On Thursday, 10yr yields came close to spiking 20bps, trough to peak, in the wake of hotter CPI data and a lousy 30yr bond auction. That’s a brisk day of selling and one that didn’t line up with this week’s theme (adjusting to softer Fed comments and pricing in some safe-haven flows surrounding the Israel/Gaza War). Today’s rally started early and stayed strong all night. A pop in consumer inflation expectations brought the rally to an end, but bonds held on to gains without any drama in the PM hours. MBS underperformed along with the short end of the yield curve.

Import Prices

0.1 vs 0.5 f’cast, 0.6 prev

Export Prices

0.7 vs 0.5 f’cast 1.1 prev

Consumer Sentiment

63.0 vs 67.2, 68.1 prev

1yr inflation expectations

3.8 vs 3.2 prev

5yr inflation expectations

3.0 vs 2.8 prev

10:11 AM

Steady gains overnight, flattening out into domestic hours. 10yr down 7.6bps at 4.621. MBS up a quarter point

11:46 AM

Slightly weaker into mid-day. Consumer inflation expectations aren’t helping. MBS up only an eighth on the day. 10yr down 5.8bps at 4.639.

03:42 PM

Very flat all day after earlier selling. 10yr down 7.2bps at 4.625, MBS up just over an eighth of a point.

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.

Mortgage rates that spiked last year have continued to rattle Colorado Springs’ housing market in 2023.

In September, for example, year-over-year home sales fell for the 16th consecutive month, a recent Pikes Peak Association of Realtors market trends report shows.

Homeowners who were able to sell their properties within days — and even hours — two to three years ago waited more than five weeks, on average, last month for a buyer to come along, according to the report.

A Pikes Peak Regional Building Department report shows that while single-family building permits — which signal the construction of new homes — rose modestly in September compared with the same time last year, last month’s total nevertheless was the lowest for any September since 2011 and continued a mostly weak trend of building permit numbers for the year.

“The market was dramatically affected by the rapid, historical increase in mortgage rates,” said Gordon Dean, a real estate agent with Re/Max Advantage in Colorado Springs and the incoming board chairman of the Pikes Peak Association of Realtors.

From mid-2019 through 2021, 30-year, fixed-rate mortgages — the most common loan for homebuyers —plunged to an average of 3% and below nationally, according to mortgage buyer Freddie Mac.

Those historically low rates fueled homebuying nationwide and, combined with a shortage of new and existing properties available for purchase, sent home prices to record highs in markets such as Colorado Springs. Home sellers often fielded multiple offers for their properties and frequently received bids that topped their asking prices by thousands and tens of thousands of dollars.

When 2022 began, 30-year, fixed-rate loans averaged 3.22% nationally, Freddie Mac figures show.

After the Federal Reserve began to hike interest rates last year to curtail soaring inflation, however, mortgage rates began a steady ascent. By year’s end, after briefly topping 7%, long-term mortgage rates stood at 6.42%.

Long-term rates stayed below 7% for much of this year, but began to climb again in late summer. By mid-August, 30-year, fixed-rate mortgages had jumped again; on Thursday, they rose to a national average of 7.57%, which was the highest since 2000.

“Several factors, including shifts in inflation, the job market and uncertainty around the Federal Reserve’s next move, are contributing to the highest mortgage rates in a generation,” Sam Khater, Freddie Mac’s chief economist, said in a news release this month. “Unsurprisingly, this is pulling back homebuyer demand.”

And because many homebuyers felt priced out of the market because of higher rates or they no longer could qualify for a mortgage, the pace of buying, selling and construction slowed in Colorado Springs and the Pikes Peak region, along with other areas nationwide.

“I think it’s a good market because the demand is high,” said Grace Covington co-owner and co-CEO of Covington Homes, a Springs builder.

“We have a lot of people who are ready, willing and want to buy, (but) just not able because of interest rates.”

With the third quarter in the books, here’s a snapshot look at where conditions stand for Colorado Springs’ single-family housing market:

• Home sales have fallen and can’t get up — or so it seems.

Space Command decision expected to positively impact Colorado Springs real estate market

In September, Colorado Springs-area home sales totaled 1,008, a 22.1% decline from the same month last year, the Realtors Association’s market trends report and Gazette historical data show. Likewise, last month’s total was the fewest number of home sales for any September since 2013.

“That’s not much, literally,” real estate agent Harry Salzman of Salzman Real Estate Services and ERA Shields Real Estate said of September’s sales.

Other numbers in the association’s market trends report and Gazette historical data that underscore the slowdown in sales: Year-over-year home sales have dropped each month since June 2022; sales for the first three quarters of this year totaled 9,402, a 24% drop from the same period a year ago; and year-to-date sales for 2023 are at their lowest point since the same period in 2014.

Also, homes spent an average of 38 days on the market before selling in September, up from 25 days a year ago.

• Pickings still are relatively slim when it comes to finding a home to purchase.

The supply of homes listed for sale at the end of September totaled 2,484. On the one hand, that total rose 2.6% over August and was the highest for any month since October of last year.

Yet, from a historical standpoint, inventory is low. In pre-Great Recession years, September listings routinely topped 4,000, which provided homebuyers with many more choices, Gazette historical data show.

Residents in Colorado Springs’ outlying areas watch as growth creeps closer

Some owners who bought their properties or refinanced when mortgage rates were in the 3% neighborhood and are considering selling are holding on to their properties for now, which has contributed to the tight inventory, real estate experts say.

Sure, those homeowners might want to move up or downsize, but they’re not willing to abandon their rock-bottom mortgage rate and take on a new loan that’s in the 6% to 7% range, the experts say.

At the same time, some homebuyers who purchased in 2021 or 2022 haven’t seen their values appreciate enough to a point where they can sell their property and get the price they need to pay off their mortgage and real estate costs, said Patrick Muldoon, broker/owner and president of Colorado Springs real estate company Muldoon Associates.

As a result, those homeowners aren’t selling, he said. Instead, they’re calling the property management side of his business, Muldoon said, and looking to rent their homes. That keeps those properties from being added to the overall inventory of houses for sale.

“I can’t sell my house or I tried to sell my house or I’m upside down on my house and my next option is, I’m a forced landlord,’” Muldoon said he’s hearing from some homeowners.

• Despite slow sales, home prices rose in September.

The median price of homes that sold last month rose to $475,000, a 3.3% year-over-year increase, the Realtors Association report shows. It was the first year-over-year increase in median prices since November 2022.

But if sales fell in September, why did prices increase? Blame tight inventory, Salzman said.

“It’s got to be supply and demand. Not a doubt,” he said. “We don’t have very many selections for people to take a look at, no matter what the price range is. Particularly, even if you’re, say, under $500,000 in a purchase price? There’s not much inventory to select.”

As a result, some sellers can list their homes at prices that are a little more aggressive than a few months ago, Salzman said.

“You’re going to get a better price today because if you’ve got a buyer today at these interest rates, they’re a motivated buyer,” he said. “And when you’re a motivated buyer, sometimes you might have to pay a little more, like we did a couple years ago, because there’s no inventory.”

Sign up for free: News Alerts

Stay in the know on the stories that affect you the most.

Success! Thank you for subscribing to our newsletter.

5 growth hotspots around Colorado Springs: A closer look

Muldoon suggested that the latest figures showing an increase in median prices in September might be misleading. Some of the homes that sold last month are on the high end of the price range, which pushed up the overall median price, he said.

A real estate agent friend told him “we’re only grading the winners,” Muldoon said. “We’re looking at the stats and we’re only grabbing the houses that have sold, and those houses that have sold are the upper end of the bell curve.”

And some sellers still are getting top dollar for their properties, even as the market has cooled.

Attractive properties that are in good condition and priced correctly to reflect the current market and comparable homes in their neighborhood still can receive multiple offers — just not nearly as many as a few years ago, said Dean, of Re/Max Advantage.

“When you can provide someone in a desirable school district and great condition and, hypothetically, a stucco rancher with three bedrooms on the main (floor), that is a golden goose egg in the marketplace and I would be shocked if, priced correctly … it’s probably going to draw multiple offers,” Dean said.

In fact, he said he and his wife, Amy, who’s also a real estate agent, marketed a home that fit that description — and fielded a cash offer that came in about $15,000 over the seller’s asking price.

• The new home side of the housing market also has felt the effects of high mortgage rates.

In September, building permits issued for the construction of single-family, detached homes totaled 136, a slight, 1.5% increase over the same month a year earlier, according to the Pikes Peak Regional Building Department. That figure doesn’t include townhomes, condominiums or duplexes.

As Colorado Springs grows, 20-somethings are the fastest growing cohort

Even with last month’s increase, and an inflated number of permits that builders pulled in June in advance of a building code change taking effect, single-family permits for the first nine months of 2023 totaled 1,791 — a nearly 35% nosedive from 2,738 during the same period in 2022.

“The interest rate environment is certainly the main culprit for that,” said Tom Hennessy, president and CEO of Challenger Homes, one of Colorado Springs’ largest builders. “When you have interest rates pushing 8%, you’re just making affordability that much more difficult for that many more people.”

The difficulty in affording today’s higher mortgage rates stands in contrast to a generally positive outlook for the Springs, Hennessy said.

“What’s really kind of interesting is, there’s still people looking (for homes) and Colorado Springs’ economy is still generally pretty good,” he said. “Unemployment is still low. We still have a lot of jobs moving in. We have a lot of military in and out of the area. People want to buy. It’s just of matter of can they buy?”

Not only have buyers been stymied by high mortgage rates, but their costs for consumer goods, utilities and other expenses have soared because of inflation, said Covington, who’s co-CEO and co-owner of her homebuilding company with her husband, Ron.

Businesses saddled with high interest rates for loans have passed on their increased costs to consumers, which also affects their personal finances and their ability to buy homes, Grace Covington said.

“We really just need to get inflation under control and rates down again,” she said.

For now, Challenger, Covington and other builders continue to woo buyers with mortgage rate buydowns — incentive programs in which they effectively reduce, or buy down, a mortgage rate for the first few years of a loan to help buyers afford monthly payments and get them into a new home.

A year ago, builders also might have offered incentives such as discounts on premium lots or reduced prices on home upgrades to interest a buyer, Hennessy said.

Now, however, mortgage buydowns are the main focus for builders, he said.

“Today, it pretty much all deals with house payment and buying down the mortgage rate,” Hennessy said.

“The name of the game today is house payment. How can I get into a house with a payment that I can afford?”

• What’s ahead for Colorado Springs’ housing market?

That’s a question that every real estate agent and builder wants to know.

Who Are We? What the population numbers for El Paso County and Colorado Springs show

Salzman advices homebuyers who can afford a home to take the plunge now, even if prices remain high. The value of their investment always will appreciate over time, he said, and today’s 7% mortgage can be refinanced lower when rates fall.

Even if rates are high today, Salzman suggests that buyers talk with their mortgage lender to ask about getting a break on their loan origination fee in exchange for agreeing to refinance with the same lender in two to three years.

“Because their business is way down, anything is negotiable,” Salzman said of mortgage lenders.

A drop in mortgage rates, not surprisingly, would help boost sales and the overall market, Dean said. But how far would rates have to fall?

Six percent and below, he said, would help encourage borderline buyers to jump back into the market and persuade owners with a low mortgage rate to feel comfortable leaving it behind and accepting a higher rate to get the home they want.

“If we do see a reasonable drop, and I say reasonable, 6 flat on interest rates, we’re going to have a very robust market again,” Dean said.

Colorado Springs’ ‘beating heart?’ Check the pulse of downtown, mayor and area backers say

“For me personally, at the end of the day … it’s that interest rate that’s going to be the main driver for anybody,” he added. “Affordability. That’s affordability, in my opinion.”

Muldoon, however, echoed his previous bearish comments on the outlook for the housing market.

A recession in 2024, waves of layoffs, more bank failures, continued high interest rates and other national economic forces could have a ripple effect on local businesses and employers in Colorado Springs, Muldoon said. As a result, the local housing slowdown could continue and even worsen — with falling prices being one of the biggest impacts, he said.

“If Colorado Springs started showing signs of economic issues,” Muldoon said, “then you would see sellers start with some pretty swift reductions on prices.”

Inside: Looking for a job that pays at least $25 per hour? This list has the best jobs that fit that description. Each job offers unique benefits and opportunities, so take a look and see if any of them match your interests and skills.

Making $25 an hour is not a pipe dream; it’s a viable reality for thousands of people worldwide.

Earning such an income not only instills a sense of financial well-being but also provides a robust platform to plan for the future.

Today, we dive into elucidating the different opportunities potential jobs offer, aligning your skills and experience with an hourly rate that feels just right for your wallet.

Hence, securing such a job is not a function of luck but more a strategic alignment of skills, passion, and industry demands. But if you’re not entirely sure about where to begin or how to hone your skills for these high-paying jobs, don’t worry.

Imagine earning smooth entry-level jobs 25 an hour, all from the comfort of your workspace. Sounds enticing, right?

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Jobs That Pay $25 an Hour

This section will highlight various professions across distinct fields that provide such a desirable pay rate.

Looking for jobs that pay $25 per hour? We’ve got you covered.

Whether you’re transitioning careers or just starting, this list could help you discover a role that fits your skills and experience.

1. Paralegal

A paralegal role is an excellent job choice due to the vast knowledge gained in the field of law and legal procedures.

Being a paralegal involves a variety of interesting tasks, such as helping lawyers prepare for hearings, trials, and corporate meetings.

This position is not solely monetarily advantageous, it also presents opportunities for growth and professional development in the legal sector.

Earning Potential: It offers rewarding prospects with an average pay of $25 per hour, with the potential to earn up to $40 an hour depending on experience and expertise.

2. Landscaper

Why toil in a stuffy office when the great outdoors can be your workspace? Relish the satisfaction of planting, pruning, and mowing yourself into a healthier, happier lifestyle.

Ideal for nature enthusiasts and people persons out there, landscaping combines green-thumbed work with personnel management. A knack for the outdoors and previous work experience will be your stepping stones, while a certificate in grounds maintenance can make your application stand out.

Start by volunteering in your local community gardens or offering your services to neighbors. Through this, not only will your skills blossom, but your resume will flourish, too.

Earning Potential: You can expand your lucrative landscaping journey by owning your own company and training others to be laborers.

3. Truck Driver

Why is it a top-tier job, you ask? Consider this: truck drivers are the beating heart of global commerce, pivotal figures in ensuring warehouses stay stocked and goods reach their desired destinations. Plus, you’re free of the traditional office environment.

This job is perfect for those who prefer to work alone as well as those who prefer delivery routes that often stretch into the night.

You must be over the age of 21 years old and able to pass a CDL exam. Many truck drivers to a training course to get a jumpstart in the industry.

Earning Potential: Many truck drivers start their own company and will employ a couple of rigs to make passive income.

4. Social Media Marketing

Do you have a knack for creating engaging captions or a Sherlockian eye for data? Then Social Media Marketing could be your calling.

This position, hot in demand and rewarding, calls for creativity and analytical prowess.

Why is it a top job? Well, it’s not for the adrenaline rush of its fast pace. It’s the fact that you get to put your tech-savviness to great use. Social media marketers nurture and grow brands through smart strategies and engaging content.

Earning Potential: Many people start working for someone else as a Social Media Coordinator and then go on to open up their own business.

5. Event Planners

As an event planner, you are the unseen forces behind flawless galas, memorable weddings, and standout corporate functions. If you thrive on creativity, organization, and people skills, you will ensure that each event is meticulously executed.

This role allows you to blend creativity with pragmatic decision-making: from the captivating process of selecting venues, and coordinating with caterers

It’s a dream job for you if you love putting smiles on people’s faces and making their day unforgettable.

Earning Potential: An enticing reason is its attractive pay rate: on average, $24-28 per hour, peaking up to $40, with the potential of a quick pay raise. Plus those lucrative tips!

6. Mechanical Technician

If you’re seeking a rewarding, high-paying role that gets you hands-on with varied machinery, then a Mechanical Technician career.

This role is particularly apt for those with a fascination for machinery and a problem-solving mindset. To climb the ladder to success, one needs to keenly understand how to operate and maintain industrial machines, prevent damage, and optimize performance.

So gear up to diagnose, adjust, repair, and don’t forget – your hands, mind, and machines are a team.

Earning Potential: With an average pay of $26 per hour, you can start repairing machines and set up your own company.

Virtual Savvy

If you’ve ever wanted to make a full-time income while working from home, you’re in the right place!

This intensive training combines thousands of hours of research, years of experience in growing a virtual assistant business, and the power of a coach who has helped thousands of students launch and grow their own businesses from scratch.

Swipe our exact methods to start earning a living from anywhere as a VA – no experience needed!

Learn More

Download Free Checklist

7. Maintenance Technician

This job is best suited for those who enjoy diagnosing technical puzzles and are adept at hands-on solutions.

By developing a strong mechanical aptitude, attention to detail, and top-notch problem-solving skills. Remember, your primary duty is ensuring machinery and equipment operate smoothly – the backbone of any industry.

Start by checking out some free online webinars or training programs related to industrial maintenance.

This is a low-stress job that pays well without a degree.

Earning Potential: As an entry-level worker, you can start by having a vocational certification or general education diploma (GED).

8. HVAC Technician

This role is perfect for those who love hands-on work and can’t get enough of problem-solving – who wouldn’t enjoy the thrill of being an office’s last defense against an impending heatwave?

The key to thriving in this breezy career path is training – dive into an HVAC training program at a vocational school or consider an associate degree in RACH (refrigeration, air conditioning, and heating).

Earning Potential: Being an HVAC technician pays around $25.75 an hour, which will keep your bank balance healthily ‘ventilated’. By having experience, your hourly wage can increase more.

9. IT Support Specialist

If terms like configuring, maintaining, and troubleshooting tech equipment are your weekend chat topics, you’re the perfect match for this.

Thanks to Google’s free certification program, you can start this job by having online training in your spare time.

Start your journey by heading over to Google’s free IT certification program today. Master the IT realm, earn well, and enjoy your work- the trifecta is right there!

Earning Potential: An IT Support Specialist has an average above $25 an hour wage and could rise to $51 an hour for having experience.

10. Day Trader

By poised as a top job due to its flexibility and potential for high earnings, day trading allows you to take full control of your income by making well-informed decisions about the financial market.

It’s perfect for those with an acute mind for numbers, an unflappable nerve, and those who enjoy working from the comfort of their study.

All it takes to get started is some knowledge about the stock market – something you can easily acquire by attending a free webinar or training, which is accessible online!

Of course, remember the golden rule – never invest money you can’t bear to lose. Now, conquer the finance world, one trade at a time!

Earning Potential: By having the eagerness to be a learner and acquire more knowledge about this job, you can earn way higher than you thought. But, there will always be a risk when trading stocks.

Trade & Travel

Learn to trade stocks with confidence.

Whether you want to:

Retire in peace without financial anxiety

Pay your bills without taking on a side hustle

Quit your 9-5 and do what you love

Or just make more than your current income….

Making $1,000 every.single.day is NOT a pie-in-the-sky goal.

It’s been done over and over again, and the 30,000 students that Teri has helped to be financially independent and fulfill their financial dreams are my witnesses…

11. Bartender

This job is perfect for friendly individuals! As you’re the life of the party.

Your life will be as vibrant as a well-mixed cocktail—chock-full of lively conversations and new friendships.

Bartending has a steep learning curve, but the payoff is big as it is a job that pays weekly and even daily. Know your spirits, perfect your pour, and master the mix—each skill is a toast to your increasing bank balance.

So, roll up your sleeves, flash that charismatic smile, and prepare to shake things up in the bustling world of bartending.

Earning Potential: With an entry-level job—at a local pub or a fine dining restaurant, you’ll get paid handsomely, at least $25 an hour.

12. Mechanic

The job is a perfect blend for those with a knack for solving complex issues and have the stamina to be on their feet for prolonged periods.

If you’re not averse to the roar of engines and the smell of oil, you might be the grease monkey we’re looking for.

This job is perfect for dipping your toes in oily water. So, go ahead, rev up your career with a mechanic job!

Earning Potential: Personally, my independent auto mechanic makes way more than $25 an hour, but he has years of expertise and opened his own shop.

13. Transcription

Transcription suits anyone craving flexibility or looking to dip their toes into fields like legal, medical, and entertainment.

To shine, you’ll need to master speed, accuracy, and the art of capturing every ‘um’ and ‘ah.’ Noise-canceling headphones and a quiet workspace are your best friends.

Kickstart your move to transcription with free training like a mini-course to see if you like it. Gain insights into making money and build your portfolio.

This high-demand job needs skills you convert audio into text.

Earning Potential: By working remotely as a transcription, you can earn an impressive $25 an hour or more.

Transcript Proofreading

Get the step-by-step guide Caitlin Pyle used to build a thriving at-home business making a full-time income!

A booming legal industry means that transcript proofreaders are in higher demand than ever…

Enroll Now

14. Accountant

Start your second act as an accountant today. The balance sheets await your expertise.

By aiding your clients in reviewing their financial information, preparing tax and finance documents, and updating their changes in tax laws or governmental regulations. Certified Public Accountants (CPAs) can earn exceptionally well.

The longer you’re in the industry, the more you can be able to demand potential compensation for your service. Just by conducting audits, successful financial and bookkeeping strategies. CPAs perform a pivotal role that justifies their earnings.

Earning Potential: Right now, there is a severe shortage of accountants graduating from college. So, your earning potential will substantially increase with each year of experience, and possibly earn up to $50 an hour.

15. Proofreader

Proofreader is an ideal job for detail-oriented individuals with a passion for perfect punctuation, splendid spelling, and grandiose grammar.

Did you get a degree in English or similar? Perfect! But remember, while it helps, it isn’t a must-have.

It’s an excellent stepping stone for a stay-at-home parent or anyone seeking to make some extra cash it is one of the best jobs for moms. So hop on the proofreading wagon and ride your way to a more profitable future!

Earning Potential: Just by sitting and reading on your couch, you can now hop on and start earning $25 an hour depending on experience.

16. Recreational Therapist

Bring great immense job satisfaction by improving the lives of those grappling with illness and disability.

To get started, all you need is a bachelor’s degree in recreational therapy and then obtain a Certified Therapeutic Recreation Specialist credential.

So, why wait to become an everyday hero with a salary that smiles back at your bank account?

Earning Potential: You can earn more than $25 an hour by being a Certified Therapeutic Recreational Therapist.

17. Dental Assistant

Do you have strong communication skills, and the ability to partake in a hands-on career?

Just sterilizing equipment or lending a diligent hand during treatments will be part of your daily grind. Ensure every instrument screams ‘clean’ before the dentist reaches for it.

To become a dental assistant, you typically need to earn a certification or diploma through a dental assisting program, which often takes about a year to complete.

On-the-job training may also be required, during which you’d learn about dental procedures, patient care, and office duties under the supervision of a dentist.

You may have found the tooth fairy’s best job yet! Dive in!

Earning Potential: With a wage average of $19 an hour and earning up to $25 just being a Dentist Assistant.

18. Certified Nursing Assistant

Have a career dream to dive into the healthcare industry? Familiarize yourself with basic health practices, hygiene, and safety procedures.

Start your journey as a Certified Nursing Assistant by attending to patients, assisting nurses, and providing emotional support to everyone. You will have to start a training program, but thankfully there are many to choose from.

Earning Potential: This career pays more than $25 an hour and might increase through experience and skills.

19. Housecleaners

According to Zippia, 48.9% of the housecleaner’s qualification is to have a high school diploma, but experience could help. You must have a strong understanding of cleaning procedures and practices.

Also, you can consider taking a course to learn about safety guidelines and recommendations.

Other important attributes include attention to detail, physical stamina, and excellent time management skills.

Earning Potential: Whether you’re a single mom or a high school graduate, you can potentially earn up to $25 an hour.

20. Nanny

Fascinated by child psychology or studying pedagogy? Or just love kids? Then, this job is tailored for you; it offers both consistent income and practical field experience.

Getting started can seem daunting, but it doesn’t have to be. Step into the kiddie world, it might just be the best move you make. Where you are not required to pass any school diploma.

You can find plenty of nanny gigs on Sittercity.

Earning Potential: If being a nanny is just a child game then I want in and earn up to an incredible $1000 to $1100 a week.

21. Delivery Drivers

Welcome to the job of a delivery driver, a blend of independence and earning potential on wheels. When you are good at your job, you don’t have customers wondering how late does Amazon deliver.

This career is a perfect fit for introverts who prefer their own company, the job offers flexibility with the ability to set your hours.

But, keep in mind that larger roles, such as FedEx, may require truck driving experience, the ability to lift heavy boxes, and the completion of a few additional checks.

Earning Potential: Most delivery drivers for FedEx and UPS are union workers. Thus, they have the union to fight for pay increases. Plus you can increase your salary by moving up in the ranks.

22. Licensed Plumbers

Get ready to hop into commercial, residential, and industrial projects, working flexibly based on your schedule.

If you love problem-solving and can handle the occasional wade through the muck, then this amazing career is for you! Don’t worry about your expertise level; It’s the perfect time for you to dip your toes into the world of plumbing.

Earning Potential: Don your gloves, grab your tool kit, and join the ranks of expert plumbers making upwards of $25 an hour.

23. Athletic Trainers

Are you into sports and fancy being in the thick of the action?

You are considering becoming an Athletic Trainer – a well-paid role that combines both your passions brilliantly. Then, get to work closely with athletes, which means you’re right at the heart of the sports action.

You’ll need to be certified and licensed in healthcare to offer your professional services. The ball’s in your court!

Earning Potential: Earning about $25 per hour, it’s among the few amazing careers that can up your game financially and health-wise. Also, it may take you to the Super Bowl as the team’s athletic trainer!

24. Customer Service Managers

So, you’re a people person with a knack for solving problems? Consider a job as a Customer Service Manager.

This job is best for ambitious, empathetic individuals who love making a difference in customer experience, enhancing team performance, and ensuring business profitability.

Want to up your game? Brush up on customer relationship tools like Hubspot or project management tools like Asana. Then, prepare to rule the customer service realm as an expert Customer Service Manager.

This can be a great non-phone work-from-home job as many customer service requests are handled through chat and email.

Earning Potential: One of the amazing careers that pay a satisfying $25 per hour, it’s a chance to flex those crucial customer service muscles while managing a team.

25. Freight Broker

With an average pay topping most traditional roles, this often-overlooked profession is a gem amidst the rubble.

Here’s why: Despite its lucrative nature, competition in freight brokerage is surprisingly low.

Jumpstart your journey with a free webinar or training – there are many available online. This will equip you with vital information about the ins and outs of the role and the industry.

Earning Potential: You will be surprised to learn what a freight broker’s salary can be.

Freight 360

Designed as a 101-level course on freight brokerage, you’ll learn the basics of freight brokering in this online course.

This course is designed for freight brokers in any setting, regardless of their employment status.

This course is designed to help you source more leads and move more freight. Or even start your brokerage!

Start Now

FAQs

Have you ever dreamt of earning $25 an hour with flexible hours at your convenience?

The list above are some of the jobs that can earn $25 an hour. However, try to evaluate yourself if the requirements perfectly suit you. By having skills and experience on the said job you can ace up and boost your chances of getting one of the high-paying jobs above.

Unlock and upgrade your skills now by attending any training that aligns with your dream job. Be able to receive a rewarding amount of earnings in your pocket!

These amazing careers above can fetch you at least $25 per hour. Start earning big and turn your dream into your paycheck.

Improving your skills through attending training, updating certificates, and seeking additional knowledge in your field. Plus, It increases your chances of landing a job that pays $30 an hour.

Actively applying for new jobs, particularly those that value your enhanced skills, can open the door to higher-paying opportunities potentially enabling you to reach that $30 an hour wage.

So master the craft, build your credibility, and let your work do the talking.

The ball is in your court now. Step up and start crafting your destiny, one skill (and dollar) at a time. So, start attending any training that is aligned with the career you’re looking for.

Find out what should I do for a living. Sign up for a free webinar or training. Sites like Udemy and Coursera offer a plethora of free courses to help you fine-tune your skills or discover new ones.

Which Applications will you Submit for jobs paying 25 an hour?

The possibilities in today’s remote job market are exhilarating. Amid the myriad of options, some rake in at least a solid 25-dollar-an-hour job.

Begin by brushing up on your skills or discovering new ones through free webinars or training sessions that align with your chosen profession to increase your qualifications. Make sure your resume is polished and start applying to suitable jobs in your field. The next step is nailing that job interview.

Thus, finding and applying for such lucrative positions is not just an aspiration for a better standard of living, but a practical step towards improved financial stability.

Remember to job-seek smartly and relentlessly. The end game is finding that perfect remote job – working on your terms, from your comfy corner of the world, and padding your bank account one $25 hour at a time. It’s time to get cracking!

Know someone else that needs this, too? Then, please share!!

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

Cybersecurity, CE, CRM, Warehouse Products; Disaster News and Insurance – Scaling Back in FL and CA

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

Cybersecurity, CE, CRM, Warehouse Products; Disaster News and Insurance – Scaling Back in FL and CA

By: Rob Chrisman

Tue, Oct 3 2023, 11:00 AM

How will you always know that this Commentary is not produced by some AI thingy? Because of mistakes like yesterday, leaving Illinois off the list of top pumpkin growing states as several folks pointed out (thank you). Here are pumpkin stats out the proverbial wazoo. What autumn would be complete without this map of when fall foliage is peaking across the nation? While we’re on maps, the U.S. Census Bureau released an interactive map illustrating 2020 Census data about homeownership by the age, race, and ethnicity of the householder. The map provides data at the national, state and county levels and data from the 2010 Census for comparison. The Census Bureau also released the brief Housing Characteristics: 2020, which provides an overview of homeownership, renters, vacant housing and other 2020 Census housing statistics previously released through the 2020 Census Demographic and Housing Characteristics File (DHC). (Today’s podcast can be found here and this week’s is sponsored by TRUE. TRUE creates accurate data that powers automation and optimizes every step of the lending lifecycle, helping lending organizations rapidly process loans, dramatically cut costs and risk, and radically improve the customer experience. Interview between Robbie and Rob Chrisman on chatter from the capital markets and why people should tune in to their weekly Mortgage Matters video show each Wednesday.)

Lender and Broker Software, Programs, and Services

Not many lenders know this, but you can buy down points with down payment assistance (DPA). DPA has evolved over the years, and there are 2,373 to choose from today according to Down Payment Resource’s Q2 HPI report. What’s more, consumer interest in DPA is savage, and lenders who offer it have a competitive edge. Just ask anyone who originated one of the 2,300 CalHFA programs that disappeared in just 11 days. DPA is one of the best tools lenders have in today’s market and for the foreseeable future. Want to know how many homebuyer assistance programs are offered in your markets or to learn more about how Down Payment Resource makes it easy to support DPA? Schedule a demo with the Down Payment Resource team today.

The MBA Annual Conference & Expo is just around the corner. Be sure to book time with the key players at Flagstar Bank if you’re headed to Philly for the big event. Right now, you can secure private meetings with their top execs in Corporate Mortgage Finance, Secondary Marketing, Specialized Mortgage Banking Solutions, Treasury Management, TPO Sales, and more. Don’t miss your chance to get a scoop on what’s ahead for this $119 billion asset bank, from product enhancements to tech rollouts and warehouse lending opportunities. Connect with your RM or AE to reserve a time today. If you’re not a partner yet, sign up here.

“Why should you integrate your mortgage and consumer loan origination systems? We’re sharing five key ways MeridianLink’s end-to-end digital LOS can help you break down silos, facilitate seamless communication, boost cross-sell potential, and enhance the overall borrower journey. Learn more now.”

Making meaningful, in-person connections is critical for success and at the heart of ICE Experience. Registration opened this week for ICE Experience 2024, taking place on March 18-20 at the Wynn Las Vegas, and the agenda is packed full of even more ways for mortgage professionals to grow their skillset and professional network. Plus, registration fees for this year’s conference are at a new low price of $995 when you register by January 31, 2024. If you are an ICE customer, now is the time to secure your seat to soak up the latest information, address your most pressing challenges, see new innovative solutions up-close and strengthen the relationships that are the foundation of your business. Click here to learn more.

OptiFunder announces the release of Greyhound, a highly configurable and automated system for Warehouse Lenders. OptiFunder has changed the game for IMBs by optimizing and automating the historically manual funding process. As we continue our mission to connect the primary and capital markets, we’re expanding our software offering to include a highly configurable, automated Warehouse Lending System, called Greyhound. Greyhound connects warehouse lenders with all major LOS systems, giving lenders the ability to easily onboard new clients, receive loans, and manage their entire portfolio. Leveraging OptiFunder’s LOS integrations means warehouse lenders are directly connected to over 70 percent of total industry loan volume. Greyhound offers real-time insights into pipeline management, loan/collateral tracking, operational reporting, automated LOS data import, investor shipping requests, purchase advise matching, document imaging, and more. IMBs and Warehouse Lenders should meet with OptiFunder at MBA Annual to discuss automating funding through loan sale to the capital market.

Are you well prepared to manage your servicing portfolio heading into 2024? As inflation continues to cool and the labor market starts to weaken, economists at Fannie Mae recently stated they expect a mild recession in the first part of 2024. Your servicing portfolio is a sound investment and can generate positive returns, but what happens when your portfolio starts to show signs of trouble, such as an increase in delinquencies? How will you ensure your distressed loans are making it through the proper pipeline and loss mitigation steps? It is more important than ever to ensure your servicing portfolio is ready to handle the uncertain economic future, and the team at Velocity Servicing, a LoanCare division, is ready to help! Backed by LoanCare Analytics, a proprietary data analytics platform with real-time access to portfolio data, Velocity Servicing helps lenders manage troubled loans with speed and accuracy. If you want to learn more about how Velocity Servicing can change your servicing game, email Matt Stadler or click here to schedule a time to meet with them at the MBA Annual in Philadelphia!

There is a celebration going on in Denver. It’s the 15th anniversary of a company that has been providing great software for 28 years. How is this possible? Usherpa was founded in 1995 at the second largest retail mortgage company in the country and rebranded in 2008 and is truly a firm that was “Born in a Branch; Forged in a Meltdown.” It has since grown into the largest privately held CRM company in the real estate and mortgage industries. Usherpa’s Smart CRM is the industry’s most sophisticated, cloud-based Customer Engagement Platform with the most powerful CRM and Marketing Automation systems in existence. It’s helped thousands of Loan Officers stay connected with partners and clients, helping hundreds of thousands of borrowers fulfill their dreams of homeownership. Usherpa users convert 46 percent more prospects, close 2X more deals and increase repeat business by 57 percent. They show you the studies! Win more business even in this market. Find out how here.

Autumn is not just about the vibrant leaves and cooling weather; it’s also the crucial period for renewing your NMLS license! As the seasons transition, ensure your professional credentials don’t fall behind. Diehl offers the top-tier Continuing Education (CE) you need! Our live, interactive webinars aren’t just about compliance; they’re engaging, insightful, and designed to meet NMLS requirements for the 2023 renewal season. We make mandatory learning enjoyable! With multiple dates to choose from, we have a class that works for you. Don’t wait until it’s too late! Sign up today before spaces run out!

“With over 35 years of experience in mortgage banking, Richey May knows the industry from every angle. Many of our team members are credentialed industry experts who dedicate much time to building up other industry experts. From this expertise, Richey May has created a wealth of services and products to help lenders stay ahead: audit and tax services, cybersecurity solutions designed to protect company assets and sensitive borrower information, intelligent automation tools for streamlined operations…you name it! Whether you’re leveraging our innovative platforms or having us work as your extended team for outsourced internal audit or accounting services, get ready to tackle challenges faster with some serious firepower on your side. Everything you need: contact our experts today!”

Disasters and Insurance

Many will say that it doesn’t matter whether or not you believe in climate change, manmade or natural. What matters is that investors in mortgages, servicers, and insurance companies do, as that pricing impacts people in those areas, and therefore clients and borrowers.

Progressive insurance is rebalancing its exposure in the state of Florida, and will not renew 47,000 DP-3 policies and 53,000 high-risk homeowner’s policies in the state. DP-3 policies tend to cover vacation homes and properties that are not a primary residence. That said, Progressive plans to transfer the policies to Loggerhead Insurance in a deal that will affect 100,000 policyholders. Multiple insurers are winding down parts of their business in Florida as an insurance crisis hits the state, which has high exposure to natural disasters and a ruthless roofing scam industry that has made it difficult for insurers to operate there. This has driven many homeowners to the state-backed insurer of last resort, Citizens Property Insurance Corp, which now has 1.3 million policies, up from 500,000 as of July 2020.

Florida isn’t alone. Several top insurance companies (like Farmers, State Farm and Allstate) have reduced their footprint in California over the last several months. State Farm and Allstate say they’re not writing any new homeowner insurance policies in California moving forward due to it being too expense. And just ask a homeowner in a low-lying area of Florida, Louisiana, or the Carolinas how it’s going.

Recall that in August the Biden administration urged a federal judge to reject a challenge by Florida and other states to an overhaul of the National Flood Insurance Program that has led to higher premiums for many property owners.

Nearly every part of the United States faces natural disasters, whether they be earthquakes, hurricanes, tornadoes, forest fires, drought, or volcanoes. A declaration by FEMA triggers lender and servicer policies and procedures.

On 9/19/2023, with Amendment No. 9 to DR-4720, FEMA updated the Incident Period End Date to 7/21/2023, for Vermont counties affected by severe storms, flooding, landslides, & mudslides from 7/7/2023 to 7/21/2023. See AmeriHome Mortgage Announcement 20230909-CL for inspection requirements.

PHH Correspondent posted information regarding Illinois DR-4728: New Disaster Declared, Mississippi DR-4727, and Vermont DR-4720. Go to the PHH company library to view the announcements and for all disaster declared counties, requirements, procedure.

In addition to the previously declared counties, a disaster declaration is being issued or modified pertaining to Hurricane Idalia landing causing wide-spread damage around Florida. Until FEMA has officially announced all Declared counties, PHH needs to cover this gap for areas determined to be of considerable concern to be declared a disaster by FEMA. Areas in Florida of concern not yet declared: Flood Zones only in both Hillsborough and Wakulla Counties. Go to the PHH company library to view the announcements and for all disaster declared counties, requirements, procedure.

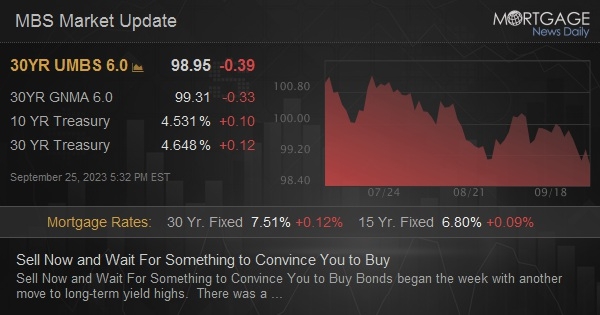

Capital Markets

As foreign and bank buying of fixed-income securities has declined, you’ll notice all talk of an inverted yield curve leading to a recession has vanished. (The 2-year is yielding 5.12, the 10-year is at 4.73 percent.) Remember when that was trendy? A recession will happen at some point, but probably not in the near future. As markets adjust to continuously high interest rates, it is creating a new reality for bond yields, with investors now wondering how high they can go. Over the last few months, the markets were wrong because they thought inflation would come down quickly and central banks would be very dovish. Everything will depend on how inflation lands over the medium to long run, but it’s fair to say that we have changed from the ultra-low-yield regime.

Rates continued their rise to open the quarter, which means that government shutdown fears weren’t the main driver of recent yield increases. That was also despite economic activity in the manufacturing sector contracting in September for the 11th consecutive month following a 28-month period of growth, per the latest Manufacturing ISM report. PMI did exceed both expectations and August’s reading. The report will be construed as an economy tracking more for a soft landing than a hard landing at this juncture. Total construction spending increased 0.5 percent month-over-month in August, as expected. On a year-over-year basis, total construction spending was up 7.4 percent.

There was increased talk over the last week as to whether a “soft landing” will be achieved as the elevated inflationary environment experienced over the last two years subsides. New home sales declined to a worse than expected 8.7 percent in August as the recent move in interest rates towards 8 percent moves potential buyers to the sidelines. Builders have been able to take advantage of low inventory this year, however the recent home builder survey from the NAHB reported buyer traffic at a seven-month low in September. This has increased the number of builders offering discounts to 32 percent, the highest share since December 2022.

Meanwhile consumer confidence fell for the second straight month as consumers weighed the effects of rising food and gas prices, higher interest rates, and generally persistent elevated inflation. It is possible that consumers may finally start to pull back on spending as labor market growth slows, interest rates remain higher for longer, savings dwindle, and student loan payments resume.

Today’s economic calendar gets under way with remarks from Atlanta Fed President Bostic, and will be followed by Redbook same store sales, JOLTS job openings for August, and the latest monetary policy decision from the RBA. We begin the day with Agency MBS prices worse .125-.250 and the 10-year yielding 4.73 after closing yesterday at 4.68 percent.

LO Job Openings

A team of warehouse experts seeks an operations leader, with 5 plus years of experience managing internal warehouse operating platforms. This is a ground floor opportunity to launch and build a national warehouse lending business. If interested in this COO role, please send your confidential resume to Anjelica Nixt and specify this opportunity.

In the Northwest and California, Banner Bank is searching for Mortgage Loan Officers looking to create lasting Realtor and builder relationships at a bank focused on the market today. Banner has opportunities for lenders looking for local decision making with FHA, VA, USDA, state bond and true Portfolio lending opportunities along with servicing retained Fannie and Freddie loans to assist in client retention. Additional highlighted products cover CRA lending with private label no payment down payment assistance to help assist all borrowers with the right opportunity. Banner is the right fit for an established team, or the individual looking to grow their business and take the next step in their career. Please send resumes to Aaron Miller.

Download our mobile app to get alerts for Rob Chrisman’s Commentary.

Share via Social Media:

All social media shares will include the image and link to this page.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?