at any time to talk directly to a loan officer.

This can be especially helpful for a refinance because there are many reasons for refinancing and many ways to refinance.

After defining your goals, they let you choose from both fixed-rate and adjustable-rate loans. There are other loan types available, such as jumbo and government, or even home equity loans. The minimum credit score is 620.

They are committed to customer satisfaction and back it up with extensive refinance products.

Terms and conditions apply.

Read our full review of loanDepot

2. LendingTree

LendingTree offers a ton of benefits when it comes to refinancing. First, the online process is very easy and can even get you a mortgage rate quote in under three minutes.

LendingTree isn’t a direct lender and instead matches you up with multiple loan offers with mortgage lenders, so you can compare your options.

Here’s why that’s so helpful.

It makes LendingTree’s refinance options much more robust than many other online lenders. For example, you can convert an adjustable-rate mortgage into a fixed rate or refinance your FHA loan or even VA loan.

You can also cash out home equity as part of your refinance or choose from multiple loan terms.

If you’re still in the information-gathering stage of your refinance journey, LendingTree’s website has many valuable resources.

Play around with numbers to check out different scenarios using tools like their refinance calculator and cost estimator.

Read our full review of LendingTree

3. Rocket Mortgage

Another driving force in the online refinance marketplace is Rocket Mortgage, which is part of Quicken Loans.

The application process is straightforward and can be completed entirely online. You can pick your goal for your refinance to help Rocket tailor your loan offers.

You can even link your financials and property information so that you don’t have to gather and upload all the documentation manually. In fact, 98% of financial institutions in the U.S. can be imported for both your bank statements and investment assets.

Rocket Mortgage also allows you not only to browse different options but also customize them. You can choose from a traditional mortgage product, FHA loans, VA loans, USDA loans as well as fixed or adjustable rates. The minimum credit score is 620.

For an exceptional customer service focused experience that’s entirely based online, Rocket Mortgage is certainly worth exploring.

Read our full review of Rocket Mortgage

4. New American Funding

Another direct lender, New American Funding, is a mortgage company that simplifies the online mortgage process. Get started by selecting the type of real estate you want to refinance.

You can choose from:

Single family home

Condo

Townhouse

Multi-unit

Other

You’ll then answer a series of questions about your personal information, including the existing loan amount and your credit scores.

Afterward, you’ll get a quote estimate on the type of refinance loan you could potentially receive. You can also call the 800-number at any time to speak to one of New American Funding’s loan officers.

The average refinance saves their customers about $360 per month. So, they’re definitely worth checking out, especially if your goal is to lower your payment amount.

Read our full review of New American Funding

5. SoFi

SoFi started as a student loan refinance company and has recently branched out to mortgage refinancing as well. One of the key advantages here is that they go beyond the traditional credit score and base your qualification on high-tech algorithms using various criteria.

In addition to the typical refinance and cash-out refinance options, SoFi also offers a refinance product specific to paying off your student loan debt.

As a result, you could end up lowering your monthly mortgage payment on top of getting rid of your student loan payments.

SoFi lets you check your prequalification for a refinance in just two minutes without affecting your credit score. You can usually close on your new loan within 30 days, and you don’t have to pay any lender origination fees.

A final bonus? If you have an existing SoFi loan, you can qualify for an additional 0.125% rate discount on your refinance.

Read our full review of SoFi

6. Guaranteed Rate

This major lender has offices in each state (plus the District of Columbia) but also lets you get started using its Digital Mortgage platform.

Guaranteed Rate requires a minimum credit score of 620 for mortgage approval. However, alternative credit data, such as utility and rent payments, are considered in some cases.

Guaranteed Rate is highly rated for customer service. They consistently receive stellar customer reviews with a satisfaction rate above 95%.

Whether you want a completely online refinance experience or a more personal one, they deliver.

Read our full review of Guaranteed Rate

7. Carrington Mortgage Services

Carrington begins the process by asking you to select one of four goals:

Lowering your interest rate

Lowering your payments or consolidating debt

Remodeling your home

Getting cash out

Fill out a contact form to have them get in touch with you. Alternatively, you can call Carrington anytime between 7:00 a.m. and 6:00 p.m. PST, Monday through Friday.

If you like a lot of personal care and attention throughout the process, you’ll appreciate Carrington. Their mortgage professionals walk with you every step of the way to ensure you have a speedy and successful closing.

Read our full review of Carrington Mortgage Services

8. Bank of America

One of the biggest banks out there, Bank of America puts its resources to good use by creating a comprehensive and easy online user experience.

You can zip through the application from start to finish by uploading all of your supporting documentation and e-signing with a touch of your finger.

Plus, Bank of America practically has a complete offering of refinancing products, including fixed-rate loans, ARMs, jumbo loans, FHA loans, and VA loans. B of A’s interactive website also makes it easy to get a rough estimate of current mortgage interest rates.

All you have to do is type in your zip code and desired loan amount, and you can see where refinance rates start for various mortgage types.

If you already bank with B of A and are a Preferred Rewards member, you may also be eligible for a reduction of your mortgage origination fee anywhere between $200 and $600.

Read our full review of Bank of America

9. Chase

You don’t need to be a bank member to refinance with Chase. And if you prefer to work with a traditional bank over a strictly online lender or matching website, then Chase is a strong choice.

Start the process online by choosing one of two goals: lowering your monthly payment or cashing out your home equity.

From there, you can get started on the prequalification form. Be prepared to enter information on your current mortgage and your finances.

If you ever have a question before or during the application process, you can either call or connect with a home lending advisor in person in one of 28 states.

There are plenty of refinancing options available through Chase, including jumbo, FHA, VA, and HARP loans. As with most other lenders, the minimum credit score is also 620.

Read our full review of Chase

How does refinancing a mortgage work?

Applying for a refinance is very similar to applying for a home loan. It’s also important to note that you don’t have to use your current lender or servicer. You can pick any mortgage lender that you’d like for your refinance.

After shopping around for lenders and comparing your loan options, you’ll have to complete a formal application. This involves submitting your income and financial statements. The loan officer and underwriter will review your materials to make sure you can afford the new terms.

Mortgage Refinance Requirements

Mortgage refinance lenders are primarily concerned with three things: credit score, debt-to-income ratio, and average loan-to-value ratio (LTV).

Credit score: The minimum credit score for most mortgage refinance companies is around 620.

Debt-to-income ratio: Your monthly debt should not exceed 43% of your monthly take-home pay, just like a regular mortgage. In addition to personal loans and credit card debt, they also include your new mortgage payment in that number.

Loan-to-value ratio (LTV): Lenders would like to see a low loan-to-value ratio (LTV). Typically, you should have at least a 20% equity in your home. In addition to personal loans and credit card debt, they also include your new mortgage payment in that number.

You’ll be required to get an appraisal of your home as part of the process. This makes sure the property lives up to its estimated value and helps determine your total equity in the home. You don’t need to do anything special before the appraiser arrives. However, it is wise to clean and tidy up to make a favorable impression.

Thereafter, you just have to wait for closing. Usually, your lender lets you pick the date, time, and location. Next, they’ll send a notary who will walk you through signing the closing documents. Then, you’ll start fresh with your new payment schedule. If you’ve cashed out some of your home equity, you can typically receive a check or have it deposited directly into your bank account.

How to Choose a Lender to Refinance Your Mortgage

When you decide to refinance, picking the right lender is vital to your financial success.

Mortgage refinance lenders structure loans differently, depending on whether you want to minimize closing costs or lower monthly payments—or a combination of the two.

The first thing to look at is what kind of refinance loans the lender offers. For example, you can find FHA refinance loans with lower minimum credit score requirements than conventional loans if you’re looking for a government-backed refinance.

Loan Terms

Alternatively, you may want to refinance into a shorter term than the standard 30-year fixed mortgage. Look for mortgage refinance companies that offer multiple options, such as 10, 15, or 20-year mortgages. Then, you can compare refinance rates and payments and pick the best one.

As with any kind of loan, you also want to shop around for mortgage rates. Not every lender automatically offers the same interest rate or APR. You’ll also want to compare closing costs as part of the evaluation process. You need to know both your upfront costs and long-term costs in terms of interest.

Closing Costs

If you want to minimize the amount of cash you bring to the table, ask whether your closing costs can be rolled into the loan.

There are numerous ways you can tackle mortgage refinancing. That’s why picking the right refinance lender can make a huge difference. They can help you understand the pros and cons of different options, so you can make the right choice.

Don’t be afraid to ask questions. Ask for specific numbers, and talk to a few different lenders to get an idea of their recommendations and refinance process.

When to Refinance a Mortgage

Now that you’ve learned of the best refinance lenders out there, make sure you’re refinancing for the right reasons. Here are some of the most common reasons for refinancing a mortgage.

Lower Your Monthly Payments

It’s entirely possible to refinance to lower your payment amount. To save money over the life of your loan, you could refinance into a lower interest rate if mortgage rates have dropped since you got your loan. Or, if your credit score has improved, you might be able to qualify for a lower refinance rate as well.

If you’re having trouble making your payments, you could also consider refinancing into a longer loan term. This spreads out your existing mortgage amount over more years.

For example, if you’ve been paying your mortgage for 10 years on a 30-year loan, you could extend the existing 20 years over another 30 years. However, you should proceed with caution, depending on your financial situation and retirement plans.

Cash Out Your Home Equity

If you have equity in your home—at least 20%—you could potentially qualify for a cash-out refinance. This allows you to get a lump sum of money and then add that amount to your existing loan. Usually, you can borrow up to 80% of your equity.

Let’s take a look at an example.

Say your home is valued at $200,000, and your mortgage is down to $150,000. That leaves you with $50,000 in equity. The bank will let you borrow up to 80% of that, which is $40,000.

If you qualify for the mortgage, you could then refinance a total of $190,000. You can then use the cash for home renovations, college tuition, medical bills, high-interest debt, or anything else.

Change the Terms

Shorter loan terms typically come with lower mortgage rates since there’s less of a chance for you to default on the loan. Once you’ve paid off a portion of your current 30-year mortgage, you may be able to save on interest by switching to a 15-year mortgage.

If, for example, you’re 15 years into a 30-year fixed mortgage, you only have 15 years left to pay. So, you could potentially save thousands by getting a lower interest rate via an actual 15-year fixed mortgage.

Switch to a Fixed Rate Mortgage

If you initially took out an adjustable-rate mortgage (or ARM) and your fixed period is ending, you should consider refinancing your loan. There’s a cap on how high your adjustable mortgage can go. It could potentially be much higher than current fixed interest rates.

Talk to a lender to see the best option to avoid a significant jump in your monthly payment. And be sure to plan ahead since it can take time for the approval process to finish.

See also: How to Refinance Your Mortgage

When Not to Refinance

When shouldn’t you refinance? If your credit score has dropped significantly since you took out your original mortgage, you may be surprised by higher interest rates. Similarly, refinancing today may not save you money if you qualified for a rock-bottom rate during the recession.

Furthermore, consider that every mortgage refinance comes with closing costs, just like your initial home loan. Therefore, you need to make sure any financial benefits you expect to receive from your refinance outweigh the added closing costs.

All of these considerations can be discussed with a suitable lender, whether in person, on the phone, or online. Do the research it takes to make sure you’re making an intelligent decision on your next home refinance.

Frequently Asked Questions

What are the steps to refinancing a mortgage?

The process of refinancing a mortgage typically includes the following steps:

Determine if refinancing makes sense for your financial situation and goals.

Research and compare different mortgage lenders.

Choose the right lender and loan product for your needs.

Complete a formal application, providing all necessary income and financial documents.

Wait for the lender’s underwriting process, which includes verifying your information and appraising the home.

Once approved, arrange for a closing where you will sign all required documents.

Begin your new payment schedule, or receive your funds if you’ve done a cash-out refinance.

How does refinancing a mortgage affect my credit score?

Refinancing a mortgage can temporarily lower your credit score, as the lender will perform a hard credit check during the application process. This is typically a small drop and should recover over time as long as you continue to make regular, on-time payments. Additionally, the old mortgage will be marked as paid off on your credit report, which can be beneficial to your credit history in the long run.

What are some reasons I might not qualify for a mortgage refinance?

If your credit score has significantly dropped since you took out your original mortgage, you may not qualify for a favorable interest rate, making refinancing less beneficial. Additionally, if your debt-to-income ratio is too high, you may not qualify. Lastly, if you do not have sufficient equity in your home (usually at least 20%), you may not qualify for certain types of refinancing.

Can I refinance my mortgage with bad credit?

While it may be more difficult to refinance your mortgage with bad credit, it’s not impossible. Some lenders specialize in loans for individuals with poor credit, and government programs like the FHA refinance loans may have lower credit score requirements. However, be aware that you will likely be offered higher interest rates.

How much does it cost to refinance a mortgage?

The cost of refinancing a mortgage typically includes an origination fee, an application fee, an appraisal fee, and closing costs, among other potential costs. This can usually amount to between 2% and 6% of the loan amount. However, in some cases, you may be able to roll these costs into your loan to reduce your out-of-pocket expenses at closing.

Can I refinance my mortgage more than once?

Yes, you can refinance your mortgage more than once. However, it’s important to consider the costs of refinancing, such as closing costs and possible prepayment penalties, and weigh them against the benefits you expect to receive. You’ll want to make sure that refinancing makes financial sense each time.

What’s the difference between a cash-out refinance and a rate-and-term refinance?

In a cash-out refinance, you take out a new mortgage for more than what you currently owe, and then receive the difference in cash. This can be useful if you need to cover large expenses or consolidate higher-interest debt.

A rate-and-term refinance, on the other hand, changes the interest rate, the term length, or both of your existing mortgage, but you don’t receive any cash. This is typically done to lower monthly payments or to pay off the loan faster.

When should I consider a fixed-rate mortgage over an adjustable-rate mortgage?

A fixed-rate mortgage may be a better option if you plan to stay in your home for a long period of time and want predictable, stable monthly payments. On the other hand, an adjustable-rate mortgage (ARM) may initially offer a lower interest rate, but it can fluctuate over time. An ARM could be a suitable option if you plan to sell or refinance your home before the interest rate starts adjusting.

Inside: Are you looking for ways to make money while you’re still in college? This guide has a variety of ideas for side hustles for college students that can help you get started. From online businesses to odd jobs, there’s something for everyone.

Are you a college student searching for ways to increase your income and improve your financial situation while balancing your academic commitments? We’ve got your back!

In this student-friendly guide, we’ll share side hustles for college students, giving you many opportunities to earn extra cash.

You can even learn to get paid to go to school!

Whether you’re tech-savvy, creative, or inclined towards offline work, you’ll find something that suits your preferences.

Let’s jump in and explore how you can transform your free time into a valuable money-making asset!

What is a Side Hustle?

Simply put, a side hustle is like having a little extra adventure on the side while you’re busy with your main gig, which in this case might be college classes.

It’s your chance to boost your finances and gather valuable experience that could pave the way for future career opportunities. It’s like adding a dash of extra flavor to your college life along with extra cash!

What side hustles can I do as a college student?

As a college student, you possess a unique set of skills and resources that can be leveraged to generate income.

Whether you aspire to know how to make quick money in one day or debate what should I do for a living, opportunities await you.

Stay tuned for the second part of this article, where we’ll explore a treasure trove of side hustles perfectly tailored for college students.

What can I do to make extra money as a college student?

As a college student, there are various ways to earn extra money.

Most importantly, you need to find something that works well into your college schedule.