Flexibility can be a real asset in a career. Maybe you’re young and figuring out your post-graduation path. Or you’re busy balancing the demands of running a home and caring for a family. Or you’re an athlete who needs plenty of time for training and recovery.

There are lots of flexible-schedule jobs out there, if you know where to look. Let’s check out some part-time jobs with flexible schedules.

What It Means for a Job to Have a Flexible Schedule

Whether you’re in college or caring for children or pursuing an unpaid passion, there are many reasons why someone would want some flexibility in their career.

But what does a flexible schedule mean exactly? According to the U.S. Department of Labor, a flexible schedule is one that allows people to work outside traditional 9 to 5 office hours. Aside from that, situations vary depending on the role and employer.

Workers may be able to choose the time they arrive at and depart work, for instance. With certain flexible work policies, employees still have to work a set number of hours per pay period or be available during a daily “core time.” So while the employee may not have to show up at 9am on the dot and leave at exactly 5pm, they may need to at least show up by 11am and stay until after 3pm. However, this type of shortened schedule could work for many people, including parents who are self-employed. 💡 Quick Tip: We love a good spreadsheet, but not everyone feels the same. An online budget planner can give you the same insight into your budgeting and spending at a glance, without the extra effort.

Tips for Finding a Flexible Part-time Job in 2023

Flexible part-time jobs can be logistical, analytical, creative, or involve a skilled trade. When it comes time to search for flexible-schedule jobs, keep in mind these tips.

• Stay focused. Job applicants who know what they’re looking for and what they can offer an employer can plan a more effective job search. If someone knows they have to have a flexible part-time schedule in order to accept a job, they can save a lot of time and energy by only applying for jobs that offer that. Trying to convince an employer to change their staffing plans is an uphill battle.

• Prepare to hear No. Know that it will take a while to find the right fit, and that rejection is a normal part of any job search. Psychologically preparing yourself can help you persevere until the right job comes along.

• Don’t be a square peg. If a flexible part-time schedule is what matters most, you may need to be flexible yourself in other areas. For example, accept that you may need to compromise on title, salary, or industry. Giving up the highest-paying job for one with a more relaxed schedule can be worth it.

• Go remote. Work-from-home jobs with flexible schedules can often be easier to find than on-site jobs that have flexible schedules. When reviewing online job boards, look for flexible schedule remote jobs.

Recommended: Does Net Worth Include Home Equity?

Why It Can Be Difficult to Find Part-time Jobs With Flexible Schedules

It can be difficult to find flexible-schedule part-time jobs because many jobs require being in a certain location at a certain time. For example, a hairstylist has to show up for work when they have appointments scheduled. A restaurant has to know they have enough servers on hand during operating hours. Even a corporate job where some work can be done remotely and independently can require being online during set times so that it’s easy to communicate with coworkers.

Check your score with SoFi Insights

Track your credit score for free. Sign up and get $10.*

Great Part-Time Jobs With Flexible Schedules

Perhaps someone wants to take on a second job to help them pay down their debt or save for a dream vacation. Whatever the reason, it’s easy to see the appeal of a part-time job with a flexible schedule.

While there are countless part-time jobs on the market that can suit a variety of workers’ desired schedules, these are some of the best flexible schedule jobs for Gen Zers and Millennials. And if you’re in college, don’t miss our list of the best on-campus jobs.

1. Landscaper and Groundskeeper

Average hourly wage: $17.39

Job description: Landscapers and groundskeepers typically set their own schedules and plan which days they’ll tend to a client’s yard, but they don’t have to tell them exactly what hour they’ll show up to do their work.

Requirements: In some areas a license may be required to use pesticides and fertilizers.

Schedule flexibility: 4

Duties:

• Mowing lawns

• Removing weeds

• Planting and maintaining flowers, bushes, and trees

2. Recreation and Fitness Worker

Average hourly wage: $22

Job description: Running a fitness or recreation class can be fun and rewarding work that is often performed on a part-time basis. Many instructors can choose when they host their classes (like when their young child is in school), but they do have to stick to those times.

Requirements: Licensing or background checks may be required.

Schedule flexibility: 4

Duties:

• Plan programming

• Run classes

• Clean up post-class

3. Freelance Software Developer

Average hourly wage: $37

Job description: Many businesses hire freelance software developers to create computer programs and applications for business or consumer use. Some meetings during business hours may be required.

Requirements: Knowledge of select programming languages.

Schedule flexibility: 4

Duties:

• Write code

• Test code

• Meet with project stakeholders

4. Virtual Assistant

Average hourly wage: $34

Job description: Plenty of professionals can’t afford or don’t need a full-time assistant. Instead, they hire virtual assistants who can tackle administrative work for a few hours a week. Virtual assistance can be a rewarding job for introverts who are conscientious and organized.

Requirements: Office skills

Schedule flexibility: 4

Duties:

• Scheduling meetings

• Managing clients’ inbox

• Helping with administrative work

5. Freelance Copywriter

Average hourly wage: $28

Job description: A writer can work with many different brands as a freelance copywriter and can choose when they want to take on new projects and what hours of the week they work on them. Working as a freelance copywriter is also a great side hustle.

Requirements: Bachelor’s degree and industry experience

Schedule flexibility: 5

Duties:

• Research

• Writing copy

• Editing copy

6. Freelance Web Designer

Average hourly wage: $35

Job description: Freelance web designers work independently designing websites for a variety of clients, instead of a full-time job. Work-from-home web design can be a well-paying and fulfilling job for antisocial people.

Requirements: Knowledge of design programs, and HTML and CSS programing languages.

Schedule flexibility: 3

Duties:

• Design web pages and sites

• Code designs

• Present to clients and incorporate feedback

7. Freelance Editor

Average hourly wage: $31

Job description: Similar to copywriters, editors can work freelance for multiple clients.

Requirements: Bachelor’s degree and industry experience

Schedule flexibility: 4

Duties:

• Nurturing writers

• Editing copy

• Publishing content

8. Business Consultant

Average hourly wage: $37

Job description: A business consultant can offer services to multiple businesses who need support as a whole or who are looking to improve a certain area of their business, such as their marketing efforts, operations, or HR.

Requirements: Bachelor’s degree, master’s degree (more advantageous), or a certification from a business consultant association.

Schedule flexibility: 3

Duties:

• Assess potential areas of improvement

• Create improvement plans

• Find ways to cut costs

💡 Quick Tip: Income, expenses, and life circumstances can change. Consider reviewing your budget a few times a year and making any adjustments if needed.

The Takeaway

There are plenty of great flexible-schedule jobs that millennials and Gen Zers can pursue to give them the time they need to attend school, start a business, or take care of young children. Some remote freelance roles can be entirely flexible — such as web designers, writers and editors — while other jobs require your presence during certain core hours.

Choose whether you prefer a more physically demanding job — such as landscaper or fitness worker — or an office job that requires a laptop (like virtual assistant). It may take time to find the right position, so be patient. It’s also a good idea to keep an eye on how your money comes and goes to ensure you’re sticking to your savings goals.

Take control of your finances with the SoFi Insights money tracker app. Connect all of your accounts in one convenient dashboard. From there, you can see your various balances, spending breakdowns, and credit score. Plus you can easily set up budgets and discover valuable financial insights — all at no cost.

SoFi helps you stay on top of your finances.

FAQ

What part-time job has the most flexible hours?

There is no single part-time job that has the most flexible hours. That said, jobs where work can be done independently and remotely usually have the most flexibility. Jobs like working as a freelance writer or graphic designer are good examples of jobs someone can usually do during times that work well for them.

What job gives you the most free time?

Flexible-schedule work-from-home jobs can give workers the most free time because they don’t have to worry about a commute. It’s also usually easier to control your work schedule when you work from home. As a bonus, you can use your breaks to be productive — by tackling household chores or working out — or enjoy down time.

What jobs can I make my own hours?

Some jobs with flexible schedules allow workers to set their own hours. The key is to look for a job where the hours someone works doesn’t matter as much as the type of work they produce.

Photo credit: iStock/Eva-Katalin

SoFi’s Insights tool offers users the ability to connect both in-house accounts and external accounts using Plaid, Inc’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a Vantage Score® based on TransUnion™ (the “Processing Agent”) data.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

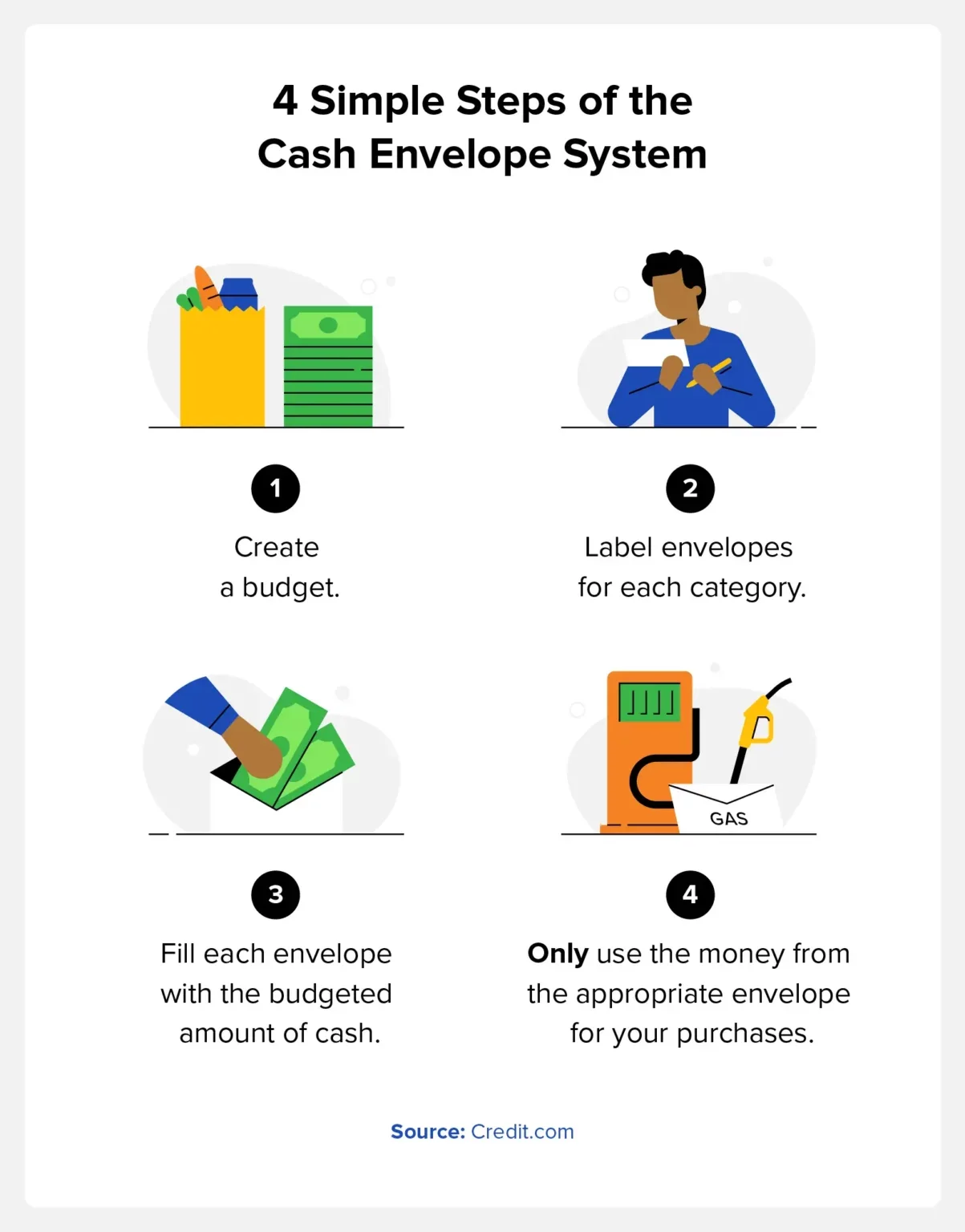

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

This article is part of a series put together by the Total Mortgage marketing team that provides loan officers and other sales professionals with a crash course in marketing and self-promotion. To read other articles in this series, click here.

This article is designed to teach loan officers and other sales professionals how to properly maintain and boost their social media presence. It will hit all the key points such as connecting, managing multiple profiles, engaging with influencers, and what to post.

Want to jump ahead?

LinkedIn

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Facebook

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

Twitter

Connecting & Following

Managing Multiple Profiles

Properly Engaging with Influencer

How and What to Post

Google +

Connecting & following

Managing Multiple Profiles

Properly Engaging with Influencers

How and What to Post

LinkedIn

How to Gain/Find Connections

When you first started setting up your LinkedIn account, you were prompted to import your contacts from your email address book. If you clicked yes, you probably already have a few dozen connections. However, once your profile is completed, you will need to search for those connections you didn’t have on your contact list, like loan officers you met at a conference or realtors you haven’t had a chance to work with yet. There are many different ways to go about finding and linking with connections on LinkedIn.

The first way is arguably the easiest way: using the Search box. It can be found on the top of any tab of the LinkedIn interface. There are also many “Advanced Search” options available if you click the “Advanced” text link right next to the search button.

You could also find connections from clicking onto your Profile, scrolling down to your experience and hovering over your business place icon and then clicking onto the icon or your company title, highlighted by the red arrow.

After clicking on your company’s icon, scroll down until you see the “How You’re Connected” on the right side of the screen. Click “See all.”

Now you have the opportunity to see coworkers and contacts who you’re not connected to.

Managing Multiple Profiles

LinkedIn is generally a place where you focus on one personal profile. However, if you run your own business, you will want to create a company page for it. If you need help creating a company page, check out my Social Media Basics post. If you only manage one page, then this section may not be that useful.

If you are on your profile page and you want to switch to your company page, you simply click on the small icon on the top right hand corner of your screen (where the arrow is shown) then on “Company Page.”

This will lead you to this screen.

You’ll now be able manage, change, analyze, and update your company page. If you want to switch back to your profile page, just click on the home tab or profile tab.

Engaging with Influencers

Connecting with influencers—that is, the people who are active, established, and popular in your industry—is a great way to widen your reach. Of course, engaging with influencers on LinkedIn is not something you should do blindly. It takes strategy and time to do correctly.

Do Not:

Do not connect with an influencer without ever interacting with them

Do not like, comment, or share everything they post

Do not post more than 3 times per day

Do:

Do connect if you had previous relations

Do connect if you are connected on other networks

Do connect if you have exchanged emails or contact info

How and What to Post on LinkedIn

Posting on LinkedIn is very straight forward. LinkedIn allows you to share updates, publish a post, upload a photo, share in groups, and post job opportunities. You can access these options in the home tab, except for sharing in groups and posting job opportunities.

Sharing in a Group

Sharing in a group could be a great way to get your content to a broader audience. Joining groups on LinkedIn is very easy. First, click on the “Interests” tab and then click on “Groups” If you are already a member of a group it will appear under the “My Groups” section. If you aren’t a member of any groups, just click on the “Discover” tab and LinkedIn will provide recommendations for groups to join. You have the option to select “not interested,” “ask to join,” or you can ignore and continue to scroll.

Once you ask to join a group, your request must get approved by an admin, which can take a day or two depending on how busy they are. After you’re accepted, you can view what the others in the group are posting. To get started, click on “Start a conversation with your group.” The box will expand and you get the options listed below. At this screen, type in your title and a brief description with a link to the real content. Follow the same process for posting a job opportunity in a group.

If you run a LinkedIn business page, then you have the option of posting a job ad through the “Business Services” tab. Once you hover over “Business Services,” click on “Post a Job” to get to this screen.

After you fill out the appropriate information and click “Start job post,” LinkedIn will walk you through a series of prompts, where you will fill out information like job function, company industry, and job description. Once that’s done, review everything and click submit.

What to Post:

Career status updates

News and events

Articles shared by your connections

Your own articles

What not to Post:

Quotes

Updates trying to sell services/items

Material you deem not appropriate for the workplace

Facebook:

How to Gain Followers:

With more than 1.65 billion monthly active users, Facebook has the potential to connect you to people across the globe. If you’re using Facebook for business purposes, you need to understand how to properly navigate it to connect with others.

There are multiple strategies to take. For example, you can create a personal account, a business page, or both. If you’re in an industry where you need to keep things professional (like, for instance, the mortgage and financial industry), then I recommend creating a business page so you can separate your professional life from your personal life. You have to mindful of whom you invite to like your page, but we’ll touch on that topic a little later.

If you’re completely new to Facebook, prepare to spend some time connecting with people you know. You can manually add friends by clicking in the search box at the top of the screen and typing the name of the person you are trying to find. Eventually Facebook will tailor a carousel of “People You May Know,” which will allow you to click “Add Friend.” Thankfully, Facebook has implemented a few tricks to make it easier to add friends in bulk.

Go to the Friends Request page then to the “Add Personal Contacts,” enter your email and click find friends.

After you enter your email it will take you through to a similar screen. Click “Agree,” then follow the on-screen instructions.

On the Go

You can also import contacts from your mobile device.

Tap

Hit “Find Friends” in the Apps section

Tap “Contacts,” then follow the on-screen instructions

Connecting to Others Via Your Business Page

Click on the triangle in the top right corner of your home page.

Click on the drop down menu and select your business page.

Click on the […] on your cover photo and then click on “Invite Friends.”

Search all friends: click the invite box next to your friends’ names to invite them to like your page—or type their names in the search box.

Managing Multiple Profiles

Facebook does a fantastic job of making it easy to manage as many pages as you want. Their interface organizes your pages so you can easily switch through and manage every single of one of them. Every time you create a new page, Facebook allows you to add that page into your “Favorites” section. I highly recommend doing this, because it keeps all of your pages in easy reach, which you can see in the image below.

You can also switch between pages by clicking the drop-down triangle on the upper right corner of your home page. In that menu, you’ll find a list of three of your pages. Shown below:

If you manage more than 3 pages—like we do here at Total Mortgage—you can just click on “See More…” and it will give you a list of all the Facebook pages that you manage. To switch back to your personal page, you simply just need to hit the “Home” button and it will take you back to your feed.

Properly Engaging with Influencers

Recently, Facebook has changed how you interact with other people or businesses when you’re on your business page. Once, you were able to be on your business profile, click on “Home” and interact with people and businesses that follow your business page. However, that is essentially nonexistent today. Now you really need to be creative if you want to engage with influencers in your community.

To Like a Different Page as Your Business Profile

Go to the page you want to like and click on the […]

Click “Like As Your Page.” Then this screen will pop up and you choose the business account that you want your like to come from. Click “Save.”

Tagging other influencers in your Facebook posts is simple if you know the name of their business page. A lot of influencers have both personal and professional profiles, however, so make sure you know which one you’d like to connect with.

Unfortunately, you can’t tag a personal account from your business profile. If you want to tag a professional account from your business page, you craft your post, then add the appropriate tag at the end. You always want to convey that you got the content from a source and you are using it credibly.

In the picture below, you see that I have crafted a draft of my message and tagged the source I got it from with the tag “via @[name].” Instead of via you could use from, by, thanks to, etc. When possible, try to use a link shortener such as Buffer or Hootsuite to keep things looking tidy.

Once you get the proper etiquette down for interacting with influencers, now it’s time to engage with them. Like I mentioned above, you can like other pages as your page. You are able to do the same for posts. You do that by going to the page you want to like something on and scrolling to the post that you want to interact with. Before you like the post or comment, make sure you switch from your profile to your business profile. You do this by:

1. Clicking on the downwards arrow next to your small Facebook default icon

2. Click on the account you want to like and comment as.

You are now liking and commenting as your business account. This is the best way you can engage with your influencers. There are 3 important things you must always remember to do and don’t do before you start engaging with influencers.

Do Not:

Do not like/comment on everything that they post

Do not ask for a favor like sharing a post right away

Do not reach out to them right away

Do:

Gradually interact with them by liking their page and commenting on a few posts/pictures 1-3 times a week

Share some of their posts 1-2 times a week

Always remember to thank them for sharing information that you find important

Here’s where you use your gut. Once you think you’ve earned yourself a spot on the influencer’s radar, the next step is to reach out personally. This can be done in an open forum through commenting, or it can be done through private message. The eventual goal is to take the conversation “offline” through either phone or email so you can begin building an even more personal relationship.

How and What to Post on Facebook

Posting and sharing on Facebook is very easy. If you have a personal Facebook, you already know the drill. If this is your first time on Facebook or you don’t know how to post to your business page, then keep reading.

Posting on Your Personal Page

Bring your mouse to the top tab and click on your name

Click on the box where it says:

3. Click on the kind of post you want to craft: status, photo/video, or life event. Finish typing it with the appropriate tags (if needed) and click post.

Posting on your Business Page

Make your way over to your business page

Click on the box where it says “status, photo/video, or life event” and create the post you want to send out

When you are finished, click “Publish”

What to Post on Facebook

There are two types of content that you should post on Facebook. The difference depends on what account you plan to post with. For both profiles, you should post content that really resonates with your audience and makes people see you as a credible source (i.e. if you’re a loan officer, try content based around changes in the industry or tips on how to make the mortgage process easier).

Content like this positions you as an authority and encourages your audience to consider using your services if they are shopping for a home or refinancing. Every once in a while, it’s okay to throw in a shameless plug, whether you’re asking for referrals or encouraging people to use your services. Your personal page can have all the other updates—photos of your family, your dog, things you’re passionate about, etc. It is ok to post some business topics on your personal page, but make sure to do so sparingly. Your personal page is meant for personal things.

Twitter:

How to Gain Followers

Twitter is a great place to gain followers based on things that you find interesting. You can use the search box to find other professionals and people in your industry by looking for relevant hashtags, like #realestate.

Top Tips for Gaining Followers

Try finding your connections from other places like Facebook and LinkedIn on Twitter

Follow users who follow your followers

Follow the accounts recommended by Twitter

Join a Twitter chat

Managing Multiple Profiles

Unfortunately, Twitter doesn’t have an interface within itself to switch profiles easily—unless you are on your mobile device or want to use multiple web browsers. However, there are certain tricks, tips and hacks you can use to make managing multiple profiles easier.

Toggling Profiles in the Twitter App for iOS

From the “Me“ tab, tap the people icon

Tap “More options.”

From here you can “Create new account” or “Add an existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the people icon.

Toggling Profiles in the Twitter App for Android:

Tap the overflow icon

Tap “Accounts.”

From here you can “Create new account” or “Add existing account.”

Once you’ve added your additional account, you can toggle between accounts by tapping the overflow icon, then tapping “Accounts.”

If you’re uninterested in downloading the Twitter app for your mobile device, there are other options. If you manage more than one profile you can easily manage multiple accounts if you use a tool like Tweetdeck, Buffer, or Hootsuite. All of these applications have free versions, so you don’t have to worry about spending money.

These apps make it easy to manage countless amounts of accounts. My personal favorite of the three is Buffer, because the interface is very easy to use and it provides multiple tabs to check out how your account is doing in terms of analytics. It also has a built-in link shortener that automatically shrinks your links when you are adding them to a post. Shown below is a screenshot of my Buffer interface.

Engaging with Influencers

Engaging with influencers on Twitter is a great way to kick-start your influencer marketing strategy. This is where Twitter search comes in handy; you can use it to find the people who tweet regularly in your industry regularly. If you want to stay organized, I recommend creating a spreadsheet that has a list of your influencers, their names, follower count, and what stage of your relationship you’re in. Once you’ve found a handful of them, it’s time to start engaging.

Do not:

Tweet, retweet, or like everything that they tweet

Try to directly reach out to them—it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally tweet, retweet, or like their posts to get on their radar

Appreciate their content by tweeting it out to your audience (and making sure your attribute the author)

Once you established a relationship, make it easy for them to tweet about your service by crafting an email with a few sample tweets that they could send out about your services. Make sure you convey the message that you are willing to reciprocate the favor

How and What to Post:

Posting on Twitter is very simple. If you are on the web browser version of Twitter the tweet box is one of the first things that you see. You can find it by looking for the “What’s happening?” text.

To compose a tweet you just click on this box and type the content you want to share.

Posting a Tweet on a Mobile Device

Tap the compose Tweet icon accessible from your Home timeline, the Notifications tab, or your profile (usually located on the upper right hand of your screen.)

Start typing where it says “What’s happening?”

If you’d like to Tweet an image, tap the camera icon

Tap “Tweet” to post.

What to Post

Just like any other platform, choosing what to post comes down to a few key factors.

Who your audience is

What kind of message are you trying to portray

What kind of content will resonate with that audience

Make sure you don’t forget to utilize the power of hashtags on Twitter. To see how a hashtag is performing simply search the hashtag in the search box before you post the tweet or check it out on Tagboard.

You want to have the appropriate amount of hashtags to text ratio. Most marketers recommend using no more than 3 hashtags per tweet. However, if your tweet only contains 3 words, don’t hashtag them all. Finding the perfect mix of creativity and content is surely a challenge but once you find your niche you will be good to go.

Google Plus

Google+ is one of the most underrated social media platforms, but it could be a great asset to your strategy if used properly.

How to Gain Followers

Make Your Profile Look Good

I know, it sounds obvious, but a lot of people just use the default graphics that Google supplies. Make sure your profile looks good and is customized so you reach people in your niche.

Follow other Google Plus People

Just like other social platforms, you’ll need to work for your followers. You do this by following as many people as possible. There are multiple ways of doing this. If you are looking for people to connect with , search for something relevant to your industry like, for example, “Real Estate.” A list like below will pop up and you will be able to decide who what you want to follow, whether it be collections, communities, people & pages, or if you just want to view posts.

You can also follow people manually:

Click the People Icon on the left side of the screen

You should see a “Find People” option. Click on that

Go through the list of people and see who you want to add

You can add them to just your follower base or you can add them to relevant circles, such as “Realtors”

Join Communities

If you’re looking for the fast track way of getting your name in front of dozens, even hundreds of people at once, then you’re looking for communities. When you join a community, you are part of a much larger group of people who are interested in a certain topic. This is how you engage the right kind of followers.

Utilize Hashtags

With Google Plus know you can search content by words, phrases, and hashtags. Even though hashtags are more popular on Twitter, they work the same way on Google+.

Let’s say you hashtag a word or phrase in your post, i.e. #RealEstate. Thanks to that hashtag, your post enters a stream with hundreds of other posts with that same hashtag. Meaning, anyone watching that stream or looking for specific information centered on that topic will easily find your post.

Add a Google+ Badge to Your Website

If you have your own website, it’s a sin in 2016 to not have visible social widgets. These are clickable icons that take you right to your social media pages. They take the hassle out of finding your social pages, making it easier to gain followers.

Managing Multiple Profiles

Managing multiple profiles on Google+ is very simple if you add all your accounts to one email address. Once you associate all your different profiles to that one email address it becomes very easy to switch back and forth between the different profiles from the Google+ interface. Don’t forget—you can always use a social media management tool like Buffer to switch profiles simultaneously.

Switching Profiles:

Click the icon on the upper right hand corner (Note: Your icon will be different from ours)

Once you click on that icon it will release a drop down menu of all the other profiles you have connected to your account

Now you are free to switch through whichever profile you deem necessary

Properly Engaging with Influencers

Engaging with influencers is a lot like engaging with influencers on any other platform—you need a strategy and you need to find the right influencers.

Do not:

Plus one (+1) everything they share

Try to directly reach out to them–it comes off creepy

Follow them on other networks without establishing a relationship with them

Do:

Occasionally +1, comment, and share their posts

Appreciate their content by sharing it in your communities

Share some of their posts 1-2 times a week

Thank them for sharing information that you find important

How and What to Post

Posting on Google+ seems a lot more complicated than it really is. Just keep in mind that you can post publicly, in a community, or in a group. To post you simply go to the page, community or group you want to post to.

Click on the pencil icon on the bottom right hand corner

Which will bring you to this screen

Here you type in the text of the message you want to draft in the ‘What’s new with you?’ section. If you are adding a link, click on the. If you want to add a picture (recommended) click on the camera icon. You can also add your location by clicking on the location pin.

What to Post

Just like any other network, you need to find your niche before posting blindly. Finding content that really resonates with your audience is half the battle. Like I said previously, try testing a few types of content to see what works best.

Don’t be afraid to use content with a lot of pictures like infographics. The more pictures the better. A very good post is a combination of clever content, great pictures and captive CTA’s (call to actions.) Once you find this balance roll with it and optimize your Google+ account to its full potential.

Thinking About Your Next Steps?

All of these social media platforms are great for connecting and getting your content out there. Each platform is a little different from the next, so don’t try to implement the same strategy throughout all of them. Finding your groove might take some time, but keep working towards it and tweaking your strategy to see what gives you the best results. Once you hit that sweet spot, roll with it.

You can learn more about what the Total Mortgage marketing team does for our loan officers by checking out other articles in this series, or by visiting our career portal.

Carter Wessman

Carter Wessman is originally from the charming town of Norfolk, Massachusetts. When he isn’t busy writing about mortgage related topics, you can find him playing table tennis, or jamming on his bass guitar.

According to reports from the second quarter of 2022, the total of all household debt in the United States is a whopping $16.15 trillion. Mortgages make up the bulk of that debt, with student loan, auto loan and credit card debt trailing behind.

On average, adults in the United States carry debt loads ranging between $20,800 and $146,200. If you’re in debt and looking for a way to pay it off, making a plan is a critical step. Find out more about how to get out of debt below.

1. Collect All Your Paperwork in One Place

Before you can get out of debt, you need to know how much debt you actually have. You should also know who you owe and what the terms are, as this can help you prioritize debt payments to pay them off faster.

Start by collecting all your debt paperwork in one place and creating a master list of everything you owe. You can do this in a spreadsheet or with a pen and paper. Information to gather includes:

Statements for all your debts. One way to do this is to spend a month saving all your financial mail and email so you have a comprehensive picture of your debt.

Regular bills that aren’t debts. Your cell phone and utility bills, as well as your rent, should all be included when you gather this financial information. Information about income. Look at paycheck stubs or your bank accounts so you know what, on average, you can expect in income each month.

Your credit reports. Get your free credit reports at AnnualCreditReport.com to ensure you know about all the debt you owe.

Tip: Sign up for ExtraCredit to see your credit reports and 28 FICO® scores in one place.

2. Create a Budget and Determine What You Can Pay Every Month

Using the information you gathered in the above step, create a monthly budget. Make sure you cover all your bills and minimum debt payments. When possible, include an amount that can go toward building your savings. Allocate funds for essentials, such as groceries and gas.

Once you cover all the needs for the month, figure out how much money you have left. How much of that can you put toward extra debt payments so you can start getting ahead on debt?

3. Manage Your Debts in Collections

If you see that you have any debts in collections when you pull your credit reports, make sure you have a plan for taking care of them. Collection accounts have a serious negative impact on your credit score. Creditors may also sue you and try to collect on these accounts via wage garnishments or bank levies if you don’t take action to manage collections. That can throw a huge wrench into your plan for getting out of debt.

Tip: If you don’t enjoy manual calculations, check out Tally. You can use Tally to total up your expenses, pay down credit card bills, and generally figure out where you stand.

4. Consider Your Options

There are two main approaches to paying off debt as quickly as possible: the snowball method and the avalanche method.

The snowball method involves paying off accounts with the lowest balances first. You take any extra money you have—even if it’s just $50—and add it to your regular minimum monthly payment on that small balance. When that balance is paid off, you take the extra $50 plus the minimum payment and add it to the next biggest balance. You keep doing this as you work your way up to larger balances, paying your debt off faster and faster.

With the avalanche method, you tackle accounts according to interest rates. You start by paying off accounts with the highest interest rates first. The thought behind this method is that you save money in the long run by tackling high-interest debt first.

5. Try to Reduce Your Interest Rates

Interest refers to how much your debt costs. If you have a lower interest rate, your debt costs less and you can pay it off faster. Here are some ways you can try to reduce interest rates on your debts:

Ask for a lower interest rate. If you’re a credit card account holder in good standing and your credit history and score has improved since you got the card, you may be able to get a better rate. Call customer service for your card and let them know you are looking for a better deal. They may agree to lower the rate to keep you as a cardholder.

Look into debt consolidation or refinancing. A debt consolidation loan provides funds you can use to pay off higher-interest debts. Refinancing occurs when you get a new loan for a home or car. If you had lackluster credit when you got your auto loan, for example, you may be able to refinance it for a lower rate if your credit has improved.

Get a balance transfer credit card. You may be able to transfer balances from a credit card with a high interest rate to one that has an introductory low APR offer. This may allow you to pay off the debt over the course of 12 to 22 months without incurring any more interest expense.

Upgrade Triple Cash Rewards Visa®

$200 bonus after opening a Rewards Checking Plus account and making 3 debit card transactions*

Unlimited cash back on payments: 3% on Home, Auto, and Health categories and 1% on everything else after you make payments on your purchases

No annual fee

Combine the flexibility of a credit card with the predictability of a personal loan

No touch payments with contactless technology built in

See if you qualify in minutes without hurting your credit score

Great for large purchases with predictable payments you can budget for

Mobile app to access your account anytime, anywhere

Enjoy peace of mind with $0 Fraud liability

*To qualify for the welcome bonus, you must open and fund a new Rewards Checking Plus account through Upgrade and make 3 qualifying debit card transactions from your Rewards Checking Plus account within 60 days of the date the Rewards Checking Plus account is opened. If you have previously opened a checking account through Upgrade or do not open a Rewards Checking Plus account as part of this application process, you are not eligible for this welcome bonus offer. Your Upgrade Card and Rewards Checking Plus account must be open and in good standing to receive a bonus. To qualify, debit card transactions must have settled and exclude ATM transactions. Please refer to the applicable Upgrade VISA® Debit Card Agreement and Disclosures for more information. Welcome bonus offers cannot be combined, substituted, or applied retroactively. The bonus will be applied to your Rewards Checking Plus account as a one-time payout credit within 60 days after meeting the conditions.

Do Your Best to Pay More Than the Minimum

Only paying the minimum on high-interest debt, such as credit card debt, doesn’t get you out of debt fast. It can take years—dozens of them—to pay off credit card balances if you’re only making minimum payments.

Instead, put more than the minimum on your debt whenever possible. You may also want to put any additional funds you receive—such as a tax refund—on your debt to help with this process.

Consider More Options for Getting Out of Debt

Creating a budget, managing your money wisely, and making extra payments toward your debt all help you get out of debt. Here are some other ways you can deal with debt:

Increase your income while cutting unnecessary spending. Join the gig economy with a side job to earn extra money, or sell things you don’t need via online marketplaces.

Undergo credit education and counseling. These services can help you make the most of your monthly budget.

Engage in debt settlement. You may be able to negotiate with creditors, especially for accounts in collections, to settle debts for less than you owe. Just make sure you understand any effects on your credit.

Enter a debt management plan. During such a plan, you make a single payment to a trustee. They use those funds to pay your debts, hopefully in a way that gets you out of debt faster. Declare bankruptcy. If you find you’re unable to pay your debts, much less make extra payments, you may need another option. Chapter 7 and Chapter 13 bankruptcy are potential considerations.

How to Avoid Getting into Debt

Paying off debt doesn’t have to be impossible, but it can be challenging. For many people, it requires altering years’ worth of financial habits. If you’re not already in debt, it may be easier to stay out of it. Create a budget and stick to it, spend wisely and avoid using credit cards for things you don’t need or can’t afford to buy with cash.

Here’s how this social worker has paid off $28,000 of student loan debt in 15 months.

Today, I have a great debt payoff progress story to share from Taylor. Taylor is a social worker who is working on paying off $277,000 of debt and retiring early. She shares tips on how she is cutting her expenses, the ways they’ve increased their income through various side hustles, house hacking advice, and how she qualified for an $88,000 student loan award.Enjoy!

Now, don’t let the title deceive you into thinking we are debt free; we most certainly are not.

As of this writing, we still have $251,195.39 of debt (all student loans).

This is our story about the debt payoff strategies we used in paying off $28,026.02 of debt and our goals for the future!

Who are we?

My name is Taylor, and I am a 29-year-old medical social worker who finished grad school in 2018. I am also a part-time social media coordinator and with both jobs combined, I make $96,000 (gross).

I live with my husband, Bret, who I have been with for 11 years and married for 3. He is a full-time student and has been in grad school since September 2020 (he has about 2 more years left). We love to travel, try new restaurants, hang out with our friends and family, and just have a good time.

I also have a blog at Social Work to Wealth.

Related articles:

How did we get here?

First, I need to give you some background before we get into the nitty gritty of our debt numbers and payoff strategies.

2012: We met when both of us were in college. I was 18 and Bret was 22. Soon after we met, Bret took a few years off from school while I finished my bachelor’s. I relied entirely on student loans, and don’t remember applying to any scholarships. When Bret returned to school to finish his bachelor’s, he did receive some scholarships and worked a summer job to pay forhousing but still needed to rely on student loans to pay the bulk of his tuition.

I will speak for myself when I say I didn’t take the time to calculate how much loan money I actually needed and blindly accepted the total amount. Looking back, maybe I would have needed it all or maybe not, but I wish I would have at least done the exercise.

We have always been open with talking about our debt and money in general, but I remember us both expressing the thought that we would probably always have our student loans. We would just live our life, pay our minimum payments, and that would be that. There was never any talk about debt payoff strategies, or any money management strategies, really.

We went through many life transitions. Living apart for two years while I went to grad school, him returning to school to finish his bachelor’s, various jobs, and a post-bach program.

2019: Bret was finishing up his post-bach program and got accepted into grad school. We were newly engaged and began planning and saving for our wedding scheduled for July 11th, 2020. Such exciting stuff!

March 2020: We got the news our wedding venue was closing for the foreseeable future due to the COVID-19 pandemic, and we decide to cancel our wedding. We switched gears and used the money we saved for a down payment on a new home. Then, we had a small intimate wedding featuring a hot-air balloon with 18 of our closest family members! We personally saved a ton and also had tremendous help from our family.

September 2020: I start a new job and Bret starts grad school. We are newlyweds and settling into our new home in a new city.

I wish I could talk more about 2020 because it was a HUGE year for us with buying a home, moving, getting married, Bret starting grad school and me starting a new job, but that’s a conversation for another day!

Our wedding

From frugal to spenders

When we were saving for our wedding, we were very frugal. Any extra money we had, we put toward our wedding savings (which again, ended up being used for the down payment on our house and a smaller wedding ceremony).

We went from frugal to swiping our cards left and right to prepare for our wedding and furnish our house. It was sooo nice to finally be able to spend the money we had been saving for so long! But this continued into 2020… and 2021…

We were mostly spending on eating out and experiences. We do like to buy “things” but we definitely value food and experiences a lot more. We even decided to put a trip to Hawaii on our credit card costing us around $5,000, along with other expenses, because why not? We deserved it!

We didn’t have much of a budget, our bills were getting paid, but the credit card bill kept increasing. Since I was the only one bringing in income, we took out some student loans to help with a portion of our living expenses. And the credit card bill continued to increase.

The “wake-up call”

The “wake-up call” is such a theme throughout many debt payoff stories. So, here’s mine.

I went to breakfast with two friends in December 2021, and one of them brought up high-yield savings accounts (HYSA). I had never heard of this type of account before and was shocked to learn that these savings accounts had a way better interest rate than a regular savings account.

How was I just hearing about this at 28 years old? My mind was blown!

I thought, what else don’t I know? So of course, that led me to deep dive into the world of personal finance. I consumed any book, video, blog, or podcast I could get my hands on. I read stories after stories of people paying off thousands of dollars’ worth of debt, leveraging credit card points for free travel, investing, and so much more!

It was so motivating. I was hooked! (And still am.)

Bret was open and willing for me to share with him what I was learning. We started realizing that for the last year and a half, we hadn’t been telling ourselves “No”. We had just been buying whatever we wanted, and we had the credit card bill and no savings to show for it.

We learned that we could pay off all our debt and it didn’t have to stay with us forever. We learned there was a way to use a credit card responsibly (we thought we were). We learned that we could even retire early. That one sounded real nice! We dreamed of having more time doing our hobbies, traveling and being with our friends and family. And if we ever had kids, we dreamed of being able to work part-time so we could be home more with them and available for school activities.

Knowing this, we started reining in our spending, trying to just be more “mindful”, but no major change was made.

We take on more debt

April 2022: People in our neighborhood were getting new fences. We started thinking, “Hey, we need a new fence, too…” In some areas it was broken, it hadn’t been stained so was rotting, and was 15 years old. We were also going to get an updated appraisal to see if we could get our primary mortgage insurance (PMI) removed after just two years of owning our home and thought a new fence might help.

A coworker told me she was using a home equity loan to buy a fence and to do some other home renovations. We investigated options and ended up opening a $20,000 home equity line of credit (HELOC) instead with about a 4% interest rate. We buy our fence which ends up being about ~10,000 and we were set on it…

The second “wake-up call”

When it was all said and done, we loved our fence. We still love our fence, it’s beautiful! (And it better be at that price!) We stained it and we believe it will last us for many years.

But we start talking again about our debt and how we probably didn’t need this fence right now. We know we didn’t need this fence right now. Our PMI was removed, and it could have maybe happened even without the fence. Who knows.

We began thinking we need to make some serious changes in the way we manage our money. We need to do more than just be “mindful” about our spending. We make a real plan. We plan to make an actual budget, stop taking on unnecessary debt, and take a break from using our credit cards for the foreseeable future.

May 2022: Beginning of our debt payoff journey

Since we were serious about our new money management changes, I documented how much debt we had so we could track our progress.

$277,721.41

Here was the breakdown:

$260,390.25 in student loans, Bret & I’s combined – various interest rates

$10,676.24 HELOC – 4% interest rate

$5,430.76 is from credit card spending – 4% interest rate*

$449 for furniture – 0% interest rate

$775.16 for Peloton bike – 0% interest rate

*We moved our credit card debt to our HELOC since our credit card was around a 25% interest rate.

July 2023: Current debt numbers

Our current debt balance is $251,195.39, * which are all student loans.

We have paid off a total of $28,026.02 of debt!

*Our current balance will increase to ~$255,000 once Bret gets his final student loan disbursement (more on that later).

I want to also mention that we do have our mortgage, but we aren’t trying to pay that down as quickly as possible for a few reasons: we have a 3% interest rate, we don’t plan on this being our forever home, and one day we might rent it out or sell it.

Actions that helped us pay off $28,026.02 of debt in 15 months

We found a budgeting method that worked for us

We realized we could live off my income alone and not take on anymore debt, but we would have to have a somewhat rigid budget.

Finding a budgeting method that worked for us took some time. I don’t know how many times over the years I have tried to track my expenses in a budget app or an excel sheet, only to find out it was too overwhelming and that I was still overspending!

I am a visual person and learned about the envelope budgeting method, so we decided to give that a try, but use a digital variation.

So, for our entire money management system we have 4 checking accounts and 2 savings accounts (short-term and emergency fund). Our checking accounts include bills, food and miscellaneous, and two personal spending accounts.

This may seem like a lot of accounts to some, but it has worked tremendously for us. I love having a separate account for each major category in our budget so I can easily see how much money we have left in a certain category without having to add every expense into an app or Excel spreadsheet. We are joint owners on all of these accounts.

We then use the zero-based budget method to determine how much goes into each account.

We do have multiple cards to manage, but the pros VERY MUCH outweigh the cons here.

And with our own spending accounts, we have a certain amount of money allotted to us each month, so we individually have some spending freedom. We don’t have to feel guilty and know this money is set aside specifically for our personal spending.

Cut expenses and increased our income

I know some people are tired of hearing about this recommendation, but it’s something that really did help us! We reined in our spending a bit but mostly we had to increase our income. At a certain point, there wasn’t much more to cut.

We didn’t have many streaming services, started to limit our eating out, we didn’t have car payments, and we meal planned and prepped. We did (and still do) aaalll the things. We had to increase our income somehow.

Ways we increased our income

My income increase

I continued with my second job as a social media manager and then started dog sitting.

I have been dog sitting for about 5 years and have primarily used the Rover platform to list myself as a dog sitter. I like this app because it’s easy to use and I can specify various services to offer (e.g., house sitting, boarding, drop in visits, day care, or dog walking).

It also allows me to mark which days I am available and then people reach out to me if I seem like a good fit and my availability matches with their needs! Setting up my profile took some time, but now that it’s done, everything else is fairly low maintenance.

I now just have to respond to inquiries in a timely manner and set up a meet and greet if it seems like a good fit.

I currently only offer house sitting and on Rover and I charge $65/night. Rover takes a cut, so I end up pocketing $52. I also have private clients who pay me directly, and I have gotten those by referrals from past Rover clients. I charge my private clients $40/night.

I recently increased my rates on Rover and have been slow to increase my price with my private clients because they’re loyal.

I don’t make a ton of money dog sitting, but I am able to make a couple hundred dollars a month. My schedule is very limited, but there are people with better availability who make significantly more than I do!

I love animals and we don’t have any due to our sporadic work schedules, so it’s a great way for me to spend time with pets and get paid, too!

Bret’s income increase

Last year, Bret decided to take a break from grad school and soon after, he was offered a summer job in Alaska.

When we first started dating, he used to spend almost every summer there working for a family who owned a set-netting fishery. His uncle had spent many summers in Alaska working for this family and one summer brought Bret to work with him. They would catch salmon and sell it to a buying station in their area.

He went up there for about 6 summers in a row, until he got too busy with school and couldn’t go anymore.

He hadn’t been to Alaska in over 5 years, but someone who worked for the buying station remembered Bret, called him, and asked if he’d be interested in working at the buying station! Since he was already on a break from school, he said yes and worked up there for 8 weeks.

We were able to put every paycheck he earned towards our debt because we could manage all our expenses on my income alone. It was also a great way for Bret to spend part of his summer and I was finally able to visit as I never gotten the chance in previous years.

House hacking

We also started house hacking! We had a spare bedroom and bathroom I would use for my office and occasionally, for guests. A friend of mine and her husband are really into the real estate space and gave us the idea to rent it out.

We weren’t comfortable with the idea of having a long-term roommate, and with both of us working in healthcare, we knew there was a need for short-term and furnished housing for travelling healthcare professionals.

For us, short-term meant renting for 1-6 months, but we were open to individuals staying longer if it worked well for everyone involved!

Some questions we had to address before renting:

Did we need a permit?

How much should we charge for the deposit, rent and pets?

What furniture and amenities are important for travelers?

Where should we list the room?

How to create a lease agreement?

In our county, we did not need a permit to rent out the room if we were renting for at least 30+ days at a time.

After researching rental prices in our area, I found rooms that were of similar caliber listed for $1,100 per month or more. We wanted to be competitive and so we initially settled on $900 per month and have steadily increased it. We have now landed on $995 per month which includes all utilities and internet.

We set the deposit at $995, with an additional $300 for a pet deposit, and no ongoing pet rent.

We wanted to upgrade the furniture in the room and IKEA was a great place for us to find affordable, durable, and aesthetically pleasing furniture. We made sure the room had a bed, large dresser, bedside table, and we kept my desk in there too.

I read it’s important for travelers to have their own TV available so they can unwind in their room. We were able to find a decently priced smart TV off Facebook Marketplace.

Furnished Finder is where we decided to list our room, which started out as a platform for traveling nurses to find furnished housing. It is now used heavily by many healthcare professionals, students, and professionals in other fields.

Travelers reach out to us through the Furnished Finder website and if the dates work out, we move forward with scheduling a video interview. It’s important for us to be able to talk to the person, even if it’s just over video, and we want them to see our faces and home in real time as well.

For the lease agreement, we used ez Landlord Forms, because they have leases for each state with specific information on what’s required to include.

We don’t ask for anything major from tenants. The most important things to us are that they are respectful of our space, don’t smoke in the house, and pay their rent on time. We also added a page at the end for tenants to add two emergency contacts in case we need to call someone on their behalf.

We have had 4 renters so far with the room being occupied for 13 out of the last 14 months. It has really helped us with our debt payoff goals and we have also met some awesome people through the process! We plan to continue renting it out for the foreseeable future.

Applied for in-state student loan help

My state offered a program called the Oregon Behavioral Health Loan Repayment Program where they help minorities in the behavioral health field, or those who serve them, pay back their student loans.

This program is funded by The Behavioral Health Workforce Initiative which has the goal of recruiting and retaining behavioral health providers who, “Are people of color, tribal members, or residents of rural areas of Oregon, and can provide culturally responsive care for diverse communities.”

To apply, I had to show I was employed and actively providing behavioral health services and give them detailed documentation about my student loans. I also had to answer two essay questions related to being a part of and/or working with communities who are underserved and how my training has equipped me with supporting these communities.

I applied last year and was a recipient of an award!

As a recipient, there is a two-year service commitment which means I have to continue providing some sort of behavioral health service during that time frame (which I planned to). Over the next two years, I will be getting ~$88,000 in quarterly disbursements to put towards my student loans. So far this year, I have received ~$11,000, and it’s been life changing to say the least!

Alongside this support, I am also pursuing Public Service Loan Forgiveness (PSLF) for additional student loan relief.

Managing our mental health while paying off debt

Since I am a social worker, I often think about how money and debt affect individuals’ mental health. It’s one of the reasons why I started my blog in the first place.

I realized managing money is a universal task and many of us don’t know what we are doing because talking about money is taboo. And when you have financial stress, it can really take a toll on your mental health. So, I wanted to share our journey in hopes of helping others.

Bret and I aren’t those individuals who want to avoid eating out and fun experiences until we are debt free. And, we are also privileged to not have to take those extreme measures either. It has been important for us to make this journey sustainable and not deprive ourselves of experiences while we are going through it.

Here’s how we are making our journey sustainable:

Still going out to eat

Budgeting for personal spending money, aka fun

Setting realistic debt payoff goals

Putting aside money for travel

Not comparing and thinking other people are better than us because they’re able to pay off their debt quicker

Tracking our debt payoff progress (we use Excel). With so much debt left to pay off, being able to see our progress is really motivating

Openly talking about our debt. Avoidance is a coping mechanism for many, for us, acknowledging and addressing it has been so freeing (but it wasn’t always this way).

Talking about our dreams and reminding ourselves why we want to do this in the first place

We know that if we eliminated going out to eat, budgeting for fun, or both, we could be paying off our debt much quicker. However, that sounds miserable to us. It’s worth it to still go out to dinner, travel, or buy plants (in my case) than to deprive ourselves of the joy these things bring.

We are making great progress and we know in time, we will be debt free.

Our debt payoff journey is not linear

A few months ago, we decided to take out $6,000 of student loans. Bret currently has a full tuition scholarship, so we are tremendously lucky in that regard, but he just learned about some conferences that would be really helpful to his professional growth. We have gotten $1,500 of this loan money already which is included in our current debt balance, but we haven’t received all of it yet.

We could have pinched and saved to avoid taking on any of this debt, but that would have caused me to work more than I currently am. Again, not in line with our current goal of making this journey sustainable!

We were very intentional about how much to take out. We estimated how much he would need for a few conferences and declined the rest. We even opened a separate savings account for the money to make sure it didn’t get accidentally spent on anything.

I’m SO proud of us for that!

The goal here is progress not perfection. So cliche, I know. But we are learning how to think critically about our money, spend thoughtfully, use our money as a tool to reach our goals, and enjoy our life along the way. And right now, that meant taking on a little more debt.

We are moving in the right direction, and we know when he starts working, that will really accelerate our debt payoff journey since we have proven to ourselves we can live on my income alone.

Our plan going forward

Bret is still in school which means his loans are on deferment, so we currently have his on the back burner.

With the loan payment assistance I am receiving, it’s allowing us to put any extra money we have each month towards our savings. Our priority right now is building up a good emergency fund of about $16,000 (~4 months’ worth of expenses).

This has been difficult because of inflation and just little emergencies that keep popping up, but we are slowly making progress.

I am also prioritizing investing in my employer retirement plan, but only up to the amount that gets me my employer match which is 6% of my income.

Bret will be graduating in 2025, so at that time, we will pivot to incorporating his loans into our budget. Our goal is to be debt free by 2028.

It will take a lot of discipline and persistence, but I think we can do it. I am manifesting it!

We want to continue to learn, implement, and grow. We want to keep having transparent discussions about money and building our money foundations. And I personally want to continue sharing our journey with hopes of inspiring, encouraging and educating others. Here’s to sharing the wealth.

Do you have debt? What are you doing to pay it off?

Taylor is a social worker and personal finance blogger at Social Work to Wealth where she shares tips, resources, and lessons learned on her family’s journey to paying off $277,000 of debt and retiring early. She hopes to inspire and empower social workers with financial education so they can have a better relationship with their money. When she’s not working or blogging, you can find her traveling, gardening, trying a new restaurant, or buying too many plants.

Paper trading is simulated trading, done for practice without real money. It’s a way to test different trading strategies without the risk of losing money, before an investor starts trading with real capital.

The practice gets its name from how investors would once mark down their hypothetical stock purchases and sales — and track their returns and losses — on paper. But today, investors typically use digital platforms to virtually test out hypothetical investment portfolios, day-trading tactics, and broader investing strategies.

How do Paper Trades Work?

What is paper trading? In its most basic form, paper trading involves selecting a stock, group of stocks, or a sector, then writing down the ticker or tickers and choosing a time to buy the stock. The paper trader then writes down the purchase price or prices.

When they sell the stock or stocks, they write down that price as well, and tally up their return. 💡 Quick Tip: Before opening any investment account, consider what level of risk you are comfortable with. If you’re not sure, start with more conservative investments, and then adjust your portfolio as you learn more.

Pros and Cons of Paper Trading

Paper trading has both benefits and drawbacks. Here are a few factors to consider before you try paper trading.

The Pros of Paper Trading

Build skills: Paper trading is a way to learn and build trading skills in either a bear or a bull market. For new traders, a virtual trading platform offers a way to make rookie mistakes without risking real money. It’s a method to get comfortable with the process of buying and selling stocks, and making sure you don’t enter a limit order when you mean to place a market order.

Test out strategies: Paper stock trading allows for experimentation. For example, an investor might hear about shorting a stock. But they may not know how the process works, and what it actually pays out. Paper trading permits investors to learn how these trades work in practical terms. Or, they might want to try out other strategies, such as swing trading.

Learn about strengths and weaknesses: Paper trading is also a way for investors to learn about their own strengths and weaknesses. Traders lose money in the markets for a number of personal reasons. Some stick to their guns too long, while others give up too soon when the market is down. Some lose money because they panic, while others lose money because they ignore clear warning signs. Paper trading is a way for investors to learn their own tendencies and weaknesses without paying for the lesson.

Keep emotions out of it: Finally, paper trading can help teach investors to keep their emotions in check while the markets are going up and down. Investing with hypothetical dollars can be good practice in the valuable art of making rational decisions in stressful situations and allow investors to find risk management techniques that work best for them.

The Cons of Paper Trading

It’s not real: The biggest drawback of paper trading is that it’s not real. An investor can’t keep the returns they earn paper trading. And those paper returns can lead the investor to have an unrealistic sense of confidence, and a false sense of security. Paper trading also doesn’t account for real-life situations that might require an investor to withdraw money from the market for personal reasons or the impact of an unexpected recession.