Collectively, Americans carry trillions in household debt. And the biggest single element of that burden by far is mortgage debt: It comprises close to $12 trillion of the $17.29 trillion overall.

Latest statistics on average mortgage debt

Mortgage

The average mortgage debt balance per household is $241,815 as of Q2 2023, a 4% increase from 2022.

The total mortgage debt balance in the U.S. is $12.14 trillion as of Q3 2023, an increase of $126 billion over the previous quarter.

The average mortgage balance exceeds $1 million in 26 U.S. cities, primarily on the East and West Coasts.

Mortgage originations collectively total $386 billion, as of Q3 2023, well below the trillion-dollar levels in 2020-21.

Total home equity line of credit debt equals $349 billion as of Q3 2023, more than a $25 billion year-over-year increase.

The average credit score for purchase mortgage holders is 733 as of November 2023.

The total debt service to income ratio (DTI) of U.S. households is projected to rise to 11.7% by 2025, up from 9.9% in 2022. The mortgage DTI alone will increase to 4.5%.

Total U.S. household debt is $17.29 trillion as of Q3 2023, an increase of $3.1 trillion since the end of 2019.

Annual average mortgage debt

Mortgage debt is the heavyweight when it comes to household debt, dwarfing credit card balances, student loans and auto loans. After the tough blow dealt by the 2007-08 subprime mortgage crisis, the annual average mortgage debt declined sharply. However, since 2013, the pendulum began to swing back, with mortgage debt on a steady rise. Since the pandemic, increases in home prices and in interest rates kicked the climb into overdrive.

So, what does this mean for the annual average American mortgage debt in 2024? With housing inventory still tight, interest rates still elevated, and people seeking larger homes to accommodate their evolving lifestyles, mortgage balances will likely continue to grow, though perhaps at a slower pace.

Most common types of debt

Mortgages continue to be a significant portion of household debt in the United States, with a current total of $12.14 trillion owed on 84 million mortgages. This equates to an average American mortgage debt of $144,593 per person listed with a mortgage on their credit report. Despite interest rates hovering above 7 percent, mortgage demand remains strong, driven by two key factors: an increase in the number of people seeking mortgages, and larger mortgages at that.

The record-low mortgage interest rates of recent years allowed buyers to purchase higher-priced homes or refinance their existing mortgages while maintaining low monthly payments. This has led to a rise in outstanding mortgage debt, which currently accounts for 70.2 percent of consumer debt in the U.S., according to New York Federal Reserve figures.

Here’s a look at the other common types of debt among American households, based on credit reporting company Experian’s midyear consumer debt review:

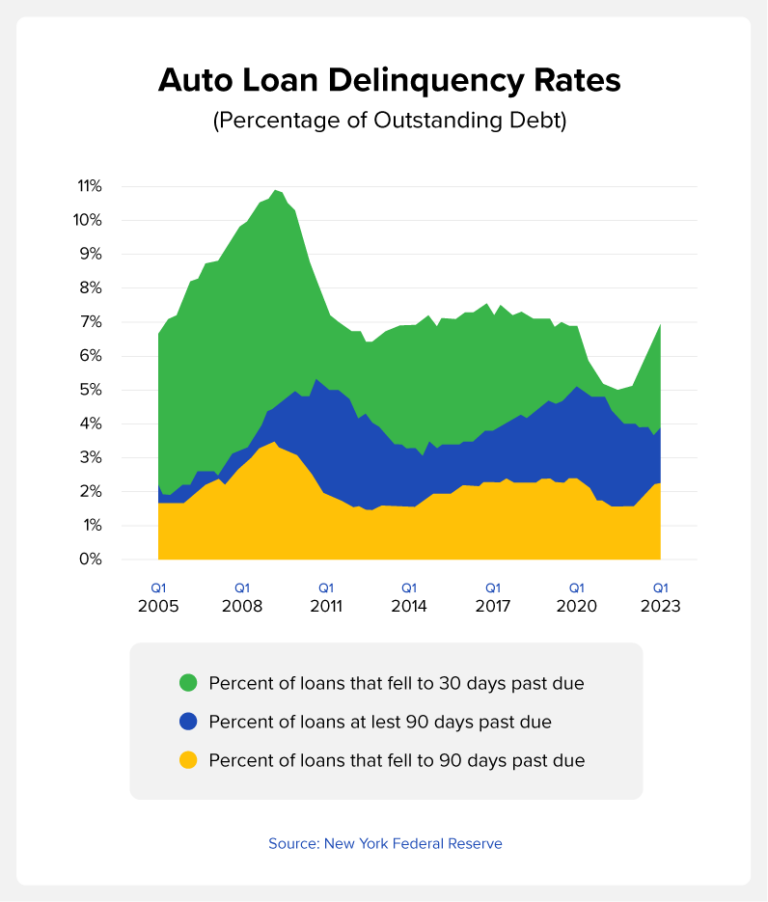

Auto loans. In the year between Q2 2022 and Q2 2023, auto loan debt witnessed a 5.8 percent increase, rising from $1.42 trillion to $1.5 trillion. This rising trend in auto loan debt can be attributed to persistent inventory shortages, escalating prices for new and used vehicles, and supplementary expenses such as auto insurance.

Credit card debt. Between Q2 2022 and Q2 2023, credit card debt surged by 16.3 percent, amounting to a total of $1.02 trillion. This increase is largely attributed to factors such as inflation and increasing credit card interest APRs. In a similar vein, unsecured personal loans also saw a 21.3 percent growth spurt, moving from $156.1 billion in 2022 to $189.4 billion in 2023.

Home equity lines of credit (HELOCs). As of Q2 2023, HELOCs have seen an 8.5 percent increase compared to the same quarter in 2022, reaching a total of $322 billion. This growth can be attributed to several factors. Firstly, the ongoing rise in home prices has increased homeowners’ equity, making it easier for them to tap into their home’s value through HELOCs. Additionally, the current high interest rate environment has made borrowing against home equity more attractive than refinancing a mortgage or taking out other types of loans.

Student loan debt balances. Student loan debt has long been a significant player in U.S. household debt. However, an 8 percent decrease occurred between Q2 2022 and Q2 2023, with loan balances falling from $1.51 trillion to $1.39 trillion. Influential factors behind this decline include the moratorium on interest on student loans, borrowers making payments during the three-year payment pause that concluded this year, and loan forgiveness initiatives introduced by the Department of Education.

Average mortgage debt by generation

Americans generally begin taking on debt as young adults, taper off their pace of borrowing in middle age and work to pay off loans near or during retirement.

Generation

Average mortgage debt

Generation Z

$229,897

Millennials

$295,689

Generation X

$277,153

Baby boomers

$190,441

Silent Generation

$141,148

Source: Experian

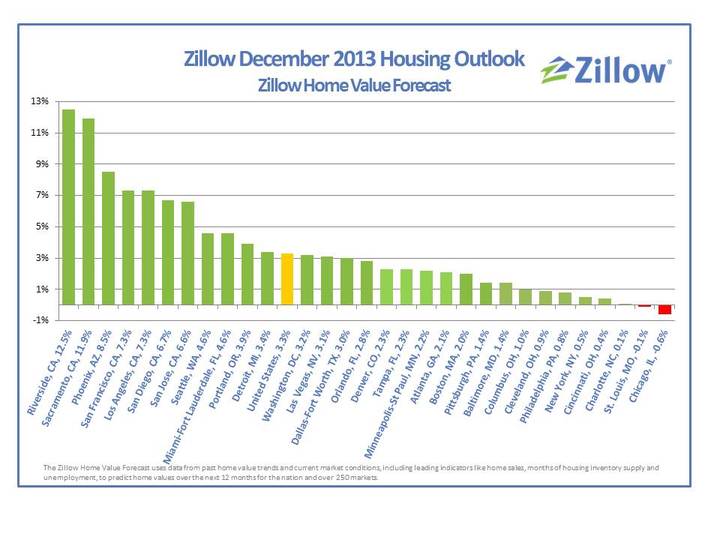

For each generation, this trend has taken place in tandem with mortgage rate fluctuations and home price appreciation, which has accelerated dramatically in recent years. In February 2012, the median existing-home price was $155,600, according to the National Association of Realtors. By the same time in 2017, the median was $228,200. As of November 2023, the median home price was $387,600.

States with the highest and lowest mortgage debt

These states had the highest average outstanding mortgage balance per borrower as of the end of 2022, according to Experian:

District of Columbia – $492,745

California – $422,909

Hawaii – $387,277

Washington – $331,658

Colorado – $319,981

In these states, borrowers are much closer to paying off their home loans:

West Virginia – $124,445

Mississippi – $139,046

Ohio – $139,618

Indiana – $141,238

Kentucky – $144,222

How mortgage debt compares to other household debt

In comparison to other types of household debt, mortgage debt often tends to take the lion’s share — largely due to the substantial cost of real estate (a home is likely to be the single biggest asset an individual ever purchases). While mortgage debt tends to be sizable, it is spread over a lengthy period, usually over a term of 15 to 30 years. This mitigates its impact on a household’s monthly budget, especially when compared to high-interest, short-term debt like credit card balances.

That longevity works to borrowers’ advantage in another way: Lenders often view mortgage-holders favorably for their demonstrated ability to manage large, long-term financial commitments. In fact, in contrast to other obligations, a mortgage is often viewed in a positive light by creditors, because — unlike with personal loans or credit card bills — your payment acts as an investment in an appreciating asset. Each monthly installment you pay reduces the principal owed on your house, increasing your stake in the property over time. This home equity can later be leveraged for financial liquidity or for securing lower-interest loans — or just held onto, enhancing your net worth and those of your descendants.

In short, a mortgage is considered “good debt,” due to its role in building equity, growing wealth and demonstrating creditworthiness.

From high prices to low inventory, potential home buyers know it’s gnarly out there. But if you’re ready for homeownership, the long-term benefit of buying often outweighs the pain of toughing out the search — even these days.

Think of it like your 5 a.m. spin class: You know it’s good for you, even if it takes grit (and leaves you feeling sore).

With some market savvy, you can make the most of today’s challenging conditions. Here’s your game plan for buying a house in 2024.

The challenge: Stubbornly high mortgage rates squeeze shoppers’ buying power

Buyers have been at the mercy of mortgage rates’ meteoric rise, holding on as the average 30-year fixed rate climbed from 3% to nearly 7% in 2022. In October 2023, rates topped 8% for the first time since 2000 — a surprise even many top economists didn’t predict. But throughout November, they dropped slightly, landing at an average of 7.03% for the week ending Dec. 7.

Higher interest rates make it more expensive to get a mortgage. To put that in perspective: Let’s say you can afford $1,800 per month in principal and interest. At a 3% interest rate, you could afford to borrow $426,900. But at a 7% interest rate, you could afford to borrow only $270,600. Why? Because you’d pay a full $156,300 more in mortgage interest with the higher rate.

For now, economic signals suggest more positive news for buyers in 2024. Dan Moralez, regional vice president at Dart Bank in Holland, Michigan, points to a cooling economy and the pause on Fed interest rate hikes. “All of that stuff really lends itself to mortgage rates getting better and the cost to borrow getting cheaper,” Moralez says.

Let’s set realistic expectations, though: No experts are forecasting a return to 3% rates anytime soon. More likely, we’ll see the 30-year mortgage rate decline modestly below 7% in the second half of 2024, according to forecasts from the Mortgage Bankers Association and the National Association of Realtors.

Your strategy: Do your research to find the best deal

Don’t let high rates keep you on the sidelines for too long. When rates go down, competition goes up — another reason there’s no time like the present to start house hunting.

And whichever way rates move in 2024, you’ll save money if you shop around. Aim to get an estimate from at least three mortgage lenders. The Consumer Financial Protection Bureau estimates borrowers can save $100 per month (or more) this way. And look at the annual percentage rate, or APR, to understand the total cost of the loan, which includes fees and other charges.

With buyers wincing at high rates, some lenders are advertising “buy now, refinance later” offers. Others are offering temporary buydowns, where the buyer’s effective monthly payment is reduced for a year (or a few). Before signing up for a discount, ask questions to understand how it works. Each option could potentially save money, but Moralez says it could also be “smoke and mirrors” if the flashy deal is offset by higher fees.

“It’s one of those things where I tell folks, ‘There’s no free lunch, OK?’” he says. “You know, somebody is paying for it somewhere.”

The challenge: Low inventory means slim pickings for buyers

The rate of existing home sales is the lowest it’s been in 13 years, according to October 2023 data from the National Association of Realtors (NAR). The current market has a 3.6-month supply of unsold home inventory, meaning it would take listed homes 3.6 months to sell at the current sales pace. A balanced market has a supply of five to six months.

So why aren’t sellers selling? Octavius Smiley-Humphries, a real estate agent with The Smiley Group in Apex, North Carolina, points to higher prices and the “rate lock-in effect.”

“At this point, you’d be paying either double your mortgage for the same price house that you have, or a similar mortgage if you’re trying to even downsize,” he says. “So I think the more intelligent buyer is kind of thinking, ‘What’s the benefit?’ unless you absolutely have to move.”

Some hope: Single-family construction permits are on the rise, with more issued in October 2023 than at any other time in the past year, according to the Federal Reserve Bank of St. Louis, so we’ll see more new houses boosting supply soon. And despite larger shortages, 92% of markets have seen modest inventory growth over the last three months, according to a November 2023 report from ICE Mortgage Technology.

Your strategy: Cast a wider net

You can’t control who puts their house on the market. So focus on what you can change: your expectations.

Let go of the fantasy of finding the perfect home when a “good enough” home can get your foot in the door sooner. That’s especially true for first-time home buyers who are eager to build equity.

“Real estate has always been a really solid investment,” Smiley-Humphries says. “So what you essentially lose by waiting six months or a year could mean tens of thousands of dollars.”

For now, maybe you expand your search to include condos or townhouses. Maybe you settle for fewer bathrooms or a dated interior. Keep your chin up — even if you have to tolerate less square footage or weird linoleum floors for a while, you’ll have equity to remodel or sell in a few years.

The challenge: High prices push affordability to the worst it’s been in almost 40 years

Housing is the least affordable it’s been since 1984, according to a November 2023 report from ICE Mortgage Technology. Why? Home prices are growing faster than income, and on top of that, higher mortgage rates increase the cost of borrowing.

In October 2023, the median existing home sales price climbed to a record high of $391,800, according to the NAR. To buy a median-priced home at that time, buyers would need to shell out $2,567 per month just in principal in interest, ICE estimates. That’s another all-time high since ICE has been keeping track — and nearly double the median monthly payment of $1,327 just two years ago.

Until supply catches up to demand, prices are unlikely to fall. Realtor.com estimates prices will fall less than 2% next year. That’s another reason to jump in now: A big drop in prices could trigger more competition.

Your strategy: Make a budget and stick to it

If you’re Zillow-stalking houses you can’t afford, stop. Instead, channel that energy toward your plan to shop for a house in real life — starting with setting a realistic budget.

First, talk to a financial advisor or use an online calculator to see how much house you can afford. Understand how mortgage lenders will determine your eligibility, including analyzing your credit score, cash savings and monthly debt payments.

Next, find a buyer’s agent who knows how far your budget can go in your local market. An experienced agent can advocate for you and help you snag a good deal.

One bargain-hunting tip: Start searching in the winter, suggests Ellie Kowalchik, a real estate agent who leads the Move2Team with Keller Williams Pinnacle Group in Cincinnati, Ohio.

“There are good houses on the market now that aren’t getting the attention they may get in the spring with more buyer activity,” she says. “Less competition is good for buyers.”

The challenge: Multiple offers are common, and first-time buyers have less cash

More than one in four homes are still selling for above list price, according to October 2023 data from the NAR: 28% of homes sold for above list price that month. Homes for sale spent a median of 23 days on the market and saw an average of 2.5 offers, a sign that competition remains tough.

“Limited housing inventory is significantly preventing housing demand from fully being satisfied,” Lawrence Yun, NAR chief economist, said in a press release. “Multiple offers, of course, yield only one winner, with the rest left to continue their search.”

In general, first-time buyers come to the negotiating table with less cash than repeat buyers, reports the NAR. First-time buyers make a median down payment of 8%, while repeat buyers put down a median 19%.

And nearly one in three (29%) of sales were made in cash, reports the NAR, up slightly from 26% in 2022.

Your strategy: Use leverage where you have it

A good real estate agent can help you craft a strong offer, even if other buyers flash more cash.

Aziz Alhees, a real estate agent with Compass in Pasadena, California, has seen his share of wealthy investors making cash offers. He notes that they tend to bid below asking price since cash sales close faster. The promise of a quick closing is enough to get some sellers to turn down higher offers that ask for more time.

So Alhees competes on speed: With a mortgage preapproval and all other paperwork in hand, he prepares his buyers to close in 14 days.

“We’re not afraid of cash offers anymore,” he says.

On the flip side, if the sellers need more time to move out, a flexible closing timeline can sweeten some deals, too. But don’t waive the home inspection when you’re negotiating. It can be tempting, but you’re only hurting yourself if you later discover expensive problems.

The bottom line: Set realistic expectations

It’s fair to feel bummed out about high costs and low inventory. That’s especially true for first-time buyers who have been putting off their search, only to see the market remaining rough.

The solution: Think long term. Holding out for lower rates likely means you’ll face steeper prices and more competition. So if you’re determined to buy, find a place that suits your needs and budget as-is. Expecting perfection often means setting yourself up for disappointment.

“Sometimes I have clients that think they’re going to hit a home run the very first house they buy,” Moralez says. “And a lot of times I tell clients, well, sometimes it’s OK to be happy just getting on base.”

Federal Reserve left its key short-term interest rate unchanged again Wednesday, hinted that rate hikes are likely over and forecast three cuts next year amid falling inflation and a cooling economy.

That’s more rate cuts than many economists expected.

The decision leaves the Fed’s benchmark short-term rate at a 22-year high of 5.25% to 5.5% following a flurry of rate increases aimed at subduing the nation’s sharpest inflation spike in four decades. The central bank has now held its key rate steady for three straight meetings since July.

That provides another reprieve for consumers who have faced higher borrowing costs for credit cards, adjustable-rate mortgages and other loans as a result of the Fed’s moves. Yet Americans, especially seniors, are finally reaping healthy bank savings yields after years of paltry returns.

Best high-yield savings accounts of 2023

401(k) boon:Stocks surge, Dow Jones hits all-time high at close after Fed forecasts lower rates

Leaving savings behind:Many Americans are missing out on high-interest savings accounts. Don’t be one of them

Is a soft landing in sight? What the Fed funds rate and mortgage rates are hinting at

Will the Fed raise interest rates again?

The central bank didn’t rule out another rate increase as it downgraded its economic outlook for next year while lowering its inflation forecast. In a statement after a two-day meeting, it repeated that it would assess the economy and financial developments, among other factors, to determine “the extent of any additional (rate hikes) that may be appropriate to return inflation to 2% over time.”

Fed Chair Jerome Powell said at a news conference, noting the Fed’s key rate is “at or near its peak.”

while the Dow Jones Industrial Average closed at a record high after rising 1.4% following the Fed’s signals that it’s probably done lifting rates and is forecasting three cuts next year. The 10-year Treasury was down to about 4% from 4.21% on Tuesday.

Last month, Powell said high Treasury yields, if persistent, likely would constrain the economy and require fewer Fed rate increases,

In its statement Wednesday, however, the central bank didn’t acknowledge the recent decline in Treasury yields, suggesting yields are still relatively high and could spike again, crimping the economy.

“Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring and inflation,” the Fed said, repeating the language of its previous statement.

Is inflation really slowing down?

The Fed’s middle-ground approach may have been cemented Tuesday by a mixed report on the consumer price index. The good news was that overall inflation barely budged in November amid falling gasoline prices, pushing down annual price gains to 3.1% from 3.2%, still well above the Fed’s 2% goal.

The Federal Reserve System is the U.S.’s central bank.

When does the Fed meet again?

The first Federal Reserve meeting of the new year will be from Jan. 30 through 31.

Federal reserve calendar

Jan. 30-31

March 19-20

April 30- May 1

June 11-12

July 30-31

Sept. 17-18

Nov. 6-7

Dec. 17-18

The U.S. economy was strong in the third quarter as consumers continued to spend despite high interest rates and inflation.

The value of all services and products generated in the U.S., or GDP, rose at a seasonally adjusted 4.9% for the year in the months spanning July to September, according to the Commerce Department. That was more than twice the 2.1% increase in the previous quarter and the most aggressive pace of growth since the end of 2021 when the economy surged back from a recession sparked by the pandemic.

a recession over the next year, down from the 61% odds forecast in May.

Barclays predicted a loss of roughly 375,000 jobs by the middle of next year. But consumer spending remains robust despite high inflation and interest rates that are making credit card use and consumer loans more expensive. And that may help stave off a recession, says Barclays economist Jonathan Millar.

What does FOMC stand for?

The FOMC is the Federal Open Market Committee, the voting body responsible for setting interest rates. The 12-member committee includes seven members of the Board of Governors and five of the 12 Reserve Bank presidents.

What causes inflation?

Inflation can have many roots. Typically, it’s caused by “a macroeconomic excess of spending over the economy’s relative ability to produce goods and services,” said Josh Bivens, the director of research at the Economic Policy Institute, a left-leaning think tank based in Washington D.C.

That means more people are wanting items and services than there is adequate supply, leading producers to raise prices.

“If everyone in the economy, tomorrow, decided they weren’t going to save any money from their paychecks, and they’re just going to spend every last dollar out of the blue, they would all run to the stores and try to buy things,” Bivens said. “But, producers haven’t produced enough to accommodate that big surge of across-the-board spending. So, you would see prices bid up.”

Inflation can also happen when there are too few producers, or there aren’t enough employees to provide the coveted products and services, Bivens said.

Finally, economies also have some “built-in inflation” to help keep inflation in check. In the U.S., that target is 2%, meaning businesses can raise prices 2% annually year and that shouldn’t overburden consumers. That’s also the typical cost of living raise offered by employers.

Inflation meaning

Inflation is the term for a “generalized rise in prices,” according to Josh Bivens, head of research at the Economic Policy Institute, a left-leaning think tank based in Washington D.C.

Everything from food to rent can become costlier due to inflation. But it is the overall impact that determines what the inflation rate actually is.

“Inflation, though, really is meant to only refer to all goods and services, together, rising in price by some common amount,” Bivens said. The Federal Reserve’s inflation goal is 2%, which means businesses can hike prices by 2% a year and that shouldn’t cause consumers financial distress. Cost of living increases to workers’ pay are also expected to meet that target to ensure consumers can adequately deal with the rising costs of goods and services.

What is CPI?

In November, the Consumer Price Index (CPI) ‒ a measure of the average shift in prices for different products and services ‒ was 3.1%, down slightly from the month before.

Annual inflation is down dramatically from the 9.1% in June 2022 that marked a 40-year high but remains above the 2% target the Fed sees as the level that signals the rate of price increases is under control.

Why is CPI important?

The Federal Reserve watches two key aspects of the economy, price stability and maximum employment, and those are the main factors it takes into account for its interest rate decisions. The CPI is a primary measure the Fed looks at to help determine if prices are “stable.’’

What is the difference between CPI and core CPI?

Core prices don’t count the volatile costs of food and energy items, giving a more accurate window into longer-term trends.

Are wages going up in 2024?

If you’re deemed a top performer at a company that is offering raises, you’ve got a pretty good chance of getting a pay boost next year.

About 3 out of four business leaders told ResumeBuilder.com they intended to give raises. But half of those company executives said only 50% or less of their staff members would see a pay hike, and 82% of the raises would hinge on performance. For those who do manage to get the salary boost, 79% of employers said the pay hikes would be greater than those given in recent years.

Are U.S. Treasury yields rising?

Not recently.

The 10-year Treasury yield was above 5% in November when the Fed kept rates steady for the second consecutive month the first time it had left the key rate unchanged two months in a row in almost two years.

That led to mortgage rates spiking to almost 8% and pushed up other borrowing costs for consumers and businesses. Stocks meanwhile sank close to a recent low, leading Fed Chair Jerome Powell to say such financial pressures could achieve the same cooling effect on the economy as additional rate hikes.

But in the following weeks, 10-year Treasury yields dipped to 4.2% and stocks rebounded. That might make the Fed resist rate cuts in case the economy heats up and causes the broader dip in prices “to stall at an uncomfortably elevated level,” Barclays says.

Barclays and Goldman Sachs forecast that rate cuts won’t happen until the spring, and that there will be only two, to a range of 4.75% to 5%, with more cuts implemented in the next two years.

When will inflation go back to normal?

It may take a little while.

Inflation’s decline likely “won’t show much progress in coming months,” Barclays wrote in a research note.

Overall price hikes have eased significantly since peaking at 9.1% in June 2022, a four-decade high. And in October, broader inflation as well as core prices experienced a dip, leading to a lower 10-year Treasury yield.

But core prices, which exclude the volatile costs of food and energy, will probably rise 0.3% each of the next three months, Goldman Sachs says. Used cars and furniture have been getting cheaper as the supply-chain shortages of the pandemic end. Meanwhile, health care, auto repairs, car insurance and rent continue to get more expensive, as employers pay higher wages to attract workers amid a labor shortage lingering from the global health crisis.

What is core inflation right now?

Core prices, which leave out the more volatile costs of food and energy, bumped up 0.3% in November, slightly more than the 0.2% uptick seen the previous month. That kept the yearly increase at 4%, the lowest rate since September 2021.

New inflation tax brackets

Inflation may also impact the amount of taxes you have to pay.

The Internal Revenue Service said in its annual inflation adjustments report that there will be a 5.4% bump in income thresholds to reach each new level in next year’s tax season.

In 2024, the lowest rate of 10% will apply to individuals with taxable income up to $11,600 and joint filers up to $23,200. The top rate of 37% will apply to individuals earning over $609,350, and married couples filing jointly who make at least $731,200 a year.

The IRS makes these adjustments annually, using a formula based on the consumer price index to account for inflation and stave off “bracket creep,” which happens when inflation shifts taxpayers into a higher bracket though they’re not seeing any real rise in pay or purchasing power.

The 2024/25 increase is less than last year’s 7% increase, but much more than recent years when inflation was below the current 3.1% inflation rate.

Will Social Security get a raise because of inflation?

Yes, but it will be a lot less than what recipients received in 2023.

The cost-of-living adjustment, or COLA, to Social Security benefits will be 3.2% next year. That’s roughly one-third of the 8.7% increase given in 2023, which marked a forty-year high.

The 2024 COLA hike is above the average 2.6% raise recipients have received over the past two decades, but seniors remain concerned about being able to pay their expenses as well as the increasing possibility Social Security benefits will be reduced in coming years, according to a retirement survey of 2,258 people by The Senior Citizens League, a nonprofit seniors group.

How does raising rates lower inflation?

The federal funds rate is what banks pay each other to borrow overnight. If that rate increases, banks usually pass along that extra cost, meaning it becomes more expensive for businesses and consumers to borrow as rates rise on credit cards, adjustable rate mortgages and other loans. That’s why the funds rate is the key mechanism used by the Federal Reserve to calm inflation.

Simply put, companies and consumers don’t borrow as much when loans cost them more, and that means an overheated economy can cool and inflation may dip.

Will credit card interest rates continue to rise this holiday season?

The Fed’s string of rate hikes, aimed at easing the highest inflation in four decades, are a big reason credit card interest rates have reached record highs just in time for the holiday season.

Some retail credit cards now charge more than 33% interest, topping a 30% threshold that stores and banks were previously able to bypass but seldom did – until now.

“They can charge that much,” said Chi Chi Wu, a senior attorney at the nonprofit National Consumer Law Center. “Credit cards can actually charge whatever they want. It’s a little-known fact.”

The domino effect of a high benchmark rate and soaring credit card interest could put many Americans in financial straits this holiday season.

Though some consumers are paring back to deal with high prices, rising debt and shrinking savings, the average shopper expects to spend $1,652 this year on holiday purchases, according to the consultancy Deloitte, more than was typically spent in the last three years.

A lot of the buying will be done with credit cards. In an October poll of 1,036 shoppers by CardRates.com, nearly 4 in 10 respondents said they intend to have holiday credit card debt in the new year.

The nation’s collective credit card debt was $1.08 trillion, at the end of September, a record high. And the average interest rate was 21%, the highest ever documented by the Federal Reserve.

Savings account impact of high rates

The upside to the Fed’s string of rate hikes has been that consumers were able to earn good interest on their savings for the first time in years. Even when the Fed leaves interest rates unchanged, savers can do well.

Unfortunately, most account holders aren’t making the most of that potential opportunity.

Roughly one-fifth of Americans who have savings accounts don’t know how much interest they’re earning, according to a quarterly Paths to Prosperity study by Santander US, part of the global bank Santander. Among those who did know their account’s interest rate, most were earning less than 3%.

But consumers have time to make a change that could enable them to make more from their savings.

“We’re still a long way from (the Fed) beginning to cut rates,” said Greg McBride, chief financial analyst at financial services platform Bankrate. “This is great news for savers, who will continue to enjoy inflation-beating returns in the top-yielding, federally insured online savings accounts and certificates of deposit. For borrowers, interest rates staying higher for a longer period underscores the urgency to pay down and pay off costly credit card debt and home equity lines.”

The string of Fed rate hikes that began in March 2022 has made it costlier for consumers to borrow as interest rates on credit cards and other loans increased dramatically.

At the same time, inflation has made daily needs more expensive, pushing more Americans to lean on credit cards to get by. But lenders have become more reluctant to issue new cards, so in the midst of the holiday season, more shoppers are seeking higher credit limits, experts say.

In October, the application rate for higher limits rose to 17.8% from 11.2% in the same month the previous year, and from 12.0% in 2019, New York Fed data showed.

For some consumers, a higher limit on a card they already have is about their only option.

“After COVID, inflation and interest rates went out of control … people have less emergency funds for car repairs or buying presents,” said Brandon Robinson, president and founder of JBR Associates, which specializes in retirement strategies. “What they’re doing is using more credit card utilization – over 30% or well over 50% of their credit card allowance – and then can’t get approved for another card because their credit rating is down.”

Inflation is leading more Americans to work multiple jobs

The number of Americans working at least two jobs is at its highest peak since before the COVID-19 pandemic, according to federal data, an uptick that may reflect the financial pressure people are feeling amid high inflation.

Almost 8.4 million people had multiple jobs in October, the Labor Department said, a figure that represents 5.2% of the laborforce, the highest percentage since January 2020.

“Paying for necessities has become more of a challenge, and affording luxuries and discretionary items has become more difficult, if not impossible for some, particularly those at the lower ends of the income and wealth spectrums,” Mark Hamrick, senior economic analyst at Bankrate, told USA TODAY in an email.

People may also be moonlighting to sock away cash in case they’re laid off since job cuts typically peak at the start of a new year.

What is the Federal Reserve’s 2024 meeting schedule? Here is when the Fed will meet again.

What is the mortgage interest rate today?

Mortgage rates are falling, so is it time to buy?

It depends.

First of all, the Fed doesn’t directly set mortgage rates, but its actions have an impact. For instance, when the central bank was steadily boosting its key rate, the yield on the 10-year treasury bond went up as well. Because those bonds are a gauge for the interest applied to an average 30-year loan, mortgage rates increased.

But over the past six weeks, mortgage rates have been declining, averaging 7% for a 30-year fixed mortgage. That’s down from almost 7.8% at the end of October, according to data released by Freddie Mac on Dec. 7.

That may be giving some wannabe homeowners the confidence to start house hunting. For the week ending Dec. 1, mortgage applications rose 2.8% from the prior week, according to the Mortgage Bankers Association.

“However, in the big picture, mortgage rates remain pretty high,” says Danielle Hale, senior economist for Realtor.com. “The typical mortgage rate according to Freddie Mac data is roughly in line with what we saw in August and early to mid-September, which were then 20 plus year highs.”

So, many potential buyers may still need to sit on the sidelines, waiting for rates to drop further, says Sam Khater, chief economist for Freddie Mac. Hale and many other experts believe mortgage rates will dip next year.

Interest rate projection 2024

The Fed is expected to cut interest rates next year, though markets and economists disagree about how many rate cuts there will be.

Futures markets forecast there will be four or five rate cuts in 2024, amounting to a quarter of a percentage point each. The cuts, they predict, should start by spring, and ultimately drop interest rates as low as 4% to 4.25%.

But core prices, which leave out the volatile costs of food and energy and are the metric followed more closely by the Fed, ticked up 0.3% in November, higher than the 0.2% increase the month before. That might make the Fed more hesitant to nip rates in the immediate future.

Goldman Sachs and Barclays expect there to be only two rate decreases in 2024. And Fed Chair Jerome Powell has cautioned in recent public remarks that it was “premature” to talk about rate cuts.

November inflation report

Inflation dipped slightly last month, with falling gas prices mitigating the impact of rising rents.

Consumer prices overall increased 3.1% from a year earlier, slightly below the 3.2% rise in October, according to the Labor Department’s consumer price index. That slower pace moves the inflation rate nearer to the level, reached in June, that was the lowest in over two years. Month over month, prices increased a slight 0.1%.

Core prices, however, which leave out the more erratic costs of food and energy and which are more closely monitored by the Fed, increased 0.3% in November after rising 0.2% the previous month. That means core inflation’s yearly increase remained at 4%, though it’s the lowest level since September 2021.

Companies issue earnings frequently, often on a quarterly basis. But knowing how to read an earnings report isn’t easy, and it requires a bit of legwork to get up to speed and understand the financials that businesses are reporting. Even so, it can be important, as those financials may help dictate your next investment moves.

Again, by learning how to read an earnings report, you could unlock invaluable information about the state of a company over time, as well as come to your own conclusions about whether the company’s stock is a worthwhile buy for you.

The Basics of Earnings Reports

When you invest in a stock, you are investing in a small sliver of ownership in a publicly traded company. To be publicly traded, companies are required to file quarterly (and annual) financial statements with the U.S. Securities and Exchange Commission (SEC).

For the uninitiated, looking at an earnings report may be akin to trying to read hieroglyphics. But you can break down the essentials and with some practice, it should all start to make sense.

Understanding the Essentials of Earnings Reports

Again, earnings reports are financial filings that keep shareholders and regulators apprised of the financial and legal standing of a company, typically filed quarterly. Financial transparency also allows current and potential investors to make decisions about the company through their own analysis and judgment.

Earnings reports contain information about company performance and critical metrics such as profits and revenue (or similar terms, like “net income”), and how those metrics compare to previous quarters or years. They also generally include some guidance or comments from company leadership.

The Timing of Earnings Releases

Generally, when you hear someone speaking of a general “earnings report,” they are referring to the forms 10-Q and 10-K, which are quarterly and annual financial filings, respectively. Both disclose a company’s revenue, expenses, profit, and other financial information each quarter.

The Anatomy of an Earnings Report

Some earnings reports are more in-depth than others, but they tend to all have at least some common elements. That includes an income statement (which, again, contains information related to profits, revenues, and losses), balance sheet, cash flow statement insights, and a statement of shareholder equity, which could be a breakdown of a company’s complete financial picture, along with assets and liabilities. In all, the report could be dozens of pages long.

Going deeper, here are some of the key elements.

Income Statement: How much money a company made over a period of time. Usually, the current quarter’s information is compared to previous quarters or multiple quarters.

Balance Sheet: What a company owns and what they owe—its assets and liabilities.

Cash Flow Statement: This section details the exchange of money between the company and the outside world over a given period of time.

Statement of Shareholder Equity: Changes of interest for the company’s shareholders over a given period of time. Here, you’ll find information on the value of all outstanding shares along with the potential dividend payment made by the company during the previous quarter(s).

For many investors, the income statement is of particular interest. This document details how much a company earns, how much it spends, and how profitable it is over a certain period of time. These numbers can reveal a lot about where a business is at and where they’re headed. 💡 Quick Tip: Investment fees are assessed in different ways, including trading costs, account management fees, and possibly broker commissions. When you set up an investment account, be sure to get the exact breakdown of your “all-in costs” so you know what you’re paying.

Beyond the Numbers: Interpreting Earnings Reports

Understanding the basics of an earnings report is one thing. Using what’s gleaned from those reports is another.

Reading Between the Financial Lines

What does an earnings report actually tell you, as an investor? It’s not always so clear. In that sense, it’s important to try and put the numbers in the report into context so that it can help you plan your next market move – if you make one at all.

Looking deeper at the financials, though, here are some key terms and items to look for, which are typically found in the income statement.

Revenue: A company’s sales. This is also known as the “top line,” because it sits at the top of the cash flow statement. This figure does not take into account the costs of running a business, so may not be the best indicator as to the overall financial health of a company.

Cost of Revenue/Cost of Sales: Directly under the revenue or sales figure you’ll find a section that details the costs of producing the goods sold, such as production and manufacturing. To be clear, these are not all of the costs associated with running a business, only the costs directly associated with the sale of the product or service.

Below this figure, you will find the section referred to as “gross profit” or “gross margin,” which is the cost of revenue subtracted from the revenue. It is called “gross” because the figure is not net of all costs associated with running a business—only the costs associated with sales.

Operating Expenses: These are the costs of running a business that cannot necessarily be attributed to a company’s operations for a given period. Research and development, marketing expenses, and salaries of administrative personnel are all examples.

Here, it is possible to account for depreciation expenses, such as the wear and tear on assets such as machinery and tools or other assets that are used over long periods of time.

At this point in the cash flow statement, a company may account for adjustments to income due to interest earnings or expenses (such as earning interest in a savings account or paying interest on debts) or income taxes. Sometimes, this information is listed separately.

Earnings: This is a company’s profits, also known as the net income or “bottom line,” because earnings exist at the bottom of the cash flow statement after all costs are subtracted. This is the money that the company made in the previous quarter after all costs of running the business are accounted for. Ultimately, this is going to be the number that most concerns shareholders, as a profitable business model is what attracts many investors.

Not all businesses are profitable all of the time, so it is possible that an earnings number can reflect a loss. When a company is recording a loss, the number is written inside of parentheses.

Earnings Per Share (EPS): While the earnings figure is certainly important, it’s helpful to have some context as to what that means to investors. The EPS calculation divides the earnings figure by the number of outstanding shares to derive a figure that represents what it would look like if those earnings were to be evenly spread across all shareholders.

For example, an EPS number of $1 would indicate a $1 earning per share of outstanding stock. However, a $1 EPS does not necessarily mean that’s what the company pays out to each shareholder.

Instead, it’s a way for investors to compare profitability across businesses within the same industry, to a business’s past profitability, or to expectations for a company’s future profitability. More than anything, it is used as a tool for analysis.

For a more qualitative look at a business, you could take a look at the section titled Management’s Discussion and Analysis. Here, executives summarize both the numbers detailed in the financial statements and what’s going on in the business that might not be outwardly obvious simply by looking at the numbers.

For example, executives could take this time to discuss a merger or other market factors that may have led to skewed numbers for that quarter.

Assessing Financial Risk Factors in Reports

All businesses are facing some sort of risk, be it from growing competition in a specific sector, or increasing interest rates. Often, company leadership might discuss those risks in the commentary in an earnings release, or in an accompanying earnings call. Other times, investors can suss out potential risk in the numbers themselves (are revenues in a specific area falling, and why?). The important thing to know is that if businesses are facing some sort of risk, investors may be able to find clues as to how big of a threat those risks are in the filings.

The Earnings Season Explained

Investors are likely to become familiar with the term “earnings season,” and for good reason.

What is Earnings Season and Why it Matters

Earnings season refers to the four times during the year when companies release quarterly earnings reports, and many of them tend to do so around the same time. As such, it’s a sort of “season,” as investors get to dig through several earnings reports and try to suss out trends and make decisions regarding their portfolios.

The Impact of Earnings Reports on Stock Prices

Earnings season can be a volatile time for stock prices, as a company’s performance, put on paper and released to the world, allows everyone to see how it’s doing – and decide whether to buy, sell, or hold their stock. As such, an unexpected earnings report – good or bad – can create volatility in the market. That’s why investors will want to pay attention around earnings season.

Earnings Calls: What to Expect

Investors are able to take part in earnings calls, which often requires tuning in either online or by phone. While every earnings call is different, they tend to have the same elements: Company management (usually the CEO or another C-suite executive) discusses the top-line financial results for the period, and then discusses what’s ahead. 💡 Quick Tip: Look for an online brokerage with low trading commissions as well as no account minimum. Higher fees can cut into investment returns over time.

Getting the Most Out of Earnings Reports

As an investor, you’ll want to do what you can with the latest earnings reports. That includes pulling out the most pertinent information, knowing what to anticipate, and then synthesizing it all into actionable insights.

Analyzing the Report: TL;DR for Financial Reports

For most investors, the top-line financials, and perhaps any comments from company leadership, are the most important things to check out in an earnings report. For instance: did the company generate a profit? Was it more or less than expected? Are executives bullish or bearish about the coming quarter? If you’re strapped for time, those are the things you’ll want to know as an investor.

Upcoming Earnings Report Calls: What to Anticipate

Companies generally announce earnings calls well in advance – sometimes even months in advance. That gives investors plenty of time to plan to attend, and to make any pre-earnings market moves. It may be a good idea to read financial media or analyst reports, too, to get a sense of what to expect. Expectations are a huge element in the market, and even if a company reports strong numbers, they may be below expectations, causing share values to fall.

Leveraging Earnings Reports

At the end of the day (or earnings season), earnings reports are tools that investors can use to plan their next moves and hone in their investment strategy. But there are also sub-strategies that they can use during earnings season, too.

Strategies for Investors During Earnings Season

While some investors may find it profitable to day-trade or even swap options during earnings season, many investors may want to try and get a sense of where expectations lie, and position themselves accordingly. For instance, if expectations are that a company’s report will show it lost money, then an investor may want to sell their holdings, anticipating a fall in share prices the day earnings come out.

The opposite can also be true, however. Perhaps the safest play, though, is to stick to a buy-and-hold strategy, and not let any market volatility – earnings-induced, or otherwise – change that strategy.

Things to Consider for Quarterly Reports

As noted, considering top-line financial metrics and company leadership’s posturing is important for investors. But you may also want to think about the context of the earnings report – which quarter, or time of the year is it covering, for instance. If a retail company reports strong Q4 earnings, for instance, that may have been influenced by the holiday shopping season.

Or, if a food company is struggling with higher costs during the summer because of a drought causing shortages, that’s something else. There are lots and lots of factors that can affect a company’s performance.

Using Earnings Reports to Forecast Market Trends

It may be tempting to try and use earnings reports to forecast market trends, but tread carefully – nobody knows what the market is going to do next. There may be some things to be gleaned about what the future holds, but be careful and perhaps consider consulting with a financial professional before making any moves based on hunches.

Again, earnings reports are critical tools and troves of information for investors, but they are backward-looking, and the world is a wild place – you never know what’s going to happen next.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

Minnesota offers a variety of financial aid options, including grants, scholarships, work-study programs and student loans. In fact, the state awarded $210 million in financial aid — not including loans — to students in 2022.

The cost of education in Minnesota

Minnesota has 74 public and private non-profit colleges and universities and has a very average cost of living; it’s the 23rd most expensive state in the country. That trend carries over to the cost of higher education in the state — the cost of attending a four-year school in Minnesota is in line with national averages. The only exception is community college, which tends to be more expensive in Minnesota.

Public four-year school (in-state): $21,858 per year, about 2.4% higher than the national average of $21,337.

Private, non-profit four-year: $45,775, about 1.2% less than the national average of $46,313.

Community college (in-state): $5,545, about 58% higher than the national average of $3,501. (Community college numbers do not include room and board).

Financial aid options in Minnesota

Minnesota has several financial aid programs, and its public colleges and universities are competitively priced. But to qualify for in-state tuition and most state-based financial aid programs, you must meet the state’s residency requirements.

In Minnesota, you are considered a resident if you meet one of the following criteria:

You graduated from a Minnesota high school while living in the state.

You received a GED after living in the state for at least 12 months.

You lived in the state for at least 12 months for non-education purposes prior to enrollment.

You are a member of the Armed Forces stationed in Minnesota.

You are the spouse or child of a member of the Armed Forces stationed in Minnesota.

You are the spouse or dependent of a veteran who is a Minnesota resident.

You immediately relocated to Minnesota within 12 months of a presidential disaster area declaration if the disaster impacted your post-secondary education.

You are a refugee who immediately settled in Minnesota.

When it comes to undocumented students, including those with Deferred Action for Childhood Arrivals (DACA) status, Minnesota’s residency policies aren’t as strict as the policies of other states. As a result, undocumented students and DACA recipients in Minnesota are eligible for both in-state tuition and state-based financial aid.

Depending on your circumstances, you may qualify for one or more of Minnesota’s financial aid programs:

529 plans.

In-state tuition.

Scholarships.

Minnesota work-study.

Minnesota student loans.

Student loan repayment assistance.

529 plans

Unlike other states, Minnesota doesn’t have a prepaid tuition plan. But it does have a 529 college saving plan, MNSAVES, which you can use to save and invest for a child’s future education. You can open an account with $25.

With 529 plans like MNSAVES, you can invest your money and it will grow tax-deferred until your child is ready for college. When you withdraw money for eligible education expenses, the withdrawals aren’t taxable as income.

Minnesota provides families with another benefit: you can qualify for a state income tax deduction for contributing to a 529. If you’re married and file a joint return, you can deduct up to $3,000 per year on your state income tax return.

In-state tuition

Minnesota’s public higher education system consists of 26 colleges and seven universities on 54 campuses throughout the state. As a resident of Minnesota, you can save money on your degree by attending a public school within the state.

Minnesota also participates in tuition reciprocity and exchange programs, which could allow you to attend college in other states at a lower cost.

Reciprocity

Minnesota has reciprocity agreements with select states and regions: Wisconsin, North Dakota, South Dakota and the Canadian province of Manitoba. It also has a limited agreement with Iowa Community College in northwestern Iowa.

Under these agreements, Minnesota residents can attend school in participating areas at a reduced rate. They cover nearly all students, including full-time, part-time, undergraduate, graduate and some enrolled in professional certificate programs.

Midwest Student Exchange Program (MSEP)

MSEP is a tuition network that allows students to attend a public school in a participating state and pay up to 150% of the in-state rate for qualifying programs. If the student attends a private school in a participating state, the tuition is reduced by 10%.

Minnesota residents eligible for reduced tuition through MSEP in the following states:

Minnesota grants

Minnesota provides more grant aid than 32 other states. On average, the state awarded about $1,000 per full-time undergraduate student in 2020-21.

Minnesota offers five grant programs:

Alliss Opportunity Grant Program for Adults Returning to College

Two-Year College Opportunity Grant: Students with financial need attending Minnesota State Colleges and enrolled in two-year programs or certificate courses can qualify for up to $1,100 per year.

University Grant: Full-time undergraduatestudents attending four-year Minnesota State Universities can qualify for a grant of up to $1,100 per year.

Fostering Independence Higher Education Grant

Minnesota residents who are under the age of 27 and were previously in foster care may be eligible for the Fostering Independence Higher Education Grant. This award is a last-dollar grant, meaning it can cover your remaining costs after deducting your expected family contribution, federal and state aid, foster care Education and Training voucher and other scholarships or grants.

To qualify, you must submit the FAFSA or Minnesota Dream Act application and attend a participating school.

Minnesota Future Together Grant

The Minnesota Future Together Grant is a program designed to help students earn degrees in high-need areas like healthcare, engineering and early childhood education. If eligible, you could qualify for a tuition-free degree from an eligible public school.

There’s an income limit, and you must submit the FAFSA or Minnesota Dream Act application to qualify. The grants are available from spring 2022 through 2024, or until all funds are dispensed, whichever comes first.

Minnesota State Grant

The Minnesota State Grant is a financial aid program for low- to moderate-income students. Award amounts vary, but the grant is based on the difference between what the student and their family are expected to pay and the actual cost of attendance at their selected college.

In 2018-19, the maximum grant award ranged from about $7,845 at a public two-year college to $12,345 at a private four-year college, and the average award was $2,603.

Minnesota Student Teacher Grants

Students enrolled in teacher preparatory programs may qualify for a Minnesota Student Teacher Grant during the term in which they complete their 12-week student teaching experience. There are two types of awards:

Minnesota Student Teachers in Shortage Areas Grant. This is awarded to students who intend to teach in rural school districts or license shortage areas.

Minnesota Underrepresented Student Teacher Grant. This is awarded to students who belong to racial or ethnic groups underrepresented in Minnesota’s education workforce.

Grant recipients can receive up to $7,500 for one term.

Minnesota scholarships

Minnesota has five college scholarship programs. These awards are typically based on merit, though some do take the student’s financial need into consideration:

Minnesota Academic Excellence Scholarship

The Minnesota Academic Excellence Scholarship is for high school graduates who enroll in a bachelor’s degree program at the University of Minnesota, a Minnesota state university or a private degree-granting school within the state the same year they graduate from high school. Depending on the school, the award can cover up to the full price of tuition and fees for one academic year. It can be renewed for up to three academic years.

To qualify, students must attend a participating school and display achievements and potential in English, creative writing, fine arts, foreign languages, math, science or the social sciences.

Minnesota Aspiring Teachers of Color Scholarship

The Minnesota Aspiring Teachers of Color Scholarship is a pilot program that provides financial aid to eligible undergraduate and graduate students preparing to enter careers as teachers who belong to underrepresented racial or ethnic groups. Qualifying students enrolled in an eligible program can receive up to $10,000 per year, up to a lifetime maximum of $25,000.

Minnesota Indian Scholarship

Students with financial need who are one-fourth or more of American Indian ancestry or who are an enrolled member or citizen of a federally-recognized American Indian tribe or Canadian First Nation may be eligible for the Minnesota Indian Scholarship program. The maximum award is $4,000 per year for undergraduate students and $6,000 per year for graduate students.

With this scholarship, students can get a lifetime maximum of up to 10 annual awards.

Minnesota Paramedic Scholarship

This award is for Minnesota residents attending an eligible paramedic program. The scholarship provides students with up to $5,000 per year for up to two years. Applications are not yet available, but students can expect them to be available after January 1, 2024.

North Star Promise Scholarship

The North Star Promise Scholarship is a new program that will be available in the fall of 2024. It is a last-dollar scholarship for Minnesota residents that covers the student’s remaining cost after deducting other scholarships, grants and tuition waivers.

To qualify, students must have a family adjusted gross income (AGI) below $80,000 and attend an eligible public school or tribal institution.

Minnesota Work-Study

Minnesota operates its own work-study program that provides eligible students with part-time jobs to offset the cost of their education. Work-study requirements and awards are set by the college’s financial aid office, but students earn an average of $1,903 per year through the program. All Minnesota public universities and most private institutions participate.

Minnesota student loans

If you have to borrow for college, consider federal student loans first. If you still have funding gaps, Minnesota offers a student loan program that might be better for you than other private loans.

SELF Loans

Minnesota’s student loan program is known as SELF. Unlike private loans, which typically base interest rates on the borrowers’ credit scores or income, SELF gives every student the same rate. Eligible students can borrow between $500 and $20,000 per year (the maximum varies by the student’s program of study).

To qualify, you must be enrolled in an eligible institution in Minnesota, or be a Minnesota resident enrolled at an eligible out of state school. You must also have a creditworthy co-signer.

Student loan repayment in Minnesota

Like many states, Minnesota has experienced worker shortages in certain fields. To address this problem, the state operates several loan repayment programs that help professionals repay their loans. In exchange, the borrower must commit to working in high-need areas for a specific period.

There are five loan repayment programs in Minnesota:

John R. Justice Loan Repayment

The John R. Justice Loan Repayment Program is a federal program administered by the Minnesota Office of Higher Education. It provides student loan repayment funding to full-time public defenders and public criminal prosecutors who serve full-time for three years. Award amounts vary based on program funding; previously, program participants received an average annual repayment award of $1,900 in 2019.

After the initial three-year commitment, eligible attorneys can reapply for more funding if they continue to serve.

Minnesota Rural Veterinarian Loan Repayment Program

The Minnesota Rural Veterinarian Loan Repayment Program is limited to current students and recent graduates of the Doctorate of Veterinary Medicine Program at the College of Veterinary Medicine, University of Minnesota. Eligible borrowers can receive up to $15,000 per year to repay their loans for up to five years, for a maximum of $75,000.

To qualify, participants must commit to working full-time for at least five years as licensed veterinarians in a designated rural area.

Minnesota Aviation Degree Loan Repayment Program

The Minnesota Aviation Degree Loan Repayment Program provides loan repayment benefits to eligible pilots and aircraft technicians living in Minnesota. To qualify, you must have received your degree in Minnesota, have a valid pilot or aircraft technician license and sign a contract agreeing to a five-year, full-time service obligation in the state.

The maximum award is $3,000 per year for aircraft technicians and $5,000 per year for pilots. The award can be renewed for up to five years.

Minnesota Agricultural Education Loan Repayment Program

Teachers who provide agriculture education to grades five through 12 at a Minnesota school may qualify for the Minnesota Agricultural Education Loan Repayment Program. By committing to a five-year service obligation, award recipients could receive up to $3,000 per year in loan repayment benefits, up to a total maximum of $15,000.

Minnesota Teacher Shortage Loan Repayment Program

Licensed teachers who work in designated shortage areas may qualify for loan repayment benefits through the Minnesota Teacher Shortage Loan Repayment Program. Recipients can receive up to $1,000 per year in loan repayment assistance paid directly to them, up to a lifetime maximum of $5,000.

How to apply for financial aid in Minnesota

To apply for Minnesota’s financial aid programs, follow these steps:

Submit the FAFSA or the Minnesota Dream Act Application. Most of Minnesota’s financial aid programs require students to submit the FAFSA. If you’re eligible for the FAFSA, you can complete and submit it at FAFSA.gov. Undocumented students who aren’t eligible for the FAFSA can still qualify for state-based aid by filling out the Minnesota Dream Act Application.

Review other requirements. Some programs, such as the Minnesota Indian Scholarship, have their own applications. Review the program’s website to find out what additional materials you may need to submit.

Contact your college’s financial aid office. Many of Minnesota’s financial aid programs are processed through college financial aid offices, so reach out to your school’s financial aid department if you have questions or to check your eligibility for certain programs.

Frequently asked questions

How many colleges are in Minnesota?

There are 74 public and private non-profit colleges and universities in Minnesota. Well-known schools include the University of Minnesota Twin Cities, Carleton College and St. Olaf College.

What is the deadline for FAFSA in Minnesota?

Minnesota’s FAFSA deadline for students who want to qualify for state-based aid is no later than 30 days after the term starts. Some Minnesota colleges may have even earlier deadlines, so contact your selected school’s financial aid office well in advance to find out exactly when you need to submit the FAFSA.

There are many pros and cons to investing in a small town as opposed to a larger town. I have many properties in small towns and larger towns and personally, I think the small towns are overlooked based on the many advantages they have. Some of the major differences in small towns are the taxes, demand, building permits, and more.

Pros of investing in real estate in a small town:

There are many advantages to investing in smaller towns. I have found some great deals in them and there were many advantages I did not think of until I had bought and operated a property in those small towns.

Lower property prices: Property prices in small towns are typically lower than in urban areas. This means that you can invest more property for your money. This is because fewer investors are looking at small towns. I have found multifamily and commercial to be much cheaper.

Higher rental yields: Rental yields in small towns are often higher than in urban areas. This means that you can generate more income from your rental properties. This rental yield comes from the fact that rents might be a little lower but prices are even lower relative to those rents producing a higher ROI.

Lower vacancy rates: Vacancy rates in small towns are typically lower than in urban areas. This means that you are more likely to find tenants for your properties. I have found this to be true as well because there are very few rentals, there are often people waiting for anything to pop up.

Stronger appreciation potential: Small towns are often experiencing population growth and economic development. This can lead to stronger appreciation potential for your investment properties. If there is a shortage of homes in the area, you could see huge appreciation if those homes are cheaper than the cost to build.

Lower taxes: In my area in Colorado the small towns often have lower property taxes and lower sales taxes. The property taxes can save thousands of dollars a year on larger properties.

Less regulations: Some small towns are also much easier to build and remodel in. Each town has different building permit processes and requirements. Some towns could be stricter but some could be very easy to work with.

Cons of investing in real estate in a small town:

Limited buyer pool: There is a smaller pool of potential buyers for properties in small towns. This can make it more difficult to sell your properties when you are ready to do so. If the town has a surplus of homes, prices could stay stagnant for many years.

Less access to amenities: Small towns may have fewer amenities than urban areas, such as shopping malls, restaurants, and entertainment options. This can make it more difficult to attract tenants and buyers.

More difficult to manage properties: It can be more difficult to manage properties in small towns, as there may be fewer qualified property managers available.

Less liquidity: Properties in small towns are typically less liquid than properties in urban areas. This means that it may be more difficult to sell your properties quickly if you need to do so.

Local politics: Some small towns may be difficult to work with or treat outsiders differently if you do not live there. This is not always the case but I have been told I can’t do certain things with a property and then had someone buy it from me in that small town and do exactly what I asked to do.

Is it worth investing in a small town?

I have had amazing luck investing in small towns. One of the properties I bought was a 4 plex for less than $200k in 2018. That property would have been at least $300k in the larger town 10 miles away. I have also had great luck with commercial property and single-family flips as well. There are challenges and just because there are advantages to investing in a small town, that does not mean it is easy.

[embedded content]

Conclusion

Before you invest in any property, make sure to research the local market and economy. This will help you understand the local roadblocks, rental yields, and surplus or shortages in the area. Talk to the city government, especially the zoning and permit people (they might be one person). Try to see if the population is increasing or decreasing and make sure you have contractors or property managers that will work in the area if you need them!

Are you a nurse who is looking to make extra income? Looking for the best side hustles for nurses? Whether you are looking for a part-time side gig or a full-time extra income stream, there are many ways to make extra cash as a nurse. Whether you are looking to pay off your student loans,…

Are you a nurse who is looking to make extra income? Looking for the best side hustles for nurses?

Whether you are looking for a part-time side gig or a full-time extra income stream, there are many ways to make extra cash as a nurse.

Whether you are looking to pay off your student loans, save for a vacation, retire earlier, or whatever else, there are many reasons why you may want a side hustle.

As a nurse, though, you may be wanting something that will fit into your already busy and tiring schedule.

When it comes to finding side work, there is no shortage of options for nurses. But, not all side jobs for nurses are created equal.

Related content on side jobs for nurses:

Best Side Hustles For Nurses

Medical transcription

Transcription is when you turn audio files or video content into a text document. As a medical transcriptionist, you would be converting voice recordings from doctors and others in the medical field into formal reports.

Medical transcriptionists are required to be knowledgeable about medical terminology, HIPAA, and more, which makes this a side hustle that a nurse would be somewhat familiar with.

Medical transcriptionists earn around $20 to $25 an hour.

There are also other types of transcription work that are not medical related. There are many businesses looking for transcriptionists – since general transcriptionists convert audio and video to text for virtually any industry, there really isn’t a typical client. Examples include marketers, authors, filmmakers, academics, speakers, and conferences of all types.

You can learn more at How To Become A Transcriptionist From Home.

Lactation consultant

A lactation consultant is someone who specializes in breastfeeding.

A hospital may have you on call, you may go in person to people’s homes to assist them with breastfeeding issues, you may start a website where you help families online, and more.

My lactation consultant at the hospital when I gave birth to my daughter Marlowe also happened to be a healthcare worker at the pediatrician’s office that we brought her to. So, she definitely had more than one form of income!

Night nanny

A night nanny (or sometimes called night nurse if they are a nurse) is someone who helps new parents take care of their children overnight.

You would be employed by a family, usually for a few weeks or a few months after a baby is born. You would be helping parents at nighttime so that they can get more sleep as well as learn how to take care of their new infant.

You will be changing diapers, feeding the baby, helping the baby go to sleep, and more.

A night nanny typically works 8-12 hours overnight.

Night nannies are sometimes licensed practical nurses or registered nurses, as new parents many times want the skills and expertise that a nurse has.

You may be able to find night nanny jobs through word of mouth, or on websites such as SitterCity.com or Care.com.

Telehealth nurse

Telehealth nurse jobs are in high demand and will continue to grow. A telehealth nurse is a nurse who sees patients online, such as by video or phone. You may be working part-time or full-time as a telehealth nurse.

As a telehealth nurse, you would be assisting patients with minor health problems as well as advising them if they should go to the emergency room or urgent care, for example.

A telehealth nurse may work from home (and simply require an internet connection), at a physician’s office, hospital, and more.

As a telehealth nurse, you are still required to be a registered nurse and to have passed the NCLEX examination.

Start a blog or website

I know a few nurses who have started blogs, and this is because a blog can help you make income in your spare time with a flexible schedule.

So, what is a blog? A blog is a website. A blog is content that is written on a website. It usually consists of articles, like the one you are reading right now.

Blogs can vary from person to person. You may create a blog to journal, to teach on a topic, to sell something, to tell a story, and so on. There are no exact rules about what your blog has to be used for.

You can blog about many different topics such as personal finance, travel, lifestyle, food, family, home, DIY, and more.

You can learn how to start a blog with my free How To Start a Blog Course (sign up by clicking here).

Become a caregiver

As a registered nurse, you have highly valuable skills that make you in demand for caregiving jobs, such as taking care of children and adults.

As a caregiver, you may be helping the elderly, helping people get ready for the day, taking care of them for a day, grocery shopping for them, and more.